As filed with the Securities and Exchange Commission on January 21, 2015

Securities Act File No. 333-200862

Investment Company Act File No. 811-07136

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-14

| REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 | ||

| Pre-Effective Amendment No. 1 | x | |

| Post-Effective Amendment No. | ¨ | |

| (Check appropriate box or boxes) |

BLACKROCK MUNIYIELD PENNSYLVANIA QUALITY FUND

(Exact Name of Registrant as Specified in Charter)

100 Bellevue Parkway

Wilmington, Delaware 19809

(Address of Principal Executive Offices: Number, Street, City, State, Zip Code)

(800) 882-0052

(Area Code and Telephone Number)

John M. Perlowski

President and Chief Executive Officer

BlackRock MuniYield Pennsylvania Quality Fund

55 East 52nd Street

New York, New York 10055

(Name and Address of Agent for Service)

With copies to:

| Thomas A. DeCapo, Esq. Skadden, Arps, Slate, Meagher & Flom LLP 500 Boylston Street Boston, Massachusetts 02116 |

Janey Ahn, Esq. BlackRock Advisors, LLC 40 East 52nd Street New York, New York 10022 |

AS SOON AS PRACTICABLE AFTER THE EFFECTIVE DATE OF THIS REGISTRATION STATEMENT

(Approximate Date of Proposed Public Offering)

CALCULATION OF REGISTRATION FEE UNDER THE SECURITIES ACT OF 1933

|

| ||||||||

| Title of Securities Being Registered | Amount Being Registered(1) |

Proposed Maximum Offering Price Per Unit(2) |

Proposed Maximum Aggregate Offering Price(1) |

Amount of Registration Fee(3) | ||||

| Common shares $0.10 par value |

1,966,576 | $16.34 | $32,133,851.84 | $3,733.95 | ||||

|

| ||||||||

|

| ||||||||

| (1) | Estimated solely for the purpose of calculating the filing registration fee, pursuant to Rule 457(o) under the Securities Act of 1933. |

| (2) | Net asset value per common share on January 14, 2015. |

| (3) | $116.20 previously paid in connection with the registration of $1,000,000 worth of common shares on December 11, 2014. |

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

EXPLANATORY NOTE

This Registration Statement is organized as follows:

| a. | Letter to Common Shareholders of The BlackRock Pennsylvania Strategic Municipal Trust (“BPS”). |

| b. | Questions and Answers for Common Shareholders of BPS. |

| c. | Notice of Special Meeting of Common Shareholders of BPS. |

| d. | Combined Proxy Statement/Prospectus regarding the proposed reorganization of BPS into BlackRock MuniYield Pennsylvania Quality Fund (“MPA”). |

| e. | Statement of Additional Information regarding the proposed reorganization of BPS into MPA. |

| f. | Part C: Other Information. |

| g. | Exhibits. |

THE BLACKROCK PENNSYLVANIA STRATEGIC MUNICIPAL TRUST

100 Bellevue Parkway

Wilmington, Delaware 19809

(800) 882-0052

January 21, 2015

Dear Common Shareholder:

You are cordially invited to attend a joint special shareholder meeting (the “Special Meeting”) of The BlackRock Pennsylvania Strategic Municipal Trust (“BPS” or the “Target Fund”) and BlackRock MuniYield Pennsylvania Quality Fund (“MPA” or the “Acquiring Fund” and together with the Target Fund, the “Funds”) to be held at the offices of BlackRock Advisors, LLC, 1 University Square Drive, Princeton, New Jersey 08540-6455, on March 12, 2015 at 4:30 p.m. (Eastern time). Before the Special Meeting, I would like to provide you with additional background information and ask for your vote on important proposal affecting the Target Fund which are described in the enclosed Combined Proxy Statement/Prospectus.

Common Shareholders of BPS: you and the preferred shareholders of the Target Fund are being asked to vote as a single class on a proposal to approve the reorganization of the Target Fund into the Acquiring Fund (the “Reorganization”). The Funds have similar (but not identical) investment objectives, investment policies and investment restrictions.

The enclosed Combined Proxy Statement/Prospectus is only being delivered to common shareholders of the Target Fund.

The preferred shareholders of each Fund are also being asked to attend the Special Meeting and to vote as a separate class on the proposal to approve the Reorganization. Each Fund is delivering to its preferred shareholders a separate Joint Proxy Statement with respect to the proposal to approve the Reorganization.

The Board of Trustees of the Target Fund believes the proposal that the common shareholders of the Target Fund are being asked to vote upon is in the best interests of the Target Fund and its shareholders and unanimously recommends that you vote “FOR” such proposal.

The enclosed materials explain this proposal in more detail, and I encourage you to review them carefully. As a shareholder, your vote is important, and we hope that you will respond today to ensure that your shares will be represented at the Special Meeting. You may vote using one of the methods below by following the instructions on your proxy card:

| • | By touch-tone telephone; |

| • | By internet; |

| • | By returning the enclosed proxy card in the postage-paid envelope; or |

| • | In person at the Special Meeting. |

If you do not vote using one of these methods described above, you may be contacted by Georgeson Inc., our proxy solicitor, to vote your shares over the telephone.

As always, we appreciate your support.

Sincerely,

JOHN M. PERLOWSKI

Chief Executive Officer and President

| Please vote now. Your vote is important. |

| To avoid the wasteful and unnecessary expense of further solicitation(s), we urge you to indicate your voting instructions on the enclosed proxy card, date and sign it and return it promptly in the postage-paid envelope provided, or record your voting instructions by telephone or via the internet, no matter how large or small your holdings may be. If you submit a properly executed proxy but do not indicate how you wish your common shares to be voted, your common shares will be voted “FOR” the proposal, as applicable. If your common shares are held through a broker, you must provide voting instructions to your broker about how to vote your common shares in order for your broker to vote your common shares as you instruct at the Special Meeting. |

January 21, 2015

IMPORTANT NOTICE

TO COMMON SHAREHOLDERS OF

THE BLACKROCK PENNSYLVANIA STRATEGIC MUNICIPAL TRUST

QUESTIONS & ANSWERS

Although we urge you to read the entire Combined Proxy Statement/Prospectus, we have provided for your convenience a brief overview of some of the important questions concerning the meeting and the proposals to be voted on. The enclosed Combined Proxy Statement/Prospectus is being sent only to the holders of common shares of beneficial interests (“Common Shares”) of The BlackRock Pennsylvania Strategic Municipal Trust (the “Target Fund”). Each of the Target Fund and BlackRock MuniYield Pennsylvania Quality Fund (the “Acquiring Fund” and together with the Target Fund, the “Funds” and each, a “Fund”) is separately soliciting the votes of holders of its Variable Rate Demand Preferred Shares (“VRDP Shares”) through a separate Joint Proxy Statement.

| Q: | Why is a shareholder meeting being held? |

| A: | Common Shareholders of The BlackRock Pennsylvania Strategic Municipal Trust (NYSE MKT Ticker: BPS): You and the holders of the VRDP Shares (“VRDP Holders”) of your Fund are being asked to vote as a single class on a proposal to approve the Agreement and Plan of Reorganization (the “Reorganization Agreement”) between the Target Fund and the Acquiring Fund, pursuant to which (i) the Acquiring Fund will acquire substantially all of the Target Fund’s assets and assume substantially all of the Target Fund’s liabilities in exchange solely for newly issued Common Shares and VRDP Shares of the Acquiring Fund, which will be distributed to the common shareholders (although cash may be distributed in lieu of fractional Common Shares) and VRDP Holders, respectively, of the Target Fund, and (ii) the Target Fund will terminate its registration under the Investment Company Act of 1940, as amended (the “1940 Act”), and liquidate, dissolve and terminate in accordance with its agreement and declaration of trust and Delaware law. |

VRDP Holders of each Fund are also being asked to vote as a separate class on the proposal to approve the Reorganization Agreement through a separate Joint Proxy Statement.

