Filed Pursuant to Rule 424(b)(2)

Registration Statement No. 333-219206

The information in this preliminary pricing supplement is not complete and may be changed. This preliminary pricing supplement is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

|

Subject to Completion. Dated August 14, 2018.

GS Finance Corp.

$

Autocallable Underlier-Linked Notes due

guaranteed by

The Goldman Sachs Group, Inc.

|

|

The notes will not bear interest. The notes will mature on the stated maturity date (expected to be August 28, 2023) unless they are automatically called on any call observation date (the dates, commencing on August 26, 2019, specified on page PS-5 of this pricing supplement). Your notes will be automatically called on a call observation date if the closing level of each of the EURO STOXX 50® Index and the iShares® MSCI Emerging Markets ETF on such date is greater than or equal to the applicable call level, resulting in a payment on the corresponding call payment date (expected to be the fifth business day after each call observation date) equal to the face amount of your notes plus the product of $1,000 times the applicable call premium amount. The applicable call level for each call observation date and the applicable call premium amount for each call payment date are each specified on page PS-5 of this pricing supplement.

The return on your notes is linked, in part, to the performance of the iShares® MSCI Emerging Markets ETF (ETF), and not to that of the MSCI Emerging Markets Index (underlying index) on which the ETF is based. The ETF follows a strategy of “representative sampling,” which means the ETF’s holdings are not the same as those of its underlying index. The performance of the ETF may significantly diverge from that of its underlying index.

The amount that you will be paid on your notes at maturity, if the notes have not been automatically called, is based on the performance of the lesser performing underlier (the underlier with the lowest underlier return). The underlier return for each underlier is the percentage increase or decrease in the final level (the closing level of the underlier on the determination date, expected to be August 21, 2023) from its initial level.

At maturity, for each $1,000 face amount of your notes, you will receive an amount in cash equal to:

| · |

if the final level of each underlier is greater than or equal to 88% of its initial level, $1,510;

|

| · |

if the final level of each underlier is greater than or equal to 60% of its initial level but the final level of any underlier is less than 88% of its initial level, $1,100; or

|

| · |

if the final level of any underlier is less than 60% of its initial level, the sum of (i) $1,000 plus (ii) the product of (a) the lesser performing underlier return times (b) $1,000. You will receive less than 60% of the face amount of your notes.

|

If the underlier return for any underlier is less than -40%, the percentage of the face amount of your notes you will receive will be based on the performance of the underlier with the lowest underlier return. In such event, you will receive less than 60% of the face amount of your notes.

You should read the disclosure herein to better understand the terms and risks of your investment, including the credit risk of GS Finance Corp. and The Goldman Sachs Group, Inc. See page PS-11.

The estimated value of your notes at the time the terms of your notes are set on the trade date is expected to be between $910 and $950 per $1,000 face amount. For a discussion of the estimated value and the price at which Goldman Sachs & Co. LLC would initially buy or sell your notes, if it makes a market in the notes, see the following page.

|

Original issue date:

|

expected to be August 23, 2018

|

Original issue price:

|

100% of the face amount

|

|

Underwriting discount:

|

% of the face amount1

|

Net proceeds to the issuer:

|

% of the face amount

|

1In addition to the %, the underwriting discount paid by us also includes a structuring fee of % and a marketing fee of %, in each case, of the face amount. See “Summary Information — Key Terms — Supplemental plan of distribution; conflicts of interest” on page PS-5.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense. The notes are not bank deposits and are not insured by the Federal Deposit Insurance Corporation or any other governmental agency, nor are they obligations of, or guaranteed by, a bank.

Goldman Sachs & Co. LLC

Pricing Supplement No. dated , 2018.

|

|

The issue price, underwriting discount and net proceeds listed above relate to the notes we sell initially. We may decide to sell additional notes after the date of this pricing supplement, at issue prices and with underwriting discounts and net proceeds that differ from the amounts set forth above. The return (whether positive or negative) on your investment in notes will depend in part on the issue price you pay for such notes.

GS Finance Corp. may use this prospectus in the initial sale of the notes. In addition, Goldman Sachs & Co. LLC or any other affiliate of GS Finance Corp. may use this prospectus in a market-making transaction in a note after its initial sale. Unless GS Finance Corp. or its agent informs the purchaser otherwise in the confirmation of sale, this prospectus is being used in a market-making transaction.

|

Estimated Value of Your Notes

The estimated value of your notes at the time the terms of your notes are set on the trade date (as determined by reference to pricing models used by Goldman Sachs & Co. LLC (GS&Co.) and taking into account our credit spreads) is expected to be between $910 and $950 per $1,000 face amount, which is less than the original issue price. The value of your notes at any time will reflect many factors and cannot be predicted; however, the price (not including GS&Co.’s customary bid and ask spreads) at which GS&Co. would initially buy or sell notes (if it makes a market, which it is not obligated to do) and the value that GS&Co. will initially use for account statements and otherwise is equal to approximately the estimated value of your notes at the time of pricing, plus an additional amount (initially equal to $ per $1,000 face amount).

Prior to , the price (not including GS&Co.’s customary bid and ask spreads) at which GS&Co. would buy or sell your notes (if it makes a market, which it is not obligated to do) will equal approximately the sum of (a) the then-current estimated value of your notes (as determined by reference to GS&Co.’s pricing models) plus (b) any remaining additional amount (the additional amount will decline to zero on a straight-line basis from the time of pricing through ). On and after , the price (not including GS&Co.’s customary bid and ask spreads) at which GS&Co. would buy or sell your notes (if it makes a market) will equal approximately the then-current estimated value of your notes determined by reference to such pricing models.

|

|

About Your Prospectus

The notes are part of the Medium-Term Notes, Series E program of GS Finance Corp., and are fully and unconditionally guaranteed by The Goldman Sachs Group, Inc. This prospectus includes this pricing supplement and the accompanying documents listed below. This pricing supplement constitutes a supplement to the documents listed below and should be read in conjunction with such documents:

The information in this pricing supplement supersedes any conflicting information in the documents listed above. In addition, some of the terms or features described in the listed documents may not apply to your notes.

|

|

We refer to the notes we are offering by this pricing supplement as the “offered notes” or the “notes”. Each of the offered notes has the terms described below. Please note that in this pricing supplement, references to “GS Finance Corp.”, “we”, “our” and “us” mean only GS Finance Corp. and do not include its subsidiaries or affiliates, references to “The Goldman Sachs Group, Inc.”, our parent company, mean only The Goldman Sachs Group, Inc. and do not include its subsidiaries or affiliates and references to “Goldman Sachs” mean The Goldman Sachs Group, Inc. together with its consolidated subsidiaries and affiliates, including us. Also, references to the “accompanying prospectus” mean the accompanying prospectus, dated July 10, 2017, references to the “accompanying prospectus supplement” mean the accompanying prospectus supplement, dated July 10, 2017, for Medium-Term Notes, Series E, and references to the “accompanying general terms supplement no. 1,734” mean the accompanying general terms supplement no. 1,734, dated July 10, 2017, in each case of GS Finance Corp. and The Goldman Sachs Group, Inc. The notes will be issued under the senior debt indenture, dated as of October 10, 2008, as supplemented by the First Supplemental Indenture, dated as of February 20, 2015, each among us, as issuer, The Goldman Sachs Group, Inc., as guarantor, and The Bank of New York Mellon, as trustee. This indenture is referred to as the “GSFC 2008 indenture” in the accompanying prospectus supplement.

