Exhibit 99.1

|

Full Year and Fourth Quarter 2018 Earnings Results

Media Relations: Jake Siewert 212-902-5400 Investor Relations: Heather Kennedy Miner 212-902-0300

|

||

|

The Goldman Sachs Group, Inc. 200 West Street | New York, NY 10282

|

Full Year and Fourth Quarter 2018 Earnings Results

Goldman Sachs Reports Earnings Per Common Share of $25.27 for 2018

Fourth Quarter Earnings Per Common Share was $6.04

|

“We are pleased with our performance for the year, achieving stronger top and bottom line results despite a challenging backdrop for our market-making businesses in the second half. For the year, we delivered double-digit revenue growth, the highest earnings per share in the firm’s history and the strongest return on equity since 2009. We are confident that we are well positioned to support an even larger universe of clients, continue to diversify our revenue mix and deliver strong returns for our shareholders in the years ahead.” |

|

- David M. Solomon, Chairman and Chief Executive Officer

|

| NEW YORK, January 16, 2019 – The Goldman Sachs Group, Inc. (NYSE: GS) today reported net revenues (1) of $36.62 billion and net earnings of $10.46 billion for the year ended December 31, 2018. Net revenues (1) were $8.08 billion and net earnings were $2.54 billion for the fourth quarter of 2018.

Diluted earnings per common share (EPS) was $25.27 (2) for the year ended December 31, 2018 compared with $9.01 (2) for the year ended December 31, 2017, and was $6.04 (2) for the fourth quarter of 2018 compared with a diluted loss per common share of $5.51 (2) for the fourth quarter of 2017 and diluted earnings per common share of $6.28 for the third quarter of 2018.

Return on average common shareholders’ equity (ROE) (3) was 13.3% (2) for 2018 and annualized ROE was 12.1% for the fourth quarter of 2018. Return on average tangible common shareholders’ equity (ROTE) (3) was 14.1% (2) for 2018 and annualized ROTE was 12.8% for the fourth quarter of 2018. |

NET REVENUES

| |||||

|

2018 |

$36.62 billion | |||||

| 4Q18

|

$8.08 billion

| |||||

|

NET EARNINGS

| ||||||

|

2018 |

$10.46 billion | |||||

| 4Q18

|

$2.54 billion

| |||||

|

EPS

| ||||||

|

2018 |

$25.27 | |||||

| 4Q18

|

$6.04

| |||||

|

ROE

| ||||||

|

2018 |

13.3% | |||||

| 4Q18

|

12.1%

| |||||

|

ROTE

| ||||||

|

2018 |

14.1% | |||||

| 4Q18

|

12.8%

| |||||

1

Goldman Sachs Reports

Full Year and Fourth Quarter 2018 Earnings Results

|

|

Annual Highlights |

|

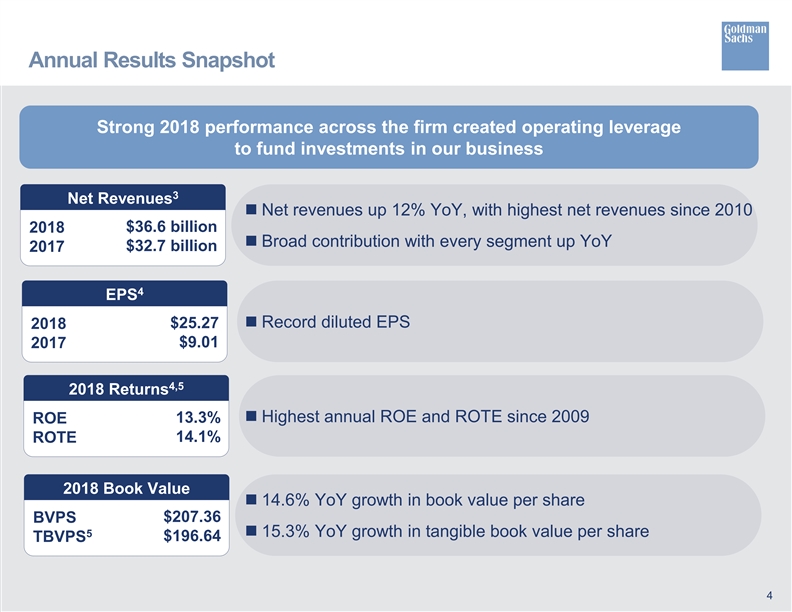

| ◾ | Net revenues of $36.62 billion and pre-tax earnings of $12.48 billion were both 12% higher compared with 2017 and the highest since 2010. |

| ◾ | The firm ranked #1 in worldwide announced and completed mergers and acquisitions, equity and equity-related offerings and common stock offerings for the year. (4) |

| ◾ | Investment Banking produced net revenues of $7.86 billion, reflecting the highest net revenues in Financial Advisory since 2007 and a strong performance in Underwriting. |

| ◾ | Equities generated net revenues of $7.60 billion, 15% higher than 2017 and the highest since 2015. |

| ◾ | Net revenues in Investing & Lending were $8.25 billion, which included record net interest income in debt securities and loans of approximately $2.70 billion. |

| ◾ | Investment Management produced record net revenues of $7.02 billion, including record management and other fees. Assets under supervision (5) of $1.54 trillion included net inflows of $89 billion during the year, with net inflows of $37 billion in long-term assets under supervision. |

| ◾ | Diluted EPS of $25.27 was a record and ROE (3) of 13.3% was the highest since 2009. |

| ◾ | Book value per common share increased 14.6% during the year to $207.36 and tangible book value per common share (3) increased 15.3% to $196.64. |

| ◾ | The Standardized and Basel III Advanced common equity tier 1 ratios (5) increased 140 basis points and 240 basis points, respectively, compared with the fully phased-in ratios at the end of 2017 (6) to 13.3% (7) and 13.1% (7). |

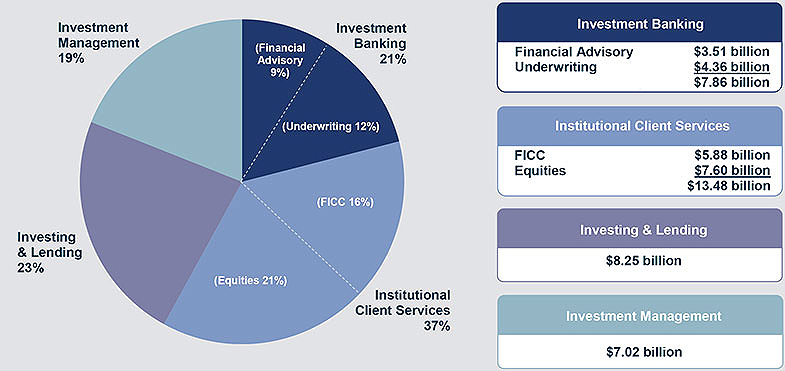

Full Year Net Revenue Mix by Segment

2

Goldman Sachs Reports

Full Year and Fourth Quarter 2018 Earnings Results

|

Net Revenues |

|

|

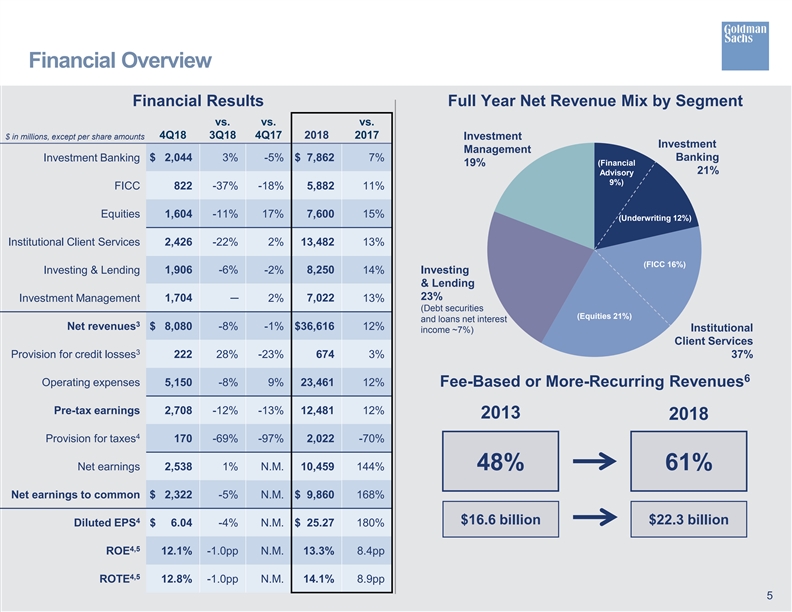

| Full Year Net revenues (1) were $36.62 billion for 2018, 12% higher than 2017, reflecting higher net revenues across all segments.

Fourth Quarter Net revenues (1) were $8.08 billion for the fourth quarter of 2018, essentially unchanged compared with the fourth quarter of 2017 and 8% lower than the third quarter of 2018. |

|

|||

|

2018 NET REVENUES

| ||||

|

$36.62 billion

| ||||

|

4Q18 NET REVENUES

| ||||

|

$8.08 billion

| ||||

|

|

|

Investment Banking |

|

|

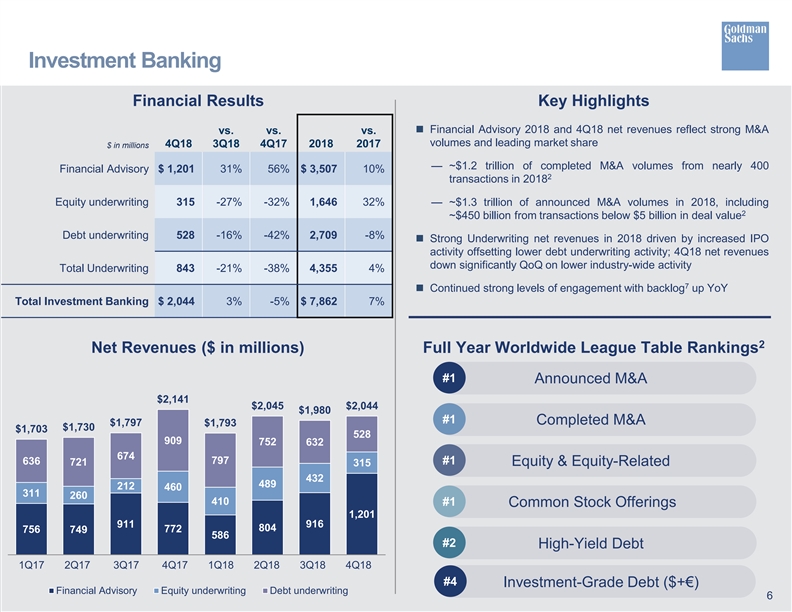

| Full Year Net revenues in Investment Banking were $7.86 billion for 2018, 7% higher than 2017.

