Exhibit

| |

ITEM 8. | FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA |

FIRST DATA CORPORATION

INDEX TO FINANCIAL STATEMENTS

COVERED BY REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

|

| |

First Data Corporation and Subsidiaries: | |

Consolidated Financial Statements: | |

| |

| |

| |

| |

| |

| |

| |

Schedules: | |

| |

Report of Independent Registered Public Accounting Firm

The Board of Directors and Stockholders of First Data Corporation

Opinion on the Financial Statements

We have audited the accompanying consolidated balance sheets of First Data Corporation as of December 31, 2017 and 2016, and the related consolidated statements of operations, comprehensive income (loss), cash flows and equity for each of the three years in the period ended December 31, 2017, and the related notes and the financial statement schedule of valuation and qualifying accounts (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the consolidated financial position of the Company at December 31, 2017 and 2016, and the consolidated results of its operations and its cash flows for each of the three years in the period ended December 31, 2017, in conformity with U.S. generally accepted accounting principles.

We also have audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States) (PCAOB), the Company's internal control over financial reporting as of December 31, 2017, based on criteria established in Internal Control-Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission (2013 framework), and our report dated February 20, 2018 expressed an unqualified opinion thereon.

Adoption of New Accounting Standards

As discussed in Note 1 to the consolidated financial statements, on January 1, 2018, the Company changed its method for accounting for pension costs and its method of presenting restricted cash and restricted cash equivalents in the statement of cash flow for each of the three years ended December 31, 2017 due to the adoption of new accounting guidance that was applied on a retrospective basis.

Basis for Opinion

These financial statements are the responsibility of the Company's management. Our responsibility is to express an opinion on the Company’s financial statements based on our audits. We are a public accounting firm registered with the PCAOB and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

|

| |

/s/ Ernst & Young LLP | |

| |

EY or one of its predecessors began serving consecutively as the Company’s (or one of its predecessors) auditor in 1980. | |

| |

Atlanta, Georgia | |

February 20, 2018, except as to Note 1, Note 5, Note 7, Note 10, Note 14, Note 18, and Note 19, as to which the date is August 13, 2018 | |

FIRST DATA CORPORATION

CONSOLIDATED STATEMENTS OF OPERATIONS

|

| | | | | | | | | | | | |

| | Year ended December 31, |

(in millions, except per share amounts) | | 2017 | | 2016 | | 2015 |

Revenues: | | |

| | |

| | |

|

Transaction and processing service fees (a) | | $ | 6,757 |

| | $ | 6,600 |

| | $ | 6,597 |

|

Product sales and other (a) | | 1,372 |

| | 1,239 |

| | 1,167 |

|

Total revenues (excluding reimbursable items) | | 8,129 |

| | 7,839 |

| | 7,764 |

|

Reimbursable debit network fees, postage, and other | | 3,923 |

| | 3,745 |

| | 3,687 |

|

Total revenues | | 12,052 |

| | 11,584 |

| | 11,451 |

|

Expenses: | | |

| | |

| | |

|

Cost of services (exclusive of items shown below) | | 2,769 |

| | 2,855 |

| | 2,874 |

|

Cost of products sold | | 359 |

| | 337 |

| | 356 |

|

Selling, general, and administrative | | 2,178 |

| | 2,035 |

| | 2,292 |

|

Depreciation and amortization | | 972 |

| | 949 |

| | 1,022 |

|

Other operating expenses | | 143 |

| | 51 |

| | 53 |

|

Total expenses (excluding reimbursable items) | | 6,421 |

| | 6,227 |

| | 6,597 |

|

Reimbursable debit network fees, postage, and other | | 3,923 |

| | 3,745 |

| | 3,687 |

|

Total expenses | | 10,344 |

| | 9,972 |

| | 10,284 |

|

Operating profit | | 1,708 |

| | 1,612 |

| | 1,167 |

|

Interest expense, net | | (931 | ) | | (1,078 | ) | | (1,534 | ) |

Loss on debt extinguishment | | (80 | ) | | (70 | ) | | (1,068 | ) |

Other income | | 16 |

| | 17 |

| | 29 |

|

Income (loss) before income taxes and equity earnings in affiliates | | 713 |

| | 481 |

| | (1,406 | ) |

Income tax (benefit) expense | | (729 | ) | | 81 |

| | 101 |

|

Equity earnings in affiliates | | 222 |

| | 260 |

| | 239 |

|

Net income (loss) | | 1,664 |

| | 660 |

| | (1,268 | ) |

Less: Net income attributable to noncontrolling interests

and redeemable noncontrolling interest | | 199 |

| | 240 |

| | 213 |

|

Net income (loss) attributable to First Data Corporation | | $ | 1,465 |

| | $ | 420 |

| | $ | (1,481 | ) |

| | | | | | |

Net income (loss) per share: | | | | | | |

Basic | | $ | 1.60 |

| | $ | 0.47 |

| | $ | (7.70 | ) |

Diluted | | $ | 1.56 |

| | $ | 0.46 |

| | $ | (7.70 | ) |

| | | | | | |

Weighted-average common shares outstanding: | | | | | | |

Basic | | 916 |

| | 902 |

| | 192 |

|

Diluted | | 940 |

| | 921 |

| | 192 |

|

| |

(a) | Includes processing fees, administrative service fees, and other fees charged to merchant alliances accounted for under the equity method of $215 million, $198 million, and $205 million for the years ended December 31, 2017, 2016, and 2015, respectively. |

See notes to consolidated financial statements.

FIRST DATA CORPORATION

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

|

| | | | | | | | | | | | |

| | Year ended December 31, |

(in millions) | | 2017 | | 2016 | | 2015 |

Net income (loss) | | $ | 1,664 |

| | $ | 660 |

| | $ | (1,268 | ) |

Other comprehensive income (loss), net of tax: | | |

| | |

| | |

|

Foreign currency translation adjustment | | 201 |

| | (153 | ) | | (290 | ) |

Pension liability adjustments | | 72 |

| | 38 |

| | (13 | ) |

Derivative instruments | | 9 |

| | 3 |

| | — |

|

Marketable securities | | — |

| | — |

| | 3 |

|

Total other comprehensive income (loss), net of tax | | 282 |

| | (112 | ) | | (300 | ) |

Comprehensive income (loss) | | 1,946 |

| | 548 |

| | (1,568 | ) |

Less: Comprehensive income attributable to noncontrolling interests and redeemable noncontrolling interest | | 211 |

| | 235 |

| | 203 |

|

Comprehensive income (loss) attributable to First Data Corporation | | $ | 1,735 |

| | $ | 313 |

| | $ | (1,771 | ) |

See notes to consolidated financial statements.

FIRST DATA CORPORATION

CONSOLIDATED BALANCE SHEETS

|

| | | | | | | | |

| | As of December 31, |

(in millions, except par value) | | 2017 | | 2016 |

ASSETS | | |

| | |

|

Current assets: | | |

| | |

|

Cash and cash equivalents | | $ | 498 |

| | $ | 385 |

|

Accounts receivable, net of allowance for doubtful accounts of $45 and $74 | | 2,176 |

| | 1,877 |

|

Settlement assets | | 20,363 |

| | 14,795 |

|

Prepaid expenses and other current assets | | 335 |

| | 360 |

|

Total current assets | | 23,372 |

| | 17,417 |

|

Property and equipment, net of accumulated depreciation of $1,588 and $1,416 | | 951 |

| | 883 |

|

Goodwill | | 17,710 |

| | 16,696 |

|

Customer relationships, net of accumulated amortization of $5,940 and $5,660 | | 2,184 |

| | 1,739 |

|

Other intangibles, net of accumulated amortization of $2,665 and $2,365 | | 1,935 |