This section is meant as a summary and should be read in conjunction with the section entitled “Supplemental Terms of the Notes” on page S-16 of the accompanying general terms supplement no. 1,734. Please note that certain features described in the accompanying general terms supplement no. 1,734 are not applicable to the notes. This pricing supplement supersedes any conflicting provisions of the accompanying general terms supplement no. 1,734.

|

Key Terms

Issuer: GS Finance Corp.

Guarantor: The Goldman Sachs Group, Inc.

Underliers: the EURO STOXX 50® Index (Bloomberg symbol, “SX5E Index”), as sponsored and maintained by STOXX Limited, and the iShares® MSCI Emerging Markets ETF (Bloomberg symbol, “EEM UP Equity”); see “The Underliers” on page PS-19

Underlying index of the iShares® MSCI Emerging Markets ETF: the MSCI Emerging Markets Index, as published by MSCI, Inc. (“MSCI”)

Specified currency: U.S. dollars (“$”)

Face amount: each note will have a face amount equal to $1,000; $ in the aggregate for all the offered notes; the aggregate face amount of the offered notes may be increased if the issuer, at its sole option, decides to sell an additional amount of the offered notes on a date subsequent to the date of this pricing supplement

Purchase at amount other than face amount: the amount we will pay you for your notes on a call payment date or the stated maturity date, as the case may be, will not be adjusted based on the issue price you pay for your notes, so if you acquire notes at a premium (or discount) to face amount and hold them to a call payment date or the stated maturity date, it could affect your investment in a number of ways. The return on your investment in such notes will be lower (or higher) than it would have been had you purchased the notes at face amount. See “Additional Risk Factors Specific to Your Notes — If You Purchase Your Notes at a Premium to Face Amount, the Return on Your Investment Will Be Lower Than the Return on Notes Purchased at Face Amount and the Impact of Certain Key Terms of the Notes Will Be Negatively Affected” on page PS-14 of this pricing supplement

Supplemental discussion of U.S. federal income tax consequences: you will be obligated pursuant to the terms of the notes — in the absence of a change in law, an administrative determination or a judicial ruling to the contrary — to characterize each note for all tax purposes as a pre-paid derivative contract in respect of the underliers, as described under “Supplemental Discussion of U.S. Federal Income Tax Consequences” herein. Pursuant to this approach, it is the opinion of Sidley Austin llp that upon the sale, exchange, redemption or maturity of your notes, it would be reasonable for you to recognize capital gain or loss equal to the difference, if any, between the amount of cash you receive at such time and your tax basis in your notes.

Automatic call feature: if, on a call observation date, the closing level of each underlier is greater than or equal to the applicable call level, your notes will be automatically called; if your notes are automatically called on any call observation date, on the corresponding call payment date you will receive the applicable amount specified in the table set forth under “Call payment dates” below, which is an amount in cash equal to the sum of (i) $1,000 plus (ii) the product of $1,000 times the applicable call premium amount, and no further payments will be made since your notes will no longer be outstanding. If, on a call observation date, the closing level of any underlier is below the applicable call level, the notes will not be automatically called.

Cash settlement amount (on any call payment date): if, on a call observation date, the closing level of each underlier is greater than or equal to the applicable call level, your notes will be automatically called on such call observation date and for each $1,000 face amount of your notes, on the related call payment date, we will pay you the applicable amount specified in the table set forth under “Call Payment Dates” below, which is an amount in cash equal to the sum of (i) $1,000 plus (ii) the product of $1,000 times the applicable call premium amount.

Cash settlement amount (on the stated maturity date): if your notes are not automatically called, for each $1,000 face amount of your notes, we will pay you on the stated maturity date an amount in cash equal to:

| · |

if the final underlier level of each underlier is greater than or equal to 88% of its initial underlier level, the sum of (i) $1,000 plus (ii) the product of (a) $1,000 times (b) the maturity date premium amount;

|

| · |

if the final underlier level of each underlier is greater than or equal to 60% of its initial underlier level but the final underlier level of any underlier is less than 88% of its initial underlier level, $1,100; or

|

| · |

if the final underlier level of any underlier is less than 60% of its initial underlier level, the sum of (i) $1,000 plus (ii) the product of (a) the lesser performing underlier return times (b) $1,000. You will receive less than 60% of the face amount of your note

|

Lesser performing underlier return: the underlier return of the lesser performing underlier

Lesser performing underlier: the underlier with the lowest underlier return

Call premium amount: with respect to any call payment date, the applicable call premium amount specified in the table set forth under “Call payment dates” below

Maturity date premium amount: 51%

Initial underlier level (to be set on the trade date): with respect to each underlier, the closing level of such underlier on the trade date

Final underlier level: with respect to each underlier, the closing level of such underlier on the determination date, subject to anti-dilution adjustments (with respect to the iShares® MSCI Emerging Markets ETF only) as described under “Supplemental Terms of the Notes — Anti-dilution Adjustments for Exchange-Traded Funds” on page S-28 of the accompanying general terms supplement no. 1,734, and except in the limited circumstances described under “Supplemental Terms of the Notes — Consequences of a Market Disruption Event or a Non-Trading Day” on page S-23 of the accompanying general terms supplement no. 1,734 and subject to adjustment as provided under “Supplemental Terms of the Notes — Discontinuance or Modification of an Underlier” on page S-27 of the accompanying general terms supplement no. 1,734

Closing level: with respect to each underlier, as described under “Supplemental Terms of the Notes — Special Calculation Provisions — Closing Level” on page S-31 of the accompanying general terms supplement no. 1,734, subject to anti-dilution adjustments (with respect to the iShares® MSCI Emerging Markets ETF only) as described under “Supplemental Terms of the Notes — Anti-dilution Adjustments for Exchange-Traded Funds” on page S-28 of the accompanying general terms supplement no. 1,734

Underlier return: with respect to each underlier, the quotient of (i) the final underlier level minus the initial underlier level divided by (ii) the initial underlier level, expressed as a positive or negative percentage

Defeasance: not applicable

No interest: the offered notes will not bear interest

No listing: the offered notes will not be listed or displayed on any securities exchange or interdealer market quotation system

Business day: as described under “Supplemental Terms of the Notes — Special Calculation Provisions — Business Day” on page S-30 of the accompanying general terms supplement no. 1,734

Trading day: as described under “Supplemental Terms of the Notes — Special Calculation Provisions — Trading Day” on page S-31 of the accompanying general terms supplement no. 1,734

Trade date: expected to be August 16, 2018

Original issue date (settlement date) (to be set on the trade date): expected to be August 23, 2018

Stated maturity date (to be set on the trade date): expected to be August 28, 2023, subject to adjustment as described under “Supplemental Terms of the Notes — Stated Maturity Date” on page S-16 of the accompanying general terms supplement no. 1,734

Determination date (to be set on the trade date): expected to be August 21, 2023, subject to adjustment as described under “Supplemental Terms of the Notes — Determination Date” on page S-16 of the accompanying general terms supplement no. 1,734

Call observation dates (to be set on the trade date): expected to be the dates specified as such in the table set forth under “Call payment dates” below, subject to adjustment as described under “Supplemental Terms of the Notes — Call Observation Dates” on page S-20 of the accompanying general terms supplement no. 1,734