The transactions contemplated by the Reorganization Agreement are referred to herein as the “Reorganization.” The term “Combined Fund” refers to the Acquiring Fund as the surviving Fund after the consummation of the Reorganization.

| Q: | Why has each Fund’s Board recommended these proposals? |

| A: | The Board of Trustees (each, a “Board” and each member thereof, a “Board Member”) of each Fund has determined that the proposed Reorganization would be in the best interests of its Fund. The proposed Reorganization seeks to achieve certain economies of scale and other operational efficiencies by combining two Funds that have similar (but not identical) investment objectives, investment policies, investment restrictions and portfolio compositions and are managed by the same investment advisor, BlackRock Advisors, LLC (the “Investment Advisor”), and portfolio management team. |

In light of these similarities, the proposed Reorganization is intended to reduce fund redundancies and create a single, larger state fund that may benefit from anticipated operating efficiencies and economies of scale. The proposed Reorganization is intended to result in the following potential benefits to common shareholders:

| (i) | lower total expenses per Common Share for common shareholders of each Fund (as common shareholders of the Combined Fund following the Reorganization) due to economies of scale resulting from the larger size of the Combined Fund; |

| (ii) | improved earnings yield on net asset value (“NAV”) for common shareholders of the Target Fund and a comparable (i.e., the same or slightly lower or higher) earnings yield on NAV for common shareholders of the Acquiring Fund; |

| (iii) | improved secondary market trading of the Common Shares of the Combined Fund; and |

| (iv) | operating and administrative efficiencies for the Combined Fund, including the potential for the following: |

| (a) | greater investment flexibility and investment options; |

| (b) | greater diversification of portfolio investments; |

| (c) | the ability to trade in larger positions and more favorable transaction terms; |

| (d) | benefits from having fewer closed-end funds offering similar products in the market, including an increased focus by investors on the remaining funds in the market (including the Combined Fund) and additional research coverage; and |

| (e) | benefits from having fewer similar funds in the same fund complex, including a simplified operational model and a reduction in risk of operational, legal and financial errors. |

The Board of each Fund, including Board Members thereof who are not “interested persons” (as defined in the 1940 Act), approved the Reorganization, concluding that the Reorganization is in the best interests of its Fund and that the interests of existing common shareholders and preferred shareholders of its Fund will not be diluted with respect to NAV and liquidation preference, respectively, as a result of the Reorganization. As a result of the Reorganization, however, common and preferred shareholders of each Fund will hold a reduced percentage of ownership in the larger Combined Fund than they did in any of the individual Funds before the Reorganization. The Board’s conclusion was based on each Board Member’s business judgment after consideration of all relevant factors taken as a whole with respect to its Fund and the Fund’s common and preferred shareholders, although individual Board Members may have placed different weight on various factors and assigned different degrees of materiality to various factors.

| Q: | How will the Reorganization affect the fees and expenses of the Funds? |

| A: | For the fiscal year ended July 31, 2014, the Total Expense Ratio for the Acquiring Fund was 1.48%. For the fiscal year ended April 30, 2014, the Total Expense Ratio for the Target Fund was 2.08%. “Total Expenses” means a Fund’s total annual operating expenses (including interest expenses). “Total Expense Ratio” means a Fund’s Total Expenses expressed as a percentage of its average net assets attributable to its Common Shares. |

As of July 31, 2014, the historical and pro forma Total Expense Ratios applicable to the Reorganization are as follows:

| Target Fund (BPS) |

Acquiring Fund (MPA) | Pro Forma Combined Fund (MPA) | ||

| 2.05% |

1.48% | 1.48% |

The Funds estimate that the completion of the Reorganization would result in a Total Expense Ratio for the Combined Fund of 1.48% on a historical and pro forma basis for the 12-month period ended July 31, 2014, representing a reduction in the Total Expense Ratio for the common shareholders of the Target Fund of 0.57% and no impact on the Total Expense Ratio for the common shareholders of the Acquiring Fund.

The Target Fund currently pays the Investment Advisor a monthly fee at an annual contractual management fee rate of 0.60% of the Target Fund’s average weekly net assets. Average weekly net assets are the average weekly value of the Target Fund’s total assets minus its total accrued liabilities. The Acquiring Fund currently pays the Investment Advisor a monthly fee at an annual contractual management fee rate of 0.50% of the Acquiring Fund’s average daily net assets. Average daily net assets are the average daily value of the Acquiring Fund’s total assets minus its total accrued liabilities. If the Reorganization is consummated, the annual contractual management fee rate of the Combined Fund will be reduced to 0.49% of the average daily net assets of the Combined Fund. Based on a pro-forma Lipper expense universe for the Combined Fund, the estimated total annual fund operating expenses (excluding investment related expenses) and contractual management fee rate

ii

are each expected to be in the first quartile. There can be no assurance that future expenses will not increase or that any expense savings for any Fund will be realized as a result of the Reorganization.

| Q: | How will the Reorganization affect the earnings, distributions and undistributed net income of the Funds? |

| A: | The Combined Fund’s earnings yield on NAV following the Reorganization is expected to be comparable (i.e., the same or slightly lower or higher) to the Acquiring Fund’s current earnings yield on NAV and potentially higher than the Target Fund’s current earnings yield on NAV; thus, assuming that the Reorganization is consummated and that the Acquiring Fund’s distribution policy remains in place after the Reorganization, common shareholders of the Acquiring Fund may experience a distribution rate on NAV comparable (i.e., the same or slightly lower or higher) to their current distribution rate on NAV and common shareholders of the Target Fund may experience a distribution rate on NAV that is potentially higher than their current distribution rate on NAV. The Combined Fund’s earnings and distribution rate on NAV will change over time, and depending on market conditions, may be significantly higher or lower than each Fund’s earnings and distribution rate on NAV prior to the Reorganization. A Fund’s earnings and net investment income are variables which depend on many factors, including its asset mix, portfolio turnover level, the amount of leverage utilized by the Fund, the costs of such leverage, the performance of its investments, the movement of interest rates and general market conditions. |

If the Reorganization is approved by shareholders, then substantially all of the undistributed net investment income, if any, of each Fund is expected to be declared to such Fund’s common shareholders prior to the effective date of the Reorganization (the “Closing Date”) (the “Pre-Reorganization Declared UNII Distributions”). The declaration date, ex-dividend date (the “Ex-Dividend Date”) and record date of the Pre-Reorganization Declared UNII Distributions will occur prior to the Closing Date. However, all or a significant portion of the Pre-Reorganization Declared UNII Distributions may be paid in one or more distributions to common shareholders of the Funds entitled to such Pre-Reorganization Declared UNII Distributions after the Closing Date. In addition, BlackRock MuniYield Pennsylvania Quality Fund (MPA) does not currently expect to declare any distributions during the first month following the Closing Date. Accordingly, persons who purchase Common Shares of any of the Funds on or after the Ex-Dividend Date for the Pre-Reorganization Declared UNII Distributions should not expect to receive any distributions from any Fund until distributions, if any, are declared by the Board of the Combined Fund and paid to shareholders entitled to any such distributions. No such distributions are expected to be paid by the Combined Fund until at least approximately two months following the Closing Date.

The Combined Fund’s earnings and distribution rate on NAV will change over time, and depending on market conditions, may be significantly higher or lower than each Fund’s earnings and distribution rate on NAV prior to the Reorganization. Each Fund reserves the right to change its distribution policy with respect to common share distributions and the basis for establishing the rate of its monthly distributions for the Common Shares at any time and may do so without prior notice to common shareholders. The payment of any distributions by any Fund is subject to, and will only be made when, as and if, declared by the Board of such Fund. There is no assurance the Board of any Fund will declare any distributions for such Fund. To the extent any Pre-Reorganization Declared UNII Distributions is not an “exempt interest dividend” (as defined in the Code), the distribution may be taxable to shareholders for U.S. Federal income tax purposes.

| Q: | Have Common Shares of each Fund historically traded at a premium or discount? |

| A: | The Common Shares of each Fund have historically traded at both a premium and a discount. The table below sets forth the market price, NAV, and the premium/discount to NAV of each Fund as of December 31, 2014. |

| Fund |

Market Price | NAV | Premium/(Discount) to NAV | |||

| MPA |

$14.34 | $16.12 | (11.04)% | |||

| BPS |

$12.78 | $14.80 | (13.65)% |

iii

To the extent the Target Fund Common Shares are trading at a wider discount (or a narrower premium) than the Acquiring Fund at the time of the Reorganization, the Target Fund’s common shareholders would have the potential for an economic benefit by the narrowing of the discount or widening of the premium. To the extent the Target Fund Common Shares are trading at a narrower discount (or wider premium) than the Acquiring Fund at the time of the Reorganization, Target Fund common shareholders may be negatively impacted if the Reorganization is consummated. Acquiring Fund common shareholders would only benefit from a premium/discount perspective to the extent the Acquiring Fund’s post-Reorganization discount (or premium) improves. There can be no assurance that, after the Reorganization, Common Shares of the Combined Fund will trade at a narrower discount to NAV or wider premium to NAV than the Common Shares of any individual Fund prior to the Reorganization.

