Exhibit 99.1

Annual Information Form

February 25, 2019

2018 Annual Information Form

Table of Contents

| Nomenclature |

1 | |||

| Cautionary Statement on Forward-Looking Information |

1 | |||

| Glossary of Technical Terms |

7 | |||

| Corporate Structure |

9 | |||

| Name, Address and Incorporation |

9 | |||

| Intercorporate Relationships |

10 | |||

| General Development of the Business |

12 | |||

| Three-Year History |

12 | |||

| 2016 |

12 | |||

| 2017 |

12 | |||

| 2018 |

14 | |||

| Description of the Business |

16 | |||

| General |

16 | |||

| Product Summary |

17 | |||

| Steelmaking Coal |

17 | |||

| Copper |

18 | |||

| Zinc |

19 | |||

| Energy |

20 | |||

| Individual Operations |

21 | |||

| Steelmaking Coal |

21 | |||

| Copper |

30 | |||

| Zinc |

45 | |||

| Energy |

50 | |||

| Exploration |

53 | |||

| Corporate |

53 | |||

| Mineral Reserves and Resources |

54 | |||

| Definitions for Mineral Reserves and Mineral Resources |

61 | |||

| Comments on Individual Operations |

63 | |||

| Risks and Uncertainties |

67 | |||

| Qualified Persons |

68 | |||

| Oil and Gas Reserves |

68 | |||

| Health and Safety and Environmental Protection |

77 | |||

| Social and Environmental Policies |

80 | |||

| Human Resources |

81 | |||

| Technology |

81 | |||

| Foreign Operations |

82 | |||

| Competitive Conditions |

82 | |||

| Risk Factors |

83 | |||

| Dividends |

101 | |||

| Description of Capital Structure |

101 | |||

| General Description of Capital Structure |

101 | |||

|

Teck Resources Limited |

Page i |

2018 Annual Information Form

| Ratings |

106 | |||

| Market for Securities |

108 | |||

| Trading Price and Volume |

108 | |||

| Directors and Officers |

109 | |||

| Directors |

109 | |||

| Officers |

110 | |||

| Audit Committee Information |

113 | |||

| Composition of the Audit Committee |

113 | |||

| Pre-Approval Policies and Procedures |

114 | |||

| Auditor’s Fees |

114 | |||

| Ownership by Directors and Officers and Interests in Material Transactions |

115 | |||

| Legal Proceedings and Regulatory Actions |

115 | |||

| Transfer Agents and Registrars |

118 | |||

| Material Contracts |

118 | |||

| Interests of Experts |

118 | |||

| Disclosure Pursuant to the Requirements of the New York Stock Exchange |

120 | |||

| Non-GAAP Measures |

120 | |||

| Additional Information |

121 | |||

| Schedule A – Audit Committee Charter |

A-1 | |||

| Schedule B – Report of Management and Directors on Reserves Data and Other Information |

B-1 | |||

| Schedule C – Report on Reserves Data by Independent Qualified Reserves Evaluator or Auditor |

C-1 | |||

| Schedule D – List of Technical Reports |

D-1 | |||

|

Teck Resources Limited |

Page ii |

2018 Annual Information Form

Nomenclature

In this Annual Information Form, unless the context otherwise dictates, “we”, “Teck” or the “Company” refers to Teck Resources Limited and its subsidiaries.

Cautionary Statement on Forward-Looking Information

This Annual Information Form contains certain forward-looking information and forward-looking statements as defined in applicable securities laws (collectively referred to as forward-looking statements). These statements relate to future events or our future performance. All statements other than statements of historical fact are forward-looking statements. The use of any of the words “anticipate”, “plan”, “continue”, “estimate”, “expect”, “may”, “will”, “project”, “predict”, “potential”, “should”, “believe” and similar expressions is intended to identify forward-looking statements. These statements involve known and unknown risks, uncertainties and other factors that may cause actual results or events to differ materially from those anticipated in such forward-looking statements. These statements speak only as of the date of this Annual Information Form. These forward-looking statements include, but are not limited to, statements concerning:

| ∎ | forecast production; |

| ∎ | forecast operating costs and capital costs; |

| ∎ | sales forecasts; |

| ∎ | our strategies and objectives; |

| ∎ | future prices and price volatility for steelmaking coal, copper, zinc, blended bitumen and other products and commodities that we produce and sell, as well as oil, natural gas and petroleum products; |

| ∎ | the demand for and supply of steelmaking coal, copper, zinc, blended bitumen and other products and commodities that we produce and sell; |

| ∎ | expected receipt of regulatory approvals, and the expected timing thereof; |

| ∎ | expected receipt or completion of prefeasibility studies, feasibility studies and other studies and the expected timing thereof; |

| ∎ | proposed or expected changes in regulatory frameworks; |

| ∎ | our interest and other expenses; |

| ∎ | our tax position and the tax rates applicable to us; |

| ∎ | the adequacy of our logistics arrangements related to Fort Hills; |

| ∎ | curtailment measures imposed by the Government of Alberta and their impact on Fort Hills; |

| ∎ | the timing and costs of construction and production with respect to, and the issuance of the necessary permits and other authorizations required for, certain of our development and expansion projects, including, among others, the Quebrada Blanca Phase 2 (QB2) project, the NuevaUnión copper project, the Frontier project and our Project Satellite projects; |

|

Teck Resources Limited |

Page 1 |

2018 Annual Information Form

| ∎ | expected mine lives and the possibility of extending mine lives; |

| ∎ | the closure of our Coal Mountain operations, including our expectation to continue to capture latent processing capacity by hauling a portion of the raw coal from Elkview to Coal Mountain for processing; |

| ∎ | our estimates of the quantity and quality of our mineral and oil reserves and resources; |

| ∎ | the production capacity, planned production levels and future production of our operations; |

| ∎ | availability of transportation for our products from our operations to our customers, including our participation in the crude-by-rail initiative; |

| ∎ | availability of any of our credit facilities; |

| ∎ | financial assurance requirements related to our projects and related agreements; |

| ∎ | potential impact of transportation, port, pipeline and other potential production disruptions; |

| ∎ | our planned capital expenditures and capital spending and timing for completion of our capital projects; |

| ∎ | our estimates of reclamation and other costs related to environmental protection; |

| ∎ | our future capital and mine production costs, including the costs and potential impact of complying with existing and proposed environmental laws and regulations in the operation and closure of various operations; |

| ∎ | the costs, steps and potential impact of managing water quality at our coal operations, including but not limited to the statements under “Description of the Business — Individual Operations — Steelmaking Coal — Elk Valley Water Management” including our expectations regarding timing and costs of active water treatment, capital spending guidance, the potential for saturated rock fills to reduce capital and operating costs associated with active water treatment, the regulatory process relating to active water treatment and estimates of our long-term costs of water management; |

| ∎ | our expectations regarding the increase in the royalty paid by POSCAN in respect of our Greenhills property; |

| ∎ | our expectation that we can upgrade Neptune Bulk Terminals’ operational capacity; |

| ∎ | our expectations regarding the regulatory application for Frontier and timelines for productions at Frontier; |

| ∎ | anticipated benefits, timing and cost of our ball mill project at Highland Valley; |

| ∎ | timing of the closing of the QB2 transaction and our expectation that the transaction will close; |

| ∎ | expectations regarding the QB 2 project, including expectations regarding financing, capacity, mine life, regulatory approvals, projected expenditures and timing of any development decision in respect thereof; |

| ∎ | expected spending and activities at our Project Satellite properties; |

|

Teck Resources Limited |

Page 2 |

2018 Annual Information Form

| ∎ | anticipated benefits, timing and costs of the Red Dog mill upgrade projects; |

| ∎ | our financial and operating objectives; |

| ∎ | our exploration, environmental, community, health and safety initiatives; |

| ∎ | the outcome of legal and regulatory proceedings and other disputes in which we are involved; |

| ∎ | the outcome of our coal sales negotiations and negotiations with metals and concentrate customers concerning treatment charges, price adjustments and premiums; |

| ∎ | our dividend policy; and |

| ∎ | general business and economic conditions. |

Canadian disclosure rules require us to present projected capital and projected operating costs for each of our material mining operations. The amounts presented for each operation are estimates, based on current mine plans and assumptions believed to be reasonable, including assumptions with respect to energy and labour costs and the Canadian/U.S. dollar exchange rate. Future capital expenditures are based on management’s best estimate of expected future capital requirements for the extraction and processing of existing reserves and resources. Cash operating costs are not a measure recognized under International Financial Reporting Standards in Canada or generally accepted accounting principles in the United States. Various factors will cause actual results to vary from the projected operating and capital costs set out below. Our disclosed cash operating costs do not include transportation costs or royalties, and may not be comparable to similar measures reported by other issuers.

