UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

Annual Report Pursuant To Section 13 or 15(d) of the Securities Exchange Act of 1934

For the Fiscal Year Ended March 31, 2013

Commission File No. 001-32632

UROPLASTY, INC.

(Exact name of registrant as specified in its Charter)

|

Minnesota

|

|

41-1719250

|

|

(State or other jurisdiction of incorporation or organization)

|

|

(I.R.S. Employer Identification No.)

|

5420 Feltl Road

Minnetonka, Minnesota 55343

(Address of principal executive offices)

(952) 426-6140

(Issuer’s telephone number, including area code)

Securities registered under Section 12(b) of the Exchange Act:

|

Title of class

|

|

Name of Exchange on which registered

|

|

Common Stock, $.01 par value

|

|

NASDAQ

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

YES o NO x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act.

YES o NO x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES x NO o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

YES x NO o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large Accelerated Filer ¨

|

Accelerated Filer x

|

Smaller Reporting Company ¨

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

YES o NO x

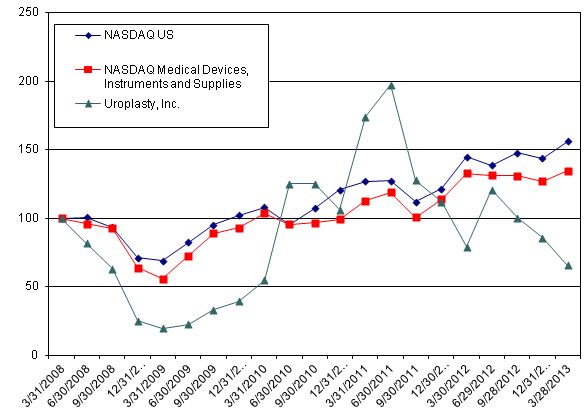

The aggregate market value of the voting stock and nonvoting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked prices of such common equity, as of September 30, 2012 was $67,481,196.

As of June 28, 2013, the registrant had 20,934,245 shares of common stock outstanding.

Documents Incorporated By Reference: Portions of our Proxy Statement for our 2011 Annual Meeting of Shareholders (the “Proxy Statement”), are incorporated by reference in Part III.

|

Item

|

|

Description

|

|

Page

|

|

|

|

|

|

|

|

PART I

|

|

|

||

|

1.

|

|

|

3

|

|

|

1A.

|

|

|

13

|

|

|

1B.

|

|

|

20

|

|

|

2.

|

|

|

20

|

|

|

3.

|

|

|

20

|

|

|

4.

|

|

|

21

|

|

|

PART II

|

||||

|

5.

|

|

|

21

|

|

|

6.

|

|

|

23

|

|

|

7.

|

|

|

23

|

|

|

7A.

|

|

|

31

|

|

|

8.

|

|

|

31

|

|

|

9.

|

|

|

31

|

|

|

9A.

|

|

|

31

|

|

|

9B.

|

|

|

32

|

|

|

PART III

|

||||

|

10.

|

|

|

33

|

|

|

11.

|

|

|

33

|

|

|

12.

|

|

|

33

|

|

|

13.

|

|

|

33

|

|

|

14.

|

|

|

33

|

|

|

PART IV

|

||||

|

15.

|

|

|

33

|

|

FORWARD LOOKING STATEMENTS

This Form 10-K contains “forward-looking statements” relating to projections, plans, objectives, estimates, and other statements of future performance. These forward-looking statements are subject to known and unknown risks and uncertainties relating to our future performance that may cause our actual results, performance, achievements, or industry results, to differ materially from those expressed or implied in any such forward-looking statements. Our business operates in highly competitive markets and our operating results and the achievement of the forward-looking statements may be impacted by changes in general economic conditions, competition, reimbursement levels, customer and market preferences, government regulation, tax regulation, foreign exchange rate fluctuations, the degree of market acceptance of products, the uncertainties of potential litigation, and other matters detailed in the “Risk Factors” contained in Item IA of this report.

We do not undertake nor assume any obligation to update any forward-looking statements that we may make from time to time.

We are a medical device company that develops, manufactures and markets innovative, proprietary products for the treatment of voiding dysfunctions. You can access, free of charge, our filings with the Securities and Exchange Commission, including our annual report on Form 10-K, our quarterly reports on Form 10-Q, current reports on Form 8-K and any other amendments to those reports, at our website www.uroplasty.com, or at the Commission’s website at www.sec.gov.

Our primary focus is on two products: the Urgent PC® Neuromodulation System, which we believe is the only FDA-cleared, minimally-invasive, neuromodulation system that delivers percutaneous tibial nerve stimulation (PTNS) for office-based treatment of overactive bladder (OAB) and the associated symptoms of urinary urgency, urinary frequency, and urge incontinence; and Macroplastique® Implants, an injectable, urethral bulking agent for the treatment of adult female stress urinary incontinence primarily due to intrinsic sphincter deficiency (ISD). Outside of the U.S., our Urgent PC System is also approved for treatment of fecal incontinence, and Macroplastique is also approved for treatment of male stress incontinence, fecal incontinence, vocal cord rehabilitation and vesicoureteral reflux.

Our primary focus is on growth in the U.S. market, which we entered in 2005 with our Urgent PC System. Prior to that time, essentially all of our business involved the sale of Macroplastique and other products outside of the U.S. We believe the U.S. market presents a significant opportunity for growth in sales of our products.

The Urgent PC Neuromodulation System uses percutaneous stimulation to deliver to the tibial nerve electrical pulses that travel to the sacral nerve plexus, a control center for bladder function. We have received regulatory clearances for sale of the Urgent PC System in the United States, Canada and Europe. We launched sales of our second generation Urgent PC System in late 2006. We have intellectual property rights relating to key aspects of our neuromodulation therapy.

We have sold Macroplastique for urological indications in over 40 countries outside the United States since 1991. In October 2006, we received from the FDA pre-market approval for the use of Macroplastique to treat adult female stress urinary incontinence. We began marketing Macroplastique in the United States in 2007.

We believe physicians prefer our products because they offer effective therapies for patients that can be administered in office or outpatient surgical-based settings and, to the extent reimbursement is available, provide the physicians a profitable revenue stream. We believe patients prefer our products because they are minimally invasive treatment alternatives that do not have the side effects associated with pharmaceutical treatment options nor the morbidity associated with surgery.

Our sales have been significantly influenced by the availability of third-party reimbursement for PTNS treatments. Sales of our Urgent PC System in the U.S. grew rapidly during fiscal 2007 and 2008 with rapid market acceptance of PTNS treatments that were reimbursed under a Category 1 Current Procedure Technology (CPT®) code. Sales declined from the first quarter of fiscal 2009 through the third quarter of fiscal 2011, because of lower or unavailable reimbursement when the American Medical Association (AMA) advised providers that reimbursement for PTNS treatments should requested under an unlisted CPT code.

We responded by sponsoring several clinical studies over the following two years that were published in U.S. peer-reviewed journals. With favorable results from these studies, we applied for, and effective January 2011 the AMA granted, a new Category 1 CPT code for PTNS treatments. As a result, we expanded our U.S. field sales and support organization from 15 employed sales representatives and six independent manufacturer’s representatives on April 1, 2010 to 39 employed sales representatives on March 31, 2013, and sales of our Urgent PC System began to increase.

