000008908912/31December 31, 20222022FYFALSE153,048,775http://fasb.org/us-gaap/2022#LongTermDebtAndCapitalLeaseObligationshttp://fasb.org/us-gaap/2022#LongTermDebtAndCapitalLeaseObligationshttp://fasb.org/us-gaap/2022#LongTermDebtAndCapitalLeaseObligationshttp://fasb.org/us-gaap/2022#Revenues00000890892022-01-012022-12-3100000890892022-06-30iso4217:USD00000890892023-02-15xbrli:shares00000890892021-01-012021-12-310000089089us-gaap:ProductMember2022-01-012022-12-310000089089us-gaap:ProductMember2021-01-012021-12-310000089089us-gaap:ProductMember2020-01-012020-12-310000089089us-gaap:ServiceMember2022-01-012022-12-310000089089us-gaap:ServiceMember2021-01-012021-12-310000089089us-gaap:ServiceMember2020-01-012020-12-310000089089us-gaap:ProductAndServiceOtherMember2022-01-012022-12-310000089089us-gaap:ProductAndServiceOtherMember2021-01-012021-12-310000089089us-gaap:ProductAndServiceOtherMember2020-01-012020-12-3100000890892020-01-012020-12-31iso4217:USDxbrli:shares00000890892022-12-3100000890892021-12-3100000890892020-12-3100000890892019-12-310000089089us-gaap:CommonStockMember2019-12-310000089089us-gaap:TreasuryStockMember2019-12-310000089089us-gaap:AdditionalPaidInCapitalMember2019-12-310000089089us-gaap:RetainedEarningsMember2019-12-310000089089us-gaap:AccumulatedOtherComprehensiveIncomeMember2019-12-310000089089us-gaap:NoncontrollingInterestMember2019-12-310000089089us-gaap:CommonStockMember2020-01-012020-12-310000089089us-gaap:TreasuryStockMember2020-01-012020-12-310000089089us-gaap:AdditionalPaidInCapitalMember2020-01-012020-12-310000089089us-gaap:RetainedEarningsMember2020-01-012020-12-310000089089us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-01-012020-12-310000089089us-gaap:NoncontrollingInterestMember2020-01-012020-12-310000089089us-gaap:CommonStockMember2020-12-310000089089us-gaap:TreasuryStockMember2020-12-310000089089us-gaap:AdditionalPaidInCapitalMember2020-12-310000089089us-gaap:RetainedEarningsMember2020-12-310000089089us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-12-310000089089us-gaap:NoncontrollingInterestMember2020-12-310000089089us-gaap:CommonStockMember2021-01-012021-12-310000089089us-gaap:TreasuryStockMember2021-01-012021-12-310000089089us-gaap:AdditionalPaidInCapitalMember2021-01-012021-12-310000089089us-gaap:RetainedEarningsMember2021-01-012021-12-310000089089us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-01-012021-12-310000089089us-gaap:NoncontrollingInterestMember2021-01-012021-12-310000089089us-gaap:CommonStockMember2021-12-310000089089us-gaap:TreasuryStockMember2021-12-310000089089us-gaap:AdditionalPaidInCapitalMember2021-12-310000089089us-gaap:RetainedEarningsMember2021-12-310000089089us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-12-310000089089us-gaap:NoncontrollingInterestMember2021-12-310000089089us-gaap:CommonStockMember2022-01-012022-12-310000089089us-gaap:TreasuryStockMember2022-01-012022-12-310000089089us-gaap:AdditionalPaidInCapitalMember2022-01-012022-12-310000089089us-gaap:RetainedEarningsMember2022-01-012022-12-310000089089us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-01-012022-12-310000089089us-gaap:NoncontrollingInterestMember2022-01-012022-12-310000089089us-gaap:CommonStockMember2022-12-310000089089us-gaap:TreasuryStockMember2022-12-310000089089us-gaap:AdditionalPaidInCapitalMember2022-12-310000089089us-gaap:RetainedEarningsMember2022-12-310000089089us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-12-310000089089us-gaap:NoncontrollingInterestMember2022-12-310000089089sci:FuneralMemberus-gaap:TradeAccountsReceivableMember2022-12-310000089089sci:CemeteryMemberus-gaap:TradeAccountsReceivableMember2022-12-310000089089sci:MiscellaneousAccountsReceivableMember2022-12-310000089089us-gaap:NotesReceivableMember2022-12-310000089089sci:FuneralMemberus-gaap:TradeAccountsReceivableMember2021-12-310000089089sci:CemeteryMemberus-gaap:TradeAccountsReceivableMember2021-12-310000089089sci:MiscellaneousAccountsReceivableMember2021-12-310000089089us-gaap:NotesReceivableMember2021-12-310000089089us-gaap:NotesReceivableMembersci:LongTermMember2022-12-310000089089us-gaap:NotesReceivableMembersci:LongTermMember2021-12-310000089089sci:MiscellaneousAccountsReceivableMembersci:LongTermMember2022-12-310000089089sci:MiscellaneousAccountsReceivableMembersci:LongTermMember2021-12-310000089089sci:FuneralMemberus-gaap:TradeAccountsReceivableMember2022-01-012022-12-310000089089sci:CemeteryMemberus-gaap:TradeAccountsReceivableMember2022-01-012022-12-310000089089us-gaap:TradeAccountsReceivableMember2021-12-310000089089us-gaap:TradeAccountsReceivableMember2022-01-012022-12-310000089089us-gaap:TradeAccountsReceivableMember2022-12-310000089089sci:CurrentMembersci:MiscellaneousAccountsReceivableMember2021-12-310000089089sci:CurrentMembersci:MiscellaneousAccountsReceivableMember2022-01-012022-12-310000089089sci:CurrentMembersci:MiscellaneousAccountsReceivableMember2022-12-310000089089sci:MiscellaneousAccountsReceivableMembersci:LongTermMember2022-01-012022-12-310000089089sci:MiscellaneousAccountsReceivableMember2022-01-012022-12-310000089089us-gaap:NotesReceivableMember2022-01-012022-12-310000089089us-gaap:FinancingReceivables1To29DaysPastDueMembersci:CurrentMembersci:MiscellaneousAccountsReceivableMember2022-12-310000089089us-gaap:Maturity30To90DaysMembersci:CurrentMembersci:MiscellaneousAccountsReceivableMember2022-12-310000089089sci:CurrentMembersci:FinancingReceivables90To180DaysPastDueMembersci:MiscellaneousAccountsReceivableMember2022-12-310000089089sci:CurrentMembersci:FinancingReceivablesEqualToGreaterThan180DaysPastDueMembersci:MiscellaneousAccountsReceivableMember2022-12-310000089089us-gaap:FinancingReceivables1To29DaysPastDueMembersci:MiscellaneousAccountsReceivableMembersci:LongTermMember2022-12-310000089089us-gaap:Maturity30To90DaysMembersci:MiscellaneousAccountsReceivableMembersci:LongTermMember2022-12-310000089089sci:FinancingReceivables90To180DaysPastDueMembersci:MiscellaneousAccountsReceivableMembersci:LongTermMember2022-12-310000089089sci:FinancingReceivablesEqualToGreaterThan180DaysPastDueMembersci:MiscellaneousAccountsReceivableMembersci:LongTermMember2022-12-310000089089us-gaap:FinancingReceivables1To29DaysPastDueMembersci:MiscellaneousAccountsReceivableMember2022-12-310000089089us-gaap:Maturity30To90DaysMembersci:MiscellaneousAccountsReceivableMember2022-12-310000089089sci:FinancingReceivables90To180DaysPastDueMembersci:MiscellaneousAccountsReceivableMember2022-12-310000089089sci:FinancingReceivablesEqualToGreaterThan180DaysPastDueMembersci:MiscellaneousAccountsReceivableMember2022-12-310000089089us-gaap:FinancingReceivables1To29DaysPastDueMemberus-gaap:NotesReceivableMember2022-12-310000089089us-gaap:Maturity30To90DaysMemberus-gaap:NotesReceivableMember2022-12-310000089089us-gaap:NotesReceivableMembersci:FinancingReceivables90To180DaysPastDueMember2022-12-310000089089us-gaap:NotesReceivableMembersci:FinancingReceivablesEqualToGreaterThan180DaysPastDueMember2022-12-310000089089us-gaap:BuildingAndBuildingImprovementsMembersrt:MinimumMember2022-01-012022-12-310000089089srt:MaximumMemberus-gaap:BuildingAndBuildingImprovementsMember2022-01-012022-12-310000089089us-gaap:EquipmentMembersrt:MinimumMember2022-01-012022-12-310000089089srt:MaximumMemberus-gaap:EquipmentMember2022-01-012022-12-310000089089srt:MaximumMemberus-gaap:LeaseholdImprovementsMember2022-01-012022-12-310000089089srt:MinimumMember2022-01-012022-12-310000089089srt:MaximumMember2022-01-012022-12-31xbrli:pure0000089089sci:FuneralMember2022-12-310000089089sci:CemeteryMember2022-12-310000089089sci:FuneralMember2021-12-310000089089sci:CemeteryMember2021-12-310000089089sci:FuneralMembersci:FinancingReceivables30To90DaysPastDueMember2022-12-310000089089sci:FuneralMembersci:FinancingReceivables91To180DaysPastDueMember2022-12-310000089089sci:FuneralMembersci:FinancingReceivablesEqualToGreaterThan180DaysPastDueMember2022-12-310000089089us-gaap:FinancingReceivables1To29DaysPastDueMembersci:CemeteryMember2022-12-310000089089sci:CemeteryMembersci:FinancingReceivables30To90DaysPastDueMember2022-12-310000089089sci:FinancingReceivables91To180DaysPastDueMembersci:CemeteryMember2022-12-310000089089sci:CemeteryMembersci:FinancingReceivablesEqualToGreaterThan180DaysPastDueMember2022-12-310000089089us-gaap:FinancingReceivables1To29DaysPastDueMember2022-12-310000089089sci:FinancingReceivables30To90DaysPastDueMember2022-12-310000089089sci:FinancingReceivables91To180DaysPastDueMember2022-12-310000089089sci:FinancingReceivablesEqualToGreaterThan180DaysPastDueMember2022-12-310000089089sci:FuneralMember2022-01-012022-12-310000089089sci:CemeteryMember2022-01-012022-12-3100000890892020-01-012020-03-310000089089us-gaap:USTreasurySecuritiesMemberus-gaap:FairValueInputsLevel2Member2022-12-310000089089us-gaap:FairValueInputsLevel2Memberus-gaap:ForeignGovernmentDebtSecuritiesMember2022-12-310000089089us-gaap:FairValueInputsLevel2Memberus-gaap:CorporateDebtSecuritiesMember2022-12-310000089089us-gaap:FairValueInputsLevel2Memberus-gaap:ResidentialMortgageBackedSecuritiesMember2022-12-310000089089us-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueInputsLevel2Member2022-12-310000089089sci:PreferredStockSecuritiesMemberus-gaap:FairValueInputsLevel2Member2022-12-310000089089us-gaap:FairValueInputsLevel1Membersci:UsCommonStockSecuritiesMember2022-12-310000089089us-gaap:FairValueInputsLevel1Membersci:CanadaCommonStockSecuritiesMember2022-12-310000089089us-gaap:FairValueInputsLevel1Membersci:OtherInternationalCommonStockSecuritiesMember2022-12-310000089089us-gaap:FairValueInputsLevel1Memberus-gaap:EquityFundsMember2022-12-310000089089us-gaap:FairValueInputsLevel1Memberus-gaap:FixedIncomeFundsMember2022-12-310000089089sci:CommingledfundsFixedincMemberus-gaap:CarryingReportedAmountFairValueDisclosureMember2022-12-310000089089sci:CommingledfundsEquityMemberus-gaap:CarryingReportedAmountFairValueDisclosureMember2022-12-310000089089us-gaap:MoneyMarketFundsMemberus-gaap:CarryingReportedAmountFairValueDisclosureMember2022-12-310000089089us-gaap:PrivateEquityFundsMemberus-gaap:CarryingReportedAmountFairValueDisclosureMember2022-12-310000089089us-gaap:CarryingReportedAmountFairValueDisclosureMember2022-12-310000089089us-gaap:EstimateOfFairValueFairValueDisclosureMember2022-12-310000089089us-gaap:USTreasurySecuritiesMemberus-gaap:FairValueInputsLevel2Member2021-12-310000089089us-gaap:FairValueInputsLevel2Memberus-gaap:ForeignGovernmentDebtSecuritiesMember2021-12-310000089089us-gaap:FairValueInputsLevel2Memberus-gaap:CorporateDebtSecuritiesMember2021-12-310000089089us-gaap:FairValueInputsLevel2Memberus-gaap:ResidentialMortgageBackedSecuritiesMember2021-12-310000089089us-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueInputsLevel2Member2021-12-310000089089sci:PreferredStockSecuritiesMemberus-gaap:FairValueInputsLevel2Member2021-12-310000089089us-gaap:FairValueInputsLevel1Membersci:UsCommonStockSecuritiesMember2021-12-310000089089us-gaap:FairValueInputsLevel1Membersci:CanadaCommonStockSecuritiesMember2021-12-310000089089us-gaap:FairValueInputsLevel1Membersci:OtherInternationalCommonStockSecuritiesMember2021-12-310000089