Exhibit 99.1

|

Third Quarter

2019 Earnings

Results

Media Relations: Jake Siewert 212-902-5400 Investor Relations: Heather Kennedy Miner 212-902-0300

|

||

|

The Goldman Sachs Group, Inc. 200 West Street | New York, NY 10282

|

Third Quarter 2019 Earnings Results

Goldman Sachs Reports Third Quarter Earnings Per Common Share of $4.79

|

“Our results through the third quarter reflect the underlying strength of our global client franchise and its ability to produce solid results in the context of a mixed operating environment. We continue to execute on our strategic priorities, including investing in important growth opportunities in our existing and new businesses and in delivering for our clients in the most efficient and effective manner possible. We believe that this focus will best position the firm to generate long-term, industry-leading returns for our shareholders.” |

|

- David M. Solomon, Chairman and Chief Executive Officer

|

Financial Summary

|

|

|

|||||||

|

Net Revenues

|

Net Earnings

|

EPS

| ||||||

|

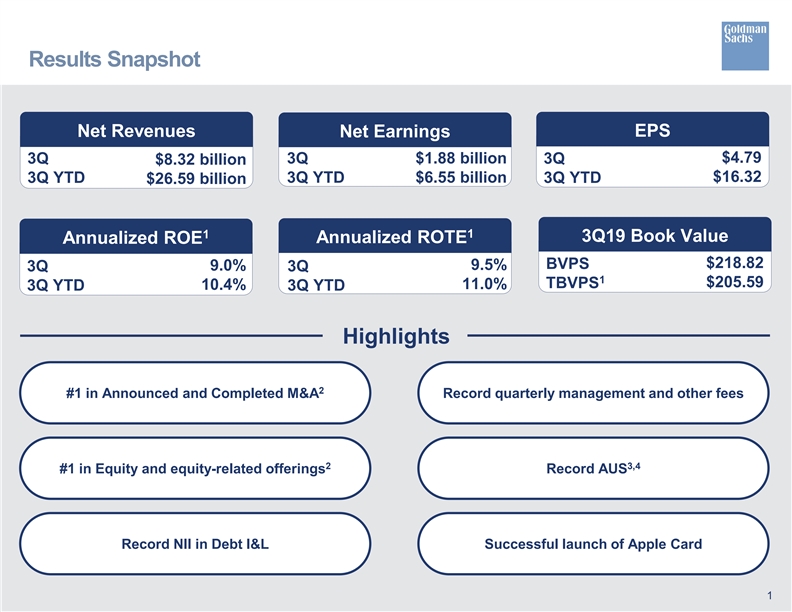

3Q $8.32 billion

3Q YTD $26.59 billion

|

3Q $1.88 billion

3Q YTD $6.55 billion

|

3Q $4.79

3Q YTD $16.32

| ||||||

|

Annualized ROE 1

|

Annualized ROTE 1

|

Book Value Per Share

| ||||||

|

3Q 9.0%

3Q YTD 10.4%

|

3Q 9.5%

3Q YTD 11.0%

|

3Q $218.82

3Q Growth 2.2%

| ||||||

NEW YORK, October 15, 2019 – The Goldman Sachs Group, Inc. (NYSE: GS) today reported net revenues of $8.32 billion and net earnings of $1.88 billion for the third quarter ended September 30, 2019. Net revenues were $26.59 billion and net earnings were $6.55 billion for the first nine months of 2019.

Diluted earnings per common share (EPS) was $4.79 for the third quarter of 2019 compared with $6.28 for the third quarter of 2018 and $5.81 for the second quarter of 2019, and was $16.32 for the first nine months of 2019 compared with $19.21 for the first nine months of 2018.

Annualized return on average common shareholders’ equity (ROE)1 was 9.0% for the third quarter of 2019 and 10.4% for the first nine months of 2019. Annualized return on average tangible common shareholders’ equity (ROTE)1 was 9.5% for the third quarter of 2019 and 11.0% for the first nine months of 2019.

1

Goldman Sachs Reports

Third Quarter 2019 Earnings Results

Highlights

| ◾ |

The firm ranked #1 in worldwide announced and completed mergers and acquisitions for the year-to-date2. The firm also ranked #1 in worldwide equity and equity-related offerings, common stock offerings and initial public offerings for the year- to-date2. |

| ◾ |

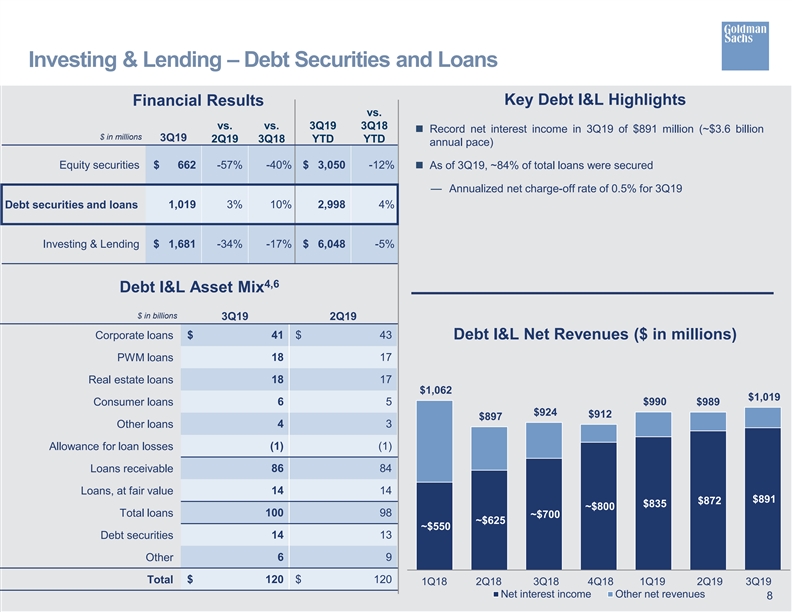

Investing & Lending net revenues included record quarterly net interest income in debt securities and loans of $891 million. |

| ◾ |

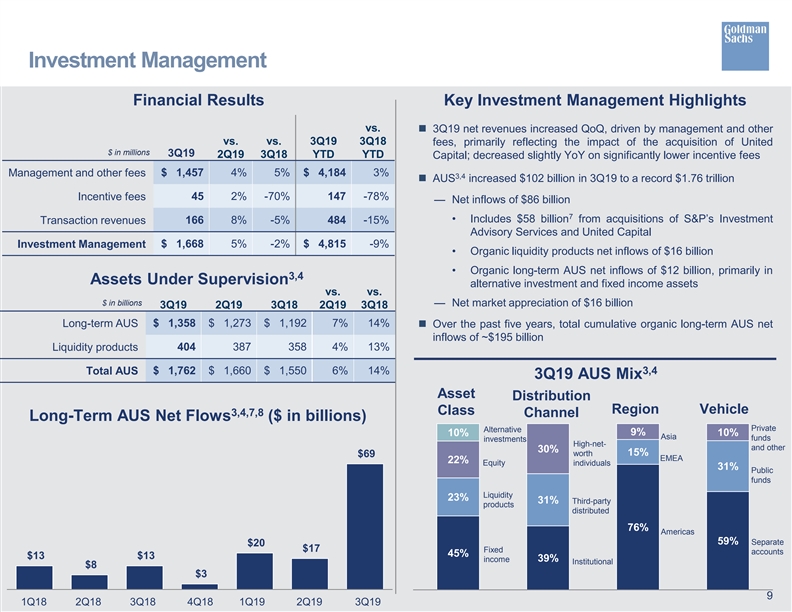

Investment Management net revenues included record quarterly management and other fees of $1.46 billion. Assets under supervision3,4 increased $102 billion5 during the quarter to a record $1.76 trillion. |

| ◾ |

Book value per common share was $218.82, 2.2% higher compared with the end of the second quarter of 2019 and 10.9% higher compared with the end of the third quarter of 2018. |