Net revenues in Financial Advisory were $3.51 billion, 10% higher than 2017, reflecting an increase in industry-wide completed mergers and acquisitions volumes.

Net revenues in Underwriting were $4.36 billion, 4% higher than 2017, due to significantly higher net revenues in equity underwriting, driven by initial public offerings, partially offset by lower net revenues in debt underwriting, reflecting a decline in leveraged finance activity.

The firm’s investment banking transaction backlog (5) increased compared with the end of 2017. |

||||||

|

2018 INVESTMENT BANKING

| ||||||

|

$7.86 billion

| ||||||

|

|

Financial Advisory |

$3.51 billion | ||||

| Underwriting

|

$4.36 billion

| |||||

|

Fourth Quarter Net revenues in Investment Banking were $2.04 billion for the fourth quarter of 2018, 5% lower than the fourth quarter of 2017 and 3% higher than the third quarter of 2018.

Net revenues in Financial Advisory were $1.20 billion, 56% higher than the fourth quarter of 2017, reflecting an increase in industry-wide completed mergers and acquisitions volumes.

Net revenues in Underwriting were $843 million, 38% lower than the fourth quarter of 2017, due to significantly lower net revenues in both debt underwriting, reflecting a decline in leveraged finance activity, and equity underwriting, reflecting a decline in secondary offerings.

The firm’s investment banking transaction backlog (5) decreased compared with the end of the third quarter of 2018. |

||||||

|

4Q18 INVESTMENT BANKING

| ||||||

|

$2.04 billion

| ||||||

| Financial Advisory |

$1.20 billion | |||||

| Underwriting

|

$843 million

| |||||

3

Goldman Sachs Reports

Full Year and Fourth Quarter 2018 Earnings Results

|

|

|

Institutional Client Services |

|

|

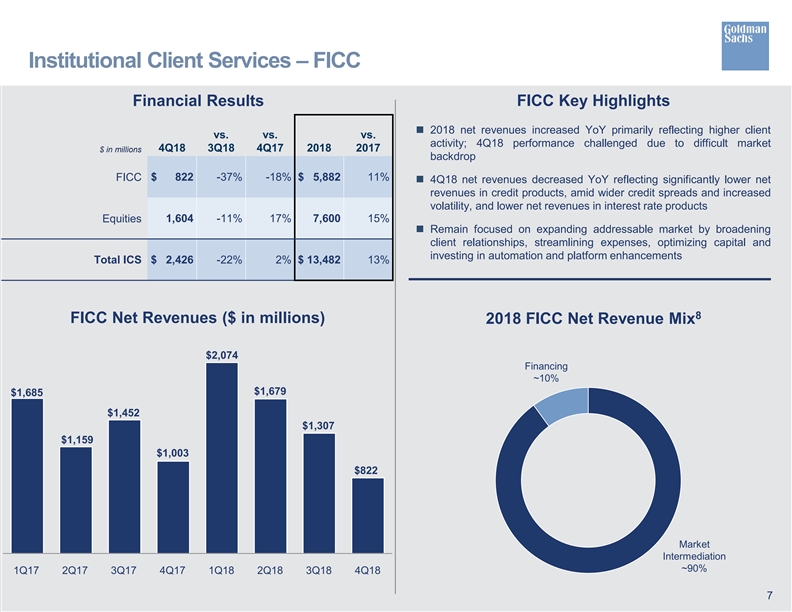

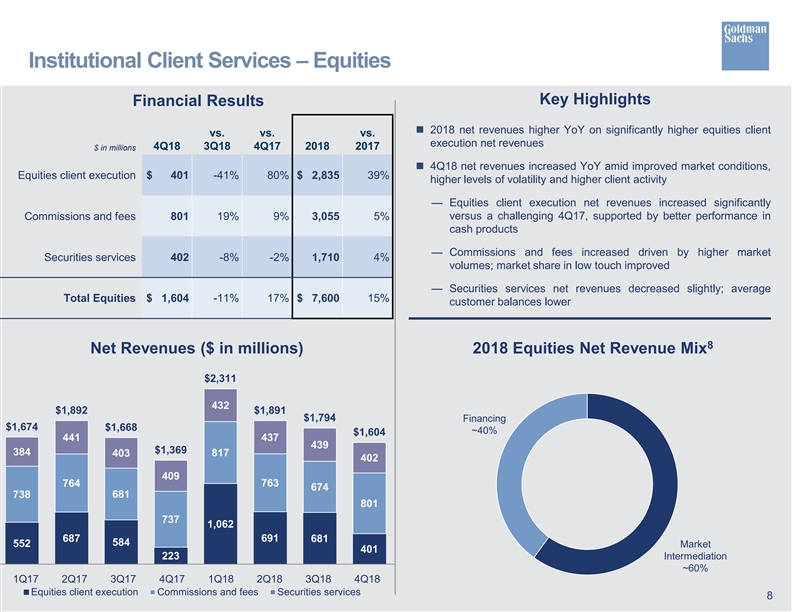

| Full Year Net revenues in Institutional Client Services were $13.48 billion for 2018, 13% higher than 2017.

Net revenues in Fixed Income, Currency and Commodities (FICC) Client Execution were $5.88 billion, 11% higher than 2017, reflecting significantly higher net revenues in commodities and currencies. Net revenues in interest rate products and mortgages were slightly lower, while net revenues in credit products were essentially unchanged. During 2018, FICC Client Execution operated in an environment characterized by higher client activity and generally less challenging market conditions compared with 2017.

Net revenues in Equities were $7.60 billion, 15% higher than 2017, primarily due to significantly higher net revenues in equities client execution, reflecting significantly higher net revenues in both cash products and derivatives. In addition, commissions and fees were higher, reflecting higher market volumes, and net revenues in securities services were slightly higher. During 2018, Equities operated in an environment characterized by generally higher volatility and improved client activity compared with 2017. |

||||||

|

2018 INSTITUTIONAL CLIENT SERVICES | ||||||

|

$13.48 billion | ||||||

|

FICC |

$5.88 billion | |||||

| Equities |

$7.60 billion | |||||

|

|

||||||

|

Fourth Quarter Net revenues in Institutional Client Services were $2.43 billion for the fourth quarter of 2018, 2% higher than the fourth quarter of 2017 and 22% lower than the third quarter of 2018.

Net revenues in FICC Client Execution were $822 million, 18% lower than the fourth quarter of 2017, reflecting significantly lower net revenues in credit products and lower net revenues in interest rate products. Net revenues in commodities, currencies and mortgages were essentially unchanged. During the quarter, FICC Client Execution operated in an environment characterized by challenging market conditions, including wider credit spreads, compared with the third quarter of 2018.

Net revenues in Equities were $1.60 billion, 17% higher than the fourth quarter of 2017, primarily due to significantly higher net revenues in equities client execution compared with a challenging prior year period. This increase reflected significantly higher net revenues in cash products, while net revenues in derivatives were essentially unchanged. Commissions and fees were higher, reflecting higher market volumes, and net revenues in securities services were slightly lower. During the quarter, Equities operated in an environment generally characterized by higher volatility but less favorable market conditions compared with the third quarter of 2018. |

