Exhibit 99.1

FOX RESTAURANT CONCEPTS, LLC FISCAL YEAR ENDED JANUARY 1, 2019

FOX RESTAURANT CONCEPTS, LLC FISCAL YEAR ENDED JANUARY 1, 2019

FOX RESTAURANT CONCEPTS, LLC FISCAL YEAR ENDED JANUARY 1, 2019 CONTENTS Page Independent auditors' report1 - 2 Consolidated financial statements: Notes to consolidated financial statements7 - 23

FOX RESTAURANT CONCEPTS, LLC FISCAL YEAR ENDED JANUARY 1, 2019 CONTENTS Page Independent auditors' report1 - 2 Consolidated financial statements: Notes to consolidated financial statements7 - 23

Independent Auditors' Report Members and Management Fox Restaurant Concepts, LLC Phoenix, AZ We have audited the accompanying consolidated financial statements of Fox Restaurant Concepts, LLC, which comprise the consolidated balance sheet as of January 1, 2019, and the related consolidated statements of operations, members' equity, and cash flows for the fiscal year then ended, and the related notes to the consolidated financial statements. Management's Responsibility for the Consolidated Financial Statements Management is responsible for the preparation and fair presentation of the consolidated financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation and maintenance of internal control relevant to the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether due to fraud or error. Auditors' Responsibility Our responsibility is to express an opinion on the consolidated financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditors' judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the Company's preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. BeachFleischman PC • beachfleischman.com 1 1985 E. River Rd., Suite 201, Tucson, AZ 85718-7176 • 520.321.4600 2201 E. Camelback Rd., Suite 200, Phoenix, AZ 85016-3431 • 602.265.7011

Independent Auditors' Report Members and Management Fox Restaurant Concepts, LLC Phoenix, AZ We have audited the accompanying consolidated financial statements of Fox Restaurant Concepts, LLC, which comprise the consolidated balance sheet as of January 1, 2019, and the related consolidated statements of operations, members' equity, and cash flows for the fiscal year then ended, and the related notes to the consolidated financial statements. Management's Responsibility for the Consolidated Financial Statements Management is responsible for the preparation and fair presentation of the consolidated financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation and maintenance of internal control relevant to the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether due to fraud or error. Auditors' Responsibility Our responsibility is to express an opinion on the consolidated financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditors' judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the Company's preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. BeachFleischman PC • beachfleischman.com 1 1985 E. River Rd., Suite 201, Tucson, AZ 85718-7176 • 520.321.4600 2201 E. Camelback Rd., Suite 200, Phoenix, AZ 85016-3431 • 602.265.7011

Opinion In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of Fox Restaurant Concepts, LLC as of January 1, 2019, and the results of its operations and its cash flows for the fiscal year then ended, in accordance with accounting principles generally accepted in the United States of America. Other Matter We have previously audited the consolidated financial statements - contractual basis of Fox Restaurant Concepts, LLC as of and for the fiscal year ended January 1, 2019 and expressed and an unmodified opinion on June 12, 2019. Phoenix, Arizona December 13, 2019

Opinion In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of Fox Restaurant Concepts, LLC as of January 1, 2019, and the results of its operations and its cash flows for the fiscal year then ended, in accordance with accounting principles generally accepted in the United States of America. Other Matter We have previously audited the consolidated financial statements - contractual basis of Fox Restaurant Concepts, LLC as of and for the fiscal year ended January 1, 2019 and expressed and an unmodified opinion on June 12, 2019. Phoenix, Arizona December 13, 2019

FOX RESTAURANT CONCEPTS, LLC CONSOLIDATED BALANCE SHEET JANUARY 1, 2019 ASSETS Current assets: Cash and cash equivalents $ 8,472,877 Receivables 7,983,645 Inventory 2,057,007 Prepaid expenses 14,590,102 Due from affiliate 49,755 Total current assets 33,153,386 Property and equipment, net 104,209,883 Investment in FRC Balance, LLC 1,539,922 Investments, other 99,890 Deferred compensation plan assets 4,549,738 Other assets 1,038,600 $ 144,591,419 LIABILITIES AND MEMBERS' EQUITY Current liabilities: Note payable, bank $ 7,000,000 Current portion of long-term debt 22,342,676 Current portion of capital leases 138,084 Note payable, member 2,000,000 Accounts payable 9,490,918 Gift cards payable 8,334,323 Accrued expenses 20,506,656 Deferred revenue, current portion 40,000 Deferred rent, current portion 351,795 Total current liabilities 70,204,452 Long-term debt, net of current portion 18,384,562 Capital leases, net of current portion 248,259 Deferred revenue, net of current portion 120,000 Deferred rent, net of current portion 9,195,491 Deemed landlord financing liability, net of current portion 12,036,207 39,984,519 Commitments and contingencies Members' equity (deficiency): Members' deficiency (30,072,752) Noncontrolling interest 66,763,909 Due from a member (2,288,709) Members' equity 34,402,448 $ 144,591,419 See notes to consolidated financial statements. 3

FOX RESTAURANT CONCEPTS, LLC CONSOLIDATED BALANCE SHEET JANUARY 1, 2019 ASSETS Current assets: Cash and cash equivalents $ 8,472,877 Receivables 7,983,645 Inventory 2,057,007 Prepaid expenses 14,590,102 Due from affiliate 49,755 Total current assets 33,153,386 Property and equipment, net 104,209,883 Investment in FRC Balance, LLC 1,539,922 Investments, other 99,890 Deferred compensation plan assets 4,549,738 Other assets 1,038,600 $ 144,591,419 LIABILITIES AND MEMBERS' EQUITY Current liabilities: Note payable, bank $ 7,000,000 Current portion of long-term debt 22,342,676 Current portion of capital leases 138,084 Note payable, member 2,000,000 Accounts payable 9,490,918 Gift cards payable 8,334,323 Accrued expenses 20,506,656 Deferred revenue, current portion 40,000 Deferred rent, current portion 351,795 Total current liabilities 70,204,452 Long-term debt, net of current portion 18,384,562 Capital leases, net of current portion 248,259 Deferred revenue, net of current portion 120,000 Deferred rent, net of current portion 9,195,491 Deemed landlord financing liability, net of current portion 12,036,207 39,984,519 Commitments and contingencies Members' equity (deficiency): Members' deficiency (30,072,752) Noncontrolling interest 66,763,909 Due from a member (2,288,709) Members' equity 34,402,448 $ 144,591,419 See notes to consolidated financial statements. 3

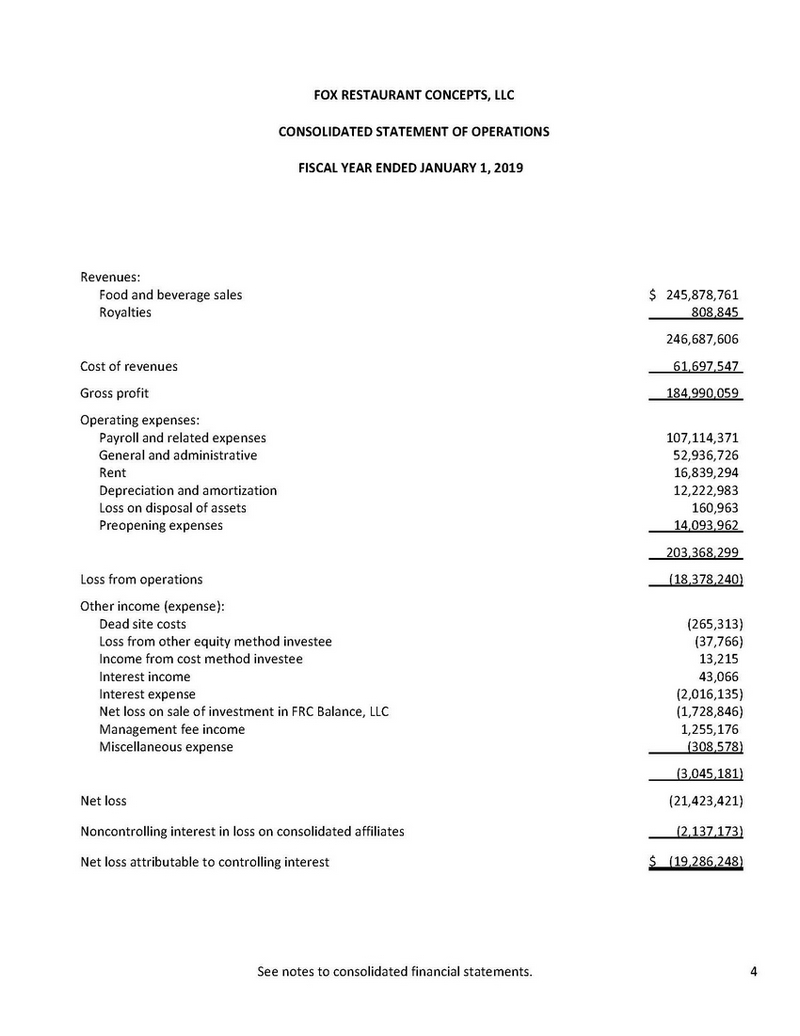

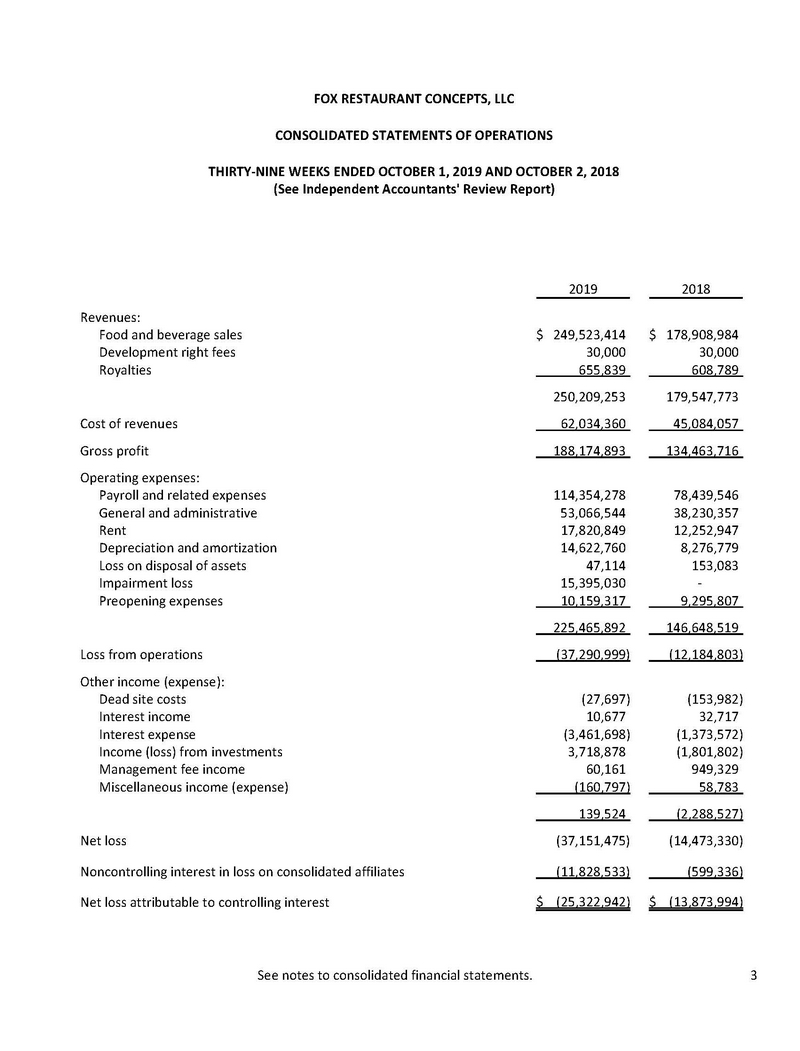

CONSOLIDATED STATEMENT OF OPERATIONS FISCAL YEAR ENDED JANUARY 1, 2019 Revenues:

CONSOLIDATED STATEMENT OF OPERATIONS FISCAL YEAR ENDED JANUARY 1, 2019 Revenues:

