Form 8-K

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant

to Section 13 or 15(d)

of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): September 22, 2014

General Cable Corporation

(Exact name of registrant as specified in its charter)

|

|

|

|

|

| Delaware |

|

001-12983 |

|

06-1398235 |

| (State or other jurisdiction

of incorporation) |

|

(Commission

File Number) |

|

(IRS Employer

Identification No.) |

|

|

| 4 Tesseneer Drive, Highland Heights, Kentucky |

|

41076-9753 |

| (Address of principal executive offices) |

|

(Zip Code) |

Registrant’s telephone number, including area code: (859) 572-8000

Not Applicable

(Former

name or former address, if changed since last report)

Check the appropriate box below

if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| ¨ |

Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ¨ |

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ¨ |

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ¨ |

Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Forward-Looking Statements

Certain statements in this current report on Form 8-K of General Cable Corporation, a Delaware corporation (sometimes referred to as the

“Company,” “General Cable,” “we,” “us,” and “our”), are forward-looking statements that involve risks and uncertainties, predict or describe future events or trends and that do not relate solely to

historical matters. Forward-looking statements include, among others, expressed expectations with regard to the following: “believe,” “expect,” “may,” “will,” “anticipate,” “intend,”

“estimate,” “project,” “plan,” “assume,” “seek to” or other similar expressions, although not all forward-looking statements contain these identifying words. Actual results may differ materially

from those discussed in forward-looking statements as a result of factors, risks and uncertainties over many of which we have no control. These factors include, but are not limited to, the risks detailed from time to time in the Company’s

filings with the Securities and Exchange Commission (“SEC”), including but not limited to, our annual report on Form 10-K filed with the SEC on March 3, 2014, and subsequent SEC filings. You are cautioned not to place undue reliance on

these forward-looking statements. General Cable does not undertake, and hereby disclaims, any obligation, unless required to do so by applicable securities laws, to update any forward-looking statements as a result of new information, future

events or other factors.

| Item 7.01 |

Regulation FD Disclosure |

Press Releases

On September 22, 2014, the Company issued a press release updating its third quarter and full year 2014 outlook. The press release is

attached hereto as Exhibit 99.1 and is incorporated herein by reference.

On September 22, 2014, the Company issued a press

release announcing the proposed offering of $250 million aggregate principal amount of senior notes due 2019 in an offering exempt from registration under the Securities Act of 1933, as amended. The press release is attached hereto as

Exhibit 99.2 and is incorporated herein by reference.

Additional Information

The Company provides the following information pursuant to Regulation FD:

Restructuring Activities

In July 2014,

we announced a comprehensive restructuring program. The restructuring program, which builds on our previously launched productivity and asset optimization plans, is expected to generate approximately $10.0 million of savings in 2014, increasing to

ongoing annual savings of approximately $75.0 million beginning in 2016. The program is focused on the closure of certain underperforming assets as well as the consolidation and realignment of other facilities. Overall, we expect 20% of our

facilities will be impacted by the restructuring program, half of which may result in closures, while the other half represents facility realignments or production reconfigurations. We are also implementing reductions in SG&A expenses globally.

The restructuring program is expected to result in pre-tax charges of approximately $200.0 million, which includes approximately $80.0 million of cash costs, primarily related to separation

expense. The remainder of the charges are expected to be non-cash, primarily related to accelerated depreciation and the write-off of property, plant and equipment resulting from facility closures. These actions are anticipated to result in the

elimination of approximately 1,000 positions globally, representing nearly 7% of our workforce. We anticipate a majority of the total charges will be incurred in 2014. We have taken prompt actions, announcing in conjunction with our second quarter

earnings release in late July, the closure of the India and Peru greenfield locations in our ROW segment, as well as the closure of one manufacturing facility in North America. In India, we plan to maintain a local sales team focused on higher

value-added products, such as extra high voltage power cables sourced from our facilities in Thailand and France. Similarly, in Peru, we plan to service our important market position from other regional assets. In North America, we are consolidating

a smaller facility that produces aftermarket ignition sets for the Mexican and Latin American markets. In June 2014, prior to announcing the restructuring program, we reduced our salaried positions in North America. The costs related to such

reduction in salaried positions are included in the expected costs of our restructuring program.

