UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2023

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

Commission file number 1-10994

(Exact name of registrant as specified in its charter)

| State or other jurisdiction of incorporation or organization | (I.R.S. Employer Identification No.) | |||||||

(Address of principal executive offices, including zip code)

Registrant's telephone number, including area code:

(800 ) 248-7971

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act:

None

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. x Yes ☐ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ☐ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). x Yes ¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definitions of "large accelerated filer," "accelerated filer," "smaller reporting company" and "emerging growth company" in Rule 12b-2 of the Exchange Act.

x | Accelerated filer | ¨ | ||||||||||||||||||

| Non-accelerated filer | ¨ | Smaller reporting company | ||||||||||||||||||

| Emerging growth company | ||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ¨

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ☐ Yes x No

The aggregate market value of the registrant's voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold (based on the closing share price as quoted on the NASDAQ Global Market) as of the last business day of the registrant's most recently completed second fiscal quarter was approximately $1.34 billion. For purposes of this calculation, shares of common stock held or controlled by executive officers and directors of the registrant have been treated as shares held by affiliates.

There were 7,087,728 shares of the registrant's common stock outstanding on February 9, 2024.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's proxy statement that will be filed with the SEC in connection with the 2024 Annual Meeting of Shareholders are incorporated by reference into Part III of this Form 10-K.

Virtus Investment Partners, Inc.

Annual Report on Form 10-K for the Fiscal Year Ended December 31, 2023

| Page | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 1B. | ||||||||

| Item 1C. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

| Item 7. | ||||||||

| Item 7A. | ||||||||

| Item 8. | ||||||||

| Item 9. | ||||||||

| Item 9A. | ||||||||

| Item 9B. | ||||||||

| Item 9C. | ||||||||

| Item 10. | ||||||||

| Item 11. | ||||||||

| Item 12. | ||||||||

| Item 13. | ||||||||

| Item 14. | ||||||||

| Item 15. | ||||||||

| Item 16. | ||||||||

"We," "us," "our," the "Company," and "Virtus" as used in this Annual Report on Form 10-K (the "Annual Report") refer to Virtus Investment Partners, Inc., a Delaware corporation, and its subsidiaries.

PART I

| Item 1. | Business. | ||||

Organization

Virtus Investment Partners, Inc. (the "Company"), a Delaware corporation, commenced operations on November 1, 1995 and became an independent publicly traded company on December 31, 2008.

Our Business

We provide investment management and related services to institutions and individuals. We use a multi-manager, multi-style approach, offering investment strategies from affiliated managers, each having its own distinct investment style, autonomous investment process, individual brand, as well as from select unaffiliated managers for certain of our retail funds. By offering a broad array of products, we believe we can appeal to a greater number of investors and have offerings across market cycles and through changes in investor preferences. Through our multi-manager model, we provide our affiliated managers with retail and institutional distribution capabilities and business and operational support.

We offer investment strategies for institutional and individual investors in different investment products and through multiple distribution channels. Our investment strategies are available in a diverse range of styles and disciplines, managed by differentiated investment managers. We have offerings in various asset classes (equity, fixed income, multi-asset and alternatives), geographies (domestic, global, international and emerging), market capitalizations (large, mid and small), styles (growth, core and value) and investment approaches (fundamental and quantitative). Our products include mutual funds registered pursuant to the Investment Company Act of 1940, as amended ("U.S. retail funds"); Undertaking for Collective Investment in Transferable Securities and Qualifying Investor Funds (collectively, "global funds") and collectively with U.S. retail funds, variable insurance funds, exchange-traded funds ("ETFs"), the "open-end funds"); closed-end funds (collectively, with open-end funds, the "funds"); and retail separate accounts that include intermediary-sold and private client accounts; and institutional separate and commingled accounts, including structured products. We also provide subadvisory services to other investment advisers and serve as the collateral manager for structured products.

Our Investment Managers

We provide investment management services through our affiliated investment managers who are registered directly and indirectly as investment advisers under the Investment Advisers Act of 1940, as amended (the "Investment Advisers Act"). The investment managers are responsible for portfolio management activities for our retail and institutional products operating under advisory, subadvisory or collateral management agreements. We also use the investment management services of select unaffiliated managers to sub-advise certain of our open- and closed-end funds. We monitor our managers' services by assessing their performance, style and consistency and the discipline with which they apply their investment process.