||||||

|

4Q18 INSTITUTIONAL CLIENT SERVICES | ||||||

|

$2.43 billion | ||||||

|

FICC |

$822 million | |||||

| Equities |

$1.60 billion | |||||

4

Goldman Sachs Reports

Full Year and Fourth Quarter 2018 Earnings Results

|

|

Investing & Lending |

|

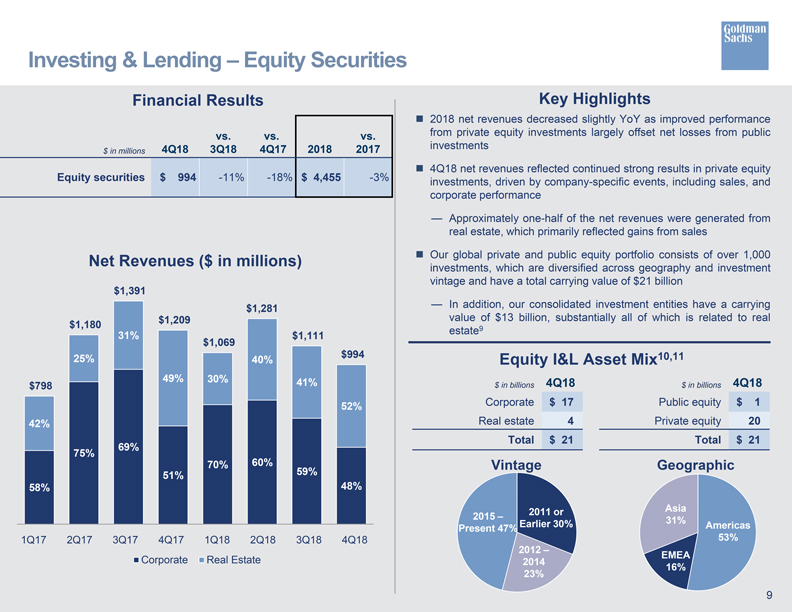

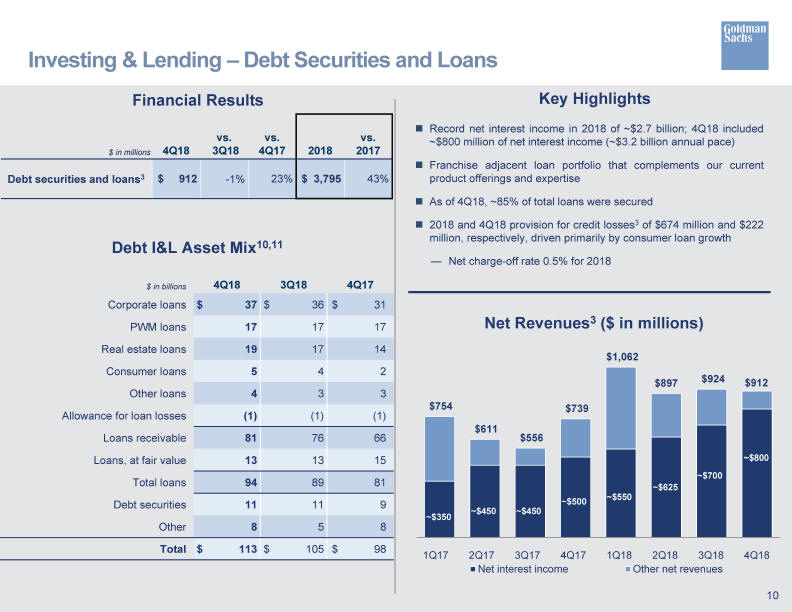

| Full Year Net revenues in Investing & Lending were $8.25 billion for 2018, 14% higher than 2017.

Net revenues in equity securities were $4.46 billion, 3% lower than 2017, reflecting net losses from investments in public equities compared with net gains in the prior year, partially offset by significantly higher net gains from investments in private equities, driven by company-specific events, including sales, and corporate performance.

Net revenues in debt securities and loans were $3.80 billion, 43% higher than 2017, primarily driven by significantly higher net interest income. 2018 included net interest income of approximately $2.70 billion compared with approximately $1.80 billion in 2017. |

||||||

|

2018 INVESTING & LENDING

| ||||||

|

$8.25 billion

| ||||||

| Equity Securities |

$4.46 billion | |||||

| Debt Securities and Loans |

$3.80 billion

| |||||

|

|

||||||

|

Fourth Quarter Net revenues in Investing & Lending were $1.91 billion for the fourth quarter of 2018, 2% lower than the fourth quarter of 2017 and 6% lower than the third quarter of 2018.

Net revenues in equity securities were $994 million, 18% lower than the fourth quarter of 2017, reflecting net losses from investments in public equities, as global equity prices decreased during the quarter. Net revenues in equity securities for the fourth quarter of 2018 included $1.26 billion of net gains from investments in private equities, driven by company-specific events, including sales, and corporate performance.

Net revenues in debt securities and loans were $912 million, 23% higher than the fourth quarter of 2017, driven by significantly higher net interest income. The fourth quarter of 2018 included net interest income of approximately $800 million compared with approximately $500 million in the fourth quarter of 2017. |

||||||

|

4Q18 INVESTING & LENDING

| ||||||

|

$1.91 billion

| ||||||

| Equity Securities |

$994 million | |||||

| Debt Securities and Loans |

$912 million

| |||||

|

|

Investment Management |

|

| Full Year Net revenues in Investment Management were $7.02 billion for 2018, 13% higher than 2017.

The increase in net revenues compared with 2017 was primarily due to significantly higher incentive fees, as a result of harvesting. Management and other fees were also higher, reflecting higher average assets under supervision and the impact of the recently adopted revenue recognition standard (8), partially offset by shifts in the mix of client assets and strategies. In addition, transaction revenues were higher.

During the year, total assets under supervision (5) increased $48 billion to $1.54 trillion. Long-term assets under supervision decreased $4 billion, including net market depreciation of $41 billion, primarily in equity assets, largely offset by net inflows of $37 billion, primarily in fixed income and equity assets. Liquidity products increased $52 billion. |

||||||

|

2018 INVESTMENT

| ||||||

|

$7.02 billion

| ||||||

| Management and Other Fees |

$5.44 billion | |||||

| Incentive Fees Transaction Revenues |

$830 million

$754 million

| |||||

|

|

||||||

5

Goldman Sachs Reports

Full Year and Fourth Quarter 2018 Earnings Results

|

|

|

Investment Management |

|

|

| Fourth Quarter Net revenues in Investment Management were $1.70 billion for the fourth quarter of 2018, 2% higher than the fourth quarter of 2017 and unchanged compared with the third quarter of 2018.

The increase compared with the fourth quarter of 2017 reflected higher incentive fees and transaction revenues. Management and other fees were essentially unchanged compared with the fourth quarter of 2017.

During the quarter, total assets under supervision (5) decreased $8 billion to $1.54 trillion. Long-term assets under supervision decreased $47 billion, including net market depreciation of $50 billion, primarily in equity assets, partially offset by net inflows of $3 billion. Liquidity products increased $39 billion. |

||||||

|

4Q18 INVESTMENT MANAGEMENT

| ||||||

|

$1.70 billion

| ||||||

|

Management and Other Fees |

$1.37 billion | |||||

| Incentive Fees |

$153 million | |||||

| Transaction Revenues

|

$186 million

| |||||

|

|

||||||

Provision for Credit Losses

| Full Year Provision for credit losses (1) was $674 million for 2018, compared with $657 million for 2017, as higher provision for credit losses primarily related to consumer loan growth in 2018 were partially offset by an impairment of a secured loan in 2017.

Fourth Quarter Provision for credit losses (1) was $222 million for the fourth quarter of 2018, compared with $290 million for the fourth quarter of 2017 and $174 million for the third quarter of 2018. The decrease compared with the fourth quarter of 2017 reflected an impairment of a secured loan in the fourth quarter of 2017, partially offset by higher provision for credit losses primarily related to consumer loan growth in the fourth quarter of 2018. |

||||

|

2018 PROVISION FOR CREDIT LOSSES

| ||||

|

$674 million

| ||||

|

4Q18 PROVISION FOR CREDIT LOSSES

| ||||

|

$222 million

| ||||

6

Goldman Sachs Reports

Full Year and Fourth Quarter 2018 Earnings Results

|

Operating Expenses |

|

|

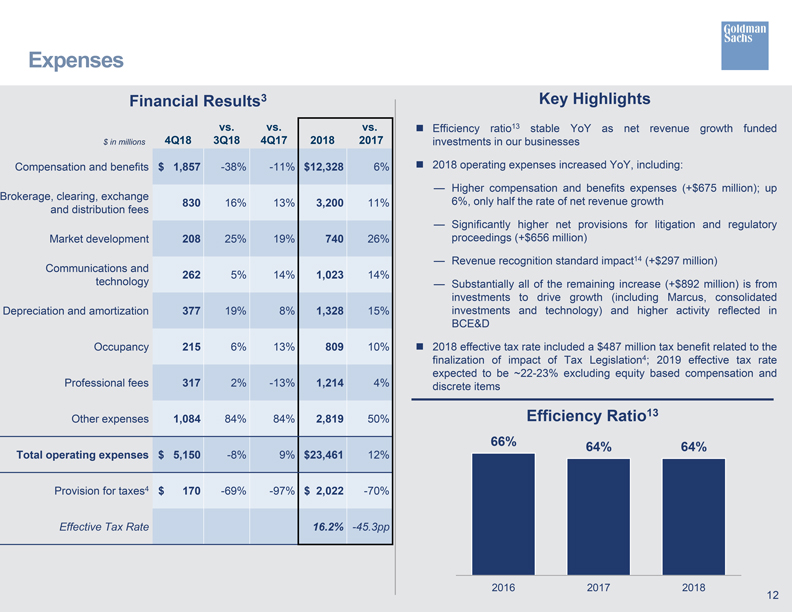

| Full Year Operating expenses were $23.46 billion for 2018, 12% higher than 2017. The firm’s efficiency ratio (9) for 2018 was 64.1%, compared with 64.0% for 2017.

The increase in operating expenses compared with 2017 was primarily due to higher compensation and benefits expenses, reflecting improved operating performance, and significantly higher net provisions for litigation and regulatory proceedings. Brokerage, clearing, exchange and distribution fees were also higher, reflecting an increase in activity levels, and technology expenses increased, reflecting higher expenses related to computing services. In addition, expenses related to consolidated investments and the firm’s digital lending and deposit platform increased, with the increases primarily in depreciation and amortization expenses, market development expenses and other expenses. The increase compared with 2017 also included $297 million related to the recently adopted revenue recognition standard (8).

Net provisions for litigation and regulatory proceedings for 2018 were $844 million compared with $188 million for 2017.

Headcount (1) increased 9% during 2018, reflecting an increase in technology professionals and investments in new business initiatives. |

|

|||

|

2018 OPERATING EXPENSES

| ||||

|

$23.46 billion

| ||||

|

2018 EFFICIENCY RATIO

| ||||

|

64.1%

| ||||

|

Fourth Quarter Operating expenses were $5.15 billion for the fourth quarter of 2018, 9% higher than the fourth quarter of 2017 and 8% lower than the third quarter of 2018.