The announced closure of a manufacturing

facility in North America in connection with our restructuring program represents the third facility closure in North America this year as, prior to announcing the restructuring program, we announced the permanent closure of two manufacturing

facilities in our electric utility business in February as part of a productivity and asset optimization plan. We expect to incur $10.0 million to $12.0 million, half of which is expected to be non-cash, in pre-tax costs in 2014 related to the

closure of these two manufacturing facilities. The $10.0 million to $12.0 million of expected costs are not included in the expected costs of our restructuring program described in the preceding paragraph. In the six fiscal months ended

June 27, 2014, we incurred charges of $10.5 million related to these closures and other cost reductions. The permanent closure of these two manufacturing facilities is expected to generate ongoing annual savings of $3.0 million to $5.0 million.

Prior to our restructuring program, we also launched productivity and asset optimization plans focused on the turnaround of greenfield

investments in Mexico, South Africa and the specialty cable business in Brazil. As a result, these businesses continue to make progress, and their performance trends are in line with performance improvement milestones established by management.

Also, over the past several years, we have been refining our pan-European go-to-market strategy, which continues to evolve, resulting in better market coverage, improved logistics and plant optimization. We have also realigned resources and lowered

our cost base in the European and Mediterranean region by reducing regional headcount, which, when combined with our pan-European go-to-market strategy, has lowered our ongoing cost base by more than $40.0 million.

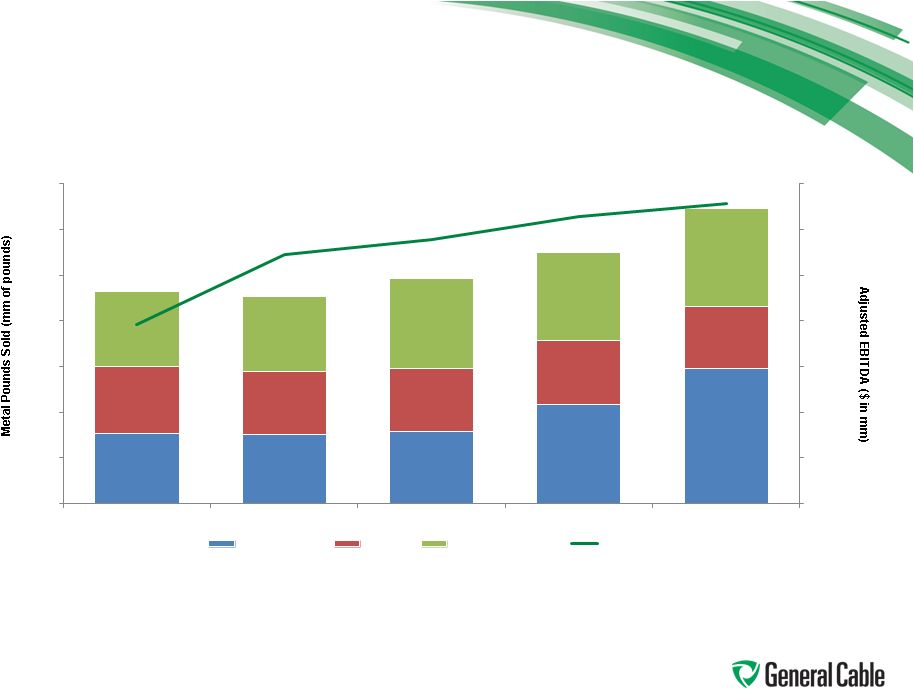

Metals Pounds Sold, Adjusted EBITDA and Revenues – Excluding Venezuela

Attached as Exhibit 99.3 and incorporated herein by reference is a slide which shows metal pounds sold, Adjusted EBITDA and revenues, each

excluding our Venezuelan operations, for the years ended December 31, 2013, December 31, 2012, December 31, 2011, December 31, 2010 and December 31, 2009.

The information being furnished pursuant to this Item 7.01, including Exhibit 99.1, Exhibit 99.2 and Exhibit 99.3, shall not be deemed to

be “filed” for purposes of Section 18 of the Securities and Exchange Act of 1934, as amended, nor shall it be deemed incorporated by reference in any filing under the Securities Act of 1933, as amended, except as shall be expressly

set forth by specific reference in such filing.