089us-gaap:FairValueInputsLevel1Memberus-gaap:EquityFundsMember2021-12-310000089089us-gaap:FairValueInputsLevel1Memberus-gaap:FixedIncomeFundsMember2021-12-310000089089us-gaap:FairValueInputsLevel3Memberus-gaap:OtherInvestmentsMember2021-12-310000089089us-gaap:EstimateOfFairValueFairValueDisclosureMember2021-12-310000089089sci:CommingledfundsFixedincMemberus-gaap:CarryingReportedAmountFairValueDisclosureMember2021-12-310000089089sci:CommingledfundsEquityMemberus-gaap:CarryingReportedAmountFairValueDisclosureMember2021-12-310000089089us-gaap:MoneyMarketFundsMemberus-gaap:CarryingReportedAmountFairValueDisclosureMember2021-12-310000089089us-gaap:PrivateEquityFundsMemberus-gaap:CarryingReportedAmountFairValueDisclosureMember2021-12-310000089089sci:ReportedAtNetAssetValueMemberus-gaap:CarryingReportedAmountFairValueDisclosureMember2021-12-310000089089us-gaap:EstimateOfFairValueFairValueDisclosureMember2021-12-310000089089sci:FuneralMember2020-12-310000089089sci:CemeteryMember2020-12-310000089089sci:FuneralMember2021-01-012021-12-310000089089sci:CemeteryMember2021-01-012021-12-310000089089us-gaap:NoncompeteAgreementsMembersrt:MinimumMember2022-01-012022-12-310000089089us-gaap:NoncompeteAgreementsMembersrt:MaximumMember2022-01-012022-12-310000089089us-gaap:NoncompeteAgreementsMember2022-12-310000089089us-gaap:NoncompeteAgreementsMember2021-12-310000089089us-gaap:CustomerRelationshipsMembersrt:MinimumMember2022-01-012022-12-310000089089us-gaap:CustomerRelationshipsMembersrt:MaximumMember2022-01-012022-12-310000089089us-gaap:CustomerRelationshipsMember2022-12-310000089089us-gaap:CustomerRelationshipsMember2021-12-310000089089us-gaap:TradeNamesMembersrt:MinimumMember2022-01-012022-12-310000089089us-gaap:TradeNamesMembersrt:MaximumMember2022-01-012022-12-310000089089us-gaap:TradeNamesMember2022-12-310000089089us-gaap:TradeNamesMember2021-12-310000089089us-gaap:OtherIntangibleAssetsMembersrt:MinimumMember2022-01-012022-12-310000089089us-gaap:OtherIntangibleAssetsMembersrt:MaximumMember2022-01-012022-12-310000089089us-gaap:OtherIntangibleAssetsMember2022-12-310000089089us-gaap:OtherIntangibleAssetsMember2021-12-310000089089us-gaap:InternalRevenueServiceIRSMember2022-01-012022-12-310000089089us-gaap:StateAndLocalJurisdictionMember2022-01-012022-12-310000089089us-gaap:ForeignCountryMember2022-01-012022-12-310000089089us-gaap:InternalRevenueServiceIRSMember2022-12-310000089089us-gaap:StateAndLocalJurisdictionMember2022-12-310000089089us-gaap:ForeignCountryMember2022-12-310000089089sci:April2027Memberus-gaap:UnsecuredDebtMember2022-12-310000089089sci:April2027Memberus-gaap:UnsecuredDebtMember2021-12-310000089089us-gaap:UnsecuredDebtMembersci:December2027Member2022-12-310000089089us-gaap:UnsecuredDebtMembersci:December2027Member2021-12-310000089089sci:June2029Memberus-gaap:UnsecuredDebtMember2022-12-310000089089sci:June2029Memberus-gaap:UnsecuredDebtMember2021-12-310000089089sci:August2030Memberus-gaap:UnsecuredDebtMember2022-12-310000089089sci:August2030Memberus-gaap:UnsecuredDebtMember2021-12-310000089089sci:May2031Memberus-gaap:UnsecuredDebtMember2022-12-310000089089sci:May2031Memberus-gaap:UnsecuredDebtMember2021-12-310000089089sci:May2024Member2022-12-310000089089sci:TermLoanDecember2022Member2021-12-310000089089sci:May2024Member2021-12-310000089089us-gaap:SubsequentEventMember2023-02-15utr:Rate0000089089sci:May2024Member2022-01-012022-12-310000089089sci:OtherNotesPayableMember2022-01-012022-12-310000089089sci:May2031Member2022-12-310000089089sci:May2024Member2021-01-012021-12-310000089089sci:April2027Member2022-01-012022-12-310000089089sci:November2021Member2021-01-012021-12-310000089089us-gaap:SubsequentEventMembersci:January2028Member2023-02-150000089089sci:April2027Member2022-12-310000089089sci:April2027Member2021-12-310000089089sci:December2027Member2022-12-310000089089sci:December2027Member2021-12-310000089089sci:June2029Member2022-12-310000089089sci:June2029Member2021-12-310000089089sci:August2030Member2022-12-310000089089sci:August2030Member2021-12-310000089089sci:May2031Member2021-12-3100000890892022-10-012022-12-310000089089sci:LessorMember2022-01-012022-12-310000089089sci:LessorMember2020-01-012020-12-310000089089sci:LessorMember2022-12-310000089089us-gaap:SubsequentEventMember2023-01-012023-02-150000089089sci:LongTermIncentive1996PlanMember2022-12-310000089089sci:LongTermIncentive2016PlanMember2021-12-310000089089us-gaap:EmployeeStockOptionMember2022-01-012022-12-310000089089us-gaap:EmployeeStockOptionMember2021-01-012021-12-310000089089us-gaap:EmployeeStockOptionMember2020-01-012020-12-310000089089us-gaap:EmployeeStockOptionMember2021-12-310000089089us-gaap:EmployeeStockOptionMember2022-12-310000089089sci:StockOptionPlanExerciseRange1Member2022-12-310000089089sci:StockOptionPlanExerciseRange2Member2022-12-310000089089sci:StockOptionPlanExerciseRange3Member2022-12-310000089089sci:StockOptionPlanExerciseRange4Member2022-12-310000089089sci:StockOptionPlanExerciseRange5Member2022-12-310000089089sci:StockOptionPlanExerciseRange6Member2022-12-310000089089us-gaap:RestrictedStockMember2021-12-310000089089us-gaap:RestrictedStockMember2022-01-012022-12-310000089089us-gaap:RestrictedStockMember2022-12-310000089089us-gaap:RestrictedStockMember2021-01-012021-12-310000089089us-gaap:RestrictedStockMember2020-01-012020-12-310000089089us-gaap:RestrictedStockUnitsRSUMember2021-12-310000089089us-gaap:RestrictedStockUnitsRSUMember2022-01-012022-12-310000089089us-gaap:RestrictedStockUnitsRSUMember2022-12-310000089089us-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310000089089us-gaap:RestrictedStockUnitsRSUMember2020-01-012020-12-310000089089sci:PerformanceOptionsMember2022-01-012022-12-310000089089sci:PerformanceOptionsMember2021-01-012021-12-310000089089sci:PerformanceOptionsMember2020-01-012020-12-310000089089sci:PerformanceOptionsMember2022-12-310000089089sci:PerformanceOptionsMember2021-12-310000089089sci:FuneralAtneedRevenueMember2022-01-012022-12-310000089089sci:FuneralAtneedRevenueMember2021-01-012021-12-310000089089sci:FuneralAtneedRevenueMember2020-01-012020-12-310000089089sci:FuneralMaturedPreneedRevenueMember2022-01-012022-12-310000089089sci:FuneralMaturedPreneedRevenueMember2021-01-012021-12-310000089089sci:FuneralMaturedPreneedRevenueMember2020-01-012020-12-310000089089sci:FuneralCoreRevenueMember2022-01-012022-12-310000089089sci:FuneralCoreRevenueMember2021-01-012021-12-310000089089sci:FuneralCoreRevenueMember2020-01-012020-12-310000089089sci:NonfuneralHomeRevenueMember2022-01-012022-12-310000089089sci:NonfuneralHomeRevenueMember2021-01-012021-12-310000089089sci:NonfuneralHomeRevenueMember2020-01-012020-12-310000089089sci:FuneralRecognizedPreneedRevenueMember2022-01-012022-12-310000089089sci:FuneralRecognizedPreneedRevenueMember2021-01-012021-12-310000089089sci:FuneralRecognizedPreneedRevenueMember2020-01-012020-12-310000089089sci:FuneralOtherRevenueMember2022-01-012022-12-310000089089sci:FuneralOtherRevenueMember2021-01-012021-12-310000089089sci:FuneralOtherRevenueMember2020-01-012020-12-310000089089sci:FuneralMember2020-01-012020-12-310000089089sci:CemeteryAtneedRevenueMember2022-01-012022-12-310000089089sci:CemeteryAtneedRevenueMember2021-01-012021-12-310000089089sci:CemeteryAtneedRevenueMember2020-01-012020-12-310000089089sci:CemeteryRecognizedPreneedPropertyRevenueMember2022-01-012022-12-310000089089sci:CemeteryRecognizedPreneedPropertyRevenueMember2021-01-012021-12-310000089089sci:CemeteryRecognizedPreneedPropertyRevenueMember2020-01-012020-12-310000089089sci:CemeteryRecognizedPreneedMerchandiseAndServiceRevenueMember2022-01-012022-12-310000089089sci:CemeteryRecognizedPreneedMerchandiseAndServiceRevenueMember2021-01-012021-12-310000089089sci:CemeteryRecognizedPreneedMerchandiseAndServiceRevenueMember2020-01-012020-12-310000089089sci:CemeteryCoreRevenueMember2022-01-012022-12-310000089089sci:CemeteryCoreRevenueMember2021-01-012021-12-310000089089sci:CemeteryCoreRevenueMember2020-01-012020-12-310000089089sci:CemeteryOtherRevenueMember2022-01-012022-12-310000089089sci:CemeteryOtherRevenueMember2021-01-012021-12-310000089089sci:CemeteryOtherRevenueMember2020-01-012020-12-310000089089sci:CemeteryMember2020-01-012020-12-310000089089us-gaap:CorporateAndOtherMember2022-01-012022-12-310000089089us-gaap:CorporateAndOtherMember2022-12-310000089089us-gaap:CorporateAndOtherMember2021-01-012021-12-310000089089us-gaap:CorporateAndOtherMember2021-12-310000089089us-gaap:CorporateAndOtherMember2020-01-012020-12-310000089089country:US2022-01-012022-12-310000089089country:CA2022-01-012022-12-310000089089country:US2022-12-310000089089country:CA2022-12-310000089089country:US2021-01-012021-12-310000089089country:CA2021-01-012021-12-310000089089country:US2021-12-310000089089country:CA2021-12-310000089089country:US2020-01-012020-12-310000089089country:CA2020-01-012020-12-310000089089sci:CurrentYearAcquisitionMember2022-12-310000089089sci:CurrentYearAcquisitionMember2022-01-012022-12-310000089089sci:CurrentYearAcquisitionMember2021-12-310000089089sci:CurrentYearAcquisitionMember2021-01-012021-12-310000089089us-gaap:AllowanceForCreditLossMember2021-12-310000089089us-gaap:AllowanceForCreditLossMember2022-01-012022-12-310000089089us-gaap:AllowanceForCreditLossMember2022-12-310000089089us-gaap:AllowanceForCreditLossMember2020-12-310000089089us-gaap:AllowanceForCreditLossMember2021-01-012021-12-310000089089us-gaap:AllowanceForCreditLossMember2019-12-310000089089us-gaap:AllowanceForCreditLossMember2020-01-012020-12-310000089089sci:AssetAllowanceForCancellationNotesReceivableMember2021-12-310000089089sci:AssetAllowanceForCancellationNotesReceivableMember2022-01-012022-12-310000089089sci:AssetAllowanceForCancellationNotesReceivableMember2022-12-310000089089sci:AssetAllowanceForCancellationNotesReceivableMember2020-12-310000089089sci:AssetAllowanceForCancellationNotesReceivableMember2021-01-012021-12-310000089089sci:AssetAllowanceForCancellationNotesReceivableMember2019-12-310000089089sci:AssetAllowanceForCancellationNotesReceivableMember2020-01-012020-12-310000089089sci:AssetAllowanceForCancellationPreneedFuneralAndCemeteryMember2021-12-310000089089sci:AssetAllowanceForCancellationPreneedFuneralAndCemeteryMember2022-01-012022-12-310000089089sci:AssetAllowanceForCancellationPreneedFuneralAndCemeteryMember2022-12-310000089089sci:AssetAllowanceForCancellationPreneedFuneralAndCemeteryMember2020-12-310000089089sci:AssetAllowanceForCancellationPreneedFuneralAndCemeteryMember2021-01-012021-12-310000089089sci:AssetAllowanceForCancellationPreneedFuneralAndCemeteryMember2019-12-310000089089sci:AssetAllowanceForCancellationPreneedFuneralAndCemeteryMember2020-01-012020-12-310000089089us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2021-12-310000089089us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2022-01-012022-12-310000089089us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2022-12-310000089089us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2021-01-012021-12-310000089089us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2020-01-012020-12-310000089089us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2020-12-31