| | 1,800 |

|

Investment in affiliates | | 1,054 |

| | 988 |

|

Other long-term assets | | 1,063 |

| | 769 |

|

Total assets | | $ | 48,269 |

| | $ | 40,292 |

|

| | | | |

LIABILITIES AND EQUITY | | |

| | |

|

Current liabilities: | | |

| | |

|

Accounts payable and accrued liabilities | | $ | 1,659 |

| | $ | 1,564 |

|

Short-term and current portion of long-term borrowings | | 1,271 |

| | 358 |

|

Settlement obligations | | 20,363 |

| | 14,795 |

|

Total current liabilities | | 23,293 |

| | 16,717 |

|

Long-term borrowings | | 17,927 |

| | 18,131 |

|

Deferred tax liabilities | | 77 |

| | 409 |

|

Other long-term liabilities | | 886 |

| | 831 |

|

Total liabilities | | 42,183 |

| | 36,088 |

|

Commitments and contingencies (See note 14) | | | | |

Redeemable noncontrolling interest | | 72 |

| | 73 |

|

First Data Corporation stockholders' equity: | | |

| | |

|

Class A Common stock, $0.01 par value; 1,600 shares authorized as of December 31, 2017 and December 31, 2016, 492 shares and 372 shares issued as of December 31, 2017 and December 31, 2016, respectively; and 482 shares and 368 shares outstanding as of December 31, 2017 and December 31, 2016, respectively | | 5 |

| | 4 |

|

Class B Common stock, $0.01 par value; 523 and 625 shares authorized as of December 31, 2017 and December 31, 2016, respectively; 443 shares and 544 shares issued and outstanding as of December 31, 2017 and December 31, 2016 respectively | | 4 |

| | 5 |

|

Preferred stock, $0.01 par value; 100 shares authorized as of December 31, 2017 and December 31, 2016 ; no shares issued and outstanding as of December 31, 2017 and December 31, 2016 | | — |

| | — |

|

Class A Treasury stock, at cost, 11 shares and 5 shares as of December 31, 2017 and December 31, 2016, respectively | | (149 | ) | | (61 | ) |

Additional paid-in capital | | 13,495 |

| | 13,210 |

|

Accumulated loss | | (9,059 | ) | | (10,524 | ) |

Accumulated other comprehensive loss | | (1,144 | ) | | (1,414 | ) |

Total First Data Corporation stockholders' equity | | 3,152 |

| | 1,220 |

|

Noncontrolling interests | | 2,862 |

| | 2,911 |

|

Total equity | | 6,014 |

| | 4,131 |

|

Total liabilities and equity | | $ | 48,269 |

| | $ | 40,292 |

|

See notes to consolidated financial statements.

FIRST DATA CORPORATION

CONSOLIDATED STATEMENTS OF CASH FLOWS |

| | | | | | | | | | | | |

| | Year ended December 31, |

(in millions) | | 2017 | | 2016 | | 2015 |

CASH FLOWS FROM OPERATING ACTIVITIES | | |

| | |

| | |

|

Net income (loss) | | $ | 1,664 |

| | $ | 660 |

| | $ | (1,268 | ) |

Adjustments to reconcile to net cash provided by operating activities: | | |

| | |

| | |

|

Depreciation and amortization (including amortization netted against equity earnings in affiliates and revenues) | | 1,073 |

| | 1,061 |

| | 1,133 |

|

Deferred income taxes | | (853 | ) | | (38 | ) | | (7 | ) |

Charges related to other operating expenses and other income | | 127 |

| | 34 |

| | 24 |

|

Loss on debt extinguishment | | 80 |

| | 70 |

| | 1,068 |

|

Stock-based compensation expense | | 245 |

| | 263 |

| | 329 |

|

Other non-cash and non-operating items, net | | 41 |

| | 45 |

| | 48 |

|

(Decrease) increase in cash, excluding the effects of acquisitions and dispositions, resulting from changes in: | | |

| | |

| | |

|

Accounts receivable, current and long term | | (196 | ) | | (81 | ) | | (184 | ) |

Other assets, current and long term | | (36 | ) | | 61 |

| | (199 | ) |

Accounts payable and other liabilities, current and long term | | (82 | ) | | 35 |

| | (162 | ) |

Income tax accounts | | (16 | ) | | 1 |

| | 13 |

|

Net cash provided by operating activities | | 2,047 |

| | 2,111 |

| | 795 |

|

CASH FLOWS FROM INVESTING ACTIVITIES | | |

| | |

| | |

|

Additions to property and equipment | | (271 | ) | | (232 | ) | | (282 | ) |

Payments to secure customer service contracts, including outlays for conversion, and capitalized systems development costs | | (247 | ) | | (245 | ) | | (320 | ) |

Acquisitions, net of cash acquired | | (1,607 | ) | | (6 | ) | | (89 | ) |

Proceeds from dispositions | | 88 |

| | 38 |

| | 4 |

|

Proceeds from the maturity of net investment hedges | | 90 |

| | — |

| | — |

|

Proceeds from sale of property and equipment | | — |

| | 38 |

| | 17 |

|

Other investing activities, net | | (5 | ) | | 46 |

| | (15 | ) |

Net cash used in investing activities | | (1,952 | ) | | (361 | ) | | (685 | ) |

CASH FLOWS FROM FINANCING ACTIVITIES | | |

| | |

| | |

|

Short-term borrowings, net | | 823 |

| | 205 |

| | (31 | ) |

Proceeds from issuance of long-term debt | | 4,968 |

| | 3,533 |

| | 10,258 |

|

Payment of call premiums and debt issuance cost | | (63 | ) | | (53 | ) | | (1,062 | ) |

Principal payments on long-term debt | | (5,409 | ) | | (5,073 | ) | | (11,568 | ) |

Payment of taxes related to net settlement of equity awards | | (94 | ) | | (61 | ) | | — |

|

Proceeds from issuance of common stock | | 50 |

| | 23 |

| | 2,718 |

|

Distributions and dividends paid to noncontrolling interests and redeemable noncontrolling interest | | (260 | ) | | (316 | ) | | (312 | ) |

Other financing activities, net | | (6 | ) | | 8 |

| | (19 | ) |

Net cash provided by (used in) financing activities | | 9 |

| | (1,734 | ) | | (16 | ) |

Effect of exchange rate changes on cash, cash equivalents and restricted cash | | 7 |

| | (34 | ) | | (23 | ) |

Change in cash, cash equivalents and restricted cash | | 111 |

| | (18 | ) | | 71 |

|

Cash, cash equivalents and restricted cash at beginning of period | | 414 |

| | 432 |

| | 361 |

|

Cash, cash equivalents and restricted cash at end of period | | $ | 525 |

| | $ | 414 |

| | $ | 432 |

|

SUPPLEMENTAL CASH FLOW INFORMATION: | | | | | | |

Income tax payments, net of refunds received | | $ | 142 |

| | $ | 118 |

| | $ | 95 |

|

Interest paid | | 916 |

| | 1,032 |

| | 1,815 |

|

Distributions received from equity method investments | | 266 |

| | 304 |

| | 289 |

|

NON-CASH TRANSACTIONS: | | | | | | |

Capital leases, net of trade-ins | | $ | 112 |

| | $ | 136 |

| | $ | 83 |

|

Other financing arrangements | | $ | 102 |

| | $ | 79 |

| | $ | — |

|

FIRST DATA CORPORATION

CONSOLIDATED STATEMENTS OF EQUITY

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | First Data Corporation Stockholders' | | | | |

| | Common Stock | | Treasury Stock | | | | | | Accumulated Other Comprehensive Income (Loss) | | | | |

(in millions) | | Class A | | Class B | | Class A | | Additional Paid-In Capital | | Accumulated Loss | | | Noncontrolling Interest | | |

| Shares | | Amount | | Shares | | Amount | | Shares | | Amount | | | | | | Total |

Balance, December 31, 2014 (a) | | — |

| | $ | — |

| | — |

| | $ | — |

| | — |

| | $ | — |

| | $ | 9,906 |

| | $ | (9,459 | ) | | $ | (1,017 | ) | | $ | 3,100 |

| | $ | 2,530 |

|

| | | | | | | | | | | | | | | | | | | | | | |

Dividends and distributions paid to noncontrolling interests (b) | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (277 | ) | | (277 | ) |