In the Reorganization, common shareholders of the Target Fund will receive Acquiring Fund Common Shares based on the relative NAVs (not the market values) of the respective Fund’s Common Shares. The market value of the Common Shares of the Combined Fund may be less than the market value of the Common Shares of each respective Fund prior to the Reorganization.

| Q: | How will holders of VRDP Shares be affected by the Reorganization? |

| A: | As of the date of the enclosed Combined Proxy Statement/Prospectus, each Fund has Series W-7 VRDP Shares outstanding. As of December 31, 2014, the Target Fund has 163 Series W-7 VRDP Shares outstanding, and the Acquiring Fund has 663 Series W-7 VRDP Shares outstanding. In connection with the Reorganization, the Acquiring Fund expects to issue 163 additional VRDP Shares to VRDP Holders of the Target Fund. Following the completion of the Reorganization, the Combined Fund is expected to have 826 VRDP Shares outstanding. |

Upon the closing of the Reorganization, the Target Fund VRDP Holders will receive on a one-for-one basis one newly issued VRDP Share of the Acquiring Fund, par value $0.05 per share and with a liquidation preference of $100,000 per share (plus any accumulated and unpaid dividends that have accrued on such Target Fund VRDP Share up to and including the day immediately preceding the effective date of the Reorganization if such dividends have not been paid prior to such effective date), in exchange for each Target Fund VRDP Share held by such Target Fund VRDP Holder immediately prior to the closing of the Reorganization. The newly issued Acquiring Fund VRDP Share may be of the same series as the Acquiring Fund’s Series W-7 VRDP Shares or a substantially identical series. No fractional Acquiring Fund VRDP Shares will be issued. Target Fund VRDP Holders will receive the same number of Acquiring Fund VRDP Shares, with terms substantially similar to the outstanding Target Fund VRDP Shares, held by such holders immediately prior to the closing of the Reorganization, with the only significant difference being that the Target Fund VRDP Shares have a mandatory redemption date of July 1, 2042 and the newly issued Acquiring Fund VRDP Shares is expected to have a mandatory redemption date of June 1, 2041.

The Acquiring Fund VRDP Shares to be issued in connection with the Reorganization will have terms that are substantially identical to the terms of the outstanding Acquiring Fund VRDP Shares and will rank on a parity with the Acquiring Fund’s existing VRDP Shares as to the payment of dividends and the distribution of assets upon dissolution, liquidation or winding up of the affairs of the Acquiring Fund. The Reorganization will not result in any changes to the terms of the Acquiring Fund’s VRDP Shares currently outstanding.

The terms of the outstanding Target Fund VRDP Shares are substantially similar to the terms of the outstanding Acquiring Fund VRDP Shares. The only significant difference between the terms of the two Funds’ VRDP Shares is that the Target Fund VRDP Shares have a mandatory redemption date of July 1, 2042 and the Acquiring Fund VRDP Shares have a mandatory redemption date of June 1, 2041. The Funds’ VRDP Shares have the same $100,000 per share liquidation preference, dividend period, dividend payment date, voting rights, redemption provisions, remarketing procedures, mandatory purchase events, mandatory tender events, transfer restrictions and covenants with respect to effective leverage, asset coverage and eligible investments. The Funds’ VRDP Shares also have the same mechanism for determining the applicable dividend rate and maximum rate, the same liquidity provider, remarketing agent, tender and

iv

paying agent. Each Fund’s VRDP Shares are currently in a three year special rate period that will end on June 24, 2015. The terms applicable to each Fund’s VRDP Shares during the special rate period are substantially identical. During the special rate period, the Funds’ VRDP Shares have the same mechanism for determining the applicable dividend rate and maximum rate, redemption premiums and transfer restrictions.

None of the expenses of the Reorganization are expected to be borne by the VRDP Holders of the Funds.

Following the Reorganization, the VRDP Holders of each Fund will be VRDP Holders of the larger Combined Fund that will have a larger asset base and more VRDP Shares outstanding than either Fund individually. With respect to matters requiring all preferred shareholders to vote separately or common and preferred shareholders to vote together as a single class, following the Reorganization, holders of VRDP Shares of the Combined Fund will hold a smaller percentage of the outstanding preferred shares of the Combined Fund as compared to their percentage holdings of outstanding preferred shares of their respective Fund prior to the Reorganization.

| Q: | How similar are the Funds? |

| A: | The Funds have the same investment advisor, portfolio managers, officers and trustees. The Target Fund is organized as a Delaware statutory trust and the Acquiring Fund is organized as a Massachusetts business trust. The Acquiring Fund has Common Shares listed on the New York Stock Exchange and the Target Fund has Common Shares listed on the NYSE MKT. Each Fund has privately placed VRDP Shares outstanding. Each Fund is managed by a team of investment professionals comprised of Phillip Soccio, Theodore R. Jaeckel, Jr. and Walter O’Connor. |

The investment objective, significant investment strategies and operating policies, and investment restrictions of the Combined Fund will be those of the Acquiring Fund.

The Funds’ Investment Objectives:

| • | The Target Fund’s investment objectives are to provide current income exempt from regular Federal and Pennsylvania income taxes, and to invest in municipal bonds that over time will perform better than the broader Pennsylvania municipal bond market. |

| • | The Acquiring Fund’s investment objective is to provide shareholders with as high a level of current income exempt from Federal and Pennsylvania income taxes as is consistent with its investment policies and prudent investment management. |

Pennsylvania Municipal Bonds:

| • | The Target Fund invests primarily (under normal market conditions, at least 65% of its total assets) in municipal bonds that pay interest that is exempt from regular Federal and Pennsylvania income taxes. |

| • | The Acquiring Fund invests at least 80% of an aggregate of its net assets (including proceeds from the issuance of any preferred shares) and the proceeds of any borrowings for investment purposes, in a portfolio of municipal obligations issued by or on behalf of the Commonwealth of Pennsylvania, its political subdivisions, agencies and instrumentalities and by other qualifying issuers, each of which pays interest that, in the opinion of bond counsel to the issuer, is excludable from gross income for U.S. federal income tax purposes (except that the interest may be includable in taxable income for purposes of the Federal alternative minimum tax) and exempt from Pennsylvania income taxes. |

Investment Grade Securities:

| • | The Target Fund invests at least 80% of its total assets in investment grade quality securities and may invest up to 20% of its total assets in securities that are rated, at the time of investment, Ba/BB or B by Moody’s Investors Service, Inc. (“Moody’s”), Standard & Poor’s Ratings Group, a |

v

| division of The McGraw-Hill Companies, Inc. (“S&P”) or Fitch Ratings (“Fitch”) or that are unrated but judged to be of comparable quality by the Investment Advisor. |

| • | Under normal market conditions, the Acquiring Fund invests primarily in a portfolio of long term municipal obligations that are commonly referred to as “investment grade” securities, which are obligations rated at the time of purchase within the four highest quality ratings as determined by either Moody’s, S&P or Fitch or, if unrated, are considered by the Fund’s investment adviser to be of comparable quality. |

Although the Acquiring Fund’s investment policy with respect to below investment grade securities may be more flexible than the investment policy of the Target Fund with respect to below investment grade securities, the Acquiring Fund currently does not intend to invest in below investment grade securities; except, that, the Acquiring Fund may acquire a de minimis amount of below investment grade securities from the Target Fund upon the consummation of the Reorganization. The Acquiring Fund may continue to hold such below investment grade securities in its portfolio after the consummation of the Reorganization.

Leverage:

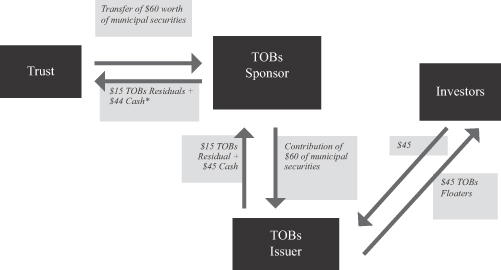

| • | Each Fund utilizes VRDP Shares and tender option bonds for leverage. |

Other Investment Policies:

| • | The Acquiring Fund may not engage in short sales or securities lending, while these are permitted activities for the Target Fund. |

It is not anticipated that there will be any significant disposition of the holdings in any Fund as a result of the Reorganization because of the similarities among the portfolio guidelines of the Funds. The risk/return profile of the Combined Fund is expected to remain comparable to those of each Fund before the Reorganization because of the similarities in the investment policies of each Fund.

| Q: | How will the Reorganization be effected? |

| A: | Assuming the Reorganization receives the requisite shareholder approvals, the Acquiring Fund will acquire substantially all of the Target Fund’s assets and assume substantially all of the Target Fund’s liabilities in exchange solely for newly issued Common Shares and VRDP Shares of the Acquiring Fund, which will be distributed to the shareholders of the Target Fund (although cash may be distributed in lieu of fractional Common Shares). The Target Fund then will terminate its registration under the 1940 Act and liquidate, dissolve and terminate in accordance with its agreement and declaration of trust and Delaware law. |

Shareholders of the Target Fund will become shareholders of the Acquiring Fund. Common shareholders of the Target Fund will receive newly issued Common Shares of the Acquiring Fund, par value $0.10 per share, the aggregate NAV (not the market value) of which will equal the aggregate NAV (not the market value) of the Common Shares of the Target Fund such shareholders held immediately prior to the closing of the Reorganization (although common shareholders may receive cash for fractional Common Shares). The NAV of the Target Fund and the Acquiring Fund immediately prior to the closing of the Reorganization will be reduced by the costs of the Reorganization borne by each Fund, if any. The NAV of Target Fund Common Shares will not be diluted as a result of the Reorganization. The common shareholders of each Fund have substantially similar voting rights and rights with respect to the payment of dividends and distribution of assets upon liquidation of their respective Fund and have no preemptive, conversion or exchange rights.