We have since focused our efforts on expanding reimbursement coverage with Medicare carriers and private payers by instituting a comprehensive program to educate their medical directors regarding the clinical effectiveness, cost effectiveness and patient benefits of PTNS treatments using our Urgent PC System. After a positive coverage decision by Wisconsin Physician Services effective June 1, 2013, regional Medicare carriers representing 48 states and the District of Columbia, with approximately 46 million covered lives, provide coverage for PTNS treatments. In addition, we estimate that private payers insuring approximately 97 million lives provide coverage for PTNS treatments. At June 1, 2013, one regional Medicare carrier representing 2 states, with approximately 3 million covered lives, continued to decline reimbursement coverage for PTNS treatments.

With the availability of a CPT Category 1 code and expanded reimbursement coverage from third-party payers, as well as an expanded sales organization, sales of our Urgent PC System in the U.S. increased 84% in the year ended March 31, 2012 over the year ended March 31, 2011, and continued this positive trend with 35% growth to $10.5 million in the year ended March 31, 2013. Overall revenue growth slowed somewhat in the year ended 2013, as sales in the U.S. of our more mature Macroplastique product and sales outside of the U.S. declined.

We expect to continue to emphasize sales of our Urgent PC System in the United States, and have retained new management to restructure our sales organization. The intent is to increase our focus on training physicians on the continued use and benefits of a treatment regime using the Urgent PC System for overactive bladder. As part of this process, we intend to test the use of clinical support specialists in some of our markets. We also have earmarked additional marketing dollars for the coming fiscal year to better introduce our products to both those members of the public most likely to require treatment with the device, and to key opinion leaders in the urology markets. We do not expect to see significant growth in our U.S. Macroplastique business, because we believe it is a small, mature market that is more competitively penetrated than the market for OAB treatment using PTNS.

Both of our products are targeted at the market for treatment of voiding dysfunctions and address overlapping submarkets. Voiding dysfunctions affect urinary or bowel control and can result in uncontrolled bladder sensations (overactive bladder) or unwanted leakage (urinary or bowel/fecal incontinence).

We believe that over the next several years a number of key demographic and technological factors will accelerate growth in the market for medical devices to treat OAB and other urinary and bowel voiding dysfunctions. These factors include the following:

| · | Aging population. The number of individuals developing voiding dysfunctions will increase as the population ages and as life expectancies rise. |

Symptoms. For individuals with overactive bladder symptoms, the nervous system control for bladder filling and urinary voiding is incompetent. For OAB patients, signals to indicate a full bladder are sent early and frequently, triggers to allow the bladder to relax for filling are ineffective, and nervous controls of the urethral sphincter to keep the bladder closed until an appropriate time are inadequate. An individual with OAB may exhibit one or all of the symptoms that characterize overactive bladder: urinary urgency, urinary frequency and urge incontinence. Urgency is the strong, compelling need to urinate and frequency is a repetitive need to void. For most individuals, normal urinary voiding is about eight times per day while individuals with OAB may seek to void over 20 times per day and more than two times during the night. Urge incontinence refers to the involuntary loss of urine associated with an abrupt, strong desire to urinate that typically results in an accident before the individual can reach a restroom.

Treatment of Symptoms. When patients seek treatment for OAB, physicians normally start with conservative therapies such as biofeedback and behavioral modification. When, as is often the case, these therapies are not entirely successful, the next treatment of choice is drug therapy. If, as is the case with a majority of the patients, the drug therapy is ineffective or cannot be tolerated by the patient, the physicians suggest other treatments. For those patients, we believe the minimally invasive Urgent PC treatments offer an alternative to the more invasive treatments such as surgery or implantation of a sacral nerve stimulation device.

Biofeedback and Behavioral Modification. Bladder training and scheduled voiding techniques, often accompanied by the use of voiding diaries, are non-invasive approaches to managing OAB. These techniques are seldom completely effective because they rely on the diligence of and compliance by the individual. In addition, these techniques may not affect the underlying cause of the condition.

Drug Therapy. The most common treatment for OAB is drug therapy using an anticholinergic agent. However, for many patients, drugs are ineffective or the side effects are so bothersome that they discontinue the medications. Common side effects include dry mouth, dry eyes, constipation, cognitive changes and blurred vision.

Neuromodulation. Normal urinary control is dependent upon properly functioning neural pathways and coordination among the central and peripheral nervous systems, the nerve pathways, the bladder and the sphincter. Unwanted, uncoordinated or disrupted signals along these pathways can lead to OAB symptoms. Therapy using neuromodulation incorporates electrical stimulation to target specific neural tissue and “jam” the pathways transmitting unwanted signals. To alter bladder function, stimulation must be delivered to the sacral nerve plexus, which innervates the bladder and pelvic floor. Neuromodulation to treat OAB may be performed by a surgically implanted sacral nerve stimulation device or performed in a physician’s office by the non-surgical PTNS procedure delivered by the Urgent PC.

The Uroplasty Solution: The Urgent PC Neuromodulation System. The Urgent PC Neuromodulation System is a minimally invasive nerve stimulation device designed for office-based treatment of OAB and the associated symptoms of urge incontinence, urinary urgency and urinary frequency. Using a small-gauge needle electrode inserted above the ankle, the Urgent PC System delivers electrical impulses to the tibial nerve that travel to the sacral nerve plexus, a control center for pelvic floor and bladder function.

We believe that the Urgent PC System is the only FDA-cleared PTNS device in the United States market for treatment of OAB. Components of the Urgent PC Neuromodulation System include a hair-width needle electrode, a lead set and an external, handheld, battery-powered stimulator. For each 30-minute office-based therapy session, the physician or other qualified health care provider inserts the needle electrode above the ankle and connects the electrode to the stimulator. Typically, a patient undergoes a course of 12 consecutive weekly treatments, and, subsequently, a personal treatment plan of single treatments at lesser frequency to sustain the therapeutic effect.

In late 2005, we received regulatory clearances for sale of the Urgent PC System in the United States, Canada and Europe. Subsequently, we launched the System for sale in those markets. We launched our second generation Urgent PC System in late 2006.

Symptoms and Prevalence. Urinary incontinence is defined as the involuntary loss of urine, and is a very common health problem, especially among women. In 2007, the US Department of Health and Human Services, Public Health Service, National Institutes of Health, National Institute of Diabetes and Digestive and Kidney Diseases reported that, depending on the definition of urinary incontinence used, 5% to 50% of the adult U.S. population suffers from some form of urinary incontinence. The prevalence of urinary incontinence increases with advancing age, and the prevalence of U.S. population with urinary incontinence is expected to grow over the next decades as the U.S. population ages. Urinary incontinence often results in social isolation, depression, and poor self-rated health and quality of life, and is a significant medical condition with considerable public health impact.