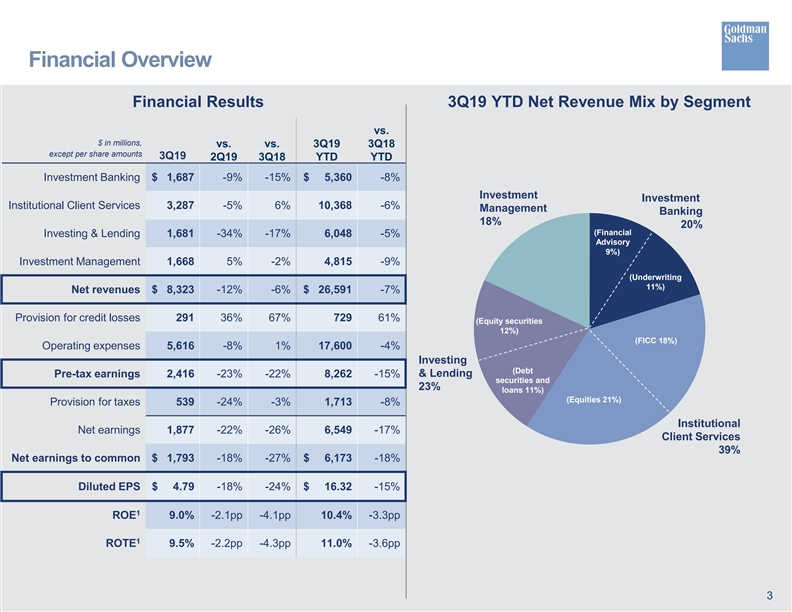

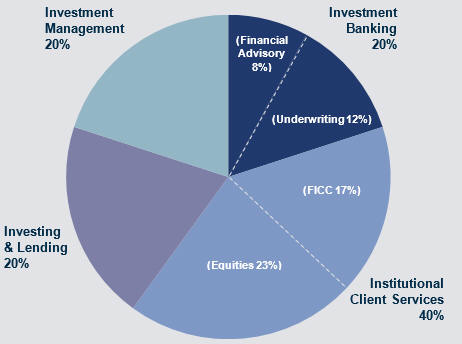

Quarterly Net Revenue Mix by Segment

|

|

|

2

Goldman Sachs Reports

Third Quarter 2019 Earnings Results

|

Net Revenues

|

|

|

| Net revenues were $8.32 billion for the third quarter of 2019, 6% lower than the third quarter of 2018 and 12% lower than the second quarter of 2019. The decrease compared with the third quarter of 2018 primarily reflected lower net revenues in Investing & Lending and Investment Banking, partially offset by higher net revenues in Institutional Client Services. |

|

Net Revenues

| ||

|

$8.32 billion

| ||||

|

|

|

Investment Banking |

|

|

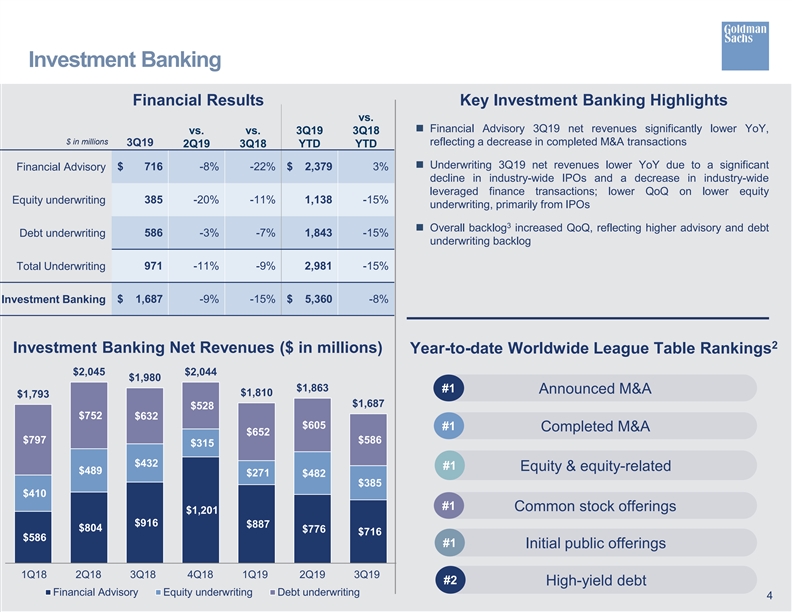

| Net revenues in Investment Banking were $1.69 billion for the third quarter of 2019, 15% lower than the third quarter of 2018 and 9% lower than the second quarter of 2019.

Net revenues in Financial Advisory were $716 million, 22% lower compared with a strong third quarter of 2018, reflecting a decrease in completed mergers and acquisitions transactions.

Net revenues in Underwriting were $971 million, 9% lower than the third quarter of 2018, due to lower net revenues in equity underwriting, reflecting a significant decline in industry-wide initial public offerings, and in debt underwriting, reflecting a decrease in industry-wide leveraged finance transactions.

The firm’s investment banking transaction backlog3 increased compared with the end of the second quarter of 2019. |

Investment Banking

| |||||

|

$1.69 billion

| ||||||

|

|

Financial Advisory |

$716 million | ||||

| Underwriting

|

$971 million

| |||||

|

|

|

Institutional Client Services |

|

|

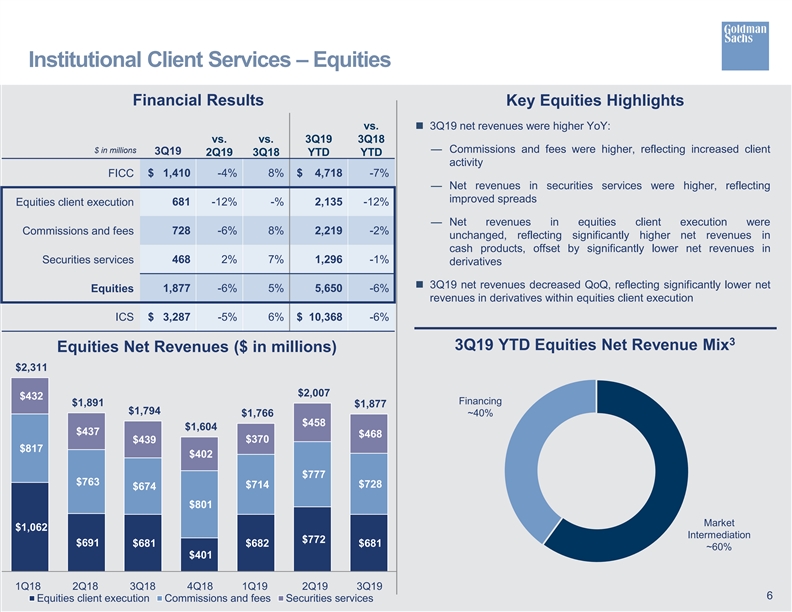

| Net revenues in Institutional Client Services were $3.29 billion for the third quarter of 2019, 6% higher than the third quarter of 2018 and 5% lower than the second quarter of 2019.