1

Our affiliated investment managers, their respective investment styles and assets under management as of December 31, 2023 were as follows:

| Affiliated Manager | Headquarters | Investment Style | Assets (in billions) | |||||||||||||||||

AlphaSimplex Founded 1999 | Boston, MA | Systematic Alternatives | $ | 7.4 | ||||||||||||||||

Ceredex Value Advisors Founded 1995 | Orlando, FL | Value Equity | $ | 6.2 | ||||||||||||||||

Duff & Phelps Investment Management Founded 1932 | Chicago, IL | Listed Real Assets | $ | 12.3 | ||||||||||||||||

Kayne Anderson Rudnick Investment Management Founded 1984 | Los Angeles, CA | Quality-Focused Equity | $ | 59.6 | ||||||||||||||||

Newfleet Asset Management (1) Founded 2011 | Hartford, CT | Multi-Sector Fixed Income | $ | 14.7 | ||||||||||||||||

NFJ Investment Group Founded 1989 | Dallas, TX | Global Value Equity | $ | 6.6 | ||||||||||||||||

Seix Investment Advisors (1) Founded 1992 | Park Ridge, NJ | Specialty Fixed Income | $ | 13.1 | ||||||||||||||||

Silvant Capital Management Founded 2008 | Atlanta, GA | Growth Equity | $ | 2.2 | ||||||||||||||||

Stone Harbor Investment Partners (1) Founded 2006 | New York, NY | Emerging Markets Debt | $ | 5.6 | ||||||||||||||||

Sustainable Growth Advisers Founded 2003 | Stamford, CT | Global Growth Equity | $ | 26.4 | ||||||||||||||||

Virtus Multi-Asset (2) Founded 2022 | Hartford, CT | Global Multi-Asset | $ | 0.2 | ||||||||||||||||

Virtus Systematic (2) Founded 2022 | San Diego, CA | Systematic Global Equity | $ | 0.4 | ||||||||||||||||

Westchester Capital Management Founded 1989 | Valhalla, NY | Event-Driven Alternatives | $ | 3.7 | ||||||||||||||||

Zevenbergen Capital Investments (3) Founded 1987 | Seattle, WA | Disruptive Growth Equity | $ | 1.9 | ||||||||||||||||

(1) Operates as a division of Virtus Fixed Income Advisors LLC, a wholly owned subsidiary of the Company.

(2) Operates as a division of Virtus Investment Advisers, Inc., a wholly owned subsidiary of the Company.

(3) Affiliated through ownership of a minority interest.

Summary information regarding our select unaffiliated subadvisers, their respective investment styles and assets under management as of December 31, 2023 were as follows:

| Unaffiliated Subadviser | Investment Style | Assets (in billions) | ||||||||||||

| Voya Investment Management | Income & Growth and Convertible | $ | 9.7 | |||||||||||

| Other | International Growth Equity, Income-Focused Equity, Risk Managed and Quantitative | $ | 2.3 | |||||||||||

2

Our Investment Products

Our assets under management are in open-end funds, closed-end funds, retail separate accounts and institutional accounts. Our earnings are primarily from asset-based fees charged for services relating to these various products, including investment management, fund administration, distribution and shareholder services.

Assets Under Management by Product as of December 31, 2023

| Products | (in billions) | ||||

| Open-end funds (1) | $ | 56.1 | |||

| Closed-end funds | 10.0 | ||||

| Retail separate accounts | 43.2 | ||||

| Institutional accounts (2) | 63.0 | ||||

| Total Assets Under Management | $ | 172.3 | |||

(1)Represents assets under management of U.S. retail funds, global funds, ETFs and variable insurance funds.

(2)Represents assets under management of institutional separate and commingled accounts, including structured products.