Target Fund VRDP Holders will receive on a one-for-one basis one newly issued VRDP Share of the Acquiring Fund, par value $0.05 per share and with a liquidation preference of $100,000 per share (plus any accumulated and unpaid dividends that have accrued on such Target Fund VRDP Share up to and including the day immediately preceding the effective date of the Reorganization if such dividends have not been paid prior to such effective date), in exchange for each Target Fund VRDP Share held by such Target Fund

vi

VRDP Holder immediately prior to the closing of the Reorganization. The newly issued Acquiring Fund VRDP Share may be of the same series as the Acquiring Fund’s Series W-7 VRDP Shares or a substantially identical series. No fractional Acquiring Fund VRDP Shares will be issued. Target Fund VRDP Holders will receive the same number of Acquiring Fund VRDP Shares, with terms substantially similar to the outstanding Target Fund VRDP Shares, held by such holders immediately prior to the closing of the Reorganization, with the only significant difference being that the Target Fund VRDP Shares have a mandatory redemption date of July 1, 2042 and the newly issued Acquiring Fund VRDP Shares is expected to have a mandatory redemption date of June 1, 2041.

Shareholders of the Acquiring Fund will remain shareholders of the Acquiring Fund, which will have additional Common Shares and VRDP Shares outstanding after the Reorganization.

| Q: | Will I have to pay any U.S. federal income taxes as a result of the Reorganization? |

| A: | The Reorganization is intended to qualify as a “reorganization” within the meaning of Section 368(a) of the Internal Revenue Code of 1986, as amended (the “Code”). If the Reorganization so qualifies, in general, shareholders of the Target Fund will recognize no gain or loss for U.S. federal income tax purposes upon the exchange of their Target Fund shares for Acquiring Fund shares pursuant to the Reorganization (except with respect to cash received in lieu of fractional Common Shares). Additionally, the Target Fund will recognize no gain or loss for U.S. federal income tax purposes by reason of the Reorganization. Neither the Acquiring Fund nor its shareholders will recognize any gain or loss for U.S. federal income tax purposes pursuant to the Reorganization. |

Shareholders of each Fund may receive distributions prior to, or after, the consummation of the Reorganization, including distributions attributable to their proportionate share of each Fund’s undistributed net investment income declared prior to the consummation of the Reorganization or the Combined Fund built-in gains, if any, recognized after the Reorganization, when such income and gains are eventually distributed by the Combined Fund. To the extent that such a distribution is not an “exempt interest dividend” (as defined in the Code), the distribution may be taxable to shareholders for U.S. federal income tax purposes.

The Funds’ shareholders should consult their own tax advisers regarding the U.S. federal income tax consequences of the Reorganization, as well as the effects of state, local and non-U.S. tax laws, including possible changes in tax laws.

| Q: | Will I have to pay any sales load, commission or other similar fees in connection with the Reorganization? |

| A: | You will pay no sales loads or commissions in connection with the Reorganization. Regardless of whether the Reorganization is completed, however, the costs associated with the proposed Reorganization, including the costs associated with the shareholder meeting, will be borne directly by each of the respective Funds incurring the expense or will otherwise be allocated among the Funds proportionately or on another reasonable basis as discussed more fully in the Combined Proxy Statement/Prospectus. |

Common shareholders of the Funds will indirectly bear the costs of the Reorganization. The expenses of the Reorganization are estimated to be $276,000 for the Target Fund and $233,000 for the Acquiring Fund. Because of the expected expense savings and other benefits for each Fund, the Investment Advisor recommended and the Board of each Fund has approved that its respective Fund be responsible for a portion of its own Reorganization expenses. The Investment Advisor will bear approximately $160,000 of the Acquiring Fund’s reorganization expenses because the common shareholders of the Acquiring Fund are not expected to experience the same level of economic benefits from the Reorganization as the common shareholders of the Target Fund. The actual costs associated with the proposed Reorganization may be more or less than the estimated costs discussed herein.

VRDP Holders of the Funds are not expected to bear any costs of the Reorganization.

vii

Neither the Funds nor the Investment Advisor will pay any expenses of shareholders arising out of or in connection with the Reorganization (e.g., expenses incurred by the shareholder as a result of attending the shareholder meeting, voting on the Reorganization or other action taken by the shareholder in connection with the Reorganization).

| Q: | What shareholder approvals are required to complete the Reorganization? |

| A: | The Reorganization is contingent upon the following approvals: |

| • | The approval of the Reorganization Agreement and the transactions contemplated therein, including the termination of the Target Fund’s registration under the 1940 Act and the dissolution of the Target Fund under Delaware law, by the Target Fund’s common shareholders and VRDP Holders voting as a single class; |

| • | The approval of the Reorganization Agreement and the transactions contemplated therein, including the termination of the Target Fund’s registration under the 1940 Act and the dissolution of the Target Fund under Delaware law, by Target Fund VRDP Holders voting as a separate class; and |

| • | The approval of the Reorganization Agreement and the transactions contemplated therein, including the issuance of additional Acquiring Fund VRDP Shares, by Acquiring Fund VRDP Holders voting as a separate class. |

If the requisite shareholder approvals are not obtained, each Fund’s Board may take such actions as it deems in the best interests of its Fund, including conducting additional solicitations with respect to the proposals or continuing to operate the Fund as a stand-alone Massachusetts business trust (with respect to the Acquiring Fund) or Delaware statutory trust (with respect to the Target Fund) registered under the 1940 Act as a non-diversified closed-end investment management company advised by the Investment Advisor. The Investment Advisor may, in connection with the ongoing management of each Fund and its product line, recommend alternative proposals to the Board of each Fund.

In order for the Reorganization to occur, each Fund must obtain all requisite shareholder approvals with respect to the Reorganization, as well as certain consents, confirmations and/or waivers from various third parties, including the liquidity provider with respect to the outstanding VRDP Shares. Because the closing of the Reorganization is contingent upon the Target Fund and the Acquiring Fund obtaining the requisite shareholder approvals and third party consents and satisfying (or obtaining the waiver of) other closing conditions, it is possible that the Reorganization will not occur, even if shareholders of either Fund entitled to vote on the Reorganization approve the Reorganization and such Fund satisfies all of its closing conditions, if the other Fund does not obtain its requisite shareholder approvals or satisfy its closing conditions. The VRDP Shares were issued on a private placement basis to one or a small number of institutional holders. To the extent that one or more VRDP Holder of a Fund owns, holds or controls, individually or in the aggregate, all or a significant portion of such Fund’s outstanding VRDP Shares, the shareholder approval required for the Reorganization may turn on the exercise of voting rights by such particular shareholder(s) and its (or their) determination as to the favorability of the proposal with respect to its (or their) interests. The Funds exercise no influence or control over the determinations of such shareholder(s) with respect to the proposal; there is no guarantee that such shareholder(s) will approve the proposal, over which it (or they) may exercise effective disposition power.

| Q: | Why is the vote of preferred shareholders of the Acquiring Fund being solicited in connection with the Reorganization? |

We are seeking the approval of the Reorganization Agreement and the transactions contemplated therein, including the issuance of additional Acquiring Fund VRDP Shares, by the Acquiring Fund VRDP Holders, voting as a separate class pursuant to the governing document of the Acquiring Fund VRDP Shares. If Acquiring Fund VRDP Holders do not approve the Reorganization Agreement as a separate class, then the Reorganization will not occur.