Inherent in forward-looking statements are risks and uncertainties beyond our ability to predict or control, including risks that may affect our operating or capital plans; risks generally encountered in the permitting and development of mineral and oil and gas properties such as unusual or unexpected geological formations, unanticipated metallurgical difficulties, delays associated with permit appeals or other regulatory processes, ground control problems, adverse weather conditions, process upsets and equipment malfunctions; risks associated with the Canadian Corruption of Foreign Public Officials Act and similar worldwide bribery laws; risks associated with labour disturbances and availability of skilled labour; risks associated with fluctuations in the market prices of our principal commodities, which are cyclical and subject to substantial price fluctuations; risks associated with changes to the tax and royalty regimes in which we operate; risks created through competition for mining and oil and gas properties; risks associated with lack of access to markets; risks associated with mineral and oil and gas reserve estimates; risks posed by fluctuations in exchange rates and interest rates, as well as general economic conditions; risks associated with access to capital; risks associated with changes to our credit ratings; risks associated with our material financing arrangements and our covenants thereunder; risks associated with climate change, environmental compliance, changes in environmental legislation and regulation and changes to our reclamation obligations; risks associated with our dependence on third parties for the provision of transportation, port, pipeline. and other critical services; risks associated with non-performance by contractual counterparties; risks associated with potential disputes with partners and co-owners; risks associated with Aboriginal title claims and other title risks; social and political risks associated with operations in foreign countries; risks associated with the preparation of our financial statements; risks related to trade barriers or

|

Teck Resources Limited |

Page 3 |

2018 Annual Information Form

import restrictions; risks of changes in tax laws or their interpretation; and risks associated with tax reassessments and legal proceedings. The amount and timing of actual capital expenditures is dependent upon, among other matters, being able to secure permits, equipment, supplies, materials and labour on a timely basis and at expected costs to enable the related capital project to be completed as currently anticipated. Fort Hills is not controlled by us and production schedules may be adjusted by our partners. Certain of our other operations and projects are operated through joint arrangements where we may not have control over all decisions, which may cause outcomes to differ from current expectations. Further factors associated with our Elk Valley Water Quality Plan are discussed under the heading “Description of the Business — Individual Operations — Steelmaking Coal — Elk Valley Water Management”. Declaration and payment of dividends is at the discretion of the Board, and our dividend policy will be reviewed regularly and may change. Closing of the QB2 transaction depends on certain regulatory approvals; if all required approvals are not received in a timely manner, the timing and ability to close will be jeopardized.

Actual results and developments are likely to differ, and may differ materially, from those expressed or implied by the forward-looking statements contained in this Annual Information Form. Such statements are based on a number of assumptions that may prove to be incorrect, including, but not limited to, assumptions about:

| ∎ | general business and economic conditions; |

| ∎ | interest rates; |

| ∎ | commodity and power prices; |

| ∎ | acts of foreign or domestic governments and the outcome of legal proceedings; |

| ∎ | the supply and demand for, deliveries of, and the level and volatility of prices of copper, coal, zinc and blended bitumen and our other metals and minerals, as well as oil, natural gas and other petroleum products; |

| ∎ | the timing of the receipt of permits and other regulatory and governmental approvals for our development projects and other operations, including mine extensions; |

| ∎ | our costs of production and our production and productivity levels, as well as those of our competitors; |

| ∎ | our ability to secure adequate transportation, pipeline and port services for our products; |

| ∎ | changes in credit market conditions and conditions in financial markets generally; |

| ∎ | the availability of funding to refinance our borrowings as they become due or to finance our development projects on reasonable terms; |

| ∎ | our ability to procure equipment and operating supplies in sufficient quantities and on a timely basis; |

| ∎ | the availability of qualified employees and contractors for our operations, including our new developments; |

| ∎ | our ability to attract and retain skilled staff; |

| ∎ | the satisfactory negotiation of collective agreements with unionized employees; |

|

Teck Resources Limited |

Page 4 |

2018 Annual Information Form

| ∎ | the impact of changes in Canadian-U.S. dollar and other foreign exchange rates on our costs and results; |

| ∎ | engineering and construction timetables and capital costs for our development and expansion projects; |

| ∎ | costs of closure, and environmental compliance costs generally, of operations; |

| ∎ | market competition; |

| ∎ | the accuracy of our reserve and resource estimates (including, with respect to size, grade and recoverability) and the geological, operational and price assumptions on which these are based; |

| ∎ | tax benefits and tax rates; |

| ∎ | the outcome of our coal price and volume negotiations with customers; |

| ∎ | the outcome of our copper, zinc and lead concentrate treatment and refining charge negotiations with customers; |

| ∎ | the market price for our blended bitumen; |

| ∎ | curtailment measures on oil production taken by the Government of Alberta; |

| ∎ | the resolution of environmental and other proceedings or disputes; |

| ∎ | the future supply of low-cost power to the Trail smelting and refining complex; |

| ∎ | our ability to obtain, comply with and renew permits in a timely manner; and |

| ∎ | our ongoing relations with our employees and with our business and joint venture partners. |

In addition, assumptions regarding the Elk Valley Water Quality Plan include assumptions that additional treatment will be effective at scale, and that the technology and facilities operate as expected, as well as additional assumptions discussed under the heading “Description of the Business — Individual Operations — Steelmaking Coal — Elk Valley Water Management”. Expectations regarding QB2 are based on current project assumptions and the final feasibility study. Expectations regarding Fort Hills are based on assumptions regarding the performance of the plant and other facilities at Fort Hills, and the operation of the project. Statements regarding the availability of our credit facilities are based on assumptions that we will be able to satisfy the conditions for borrowing at the time of a borrowing request and that the credit facilities are not otherwise terminated or accelerated due to an event of default. Assumptions relating to our expectations for the closing of the QB2 transaction, include that all regulatory approvals will be obtained in a timely manner.

We caution you that the foregoing list of important factors and assumptions is not exhaustive. Other events or circumstances could cause our actual results to differ materially from those estimated or projected and expressed in, or implied by, our forward-looking statements. You should also carefully consider the matters discussed under “Risk Factors” in this Annual Information Form and in our “Cautionary Statement on Forward-Looking Information” section of our Management’s Discussion and Analysis for the year ended December 31, 2018, and subsequent filings, that can be found under our profile on SEDAR (www.sedar.com) and on

|

Teck Resources Limited |

Page 5 |

2018 Annual Information Form

EDGAR (www.sec.gov). Except as required by law, we undertake no obligation to update publicly or otherwise revise any forward-looking statements or the foregoing list of factors, whether as a result of new information or future events or otherwise.

Cautionary Note to U.S. Investors Concerning Estimates of Measured, Indicated and Inferred Mineral Resources and Oil and Gas Reserves

This Annual Information Form has been prepared in accordance with the requirements of the securities laws in effect in Canada, which differ from the requirements of U.S. securities laws.

In this Annual Information Form we use the term “mineral resources” and its subcategories “measured”, “indicated”, and “inferred” mineral resources. Readers are advised that, while such terms are required by Canadian regulations, the U.S. Securities and Exchange Commission (SEC) does not currently require U.S. mining companies in their filings with the SEC to disclose estimates of mineral resources. Investors are cautioned not to assume that any part or all of the mineral resources in these categories will ever be converted into reserves. “Inferred mineral resources” have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. Under Canadian rules, issuers must not make any disclosure of results of an economic evaluation that includes inferred mineral resources, except in very limited cases. Investors are cautioned not to assume that part or all of an inferred mineral resource exists, or is, or will be, economically or legally mineable.