Open-End Funds

Our U.S. retail funds are offered in a variety of asset classes (domestic, global and international equity, taxable and non-taxable fixed income, multi-asset and alternatives), market capitalizations (large, mid and small), styles (growth, core and value) and investment approaches (fundamental and quantitative). Our global funds are offered in select investment strategies to non-U.S. investors. Our ETFs are offered in a range of actively managed and index-based investment capabilities across multiple asset classes. Summary information about our open-end funds as of December 31, 2023 was as follows:

| Asset Class | Number of Funds | Total Assets (in millions) | Advisory Fee Range % (1) | |||||||||||||||||

| Domestic Equity | 28 | $ | 20,159 | 2.15 - 0.29 | ||||||||||||||||

| Fixed Income | 43 | 14,454 | 1.85 - 0.17 | |||||||||||||||||

| International Equity | 13 | 3,364 | 1.85 - 0.21 | |||||||||||||||||

| Multi-Asset | 4 | 5,777 | 0.75 - 0.45 | |||||||||||||||||

| Alternatives | 17 | 7,456 | 1.65 - 0.45 | |||||||||||||||||

| Specialty Equity | 10 | 2,937 | 1.80 - 0.59 | |||||||||||||||||

| Global Equity | 7 | 1,915 | 1.85 - 0.55 | |||||||||||||||||

| Total Open-End Funds | 122 | $ | 56,062 | |||||||||||||||||

(1)Percentage of average daily net assets. The percentages listed represent the range of management advisory fees paid by the funds, from the highest to the lowest. The range indicated includes the impact of breakpoints at which management advisory fees for certain of the funds in each fund type decrease as assets in such funds increase. Subadvisory fees paid on funds managed by unaffiliated subadvisers are not reflected in the percentages listed.

3

Closed-End Funds

Our closed-end funds are offered in a variety of asset classes such as equity, fixed income, multi-asset and alternatives, each of which is traded on the New York Stock Exchange. Summary information about our closed-end funds as of December 31, 2023 was as follows:

| Asset Class | Number of Funds | Total Assets (in millions) | Advisory Fee Range % (1) | |||||||||||||||||

| Multi-Asset | 5 | $ | 7,058 | 1.00 - 0.50 | ||||||||||||||||

| Fixed Income | 6 | 1,572 | 1.00 - 0.50 | |||||||||||||||||

| Equity | 1 | 826 | 1.25 | |||||||||||||||||

| Alternatives | 1 | 570 | 1.00 | |||||||||||||||||

| Total Closed-End Funds | 13 | $ | 10,026 | |||||||||||||||||

(1)Percentage of average weekly or daily net assets. The percentages listed represent the range of management advisory fees paid by the funds, from the highest to the lowest. The range indicated includes the impact of breakpoints at which management advisory fees for certain of the funds in each fund type decrease as assets in such funds increase. Subadvisory fees paid on funds managed by unaffiliated subadvisers are not reflected in the percentages listed.

Retail Separate Accounts

Intermediary-Sold Managed Accounts

Intermediary-sold managed accounts are individual investment accounts that are contracted through intermediaries as part of investment programs offered to retail investors.

Private Client Accounts

Private client accounts are investment accounts offered by certain affiliates directly to individual investors. Services provided include wealth advisory and investment services that include third-party investment services.

The following table summarizes our retail separate accounts by asset class as of December 31, 2023:

| Total Assets | ||||||||||||||

| (in millions) | Intermediary-Sold Managed Accounts | Private Client Accounts | ||||||||||||

| Equity | ||||||||||||||

| Domestic | $ | 33,105 | $ | 29 | ||||||||||

| International equity | 81 | — | ||||||||||||

| Global equity | 366 | — | ||||||||||||

| Specialty equity | 70 | — | ||||||||||||

| Fixed Income | ||||||||||||||

| Leveraged finance | 1,444 | 2 | ||||||||||||

| Investment grade | 196 | 298 | ||||||||||||

| Multi-Asset (1) | 175 | 7,435 | ||||||||||||

| Alternatives | 1 | — | ||||||||||||

| Total Retail Separate Accounts | $ | 35,438 | $ | 7,764 | ||||||||||

(1) For private client accounts, consists of individual client accounts with substantial holdings in at least two of the following asset classes: equity, fixed income, and alternatives.