Risk Factors

The Company has updated certain of its risk factors and description of legal proceedings. The risk factors and description of legal proceedings

listed below should be read in conjunction with the risk factors and legal proceedings disclosed in the Company’s Annual Report on Form 10-K for the year ended December 31, 2013 and the Company’s Quarterly Report on Form 10-Q for the

quarter ended June 27, 2014.

We have recently recorded impairment charges with respect to certain of our long-lived assets. As a

result of our restructuring program and market and industry conditions, we expect to recognize additional impairment charges for our long-lived assets in the future, including goodwill.

As of June 27, 2014, property, plant and equipment, goodwill and other intangible assets accounted for approximately $1,135.6 million, or

26% of our total assets. In accordance with generally accepted accounting principles, we periodically assess our long-lived assets to determine if they are impaired. The testing for impairment is based on assumptions regarding our future business

outlook as well as other factors. While we continue to review and analyze many factors that can impact our business, such as industry and economic trends, our analyses are subjective and are based on conditions existing at and trends leading up to

the time the assumptions are made. Actual results could differ materially from these assumptions particularly in the event of disruptions to our business, unexpected significant changes or planned changes in the use of assets or divestitures or

expropriations of assets.

Due to events in Venezuela, including recent changes to the currency exchange system, restrictive pricing

controls, ongoing labor negotiations and lingering social unrest as well as the significant decline in our stock price during the first quarter of 2014, we recognized a goodwill impairment charge of $155.1 million and an impairment charge of $93.4

million for the indefinite-lived trade name associated with the PDIC reporting unit in the first quarter of 2014.

In addition, in the

three fiscal months ended June 27, 2014, our executive management evaluated global operations to allow us to expand productivity and asset optimization. In the early stages of the evaluation process, we reviewed the financial performance of our

General Cable India asset group (“India”) and our PDIC Peru asset group (“Peru”). Due to the ongoing weak economic conditions at both asset groups and the weak economic outlook, we decided to no longer focus on the possible

growth opportunities in our India and Peru businesses; therefore, we would no longer provide cash flow or operational support to these businesses and we performed an asset impairment review of our India and Peru asset groups. Based on the results of

the analysis, we recorded an impairment charge of $16.5 million for our India business and $6.9 million for our Peru business in the three and six fiscal months ended June 27, 2014.

A supplier of molten aluminum to a rod mill in our ROW segment has informed us that it is

reducing its output and that the amount of molten aluminum that it supplies to us will be reduced. As a result, the reduced supply of molten aluminum available may be insufficient to continue to operate this rod mill, which could result in a $15.0

million to $20.0 million non-cash impairment charge. In addition, in July 2014, we announced a comprehensive restructuring program. Future impairment charges as a result of our restructuring program or otherwise could significantly affect our

results of operations in the period recognized.

We may not be able to achieve all of our anticipated cost savings.

We recently announced a comprehensive restructuring program. The restructuring program, which builds on our previously launched productivity

and asset optimization plans, is expected to generate approximately $10.0 million of savings in 2014, increasing to ongoing annual savings of approximately $75.0 million beginning in 2016. The restructuring program is expected to result in pre-tax

charges of approximately $200.0 million, which includes approximately $80.0 million of cash costs. We may not achieve the full amount of these cost savings, or it may take us longer to achieve them than we currently anticipate. Although we have

identified some of the facilities that we expect to close, consolidate or realign as part of our restructuring program, we have not identified all those facilities. Our restructuring program will take time and will involve significant costs and

management effort to negotiate and implement employee separation packages, consolidate operations of certain of our facilities and make investments necessary to operate our business with a smaller number of facilities. We may not be successful in

these efforts. In addition, our estimates are based on a number of other assumptions that may not prove accurate. We may not achieve the cost savings we anticipate, or other unexpected costs could offset any savings we achieve. Our failure to

achieve our anticipated annual cost savings could have a material adverse effect on our results of operations in future periods.

We

source and sell products globally and are exposed to fluctuations in foreign currency exchange rates.