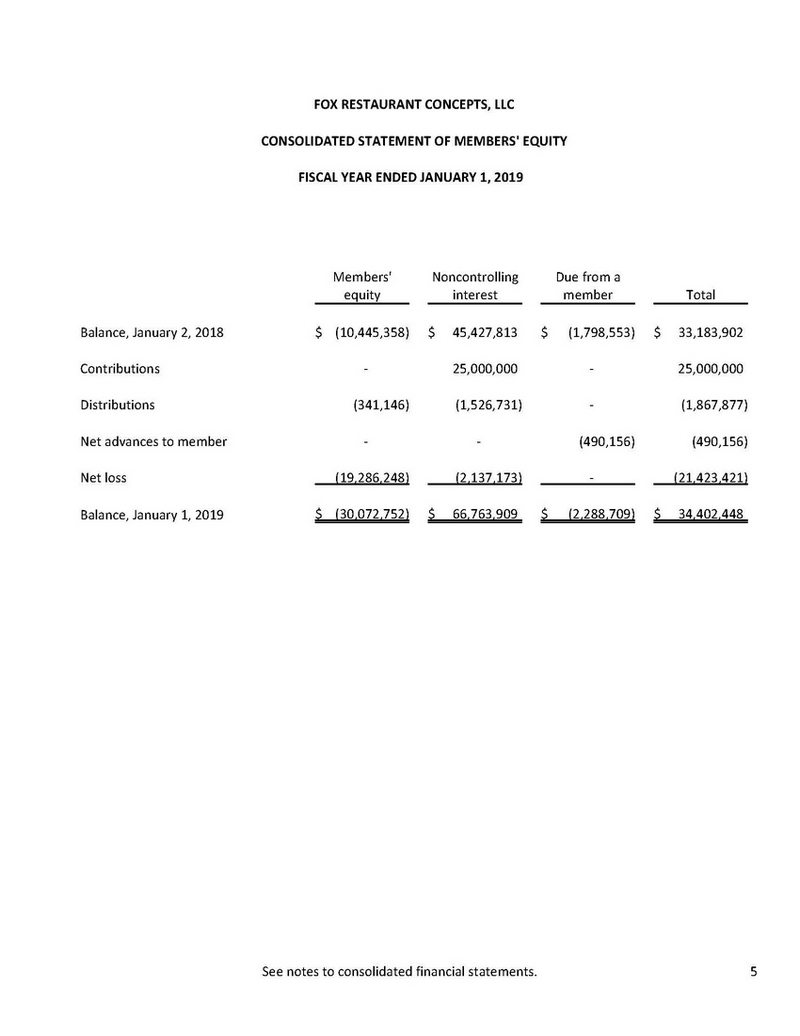

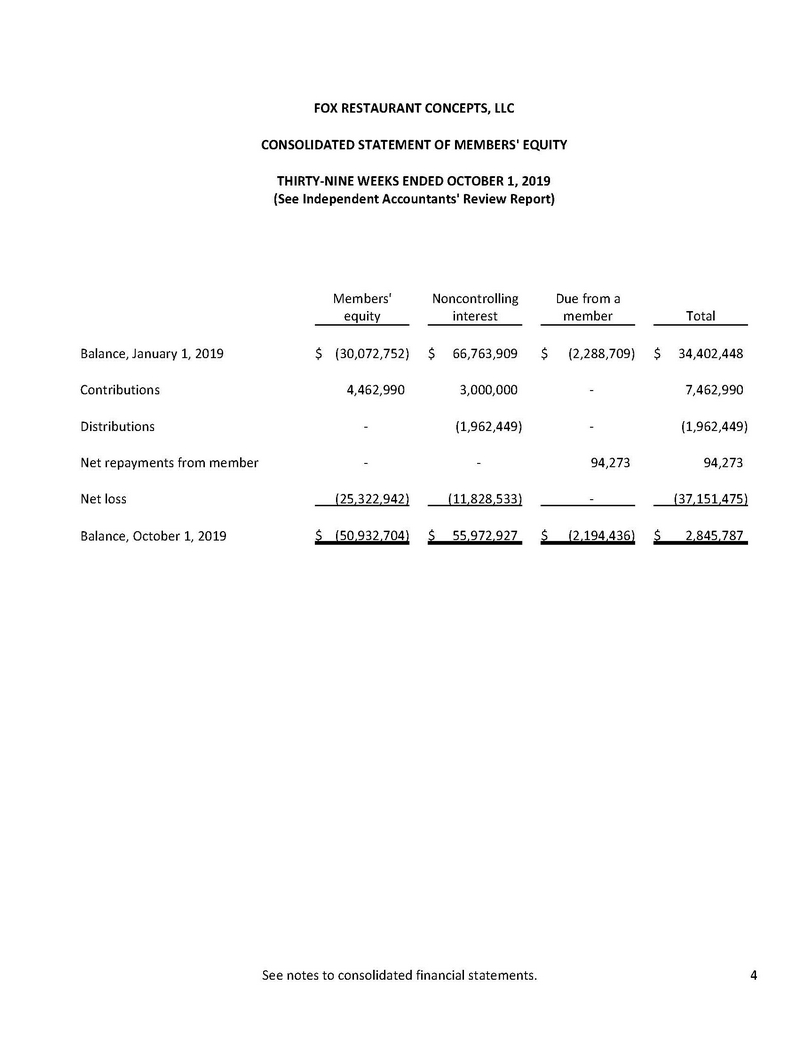

CONSOLIDATED STATEMENT OF MEMBERS' EQUITY FISCAL YEAR ENDED JANUARY 1, 2019 Members' equity Noncontrolling interest Due from a memberTotal Balance, January 2, 2018$ (10,445,358)$45,427,813$(1,798,553)$33,183,902 Contributions-25,000,000-25,000,000 Distributions(341,146)(1,526,731)-(1,867,877) Net advances to member--(490,156)(490,156) Net loss(19,286,248)(2,137,173)-(21,423,421) Balance, January 1, 2019$ (30,072,752)$66,763,909$(2,288,709)$34,402,448

CONSOLIDATED STATEMENT OF MEMBERS' EQUITY FISCAL YEAR ENDED JANUARY 1, 2019 Members' equity Noncontrolling interest Due from a memberTotal Balance, January 2, 2018$ (10,445,358)$45,427,813$(1,798,553)$33,183,902 Contributions-25,000,000-25,000,000 Distributions(341,146)(1,526,731)-(1,867,877) Net advances to member--(490,156)(490,156) Net loss(19,286,248)(2,137,173)-(21,423,421) Balance, January 1, 2019$ (30,072,752)$66,763,909$(2,288,709)$34,402,448

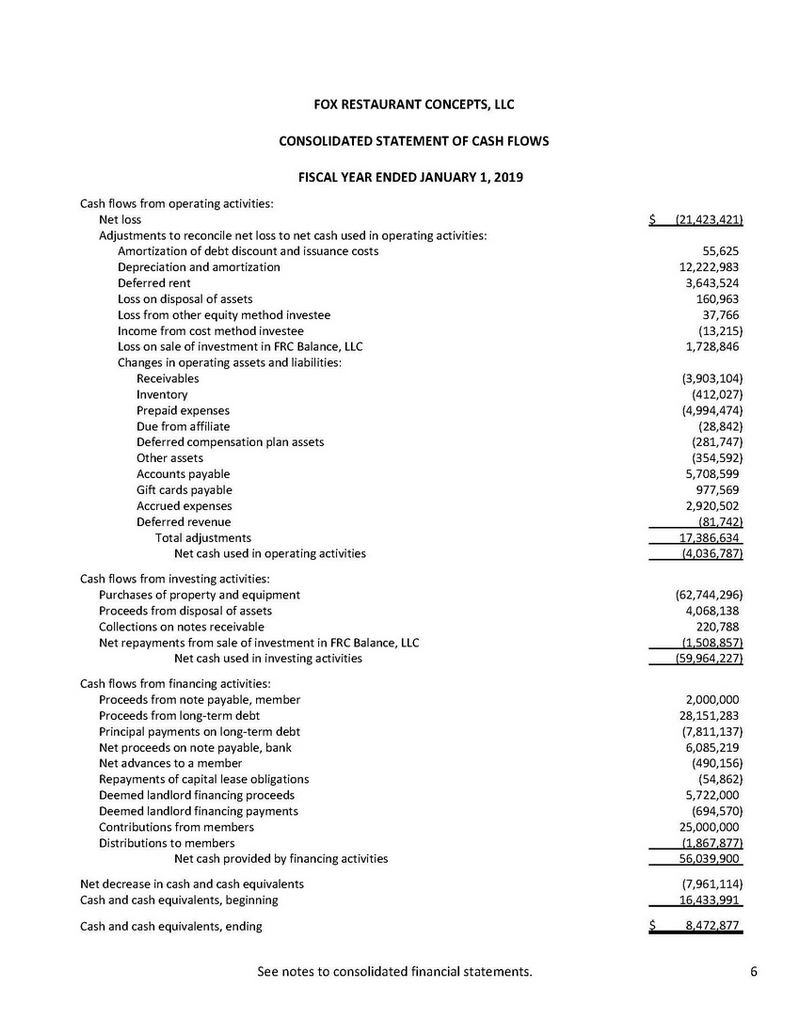

CONSOLIDATED STATEMENT OF CASH FLOWS Cash flows from operating activities: FISCAL YEAR ENDED JANUARY 1, 2019 Cash flows from investing activities:

CONSOLIDATED STATEMENT OF CASH FLOWS Cash flows from operating activities: FISCAL YEAR ENDED JANUARY 1, 2019 Cash flows from investing activities:

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS FISCAL YEAR ENDED JANUARY 1, 2019 1.Description of business and summary of significant accounting policies: History and business activity: Fox Restaurant Concepts, LLC (Fox), organized in December 1999, is a restaurant management company and owner of eleven American-style cuisine restaurants and one food truck located in Arizona, California and Texas. Three new restaurants were opened in fiscal year 2018. Wildflower Holdings, LLC (Wildflower), organized in March 1998, is a restaurant operating as "Wildflower Grill" located in Arizona and is an 81.5% owned subsidiary. North Investors, LLC (North Investors), organized in September 2016, was established for the purpose of holding Fox's investment in North Restaurants, LLC, (North Restaurants). North Restaurants, organized in May 2004, owns fifteen restaurants operating as "North". The restaurants are located in Arizona, California, Colorado, Kansas, Nevada, Pennsylvania and Texas. Three new restaurants were opened in fiscal year 2018. North Investors has a 51% ownership interest in North Restaurants at January 1, 2019. Fox has a 53% ownership interest in North Investors. Kierland Restaurant Group, LLC (Kierland), organized in March 2005, is a restaurant operating as "The Greene House" located in Arizona and is a 36% owned subsidiary. Waterfront Market, LLC (Waterfront), organized in June 2004, is a restaurant operating as "Olive and Ivy" located in Arizona. Fox's interest in Waterfront Market, LLC is held through Olive Boys, LLC (Olive Boys), a partially owned subsidiary of Fox Restaurant Concepts, LLC, organized for the purpose of holding its ownership in Waterfront Market, LLC. Olive Boys has a 60% ownership interest in Waterfront and Fox has a 65.3% ownership interest in Olive Boys. La Encantada Group, LLC (La Encantada), organized in November 2005, is a restaurant operating as "Blanco Tacos and Tequila" located in Arizona and is a 55% owned subsidiary. FRC Blanco Borgata, LLC (Borgata), organized in April 2008, is a restaurant operating as "Blanco Tacos and Tequila" located in Arizona and is a 31% owned subsidiary. FRC Waterfront III, LLC (Waterfront III), organized in July 2008, is a restaurant operating as "Culinary Dropout" located in Arizona and is a 50% owned subsidiary. FRC Cityscape, LLC (Cityscape), organized in August 2008, is a restaurant operating as "Arrogant Butcher" located in Arizona and is a 96% owned subsidiary. FRC CD 7th, LLC (CD 7th), organized in April 2012, is a restaurant operating as "Culinary Dropout" located in Arizona and is a 60% owned subsidiary.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS FISCAL YEAR ENDED JANUARY 1, 2019 1.Description of business and summary of significant accounting policies: History and business activity: Fox Restaurant Concepts, LLC (Fox), organized in December 1999, is a restaurant management company and owner of eleven American-style cuisine restaurants and one food truck located in Arizona, California and Texas. Three new restaurants were opened in fiscal year 2018. Wildflower Holdings, LLC (Wildflower), organized in March 1998, is a restaurant operating as "Wildflower Grill" located in Arizona and is an 81.5% owned subsidiary. North Investors, LLC (North Investors), organized in September 2016, was established for the purpose of holding Fox's investment in North Restaurants, LLC, (North Restaurants). North Restaurants, organized in May 2004, owns fifteen restaurants operating as "North". The restaurants are located in Arizona, California, Colorado, Kansas, Nevada, Pennsylvania and Texas. Three new restaurants were opened in fiscal year 2018. North Investors has a 51% ownership interest in North Restaurants at January 1, 2019. Fox has a 53% ownership interest in North Investors. Kierland Restaurant Group, LLC (Kierland), organized in March 2005, is a restaurant operating as "The Greene House" located in Arizona and is a 36% owned subsidiary. Waterfront Market, LLC (Waterfront), organized in June 2004, is a restaurant operating as "Olive and Ivy" located in Arizona. Fox's interest in Waterfront Market, LLC is held through Olive Boys, LLC (Olive Boys), a partially owned subsidiary of Fox Restaurant Concepts, LLC, organized for the purpose of holding its ownership in Waterfront Market, LLC. Olive Boys has a 60% ownership interest in Waterfront and Fox has a 65.3% ownership interest in Olive Boys. La Encantada Group, LLC (La Encantada), organized in November 2005, is a restaurant operating as "Blanco Tacos and Tequila" located in Arizona and is a 55% owned subsidiary. FRC Blanco Borgata, LLC (Borgata), organized in April 2008, is a restaurant operating as "Blanco Tacos and Tequila" located in Arizona and is a 31% owned subsidiary. FRC Waterfront III, LLC (Waterfront III), organized in July 2008, is a restaurant operating as "Culinary Dropout" located in Arizona and is a 50% owned subsidiary. FRC Cityscape, LLC (Cityscape), organized in August 2008, is a restaurant operating as "Arrogant Butcher" located in Arizona and is a 96% owned subsidiary. FRC CD 7th, LLC (CD 7th), organized in April 2012, is a restaurant operating as "Culinary Dropout" located in Arizona and is a 60% owned subsidiary.

