UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

———————

FORM 10-Q/A

(Amendment No. 1)

———————

| o | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended April 30, 2013

Or

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from: _____________ to _____________

Commission File Number: 0-20317

———————

COUPON EXPRESS, INC.

(Exact name of registrant as specified in its charter)

———————

| Nevada | 33-0912085 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

303 Fifth Avenue, Suite 210, New York, NY 10016

(Address of Principal Executive Office) (Zip Code)

(914) 371-2441

(Registrant’s telephone number, including area code)

(Former name, former address and former fiscal year, if changed since last report)

———————

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

ý Yes o No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company.

| Large accelerated filer | o | Accelerated filer | o | |

| Non-accelerated filer | o | (Do not check if a smaller reporting company) |

Smaller reporting company

|

ý |

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No ý

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

o Yes ý No

APPLICABLE ONLY TO CORPORATE ISSUERS:

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

As of July 10, 2013, there were 280,535,802 shares of the Registrant's Common Stock, and 120 shares of the Registrant's Series A Preferred Stock, $0.001 par value per share, outstanding.

EXPLANATORY NOTE

Coupon Express, Inc., a Nevada corporation (the “Company”), is filing this Amendment No. 1 on Form 10-Q/A (the “Amendment”) to its Quarterly Report on Form 10-Q for the period ended April 30, 2013 (the “Form 10-Q”), filed with the Securities and Exchange Commission on June 19, 2013 (the “Original Filing Date”), to amend certain disclosures made with respect to the issuance of certain shares of Common Stock in 2013 which are contained in Note 8 to the financial statements, under “Management’s Discussion and Analysis of Financial Condition and Results of Operations -- Liquidity and Capital Resources – Cash Flows” and in Part II, Item 2 -- “Unregistered Sales of Equity Securities and Use of Proceeds”, to include XBRL (Extensible Business Reporting Language) information in Exhibit 101 that was excluded from our timely filed Quarterly Report on Form 10-Q for the period ended April 30, 2013 and to remove one exhibit that was erroneously included in the Form 10-Q.

This Amendment speaks as of the Original Filing Date, does not reflect events that may have occurred subsequent to the Original Filing Date, and does not modify or update in any way, except as stated above, disclosures made in the Form 10-Q. No other changes have been made to the Form 10-Q.

Pursuant to Rule 12b-15 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”), the certifications required pursuant to the rules promulgated under the Exchange Act, as adopted pursuant to Section 302 of the Sarbanes-Oxley Act of 2002, which were included as exhibits to the Form 10-Q, have been amended, restated and re-executed as of the date of this Amendment No. 1 and are included as Exhibits 31.1 and 32.1 hereto.

COUPON EXPRESS, INC.

For The Quarterly Period Ended April 30, 2013

TABLE OF CONTENTS

| Page | ||

| Number | ||

| Part I. | FINANCIAL INFORMATION | |

| Item 1. | Financial Statements – | |

| Balance Sheets as of April 30, 2013 (unaudited) and October 31, 2012 | 2 | |

|

Statements of Income for the three and six months ended April 30, 2013 and 2012 (unaudited) |

3 | |

| Statements of Stockholders’ Equity as of April 30, 2013 (unaudited) and October 31, 2012 | 4 | |

| Statements of Cash Flows for the three and six months ended April 30, 2013and 2012 (unaudited) | 5 | |

| Notes to the Financial Statements | 6-14 | |

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 15-17 |

| Item 3. | Quantitative and Qualitative Disclosures about Market Risk | 18 |

| Item 4 | Controls and Procedures | 18 |

| PART II. | OTHER INFORMATION | |

| Item 1. | Legal Proceedings | 19 |

| Item 1A | Risk Factors | 19 |

| Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds | 19-20 |

| Item 3. | Defaults Upon Senior Securities | 20 |

| Item 4. | (Removed and Reserved) |

20 |

| Item 5. | Other Information | 20 |

| Item 6. | Exhibits |

21-23 |

| |

||

| SIGNATURES | ||

PART 1 — FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

COUPON EXPRESS, INC.

BALANCE SHEETS

| April 30, | October 31, | |||||||||||||||

| 2013 | 2012 | |||||||||||||||

| ASSETS | ||||||||||||||||

| Current assets | ||||||||||||||||

| Cash | $ | 2,282 | $ | 32,393 | ||||||||||||

| Accounts receivable (net of allowance for doubtful accounts) | 42,311 | 11,121 | ||||||||||||||

| Total current assets | 44,593 | 43,514 | ||||||||||||||

| Furniture and equipment, net | 322,174 | 320,036 | ||||||||||||||

| Other Assets | ||||||||||||||||

| Deferred leasing costs | 19,950 | — | ||||||||||||||

| Deposit - Kiosks | 60,000 | 60,000 | ||||||||||||||

| Security deposits | 7,400 | 7,650 | ||||||||||||||

| Total other assets | 87,350 | 67,650 | ||||||||||||||

| Total assets | $ | 454,117 | $ | 431,200 | ||||||||||||

| LIABILITIES AND STOCKHOLDERS' DEFICIENCY | ||||||||||||||||

| Current liabilities | ||||||||||||||||

| Accounts payable and accrued expenses - net of long-term | $ | 467,099 | $ | 328,854 | ||||||||||||

| Accrued Interest payable (PIK) | 105,108 | 102,547 | ||||||||||||||

| Preferred dividends payable | 146,537 | 49,382 | ||||||||||||||

| Deposit on purchase of common stock | 157,990 | — | ||||||||||||||

| Capital lease payable - net of long-term | 6,808 | — | ||||||||||||||

| Notes payable | 56,383 | 56,383 | ||||||||||||||

| Total current liabilities | 939,925 | 537,166 | ||||||||||||||

| Accounts payable - net of current | 144,670 | 159,670 | ||||||||||||||

| Capital lease payable - net of current | 26,192 | — | ||||||||||||||

| Total liabilities | 1,110,787 | 696,836 | ||||||||||||||

| Stockholders' deficiency | ||||||||||||||||

| Preferred stock $.001 par value; 5,000,000 shares authorized, 120 and 110 | — | — | ||||||||||||||

| issued and outstanding at April 30, 2013 and October 31, 2012, respectively | ||||||||||||||||

| Common stock, $.001 par value; 800,000,000 shares | ||||||||||||||||

| authorized, 278,035,802 and 272,203,802 shares issued and | ||||||||||||||||

| outstanding at April 30, 2013 and October 31, 2012, respectively | 278,035 | 272,203 | ||||||||||||||

| Additional paid-in capital | 23,810,382 | 23,418,435 | ||||||||||||||

| Deficit | (24,744,100 | ) | (23,955,287 | ) | ||||||||||||

| Less: common stock in Treasury | (987 | ) | (987 | ) | ||||||||||||

| Total stockholders' deficiency | (656,670 | ) | (265,636 | ) | ||||||||||||

| Total liabilities and stockholders' deficiency | $ | 454,117 | $ | 431,200 | ||||||||||||

The accompany notes are an integral part of these financial statements.

2

COUPON EXPRESS, INC.

STATEMENTS OF OPERATIONS AND COMPREHENSIVE LOSS

| For the Three months Ended | For the Six months Ended | |||||||||||||||

| April 30, | April 30, | |||||||||||||||

| 2013 | 2012 | 2013 | 2012 | |||||||||||||

| Revenue | $ | 40,768 | $ | 782 | $ | 76,723 | $ | 6,422 | ||||||||

| Selling | 91,716 | 125,617 | 196,406 | 264,677 | ||||||||||||

| Administrative expenses | 288,233 | 317,502 | 569,416 | 485,882 | ||||||||||||

| Total expenses | 379,949 | 443,119 | 765,822 | 750,559 | ||||||||||||

| Loss from operations | (339,181 | ) | (442,337 | ) | (689,099 | ) | (744,137 | ) | ||||||||

| Interest, net | 1,259 | 171,888 | 2,561 | 371,239 | ||||||||||||

| Net loss | (340,440 | ) | (614,225 | ) | (691,660 | ) | (1,115,376 | ) | ||||||||

| Preferred dividends declared | 47,772 | — | 97,154 | — | ||||||||||||

| Net loss applicable to common stock | $ | (388,212 | ) | $ | (614,225 | ) | $ | (788,814 | ) | $ | (1,115,376 | ) | ||||

| Basic and diluted weighted average shares | 275,668,484 | 261,097,234 | 275,979,090 | 261,123,753 | ||||||||||||

| Basic and diluted loss per share | $ | (0.001 | ) | $ | (0.002 | ) | $ | (0.003 | ) | $ | (0.004 | ) | ||||

The accompany notes are an integral part of these financial statements.