Canadian standards of oil and gas disclosure also differ significantly from the requirements of the SEC, and oil and gas reserve and resource information contained in this Annual Information Form may not be comparable to similar information disclosed by U.S. companies. The oil and gas reserves estimates in this Annual Information Form have been prepared in accordance with National Instrument 51-101 — Standards of Disclosure for Oil and Gas Activities, which has been adopted by securities regulatory authorities in Canada and imposes oil and gas disclosure standards for Canadian public issuers engaged in oil and gas activities and differs from the oil and gas disclosure standards of the SEC under Subpart 1200 of Regulation S-K. The SEC definitions of proved and probable reserves are different than the definitions contained in National Instrument 51-101. Therefore, proved and probable reserves disclosed in, or in the documents incorporated by reference into, this Annual Information Form in compliance with National Instrument 51-101 may not be comparable to those disclosed by U.S. companies.

|

Teck Resources Limited |

Page 6 |

2018 Annual Information Form

Glossary of Technical Terms

bitumen: a naturally occurring heavy viscous crude oil.

blended bitumen: bitumen blended with diluent to reduce its viscosity, such that the combined product can be easily pumped through a pipeline and placed in storage facilities.

cathode: an electrode in an electrolytic cell where electrons enter and which represents the final product of an electrolytic metal refining process.

clean coal: coal that has been processed to separate impurities and is in a form suitable for sale.

coking coal: coal possessing physical and chemical characteristics that facilitate the conversion into coke, which is used in the steelmaking process. Coking coal may also be referred to as metallurgical coal.

concentrate: a product containing valuable minerals from which most of the waste rock in the ore has been eliminated in a mill or concentrator.

crude oil: unrefined liquid hydrocarbons, excluding natural gas liquids.

dump leach: a process that involves dissolving and recovering minerals from typically lower-grade uncrushed ore from a mine dump.

flotation: a method of mineral separation in which a variety of reagents facilitate the attachment of certain minerals on to the surface of a froth while other minerals sink, thus effecting the separation of valuable minerals from non-valuable minerals.

grade: the classification of an ore according to its content of economically valuable material, expressed as grams per tonne for precious metals and as a percentage for most other metals.

hard coking coal: a type of coking coal used primarily for making high-strength coke for use in integrated steel mills.

heap leach: a process whereby metals are leached from a heap of crushed ore by leaching solutions seeping through the heap into a container or liner beneath the heap.

hypogene: primary sulphide ore located beneath shallow zones of ore affected by weathering processes.

LME: London Metals Exchange.

mill: a plant in which ore is ground to reduce particle size and physically liberating valuable from non-valuable minerals.

MMbbl: million barrels.

oil sands: sand and rock material that contains bitumen.

ore: naturally occurring material from which minerals of economic value can be extracted at a reasonable profit.

|

Teck Resources Limited |

Page 7 |

2018 Annual Information Form

orebody: a contiguous, well-defined mass of material of sufficient ore content to make extraction economically feasible.

pulverized coal injection (PCI) coal: coal that is pulverized and injected into a blast furnace. Those grades of coal used in the PCI process are generally non-coking. PCI grade coal is used primarily as a heat source in the steelmaking process in partial replacement for high-quality coking coals, which are typically more expensive.

semi-autogenous grinding (SAG): a method of grinding rock in which particle size reduction is achieved through tumbling action of a rotating grinding mill that primarily utilizes the contact of rock-on-rock supplemented with steel grinding balls to breakdown particles.

slag: a substance formed by way of chemical action and fusion at furnace operating temperatures; a by-product of the smelting process.

smelter: a plant in which concentrates are processed into an upgraded product by application of heat.

steelmaking coal: the various grades of coal that are used in the steelmaking process, including both coals to produce coke and coals that are pulverized for injection into the blast furnace as a fuel.

sulphide: a mineral compound containing sulphur but no oxygen.

supergene: near-surface ore that has been subject to secondary enrichment by weathering.

SX-EW: an abbreviation for solvent extraction-electrowinning, a hydrometallurgical process to produce cathode copper from leached copper ores.

tailings: the slurry that remains after selected minerals have been removed from the ore during processing.

thermal coal: coal that is used primarily for its heating value. Thermal coals tend not to have the carbonization properties possessed by coking coals. Most thermal coal is used to produce electricity in thermal power plants.

treatment and refining charges: the charge a mine pays to a smelter as a fee for conversion of concentrates into refined metal.

|

Teck Resources Limited |

Page 8 |

2018 Annual Information Form

Corporate Structure

Name, Address and Incorporation

Teck Resources Limited was continued under the Canada Business Corporations Act in 1978. It is the continuing company resulting from the merger in 1963 of the interests of The Teck-Hughes Gold Mines Ltd., Lamaque Gold Mines Limited and Canadian Devonian Petroleum Ltd., companies incorporated in 1913, 1937 and 1951, respectively. Over the years, several other reorganizations have been undertaken. These include our merger with Brameda Resources Limited and The Yukon Consolidated Gold Corporation in 1979, the merger with Highmont Mining Corporation and Iso Mines Limited in 1979, the consolidation with Afton Mines Ltd. in 1981, the merger with Copperfields Mining Corporation in 1983, and the acquisition of 100% of Cominco Ltd. in 2001. On July 23, 2001, Cominco Ltd. changed its name to Teck Cominco Metals Ltd. and on September 12, 2001, we changed our name to Teck Cominco Limited. On January 1, 2008, we amalgamated with our wholly owned subsidiary, Aur Resources Inc., by way of vertical short-form amalgamation under the name Teck Cominco Limited. On April 23, 2009, we changed our name to Teck Resources Limited from Teck Cominco Limited. On June 1, 2009 Teck Cominco Metals Ltd. changed its name to Teck Metals Ltd.

Since 1978, the Articles of Teck have been amended on several occasions to provide for various series of preferred shares and for other corporate purposes. On January 19, 1988, our Articles were amended to provide for the subdivision of our Class A common shares and Class B subordinate voting shares on a two-for-one basis. On September 12, 2001, the Articles were amended to effect the name change to Teck Cominco Limited and to convert each outstanding Class A common share into one new Class A common share and 0.2 Class B subordinate voting shares and to enact “coattail” provisions for the benefit of the Class B subordinate voting shares. Effective May 7, 2007, our Articles were amended to subdivide our Class A common shares and Class B subordinate voting shares on a two-for-one basis. See “Description of Capital Structure” below for a description of the attributes of the Class A common shares and Class B subordinate voting shares. On April 23, 2009, our Articles were amended to effect the name change to Teck Resources Limited as described above.

The registered and principal offices of Teck are located at Suite 3300, 550 Burrard Street, Vancouver, British Columbia, V6C 0B3.

|

Teck Resources Limited |

Page 9 |

2018 Annual Information Form

Intercorporate Relationships

Our financial statements consolidate the accounts of all of our subsidiaries. Our material subsidiaries as at December 31, 2018 are listed below. Unless otherwise indicated, all subsidiaries listed below are wholly owned by Teck. Indentation indicates that the majority of the voting securities of the relevant subsidiary are held by the subsidiary listed immediately above.