Net income (loss) (c) | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (1,481 | ) | | — |

| | 179 |

| | (1,302 | ) |

Other comprehensive loss | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (290 | ) | | (10 | ) | | (300 | ) |

Adjustments to redemption value of redeemable noncontrolling interest | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (8 | ) | | — |

| | — |

| | — |

| | (8 | ) |

Stock compensation expense and other | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 316 |

| | — |

| | — |

| | — |

| | 316 |

|

Cash dividends paid by First Data Corporation to former Parent | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (4 | ) | | — |

| | — |

| | (4 | ) |

Holding company merger (a) | | — |

| | — |

| | 719 |

| | 7 |

| | — |

| | — |

| | (20 | ) | | — |

| | — |

| | — |

| | (13 | ) |

Initial Public Offering | | 180 |

| | 2 |

| | — |

| | — |

| | — |

| | — |

| | 2,716 |

| | | | | | | | 2,718 |

|

Balance, December 31, 2015 (a) | | 180 |

| | 2 |

| | 719 |

| | 7 |

| | — |

| | — |

| | 12,910 |

| | (10,944 | ) | | (1,307 | ) | | 2,992 |

| | 3,660 |

|

| | | | | | | | | | | | | | | | | | | | | | |

Dividends and distributions paid to noncontrolling interests (b) | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (283 | ) | | (283 | ) |

Net income (loss) (c) | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 420 |

| | — |

| | 207 |

| | 627 |

|

Other comprehensive loss | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (107 | ) | | (5 | ) | | (112 | ) |

Adjustments to redemption value of redeemable noncontrolling interest | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 4 |

| | — |

| | — |

| | — |

| | 4 |

|

Stock compensation expense | | — |

| | — |

| | — |

| | — |

| | | | | | 263 |

| | — |

| | — |

| | — |

| | 263 |

|

Stock activity under stock compensation plans and other | | 188 |

| | 2 |

| | (175 | ) | | (2 | ) | | 5 |

| | (61 | ) | | 33 |

| | — |

| | — |

| | — |

| | (28 | ) |

Balance, December 31, 2016 | | 368 |

| | 4 |

| | 544 |

| | 5 |

| | 5 |

| | (61 | ) | | 13,210 |

| | (10,524 | ) | | (1,414 | ) | | 2,911 |

| | 4,131 |

|

| | | | | | | | | | | | | | | | | | | | | | |

Dividends and distributions paid to noncontrolling interests (b) | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (229 | ) | | (229 | ) |

Net income (loss) (c) | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 1,465 |

| | — |

| | 168 |

| | 1,633 |

|

Other comprehensive income | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 270 |

| | 12 |

| | 282 |

|

Adjustment to redemption value of redeemable noncontrolling interest | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 1 |

| | — |

| | — |

| | — |

| | 1 |

|

Stock compensation expense | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 245 |

| | — |

| | — |

| | — |

| | 245 |

|

Stock activity under stock compensation plans and other | | 114 |

| | 1 |

| | (101 | ) | | (1 | ) | | 6 |

| | (88 | ) | | 39 |

| | — |

| | — |

| | — |

| | (49 | ) |

Balance, December 31, 2017 | | 482 |

| | $ | 5 |

| | 443 |

| | $ | 4 |

| | 11 |

| | $ | (149 | ) | | $ | 13,495 |

| | $ | (9,059 | ) | | $ | (1,144 | ) | | $ | 2,862 |

| | $ | 6,014 |

|

| |

(a) | 1,000 shares relates to common stock without a class that was eliminated upon the merger with First Data Holdings. |

| |

(b) | The total distribution presented in the consolidated statements of equity for the years ended December 31, 2017, 2016, and 2015 excludes $31 million, $33 million, and $35 million, respectively, in distributions paid to redeemable non-controlling interest not included in equity. |

| |

(c) | The total net income (loss) presented in the consolidated statements of equity for the years ended December 31, 2017, 2016, and 2015 is $31 million different, $33 million different, and $34 million different, respectively, than the amount presented on the consolidated statements of operations due to the net income attributable to the redeemable noncontrolling interest not included in equity. |

See notes to consolidated financial statements.

FIRST DATA CORPORATION

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Note 1: Summary of Significant Accounting Policies

Business Description

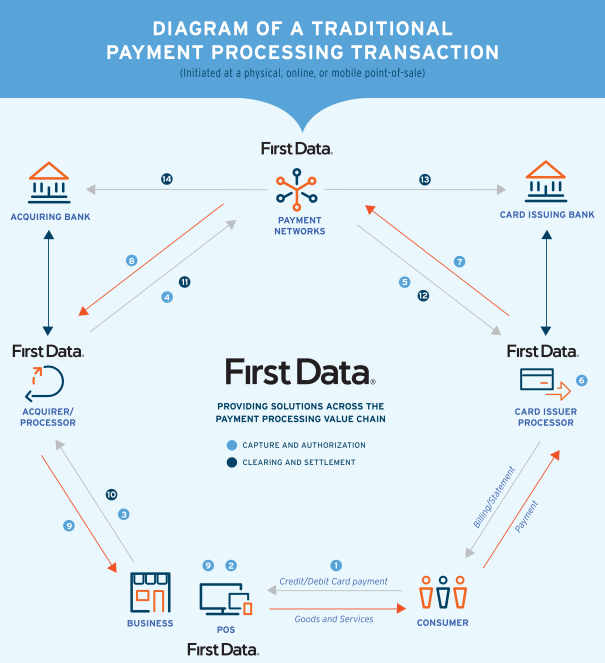

First Data Corporation (FDC or the Company) is a global leader in commerce-enabling technology and solutions for merchants, financial institutions, and card issuers. The Company provides merchant transaction processing and acquiring; credit, retail, and debit card issuing and processing; prepaid services; and check verification, settlement and guarantee services; as well as solutions to help clients grow their businesses including the Company's Clover line of payment solutions and related applications.

On October 15, 2015, the Company filed its Prospectus with the Securities and Exchange Commission pursuant to Rule 424(b). The Company issued 176,076,869 shares of Class A common stock and began trading on the New York Stock Exchange under the symbol "FDC".

On October 13, 2015, First Data Holdings Inc. (FDH), the Company's direct parent company, merged with and into First Data Corporation, with First Data Corporation being the surviving entity (HoldCo Merger). All outstanding shares of FDH were converted into Class B common stock, which are entitled to ten votes per share. All outstanding common stock of First Data Corporation were eliminated upon the merger. The Company accounted for the HoldCo Merger as a transfer of assets between entities under common control and reflected the transaction in its financial statements on a prospective basis.

On October 13, 2015, the Company amended its certificate of incorporation which affected a reverse stock split of the Company’s authorized, issued and outstanding Class B common stock, on the basis of 1 new share of Class B common stock for each 3.16091 old shares of common stock.

Consolidation

The accompanying consolidated financial statements include the accounts of the Company and its controlled subsidiaries. All significant intercompany accounts and transactions have been eliminated. Investments in unconsolidated affiliated companies are accounted for under the equity method and are included in “Investment in affiliates” in the accompanying consolidated balance sheets. The Company generally utilizes the equity method of accounting when it has an ownership interest of between 20% and 50% in an entity, provided the Company is able to exercise significant influence over the investee’s operations.

The Company consolidates an entity’s financial statements when the Company has a controlling financial interest in the entity. Control is normally established when ownership interests exceed 50% in an entity; however, when the Company does not exercise control over a majority-owned entity as a result of other investors having rights over the management and operations of the entity, the Company accounts for the entity under the equity method.

Use of Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States requires management to make estimates and assumptions that affect the amounts reported in the consolidated financial statements and accompanying notes. Actual results could differ from those estimates.

Presentation

Depreciation and amortization, presented as a separate line item on the Company’s consolidated statements of operations, does not include amortization of initial payments for new contracts which is recorded as contra-revenue within “Transaction and processing service fees.” Also not included is amortization related to equity method investments which is netted within “Equity earnings in affiliates.”