1.Description of business and summary of significant accounting policies (continued): History and business activity (continued): FRC Blanco Biltmore, LLC (Biltmore), organized in June 2013, is a restaurant operating as "Blanco Tacos and Tequila" located in Arizona and is an 85% owned subsidiary. FC Investors, LLC (FC Investors), organized in October 2016, was established for the purpose of holding Fox's investment in Flowerchild Holding Company, LLC (Flowerchild Holding). Flowerchild Holding, organized in October 2016, owns sixteen restaurants operating as "Flowerchild". The restaurants are located in Arizona, California, Colorado, Georgia, Maryland, Nevada, and Texas. Eight new restaurants were opened in fiscal year 2018. FC Investors has a 54% ownership interest in Flowerchild Holding at January 1, 2019. Fox has a 100% ownership interest in FC Investors. The liability of the members of each limited liability company is limited. Basis of presentation: Under the provisions of ASC 810, Consolidation, variable interest entities (VIEs) are primarily entities that lack sufficient equity to finance their activities without additional subordinated financial support from other parties or whose equity holders as a group lack certain power, obligations, or rights. ASC 810 requires certain VIEs to be consolidated by the primary beneficiary and expands disclosures about Fox's interest in VIEs. Fox consolidates all VIEs in which it holds a variable interest and is deemed to be the primary beneficiary of the variable interest entity. The determination of whether Fox is the primary beneficiary of the VIE is based on Fox's ability to direct the activities of the VIE that most significantly impact the VIE's economic performance and its obligation to absorb losses or right to receive the benefits of the VIE. The consolidated financial statements include the accounts of the entities listed above (collectively, "the Company" or "FRC") in which Fox has the ability to exercise significant influence over operating and financial policies. All significant intercompany accounts and transactions have been eliminated. The Company has a 52/53 week fiscal year ending on the Tuesday closest to December 31. Fiscal year 2018 contained 52 weeks. Noncontrolling interest: The Company presents noncontrolling interest in the consolidated balance sheet as a separate component of members' equity. Net loss attributed to noncontrolling interest is presented in the consolidated statement of operations.

1.Description of business and summary of significant accounting policies (continued): History and business activity (continued): FRC Blanco Biltmore, LLC (Biltmore), organized in June 2013, is a restaurant operating as "Blanco Tacos and Tequila" located in Arizona and is an 85% owned subsidiary. FC Investors, LLC (FC Investors), organized in October 2016, was established for the purpose of holding Fox's investment in Flowerchild Holding Company, LLC (Flowerchild Holding). Flowerchild Holding, organized in October 2016, owns sixteen restaurants operating as "Flowerchild". The restaurants are located in Arizona, California, Colorado, Georgia, Maryland, Nevada, and Texas. Eight new restaurants were opened in fiscal year 2018. FC Investors has a 54% ownership interest in Flowerchild Holding at January 1, 2019. Fox has a 100% ownership interest in FC Investors. The liability of the members of each limited liability company is limited. Basis of presentation: Under the provisions of ASC 810, Consolidation, variable interest entities (VIEs) are primarily entities that lack sufficient equity to finance their activities without additional subordinated financial support from other parties or whose equity holders as a group lack certain power, obligations, or rights. ASC 810 requires certain VIEs to be consolidated by the primary beneficiary and expands disclosures about Fox's interest in VIEs. Fox consolidates all VIEs in which it holds a variable interest and is deemed to be the primary beneficiary of the variable interest entity. The determination of whether Fox is the primary beneficiary of the VIE is based on Fox's ability to direct the activities of the VIE that most significantly impact the VIE's economic performance and its obligation to absorb losses or right to receive the benefits of the VIE. The consolidated financial statements include the accounts of the entities listed above (collectively, "the Company" or "FRC") in which Fox has the ability to exercise significant influence over operating and financial policies. All significant intercompany accounts and transactions have been eliminated. The Company has a 52/53 week fiscal year ending on the Tuesday closest to December 31. Fiscal year 2018 contained 52 weeks. Noncontrolling interest: The Company presents noncontrolling interest in the consolidated balance sheet as a separate component of members' equity. Net loss attributed to noncontrolling interest is presented in the consolidated statement of operations.

1.Description of business and summary of significant accounting policies (continued): Estimates: The preparation of consolidated financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. Revenue recognition: Sales of food, beverage and alcohol are recognized as products are sold, net of discounts and promotions. Management fees and royalties are recognized when earned. Proceeds from the sale of gift cards are recorded as deferred revenue and recognized as revenue when the gift card is redeemed by the holder. The amount of gift cards for which redemption is remote, referred to as breakage, is estimated based on historical redemption patterns. Breakages is recognized over a three year period in proportion to historical redemption trends and is classified as revenues in the consolidated statement of operations. Incremental direct costs related to gift card sales are deferred and recognized in earnings in the same pattern as related gift card revenue. Because of inherent uncertainties in estimating redemption rates, it is reasonably possible that the estimates used will change within the near term. The Company sells gift cards in bulk at a discount to an unrelated retail store. The discount is recorded as prepaid promotion costs and is recognized when the gift card is redeemed. The Company also offers promotional gift cards which are recorded as a prepaid promotion expense based on estimated cost to deliver services and is recognized when the gift card is redeemed. Cash and cash equivalents: The Company considers all highly liquid debt instruments purchased with a maturity of three months or less to be cash equivalents. Amounts receivable from credit card companies are also considered cash and cash equivalents because they are both short-term and highly liquid in nature and are typically converted to cash within two business days of the sales transaction. The Company places its cash and cash equivalents with various credit institutions. At times, such investments may be in excess of the FDIC insurance limits; however, management does not believe it is exposed to any significant credit risk on cash and cash equivalents. Receivables: Receivables are primarily comprised of amounts due to the Company from the sale of gift cards to a national warehouse retail outlet and amounts due from landlords for tenant improvements. Management considers amounts to be fully collectible.

1.Description of business and summary of significant accounting policies (continued): Estimates: The preparation of consolidated financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. Revenue recognition: Sales of food, beverage and alcohol are recognized as products are sold, net of discounts and promotions. Management fees and royalties are recognized when earned. Proceeds from the sale of gift cards are recorded as deferred revenue and recognized as revenue when the gift card is redeemed by the holder. The amount of gift cards for which redemption is remote, referred to as breakage, is estimated based on historical redemption patterns. Breakages is recognized over a three year period in proportion to historical redemption trends and is classified as revenues in the consolidated statement of operations. Incremental direct costs related to gift card sales are deferred and recognized in earnings in the same pattern as related gift card revenue. Because of inherent uncertainties in estimating redemption rates, it is reasonably possible that the estimates used will change within the near term. The Company sells gift cards in bulk at a discount to an unrelated retail store. The discount is recorded as prepaid promotion costs and is recognized when the gift card is redeemed. The Company also offers promotional gift cards which are recorded as a prepaid promotion expense based on estimated cost to deliver services and is recognized when the gift card is redeemed. Cash and cash equivalents: The Company considers all highly liquid debt instruments purchased with a maturity of three months or less to be cash equivalents. Amounts receivable from credit card companies are also considered cash and cash equivalents because they are both short-term and highly liquid in nature and are typically converted to cash within two business days of the sales transaction. The Company places its cash and cash equivalents with various credit institutions. At times, such investments may be in excess of the FDIC insurance limits; however, management does not believe it is exposed to any significant credit risk on cash and cash equivalents. Receivables: Receivables are primarily comprised of amounts due to the Company from the sale of gift cards to a national warehouse retail outlet and amounts due from landlords for tenant improvements. Management considers amounts to be fully collectible.

1.Description of business and summary of significant accounting policies (continued): Financing receivables: The Company grants secured and unsecured credit to a member, affiliates and third parties through interest and noninterest-bearing loans and notes. Payments received are applied to interest first then the outstanding principal balance. For notes to third parties under which interest is charged, the Company stops accruing interest when the loan becomes past due and collectibility of the interest becomes uncertain. The accrual of interest resumes once its collectibility is reasonably assured. Management continually evaluates the credit quality of these receivables using various indicators that consider both qualitative and quantitative factors including the member's, affiliates' and third parties' access to financial markets. Management has not provided an allowance for doubtful receivables based upon prior experience and management's assessment of the collectibility of the amount. Receivables are charged off when all reasonable collection efforts have been exhausted. Inventory: Inventory consists of food, beverage and alcohol and is stated at the lower of cost (first-in, first-out method) or net realizable value. Liquor licenses: The costs of obtaining non-transferable liquor licenses are capitalized and amortized over the associated lease term. Transferable liquor licenses have indefinite lives, and therefore, are not subject to amortization. Non-transferable liquor licenses are included in prepaid expenses and transferable liquor licenses are included in other assets. Property, equipment, depreciation and amortization: Property and equipment are stated at cost. Furniture, equipment, aircraft and vehicles are depreciated on a straight-line basis over the estimated service lives of the related assets, which range from five to ten years. Leasehold improvements are amortized over the shorter of the useful life of the asset or the length of the related lease term. The original cost of china, glass and silver is depreciated over five years and subsequent replacements are expensed as purchased. Equipment acquired under capital leases are stated at cost or the asset's net present value of future lease payments at the date of the lease. Amortization is provided using the straight-line method over the estimated useful lives of the assets or lease term and is included with depreciation expense.

1.Description of business and summary of significant accounting policies (continued): Financing receivables: The Company grants secured and unsecured credit to a member, affiliates and third parties through interest and noninterest-bearing loans and notes. Payments received are applied to interest first then the outstanding principal balance. For notes to third parties under which interest is charged, the Company stops accruing interest when the loan becomes past due and collectibility of the interest becomes uncertain. The accrual of interest resumes once its collectibility is reasonably assured. Management continually evaluates the credit quality of these receivables using various indicators that consider both qualitative and quantitative factors including the member's, affiliates' and third parties' access to financial markets. Management has not provided an allowance for doubtful receivables based upon prior experience and management's assessment of the collectibility of the amount. Receivables are charged off when all reasonable collection efforts have been exhausted. Inventory: Inventory consists of food, beverage and alcohol and is stated at the lower of cost (first-in, first-out method) or net realizable value. Liquor licenses: The costs of obtaining non-transferable liquor licenses are capitalized and amortized over the associated lease term. Transferable liquor licenses have indefinite lives, and therefore, are not subject to amortization. Non-transferable liquor licenses are included in prepaid expenses and transferable liquor licenses are included in other assets. Property, equipment, depreciation and amortization: Property and equipment are stated at cost. Furniture, equipment, aircraft and vehicles are depreciated on a straight-line basis over the estimated service lives of the related assets, which range from five to ten years. Leasehold improvements are amortized over the shorter of the useful life of the asset or the length of the related lease term. The original cost of china, glass and silver is depreciated over five years and subsequent replacements are expensed as purchased. Equipment acquired under capital leases are stated at cost or the asset's net present value of future lease payments at the date of the lease. Amortization is provided using the straight-line method over the estimated useful lives of the assets or lease term and is included with depreciation expense.