We manufacture and sell

products and finance operations throughout the world and are exposed to the impact of foreign currency fluctuations on our results of operations. Also, our consolidated financial results are presented in U.S. dollars; therefore, a change in the

value of currencies may adversely impact our financial statements after currency remeasurements and translation to U.S. dollars. In addition, devaluations of currencies, such as the devaluation of the Venezuelan bolivar, could negatively affect the

value of our earnings from, and the assets located, in those markets.

Effective in the first quarter of 2014 and through June 27,

2014, we expected that the majority of our Venezuelan subsidiary’s net monetary assets would be remeasured at the SICAD 1 rate. In applying the March 28, 2014 SICAD 1 exchange rate of 10.8 BsF per U.S. dollar to certain of our monetary

assets and liabilities, we recorded a devaluation charge of $83.1 million for the six fiscal months ended June 27, 2014.

On

February 19, 2014, the Venezuelan government announced plans for another currency exchange mechanism (“SICAD 2”), which allows authorized foreign exchange operators, such as regulated banks and capital market brokers, to act as

intermediaries. At this time, we do not intend to utilize the SICAD 2 foreign exchange mechanism at the prevailing exchange rates. We have assessed a number of factors, including the limited number of SICAD 2 auctions held to date, our ability to

access the SICAD 2 exchange to date, the restrictions placed on eligible participants, the amount of U.S. dollars available for purchase through the auction process, and the historical lack of official information about the resulting SICAD 2 rate.

At this time, based

upon our assessment, we do not believe it would be appropriate to use rates from the SICAD 2 exchange system for financial reporting purposes at June 27, 2014. If we had been required to

apply the June 27, 2014 SICAD 2 exchange rate (approximately 50 BsF per U.S. dollar) to our financial statements, we would have incurred a pre-tax charge of approximately $100 million as of June 27, 2014. If we were required to apply the

SICAD 2 rate in the future, or if the Venezuelan government were to introduce new currency exchange mechanisms, we cannot predict the amount of charges that we may be required to incur, and those charges could materially and adversely impact our

results of operations.

If we fail to comply with the reporting obligations of the Exchange Act or if we fail to maintain adequate

internal control over financial reporting, our business, the market value of our securities and our access to capital markets could be materially adversely affected.

As a public company, we are required to comply with the periodic reporting obligations of the Securities Exchange Act of 1934, as amended,

referred to as the “Exchange Act,” including the requirement that we file annual reports and quarterly reports with the SEC. Our failure to file required information in a timely manner could subject us to penalties under federal securities

laws, expose us to additional lawsuits, create a default under our existing debt instruments and facilities, and restrict our ability to access financing. In addition, our management is responsible for establishing and maintaining adequate internal

control over financial reporting. Our internal control over financial reporting is a process designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements in accordance with

GAAP. However, our management within the past two years has identified control deficiencies that constituted material weaknesses. These material weaknesses resulted in accounting errors that caused us to issue, in March 2013, restated consolidated

financial statements as of December 31, 2011 and 2010 and for the years ended December 31, 2011, 2010 and 2009, and unaudited restated financial statements for interim periods in 2011 and interim periods ended on March 30, 2012 and

June 29, 2012, and, to issue, in January 2014, restated consolidated financial statements as of December 31, 2012, 2011 and 2010 and for the years ended December 31, 2012, 2011, 2010 and 2009, and unaudited restated financial

statements for interim periods in 2011 and 2012 and the interim period ended on March 29, 2013.

As described below in “Legal

proceedings — Government and internal investigations,” we conducted internal investigations principally relating to the matters resulting in the restatements described above. We voluntarily contacted the SEC to advise it of our initial

internal investigation, and we have continued to provide information to the SEC on an ongoing basis, including, among other things, information regarding the matters described below in “Legal proceedings — Government and internal

investigations”. The SEC has issued a formal order of investigation. Pursuant to the formal order, the SEC issued subpoenas to us seeking relevant documents and to certain of our current and former employees seeking their testimony. We continue

to cooperate with the SEC in connection with its investigation.