The following table presents the amounts associated with such amortization for the periods presented:

|

| | | | | | | | | | | | |

| | Year ended December 31, |

(in millions) | | 2017 | | 2016 | | 2015 |

Amortization of initial payments for new contracts | | $ | 56 |

| | $ | 65 |

| | $ | 51 |

|

Amortization related to equity method investments | | 45 |

| | 47 |

| | 60 |

|

Revenue Recognition

The majority of the Company’s revenues are comprised of: 1) volume-based fees, which typically constitute a percentage of dollar volume processed; 2) fees per transaction processed; 3) fees per account on file during the period; or 4) some combination thereof.

The Company’s arrangements with clients often consist of multiple services and products (multiple-element arrangements). In accounting for multiple-element arrangements, the Company assesses the elements of the contract and whether each element has standalone value and allocates revenue to the various elements based on their estimated selling price as a component of total consideration for the arrangement. The selling price is based on current selling prices offered by the Company or another party for current products or management's best estimate of a selling price.

Revenue is comprised of fees charged to the client, net of interchange fees and assessments charged by the credit card associations, and is recognized at the time the client accepts a point of sale transaction. The fees charged to the client are a percentage of the credit card and debit card transaction’s dollar value, a fixed amount, or a combination of the two. Personal identification number based debit (PIN-debit) and PINless-debit network fees are recognized in “Reimbursable debit network fees, postage, and other” revenues and expenses in the consolidated statements of operations.

Interchange fees and assessments charged by credit card associations to the Company’s consolidated subsidiaries and network fees related to PIN-debit and PINless-debit transactions charged by debit networks were as follows for the periods presented:

|

| | | | | | | | | | | | |

| Year ended December 31, |

(in millions) | | 2017 | | 2016 | | 2015 |

Interchange fees and assessments | | $ | 26,069 |

| | $ | 23,810 |

| | $ | 21,711 |

|

Debit network fees | | 3,227 |

| | 3,121 |

| | 2,991 |

|

The Company charges processing fees to its alliances. In situations where an alliance is accounted for under the equity method, the Company’s consolidated revenues include the processing fees charged to the alliance, as presented in the consolidated statements of operations within "Transaction and processing service fees".

Revenue from check verification, settlement, and guarantee services is recognized at the time of sale less the fair value of the guarantee. The fair value of the guarantee is deferred and recognized at the later of the Company being called upon to honor the guarantee or the expiration of the guarantee. Check verification fees generally are a fixed amount per transaction while check guarantee fees generally are a percentage of the check amount.

The purchase and sale of merchant contract portfolios is an ordinary element of the Company’s businesses, and therefore, the gains from selling these revenue-generating assets are included within “Product sales and other” in the consolidated statements of operations.

Fees based on cardholder accounts on file are recognized as the requisite services or period occurs. Fees for PIN-debit transactions where the Company is the debit card processor for the financial institution are recognized on a per transaction basis. Revenues for output services are derived primarily on a per piece basis and consist of fees for the production, materials, and postage related to mailing finished products and recognized as the services are provided.

The sale and leasing of POS devices (terminals) are reported in “Product sales and other” in the consolidated statements of operations. Revenue for terminals sold or sold under a sales-type lease transaction is recognized when the following four criteria are met: evidence of an agreement exists, delivery has occurred, the selling price or minimum lease payments are fixed or determinable, and collection of the selling price or minimum lease payments is reasonably assured. Revenue for operating leases is recognized on a straight-line basis over the lease term.

Services not specifically described above are generally transaction based fees that are recognized at the time the transactions are processed or programming services that are either recorded as work is performed or are recognized over the life of the contract depending on the underlying business relationship.

Deferred Revenue

The Company records deferred revenue when it receives payments or invoices in advance of the delivery of products or the performance of services. The deferred revenue is recognized when underlying performance obligations are achieved. As of December 31, 2017 and 2016, current deferred revenue included within "Accounts payable and accrued liabilities" in the Company's consolidated balance sheets was $175 million and $149 million, respectively. As of December 31, 2017 and 2016, noncurrent deferred revenue included within "Other long-term liabilities" in the Company's consolidated balance sheets was $177 million and $184 million, respectively.

In January 2017, the Company determined that standalone value had been achieved for its Clover terminal devices, principally because a secondary market had been established. The Company accounted for the change on a prospective basis. Beginning January 1, 2017, the Company recognized revenue on sales of Clover terminal devices upon delivery, while Clover terminal devices sold prior to January 1, 2017 continued to be deferred over the term of the respective processing agreement. As of December 31, 2017, $36 million of the Company's deferred revenue represented sales of Clover terminal devices which did not have standalone value prior to the change in accounting.

Stock-Based Compensation

Stock-based compensation to employees is measured at the grant date fair values of the respective stock options and restricted stock awards. An estimate of forfeitures is applied when calculating compensation expense. To calculate the estimated forfeiture rate, the Company performed an analysis of all forfeitures over a five year period and continues to evaluate the actual forfeit rate compared to its estimate. The estimated forfeiture rate will be adjusted as actual forfeiture vary from the estimate, resulting in the recognition of compensation cost only for awards that vest. Any effect of a change in estimated forfeitures will be recognized through a cumulative catch-up adjustment. The Company recognizes compensation cost on service based awards with graded vesting on a straight-line basis over the requisite service period for the entire award. The Company recognizes compensation cost on performance-based restricted stock grants on a grant basis graded schedule. Refer to note 4 "Stock Compensation Plans" of these consolidated financial statements for details regarding the Company’s stock-based compensation plan.

Treasury Stock

In connection with the vesting of restricted stock awards or exercise of stock options, shares of Class A and Class B common stock are delivered to the Company by employees to satisfy tax withholding obligations. The Company accounts for treasury stock activities under the cost method whereby the cost of the acquired stock is recorded as treasury stock. Because Class B common stock converts automatically to Class A common stock upon any transfer, whether or not for value, except for certain transactions described in the Company's amended and restated certificate of incorporation, all shares of treasury stock reside as Class A.

Foreign Currency Translation

The U.S. dollar is the functional currency of the Company’s U.S.-based businesses and certain foreign-based businesses. Significant operations with a local currency as their functional currency include operations in the United Kingdom, Australia, Germany, Ireland, Greece, Brazil and Argentina. Foreign currency-denominated assets and liabilities for these units and other less significant operations are translated into U.S. dollars based on exchange rates prevailing at the end of the period, and revenues and expenses are translated at average exchange rates during each monthly period. The effects of foreign exchange gains and losses arising from the translation of assets and liabilities of those entities where the functional currency is not the U.S. dollar are included as a component of Other Comprehensive Income (Loss) (OCI). Intercompany loans are generally not considered invested on a long-term basis and such foreign currency gains and losses are included in "Other income" on the consolidated statements of operations. Transaction gains and losses related to operating assets and liabilities are included in “Cost of services” and “Selling, general, and administrative” in the consolidated statements of operations and were immaterial for all periods presented. Non-operating transaction gains and losses derived from non-operating assets and liabilities are included in “Other income” on the consolidated statements of operations and are separately disclosed in note 16 "Supplemental Financial Information" of these consolidated financial statements.

Derivative Financial Instruments

The Company is exposed to various financial and market risks, including those related to changes in interest rates and foreign currency exchange rates, that exist as part of its ongoing business operations. The Company uses derivative instruments (i) to mitigate cash flow risks with respect to changes in interest rates (forecasted interest payments on variable rate debt), (ii) to maintain a desired ratio of fixed rate and floating rate debt, and (iii) to protect the net investment in certain foreign subsidiaries and/or affiliates with respect to changes in foreign currency exchange rates. The Company’s objective is to engage in risk management strategies that provide adequate downside protection.

Derivative instruments are entered into for periods consistent with related underlying exposures. The Company applies strict policies to manage each of these risks, including prohibition against derivatives trading, derivatives market-making or any other speculative activities.