The increase in operating expenses compared with the fourth quarter of 2017 primarily reflected significantly higher net provisions for litigation and regulatory proceedings. The increase compared with the fourth quarter of 2017 also included $79 million related to the recently adopted revenue recognition standard (8) . These increases were partially offset by lower compensation and benefits expenses.

Net provisions for litigation and regulatory proceedings for the fourth quarter of 2018 were $516 million compared with $9 million for the fourth quarter of 2017.

The fourth quarter of 2018 included a $132 million charitable contribution to Goldman Sachs Gives. Compensation was reduced to fund this charitable contribution to Goldman Sachs Gives. |

|

|||

|

4Q18 OPERATING EXPENSES

| ||||

|

$5.15 billion

| ||||

Provision for Taxes

| The effective income tax rate for 2018 was 16.2%, down from 19.0% for the first nine months of 2018 and down from 61.5% for full year 2017, as 2017 included the estimated impact of Tax Legislation (2), which increased the effective income tax rate by 39.5 percentage points. The finalization of this impact of Tax Legislation (2) reduced the effective income tax rate for 2018 by 3.9 percentage points. |

|

|||

|

2018 EFFECTIVE TAX RATE

| ||||

|

16.2%

| ||||

7

Goldman Sachs Reports

Full Year and Fourth Quarter 2018 Earnings Results

|

Capital |

|

|

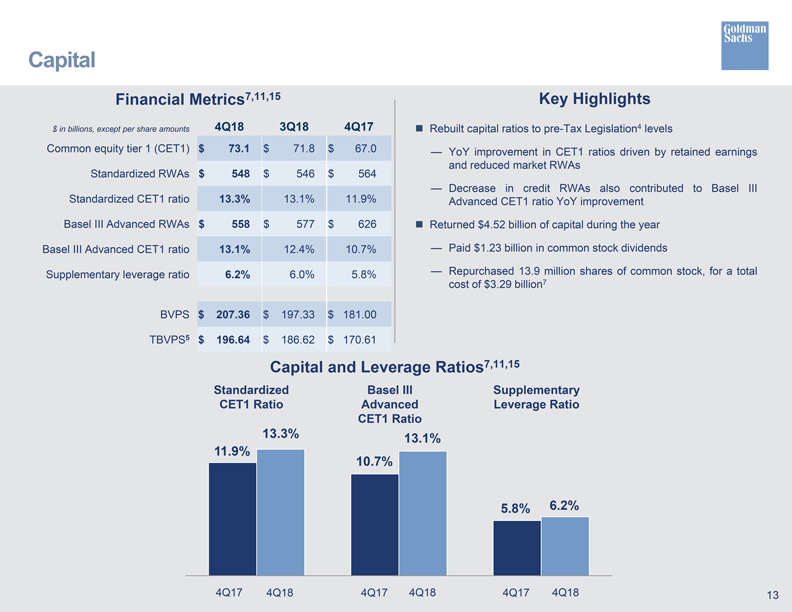

| ◾ Total shareholders’ equity was $90.19 billion (common shareholders’ equity of $78.98 billion and preferred stock of $11.20 billion) as of December 31, 2018.

◾ The Standardized common equity tier 1 ratio (5) was 13.3% (7) as of December 31, 2018, compared with 11.9% (6) as of December 31, 2017 and 13.1% as of September 30, 2018.

◾ The Basel III Advanced common equity tier 1 ratio (5) was 13.1% (7) as of December 31, 2018, compared with 10.7% (6) as of December 31, 2017 and 12.4% as of September 30, 2018.

◾ The supplementary leverage ratio (5) was 6.2% (7) as of December 31, 2018, compared with 5.8% as of December 31, 2017 and 6.0% as of September 30, 2018.

◾ On January 15, 2019, the Board of Directors of The Goldman Sachs Group, Inc. declared a dividend of $0.80 per common share to be paid on March 28, 2019 to common shareholders of record on February 28, 2019.

◾ During the year, the firm repurchased 13.9 million shares of common stock at an average cost per share of $236.22, for a total cost of $3.29 billion. This included 5.6 million shares repurchased during the fourth quarter at an average cost per share of $222.30, for a total cost of $1.25 billion. (5)

◾ Book value per common share was $207.36 and tangible book value per common share (3) was $196.64, both based on basic shares (10) of 380.9 million as of December 31, 2018. |

TOTAL SHAREHOLDERS’ EQUITY

| |||

|

$90.19 billion

| ||||

|

STANDARDIZED RATIO

| ||||

|

13.3%

| ||||

|

ADVANCED RATIO

| ||||

|

13.1%

| ||||

|

SUPPLEMENTARY LEVERAGE RATIO

| ||||

|

6.2%

| ||||

|

DECLARED QUARTERLY DIVIDEND PER COMMON SHARE

| ||||

|

$0.80

| ||||

|

COMMON SHARE REPURCHASES

| ||||

|

13.9 million shares for $3.29 billion in 2018

| ||||

|

BOOK VALUE PER COMMON SHARE

| ||||

|

$207.36

|

Other Balance Sheet and Liquidity Metrics

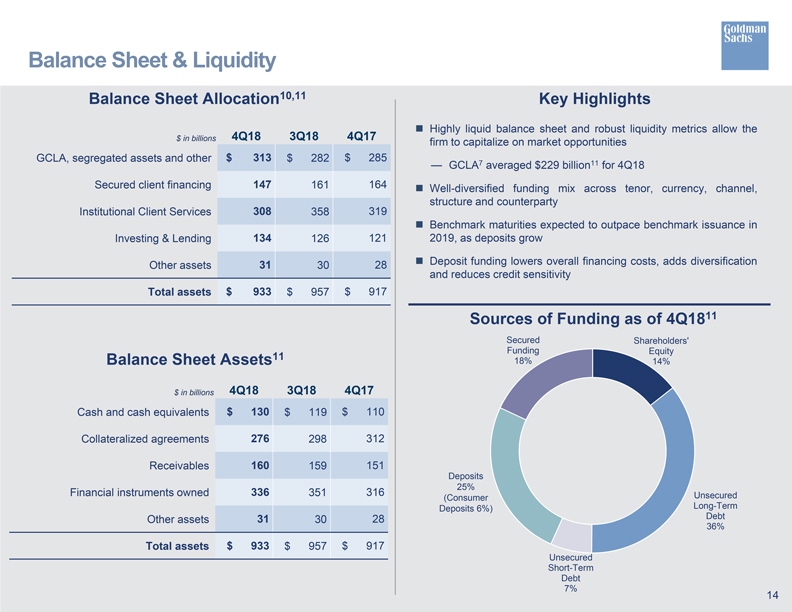

| ◾ Total assets were $933 billion (7) as of December 31, 2018, compared with $917 billion as of December 31, 2017 and $957 billion as of September 30, 2018.

◾ Global core liquid assets (5) averaged $233 billion (7) for 2018, compared with an average of $219 billion for 2017. Global core liquid assets averaged $229 billion (7) for the fourth quarter of 2018, compared with an average of $238 billion for the third quarter of 2018. |

TOTAL ASSETS

| |||

|

$933 billion

| ||||

|

AVERAGE GCLA

| ||||

|

$233 billion for 2018

| ||||

8

Goldman Sachs Reports

Full Year and Fourth Quarter 2018 Earnings Results

The Goldman Sachs Group, Inc. is a leading global investment banking, securities and investment management firm that provides a wide range of financial services to a substantial and diversified client base that includes corporations, financial institutions, governments and individuals. Founded in 1869, the firm is headquartered in New York and maintains offices in all major financial centers around the world.

|

|

Cautionary Note Regarding Forward-Looking Statements |

|

This press release contains “forward-looking statements” within the meaning of the safe harbor provisions of the U.S. Private Securities Litigation Reform Act of 1995. Forward-looking statements are not historical facts, but instead represent only the firm’s beliefs regarding future events, many of which, by their nature, are inherently uncertain and outside of the firm’s control. It is possible that the firm’s actual results and financial condition may differ, possibly materially, from the anticipated results and financial condition indicated in these forward-looking statements. For a discussion of some of the risks and important factors that could affect the firm’s future results and financial condition, see “Risk Factors” in Part I, Item 1A of the firm’s Annual Report on Form 10-K for the year ended December 31, 2017.

Information regarding the firm’s capital ratios, risk-weighted assets, supplementary leverage ratio, total assets and balance sheet data, global core liquid assets and VaR consists of preliminary estimates. These estimates are forward-looking statements and are subject to change, possibly materially, as the firm completes its financial statements.

Statements about the firm’s investment banking transaction backlog also may constitute forward-looking statements. Such statements are subject to the risk that the terms of these transactions may be modified or that they may not be completed at all; therefore, the net revenues, if any, that the firm actually earns from these transactions may differ, possibly materially, from those currently expected. Important factors that could result in a modification of the terms of a transaction or a transaction not being completed include, in the case of underwriting transactions, a decline or continued weakness in general economic conditions, outbreak of hostilities, volatility in the securities markets generally or an adverse development with respect to the issuer of the securities and, in the case of financial advisory transactions, a decline in the securities markets, an inability to obtain adequate financing, an adverse development with respect to a party to the transaction or a failure to obtain a required regulatory approval. For a discussion of other important factors that could adversely affect the firm’s investment banking transactions, see “Risk Factors” in Part I, Item 1A of the firm’s Annual Report on Form 10-K for the year ended December 31, 2017.

|

|

Conference Call |

|

A conference call to discuss the firm’s financial results, outlook and related matters will be held at 9:30 am (ET). The call will be open to the public. Members of the public who would like to listen to the conference call should dial 1-888-281-7154 (in the U.S.) or 1-706-679-5627 (outside the U.S.). The number should be dialed at least 10 minutes prior to the start of the conference call. The conference call will also be accessible as an audio webcast through the Investor Relations section of the firm’s website, www.goldmansachs.com/investor-relations. There is no charge to access the call. For those unable to listen to the live broadcast, a replay will be available on the firm’s website or by dialing 1-855-859-2056 (in the U.S.) or 1-404-537-3406 (outside the U.S.) passcode number 64774224 beginning approximately three hours after the event. Please direct any questions regarding obtaining access to the conference call to Goldman Sachs Investor Relations, via e-mail, at gs-investor-relations@gs.com.