| Company Name |

Jurisdiction of Organization or Formation

| |

| Teck South American Holdings Ltd. |

Canada | |

| Teck Chilean Holdings Ltd. |

Canada | |

| Teck Resources Chile Limitada |

Chile | |

| Teck Base Metals Ltd. |

Canada | |

| Teck Metals Ltd. | Canada | |

| Teck Resources Coal Partnership |

British Columbia | |

| Fording Partnership |

Alberta | |

| Teck Coal Partnership |

Alberta | |

| Elkview Mine Limited Partnership(1) |

Alberta | |

| Teck Highland Valley Copper Partnership |

British Columbia | |

| TCL U.S. Holdings Ltd. |

Canada | |

| TCAI Incorporated |

Washington, U.S.A. | |

| Teck American Incorporated |

Washington, U.S.A. | |

| Teck Alaska Incorporated |

Alaska, U.S.A. | |

(1) 95% held, directly or indirectly, by Teck

In addition to the above, we own, directly or indirectly:

| · | a 21.3% limited partnership interest in Fort Hills Energy Limited Partnership; |

| · | a 90% indirect share interest in Compañía Minera Teck Quebrada Blanca S.A. This is expected to decrease to 60% upon closing of the transaction with Sumitomo Metal Mining Co., Ltd. and Sumitomo Corporation – See “Description of the Business – Copper – Quebrada Blanca Mine, Chile (Copper)” for further information; |

| · | a 90% share interest in Compañía Minera Teck Carmen de Andacollo S.A.; and |

| · | a 22.5% indirect share interest in Compañía Minera Antamina S.A., which owns the Antamina copper and zinc mine in Peru. |

|

Teck Resources Limited |

Page 10 |

2018 Annual Information Form

The following chart sets out the relationships among our material subsidiaries as at December 31, 2018. Certain aspects of the ownership structure have been simplified.

|

Teck Resources Limited |

Page 11 |

2018 Annual Information Form

General Development of the Business

Three-Year History

2016

In 2016, average annual prices for our principal products increased compared to 2015, except for copper. Annual average prices in 2016 for copper and zinc were US$2.21 and US$0.95 per pound, respectively, compared with US$2.49 and US$0.87 per pound in 2015. Average realized coal prices increased from US$93 per tonne in 2015 to US$115 per tonne in 2016, due primarily to dramatic price increases in the second half of the year.

Work advanced on a number of projects through 2016. Construction of our Fort Hills oils sands project advanced through the year and was approximately 76% complete by year-end. See “Description of the Business — Energy” for a discussion of the project. We submitted a Social and Environmental Impact Assessment for our Quebrada Blanca Phase 2 Project in September 2016 and the updated feasibility study for the project was completed in the first quarter of 2017. We also announced an agreement to increase our interest in the Zafranal project in November, through the public acquisition of AQM Copper Inc., one of our partners on the project. This acquisition was completed in January 2017.

During the year we undertook a number of transactions that supported our liquidity and strengthened our financial position. In June, we issued US$1.25 billion in aggregate principal amount of senior unsecured notes maturing in 2021 and 2024, and used the proceeds to repurchase, under a tender offer, notes maturing in 2017, 2018 and 2019, reducing near-term maturities. In September and early October we repurchased an additional US$759 million face value of debt in market transactions. We also extended the maturity of US$1.14 billion of our US$1.2 billion revolving credit facility from June 2017 to June 2019. See “General Description of Capital Structure — Credit Facilities and Debt Securities” for further details of our credit facilities and debt securities.

Notwithstanding improving commodity prices, we continued to implement our cost reduction program through 2016 and were generally able to maintain or increase production and achieve significant reductions of cash unit costs across our operations during the year. Our cash and cash equivalents as at December 31, 2016 were $1.4 billion against total debt of $8.3 billion, with the decrease in our reported total debt mainly resulting from the repurchases described above.

2017

In 2017, average annual prices for our principal products increased compared to 2016. Annual average prices in 2017 for steelmaking coal, copper and zinc were US$174 per tonne, US$2.80 and US$1.31 per pound, respectively, compared with US$115 per tonne, and US$2.21 and US$0.95 per pound in 2016.

During the year we announced a new dividend policy, completed and announced a number of dispositions of non-core assets, acquired further interests in a number of our projects and advanced various initiatives and projects intended to strengthen our financial position and our core business.

|

Teck Resources Limited |

Page 12 |

2018 Annual Information Form

In April we announced a new dividend policy and the doubling of our annualized base dividend to $0.20 per share, which was declared at $0.05 per quarter. See “Dividends” below for a further discussion of our dividend policy. We also announced a normal course issuer bid, which allowed us to purchase up to 20 million Class B subordinate voting shares through to September 2018. In December, we paid a dividend of $0.45 per share consisting of a supplemental dividend of $0.40 per share and our regular base quarterly dividend of $0.05 per share, which totalled approximately $260 million. In addition, taking into account our strong cash position, we also announced our intention to apply an additional $230 million to the repurchase of shares through March 31, 2018, of which 5.9 million Class B subordinate voting shares for $175 million were repurchased in the fourth quarter.

In May we announced the sale of our two-thirds interest in the Waneta Dam and related transmission assets to Fortis Inc. for $1.2 billion cash. BC Hydro subsequently exercised its right of first offer over the assets, and the sale of the Waneta Dam and associated assets to BC Hydro closed in July 2018. We also completed the sale of our 49% interest in the Wintering Hills wind power facility in 2017, for proceeds of $59 million.

Acquisitions during the year included the closing of our purchase of AQM Copper Inc., which held an indirect 30% interest in our Zafranal copper-gold project located in Peru, and the acquisition of the minority 21% interest in our San Nicolás copper-zinc project located in Mexico. Zafranal and San Nicolás are part of our Project Satellite initiative launched in 2017, which is focused on surfacing value from substantial base metal assets in Teck’s portfolio. See “Description of the Business — Copper” for a further discussion of Project Satellite. In addition, we increased our interest in the Fort Hills oil sands mining and processing operations from 20% to 20.89% in 2017, and our interest ultimately increased to approximately 21.3% in 2018.

Work advanced on a number of projects through 2017. At our Fort Hills oil sands mining and processing operation, the mine, primary extraction, utilities and froth assets were commissioned. An intermediate product, bitumen froth, was produced in September 2017, and first oil was achieved on January 27, 2018. See “Description of the Business — Energy” for a discussion of the project. We commenced a $72 million project to install an additional ball mill at our Highland Valley Copper Operations and a US$110 million upgrade project at our Red Dog zinc operations, and continued to advance through the regulatory process for our Quebrada Blanca Phase 2 project. We also commenced and advanced studies and expansion work at in respect of other projects.

We also continued to strengthen our liquidity and financial position in 2017. Over the course of the year we retired US$1.3 billion of debt through open market repurchases, tender offers and retirement at maturity. In October, we extended the maturity of our US$3.0 billion revolving credit facility to October 2022 (from July 2020) and US$1.2 billion revolving credit facility to October 2020 (from June 2019).

Our cash and cash equivalents as at December 31, 2017 were $952 million against total debt of $6.4 billion.

|

Teck Resources Limited |

Page 13 |

2018 Annual Information Form

2018

In 2018, average annual prices for our principal products increased compared to 2017. Average realized annual prices in 2018 for steelmaking coal, copper and zinc were US$187 per tonne, US$2.96 per pound and US$1.33 per pound, respectively, compared with US$174 per tonne, US$2.80 per pound and US$1.31 per pound, respectively, in 2017. The average realized annual price for our blended bitumen in 2018 was US$35 per barrel.

During the year we achieved first oil at Fort Hills; completed the sale of our interest in the Waneta Dam; acquired an additional 13.5% interest in Compania Minera Teck Quebrada Blanca, S.A. (QBSA), our majority owned subsidiary that holds the Quebrada Blanca Phase 2 project (QB2) and subsequently announced a transaction through which a new partner will subscribe for a 30% interest in QBSA; received regulatory approval for, and approved the construction of, our QB2 project; announced the retirement of our long-time Chairman and the appointment of his replacement; and advanced various initiatives and projects intended to strengthen our financial position and our core business.

In January, first oil was produced at Fort Hills, which has now been running at full capacity for much of the fourth quarter. Start-up has exceeded our expectations with respect to both production volumes and product quality.

In April, we acquired an additional 13.5% interest in QBSA, our majority owned subsidiary that holds the QB2 project, bringing our interest to 90%, and in August we received regulatory approval to develop the QB2 project.

In July, we completed the sale of our two-thirds interest in the Waneta Dam and related transmission assets to BC Hydro for $1.2 billion cash. In connection with the sale, we entered into a 20-year arrangement with BC Hydro, with an option to extend for an additional 10 years, to purchase power for our Trail Operations.