viii

| Q: | How does the Board of my Fund suggest that I vote? |

| A: | After careful consideration, the Board of your Fund unanimously recommends that you vote “FOR” each of the items proposed for your Fund. |

| Q: | How do I vote my proxy? |

| A: | You may cast your vote by mail, phone, internet or in person at the Special Meeting. To vote by mail, please mark your vote on the enclosed proxy card and sign, date and return the card in the postage-paid envelope provided. If you choose to vote by phone or internet, please refer to the instructions found on the proxy card accompanying the Combined Proxy Statement/Prospectus. To vote by phone or internet, you will need the “control number” that appears on the proxy card. |

| Q: | Whom do I contact for further information? |

| A: | You may contact your financial advisor for further information. You may also call Georgeson Inc., the Funds’ proxy solicitor, at 1-866-628-6024. |

ix

THE BLACKROCK PENNSYLVANIA STRATEGIC MUNICIPAL TRUST

BLACKROCK MUNIYIELD PENNSYLVANIA QUALITY FUND

100 Bellevue Parkway

Wilmington, Delaware 19809

(800) 882-0052

NOTICE OF JOINT SPECIAL MEETING OF SHAREHOLDERS

TO BE HELD ON MARCH 12, 2015

Notice is hereby given that a joint special meeting of shareholders (the “Special Meeting”) of The BlackRock Pennsylvania Strategic Municipal Trust (NYSE MKT Ticker: BPS) (the “Target Fund”) and BlackRock MuniYield Pennsylvania Quality Fund (NYSE Ticker: MPA) (the “Acquiring Fund” and, together with the Target Fund, each, a “Fund”) will be held at the offices of BlackRock Advisors, LLC, 1 University Square Drive, Princeton, New Jersey 08540-6455, on March 12, 2015 at 4:30 p.m. (Eastern time) for the following purposes:

For Shareholders of the Target Fund:

Proposal 1(A): The holders of common shares (“Common Shares”) and holders of Variable Rate Demand Preferred Shares (“VRDP Shares”) of the Target Fund are being asked to vote as a single class on a proposal to approve an Agreement and Plan of Reorganization between the Target Fund and the Acquiring Fund (the “Reorganization Agreement”), pursuant to which (i) the Acquiring Fund will acquire substantially all of the Target Fund’s assets and assume substantially all of the Target Fund’s liabilities in exchange solely for newly issued Common Shares and VRDP Shares of the Acquiring Fund, which will be distributed to the common shareholders and holders of VRDP Shares (“VRDP Holders”), respectively, of the Target Fund (although cash may be distributed in lieu of fractional Common Shares), and (ii) the Target Fund will terminate its registration under the Investment Company Act of 1940, as amended (the “1940 Act”), and liquidate, dissolve and terminate in accordance with its agreement and declaration of trust and Delaware law.

Proposal 1(B): The VRDP Holders of the Target Fund are being asked to vote as a separate class on a proposal to approve the Reorganization Agreement and the transactions contemplated therein, including the termination of the Target Fund’s registration under the 1940 Act and the dissolution of the Target Fund under Delaware law.

For Shareholders of the Acquiring Fund:

Proposal 1(C): The VRDP Holders of the Acquiring Fund are being asked to vote as a separate class on a proposal to approve the Reorganization Agreement and the transactions contemplated therein, including the issuance of additional Acquiring Fund VRDP Shares.

Shareholders of record of each Fund as of the close of business on January 12, 2015 are entitled to notice of and to vote at the Special Meeting or any adjournment or postponement thereof.

The Target Fund is soliciting the vote of its common shareholders on proposal 1(A) through a Combined Proxy Statement/Prospectus.

Each Fund is separately soliciting the votes of its VRDP Holders on proposals 1(A), 1(B) and 1(C) through a separate Joint Proxy Statement and not through the Combined Proxy Statement/Prospectus.

THE BOARD OF TRUSTEES (EACH, A “BOARD”) OF EACH OF THE FUNDS RECOMMENDS THAT YOU VOTE YOUR SHARES BY INDICATING YOUR VOTING INSTRUCTIONS ON THE ENCLOSED PROXY CARD, DATING AND SIGNING SUCH PROXY CARD AND RETURNING IT IN THE ENVELOPE PROVIDED, WHICH IS ADDRESSED FOR YOUR CONVENIENCE AND NEEDS NO POSTAGE IF MAILED IN THE UNITED STATES, OR BY RECORDING YOUR VOTING INSTRUCTIONS BY TELEPHONE OR VIA THE INTERNET.

THE BOARD OF THE TARGET FUND UNANIMOUSLY RECOMMENDS THAT COMMON SHAREHOLDERS OF THE TARGET FUND CAST THEIR VOTE:

| - | FOR THE REORGANIZATION AGREEMENT AS DESCRIBED IN THE COMBINED PROXY STATEMENT/ PROSPECTUS. |

THE BOARD OF THE TARGET FUND UNANIMOUSLY RECOMMENDS THAT PREFERRED SHAREHOLDERS OF THE TARGET FUND CAST THEIR VOTE:

| - | FOR THE REORGANIZATION AGREEMENT AS DESCRIBED IN THE JOINT PROXY STATEMENT. |

THE BOARD OF THE ACQUIRING FUND UNANIMOUSLY RECOMMENDS THAT PREFERRED SHAREHOLDERS OF THE ACQUIRING FUND CAST THEIR VOTE:

| - | FOR THE REORGANIZATION AGREEMENT AS DESCRIBED IN THE JOINT PROXY STATEMENT. |

IN ORDER TO AVOID THE ADDITIONAL EXPENSE OF FURTHER SOLICITATION, WE ASK THAT YOU MAIL YOUR PROXY CARD OR RECORD YOUR VOTING INSTRUCTIONS BY TELEPHONE OR VIA THE INTERNET PROMPTLY.

For the Board of Trustees

JOHN M. PERLOWSKI

Chief Executive Officer and President of each Fund

January 21, 2015

YOUR VOTE IS IMPORTANT.

PLEASE VOTE PROMPTLY BY SIGNING AND RETURNING THE

ENCLOSED PROXY CARD OR BY RECORDING YOUR VOTING INSTRUCTIONS BY TELEPHONE OR VIA THE INTERNET, NO MATTER HOW MANY SHARES YOU OWN.

IMPORTANT NOTICE REGARDING THE AVAILABILITY OF PROXY MATERIALS FOR

THE SPECIAL MEETING OF SHAREHOLDERS TO BE HELD ON MARCH 12, 2015.

THE PROXY STATEMENT FOR THIS MEETING IS AVAILABLE AT:

HTTPS://WWW.PROXY-DIRECT.COM/BLK-26289

THE INFORMATION IN THIS COMBINED PROXY STATEMENT/PROSPECTUS IS NOT COMPLETE AND MAY BE CHANGED. WE MAY NOT SELL THESE SECURITIES UNTIL THE REGISTRATION STATEMENT FILED WITH THE SECURITIES AND EXCHANGE COMMISSION IS EFFECTIVE. THIS PROSPECTUS IS NOT AN OFFER TO SELL THESE SECURITIES AND IS NOT SOLICITING AN OFFER TO BUY THESE SECURITIES IN ANY STATE WHERE THE OFFER OR SALE IS NOT PERMITTED.

SUBJECT TO COMPLETION, DATED JANUARY 21, 2015

COMBINED PROXY STATEMENT/PROSPECTUS

THE BLACKROCK PENNSYLVANIA STRATEGIC MUNICIPAL TRUST

BLACKROCK MUNIYIELD PENNSYLVANIA QUALITY FUND

100 Bellevue Parkway

Wilmington, Delaware 19809

(800) 882-0052

This Combined Proxy Statement/Prospectus is furnished to you as a common shareholder of The BlackRock Pennsylvania Strategic Municipal Trust (NYSE MKT Ticker: BPS) (“BPS” or the “Target Fund”). A special meeting (the “Special Meeting”) of shareholders of the Target Fund and BlackRock MuniYield Pennsylvania Quality Fund (NYSE Ticker: MPA) (“MPA” or the “Acquiring Fund” and together with the Target Fund, each, a “Fund”) will be held at the offices of BlackRock Advisors, LLC (the “Investment Advisor”), 1 University Square Drive, Princeton, New Jersey 08540-6455, on March 12, 2015 at 4:30 p.m. (Eastern time) to consider the items listed below and discussed in greater detail elsewhere in this Combined Proxy Statement/Prospectus. If you are unable to attend the Special Meeting or any adjournment or postponement thereof, the Board of Trustees of the Target Fund (the “Board”) recommends that you vote your common shares of beneficial interests (“Common Shares”) by completing and returning the enclosed proxy card or by recording your voting instructions by telephone or via the internet. The approximate mailing date of this Combined Proxy Statement/Prospectus and accompanying form of proxy is February 2, 2015.