The Company formally documents all relationships between hedging instruments and the underlying hedged items, as well as its risk management objective and strategy for undertaking various hedge transactions. This process includes linking all derivatives that have been designated as cash flow hedges to forecasted transactions and net investment hedges to the underlying investment in a foreign subsidiary or affiliate. For designated hedges, the Company formally assesses, both at inception of the hedge and on an ongoing basis, whether the hedge is highly effective in offsetting changes in cash flows or foreign currency exposure of the underlying hedged items. The Company also performs an assessment of the probability of the forecasted transactions on a periodic basis. If it is determined that a derivative ceases to be highly effective during the term of the hedge or if the forecasted transaction is no longer probable, the Company discontinues hedge accounting prospectively for such derivative.

The Company monitors the financial stability of its derivative counterparties and all counterparties are investment grade. The credit risk inherent in these agreements represents the possibility that a loss may occur from the nonperformance of a counterparty to the agreements. The Company performs a review at inception of the hedge, as circumstances warrant, and at least on a quarterly basis, of the credit risk of these counterparties. The Company also monitors the concentration of its contracts with individual counterparties. The Company’s exposures are in liquid currencies (primarily in U.S. dollars, euros, Australian dollars, British pounds, and Canadian dollars), so there is minimal risk that appropriate derivatives to maintain the hedging program would not be available in the future.

The Company recognizes all derivative financial instruments in the consolidated balance sheets as assets or liabilities at fair value. Such amounts are recorded in “Other current assets”, “Other long-term assets”, “Accounts payable and accrued liabilities” or “Other long-term liabilities” in the consolidated balance sheets. The Company’s policy is to present all derivative balances on a gross basis, without regard to counterparty master netting agreements or similar arrangements. Changes in fair value of derivative instruments are recognized immediately in "Other income" on the consolidated statements of operations unless the derivative is designated and qualifies as a hedge of future cash flows or a hedge of a net investment in a foreign operation. For derivatives that qualify as hedges of future cash flows, the effective portion of changes in fair value is recorded temporarily in equity as a component of OCI and then recognized in "Other income" in the consolidated statements of operations in the same period or periods during which the hedged item affects earnings. For derivatives that qualify as a hedge of a net investment in a foreign operation, the gain or loss is reported in OCI as part of the cumulative translation adjustment to the extent the hedge is effective. Any ineffective portions of cash flow hedges and net investment hedges are recognized in “Other income” in the consolidated statements of operations during the period of change. Additional discussion of derivative instruments is provided in note 13 "Derivative Financial Instruments" of these consolidated financial statements.

Noncontrolling and Redeemable Noncontrolling Interests

Noncontrolling interests represent the minority shareholders’ share of the net income or loss and equity in consolidated subsidiaries. The Company’s noncontrolling interests are presented pretax in the consolidated statements of operations as “Net income attributable to noncontrolling interests and redeemable noncontrolling interest” because the majority of the Company’s non wholly owned consolidated subsidiaries are flow through entities for tax purposes. Noncontrolling interests are presented as a component of equity in the consolidated balance sheets and reflect the original investments by these noncontrolling shareholders in the consolidated subsidiaries, along with their proportionate share of the earnings or losses of the subsidiaries, net of dividends or distributions. Noncontrolling interests that are redeemable at the option of the holder are presented outside of equity and are carried at their estimated redemption value. Refer to note 5 "Stockholders' Equity and Redeemable Noncontrolling Interest" of these consolidated financial statements for more information. A noncontrolling interest is recorded on the date of acquisition based on the total fair value of the acquired entity and the noncontrolling interest’s share of that value.

Reserve for Merchant Credit Losses and Check Guarantees

With respect to the merchant acquiring business, the Company’s merchant customers (or those of its unconsolidated alliances) have the legal obligation to refund any charges properly reversed by the cardholder. In the event, however, that the Company is not able to collect such amounts from the merchants, the Company may be liable for any such reversed charges. The Company’s risk in this area primarily relates to situations where the cardholder has purchased goods or services to be delivered in the future.

The Company’s obligation to perform is minimal in relation to the total dollar volume processed. The Company requires cash deposits, guarantees, letters of credit or other types of collateral from certain merchants to minimize this obligation. Collateral held by the Company is classified within “Settlement assets” and the obligation to repay the collateral if it is not needed is classified within “Settlement obligations” on the Company’s consolidated balance sheets. The Company also utilizes a number of systems and procedures to manage merchant risk. Despite these efforts, the Company historically has experienced some level of losses due to merchant defaults. The amount of deposits and letters of credit held by the Company was $632 million and $628 million as of December 31, 2017 and 2016, respectively.

The Company’s contingent obligation relates to imprecision in its estimates of required collateral. A provision for this obligation is recorded based primarily on historical experience of credit losses and other relevant factors such as economic downturns or increases in merchant fraud. Merchant credit losses are included in “Cost of services” in the Company’s consolidated statements of operations. The amount of the reserves attributable to entities consolidated by the Company was $29 million and $23 million as of December 31, 2017 and 2016, respectively.

The majority of the TeleCheck business involves the guarantee of checks received by merchants. If the check is returned, TeleCheck is required to purchase the check from the merchant at its face value and pursue collection from the check writer. A provision for estimated check returns, net of anticipated recoveries, is recorded at the transaction inception based on recent history. The following table presents the estimate of losses on returned check and the fair value of check guarantees:

|

| | | | | | | | |

| | As of December 31, |

(in millions) | | 2017 | | 2016 |

Estimate of losses on returned checks | | $ | 4 |

| | $ | 5 |

|

Fair value of checks guaranteed | | 14 |

| | 17 |

|

The estimate of losses on returned checks is included in “Accounts payable and accrued liabilities” and the fair value of checks guaranteed is included in “Accounts receivable, net” in the consolidated balance sheets. The maximum potential future payments under the guarantees were approximately $456 million as of December 31, 2017 which represented an estimate of the total uncleared checks at that time.

Income Taxes

The Company and its domestic subsidiaries file a consolidated U.S. income tax return. The Company’s foreign operations file income tax returns in their local jurisdictions. Income taxes reflect the net tax effects of temporary differences between the financial reporting carrying amounts of assets and liabilities and the corresponding income tax amounts. The Company has deferred tax assets and liabilities and maintains valuation allowances where it is more likely than not that all or a portion of deferred tax assets will not be realized. To the extent the Company determines that it will not realize the benefit of some or all of its deferred tax assets, these deferred tax assets will be adjusted through the Company’s provision for income taxes in the period in which this determination is made.

The Company recognizes the tax benefits from uncertain tax positions only when it is more likely than not, based on the technical merits of the position, that the tax position will be sustained upon examination, including the resolution of any related appeals or litigation. The tax benefits recognized in the consolidated financial statements from such a position are measured as the largest benefit that has a greater than fifty percent likelihood of being realized upon ultimate resolution.

Cash and Cash Equivalents

Investments (other than those included in settlement assets) with original maturities of three months or less (that are readily convertible to cash) are considered to be cash equivalents and are stated at cost, which approximates market value. Cash and cash equivalents that were restricted from use due to regulatory requirements are included in “Other long-term assets” in the consolidated balance sheets and was $27 million and $30 million as of December 31, 2017 and 2016, respectively.

Accounts Receivable and Leasing Receivables

Accounts receivable balances are stated net of allowance for doubtful accounts. The Company records allowances for doubtful accounts when it is probable that the accounts receivable balance will not be collected. Long-term accounts receivable balances are included in “Other long-term assets” in the consolidated balance sheets.

The Company has receivables associated with its POS terminal leasing businesses. Leasing receivables are included in “Accounts receivable” and “Other long-term assets” in the consolidated balance sheets. The Company recognizes interest income on its leasing receivables using the effective interest method. Interest income from leasing receivables is included in “Product sales and other” in the consolidated statements of operations. For direct financing leases, the interest rate used incorporates initial direct costs included in the net investment in the lease. For sales type leases, initial direct costs are expensed as incurred.