3

| COUPON EXPRESS, INC. | ||||||||||||||||||||||||||||||||||

| STATEMENTS OF STOCKHOLDERS’ EQUITY | ||||||||||||||||||||||||||||||||||

| Additional | Total | |||||||||||||||||||||||||||||||||

| Common Stock | Preferred Stock | Paid-in | Accumulated | Treasury | Stockholders' | |||||||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | Capital | Deficit | Stock | Deficit | |||||||||||||||||||||||||||

| Balance, October 31, 2011 | 260,953,819 | $ | 260,953 | 0 | — | 18,647,958 | (19,816,712 | ) | (987 | ) | (908,788 | ) | ||||||||||||||||||||||

| Conversion of notes payable | 7,177,777 | 7,178 | 110 | $ | — | 3,399,322 | 3,406,500 | |||||||||||||||||||||||||||

| Issuance of shares for consulting and equipment rental services | 2,993,775 | 2,994 | 79,478 | 82,472 | ||||||||||||||||||||||||||||||

| Issuance of shares for interest | 1,078,431 | 1,078 | 92,365 | 93,443 | ||||||||||||||||||||||||||||||

| Issuance of warrants and options for officer | 1,478,825 | 1,478,825 | ||||||||||||||||||||||||||||||||

| Issuance of warrants in connections with financing - net | (279,513 | ) | (279,513 | ) | ||||||||||||||||||||||||||||||

| Retained earnings adjustment | (299,802 | ) | (299,802 | ) | ||||||||||||||||||||||||||||||

| Net loss | (3,838,773 | ) | (3,838,773 | ) | ||||||||||||||||||||||||||||||

| Balance, October 31, 2012 | 272,203,802 | $ | 272,203 | 110 | $ | — | $ | 23,418,435 | $ | (23,955,287 | ) | $ | (987 | ) | $ | (265,636 | ) | |||||||||||||||||

| Issuance of preferred stock | 10 | — | 239,500 | 239,500 | ||||||||||||||||||||||||||||||

| Issuance of common stock | 2,500,000 | 2,500 | 47,500 | 50,000 | ||||||||||||||||||||||||||||||

| Issuance of shares for directors fees | 3,332,000 | 3,332 | 63,308 | 66,640 | ||||||||||||||||||||||||||||||

| Issuance of options for officer | 41,639 | 41,639 | ||||||||||||||||||||||||||||||||

| Net loss | (788,813 | ) | (788,813 | ) | ||||||||||||||||||||||||||||||

| Balance, April 30, 2013 | 278,035,802 | $ | 278,035 | 120 | $ | — | $ | 23,810,382 | $ | (24,744,100 | ) | $ | (987 | ) | $ | (656,670 | ) | |||||||||||||||||

The accompany notes are an integral part of these financial statements.

4

COUPON EXPRESS, INC.

STATEMENTS OF CASH FLOWS

| For the Six months Ended | ||||||||

| April 30, | ||||||||

| 2013 | 2012 | |||||||

| Cash flows from operations | ||||||||

| Net income (loss) | $ | (691,660 | ) | $ | (1,115,376 | ) | ||

| Adjustment to reconcile net loss to net cash: | ||||||||

| Depreciation and amortization | 42,912 | 37,414 | ||||||

| Net shares issued(cancelled) for interest | — | (24,129 | ) | |||||

| Shares issued for consulting, director fees and equipment rental services | 66,640 | 82,472 | ||||||

| Non- cash interest cost | 2,561 | 171,888 | ||||||

| Non- cash compensation | 41,639 | — | ||||||

| Changes in operating assets and liabilities: | ||||||||

| Accounts receivable | (31,190 | ) | (269 | ) | ||||

| Other current assets | — | (12,000 | ) | |||||

| Other assets | 250 | (3,350 | ) | |||||

| Accrued interest | — | 86,010 | ||||||

| Accounts payable and accrued expenses | 123,247 | (48,716 | ) | |||||

| Net cash provided by (used for) operating activities | (445,601 | ) | (826,056 | ) | ||||

| Cash flows from investing activities | ||||||||

| Deposit on capital lease | (11,000 | ) | — | |||||

| Purchase of property and equipment | — | (30,233 | ) | |||||

| Net cash provided by (used for) investing activities | (11,000 | ) | (30,233 | ) | ||||

| Cash flows from financing activities | ||||||||

| Proceeds from issuance of preferred stock | 239,500 | — | ||||||

| Proceeds from issuance of common stock | 50,000 | — | ||||||

| Deposit on purchases of common stock | 157,990 | — | ||||||

| Deferred leasing costs in connection with capital lease transaction | (21,000 | ) | ||||||

| Repayment of debt | — | (127,640 | ) | |||||

| Net cash provided by ( used for) financing activities | 426,490 | (127,640 | ) | |||||

| Net increase (decrease) in cash | (30,111 | ) | (983,929 | ) | ||||

| Cash, beginning of period | 32,393 | 1,010,203 | ||||||

| Cash, end of period | $ | 2,282 | $ | 26,274 | ||||

| Supplemental disclosure of cash flow information | ||||||||

| and noncash investing and financing activities: | ||||||||

| Non- cash financing activities: | ||||||||

| Issuance of capital lease payable in connection with purchase of fixed assets | $ | 33,000 | $ | — | ||||

| Preferred dividends declared | $ | 49,383 | $ | — | ||||

| Cash paid during the year for: | ||||||||

| Interest | $ | — | $ | 15,110 | ||||

| Taxes | $ | — | $ | — | ||||

The accompany notes are an integral part of these financial statements.

5

COUPON EXPRESS, INC.

NOTES TO FINANCIAL STATEMENTS

April 30, 2013

1. Organization and Going Concern

Organization

Coupon Express, Inc. (“CE” or the “Company”) was organized under the laws of Nevada in June, 1991. CE provides innovative interactive customer communications systems and applications that support targeted marketing programs with unique point-of-purchase (POP) services and information that serve shoppers and distributors while building loyalty and revenue for the Company’s primary clients. Through our proprietary kiosks, we provide in-store customized couponing, in multiple languages, for immediate impact in regional, independent retailers in the grocery and convenience store industries, enabling retailers to quickly determine ideal price-points for new products and mitigate losses from hard-to-sell items.

Going Concern

Our financial statements have been prepared on the assumption that we will continue as a going concern, which contemplates the continuation of operations, the realization of assets and the liquidation of liabilities in the ordinary course of business, and do not reflect any adjustments that might result from our ability to being unable to continue as a going concern. At April 30, 2013, we had total assets of $454,117 and liabilities of $1,110, 787. Our management is aware that we need to raise additional capital not only to meet our financial obligations, but also to expand our business. These factors cumulatively indicate that there is substantial doubt about our ability to continue as a going concern. The accompanying financial statements do not include any adjustments that might be necessary should we be unable to continue as a going concern.

2. Summary of Significant Accounting Policies

Accounting Principles

The financial statements and accompanying notes are prepared in accordance with accounting principles generally accepted in the United States.

Cash and Cash Equivalents

We consider all highly liquid interest-earning investments with a maturity of three months or less at the date of purchase to be cash equivalents.

Financial Statement Presentation

We have reclassified certain prior-year amounts to conform to the current year presentation.

Loss per Common Share

The Company complies with the accounting and disclosure requirements of FASB ASC 260, “Earnings Per Share.” Basic loss per common share is computed by dividing net loss available to common stockholders by the weighted average number of common shares outstanding during the period. The calculation of diluted net loss per share excludes 245,196,487 and 141,460,964 warrants and options outstanding as of April 30, 2013 and 2012 respectively, since their effect is anti-dilutive.