Net revenues in Fixed Income, Currency and Commodities (FICC) Client Execution were $1.41 billion, 8% higher than the third quarter of 2018, reflecting higher net revenues in commodities, credit products, mortgages and interest rate products, partially offset by lower net revenues in currencies. During the quarter, FICC Client Execution operated in an environment generally characterized by solid client activity.

Net revenues in Equities were $1.88 billion, 5% higher than the third quarter of 2018, primarily due to higher commissions and fees, reflecting increased client activity, and higher net revenues in securities services, reflecting improved spreads. Net revenues in equities client execution were unchanged, reflecting significantly higher net revenues in cash products, offset by significantly lower net revenues in derivatives. During the quarter, Equities operated in an environment generally characterized by lower client activity compared with the second quarter of 2019. |

|

Institutional Client Services

| ||||

|

$3.29 billion

| ||||||

| FICC |

$1.41 billion | |||||

| Equities

|

$1.88 billion

| |||||

3

Goldman Sachs Reports

Third Quarter 2019 Earnings Results

|

|

Investing & Lending |

|

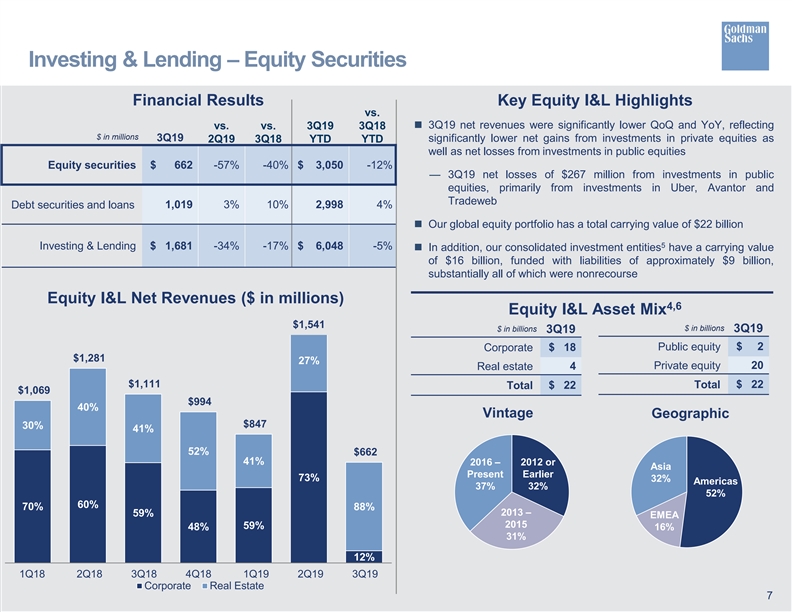

| Net revenues in Investing & Lending were $1.68 billion for the third quarter of 2019, 17% lower than the third quarter of 2018 and 34% lower than the second quarter of 2019.

Net revenues in equity securities were $662 million, 40% lower than the third quarter of 2018, reflecting significantly lower net gains from investments in private equities as well as net losses from investments in public equities.

Net revenues in debt securities and loans were $1.02 billion, 10% higher than the third quarter of 2018, driven by significantly higher net interest income. The third quarter of 2019 included net interest income of $891 million. |

Investing & Lending | |||||

|

$1.68 billion

| ||||||

| Equity Securities |

$662 million | |||||

| Debt Securities and Loans |

$1.02 billion

| |||||

|

|

||||||

|

|

Investment Management |

|

| Net revenues in Investment Management were $1.67 billion for the third quarter of 2019, 2% lower than the third quarter of 2018 and 5% higher than the second quarter of 2019.

The decrease in net revenues compared with the third quarter of 2018 was due to significantly lower incentive fees. This decrease was partially offset by higher management and other fees (including the impact of the acquisition of United Capital Financial Partners, Inc. (United Capital)), reflecting higher average assets under supervision, partially offset by shifts in the mix of client assets and strategies.

During the quarter, total assets under supervision3,4 increased $102 billion to $1.76 trillion. Long-term assets under supervision increased $85 billion, including net inflows of $69 billion5, primarily in equity and fixed income assets, and net market appreciation of $16 billion, primarily in fixed income assets. Liquidity products increased $17 billion5. |

Investment Management

| |||||

|

$1.67 billion

| ||||||

| Management and Other Fees |

$ 1.46 billion | |||||

| Incentive Fees |

$ 45 million | |||||

| Transaction Revenues |

$166 million | |||||

Provision for Credit Losses

|

Provision for credit losses was $291 million for the third quarter of 2019, 67% higher than the third quarter of 2018 and 36% higher than the second quarter of 2019. The increase compared with the third quarter of 2018 primarily reflected higher impairments. |

||||

|

Provision for Credit Losses

| ||||

|

$291 million

| ||||

4

Goldman Sachs Reports

Third Quarter 2019 Earnings Results

Operating Expenses

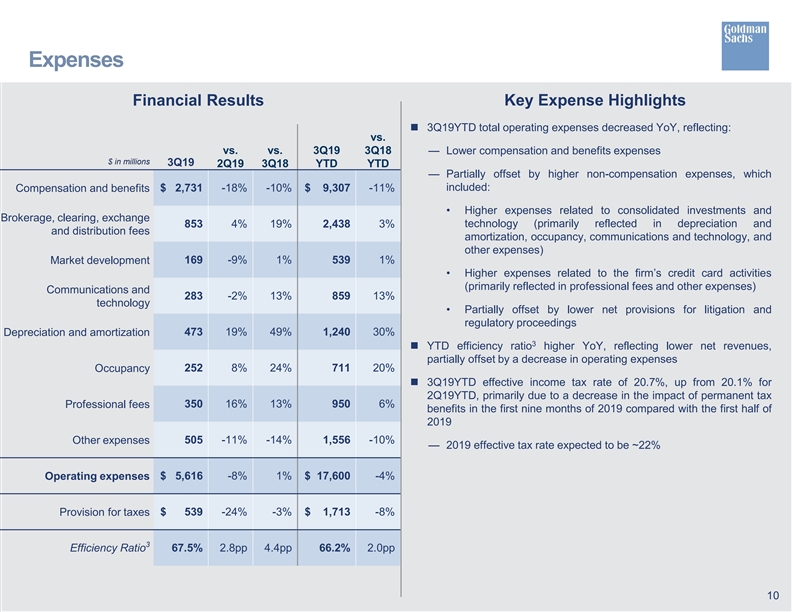

| Operating expenses were $5.62 billion for the third quarter of 2019, essentially unchanged compared with the third quarter of 2018 and 8% lower than the second quarter of 2019. The firm’s efficiency ratio3 for the first nine months of 2019 was 66.2%, compared with 64.2% for the first nine months of 2018. |