Call payment dates (to be set on the trade date): expected to be the fifth business day after each call observation date, which call payment dates are expected to be the dates specified in the table below, subject to adjustment as described under “Supplemental Terms of the Notes — Call Payment Dates” on page S-16 of the accompanying general terms supplement no. 1,734

|

Call Observation

Dates

|

Call Payment Dates

|

Call Level

(Expressed as a

Percentage of the

Initial Underlier

Level)

|

Call Premium

Amount*

|

Amount Paid on the Applicable

Call Payment Date**

|

|

August 26, 2019

|

September 3, 2019

|

100%

|

10.2%

|

$1,102

|

|

February 19, 2020

|

February 26, 2020

|

98.5%

|

15.3%

|

$1,153

|

|

August 19, 2020

|

August 26, 2020

|

97%

|

20.4%

|

$1,204

|

|

February 19, 2021

|

February 26, 2021

|

95.5%

|

25.5%

|

$1,255

|

|

August 19, 2021

|

August 26, 2021

|

94%

|

30.6%

|

$1,306

|

|

February 22, 2022

|

March 1, 2022

|

92.5%

|

35.7%

|

$1,357

|

|

August 19, 2022

|

August 26, 2022

|

91%

|

40.8%

|

$1,408

|

|

February 21, 2023

|

February 28, 2023

|

89.5%

|

45.9%

|

$1,459

|

* the applicable call premium amount will be set on the trade date

** the amount paid on the applicable call payment date will correspond to the applicable call premium amount set on the trade date

Use of proceeds and hedging: as described under “Use of Proceeds” and “Hedging” on page S-92 of the accompanying general terms supplement no. 1,734

ERISA: as described under “Employee Retirement Income Security Act” on page S-95 of the accompanying general terms supplement no. 1,734

Supplemental plan of distribution; conflicts of interest: as described under “Supplemental Plan of Distribution” on page S-96 of the accompanying general terms supplement no. 1,734 and “Plan of Distribution — Conflicts of Interest” on page 98 of the accompanying prospectus; GS Finance Corp. estimates that its share of the total offering expenses, excluding underwriting discounts and commissions, will be approximately $ .

GS Finance Corp. expects to agree to sell to Goldman Sachs & Co. LLC (“GS&Co.”), and GS&Co. expects to agree to purchase from GS Finance Corp., the aggregate face amount of the offered notes specified on the front cover of this pricing supplement. GS&Co. proposes initially to offer the notes to the public at the original issue price set forth on the cover page of this pricing supplement, and to certain securities dealers at such price less a concession not in excess of % of the face amount. In addition to the concession, any such securities dealer will receive from us a structuring fee of % of the face amount of each such note.

GS&Co. has engaged Incapital LLC to provide certain marketing services from time to time relating to notes of this series. Incapital LLC will receive a fee of % of the face amount of each note offered hereby from us in connection with such service.

GS&Co. is an affiliate of GS Finance Corp. and The Goldman Sachs Group, Inc. and, as such, will have a “conflict of interest” in this offering of notes within the meaning of Financial Industry Regulatory Authority, Inc. (FINRA) Rule 5121. Consequently, this offering of notes will be conducted in compliance with the provisions of FINRA Rule 5121. GS&Co. will not be permitted to sell notes in this offering to an account over which it exercises discretionary authority without the prior specific written approval of the account holder.

We expect to deliver the notes against payment therefor in New York, New York on August 23, 2018. Under Rule 15c6-1 of the Securities Exchange Act of 1934, trades in the secondary market generally are required to settle in two business days, unless the parties to any such trade expressly agree otherwise. Accordingly, purchasers who wish to trade notes on any date prior to two business days before delivery will be required to specify alternative settlement arrangements to prevent a failed settlement.

We have been advised by GS&Co. that it intends to make a market in the notes. However, neither GS&Co. nor any of our other affiliates that makes a market is obligated to do so and any of them may stop doing so at any time without notice. No assurance can be given as to the liquidity or trading market for the notes.

Calculation agent: GS&Co.

CUSIP no.: 40055QTP7

ISIN no.: US40055QTP71

FDIC: the notes are not bank deposits and are not insured by the Federal Deposit Insurance Corporation or any other governmental agency, nor are they obligations of, or guaranteed by, a bank

The following examples are provided for purposes of illustration only. They should not be taken as an indication or prediction of future investment results and are intended merely to illustrate (i) the impact that various hypothetical closing levels of the underliers on a call observation date and on the determination date could have on the cash settlement amount on a call payment date or on the stated maturity date, as the case may be, assuming all other variables remain constant.

The examples below are based on a range of underlier levels that are entirely hypothetical; no one can predict what the underlier level of any underlier will be on any day throughout the life of your notes, what the closing level of any underlier will be on any call observation date and what the final underlier level of the lesser performing underlier will be on the determination date. The underliers have been highly volatile in the past — meaning that the underlier levels have changed substantially in relatively short periods — and their performance cannot be predicted for any future period.

The information in the following examples reflects hypothetical rates of return on the offered notes assuming that they are purchased on the original issue date at the face amount and held to a call payment date or the stated maturity date, as the case may be. If you sell your notes in a secondary market prior to a call payment date or the stated maturity date, as the case may be, your return will depend upon the market value of your notes at the time of sale, which may be affected by a number of factors that are not reflected in the examples below such as interest rates, the volatility of the underliers, the creditworthiness of GS Finance Corp., as issuer, and the creditworthiness of The Goldman Sachs Group, Inc., as guarantor. In addition, the estimated value of your notes at the time the terms of your notes are set on the trade date (as determined by reference to pricing models used by GS&Co.) is less than the original issue price of your notes. For more information on the estimated value of your notes, see “Additional Risk Factors Specific to Your Notes — The Estimated Value of Your Notes At the Time the Terms of Your Notes Are Set On the Trade Date (as Determined By Reference to Pricing Models Used By GS&Co.) Is Less Than the Original Issue Price Of Your Notes” on page PS-11 of this pricing supplement. The information in the examples also reflects the key terms and assumptions in the box below.

|

Key Terms and Assumptions

|

|||

|

Face amount

|

$1,000

|

||

|

Call premium amount

|

The applicable call premium amount for each call payment date is specified on page PS-5 of this pricing supplement and assumes a call premium amount for such call payment date set at the bottom of the call premium amount range

|

||

|

Maturity date premium amount

|

51%

|

||

|

The notes are not automatically called, unless otherwise indicated below

Neither a market disruption event nor a non-trading day occurs on any originally scheduled call observation date or the originally scheduled determination date

|

|||

|

No change in or affecting (i) the underliers, (ii) any of the underlier stocks, (iii) the methods by which the applicable underlier sponsor calculates the EURO STOXX 50® Index or the underlying index of the iShares® MSCI Emerging Markets ETF or (iv) the policies of the iShares® MSCI Emerging Markets ETF’s investment advisor

|

|||

|

Notes purchased on original issue date at the face amount and held to a call payment date or the stated maturity date

|

|||

Moreover, we have not yet set the initial underlier levels that will serve as the baseline for determining the amount that we will pay on your notes, if any, on a call payment date or at maturity. We will not do so until the trade date. As a result, the actual initial underlier levels may differ substantially from the underlier levels prior to the trade date. They may also differ substantially from the underlier levels at the time you purchase your notes.

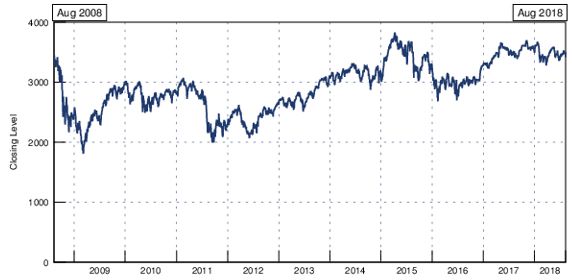

For these reasons, the actual performance of the underliers over the life of your notes, as well as the amount payable on a call payment date or at maturity, if any, may bear little relation to the hypothetical examples shown below or to the historical underlier levels shown elsewhere in this pricing supplement. For information about the underlier levels during recent periods, see “The Underliers — Historical Closing Levels of the Underliers” on page PS-23. Before investing in the notes, you should consult publicly available information to determine the underlier levels between the date of this pricing supplement and the date of your purchase of the notes.