The purposes of the Special Meeting are:

For the Shareholders of the Target Fund:

Proposal 1(A): The common shareholders and holders of Variable Rate Demand Preferred Shares (“VRDP Shares”) of the Target Fund are being asked to vote as a single class on a proposal to approve an Agreement and Plan of Reorganization between the Target Fund and the Acquiring Fund (the “Reorganization Agreement”), pursuant to which (i) the Acquiring Fund will acquire substantially all of the Target Fund’s assets and assume substantially all of the Target Fund’s liabilities in exchange solely for newly issued Common Shares and VRDP Shares (collectively, the “Shares”) of the Acquiring Fund, which will be distributed to the Target Fund’s common shareholders (although cash may be distributed in lieu of fractional Common Shares) and holders of VRDP Shares (“VRDP Holders”), respectively, and (ii) the Target Fund will terminate its registration under the Investment Company Act of 1940, as amended (the “1940 Act”), and liquidate, dissolve and terminate in accordance with its agreement and declaration of trust and Delaware law.

Proposal 1(B): The VRDP Holders of the Target Fund are being asked to vote as a separate class on the proposal to approve the Reorganization Agreement and the transactions contemplated therein, including the termination of the Target Fund’s registration under the 1940 Act and the dissolution of the Target Fund under Delaware law.

For Shareholders of the Acquiring Fund:

Proposal 1(C): The VRDP Holders of the Acquiring Fund are being asked to vote as a separate class on the proposal to approve the Reorganization Agreement and the transactions contemplated therein, including the issuance of additional Acquiring Fund VRDP Shares.

Shareholders of record of each Fund as of the close of business on January 12, 2015 (the “Record Date”) are entitled to notice of and to vote at the Special Meeting or any adjournment or postponement thereof.

Shareholders of each Fund are entitled to one vote for each Share held, with no Shares having cumulative voting rights. VRDP Holders of each Fund will have equal voting rights with the common shareholders of such Fund with respect to the proposals that require the vote of the Fund’s VRDP Shares and Common Shares as a single class. The quorum and voting requirements for each Fund are described in the section herein entitled “Voting Information and Requirements.”

This Combined Proxy Statement/Prospectus is only being delivered to the common shareholders of the Target Fund. Each Fund is separately soliciting the votes of its respective VRDP Holders on each of the foregoing proposals that require the vote of VRDP Holders through a separate joint proxy statement and not through this Combined Proxy Statement/Prospectus.

The Reorganization Agreement that Fund shareholders are being asked to consider involves transactions that will be referred to in this Combined Proxy Statement/Prospectus as the “Reorganization.” The Fund surviving the Reorganization is referred to herein as the “Combined Fund.”

The Acquiring Fund is organized as a Massachusetts business trust and the Target Fund is organized as a Delaware statutory trust. Each Fund is a non-diversified closed-end investment company registered under the 1940 Act. The Reorganization seeks to achieve certain economies of scale and other operational efficiencies by combining two funds that have similar (but not identical) investment policies and investment restrictions.

In the Reorganization, the Acquiring Fund will acquire substantially all of the assets and assume substantially all of the liabilities of the Target Fund in exchange solely for newly issued Acquiring Fund Shares in the form of book entry interests. The Acquiring Fund will list the newly issued Common Shares on the New York Stock Exchange (“NYSE”). Such newly issued Acquiring Fund Shares will be distributed to the Target Fund shareholders (although cash may be distributed in lieu of fractional Common Shares) and the Target Fund will terminate its registration under the 1940 Act and liquidate, dissolve and terminate in accordance with its agreement and declaration of trust and Delaware law. The Acquiring Fund will continue to operate after the Reorganization as a registered, non-diversified, closed-end management investment company with the investment objective, investment policies and investment restrictions described in this Combined Proxy Statement/Prospectus.

As a result of the Reorganization, each common shareholder of the Target Fund will own Acquiring Fund Common Shares that (except for cash payments received in lieu of fractional Common Shares) will have an aggregate net asset value (“NAV”) (not the market value) immediately after the closing of the Reorganization equal to the aggregate NAV (not the market value) of that shareholder’s Target Fund Common Shares immediately prior to the effective date of the Reorganization (the “Closing Date”). The NAV of the Target Fund and the Acquiring Fund immediately prior to the closing of the Reorganization will be reduced by the costs of the Reorganization borne by each Fund, if any. The value of each Fund’s net assets will be calculated net of the liquidation preference (including accumulated and unpaid dividends) of all outstanding VRDP Shares of such Fund.

Each outstanding VRDP Share of the Target Fund will, without any action on the part of the holder thereof, be exchanged for one newly issued VRDP Share of the Acquiring Fund, which will have terms that are substantially similar to the terms of the Target Fund’s outstanding VRDP Shares, with the only significant difference being that the Target Fund VRDP Shares have a mandatory redemption date of July 1, 2042 and the newly issued Acquiring Fund VRDP Shares is expected to have a mandatory redemption date of June 1, 2041. The Acquiring Fund VRDP Shares to be issued in connection with the Reorganization will have terms that are substantially identical to the terms of the outstanding Acquiring Fund VRDP Shares and will rank on a parity with the Acquiring Fund’s existing VRDP Shares as to the payment of dividends and the distribution of assets upon dissolution, liquidation or winding up of the affairs of the Acquiring Fund. The Reorganization will not result in any changes to the terms of the Acquiring Fund’s VRDP Shares currently outstanding.

If the requisite shareholder approvals are not obtained, each Fund’s Board may take such actions as it deems in the best interests of its Fund, including conducting additional solicitations with respect to the proposals or continuing to operate the Fund as a stand-alone fund and the Investment Advisor may, in connection with the ongoing management of each Fund and its product line, recommend alternative proposals to the Board of each Fund.

ii

The Board of each Fund has determined that including these proposals in one Combined Proxy Statement/Prospectus will reduce costs and is in the best interests of each Fund’s shareholders.

This Combined Proxy Statement/Prospectus sets forth concisely the information that common shareholders of the Target Fund should know before voting on the proposal and constitutes an offering of the Acquiring Fund Common Shares. Please read it carefully and retain it for future reference. A Statement of Additional Information, dated January 21, 2015, relating to this Combined Proxy Statement/Prospectus (the “Statement of Additional Information”) has been filed with the United States Securities and Exchange Commission (the “SEC”) and is incorporated herein by reference. Copies of each Fund’s most recent annual report and semi-annual report can be obtained on a website maintained by BlackRock, Inc. (“BlackRock”) at www.blackrock.com. In addition, each Fund will furnish, without charge, a copy of the Statement of Additional Information, or its most recent annual report or semi-annual report to any shareholder upon request. Any such request should be directed to BlackRock by calling (800) 882-0052 or by writing to the respective Fund at 100 Bellevue Parkway, Wilmington, Delaware 19809. The Statement of Additional Information and the annual and semi-annual reports of each Fund are available on the EDGAR Database on the SEC’s website at www.sec.gov. The address of the principal executive offices of the Funds is 100 Bellevue Parkway, Wilmington, Delaware 19809, and the telephone number is (800) 882-0052.

The Funds are subject to the informational requirements of the Securities Exchange Act of 1934 (the “Exchange Act”) and the 1940 Act and, in accordance therewith, file reports, proxy statements, proxy materials and other information with the SEC. Materials filed with the SEC can be reviewed and copied at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549 or downloaded from the SEC’s website at www.sec.gov. Information on the operation of the SEC’s Public Reference Room may be obtained by calling the SEC at (202) 551-8090. You may also request copies of these materials, upon payment at the prescribed rates of a duplicating fee, by electronic request to the SEC’s e-mail address (publicinfo@sec.gov) or by writing the Public Reference Branch, Office of Consumer Affairs and Information Services, Securities and Exchange Commission, Washington, D.C. 20549-0102.

BlackRock updates performance information for the Funds, as well as certain other information for the Funds, on a monthly basis on its website in the “Closed-End Funds” section of www.blackrock.com. Shareholders are advised to periodically check the website for updated performance information and other information about the Funds. References to BlackRock’s website are intended to allow investors public access to information regarding the Funds and do not, and are not intended to, incorporate BlackRock’s website in this Combined Proxy Statement/Prospectus.

Please note that only one copy of shareholder documents, including annual or semi-annual reports and proxy materials, may be delivered to two or more shareholders of the Funds who share an address, unless the Funds have received instructions to the contrary. This practice is commonly called “householding” and it is intended to reduce expenses and eliminate duplicate mailings of shareholder documents. Mailings of your shareholder documents may be householded indefinitely unless you instruct us otherwise. To request a separate copy of any shareholder document or for instructions as to how to request a separate copy of these documents or as to how to request a single copy if multiple copies of these documents are received, shareholders should contact the Fund at the address and phone number set forth above.