9

Goldman Sachs Reports:

Full Year and Fourth Quarter 2018 Earnings Results

The Goldman Sachs Group, Inc. and Subsidiaries

Segment Net Revenues (unaudited)

$ in millions

| YEAR ENDED | % CHANGE FROM | |||||||||||||||||

|

DECEMBER 31, |

DECEMBER 31, |

DECEMBER 31, |

||||||||||||||||

|

INVESTMENT BANKING

|

||||||||||||||||||

|

Financial Advisory |

$ 3,507 | $ 3,188 | 10 % | |||||||||||||||

| Equity underwriting |

1,646 | 1,243 | 32 | |||||||||||||||

|

Debt underwriting

|

|

2,709

|

|

|

2,940

|

|

|

(8)

|

|

|||||||||

|

Total Underwriting

|

|

4,355

|

|

|

4,183

|

|

|

4

|

|

|||||||||

|

Total Investment Banking

|

|

7,862

|

|

|

7,371

|

|

|

7

|

|

|||||||||

|

INSTITUTIONAL CLIENT SERVICES

|

||||||||||||||||||

|

FICC Client Execution |

5,882 | 5,299 | 11 | |||||||||||||||

| Equities client execution |

2,835 | 2,046 | 39 | |||||||||||||||

|

Commissions and fees |

3,055 | 2,920 | 5 | |||||||||||||||

|

Securities services

|

|

1,710

|

|

|

1,637

|

|

|

4

|

|

|||||||||

|

Total Equities

|

|

7,600

|

|

|

6,603

|

|

|

15

|

|

|||||||||

|

Total Institutional Client Services

|

|

13,482

|

|

|

11,902

|

|

|

13

|

|

|||||||||

|

INVESTING & LENDING

|

||||||||||||||||||

|

Equity securities |

4,455 | 4,578 | (3) | |||||||||||||||

|

Debt securities and loans |

3,795 | 2,660 | 43 | |||||||||||||||

|

Total Investing & Lending

|

|

8,250

|

|

|

7,238

|

|

|

14

|

|

|||||||||

|

INVESTMENT MANAGEMENT

|

||||||||||||||||||

|

Management and other fees |

5,438 | 5,144 | 6 | |||||||||||||||

|

Incentive fees |

830 | 417 | 99 | |||||||||||||||

|

Transaction revenues

|

|

754

|

|

|

658

|

|

|

15

|

|

|||||||||

|

Total Investment Management

|

|

7,022

|

|

|

6,219

|

|

|

13

|

|

|||||||||

|

Total net revenues (1)

|

|

$ 36,616

|

|

|

$ 32,730

|

|

|

12

|

|

|||||||||

|

Geographic Net Revenues (unaudited) (5) $ in millions

|

|

|||||||||||||||||

| YEAR ENDED | ||||||||||||||||||

| DECEMBER 31, 2018 |

DECEMBER 31, 2017 |

|||||||||||||||||

| Americas |

$ 22,339 | $ 19,737 | ||||||||||||||||

|

EMEA |

9,244 | 8,168 | ||||||||||||||||

|

Asia

|

|

5,033

|

|

|

4,825

|

|

||||||||||||

|

Total net revenues (1)

|

|

$ 36,616

|

|

|

$ 32,730

|

|

||||||||||||

| Americas |

61% | 60% | ||||||||||||||||

|

EMEA |

25% | 25% | ||||||||||||||||

|

Asia

|

|

14%

|

|

|

15%

|

|

||||||||||||

|

Total |

|

100% |

|

|

100% |

|

||||||||||||

10

Goldman Sachs Reports:

Full Year and Fourth Quarter 2018 Earnings Results

The Goldman Sachs Group, Inc. and Subsidiaries

Segment Net Revenues (unaudited)

$ in millions

| THREE MONTHS ENDED | % CHANGE FROM | |||||||||||||||||||||||

|

DECEMBER 31, |

SEPTEMBER 30, |

DECEMBER 31, |

SEPTEMBER 30, |

DECEMBER 31, |

||||||||||||||||||||

|

INVESTMENT BANKING

|

||||||||||||||||||||||||

| Financial Advisory |

$ 1,201 | $ 916 | $ 772 | 31 % | 56 % | |||||||||||||||||||

| Equity underwriting |

315 | 432 | 460 | (27) | (32) | |||||||||||||||||||

|

Debt underwriting

|

|

528

|

|

|

632

|

|

|

909

|

|

|

(16)

|

|

|

(42)

|

| |||||||||

|

Total Underwriting

|

|

843

|

|

|

1,064

|

|

|

1,369

|

|

|

(21)

|

|

|

(38)

|

| |||||||||

|

Total Investment Banking

|

|

2,044

|

|

|

1,980

|

|

|

2,141

|

|

|

3

|

|

|

(5)

|

| |||||||||

|

INSTITUTIONAL CLIENT SERVICES

|

||||||||||||||||||||||||

| FICC Client Execution |

822 | 1,307 | 1,003 | (37) | (18) | |||||||||||||||||||

| Equities client execution |

401 | 681 | 223 | (41) | 80 | |||||||||||||||||||

|

Commissions and fees |

801 | 674 | 737 | 19 | 9 | |||||||||||||||||||

|

Securities services

|

|

402

|

|

|

439

|

|

|

409

|

|

|

(8)

|

|

|

(2)

|

| |||||||||

|

Total Equities

|

|

1,604

|

|

|

1,794

|

|

|

1,369

|

|

|

(11)

|

|

|

17

|

| |||||||||

|

Total Institutional Client Services

|

|

2,426

|

|

|

3,101

|

|

|

2,372

|

|

|

(22)

|

|

|

2

|

| |||||||||

|

INVESTING & LENDING

|

||||||||||||||||||||||||

| Equity securities |

994 | 1,111 | 1,209 | (11) | (18) | |||||||||||||||||||

|

Debt securities and loans

|

|

912

|

|

|

924

|

|

|

739

|

|

|

(1)

|

|

|

23

|

| |||||||||

|

Total Investing & Lending

|

|

1,906

|

|

|

2,035

|

|

|

1,948

|

|

|

(6)

|

|

|

(2)

|

| |||||||||

|

INVESTMENT MANAGEMENT

|

||||||||||||||||||||||||

| Management and other fees |

1,365 | 1,382 | 1,369 | (1) | – | |||||||||||||||||||

|

Incentive fees |

153 | 148 | 129 | 3 | 19 | |||||||||||||||||||

|

Transaction revenues

|

|

186

|

|

|

174

|

|

|

165

|

|

|

7

|

|

|

13

|

| |||||||||

|

Total Investment Management

|

|

1,704

|

|

|

1,704

|

|

|

1,663

|

|

|

–

|

|

|

2

|

| |||||||||

|

Total net revenues (1)

|

|

$ 8,080

|

|

|

$ 8,820

|

|

|

$ 8,124

|

|

|

(8)

|

|

|

(1)

|

| |||||||||

|

Geographic Net Revenues (unaudited) (5) $ in millions

|

|

|||||||||||||||||||||||

| THREE MONTHS ENDED | ||||||||||||||||||||||||

|

DECEMBER 31, |

SEPTEMBER 30, |

DECEMBER 31, |

||||||||||||||||||||||

| Americas |

$ 5,178 | $ 5,351 | $ 4,921 | |||||||||||||||||||||

|

EMEA |

1,766 | 2,254 | 1,945 | |||||||||||||||||||||

|

Asia

|

|

1,136

|

|

|

1,215

|

|

|

1,258

|

|

|||||||||||||||

|

Total net revenues (1)

|

|

$ 8,080

|

|

|

$ 8,820

|

|

|

$ 8,124

|

|

|||||||||||||||

| Americas |

64% | 61% | 61% | |||||||||||||||||||||

|

EMEA |

22% | 25% | 24% | |||||||||||||||||||||

|

Asia

|

|

14%

|

|

|

14%

|

|

|

15%

|

|

|||||||||||||||

|

Total

|

|

100%

|

|

|

100%

|

|

|

100%

|

|

|||||||||||||||

11

Goldman Sachs Reports:

Full Year and Fourth Quarter 2018 Earnings Results

The Goldman Sachs Group, Inc. and Subsidiaries

Consolidated Statements of Earnings (unaudited) (1)