1.Description of business and summary of significant accounting policies (continued): Leases: The Company currently leases all of its restaurant locations. The Company evaluates each lease to determine its appropriate classification as an operating or capital lease for financial reporting purposes. All restaurant leases are classified as operating leases. Minimum base rent, which generally escalates over the term of the lease, is recorded on a straight-line basis over the lease term. The lease term includes the build-out period for the leases, where no rent payments are typically due under the terms of the lease. Contingent rent expense, which is based on a percentage of revenues, is recorded as incurred to the extent it exceeds minimum base rent per the lease agreement. The Company expends cash for leasehold improvements and furnishings, fixtures and equipment to build out and equip its leased premises. FRC may also expend cash for structural additions that the Company made to leased premises. Generally, a portion of the leasehold improvements and building costs are reimbursed to FRC by the landlords as construction contributions. If obtained, landlord construction contributions usually take the form of up-front cash. Depending on the specifics of the leased space and the lease agreement, amounts paid for structural components are recorded during the construction period as either prepaid rent or property and equipment and the landlord construction contributions are recorded as either an offset to prepaid rent or as a deemed landlord financing liability. For those leases for which the Company is deemed the owner of the property during construction, upon completion, FRC performs an analysis to determine if they qualify for sale-leaseback treatment. For those qualifying leases, the deemed landlord financing liability and the associated property and equipment are removed and the difference is reclassified to either prepaid or deferred rent and amortized over the lease term as an increase or decrease to rent expense. If the lease does not qualify for sale-leaseback treatment, due to continuing involvement, the deemed landlord financing liability is amortized over the lease term based on the rent payments designated in the lease agreement. Debt discount and issuance costs: Debt discount and issuance costs are presented in the balance sheet as a direct deduction from the carrying amount of the notes payable. The Company amortizes debt discount and issuance costs to interest expense over the life of the related note using the effective interest method. Interest expense for fiscal year 2018 related to the amortization of debt discount and issuance costs was $55,625. Investments: The Company accounts for investments in which it has the ability to exercise significant influence over the investee on the equity method of accounting. Investments in which the Company does not have the ability to exercise significant influence over the investee are accounted for on the cost method.

1.Description of business and summary of significant accounting policies (continued): Leases: The Company currently leases all of its restaurant locations. The Company evaluates each lease to determine its appropriate classification as an operating or capital lease for financial reporting purposes. All restaurant leases are classified as operating leases. Minimum base rent, which generally escalates over the term of the lease, is recorded on a straight-line basis over the lease term. The lease term includes the build-out period for the leases, where no rent payments are typically due under the terms of the lease. Contingent rent expense, which is based on a percentage of revenues, is recorded as incurred to the extent it exceeds minimum base rent per the lease agreement. The Company expends cash for leasehold improvements and furnishings, fixtures and equipment to build out and equip its leased premises. FRC may also expend cash for structural additions that the Company made to leased premises. Generally, a portion of the leasehold improvements and building costs are reimbursed to FRC by the landlords as construction contributions. If obtained, landlord construction contributions usually take the form of up-front cash. Depending on the specifics of the leased space and the lease agreement, amounts paid for structural components are recorded during the construction period as either prepaid rent or property and equipment and the landlord construction contributions are recorded as either an offset to prepaid rent or as a deemed landlord financing liability. For those leases for which the Company is deemed the owner of the property during construction, upon completion, FRC performs an analysis to determine if they qualify for sale-leaseback treatment. For those qualifying leases, the deemed landlord financing liability and the associated property and equipment are removed and the difference is reclassified to either prepaid or deferred rent and amortized over the lease term as an increase or decrease to rent expense. If the lease does not qualify for sale-leaseback treatment, due to continuing involvement, the deemed landlord financing liability is amortized over the lease term based on the rent payments designated in the lease agreement. Debt discount and issuance costs: Debt discount and issuance costs are presented in the balance sheet as a direct deduction from the carrying amount of the notes payable. The Company amortizes debt discount and issuance costs to interest expense over the life of the related note using the effective interest method. Interest expense for fiscal year 2018 related to the amortization of debt discount and issuance costs was $55,625. Investments: The Company accounts for investments in which it has the ability to exercise significant influence over the investee on the equity method of accounting. Investments in which the Company does not have the ability to exercise significant influence over the investee are accounted for on the cost method.

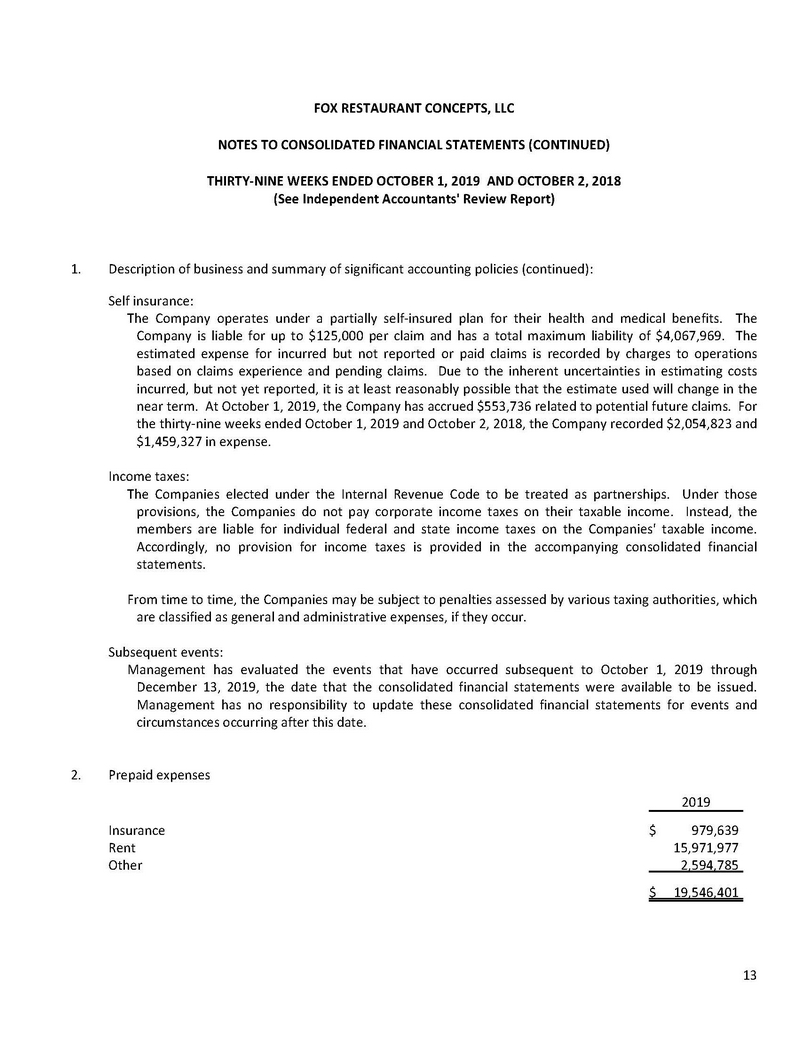

Description of business and summary of significant accounting policies (continued): Sales tax: The states and cities in which the Company operates impose sales tax on all nonexempt sales. The Company collects the sales tax from customers and remits the entire amount to the appropriate taxing authority. The Company's accounting policy is to exclude the tax collected and remitted from revenues and cost of revenues. Advertising: The Company follows a policy of charging costs of advertising to expense as incurred. Total advertising expense for fiscal year 2018 was $4,299,179. Preopening expenses: Preopening expenses, consisting primarily of manager salaries and relocation expense, employee payroll and related training costs, and other general costs incurred prior to the opening of a restaurant, are expensed as incurred. Self insurance: The Company operates under a partially self-insured plan for their health and medical benefits. The Company is liable for up to $125,000 per claim and has a total maximum liability of $3,493,512. The estimated expense for incurred but not reported or paid claims is recorded by charges to operations based on claims experience and pending claims. Due to the inherent uncertainties in estimating costs incurred, but not yet reported, it is at least reasonably possible that the estimate used will change in the near term. At January 1, 2019, the Company has accrued $330,000 related to potential future claims. For fiscal year 2018, the Company recorded $1,628,030 in expense, net of $264,639 reimbursed by FRC Balance, LLC (Balance). Income taxes: The Companies elected under the Internal Revenue Code to be treated as partnerships. Under those provisions, the Companies do not pay corporate income taxes on their taxable income. Instead, the members are liable for individual federal and state income taxes on the Companies' taxable income. Accordingly, no provision for income taxes is provided in the accompanying consolidated financial statements. From time to time, the Companies may be subject to penalties assessed by various taxing authorities, which are classified as general and administrative expenses, if they occur.

Description of business and summary of significant accounting policies (continued): Sales tax: The states and cities in which the Company operates impose sales tax on all nonexempt sales. The Company collects the sales tax from customers and remits the entire amount to the appropriate taxing authority. The Company's accounting policy is to exclude the tax collected and remitted from revenues and cost of revenues. Advertising: The Company follows a policy of charging costs of advertising to expense as incurred. Total advertising expense for fiscal year 2018 was $4,299,179. Preopening expenses: Preopening expenses, consisting primarily of manager salaries and relocation expense, employee payroll and related training costs, and other general costs incurred prior to the opening of a restaurant, are expensed as incurred. Self insurance: The Company operates under a partially self-insured plan for their health and medical benefits. The Company is liable for up to $125,000 per claim and has a total maximum liability of $3,493,512. The estimated expense for incurred but not reported or paid claims is recorded by charges to operations based on claims experience and pending claims. Due to the inherent uncertainties in estimating costs incurred, but not yet reported, it is at least reasonably possible that the estimate used will change in the near term. At January 1, 2019, the Company has accrued $330,000 related to potential future claims. For fiscal year 2018, the Company recorded $1,628,030 in expense, net of $264,639 reimbursed by FRC Balance, LLC (Balance). Income taxes: The Companies elected under the Internal Revenue Code to be treated as partnerships. Under those provisions, the Companies do not pay corporate income taxes on their taxable income. Instead, the members are liable for individual federal and state income taxes on the Companies' taxable income. Accordingly, no provision for income taxes is provided in the accompanying consolidated financial statements. From time to time, the Companies may be subject to penalties assessed by various taxing authorities, which are classified as general and administrative expenses, if they occur.

Description of business and summary of significant accounting policies (continued): Subsequent events: Management has evaluated the events that have occurred subsequent to January 1, 2019 through December 13, 2019, the date that the consolidated financial statements were available to be issued. Management has no responsibility to update these consolidated financial statements for events and circumstances occurring after this date. Contractual basis statements: We have previously audited the consolidated financial statements - contractual basis of Fox Restaurant Concepts, LLC as of and for the fiscal year ended January 1, 2019 and expressed and an unmodified opinion on June 12, 2019. Prepaid expenses Insurance$1,076,534 Rent11,118,195 Other2,395,373 $14,590,102

Description of business and summary of significant accounting policies (continued): Subsequent events: Management has evaluated the events that have occurred subsequent to January 1, 2019 through December 13, 2019, the date that the consolidated financial statements were available to be issued. Management has no responsibility to update these consolidated financial statements for events and circumstances occurring after this date. Contractual basis statements: We have previously audited the consolidated financial statements - contractual basis of Fox Restaurant Concepts, LLC as of and for the fiscal year ended January 1, 2019 and expressed and an unmodified opinion on June 12, 2019. Prepaid expenses Insurance$1,076,534 Rent11,118,195 Other2,395,373 $14,590,102