Causes of Urinary Incontinence. The mechanisms of urinary continence are complex and involve the interaction among several anatomical structures. In females, urinary continence is controlled by the sphincter muscle and pelvic floor support structures that maintain proper urethral position. The sphincter muscle surrounds the urethra and provides constrictive pressure to prevent urine from flowing out of the bladder, especially with increased intra-abdominal pressure. Urination occurs when the sphincter relaxes as the bladder contracts, allowing urine to flow through the urethra. Incontinence may result when any part of the urinary tract fails to function as intended. Incontinence may be caused by damage during childbirth, pelvic trauma, spinal cord injuries, neurological diseases (e.g., multiple sclerosis and poliomyelitis), birth defects (e.g., spina bifida) and degenerative changes associated with aging.

| · | Overflow Incontinence — Overflow incontinence is associated with an over-distention of the bladder. This can be the result of an under-active bladder or an obstruction in the bladder or urethra. |

Treatments. There are two general approaches to dealing with urinary incontinence. One approach is to manage symptoms, such as through absorbent products, catheters, behavior modification and drug therapy. The other approach is to undergo curative treatments in an attempt to restore continence, such as injection of urethral bulking agents or surgery, or a combination of the two. We believe that patients prefer less invasive treatments that provide the most benefit and have little or no side effects.

Injectable Bulking Agents. Urethral bulking agents (UBAs) are injected into the area around the urethra, to augment the surrounding tissue for increased capacity to control the release of urine for patients with SUI. Hence, these materials are often called “bulking agents” or “injectables” and are an attractive alternative to surgery because they are considerably less invasive, offer a quick recovery, and do not require the use of an operating room for placement; UBAs can be implanted in an office or out-patient facility. Additionally, the use of a UBA does not preclude the subsequent use of more invasive treatments if required. Furthermore, UBAs may be used to resolve lingering symptoms for patients who have undergone certain more invasive treatments, such as mid-urethral slings, which failed to completely resolve the stress urinary incontinence conditions.

Surgery. In women, SUI may be corrected through surgery with a mid-urethral sling which provides a hammock-type support for the urethra to prevent its downward movement and the associated leakage of urine.

The Uroplasty Solution: Macroplastique Implants. Macroplastique is used to treat adult female stress urinary incontinence due to ISD. It is designed to restore the patient’s urinary continence immediately following treatment. Macroplastique is a soft-textured, permanent implant injected, under endoscopic visualization, around the urethra distal to the bladder neck. It is a proprietary composition of heat vulcanized, solid, soft, irregularly shaped polydimethylsiloxane (solid silicone elastomer) implants suspended in a biocompatible excretable carrier gel. We believe our compound is better than other commercially available bulking agents because, with its unique composition, shape and size, it does not degrade, is not absorbed into surrounding tissues and does not migrate from the implant site.

We have sold Macroplastique for several urological indications in over 40 countries outside the United States since 1991. In October 2006, we received FDA pre-market approval for the use of Macroplastique to treat adult female SUI due to ISD. We began marketing Macroplastique in the United States in early 2007.

Macroplastique® for Vesicoureteral Reflux. Outside the U.S., we market the Macroplastique Implant products for treatment of vesicoureteral reflux: the abnormal backflow of urine from the bladder into the ureters or kidneys that is most prevalent in infants and children where the ureters did not fully develop. In this application a bolus of the elastomer implant is injected around the orifice or valve where the ureter enters the bladder.

PTQ® Implants. We also market our silicone elastomer implants under the name PTQ® Implants outside of the U.S. as a minimally invasive product to address fecal incontinence (sometimes referred to as bowel incontinence). Our PTQ Implants offer minimally-invasive, soft-textured permanent implant for treatment of fecal incontinence. PTQ is implanted circumferentially into the submucosa of the anal canal, creating a “bulking” and supportive effect around the anal sphincter. PTQ is CE marked and currently sold outside the United States in various international markets.

Urgent PC for Fecal Incontinence. The Urgent PC Neuromodulation System is CE marked and sold outside of the United States for the treatment of fecal incontinence. We also intend to explore the commercialization of Urgent PC for this application in the U.S. and started on a multiyear pilot clinical trial in fiscal 2013 as a prelude to a full clinical study for FDA clearance.

VOX® Implants. In addition to urological applications, we market our silicone elastomer bulking material outside the United States to help improve speech and swallowing function in patients with unilateral vocal cord paralysis. The implants are sold for vocal cord rehabilitation applications under the trade name VOX® Implants.

Distributed Products. In The Netherlands and United Kingdom only, we distribute certain wound care products in accordance with a distributor agreement. Under the terms of the distributor agreement, we are not obligated to purchase any minimum level of wound care products.

Our goal is to become the leading provider of minimally invasive, office and outpatient surgical-based solutions to treat and improve the quality of life for patients suffering the physical and emotional stress resulting from voiding dysfunction problems. We believe that with our Urgent PC Neuromodulation System and Macroplastique products we can increasingly garner the attention of key physicians and distributors to grow our revenue. The key elements of our strategy are to:

We are focusing our sales and marketing efforts primarily on urologists, urogynecologists and gynecologists with significant office-based and outpatient surgery-based patient volume.

To support our business in the United States, we have a sales organization, consisting primarily of 39 direct field sales representatives, a marketing organization to market our products directly to our customers and a reimbursement department. We anticipate further increasing our sales and marketing organization in the United States, as needed, to support our sales growth.

Outside of the United States, we sell our products primarily through a direct sales organization in the United Kingdom and The Netherlands, and in all other markets primarily through distributors. Each of our distributors has a territory-specific distribution agreement, including requirements indicating they may not sell products that compete directly with ours. Collectively, distributors accounted for approximately 14%, 17% and 25% of our total net sales for fiscal 2013, 2012 and 2011, respectively.

We use clinical studies and worldwide scientific community awareness programs to demonstrate the safety and efficacy of our products. This data is important to obtain regulatory approval and to support our sales staff and distributors in securing product reimbursement in their territories. Publications of clinical data in peer-reviewed journals and presentations at professional society meetings by clinical researchers add to the scientific community awareness of our products, including patient indications, treatment technique and expected outcomes. We provide a range of activities designed to support physicians in their clinical research.

In the United States as well as in foreign countries, sales of our products depend in significant part on the availability of reimbursement from third-party payers. In the United States, third-party payers consist of government programs such as Medicare, private health insurance plans, managed care organizations and other similar programs. For any product, three factors are critical to reimbursement:

| · | coding, which ensures uniform descriptions of procedures, diagnoses and medical products; |

| · | coverage, which is the payer’s policy describing the clinical circumstances under which it will pay for a given treatment; and |

| · | payment processes and amounts. |

We believe the availability of a Category 1 CPT code for PTNS treatments has encouraged, and will continue to encourage, broader use of and reimbursement for our Urgent PC System in the U.S. However, each governmental and private payer makes its own coverage decision.

With respect to Medicare reimbursement, each regional Medicare carrier is entitled to make a separate decision to provide coverage if at all, and the number of PTNS treatments covered. After a positive coverage decision by Wisconsin Physician Services effective June 1, 2013, regional Medicare carriers representing 48 states and the District of Columbia, with approximately 46 million covered lives, provide coverage for PTNS treatments. In addition, we estimate that private payers insuring approximately 97 million lives provide coverage for PTNS treatments. At June 1, 2013, one regional Medicare carrier representing 2 states, with approximately 3 million covered lives, continued to decline reimbursement coverage for PTNS treatments. Further the amount reimbursed and number of treatments that may be covered can vary from region to region and we continue to work with the various carriers to educate them in the positive results we have achieved with longer term clinical studies.