6

COUPON EXPRESS, INC.

NOTES TO FINANCIAL STATEMENTS

April 30, 2013

Summary of Significant Accounting Policies (continued)

Income Taxes

In accordance with GAAP, the Company is required to determine whether a tax position of the Company is more likely than not to be sustained upon examination by the applicable taxing authority, including resolution of any related appeals or litigation processes, based on the technical merits of the position. The Company files an income tax return in the U.S. federal jurisdiction, and may file income tax returns in various U.S. state and local jurisdictions. The tax benefit to be recognized is measured as the largest amount of benefit that is greater than fifty percent likely of being realized upon ultimate settlement. De-recognition of a tax benefit previously recognized could result in the Company recording a tax liability that would reduce net assets. This policy also provides guidance on thresholds, measurement, de-recognition, classification, interest and penalties, accounting in interim periods, disclosure, and transition that is intended to provide better financial statement comparability among different entities. It must be applied to all existing tax positions upon initial adoption and the cumulative effect, if any, is to be reported as an adjustment to stockholder's equity as of November 1, 2012.

Based on its analysis, the Company has determined that the adoption of this policy did not have a material impact on the Company's financial statements upon adoption. However, management's conclusions regarding this policy may be subject to review and adjustment at a later date based on factors including, but not limited to, on-going analyses of and changes to tax laws, regulations and interpretations thereof.

Interest and Penalty Recognition on Unrecognized Tax Benefits

We recognize interest accrued related to unrecognized tax benefits in interest expense and penalties in operating expenses. No interest expense or penalties have been recognized for the three months ended April 30, 2013.

Stock-Based Compensation

The Company complies with FASB ASC Topic 718 "Compensation - Stock Compensation," which establishes standards for the accounting for transactions in which an entity exchanges its equity instruments for goods or services. It also addresses transactions in which an entity incurs liabilities in exchange for goods or services that are based on the fair value of the entity's equity instruments or that may be settled by the issuance of those equity instruments. FASB ASC Topic 718 focuses primarily on accounting for transactions in which an entity obtains employee services in share-based payment transactions. FASB ASC Topic 718 requires an entity to measure the cost of employee services received in exchange for an award of equity instruments based on the grant-date fair value of the award (with limited exceptions). That cost will be recognized over the period during which an employee is required to provide service in exchange for the award the requisite service period (usually the vesting period). No compensation costs are recognized for equity instruments for which employees do not render the requisite service. The grant-date fair value of employee share options and similar instruments will be estimated using option-pricing models adjusted for the unique characteristics of those instruments (unless observable market prices for the same or similar instruments are available). If an equity award is modified after the grant date, incremental compensation cost will be recognized in an amount equal to the excess of the fair value of the modified award over the fair value of the original award immediately before the modification.

7

COUPON EXPRESS, INC.

NOTES TO FINANCIAL STATEMENTS

April 30, 2013

Summary of Significant Accounting Policies (continued)

Valuation of Investments in Securities at Fair Value-Definition and Hierarchy

FASB ASC Topic 820 "Fair Value Measurements and Disclosures" provides a framework for measuring fair value under generally accepted accounting principles in the United States and requires expanded disclosures regarding fair value measurements. ASC 820 defines fair value as the exchange price that would be received for an asset or paid to transfer a liability (i.e., the "exit price") in an orderly transaction between market participants at the measurement date.

In determining fair value, the Company uses various valuation approaches. In accordance with GAAP, a fair value hierarchy for inputs is used in measuring fair value that maximizes the use of observable inputs and minimizes the use of unobservable inputs by requiring that the most observable inputs be used when available. Observable inputs are those that market participants would use in pricing the asset or liability based on market data obtained from sources independent of the Company. Unobservable inputs reflect the Company's assumptions about the inputs market participants would use in pricing the asset or liability developed based on the best information available in the circumstances. FASB ASC Topic 820 establishes a three-tiered fair value hierarchy that prioritizes inputs to valuation techniques used in fair value calculations, as follows:

Level 1 - Valuations based on unadjusted quoted prices in active markets for identical assets or liabilities that the Company has the ability to access. Valuation adjustments and block discounts are not applied to Level 1 securities. Since valuations are based on quoted prices that are readily and regularly available in an active market, valuation of these securities does not entail a significant degree of judgment.

Level 2 - Valuations based on quoted prices in markets that are not active or for which all significant inputs are observable, either directly or indirectly.

Level 3 - Valuations based on inputs that are unobservable and significant to the overall fair value measurement.

The availability of valuation techniques and observable inputs can vary from security to security and is affected by a wide variety of factors including, the type of security, whether the security is new and not yet established in the marketplace, and other characteristics particular to the transaction. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment.

Those estimated values do not necessarily represent the amounts that may be ultimately realized due to the occurrence of future circumstances that cannot be reasonably determined.

Because of the inherent uncertainty of valuation, those estimated values may be materially higher or lower than the values that would have been used had a ready market for the securities existed. Accordingly, the degree of judgment exercised by the Company in determining fair value is greatest for securities categorized in Level 3. In certain cases, the inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement in its entirety falls is determined based on the lowest level input that is significant to the fair value measurement.

Fair value is a market-based measure considered from the perspective of a market participant rather than an entity-specific measure. Therefore, even when market assumptions are not readily available, the Company's own assumptions are set to reflect those that market participants would use in pricing the asset or liability at the measurement date. The Company uses prices and inputs that are current as of the measurement date, including periods of market dislocation. In periods of market dislocation, the observability of prices and inputs may be reduced for many securities. This condition could cause a security to be reclassified to a lower level within the fair value hierarchy.

8

COUPON EXPRESS, INC.

NOTES TO FINANCIAL STATEMENTS

April 30, 2013

Summary of Significant Accounting Policies (continued)

Valuation Techniques

We value investments in securities that are freely tradable and are listed on a national securities exchange or reported on the NASDAQ national market at their last sales price as of the last business day of the year.

Property and Equipment

Property and equipment are stated at cost and depreciated using the straight-line method over the estimated life of the asset of 5 years.

Long-Lived Assets

In accordance with FASB ASC Topic 360 "Property, Plant, and Equipment," the Company records impairment losses on long-lived assets used in operations when indicators of impairment are present and the undiscounted cash flows estimated to be generated by those assets are less than the assets' carrying amounts.

Fair Value of Financial Instruments

The fair values of the Company's assets and liabilities that qualify as financial instruments under FASB ASC Topic 825, "Financial Instruments," approximate their carrying amounts presented in the accompanying balance sheets at April 30, 2013 and October 31, 2012.

Revenue Recognition.

Online advertising revenue derived from the kiosks and signage will be recognized as revenue as they are displayed. The Company’s current revenue models include a fixed fee plus click charge and a fixed price per store model.

Use of estimates

The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect certain reported amounts of assets and liabilities at the date of the financial statements, as well as their related disclosures. Such estimates and assumptions also affect the reported amounts of revenues and expenses during the reporting period. Actual results could significantly differ from those estimates.

Recently Adopted Accounting Pronouncements

There are no recent pronouncements that have a material effect on the Company.

9

COUPON EXPRESS, INC.

NOTES TO FINANCIAL STATEMENTS

April 30, 2013

3. Fixed Assets

Furniture and equipment consist of the following:

| April 30, | October 31, | ||||

| Description | 2013 | 2012 | |||

| Kiosks | $721,562 | $677,562 | |||

| Less: accumulated depreciation | 399,388 | 357,526 | |||

| $322,174 | $320,036 | ||||

Depreciation expense for the six months ended April 30, 2013 and year ended October 31, 2012 was $41,862 and $234,708 respectively.