Two civil complaints were filed in the United States District Court for

the Southern District of New York on October 21, 2013 and December 4, 2013 by named plaintiffs, on behalf of purported classes of persons who purchased or otherwise acquired our publicly traded securities, against us, Gregory Kenny, our

President and Chief Executive Officer, and Brian Robinson, our Executive Vice President and Chief Financial Officer. On our motion, the complaints were transferred to the United States District Court for the Eastern District of Kentucky, the actions

were consolidated, and a consolidated complaint was filed in that Court on May 20, 2014 by City of Livonia Employees Retirement System, as lead plaintiff on behalf of a purported class of all persons or entities who purchased our securities

between November 3, 2010 and October 14, 2013, referred to as the

City of Livonia Complaint. The City of Livonia Complaint alleges claims under the antifraud and controlling person liability provisions of the Exchange Act, alleging generally, among other

assertions, that we employed inadequate internal financial reporting controls that resulted in, among other things, improper revenue recognition, understated cost of sales, overstated operating income, net income and earnings per share, and the

failure to detect inventory lost through theft; that we issued materially false financial results that had to be restated on two occasions; and that statements of Messrs. Kenny and Robinson that they had tested and found effective General

Cable’s internal controls over financial reporting and disclosure were false.

The City of Livonia Complaint alleges that as a result

of the foregoing, our stock price was artificially inflated and the plaintiffs suffered damages in connection with their purchase of our stock. The City of Livonia Complaint seeks damages in an unspecified amount; reasonable costs and expenses,

including counsel and experts fees; and such equitable injunctive or other relief as the Court deems just and proper. On July 18, 2014, defendants filed a motion to dismiss the City of Livonia Complaint based on plaintiff’s failure to

state a claim upon which relief could be granted. On August 28, 2014, the plaintiff filed a response opposing the motion, and on September 11, 2014, defendants filed a reply to plaintiff’s response. The motion is pending. In addition,

a derivative complaint was filed on January 7, 2014 in the Campbell County, Kentucky Circuit Court against all but one member of our Board of Directors, including Mr. Kenny, two former directors, Mr. Robinson and two former ROW

officials, one of whom is a former executive officer of our company. The derivative complaint alleges that the defendants breached their fiduciary duties by knowingly failing to ensure that we implemented and maintained adequate internal controls

over our accounting and financial reporting functions and by knowingly disseminating to stockholders materially false and misleading statements concerning our financial results and internal controls. The derivative complaint seeks damages in an

unspecified amount, appropriate equitable relief to remedy the alleged breaches of fiduciary duty, attorney’s fees, experts’ fees and other costs. On March 5, 2014, the derivative case was placed on inactive status until a motion is

filed by a party to reinstate the action to the court’s active docket. We believe the derivative complaint, insofar as it relates to our current and former directors, including Mr. Kenny, and to Mr. Robinson, and the City of Livonia

Complaint are without merit and intend to vigorously contest the actions.

In response to the material weaknesses identified by us, we

instituted a number of actions and designed and commenced implementation of changes in our internal control over financial reporting. Based on the actions, our management concluded that the material weakness related to inventory control deficiencies

in Brazil and control deficiencies related to the prior executive management team in place in our ROW segment have been remediated as of December 31, 2013. We cannot provide assurance that we have identified all, or that we will not in the

future have additional, material weaknesses in our internal control over financial reporting. As a result, we may be required to implement further remedial measures and to design enhanced processes and controls to address deficiencies, which could

result in significant costs to us and require us to divert substantial resources, including management time, from other activities. If we identify material weaknesses or fail to maintain adequate internal controls over financial reporting in the

future, we may not be able to prepare reliable financial reports and comply with our reporting obligations under the Exchange Act on a timely basis. Any such delays in the preparation of financial reports and the filing of our periodic reports may

result in a loss of public confidence in the reliability of our financial statements, the commencement of additional litigation, or the commencement of regulatory action against us, which may include court actions or administrative proceedings, any

of which could materially adversely affect our business, the market value of our securities and our access to the capital markets.

Compliance with foreign and U.S. laws and regulations applicable to our international

operations, including the Foreign Corrupt Practices Act (“FCPA”), other applicable anti-corruption laws and anti-competition regulations, may increase the cost of doing business in international jurisdictions.

Various laws and regulations associated with our current international operations are complex and increase our cost of doing business.