The Centers for Medicare and Medicaid Services has announced consolidation of some of the regional Medicare claims administrators. When this consolidation occurs, there is no guarantee that Medicare beneficiaries in a region with reimbursement coverage will continue to be reimbursed when consolidated into a regional Medicare carrier with a negative reimbursement policy, or, if reimbursed, the coverage would remain unchanged. We continue to work to clinically prove the benefits of longer term treatment using PTNS and to educate regional carriers about those benefits.

Outside of the U.S., Urgent PC treatments are reimbursed under an available reimbursement code in the Netherlands. In other countries in Europe there are no specific reimbursement codes for Urgent PC treatments and generally reimbursement is from fund-holder trusts or global hospital budgets.

We believe there are appropriate CPT codes available to describe the use of Macroplastique to treat adult female SUI due to ISD in the United States. Outside of the United States, government managed health care systems and private insurance control reimbursement for devices and procedures. Reimbursement systems in international markets vary significantly by country. In the European Union, reimbursement decision-making is neither regulated nor integrated at the European Union level. Each country has its own system, often closely protected by its corresponding national government. Reimbursement for Macroplastique has been successful in multiple international markets where hospitals and physicians have budgets approved by fund-holder trusts or global hospital budgets.

We subcontract the manufacturing of the Urgent PC System and its related components, and have a U.S. FDA-registered manufacturing facility in Minnetonka, Minnesota, where we manufacture all of our tissue bulking products. Our facility uses dedicated heating, cooling, ventilation and high efficiency particulate air filtration systems to provide cleanroom and other controlled working environments. Our trained technicians perform all critical manufacturing processes in qualified environments according to validated written procedures. We use qualified vendors to sterilize our products using validated methods.

Our manufacturing facility and systems are periodically audited by regulatory agencies and other authorities to ensure compliance with ISO 13485 (medical device quality management systems), applicable European and Canadian medical device requirements, as well as FDA’s Quality Systems Regulations. We also are subject to additional state, local, and federal government regulations applicable to the manufacture of our products. While we believe we are compliant with all applicable regulations, we cannot guarantee that we will pass each regulatory audit.

We purchase several medical grade materials and other components for use in our finished products from single source suppliers meeting our quality and other requirements. Although we believe our sources of supply could be replaced if necessary without undue disruption, it is possible that the process of qualifying new suppliers could cause an interruption in our ability to manufacture our products, which could have a negative impact on sales.

The market for voiding dysfunction products is intensely competitive. Competitors offer management and curative treatments, pharmaceutical products such as anticholinergic drugs, injectable drugs, implantable including neuromodulation devices, urethral injectables and urethral sling products. We believe the principal decision factors among treatment methods include severity of patient symptoms and procedure risk, physician and patient acceptance of the treatment method, cost, availability of third-party reimbursement, and marketing and sales coverage. In addition to adequately addressing the decision factors, our ability to compete in this market will also depend on the consistency of our product quality as well as delivery and product pricing. Other factors affecting our success include our product development and innovation capabilities, clinical study results, ability to obtain required regulatory approvals, ability to protect our proprietary technology, manufacturing and marketing capabilities and ability to attract and retain skilled employees.

PTNS. We believe the Urgent PC Neuromodulation System offers a minimally invasive, office-based treatment alternative in the continuum of care for OAB patients. Conservative therapies such as dietary restrictions, pelvic floor exercises, bladder retraining, biofeedback, and anticholinergic drugs usually precede Urgent PC treatments. Anticholinergic medications that could be seen as competing with PTNS include Detrol® and Toviaz® (both by Pfizer Inc.); Ditropan® (Johnson and Johnson); Enablex® (Novartis); Sanctura® (Allergan) and Vesicare® (GlaxoSmithKline). These medications treat symptoms of overactive bladder, some by preventing unwanted bladder contractions and others by tightening the bladder or urethra muscles or by relaxing bladder muscles. We believe our Urgent PC System normally is prescribed after these drugs are used but discontinued because they were ineffective or had unwanted side effects. In the case of anticholinergic medications, the side effects often include dry eyes, dry mouth, constipation, cognitive changes and blurred vision.

Allergan, Inc. recently began to commercialize Botulinum toxin A (Botox®) for OAB treatments, and this treatment could be seen as direct competitor for Urgent PC following unsuccessful drug therapy. In this procedure, Botox is injected in and around the urethra, often with dozens of individual injection sites, to numb and mask the symptoms of urgency and frequency. Nevertheless, although we believe that marketing campaigns by Allergan will increase awareness of OAB, we also believe that the side effects of Botox injections for this application, which can include urine retention and urinary tract infection, will lead many patients to choose our less invasive solution.

The Medtronic InterStim neuromodulation device, which stimulates the sacral nerve, requires surgical implantation of a lead near the patient’s spine in addition to a battery powered stimulator in the buttocks. In contrast, the Urgent PC Neuromodulation System allows minimally invasive stimulation of the sacral nerve plexus in an office-based setting without any surgical intervention. Other companies may also enter the U.S. market with neuromodulation or other products for the treatment of OAB.

Bulking. Injectable urethral bulking agents for SUI competing directly with Macroplastique in the United States include: Durasphere® manufactured by Carbon Medical Technologies and distributed by Coloplast; and Coaptite® manufactured by BioForm, Inc. and distributed by Boston Scientific. We believe Macroplastique competes favorably against these products because it will not degrade, resorb or migrate, has no special preparation or storage requirements, and is safe and effective for treating adult female stress urinary incontinence.

Outside of the United States, Deflux® (manufactured by Q-Med AB, Sweden and distributed by Salix Pharmaceuticals) and Bulkamid® (manufactured by Contura, Denmark and distributed by Johnson and Johnson) compete with Macroplastique for vesicoureteral reflux and SUI, respectively.

Many of our competitors and potential competitors have significantly greater financial, manufacturing, marketing and distribution resources and experience than us. In addition, many of our competitors offer broader product lines within the urology market, which may give these competitors the ability to negotiate exclusive, long-term supply contracts and to offer comprehensive pricing for their products. It is possible other large health care and consumer products companies may enter this industry in the future. Furthermore, smaller companies, academic institutions, governmental agencies and other public and private research organizations will continue to conduct research, seek patent protection and establish arrangements for commercializing products. These products may compete directly with any products that we may offer in the future.

The testing, manufacturing, promotion, marketing and distribution of our products in the United States, Europe and other parts of the world are subject to regulation by numerous governmental authorities, including the FDA, the European Union and other analogous agencies.

Our products are regulated in the United States as medical devices by the FDA under the Food, Drug and Cosmetic Act, or FDC Act. Noncompliance with applicable requirements can result in, among other things:

Depending on the degree of risk posed by the medical device and the extent of controls needed to ensure safety and effectiveness, there are two pathways for FDA marketing clearance of medical devices. For devices deemed by FDA to pose relatively less risk (Class I or Class II devices), manufacturers, in most instances, must submit a pre-market notification requesting permission for commercial distribution, known as 510(k) clearance. Devices deemed by FDA to pose the greatest risk (Class III devices), such as life-sustaining, life-supporting or implantable devices, or a device deemed not to be substantially equivalent to a previously cleared 510(k) device, require the submission of a pre-market approval (PMA) application. The FDA can also impose restrictions on the sale, distribution or use of devices at the time of their clearance or approval, or subsequent to marketing.