Work advanced on a number of projects through 2018. Our project to install an additional ball mill at our Highland Valley Copper Operations progressed, targeting commissioning in 2019, and installation of our new acid plant at our Trail Operations advanced towards commissioning in mid-2019. Work also continued on an upgrade project at our Red Dog zinc operations with planned start-up in the first quarter of 2020.

In December our Board approved the QB2 project for full construction, with first production targeted for late 2021. Concurrently, we announced a transaction through which Sumitomo Metal Mining Co. Ltd. and Sumitomo Corporation will subscribe for a 30% indirect interest in QBSA, which holds the QB2 project, by contributing US$1.2 billion to the project with additional contingent consideration payable in certain circumstances. Following closing of the transaction, Teck will hold a 60% interest in QBSA; Sumitomo Metal Mining Co., Ltd. and Sumitomo Corporation will collectively hold a 30% interest and Empresa Nacional de Minería will continue to hold a 10% carried interest.

In September, Dominic S. Barton joined our Board of Directors and in October Mr. Barton became Chair of the Board, replacing our long-standing Chairman of the Board, Dr. Norman B. Keevil, who retired, along with Mr. Warren S. R. Seyffert, Q.C., at the end of the year.

|

Teck Resources Limited |

Page 14 |

2018 Annual Information Form

In October, we announced a normal course issuer bid, which allows us to purchase up to 40 million Class B subordinate voting shares through to October 2019. In December, we paid a dividend of $0.15 per share consisting of a supplemental dividend of $0.10 per share and our regular base quarterly dividend of $0.05 per share, which totalled approximately $86 million. In addition, taking into account our strong cash position, we also announced that the Board has directed management to apply an additional $400 million to the repurchase of shares, of which 4.7 million Class B subordinate voting shares were repurchased in the fourth quarter for $131 million.

We also continued to strengthen our liquidity and financial position in 2018. Over the course of the year we retired US$1.0 billion of debt through open market repurchases, tender offers and retirement at maturity. In light of our strong financial position, we were able to terminate the subsidiary guarantees of our various credit facilities and public notes that were introduced during the commodity downturn in 2016.

Our cash and cash equivalents as at December 31, 2018 were $1.7 billion against total debt of $5.5 billion.

|

Teck Resources Limited |

Page 15 |

2018 Annual Information Form

Description of the Business

General

Teck’s business is exploring for, acquiring, developing and producing natural resources. Our activities are organized into business units focused on copper, steelmaking coal, zinc and energy. These are supported by Teck’s corporate offices, which manage corporate growth initiatives and provide marketing, administrative, technical, financial and other services.

We have interests in the following operations:

|

Type of Operation

|

Jurisdiction

| |||

| Elkview

|

Steelmaking Coal Mine

|

British Columbia, Canada

| ||

| Fording River

|

Steelmaking Coal Mine

|

British Columbia, Canada

| ||

| Greenhills

|

Steelmaking Coal Mine

|

British Columbia, Canada

| ||

| Line Creek

|

Steelmaking Coal Mine

|

British Columbia, Canada

| ||

| Coal Mountain

|

Steelmaking Coal Mine

|

British Columbia, Canada

| ||

| Cardinal River

|

Steelmaking Coal Mine

|

Alberta, Canada

| ||

| Highland Valley

|

Copper/Molybdenum Mine

|

British Columbia, Canada

| ||

| Antamina

|

Copper/Zinc Mine

|

Ancash, Peru

| ||

| Quebrada Blanca

|

Copper Mine

|

Region I, Chile

| ||

| Carmen de Andacollo

|

Copper/Gold Mine

|

Region IV, Chile

| ||

| Trail Operations

|

Zinc/Lead Refinery

|

British Columbia, Canada

| ||

| Red Dog

|

Zinc/Lead Mine

|

Alaska, U.S.A.

| ||

| Pend Oreille

|

Zinc/Lead Mine

|

Washington, U.S.A.

| ||

| Fort Hills

|

Oil Sands Mining and Processing Operation

|

Alberta, Canada

| ||

Our principal products are steelmaking coal, copper, zinc and blended bitumen. In addition we produce lead, silver, molybdenum, and various specialty and other metals, chemicals and fertilizers. We also actively explore for copper, zinc and gold.

|

Teck Resources Limited |

Page 16 |

2018 Annual Information Form

The following table sets out our revenue by product for each of our last two financial years:

|

2018

|

%

|

2017(1)

|

%

| |||||||||

| Copper(2)

|

|

2.242

|

|

18

|

|

2.022

|

|

17

| ||||

| Coal

|

|

6.349

|

|

50

|

|

6.014

|

|

50

| ||||

| Zinc(3)

|

|

2.391

|

|

19

|

|

2.364

|

|

20

| ||||

| Bitumen

|

|

0.407

|

|

3

|

|

-

|

|

-

| ||||

| Other(4)

|

|

1.175

|

|

10

|

|

1.510

|

|

13

| ||||

| Total

|

|

12.564

|

|

100

|

|

11.910

|

|

100

| ||||

|

| ||||||||||||

| (1) | Certain 2017 comparative figures have been restated for new IFRS pronouncements. Please refer to Note 32 to our audited annual consolidated financial statements for the year ended December 31, 2018. |

| (2) | Copper revenues include sales of copper contained in concentrates and cathode copper. |

| (3) | Zinc revenues include sales of refined zinc and zinc concentrate. |

| (4) | Other revenues include sales of silver, lead, gold, molybdenum, various specialty metals, chemicals, energy and fertilizer. |

Product Summary

Steelmaking Coal

Teck is the second-largest seaborne exporter of steelmaking coal in the world. Our hard coking coal, a type of steelmaking coal, is used primarily for making coke by integrated steel mills in Asia, Europe and the Americas. In 2018, sales to Asia accounted for approximately 75% of our annual coal sales volume, higher than in 2017 due to increased sales volumes to areas with the greatest demand growth, such as India and South East Asia. Approximately 75% of all coal we produce is high-quality hard coking coal, although the percentages can vary from period to period. We also produce lesser quality semi-hard coking coal, semi-soft coking coal, PCI and thermal coal products, which in aggregate accounted for a little over 25% of our annual sales volume in 2018.

Coal is processed at our mine sites. Processed coal is primarily shipped westbound from our mines by rail to terminals along the coast of British Columbia and from there by vessel to overseas customers. In 2018, approximately 5% of our processed coal was shipped eastbound directly by rail, or by rail and by ship via Thunder Bay, to customers in North America.

Globally, we compete in the steelmaking coal market primarily with producers based in Australia and the United States. For sales to China, we also compete with Mongolian and Chinese domestic coal producers. Coal pricing is generally established in U.S. dollars and the competitive positioning among producers can be significantly affected by exchange rates. Our competitive position in the coal market continues to be determined primarily by the quality of our various coal products and our reputation as a reliable supplier, as well as by our production and transportation costs compared to other producers throughout the world.

The high-quality seaborne steelmaking coal markets are cyclical, being driven by a combination of demand, production and export capacity. Strong steel market fundamentals support demand

|

Teck Resources Limited |

Page 17 |

2018 Annual Information Form

and pricing for high-quality seaborne steelmaking coal. Conversely, in difficult steel markets, steelmakers can use a higher proportion of semi-soft and PCI coal products in their production process, which can result in reduced pricing premiums for higher quality hard coking coals.

Global steel production and demand for seaborne steelmaking coal remained strong in 2018. The World Steel Association reported strong steel production across all regions due to resilient steel pricing and demand supported by the recovery in investment activities in developed economies and the improved performance of emerging economies. Depletion and reduced production of some Eastern European coal mines continued to increase demand for seaborne steelmaking coal from European steel mills. A robust steelmaking coal market is supported by concerns regarding supply from Australia and the U.S, as well as demand impact of continued capacity growth in India and the relocation of steel production to coastal areas in China. While demand for steelmaking coal remains strong, pricing corrected from the beginning of 2019 reflecting shorter vessel queues in Australia and the relaxation of import restrictions in China in November 2018. We continue to monitor the effects that government policy and trade uncertainty might have on potential price volatility.