4

Institutional Accounts

Our institutional clients include corporations, multi-employer retirement funds, public employee retirement systems, foundations and endowments. We also act as collateral manager for nine collateralized loan obligations ("CLOs"). In addition, we provide subadvisory services to unaffiliated mutual funds. Summary information about our institutional accounts as of December 31, 2023 was as follows:

| Asset Class | Total Assets (in millions) | |||||||

| Equity | ||||||||

| Domestic | $ | 23,970 | ||||||

| International | 1,610 | |||||||

| Global | 8,271 | |||||||

| Fixed Income | ||||||||

| Leveraged finance | 10,303 | |||||||

| Investment grade | 8,923 | |||||||

| Alternatives | 8,926 | |||||||

| Multi-Asset | 966 | |||||||

| Total Institutional Accounts | $ | 62,969 | ||||||

Other Fee Earning Assets

Other fee earning assets include assets for which we provide services for an asset-based fee but do not serve as the investment adviser. Other fee earning assets are not included in our assets under management. At December 31, 2023, we had $2.6 billion of other fee earning assets.

Our Investment Management, Administration and Shareholder Services

Our investment management, administration and shareholder service fees earned in each of the last three years were as follows:

| Years Ended December 31, | |||||||||||||||||

| (in thousands) | 2023 | 2022 | 2021 | ||||||||||||||

| Open-end funds | $ | 305,238 | $ | 335,585 | $ | 395,152 | |||||||||||

| Closed-end funds | 58,136 | 63,841 | 63,301 | ||||||||||||||

| Retail separate accounts | 171,357 | 171,509 | 174,919 | ||||||||||||||

| Institutional accounts | 176,744 | 157,404 | 148,213 | ||||||||||||||

| Total investment management fees | 711,475 | 728,339 | 781,585 | ||||||||||||||

| Administration fees | 52,858 | 61,344 | 73,113 | ||||||||||||||

| Shareholder service fees | 20,999 | 24,518 | 29,418 | ||||||||||||||

| Total | $ | 785,332 | $ | 814,201 | $ | 884,116 | |||||||||||

Investment Management Fees

We provide investment management services through our affiliated investment managers (each an "Adviser") pursuant to investment management agreements. For our sponsored funds, we earn fees based on each fund's average daily or weekly net assets with most fee schedules providing for rate declines or "breakpoints" as asset levels increase to certain thresholds. For funds managed by subadvisers, the day-to-day investment management of the fund's portfolio is performed by the subadviser, which receives a fee based on a percentage of the management fee. Each fund bears all expenses associated with its operations. In some cases, to the extent total fund expenses exceed a specified percentage of a fund's average net assets, the Adviser has agreed to reimburse the fund's expenses in excess of that level.

For retail separate accounts and institutional accounts, investment management fees are negotiated and based primarily on portfolio size and complexity, individual client requests and investment strategy capacity, as appropriate. In certain instances, institutional fees may include performance-related fees, generally earned if the returns on the portfolios exceed agreed upon periodic or cumulative return targets, primarily benchmark indices. Fees for CLOs are generally

5

calculated at a contractual fee rate applied against the end of the preceding quarter par value of the total collateral being managed.

Administration Fees

We provide various administrative services to our U.S. retail funds, ETFs and the majority of our closed-end funds. We earn fees based on each fund's average daily or weekly net assets. These services include: record keeping, preparing and filing documents required to comply with securities laws, legal administration and compliance services, customer service, supervision of the activities of the funds' service providers, tax services and treasury services as well as providing office space, equipment and personnel that may be necessary for managing and administering the business affairs of the funds.

Shareholder Service Fees

We provide shareholder services to our U.S. retail funds. We earn fees based on each fund's average daily net assets. Shareholder services include maintaining shareholder accounts, processing shareholder transactions, preparing filings and performing necessary reporting, among other things.

Our Distribution Services

Our products are offered through various retail and institutional distribution channels.

Retail

Our retail distribution resources in the U.S. consist of regional sales professionals, a national account relationship group and specialized teams for retirement and ETFs. Our U.S. retail funds and retail separate accounts are distributed through financial intermediaries. We have broad distribution access in the U.S. retail market, with distribution partners that include national and regional broker-dealers, independent broker-dealers and registered investment advisers, banks and insurance companies. In many of these firms, we have a number of products that are on preferred or "recommended" lists and on fee-based advisory programs. Our private client business is marketed directly to individual clients by financial advisory teams at our affiliated investment managers.