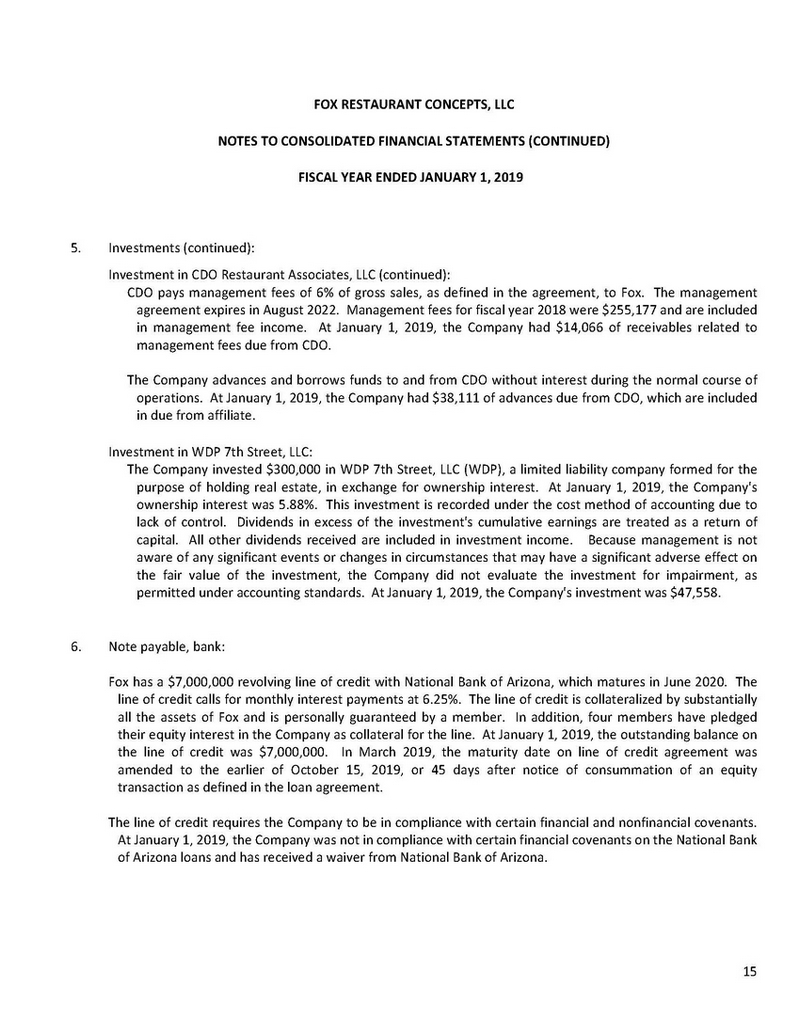

5.Investments: Investment in FRC Balance, LLC: In 2008, Fox invested in FRC Balance, LLC (Balance). Fox's investment in Balance was 24.5% at December 28, 2016 and was recorded under the equity method of accounting until October 13, 2017 when Fox sold a portion of their investment for $36,430,716, reducing their ownership interest from 24.5% to 2.5%. The 2017 sale resulted in a gain of $25,225,368. Due to loss of control, the investment was accounted for under the cost method of accounting following the sale. In 2018, Fox sold a .31% interest in Balance for $748,109 resulting in a gain of $528,120, and reducing their ownership interest to 2.19%. The 2017 sales price was based on, among other factors, projected sales through July 2018. In 2018 a true-up of the sales price was calculated which resulted in a decrease of the 2017 sales price of $2,016,968 which was recorded and repaid to Balance in 2018. Under the cost method of accounting, dividends in excess of the investment's cumulative earnings are treated as a return of capital. All other dividends received are included in investment income. Because management is not aware of any significant events or changes in circumstances that may have a significant adverse effect on the fair value of the investment, the Company did not evaluate the investment for impairment, as permitted under accounting standards. At January 1, 2019, Fox's investment in Balance totaled $1,539,922. During fiscal year 2018, Balance paid FRC $1,000,000 for transition services, which is included in management fee income. At January 1, 2019, the Company had $83,333 of receivables related to fees due from Balance. The Company advances and borrows funds to and from Balance without interest during the normal course of operations. At January 1, 2019, the Company had $176,742 of receivables due from Balance. Investment in CDO Restaurant Associates, LLC: In 2012, Fox invested in CDO Restaurant Associates, LLC (CDO). At January 1, 2019, Fox's investment in CDO totaled $52,332 and ownership interest in CDO was 20%. The loss related to this equity method investee totaled $37,766 in fiscal year 2018. The loss represents Fox's portion of CDO's net losses in fiscal year 2018 and are recorded as other expenses in the consolidated statement of operations. The CDO operating agreement states members are paid a preferred return of 8% annually on the average daily balance of the member's invested capital account. Fox's preferred return was $40,209 for fiscal year 2018 and is included in interest income. At January 1, 2019, the Company had $157,340 of preferred returns due from CDO, which are included in receivables.

5.Investments: Investment in FRC Balance, LLC: In 2008, Fox invested in FRC Balance, LLC (Balance). Fox's investment in Balance was 24.5% at December 28, 2016 and was recorded under the equity method of accounting until October 13, 2017 when Fox sold a portion of their investment for $36,430,716, reducing their ownership interest from 24.5% to 2.5%. The 2017 sale resulted in a gain of $25,225,368. Due to loss of control, the investment was accounted for under the cost method of accounting following the sale. In 2018, Fox sold a .31% interest in Balance for $748,109 resulting in a gain of $528,120, and reducing their ownership interest to 2.19%. The 2017 sales price was based on, among other factors, projected sales through July 2018. In 2018 a true-up of the sales price was calculated which resulted in a decrease of the 2017 sales price of $2,016,968 which was recorded and repaid to Balance in 2018. Under the cost method of accounting, dividends in excess of the investment's cumulative earnings are treated as a return of capital. All other dividends received are included in investment income. Because management is not aware of any significant events or changes in circumstances that may have a significant adverse effect on the fair value of the investment, the Company did not evaluate the investment for impairment, as permitted under accounting standards. At January 1, 2019, Fox's investment in Balance totaled $1,539,922. During fiscal year 2018, Balance paid FRC $1,000,000 for transition services, which is included in management fee income. At January 1, 2019, the Company had $83,333 of receivables related to fees due from Balance. The Company advances and borrows funds to and from Balance without interest during the normal course of operations. At January 1, 2019, the Company had $176,742 of receivables due from Balance. Investment in CDO Restaurant Associates, LLC: In 2012, Fox invested in CDO Restaurant Associates, LLC (CDO). At January 1, 2019, Fox's investment in CDO totaled $52,332 and ownership interest in CDO was 20%. The loss related to this equity method investee totaled $37,766 in fiscal year 2018. The loss represents Fox's portion of CDO's net losses in fiscal year 2018 and are recorded as other expenses in the consolidated statement of operations. The CDO operating agreement states members are paid a preferred return of 8% annually on the average daily balance of the member's invested capital account. Fox's preferred return was $40,209 for fiscal year 2018 and is included in interest income. At January 1, 2019, the Company had $157,340 of preferred returns due from CDO, which are included in receivables.

Investments (continued): Investment in CDO Restaurant Associates, LLC (continued): CDO pays management fees of 6% of gross sales, as defined in the agreement, to Fox. The management agreement expires in August 2022. Management fees for fiscal year 2018 were $255,177 and are included in management fee income. At January 1, 2019, the Company had $14,066 of receivables related to management fees due from CDO. The Company advances and borrows funds to and from CDO without interest during the normal course of operations. At January 1, 2019, the Company had $38,111 of advances due from CDO, which are included in due from affiliate. Investment in WDP 7th Street, LLC: The Company invested $300,000 in WDP 7th Street, LLC (WDP), a limited liability company formed for the purpose of holding real estate, in exchange for ownership interest. At January 1, 2019, the Company's ownership interest was 5.88%. This investment is recorded under the cost method of accounting due to lack of control. Dividends in excess of the investment's cumulative earnings are treated as a return of capital. All other dividends received are included in investment income. Because management is not aware of any significant events or changes in circumstances that may have a significant adverse effect on the fair value of the investment, the Company did not evaluate the investment for impairment, as permitted under accounting standards. At January 1, 2019, the Company's investment was $47,558. Note payable, bank: Fox has a $7,000,000 revolving line of credit with National Bank of Arizona, which matures in June 2020. The line of credit calls for monthly interest payments at 6.25%. The line of credit is collateralized by substantially all the assets of Fox and is personally guaranteed by a member. In addition, four members have pledged their equity interest in the Company as collateral for the line. At January 1, 2019, the outstanding balance on the line of credit was $7,000,000. In March 2019, the maturity date on line of credit agreement was amended to the earlier of October 15, 2019, or 45 days after notice of consummation of an equity transaction as defined in the loan agreement. The line of credit requires the Company to be in compliance with certain financial and nonfinancial covenants. At January 1, 2019, the Company was not in compliance with certain financial covenants on the National Bank of Arizona loans and has received a waiver from National Bank of Arizona.

Investments (continued): Investment in CDO Restaurant Associates, LLC (continued): CDO pays management fees of 6% of gross sales, as defined in the agreement, to Fox. The management agreement expires in August 2022. Management fees for fiscal year 2018 were $255,177 and are included in management fee income. At January 1, 2019, the Company had $14,066 of receivables related to management fees due from CDO. The Company advances and borrows funds to and from CDO without interest during the normal course of operations. At January 1, 2019, the Company had $38,111 of advances due from CDO, which are included in due from affiliate. Investment in WDP 7th Street, LLC: The Company invested $300,000 in WDP 7th Street, LLC (WDP), a limited liability company formed for the purpose of holding real estate, in exchange for ownership interest. At January 1, 2019, the Company's ownership interest was 5.88%. This investment is recorded under the cost method of accounting due to lack of control. Dividends in excess of the investment's cumulative earnings are treated as a return of capital. All other dividends received are included in investment income. Because management is not aware of any significant events or changes in circumstances that may have a significant adverse effect on the fair value of the investment, the Company did not evaluate the investment for impairment, as permitted under accounting standards. At January 1, 2019, the Company's investment was $47,558. Note payable, bank: Fox has a $7,000,000 revolving line of credit with National Bank of Arizona, which matures in June 2020. The line of credit calls for monthly interest payments at 6.25%. The line of credit is collateralized by substantially all the assets of Fox and is personally guaranteed by a member. In addition, four members have pledged their equity interest in the Company as collateral for the line. At January 1, 2019, the outstanding balance on the line of credit was $7,000,000. In March 2019, the maturity date on line of credit agreement was amended to the earlier of October 15, 2019, or 45 days after notice of consummation of an equity transaction as defined in the loan agreement. The line of credit requires the Company to be in compliance with certain financial and nonfinancial covenants. At January 1, 2019, the Company was not in compliance with certain financial covenants on the National Bank of Arizona loans and has received a waiver from National Bank of Arizona.

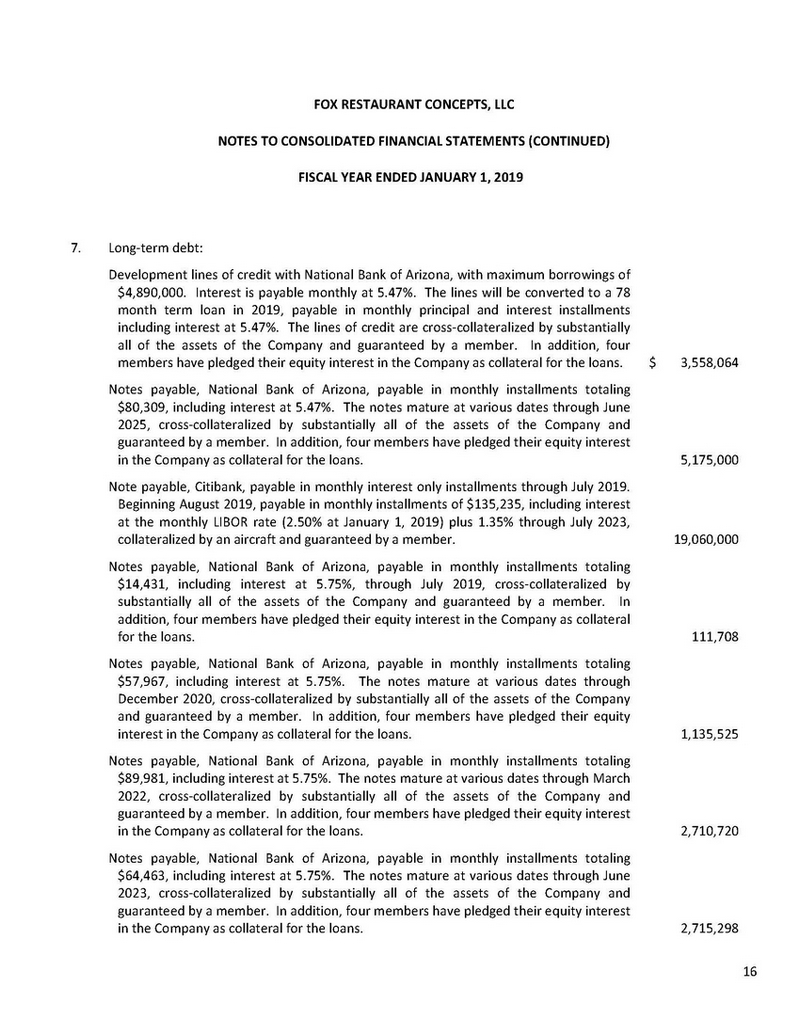

Long-term debt: Development lines of credit with National Bank of Arizona, with maximum borrowings of $4,890,000. Interest is payable monthly at 5.47%. The lines will be converted to a 78 month term loan in 2019, payable in monthly principal and interest installments including interest at 5.47%. The lines of credit are cross-collateralized by substantially all of the assets of the Company and guaranteed by a member. In addition, four members have pledged their equity interest in the Company as collateral for the loans.$3,558,064 Notes payable, National Bank of Arizona, payable in monthly installments totaling $80,309, including interest at 5.47%. The notes mature at various dates through June 2025, cross-collateralized by substantially all of the assets of the Company and guaranteed by a member. In addition, four members have pledged their equity interest in the Company as collateral for the loans.5,175,000 Note payable, Citibank, payable in monthly interest only installments through July 2019. Beginning August 2019, payable in monthly installments of $135,235, including interest at the monthly LIBOR rate (2.50% at January 1, 2019) plus 1.35% through July 2023, collateralized by an aircraft and guaranteed by a member.19,060,000 Notes payable, National Bank of Arizona, payable in monthly installments totaling $14,431, including interest at 5.75%, through July 2019, cross-collateralized by substantially all of the assets of the Company and guaranteed by a member. In addition, four members have pledged their equity interest in the Company as collateral for the loans.111,708 Notes payable, National Bank of Arizona, payable in monthly installments totaling $57,967, including interest at 5.75%. The notes mature at various dates through December 2020, cross-collateralized by substantially all of the assets of the Company and guaranteed by a member. In addition, four members have pledged their equity interest in the Company as collateral for the loans.1,135,525 Notes payable, National Bank of Arizona, payable in monthly installments totaling $89,981, including interest at 5.75%. The notes mature at various dates through March 2022, cross-collateralized by substantially all of the assets of the Company and guaranteed by a member. In addition, four members have pledged their equity interest in the Company as collateral for the loans.2,710,720 Notes payable, National Bank of Arizona, payable in monthly installments totaling $64,463, including interest at 5.75%. The notes mature at various dates through June 2023, cross-collateralized by substantially all of the assets of the Company and guaranteed by a member. In addition, four members have pledged their equity interest in the Company as collateral for the loans.2,715,298