In October 2005, our initial version of the Urgent PC System received 510(k) clearance for sale within the United States. In July 2006, our second generation Urgent PC System received 510(k) clearance for sale within the United States.

In October 2006, we received FDA pre-market approval for the use of Macroplastique to treat female stress urinary incontinence in the United States. As part of the FDA-approval process, we are conducting a customary post-market study.

| · | Quality System Regulations, which require manufacturers to follow design, testing, control, documentation and other quality assurance procedures during the manufacturing process; |

The FDC Act requires that medical devices be manufactured in accordance with FDA’s current Quality System Regulations, which require, among other things, that we:

| · | regulate our design and manufacturing processes and control them by the use of written procedures; |

| · | allow the FDA to inspect our manufacturing facilities on a periodic basis to monitor our compliance with Quality System Regulations. |

Our manufacturing facility and processes have been inspected and certified in compliance with ISO 13485, applicable European medical device directives and Canadian Medical Device Requirements.

The European Union has adopted rules that require that medical products receive the right to affix the CE mark, which stands for Conformité Européenne. The CE mark demonstrates adherence to quality standards and compliance with relevant European medical device directives. Products that bear the CE mark can be imported to, sold or distributed within the European Union.

Our initial version of the Urgent PC System received CE marking in November 2005. Our second generation Urgent PC System received CE mark approval and approval from the Canadian Therapeutic Products Directorate of Health in June 2006.

We received the CE mark approval for Macroplastique in 1996 for the treatment of male and female stress urinary incontinence and vesicoureteral reflux; for VOX in 2000 for vocal cord rehabilitation and; for PTQ in 2002 for the treatment of fecal incontinence. Our manufacturing facilities and processes have been inspected and certified by AMTAC Certification Services, a recognized Notified Body, a testing and certification firm based in the United Kingdom.

We currently sell our products in approximately 40 foreign countries, including those within the European Union. Requirements pertaining to medical devices vary widely from country to country, ranging from no health regulations to detailed submissions such as those required by the FDA. We have obtained regulatory approvals in countries where required of us to sell our products. We believe the extent and complexity of regulations for medical devices such as those produced by us are increasing worldwide. We anticipate that this trend will continue and that the cost and time required to obtain approval to market in any given country will increase.

We seek to establish and protect our proprietary technology using a combination of patents, trademarks, copyrights, trade secrets, and nondisclosure and non-competition agreements. We file patent applications for patentable technologies we consider important to the development of our business based on an analysis of the cost of obtaining a patent, the likely scope of protection, and the relative benefits of patent protection compared to trade secret protection, among other considerations.

We have obtained, by filing and by acquisition, various issued U.S. and foreign patents and pending patent applications related to electro-nerve stimulation. In addition, we hold multiple U.S. and foreign patents covering soft-tissue bulking materials, processes and applications. While we believe that our patents adequately protect our technologies, there can be no assurance that any of our issued patents are of sufficient scope or strength to provide meaningful protection and that any of our pending patent applications will result in patents being issued to us. In addition, there can be no assurance that any of our current or future patents will not be challenged, narrowed, invalidated or circumvented by others, or that our patents will provide us with any competitive advantage. Any legal proceedings to maintain, defend or enforce our patent rights could be lengthy and costly, with no guarantee of success. Third parties could also hold patents that may require us to negotiate licenses to conduct our business, and there can be no assurance that the required licenses would be available on reasonable terms, or at all.

We also seek to protect our trade secrets by requiring employees, consultants, and other parties to sign confidentiality agreements and noncompetition agreements, and by limiting access by outside parties to confidential information. There can be no assurance that these measures will prevent the unauthorized disclosure or use of this information or that others will not be able to independently develop this information.

In the U.S. and throughout the European Union, we have registered “Uroplasty” as our Company name, “Urgent” for our neuromodulation product, “Macroplastique” for our urological tissue bulking products, “VOX” for our otolaryngology tissue bulking products, and “PTQ” for our colorectal tissue bulking products.

We have certain royalty agreements under which we pay royalties on sales of Macroplastique and the Macroplastique implantation needle-positioning device.

We have a research and development program to develop, enhance and evaluate potential new incontinence products for which we incur costs for regulatory submissions, regulatory compliance and clinical research. Our expenditures for clinical research include studies for new applications or indications for existing products, post-approval regulatory compliance and marketing and reimbursement approval by third-party payers. Our expenditures for research and development totaled approximately $2.4 million, $1.9 million and $1.7 million for fiscal 2013, 2012 and 2011, respectively.

The medical device industry is subject to substantial litigation. We face an inherent risk of liability for claims alleging adverse effects to the patient. We currently carry $10 million of worldwide product liability insurance. However, we cannot assure you that our existing insurance coverage limits are adequate to protect us from liabilities we might incur. Product liability insurance is expensive and in the future may not be available to us on acceptable terms, or at all. Furthermore, we do not expect to be able to obtain insurance covering our costs and losses as a result of any product recall. A successful claim in excess of our insurance coverage could materially deplete our assets. Moreover, any claim against us could generate negative publicity, which could decrease the demand for our products and our ability to generate revenues.

Compliance by us with applicable environmental requirements during fiscal years 2013, 2012 and 2011, respectively has not had a material effect upon our capital expenditures, earnings or competitive position.

During fiscal 2013, 2012 and 2011, none of our customers accounted for 10% or more of our net sales.

We did not have significant backlog at fiscal year-end 2013, 2012 or 2011. We process customer orders generally within one or two days of receipt of the order.

As of March 31, 2013, we had 101 employees, of which 96 were full-time and 5 were part-time. No employee was subject to a collective bargaining agreement. We believe we maintain good relations with our employees.

We were incorporated in January 1992 as a Minnesota corporation and a wholly owned subsidiary of our original parent. In February 1995, we became a stand-alone, privately held company pursuant to a Plan of Reorganization confirmed by the U.S. Bankruptcy Court. We became a reporting company pursuant to a registration statement filed with the Securities and Exchange Commission in July 1996.

|

Uroplasty BV

|

Incorporated in The Netherlands, distributes the Urgent PC Neuromodulation System, Macroplastique Implants, VOX Implants, PTQ Implants, all of their accessories, and wound care products. Products are sold primarily through distributors.

|

|

|

|

|

Uroplasty LTD

|

Incorporated in the United Kingdom and acts as the sole distributor of the Urgent PC Neuromodulation System, Macroplastique Implants, PTQ Implants, all of their accessories, and wound care products in the United Kingdom and Ireland. Products are sold primarily through a direct sales organization.

|

Our operations are subject to a number of risks and uncertainties that may affect our financial results, our accounting, and the accuracy of the statements we make in this Form 10-K. For example, we make statements about our belief in the efficacy of our product, the impact of regulatory and reimbursement approvals on our products and revenues, trends in international regulation, the attributes of our products versus those of our competitors, the adequacy of our resources, including cash, available to us, and other matters all of which represent our expectations or beliefs about future events. Our actual results may vary from these expectations because of a number of factors that affect our business, the most important of which include the following:

We have incurred net losses in each of the last five fiscal years. As of March 31, 2013, we had an accumulated deficit of approximately $39 million primarily because of costs relating to the development, including seeking regulatory approvals, and commercialization of our products. We expect our operating expenses relating to sales and marketing activities, product development and clinical trials, including an FDA-mandated post-market clinical study for our Macroplastique product, will continue during the foreseeable future. To achieve profitability, we must generate substantially more revenue than we have in prior years. Our ability to achieve significant revenue growth will depend, in large part, on our ability to achieve widespread market acceptance and third-party reimbursement for our products and successfully expand our business in the U.S. We may never achieve substantial market acceptance, realize significant revenue from the sale of our products or be profitable.