The Common Shares of BlackRock MuniYield Pennsylvania Quality Fund are listed on the NYSE under the ticker symbol “MPA” and will continue to be so listed after the completion of the Reorganization. The Common Shares of The BlackRock Pennsylvania Strategic Municipal Trust are listed on the NYSE MKT under the ticker symbol “BPS.” Reports, proxy statements and other information concerning the Funds may be inspected at the offices of the NYSE, 20 Broad Street, New York, New York 10005.

This Combined Proxy Statement/Prospectus serves as a prospectus of the Acquiring Fund in connection with the issuance of the newly issued Acquiring Fund Common Shares in connection with the Reorganization

iii

(the “Issuance”). No person has been authorized to give any information or make any representation not contained in this Combined Proxy Statement/Prospectus and, if so given or made, such information or representation must not be relied upon as having been authorized. This Combined Proxy Statement/Prospectus does not constitute an offer to sell or a solicitation of an offer to buy any securities in any jurisdiction in which, or to any person to whom, it is unlawful to make such offer or solicitation.

Photographic identification and proof of ownership will be required for admission to the meeting. For directions to the meeting, please contact Georgeson Inc., the firm assisting us in the solicitation of proxies, at 1-866-628-6024.

THE SEC HAS NOT APPROVED OR DISAPPROVED THESE SECURITIES OR PASSED UPON THE ADEQUACY OF THIS COMBINED PROXY STATEMENT/PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

The date of this Combined Proxy Statement/Prospectus is January 21, 2015.

iv

| 1 | ||||

| 11 | ||||

| 12 | ||||

| 34 | ||||

| 46 | ||||

| 47 | ||||

| 68 | ||||

| 80 | ||||

| 83 | ||||

| 85 | ||||

| 90 | ||||

| 94 | ||||

| 96 | ||||

| 98 | ||||

| 100 | ||||

| 101 | ||||

| 101 | ||||

| 102 | ||||

| 102 | ||||

| CERTAIN U.S. FEDERAL INCOME TAX CONSEQUENCES OF THE REORGANIZATION |

102 | |||

| 105 | ||||

| 107 | ||||

| 107 | ||||

| 108 | ||||

| 108 | ||||

| 108 | ||||

| 108 | ||||

| 108 | ||||

| 109 | ||||

| 109 | ||||

| 110 |

v

The following is a summary of certain information contained elsewhere in this Combined Proxy Statement/Prospectus and is qualified in its entirety by reference to the more complete information contained in this Combined Proxy Statement/Prospectus and in the Statement of Additional Information. Shareholders should read the entire Combined Proxy Statement/Prospectus carefully.

| The Proposed Reorganization |

Assuming the Reorganization receives the requisite shareholder approvals, the Acquiring Fund will acquire substantially all of the assets and assume substantially all of the liabilities of the Target Fund in exchange solely for newly issued Acquiring Fund Shares in the form of book entry interests. The Acquiring Fund will list the newly issued Common Shares on the NYSE. Such newly issued Acquiring Fund Shares will be distributed to the Target Fund shareholders (although cash may be distributed in lieu of fractional Common Shares) and the Target Fund will terminate its registration under the 1940 Act and liquidate, dissolve and terminate in accordance with its agreement and declaration of trust and Delaware law. The Acquiring Fund will continue to operate after the Reorganization as a registered, non-diversified, closed-end management investment company with the investment objective, investment policies and investment restrictions described in this Combined Proxy Statement/Prospectus. |

| As a result of the Reorganization, each common shareholder of the Target Fund will own Acquiring Fund Common Shares that (except for cash payments received in lieu of fractional Common Shares) will have an aggregate NAV (not the market value) immediately after the closing of the Reorganization equal to the aggregate NAV (not the market value) of that shareholder’s Target Fund Common Shares immediately prior to the Closing Date. The NAV of the Target Fund and the Acquiring Fund immediately prior to the closing of the Reorganization will be reduced by the costs of the Reorganization borne by each Fund, if any. The value of each Fund’s net assets will be calculated net of the liquidation preference (including accumulated and unpaid dividends) of all outstanding VRDP Shares of such Fund. |

| Each outstanding VRDP Share of the Target Fund will, without any action on the part of the holder thereof, be exchanged for one newly issued VRDP Share of the Acquiring Fund, which will have terms that are substantially similar to the terms of the Target Fund’s outstanding VRDP Shares. The Reorganization will not result in any changes to the terms of the Acquiring Fund’s VRDP Shares currently outstanding. |

| Subject to the requisite approval of the shareholders of each Fund with respect to the Reorganization, it is expected that the Closing Date of the Reorganization will be sometime during the second quarter of 2015, but it may be at a different time as described herein. |

| If the Reorganization is not consummated, then each Fund will continue to operate for the time being as a stand-alone Delaware statutory trust or Massachusetts business trust, as applicable, and will |

1

| continue to be advised by the Investment Advisor. However, if the Reorganization is not consummated, the Investment Advisor may, in connection with ongoing management of each Fund and its product line, recommend alternative proposals to the Board of each Fund. |

| Background and Reasons for the Proposed Reorganization |

The proposed Reorganization seeks to achieve certain economies of scale and other operational efficiencies by combining two funds that have similar (but not identical) investment objectives, investment policies, investment restrictions and portfolio compositions and are managed by the same investment advisor and portfolio management team. |

| The proposed Reorganization is intended to result in the following potential benefits to common shareholders: (i) lower total expenses per Common Share for common shareholders of each Fund (as common shareholders of the Combined Fund following the Reorganization) due to economies of scale resulting from the larger size of the Combined Fund; (ii) improved earnings yield on NAV for common shareholders of the Target Fund and a comparable (i.e., the same or slightly lower or higher) earnings yield on NAV for common shareholders of the Acquiring Fund; (iii) improved secondary market trading of the Common Shares; and (iv) operating and administrative efficiencies for the Combined Fund, including the potential for the following: (a) greater investment flexibility and investment options; (b) greater diversification of portfolio investments; (c) the ability to trade in larger positions and more favorable transaction terms; (d) benefits from having fewer closed-end funds offering similar products in the market, including an increased focus by investors on the remaining funds in the market (including the Combined Fund) and additional research coverage; and (e) benefits from having fewer similar funds in the same fund complex, including a simplified operational model and a reduction in risk of operational, legal and financial errors. |

| The Board of Trustees (the “Board”) of each Fund, including the trustees (“Board Members”) who are not “interested persons” of each Fund (as defined in the 1940 Act) (“Independent Board Members”), has unanimously approved the Reorganization, concluding that the Reorganization is in the best interests of its Fund and that the interests of existing common shareholders and VRDP Holders of its Fund will not be diluted with respect to NAV and liquidation preference, respectively, as a result of the Reorganization. As a result of the Reorganization, however, common and preferred shareholders of each Fund will hold a reduced percentage of ownership in the larger Combined Fund than they did in any of the individual Funds before the Reorganization. The Board’s conclusion was based on each Board Member’s business judgment after consideration of all relevant factors taken as a whole with respect to its Fund and the Fund’s common and preferred shareholders, although individual Board Members may have placed different weight on various factors and assigned different degrees of materiality to various factors. Please see |

