FALSE2021FY0000886163http://fasb.org/us-gaap/2021-01-31#AccountingStandardsUpdate201613MemberP3Y12.502.08http://fasb.org/us-gaap/2021-01-31#OtherLiabilitiesNoncurrenthttp://fasb.org/us-gaap/2021-01-31#OtherLiabilitiesNoncurrent0.01332510.0040244P3Y00008861632021-01-012021-12-3100008861632021-06-30iso4217:USD00008861632022-02-23xbrli:shares00008861632021-12-3100008861632020-12-31iso4217:USDxbrli:shares0000886163us-gaap:RoyaltyMember2021-01-012021-12-310000886163us-gaap:RoyaltyMember2020-01-012020-12-310000886163us-gaap:RoyaltyMember2019-01-012019-12-310000886163lgnd:MaterialSalesCaptisolMember2021-01-012021-12-310000886163lgnd:MaterialSalesCaptisolMember2020-01-012020-12-310000886163lgnd:MaterialSalesCaptisolMember2019-01-012019-12-310000886163lgnd:ContractRevenueMember2021-01-012021-12-310000886163lgnd:ContractRevenueMember2020-01-012020-12-310000886163lgnd:ContractRevenueMember2019-01-012019-12-3100008861632020-01-012020-12-3100008861632019-01-012019-12-310000886163lgnd:VernalisMember2021-01-012021-12-310000886163lgnd:VernalisMember2020-01-012020-12-310000886163lgnd:VernalisMember2019-01-012019-12-310000886163lgnd:PromactaMember2021-01-012021-12-310000886163lgnd:PromactaMember2020-01-012020-12-310000886163lgnd:PromactaMember2019-01-012019-12-310000886163us-gaap:CommonStockMember2018-12-310000886163us-gaap:AdditionalPaidInCapitalMember2018-12-310000886163us-gaap:AccumulatedOtherComprehensiveIncomeMember2018-12-310000886163us-gaap:RetainedEarningsMember2018-12-3100008861632018-12-310000886163us-gaap:CommonStockMember2019-01-012019-12-310000886163us-gaap:AdditionalPaidInCapitalMember2019-01-012019-12-310000886163us-gaap:AccumulatedOtherComprehensiveIncomeMember2019-01-012019-12-310000886163us-gaap:RetainedEarningsMember2019-01-012019-12-310000886163us-gaap:CommonStockMember2019-12-310000886163us-gaap:AdditionalPaidInCapitalMember2019-12-310000886163us-gaap:AccumulatedOtherComprehensiveIncomeMember2019-12-310000886163us-gaap:RetainedEarningsMember2019-12-3100008861632019-12-310000886163us-gaap:CommonStockMember2020-01-012020-12-310000886163us-gaap:AdditionalPaidInCapitalMember2020-01-012020-12-310000886163us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-01-012020-12-310000886163srt:CumulativeEffectPeriodOfAdoptionAdjustmentMemberus-gaap:RetainedEarningsMember2019-12-310000886163srt:CumulativeEffectPeriodOfAdoptionAdjustmentMember2019-12-310000886163us-gaap:RetainedEarningsMember2020-01-012020-12-310000886163us-gaap:CommonStockMember2020-12-310000886163us-gaap:AdditionalPaidInCapitalMember2020-12-310000886163us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-12-310000886163us-gaap:RetainedEarningsMember2020-12-310000886163us-gaap:CommonStockMember2021-01-012021-12-310000886163us-gaap:AdditionalPaidInCapitalMember2021-01-012021-12-310000886163us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-01-012021-12-310000886163us-gaap:RetainedEarningsMember2021-01-012021-12-310000886163us-gaap:CommonStockMember2021-12-310000886163us-gaap:AdditionalPaidInCapitalMember2021-12-310000886163us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-12-310000886163us-gaap:RetainedEarningsMember2021-12-31lgnd:segment0000886163lgnd:PartnerAMemberus-gaap:SalesRevenueNetMemberus-gaap:CustomerConcentrationRiskMember2021-01-012021-12-31xbrli:pure0000886163lgnd:PartnerAMemberus-gaap:SalesRevenueNetMemberus-gaap:CustomerConcentrationRiskMember2020-01-012020-12-310000886163us-gaap:SalesRevenueNetMemberlgnd:PartnerBMemberus-gaap:CustomerConcentrationRiskMember2021-01-012021-12-310000886163us-gaap:SalesRevenueNetMemberlgnd:PartnerBMemberus-gaap:CustomerConcentrationRiskMember2020-01-012020-12-310000886163us-gaap:SalesRevenueNetMemberlgnd:PartnerBMemberus-gaap:CustomerConcentrationRiskMember2019-01-012019-12-310000886163us-gaap:SalesRevenueNetMemberlgnd:PartnerCMemberus-gaap:CustomerConcentrationRiskMember2019-01-012019-12-310000886163lgnd:MaterialSalesCaptisolMember2021-12-310000886163lgnd:MaterialSalesCaptisolMember2020-12-310000886163srt:MinimumMember2021-01-012021-12-310000886163srt:MaximumMember2021-01-012021-12-310000886163lgnd:PfenexMember2020-10-010000886163lgnd:IcagenMember2020-04-010000886163lgnd:MetabasisTherapeuticsMember2010-01-31lgnd:right0000886163lgnd:AziyoandCorMatrixMemberus-gaap:LicensingAgreementsMember2021-12-310000886163lgnd:AziyoandCorMatrixMemberus-gaap:LicensingAgreementsMember2020-12-310000886163lgnd:SelexisAndDianomiMemberus-gaap:LicensingAgreementsMember2021-12-310000886163lgnd:SelexisAndDianomiMemberus-gaap:LicensingAgreementsMember2020-12-310000886163us-gaap:LicensingAgreementsMember2021-12-310000886163us-gaap:LicensingAgreementsMember2020-12-310000886163lgnd:NovanMolluscumProductsMemberus-gaap:LicensingAgreementsMember2019-05-012019-05-310000886163lgnd:NovanMolluscumProductsMemberus-gaap:RoyaltyAgreementsMember2019-05-310000886163lgnd:NovanMolluscumProductsMemberus-gaap:RoyaltyAgreementsMembersrt:MinimumMember2019-05-310000886163lgnd:NovanMolluscumProductsMemberus-gaap:RoyaltyAgreementsMembersrt:MaximumMember2019-05-310000886163us-gaap:RoyaltyAgreementsMemberlgnd:PalvellaTherapeuticsIncMember2018-12-310000886163us-gaap:RoyaltyAgreementsMembersrt:MinimumMemberlgnd:PalvellaTherapeuticsIncMember2018-12-310000886163us-gaap:RoyaltyAgreementsMembersrt:MaximumMemberlgnd:PalvellaTherapeuticsIncMember2018-12-310000886163us-gaap:LicensingAgreementsMemberlgnd:PalvellaTherapeuticsIncMember2018-12-012018-12-310000886163us-gaap:LicensingAgreementsMemberlgnd:PalvellaTherapeuticsIncMember2020-12-310000886163lgnd:ContractRevenueMemberlgnd:PalvellaTherapeuticsIncMember2020-01-012020-12-310000886163lgnd:AziyoMemberus-gaap:RoyaltyAgreementsMember2017-05-312017-05-310000886163lgnd:AziyoMemberus-gaap:RoyaltyAgreementsMember2017-05-310000886163us-gaap:RoyaltyAgreementsMember2017-05-310000886163lgnd:AziyoMemberus-gaap:RoyaltyAgreementsMembersrt:MaximumMember2017-05-310000886163us-gaap:RoyaltyAgreementsMemberlgnd:CorMatrixMember2017-05-310000886163us-gaap:RoyaltyAgreementsMemberlgnd:CorMatrixMember2017-05-312017-05-310000886163lgnd:AziyoMemberus-gaap:RoyaltyAgreementsMember2021-01-012021-12-310000886163lgnd:SelexisMemberus-gaap:RoyaltyAgreementsMember2021-01-012021-12-310000886163us-gaap:AccountingStandardsUpdate201613Memberus-gaap:LicensingAgreementsMember2020-01-010000886163lgnd:RoyaltyKyprolisMember2021-01-012021-12-310000886163lgnd:RoyaltyKyprolisMember2020-01-012020-12-310000886163lgnd:RoyaltyKyprolisMember2019-01-012019-12-310000886163lgnd:RoyaltyEvomelaMember2021-01-012021-12-310000886163lgnd:RoyaltyEvomelaMember2020-01-012020-12-310000886163lgnd:RoyaltyEvomelaMember2019-01-012019-12-310000886163lgnd:RoyaltyOtherMember2021-01-012021-12-310000886163lgnd:RoyaltyOtherMember2020-01-012020-12-310000886163lgnd:RoyaltyOtherMember2019-01-012019-12-310000886163lgnd:RoyaltyPromactaMember2019-01-012019-12-310000886163us-gaap:ServiceMember2021-01-012021-12-310000886163us-gaap:ServiceMember2020-01-012020-12-310000886163us-gaap:ServiceMember2019-01-012019-12-310000886163lgnd:LicenseFeesMember2021-01-012021-12-310000886163lgnd:LicenseFeesMember2020-01-012020-12-310000886163lgnd:LicenseFeesMember2019-01-012019-12-310000886163lgnd:MilestoneMember2021-01-012021-12-310000886163lgnd:MilestoneMember2020-01-012020-12-310000886163lgnd:MilestoneMember2019-01-012019-12-310000886163lgnd:LicenseFeesMilestonesAndOtherProductOtherMember2021-01-012021-12-310000886163lgnd:LicenseFeesMilestonesAndOtherProductOtherMember2020-01-012020-12-310000886163lgnd:LicenseFeesMilestonesAndOtherProductOtherMember2019-01-012019-12-310000886163us-gaap:PerformanceSharesMember2021-01-012021-12-310000886163srt:MinimumMemberus-gaap:PerformanceSharesMember2021-01-012021-12-310000886163srt:MaximumMemberus-gaap:PerformanceSharesMember2021-01-012021-12-310000886163us-gaap:MeasurementInputExpectedDividendRateMember2021-12-3100008861632007-01-012007-12-310000886163lgnd:TwoThousandTwoStockIncentivePlanMemberlgnd:VestingPeriodOneMemberus-gaap:EmployeeStockOptionMember2021-01-012021-12-310000886163lgnd:VestingPeriodTwoMemberlgnd:TwoThousandTwoStockIncentivePlanMemberus-gaap:EmployeeStockOptionMember2021-01-012021-12-310000886163lgnd:RestrictedStockUnitsAndPerformanceSharesMember2021-01-012021-12-310000886163lgnd:TwoThousandTwoStockIncentivePlanMemberus-gaap:EmployeeStockOptionMember2021-01-012021-12-310000886163lgnd:ConvertibleSeniorNotesDue2023Memberus-gaap:SeniorNotesMember2018-05-310000886163us-gaap:ConvertibleNotesPayableMemberlgnd:ConvertibleSeniorNotesDue2019Member2014-08-310000886163lgnd:ConvertibleSeniorNotesDue2019Member2019-08-150000886163us-gaap:StockCompensationPlanMember2020-01-012020-12-310000886163us-gaap:RestrictedStockMember2021-01-012021-12-310000886163us-gaap:RestrictedStockMember2020-01-012020-12-310000886163us-gaap:RestrictedStockMember2019-01-012019-12-310000886163us-gaap:EmployeeStockOptionMember2021-01-012021-12-310000886163us-gaap:EmployeeStockOptionMember2020-01-012020-12-310000886163us-gaap:EmployeeStockOptionMember2019-01-012019-12-310000886163lgnd:VernalisMemberus-gaap:DisposalGroupHeldForSaleOrDisposedOfBySaleNotDiscontinuedOperationsMember2020-12-022020-12-020000886163lgnd:VernalisMemberus-gaap:DisposalGroupHeldForSaleOrDisposedOfBySaleNotDiscontinuedOperationsMemberus-gaap:InProcessResearchAndDevelopmentMember2020-12-010000886163lgnd:VernalisMemberus-gaap:DisposalGroupHeldForSaleOrDisposedOfBySaleNotDiscontinuedOperationsMember2021-01-012021-12-310000886163lgnd:PromactaMemberus-gaap:DisposalGroupHeldForSaleOrDisposedOfBySaleNotDiscontinuedOperationsMember2019-03-062019-03-060000886163lgnd:PromactaMemberus-gaap:DisposalGroupHeldForSaleOrDisposedOfBySaleNotDiscontinuedOperationsMemberus-gaap:InProcessResearchAndDevelopmentMember2019-03-060000886163lgnd:PromactaMemberus-gaap:DisposalGroupHeldForSaleOrDisposedOfBySaleNotDiscontinuedOperationsMember2019-01-012019-03-060000886163lgnd:VikingTherapeuticsInc.Member2021-01-012021-12-310000886163us-gaap:WarrantMember2020-12-3100008861632019-01-012021-12-31lgnd:acquisition0000886163lgnd:PfenexMember2020-10-012020-10-010000886163lgnd:PfenexMemberus-gaap:MeasurementInputDiscountRateMember2020-10-010000886163lgnd:PfenexMember2021-01-012021-12-310000886163lgnd:PfenexMember2020-10-012020-12-310000886163lgnd:PfenexMemberlgnd:ContractualRelationshipsAlvogenMember2020-10-010000886163lgnd:PfenexMemberlgnd:ContractualRelationshipsAlvogenMember2020-10-012020-10-010000886163lgnd:PfenexMemberlgnd:ContractualRelationshipsMerckMember2020-10-010000886163lgnd:PfenexMemberlgnd:ContractualRelationshipsMerckMember2020-10-012020-10-010000886163lgnd:PfenexMemberlgnd:ContractualRelationshipsJazzMember2020-10-010000886163lgnd:PfenexMemberlgnd:ContractualRelationshipsJazzMember2020-10-012020-10-010000886163lgnd:PfenexMemberlgnd:ContractualRelationshipsSIIMember2020-10-010000886163lgnd:PfenexMemberlgnd:ContractualRelationshipsSIIMember2020-10-012020-10-010000886163lgnd:PfenexMemberlgnd:ContractualRelationshipsArcellxMember2020-10-010000886163lgnd:PfenexMemberlgnd:ContractualRelationshipsArcellxMember2020-10-012020-10-010000886163us-gaap:TechnologyBasedIntangibleAssetsMemberlgnd:PfenexMember2020-10-010000886163us-gaap:TechnologyBasedIntangibleAssetsMemberlgnd:PfenexMembersrt:MinimumMember2020-10-012020-10-010000886163us-gaap:TechnologyBasedIntangibleAssetsMemberlgnd:PfenexMembersrt:MaximumMember2020-10-012020-10-010000886163lgnd:PfenexMembersrt:MinimumMemberus-gaap:CustomerRelationshipsMember2020-04-012020-04-010000886163lgnd:PfenexMembersrt:MaximumMemberus-gaap:CustomerRelationshipsMember2020-04-012020-04-010000886163lgnd:PfenexMember2020-01-012020-12-310000886163lgnd:PfenexMember2019-01-012019-12-310000886163lgnd:TaurusBiosciencesLLCMember2020-09-092020-09-090000886163lgnd:TaurusBiosciencesLLCMemberlgnd:ContingentValueRightForInternalResearchAndDevelopmentMember2020-09-090000886163lgnd:TaurusBiosciencesLLCMemberlgnd:ContingentValueRightOnProductRevenuesMember2020-09-090000886163lgnd:TaurusBiosciencesLLCMemberlgnd:ContingentValueRightOnProductRevenuesMember2020-09-092020-09-090000886163lgnd:TaurusBiosciencesLLCMember2021-01-012021-12-310000886163lgnd:TaurusBiosciencesLLCMember2020-09-090000886163us-gaap:TechnologyBasedIntangibleAssetsMemberlgnd:TaurusBiosciencesLLCMember2020-09-092020-09-090000886163lgnd:XCellaBiosciencesIncMember2020-09-082020-09-080000886163lgnd:EarnoutRightsForPartnerResearchAndDevelopmentMemberlgnd:XCellaBiosciencesIncMember2020-09-080000886163lgnd:MilestonePaymentsMemberlgnd:XCellaBiosciencesIncMember2020-09-080000886163lgnd:MilestonePaymentsMemberlgnd:XCellaBiosciencesIncMember2020-09-082020-09-080000886163lgnd:XCellaBiosciencesIncMember2021-01-012021-12-310000886163lgnd:XCellaBiosciencesIncMember2020-09-080000886163us-gaap:TechnologyBasedIntangibleAssetsMemberlgnd:XCellaBiosciencesIncMember2020-09-082020-09-080000886163lgnd:IcagenMember2020-04-012020-04-010000886163lgnd:IcagenMemberus-gaap:MeasurementInputDiscountRateMember2020-04-010000886163lgnd:IcagenMember2021-01-012021-12-310000886163us-gaap:CustomerRelationshipsMemberlgnd:IcagenMember2020-04-010000886163us-gaap:TechnologyBasedIntangibleAssetsMemberlgnd:IcagenMember2020-04-010000886163us-gaap:CustomerRelationshipsMemberlgnd:IcagenMember2020-04-012020-04-010000886163us-gaap:TechnologyBasedIntangibleAssetsMemberlgnd:IcagenMember2020-04-012020-04-010000886163lgnd:AbInitioMember2019-07-232019-07-230000886163lgnd:AbInitioMember2021-01-012021-12-310000886163lgnd:AbInitioMember2019-07-230000886163us-gaap:TechnologyBasedIntangibleAssetsMemberlgnd:AbInitioMember2019-07-232019-07-230000886163us-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMember2021-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Memberus-gaap:ShortTermInvestmentsMember2021-12-310000886163us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMember2021-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Memberus-gaap:ShortTermInvestmentsMember2021-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberus-gaap:EquitySecuritiesMember2021-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberus-gaap:EquitySecuritiesMemberus-gaap:FairValueInputsLevel1Member2021-12-310000886163us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:EquitySecuritiesMember2021-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberus-gaap:EquitySecuritiesMemberus-gaap:FairValueInputsLevel3Member2021-12-310000886163us-gaap:FairValueMeasurementsRecurringMember2021-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2021-12-310000886163us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2021-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberlgnd:LiabilityForContingentValueRightsCompanyCydexMember2021-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberlgnd:LiabilityForContingentValueRightsCompanyCydexMemberus-gaap:FairValueInputsLevel1Member2021-12-310000886163us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberlgnd:LiabilityForContingentValueRightsCompanyCydexMember2021-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberlgnd:LiabilityForContingentValueRightsCompanyCydexMemberus-gaap:FairValueInputsLevel3Member2021-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberlgnd:LiabilityForContingentValueRightsCompanyMetabasisMember2021-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberlgnd:LiabilityForContingentValueRightsCompanyMetabasisMemberus-gaap:FairValueInputsLevel1Member2021-12-310000886163us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberlgnd:LiabilityForContingentValueRightsCompanyMetabasisMember2021-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberlgnd:LiabilityForContingentValueRightsCompanyMetabasisMemberus-gaap:FairValueInputsLevel3Member2021-12-310000886163lgnd:LiabilityForContingentValueRightsCompanyIcagenMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310000886163lgnd:LiabilityForContingentValueRightsCompanyIcagenMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2021-12-310000886163us-gaap:FairValueInputsLevel2Memberlgnd:LiabilityForContingentValueRightsCompanyIcagenMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310000886163lgnd:LiabilityForContingentValueRightsCompanyIcagenMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2021-12-310000886163lgnd:LiabilityForRestrictedInvestmentsOwedToFormerLicenseesMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310000886163lgnd:LiabilityForRestrictedInvestmentsOwedToFormerLicenseesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2021-12-310000886163us-gaap:FairValueInputsLevel2Memberlgnd:LiabilityForRestrictedInvestmentsOwedToFormerLicenseesMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310000886163lgnd:LiabilityForRestrictedInvestmentsOwedToFormerLicenseesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2021-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMember2020-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Memberus-gaap:ShortTermInvestmentsMember2020-12-310000886163us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ShortTermInvestmentsMember2020-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Memberus-gaap:ShortTermInvestmentsMember2020-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberus-gaap:EquitySecuritiesMember2020-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberus-gaap:EquitySecuritiesMemberus-gaap:FairValueInputsLevel1Member2020-12-310000886163us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:EquitySecuritiesMember2020-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberus-gaap:EquitySecuritiesMemberus-gaap:FairValueInputsLevel3Member2020-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberus-gaap:WarrantMember2020-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Memberus-gaap:WarrantMember2020-12-310000886163us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:WarrantMember2020-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Memberus-gaap:WarrantMember2020-12-310000886163us-gaap:FairValueMeasurementsRecurringMember2020-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2020-12-310000886163us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2020-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2020-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberlgnd:LiabilityForContingentValueRightsCompanyCrystalMember2020-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Memberlgnd:LiabilityForContingentValueRightsCompanyCrystalMember2020-12-310000886163us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberlgnd:LiabilityForContingentValueRightsCompanyCrystalMember2020-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Memberlgnd:LiabilityForContingentValueRightsCompanyCrystalMember2020-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberlgnd:LiabilityForContingentValueRightsCompanyCydexMember2020-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberlgnd:LiabilityForContingentValueRightsCompanyCydexMemberus-gaap:FairValueInputsLevel1Member2020-12-310000886163us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberlgnd:LiabilityForContingentValueRightsCompanyCydexMember2020-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberlgnd:LiabilityForContingentValueRightsCompanyCydexMemberus-gaap:FairValueInputsLevel3Member2020-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberlgnd:LiabilityForContingentValueRightsCompanyMetabasisMember2020-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberlgnd:LiabilityForContingentValueRightsCompanyMetabasisMemberus-gaap:FairValueInputsLevel1Member2020-12-310000886163us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberlgnd:LiabilityForContingentValueRightsCompanyMetabasisMember2020-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberlgnd:LiabilityForContingentValueRightsCompanyMetabasisMemberus-gaap:FairValueInputsLevel3Member2020-12-310000886163lgnd:LiabilityForContingentValueRightsCompanyIcagenMemberus-gaap:FairValueMeasurementsRecurringMember2020-12-310000886163lgnd:LiabilityForContingentValueRightsCompanyIcagenMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2020-12-310000886163us-gaap:FairValueInputsLevel2Memberlgnd:LiabilityForContingentValueRightsCompanyIcagenMemberus-gaap:FairValueMeasurementsRecurringMember2020-12-310000886163lgnd:LiabilityForContingentValueRightsCompanyIcagenMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2020-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberlgnd:LiabilityForContingentValueRightsCompanyPfenexMember2020-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberlgnd:LiabilityForContingentValueRightsCompanyPfenexMemberus-gaap:FairValueInputsLevel1Member2020-12-310000886163us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberlgnd:LiabilityForContingentValueRightsCompanyPfenexMember2020-12-310000886163us-gaap:FairValueMeasurementsRecurringMemberlgnd:LiabilityForContingentValueRightsCompanyPfenexMemberus-gaap:FairValueInputsLevel3Member2020-12-310000886163lgnd:LiabilityForRestrictedInvestmentsOwedToFormerLicenseesMemberus-gaap:FairValueMeasurementsRecurringMember2020-12-310000886163lgnd:LiabilityForRestrictedInvestmentsOwedToFormerLicenseesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2020-12-310000886163us-gaap:FairValueInputsLevel2Memberlgnd:LiabilityForRestrictedInvestmentsOwedToFormerLicenseesMemberus-gaap:FairValueMeasurementsRecurringMember2020-12-310000886163lgnd:LiabilityForRestrictedInvestmentsOwedToFormerLicenseesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2020-12-310000886163lgnd:LiabilityForContingentValueRightsCompanyCrystalMember2020-01-012020-12-31lgnd:agreement0000886163us-gaap:TransferredOverTimeMembersrt:MaximumMemberlgnd:DevelopmentRegulatoryCommercialMilestonesAndTieredRoyaltiesMember2021-12-310000886163us-gaap:TransferredOverTimeMemberlgnd:Phase3ClinicalTrialMember2021-12-310000886163lgnd:LiabilityForContingentValueRightsCompanyIcagenMember2021-01-012021-12-310000886163lgnd:LiabilityForContingentValueRightsCompanyPfenexMember2021-01-012021-12-310000886163us-gaap:FairValueInputsLevel3Member2020-12-310000886163us-gaap:FairValueInputsLevel3Member2021-01-012021-12-310000886163us-gaap:FairValueInputsLevel3Member2021-12-310000886163lgnd:MaterialSalesCaptisolMember2020-10-012020-10-310000886163srt:MaximumMember2021-12-310000886163us-gaap:BuildingMember2021-12-310000886163us-gaap:ConvertibleNotesPayableMemberlgnd:ConvertibleSeniorNotesDue2019Member2014-08-012014-08-310000886163us-gaap:ConvertibleNotesPayableMemberlgnd:ConvertibleSeniorNotesDue2019Memberus-gaap:DebtInstrumentRedemptionPeriodOneMember2014-08-012014-08-31lgnd:trading_day0000886163us-gaap:ConvertibleNotesPayableMemberlgnd:ConvertibleSeniorNotesDue2019Memberus-gaap:DebtInstrumentRedemptionPeriodTwoMember2014-08-012014-08-31lgnd:day0000886163us-gaap:ConvertibleNotesPayableMemberlgnd:ConvertibleSeniorNotesDue2019Member2018-05-222018-05-220000886163us-gaap:ConvertibleNotesPayableMemberlgnd:ConvertibleSeniorNotesDue2019Member2018-12-312018-12-310000886163us-gaap:ConvertibleNotesPayableMemberlgnd:ConvertibleSeniorNotesDue2019Member2018-01-012018-12-310000886163us-gaap:ConvertibleNotesPayableMemberlgnd:ConvertibleSeniorNotesDue2019Member2018-03-012018-04-300000886163us-gaap:ConvertibleNotesPayableMemberlgnd:ConvertibleSeniorNotesDue2019Member2018-07-012018-08-310000886163us-gaap:ConvertibleNotesPayableMemberlgnd:ConvertibleSeniorNotesDue2019Member2018-10-012018-11-300000886163us-gaap:ConvertibleNotesPayableMemberlgnd:ConvertibleSeniorNotesDue2019Member2019-01-012019-12-310000886163us-gaap:ConvertibleNotesPayableMemberlgnd:ConvertibleSeniorNotesDue2019Member2019-06-012019-06-300000886163us-gaap:ConvertibleNotesPayableMemberlgnd:ConvertibleSeniorNotesDue2019Member2019-08-152019-08-150000886163us-gaap:ConvertibleNotesPayableMemberlgnd:ConvertibleSeniorNotesDue2019Member2019-08-1500008861632014-08-310000886163us-gaap:ConvertibleNotesPayableMemberlgnd:ConvertibleSeniorNotesDue2019Memberus-gaap:OtherExpenseMember2019-01-012019-12-310000886163lgnd:ConvertibleSeniorNotesDue2023Memberus-gaap:ConvertibleNotesPayableMember2018-05-220000886163lgnd:ConvertibleSeniorNotesDue2023Memberus-gaap:ConvertibleNotesPayableMember2018-05-012018-05-310000886163lgnd:ConvertibleSeniorNotesDue2023Memberus-gaap:ConvertibleNotesPayableMemberus-gaap:DebtInstrumentRedemptionPeriodOneMember2018-05-012018-05-310000886163lgnd:ConvertibleSeniorNotesDue2023Memberus-gaap:ConvertibleNotesPayableMemberus-gaap:DebtInstrumentRedemptionPeriodTwoMember2018-05-012018-05-310000886163lgnd:ConvertibleSeniorNotesDue2023Memberus-gaap:ConvertibleNotesPayableMember2021-12-310000886163lgnd:ConvertibleSeniorNotesDue2023Memberus-gaap:ConvertibleNotesPayableMember2020-12-310000886163lgnd:ConvertibleSeniorNotesDue2023Memberus-gaap:ConvertibleNotesPayableMember2020-01-012020-12-310000886163lgnd:ConvertibleSeniorNotesDue2023Memberus-gaap:ConvertibleNotesPayableMember2021-01-012021-12-310000886163lgnd:ConvertibleSeniorNotesDue2023Memberus-gaap:SubsequentEventMemberus-gaap:ConvertibleNotesPayableMember2022-02-280000886163lgnd:ConvertibleSeniorNotesDue2023Memberus-gaap:SubsequentEventMemberus-gaap:ConvertibleNotesPayableMember2022-02-012022-02-280000886163lgnd:ConvertibleSeniorNotesDue2023Memberus-gaap:ConvertibleNotesPayableMember2018-05-222018-05-220000886163lgnd:ConvertibleSeniorNotesDue2023Memberus-gaap:ConvertibleNotesPayableMember2018-05-310000886163lgnd:ConvertibleSeniorNotesDue2023Memberus-gaap:ConvertibleNotesPayableMember2020-04-300000886163lgnd:ConvertibleSeniorNotesDue2023Memberus-gaap:ConvertibleNotesPayableMember2020-04-012020-04-300000886163lgnd:ConvertibleSeniorNotesDue2023Memberus-gaap:ConvertibleNotesPayableMember2021-01-310000886163lgnd:ConvertibleSeniorNotesDue2023Memberus-gaap:ConvertibleNotesPayableMember2021-01-012021-01-31lgnd:option0000886163us-gaap:MutualFundMember2021-12-310000886163us-gaap:DemandDepositsMember2021-12-310000886163us-gaap:CommercialPaperMember2021-12-310000886163us-gaap:CorporateDebtSecuritiesMember2021-12-310000886163us-gaap:EquitySecuritiesMember2021-12-310000886163us-gaap:USGovernmentDebtSecuritiesMember2021-12-310000886163us-gaap:WarrantMember2021-12-310000886163us-gaap:ShortTermInvestmentsMember2021-12-310000886163us-gaap:MutualFundMember2020-12-310000886163us-gaap:DemandDepositsMember2020-12-310000886163us-gaap:CommercialPaperMember2020-12-310000886163us-gaap:CorporateDebtSecuritiesMember2020-12-310000886163us-gaap:AgencySecuritiesMember2020-12-310000886163us-gaap:EquitySecuritiesMember2020-12-310000886163us-gaap:USTreasurySecuritiesMember2020-12-310000886163us-gaap:WarrantMember2020-12-310000886163us-gaap:ShortTermInvestmentsMember2020-12-310000886163us-gaap:DemandDepositsMember2021-12-310000886163us-gaap:CorporateDebtSecuritiesMember2021-12-310000886163us-gaap:CommercialPaperMember2021-12-310000886163us-gaap:USGovernmentDebtSecuritiesMember2021-12-310000886163us-gaap:DemandDepositsMember2020-12-310000886163us-gaap:CorporateDebtSecuritiesMember2020-12-310000886163us-gaap:CommercialPaperMember2020-12-31lgnd:position0000886163us-gaap:OfficeEquipmentMember2021-12-310000886163us-gaap:OfficeEquipmentMember2020-12-310000886163us-gaap:LeaseholdImprovementsMember2021-12-310000886163us-gaap:LeaseholdImprovementsMember2020-12-310000886163lgnd:ComputerEquipmentAndSoftwareMember2021-12-310000886163lgnd:ComputerEquipmentAndSoftwareMember2020-12-310000886163us-gaap:PatentedTechnologyMember2021-12-310000886163us-gaap:PatentedTechnologyMember2020-12-310000886163us-gaap:TradeNamesMember2021-12-310000886163us-gaap:TradeNamesMember2020-12-310000886163us-gaap:CustomerRelationshipsMember2021-12-310000886163us-gaap:CustomerRelationshipsMember2020-12-310000886163us-gaap:ContractualRightsMember2021-12-310000886163us-gaap:ContractualRightsMember2020-12-3100008861632010-01-310000886163lgnd:CydexPharmaceuticalsIncMember2019-12-310000886163lgnd:CydexPharmaceuticalsIncMember2020-01-012020-12-310000886163lgnd:CydexPharmaceuticalsIncMember2020-12-310000886163lgnd:CydexPharmaceuticalsIncMember2021-01-012021-12-310000886163lgnd:CydexPharmaceuticalsIncMember2021-12-310000886163lgnd:MetabasisTherapeuticsMember2019-12-310000886163lgnd:MetabasisTherapeuticsMember2020-01-012020-12-310000886163lgnd:MetabasisTherapeuticsMember2020-12-310000886163lgnd:MetabasisTherapeuticsMember2021-01-012021-12-310000886163lgnd:MetabasisTherapeuticsMember2021-12-310000886163lgnd:CrystalMember2019-12-310000886163lgnd:CrystalMember2020-01-012020-12-310000886163lgnd:CrystalMember2020-12-310000886163lgnd:CrystalMember2021-01-012021-12-310000886163lgnd:CrystalMember2021-12-310000886163lgnd:IcagenMember2019-12-310000886163lgnd:IcagenMember2020-01-012020-12-310000886163lgnd:IcagenMember2020-12-310000886163lgnd:IcagenMember2021-12-310000886163lgnd:PfenexMember2019-12-310000886163lgnd:PfenexMember2020-12-310000886163lgnd:PfenexMember2021-12-310000886163lgnd:XCellaBiosciencesIncMember2019-12-310000886163lgnd:XCellaBiosciencesIncMember2020-01-012020-12-310000886163lgnd:XCellaBiosciencesIncMember2020-12-310000886163lgnd:XCellaBiosciencesIncMember2021-12-310000886163us-gaap:ResearchAndDevelopmentExpenseMember2021-01-012021-12-310000886163us-gaap:ResearchAndDevelopmentExpenseMember2020-01-012020-12-310000886163us-gaap:ResearchAndDevelopmentExpenseMember2019-01-012019-12-310000886163us-gaap:GeneralAndAdministrativeExpenseMember2021-01-012021-12-310000886163us-gaap:GeneralAndAdministrativeExpenseMember2020-01-012020-12-310000886163us-gaap:GeneralAndAdministrativeExpenseMember2019-01-012019-12-310000886163lgnd:TwoThousandTwoStockIncentivePlanMember2020-12-012020-12-310000886163lgnd:TwoThousandTwoStockIncentivePlanMemberus-gaap:EmployeeStockOptionMember2021-12-3100008861632018-01-012018-12-310000886163lgnd:ExercisePriceRangeOneMember2021-01-012021-12-310000886163lgnd:ExercisePriceRangeOneMember2021-12-310000886163lgnd:ExercisePriceRangeTwoMember2021-01-012021-12-310000886163lgnd:ExercisePriceRangeTwoMember2021-12-310000886163lgnd:ExercisePriceRangeThreeMember2021-01-012021-12-310000886163lgnd:ExercisePriceRangeThreeMember2021-12-310000886163lgnd:ExercisePriceRangeFourMember2021-01-012021-12-310000886163lgnd:ExercisePriceRangeFourMember2021-12-310000886163lgnd:ExercisePriceRangeFiveMember2021-01-012021-12-310000886163lgnd:ExercisePriceRangeFiveMember2021-12-310000886163lgnd:ExercisePriceRangeSixMember2021-01-012021-12-310000886163lgnd:ExercisePriceRangeSixMember2021-12-310000886163lgnd:ExercisePriceRangeSevenMember2021-01-012021-12-310000886163lgnd:ExercisePriceRangeSevenMember2021-12-310000886163lgnd:ExercisePriceRangeEightMember2021-01-012021-12-310000886163lgnd:ExercisePriceRangeEightMember2021-12-310000886163lgnd:ExercisePriceRangeNineMember2021-01-012021-12-310000886163lgnd:ExercisePriceRangeNineMember2021-12-310000886163lgnd:ExercisePriceRangeTenMember2021-01-012021-12-310000886163lgnd:ExercisePriceRangeTenMember2021-12-310000886163lgnd:ExercisePriceRangeElevenMember2021-12-310000886163lgnd:ExercisePriceRangeElevenMember2021-01-012021-12-310000886163srt:MinimumMember2020-01-012020-12-310000886163srt:MaximumMember2020-01-012020-12-310000886163srt:MinimumMember2019-01-012019-12-310000886163srt:MaximumMember2019-01-012019-12-310000886163us-gaap:EmployeeStockOptionMember2021-12-310000886163us-gaap:RestrictedStockMember2018-12-310000886163us-gaap:RestrictedStockMember2019-12-310000886163us-gaap:RestrictedStockMember2020-12-310000886163us-gaap:RestrictedStockMember2021-12-310000886163lgnd:AmendedESPPMember2021-12-310000886163lgnd:AmendedESPPMember2021-01-012021-12-310000886163lgnd:AmendedESPPMember2020-01-012020-12-310000886163lgnd:AmendedESPPMember2019-01-012019-12-3100008861632019-09-1100008861632019-09-112019-09-1100008861632019-01-230000886163lgnd:LupinPatentInfringementMember2019-10-292019-10-29lgnd:patent0000886163lgnd:USDistrictCourtForTheNorthernDistrictOfOhioMember2019-10-312019-10-31lgnd:civil_complaint0000886163us-gaap:InternalRevenueServiceIRSMember2021-12-310000886163us-gaap:StateAndLocalJurisdictionMember2021-12-310000886163us-gaap:ResearchMember2021-12-310000886163us-gaap:StateAndLocalJurisdictionMemberlgnd:CaliforniaAndNewJerseyResearchTaxCreditCarryforwardMember2021-12-310000886163us-gaap:ForeignCountryMember2021-12-310000886163us-gaap:CapitalLossCarryforwardMemberus-gaap:ForeignCountryMember2021-12-310000886163us-gaap:ForeignCountryMember2020-12-310000886163us-gaap:CapitalLossCarryforwardMemberus-gaap:ForeignCountryMember2020-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_____________________________________________________________________________________________