4. Stockholders' Equity

Warrants

| Warrant transactions are as follows: | Weighted | |||||||||

| Number of | Average | |||||||||

| Warrants | Exercise Price | |||||||||

| Outstanding, October 31, 2011 | 142,107,075 | $0.13 | ||||||||

| Granted | 102,360,795 | 0.04 | ||||||||

| Exercised | — | - | ||||||||

| Expired | 11,198,179 | 0.10 | ||||||||

| Outstanding October 31, 2012 | 233,269,691 | $0.06 | ||||||||

| Granted | 17,149,500 | 0.03 | ||||||||

| Exercised | — | |||||||||

| Expired | 5,222,704 | 0.04 | ||||||||

| Outstanding April 30, 2013 | 245,196,487 | $0.04 | ||||||||

5. Debt

Bridge Loans

In February and March 2007, we entered into notes (“Bridge Notes”) with several unrelated parties totaling approximately $325,000. The Bridge Notes were originally due on November 11, 2009 and incurred an interest rate of 12% per annum.

In August 2007, we entered into exchange agreements with the holders of $300,000 of the Bridge Notes, wherein the notes were to be converted into 3,000,000 shares of our common stock. We originally expected these notes to be converted into common stock shares during the first or second quarter of the fiscal year ending October 31, 2011. One of the note holders converted his $25,000 note into 208,333 shares of common stock in December 2008.

In May and June of 2008, we entered into a new series of Bridge Notes with several unrelated parties totaling $470,000. The Bridge Notes were originally due six months from the date of issuance and incur interest at the rate of 10% per annum. On July 2, 2010, the Bridge Note was amended to extend the due date to December 1, 2010. The notes are convertible by the holder at any time at a conversion price equal to the per share price of a new issuance. In connection with the Bridge Notes, we also issued warrants to purchase 470,000 shares of our common stock at an exercise price $.15 and warrants to purchase 470,000 shares of our common stock at an exercise price of $.25, reduced to $.05 and $.15, respectively, by the July 2, 2010 Amendment to the Bridge Notes. The warrants may be exercisable at any time for a period of 5 years.

10

COUPON EXPRESS, INC

NOTES TO FINANCIAL STATEMENTS

April 30, 2013

5. Debt (continued)

In connection with the issuance of the warrants, we reflected a value for the warrants totaling $47,112; no value adjustment was reflected for the price reduction, as the value change was not material. The fair value of the warrant grant was estimated on the date of the grant using the Black-Scholes option-pricing model with the following weighted average assumptions: expected volatility of 15%, risk free interest rate of 4.86%; and expected lives of 5 years. On December 1, 2010, we amended these notes to change the warrant exercise price to $.05. During the fiscal year ended October 31, 2010, we issued 3,047,800 common stock shares in connection with the Bridge Note amendments. During the year ended October 31, 2011, the company issued 43,097,752 shares of common stock in payment of accrued interest and principal. In November 2011, $50,000 was repaid to one of the outstanding note holders. In November 2011 and February 2012 $75,000 was repaid to the remaining outstanding note holders.

Round D Loans

Commencing May through October 2007, we entered into notes (“Round D Notes”) with several unrelated parties totaling approximately $2,916,000. The Round D Notes incurred interest at rates ranging from 12% to 14% per annum, payable semi-annually and were due 3 years from the date of issuance. These notes were not paid by October 31, 2010. In connection with the Round D Notes, we also issued warrants to purchase 9,445,744 shares of our common stock at an exercise price of $.15. The warrants may be exercisable at any time for a period of 5 years. In connection with the issuance of the warrants, we reflected a value for the warrants totaling $549,011. The fair value of the warrant grant was estimated on the date of the grant using the Black-Scholes option-pricing model with the following weighted average assumptions: expected volatility of 15%, risk free interest rate of 3.57%; and expected lives of 5 years. For the years ending October 31, 2011 and 2010 the company issued 48,372,496 and 13,606,592 shares of common stock respectively in payment of accrued interest and principal. In addition, note holders of $646,000 of the remaining $711,000 outstanding convertible notes, have agreed to extend the due dates of their notes until October 2012 and also to subordinate their notes to the new Senior Convertible Notes. In November 2011, $50,000 was repaid to one of the outstanding note holders. On August 7, 2012 the company issued 8,333,497 shares in payment of outstanding principal of $646,000 and interest of $117,572.

In March 2009, we obtained interest free advances from two of its officers totaling $40,000. In November 2011, one of these loans totaling $20,000 was repaid.

Round G Loans

In May through October 2010, we entered into a series of convertible notes aggregating $485,000. The notes were originally due one year from the date of issuance at an interest rate of 10% per annum. The interest was payable in cash or common shares at our discretion. The notes were convertible into common shares at a conversion price of $.035 per share. In connection with the notes, we issued five year warrants to purchase 13,857,143 shares of our common stock at an exercise price of $.05/share. Through October 31, 2010, we issued 2,900,157 shares of common stock in payment of accrued interest and principal. In connection with the issuance of the warrants and conversion features, we reflected a value totaling $118,067. The fair value of the warrant grant was estimated on the date of grant using the Black-Sholes option-pricing model with the following weighted average assumptions: expected volatility of 15%, risk free interest rates between 1.23% and 2.03%, and expected lives of five years. In October 2011 the company issued 23,568,072 shares in payment of accrued interest and principal due all but one note holder. In December 2011, $100,000 was repaid to the remaining outstanding note holder.

For all of the debt financing describe above, the Company had the option to either pay the interest due in cash or in shares of our common stock. During the year ended October 2012 the company offered its outstanding warrant holders (for all rounds prior to 2011) to extend the due date of their warrants in exchange for a lower price.

11

COUPON EXPRESS, INC

NOTES TO FINANCIAL STATEMENTS

April 30, 2013

5. Debt (continued)

Cumulative Convertible Senior Notes

In October 2011, May 2012, July 2012, and December 2012 we completed a private placement of $3,000,000 aggregate principal amount of cumulative convertible senior notes (“Senior Notes”) and warrants to certain investors, that included the Company’s existing Series A Preferred Stockholders. In August 2012, the Senior Notes were converted into 110.42 shares of preferred stock. In December 2012, we issued an additional 9.58 shares of preferred stock and warrants for proceeds of $239,500.

The shares of preferred stock bear a cumulative dividend of 7% per annum. Upon liquidation, and upon an acquisition of the Company, the holders of preferred stock are entitled to a liquidation preference equal to the greater of (i) the amount invested plus all accrued and unpaid dividends, or the amount the holders of Preferred Stock would receive had they converted the preferred stock to common Stock immediately prior to such event. Each share of preferred stock is convertible into 1,250,000 shares of the Company’s common stock, subject to certain adjustments. The Certificate of Designation of the preferred stock provides that without the consent of a majority of the outstanding series A preferred stock, the Company may not:

The warrants are exercisable until 2016 and 2017 at a price of $.04 per share (subject to certain adjustments) and entitle the holder to purchase 1,250,000 shares of the Company’s common stock for each $25,000 of principal amount of Senior Notes. As of October 31, 2012 the Company is authorized to issue 800,000,000 shares of common stock. The investors have entered into an Investors’ Rights Agreement which among other things, provides for board representation, registration rights, and certain provisions regarding future sales of securities by the Company.

In prior rounds of financing, described in Note 5 Debt, the Company issued certain warrants, rights convertible into or exercisable or exchangeable for common stock (collectively the “Derivative Securities”). The Derivative Securities contain certain anti-dilution provisions, which provide for adjustment of the conversion price, exercise price or number of shares issuable, upon the occurrence of certain events. The Company, obtained from most of the holders of the unexpired Derivative Securities, a waiver, except in the case of any capital reorganization, split, combination or subdivision or reclassification, of any anti-dilution adjustments, it may have with respect to the Derivative Securities.

12

COUPON EXPRESS, INC

NOTES TO FINANCIAL STATEMENTS

April 30, 2013

5. Debt (continued)

Capital lease

In March 2013, the Company entered into a Kiosk leasing facility with Premium Leasing, LLC of Vestal, New York. The term of the lease agreement is for 60 months and includes a twenty five (25%) percent down payment for each Kiosk leased and a commitment fee of $21,000. The current cost of each kiosk is $5,500. The Company will pay the 25% down payment or $1,375 and the remaining seventy-five (75%) balance shall be paid in monthly installments of $85.82 including interest at nine percent (9%) per annum. As security for each lease, the Company has agreed to issue Premium Leasing its common stock equal to the leased value of kiosks under lease. The common stock will be held in escrow as defined in the agreement. In addition, the company has also granted Premium Leasing three (3) warrants to purchase in the aggregate five million shares of the company’s common stock until March 2018. The warrant to purchase 3,000,000 shares of common stock is immediately exercisable at $.02 per share, with the two (2) remaining warrants, each to purchase 1,000,000 shares of common stock exercisable one (1) year from date of grant, at $.03 and $.04 per share, respectively. As of April 30, 2013 the Company has leased 8 kiosks under this facility.