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| | | | | | | | | | | |

| ☒ | | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

| | For the fiscal year ended | DECEMBER 31, 2022 |

| OR |

| ☐ | | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to |

Commission file number 1-6402-1

SERVICE CORPORATION INTERNATIONAL

(Exact name of registrant as specified in its charter)

| | | | | | | | | | | | | | | | | |

| Texas | | | 74-1488375 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. employer identification no.) |

| 1929 Allen Parkway | | | |

| Houston | | | |

| Texas | | 77019 |

| (Address of principal executive offices) | | (Zip code) |

Registrant’s telephone number, including area code: (713) 522-5141 Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

| Title of Each Class | | Trading Symbol (s) | | Name of Each Exchange on Which Registered |

| Common Stock ($1 par value) | | SCI | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

| | | | | | | | | | | | | | |

| Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. | Yes | þ | No | ¨ |

| Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. | Yes | ¨ | No | þ |

| Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | Yes | þ | No | ¨ |

| Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). | Yes | þ | No | ¨ |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act. (Check one): |

Large accelerated filer | þ | Accelerated filer | ¨ | Non-accelerated filer | ¨ | Smaller reporting company | ☐ | Emerging growth company | ☐ |

| | | | | | | | | | | | | | |

| If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. | ¨ | | | |

| Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. | ☑ | | | |

| If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. | ¨ | | | |

| Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). | ¨ | | | |

| Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the act). | Yes | ☐ | No | þ |

The aggregate market value of the common stock held by non-affiliates of the registrant (assuming that the registrant’s only affiliates are its executive officers and directors) was $10,609,438,787 based upon a closing market price of $69.12 on June 30, 2022 of a share of common stock as reported on the New York Stock Exchange.