In millions, except per share amounts

| YEAR ENDED | % CHANGE FROM | |||||||||||||||||

| DECEMBER 31, 2018 |

DECEMBER 31, 2017 |

DECEMBER 31, 2017 |

||||||||||||||||

|

REVENUES |

||||||||||||||||||

| Investment banking |

$ 7,862 | $ 7,371 | 7 % | |||||||||||||||

|

Investment management |

6,514 | 5,803 | 12 | |||||||||||||||

|

Commissions and fees |

3,199 | 3,051 | 5 | |||||||||||||||

|

Market making |

9,451 | 7,660 | 23 | |||||||||||||||

|

Other principal transactions

|

|

5,823

|

|

|

5,913

|

|

|

(2)

|

|

|||||||||

|

Total non-interest revenues

|

|

32,849

|

|

|

29,798

|

|

|

10

|

|

|||||||||

| Interest income |

19,679 | 13,113 | 50 | |||||||||||||||

|

Interest expense

|

|

15,912

|

|

|

10,181

|

|

|

56

|

|

|||||||||

|

Net interest income

|

|

3,767

|

|

|

2,932

|

|

|

28

|

|

|||||||||

|

Total net revenues

|

|

36,616

|

|

|

32,730

|

|

|

12

|

|

|||||||||

|

Provision for credit losses

|

|

674

|

|

|

657

|

|

|

3

|

|

|||||||||

|

OPERATING EXPENSES

|

||||||||||||||||||

| Compensation and benefits |

12,328 | 11,653 | 6 | |||||||||||||||

|

Brokerage, clearing, exchange and distribution fees |

3,200 | 2,876 | 11 | |||||||||||||||

|

Market development |

740 | 588 | 26 | |||||||||||||||

|

Communications and technology |

1,023 | 897 | 14 | |||||||||||||||

|

Depreciation and amortization |

1,328 | 1,152 | 15 | |||||||||||||||

|

Occupancy |

809 | 733 | 10 | |||||||||||||||

|

Professional fees |

1,214 | 1,165 | 4 | |||||||||||||||

|

Other expenses

|

|

2,819

|

|

|

1,877

|

|

|

50

|

|

|||||||||

|

Total operating expenses

|

|

23,461

|

|

|

20,941

|

|

|

12

|

|

|||||||||

| Pre-tax earnings |

12,481 | 11,132 | 12 | |||||||||||||||

|

Provision for taxes

|

|

2,022

|

|

|

6,846

|

|

|

(70)

|

|

|||||||||

|

Net earnings

|

|

10,459

|

|

|

4,286

|

|

|

144

|

|

|||||||||

|

Preferred stock dividends

|

|

599

|

|

|

601

|

|

|

–

|

|

|||||||||

|

Net earnings applicable to common shareholders

|

|

$ 9,860

|

|

|

$ 3,685

|

|

|

168

|

|

|||||||||

|

EARNINGS PER COMMON SHARE

|

||||||||||||||||||

| Basic (11) |

$ 25.53 | $ 9.12 | 180 % | |||||||||||||||

|

Diluted |

25.27 | 9.01 | 180 | |||||||||||||||

|

AVERAGE COMMON SHARES

|

||||||||||||||||||

| Basic |

385.4 | 401.6 | (4) | |||||||||||||||

|

Diluted

|

|

390.2

|

|

|

409.1

|

|

|

(5)

|

|

|||||||||

12

Goldman Sachs Reports:

Full Year and Fourth Quarter 2018 Earnings Results

The Goldman Sachs Group, Inc. and Subsidiaries

Consolidated Statements of Earnings (unaudited) (1)

In millions, except per share amounts and headcount

| THREE MONTHS ENDED | % CHANGE FROM | |||||||||||||||||||||

|

DECEMBER 31, |

SEPTEMBER 30, |

DECEMBER 31, |

SEPTEMBER 30, |

DECEMBER 31, |

||||||||||||||||||

|

REVENUES

|

||||||||||||||||||||||

| Investment banking |

$ 2,044 | $ 1,980 | $ 2,141 | 3 % | (5) % | |||||||||||||||||

|

Investment management |

1,567 | 1,580 | 1,554 | (1) | 1 | |||||||||||||||||

|

Commissions and fees |

838 | 704 | 772 | 19 | 9 | |||||||||||||||||

|

Market making |

1,420 | 2,281 | 1,215 | (38) | 17 | |||||||||||||||||

|

Other principal transactions

|

|

1,220

|

|

|

1,419

|

|

|

1,544

|

|

|

(14)

|

|

|

(21)

|

| |||||||

|

Total non-interest revenues

|

7,089 | 7,964 | 7,226 | (11) | (2) | |||||||||||||||||

| Interest income |

5,468 | 5,061 | 3,736 | 8 | 46 | |||||||||||||||||

|

Interest expense

|

|

4,477

|

|

|

4,205

|

|

|

2,838

|

|

|

6

|

|

|

58

|

| |||||||

|

Net interest income

|

|

991

|

|

|

856

|

|

|

898

|

|

|

16

|

|

|

10

|

| |||||||

|

Total net revenues

|

|

8,080

|

|

|

8,820

|

|

|

8,124

|

|

|

(8)

|

|

|

(1)

|

| |||||||

|

Provision for credit losses

|

|

222

|

|

|

174

|

|

|

290

|

|

|

28

|

|

|

(23)

|

| |||||||

|

OPERATING EXPENSES

|

||||||||||||||||||||||

|

Compensation and benefits |

1,857 | 3,019 | 2,098 | (38) | (11) | |||||||||||||||||

|

Brokerage, clearing, exchange and distribution fees |

830 | 714 | 732 | 16 | 13 | |||||||||||||||||

|

Market development |

208 | 167 | 175 | 25 | 19 | |||||||||||||||||

|

Communications and technology |

262 | 250 | 230 | 5 | 14 | |||||||||||||||||

|

Depreciation and amortization |

377 | 317 | 350 | 19 | 8 | |||||||||||||||||

|

Occupancy |

215 | 203 | 190 | 6 | 13 | |||||||||||||||||

|

Professional fees |

317 | 310 | 363 | 2 | (13) | |||||||||||||||||

|

Other expenses

|

|

1,084

|

|

|

588

|

|

|

588

|

|

|

84

|

|

|

84

|

| |||||||

|

Total operating expenses

|

|

5,150

|

|

|

5,568

|

|

|

4,726

|

|

|

(8)

|

|

|

9

|

| |||||||

| Pre-tax earnings |

2,708 | 3,078 | 3,108 | (12) | (13) | |||||||||||||||||

|

Provision for taxes |

170 | 554 | 5,036 | (69) | (97) | |||||||||||||||||

|

Net earnings / (loss) |

|

2,538

|

|

|

2,524

|

|

|

(1,928)

|

|

|

1

|

|

|

N.M.

|

| |||||||

|

Preferred stock dividends

|

|

216

|

|

|

71

|

|

|

215

|

|

|

N.M.

|

|

|

–

|

| |||||||

|

Net earnings / (loss) applicable to common shareholders

|

|

$ 2,322

|

|

|

$ 2,453

|

|

|

$ (2,143)

|

|

|

(5)

|

|

|

N.M.

|

| |||||||

|

EARNINGS / (LOSS) PER COMMON SHARE

|

||||||||||||||||||||||

| Basic (11) |

$ 6.11 | $ 6.35 | $ (5.51) | (4) % | N.M. % | |||||||||||||||||

|

Diluted |

6.04 | 6.28 | (5.51) | (4) | N.M. | |||||||||||||||||

|

AVERAGE COMMON SHARES

|

||||||||||||||||||||||

| Basic |

379.5 | 385.4 | 389.8 | (2) | (3) | |||||||||||||||||

|

Diluted |

384.3 | 390.5 | 389.8 | (2) | (1) | |||||||||||||||||

|

SELECTED DATA AT PERIOD-END

|

||||||||||||||||||||||

| Headcount

|

|

36,600

|

|

|

36,300

|

|

|

33,600

|

|

|

1

|

|

|

9

|

| |||||||

13

Goldman Sachs Reports:

Full Year and Fourth Quarter 2018 Earnings Results

The Goldman Sachs Group, Inc. and Subsidiaries

Condensed Consolidated Statements of Financial Condition (unaudited) (7)

$ in billions

| AS OF | ||||||||||||||||||||||

|

DECEMBER 31, |

SEPTEMBER 30, |

DECEMBER 31, |

||||||||||||||||||||

|

ASSETS

|

||||||||||||||||||||||

|

Cash and cash equivalents |

$ 130 | $ 119 | $ 110 | |||||||||||||||||||

|

Collateralized agreements |

276 | 298 | 312 | |||||||||||||||||||

|

Receivables |

160 | 159 | 151 | |||||||||||||||||||

|

Financial instruments owned |

336 | 351 | 316 | |||||||||||||||||||

|

Other assets

|

|

31

|

|

|

30

|

|

|

28

|

|

|||||||||||||

|

Total assets

|

|

933

|

|

|

957

|

|

|

917

|

|

|||||||||||||

|

LIABILITIES AND SHAREHOLDERS’ EQUITY

|

||||||||||||||||||||||

|

Deposits |

158 | 151 | 139 | |||||||||||||||||||

|

Collateralized financings |

113 | 129 | 124 | |||||||||||||||||||

|

Payables |

180 | 190 | 178 | |||||||||||||||||||

|

Financial instruments sold, but not yet purchased |

109 | 113 | 112 | |||||||||||||||||||

|

Unsecured short-term borrowings |

41 | 42 | 47 | |||||||||||||||||||

|

Unsecured long-term borrowings |

224 | 229 | 218 | |||||||||||||||||||

|

Other liabilities

|

|

18

|

|

|

16

|

|

|

17

|

|

|||||||||||||

|

Total liabilities

|

|

843

|

|

|

870

|

|

|

835

|

|

|||||||||||||

|

Shareholders’ equity

|

|

90

|

|

|

87

|

|

|

82

|

|

|||||||||||||

|

Total liabilities and shareholders’ equity

|

|

$ 933

|

|

|

$ 957

|

|

|

$ 917

|

|

|||||||||||||

|

Capital Ratios (unaudited) (5) (6) (7) $ in billions

|

|

|||||||||||||||||||||

| AS OF | ||||||||||||||||||||||

|

DECEMBER

31, |

SEPTEMBER 30, |

DECEMBER

31, |

||||||||||||||||||||

| Common equity tier 1 |

$ 73.1 | $ 71.8 | $ 67.0 | |||||||||||||||||||

|

STANDARDIZED CAPITAL RULES

|

||||||||||||||||||||||

|

Risk-weighted assets |

$ 548 | $ 546 | $ 564 | |||||||||||||||||||

|

Common equity tier 1 ratio |

13.3% | 13.1% | 11.9% | |||||||||||||||||||

|

BASEL III ADVANCED CAPITAL RULES

|

||||||||||||||||||||||

|

Risk-weighted assets |

$ 558 | $ 577 | $ 626 | |||||||||||||||||||

|

Common equity tier 1 ratio |

13.1% | 12.4% | 10.7% | |||||||||||||||||||

|

Average Daily VaR (unaudited) (5) (7) $ in millions

|

|

|||||||||||||||||||||

| THREE MONTHS ENDED | YEAR ENDED | |||||||||||||||||||||

|

DECEMBER 31, |

SEPTEMBER 30, |

DECEMBER

31, |

DECEMBER 31, |

DECEMBER 31, |

||||||||||||||||||

|

RISK CATEGORIES

|

||||||||||||||||||||||

| Interest rates |

$ 40 | $ 41 | $ 40 | $ 46 | $ 40 | |||||||||||||||||

|

Equity prices |

28 | 28 | 28 | 31 | 24 | |||||||||||||||||

|

Currency rates |

19 | 15 | 9 | 14 | 12 | |||||||||||||||||

|

Commodity prices |

12 | 10 | 9 | 11 | 13 | |||||||||||||||||

|

Diversification effect

|

|

(50)