Also, the hypothetical examples shown below do not take into account the effects of applicable taxes. Because of the U.S. tax treatment applicable to your notes, tax liabilities could affect the after-tax rate of return on your notes to a comparatively greater extent than the after-tax return on the underlier stocks.

The following examples reflect hypothetical cash settlement amounts that you could receive on the applicable call payment dates. While there are eight potential call payment dates with respect to your notes, the examples below only illustrate the amount you will receive, if any, on the first and second call payment date.

Hypothetical Payment on a Call Payment Date

If the notes are automatically called on the first call observation date (i.e., on the first call observation date the closing level of each underlier is greater than or equal to 100% of its initial underlier level), the cash settlement amount that we would deliver for each $1,000 face amount of your notes on the applicable call payment date would be the sum of $1,000 plus the product of the applicable call premium amount times $1,000. If, for example, the closing level of each underlier was determined to be 120% of its initial underlier level, your notes would be automatically called and the cash settlement amount that we would deliver on your notes on the corresponding call payment date would be 110.2% of the face amount of your notes or $1,102 for each $1,000 of the face amount of your notes.

If the notes are not automatically called on the first call observation date and are automatically called on the second call observation date (i.e., on the first call observation date the closing level of any underlier is less than 100% of its initial underlier level and on the second call observation date the closing level of each underlier is greater than or equal to 98.5% of its initial underlier level), the cash settlement amount that we would deliver for each $1,000 face amount of your notes on the applicable call payment date would be the sum of $1,000 plus the product of the applicable call premium amount times $1,000. If, for example, the closing level of each underlier was determined to be 99% of its initial underlier level, your notes would be automatically called and the cash settlement amount that we would deliver on your notes on the corresponding call payment date would be 115.3% of the face amount of your notes or $1,153 for each $1,000 of the face amount of your notes.

Hypothetical Payment at Maturity

If the notes are not automatically called on any call observation date (i.e., on each call observation date the closing level of any underlier is less than the applicable call level), the cash settlement amount we would deliver for each $1,000 face amount of your notes on the stated maturity date will depend on the performance of the lesser performing underlier on the determination date, as shown in the table below. The table below assumes that the notes have not been automatically called on a call observation date and reflects hypothetical cash settlement amounts that you could receive on the stated maturity date.

The levels in the left column of the table below represent hypothetical final underlier levels of the lesser performing underlier and are expressed as percentages of the initial underlier level of the lesser performing underlier. The amounts in the right column represent the hypothetical cash settlement amounts, based on the corresponding hypothetical final underlier level of the lesser performing underlier (expressed as a percentage of the initial underlier level of the lesser performing underlier), and are expressed as percentages of the face amount of a note (rounded to the nearest one-thousandth of a percent). Thus, a hypothetical cash settlement amount of 100.000% means that the value of the cash payment that we would deliver for each $1,000 of the outstanding face amount of the offered notes on the stated maturity date would equal 100.000% of the face amount of a note, based on the corresponding hypothetical final underlier level of the lesser performing underlier (expressed as a percentage of the initial underlier level of the lesser performing underlier) and the assumptions noted above.

|

The Notes Have Not Been Automatically Called

|

|

|

Hypothetical Final Underlier Level of the

Lesser Performing Underlier

|

Hypothetical Cash Settlement Amount

at Maturity if the Notes Have Not Been

Automatically Called on a Call

Observation Date

|

|

(as Percentage of Initial Underlier Level)

|

(as Percentage of Face Amount)

|

|

175.000%

|

151.000%

|

|

160.000%

|

151.000%

|

|

151.000%

|

151.000%

|

|

125.000%

|

151.000%

|

|

100.000%

|

151.000%

|

|

88.000%

|

151.000%

|

|

87.999%

|

110.000%

|

|

85.000%

|

110.000%

|

|

80.000%

|

110.000%

|

|

60.000%

|

110.000%

|

|

59.999%

|

59.999%

|

|

30.000%

|

30.000%

|

|

25.000%

|

25.000%

|

|

10.000%

|

10.000%

|

|

0.000%

|

0.000%

|

If, for example, the notes have not been automatically called on a call observation date and the final underlier level of the lesser performing underlier were determined to be 25.000% of its initial underlier level, the cash settlement amount that we would deliver on your notes at maturity would be 25.000% of the face amount of your notes, as shown in the table above. As a result, if you purchased your notes on the original issue date at the face amount and held them to the stated maturity date, you would lose 75.000% of your investment (if you purchased your notes at a premium to face amount you would lose a correspondingly higher percentage of your investment). If the notes have not been automatically called on a call observation date and the final underlier level of the lesser performing underlier were determined to be 80.000% of its initial underlier level, the cash settlement amount that we would deliver on your notes at maturity would be 110.000% of the face amount of your notes, as shown in the table above. In addition, if the final underlier level of the lesser performing underlier were determined to be 175.000% of its initial underlier level, the cash settlement amount that we would deliver on your notes at maturity would be limited to 151.000% of each $1,000 face amount of your notes, as shown in the table above. As a result, if you held your notes to the stated maturity date, the cash settlement amount will be capped, and you would not benefit from any increase in the final underlier level over the initial underlier level.

The cash settlement amounts shown above are entirely hypothetical; they are based on market prices for the underlier stocks that may not be achieved on the determination date and on assumptions that may prove to be erroneous. The actual market value of your notes on the stated maturity date or at any other time, including any time you may wish to sell your notes, may bear little relation to the hypothetical cash settlement amounts shown above, and these amounts should not be viewed as an indication of the financial return on an investment in the offered notes. The hypothetical cash settlement amounts on notes held to the stated maturity date in the examples above assume you purchased your notes at their face amount and have not been adjusted to reflect the actual issue price you pay for your notes. The return on your investment (whether positive or negative) in your notes will be affected by the amount you pay for your notes. If you purchase your notes for a price other than the face amount, the return on your investment will differ from, and may be significantly lower than, the hypothetical returns suggested by the above examples. Please read “Additional Risk Factors Specific to Your Notes — The Market Value of Your Notes May Be Influenced by Many Unpredictable Factors” on page S-3 of the accompanying general terms supplement no. 1,734.

Payments on the notes are economically equivalent to the amounts that would be paid on a combination of other instruments. For example, payments on the notes are economically equivalent to a combination of an interest-bearing bond bought by the holder and one or more options entered into between the holder and us (with one or more implicit option premiums paid over time). The discussion in this paragraph does not modify or affect the terms of the notes or the U.S. federal income tax treatment of the notes, as described elsewhere in this pricing supplement.

|

We cannot predict the actual closing levels of the underliers on any day, the final underlier levels or what the market value of your notes will be on any particular trading day, nor can we predict the relationship between the closing levels of the underliers and the market value of your notes at any time prior to the stated maturity date. The actual amount that you will receive on a call payment date or the stated maturity date, if any, and the rate of return on the offered notes will depend on whether or not the notes are automatically called and the actual initial underlier levels, which we will set on the trade date, and on the actual closing levels of the underliers on the call observation dates and the actual final underlier levels determined by the calculation agent as described above. Moreover, the assumptions on which the hypothetical examples are based may turn out to be inaccurate. Consequently, the cash amount to be paid in respect of your notes on a call payment date or the stated maturity date, as applicable, may be very different from the information reflected in the examples above.