Property and Equipment

Property and equipment are stated at cost less accumulated depreciation. Depreciation expense is computed using the straight-line method over the lesser of the estimated useful life of the related assets (generally three years to 10 years for equipment, furniture, and leasehold improvements, and 30 years for buildings) or the lease term. Maintenance and repairs which do not extend the useful life of the respective assets are expensed as incurred.

The following table presents depreciation expense related to property and equipment, including equipment under capital lease:

|

| | | | |

Year ended December 31, | | |

(in millions) | | Amount |

2017 | | $ | 321 |

|

2016 | | 300 |

|

2015 | | 290 |

|

Goodwill and Other Intangibles

Goodwill represents the excess of purchase price over tangible and intangible assets acquired less liabilities assumed arising from business combinations. Goodwill is generally allocated to reporting units based upon relative fair value (taking into consideration other factors such as synergies) when an acquired business is integrated into multiple reporting units. The Company’s reporting units are at the operating segment level or one level below the operating segment level for which discrete financial information is prepared and regularly reviewed by management. When a business within a reporting unit is disposed of, goodwill is allocated to the disposed business using the relative fair value method. Relative fair value is estimated using a discounted cash flow analysis.

The Company tests goodwill annually for impairment, as well as upon an indicator of impairment, at the reporting unit level. The Company performed its annual goodwill impairment test in the fourth quarters of 2017 and 2016. As of October 1, 2017, the most recent impairment analysis date, the fair value of each reporting unit exceeded its carrying value. The Company did not record any goodwill impairment charges in 2017, 2016, and 2015.

Customer relationships represent the estimated value of the Company’s relationships with customers, primarily merchants and financial institutions, to which it provides services. Customer relationships are amortized based on the pattern of undiscounted cash flows for the period as a percentage of total projected undiscounted cash flows. The Company selected this amortization method for these customer relationships based on a conclusion that the projected undiscounted cash flows could be reliably determined.

The Company capitalizes initial payments for new contracts, contract renewals, and conversion costs associated with customer processing relationships to the extent recoverable through cash flows from future operations, contractual minimums, and/or penalties in the case of early termination. The Company’s accounting policy is to limit the amount of capitalized costs for a given contract to the lesser of the estimated ongoing future cash flows from the contract or the termination fees the Company would receive in the event of early termination of the contract by the customer. The initial payments for new contracts and contract renewals are amortized over the term of the contract as a reduction of the associated revenue (transaction and processing service fees). Conversion costs are also amortized over the term of the contract but are recorded as an expense in “Depreciation and amortization” in the consolidated statements of operations.

The Company develops software that is used in providing processing services to customers. To a lesser extent, the Company also develops software to be sold or licensed to customers. Costs incurred during the preliminary project stage are expensed as incurred.

Capitalization of costs begins when the preliminary project stage is completed and management, with the relevant authority, authorizes and commits to funding the project and it is probable that the project will be completed and the software will be used to perform the function intended. Capitalization of costs ceases when the software is substantially complete and ready for its intended use. Software development costs are amortized using the straight-line method over the estimated useful life of the software, which is generally 5 years. Software acquired in connection with business combinations is amortized using the straight-line method over the estimated useful life of the software which generally ranges from three years to 10 years.

In addition to capitalized contract and software development costs, other intangibles include copyrights, patents, purchased software, and trademarks acquired in business combinations. Other intangibles, except for the First Data trade name discussed in note 3 “Goodwill and Other Intangibles” of these consolidated financial statements, are amortized on a straight-line basis over the length of the contract or benefit period, which generally ranges from three years to 25 years.

Assets and Liabilities Measured at Fair Value on a Recurring Basis

Fair value is defined by accounting guidance as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The Company uses the hierarchy prescribed in the accounting guidance for fair value measurements, based upon the available inputs to the valuation and the degree to which they are observable or not observable in the market. The Company maximizes the use of relevant observable inputs and minimizes the use of unobservable inputs. The three levels in the hierarchy are as follows:

| |

• | Level 1 Inputs—Quoted prices (unadjusted) for identical assets or liabilities in active markets that are accessible as of the measurement date. |

| |

• | Level 2 Inputs—Inputs other than quoted prices within Level 1 that are observable either directly or indirectly, including but not limited to quoted prices in markets that are not active, quoted prices in active markets for similar assets or liabilities, and observable inputs other than quoted prices such as interest rates or yield curves. |

| |

• | Level 3 Inputs—Unobservable inputs reflecting the Company’s own assumptions about the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk. |

Assets and Liabilities Measured at Fair Value on a Non-Recurring Basis

During the years ended December 31, 2017 and 2016, the Company did not record any adjustments over $5 million to the carrying value of existing assets based on non-recurring fair value measurements, other than as discussed in note 10 "Other Operating Expenses."

Net Income (Loss) Per Share

Basic net income (loss) per share is calculated by dividing Net income (loss) attributable to First Data Corporation by the weighted-average shares outstanding during the period, without consideration for any potential dilutive shares. Diluted net income (loss) per share is computed by dividing Net income (loss) attributable to First Data Corporation by the weighted-average number of shares of common stock outstanding during the period increased to include the number of additional shares of common stock that would have been outstanding if the potentially dilutive securities had been issued. Potentially dilutive securities include outstanding stock options, unvested restricted stock and unvested restricted stock awards. The dilutive effect of potentially dilutive securities is reflected in diluted net income per share by application of the treasury stock method. Under the treasury stock method, an increase in the fair market value of the Company’s common stock can result in a greater dilutive effect from potentially dilutive securities. For any period where Net income (loss) attributable to First Data Corporation is presented, shares used in the diluted net income per share calculation represent basic shares because using diluted shares would be anti-dilutive.

Reclassifications

Certain amounts for prior years have been reclassified to conform with the current year financial statement presentation. During 2017, the Company revised its financial statements to reflect immaterial adjustments to its accounting for deferred income taxes. In the periods prior to 2015, the Company had incorrectly recorded deferred income tax assets on foreign currency translation adjustments included in other comprehensive income (loss) which the Company provided a full valuation. The adjustment resulted in a decrease of $88 million to the previously reported balances of "Accumulated Loss" and an offsetting increase to "Accumulated Other Comprehensive Income (Loss)" at December 31, 2014, and a reduction to deferred tax assets and related valuation allowance of $124 million at December 31, 2016. Additionally, the consolidated balance sheet as of December 31, 2016 reflects a $102 million reclassification related to settlement activities to conform certain domestic and international businesses to the Company's

global policies, which increased "Cash and cash equivalents" and decreased "Accounts receivable". The consolidated statements of cash flows for the year ended December 31, 2016 reflects the reclassification of $102 million within “Net cash provided by operating activities”.

New Accounting Guidance

Revenue Recognition

In May 2014, the Financial Accounting Standards Board (FASB) issued guidance that requires companies to recognize revenue to depict the transfer of goods or services to customers in amounts that reflect the consideration to which the Company expects to be entitled in an exchange for those goods or services. It also requires enhanced disclosures about revenue, provides guidance for transactions that were not previously addressed comprehensively, and improves guidance for multiple-element arrangements. The FASB has subsequently issued several amendments to the standard, including clarification on accounting for licenses, identifying performance obligations, and principal versus agent consideration (reporting revenue gross vs. net).

Since the issuance of ASC 606 and ASC 340-40 (collectively, the New Revenue Standard) in May 2014, the Company has been preparing for the adoption of the New Revenue Standard. The Company has been monitoring the activity of the FASB and the Transition Resource Group as it relates to specific industry interpretive guidance and further overall interpretations and clarifications. The Company has completed two phases of its three-phase plan to-adopt and implement of the New Revenue Standard. Phase III has begun and includes activities such as running parallel reporting for impacted areas under the New and Current Revenue Standard (ASC 605), recording the accounting adjustments that were identified in Phase II, and revising the Company’s financial statement disclosures. This final phase will be completed during Q1 2018.