FORM 10-K

_____________________________________________________________________________________________

| | | | | |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended December 31, 2021

OR | | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission File No. 001-33093

LIGAND PHARMACEUTICALS INCORPORATED

(Exact name of registrant as specified in its charter) | | | | | | | | |

| Delaware | | 77-0160744 |

(State or other jurisdiction of incorporation or organization) | | (IRS Employer Identification No.) |

| | |

5980 Horton Street, Suite 405 | | |

| Emeryville | | |

| CA | | 94608 |

| (Address of Principal Executive Offices) | | (Zip Code) |

Registrant’s telephone number, including area code: (858) 550-7500

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of Each Class | Trading Symbol | Name of Each Exchange on Which Registered |

| Common Stock, par value $.001 per share | LGND | The Nasdaq Global Market |

| | |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Securities Exchange Act of 1934. Yes ☐ No ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definition of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Large Accelerated Filer | ☒ | | Accelerated Filer | ☐ | Non-accelerated Filer | ☐ | Smaller reporting company | ☐ | Emerging growth company | ☐ |

| | | | | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Exchange Act Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the Registrant’s voting and non-voting stock held by non-affiliates was approximately $1.8 billion based on the last sales price of the Registrant’s Common Stock on the Nasdaq Global Market of the Nasdaq Stock Market LLC on June 30, 2021. For purposes of this calculation, shares of Common Stock held by directors, officers and 10% stockholders known to the Registrant have been deemed to be owned by affiliates which should not be construed to indicate that any such person possesses the power, direct or indirect, to direct or cause the direction of the management or policies of the Registrant or that such person is controlled by or under common control with the Registrant.

As of February 23, 2022, the Registrant had 16,852,650 shares of Common Stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for the Registrant’s 2021 Annual Meeting of Stockholders to be filed with the Commission within 120 days of December 31, 2021 are incorporated by reference in Part III of this Annual Report on Form 10-K. With the exception of those portions that are specifically incorporated by reference in this Annual Report on Form 10-K, such Proxy Statement shall not be deemed filed as part of this Report or incorporated by reference herein.