6. Commitments

Operating Leases

Real Estate

Until November 30, 2011, we leased 2,061 square feet of office space in Colorado for $3,200 per month. In December 2011, we moved into shared office space, subletting this space for $250 per month on a month to month arrangement. In December 2011, this shared office was closed and the activities were moved and consolidated to the South Carolina office. In November 2011, we leased additional space in South Carolina for our IT and Customer Service department. The lease provides for rent of $1,000 per month plus common area charges until November 2012. In November 2012 the company renewed the lease for an additional 3 years with the first year monthly rent amounting to $1,130 plus common area charges. Our New York headquarters lease is month to month. The total rent expense for these operating leases were approximately $16,130 and $12,804 for the six months ended April 30, 2013 and 2012, respectively.

Equipment

In June 2011, the Company entered into a Master Leasing Agreement with Yellow Box Leasing LLC. The terms of the agreement provide up to $1.25 million in equipment lease financing for Coupon Express Kiosks. The lease provides for the creation of sub-leases for each 25 Kiosks ordered. In September 2011 and in March 2012, the Company received 50 new Kiosks with a value of $ 250,000. Terms of this sub-lease provide for payments of $140/month for each Kiosk over 3 years. However, Yellow box has recently advised the Company that they are presently unable to finance the purchase of additional kiosks.

Minimum rental commitments at October 31, 2012 under all leases having a non-cancelable term of more than one year are shown below:

| 2013 | $73,968 | |

| 2014 | 29,328 | |

| $103,296 |

13

COUPON EXPRESS, INC

NOTES TO FINANCIAL STATEMENTS

April 30, 2013

6. Commitments (continued)

Legal

The Company is involved in a dispute over a services contract. S.O.S. Resources (“SOS”) and its president claim that SOS fully performed under an agreement with the Company and is entitled to receive 3,110,000 shares of our registered common stock, and later asserted that they would seek a sum of $1,191,600 from the Company. The Company believes that SOS and its president did not perform under the contract, and intends to vigorously defend itself against such claim as well as file a claim for fraud against SOS and its president. The Company believes that the suit filed by SOS and its president is without merit; however, we will have to pay costs associated with arbitrating this claim.

The Company has settled an action commenced by the law firm Cozen O’Connor seeking payment of approximately $195,000 in legal fees for services allegedly rendered by the firm in 2007. The Company has agreed to remit the sum of $3,000 per month for thirty (30) months, commencing on August 1, 2012 with a final payment of $114,671 due on January 1, 2015.

A judgement was entered against the company on May 17, 2013 in the amount of $31,269.68 in an action arising out of an arbitration award.

7. Income Taxes

We have not filed federal or state tax returns for the years ended October 31, 2004 - 2012. We did not believe that we owed material federal or state taxes for these fiscal years as a result of our operating losses. At April 30, 2013, we had approximately $24 million of net operating losses (“NOL”) carryforwards for federal and state income purposes. These losses are available for future years and expire through 2032. Utilization of these losses may be severely or completely limited if we undergo an ownership change pursuant to Internal Revenue Code Section 382.

Generally accepted accounting principles requires that the tax benefit of net operating losses, temporary differences and credit carryforwards be recorded as an asset to the extent that management assesses that realization is “more likely than not.” Realization of the future tax benefits is dependent on the Company’s ability to generate sufficient taxable income within the carryforward period. Because of our history of operating losses, management has provided a valuation allowance equal to its net deferred tax assets.

8. Subsequent events

During May 2013, the Company’s chief executive officer resigned from the company and the board of directors. In connection with the resignation, the company entered into an agreement that governs the terms of the chief executive officer’s separation from the Company. Pursuant to the agreement with the former chief executive officer, the Company will pay severance of $204,996 over an eighteen month period commencing immediately after a one-year consulting period of $10,000 per month plus bonuses as defined in the agreement.