Long-term debt: Development lines of credit with National Bank of Arizona, with maximum borrowings of $4,890,000. Interest is payable monthly at 5.47%. The lines will be converted to a 78 month term loan in 2019, payable in monthly principal and interest installments including interest at 5.47%. The lines of credit are cross-collateralized by substantially all of the assets of the Company and guaranteed by a member. In addition, four members have pledged their equity interest in the Company as collateral for the loans.$3,558,064 Notes payable, National Bank of Arizona, payable in monthly installments totaling $80,309, including interest at 5.47%. The notes mature at various dates through June 2025, cross-collateralized by substantially all of the assets of the Company and guaranteed by a member. In addition, four members have pledged their equity interest in the Company as collateral for the loans.5,175,000 Note payable, Citibank, payable in monthly interest only installments through July 2019. Beginning August 2019, payable in monthly installments of $135,235, including interest at the monthly LIBOR rate (2.50% at January 1, 2019) plus 1.35% through July 2023, collateralized by an aircraft and guaranteed by a member.19,060,000 Notes payable, National Bank of Arizona, payable in monthly installments totaling $14,431, including interest at 5.75%, through July 2019, cross-collateralized by substantially all of the assets of the Company and guaranteed by a member. In addition, four members have pledged their equity interest in the Company as collateral for the loans.111,708 Notes payable, National Bank of Arizona, payable in monthly installments totaling $57,967, including interest at 5.75%. The notes mature at various dates through December 2020, cross-collateralized by substantially all of the assets of the Company and guaranteed by a member. In addition, four members have pledged their equity interest in the Company as collateral for the loans.1,135,525 Notes payable, National Bank of Arizona, payable in monthly installments totaling $89,981, including interest at 5.75%. The notes mature at various dates through March 2022, cross-collateralized by substantially all of the assets of the Company and guaranteed by a member. In addition, four members have pledged their equity interest in the Company as collateral for the loans.2,710,720 Notes payable, National Bank of Arizona, payable in monthly installments totaling $64,463, including interest at 5.75%. The notes mature at various dates through June 2023, cross-collateralized by substantially all of the assets of the Company and guaranteed by a member. In addition, four members have pledged their equity interest in the Company as collateral for the loans.2,715,298

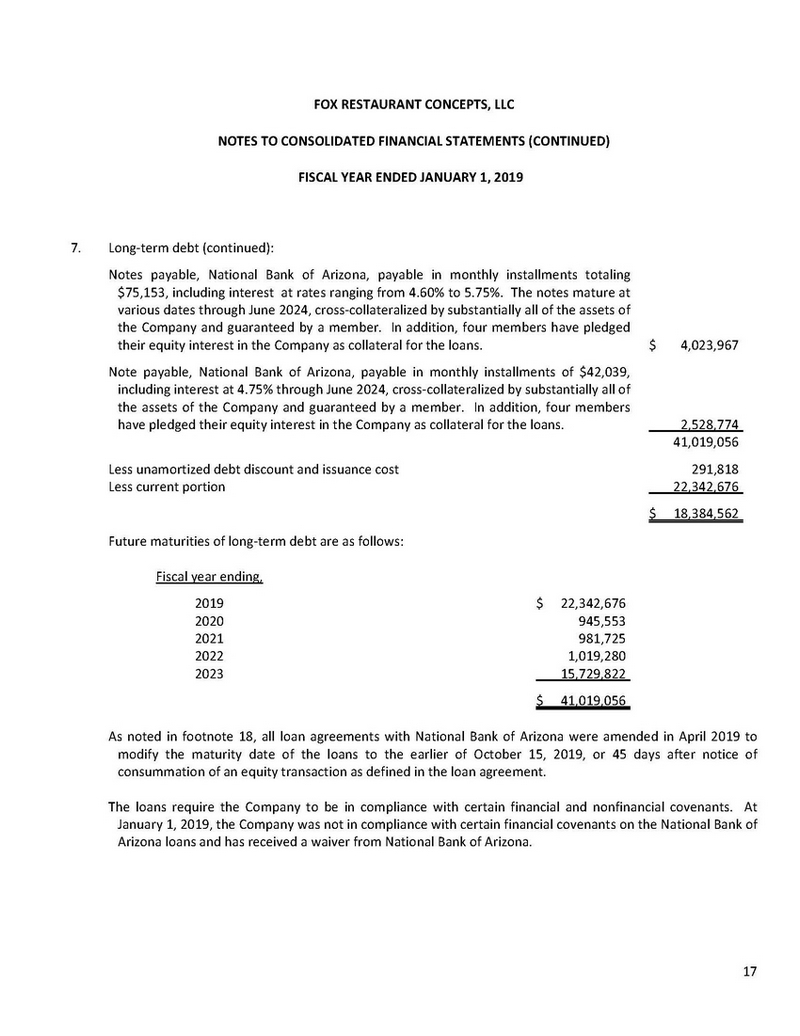

Long-term debt (continued): Notes payable, National Bank of Arizona, payable in monthly installments totaling $75,153, including interest at rates ranging from 4.60% to 5.75%. The notes mature at various dates through June 2024, cross-collateralized by substantially all of the assets of the Company and guaranteed by a member. In addition, four members have pledged their equity interest in the Company as collateral for the loans.$4,023,967 Note payable, National Bank of Arizona, payable in monthly installments of $42,039, including interest at 4.75% through June 2024, cross-collateralized by substantially all of the assets of the Company and guaranteed by a member. In addition, four members As noted in footnote 18, all loan agreements with National Bank of Arizona were amended in April 2019 to modify the maturity date of the loans to the earlier of October 15, 2019, or 45 days after notice of consummation of an equity transaction as defined in the loan agreement. The loans require the Company to be in compliance with certain financial and nonfinancial covenants. At January 1, 2019, the Company was not in compliance with certain financial covenants on the National Bank of Arizona loans and has received a waiver from National Bank of Arizona.

Long-term debt (continued): Notes payable, National Bank of Arizona, payable in monthly installments totaling $75,153, including interest at rates ranging from 4.60% to 5.75%. The notes mature at various dates through June 2024, cross-collateralized by substantially all of the assets of the Company and guaranteed by a member. In addition, four members have pledged their equity interest in the Company as collateral for the loans.$4,023,967 Note payable, National Bank of Arizona, payable in monthly installments of $42,039, including interest at 4.75% through June 2024, cross-collateralized by substantially all of the assets of the Company and guaranteed by a member. In addition, four members As noted in footnote 18, all loan agreements with National Bank of Arizona were amended in April 2019 to modify the maturity date of the loans to the earlier of October 15, 2019, or 45 days after notice of consummation of an equity transaction as defined in the loan agreement. The loans require the Company to be in compliance with certain financial and nonfinancial covenants. At January 1, 2019, the Company was not in compliance with certain financial covenants on the National Bank of Arizona loans and has received a waiver from National Bank of Arizona.

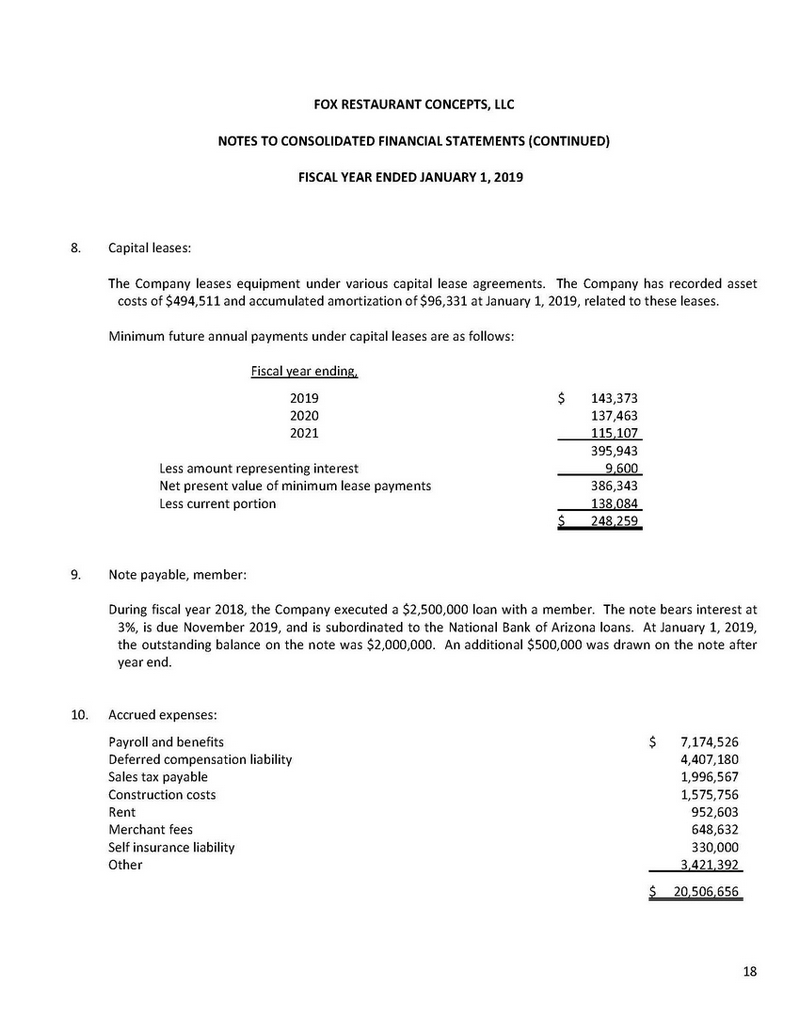

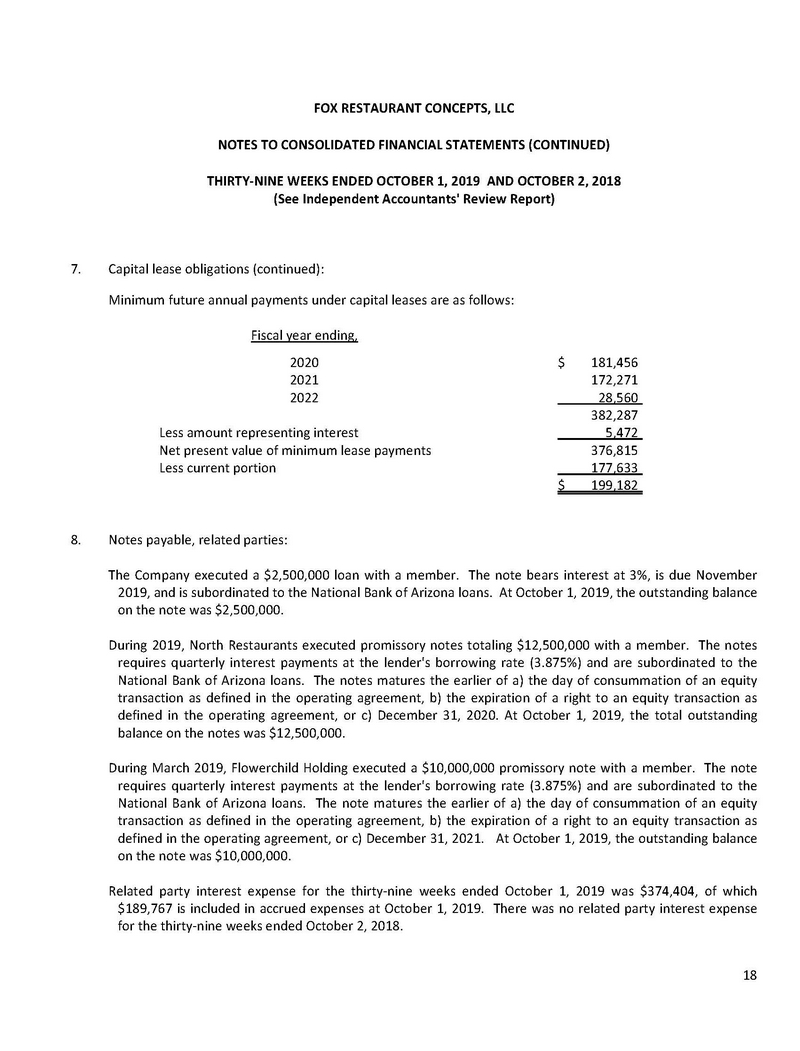

Capital leases: The Company leases equipment under various capital lease agreements. The Company has recorded asset costs of $494,511 and accumulated amortization of $96,331 at January 1, 2019, related to these leases. Minimum future annual payments under capital leases are as follows: Note payable, member: During fiscal year 2018, the Company executed a $2,500,000 loan with a member. The note bears interest at 3%, is due November 2019, and is subordinated to the National Bank of Arizona loans. At January 1, 2019, the outstanding balance on the note was $2,000,000. An additional $500,000 was drawn on the note after year end.