|

Operating Expenses

| ||

|

$5.62 billion

| ||||

|

Operating expenses, compared with the third quarter of 2018, reflected higher expenses for consolidated investments (increase was primarily in depreciation and amortization, occupancy and other expenses) and higher brokerage, clearing, exchange and distribution fees, reflecting an increase in activity levels. In addition, the third quarter of 2019 included higher expenses related to technology and the firm’s credit card activities (increases were primarily in depreciation and amortization, communications and technology, professional fees and other expenses) and also included expenses related to United Capital. These increases were offset by lower compensation and benefits expenses and lower net provisions for litigation and regulatory proceedings.

Net provisions for litigation and regulatory proceedings for the third quarter of 2019 were $47 million compared with $136 million for the third quarter of 2018.

Headcount increased 6% during the third quarter of 2019, primarily reflecting the timing of campus hires and the acquisition of United Capital.

|

YTD Efficiency Ratio

| |||

|

66.2%

| ||||

Provision for Taxes

| The effective income tax rate for the first nine months of 2019 increased to 20.7% from 20.1% for the first half of 2019, primarily due to a decrease in the impact of permanent tax benefits in the first nine months of 2019 compared with the first half of 2019. |

YTD Effective Tax Rate

| |||

|

20.7%

| ||||

Other Matters

| ◾ On October 14, 2019, the Board of Directors of The Goldman Sachs Group, Inc. declared a dividend of $1.25 per common share to be paid on December 30, 2019 to common shareholders of record on December 2, 2019.

◾ During the quarter, the firm returned $1.14 billion of capital to common shareholders, including $673 million of share repurchases (3.1 million shares at an average cost of $217.66) and $466 million of common stock dividends.3

◾ Global core liquid assets3 averaged $238 billion4 for the third quarter of 2019, compared with an average of $225 billion for the second quarter of 2019. |

Declared Quarterly Dividend Per Common Share

| |||

|

$1.25

| ||||

|

Common Share Repurchases

| ||||

|

3.1 million shares for $673 million

| ||||

|

Average GCLA

| ||||

|

$238 billion

|

5

Goldman Sachs Reports

Third Quarter 2019 Earnings Results

The Goldman Sachs Group, Inc. is a leading global investment banking, securities and investment management firm that provides a wide range of financial services to a substantial and diversified client base that includes corporations, financial institutions, governments and individuals. Founded in 1869, the firm is headquartered in New York and maintains offices in all major financial centers around the world.

|

|

Cautionary Note Regarding Forward-Looking Statements |

|

This press release contains “forward-looking statements” within the meaning of the safe harbor provisions of the U.S. Private Securities Litigation Reform Act of 1995. Forward-looking statements are not historical facts, but instead represent only the firm’s beliefs regarding future events, many of which, by their nature, are inherently uncertain and outside of the firm’s control. It is possible that the firm’s actual results and financial condition may differ, possibly materially, from the anticipated results and financial condition indicated in these forward-looking statements. For information about some of the risks and important factors that could affect the firm’s future results and financial condition, see “Risk Factors” in Part I, Item 1A of the firm’s Annual Report on Form 10-K for the year ended December 31, 2018.

Information regarding the firm’s assets under supervision, capital ratios, risk-weighted assets, supplementary leverage ratio, balance sheet data, global core liquid assets and VaR consists of preliminary estimates. These estimates are forward-looking statements and are subject to change, possibly materially, as the firm completes its financial statements.

Statements about the firm’s investment banking transaction backlog also may constitute forward-looking statements. Such statements are subject to the risk that transactions may be modified or not completed at all and associated net revenues may not be realized or may be materially less than those currently expected. Important factors that could have such a result include, for underwriting transactions, a decline or weakness in general economic conditions, outbreak of hostilities, volatility in the securities markets or an adverse development with respect to the issuer of the securities and, for financial advisory transactions, a decline in the securities markets, an inability to obtain adequate financing, an adverse development with respect to a party to the transaction or a failure to obtain a required regulatory approval. For information about other important factors that could adversely affect the firm’s investment banking transactions, see “Risk Factors” in Part I, Item 1A of the firm’s Annual Report on Form 10-K for the year ended December 31, 2018.

|

|

Conference Call |

|

A conference call to discuss the firm’s financial results, outlook and related matters will be held at 11:00 am (ET). The call will be open to the public. Members of the public who would like to listen to the conference call should dial 1-888-281-7154 (in the U.S.) or 1-706-679-5627 (outside the U.S.). The number should be dialed at least 10 minutes prior to the start of the conference call. The conference call will also be accessible as an audio webcast through the Investor Relations section of the firm’s website, www.goldmansachs.com/investor-relations. There is no charge to access the call. For those unable to listen to the live broadcast, a replay will be available on the firm’s website or by dialing 1-855-859-2056 (in the U.S.) or 1-404-537- 3406 (outside the U.S.) passcode number 64774224 beginning approximately three hours after the event. Please direct any questions regarding obtaining access to the conference call to Goldman Sachs Investor Relations, via e-mail, at gs-investor- relations@gs.com.