|

|

An investment in your notes is subject to the risks described below, as well as the risks and considerations described in the accompanying prospectus, in the accompanying prospectus supplement and under “Additional Risk Factors Specific to the Notes” in the accompanying general terms supplement no. 1,734. You should carefully review these risks and considerations as well as the terms of the notes described herein and in the accompanying prospectus, the accompanying prospectus supplement and the accompanying general terms supplement no. 1,734. Your notes are a riskier investment than ordinary debt securities. Also, your notes are not equivalent to investing directly in the underlier stocks, i.e., with respect to an underlier to which your notes are linked, the stocks comprising such underlier. You should carefully consider whether the offered notes are suited to your particular circumstances.

|

The Estimated Value of Your Notes At the Time the Terms of Your Notes Are Set On the Trade Date (as Determined By Reference to Pricing Models Used By GS&Co.) Is Less Than the Original Issue Price Of Your Notes

The original issue price for your notes exceeds the estimated value of your notes as of the time the terms of your notes are set on the trade date, as determined by reference to GS&Co.’s pricing models and taking into account our credit spreads. Such estimated value on the trade date is set forth above under “Estimated Value of Your Notes”; after the trade date, the estimated value as determined by reference to these models will be affected by changes in market conditions, the creditworthiness of GS Finance Corp., as issuer, the creditworthiness of The Goldman Sachs Group, Inc., as guarantor, and other relevant factors. The price at which GS&Co. would initially buy or sell your notes (if GS&Co. makes a market, which it is not obligated to do), and the value that GS&Co. will initially use for account statements and otherwise, also exceeds the estimated value of your notes as determined by reference to these models. As agreed by GS&Co. and the distribution participants, this excess (i.e., the additional amount described under “Estimated Value of Your Notes”) will decline to zero on a straight line basis over the period from the date hereof through the applicable date set forth above under “Estimated Value of Your Notes”. Thereafter, if GS&Co. buys or sells your notes it will do so at prices that reflect the estimated value determined by reference to such pricing models at that time. The price at which GS&Co. will buy or sell your notes at any time also will reflect its then current bid and ask spread for similar sized trades of structured notes.

In estimating the value of your notes as of the time the terms of your notes are set on the trade date, as disclosed above under “Estimated Value of Your Notes”, GS&Co.’s pricing models consider certain variables, including principally our credit spreads, interest rates (forecasted, current and historical rates), volatility, price-sensitivity analysis and the time to maturity of the notes. These pricing models are proprietary and rely in part on certain assumptions about future events, which may prove to be incorrect. As a result, the actual value you would receive if you sold your notes in the secondary market, if any, to others may differ, perhaps materially, from the estimated value of your notes determined by reference to our models due to, among other things, any differences in pricing models or assumptions used by others. See “Additional Risk Factors Specific to the Notes — The Market Value of Your Notes May Be Influenced by Many Unpredictable Factors” on page S-3 of the accompanying general terms supplement no. 1,734.

The difference between the estimated value of your notes as of the time the terms of your notes are set on the trade date and the original issue price is a result of certain factors, including principally the underwriting discount and commissions, the expenses incurred in creating, documenting and marketing the notes, and an estimate of the difference between the amounts we pay to GS&Co. and the amounts GS&Co. pays to us in connection with your notes. We pay to GS&Co. amounts based on what we would pay to holders of a non-structured note with a similar maturity. In return for such payment, GS&Co. pays to us the amounts we owe under your notes.

In addition to the factors discussed above, the value and quoted price of your notes at any time will reflect many factors and cannot be predicted. If GS&Co. makes a market in the notes, the price quoted by GS&Co. would reflect any changes in market conditions and other relevant factors, including any deterioration in our creditworthiness or perceived creditworthiness or the creditworthiness or perceived creditworthiness of The Goldman Sachs Group, Inc. These changes may adversely affect the value of your

notes, including the price you may receive for your notes in any market making transaction. To the extent that GS&Co. makes a market in the notes, the quoted price will reflect the estimated value determined by reference to GS&Co.’s pricing models at that time, plus or minus its then current bid and ask spread for similar sized trades of structured notes (and subject to the declining excess amount described above).

Furthermore, if you sell your notes, you will likely be charged a commission for secondary market transactions, or the price will likely reflect a dealer discount. This commission or discount will further reduce the proceeds you would receive for your notes in a secondary market sale.

There is no assurance that GS&Co. or any other party will be willing to purchase your notes at any price and, in this regard, GS&Co. is not obligated to make a market in the notes. See “— Your Notes May Not Have an Active Trading Market” below.

The Underwriting Discount and Commissions, Including the Structuring Fee and Marketing Fee, and Other Expenses, Result in Less Favorable Economic Terms of the Notes and Could Adversely Affect Any Secondary Market Price for the Notes

The economic terms of the notes, as well as the difference between the estimated value of your notes as of the time the terms of your notes are set on the trade date and the original issue price, take into consideration, among other expenses, the underwriting discount and commissions, including the structuring fee and marketing fee, paid in connection with the notes. Therefore, the economic terms of the notes are less favorable to you than they would have been if these expenses had not been paid or had been lower. Further, the price, if any, at which GS&Co. will buy or sell your notes (if GS&Co. makes a market, which it is not obligated to do) at any time will reflect, among other things, the economic terms of the notes. Therefore, the secondary market price for the notes could also be adversely affected by the underwriting discount and commissions, including the structuring fee and marketing fee, and other expenses paid in connection with the notes. See “The Estimated Value of Your Notes At the Time the Terms of Your Notes Are Set On the Trade Date (as Determined By Reference to Pricing Models Used By GS&Co.) Is Less Than the Original Issue Price Of Your Notes” above.

The Notes Are Subject to the Credit Risk of the Issuer and the Guarantor

Although the return on the notes will be based on the performance of each underlier, the payment of any amount due on the notes is subject to the credit risk of GS Finance Corp., as issuer of the notes, and the credit risk of The Goldman Sachs Group, Inc., as guarantor of the notes . The notes are our unsecured obligations. Investors are dependent on our ability to pay all amounts due on the notes, and therefore investors are subject to our credit risk and to changes in the market’s view of our creditworthiness. Similarly, investors are dependent on the ability of The Goldman Sachs Group, Inc., as guarantor of the notes, to pay all amounts due on the notes, and therefore are also subject to its credit risk and to changes in the market’s view of its creditworthiness. See “Description of the Notes We May Offer — Information About Our Medium-Term Notes, Series E Program — How the Notes Rank Against Other Debt” on page S-4 of the accompanying prospectus supplement and “Description of Debt Securities We May Offer— Guarantee by The Goldman Sachs Group, Inc.” on page 42 of the accompanying prospectus.

You May Lose Your Entire Investment in the Notes

You can lose your entire investment in the notes. Assuming your notes are not automatically called, the cash settlement amount on your notes, if any, on the stated maturity date will be based on the performance of the lesser performing of the EURO STOXX 50® Index and the iShares® MSCI Emerging Markets ETF (“the ETF”), in each case as measured from their initial underlier levels (set on the trade date) to their closing levels on the determination date. If the underlier return of any underlier is less than -40%, you will have a loss for each $1,000 of the face amount of your notes equal to the product of the lesser performing underlier return times $1,000. Thus, you may lose your entire investment in the notes, which would include any premium to face amount you paid when you purchased the notes.

Also, the market price of your notes prior to a call payment date or the stated maturity date, as the case may be, may be significantly lower than the purchase price you pay for your notes. Consequently, if you sell your notes before the stated maturity date, you may receive far less than the amount of your investment in the notes.