Table of Contents

| | | | | | | | |

| Part I | |

| Item 1. | | |

| Item 1A. | | |

| Item 1B. | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| |

| Part II | |

| Item 5. | | |

| Item 6. | | |

| Item 7. | | |

| Item 7A. | | |

| Item 8. | | |

| Item 9. | | |

| Item 9A. | | |

| Item 9B. | | |

| Item 9C. | | |

| |

| Part III | |

| Item 10. | | |

| Item 11. | | |

| Item 12. | | |

| Item 13. | | |

| Item 14. | | |

| |

| Part IV | |

| Item 15. | | |

| Item 16. | | |

| |

| | | | | |

| GLOSSARY OF TERMS AND ABBREVIATIONS |

| Abbreviation | Definition |

| 2019 Notes | $245.0 million aggregate principal amount of convertible senior unsecured notes due 2019 |

| 2023 Notes | $750.0 million aggregate principal amount of convertible senior unsecured notes due 2023 |

| Ab Initio | Ab Initio Biotherapeutics, Inc. |

| Abvivo | Abvivo, LLC |

| Aldeyra | Aldeyra Therapeutics, Inc. |

| Amgen | Amgen, Inc. |

| ANDA | Abbreviated New Drug Application |

| API | Active pharmaceutical ingredient |

| Aptevo | Aptevo Therapeutics |

| Arcus | Arcus Biosciences, Inc. |

| ASC | Accounting Standards Codification |

| ASCO | American Society of Clinical Oncology |

| ASCT | Autologous Stem Cell Transplantation |

| ASU | Accounting Standards Update |

| Aurobindo | Aurobindo Pharma Ltd |

| Aziyo | Aziyo Med, LLC |

| Baxter | Baxter International, Inc. |

| BendaRx | BendaRx Corp. |

| Bexson Biomedical | Bexson Biomedical, Inc. |

| BLA | Biologics license application |

| CStone | CStone Pharmaceuticals (Suzhou) Co., Ltd. |

| CASI | CASI Pharmaceuticals, Inc. |

| CI-AKI | Contrast-induced acute kidney injury |

| Code of Conduct | Code of Conduct and Ethics Policy |

| CoM | Composition of Matter |

| Company | Ligand Pharmaceuticals Incorporated, including subsidiaries |

| Convertible Note | Senior Convertible Promissory Note |

| COPD | Chronic obstructive pulmonary disease |

| Cormatrix | Cormatrix Cardiovascular, Inc. |

| Corvus | Corvus Pharmaceuticals, Inc. |

| COSO | Committee of Sponsoring Organizations of the Treadway Commission |

| CRO | Contract Research Organization |

| Crystal | Crystal Bioscience, Inc. |

| Cumulus | Cumulus Oncology, Ltd. |

| CVR | Contingent value right |

| CyDex | CyDex Pharmaceuticals, Inc. |

| Daiichi Sankyo | Daiichi Sankyo Company, Ltd. |

| Dianomi | Dianomi Therapeutics, Inc. |

| DMF | Drug Master File |

| ESG | Environmental, Social and Governance |

| Eisai | Eisai Inc. |

| Eli Lilly | Eli Lilly and Company |

| ECM | Extracellular matrix |

| EPA | Environmental Protection Agency |

| ESPP | Employee Stock Purchase Plan, as amended and restated |

| | | | | |

| EU | European Union |

| Exelixis | Exelixis, Inc. |

| FASB | Financial Accounting Standards Board |

| FDA | U.S. Food and Drug Administration |

| FSGS | Focal segmental glomerulosclerosis |

| GAAP | Generally accepted accounting principles in the United States |

| Genagon | Genagon Therapeutics AB |

| GCSF | Granulocyte-colony stimulating factor |

| GigaGen | GigaGen, Inc. |

| Gilead | Gilead Sciences, Inc. |

| GPCR | G-protein coupled receptor |

| GRA | Glucagon receptor antagonist |

| HanAll | HanAll Biopharma Co., Ltd. |

| Harbour | Harbour BioMed Shanghai Co., Ltd. |

| HBV | Hepatitis B Virus |

| Hikma | Hikma Pharmaceuticals PLC |

| Hovione | Hovione FarmCiencia, S.A. |

| Icagen | Icagen, Inc. |

| IPR&D | In-Process Research and Development |

| IRS | Internal Revenue Service |

| IV | Intravenous |

| Immunovant | Immunovant Sciences GmbH |

| IND | Investigational New Drug |

| Jazz | Jazz Pharmaceuticals, Inc. |

| Ligand | Ligand Pharmaceuticals Incorporated, including subsidiaries |

| LTP | Liver targeting prodrug |

| Lundbeck | Lundbeck A/S |

| Marinus | Marinus Pharmaceuticals, Inc. |

| Melinta | Melinta Therapeutics, Inc. |

| Merck | Merck & Co., Inc. |

| Metabasis | Metabasis Therapeutics, Inc. |

| Millennium | Millennium Pharmaceuticals, Inc. |

| NASH | Non-alcoholic steatohepatitis |

| NDA | New Drug Application |

| NOLs | Net Operating Losses |

| Novan | Novan, Inc. |

| Novartis | Novartis AG |

| Nucorion | Nucorion Pharmaceuticals, Inc. |

| OMT | Open Monoclonal Technology, Inc. |

| Ono | Ono Pharmaceutical Co., Ltd. |

| Opthea | Opthea Limited |

| Orange Book | Publication identifying drug products approved by the FDA based on safety and effectiveness |

| Original Interest Purchase Agreement | Interest Purchase Agreement, dated May 3, 2016, between the Company and CorMatrix Cardiovascular, Inc. |

| Palvella | Palvella Therapeutics, Inc. |

| Par | Par Pharmaceutical, Inc. |

| Pfenex | Pfenex Inc. |

| | | | | |

| Pfizer | Pfizer, Inc. |

| PFS | Progression-free Survival |

| Pharmacopeia | Pharmacopeia, Inc. |

| Phoenix Tissue | Phoenix Tissue Repair |

| PPD | Post-Partum Depression |

| PSU | Performance stock unit |

| R&D | Research and Development |

| Roivant | Roivant Sciences GMBH |

| RSU | Restricted stock unit |

| SAGE | Sage Therapeutics, Inc. |

| SARM | Selective Androgen Receptor Modulator |

| SEC | Securities and Exchange Commission |

| Sedor | Sedor Pharmaceuticals, Inc., or RODES, Inc. |

| Seelos | Seelos Therapeutics, Inc. |

| Selexis | Selexis, SA |

| Sermonix | Sermonix Pharmaceuticals, LLC |

| SII | Serum Institute of India |

| SQ Innovation | SQ Innovation, Inc. |

| Sunshine Lake Pharma | Sunshine Lake Pharma Co., Ltd. |

| Takeda | Takeda Pharmaceuticals Company Limited |

| Talem | Talem Therapeutics LLC |

| Taurus | Taurus Biosciences LLC |

| Tax Act | The Tax Cuts and Jobs Act |

| Teva | Teva Pharmaceuticals USA, Inc., Teva Pharmaceutical Industries Ltd. and Actavis, LLC |

| Travere | Travere Inc. |

| TR-Beta | Thyroid hormone receptor beta |

| Valanbio | Valanbio Therapeutics, Inc. |

| VDP | Vernalis Design Platform |

| VentiRx | VentiRx Pharmaceuticals, Inc. |

| Vernalis | Vernalis plc |

| Verona | Verona Pharma plc |

| Viking | Viking Therapeutics |

| WuXi | WuXi Biologics Ireland Limited |

| WuXi Agreement | The Platform License Agreement, dated March 23, 2015, by and between Ligand and WuXi, as amended |

| Xi'an Xintong | Xi'an Xintong Medicine Research |

| X-ALD | X-linked adrenoleukodystrophy |

| xCella Biosciences | xCella Biosciences, Inc. |

| Zydus Cadila | Zydus Cadila Healthcare, Ltd |

PART I

Cautionary Note Regarding Forward-Looking Statements:

You should read the following report together with the more detailed information regarding our company, our common stock and our financial statements and notes to those statements appearing elsewhere in this document.

This report contains forward-looking statements that involve a number of risks and uncertainties. Although our forward-looking statements reflect the good faith judgment of our management, these statements can only be based on facts and factors currently known by us. Consequently, these forward-looking statements are inherently subject to risks and uncertainties, and actual results and outcomes may differ materially from results and outcomes discussed in the forward-looking statements.

Forward-looking statements can be identified by the use of forward-looking words such as “believes,” “expects,” “may,” “will,” “plan,” “intends,” “estimates,” “would,” “continue,” “seeks,” “pro forma,” or “anticipates,” or other similar words (including their use in the negative), or by discussions of future matters such as those related to our future results of operations and financial position, royalties and milestones under license agreements, Captisol material sales, product development, and product regulatory filings and approvals, and the timing thereof, as well as other statements that are not historical. You should be aware that the occurrence of any of the events discussed under the caption “Risk Factors” could negatively affect our results of operations and financial condition and the trading price of our stock.

The cautionary statements made in this report are intended to be applicable to all related forward-looking statements wherever they may appear in this report. We urge you not to place undue reliance on these forward-looking statements, which speak only as of the date of this report. Except as required by law, we assume no obligation to update our forward-looking statements, even if new information becomes available in the future. This caution is made under the safe harbor provisions of Section 21E of the Securities Exchange Act of 1934, as amended.

References to “Ligand Pharmaceuticals Incorporated,” “Ligand,” the “Company,” “we,” “our” and “us” include Ligand Pharmaceuticals Incorporated and our wholly-owned subsidiaries.

Partner Information

Information regarding partnered products and programs comes from information publicly released by our partners and licensees.

Trademarks

Our trademarks, trade names and service marks referenced herein include Ligand®, 3 Species, 1 License®, Absolutely Omniab™, Advasep®, Animal Intelligence™, BEPro™, Biological Intelligence™, Bonsity®, Captisol®, CyDex®, Icagen®, LTP®, LTP Technology™, Naturally Optimized Human Antibodies®, OmniAb®, OmniChicken®, OmniClic®, OmniDab™, OmniDeep®, OmniFlic®, OmniMouse®, OmniRat®, OmniTaur™, Pelican Expression Technology™, PeliCRM™, Pfenex Expression Technology™, Picobodies™, Three Species, One License®, xCella Biosciences®, XPloration® and XRPro®, which are protected under applicable intellectual property laws and are our property. All other trademarks, trade names and service marks including Kyprolis®, Evomela®, Veklury®, Livogiva®, Zulresso®, Rylaze™, VAXNEUVANCE™, Pneumosil®, Minnebro®, Baxdela®, Carnexiv™, Conbriza®, Nexterone®, Noxafil® and Duavee®, are the property of their respective owners. Solely for convenience, trademarks, trade names and service marks referred to in this report may appear without the ®, ™ or SM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the right of the applicable licensor to such trademarks, trade names and service marks. Use or display by us of other parties’ trademarks, trade dress or products is not intended to and does not imply a relationship with, or endorsement or sponsorship of, us by the trademark or trade dress owners.

Overview

We are a biopharmaceutical company focused on developing or acquiring technologies that help pharmaceutical companies discover and develop medicines. We employ research technologies such as antibody discovery technologies, ion channel discovery technology, Pseudomonas fluorescens protein expression technology, formulation science and liver targeted pro-drug technologies to assist companies in their work toward securing prescription drug and biologic approvals. We currently have partnerships and license agreements with over 140 pharmaceutical and biotechnology companies. Over 400 programs are in various stages of commercialization, development or research and are fully funded by our collaboration partners and licensees. We have contributed novel research and technologies for approved medicines that treat cancer, osteoporosis, fungal infections and postpartum depression, among others. Our collaboration partners and licensees have programs currently in clinical development targeting cancer, seizure, diabetes, cardiovascular disease, muscle wasting, liver disease, and kidney disease, among others. We have over 1,600 issued patents worldwide.