6

Goldman Sachs Reports

Third Quarter 2019 Earnings Results

The Goldman Sachs Group, Inc. and Subsidiaries

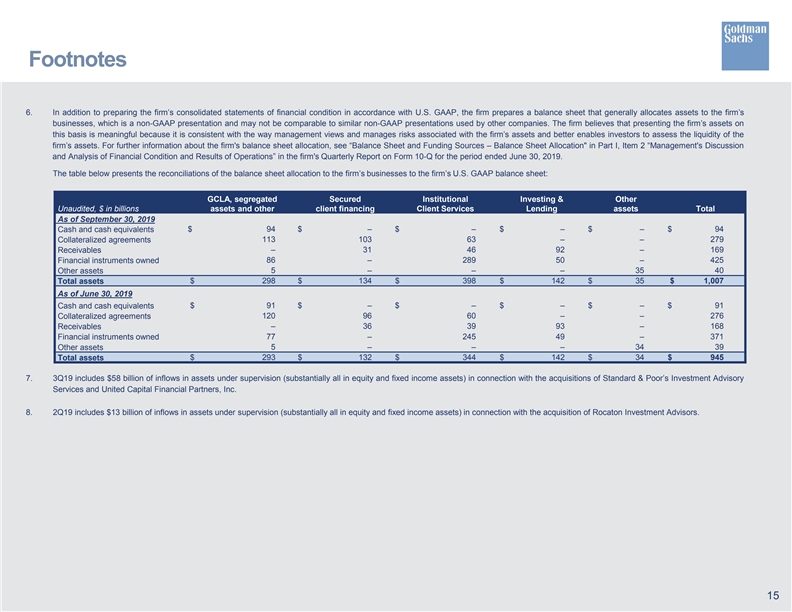

Segment Net Revenues (unaudited)6

$ in millions

| THREE MONTHS ENDED | % CHANGE FROM | |||||||||||||||||||||||

| SEPTEMBER 30, 2019 |

JUNE 30, 2019 |

SEPTEMBER 30, 2018 |

JUNE 30, 2019 |

SEPTEMBER 30, 2018 |

||||||||||||||||||||

|

INVESTMENT BANKING

|

||||||||||||||||||||||||

|

Financial Advisory |

$ 716 | $ 776 | $ 916 | (8) % | (22) % | |||||||||||||||||||

| Equity underwriting |

385 | 482 | 432 | (20) | (11) | |||||||||||||||||||

|

Debt underwriting

|

|

586

|

|

|

605

|

|

|

632

|

|

|

(3)

|

|

|

(7)

|

| |||||||||

|

Total Underwriting

|

|

971

|

|

|

1,087

|

|

|

1,064

|

|

|

(11)

|

|

|

(9)

|

| |||||||||

|

Total Investment Banking

|

|

1,687

|

|

|

1,863

|

|

|

1,980

|

|

|

(9)

|

|

|

(15)

|

| |||||||||

|

INSTITUTIONAL CLIENT SERVICES

|

||||||||||||||||||||||||

|

FICC Client Execution |

1,410 | 1,469 | 1,307 | (4) | 8 | |||||||||||||||||||

| Equities client execution |

681 | 772 | 681 | (12) | – | |||||||||||||||||||

|

Commissions and fees |

728 | 777 | 674 | (6) | 8 | |||||||||||||||||||

|

Securities services

|

|

468

|

|

|

458

|

|

|

439

|

|

|

2

|

|

|

7

|

| |||||||||

|

Total Equities

|

|

1,877

|

|

|

2,007

|

|

|

1,794

|

|

|

(6)

|

|

|

5

|

| |||||||||

|

Total Institutional Client Services

|

|

3,287

|

|

|

3,476

|

|

|

3,101

|

|

|

(5)

|

|

|

6

|

| |||||||||

|

INVESTING & LENDING

|

||||||||||||||||||||||||

|

Equity securities |

662 | 1,541 | 1,111 | (57) | (40) | |||||||||||||||||||

|

Debt securities and loans

|

|

1,019

|

|

|

989

|

|

|

924

|

|

|

3

|

|

|

10

|

| |||||||||

|

Total Investing & Lending

|

|

1,681

|

|

|

2,530

|

|

|

2,035

|

|

|

(34)

|

|

|

(17)

|

| |||||||||

|

INVESTMENT MANAGEMENT

|

||||||||||||||||||||||||

|

Management and other fees |

1,457 | 1,395 | 1,382 | 4 | 5 | |||||||||||||||||||

|

Incentive fees |

45 | 44 | 148 | 2 | (70) | |||||||||||||||||||

|

Transaction revenues

|

|

166

|

|

|

153

|

|

|

174

|

|

|

8

|

|

|

(5)

|

| |||||||||

|

Total Investment Management

|

|

1,668

|

|

|

1,592

|

|

|

1,704

|

|

|

5

|

|

|

(2)

|

| |||||||||

|

Total net revenues

|

|

$ 8,323

|

|

|

$ 9,461

|

|

|

$ 8,820

|

|

|

(12)

|

|

|

(6)

|

| |||||||||

|

Geographic Net Revenues (unaudited)3,6 |

|

|||||||||||||||||||||||

| $ in millions

|

||||||||||||||||||||||||

| THREE MONTHS ENDED | ||||||||||||||||||||||||

| SEPTEMBER 30, 2019 |

JUNE 30, 2019 |

SEPTEMBER 30, 2018 |

||||||||||||||||||||||

|

Americas |

$ 4,941 | $ 5,652 | $ 5,351 | |||||||||||||||||||||

|

EMEA |

2,329 | 2,689 | 2,254 | |||||||||||||||||||||

|

Asia

|

|

1,053

|

|

|

1,120

|

|

|

1,215

|

|

|||||||||||||||

|

Total net revenues

|

|

$ 8,323

|

|

|

$ 9,461

|

|

|

$ 8,820

|

|

|||||||||||||||

| Americas |

59% | 60% | 61% | |||||||||||||||||||||

|

EMEA |

28% | 28% | 25% | |||||||||||||||||||||

|

Asia

|

|

13%

|

|

|

12%

|

|

|

14%

|

|

|||||||||||||||

|

Total

|

|

100%

|

|

|

100%

|

|

|

100%

|

|

|||||||||||||||

7

Goldman Sachs Reports

Third Quarter 2019 Earnings Results

The Goldman Sachs Group, Inc. and Subsidiaries

Segment Net Revenues (unaudited)6

$ in millions

| NINE MONTHS ENDED | % CHANGE FROM | |||||||||||||||||||

| SEPTEMBER 30, 2019 |

SEPTEMBER 30, 2018 |

SEPTEMBER 30, 2018 |

||||||||||||||||||

|

INVESTMENT BANKING

|

||||||||||||||||||||

|

Financial Advisory |

$ 2,379 | $ 2,306 | 3 % | |||||||||||||||||

| Equity underwriting |

1,138 | 1,331 | (15) | |||||||||||||||||

|

Debt underwriting

|

|

1,843

|

|

|

2,181

|

|

|

(15)

|

|

|||||||||||

|

Total Underwriting

|

|

2,981

|

|

|

3,512

|

|

|

(15)

|

|

|||||||||||

|

Total Investment Banking

|

|

5,360

|

|

|

5,818

|

|

|

(8)

|

|

|||||||||||

|

INSTITUTIONAL CLIENT SERVICES

|

||||||||||||||||||||

| FICC Client Execution |

4,718 | 5,060 | (7) | |||||||||||||||||

| Equities client execution |

2,135 | 2,434 | (12) | |||||||||||||||||

|

Commissions and fees |

2,219 | 2,254 | (2) | |||||||||||||||||

|

Securities services

|

|

1,296

|

|

|

1,308

|

|

|

(1)

|

|

|||||||||||

|

Total Equities

|

|

5,650

|

|

|

5,996

|

|

|

(6)

|

|

|||||||||||

|

Total Institutional Client Services

|

|

10,368

|

|

|

11,056

|

|

|

(6)

|

|

|||||||||||

|

INVESTING & LENDING

|

||||||||||||||||||||

|

Equity securities |

3,050 | 3,461 | (12) | |||||||||||||||||

|

Debt securities and loans

|

|

2,998

|

|

|

2,883

|

|

|

4

|

|

|||||||||||

|

Total Investing & Lending

|

|

6,048

|

|

|

6,344

|

|

|

(5)