In the past few years, a number of our customers reduced the proportion of coal purchased through quarterly priced agreements and requested pricing for a portion of contract volumes on a spot basis in an effort to control costs in an environment of low steel prices. Coincident with the cyclone-induced price spike in April 2017, the pricing methodology for our quarterly contract sales changed from a negotiated quarterly benchmark to an index-linked pricing mechanism based on the average of key premium steelmaking coal price assessments. Quarterly priced sales represent approximately 40% of our sales, with the balance of our sales priced at levels reflecting market conditions when sales are concluded. Lower-grade semi-soft coals and PCI pricing continues to be negotiated on a quarterly benchmark basis.

Substantially all of our revenues from sales of coal products were derived from sales to third-party end users, most of which are steelmakers.

Copper

We produce both copper concentrates and copper cathode. Our principal market for copper concentrates is Asia, with a lesser amount sold in Europe. Copper concentrates produced at the Highland Valley Copper mine are distributed to customers in Asia by rail to a port in Vancouver, British Columbia, and from there by ship. Copper concentrates produced at Antamina are transported by a slurry pipeline to a port at Huarmey, Peru, and from there go by ship to customers in Asia and Europe. Copper concentrates produced at Carmen de Andacollo are trucked to the port of Coquimbo, Chile, and from there go by ship to customers in Asia and Europe. Copper concentrates are sold primarily under long-term contracts, with treatment and refining charges negotiated on an annual basis. Copper cathode from our Quebrada Blanca and Carmen de Andacollo mines is trucked from the mines and sold primarily under annual contracts to customers in Asia, Europe and North America.

The copper business is cyclical. Copper concentrate treatment charges rise and fall depending upon the supply of copper concentrates in the market and the demand for custom copper concentrates by the copper smelting and refining industry. Prices for copper cathode also rise and fall as a result of changes in demand for, and supply of, refined copper metal. The major use

|

Teck Resources Limited |

Page 18 |

2018 Annual Information Form

of refined copper is in electrical wiring and electronic applications, with prices and premiums highly dependent on the demand for electrical wire in construction, communications and automotive applications. We compete with other producers of copper concentrates and cathodes, as well as copper sourced through scrap sources.

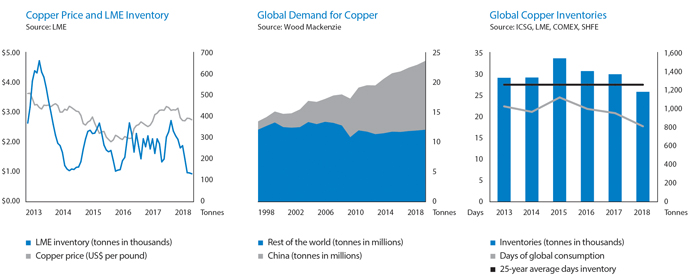

Global demand for copper metal is estimated by Wood Mackenzie to have grown by 3.0% in 2018 to reach an estimated 23.7 million tonnes. Demand improved in Asia with Chinese copper cathode demand growth estimated at 5.0% over 2017, much higher than initial projections at the beginning of the year. Demand growth in Europe was relatively flat, while demand in North America was up 3.3% with better semi-fabricated copper demand in Mexico, Canada and the US. Copper demand in South East Asia was stronger on improved export demand in several countries to meet increasing Indian demand, which was up 9.2% to 0.54 million tonnes. India was left undersupplied when one of the two domestic Indian smelters was shut during 2018, increasing export demand in South East Asia. Copper scrap availability decreased in 2018 as global trade patterns were disrupted by environmental restrictions on certain types of scrap imports into China. Scrap and unrefined copper imports into China, including blister and anode, were down 15% year-over-year to September 2018.

All of our revenues from sales of copper concentrates and cathode copper were derived from sales to third parties.

Zinc

We produce refined zinc through our metallurgical operations at Trail and zinc concentrates through our mining operations. Our principal markets for refined zinc are North America and Asia. Refined zinc produced at our metallurgical operations at Trail, British Columbia, is distributed to customers in North America by rail and/or truck and to customers in Asia by ship.

Our principal markets for zinc concentrates are Asia and Europe. In addition, in 2018 approximately 34% of zinc concentrate produced at Red Dog was sold to our metallurgical operations at Trail for treatment and refining. All of the production from our Pend Oreille zinc mine is sold to Trail.

All of our 2018 revenues from sales of refined zinc and zinc concentrates (other than zinc concentrates produced at Red Dog or Pend Oreille that are sold to Trail) were derived from sales to third parties. We strive to differentiate our refined metal products by producing the alloys, sizes and shapes best suited to our customers’ needs. We have substantial long-term frame contracts for the sale of zinc concentrates from the Red Dog mine to customers in Asia and Europe.

Trail’s supply of zinc and lead concentrates, other than those sourced from Red Dog or Pend Oreille, is provided primarily through long-term contracts with mine producers in North America, South America and Australia.

The zinc business is cyclical. Treatment and refining charges rise and fall depending upon the supply of zinc concentrates in the market and the demand for custom zinc concentrates by the zinc smelting and refining industry. Refined zinc is used primarily for galvanizing steel, and prices and premiums are highly dependent on the demand for steel products.

|

Teck Resources Limited |

Page 19 |

2018 Annual Information Form

Energy

In January 2018 the Fort Hills mine in Alberta, which is operated by an affiliate of Suncor Energy Inc., produced first bitumen. As required by pipelines to meet shipping viscosity requirements, we purchase diluent to blend with our bitumen production and sell a blended bitumen product known as Fort Hills Reduced Carbon Lifecycle Dilbit Blend, or FRB.

Teck’s principal markets for the blended bitumen are refinery operators in Alberta, Ontario, the U.S. Midwest and the U.S. Gulf Coast. Bitumen production from Fort Hills is transported on the Northern Courier Pipeline to the East Tank Farm in Alberta, which is owned by the Thebacha Limited Partnership and operated by an affiliate of Suncor. At the East Tank Farm, the Fort Hills bitumen is blended with diluent that has been sourced and delivered from Edmonton on the Norlite Pipeline. The blended bitumen is subsequently transported from the East Tank Farm on the Wood Buffalo Pipeline to Hardisty, Alberta, where Teck has contracted storage capacity for blended bitumen.

Our tankage at Hardisty is connected to major export pipelines, including the Enbridge common carrier pipeline, the existing Keystone pipeline and the Express crude oil pipeline; it is also connected to a large unit train loading facility. We sell our share of FRB to variety of customers at the Hardisty market hub and on the U.S. Gulf Coast. Approximately 80% of our blended bitumen sales are at Hardisty, with the remainder at the U.S. Gulf Coast. We have entered into a long-term take-or-pay transportation agreement on the existing Keystone pipeline to ship 10,000 barrels per day (bpd) of blended bitumen to customers on the U.S. Gulf Coast. The balance of our production will be either sold at Hardisty or shipped to customers via the Enbridge common carrier pipeline, or transported by rail if required.

Export pipeline capacity for Canadian crude oil versus overall supply was in deficit through 2018 and is expected to remain so through 2019 and beyond, until new export capacity is developed. Exacerbating the imbalance was a slower than expected ramp-up of crude-by-rail takeaway capacity.

In support of future export pipeline expansions, we have entered into long-term transportation contracts on the proposed Kinder Morgan TransMountain and TransCanada Keystone XL pipeline expansions that, if built, will deliver to Burnaby, British Columbia and the US Gulf Coast, respectively.