We have assembled our large portfolio of fully-funded programs either by licensing our own proprietary drug development programs, licensing our platform technologies such as Captisol or OmniAb to partners for use with their proprietary programs, or acquiring existing partnered programs from other companies. Fully-funded programs, which we refer to as “shots on goal,” are those for which our partners pay all of the development and commercialization costs. For our internal programs, we generally plan to advance drug candidates through early-stage drug development or clinical proof-of-concept and then seek partners to continue development and potential commercialization.

Our business model creates value for stockholders by providing a diversified portfolio of biotech and pharmaceutical product revenue streams that are supported by an efficient and low corporate cost structure. Our goal is to offer investors an opportunity to participate in the promise of the biotech industry in a profitable, diversified and lower-risk business, in contrast to a typical biotech company. Our business model is based on doing what we do best: drug discovery, early-stage drug development, product reformulation and partnering. We partner with other pharmaceutical companies to leverage what they do best (late-stage development, regulatory management and commercialization) to ultimately generate our revenue. We believe that focusing on discovery and early-stage drug development while benefiting from our partners’ development and commercialization expertise will reduce our internal expenses and allow us to have a larger number of drug candidates progress to later stages of drug development.

Our revenue consists of three primary elements: royalties from commercialized products, sales of Captisol material, and contract revenue from license, milestone and other service payments. In addition to discovering and developing our own proprietary drugs, we selectively pursue acquisitions to bring in new assets, pipelines, and technologies to aid in generating additional potential new revenue streams.

Impact of COVID-19 Pandemic

Please see impact of COVID-19 pandemic described in Item 8. Consolidated Financial Statements -Note 1, “Basis of Presentation and Summary of Significant Accounting Policies”. For additional information on the various risks posed by COVID-19 pandemic, please read Item 1A. Risk Factors included in this report.

Technologies

A variety of technology platforms that enable elements of drug discovery or development form the basis of our portfolio of fully-funded shots on goal. Platform technologies or individual drugs discovered by Ligand are related to a broad estate of intellectual property that includes over 1,600 patents issued worldwide.

OmniAb Technologies

The OmniAb platform creates and screens diverse antibody pools and is designed to quickly identify optimal antibodies for our partners’ drug development efforts. We harness the power of Biological Intelligence, which we built into our proprietary transgenic animals and paired with our high-throughput screening technologies, to enable the discovery of high-quality, fully-human antibody therapeutic candidates. We believe these antibodies are high quality because they are naturally optimized in our proprietary host systems for affinity, specificity, developability and functional performance. Our partners have access to these antibody therapeutic candidates that are based on unmatched biological diversity and optimized through integration across a full range of technologies, including antigen design, transgenic animals, deep screening and characterization. We provide our partners both integrated end-to-end capabilities and highly customizable offerings, which address critical industry challenges and provide optimized antibody discovery solutions.

As of December 31, 2021, OmniAb had 57 partners and over 250 active discovery programs, including 25 OmniAb-derived antibodies in clinical development and two approved products, including zimberelimab, which was approved in China for the treatment of recurrent or refractory classical Hodgkin’s lymphoma, and sugemalimab, which was approved in China for the first-line treatment of metastatic (stage IV) nonsmall cell lung cancer in combination with chemotherapy.

Pelican Expression Technology™ Platform

The Pelican Expression Technology platform is a robust, validated, cost-effective and scalable platform for recombinant protein production, and is especially well-suited for complex, large-scale protein production. Global manufacturers have demonstrated consistent success with the platform and the technology is currently out-licensed for multiple commercial and development-stage programs. The versatility of the platform has been demonstrated in the production of enzymes, peptides, antibody derivatives and engineered non-natural proteins. Partners seek the platform as it contributes significant value to biopharmaceutical development programs by reducing timelines and costs associated with research and development through commercial manufacturing of therapeutics and vaccines. Given pharmaceutical industry trends toward large molecules with increased structural complexities, the Pelican Expression Technology platform is well positioned to meet these growing needs as the most comprehensive and broadly available, commercially validated protein production platform in the industry.

We acquired the Pelican Expression Technology through our acquisition of Pfenex in October 2020. As of December 31, 2021, we have agreements with more than 20 partners using this technology in more than 30 active programs. Several of our partners have commercial products and late stage clinical product candidates utilizing Pelican Expression Technology.

Captisol Technology

Captisol is a patent-protected, chemically modified cyclodextrin with a structure designed to optimize the solubility and stability of drugs. Captisol was invented and initially developed by scientists in the laboratories of Dr. Valentino Stella, University Distinguished Professor at the University of Kansas’ Higuchi Biosciences Center for specific use in drug development and formulation. This unique technology has enabled several FDA-approved products, including Gilead’s Veklury®, Amgen’s Kyprolis®, Baxter International’s Nexterone®, Acrotech Biopharma L.L.C.’s and CASI Pharmaceuticals’ Evomela®, Melinta Therapeutics’ Baxdela® and Sage Therapeutics’ Zulresso® There are many Captisol-enabled products currently in various stages of development. We maintain a broad global patent portfolio for Captisol with approximately 440 issued patents worldwide relating to the technology (including 45 in the U.S.) and with the latest expiration date in 2035. Other patent applications covering methods of making Captisol, if issued, extend to 2041.

In addition to solid Captisol powder, we offer our partners access to cGMP manufactured aqueous Captisol concentrate. This product offering was established in 2017 to reduce cycle time and increase Captisol production capacity for large volume drug products. We maintain both Type IV and Type V DMFs with the FDA. These DMFs contain manufacturing and safety information relating to Captisol that our licensees can reference when developing Captisol-enabled drugs. We also have active DMFs in Japan, China and Canada. As of December 31, 2021, Captisol-enabled drugs were being marketed in more than 70 countries, and over 50 partners had Captisol-enabled drugs in development.

HepDirect, LTP, and BEPro Technology Platform

The HepDirect and LTP platforms are our proprietary liver-targeting prodrug technologies that can deliver many different chemical classes of drugs to the liver by using a chemical modification that renders an API biologically inactive until cleaved by a liver-specific enzyme. These technologies may improve the efficacy and/or safety of certain drugs and can be applied to marketed or new drug products to treat liver diseases or diseases caused by hemostasis imbalance of circulating molecules controlled by the liver. As of December 31, 2021, we had active HepDirect/LTP programs with three partners using these technologies across five programs.

The BEPro technology platform is a next generation prodrug technology distinct from HepDirect and LTP prodrug technologies, expanding use to non-liver related diseases. BEPro is specifically applicable to nucleotides and nucleotide analogs for the development of compounds with improved product profiles. Ligand has demonstrated improvements in cell penetration and oral, intravenous and inhaled pharmacokinetics with BEPro-enabled nucleotide analogs. As of December 31, 2021, we have one partner using this technology.

SUREtechnology Platform (owned by Selexis)

We acquired economic rights to various SUREtechnology Platform programs from Selexis. The SUREtechnology Platform, developed and owned by Selexis, is a novel technology that improves the way that cells are utilized in the development and manufacturing of recombinant proteins and drugs. As of December 31, 2021, we are entitled to certain economic rights to SUREtechnology Platform license agreements with 11 partners developing or having commercialized 17 programs.

2021 and Recent Major Business Highlights

The Separation and Distribution of OmniAb Business

In November 2021, we announced plans to explore multiple paths for OmniAb to become a stand-alone public company, with the leading option under consideration at that time being an IPO and eventual distribution of OmniAb shares to Ligand shareholders. We now expect to pursue separation of OmniAb through a direct spin-off of 100% of OmniAb equity to shareholders with Ligand capitalizing the OmniAb business directly with $70 million. OmniAb expects to file a Form 10 with the Securities and Exchange Commission and complete its separation in the first half of 2022. The distribution is expected to qualify as a tax-free transaction for U.S. federal income tax purposes to both Ligand and its shareholders. The separation remains subject to final approval by Ligand’s Board of Directors, and Ligand will continue to evaluate other options to optimize value and ensure flexibility to invest in growth. There can be no assurance that this process will result in Ligand pursuing a particular transaction or consummating any such transaction, or that the anticipated benefits of a separation will materialize should the separation be completed.

OmniAb Technology Platform and Partner Updates

CStone Pharmaceuticals received approval from China’s NMPA for Celjemy® (sugemalimab), an OmniAb-derived anti-PD-L1 monoclonal antibody for the first-line treatment of advanced non-small cell lung cancer (NSCLC) in combination with chemotherapy. Sugemalimab is the second OmniAb-derived antibody to receive regulatory approval. CStone announced complete enrollment in two Phase 3 registrational clinical trials investigating sugemalimab in combination with chemotherapy for the first-line treatment of metastatic gastric adenocarcinoma/gastro-esophageal junction adenocarcinoma or esophageal squamous cell carcinoma. CStone and its partner EQRx announced the publication of positive results from two Phase 3 trials with sugemalimab in Stage III and Stage IV NSCLC in The Lancet Oncology. CStone also announced that its Phase 2 GEMSTONE-201 trial met the primary endpoint of objective response rate in patients with relapsed/refractory (R/R) extranodal natural killer/T-cell lymphoma.

Janssen submitted a BLA to the U.S. FDA in December 2021 seeking approval for teclistamab in R/R multiple myeloma. Teclistamab is an OmniAb-derived bispecific antibody targeting BCMA and CD3. Janssen also presented new data at the American Society of Hematology 2021 conference (ASH) from the MajesTEC-1 study, which showed continued deep and durable response in heavily pretreated patients with multiple myeloma. Janssen previously announced that teclistamab had received U.S. FDA Breakthrough Designation for treatment of R/R multiple myeloma.

Immunovant announced alignment with the FDA on the design of a Phase 3 trial for batoclimab in patients with myasthenia gravis. Immunovant plans to start the Phase 3 study in the first half of 2022, and also expects to initiate pivotal trials in two additional indications during 2022.