The Cash Settlement Amount You Will Receive on a Call Payment Date or on the Stated Maturity Date, as the Case May Be, Will Be Capped

Regardless of the closing levels of the underliers on each of the call observation dates, the cash settlement amount you may receive on a call payment date is capped. Even if the closing level of each underlier on a call observation date exceeds the applicable call level, causing the notes to be automatically called on such day, the cash settlement amount on the call payment date will be capped, and you will not benefit from any increase in the closing level of any underlier above the initial underlier level on a call observation date. If your notes are automatically called on a call observation date, the maximum payment you will receive for each $1,000 face amount of your notes on the call payment date will depend on the applicable call premium amount. In addition, if the notes have not been automatically called and the closing level of each underlier on the determination date is greater than 88% of its initial underlier level, the cash settlement amount you will receive on the stated maturity date will be capped and your return will be limited to the maturity date premium amount, regardless of any increase in the closing level of any underlier above its initial underlier level.

Your Notes Are Subject to Automatic Redemption

We will automatically call your notes on a call observation date and redeem all, but not part, of your notes on the corresponding call payment date if the closing level of each underlier on the call observation date is greater than or equal to the applicable call level. Therefore, the term for your notes may be reduced to approximately one year after the original issue date. You may not be able to reinvest the proceeds from an investment in the notes at a comparable return for a similar level of risk in the event the notes are automatically called prior to maturity.

The Cash Settlement Amount You Will Receive on a Call Payment Date or on the Stated Maturity Date is Not Linked to the Closing Level of the Underliers at Any Time Other Than on the Applicable Call Observation Date or on the Determination Date, as the Case May Be

The cash settlement amount you will receive on a call payment date, if any, will be paid only if the closing level of each underlier on the call observation date is equal to or greater than the applicable call level. Therefore, the closing levels of the underliers on dates other than the call observation dates will have no effect on any cash settlement amount paid in respect of your notes on the call payment date. In addition, the cash settlement amount you will receive on the stated maturity date, if any, will be based on the closing level of the underliers on the determination date (which is subject to postponement in case of market disruption events or non-trading days), and therefore not the simple performance of the underliers over the life of your notes. Therefore, if the closing level of the underliers dropped precipitously on the determination date, the cash settlement amount for your notes may be significantly less than it would have been had the cash settlement amount been linked to the closing level of the underliers prior to such drop in the level of the underliers.

The Cash Settlement Amount Will Be Based Solely on the Lesser Performing Underlier

If the notes are not automatically called, the cash settlement amount will be based on the lesser performing underlier without regard to the performance of the other underlier. As a result, you could lose all or some of your initial investment if the lesser performing underlier return is negative, even if there is an increase in the level of the other underlier. This could be the case even if the other underlier increased by an amount greater than the decrease in the lesser performing underlier.

Your Notes Will Not Bear Interest

You will not receive any interest payments on your notes. As a result, even if the cash settlement amount payable for your notes on a call payment date or the stated maturity date, as applicable, exceeds the face amount of your notes, the overall return you earn on your notes may be less than you would have earned by investing in a non-indexed debt security of comparable maturity that bears interest at a prevailing market rate.

The Return on Your Notes May Change Significantly Despite Only a Small Change in the Final Underlier Level of the Lesser Performing Underlier

If the final underlier level of the lesser performing underlier is less than 60% of its initial underlier level, you will receive less than the face amount of your notes and you could lose all or a substantial portion of your investment in the notes. This means that while a 40% drop between the initial underlier level of the lesser performing underlier and its final underlier level will result in a cash settlement amount equal to 110% of the face amount of your notes, a decrease in the final underlier level of the lesser performing underlier to less than 60% of its initial underlier level will result in a loss of a significant portion of your investment in the notes despite only a small change in the final underlier level of the lesser performing underlier.

If You Purchase Your Notes at a Premium to Face Amount, the Return on Your Investment Will Be Lower Than the Return on Notes Purchased at Face Amount and the Impact of Certain Key Terms of the Notes Will Be Negatively Affected

The cash settlement amount you will be paid for your notes on the stated maturity date, if any, or the amount you will be paid on a call payment date will not be adjusted based on the issue price you pay for the notes. If you purchase notes at a price that differs from the face amount of the notes, then the return on your investment in such notes held to a call payment date or the stated maturity date will differ from, and may be substantially less than, the return on notes purchased at face amount. If you purchase your notes at a premium to face amount and hold them to a call payment date or the stated maturity date, the return on your investment in the notes will be lower than it would have been had you purchased the notes at face amount or a discount to face amount.

Your Notes May Not Have an Active Trading Market

Your notes will not be listed or displayed on any securities exchange or included in any interdealer market quotation system, and there may be little or no secondary market for your notes. Even if a secondary market for your notes develops, it may not provide significant liquidity and we expect that transaction costs in any secondary market would be high. As a result, the difference between bid and asked prices for your notes in any secondary market could be substantial.

We May Sell an Additional Aggregate Face Amount of the Notes at a Different Issue Price

At our sole option, we may decide to sell an additional aggregate face amount of the notes subsequent to the date of this pricing supplement. The issue price of the notes in the subsequent sale may differ substantially (higher or lower) from the issue price you paid as provided on the cover of this pricing supplement.

The Return on Your Notes Will Not Reflect Any Dividends Paid on the ETF or Any Underlier Stock

The return on your notes will not reflect the return you would realize if you actually owned the ETF and received the distributions paid on the shares of the ETF. You will not receive any dividends that may be paid on any of the underlier stocks by the underlier stock issuers or the shares of the ETF. See “—You Have No Shareholder Rights or Rights to Receive Any Shares of the ETF or Any Underlier Stock” below for additional information.

You Have No Shareholder Rights or Rights to Receive Any Shares of the ETF or Any Underlier Stock

Investing in your notes will not make you a holder of any shares of the ETF or any underlier stocks. Neither you nor any other holder or owner of your notes will have any rights with respect to the ETF or the underlier stocks, including any voting rights, any right to receive dividends or other distributions, any rights to make a claim against the ETF or the underlier stocks or any other rights of a holder of any shares of the ETF or the underlier stocks. Your notes will be paid in cash and you will have no right to receive delivery of any shares of the ETF or any underlier stocks.

The Policies of the ETF’s Investment Advisor, BlackRock Fund Advisors, and MSCI, the Sponsor of the Underlying Index, Could Affect the Amount Payable on Your Notes and Their Market Value

The ETF’s investment advisor, BlackRock Fund Advisors (“BFA” or the “ETF investment advisor”), may from time to time be called upon to make certain policy decisions or judgments with respect to the implementation of policies of the ETF investment advisor concerning the calculation of the net asset value of the ETF, additions, deletions or substitutions of securities in the ETF and the manner in which changes affecting the underlying index are reflected in the ETF that could affect the market price of the shares of the ETF, and therefore, the amount payable on your notes on the stated maturity date. The amount payable on your notes and their market value could also be affected if the ETF investment advisor changes these policies, for example, by changing the manner in which it calculates the net asset value of the ETF, or if the ETF investment advisor discontinues or suspends calculation or publication of the net asset value of the ETF, in which case it may become difficult or inappropriate to determine the market value of your notes.

If events such as these occur, the calculation agent — which initially will be GS&Co. — may determine the closing level of the ETF on a call observation date or the determination date, as applicable — and thus the amount payable on a call payment date or the stated maturity date, if any — in a manner, in its sole discretion, it considers appropriate. We describe the discretion that the calculation agent will have in determining the closing level of the ETF and the amount payable on your notes more fully under “Supplemental Terms of the Notes — Discontinuance or Modification of an Underlier” on page S-27 of the accompanying general terms supplement no. 1,734.

In addition, MSCI (the “underlying index sponsor”) owns the underlying index and is responsible for the design and maintenance of the underlying index. The policies of the underlying index sponsor concerning the calculation of the underlying index, including decisions regarding the addition, deletion or substitution of the equity securities included in the underlying index, could affect the level of the underlying index and, consequently, could affect the market prices of shares of the ETF and, therefore, the amount payable on your notes and their market value.