The number of shares outstanding of the registrant’s common stock as of February 13, 2023 was 153,048,775 (net of treasury shares).

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Proxy Statement in connection with its 2023 Annual Meeting of Stockholders (Part III).

2 Service Corporation International

Glossary

The following terms are common to the deathcare industry, are used throughout this report, and have the following meanings:

Atneed — Funeral, including cremation, and cemetery arrangements sold once death has occurred.

Average Revenue per Service — Average revenue per funeral service performed, excluding the impact of funeral recognized preneed revenue, GA revenue, and certain other revenue.

Cancellation — Termination of a preneed contract, which relieves us of the obligation to provide the goods and services included in the contract. Cancellations may be requested by the customer or be initiated by us for failure to comply with the contractual terms of payment. State or provincial laws govern the amount of refund, if any, owed to the customer.

Care Trusts' Corpus — The deposits and net realized capital gains included in the perpetual care trusts that may not be withdrawable. In certain states, some or all of the net realized capital gains can also be distributed. Additionally, some states allow a total return distribution that may contain elements of income, capital appreciation, and principal.

Cemetery Marker — An item used to identify the deceased person in a particular burial space, crypt, niche, or cremation memorialization property. Permanent burial and cremation memorialization cemetery markers are usually made of bronze or stone.

Cemetery Merchandise and Services — Merchandise and services used in connection with a cemetery interment, including stone and bronze memorials, cemetery markers, outer burial containers, floral placement, graveside services, merchandise installations, urns, and interments.

Cemetery Perpetual Care Trust or Endowment Care Fund (ECF) — A trust fund established for the purpose of maintaining cemetery grounds and property into perpetuity. For these trusts, the corpus remains in the trust in perpetuity and the investment earnings or elected distributions are withdrawn regularly and are intended to defray our expenses incurred to maintain the cemetery. In certain states, some or all of the net realized capital gains can also be distributed. Additionally, some states allow a total return distribution that may contain elements of income, capital appreciation, and principal.

Cemetery Property — Developed lots, lawn crypts, mausoleum spaces, niches, and cremation memorialization property items (constructed and ready to accept interments) and undeveloped land we intend to develop for the sale of interment rights. Includes the construction-in-progress balance during the pre-construction and construction phases of projects creating new developed property items.

Cemetery Property Amortization or Amortization of Cemetery Property — The non-cash recognized expenses of cemetery property interment rights, which are recorded by specific identification with the cemetery property revenue for each contract.

Cemetery Property Interment Rights — The exclusive right to determine the human remains that will be interred in a specific cemetery property space. See also Cemetery Property Revenue below.

Cemetery Property Revenue — Recognized sales of interment rights in cemetery property when the receivable is deemed collectible and the property is fully constructed and available for interment.

Combination Location (Combos) — Locations where a funeral service location is physically located within or adjoining a SCI-owned cemetery location.

Cremation — The reduction of human remains to bone fragments by intense heat.

Cremation Memorialization — Products specifically designed to commemorate and honor the life of an individual who has been cremated. These products include cemetery property items that provide for the disposition of cremated remains within our cemeteries such as benches, boulders, statues, niches, etc. They also include memorial walls and books where the name of the individual is inscribed but the remains have been scattered or kept by the family.

Funeral Merchandise and Services — Merchandise such as burial caskets and related accessories, outer burial containers, urns and other cremation receptacles, casket and cremation memorialization products, flowers, and professional services relating to funerals including arranging and directing services, use of funeral facilities and motor vehicles, removal, preparation, embalming, cremations, memorialization, visitations, travel protection, and catering.

Funeral Recognized Preneed Revenue — Funeral merchandise and travel protection, net, sold to a preneed customer and delivered before a death has occurred.

Funeral Services Performed — The number of funeral services, including cremations, provided after the date of death, sometimes referred to as funeral volume.

General Agency (GA) Revenue — Commissions we receive from third-party life insurance companies for life insurance policies sold to preneed customers for the purpose of funding preneed funeral arrangements. The commission rate paid is determined based on the product type sold, the length of payment terms, and the health and age of the insured/annuitant.

Interment — The burial or final placement of human remains in the ground (interment), in mausoleums (entombment), in niches (inurnment), or in cremation memorialization property (inurnment).

Lawn Crypt — Cemetery property in which an underground outer burial receptacle constructed of concrete and reinforced steel has been pre-installed in predetermined designated areas.

Maturity — When the underlying contracted merchandise is delivered or service is performed, typically at death. This is the point at which preneed funeral contracts are converted to atneed contracts (note — delivery of certain merchandise and services can occur prior to death).

Mausoleum — An above ground structure that is designed to house caskets and/or cremation urns.

Merchandise and Service Trust — A trust account established in accordance with state or provincial law into which we deposit the required percentage of customers’ payments for preneed funeral, cremation, or cemetery merchandise and services to be delivered or performed by us in the future. The amounts deposited can be withdrawn only after we have completed our obligations under the preneed contract or upon the cancellation of the contract. Also referred to as a preneed trust.

Outer Burial Container — A reinforced container intended to inhibit the subsidence of the earth and house the casket after it is placed in the ground, also known as a burial vault.

Preneed — Purchase of cemetery property interment rights or any funeral or cemetery merchandise and services prior to death occurring.

Preneed Backlog or Backlog of Preneed Revenue — Future revenue from unfulfilled preneed funeral, cremation, and cemetery contractual arrangements.

Preneed Cemetery Sales Production — Sales of preneed cemetery contracts. These sales are recorded in Deferred revenue, net until the merchandise is delivered, the service is performed, or the property has been constructed and is available for interment.

Preneed Funeral Sales Production — Sales of preneed funeral trust-funded and insurance-funded contracts. Preneed funeral trust-funded contracts are recorded in Deferred revenue, net until the merchandise is delivered or the service is performed. We do not reflect the unfulfilled insurance-funded preneed funeral contract amounts in our Consolidated Balance Sheet. The proceeds of the life insurance policies will be reflected in revenue as these funerals are performed by us in the future.

Preneed Receivables, Net — Amounts due from customers when we have delivered the merchandise, performed the service, or transferred control of the cemetery property interment rights prior to a death occurring and amounts due from customers on irrevocable preneed contracts.

Travel Protection — A service provided by a third-party that provides shipment of remains to the servicing funeral home of choice if the purchaser passes away outside of a certain radius of their residence, without any additional expense to the family.

Trust Fund Income — Recognized investment earnings from our merchandise and service and perpetual care trust investments.

As used herein, “SCI,” “Company,” “we,” “our,” and “us” refer to Service Corporation International and companies owned directly or indirectly by Service Corporation International, unless the context requires otherwise. Management has published a white paper on the corporate website for further understanding of accounting for preneed sales. You can view the white paper at http://investors.sci-corp.com under Featured Documents. Documents and information on our website are not incorporated by reference herein.

4 Service Corporation International

Item 1. Business

General

We are North America’s largest provider of deathcare products and services, with a network of funeral service locations and cemeteries unequaled in geographic scale and reach. At December 31, 2022, we operated 1,474 funeral service locations and 490 cemeteries (including 303 funeral service/cemetery combination locations), which are geographically diversified across 44 states, eight Canadian provinces, the District of Columbia, and Puerto Rico.

We are well known for our Dignity Memorial® brand, North America's first transcontinental brand of deathcare products and services. Our other brands include Dignity Planning™, National Cremation Society®, Advantage® Funeral and Cremation Services, Funeraria del Angel™, Making Everlasting Memories®, Neptune Society™ and Trident Society™. Our funeral service and cemetery operations consist of funeral service locations, cemeteries, funeral service/cemetery combination locations, crematoria, and other related businesses, which enable us to serve a wide array of customer needs. We sell cemetery property and funeral and cemetery merchandise and services at the time of need and on a preneed basis.

Human Capital Management

At December 31, 2022, we employed 17,589 full-time individuals and 7,550 part-time individuals. Of the full-time associates, 15,028 were employed in the funeral and cemetery operations and 2,561 were employed in corporate or other overhead areas of our business. Approximately 2.1% of our associates are represented by unions. Although labor disputes occur from time to time, relations with associates are generally considered favorable. We reach out to our associates for feedback throughout their employment at SCI using a variety of voluntary surveys ensuring we are meeting the needs and expectations of our large and diverse workforce.