Furthermore, these laws and regulations expose us to fines and penalties if we fail to comply with them. These laws and regulations include import and export requirements, anti-competition regulations, U.S. laws such as the FCPA, and local laws

prohibiting payments to governmental officials and other corrupt practices. Although we have implemented policies and procedures designed to ensure compliance with these laws, there can be no assurance that our employees, contractors and agents will

not take actions in violation of our policies, particularly as we expand our operations through organic growth and acquisitions. Any such violations could subject us to civil or criminal penalties, including material fines or prohibitions on our

ability to offer our wire and cable products in one or more countries, and could also materially damage our reputation, brand, international expansion efforts, business and operating results. In addition, if we fail to address the challenges and

risks associated with our international expansion and acquisition strategy, we may encounter difficulties implementing this strategy, which could impede our growth or harm our operating results.

We have been reviewing, with the assistance of external counsel, certain commission payments involving sales to customers of our subsidiary in

Angola. The review has focused upon payment practices with respect to employees of public utility companies, use of agents in connection with such payment practices, and the manner in which the payments were reflected on our books and records. We

have determined at this time that certain employees in our Portugal and Angola subsidiaries directly and indirectly made payments at various times from 2002 through 2013 to officials of Angola government-owned public utilities that raise concerns

under the FCPA and possibly under the laws of other jurisdictions. We also have been reviewing, with the assistance of external counsel, our use and payment of agents in connection with our Thailand and India operations, which may have implications

under the FCPA. We have voluntarily disclosed these matters to the SEC and the United States Department of Justice (“DOJ”) and have provided them with additional information at their request. The SEC and DOJ inquiries into these matters

are ongoing. We continue to cooperate with the DOJ and the SEC with respect to these matters. We are implementing a screening process relating to sales agents that we use outside of the United States, including, among other things, a review of the

agreements under which they were retained and a risk-based assessment of such agents to determine the scope of due diligence measures to be performed by a third-party investigative firm. However, this screening process may not be effective in

preventing future payments or other activities that may raise concerns under the FCPA or other laws.

At this time, we are unable to

predict the nature of any action that may be taken by the DOJ or SEC or any remedies these agencies may pursue as a result of such actions. Any determination that our operations or activities are not in compliance with existing laws or regulations

could result in the imposition of substantial fines, civil and criminal penalties, and equitable remedies, including disgorgement and injunctive relief. Because our review regarding commission payment practices and our use and payment of agents

described above is ongoing, we are unable to predict its duration, scope, results, or consequences. Dispositions of these types of matters can result in modifications to business practices and compliance programs, and in some cases the appointment

of a monitor to review future business and practices with the objective of effecting compliance with the FCPA and other applicable laws.

Legal Proceedings

Government and internal investigations

We have been reviewing, with the assistance of external counsel, certain commission payments involving sales to customers of our subsidiary in

Angola. The review has focused upon payment practices with respect to employees of public utility companies, use of agents in connection with such payment practices, and the manner in which the payments were reflected on our books and records. We

have determined at this time that certain employees in our Portugal and Angola subsidiaries directly and indirectly made payments at various times from 2002 through 2013 to officials of Angola government-owned public utilities that raise concerns

under the FCPA and possibly under the laws of other jurisdictions. We also have been reviewing, with the assistance of external counsel, our use and payment of agents in connection with our Thailand and India operations, which may have implications

under the FCPA. We have voluntarily disclosed these matters to the SEC and the DOJ and have provided them with additional information at their request. The SEC and DOJ inquiries into these matters are ongoing. We continue to cooperate with the DOJ

and the SEC with respect to these matters. At this time, we are unable to predict the nature of any action that may be taken by the DOJ or SEC or any remedies these agencies may pursue as a result of such actions. We are implementing a screening

process relating to sales agents that we use outside of the United States, including, among other things, a review of the agreements under which they were retained and a risk-based assessment of such agents to determine the scope of due diligence

measures to be performed by a third-party investigative firm.