The use and acceptance of our products is heavily dependent upon the availability of third-party reimbursement for the procedures in which our products are used.

In the United States, healthcare providers that purchase medical devices, including our products, generally rely on third-party payers, including Medicare, Medicaid, private health insurance carriers and managed care organizations, to reimburse all or part of the cost and fees associated with the procedures performed using these devices. The commercial success of our products will depend on the ability of healthcare providers to obtain adequate reimbursement from third-party payers for the procedures in which our products are used. Third-party payers are increasingly challenging the coverage and pricing of medical products and procedures.

Even if a procedure is eligible for reimbursement, the level of reimbursement may not be adequate to justify the use of our products. In addition, third-party payers may deny reimbursement if they determine that the device used in the treatment was not cost-effective or was used for a non-approved indication, particularly if there is not a published CPT code for reimbursement. For example, in 2009, the AMA advised the medical community that the previously recommended Category 1 CPT code for PTNS treatments should be replaced with an unlisted code. As a result, many third-party insurers delayed or denied reimbursement for PTNS treatments, significantly impacting the sales of our Urgent PC, until a new code was effective in January 2011.

The availability of the new Category 1 CPT code for PTNS treatments has encouraged broader use of our Urgent PC Neuromodulation System, but it has not resulted in universal coverage and there can be no assurance that additional payers will agree to create coverage policies or that the policies, if they are created, will provide adequate reimbursement, that existing coverage will not again be challenged (as it was in fiscal 2009), or that government actions will not decrease the level of reimbursement.

Reimbursement and healthcare payment systems in international markets vary significantly by country, with some countries offering government-sponsored healthcare or private insurance, or both. In many countries where there is government-sponsored healthcare reimbursement, decisions are made by individual hospitals with the government setting an upper limit of reimbursement. In most foreign countries, there are also insurance systems that may offer payments for alternative procedures. We cannot be certain that we, or in countries in which we work with our distributors, will successfully and cost-effectively manage all of these payment systems.

All third-party reimbursement programs, whether government-funded or insured commercially, inside the United States or outside, are developing increasingly sophisticated methods of controlling health care costs through prospective reimbursement and capitation programs, group purchasing, redesign of benefits, second opinions, careful review of bills, encouragement of healthier lifestyles and exploration of more cost-effective methods of delivering healthcare. These types of programs can potentially limit the amount that healthcare providers may be willing to pay for medical devices and could have a material adverse effect on our financial position and results of operations.

Medicare claims administrators are scheduled to undergo consolidation and that could affect reimbursement.

The Centers for Medicare and Medicaid Services expects to continue to consolidate the Medicare claims regions over the next several years, and to correspondingly reduce or consolidate claims administrators. To the extent that, as part of this consolidation, regions in which there is coverage for PTNS treatments are consolidated into a region that does not provide coverage for PTNS treatments, it is unclear whether PTNS treatments using our Urgent PC will continue to be reimbursed, or, if reimbursed, whether the coverage will remain unchanged. Some of the future consolidation decisions have been announced and are currently being disputed by administrators whose regions were reduced or eliminated, creating uncertainty in the marketplace. Accordingly, this consolidation process and the uncertainty it creates could negatively impact reimbursement for PTNS treatments using our products, and negatively impact our sales.

In addition to the availability of third-party reimbursement, market acceptance of our products will depend on our ability to demonstrate the safety, clinical efficacy, perceived benefits, and cost-effectiveness of our products compared to products or treatment options of our competitors. We cannot assure you that we will be successful in educating the marketplace about the benefits of our products. Our Urgent PC product requires a new treatment protocol for the physicians and their staff to implement repeatedly. Even if customers accept our products, this acceptance may not translate into repeat sales if our customers do not fully adopt the new treatment protocol in their practice.

We are subject to changing federal and state regulations that could increase the cost of doing business or impose requirements with which we cannot comply

In response to perceived increases in health care costs in recent years, there have been and continue to be proposals by the federal government, state governments, regulators and third-party payers to control these costs and, more generally, to reform the U.S. healthcare system. Certain of these proposals could limit the prices we are able to charge for our products or the amounts of reimbursement available for our products and could limit the acceptance and availability of our products, adversely affecting our financial position and results of operations.

The 2010 Healthcare Reform Legislation imposes an excise tax on us that we may be unable to recoup, and requires cost controls that may impact the rate of reimbursement for our products.

Significant U.S. healthcare reform legislation, the Patient Protection and Affordable Care Act, as reconciled by the Health Care and Education Reconciliation Act of 2010 (collectively the “PPACA”), was enacted into law in March 2010. Commencing January 1, 2013, the PPACA imposes on manufacturers or producers making sales of medical devices in the U.S., other than sales at retail for individual use, an excise tax. Our U.S. net sales, all subject to the excise tax, represented approximately 73% of our worldwide consolidated net sales in fiscal 2013 and we expect U.S. sales to continue to grow and become a greater proportion of our worldwide consolidated net sales. To the extent the clinics and physicians will not absorb increased costs represented by the tax because of reimbursement limitations, we likely will not be able to offset the tax with increased revenue. Accordingly, the new tax will adversely affect our business, cash flows and results of operations. Although several bills have been proposed in U.S. Congress to eliminate the tax, including a bill passed by the U.S. Senate, most of these bills are tied to corresponding increases in taxes from other sources, and therefore face substantial opposition.

The PPACA also contains provisions aimed at improving the quality and decreasing the costs of healthcare. The Medicare provisions include value-based payment programs, increased funding of comparative effectiveness research, reduced hospital payments for avoidable readmissions and hospital acquired conditions, and pilot programs to evaluate alternative payment methodologies that promote care coordination (such as bundled physician and hospital payments). Additionally, the PPACA includes a reduction in the annual rate of inflation for hospitals that began in 2011 and provides for the establishment of an independent payment advisory board to recommend ways of reducing the rate of growth in Medicare spending beginning in 2014. Many of these provisions will not be effective for a number of years and there are many programs and requirements for which the details have not yet been fully established. Accordingly, although it remains impossible to predict the extent of the regulation and the full impact of the PPACA, any changes that lower reimbursement for our products or reduce medical procedure volumes could adversely affect our business and results of operations.

The FDA has recently increased significantly the scrutiny applied to 510(k) submissions, and it may also focus more scrutiny on other regulation within its purview. Both the FDA and the United States Congress are influenced by high profile events, injuries and cases that generate publicity and public attention, and new legislation is often generated as a result of those events. There can be no assurance that new products we introduce will not be delayed by the current level of scrutiny applied to applications at the FDA or that new laws and regulations will not be adopted that impact the cost of production and marketing of our existing products.