Institutional

Our institutional distribution resources include affiliate-specific institutional sales teams primarily focused on the U.S. market, supported by shared consultant relations and U.S. and non-U.S. institutional sales distribution. Our institutional products are marketed through relationships with consultants as well as directly to clients. We target key market segments, including foundations and endowments, corporations, public and private pension plans, sovereign wealth funds and subadvisory relationships.

Our Broker-Dealer Services

We operate a broker-dealer that is registered under the Securities Exchange Act of 1934, as amended (the "Exchange Act"), and is a member of the Financial Industry Regulatory Authority ("FINRA"). Our broker-dealer serves as the principal underwriter and distributor of our funds, provides market advisory services to sponsors of retail separate accounts, and is also a program manager and distributor of a qualified tuition plan under Section 529 of the Internal Revenue Code ("529 Plan"). Our broker-dealer is subject to, among others, the net capital rule of the Securities and Exchange Commission (the "SEC"), which is designed to enforce minimum standards regarding the general financial condition and liquidity of broker-dealers.

Our Competition

We face significant competition from a wide variety of financial institutions, including other investment management companies, as well as from proprietary products offered by our distribution partners such as banks, broker-dealers and financial planning firms. Competition in our businesses is based on several factors, including investment performance, fees charged, access to distribution channels, and service to financial advisors and their clients. Our competitors, many of which are larger than us, often offer similar products and use similar distribution sources, and may also offer less expensive products, have greater access to key distribution channels and have greater resources than we do.

6

Our Regulatory Matters

The financial services industry is highly regulated, regulations are complex, and failure to comply with related laws and regulations can result in the revocation of registrations, the imposition of censures or fines and the suspension or expulsion of a firm and/or its employees from the industry. We are subject to regulation by the SEC, other federal and state agencies, certain international regulators, as well as FINRA and other self-regulatory organizations.

Each of our affiliated investment managers is registered directly and indirectly as an investment adviser with the SEC under the Investment Advisers Act. The Investment Advisers Act imposes numerous obligations on registered investment advisers, including fiduciary duties, compliance and disclosure obligations, and operational and recordkeeping requirements. Certain investment management affiliates are also members of the National Futures Association and are regulated by the U.S. Commodity Futures trading Commission ("CFTC") with respect to the management of funds and other products that utilize futures, swaps, or other CFTC regulated instruments.

Our affiliated investment managers also advise registered and unregistered funds in the U.S. and other jurisdictions and are subject to the regulatory requirements in the jurisdiction where those funds are sponsored or offered, including with respect to mutual funds and closed end funds in the U.S., the Investment Company Act of 1940, as amended (the "Investment Company Act"). The Investment Company Act governs the operations of mutual funds and imposes obligations on their advisers, including investment restrictions and other governance, compliance, reporting and fiduciary obligations with respect to the management of those funds.

Affiliated investment managers operating outside of the U.S. are also subject to regulation by various regulatory authorities and exchanges in the relevant jurisdiction. Some of our investment affiliates are subject to directives and regulations in the European Union and other jurisdictions related to funds, such as the Undertakings for the Collective Investment of Transferable Securities ("UCITS") Directive and the Alternative Investment Fund Managers Directive ("AIFMD"), with respect to depository functions, remuneration policies and sanctions and other matters. Our global funds are registered with and subject to regulation by the Central Bank of Ireland. New regulations or interpretations of existing laws may result in enhanced disclosure obligations. Increased regulations generally increase our costs, and we could continue to experience higher costs if new laws require us to spend more time, hire additional personnel, or purchase new technology to comply effectively.

Our broker-dealer is subject to SEC and FINRA rules and regulations, including extensive regulatory requirements related to sales practices, registration of personnel, compliance and supervision and compensation and disclosure. Sales and marketing activities of investment management services are also subject to regulation by non-U.S. authorities in the jurisdictions in which investment management products and services are offered. The ability to transact business in these jurisdictions and to conduct cross-border activities, is subject to the continuing availability of regulatory authorizations and exemptions. We have distribution teams that operate offices in the United Kingdom and Singapore and are subject to regulation by the Financial Conduct Authority and Monetary Authority of Singapore, respectively.

Due to the extensive laws and regulations to which we and our investment management affiliates are subject, we and our investment management affiliates must devote substantial time, expense, and effort to remain current on, and to address, legal and regulatory compliance matters. We and our investment management affiliates have established compliance programs to address regulatory compliance and we have experienced legal and compliance professionals in place to address these requirements. We also have established legal and regulatory advisers in each of the countries where we conduct business.