|

|

|||||||||||

|

INVESTMENT MANAGEMENT

|

||||||||||||||||||||

|

Management and other fees |

4,184 | 4,073 | 3 | |||||||||||||||||

|

Incentive fees |

147 | 677 | (78) | |||||||||||||||||

|

Transaction revenues

|

|

484

|

|

|

568

|

|

|

(15)

|

|

|||||||||||

|

Total Investment Management

|

|

4,815

|

|

|

5,318

|

|

|

(9)

|

|

|||||||||||

|

Total net revenues

|

|

$ 26,591

|

|

|

$ 28,536

|

|

|

(7)

|

|

|||||||||||

|

Geographic Net Revenues (unaudited)3,6 $ in millions

|

|

|||||||||||||||||||

| NINE MONTHS ENDED | ||||||||||||||||||||

| SEPTEMBER 30, 2019 |

SEPTEMBER 30, 2018 |

|||||||||||||||||||

| Americas |

$ 15,838 | $ 17,161 | ||||||||||||||||||

|

EMEA |

7,477 | 7,478 | ||||||||||||||||||

|

Asia

|

|

3,276

|

|

|

3,897

|

|

||||||||||||||

|

Total net revenues

|

|

$ 26,591

|

|

|

$ 28,536

|

|

||||||||||||||

| Americas |

60% | 60% | ||||||||||||||||||

|

EMEA |

28% | 26% | ||||||||||||||||||

|

Asia

|

|

12%

|

|

|

14%

|

|

||||||||||||||

|

Total

|

|

100%

|

|

|

100%

|

|

||||||||||||||

8

Goldman Sachs Reports

Third Quarter 2019 Earnings Results

The Goldman Sachs Group, Inc. and Subsidiaries

Consolidated Statements of Earnings (unaudited)6

In millions, except per share amounts and headcount

| THREE MONTHS ENDED | % CHANGE FROM | |||||||||||||||||||||||||

| SEPTEMBER 30, 2019 |

JUNE 30, 2019 |

SEPTEMBER 30, 2018 |

JUNE 30, 2019 |

SEPTEMBER 30, 2018 |

||||||||||||||||||||||

|

REVENUES

|

||||||||||||||||||||||||||

|

Investment banking |

$ 1,687 | $ 1,863 | $ 1,980 | (9) % | (15) % | |||||||||||||||||||||

|

Investment management |

1,556 | 1,480 | 1,580 | 5 | (2) | |||||||||||||||||||||

|

Commissions and fees |

758 | 807 | 704 | (6) | 8 | |||||||||||||||||||||

|

Market making |

2,384 | 2,423 | 2,281 | (2) | 5 | |||||||||||||||||||||

|

Other principal transactions

|

|

930

|

|

|

1,817

|

|

|

1,419

|

|

|

(49)

|

|

|

(34)

|

|

|||||||||||

|

Total non-interest revenues

|

|

7,315

|

|

|

8,390

|

|

|

7,964

|

|

|

(13)

|

|

|

(8)

|

|

|||||||||||

| Interest income |

5,459 | 5,760 | 5,061 | (5) | 8 | |||||||||||||||||||||

|

Interest expense

|

|

4,451

|

|

|

4,689

|

|

|

4,205

|

|

|

(5)

|

|

6 | |||||||||||||

|

Net interest income

|

|

1,008

|

|

|

1,071

|

|

|

856

|

|

|

(6)

|

|

|

18

|

|

|||||||||||

|

Total net revenues

|

|

8,323

|

|

|

9,461

|

|

|

8,820

|

|

|

(12)

|

|

|

(6)

|

|

|||||||||||

|

Provision for credit losses

|

|

291

|

|

|

214

|

|

|

174

|

|

|

36

|

|

|

67

|

|

|||||||||||

|

OPERATING EXPENSES

|

||||||||||||||||||||||||||

|

Compensation and benefits |

2,731 | 3,317 | 3,019 | (18) | (10) | |||||||||||||||||||||

|

Brokerage, clearing, exchange and distribution fees |

853 | 823 | 714 | 4 | 19 | |||||||||||||||||||||

|

Market development |

169 | 186 | 167 | (9) | 1 | |||||||||||||||||||||

|

Communications and technology |

283 | 290 | 250 | (2) | 13 | |||||||||||||||||||||

|

Depreciation and amortization |

473 | 399 | 317 | 19 | 49 | |||||||||||||||||||||

|

Occupancy |

252 | 234 | 203 | 8 | 24 | |||||||||||||||||||||

|

Professional fees |

350 | 302 | 310 | 16 | 13 | |||||||||||||||||||||

|

Other expenses

|

|

505

|

|

|

569

|

|

|

588

|

|

|

(11)

|

|

|

(14)

|

|

|||||||||||

|

Total operating expenses

|

|

5,616

|

|

|

6,120

|

|

|

5,568

|

|

|

(8)

|

|

|

1

|

|

|||||||||||

| Pre-tax earnings |

2,416 | 3,127 | 3,078 | (23) | (22) | |||||||||||||||||||||

|

Provision for taxes

|

|

539

|

|

|

706

|

|

|

554

|

|

|

(24)

|

|

|

(3)

|

|

|||||||||||

|

Net earnings

|

|

1,877

|

|

|

2,421

|

|

|

2,524

|

|

|

(22)

|

|

|

(26)

|

|

|||||||||||

| Preferred stock dividends

|

|

84

|

|

|

223

|

|

|

71

|

|

|

(62)

|

|

|

18

|

|

|||||||||||

|

Net earnings applicable to common shareholders

|

|

$ 1,793

|

|

|

$ 2,198

|

|

|

$ 2,453

|

|

|

(18)

|

|

|

(27)