|

|

|

(41)

|

|

|

(32)

|

|

|

(42)

|

|

|

(35)

|

| |||||||

|

Total

|

|

$ 49

|

|

|

$ 53

|

|

|

$ 54

|

|

|

$ 60

|

|

|

$ 54

|

| |||||||

14

Goldman Sachs Reports:

Full Year and Fourth Quarter 2018 Earnings Results

The Goldman Sachs Group, Inc. and Subsidiaries

Assets Under Supervision (unaudited) (5)

$ in billions

| AS OF | % CHANGE FROM | |||||||||||||||||||||

|

DECEMBER 31, |

SEPTEMBER 30, |

DECEMBER 31, |

SEPTEMBER 30, |

DECEMBER 31, |

||||||||||||||||||

|

ASSET CLASS

|

||||||||||||||||||||||

|

Alternative investments |

$ 167 | $ 175 | $ 168 | (5) % | (1) % | |||||||||||||||||

|

Equity |

301 | 349 | 321 | (14) | (6) | |||||||||||||||||

|

Fixed income

|

|

677

|

|

|

668

|

|

|

660

|

|

|

1

|

|

|

3

|

| |||||||

|

Total long-term AUS

|

|

1,145

|

|

|

1,192

|

|

|

1,149

|

|

|

(4)

|

|

|

–

|

| |||||||

|

Liquidity products

|

|

397

|

|

|

358

|

|

|

345

|

|

|

11

|

|

|

15

|

| |||||||

|

Total AUS

|

|

$ 1,542

|

|

|

$ 1,550

|

|

|

$ 1,494

|

|

|

(1)

|

|

|

3

|

| |||||||

| THREE MONTHS ENDED | YEAR ENDED | |||||||||||||||||||||

|

DECEMBER 31, |

SEPTEMBER 30, |

DECEMBER 31, |

DECEMBER 31, |

DECEMBER 31, |

||||||||||||||||||

| Beginning balance |

$ 1,550 | $ 1,513 | $ 1,456 | $ 1,494 | $ 1,379 | |||||||||||||||||

|

Net inflows / (outflows): |

||||||||||||||||||||||

|

Alternative investments |

(4) | 3 | (2) | 1 | 15 | |||||||||||||||||

|

Equity |

(1) | 7 | 1 | 13 | 2 | |||||||||||||||||

|

Fixed income

|

|

8

|

|

|

3

|

|

|

–

|

|

|

23

|

|

|

25

|

| |||||||

|

Total long-term AUS net inflows / (outflows)

|

|

3

|

|

|

13

|

|

|

(1)

|

|

|

37

|

|

|

42

|

| |||||||

|

Liquidity products

|

|

39

|

|

|

8

|

|

|

17

|

|

|

52

|

|

|

(13)

|

| |||||||

|

Total AUS net inflows / (outflows)

|

|

42

|

|

|

21

|

|

|

16

|

|

|

89

|

|

|

29 (12)

|

| |||||||

|

Net market appreciation / (depreciation)

|

|

(50)

|

|

|

16

|

|

|

22

|

|

|

(41)

|

|

|

86

|

| |||||||

|

Ending balance

|

|

$ 1,542

|

|

|

$ 1,550

|

|

|

$ 1,494

|

|

|

$ 1,542

|

|

|

$ 1,494

|

| |||||||

15

Goldman Sachs Reports

Full Year and Fourth Quarter 2018 Earnings Results

|

|

Footnotes |

|

| (1) |

The following reclassifications have been made to previously reported amounts to conform to the current presentation. |

| • |

Provision for credit losses, previously reported in other principal transactions revenues (and Investing & Lending segment net revenues), is now reported as a separate line item in the Consolidated Statements of Earnings. |

| • |

Headcount consists of the firm’s employees, and excludes consultants and temporary staff previously reported as part of total staff. As a result, expenses related to consultants and temporary staff previously reported in compensation and benefits expenses are now reported in professional fees. |

| • |

Regulatory-related fees that are paid to exchanges, reported in other expenses prior to 2018, are now reported in brokerage, clearing, exchange and distribution fees. |

| (2) |

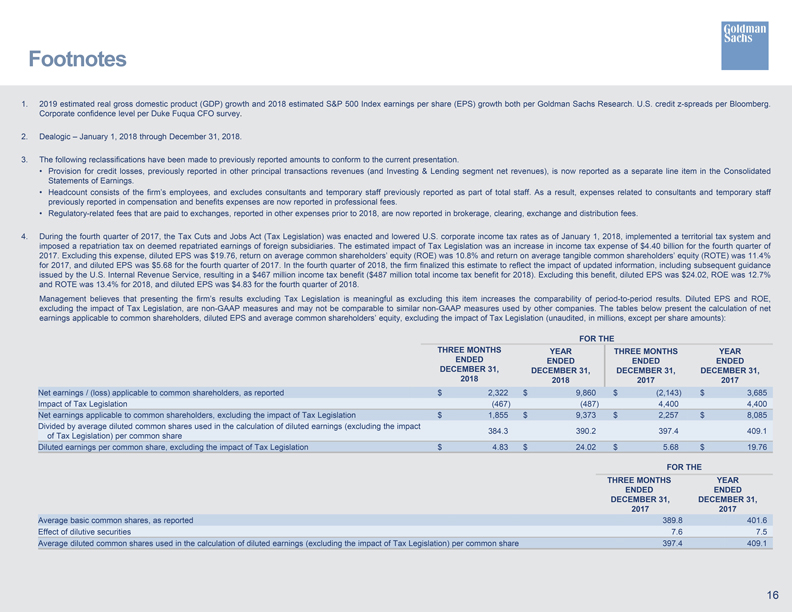

During the fourth quarter of 2017, the Tax Cuts and Jobs Act (Tax Legislation) was enacted and lowered U.S. corporate income tax rates as of January 1, 2018, implemented a territorial tax system and imposed a repatriation tax on deemed repatriated earnings of foreign subsidiaries. The estimated impact of Tax Legislation was an increase in income tax expense of $4.40 billion for the fourth quarter of 2017. Excluding this expense, diluted EPS was $19.76, ROE was 10.8% and ROTE was 11.4% for 2017, and diluted EPS was $5.68 for the fourth quarter of 2017. In the fourth quarter of 2018, the firm finalized this estimate to reflect the impact of updated information, including subsequent guidance issued by the U.S. Internal Revenue Service, resulting in a $467 million income tax benefit ($487 million total income tax benefit for 2018). Excluding this benefit, diluted EPS was $24.02, ROE was 12.7% and ROTE was 13.4% for 2018, and diluted EPS was $4.83 for the fourth quarter of 2018. |

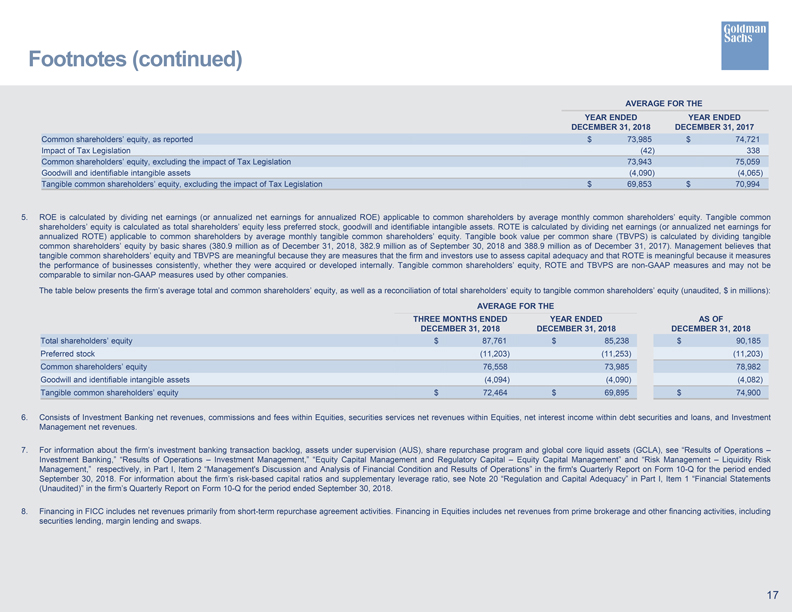

Management believes that presenting the firm’s results excluding Tax Legislation is meaningful as excluding this item increases the comparability of period-to-period results. Diluted EPS and ROE, excluding the impact of Tax Legislation, are non-GAAP measures and may not be comparable to similar non-GAAP measures used by other companies. The tables below present the calculation of net earnings applicable to common shareholders, diluted EPS and average common shareholders’ equity, excluding the impact of Tax Legislation (unaudited, in millions, except per share amounts):

| FOR THE | ||||||||||

|

THREE MONTHS ENDED DECEMBER 31, |

YEAR ENDED DECEMBER 31, 2018 |

THREE MONTHS ENDED |

YEAR ENDED DECEMBER 31, 2017 |

|||||||

| Net earnings / (loss) applicable to common shareholders, as reported |

$ 2,322 | $ 9,860 | $ (2,143) | $ 3,685 | ||||||

| Impact of Tax Legislation |

(467) | (487) | 4,400 | 4,400 | ||||||

|

Net earnings applicable to common shareholders, excluding the impact of Tax Legislation |