As previously disclosed, we conducted internal investigations, subject to

the oversight of the Audit Committee of our Board of Directors and with the assistance of external counsel, principally relating to matters resulting in restatements of a number of our previously issued financial statements. The matters addressed in

the investigations included (i) inventory accounting errors addressed in the restatements, including those resulting from inventory theft in Brazil, as well as the timing of internal reporting of the inventory accounting issues to senior

corporate management at our headquarters in Highland Heights, Kentucky and (ii) historical revenue recognition accounting practices with regard to “bill and hold” sales in Brazil related to aerial transmission projects, including

instances where we have determined that the requirements for revenue recognition under GAAP with respect to the bill and hold sales were not met. (“Bill and hold” sales generally are sales meeting specified criteria under GAAP that enable

the seller to recognize revenue at the time title to goods and ownership risk is transferred to the customer, even though the seller does not ship the goods until a later time. In typical sales transactions other than those accounted for as bill and

hold, title to goods and ownership risk is transferred to the customer at the time of shipment or delivery.) In connection with these matters, among others, our management identified control deficiencies that constituted material weaknesses in our

internal control over financial reporting. These material weaknesses resulted in accounting errors that caused us to issue two sets of restated financial statements. In March 2013, principally to correct the inventory accounting errors, we issued

restated consolidated financial statements as of December 31, 2011 and 2010 and for the years ended December 31, 2011, 2010 and 2009, and unaudited restated financial statements for interim periods in 2011 and interim periods ended on

March 30, 2012 and June 29, 2012. In January 2014, principally to correct errors relating to revenue recognition with respect to the bill and hold sales, we issued restated consolidated financial statements (which also encompassed matters

addressed in the earlier restatement) as of December 31, 2012, 2011 and 2010 and for the years ended December 31, 2012, 2011, 2010 and 2009, and unaudited restated financial statements for interim periods in 2011 and 2012 and the interim

period ended on March 29, 2013. For more information regarding these material weaknesses and the steps we have taken to remediate them, see “Item 9A. Controls and Procedures” in our annual report on Form 10-K for the year ended

December 31, 2013.

We voluntarily contacted the SEC to advise it of our initial internal investigation, and we have

continued to provide information to the SEC on an ongoing basis, including, among other things, information regarding the matters described above and certain earnings management activities by employees in our ROW segment prior to the end of 2012. As

we previously disclosed, these earnings management activities (none of which identified to date had a material effect on our consolidated financial statements) were designed to delay the reporting of expenses or other charges, including improper

capitalization of costs, misuse of accruals and failure to timely report inventory shortfalls identified through physical inventory counts. The SEC has issued a formal order of investigation. Pursuant to the formal order, the SEC issued subpoenas to

us seeking relevant documents and to certain of our current and former employees seeking their testimony. The SEC has requested information regarding, among other things, the above-described Angola matter, matters that were subject to our internal

investigations and earnings management activities by ROW employees. We continue to cooperate with the SEC in connection with its investigation.

Any determination that our operations or activities are not in compliance with existing laws or regulations could result in the imposition of

substantial fines, civil and criminal penalties, and equitable remedies, including disgorgement and injunctive relief. Because the government investigations and our review regarding commission payment practices and our use and payment of agents

described above are ongoing, we are unable to predict their duration, scope, results, or consequences. Dispositions of these types of matters can result in modifications to business practices and compliance programs, and in some cases the

appointment of a monitor to review future business and practices with the objective of effecting compliance with the FCPA and other applicable laws.

Purported class action and derivative litigation

The matters described above under “— Government and internal investigations” relating to our Brazilian business that caused us

to restate our financial statements apparently also have, in part, led to litigation against us and certain of our current and former directors, executive officers and employees.

Two civil complaints were filed in the United States District Court for the Southern District of New York on October 21, 2013 and

December 4, 2013 by named plaintiffs, on behalf of purported classes of persons who purchased or otherwise acquired our publicly traded securities, against us, Gregory Kenny, our President and Chief Executive Officer, and Brian Robinson, our

Executive Vice President and Chief Financial Officer. On our motion, the complaints were transferred to the United States District Court for the Eastern District of Kentucky, the actions were consolidated, and a consolidated complaint was filed in

that Court on May 20, 2014 by City of Livonia Employees Retirement System, as lead plaintiff on behalf of a purported class of all persons or entities who purchased our securities between November 3, 2010 and October 14, 2013 (the