|

|

|||||||||||

|

EARNINGS PER COMMON SHARE

|

||||||||||||||||||||||||||

|

Basic3 |

$ 4.83 | $ 5.86 | $ 6.35 | (18) % | (24) % | |||||||||||||||||||||

|

Diluted |

$ 4.79 | $ 5.81 | $ 6.28 | (18) | (24) | |||||||||||||||||||||

|

AVERAGE COMMON SHARES

|

||||||||||||||||||||||||||

|

Basic |

370.0 | 374.5 | 385.4 | (1) | (4) | |||||||||||||||||||||

|

Diluted |

374.3 | 378.0 | 390.5 | (1) | (4) | |||||||||||||||||||||

|

SELECTED DATA AT PERIOD-END

|

||||||||||||||||||||||||||

|

Common shareholders’ equity |

$ 80,809 | $ 79,689 | $ 75,559 | 1 | 7 | |||||||||||||||||||||

|

Basic shares3 |

369.3 | 372.2 | 382.9 | (1) | (4) | |||||||||||||||||||||

|

Book value per common share |

$ 218.82 | $ 214.10 | $ 197.33 | 2 | 11 | |||||||||||||||||||||

| Headcount

|

|

37,800

|

|

|

35,600

|

|

|

36,300

|

|

|

6

|

|

|

4

|

|

|||||||||||

9

Goldman Sachs Reports

Third Quarter 2019 Earnings Results

The Goldman Sachs Group, Inc. and Subsidiaries

Consolidated Statements of Earnings (unaudited)6

In millions, except per share amounts

| NINE MONTHS ENDED | % CHANGE FROM | |||||||||||||||||

| SEPTEMBER 30, 2019 |

SEPTEMBER 30, 2018 |

SEPTEMBER 30, 2018 |

||||||||||||||||

|

REVENUES

|

||||||||||||||||||

|

Investment banking |

$ 5,360 | $ 5,818 | (8) % | |||||||||||||||

|

Investment management |

4,469 | 4,947 | (10) | |||||||||||||||

|

Commissions and fees |

2,308 | 2,361 | (2) | |||||||||||||||

|

Market making |

7,346 | 8,031 | (9) | |||||||||||||||

|

Other principal transactions

|

|

3,811

|

|

|

4,603

|

|

|

(17)

|

|

|||||||||

|

Total non-interest revenues

|

|

23,294

|

|

|

25,760

|

|

|

(10)

|

|

|||||||||

| Interest income |

16,816 | 14,211 | 18 | |||||||||||||||

|

Interest expense

|

|

13,519

|

|

|

11,435

|

|

|

18

|

|

|||||||||

|

Net interest income

|

|

3,297

|

|

|

2,776

|

|

|

19

|

|

|||||||||

|

Total net revenues

|

|

26,591

|

|

|

28,536

|

|

|

(7)

|

|

|||||||||

|

Provision for credit losses

|

|

729

|

|

|

452

|

|

|

61

|

|

|||||||||

|

OPERATING EXPENSES

|

||||||||||||||||||

|

Compensation and benefits |

9,307 | 10,471 | (11) | |||||||||||||||

|

Brokerage, clearing, exchange and distribution fees |

2,438 | 2,370 | 3 | |||||||||||||||

|

Market development |

539 | 532 | 1 | |||||||||||||||

|

Communications and technology |

859 | 761 | 13 | |||||||||||||||

|

Depreciation and amortization |

1,240 | 951 | 30 | |||||||||||||||

|

Occupancy |

711 | 594 | 20 | |||||||||||||||

|

Professional fees |

950 | 897 | 6 | |||||||||||||||

|

Other expenses

|

|

1,556

|

|

|

1,735

|

|

|

(10)

|

|

|||||||||

|

Total operating expenses

|

|

17,600

|

|

|

18,311

|

|

|

(4)

|

|

|||||||||

| Pre-tax earnings |

8,262 | 9,773 | (15) | |||||||||||||||

|

Provision for taxes

|

|

1,713

|

|

|

1,852

|

|

|

(8)

|

|

|||||||||

|

Net earnings

|

|

6,549

|

|

|

7,921

|

|

|

(17)

|

|

|||||||||

|

Preferred stock dividends

|

|

376

|

|

|

383

|

|

|

(2)

|

|

|||||||||

|

Net earnings applicable to common shareholders

|

|

$ 6,173

|

|

|

$ 7,538

|

|

|

(18)

|

|

|||||||||

|

EARNINGS PER COMMON SHARE

|

||||||||||||||||||

|

Basic3 |

$ 16.43 | $ 19.42 | (15) % | |||||||||||||||

|

Diluted |

$ 16.32 | $ 19.21 | (15) | |||||||||||||||

|

AVERAGE COMMON SHARES

|

||||||||||||||||||

|

Basic |

374.7 | 387.4 | (3) | |||||||||||||||

|

Diluted

|

|

378.2

|

|

|

392.3

|

|

|

(4)

|

|

|||||||||

10

Goldman Sachs Reports

Third Quarter 2019 Earnings Results

The Goldman Sachs Group, Inc. and Subsidiaries

Condensed Consolidated Statements of Financial Condition (unaudited)4

$ in billions

| AS OF | ||||||||||||||||

| SEPTEMBER 30, 2019 |

JUNE 30, 2019 |

|||||||||||||||

|

ASSETS

|

||||||||||||||||

|

Cash and cash equivalents |

$ 94 | $ 91 | ||||||||||||||

|

Collateralized agreements |

279 | 276 | ||||||||||||||

|

Receivables |

169 | 168 | ||||||||||||||

|

Financial instruments owned |

425 | 371 | ||||||||||||||

|

Other assets

|

|

40

|

|

|

39

|

|

||||||||||

|

Total assets

|

|

$ 1,007

|

|

|

$ 945

|

|

||||||||||

|

LIABILITIES AND SHAREHOLDERS’ EQUITY

|

||||||||||||||||

|

Deposits |

$ 183 | $ 166 | ||||||||||||||

|

Collateralized financings |

140 | 103 | ||||||||||||||

|

Payables |

188 | 185 | ||||||||||||||

|

Financial instruments sold, but not yet purchased |

116 | 111 | ||||||||||||||

|

Unsecured short-term borrowings |

52 | 50 | ||||||||||||||

|

Unsecured long-term borrowings |

217 | 221 | ||||||||||||||

|

Other liabilities

|

|

19

|

|

|

18

|

|

||||||||||

|

Total liabilities

|

|

915

|

|

|

854

|

|

||||||||||

|

Shareholders’ equity

|

|

92

|

|

|

91

|

|

||||||||||

|

Total liabilities and shareholders’ equity

|

|

$ 1,007

|

|

|

$ 945

|

|

||||||||||

|

Capital Ratios and Supplementary Leverage Ratio (unaudited)3,4 $ in billions

|

|

|||||||||||||||

| AS OF | ||||||||||||||||

| SEPTEMBER 30, 2019 |

JUNE 30, 2019 |

|||||||||||||||

|

Common equity tier 1 capital |

$ 75.7 | $ 75.6 | ||||||||||||||

|

STANDARDIZED CAPITAL RULES

|

||||||||||||||||

|

Risk-weighted assets |

$ 557 | $ 548 | ||||||||||||||

|

Common equity tier 1 capital ratio |

13.6% | 13.8% | ||||||||||||||

|

BASEL III ADVANCED CAPITAL RULES

|

||||||||||||||||

|

Risk-weighted assets |

$ 566 | $ 559 | ||||||||||||||

|

Common equity tier 1 capital ratio |

13.4% | 13.5% | ||||||||||||||

| Supplementary leverage ratio |

6.2% | 6.4% | ||||||||||||||

|

Average Daily VaR (unaudited)3,4 $ in millions

|

|

|||||||||||||||

| THREE MONTHS ENDED | ||||||||||||||||

| SEPTEMBER 30, 2019 |

JUNE 30, 2019 |

|||||||||||||||

|

RISK CATEGORIES

|

||||||||||||||||

|

Interest rates |

$ 49 | $ 41 | ||||||||||||||

|

Equity prices |

28 | 27 | ||||||||||||||

|

Currency rates |

12 | 10 | ||||||||||||||

|

Commodity prices |

12 | 12 | ||||||||||||||

|

Diversification effect

|

|

(43)