There Are Risks Associated with the ETF

Although the ETF’s shares are listed for trading on NYSE Arca, Inc. (the “NYSE Arca”) and a number of similar products have been traded on the NYSE Arca or other securities exchanges for varying periods of time, there is no assurance that an active trading market will continue for the shares of the ETF or that there will be liquidity in the trading market.

In addition, the ETF is subject to management risk, which is the risk that the ETF investment advisor’s investment strategy, the implementation of which is subject to a number of constraints, may not produce the intended results. For example, the ETF investment advisor may select up to 10% of the ETF’s assets to be invested in shares of equity securities that are not included in the underlying index. The ETF is also not actively managed and may be affected by a general decline in market segments relating to the underlying index. The ETF investment advisor invests in securities included in, or representative of, the underlying index regardless of their investment merits. The ETF investment advisor does not attempt to take defensive positions in declining markets.

In addition, the ETF is subject to custody risk, which refers to the risks in the process of clearing and settling trades and to the holding of securities by local banks, agent and depositories. Low trading volumes and volatile prices in less developed markets make trades harder to complete and settle, and governments or trade groups may compel local agents to hold securities in designated depositories that are not subject to independent evaluation. The less developed a country’s securities market is, the greater the likelihood of custody problems.

Further, under continuous listing standards adopted by the NYSE Arca, the ETF will be required to confirm on an ongoing basis that the components of the underlying index satisfy the applicable listing requirements. In the event that its underlying index does not comply with the applicable listing requirements, the ETF would be required to rectify such non-compliance by requesting that the underlying index sponsor modify such underlying index, adopting a new underlying index or obtaining relief from the Securities and Exchange Commission. There can be no assurance that the underlying index sponsor would so modify the underlying index or that relief would be obtained from the Securities and Exchange Commission and, therefore, non-compliance with the continuous listing standards may result in the ETF being delisted by the NYSE Arca.

The ETF and its Underlying Index are Different and the Performance of the ETF May Not Correlate with the Performance of its Underlying Index

The ETF uses a representative sampling strategy (more fully described under “The Underliers”) to attempt to track the performance of its underlying index. The ETF may not hold all or substantially all of the equity securities included in its underlying index and may hold securities or assets not included in its underlying index. Therefore, while the performance of the ETF is generally linked to the performance of its underlying index, the performance of the ETF is also linked in part to shares of equity securities not included in its underlying index and to the performance of other assets, such as futures contracts, options and swaps, as well as cash and cash equivalents, including shares of money market funds affiliated with the ETF investment advisor.

Imperfect correlation between the ETF’s portfolio securities and those in its underlying index, rounding of prices, changes to its underlying index and regulatory requirements may cause tracking error, which is the divergence of the ETF’s performance from that of its underlying index.

In addition, the performance of the ETF will reflect additional transaction costs and fees that are not included in the calculation of its underlying index and this may increase the tracking error of the ETF. Also, corporate actions with respect to the sample of equity securities (such as mergers and spin-offs) may impact the performance differential between the ETF and its underlying index. Finally, because the shares of the ETF are traded on the NYSE Arca and are subject to market supply and investor demand, the market value of one share of the ETF may differ from the net asset value per share of the ETF.

For all of the foregoing reasons, the performance of the ETF may not correlate with the performance of its underlying index. Consequently, the return on the notes will not be the same as investing directly in the underlying index or in the underlying index stocks, and will not be the same as investing in a debt security with a payment at maturity linked to the performance of the underlying index.

Investment in the Offered Notes Is Subject to Risks Associated with Foreign Securities Markets

The value of your notes is linked, in part, to the EURO STOXX 50® Index, which is comprised of stocks from one or more foreign securities markets, and, in part, to the iShares® MSCI Emerging Markets ETF, which holds stocks traded in the equity markets of emerging market countries. Investments linked to the value of foreign equity securities involve particular risks. Any foreign securities market may be less liquid, more volatile and affected by global or domestic market developments in a different way than are the U.S. securities market or other foreign securities markets. Both government intervention in a foreign securities market, either directly or indirectly, and cross-shareholdings in foreign companies, may affect trading prices and volumes in that market. Also, there is generally less publicly available information about foreign companies than about those U.S. companies that are subject to the reporting requirements of the U.S. Securities and Exchange Commission. Further, foreign companies are subject to accounting, auditing and financial reporting standards and requirements that differ from those applicable to U.S. reporting companies.

The prices of securities in a foreign country are subject to political, economic, financial and social factors that are unique to such foreign country’s geographical region. These factors include: recent changes, or the possibility of future changes, in the applicable foreign government’s economic and fiscal policies; the possible implementation of, or changes in, currency exchange laws or other laws or restrictions applicable to foreign companies or investments in foreign equity securities; fluctuations, or the possibility of fluctuations, in currency exchange rates; and the possibility of outbreaks of hostility, political instability, natural disaster or adverse public health developments. The United Kingdom has voted to leave the European Union (popularly known as “Brexit”). The effect of Brexit is uncertain, and Brexit has and may continue to contribute to volatility in the prices of securities of companies located in Europe and currency exchange rates, including the valuation of the euro and British pound in particular. Any one of these factors, or the combination of more than one of these factors, could negatively affect such foreign securities market and the price of securities therein. Further, geographical regions may react to global factors in different ways, which may cause the prices of securities in a foreign securities market to fluctuate in a way that differs from those of securities in the U.S. securities market or other foreign securities markets. Foreign economies may also differ from the U.S. economy in important respects, including growth of gross national product, rate of inflation, capital reinvestment, resources and self-sufficiency, which may have a positive or negative effect on foreign securities prices.

Because foreign exchanges may be open on days when the ETF is not traded, the value of the securities underlying the ETF may change on days when shareholders will not be able to purchase or sell shares of the ETF.

The countries whose markets are represented by the ETF include Brazil, Chile, China, Colombia, the Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Malaysia, Mexico, Pakistan, Peru, Philippines, Poland, Qatar, Russia, South Africa, South Korea, Taiwan, Thailand, Turkey and United Arab Emirates.

Countries with emerging markets may have relatively unstable governments, may present the risks of nationalization of businesses, restrictions on foreign ownership and prohibitions on the repatriation of assets, and may have less protection of property rights than more developed countries. The economies of

countries with emerging markets may be based on only a few industries, may be highly vulnerable to changes in local or global trade conditions, and may suffer from extreme and volatile debt burdens or inflation rates. Local securities markets may trade a small number of securities and may be unable to respond effectively to increases in trading volume, potentially making prompt liquidation of holdings difficult or impossible at times. It will also likely be more costly and difficult for the investment advisor to enforce the laws or regulations of a foreign country or trading facility, and it is possible that the foreign country or trading facility may not have laws or regulations which adequately protect the rights and interests of investors in the stocks included in the ETF.

Your Investment in the Notes Will Be Subject to Foreign Currency Exchange Rate Risk

The ETF holds assets that are denominated in non-U.S. dollar currencies. The value of the assets held by the ETF that are denominated in non-U.S. dollar currencies will be adjusted to reflect their U.S. dollar value by converting the price of such assets from the non-U.S. dollar currency to U.S. dollars. Consequently, if the value of the U.S. dollar strengthens against the non-U.S. dollar currency in which an asset is denominated, the level of the ETF may not increase even if the non-dollar value of the asset held by the ETF increases.