$ 1,855 | $ 9,373 | $ 2,257 | $ 8,085 | ||||||

| Divided by average diluted common shares used in the calculation of diluted earnings (excluding the impact of Tax Legislation) per common share |

384.3 | 390.2 | 397.4 | 409.1 | ||||||

|

Diluted EPS, excluding the impact of Tax Legislation |

$ 4.83 | $ 24.02 | $ 5.68 | $ 19.76 | ||||||

| FOR THE | ||||||||||

|

THREE MONTHS ENDED |

YEAR ENDED DECEMBER 31, 2017 |

|||||||||

| Average basic common shares, as reported |

389.8 | 401.6 | ||||||||

| Effect of dilutive securities |

7.6 | 7.5 | ||||||||

|

Average diluted common shares used in the calculation of diluted earnings (excluding the impact of Tax Legislation) per common share |

397.4 | 409.1 | ||||||||

| AVERAGE FOR THE | ||||||||||

|

YEAR ENDED |

YEAR ENDED |

|||||||||

| Common shareholders’ equity, as reported |

$ 73,985 | $ 74,721 | ||||||||

| Impact of Tax Legislation |

(42) | 338 | ||||||||

|

Common shareholders’ equity, excluding the impact of Tax Legislation |

73,943 | 75,059 | ||||||||

| Goodwill and identifiable intangible assets |

(4,090) | (4,065) | ||||||||

|

Tangible common shareholders’ equity, excluding the impact of Tax Legislation |

$ 69,853 | $ 70,994 | ||||||||

16

Goldman Sachs Reports

Full Year and Fourth Quarter 2018 Earnings Results

|

|

Footnotes (continued) |

|

| (3) | ROE is calculated by dividing net earnings (or annualized net earnings for annualized ROE) applicable to common shareholders by average monthly common shareholders’ equity. Tangible common shareholders’ equity is calculated as total shareholders’ equity less preferred stock, goodwill and identifiable intangible assets. ROTE is calculated by dividing net earnings (or annualized net earnings for annualized ROTE) applicable to common shareholders by average monthly tangible common shareholders’ equity. Tangible book value per common share is calculated by dividing tangible common shareholders’ equity by basic shares. Management believes that tangible common shareholders’ equity and tangible book value per common share are meaningful because they are measures that the firm and investors use to assess capital adequacy and that ROTE is meaningful because it measures the performance of businesses consistently, whether they were acquired or developed internally. Tangible common shareholders’ equity, ROTE and tangible book value per common share are non-GAAP measures and may not be comparable to similar non-GAAP measures used by other companies. |

The table below presents the firm’s average total and common shareholders’ equity, as well as a reconciliation of total shareholders’ equity to tangible common shareholders’ equity (unaudited, $ in millions):

|

AVERAGE FOR THE |

|||||||||||||||||||

|

THREE MONTHS ENDED |

YEAR ENDED DECEMBER 31, 2018 |

|

AS OF DECEMBER 31, 2018 |

||||||||||||||||

|

Total shareholders’ equity |

$ 87,761 | $ 85,238 | $ 90,185 | ||||||||||||||||

|

Preferred stock |

(11,203) | (11,253) | (11,203) | ||||||||||||||||

|

Common shareholders’ equity

|

|

76,558

|

|

|

73,985

|

|

|

78,982

|

|

||||||||||

|

Goodwill and identifiable intangible assets |

(4,094) | (4,090) | (4,082) | ||||||||||||||||

|

Tangible common shareholders’ equity

|

|

$ 72,464

|

|

|

$ 69,895

|

|

|

$ 74,900

|

|

||||||||||

| (4) | Dealogic – January 1, 2018 through December 31, 2018. |

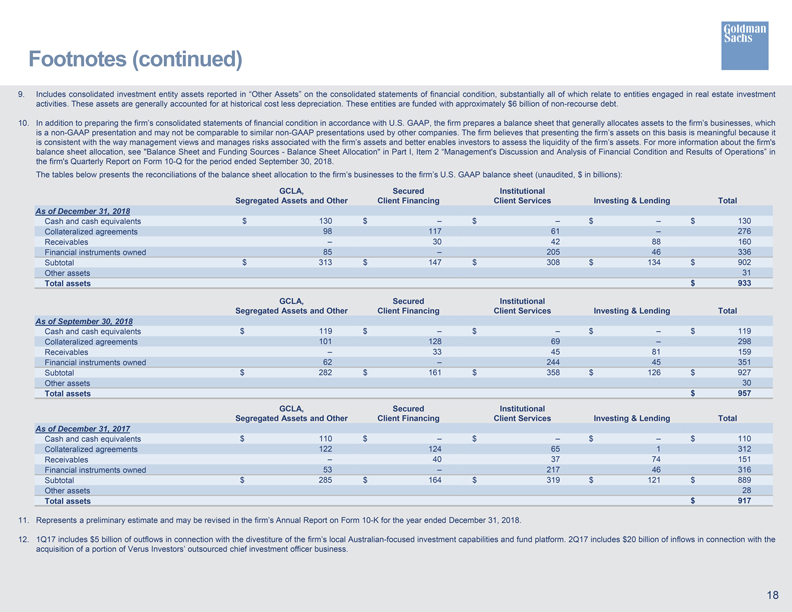

| (5) | For information about the firm’s investment banking transaction backlog, assets under supervision, share repurchase program, global core liquid assets and VaR, see “Results of Operations – Investment Banking,” “Results of Operations – Investment Management,” “Equity Capital Management and Regulatory Capital – Equity Capital Management,” “Risk Management – Liquidity Risk Management” and “Risk Management – Market Risk Management,” respectively, in Part I, Item 2 “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in the firm’s Quarterly Report on Form 10-Q for the period ended September 30, 2018. For information about the firm’s risk-based capital ratios and supplementary leverage ratio, and geographic net revenues, see Note 20 “Regulation and Capital Adequacy” and Note 25 “Business Segments,” respectively, in Part I, Item 1 “Financial Statements (Unaudited)” in the firm’s Quarterly Report on Form 10-Q for the period ended September 30, 2018. |

| (6) | As of December 31, 2017, the firm’s capital ratios on a fully phased-in basis were non-GAAP measures and may not be comparable to similar non-GAAP measures used by other companies. Management believes that the firm’s capital ratios on a fully phased-in basis are meaningful because they are measures that the firm and investors use to assess capital adequacy. The table below presents reconciliations, for both the Standardized approach and the Basel III Advanced approach, of common equity tier 1 and risk-weighted assets on a transitional basis to a fully phased-in basis as of December 31, 2017 (unaudited, $ in billions): |

| AS OF DECEMBER 31, 2017 | ||||||||

|

STANDARDIZED |

BASEL III ADVANCED |

|||||||

| Common equity tier 1, transitional basis |

$ 67.1 | $ 67.1 | ||||||

| Transitional adjustments |

(0.1) | (0.1) | ||||||

|

Common equity tier 1, fully phased-in basis |

$ 67.0 | $ 67.0 | ||||||

| Risk-weighted assets, transitional basis |

$ 556 | $ 618 | ||||||

| Transitional adjustments |

8 | 8 | ||||||

|

Risk-weighted assets, fully phased-in basis |

$ 564 | $ 626 | ||||||

| Common equity tier 1 ratio, transitional basis |

12.1% | 10.9% | ||||||

| Common equity tier 1 ratio, fully phased-in basis |

11.9% | 10.7% | ||||||

| (7) | Represents a preliminary estimate and may be revised in the firm’s Annual Report on Form 10-K for the year ended December 31, 2018. |

| (8) | In the first quarter of 2018, the firm adopted ASU No. 2014-09, “Revenue from Contracts with Customers (Topic 606),” which required a change in the presentation of certain costs from a net presentation within revenues to a gross basis and vice versa. For information about ASU No. 2014-09, see Note 3 “Significant Accounting Policies” in Part I, Item 1 “Financial Statements (Unaudited)” in the firm’s Quarterly Report on Form 10-Q for the period ended September 30, 2018. |

| (9) | Efficiency ratio is calculated by dividing total operating expenses by total net revenues. |

| (10) | Basic shares include common shares outstanding and restricted stock units granted to employees with no future service requirements. |

| (11) | Unvested share-based awards that have non-forfeitable rights to dividends or dividend equivalents are treated as a separate class of securities in calculating EPS. The impact of applying this methodology was a reduction in basic EPS of $0.05 and $0.06 for the years ended December 31, 2018 and December 31, 2017, respectively, and $0.01 for both the three months ended December 31, 2018 and September 30, 2018. The impact of applying this methodology for the three months ended December 31, 2017 was a loss per common share (basic and diluted) of $0.01. |

| (12) | Included $23 billion of inflows ($20 billion in long-term assets under supervision and $3 billion in liquidity products) in connection with the acquisition of a portion of Verus Investors’ outsourced chief investment officer business and $5 billion of equity asset outflows in connection with the divestiture of the firm’s local Australian-focused investment capabilities and fund platform. |

17