Associate Benefits

Eligible associates in the United States may elect coverage under our group health and life insurance plans. Associates covered by a collective bargaining agreement are typically covered by union health plans and, therefore, do not participate in our health insurance plan. At December 31, 2022 and 2021, there were 9,478 and 9,685 associates, respectively, who had elected to participate in our group health insurance plans.

Eligible associates in the United States are covered by retirement plans of SCI or various subsidiaries, while international associates are covered by other SCI (or SCI subsidiary) defined contribution or government-mandated benefit plans. We have an employee savings plan that qualifies under Section 401(k) of the Internal Revenue Code for the exclusive benefit of our United States employees. We contribute a matching contribution based on the employee's contribution and years of vesting service. For more information about our retirement plans, see Note 12 of Part II, Item 8. Financial Statements and Supplementary Data. We understand the importance of work-life balance and provide other benefits such as baby bonding time, paid time off for various reasons, and financial planning support for our associates. Additionally, we offer an employee assistance program that offers free and confidential counseling by masters level counselors for associates who may be facing mental health challenges.

Inclusion and Diversity

We believe in the power of inclusion and respecting our fellow associates’ work, ideas, beliefs, and lifestyles. Our Inclusion and Diversity (I&D) Committee, which is a cross-functional team of associates, has been key to the development of programs such as our Women’s Leadership Conference and Associate Resource Communities (ARCs). The ARCs allow colleagues with similar backgrounds or interests to connect for networking, provide opportunities for growth, and support the communities and customers we serve. Our leadership team is committed to advancing inclusion and diversity within the workplace. By embracing the many backgrounds and perspectives that make each of us unique, we are able to remain relevant to the diverse families we serve. We have created an I&D senior management position to support the Company's belief that diversity of talent and people is a key driver of better business outcomes.

Training and Development

We provide opportunities for career growth and supporting the personal and professional goals of our associates is a priority for us. In addition to development programs and a robust online training portal offering thousands of courses, books, audiobooks, and videos, associates can participate in mentoring programs and take advantage of discounts and tuition reimbursement through our many university partnerships. We are also proud to offer scholarship and apprentice programs to those interested in joining our profession.

Regulation

Our funeral operations are regulated by the Federal Trade Commission (the “FTC”) under the FTC’s Trade Regulation Rule on Funeral Industry Practices (the “Funeral Rule”), which went into effect in 1984. The Funeral Rule defines certain acts or practices as unfair or deceptive and contains certain requirements to prevent these acts or practices. The preventive measures require a funeral provider to give consumers accurate, itemized price information and various other disclosures about funeral merchandise and services and prohibit a funeral provider from: 1) misrepresenting legal, crematory, and cemetery requirements; 2) embalming for a fee without permission; 3) requiring the purchase of a casket for direct cremation; and 4) requiring consumers to buy certain funeral merchandise or services as a condition for furnishing other funeral merchandise or services.

Our operations are also subject to regulation, supervision, and licensing under numerous federal, state, and local laws and regulations as well as Canadian provincial laws and regulations. For example, state laws impose licensing requirements for funeral service locations and funeral directors and regulate preneed sales including our preneed trust activities. Our facilities are subject to environmental, health, and safety regulations. We take various measures to comply with the Funeral Rule and all laws and regulations. For example, we have established and maintain policies and procedures around our business practices; we provide training of our personnel; and we perform ongoing reviews of our compliance efforts. We are currently in substantial compliance with the Funeral Rule and all laws and regulations.

Federal, state, and local legislative bodies and regulatory agencies (including Canadian legislative bodies and agencies) frequently propose new laws and regulations, some of which could have a material effect on our operations and on the deathcare industry in general. We cannot accurately predict the outcome of any proposed legislation or regulation or the effect that any such legislation or regulation might have on us.

History

We were incorporated in Texas in July of 1962. Our original business plan was based on efficiencies of scale, specifically reducing overhead costs by sharing resources such as preparation services, back office administration support, transportation, and personnel among funeral service locations in a business “cluster.” After proving the plan’s effectiveness in Houston in the early 1960s, we set out to apply this operating strategy through the acquisition of deathcare businesses in other markets over the next three decades. Beginning in 1993, we expanded beyond North America, acquiring major deathcare companies in Australia, the United Kingdom, and France, plus smaller holdings in other European countries, Asia, and South America.

During the mid to late 1990s, acquisitions of deathcare facilities became extremely competitive, resulting in increased prices for acquisitions and substantially reduced returns on invested capital. In 1999, we significantly reduced our level of acquisition activity and over the next several years implemented various initiatives to pay down debt, increase cash flow, reduce overhead costs, increase efficiency, and leverage our scale. We divested our international businesses and many North American funeral service locations and cemeteries that were either underperforming or did not fit within our long-term strategy. At the same time, we began to capitalize on the strength of our network by introducing to North America the first transcontinental brand of deathcare services and products — Dignity Memorial® (see www.dignitymemorial.com). Information contained on our website is not part of this report.

In late 2006, having arrived at a position of financial stability and improved operating efficiency, we acquired the then second largest company in the North American deathcare industry, Alderwoods Group. In early 2010, we acquired the then fifth largest company in the North American deathcare industry, Keystone North America. In June 2011, we acquired 70% of the outstanding shares of The Neptune Society, Inc. (Neptune), which is the nation's largest direct cremation organization, now known as SCI Direct. Subsequently, in 2013 and 2014, we acquired the remaining 30% of the outstanding shares of Neptune. In December 2013, we purchased Stewart Enterprises, Inc. (Stewart), the then second largest operator of funeral service locations and cemeteries in North America. We continue to pursue strategic acquisitions and complete divestitures of non-strategic funeral homes and cemeteries.

Funeral and Cemetery Operations

Our funeral service and cemetery operations consist of funeral service locations, cemeteries, funeral service/cemetery combination locations, crematoria, and other related businesses. See Note 13 in Part II, Item 8. Financial Statements and Supplementary Data, for financial information about our business segments and geographic areas. We have the largest number of combination locations in North America. Funeral service/cemetery combination locations are businesses in which a funeral service location is physically located within or adjoining a cemetery that we own. Combination locations allow certain facility, personnel, and equipment costs to be shared between the funeral service location and a cemetery location. Combination facilities typically are more cost competitive and have a higher gross margin than funeral and

6 Service Corporation International

cemetery operations that are operated separately. Combination locations also create synergies between funeral and cemetery sales personnel and give families added convenience to purchase both funeral and cemetery merchandise and services at a single location.

Funeral service locations provide all professional services related to funerals and cremations, including the use of funeral home facilities and motor vehicles, arranging and directing services, removal, preparation, embalming, cremations, memorialization, and catering. Funeral merchandise, including burial caskets and related accessories, urns and other cremation receptacles, outer burial containers, flowers, online and video tributes, stationery products, casket and cremation memorialization products, and other ancillary merchandise, is sold at funeral service locations.

Our cemeteries provide cemetery property interment rights, including developed lots, lawn crypts, mausoleum spaces, niches, and other cremation memorialization and interment options. Cemetery merchandise and services, including memorial cemetery markers and bases, outer burial containers, flowers and floral placement, other ancillary merchandise, graveside services, merchandise installation, and interments, are sold at our cemeteries.

We also sell cemetery property interment rights and funeral and cemetery merchandise and services whereby a customer contractually agrees to the terms of certain products and services to be delivered and performed in the future. We define these sales as preneed sales. As a result of such preneed sales, our preneed backlog of unfulfilled funeral and cemetery contracts was $13.7 billion at December 31, 2022 and 2021.