Foreign currency exchange rates vary over time, and may vary considerably during the term of your notes. Changes in a particular exchange rate result from the interaction of many factors directly or indirectly affecting economic and political conditions. Of particular importance are:

| ● |

existing and expected rates of inflation;

|

| ● |

existing and expected interest rate levels;

|

| ● |

the balance of payments among countries;

|

| ● |

the extent of government surpluses or deficits in the relevant foreign country and the United States; and

|

| ● |

other financial, economic, military and political factors.

|

All of these factors are, in turn, sensitive to the monetary, fiscal and trade policies pursued by the governments of the relevant foreign countries and the United States and other countries important to international trade and finance.

The market price of the notes and level of the ETF could also be adversely affected by delays in, or refusals to grant, any required governmental approval for conversions of a local currency and remittances abroad or other de facto restrictions on the repatriation of U.S. dollars.

It has been reported that the U.K. Financial Conduct Authority and regulators from other countries are in the process of investigating the potential manipulation of published currency exchange rates. If such manipulation has occurred or is continuing, certain published exchange rates may have been, or may be in the future, artificially lower (or higher) than they would otherwise have been. Any such manipulation could have an adverse impact on any payments on, and the value of, your notes and the trading market for your notes. In addition, we cannot predict whether any changes or reforms affecting the determination or publication of exchange rates or the supervision of currency trading will be implemented in connection with these investigations. Any such changes or reforms could also adversely impact your notes.

The Tax Consequences of an Investment in Your Notes Are Uncertain

The tax consequences of an investment in your notes are uncertain, both as to the timing and character of any inclusion in income in respect of your notes.

The Internal Revenue Service announced on December 7, 2007 that it is considering issuing guidance regarding the tax treatment of an instrument such as your notes, and any such guidance could adversely affect the value and the tax treatment of your notes. Among other things, the Internal Revenue Service may decide to require the holders to accrue ordinary income on a current basis and recognize ordinary income on payment at maturity, and could subject non-U.S. investors to withholding tax. Furthermore, in 2007, legislation was introduced in Congress that, if enacted, would have required holders that acquired instruments such as your notes after the bill was enacted to accrue interest income over the term of such instruments even though there will be no interest payments over the term of such instruments. It is not

possible to predict whether a similar or identical bill will be enacted in the future, or whether any such bill would affect the tax treatment of your notes. We describe these developments in more detail under “Supplemental Discussion of U.S. Federal Income Tax Consequences – United States Holders – Possible Change in Law” below. You should consult your tax advisor about this matter. Except to the extent otherwise provided by law, GS Finance Corp. intends to continue treating the notes for U.S. federal income tax purposes in accordance with the treatment described under “Supplemental Discussion of U.S. Federal Income Tax Consequences” on page PS-26 below unless and until such time as Congress, the Treasury Department or the Internal Revenue Service determine that some other treatment is more appropriate. Please also consult your tax advisor concerning the U.S. federal income tax and any other applicable tax consequences to you of owning your notes in your particular circumstances.

Your Notes May Be Subject to the Constructive Ownership Rules

There exists a risk that the constructive ownership rules of Section 1260 of the Internal Revenue Code could apply to all or a portion of your notes. If all or a portion of your notes were subject to the constructive ownership rules, then all or a portion of any long-term capital gain that you realize upon the sale, exchange, redemption or maturity of your notes (or the relevant portion of your notes) would be re-characterized as ordinary income (and you would be subject to an interest charge on deferred tax liability with respect to such re-characterized capital gain) to the extent that such capital gain exceeds the amount of “net underlying long-term capital gain” (as defined in Section 1260 of the Internal Revenue Code). Because the application of the constructive ownership rules is unclear, you are strongly urged to consult your tax advisor with respect to the possible application of the constructive ownership rules to your investment in the notes.

Foreign Account Tax Compliance Act (FATCA) Withholding May Apply to Payments on Your Notes, Including as a Result of the Failure of the Bank or Broker Through Which You Hold the Notes to Provide Information to Tax Authorities

Please see the discussion under “United States Taxation — Taxation of Debt Securities — Foreign Account Tax Compliance Act (FATCA) Withholding” in the accompanying prospectus for a description of the applicability of FATCA to payments made on your notes.

The EURO STOXX 50® Index is a free-float market capitalization-weighted index of 50 European blue-chip stocks and was created by and is sponsored and maintained by STOXX Limited. Publication of the EURO STOXX 50® Index began on February 26, 1998, based on an initial index value of 1,000 at December 31, 1991. The level of the EURO STOXX 50® Index is disseminated on the STOXX Limited website. STOXX Limited is under no obligation to continue to publish the index and may discontinue publication of it at any time. Additional information regarding the EURO STOXX 50® Index may be obtained from the STOXX Limited website: stoxx.com. We are not incorporating by reference the website or any material it includes in this pricing supplement.

The top ten constituent stocks of the EURO STOXX 50® Index as of August 9, 2018, by weight, are: Total S.A. (6.10%), SAP SE (4.50%), Siemens AG (3.96%), Bayer AG (3.70%), Allianz SE (3.46%), Sanofi (3.43%), LVMH Moët Hennessy Louis Vuitton SE (3.39%), ASML Holding N.V. (3.28%), Banco Santander S.A. (3.13%) and Unilever N.V. (3.12%); constituent weights may be found at stoxx.com/download/indices/factsheets/SX5GT.pdf under “Factsheets and Methodologies” and are updated periodically.

As of August 9, 2018, the sixteen industry sectors which comprise the EURO STOXX 50® Index represent the following weights in the index: Automobiles & Parts (4.44%), Banks (12.95%), Chemicals (5.00%), Construction & Materials (3.79%), Food & Beverage (4.52%), Health Care (10.89%), Industrial Goods & Services (10.97%), Insurance (6.53%), Media (0.94%), Oil & Gas (7.82%), Personal & Household Goods (10.23%), Real Estate (1.09%), Retail (2.38%), Technology (8.86%), Telecommunications (4.62%) and Utilities (4.96%); industry weightings may be found at stoxx.com/download/indices/factsheets/SX5GT.pdf under “Factsheets and Methodologies” and are updated periodically. Percentages may not sum to 100% due to rounding. Sector designations are determined by the underlier sponsor using criteria it has selected or developed. Index sponsors may use very different standards for determining sector designations. In addition, many companies operate in a number of sectors, but are listed in only one sector and the basis on which that sector is selected may also differ. As a result, sector comparisons between indices with different index sponsors may reflect differences in methodology as well as actual differences in the sector composition of the indices.

As of August 9, 2018, the eight countries which comprise the EURO STOXX 50® Index represent the following weights in the index: Belgium (2.72%), Finland (1.09%), France (38.52%), Germany (31.88%), Ireland (0.99%), Italy (4.65%), Netherlands (11.01%) and Spain (9.13%); country weightings may be found at stoxx.com/download/indices/factsheets/SX5GT.pdf under “Factsheets and Methodologies” and are updated periodically.

The above information supplements the description of the underlier found in the accompanying general terms supplement no. 1,734. This information was derived from information prepared by the underlier sponsor, however, the percentages we have listed above are approximate and may not match the information available on the underlier sponsor’s website due to subsequent corporation actions or other activity relating to a particular stock. For more details about the underlier , the underlier sponsor and license agreement between the underlier sponsor and the issuer, see “The Underliers — EURO STOXX 50® Index” on page S-75 of the accompanying general terms supplement no. 1,734.

The EURO STOXX 50® is the intellectual property of STOXX Limited, Zurich, Switzerland and/or its licensors (“Licensors”), which is used under license. The securities or other financial instruments based on the index are in no way sponsored, endorsed, sold or promoted by STOXX and its Licensors and neither STOXX nor its Licensors shall have any liability with respect thereto.

The iShares® MSCI Emerging Markets ETF