If we are not able to attract, retain and motivate our sales force and expand our distribution channels, our sales and revenues will suffer.

In the U.S., we have a sales organization consisting primarily of direct sales representatives, and a marketing organization to market our products directly and support our distributor organizations. We expect to expand our sales and marketing organization, as needed, to support our growth. We have and will continue to incur significant additional expenses to support this organization. We cannot be certain that our sales organization will be able to generate sales of Urgent PC at levels that justify its expense, or even if it can, that we will be able to recruit, train, motivate or retain qualified sales and marketing personnel or independent sales representatives. Outside of the United States, United Kingdom and The Netherlands, we sell our products through a network of independent distributors. Our ability to increase product sales in foreign markets will largely depend on our ability to develop and maintain relationships with our distributors and on their ability to successfully market and sell our products. We may not be able to retain distributors who are willing to commit the necessary resources to market and sell our products to the level of our expectations. Failure to maintain or expand our distribution channels or to recruit, retain and motivate qualified personnel could have a material adverse effect on our product sales and revenues.

The size and resources of our competitors may render it difficult for us to successfully compete in the marketplace.

Our products compete against similar medical devices and other treatment methods, including drugs, for treating voiding dysfunctions. Many of our competitors, which include some of the largest medical products and pharmaceutical companies in the world, have significantly greater financial, research and development, manufacturing and marketing resources than we have. Our competitors could use these resources to develop or acquire products that are safer, more effective, less invasive, less expensive or more readily accepted than our products. Their products could make our technology and products obsolete or noncompetitive. Our competitors could also devote greater resources to the marketing and sale of their products and adopt more aggressive pricing policies than we can.

We are primarily dependent on sales of two product lines and our business would suffer if sales of either of these product lines decline.

Currently, we are dependent on sales of our Urgent PC System and Macroplastique products. In fiscal 2013, sales of our Urgent PC System and Macroplastique accounted for approximately 57% and 38%, respectively, of our total revenue. If demand for any or both of the product lines declines, our revenues and business prospects may suffer.

We may require additional financing and may find it difficult to obtain the financing on favorable terms, or at all.

Our future liquidity and capital requirements will depend on numerous factors, including: the timing and cost required to expand our sales, marketing and distribution capabilities in the United States markets; the cost and effectiveness of our marketing and sales efforts of our products in international markets; the effect of competing technologies and market, reimbursement and regulatory developments; and the cost involved in protecting our proprietary rights. Although we currently have an adequate cash balance, we may need to raise additional financing to support our operations and planned growth activities in the future because we have yet to achieve profitability and generate positive cash flows. Any equity financing could substantially dilute your equity interests in our company and any debt financing could impose significant financial and operational restrictions on us. We cannot assure you that we will obtain additional financing on acceptable terms, or at all.

We could be subject to fines and penalties, or required to temporarily or permanently cease offering products, if we fail to comply with the extensive regulations applicable to the sale and manufacture of medical products.

The production and marketing of our products and our ongoing research and development, preclinical testing and clinical trial activities are subject to extensive regulation and review by numerous governmental authorities both in the United States and abroad. U.S. and foreign regulations applicable to medical devices are wide-ranging and govern, among other things, the testing, marketing and pre-market review of new medical devices, and the manufacturing practices, reporting, advertising, exporting, labeling and record keeping procedures. We are required to obtain regulatory approval or clearance before we can market our products in the United States and certain foreign countries. The regulatory process requires significant time, effort and expenditures to bring our products to market, and we cannot assure you that the regulatory authority we currently possess to market our products will remain available, or that we will be able to obtain authority to sell new or existing products in new markets. Further, the manufacture and manufacturing facilities of medical products are subject to periodic reviews and inspection by the FDA and foreign regulatory authorities. Our failure to comply with regulatory requirements could result in governmental agencies:

Even if we receive regulatory approval or clearance of a product, the approval or clearance could limit the uses for which we may label and promote the product, which may limit the market for our products.

We often rely on our distributors in countries outside the United States in seeking regulatory approval to market our products in particular countries. To the extent we do so, we are dependent on persons outside of our direct control to make regulatory submissions and secure approvals, and we do or will not have direct access to health care agencies in those markets to ensure timely regulatory approvals or prompt resolution of regulatory or compliance matters. If our distributors fail to obtain the required approvals or do not do so in a timely manner, our sales from our international operations and our results of operations may be adversely affected.

We may not have the resources to successfully market our products, which would adversely affect our business and results of operations.

The marketing of our products requires a significant amount of time and expense in order to identify the physicians who would use our products and to train a sales force that is large enough to interact with the targeted physicians. The ease and predictability of third-party reimbursement significantly impacts the success of our marketing activities. We may not have adequate resources to market our products successfully against larger competitors who have more resources than we do. If we cannot market our products successfully, our business and results of operations would be adversely affected.

If third parties claim that we infringe upon their intellectual property rights, we may incur liabilities and costs and may have to redesign or discontinue selling the affected product.

The medical device industry is litigious with respect to patents and other intellectual property rights. Companies operating in our industry routinely seek patent protection for their product designs, and many of our principal competitors have large patent portfolios. Companies in the medical device industry have used intellectual property litigation to gain a competitive advantage. Whether a product infringes a patent involves complex legal and factual issues, the determination of which is often uncertain. We face the risk of claims that we have infringed on third parties’ intellectual property rights. Our efforts to identify and avoid infringing on third parties’ intellectual property rights may not always be successful. Any claims of patent or other intellectual property infringement, even those without merit, could:

| · | cause us to cease making or selling products that incorporate the challenged intellectual property; |

| · | result in our customers or potential customers deferring or limiting their purchases or use of the affected products until resolution of the litigation. |

In addition, new patents obtained by our competitors could threaten our product’s continued life in the market even after it has already been introduced.

If we are unable to adequately protect our intellectual property rights, we may not be able to compete effectively.

Our success depends in part on our ability to protect the proprietary rights to the technologies used in our products. We rely on patent protection, as well as a combination of trademark laws and confidentiality, noncompetition and other contractual arrangements to protect our proprietary technology. However, these legal means afford only limited protection and may not adequately protect our rights or permit us to gain or keep a competitive advantage. Our patents and patent applications, if issued, may not be broad enough to prevent competitors from introducing similar products into the market. Our patents, if challenged or if we attempt to enforce them, may not necessarily be upheld by the courts. In addition, patent protection in foreign countries may be different from patent protection under U.S. laws and may not be favorable to us.

We also rely on unpatented proprietary technology. We cannot assure you that we can meaningfully protect all of our rights in our unpatented proprietary technology or that others will not independently develop substantially equivalent products or processes or otherwise gain access to our unpatented proprietary technology. We attempt to protect our trade secrets and other unpatented proprietary technology through the use of confidentiality and noncompetition agreements with our current key employees and with other parties to whom we have divulged trade secrets. However, these agreements may not be enforceable or may not provide meaningful protection for our proprietary information in the event of unauthorized use or disclosure or other breaches of the agreements or in the event competitors discover or independently develop similar proprietary information.