Capital leases: The Company leases equipment under various capital lease agreements. The Company has recorded asset costs of $494,511 and accumulated amortization of $96,331 at January 1, 2019, related to these leases. Minimum future annual payments under capital leases are as follows: Note payable, member: During fiscal year 2018, the Company executed a $2,500,000 loan with a member. The note bears interest at 3%, is due November 2019, and is subordinated to the National Bank of Arizona loans. At January 1, 2019, the outstanding balance on the note was $2,000,000. An additional $500,000 was drawn on the note after year end.

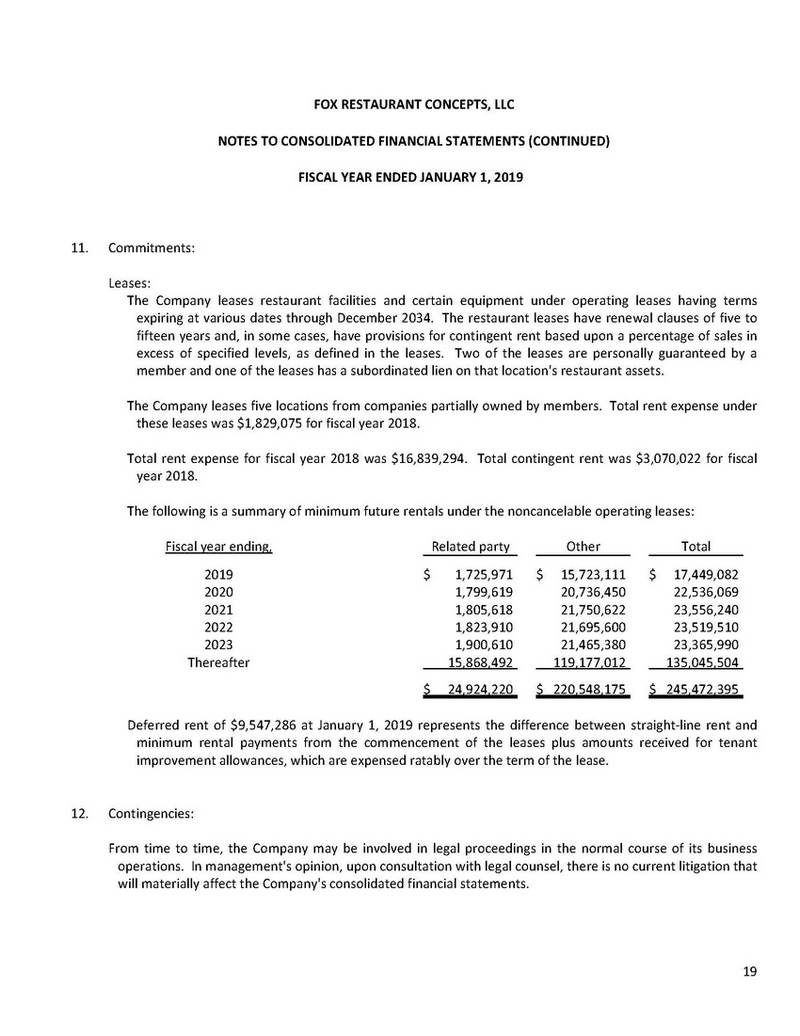

Commitments: Leases: The Company leases restaurant facilities and certain equipment under operating leases having terms expiring at various dates through December 2034. The restaurant leases have renewal clauses of five to fifteen years and, in some cases, have provisions for contingent rent based upon a percentage of sales in excess of specified levels, as defined in the leases. Two of the leases are personally guaranteed by a member and one of the leases has a subordinated lien on that location's restaurant assets. The Company leases five locations from companies partially owned by members. Total rent expense under these leases was $1,829,075 for fiscal year 2018. Total rent expense for fiscal year 2018 was $16,839,294. Total contingent rent was $3,070,022 for fiscal year 2018. The following is a summary of minimum future rentals under the noncancelable operating leases: Deferred rent of $9,547,286 at January 1, 2019 represents the difference between straight-line rent and minimum rental payments from the commencement of the leases plus amounts received for tenant improvement allowances, which are expensed ratably over the term of the lease. Contingencies: From time to time, the Company may be involved in legal proceedings in the normal course of its business operations. In management's opinion, upon consultation with legal counsel, there is no current litigation that will materially affect the Company's consolidated financial statements.

Commitments: Leases: The Company leases restaurant facilities and certain equipment under operating leases having terms expiring at various dates through December 2034. The restaurant leases have renewal clauses of five to fifteen years and, in some cases, have provisions for contingent rent based upon a percentage of sales in excess of specified levels, as defined in the leases. Two of the leases are personally guaranteed by a member and one of the leases has a subordinated lien on that location's restaurant assets. The Company leases five locations from companies partially owned by members. Total rent expense under these leases was $1,829,075 for fiscal year 2018. Total rent expense for fiscal year 2018 was $16,839,294. Total contingent rent was $3,070,022 for fiscal year 2018. The following is a summary of minimum future rentals under the noncancelable operating leases: Deferred rent of $9,547,286 at January 1, 2019 represents the difference between straight-line rent and minimum rental payments from the commencement of the leases plus amounts received for tenant improvement allowances, which are expensed ratably over the term of the lease. Contingencies: From time to time, the Company may be involved in legal proceedings in the normal course of its business operations. In management's opinion, upon consultation with legal counsel, there is no current litigation that will materially affect the Company's consolidated financial statements.

Profit sharing plan: The Company maintains a 401(k) profit sharing plan for nonhighly compensated management employees who meet eligibility requirements. The employer has the option to match 50% of the employees' contributions up to 6% of pay. In 2018, the Company made matching contributions of $317,408. Deferred compensation plan: The Company maintains a nonqualified deferred compensation plan for certain employees. The plan allows eligible employees to defer a percentage of their pay and the Company has the option to make discretionary contributions to the plan. Contributions to the plan by the employees and employer are assets of the Company and the employees have the rights of an unsecured creditor in the event of bankruptcy. In fiscal year 2018, the Company made matching contributions of $188,431. At January 1, 2019, the plan assets are $4,549,738, which represent the cash surrender value of life insurance policies on the Company's majority member and mutual funds. At January 1, 2019, the plan liabilities of $4,407,180 are included with accrued expenses. Joint venture: In 2010, Fox entered into a joint venture agreement with Host International, Inc. (Host). Host has a 75% ownership in the joint venture and Fox has a 25% ownership. The agreement authorizes Host to use the names and logos of four restaurant concepts in the development and operation of one or more restaurants, snack bars or other food and beverage facilities at Phoenix Sky Harbor Airport. Fox received $100,000 to negotiate the agreement. Under the terms of the agreement, Fox received a $100,000 licensing fee per location and will receive 5% of gross sales. Fox's 25% investment will be funded by Host through Fox's cash flow from the operations. Fox recognized royalty income of $803,626 in fiscal year 2018. The Company accounts for the joint venture on the equity method of accounting. Fox's investment in Host was $0 at January 1, 2019.

Profit sharing plan: The Company maintains a 401(k) profit sharing plan for nonhighly compensated management employees who meet eligibility requirements. The employer has the option to match 50% of the employees' contributions up to 6% of pay. In 2018, the Company made matching contributions of $317,408. Deferred compensation plan: The Company maintains a nonqualified deferred compensation plan for certain employees. The plan allows eligible employees to defer a percentage of their pay and the Company has the option to make discretionary contributions to the plan. Contributions to the plan by the employees and employer are assets of the Company and the employees have the rights of an unsecured creditor in the event of bankruptcy. In fiscal year 2018, the Company made matching contributions of $188,431. At January 1, 2019, the plan assets are $4,549,738, which represent the cash surrender value of life insurance policies on the Company's majority member and mutual funds. At January 1, 2019, the plan liabilities of $4,407,180 are included with accrued expenses. Joint venture: In 2010, Fox entered into a joint venture agreement with Host International, Inc. (Host). Host has a 75% ownership in the joint venture and Fox has a 25% ownership. The agreement authorizes Host to use the names and logos of four restaurant concepts in the development and operation of one or more restaurants, snack bars or other food and beverage facilities at Phoenix Sky Harbor Airport. Fox received $100,000 to negotiate the agreement. Under the terms of the agreement, Fox received a $100,000 licensing fee per location and will receive 5% of gross sales. Fox's 25% investment will be funded by Host through Fox's cash flow from the operations. Fox recognized royalty income of $803,626 in fiscal year 2018. The Company accounts for the joint venture on the equity method of accounting. Fox's investment in Host was $0 at January 1, 2019.

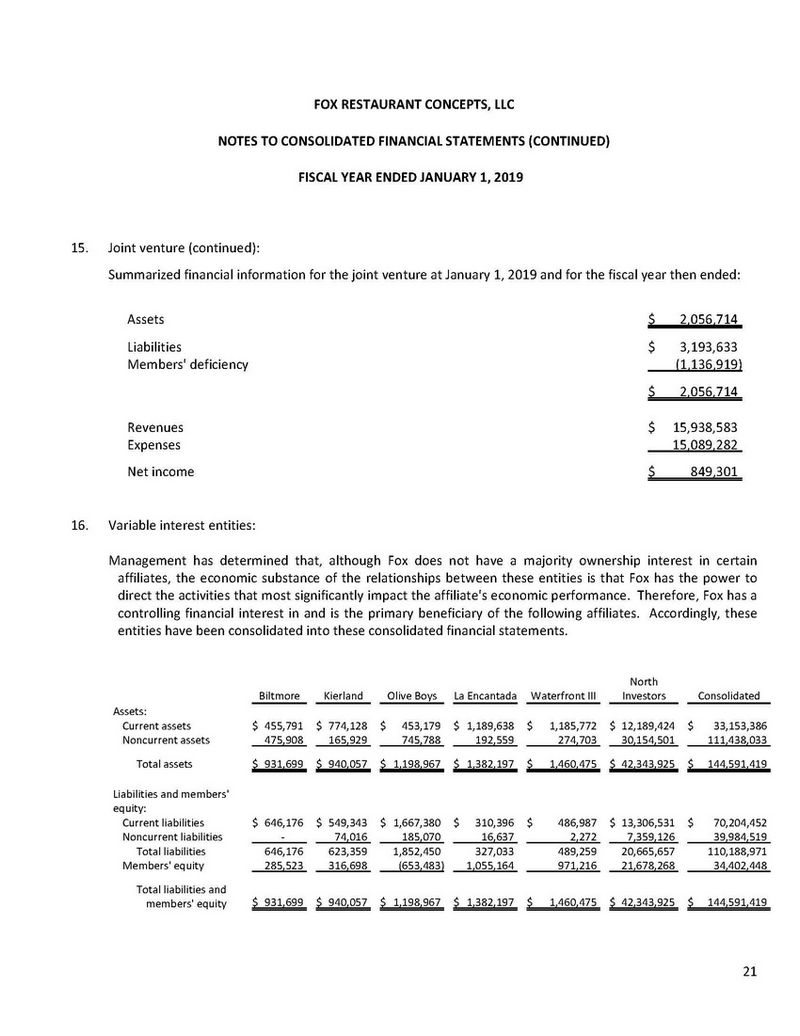

Joint venture (continued): Summarized financial information for the joint venture at January 1, 2019 and for the fiscal year then ended: Variable interest entities: Management has determined that, although Fox does not have a majority ownership interest in certain affiliates, the economic substance of the relationships between these entities is that Fox has the power to direct the activities that most significantly impact the affiliate's economic performance. Therefore, Fox has a controlling financial interest in and is the primary beneficiary of the following affiliates. Accordingly, these entities have been consolidated into these consolidated financial statements. North Biltmore Kierland Olive Boys La Encantada Waterfront III Investors Consolidated ssets: Current assets$ 455,791 $ 774,128 $453,179 $ 1,189,638 $1,185,772 $ 12,189,424 $33,153,386 Noncurrent assets 475,908 165,929 745,788 192,559 274,703 30,154,501 111,438,033 Total assets $ 931,699 $ 940,057 $ 1,198,967 $ 1,382,197 $1,460,475 $ 42,343,925 $ 144,591,419 Liabilities and members' equity:

Joint venture (continued): Summarized financial information for the joint venture at January 1, 2019 and for the fiscal year then ended: Variable interest entities: Management has determined that, although Fox does not have a majority ownership interest in certain affiliates, the economic substance of the relationships between these entities is that Fox has the power to direct the activities that most significantly impact the affiliate's economic performance. Therefore, Fox has a controlling financial interest in and is the primary beneficiary of the following affiliates. Accordingly, these entities have been consolidated into these consolidated financial statements. North Biltmore Kierland Olive Boys La Encantada Waterfront III Investors Consolidated ssets: Current assets$ 455,791 $ 774,128 $453,179 $ 1,189,638 $1,185,772 $ 12,189,424 $33,153,386 Noncurrent assets 475,908 165,929 745,788 192,559 274,703 30,154,501 111,438,033 Total assets $ 931,699 $ 940,057 $ 1,198,967 $ 1,382,197 $1,460,475 $ 42,343,925 $ 144,591,419 Liabilities and members' equity:

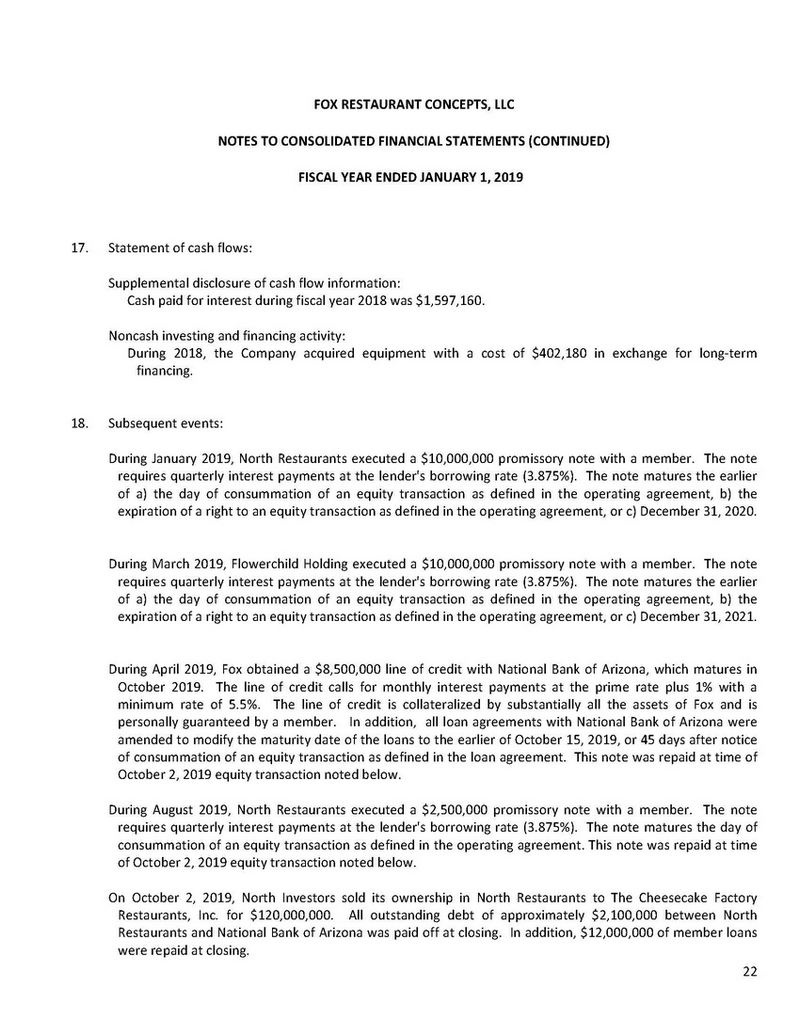

Statement of cash flows: Supplemental disclosure of cash flow information: Cash paid for interest during fiscal year 2018 was $1,597,160. Noncash investing and financing activity: During 2018, the Company acquired equipment with a cost of $402,180 in exchange for long-term financing. Subsequent events: During January 2019, North Restaurants executed a $10,000,000 promissory note with a member. The note requires quarterly interest payments at the lender's borrowing rate (3.875%). The note matures the earlier of a) the day of consummation of an equity transaction as defined in the operating agreement, b) the expiration of a right to an equity transaction as defined in the operating agreement, or c) December 31, 2020. During March 2019, Flowerchild Holding executed a $10,000,000 promissory note with a member. The note requires quarterly interest payments at the lender's borrowing rate (3.875%). The note matures the earlier of a) the day of consummation of an equity transaction as defined in the operating agreement, b) the expiration of a right to an equity transaction as defined in the operating agreement, or c) December 31, 2021. During April 2019, Fox obtained a $8,500,000 line of credit with National Bank of Arizona, which matures in October 2019. The line of credit calls for monthly interest payments at the prime rate plus 1% with a minimum rate of 5.5%. The line of credit is collateralized by substantially all the assets of Fox and is personally guaranteed by a member. In addition, all loan agreements with National Bank of Arizona were amended to modify the maturity date of the loans to the earlier of October 15, 2019, or 45 days after notice of consummation of an equity transaction as defined in the loan agreement. This note was repaid at time of October 2, 2019 equity transaction noted below. During August 2019, North Restaurants executed a $2,500,000 promissory note with a member. The note requires quarterly interest payments at the lender's borrowing rate (3.875%). The note matures the day of consummation of an equity transaction as defined in the operating agreement. This note was repaid at time of October 2, 2019 equity transaction noted below. On October 2, 2019, North Investors sold its ownership in North Restaurants to The Cheesecake Factory Restaurants, Inc. for $120,000,000. All outstanding debt of approximately $2,100,000 between North Restaurants and National Bank of Arizona was paid off at closing. In addition, $12,000,000 of member loans were repaid at closing.

Statement of cash flows: Supplemental disclosure of cash flow information: Cash paid for interest during fiscal year 2018 was $1,597,160. Noncash investing and financing activity: During 2018, the Company acquired equipment with a cost of $402,180 in exchange for long-term financing. Subsequent events: During January 2019, North Restaurants executed a $10,000,000 promissory note with a member. The note requires quarterly interest payments at the lender's borrowing rate (3.875%). The note matures the earlier of a) the day of consummation of an equity transaction as defined in the operating agreement, b) the expiration of a right to an equity transaction as defined in the operating agreement, or c) December 31, 2020. During March 2019, Flowerchild Holding executed a $10,000,000 promissory note with a member. The note requires quarterly interest payments at the lender's borrowing rate (3.875%). The note matures the earlier of a) the day of consummation of an equity transaction as defined in the operating agreement, b) the expiration of a right to an equity transaction as defined in the operating agreement, or c) December 31, 2021. During April 2019, Fox obtained a $8,500,000 line of credit with National Bank of Arizona, which matures in October 2019. The line of credit calls for monthly interest payments at the prime rate plus 1% with a minimum rate of 5.5%. The line of credit is collateralized by substantially all the assets of Fox and is personally guaranteed by a member. In addition, all loan agreements with National Bank of Arizona were amended to modify the maturity date of the loans to the earlier of October 15, 2019, or 45 days after notice of consummation of an equity transaction as defined in the loan agreement. This note was repaid at time of October 2, 2019 equity transaction noted below. During August 2019, North Restaurants executed a $2,500,000 promissory note with a member. The note requires quarterly interest payments at the lender's borrowing rate (3.875%). The note matures the day of consummation of an equity transaction as defined in the operating agreement. This note was repaid at time of October 2, 2019 equity transaction noted below. On October 2, 2019, North Investors sold its ownership in North Restaurants to The Cheesecake Factory Restaurants, Inc. for $120,000,000. All outstanding debt of approximately $2,100,000 between North Restaurants and National Bank of Arizona was paid off at closing. In addition, $12,000,000 of member loans were repaid at closing.

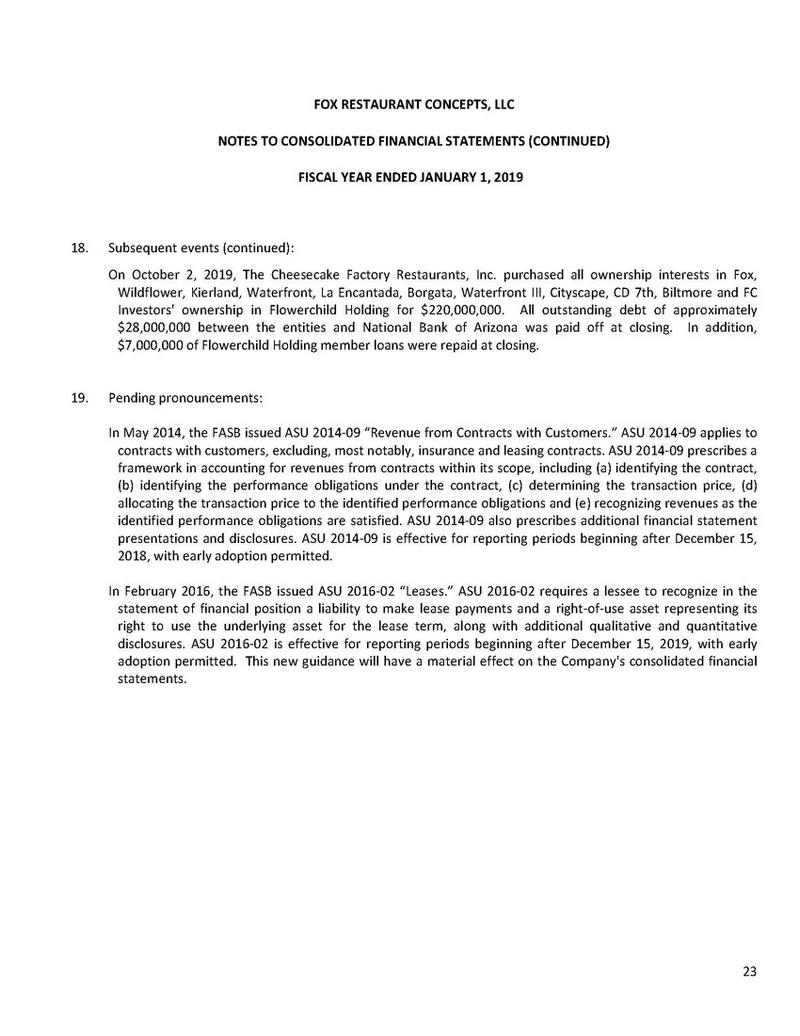

Subsequent events (continued): On October 2, 2019, The Cheesecake Factory Restaurants, Inc. purchased all ownership interests in Fox, Wildflower, Kierland, Waterfront, La Encantada, Borgata, Waterfront III, Cityscape, CD 7th, Biltmore and FC Investors' ownership in Flowerchild Holding for $220,000,000. All outstanding debt of approximately $28,000,000 between the entities and National Bank of Arizona was paid off at closing. In addition, $7,000,000 of Flowerchild Holding member loans were repaid at closing. Pending pronouncements: In May 2014, the FASB issued ASU 2014-09 “Revenue from Contracts with Customers.” ASU 2014-09 applies to contracts with customers, excluding, most notably, insurance and leasing contracts. ASU 2014-09 prescribes a framework in accounting for revenues from contracts within its scope, including (a) identifying the contract, (b) identifying the performance obligations under the contract, (c) determining the transaction price, (d) allocating the transaction price to the identified performance obligations and (e) recognizing revenues as the identified performance obligations are satisfied. ASU 2014-09 also prescribes additional financial statement presentations and disclosures. ASU 2014-09 is effective for reporting periods beginning after December 15, 2018, with early adoption permitted. In February 2016, the FASB issued ASU 2016-02 “Leases.” ASU 2016-02 requires a lessee to recognize in the statement of financial position a liability to make lease payments and a right-of-use asset representing its right to use the underlying asset for the lease term, along with additional qualitative and quantitative disclosures. ASU 2016-02 is effective for reporting periods beginning after December 15, 2019, with early adoption permitted. This new guidance will have a material effect on the Company's consolidated financial statements.