Prices for our blended bitumen are market based, and determined through a combination of global and Canadian benchmark indices. Like our other commodities, the oil industry is cyclical and is highly competitive. Blended bitumen prices are influenced by a combination of North American crude oil benchmark prices, including the New York Mercantile Exchange (NYMEX) light sweet crude oil (WTI). Canadian heavy crude oil of the kind we produce trades at a differential to WTI, and is known as Western Canadian Select or WCS. WCS is a widely-marketed crude grade with transparent market price references quoted at the Hardisty market hub in Canada and the U.S. Gulf Coast. The WCS discount to WTI varies over time depending on the supply and demand for heavy crude production and the markets available to producers of those products, which are in turn influenced by available pipelines and other transportation options.

|

Teck Resources Limited |

Page 20 |

2018 Annual Information Form

WCS at Hardisty values were highly volatile throughout 2018 with differentials widening significantly in the third and fourth quarter. The widening was the result of overall increased Canadian crude production competing for limited export capacity and markets, exacerbated by planned maintenance turnarounds at refineries in the U.S. Midwest and Gulf Coast. The impact of these wider differentials at Hardisty to our sales values are somewhat mitigated by our sales into the U.S. Gulf Coast market.

WCS at Hardisty differentials have since materially improved, and are now reflective of the long-term average. Supply was reduced due to the announced 325,000 barrels per day production curtailment mandated by the Government of Alberta for the first quarter of 2019. The government subsequently revised the first quarter curtailment level to 250,000 barrels per day for the production months of February and March. In addition, Canadian crude-by-rail shipments sharply increased throughout 2018 and are now forecast to exceed 400,000 bpd in 2019. Throughout 2019, we will participate in the crude-by-rail initiative through an agreement to load 10,000 bpd of FRB blend onto customers’ railcars at Hardisty.

Individual Operations

Steelmaking Coal

Our coal mineral holdings consist of a mix of fee simple lands owned by us and Crown leases and licences, which are subject to licensing and leasing fees. In the past, renewals of these licences and leases have generally been granted, although there can be no assurance that this will continue in the future.

Five of Teck’s six operating coal mines are in British Columbia and are therefore subject to the B.C. Mineral Tax which is a two-tier tax with a minimum rate of 2% and a maximum rate of 13%. A minimum tax of 2% applies to operating cash flows, as defined by the regulations. A maximum tax rate of 13% applies to cash flows after taking available deductions for capital expenditures and other permitted deductions. The Alberta Coal Royalty, which is assessed on a similar basis, at rates of 1% and 13%, apply to the Cardinal River mine in Alberta.

All of Teck’s coal mines are conventional open pit operations and are designed to operate on a continuous basis, 24 hours per day, 365 days per year. Operating schedules can be varied depending on market conditions and are subject to shutdowns for maintenance activities. Capacity may be restricted for a variety of reasons and actual production will depend on sales volumes. All of the mines are accessed by two-lane all-weather roads that connect to public highways. All the mines operate under permits granted by provincial and/or federal regulatory authorities. Each of the mines will require additional permits as they progress through their long-term mine plans. The issuance of certain permits for mine life extensions may depend on a number of factors including our ability to meet the water quality targets set out in the Elk Valley Water Quality Plan, as discussed below. All permits necessary for the current operations of the mines are in hand and in good standing. Annual infill drilling programs are conducted to confirm and update the geological models used to develop the yearly mine plans.

Following mining, the coal is washed in coal preparation plants using a variety of conventional techniques and conveyed to coal or gas-fired dryers for drying. Processed coal is conveyed to clean coal silos or other storage facilities for intermediate storage and load-out to railcars.

|

Teck Resources Limited |

Page 21 |

2018 Annual Information Form

Our 2018 production of 26.2 million tonnes was a slight decline of 400,000 thousand tonnes from 2017, primarily due to declining production at Coal Mountain Operations as it reached the end of its life. The pressure event in the coal dryer at Elkview Operations that impacted production in the first quarter was fully offset in subsequent quarters by hauling a portion of raw coal from Elkview Operations to Coal Mountain Operations for processing.

Steelmaking coal production in 2019 is expected to be between 26.0 and 26.5 million tonnes. The business unit will continue to evaluate 2019 raw coal processing opportunities through the latent production capacity of Elk Valley processing plants. As in prior years, annual production volumes can be adjusted to reflect market demand for our products, subject to adequate rail and port service. Assuming that current market conditions persist, annual production from 2020 to 2022 is expected to be higher than in 2019.

Elk Valley Water Management

We continue to implement the water quality management measures required by the Elk Valley Water Quality Plan (the Plan), an area-based management plan that was approved in 2014 by the British Columbia Minister of Environment. The Plan establishes short-, medium- and long-term water quality targets for selenium, nitrate, sulphate and cadmium to protect the environment and human health, as well as a plan to manage calcite formation. In accordance with the Plan, we have constructed and are operating the first active water treatment facility (AWTF) at West Line Creek. In the fourth quarter of 2018, we commissioned an additional treatment step to address an issue regarding selenium compounds in effluent from the West Line Creek AWTF. The facility is operating as designed. We have commenced construction on our next AWTF at Fording River Operations, which will use the same treatment process as the modified West Line Creek AWTF.

In 2018, we successfully operated our first saturated rock fill (SRF) project at Elkview Operations. The SRF has been in operation for the past 12 months and is demonstrating near-complete removal of nitrate and selenium from the feed water. Results to date from the full-scale trial show that the technology has the potential to replace future AWTFs, as well as to reduce capital and operating costs for water treatment. We are working to increase the capacity of the Elkview SRF to potentially reduce reliance on active water treatment. This approach has not yet received necessary approvals and we continue to progress the construction of additional AWTFs to comply with the Plan.

Capital spending on water treatment in 2019 is expected to be approximately $235 million, including advancing a clean water diversion at Fording River, application of SRF technology at Elkview, construction of Fording River South AWTF, and advancing management of calcite and the early development of water treatment for Fording River North. This compares to approximately $57 million of capital spending on water treatment in 2018.

In our previous guidance, we estimated total capital spending for water treatment between 2018 and 2022 of $850 to $900 million. We intend to complete construction of the Fording River South AWTF, currently under construction. If we are successful in permitting SRF projects to replace the Elkview AWTF and the Fording River North AWTF, we estimate that total capital spending on water treatment during this period would reduce to $600 to $650 million. If no reduction in AWTF capacity is permitted, overall capital in the same period would increase by approximately $250 million over our previous guidance as a result of engineering scope changes at the Elkview

|

Teck Resources Limited |

Page 22 |

2018 Annual Information Form

AWTF and an increased volume of water treated at the Fording River North AWTF. We have presented regulators with evidence that SRFs are a viable technical alternative to active water treatment and are working through a review process. We expect that this process will result in a decision in the first half of 2019.

We continue to advance research and development, including the SRF technology. We estimate that over the longer term, SRFs will have capital and operating costs that are 20% and 50%, respectively, of AWTFs of similar capacity. If we are successful in replacing a substantial portion of active water treatment capacity with SRFs, we believe that our long-term operating costs associated with water treatment could be reduced substantially.

All of the foregoing estimates are uncertain. Final costs of implementing the Plan will depend in part on the technologies applied and on the results of ongoing environmental monitoring and modelling. The timing of expenditures will depend on resolution of technical issues, permitting timelines and other factors. We expect that, in order to maintain water quality, some form of water treatment will continue for an indefinite period after mining operations end. The Plan contemplates ongoing monitoring to ensure that the water quality targets set out in the Plan are in fact protective of the environment and human health, and provides for adjustments if warranted by monitoring results. This ongoing monitoring, as well as our continued research into treatment technologies, could reveal unexpected environmental impacts, technical issues or advances associated with potential treatment technologies that could substantially increase or decrease both capital and operating costs associated with water quality management.

Inability to meet targets in the Plan or new information regarding environment inputs could adversely affect our ability to extend mining operations into new areas. See “Risk Factors — We face risks associated with the issuance and renewal of environmental permits”, “Risk Factors - Failure to comply with environmental, health and safety laws may have a material adverse effect on our operations and projects” and “Risk Factors — Changes in environmental, health and safety laws may have a material adverse effect on our operations” for a further discussion of permitting and water quality management.