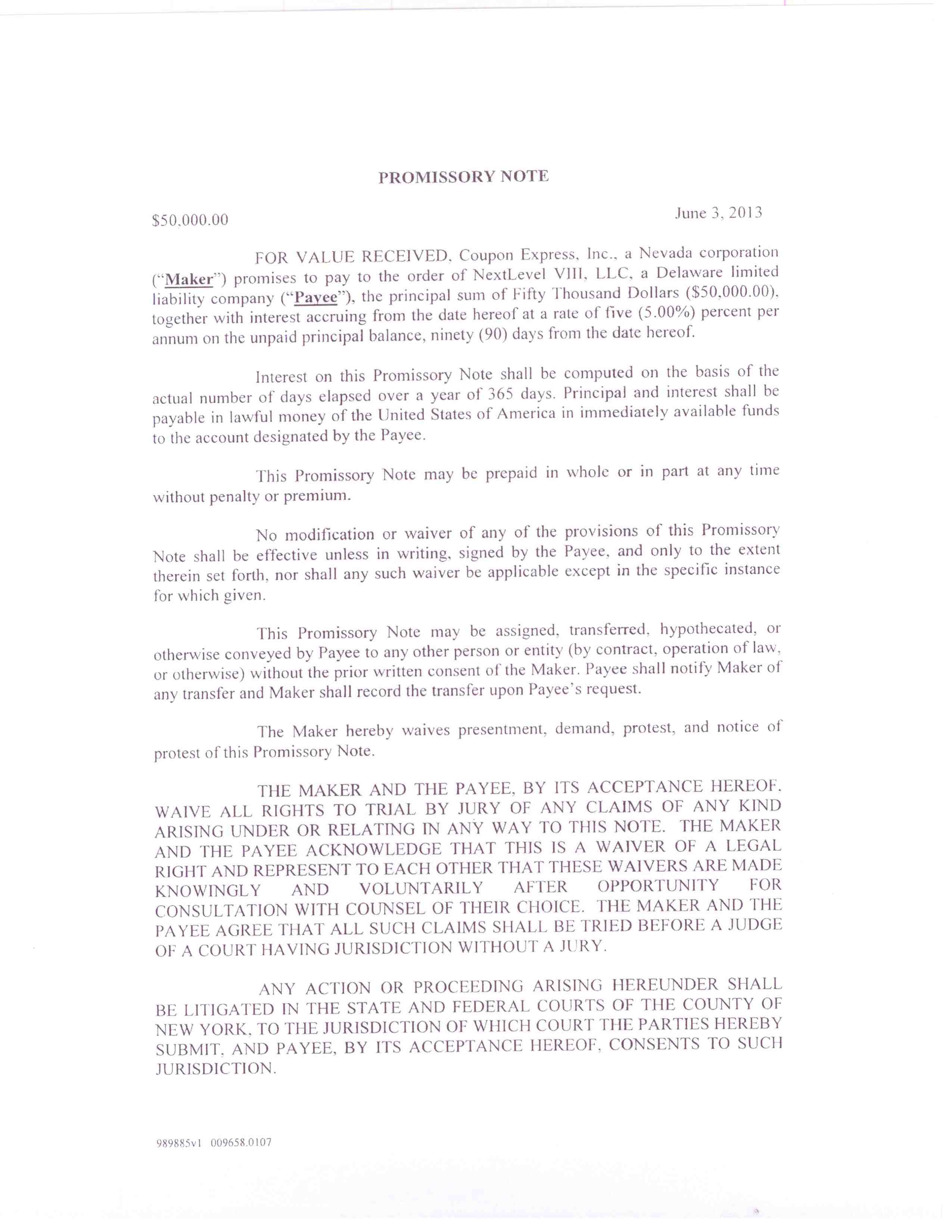

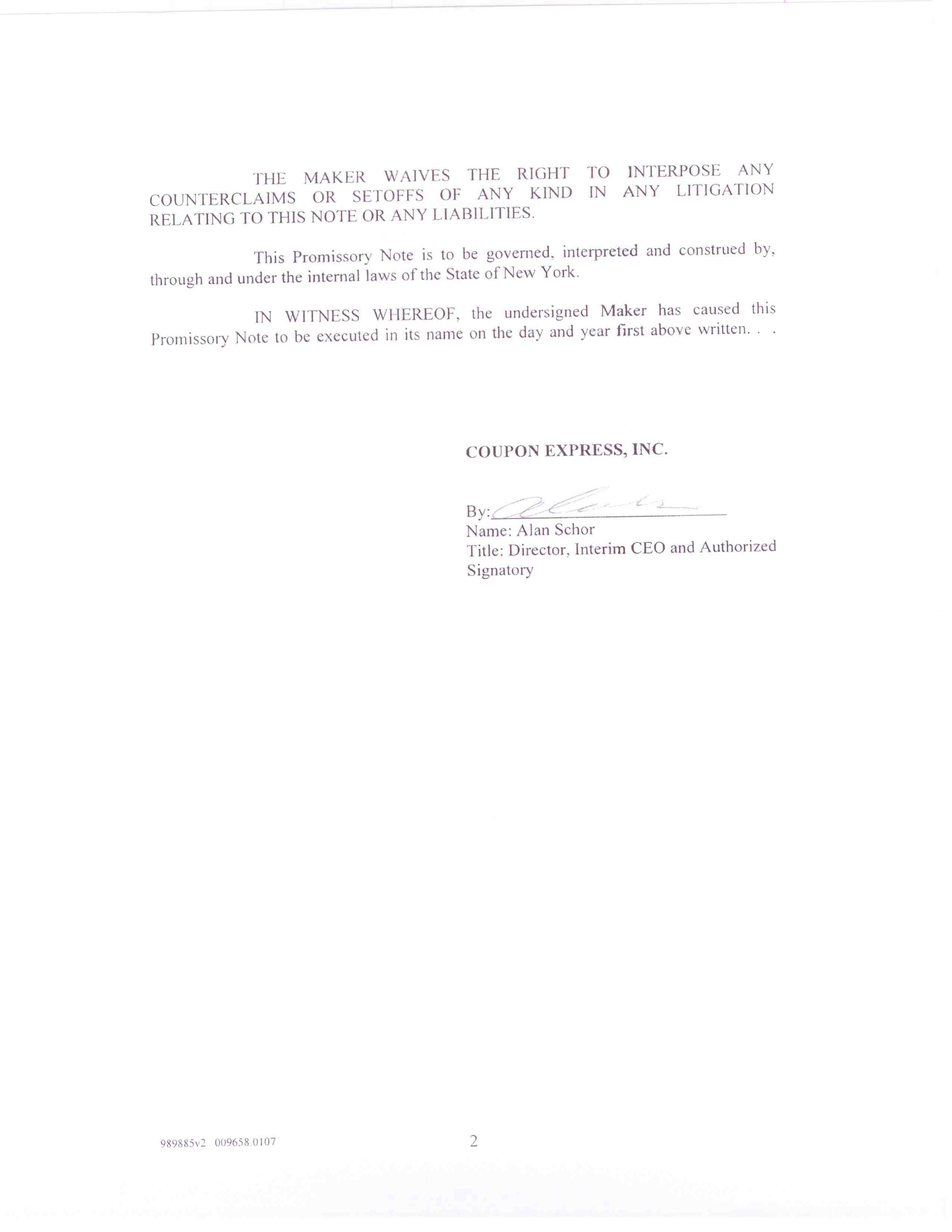

In May and June 2013, the Company entered into a series of promissory notes with a significant shareholder, Next Level Partners, pursuant to which the Company, in exchange for loans of $120,303.42. The notes mature in 90 days and bear interest at 5% per annum.

In June 2013, the Company issued 2,500,000 shares of common stock for gross proceeds of $50,000.

14

ITEM 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The discussion of the financial condition and result of operations of the Company set forth below should be read in conjunction with the consolidated financial statements and related notes thereto included elsewhere in this Form 10-Q. This Form 10-Q contains forward-looking statements that involve risks and uncertainties. The statements contained in this Form 10-Q that are not purely historical are forward-looking statements within the meaning of Section 27a of the Securities Act and Section 21e of the Exchange Act. When used in this Form 10-Q, or in the documents incorporated by reference into this Form 10-Q, the words “anticipate,” “believe,” “estimate,” “intend” and “expect” and similar expressions are intended to identify such forward-looking statements. Such forward-looking statements include, without limitation, the statements regarding the Company’s strategy, future sales, future expenses, future liquidity and capital resources. All forward-looking statements in this From 10-Q including those relating to the Company’s (i) ability to obtain licenses to any necessary third-party intellectual property; (ii) ability to retain and hire necessary employees and appropriately staff our development programs; (iii) cash requirements; and (iv) financial performance are based upon information available to the Company on the date of this Form 10-Q, and the Company assumes no obligation to update any such forward-looking statements. The Company’s actual results could differ materially from those discussed in this Form 10-Q. Factors that could cause or contribute to such differences (“Cautionary Statements”) include, but are not limited to, those discussed in Item 1. Business – “Risk Factors” and elsewhere in the Company’s Annual Report on Form 10-K, which are incorporated by reference herein and in this report. All subsequent written and oral forward-looking statements attributable to the Company, or persons acting on the Company’s behalf, are expressly qualified in their entirety by the Cautionary Statements.

Introduction

Management’s Discussion and Analysis (“MD&A”) is intended to facilitate an understanding of our business and results of operations. This MD&A should be read in conjunction with our financial statements and the accompanying notes to the financial statements included elsewhere in this report. MD&A consists of the following sections:

Overview

We are a business services corporation headquartered in New York, New York. We aim to provide innovative interactive customer communications systems and applications that support targeted marketing programs with unique point-of-purchase (POP) services and information that serve shoppers and distributors while building loyalty and revenue for the our primary clients. Through our proprietary Coupon Express kiosks and services, we provide in-store customized couponing, in multiple languages, for immediate impact in regional, independent retailers in the grocery and convenience store industries by enabling retailers to quickly determine ideal price-points for new products and mitigate losses from hard-to-sell items. Our kiosks provide consumers with information and functionality needed to redeem coupons for obtaining immediate discounts in store. Digital signage screens attached to the kiosks provide advertising opportunities for both national and local advertisers.

The kiosks are primarily placed in supermarkets. The kiosks display promoted products on the digital screen as well as providing the ability to redeem coupons in order to purchase the products at a discounted rate. The system tracks the number of dispensed coupons and calculates the rebates that the store is due. The upper screen can be used as a tool to advertise store promotions and it has an interface allowing the local store to display and show special promotions. It receives its information from central servers that distributes the data to specific locations as required. The loyalty enrollment program and dispensing of loyalty cards is designed to automate the manual function provided by the store employees and allow the system to gather information on specific purchase trends.

15

Results of Operations

For the three and six months ended April 30, 2013 and 2012, the Company reported revenues of $40,768 and $76,723 and $782 and $6,422 respectively, an increase of $39,986 (5113 %) and $70,301(1,095%), respectively.

For the three month periods ended April 30, 2013 and 2012, the Company reported net loss applicable to common stock of $388,212 and 614,225, respectively, a decrease in net loss of $226,013 (36.8%). For the six months ended April 30, 2013 and 2012, the Company reported net loss applicable to common stock of $788,814 and $1,115,376, a decrease in net loss of $326,562, or (29.3%). The details of the decrease in net loss are discussed below.

Selling expenses decreased for the three and six months ended April 30, 2013 and 2012, $33,901 (27%) and $68,271 (26%), respectively. The decrease in selling expenses is attributable to the installation and deployment of fewer kiosks during the three and six months ended April 30, 2013.

Administrative expenses decreased for the three months ended April 30, 2013, $29,269(9.2%) and increased $83,534 (17%), for the six months ended April30, 2013 The increase in administrative expenses for the six months ended April 30, 2013 is primarily attributable to the recognition of the non-cash cost of granting options and warrants to its chief executive and chief financial officer of $41,639 and increases in other expenses.