“City of Livonia Complaint”). The City of Livonia Complaint alleges claims under the antifraud and controlling person liability provisions of the Exchange Act, alleging generally, among other assertions, that we employed inadequate

internal financial reporting controls that resulted in, among other things, improper revenue recognition, understated cost of sales, overstated operating income, net income and earnings per share, and the failure to detect inventory lost through

theft; that we issued materially false financial results that had to be restated on two occasions; and that statements of Messrs. Kenny and Robinson that they had tested and found effective our internal controls over financial reporting and

disclosure were false. The City of Livonia Complaint alleges that as a result of the foregoing, our stock price was artificially inflated and the plaintiffs suffered damages in connection with their purchase of our stock. The City of Livonia

Complaint seeks damages in an unspecified amount; reasonable costs and expenses, including counsel and experts fees; and such equitable injunctive or other relief as the Court deems just and proper. On July 18, 2014, defendants filed a motion

to dismiss the City of Livonia Complaint based on plaintiff’s failure to state a claim upon which relief could be granted. On August 28,

2014, the plaintiff filed a response opposing the motion, and on September 11, 2014, defendants filed a reply to plaintiff’s response. The motion is pending. In addition, a derivative

complaint was filed on January 7, 2014 in the Campbell County, Kentucky Circuit Court against all but one member of our Board of Directors, including Mr. Kenny, two former directors, Mr. Robinson and two former ROW officials, one of

whom is our former executive officer. The derivative complaint alleges that the defendants breached their fiduciary duties by knowingly failing to ensure that we implemented and maintained adequate internal controls over our accounting and financial

reporting functions and by knowingly disseminating to stockholders materially false and misleading statements concerning our financial results and internal controls. The derivative complaint seeks damages in an unspecified amount, appropriate

equitable relief to remedy the alleged breaches of fiduciary duty, attorneys’ fees, experts’ fees and other costs. On March 5, 2014, the derivative case was placed on inactive status until a motion is filed by a party to reinstate the

action to the Court’s active docket.

We believe the derivative complaint, insofar as it relates to our current and former directors,

including Mr. Kenny, and to Mr. Robinson, and the City of Livonia Complaint are without merit and intend to vigorously contest the actions.

We also are involved in certain other legal proceedings and administrative actions that are described in Footnote 18, “Commitments and

Contingencies,” to our unaudited condensed consolidated financial statements included in our Quarterly Report on Form 10-Q for the quarter ended June 27, 2014.

In addition, we are involved in various routine legal proceedings and administrative actions incidental to our business. In the opinion of our

management, these routine proceedings and actions should not, individually or in the aggregate, have a material adverse effect on our consolidated results of operations, cash flows or financial position. However, in the event of unexpected future

developments, it is possible that the ultimate resolution of these matters or other similar matters, if unfavorable, may have such adverse effects.

In accordance with GAAP, we record a liability when it is both probable that a liability has been incurred and the amount of the loss can be

reasonably estimated. These provisions are reviewed at least quarterly and adjusted to reflect the impacts of negotiations, settlements, rulings, advice of legal counsel, and other information and events pertaining to a particular case. To the

extent additional information arises or our strategies change, it is possible that our estimate of our probable liability in these matters may change.

| Item 9.01 |

Financial Statements and Exhibits. |

(d) Exhibits.

The following exhibits are furnished herewith.

|

|

|

| Exhibit

Number |

|

Description |

|

|

| 99.1 |

|

General Cable Corporation Press Release, dated September 22, 2014 |

|

|

| 99.2 |

|

General Cable Corporation Press Release, dated September 22, 2014 |

|

|

| 99.3 |

|

Metal Pounds Sold, Adjusted EBITDA and Revenues – Excluding Venezuela |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by

the undersigned hereunto duly authorized.

|

|

|

|

|

|

|

| Dated: September 22, 2014 |

|

GENERAL CABLE CORPORATION |

|

|

|

|

|

|

|

|

By: |

|

/s/ Brian J. Robinson |

|

|

|

|

Name: |

|

Brian J. Robinson |

|

|

|

|

Title: |

|

Executive Vice President and

Chief Financial Officer |

INDEX TO EXHIBITS

|

|

|

| Exhibit

Number |

|

Description |

|

|

| 99.1 |

|

General Cable Corporation Press Release, dated September 22, 2014 |

|

|

| 99.2 |

|

General Cable Corporation Press Release, dated September 22, 2014 |

|

|

| 99.3 |

|

Metal Pounds Sold, Adjusted EBITDA and Revenues – Excluding Venezuela |