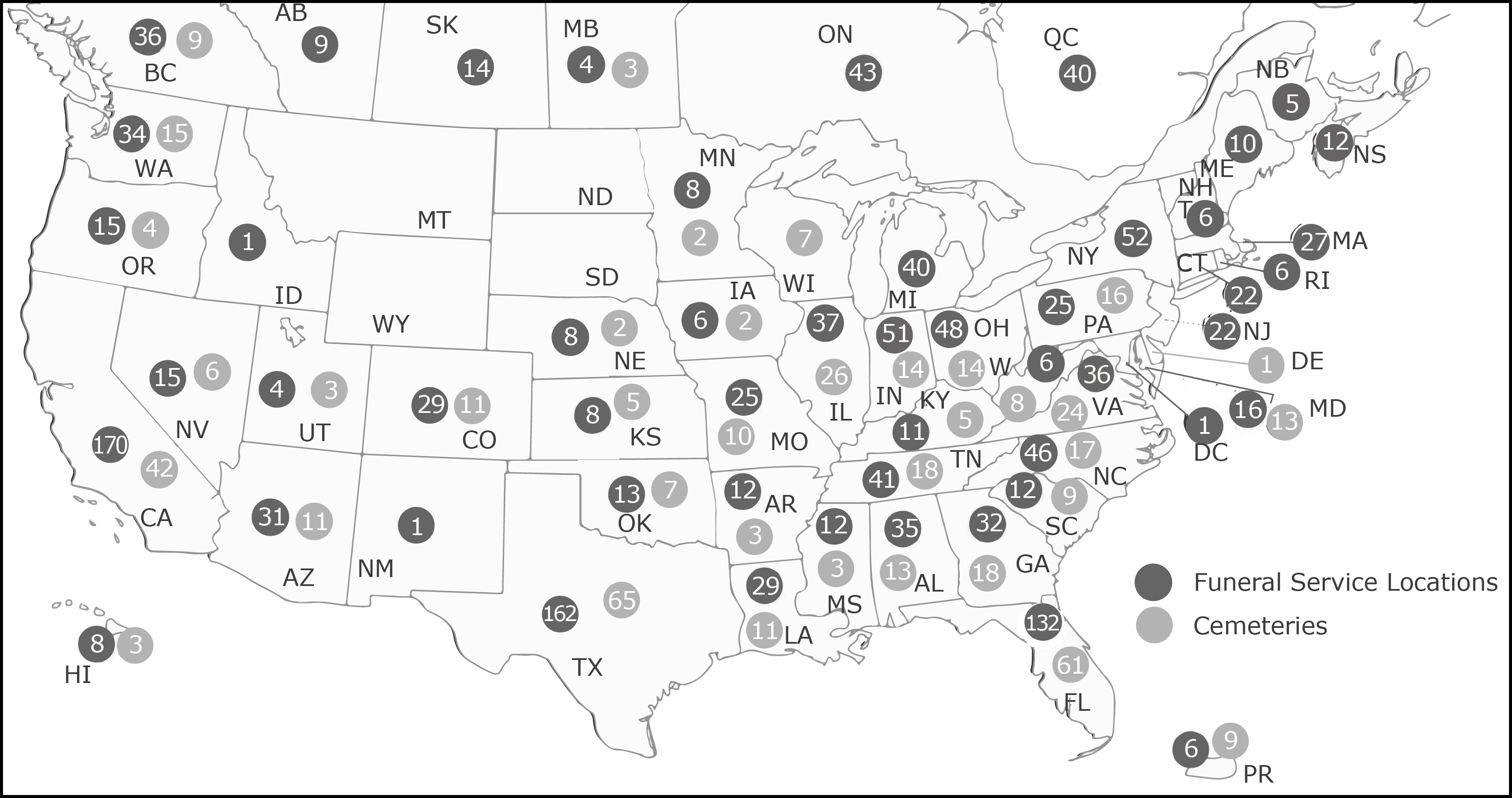

The following table at December 31, 2022 provides the number of our funeral service locations and cemeteries by country, and by state, territory, or province:

| | | | | | | | | | | | | | | | | | | | |

| Country, State/Territory/Province | | Number of Funeral Service Locations | | Number of Cemeteries | | Total |

| United States | | | | | | |

| Alabama | | 35 | | | 13 | | | 48 | |

| Arizona | | 31 | | | 11 | | | 42 | |

| Arkansas | | 12 | | | 3 | | | 15 | |

| California | | 170 | | | 42 | | | 212 | |

| Colorado | | 29 | | | 11 | | | 40 | |

| Connecticut | | 22 | | | — | | | 22 | |

| Delaware | | — | | | 1 | | | 1 | |

| District of Columbia | | 1 | | | — | | | 1 | |

| Florida | | 132 | | | 61 | | | 193 | |

| Georgia | | 32 | | | 18 | | | 50 | |

| Hawaii | | 8 | | | 3 | | | 11 | |

| Idaho | | 1 | | | — | | | 1 | |

| Illinois | | 37 | | | 26 | | | 63 | |

| Indiana | | 51 | | | 14 | | | 65 | |

| Iowa | | 6 | | | 2 | | | 8 | |

| Kansas | | 8 | | | 5 | | | 13 | |

| Kentucky | | 11 | | | 5 | | | 16 | |

| Louisiana | | 29 | | | 11 | | | 40 | |

| Maine | | 10 | | | — | | | 10 | |

| Maryland | | 16 | | | 13 | | | 29 | |

| Massachusetts | | 27 | | | — | | | 27 | |

| Michigan | | 40 | | | — | | | 40 | |

| Minnesota | | 8 | | | 2 | | | 10 | |

| Mississippi | | 12 | | | 3 | | | 15 | |

| Missouri | | 25 | | | 10 | | | 35 | |

| Nebraska | | 8 | | | 2 | | | 10 | |

| Nevada | | 15 | | | 6 | | | 21 | |

| | | | | | | | | | | | | | | | | | | | |

| Country, State/Territory/Province | | Number of Funeral Service Locations | | Number of Cemeteries | | Total |

| New Hampshire | | 6 | | | — | | | 6 | |

| New Jersey | | 22 | | | — | | | 22 | |

| New Mexico | | 1 | | | — | | | 1 | |

| New York | | 52 | | | — | | | 52 | |

| North Carolina | | 46 | | | 17 | | | 63 | |

| Ohio | | 48 | | | 14 | | | 62 | |

| Oklahoma | | 13 | | | 7 | | | 20 | |

| Oregon | | 15 | | | 4 | | | 19 | |

| Pennsylvania | | 25 | | | 16 | | | 41 | |

| Puerto Rico | | 6 | | | 9 | | | 15 | |

| Rhode Island | | 6 | | | — | | | 6 | |

| South Carolina | | 12 | | | 9 | | | 21 | |

| Tennessee | | 41 | | | 18 | | | 59 | |

| Texas | | 162 | | | 65 | | | 227 | |

| Utah | | 4 | | | 3 | | | 7 | |

| | | | | | |

| Virginia | | 36 | | | 24 | | | 60 | |

| Washington | | 34 | | | 15 | | | 49 | |

| West Virginia | | 6 | | | 8 | | | 14 | |

| Wisconsin | | — | | | 7 | | | 7 | |

| Canada | | | | | | |

| Alberta | | 9 | | | — | | | 9 | |

| British Columbia | | 36 | | | 9 | | | 45 | |

| Manitoba | | 4 | | | 3 | | | 7 | |

| New Brunswick | | 5 | | | — | | | 5 | |

| Nova Scotia | | 12 | | | — | | | 12 | |

| Ontario | | 43 | | | — | | | 43 | |

| Quebec | | 40 | | | — | | | 40 | |

| Saskatchewan | | 14 | | | — | | | 14 | |

| Total funeral service locations and cemeteries | | 1,474 | | | 490 | | | 1,964 | |

We believe we have satisfactory title to the properties owned and used in our business, subject to various liens, encumbrances, and easements that are incidental to ownership rights and uses and do not materially detract from the value of the property. At December 31, 2022, we owned approximately 90% of the real estate and buildings used at our facilities, and the remainder of the facilities were leased under both finance and operating leases. At December 31, 2022, our 490 cemeteries contained a total of approximately 35,500 acres, of which approximately 66% was developed. Interment rights for approximately 2,000 acres of the developed acreage are unsold.

Our corporate headquarters are located at 1929 Allen Parkway, Houston, Texas 77019. The property consists of approximately 160,000 square feet of office space and 185,000 square feet of parking space on approximately seven acres. We own a building in Jefferson, Louisiana with approximately 96,200 square feet of office space that we use, in part, for corporate activities.

8 Service Corporation International

A map of our locations in North America is presented below:

COVID-19 Impact

Since the World Health Organization declared the worldwide outbreak of a novel strain of coronavirus (COVID-19) a global pandemic in March 2020, we have worked continuously to meet the challenges it presented. Like many businesses worldwide, COVID-19 is still directly and indirectly impacting various aspects of our business operations.

We continue to maintain a high priority focus on the health, safety, and mental well-being of our associates. We provide an employee assistance program that offers free and confidential counseling by masters level counselors for our associates' overall mental health. We have avoided layoffs, mandatory furloughs, and any widespread reductions in pay as a result of the impact of COVID-19. Over the last several years, we have awarded discretionary bonuses to associates in recognition of their courageous efforts and dedication to serving families throughout the pandemic.

To ensure both associate and customer safety, we quickly implemented technology solutions during the early part of the pandemic to overcome social distancing restrictions. Many of these solutions are still in place today and helped us accelerate the use of technology throughout our organization, particularly within our sales team with the use of our customer relationship management system and digital leads. By capitalizing on our physical and digital presence in our response to the COVID-19 crisis, we were able to further leverage our scale. This accelerated the use of new technology required to successfully meet customer needs during COVID-19 and has provided many advantages which further differentiates us from our competitors. We view the demand for robust services and celebrations of life through the COVID-19 pandemic as evidence that our customers value what our team does best, which is helping our client families gain closure and healing through the process of grieving, remembrance, and celebration.

Competition

Although there are several public companies that own funeral service locations and cemeteries, the majority of deathcare businesses in North America are locally-owned, independent operations. We estimate that our funeral and cemetery market share in North America is approximately 15%-16% based on estimated total industry revenue. The success of a single funeral service location or cemetery in any community is a function of the name, reputation, and location of that funeral service location or cemetery. Competitive pricing, professional service and attention, and well-maintained locations are also important.