The Company adopted the New Revenue Standard using a modified retrospective basis on January 1, 2018. The Company expects the adoption to result in a cumulative adjustment to retained earnings of less than $100 million to apply the New Revenue Standard. This impact was principally driven by certain software arrangements being recognized sooner; changes related to costs to obtain customers, including the related amortization period; and the release of deferred revenue associated with Clover terminals that had previously lacked standalone value. Under the modified retrospective basis, the Company will not restate the prior consolidated financial statements presented for these effects.

The Company currently expects the most significant ongoing impact of adopting the New Revenue Standard in 2018 to be driven by changes in principal versus agent considerations, with the majority of the change overall in total revenues attributable to FDC reflecting our PIN-debit and PINless debit transactions on a net basis prospectively, as opposed to our gross presentation of $3.2 billion in 2017. The Company does not expect the adoption of the New Revenue Standard to have a material impact on net income. The Company will include additional disclosures of the amount by which each financial statement line item is affected during 2018, as compared to the guidance that was in effect before the change, and an explanation of the reasons for significant changes.

Leases

In February 2016, the FASB issued guidance which requires lessees to put most leases on their balance sheets. The guidance also modifies the classification criteria and the accounting for sales-type and direct financing leases for lessors and provides new presentation and disclosure requirements for both lessees and lessors. The standard is effective for financial statements issued for fiscal years beginning after December 15, 2018, and interim periods within those fiscal years. Early adoption is permitted in any interim or annual period subsequent to adoption of the preceding revenue recognition guidance. The Company is currently evaluating the impact of adoption of the new guidance on its consolidated financial statements.

Stock-based Compensation

In March 2016, the FASB issued guidance that will change some aspects of the accounting for stock-based payments to employees. Under the new guidance, companies will be required to record all excess tax benefits and tax deficiencies as income tax expense or benefit in the income statement and to present excess tax benefits as an operating activity on the statement of cash flows. The guidance may also change how companies account for forfeitures and an employee’s use of shares to satisfy the employer’s statutory income tax withholding obligation. The Company adopted the various amendments in its consolidated financial statements for the quarterly period ending March 31, 2017 with an effective date on January 1, 2017. The Company has elected to continue to estimate forfeitures expected to occur to determine the amount of compensation cost to be recognized in each period. The adoption of these amendments did not have a material effect on its consolidated financial statements as the Company still had income tax valuation allowances within the U.S. The Company released its U.S. valuation allowances in the fourth quarter of 2017 and as a result the Company could experience volatility in its income tax expense.

In May 2017, the FASB issued guidance that will clarify when changes to terms or conditions of a stock-based payment award must be accounted for as a modification. Under the new guidance, companies will only apply modification accounting guidance if the value, vesting conditions or classification of an award changes. This new guidance will be effective for fiscal years beginning after December 15, 2017 for all entities, including interim periods within those fiscal years with early adoption permitted. The guidance is adopted prospectively to awards modified on or after the adoption date. The Company will adopt the new guidance on January 1, 2018. The impact of adoption on the Company's consolidated financial statements is dependent on future changes to share-based compensation awards.

Credit Losses

In June 2016, the FASB issued guidance that will change the accounting for credit impairment. Under the new guidance, companies are required to measure all expected credit losses for financial instruments held at the reporting date based on historical experience, current conditions and reasonable supportable forecasts. This replaces the existing incurred loss model and is applicable to the measurement of credit losses on financial assets measured at amortized cost and applies to some off-balance sheet credit exposures. This new guidance will be effective for public companies for fiscal years beginning after December 15, 2019, including interim periods within those fiscal years. Early adoption is permitted for fiscal years beginning after December 15, 2018. The Company is currently evaluating the impact of the new guidance on its consolidated financial statements.

Statement of Cash Flows

In November 2016, the FASB issued guidance that will change the presentation of restricted cash and restricted cash equivalents on the statement of cash flows. Under the new guidance, companies will be required to include restricted cash and restricted cash equivalents with the cash and cash equivalents line item when reconciling beginning-of-period and end-of-period total amounts shown on the statement of cash flows. Given this change, transfers between cash, cash equivalents, and restricted cash and cash equivalents will not be reported as cash flow activities on the statement of cash flows. In addition, the guidance requires entities to disclose information about the nature of restrictions on its cash and cash equivalents, including restricted cash and cash equivalents. The Company adopted the new guidance on January 1, 2018, using a retrospective approach, with no material impact to its statement of cash flows. The adoption of this standard has been reflected in all periods within these financial statements. The Company held restricted cash within "Other long-term assets" of $27 million, $30 million, and $3 million for the years ended December 31, 2017, 2016 and 2015, respectively.

Goodwill

In January 2017, the FASB issued guidance simplifying the test for goodwill impairment. This standard eliminates Step 2 from the goodwill impairment test, instead requiring an entity to recognize a goodwill impairment charge for the amount by which the goodwill carrying amount exceeds the reporting unit’s fair value. This guidance is effective for interim and annual goodwill impairment tests in fiscal years beginning after December 15, 2019, and early adoption is permitted. This guidance must be applied on a prospective basis. The Company adopted the new guidance during the fourth quarter of 2017 with no impact to its consolidated financial statements.

Pension Costs

In March 2017, the FASB issued guidance that requires employers that sponsor defined benefit plans for pensions and/or other post-retirement benefits to present the service cost component of net periodic benefit cost in the same income statement line item as other employee compensation costs arising from services rendered during the period. Only the service cost component will be eligible for capitalization in assets. Employers will present the other components of the net periodic benefit cost separately from the line item that includes the service cost and outside of any subtotal of operating income, if one is presented. The Company adopted the new guidance on January 1, 2018, using a retrospective approach. The adoption of this standard has been reflected in all periods within these financial statements. The impact on the Company's financial statements for the years ended December 31, 2017, 2016 and 2015 was an increase (decrease) in operating expense and a decrease (increase) in "Interest expense, net" of $6 million, ($10) million, and $3 million, respectively.

Derivatives and Hedging

In August 2017, the FASB issued guidance to simplify the current application of hedge accounting. This standard is intended to better align a company’s risk management strategies and financial reporting for hedging relationships through changes to both designation and measurement for qualifying hedging relationships and more accurately presenting the economic effects in the financial statements. In addition, the new guidance establishes flexibility in the requirements to qualify and maintain hedge accounting. This guidance is effective for fiscal years beginning after December 15, 2018 and for interim periods therein, with

early adoption permitted. The Company will adopt the new guidance on January 1, 2018. The Company does not expect the adoption of this guidance to have a material impact on the Company’s consolidated financial statements.

Note 2: Borrowings

|

| | | | | | | | |

| | As of December 31, |

(in millions) | | 2017 | | 2016 |

Short-term borrowings: | | |

| | |

|

Foreign lines of credit and other arrangements | | $ | 205 |

| | $ | 84 |

|

Senior Secured Revolving Credit Facility June 2, 2020 at LIBOR plus 3.50% or a base rate plus 2.50% | | 272 |

| | — |

|

Receivable securitized loan at LIBOR plus 1.5% or a base rate equal to the highest of (i) the applicable lender's prime rate, or (ii) the federal funds rate plus 0.50% | | 600 |

| | 160 |

|

Unamortized deferred financing costs(a) | | (3 | ) | | (2 | ) |

Total short-term borrowings | | 1,074 |

| | 242 |

|

Current portion of long-term borrowings: | | | | |

|

Senior secured term loan facility due June 2020 at LIBOR plus 1.75% or a base rate plus 0.75% | | 78 |

| | — |

|

Other arrangements and capital lease obligations | | 119 |

| | 116 |

|

Total current portion of long-term borrowings | | 197 |

| | 116 |

|

Total short-term and current portion of long-term borrowings | | 1,271 |

| | 358 |

|

Long-term borrowings: | | | | |

|

Senior secured term loan facility due April 2024 at LIBOR plus 2.25% or a base rate plus 1.25% | | 3,892 |

| | — |

|

Senior secured term loan facility due July 2022 at LIBOR plus 2.25% or a base rate plus 1.25% | | 3,758 |

| | — |

|

Senior secured term loan facility due June 2020 at LIBOR plus 1.75% or a base rate plus 0.75% | | 1,404 |

| | — |

|

Senior secured term loan facility due March 2021 at LIBOR and euro LIBOR plus 3.0% or, solely with respect to U.S. dollar-denominated term loans, a base rate plus 2.0% | | — |

| | 4,379 |

|

Senior secured term loan facility due July 2022 at LIBOR plus 3.0% or a base rate plus 2.0%, or solely with respect to euro-denominated term loans, euro LIBOR plus 3.25% | | — |

| | 3,583 |

|

6.75% Senior secured first lien notes due 2020 | | — |

| | 1,398 |

|

5.375% Senior secured first lien notes due 2023 | | 1,210 |

| | 1,210 |

|

5.0% Senior secured first lien notes due 2024 | | 1,900 |

| | 1,900 |

|

5.75% Senior secured second lien notes due 2024 | | 2,200 |

| | 2,200 |

|

7.0% Senior unsecured notes due 2023 | | 3,400 |

| | 3,400 |

|

Unamortized discount and unamortized deferred financing costs (a) | | (123 | ) | | (154 | ) |