During the third quarter of 2018, Teck received notice from Canadian federal prosecutors of potential charges under the Fisheries Act in connection with discharges of selenium and calcite from coal mines in the Elk Valley. Since 2014, compliance limits and site performance objectives for selenium and other constituents, as well as requirements to address calcite, in surface water throughout the Elk Valley and in the Koocanusa Reservoir have been established under a regional permit issued by the Provincial government, which references the Plan. If Federal charges are laid, potential penalties may include fines as well as orders with respect to operational matters. We expect that discussions with respect to the draft charges will continue at least into the third quarter of 2019. It is not possible at this time to fully assess the viability of our potential defences to any charges, or to estimate the potential financial impact on us of any conviction. Nonetheless, that impact may be material. See “Risk Factors — Litigation” for a further discussion of risks associated with this issue.

|

Teck Resources Limited |

Page 23 |

2018 Annual Information Form

Coal Transportation

Most of the coal produced at the mines in the Elk Valley region of British Columbia and at the Cardinal River mine in west-central Alberta is shipped to west coast ports in British Columbia.

Westbound rail service from the mines located in the Elk Valley is provided by Canadian Pacific Railway Company (CPR) pursuant to a 10-year agreement that expires in 2021. CPR transports a portion of these westbound shipments to Kamloops, B.C., and interchanges the trains with Canadian National Railway Company (CN) for further transportation to the west coast. CN also provides rail service from the Cardinal River mine to the west coast. Both CN’s Cardinal River services and Kamloops’ interchange services are provided to Teck Coal under a two-year agreement that expired on December 31, 2017. We are in discussions with CN in regard to a new contract and currently operate under Tariff for each segment.

A small portion of the coal produced at the mines in the Elk Valley is transported by rail and ship via Thunder Bay Terminals in Thunder Bay, Ontario, to customers in the Great Lakes region of Canada and by direct rail to the United States. CPR transports the United States shipments via CPR directly or via the Burlington Northern Santa Fe railway, in which case CPR transports the coal from Elk Valley to Coutts, Alberta, and then interchanges the trains with the Burlington Northern Santa Fe for further transport to the United States. Rail shipments destined for Thunder Bay and the United States are transported under rail tariff and related agreements.

Teck exports its seaborne coal primarily through three west coast terminals (Westshore, Neptune and Ridley). Westshore Terminals provides ship-loading services at Roberts Bank, British Columbia, and in 2018 provided services for approximately 66% of Teck’s coal shipments. Our contract with Westshore Terminals provides us with 19 million tonnes of annual capacity through to March 2021, and we have contracted capacity at Ridley Terminals near Prince Rupert to provide for steelmaking coal shipments from our Cardinal River Operations in Alberta and surge capacity to manage interruptions throughout the supply chain.

Neptune Bulk Terminals, in which we have a 46% ownership interest, has a current annual capacity for steelmaking coal shipments of 12.5 million tonnes and provides ship-loading services for steelmaking coal shipments loaded on a cost-of-service basis. Construction work to upgrade Neptune’s operational capacity commenced in 2018 and is expected to be completed in the third quarter of 2020.

Property Description

The following sections cover details for each of the operating mines and potential projects. For the operating mines, the remaining reserve life is shown, calculated by dividing remaining reserves by current annual production rates. As mine plans and capacities change, these reserve lives will also change. Because each mine covers a substantial lease area, the development required for accessing the reserves can be substantial, and can involve a range of expenditures in terms of pit access and development and infrastructure to support the development. The reserve lives also assume that the required permits for life extensions will be obtained in a timely fashion to maintain production continuity, as has been the case in previous years.

|

Teck Resources Limited |

Page 24 |

2018 Annual Information Form

Geology of the Elk Valley Mines (B.C., Canada)

In the mines in the Elk Valley Region of British Columbia, coal is contained within the sedimentary Mist Mountain Formation of the lower Cretaceous Kootenay Group. The Mist Mountain sediments were involved in the mountain-building movements of the late Cretaceous to early Tertiary Laramide orogeny and are approximately 500 metres thick, with the depth of burial ranging from zero to 1,500 metres. The major structural features are north-south trending synclines with near horizontal to steep westerly dipping thrust faults and a few high-angle normal faults. This faulting has allowed for the Mist Mountain sequence to be repeated throughout the Elk Valley.

Fording River Mine, B.C., Canada

The Fording River mine is located 29 kilometres northeast of the community of Elkford, in southeastern British Columbia. The mine site consists of approximately 23,000 hectares of coal lands, including four operating surface coal pits along with several areas planned for surface mine development held under multiple contiguous coal leases and licences. The leases and licences relating to Fording River are held by Teck Coal. Teck Coal also controls the surface and subsurface rights to the properties that are in operation and those that are planned for development.

Coal mined at Fording River is primarily steelmaking coal, although a small amount of thermal coal is also produced. The current annual production capacities of the mine and preparation plant are approximately 9.0 million and 9.5 million tonnes of clean coal, respectively.

Approximately half of the current production is derived from the Eagle Mountain pit area with the other half produced from the Swift pit area. Proven and probable reserves at Fording River are projected to support mining at planned production rates for a further 43 years. Fording River’s reserve areas include Eagle Mountain, Swift, Turnbull, and Castle Mountain.

2019 projected capital costs for Fording River are approximately $171 million. The major components of the projected capital costs are:

|

Component

|

Approximate projected cost ($/million)

| |

| Sustaining |

102 | |

|

Major Enhancement |

69 | |

|

Teck Resources Limited |

Page 25 |

2018 Annual Information Form

2019 projected cash operating costs for Fording River are approximately $575 million. The major components of the projected cash operating costs are:

|

Component

|

Approximate projected cost ($/million)

| |

| Labour |

251 | |

|

Supplies |

235 | |

| Energy |

124 | |

|

Other (including general & administrative, inventory changes) |

44 | |

| Less amounts associated with projected capitalized stripping |

(79) | |

|

Total |

575 | |

The cash operating costs presented above do not include transportation or royalties.

Elkview Mine, B.C., Canada

Teck Coal has a 95% partnership interest in the Elkview Mine. The remaining 5% is indirectly held equally by Nippon Steel & Sumitomo Metal Corporation, a Japanese steel producer, and POSCO, a Korean steel producer, each of which acquired a 2.5% interest in 2005. The Elkview mine is an open pit coal mine located approximately 3 kilometres east of Sparwood in southeastern British Columbia. The mine site consists of approximately 27,100 hectares of coal lands.

The coal produced is a high-quality mid-volatile hard coking coal. Lesser quantities of lower-grade hard coking coal are also produced. The current annual production capacities of the mine and preparation plant (on a 100% basis) are approximately 7.0 million and 7.0 million tonnes of clean coal, respectively.

Proven and probable reserves at Elkview are projected to support mining at planned production rates for a further 38 years.

2019 projected capital costs for Elkview are approximately $127 million. The major components of the projected capital costs are:

|

Component

|

Approximate projected cost ($/million)

| |

| Sustaining |

37 | |

| Major Enhancement |

90 | |

|

Teck Resources Limited |

Page 26 |

2018 Annual Information Form

2019 projected cash operating costs for Elkview are approximately $345 million. The major components of the projected cash operating costs are:

|

Component

|

Approximate projected cost ($/million)

| |

| Labour |

201 | |

| Supplies |

185 | |

| Energy |

104 | |

| Other (including general & administrative, inventory changes) |

62 | |

| Less amounts associated with projected capitalized stripping |

(207) | |

|

Total

|

345

| |

The cash operating costs presented above do not include transportation or royalties.

Greenhills Mine, B.C., Canada

Greenhills is operated under a joint venture agreement among Teck Coal, POSCO Canada Limited (POSCAN) and POSCAN’s parent, POSCO. Pursuant to the joint venture agreement, Teck Coal has an 80% interest in the joint venture while POSCAN has a 20% interest. Teck Coal and POSCAN own the mine equipment and preparation plant in proportion to their respective joint venture interests. Under the joint venture agreement, Teck Coal is the manager and operator of Greenhills and takes 80% of all coal produced at Greenhills. POSCAN takes the remaining 20% and pays a quarterly royalty based on the price achieved for Greenhills coal sales.