2

| “Information about the Reorganization—Reasons for the Reorganization” for additional information about the factors considered by each Board. |

| Net and Managed Assets |

As of December 31, 2014, the Target Fund has $30,069,794 in net assets and $47,913,233 in managed assets, and the Acquiring Fund has $185,462,976 in net assets and $288,829,183 in managed assets. |

| Total Expenses and Management Fees |

For the fiscal year ended July 31, 2014, the Total Expense Ratio for the Acquiring Fund was 1.48%. For the fiscal year ended April 30, 2014, the Total Expense Ratio for the Target Fund was 2.08%. “Total Expenses” means a Fund’s total annual operating expenses (including interest expenses). “Total Expense Ratio” means a Fund’s Total Expenses expressed as a percentage of its average net assets attributable to its Common Shares. |

| As of July 31, 2014, the historical and pro forma Total Expense Ratios applicable to the Reorganization are as follows: |

| Target Fund (BPS) |

Acquiring Fund (MPA) | Pro Forma Combined Fund (MPA) | ||

| 2.05% |

1.48% | 1.48% |

| The Funds estimate that the completion of the Reorganization would result in a Total Expense Ratio for the Combined Fund of 1.48% on a historical and pro forma basis for the 12-month period ended July 31, 2014, representing a reduction in the Total Expense Ratio for the common shareholders of the Target Fund of 0.57% and no impact on the Total Expense Ratio for the common shareholders of the Acquiring Fund. |

| The Target Fund currently pays the Investment Advisor a monthly fee at an annual contractual management fee rate of 0.60% of the Target Fund’s average weekly net assets. Average weekly net assets are the average weekly value of the Target Fund’s total assets minus its total accrued liabilities. The Acquiring Fund currently pays the Investment Advisor a monthly fee at an annual contractual management fee rate of 0.50% of the Acquiring Fund’s average daily net assets. Average daily net assets are the average daily value of the Acquiring Fund’s total assets minus its total accrued liabilities. If the Reorganization is consummated, the annual contractual management fee rate of the Combined Fund will be reduced to 0.49% of the average daily net assets of the Combined Fund. Based on a pro-forma Lipper expense universe for the Combined Fund, the estimated total annual fund operating expenses (excluding investment related expenses) and contractual management fee rate are each expected to be in the first quartile. |

| There can be no assurance that future expenses will not increase or that any expense savings for any Fund will be realized as a result of the Reorganization. |

3

| Earnings, Distributions and Undistributed Net Investment Income |

Earnings and Distribution Rate: The Combined Fund’s earnings yield on NAV following the Reorganization is expected to be comparable (i.e., the same or slightly lower or higher) to the Acquiring Fund’s current earnings yield on NAV and potentially higher than the Target Fund’s current earnings yield on NAV; thus, assuming that the Reorganization is consummated and that the Acquiring Fund’s distribution policy remains in place after the Reorganization, common shareholders of the Acquiring Fund may experience a distribution rate on NAV comparable (i.e., the same or slightly lower or higher) to their current distribution rate on NAV and common shareholders of the Target Fund may experience a distribution rate on NAV that is potentially higher than their current distribution rate on NAV. The Combined Fund’s earnings and distribution rate on NAV will change over time, and depending on market conditions, may be significantly higher or lower than each Fund’s earnings and distribution rate on NAV prior to the Reorganization. A Fund’s earnings and net investment income are variables which depend on many factors, including its asset mix, portfolio turnover level, the amount of leverage utilized by the Fund, the costs of such leverage, the performance of its investments, the movement of interest rates and general market conditions. There can be no assurance that the future earnings of a Fund, including the Combined Fund after the Reorganization, will remain constant. |

| Distribution Policy: Each Fund intends to make regular monthly cash distributions of all or a portion of its net investment income to holders of such Fund’s shares of common stock, except as described below under “Undistributed Net Investment Income.” Each Fund intends to pay any capital gains distributions at least annually. A return of capital distribution may involve a return of the common shareholder’s original investment. Though not currently taxable, such a distribution may lower a common shareholder’s basis in such Fund, thus potentially subjecting the common shareholder to future tax consequences in connection with the sale of Fund Common Shares, even if sold at a loss to the common shareholder’s original investment. When total distributions exceed total return performance for the period, the difference will reduce a Fund’s total assets and NAV and, therefore, could have the effect of increasing the Fund’s expense ratio and reducing the amount of assets the Fund has available for long term investment. |

| Automatic Dividend Reinvestment: Common shareholders of each Fund will automatically have all dividends and distributions reinvested in Common Shares of such Fund in accordance with such Fund’s dividend reinvestment plan, unless an election is made to receive cash by contacting the Reinvestment Plan Agent (as defined herein), at (800) 699-1236. See “Automatic Dividend Reinvestment Plan.” |

4

| Undistributed Net Investment Income: If the Reorganization is approved by shareholders, then substantially all of the undistributed net investment income, if any, of each Fund is expected to be declared to such Fund’s common shareholders prior to the Closing Date (the “Pre-Reorganization Declared UNII Distributions”). The declaration date, ex-dividend date (the “Ex-Dividend Date”) and record date of the Pre-Reorganization Declared UNII Distributions will occur prior to the Closing Date. However, all or a significant portion of the Pre-Reorganization Declared UNII Distributions may be paid in one or more distributions to common shareholders of the Funds entitled to such Pre-Reorganization Declared UNII Distributions after the Closing Date. In addition, BlackRock MuniYield Pennsylvania Quality Fund (MPA) does not currently expect to declare any distributions during the first month following the Closing Date. Accordingly, persons who purchase Common Shares of any of the Funds on or after the Ex-Dividend Date for the Pre-Reorganization Declared UNII Distributions should not expect to receive any distributions from any Fund until distributions, if any, are declared by the Board of the Combined Fund and paid to shareholders entitled to any such distributions. No such distributions are expected to be paid by the Combined Fund until at least approximately two months following the Closing Date. |

| The Combined Fund’s earnings and distribution rate on NAV will change over time, and depending on market conditions, may be significantly higher or lower than each Fund’s earnings and distribution rate on NAV prior to the Reorganization. Each Fund reserves the right to change its distribution policy with respect to common share distributions and the basis for establishing the rate of its monthly distributions for the Common Shares at any time and may do so without prior notice to common shareholders. The payment of any distributions by any Fund is subject to, and will only be made when, as and if, declared by the Board of such Fund. There is no assurance the Board of any Fund will declare any distributions for such Fund. To the extent any Pre-Reorganization Declared UNII Distributions is not an “exempt interest dividend” (as defined in the Code), the distribution may be taxable to shareholders for U.S. Federal income tax purposes. |

| Premium/Discount to NAV of Common Shares |

The Common Shares of each Fund have historically traded at both a premium and a discount. The table below sets forth the market price, NAV, and the premium/discount to NAV of each Fund as of December 31, 2014. |

| Fund |

Market Price | NAV | Premium/(Discount) to NAV | |||

| MPA |

$14.34 | $16.12 | (11.04)% | |||

| BPS |

$12.78 | $14.80 | (13.65)% |

5

| To the extent the Target Fund Common Shares are trading at a wider discount (or a narrower premium) than the Acquiring Fund at the time of the Reorganization, the Target Fund’s common shareholders would have the potential for an economic benefit by the narrowing of the discount or widening of the premium. To the extent the Target Fund Common Shares are trading at a narrower discount (or wider premium) than the Acquiring Fund at the time of the Reorganization, Target Fund common shareholders may be negatively impacted if the Reorganization is consummated. Acquiring Fund common shareholders would only benefit from a premium/discount perspective to the extent the Acquiring Fund’s post-Reorganization discount (or premium) improves. There can be no assurance that, after the Reorganization, Common Shares of the Combined Fund will trade at a narrower discount to NAV or wider premium to NAV than the Common Shares of any individual Fund prior to the Reorganization. |

| In the Reorganization, common shareholders of the Target Fund will receive Acquiring Fund Common Shares based on the relative NAVs (not the market values) of the respective Fund’s Common Shares. The market value of the Common Shares of the Combined Fund may be less than the market value of the Common Shares of each respective Fund prior to the Reorganization. |

| VRDP Shares |

As of December 31, 2014, the Target Fund has 163 Series W-7 VRDP Shares outstanding, and the Acquiring Fund has 663 Series W-7 VRDP Shares outstanding. In connection with the Reorganization, the Acquiring Fund expects to issue 163 additional Acquiring Fund VRDP Shares to Target Fund VRDP Holders. Following the completion of the Reorganization, the Combined Fund is expected to have 826 VRDP Shares outstanding. |

| Upon the closing of the Reorganization, the Target Fund VRDP Holders will receive on a one-for-one basis one newly issued VRDP Share of the Acquiring Fund, par value $0.05 per share and with a liquidation preference of $100,000 per share (plus any accumulated and unpaid dividends that have accrued on such Target Fund VRDP Share up to and including the day immediately preceding the Closing Date if such dividends have not been paid prior to the Closing Date), in exchange for each Target Fund VRDP Share held by such Target Fund VRDP Holder immediately prior to the closing of the Reorganization. The newly issued Acquiring Fund VRDP Share may be of the same series as the Acquiring Fund’s Series W-7 VRDP Shares or a substantially identical series. No fractional Acquiring Fund VRDP Shares will be issued. Target Fund VRDP Holders will receive the same number of Acquiring Fund VRDP Shares, with terms substantially similar to the outstanding Target Fund VRDP Shares, held by such holders immediately prior to the closing of the Reorganization, with the only significant difference being that the Target Fund VRDP Shares have a mandatory redemption date of July 1, 2042 and the newly issued Acquiring Fund VRDP Shares is expected to have a mandatory redemption date of June 1, 2041. |

6