Interest expense decreased for the three and six month April 30, 2013 ended $170,628 and $368,679, respectively, as a result of the conversion of the convertible notes to common and preferred stock.

Our revenues for the three and six months ended April 30, 2013 and 2012 were derived exclusively from advertising revenue. Our losses from operations for the three and six months ended April 30, 2013 and 2012 were attributable to our inability to achieve significant revenues while incurring material working capital costs, including costs of development and deploying our kiosks.

The Company’s current revenue models include a fixed fee plus click charge and a fixed price per store model. Management believes that future deployments may incorporate one or both of these models. We anticipate that as more kiosks are installed throughout the United States, advertisers/manufacturers will be able to reach a critical mass of consumers that should result in generating additional advertising revenue from the kiosks. As of April 30, 2013, we had 130 kiosks installed, compared to 35 kiosks as of April 30, 2012, which have generated limited revenue to date. The cost to have each kiosk manufactured is approximately $5,500, which will be financed with the Premium Leasing sale leaseback program. Our monthly cash requirements are approximately $85,000 at the current rate of kiosk installments. Our cash on hand is expected to sustain operations for no more the next 30 days, at which time the Company will require additional capital to support its operations. We anticipate that the Company will need to raise additional capital of up to $1,500,000 in order to fund operations, including the purchase of additional kiosks, in the next 12 months.

Liquidity and Capital Resources

Cash Flows

Cash used in operations for the six months ended April 30, 2013and 2012 was approximately $445,601 and $826,056, respectively, a decrease of approximately $380,455 (46.0 %). Cash flows used in investing activities for the six months ended April 30, 2013 and 2012 were approximately $11, 000 and $30, 233, respectively, a decrease of $19,233. Cash flows provided by or (used in) financing activities for the six months ended April 30, 2013 and 2012 were approximately $426,000, and $(128, 000), respectively, an increase in cash flows provided by of approximately $554,000.

In the event we do not generate sufficient funds from revenues or financing through the issuance of our common stock or from debt financing, we may unable to fully implement our business plan and pay our obligations as they became due, any of which circumstances would have a material adverse effect on our business prospects.

16

On December 3, 2012, the Company issued 9.58 additional Series A Preferred Stock (the “Preferred Stock”) and warrants (the “2012 Warrants”) to purchase 11,975,000 shares of common stock, pursuant to a cumulative convertible senior note and warrant purchase agreement dated as of May 31, 2012 (the “2012 Purchase Agreement”) for proceeds of $239,500. The shares of Preferred Stock bear a cumulative dividend of 7% per annum. Upon liquidation, and upon an acquisition of the Company, the holders of Preferred Stock are entitled to a liquidation preference equal to the greater of (i) the amount invested plus all accrued and unpaid dividends, and (ii) the amount the holders of Preferred Stock, would receive had they converted the Preferred Stock to common stock immediately prior to such event. Each share of Preferred Stock is convertible into 1,250,000 shares of the Company’s common stock, subject to certain adjustments.

On December 28, 2012, the Company issued 6,835,900 shares of common stock and warrants to purchase 5,649,500 shares of common stock to a certain investor, pursuant to a common stock and warrant purchase agreement dated as of December 28, 2012 (the “Purchase Agreement”) for proceeds of $112,990.

In March 2013 the Company entered into a Kiosk leasing facility with Premium Leasing, LLC of Vestal, and New York. The term of the lease agreement is for 60 months and includes a twenty five (25%) percent down payment for each Kiosk leased and a commitment fee of $21,000. The current cost of each kiosk is $5,500. The Company will pay the 25% down payment or $1,375 and the remaining seventy-five (75%) balance shall be paid in monthly installments of $85.82 including interest at nine percent (9%) per annum. As security for each lease, the Company has agreed to issue Premium Leasing its common stock equal to the leased value of kiosks under lease. The common stock will be held in escrow as defined in the agreement. In addition, the company has also granted Premium Leasing three (3) warrants to purchase in the aggregate five million shares of the company’s common stock until March 2018. The warrant to purchase 3,000,000 shares of common stock is immediately exercisable at $.02 per share, with the two (2) remaining warrants, each to purchase 1,000,000 shares of common stock exercisable one (1) year from date of grant, at $.03 and $.04 per share, respectively. As of April 30, 2013 the Company has leased 8 kiosks under this facility.

In April 2013, the Company issued 2,500,000 shares of common stock for gross proceeds of $50,000.

Other Debt Transactions

None

Cash and cash equivalents

We had cash and cash equivalents of $2,282 as of April 30, 2013.

Due to the substantial doubt of our ability to meet our working capital needs, history of losses and current shareholders’ deficit, in their report on the annual financial statements for the year ended October 31, 2012 our independent auditors included an explanatory paragraph regarding concerns about our ability to continue as a going concern. Our financial statements contain additional note disclosures describing the circumstances that lead to this disclosure by our independent auditors.

Critical Accounting Policies and Procedures and Recent Accounting Pronouncements

The preparation of our financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent liabilities and the reported amounts of revenues and expenses. Our estimates are based on assumptions we believe are reasonable under the circumstances. We will evaluate our estimates on an ongoing basis and make changes as experience develops or as we become aware of new information. Actual results may differ from these estimates.

Off-Balance Sheet Arrangements

We currently have no off-balance sheet arrangements that have or are reasonably likely to have a current or future material effect on our financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources.

17

Item 3.

Quantitative and Qualitative Disclosures about Market Risk

The Company does not invest in market risk sensitive instruments. At times, the Company's cash equivalents consist of overnight deposits with banks and money market accounts. The Company's objective in connection with its investment strategy is to maintain the security of its cash reserves without taking market risk with principal.

Item 4.

Controls and Procedures

EVALUATION OF DISCLOSURE CONTROLS AND PROCEDURES

The Company maintains a set of disclosure controls and procedures designed to ensure that information required to be disclosed by the Company in the reports filed under the Securities Exchange Act, is recorded, processed, summarized and reported within the time periods specified by the SEC’s rules and forms. Disclosure controls are also designed with the objective of ensuring that this information is accumulated and communicated to the Company’s management, including the Company’s chief executive officer and chief financial officer, as appropriate, to allow timely decisions regarding required disclosure.

The chief executive officer and chief financial officer of the Company have evaluated the effectiveness of our disclosure controls and procedures as required by Exchange Act Rule 13a-15(b) as of the end of the period covered by this report. Based on that evaluation, the chief executive officer and chief financial officer have concluded that these disclosure controls and procedures are effective. There were no changes in our internal control over financial reporting during the Company's last fiscal quarter that have materially affected, or are reasonably likely to materially affect, our internal control over financial reporting.

CHANGES IN INTERNAL CONTROL OVER FINANCIAL REPORTING

No changes in the Company's internal control over financial reporting have come to management's attention during the Company's last fiscal quarter that have materially affected, or are likely to materially affect, the Company's internal control over financial reporting.

18

PART II

OTHER INFORMATION

Item 1.

Legal Proceedings

The Company is involved in a dispute over a services contract. S.O.S. Resources (“SOS”) and its president claim that SOS fully performed under an agreement with the Company and is entitled to receive 3,110,000 shares of our registered common stock, and later asserted that they would seek a sum of $1,191,600 from the Company. The Company believes that SOS and its president did not perform under the contract, and intends to vigorously defend itself against such claim as well as file a claim for fraud against SOS and its president. The Company believes that the suit filed by SOS and its president is without merit; however, we will have to pay costs associated with arbitrating this claim.

The Company has settled an action commenced by the law firm Cozen O’Connor seeking payment of approximately $195,000 in legal fees for services allegedly rendered by the firm in 2007. The Company has agreed to remit the sum of $3,000 per month for thirty (30) months, commencing on August 1, 2012 with a final payment of $114,670.66 due on January 1, 2015.

A judgement was entered against the company on May 17, 2013 in the amount of $31,269.68 in an action arising out of an arbitration award.

From time to time the Company may become party to litigation or other legal proceedings that we consider to be a part of the ordinary course of business.

Item 1A.

Risk Factors

There have been no material changes to our Risk Factors disclosed in Item 1A of our Annual Report on Form 10-K for the year ended October 31, 2012.