Ligand expanded an existing collaboration and license agreement with GlaxoSmithKline (GSK) to leverage Ligand’s Icagen Ion Channel Technology to target neurological diseases. Ligand received an upfront payment of $10 million and is eligible for milestones of up to $247.5 million, and tiered royalties on net sales of any drug from the collaboration commercialized by GSK.

Pelican Platform Updates

Merck announced European Commission approval of VAXNEUVANCE™ for adults 18 years of age and older. VAXNEUVANCE is a 15-valent pneumococcal vaccine utilizing CRM197 vaccine carrier protein produced using the Pelican Expression Technology platform. Additionally, Merck announced the U.S. FDA accepted for priority review the supplemental Biologics License Application (sBLA) for VAXNEUVANCE in infants and children.

Jazz Pharmaceuticals announced submission of an sBLA to the FDA seeking approval for a Monday/Wednesday/Friday (M/W/F) intramuscular dosing schedule for Rylaze™, as a component of a multi-agent chemotherapeutic regimen for the treatment of acute lymphoblastic leukemia (ALL) and lymphoblastic lymphoma (LBL) in adult and pediatric patients one month and older who have developed hypersensitivity to E. coli-derived asparaginase. Jazz presented initial results at ASH from a Phase 2/3 study of Ryalze in adult and pediatric ALL and LBL patients showing Rylaze maintained clinically meaningful level of asparaginase activity throughout the entire duration of treatment on a M/W/F dosing schedule.

Arcellx recently announced the pricing of a $123.8 million initial public offering with proceeds planned to be used to advance their pipeline. Arcellx uses the Pelican Expression Technology platform for the expression of certain proprietary sparX proteins which are used in Arcellx's ARC-SparX platform.

Captisol Technology Updates

Amgen announced U.S. FDA approval of a new Kyprolis® combination regimen with DARZALEX FASPRO and dexamethasone for patients with multiple myeloma at first or subsequent relapse. Additionally, Amgen presented results from a

Phase 1b study at ASH showing Captisol-enabled Kyprolis in combination with vincristine, dexamethasone, PEG-asparaginase, daunorubicin (VXLD) induction therapy showed positive efficacy results in highly advanced relapsed/refractory pediatric ALL.

Gilead announced the U.S. FDA granted accelerated approval of a supplemental NDA for Veklury in non-hospitalized patients at high risk of disease progression.

Other Business Updates

Travere Therapeutics provided an update on their plans for regulatory submission of sparsentan. Travere plans to submit a NDA to the FDA seeking accelerated approval of sparsentan for IgA nephropathy in the first quarter of 2022 and for FSGS in mid-2022. Travere, in collaboration with its partner Vifor Pharma, plans to submit a combined IgA nephropathy and FSGS Marketing Authorization Application in mid-2022 seeking conditional marketing authorization in Europe.

Verona Pharma announced completion of enrollment in the Phase 3 ENHANCE-1 and ENHANCE-2 randomized trials evaluating ensifentrine for the maintenance treatment of COPD with top-line data expected by the end of 2022 and in the third quarter of 2022, respectively. Verona also reported ensifentrine met all safety objectives in a thorough QT study designed to evaluate effects, if any, of ensifentrine on cardiac conduction in healthy individuals. The results from these studies will support the planned NDA submission of ensifentrine for the maintenance treatment of COPD.

Sermonix Pharmaceuticals closed a $40 million financing with proceeds planned to advance lasofoxifene through late-stage clinical development as an oral SERM to treat women with ESR1 breast cancer mutations. Topline data are expected in the first half of 2022 for the Phase 2 ELAINE 1 trial assessing oral lasofoxifene versus intramuscular fulvestrant and the Phase 2 ELAINE 2 trial of oral lasofoxifene in combination with Eli Lilly and Company's CDK4 and 6 inhibitor Verzenio® (abemaciclib) for the treatment of ER+/HER2- breast cancer in patients with an ESR1 mutation.

Corporate and Governance Highlights

We are committed to policies and practices focused on environmental sustainability, positively impacting our social community and maintaining and cultivating good corporate governance. By focusing on such ESG policies and practices, we believe we can affect a meaningful and positive change in our community and maintain our open, collaborative corporate culture. We will continue our proactive shareholder and employee engagement in 2022. See www.ligand.com for information about our ESG policies and practices.

Partners and Licensees

We currently have partnerships and license agreements with over 140 pharmaceutical and biotechnology companies. Below is a list of our disclosed partners.

| | | | | | | | | | | | | | | | | | | | | | | |

| Big Pharma | Ticker | | Biotech | Ticker | | Biotech, continued | Ticker |

| Abbott | ABT | | ABBA | Private | | Melinta | Private |

| AstraZeneca | AZN | | Abvivo | Private | | Menarini | Private |

| Baxter | BAX | | Adept | Private | | Nanjing King-Friend | 603707 |

| Boehringer Ingelheim | Private | | Aldeyra | ALDX | | Neuritek | Private |

| Eisai | 4523 | | ALX Oncology | ALXO | | Novan | NOVN |

| GSK | GSK | | Amgen | AMGN | | Nucorion | Private |

| Janssen | JNJ | | Anebulo | Private | | Ohara | Private |

| Jazz | JAZZ | | Aptevo | APVO | | Oncternal | ONCT |

| Merck | MRK | | Arcellx | ACLX | | OnKure | Private |

| Merck KGaA | MRK.DE | | Arcus | RCUS | | Opthea | OPT |

| Novartis | NVS | | Asahi Kasei | 3407 | | Outlook | OTLK |

| Ono | 4528 | | Ascella | Private | | Palvella | Private |

| Pfizer | PFE | | BendaRx | Private | | Pandion | MRK |

| Roche | RHHBY | | Bexson Biomedical | Private | | Phoenix Tissue | Private |

| Sanofi | SNY | | Biocity | Private | | Pierre-Fabre | Private |

| Takeda | 4502 | | Cantex | Private | | Praxis | PRAX |

| | | Corvus | CRVS | | Precision Biologics | Private |

| | | CStone | 2616.HK | | Revision | Private |

| | | | | | | | | | | | | | | | | | | | | | | |

| Specialty Pharma | Ticker | | CSL | Private | | RubrYc | Private |

| Acrotech (Aurobindo) | AUROPHARMA | | CR Double-Crane | Private | | Sage | SAGE |

| Genovac | Private | | Cumulus | Private | | Salubris Bio | Private |

| Aytu Bioscience | AYTU | | Curon | Private | | Seagen | SGEN |

| Aziyo | AZYO | | Daxor | DXR | | Seelos | SEEL |

| Beloteca | Private | | Denovo | Private | | Sepsia | Private |

| BF Bioscience | Private | | Electra | Private | | Servier | Private |

| CASI | CASI | | Elevation | Private | | Serum Inst. of India | Private |

| CorMatrix | Private | | Exelixis | EXEL | | Softkemo | Private |

| EQRx | EQRX | | Foghorn | FHTX | | Sunshine Lake | Private |

| Ferring | Private | | Genmab | GMAB | | Talem | Private |

| Gloria | 2437 | | Genagon | Private | | Tizona | Private |

| Goodness Growth | VRNOF | | Genentech (Roche) | RHHBY | | Travere | TVTX |

| Lundbeck | LUN | | Genovac | Private | | Tremeau | Private |

| Sedor | Private | | GigaGen | Private | | Unity | UBX |

| Sermonix | Private | | Gilead Sciences | GILD | | Valanbio | Private |

| Shionogi | SGIOY | | Gordian | Private | | Vaxxas | Private |

| SQ Innovation | Private | | Halo | Private | | Vega | Private |

| | | HanAll | 9420 | | VenBio | Private |

| Generics | Ticker | | Harbour | 2142 | | VentiRx | Private |

| Alvogen | Private | | IBC Generium | Private | | Verona | VRNA |

| Adalvo | Private | | Ichnos | Private | | Viking | VKTX |

| Apotex | Private | | iMetabolic | Private | | Xi'an Xintong | Private |

| BioCad | Private | | Immunovant | IMVT | | WuXi | 2269 |

| Gufic | GUFICBIO | | Innolake Biopharm | Private | | Zhilkang Hongyi | Private |