We have an unparalleled network of funeral service locations and cemeteries that offers high quality products and services at prices that are competitive with local competing funeral service locations, cemeteries, and retail locations. Within this network, the funeral service locations and cemeteries operate under various names as most operations were acquired as existing businesses. We have co-branded the majority of our operations under the name Dignity Memorial®. Our branding strategy gives us a strategic advantage and identity in the industry. While this branding process is intended to emphasize our seamless national network of funeral service locations and cemeteries, the original names associated with acquired operations, and their inherent goodwill and heritage, generally remain the same. For example, Geo. H. Lewis & Sons Funeral Directors is now Geo. H. Lewis & Sons Funeral Directors, a Dignity Memorial® provider.

Strategies for Growth

We are the largest consolidated deathcare company in North America and are well positioned for long-term profitable growth. Like most businesses world-wide, COVID-19 has impacted various aspects of our business operations, however, our fundamental strategy has not changed. Over the next several years, our industry will be largely shaped by the aging of the Baby Boomer generation in the deathcare space and we are poised to benefit from the aging of the North American population. In each stage of life, Baby Boomers have set new trends, transformed society, and redefined norms, and we anticipate the impact will be the same for our industry. We have already begun to see the impact of the Baby Boomers through the growth in our preneed cemetery sales production. We expect to see a similar impact on our preneed funeral results and ultimately our atneed results as these preneed contracts mature. In every aspect of our business, we are listening and responding to our customer’s changing needs and leveraging our scale to deliver unparalleled experiences - both digitally and in person - to meet those changing needs.

The following strategies remain the core of our foundation: 1) grow revenue, 2) leverage our unparalleled scale, and 3) invest capital. While these strategies remain unchanged, a shift to increased utilization of technology during the COVID-19 pandemic has influenced how we serve our customers and how we invest our capital.

Grow Revenue

We plan to grow revenue by remaining relevant to our customers as their preferences evolve through a combination of price, product, and service differentiation strategies. We also expect that continued growth in our preneed sales will drive future revenue expansion.

Remaining Relevant to the Customer

Remaining relevant to our customer is key to generating revenue growth in a changing customer environment. We are constantly evolving to meet the varying preferences and needs of our customers. Whether choosing burial or cremation, the Baby Boomers are redefining the traditional funeral by transitioning away from solemnly mourning a death to a personalized celebration of life ceremony. In certain markets, we are responding to this trend by spending capital to repurpose traditional casket selection rooms to event rooms that can accommodate a celebration. We are offering a customer friendly digital presentation of options that allow the customer to choose merchandise and services including unique celebration, catering, and celebrant services.

In our funeral business, we focus on memorialization merchandise and services that are meaningful to both our burial and cremation customers. The growing trend of cremation requires more flexibility in providing products and services. We have developed cremation service packages, which may or may not include a celebratory memorialization, depending on the consumers preference.

In our cemetery business, we continue to grow revenue by responding to the customer’s desire for personalized and unique options by expanding our tiered product and cemetery property options. Over the past several years, we have substantially increased our property options to offer many unique choices. From high-end family estates, which capture incredible views, to nicely landscaped hedge estates, we continue to develop property selections that resonate with our customers. For cemetery merchandise and services, we have developed innovative products such as recurring floral placements, customized cemetery property offerings, and specialized graveside service options. We continue to embrace cremation opportunities for customers in our cemetery segment by offering an increased variety of cremation property options, including glass-front niches and scattering gardens.

As we evolve to meet ever-changing customer preferences, we will continue catering to the religious, ethnic, and cultural traditions important to many of our customers. We have remained flexible to meet the varying needs of customers, demonstrating our resolve to remain relevant to changing customer preferences.

10 Service Corporation International

Growing Preneed Sales

Our preneed sales program drives current and future revenue growth. Baby Boomers have been influencing our cemetery preneed sales for several years and are beginning to positively affect the growth of our preneed funeral sales programs. Our highly trained sales force of approximately 3,750 counselors provide customers with informed guidance about various service and merchandise options tailored for today’s consumers. Utilizing our scale, our counselors are reaching out to consumers through multiple lead channels, driving future revenue growth. We sponsor community events and seminars to educate and provide guidance around preplanning both funeral and cemetery services and merchandise. We have adopted a more sophisticated and targeted direct mail approach, and we continue increasing our digital presence through search engine optimization and other marketing channels. We have a unique competitive advantage to continue growing preneed sales benefiting from our size and scale. Our preneed program provides us with an opportunity to develop greater brand awareness, gives consumers peace of mind about their end of life arrangements, and secures future market share. In addition, our increased digital presence has provided significant growth in our digital lead channels over the last several years.

Leverage Our Unparalleled Scale

As the largest deathcare company in North America, we leverage our scale by developing our sales organization and optimizing the use of our network using technology, which benefits our preneed backlog. Our scale enables cost efficiencies through purchasing power and utilizing economies of scale through our supply chain channel. During the COVID-19 pandemic, we were able to continue to operate without any major disruptions to our business, which highlights the strength of our scale.

Developing Our Sales Organization

Over the last several years, we have continued to invest significantly in the development of our sales organization with best in class tools and technologies. These investments include a customer relationship management system, which drives improvements in productivity and sales production by leveraging data analytics, rigorous lead tracking, and effective follow up campaigns. We continue to diversify our sales force to understand and cater to the religious, ethnic, and cultural traditions important to our customers. Our premier combination locations and other large and recognizable cemeteries and funeral homes attract high-quality sales talent. Our scale allows us to operate and expand our sales organization in a manner that would be difficult for our competitors to replicate.

Optimizing Our Network and Deploying Customer-Facing Technology

We continue driving operating discipline and leveraging our scale through standardizing processes and capitalizing on new technologies to improve the customer experience. Our advancements in technology are changing the way we present our product and service offerings to customers. Our atneed point of sale system, HMIS+, uses a digital platform enabled with high resolution video and photographs to create a seamless presentation of our products and service offerings. Our mobile preneed sales system, Beacon, provides customers with a full digital presentation experience in their home or other place of their choosing.

Our Dignity Memorial® location websites feature a modern and user-friendly design. Our location-specific websites are designed for mobile use and optimized for better search engine ranking. In addition to the contemporary and sophisticated design, client families enjoy innovative features such as an interactive obituary experience, social media sharing capabilities, the ability to create and share personalized content in memory of their loved one, and the ability to see venue and catering options for locations.

We have reduced the time it takes to receive customer feedback through digital J.D. Power surveys. Online reviews provide visibility of customer engagement down to the location level and shorten our response time in addressing any customer concerns. We have established a social media presence for a number of our funeral and cemetery businesses, including the ability to livestream services at many of our locations. These digital efforts resulted in favorable customer satisfaction ratings and increased digital sales leads over the last several years.

Although the last several years were difficult in many unexpected ways through the COVID-19 pandemic, we learned valuable lessons around our ability to quickly deploy customer-facing technology. Our associates and client families embraced an increasingly digital world and we utilized various online tools to complete sales and meet families. We are encouraged by the increased digitization and we are making great strides with internal projects leveraging technology and simplifying nearly every facet of service delivery.

Growing Our Preneed Backlog

Our preneed backlog, which includes both insurance and trust-funded merchandise and service products, allows us the opportunity to grow future revenue in a more stable and efficient manner than selling at the time of need. The scale of our multi-billion dollar trust portfolios allows us to leverage access to preeminent money managers with favorable fee structures generating above average returns. Our blended funding approach between insurance and trust-funded merchandise and service products allows us to combine the positive cash flow and predictability of the insurance product with the potential upside of higher returns from our trusted merchandise and service products. This blended approach also helps our ability to grow our preneed backlog in a cash flow neutral manner.

Invest Capital

We maximize capital deployment opportunities in a disciplined and balanced manner to the highest relative return. Our strong liquidity, favorable debt maturity profile, and robust cash flow generation enables us to continue our long-standing commitment to use capital deployment to opportunistically grow our business and enhance shareholder value. Typically, our highest relative return opportunities come from acquisitions and funeral service and cemetery new builds.

Investing in Acquisitions and Building New Funeral Service and Cemetery Locations

We manage our footprint by focusing on strategic acquisitions and building new funeral service and cemetery locations where the expected returns are attractive and meaningfully exceed our weighted average cost of capital. We target businesses with favorable customer dynamics and locations where we can achieve additional economies of scale. Over the last several years, we have increased our growth capital spend on new funeral service locations, enlarging our footprint into new communities as well as expanding existing locations to remain relevant to our customers. For our cemetery businesses, we plan to pursue strategic acquisitions to create more opportunities to serve Baby Boomers through our tiered cemetery options. Additionally, we acquire land for future cemetery development in some of our largest markets. This investment in our future will allow us to continue creating cemetery offerings that appeal to varying preferences in those markets for many years to come. We invested $102.6 million in acquiring 18 funeral service locations and 3 cemeteries, which included 3 combination locations, in 2022.