Item 2

Unregistered Sales of Equity Securities and Use of Proceeds

On December 3, 2012, the Company issued 9.58 additional Series A Preferred Stock (the “Preferred Stock”) and warrants (the “2012 Warrants”) to purchase 11,975,000 shares of common stock, pursuant to a cumulative convertible senior note and warrant purchase agreement dated as of May 31, 2012 (the “2012 Purchase Agreement”) for proceeds of $239,500. The shares of Preferred Stock bear a cumulative dividend of 7% per annum. Upon liquidation, and upon an acquisition of the Company, the holders of Preferred Stock are entitled to a liquidation preference equal to the greater of (i) the amount invested plus all accrued and unpaid dividends, and (ii) the amount the holders of Preferred Stock, would receive had they converted the Preferred Stock to common stock immediately prior to such event. Each share of Preferred Stock is convertible into 1,250,000 shares of the Company’s common stock, subject to certain adjustments.

On December 28, 2012, the Company issued 6,835,900 shares of common stock and warrants to purchase 5,649,500 shares of common stock to a certain investor, pursuant to a common stock and warrant purchase agreement dated as of December 28, 2012 (the “Purchase Agreement”) for proceeds of $112,990.

In April and June 2013, the Company issued 5,000,000 shares of common stock for gross proceeds of $100,000.

19

Item 2 (continued)

In March 2013 the Company entered into a Kiosk leasing facility with Premium Leasing, LLC of Vestal, New York. The term of the lease agreement is for 60 months and includes a twenty five (25%) percent down payment for each Kiosk leased and a commitment fee of $21,000. The current cost of each kiosk is $5,500. The Company will pay the 25% down payment or $1,375 and the remaining seventy-five (75%) balance shall be paid in monthly installments of $85.82 including interest at nine percent (9%) per annum. As security for each lease, the Company has agreed to issue Premium Leasing its common stock equal to the leased value of kiosks under lease. The common stock will be held in escrow as defined in the agreement. In addition, the company has also granted Premium Leasing three (3) warrants to purchase in the aggregate five million shares of the company’s common stock until March 2018. The warrant to purchase 3,000,000 shares of common stock is immediately exercisable at $.02 per share, with the two (2) remaining warrants, each to purchase 1,000,000 shares of common stock exercisable one (1) year from date of grant, at $.03 and $.04 per share, respectively. As of April 30, 2013 the Company has leased 8 kiosks under this facility.

Item 3.

Defaults Upon Senior Securities

NONE

Item 4.

Mine Safety Disclosures Not Applicable

Item 5.

Other Information

This quarterly report does not include an attestation report of the Company’s registered public accounting firm regarding internal control over financial reporting. Management’s report was not subjected to attestation by the Company’s registered public accounting firm pursuant to temporary rules of the Securities and Exchange Commission that permit the Company to provide only management’s report in this quarterly report.

20

Item 6.

| Exhibits | |||

| EXHIBIT | |||

| NUMBER | DESCRIPTION | ||

| 10.1 |

Form of Promissory Note dated June 3, 2013 issued to NextLevel VIII, LLC(1) | ||

|

|

|||

| 31.1 |

Certification of Principal Executive Officer and Principal Financial Officer pursuant to Sarbanes-Oxley Section 302(1) | ||

|

|

|||

| 32.1 |

Certification of Principal Executive Officer and Principal Financial Officer pursuant to Sarbanes-Oxley Section 906(1) |

||

|

|

|||

| 101.INS XBRL |

Instance Document(2) |

||

|

|

|||

| 101.SCH XBRL |

Taxonomy Extension Scheme(2) |

||

|

|

|||

| 101.CAL XBRL |

Taxonomy Extension Calculation Linkbase(2) |

||

|

|

|||

| 101.DEF XBRL |

Taxonomy Extension Definition Linkbase(2) |

||

|

|

|||

| 101.LAB XBRL |

Taxonomy Extension Label Linkbase(2) |

||

|

|

|||

| 101.PRE XBRL |

Taxonomy Presentation Linkbase(2) |

||

(1) Filed herewith.

(2) Furnished herewith.

21

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has caused this report to be signed on its behalf by the undersigned thereunto duly authorized.

| Coupon Express, Inc. | |||

| By: | /s/ Alan Schor | ||

| Name: | Alan Schor | ||

| Title: | Interim Chief Executive Officer and Chief Financial Officer (Principal Executive and Financial Officer) | ||

| Date: | July 19, 2013 | ||

22

EXHIBIT 31.1

CERTIFICATION OF

PRINCIPAL EXECUTIVE AND FINANCIAL OFFICER PURSUANT TO

SECTION 302(a) OF THE SARBANES-OXLEY ACT OF 2002

I, Alan Schor, certify that:

1. |

I have reviewed this quarterly report on Form 10-Q of Coupon Express, Inc. (the “registrant”) for the quarter ended April 30, 2013; |

2. |

Based on my knowledge, this report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this report; |

3. |

Based on my knowledge, the financial statements, and other financial information included in this report, fairly present in all material respects the financial condition, results of operations and cash flows of the registrant as of, and for, the periods presented in this report; |

4. |

The registrant’s other certifying officer(s), and I are responsible for establishing and maintaining disclosure controls and procedures (as defined in Exchange Act Rules 1 3a- 15(e) and 1 5d- 15(e)) and internal control over financial reporting (as defined in Exchange Act Rules l3a-l5(f) and l5d-15(f)) for the registrant and have: |

a. |

Designed such disclosure controls and procedures, or caused such disclosure controls and procedures to be designed under our supervision, to ensure that material information relating to the registrant, including its consolidated subsidiaries, is made known to us by others within those entities, particularly during the period in which this report is being prepared; |

b. |

Designed such internal control over financial reporting, or caused such internal control over financial reporting to be designed under our supervision, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles; |

c. |

Evaluated the effectiveness of the registrant’s disclosure controls and procedures and presented in this report our conclusions about the effectiveness of the disclosure controls and procedures, as of the end of the period covered by this report based on such evaluation; and |

d. |

Disclosed in this report any change in the registrant’s internal control over financial reporting that occurred during the registrant’s most recent fiscal quarter that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control over financial reporting; and |

5. |

The registrant’s other certifying officer(s), and I have disclosed, based on our most recent evaluation of internal control over financial reporting, to the registrant’s auditors and the audit committee of the registrant’s board of directors (or persons performing the equivalent functions): |

a. |

All significant deficiencies and material weaknesses in the design or operation of internal control over financial reporting which are reasonably likely to adversely affect the registrant’s ability to record, process, summarize and report financial information; and |

b. |

Any fraud, whether or not material, that involves management or other employees who have a significant role in the registrant’s internal control over financial reporting. |

Date: July 19, 2013

| By: | /s/ Alan Schor | |

| Name: | Alan Schor | |

| Title: | Interim Chief Executive Officer and Chief Financial Officer (Principal Executive and Financial Officer) |

23

EXHIBIT 32.1

CERTIFICATION PURSUANT TO

18 U.S.C. SECTION 1350

AS ADOPTED PURSUANT TO

SECTION 906 OF THE SARBANES-OXLEY ACT OF 2002

Alan Schor, interim chief executive officer and chief financial officer of Coupon Express, Inc. (the “Registrant”) certifies, under the standards set forth and solely for the purposes of 18 U.S.C. 1350, as adopted pursuant to Section 906 of the Sarbanes-Oxley Act of 2002, that, to his knowledge, the Quarterly Report on Form 10-Q of the Registrant for the quarter ended April 30, 2013 fully complies with the requirements of Section 13(a) or 15(d) of the Securities Exchange Act of 1934 and information contained in that Form 10-Q fairly presents, in all material respects, the financial condition and results of operations of the Registrant.

| Date: | July 19, 2013 |

| By: | /s/ Alan Schor |

| Name: | Alan Schor |

| Title: | Interim Chief Executive Officer and Chief Financial Officer (Principal Executive and Financial Officer) |

A signed original of this written statement required by Section 906 has been provided to the Registrant and will be retained by the Registrant and furnished to the Securities and Exchange Commission or its staff upon request.