| Hetero | Private | | Interventional Analgesix | Private | | | |

| Hikma | HIK | | J-Pharma | Private | | | |

| Indofarma | INAF | | Jupiter | Private | | | |

| Jubilant | Private | | Kangchen | Private | | | |

| Mylan | VTRS | | Kira | Private | | | |

| Par | Private | | Marinus | MRNS | | | |

| Zydus Cadila | CADILAHC | | MEI | MEIP | | | |

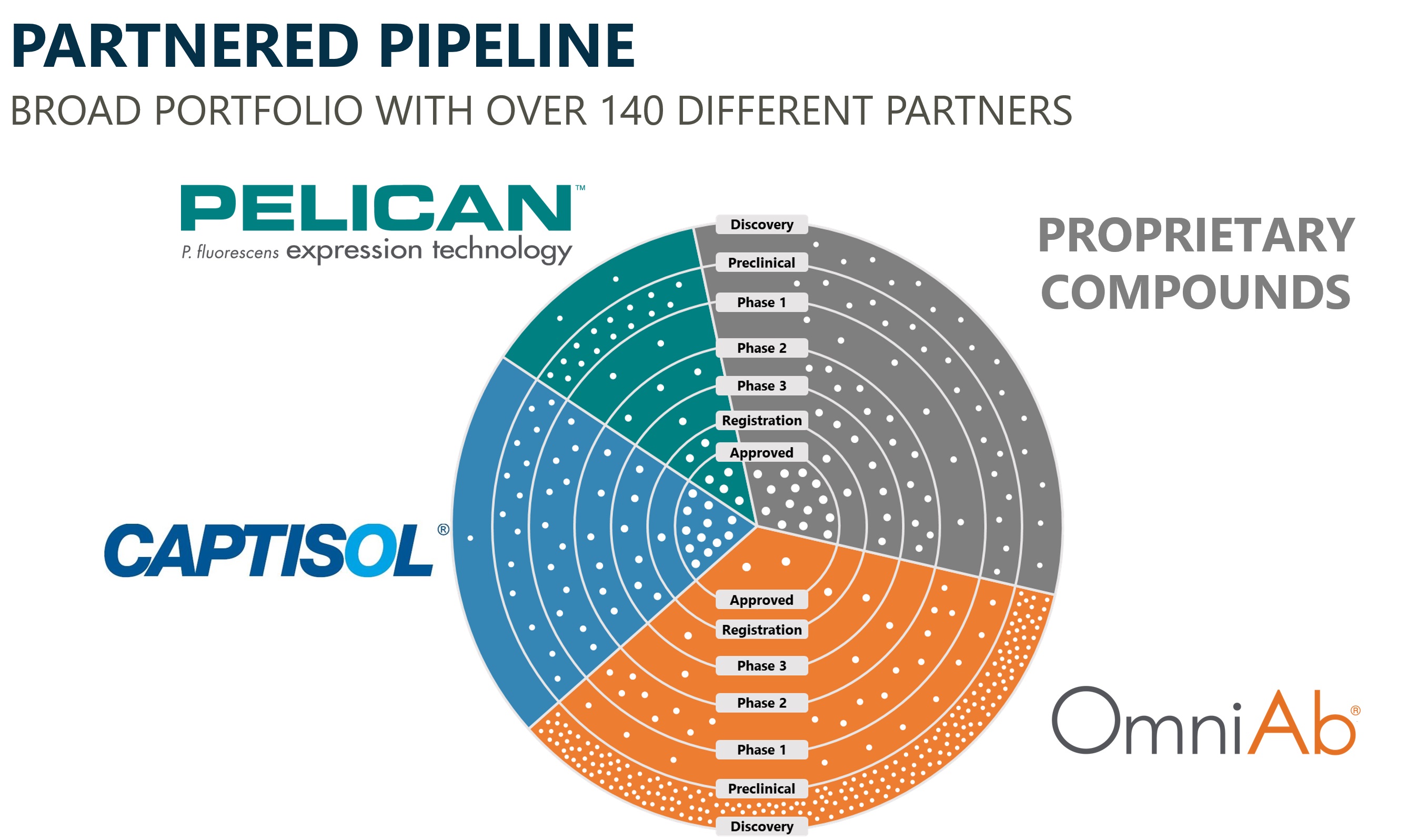

Commercial and Clinical Stage Partnered Portfolio

We have a large portfolio of current and future potential revenue-generating programs, including over 400 fully-funded by our partners. Each white dot on our partnered pipeline chart below represents a fully-funded partnered program, with each section of the chart representing a major Ligand technology or platform.

| | | | | | | | |

| Approved |

| Partner Name | Program | Therapeutic Area |

| | |

| Acrotech/CASI | Evomela | Cancer |

| Alvogen/Adalvo | Teriparatide | Women's Health |

| Alvogen/Hikma/Nanjing King-Friend | Voriconazole | Infectious Disease |

| Amgen/Beigene/Ono | Kyprolis | Cancer |

| Aytu | Tuzistra | Infectious Disease |

| Aziyo | ECM portfolio | Medical device/Cardiology |

| Baxter | Nexterone | Cardiovascular |

| BendaRx | Bendamustine | Cancer |

| BF Bio/Gufic/Hetero/Indofarma/Jubilant/Zydus | Generic Remdesivir | Infectious Disease |

| Biocad | Teberif | Inflammatory/Metabolic |

| C-Stone/Pfizer | Sugemalimab | Cancer |

| Exelixis/Daiichi-Sankyo | Minnebro | Cardiovascular |

| Gilead | Veklury | Infectious Disease |

| Gloria/EQRx | Zimberelimab | Cancer |

| IBC Generium | GNR-008 | Severe and Rare |

| | | | | | | | |

| Jazz | Rylaze | Cancer |

| Lundbeck | Carnexiv | Central Nervous System |

| Melinta | Baxdela | Infectious Disease |

| Menarini | Frovatriptan | Central Nervous System |

| Merck | Noxafil-IV | Infectious Disease |

| Merck | Vaxneuvance | Infectious Disease |

| Par | Posaconazole | Infectious Disease |

| Pfizer | Viviant/Conbriza | Inflammatory/Metabolic |

| Pfizer | Duavee | Inflammatory/Metabolic |

| Pfizer | Vfend-IV | Infectious Disease |

| SAGE | Zulresso | Central Nervous System |

| Sedor | Sesquient | Central Nervous System |

| Serum Institute of India | Pneumosil | Infectious Disease |

| Zydus Cadila | Vivitra | Cancer |

| Zydus Cadila | Bryxta/ZyBev | Cancer |

| Zydus Cadila | Maropitant | Central Nervous System |

| Zydus Cadila | Exemptia | Inflammatory/Metabolic |

| Zydus Cadila | Vortuxi | Inflammatory/Metabolic |

| | |

| | |

| Phase 3/Pivotal or Regulatory Submission Stage |

| Partner Name | Program | Therapeutic Area |

| | |

| Aldeyra | Reproxalap | Other/Undisclosed |

| Arcus | Zimberelimab | Cancer |

| Aytu Bioscience | CCP-07 and CCP-08 | Infectious disease |

| Eisai | FYCOMPA | Central Nervous System |

| Harbour | Batoclimab | Cancer |

| Janssen | Teclistamab | Cancer |

| Jazz | Rylaze | Cancer |

| Marinus | Ganaxalone IV | Central Nervous System |

| Novan | SB206 | Infectious Disease |

| Novartis | Mekinist (CE-Trametinib) | Cancer |

| Opthea | OPT-302 | Ophthalmology |

| Outlook Therapeutics | ONS-5010 | Other/Undisclosed |

| Palvella | PTX-022 | Other/Undisclosed |

| Sage | Zulresso | Infectious disease |

| Serum Institute | CRM197 | Infectious Disease |

| SQ Innovation | CE-Furosemide | Cardiovascular disease |

| Sunshine Lake | Vilazodone | Central Nervous System |

| Takeda | Pevonedistat | Cancer |

| Travere | Sparsentan | Severe and Rare |

| Verona | Ensifentrine (RPL554) | Respiratory Disease |

| Various | Teriparatide | Women's Health |

| Xi'an Xintong | Pradefovir | Infectious Disease |

| | | | | | | | |

| | |

| | |

| Phase 2 |

| Partner Name | Program | Therapeutic Area |

| | |

| Cantex | CX-01 | Cancer |

| Corvus | Ciforadenant | Cancer |

| DeNovo | Lisfensine | Neurology |

| Elevation Oncology | Seribantumab | Cancer |

| Genmab | Gen1046 | Cancer |

| Immunovant | Batoclimab | Inflammatory/Metabolic |

| Janssen | Teclistimab | Cancer |

| Merck | Berzosertib | Cancer |

| Merck | V116 | Infectious Disease |

| Novartis | ECF843 | Inflammatory/Metabolic |

| Oncternal | Cirmtuzumab | Cancer |

| Palvella | PTX-022 | Other/Undisclosed |

| Phoenix Tissue | PTR-01 | Genetic Disease |

| Precision Biologics | NPC-1C | Cancer |

| Seelos | Aplindore | Central Nervous System |

| Sermonix | Lasofoxifene | Cancer |

| VentiRx | Motolimod | Cancer |

| Various | JPH-203 | Cancer |

| Viking | VK5211 | Inflammatory/Metabolic |

| Viking | VK2809 | Inflammatory/Metabolic |

| Viking | VK0612 | Inflammatory/Metabolic |

| | |

| Phase 1 |

| Partner Name | Program | Therapeutic Area |

| | |

| Amgen | AMG-330 | Cancer |

| Apotex | Meloxicam | Migraine |

| Aptevo | APVO436 | Cancer |

| Boehringer Ingelheim | Undisclosed | Other/Undisclosed |

| CSL | CSL-324 | Immunology |

| Curon | CN1 | Cancer |

| Daxor | I131 | Cardiovascular disease |

| Foghorn | FHD-609/BRD9 | Cancer |

| Halo | CE-Oleic acid | Infectious disease |

| Hanall | Batoclimab | Cancer |

| Janssen | JNJ-78306358 | Cancer |

| Janssen | JNJ-67371244 | Cancer |

| Janssen | JNJ-70218902 | Cancer |

| Jupiter Bioscience | Viright | Cancer |

| MEI Pharma | ME-344 | Cancer |

| Merck | M6233 | Cancer |

| | | | | | | | |

| Novartis | MIK-665 | Cancer |

| Novartis | BCL-201 | Cancer |

| Nucorion | NUC-1010 | Infectious disease |

| Revision Therapeutics | Rev0100 | Ophthalmology |

| Sage | SAGE-689 | Central Nervous System |

| SalubrisBio | SAL003 | Metabolic disease |

| Symphogen/Servier | SYM022/SYM023/SYM024/S095029 | Cancer |

| Takeda | TAK-925 | Severe and Rare |

| Takeda | TAK-243 | Cancer |

| Vaxxas | Nanopatch | Infectious Disease |

| Viking | VK-0214 | Genetic Disease |

| Xi'an Xintong | MB07133 | Cancer |

| Zhilkang Hongyi | Anti-4-1BB | Cancer |

Selected Commercial Programs

We have multiple programs under license with other companies that have products that are already being commercialized. The following programs represent components of our current portfolio of revenue-generating assets and potential for near-term growth in royalty and other revenue. For information about the royalties owed to us for these programs, see “Royalties” later in this business section.

Kyprolis (Amgen)

We supply Captisol to Amgen for use with Kyprolis (carfilzomib), and granted Amgen an exclusive product-specific license under our patent rights with respect to Captisol. Kyprolis is formulated with Ligand’s Captisol technology and is approved in the United States for the following:

•In combination with dexamethasone, lenalidomide plus dexamethasone, daratumumab plus dexamethasone, or daratumumab and hyaluronidase-fihj and dexamethasone for the treatment of patients with relapsed or refractory multiple myeloma who have received one to three lines of therapy.

•As a single agent for the treatment of patients with relapsed or refractory multiple myeloma who have received one or more lines of therapy.

| | | | | | | | | | | | | | |

| Kyprolis (Amgen) |

| < $250 million | 1.5% |

| $250 to $500 million | 2.0% |

| $500 to $750 million | 2.5% |

| >$750 million | 3.0% |

Our agreement with Amgen may be terminated by either party in the event of material breach or bankruptcy, or unilaterally by Amgen with prior written notice, subject to certain surviving obligations. Absent early termination, the agreement will terminate upon expiration of the obligation to pay royalties. Under this agreement, we are entitled to receive revenue from clinical and commercial Captisol material sales and royalties on annual net sales of Kyprolis.

Veklury (Gilead)