Efforts on our part to enforce any of our proprietary rights could be time-consuming and expensive, which could adversely affect our business and prospects and divert our management’s attention.

The manufacture and sale of medical devices exposes us to significant risk of product liability claims, some of which may have a negative impact on our business. Any defects or risks that we have not yet identified with our products may give rise to product liability claims. Our existing $10 million of worldwide product liability insurance coverage may be inadequate to protect us from liabilities we may incur or we may not be able to maintain adequate product liability insurance at acceptable rates. If a product liability claim or series of claims is brought against us for uninsured liabilities or in excess of our insurance coverage and it is ultimately determined that we are liable, our business could suffer. Additionally, we could experience a material design or manufacturing failure in our products, a quality system failure, other safety issues or heightened regulatory scrutiny that would warrant a recall of some of our products. A recall of any of our products likely would be costly, would be uninsured and could also result in increased product liability claims. Further, while we train our physician customers in the proper use of our products, we cannot be certain that they will implement our instructions accurately. If our products are used incorrectly by our customers, injury may result and this could give rise to product liability claims against us.

The loss or interruption of materials from any of our key suppliers could delay the manufacture of our products, which would limit our ability to generate sales and revenues.

We currently purchase several key materials used in our products from single source suppliers, including the finished products for our Urgent PC System. If one of these suppliers delayed or curtailed shipments to us, our ability to manufacture and deliver product would be impaired, our sales would decline or be curtailed for that product, and we would be forced to quickly locate an alternative source of supply. We cannot be sure that acceptable alternative arrangements could be made on a timely basis. Further, our reliance on such suppliers and the cost and difficulty we would encounter in qualifying an alternative subjects us to increased risk of price increase by single source suppliers. Additionally, the qualification of materials and processes as a result of a supplier change could be deemed as unacceptable to regulatory authorities and cause delays and increased costs due to additional test requirements. A significant interruption in the supply of materials, for any reason, could delay the manufacture and sale of our products, which would limit our ability to generate revenues.

If we are not able to maintain sufficient quality controls, regulatory approvals of our products by the European Union, Canada, the FDA or other relevant authorities could be delayed or denied and our sales and revenues will suffer.

The FDA, European Union, Canada or other related authorities could stop or delay approval of production of products if our manufacturing facilities do not comply with applicable manufacturing requirements. The FDA’s Quality System Regulations impose extensive testing, control, documentation and other quality assurance requirements. Canada and the European Union also impose requirements on quality systems of manufacturers, who are inspected and certified on a periodic basis and may be subject to additional unannounced inspections. Further, our suppliers are also subject to these regulatory requirements. Failure by any of our suppliers or us to comply with these requirements could prevent us from obtaining or retaining approval for and marketing of our products.

If we are not able to acquire or license other products, our business and future growth prospects could suffer.

As part of our growth strategy, we intend to acquire or license additional products and technologies for development and commercialization. The success of this strategy depends upon our ability to identify, select and acquire the right products and technologies.

Products and technologies that we license or acquire may require additional development prior to sale, including clinical testing and approval by the FDA and other regulatory bodies, and we may encounter difficulty or delays in completing the development or receiving the necessary approvals. We may find that the product or technology cannot be manufactured economically or commercialized successfully. We may not be able to acquire or license the right to products on terms that we find acceptable, or at all.

Even if we complete future acquisitions, our business, financial condition and the results of operations could be negatively affected because:

| · | we may be unable to integrate the acquired business or products successfully and realize anticipated economic, operational and other benefits in a timely manner; and |

| · | the acquisition may disrupt our ongoing business, distract our management and divert our resources. |

Our business strategy relies on assumptions about the market for our products, which, if incorrect, would adversely affect our business prospects and profitability.

We are focused on the market for minimally invasive therapies used to treat voiding dysfunctions. We believe that the aging of the general population will continue and that these trends will increase the need for our products. However, the projected demand for our products could materially differ from actual demand if our assumptions regarding these trends and acceptance of our products by the medical community prove to be incorrect or do not materialize. Actual demand for our products could also be affected if drug therapies gain more widespread acceptance as a viable alternative treatment, which in each case would adversely affect our business prospects and profitability.

Negative publicity regarding the use of silicone material in medical devices could harm our business and result in a material decrease in revenues.

Macroplastique is comprised of medical grade, heat-vulcanized polydimethylsiloxane, which results in a solid, flexible, highly-textured silicone elastomer. In the early 1990’s, the United States silicone gel breast implant industry became the subject of significant controversies surrounding the possible effects upon the human body of the use of semi-liquid silicone gel in breast implants, resulting in product liability litigation and leading to the bankruptcy of several companies. We use only medical grade solid silicone material in our tissue bulking products and do not use semi-liquid silicone gel, as was used in breast implants. Negative publicity regarding the use of silicone materials in our products or in other medical devices could have a significant adverse effect on the overall acceptance of our products.

We derive a significant portion of our sales from outside of the United States and are subject to the risks of international operations.

We derived approximately 27% of our net sales in fiscal 2013 from customers and operations in international markets. The sale and shipping of our products and services across international borders, as well as the purchase of components and products from international sources, subject us to a number of risks, including:

| · | difficulties in recruiting and maintaining distributors and staff in remote locations, including sales people; |

| · | the imposition of restrictions on the activities of foreign agents, representatives and distributors; |

| · | difficulties in enforcing agreements and collecting receivables through certain foreign legal systems; and |

Our stock is thinly traded and you may find it difficult to sell your investment in our stock at quoted prices.

There is only a limited trading market for our common stock, which is quoted on the NASDAQ. Transactions in our common stock may lack the volume and liquidity necessary to maintain an orderly trading market and this could result in both depressed and highly variable trading prices.

The market price of our common stock may be subject to significant fluctuations due to the following factors, among others:

The stock market in recent years has experienced extreme price and volume fluctuations that have often been unrelated or disproportionate to the operating performance of affected companies. These broad market fluctuations may cause the price of our common stock to fall abruptly or remain significantly depressed.

The market price of our common stock could decline due to sales by our existing shareholders of a large number of shares of our common stock or the perception that these sales could occur. These sales could also make it more difficult for us to raise capital through the sale of common stock at a time and price we deem appropriate.

Our corporate documents and Minnesota law contain provisions that could discourage, delay or prevent a change in control of our company.

Provisions in our articles of incorporation may discourage, delay or prevent a merger or acquisition, even if our stockholders consider the terms favorable. Our articles of incorporation provide for a staggered board of directors, requiring our directors to serve for three-year terms, with approximately one third of the directors standing for reelection each year. A staggered board could make it more difficult for a third party to obtain control of our board of directors through a proxy contest, which may be a necessary step in an acquisition of us that is not favored by our board of directors.

We are also subject to the anti-takeover provisions of Section 302A.673 of the Minnesota Business Corporation Act. Under these provisions, if anyone becomes an “interested shareholder” in a transaction not approved by a committee consisting of disinterested members of our board of directors, we may not enter into a “business combination” with that person for four years, which could discourage a third party from making a takeover offer and could delay or prevent a change of control. For purposes of Section 302A.673, “interested shareholder” generally means someone owning 10% or more of our outstanding voting stock or an affiliate of ours that owned 10% or more of our outstanding voting stock during the past four years, subject to certain exceptions.