Other arrangements and capital lease obligations | | 286 |

| | 215 |

|

Total long-term borrowings (b) | | 17,927 |

| | 18,131 |

|

Total borrowings (c) | | $ | 19,198 |

| | $ | 18,489 |

|

| |

(a) | Unamortized deferred financing costs and certain lenders' fees associated with debt transactions were capitalized as discounts are amortized on a straight-line basis, which approximates the effective interest method, over the remaining term of the respective debt. |

| |

(b) | As of December 31, 2017 and 2016, the fair value of the Company's long-term borrowings was $18.2 billion and $18.8 billion, respectively. The estimated fair value of the Company's long-term borrowings was primarily based on market trading prices and is considered to be a Level 2 measurement. |

| |

(c) | The effective interest rate is not substantially different than the coupon rate on any of the Company's debt tranches. |

Foreign Lines of Credit and Other Arrangements

As of December 31, 2017 and 2016, the Company had $546 million and $489 million, respectively, available under short-term lines of credit and other arrangements with foreign banks and alliance partners primarily to fund settlement activity. As of December 31, 2017 and 2016, this includes a $355 million committed line of credit for one of the Company's consolidated alliances. The remainder of these arrangements are primarily associated with international operations and are in various functional currencies, the most significant of which are the Australian dollar, the Polish zloty, and the euro. Of the amounts outstanding as of December 31, 2017 and 2016, $15 million and $10 million, respectively, were uncommitted. The weighted-average interest rate associated with foreign lines of credit was 2.9% and 2.6% for the years ended December 31, 2017 and 2016, respectively.

Senior Secured Revolving Credit Facility

The Company has a $1.25 billion senior secured revolving credit facility maturing on June 2, 2020. Up to $250 million of the senior secured revolving credit facility is available for letters of credit, of which $29 million and $41 million of letters of credit were issued under the facilities as of December 31, 2017 and 2016, respectively. As of December 31, 2017, $949 million remained available. Interest on the senior secured revolving credit facility is payable at a rate equal to, at Company’s option, either (a) LIBOR for deposits in the applicable currency plus 3.50% or (b) solely with respect to revolving loans denominated in U.S. dollars, a base rate plus 2.50%. The weighted-average interest rate on these facilities was 5.74% and 4.60% for the years ended December 31, 2017 and 2016, respectively. The commitment fee rate for the unused portion of the facility is 0.50% per year, though it may be reduced by the Company’s leverage ratio.

Receivable Securitization Agreement

The Company has a consolidated wholly-owned subsidiary, First Data Receivables, LLC (FDR). FDR and FDC entered into an agreement where certain wholly owned subsidiaries of FDC agreed to transfer and contribute receivables to FDR. FDR’s assets are not available to satisfy obligations of any other entities or affiliates of FDC. FDR's creditors will be entitled, upon its liquidation, to be satisfied out of FDR’s assets prior to any assets or value in FDR becoming available to FDR’s equity holders. As of December 31, 2017, the Company transferred $748 million in receivables to FDR as part of the securitization program and FDR utilized the receivables as collateral in borrowings of $600 million. As of December 31, 2017, the receivables held by FDR are recorded within “Accounts receivable, net” in the Company’s consolidated balance sheets. The weighted-average interest rate on the securitization facility was 2.8% for the year ended December 31, 2017.

Senior Unsecured Revolving Credit Facility

On December 14, 2017 the Company executed a $33 million senior unsecured revolving credit facility maturing December 20, 2019, available for letters of credit. The interest rate associated with the credit facility was 1.85% for the year ended December 31, 2017.

Senior Secured Term Loan Facility

The original terms of the Company’s senior secured term loan facilities required the Company to pay equal quarterly installments in aggregate annual amounts equal to 1% of the original principal amount. However, in conjunction with debt modifications and amendments over the last several years, proceeds from the issuance of the notes were used to prepay portions of the principal balances of the Company’s senior secured term loans which satisfied the future quarterly principal payments. Therefore, the Company made no scheduled principal payments during 2017 or 2016, for the senior secured term loan facility other than $70 million related to June 2020 senior secured term loan facility. The senior secured term loan facilities also require mandatory prepayments based on a percentage of excess cash flow generated by the Company if the Company does not satisfy the leverage ratio. All obligations under the senior secured loan facilities are fully and unconditionally guaranteed by most of the domestic, wholly owned material subsidiaries of the Company, subject to certain exceptions.

Senior Secured Term Loan Facility Due June 2020

On January 23, 2017, the Company incurred an aggregate principal amount of $1.3 billion in new U.S. dollar denominated term loans maturing on June 2, 2020. The interest rate applicable to the new term loans is either LIBOR plus 1.75% or a base rate plus 0.75%. The Company is required to make quarterly principal payments of 1.25% on the new term loans. The new term loans were utilized to pay down a portion of the existing 6.75% senior secured first lien notes. In connection with this transaction, the Company expensed $56 million in loss on debt extinguishment. In November 2017, the Company incurred additional debt of $250 million against this facility to partially fund the purchase of BluePay. The Company made principal payments of $70 million in 2017.

Senior Secured Term Loan Facility Due April 2024

On November 15, 2017, the Company refinanced approximately $3.9 billion of U.S. dollar-denominated senior secured term loans maturing on April 2024. The interest rate applicable to the new loan is either LIBOR plus 2.25% or a base rate plus 1.25%. The proceeds were utilized to pay down the existing March 2021 term loan facility. In connection with this transaction, the Company expensed $9 million in loss on debt extinguishment.

Senior Secured Term Loan Facility Due July 2022

On June 14, 2017, the Company refinanced approximately $2.7 billion of U.S. dollar-denominated senior secured term loans maturing on July 2022 and paid off approximately $1.0 billion of euro-denominated senior secured term loans maturing on March 2021 and July 2022. The U.S. dollar-denominated July 2022 term loan facility was upsized by $1.0 billion, to pay off the euro-denominated term loans. Post transaction, the U.S. dollar-denominated July 2022 term loan facility approximates $3.8 billion of U.S. dollar-denominated term loans maturing July 2022 at an interest rate of LIBOR plus 2.25% or a base rate plus 1.25%. In connection with this transaction, the Company expensed $9 million in loss on debt extinguishment and $4 million in debt issuance costs.

5.375% Senior Secured First Lien Notes

On August 11, 2015, the Company issued approximately $1.2 billion aggregate principal amount of 5.375% senior secured first lien notes due August 15, 2023. Interest on the notes will be payable semi-annually in cash each year, commencing on February 15, 2016. The Company may redeem the notes, in whole or in part, prior to August 15, 2018 at a price equal to 100% of the notes redeemed plus accrued and unpaid interest to the redemption date and a "make-whole premium". Thereafter, the Company may redeem the notes, in whole or in part, at established redemption prices.

5.0% Senior Secured First Lien Notes