Managing Debt

We continue to focus on maintaining optimal levels of liquidity and financial flexibility. Our flexible capital strategy allows us to manage our debt maturity profile by making open market debt repurchases when it is opportunistic to do so. We generate a relatively consistent annual cash flow stream that is generally resistant to down economic cycles. This cash flow stream and our significant liquidity allow us to substantially reduce our long-term debt maturities should we choose to do so. In January 2023, we entered into a new bank credit agreement that consists of a $675.0 million Term Loan due January 2028 and an increased Bank Credit Facility due January 2028 providing for borrowings of up to $1.5 billion. Proceeds from this new bank credit agreement were used to settle our existing Term Loan and Bank Credit Facility due May 2024. The new bank credit agreement provides us with flexibility for incremental liquidity, capital investment, working capital, and other general corporate purposes.

Return Excess Cash to Shareholders

Absent any strategic acquisition or new build opportunities, we intend to return excess cash to shareholders. Our quarterly dividend rate has steadily grown from $0.025 per common share in 2005 to $0.27 per common share at the end of 2022. We target a payout ratio of 30% to 40% of after-tax earnings excluding special items and intend to grow our cash dividend commensurate with the growth in our business.

Other

We make available free of charge, on or through our website, our annual, quarterly, and current reports and any amendments to those reports, as soon as reasonably practicable after electronically filing such reports with the Securities and Exchange Commission (SEC). Our website is http://www.sci-corp.com and our telephone number is (713) 522-5141. We also post announcements, updates, events and investor information and presentations on our website in addition to copies of all recent news releases. We may use the Investors section of our website to communicate with investors. It is possible that the financial and other information posted there could be deemed material information. Each of our Board of Directors’ standing committee charters, our Corporate Governance Guidelines, our Code of Ethics for Board Members, and our Code of Conduct for Officers and Employees are available, free of charge, through our website or, upon request, in print. We will post on our internet website all waivers to, or amendments of, our Code of Conduct for Officers and Employees, which are required to be disclosed by applicable law and rules of the New York Stock Exchange listing standards. Information contained on our website is not part of this report. In addition, the SEC also maintains a website that contains reports, proxy and information statements, and other information regarding issuers where you may obtain a copy of all of the material we file publicly with the SEC. The SEC website address is http://www.sec.gov.

12 Service Corporation International

Executive Officers of the Company

The following table sets forth, as of February 15, 2023, the name and age of each executive officer of the Company, the office held, and the year first elected an officer.

| | | | | | | | | | | | | | | | | | | | |

| Officer Name | | Age | | Position | | Year First

Became Officer |

| Thomas L. Ryan | | 57 | | Chairman of the Board, Chief Executive Officer, and President | | 1999 |

| Sumner J. Waring, III | | 54 | | Senior Vice President, Chief Operating Officer | | 2002 |

| Eric D. Tanzberger | | 54 | | Senior Vice President, Chief Financial Officer | | 2000 |

| Gregory T. Sangalis | | 67 | | Senior Vice President, General Counsel and Secretary | | 2007 |

| Elisabeth G. Nash | | 61 | | Senior Vice President, Operations Services | | 2004 |

| John H. Faulk | | 47 | | Senior Vice President, Revenue and Business Development | | 2010 |

| Steven A. Tidwell | | 61 | | Senior Vice President, Sales and Marketing | | 2010 |

| Tammy R. Moore | | 55 | | Vice President and Corporate Controller | | 2010 |

Mr. Ryan was elected Chairman of the Board of SCI effective in January 2016, appointed Chief Executive Officer in February 2005, and President in 2019. He joined the Company in 1996 and served in a variety of financial management roles until November 2000, when he was asked to serve as Chief Executive Officer of European Operations based in Paris, France. In July 2002, Mr. Ryan returned to the United States where he was appointed President and Chief Operating Officer of SCI. Before joining SCI, Mr. Ryan was a certified public accountant with Coopers & Lybrand LLP for eight years. He holds a bachelor's degree in business administration from the University of Texas at Austin. Mr. Ryan serves as a member of the University of Texas McCombs Business School Advisory Council and is a senior member of the University of Texas MD Anderson Cancer Center Board of Visitors.

Mr. Waring, Senior Vice President and Chief Operating Officer, is responsible for North American Operations. He joined SCI in 1996 as Area Vice President of Operations when SCI acquired his family's funeral business. He was appointed President of the Northeast Region in 1999 and President of the Pacific Region in September 2001. In September 2002, Mr. Waring was appointed Vice President, Western Operations, a position he held until May 2004 when he was appointed Vice President, Major Market Operations. He was promoted to Senior Vice President in 2006. In May 2015, Mr. Waring's responsibilities were expanded to include all operations in North America. Mr. Waring holds a bachelor's degree in business administration from Stetson University, a degree in mortuary science from Mount Ida College, and a master's degree in business administration from the University of Massachusetts Dartmouth. Mr. Waring serves on the Board of Directors of BankFive and the Greater Houston Partnership.

Mr. Tanzberger was appointed Senior Vice President and Chief Financial Officer in June 2006 and also served as Treasurer from July 2007 to February 2017. Mr. Tanzberger joined the Company in August 1996 and held various management positions prior to being promoted to Corporate Controller in August 2002. In 2022, his responsibilities were expanded to include information technology. Before joining SCI, Mr. Tanzberger began his financial career at Coopers and Lybrand LLP. Mr. Tanzberger holds a Bachelor of Business Administration degree from the University of Notre Dame. Mr. Tanzberger is currently a member of the Board of Directors and Chair of the Audit Committee of Sanara MedTech Inc. (NASDAQ: SMTI). He is also a current member of the Executive Committee and the Audit Committee Chair of the United Way of Greater Houston. Mr. Tanzberger is a former member of the Board of Trustees of Junior Achievement of Southeast Texas and the National Funeral Directors Association Funeral Service Foundation.

Mr. Sangalis joined the Company in 2007 as Senior Vice President, General Counsel and Secretary. He previously served as Senior Vice President, Law and Administration for Team Inc., a leading provider of specialty industrial maintenance and construction services. Prior to that, Mr. Sangalis served as Managing Director and General Counsel of Main Street Equity Ventures II, a private equity investment firm, and as Senior Vice President, General Counsel and Secretary for Waste Management, Inc., the leading provider of waste management services in North America. Mr. Sangalis holds a bachelor's degree in finance from Indiana University and a master's degree in business administration from the University of Minnesota. He earned his juris doctorate from the University of Minnesota Law School. In 2022, Mr. Sangalis announced his intent to retire in March of 2023.

Ms. Nash was named Senior Vice President of Operations Services in 2010 and is currently responsible for a variety of support functions, including human resources, supply chain, and program management. Prior to that she was Vice President of Process Improvement and Technology, where she led the redefinition of our field and home office processes and systems. Before joining SCI, Ms. Nash served in various senior management accounting and financial positions with Pennzoil Corp. She holds a bachelor's degree in business administration in accounting from Texas A&M University. Ms. Nash serves as Chair of the Board of Directors of Genesys Works Houston.

Mr. Faulk was named Senior Vice President of Revenue and Business Development in 2018. He joined SCI in March 2010 as Vice President, Business Development, to oversee the Company's strategic growth, including mergers and acquisitions, real estate, and construction. His promotion in 2018 expanded his role to include setting direction for the company’s pricing and cemetery development functions. Prior to joining the Company, Mr. Faulk worked for Bain & Company, Inc. where he helped

Fortune 500 Companies and specialty retailers identify profit growth opportunities and achieve strong operating results. He holds a master's degree in business administration from the Darden Graduate School of Business at the University of Virginia and a bachelor's degree in electrical engineering from the University of Virginia.

Mr. Tidwell joined SCI as Vice President, Main Street Market Operations, in March 2010 and was promoted to Senior Vice President of Sales and Merchandising in 2012. As a co-founder of Keystone North America, Inc., Mr. Tidwell served as its President and Chief Executive Officer from May 2007 until it was acquired by SCI in March 2010. In his role, Mr. Tidwell worked closely with Keystone's Senior Leadership Team to develop and implement organic growth strategies as well as external growth and acquisition strategies. He began his career as a licensed funeral director and embalmer in Nashville, Tennessee, and has been actively involved in the funeral and cemetery profession for over forty years. He holds an associate of arts degree from John A. Gupton College and has attended Executive Management and Leadership programs at the Harvard Business School, Vanderbilt University Owen Graduate School of Management, and the Center for Creative Leadership. Mr. Tidwell has served for over three years as the Chairman of the Board of Regents of Commonwealth Institute of Funeral Service.

Mrs. Moore joined the Company in August 2002 as Manager of Financial Reporting. She was promoted to Director of Financial Reporting in 2004 and Managing Director and Assistant Controller in June 2006. In February 2010, she was promoted to Vice President and Corporate Controller and oversees trust accounting and compliance, general accounting, internal and external reporting and customer service. Prior to joining the Company, Mrs. Moore was a certified public accountant with PricewaterhouseCoopers LLP. She holds a bachelor's degree in business administration in accounting from the University of Texas at San Antonio. Since 2019, Mrs. Moore has served on the Board of Regents of Commonwealth Institute of Funeral Service.

Item 1A. Risk Factors

Cautionary Statement on Forward-Looking Statements