|

|

|

(38)

|

|

||||||||||

|

Total

|

|

$ 58

|

|

|

$ 52

|

|

||||||||||

11

Goldman Sachs Reports

Third Quarter 2019 Earnings Results

The Goldman Sachs Group, Inc. and Subsidiaries

Assets Under Supervision (unaudited)3,4

$ in billions

| AS OF | ||||||||||||||||||||||||

| SEPTEMBER 30, 2019 |

JUNE 30, 2019 |

SEPTEMBER 30, 2018 |

||||||||||||||||||||||

|

ASSET CLASS

|

||||||||||||||||||||||||

|

Alternative investments

|

|

$ 182

|

|

|

$ 174

|

|

|

$ 175

|

|

|||||||||||||||

| Equity

|

|

392

|

|

|

350

|

|

|

349

|

|

|||||||||||||||

| Fixed income

|

|

784

|

|

|

749

|

|

|

668

|

|

|||||||||||||||

|

Total long-term AUS

|

|

1,358

|

|

|

1,273

|

|

|

1,192

|

|

|||||||||||||||

|

Liquidity products

|

|

404

|

|

|

387

|

|

|

358

|

|

|||||||||||||||

|

Total AUS

|

|

$ 1,762

|

|

|

$ 1,660

|

|

|

$ 1,550

|

|

|||||||||||||||

| THREE MONTHS ENDED | ||||||||||||||||||||||||

| SEPTEMBER 30, 2019 |

JUNE 30, 2019 |

SEPTEMBER 30, 2018 |

||||||||||||||||||||||

|

Beginning balance

|

|

$ 1,660

|

|

|

$ 1,599

|

|

|

$ 1,513

|

|

|||||||||||||||

| Net inflows / (outflows):

|

||||||||||||||||||||||||

| Alternative investments

|

|

8

|

|

|

1

|

|

|

3

|

|

|||||||||||||||

| Equity

|

|

41

|

|

|

4

|

|

|

7

|

|

|||||||||||||||

| Fixed income

|

|

20

|

|

|

12

|

|

|

3

|

|

|||||||||||||||

|

Total long-term AUS net inflows / (outflows)

|

|

69

|

|

|

17

|

|

|

13

|

|

|||||||||||||||

|

Liquidity products

|

|

17

|

|

|

12

|

|

|

8

|

|

|||||||||||||||

|

Total AUS net inflows / (outflows)

|

|

86

|

5

|

|

29

|

7

|

|

21

|

|

|||||||||||||||

|

Net market appreciation / (depreciation)

|

|

16

|

|

|

32

|

|

|

16

|

|

|||||||||||||||

|

Ending balance

|

|

$ 1,762

|

|

|

$ 1,660

|

|

|

$ 1,550

|

|

|||||||||||||||

12

Goldman Sachs Reports

Third Quarter 2019 Earnings Results

|

Footnotes |

|

|

| 1. | Annualized ROE is calculated by dividing annualized net earnings applicable to common shareholders by average monthly common shareholders’ equity. Annualized ROTE is calculated by dividing annualized net earnings applicable to common shareholders by average monthly tangible common shareholders’ equity (tangible common shareholders’ equity is calculated as total shareholders’ equity less preferred stock, goodwill and identifiable intangible assets). Management believes that ROTE is meaningful because it measures the performance of businesses consistently, whether they were acquired or developed internally, and that tangible common shareholders’ equity is meaningful because it is a measure that the firm and investors use to assess capital adequacy. ROTE and tangible common shareholders’ equity are non-GAAP measures and may not be comparable to similar non-GAAP measures used by other companies. |

The table below presents average equity and a reconciliation of average common shareholders’ equity to average tangible common shareholders’ equity:

| AVERAGE FOR THE | ||||||||||||

| Unaudited, $ in millions | THREE MONTHS ENDED SEPTEMBER 30, 2019 |

NINE MONTHS ENDED SEPTEMBER 30, 2019 |

||||||||||

|

Total shareholders’ equity

|

|

$ 91,054

|

|

|

$ 90,265

|

|

||||||

| Preferred stock

|

|

(11,203)

|

|

|

(11,203)

|

|

||||||

|

Common shareholders’ equity

|

|

79,851

|

|

|

79,062

|

|

||||||

|

Goodwill and identifiable intangible assets

|

|

(4,704)

|

|

|

(4,347)

|

|

||||||

|

Tangible common shareholders’ equity

|

|

$ 75,147

|

|

|

$ 74,715

|

|

||||||

| 2. | Dealogic – January 1, 2019 through September 30, 2019. |

| 3. | For information about the following items, see the referenced sections in Part I, Item 2 “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in the firm’s Quarterly Report on Form 10-Q for the period ended June 30, 2019: (i) investment banking transaction backlog – see “Results of Operations – Investment Banking” (ii) assets under supervision – see “Results of Operations – Investment Management” (iii) efficiency ratio – see “Results of Operations – Operating Expenses” (iv) share repurchase program – see “Equity Capital Management and Regulatory Capital – Equity Capital Management” (v) global core liquid assets – see “Risk Management – Liquidity Risk Management” (vi) basic shares – see “Balance Sheet and Funding Sources – Balance Sheet Analysis and Metrics” and (vii) VaR – see “Risk Management – Market Risk Management.” |

For information about the following items, see the referenced sections in Part I, Item 1 “Financial Statements (Unaudited)” in the firm’s Quarterly Report on Form 10-Q for the period ended June 30, 2019: (i) risk-based capital ratios and supplementary leverage ratio – see Note 20 “Regulation and Capital Adequacy” (ii) geographic net revenues – see Note 25 “Business Segments” and (iii) unvested share-based awards that have non-forfeitable rights to dividends or dividend equivalents in calculating basic EPS – see Note 21 “Earnings Per Common Share.”

| 4. | Represents a preliminary estimate for the third quarter of 2019 and may be revised in the firm’s Quarterly Report on Form 10-Q for the period ended September 30, 2019. |

| 5. | Includes $58 billion of inflows in assets under supervision (substantially all in equity and fixed income assets) in connection with the acquisitions of Standard & Poor’s Investment Advisory Services and United Capital Financial Partners, Inc. |

| 6. | The following reclassifications have been made to previously reported amounts for the third quarter and first nine months of 2018 to conform to the current presentation: (i) provision for credit losses, previously reported in other principal transactions revenues (and Investing & Lending segment net revenues), is now reported as a separate line item in the consolidated statements of earnings and (ii) headcount consists of the firm’s employees, and excludes consultants and temporary staff previously reported as part of total staff. As a result, expenses related to these consultants and temporary staff, previously reported in compensation and benefits, are now reported in professional fees. |

| 7. | Includes $13 billion of inflows in assets under supervision (substantially all in equity and fixed income assets) in connection with the acquisition of Rocaton Investment Advisors. |

13