Our officers, directors and employees may, from time to time, own securities that are also held by one or more of our funds or strategies offered to clients. We have adopted a Code of Ethics pursuant to the provisions of the Investment Company Act and the Investment Advisers Act that require the disclosure of personal securities holdings and trading activity by all employees on a quarterly and annual basis. Employees with investment discretion or access to investment decisions are subject to additional restrictions with respect to the pre-clearance of the purchase or sale of securities over which they have investment discretion or beneficial interest. Our Code of Ethics also imposes restrictions with respect to personal transactions in securities that are held, recently sold, or contemplated for purchase by our mutual funds, and certain transactions are restricted so as to avoid the possibility of improper use of information relating to the management of client accounts.

7

Human Capital

As of December 31, 2023, we employed 824 employees and operated offices throughout the U.S., and in the U.K. and Singapore. We strive to attract and retain talented individuals by creating an environment of excellence and opportunity that serves as a foundation for all employees to reach their potential and make meaningful contributions to the organization.

We offer competitive salaries and a comprehensive suite of benefits, including programs that support wellness, financial security, and professional development. As part of our offerings, we:

▪Regularly assess and benchmark our compensation and benefit practices and conduct internal and external pay comparisons to assist us in ensuring that employees are compensated fairly, equitably and competitively.

▪Offer career enhancement opportunities to maximize each employee's potential and develop leaders throughout the organization.

▪Provide an education assistance program with tuition reimbursement for employees who wish to continue their education to secure increased responsibility and growth within the organization and in their careers.

▪Offer benefits that promote financial and personal security including comprehensive medical, dental, prescription, disability and life insurance coverages as well as an employee assistance program; company match to employees' 401(k) contributions; and an employee stock purchase plan.

▪Provide wellness programs that include health screenings and wellness earned premium rebates, as well as paid time off for vacation, illness, bereavement, parental and family care leave, and volunteer activities.

We rely upon key personnel to manage our business, including senior executives, portfolio managers, securities analysts, investment advisers, sales personnel and other professionals. The retention of senior executives and key investment personnel is material to the management of our business.

Our value as a company derives from the talents and diversity of all employees, and we are committed to creating and maintaining an environment where every employee is treated with dignity and respect. The collective sum of employees' backgrounds, unique skills, and life experiences creates an environment where they and the company can achieve the highest levels of performance. Programs and practices - including those supporting workforce diversity, an inclusive culture, employee involvement in community activities and corporate philanthropy - are designed to help us deliver on our commitment to maintaining an organization that is diverse and inclusive for all employees.

▪As an employer, we prohibit any form of discrimination and have no tolerance for harassment in any form or any behavior that may contribute to a hostile, intimidating, unwelcoming, and/or inaccessible work environment.

▪Collaborative efforts with organizations, institutions, and referral sources support us in identifying diverse talent pools, increasing the diversity of potential candidates, and engaging with employees across the organization to raise the awareness of and advance our inclusion efforts.

▪Community engagement is ingrained into our culture. The Company and employees have supported a wide range of philanthropic activities that help to enrich and sustain the communities in which we have a business presence.

Available Information

Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and all amendments to these reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act, as well as proxy statements, are available free of charge on our website located at www.virtus.com as soon as reasonably practicable after they are filed with, or furnished to, the SEC. Reports, proxy statements and other information regarding issuers that file electronically with the SEC, including our filings, are also available to the public on the SEC's website at http://www.sec.gov.

A copy of our Corporate Governance Guidelines, our Code of Conduct and the charters of our Audit Committee, Compensation Committee, and Governance Committee are posted on our website at http://ir.virtus.com under "Corporate Governance" and are available in print without charge to any person who requests copies by contacting Investor Relations by email to: investor.relations@virtus.com or by mail to Virtus Investment Partners, Inc., c/o Investor Relations, One Financial Plaza, Hartford, CT 06103. The Company may use its website as a distribution channel of material company information. Financial and other important information regarding the Company is routinely posted on and accessible through the Company’s website at http://ir.virtus.com. In addition, you may automatically receive email alerts and other information about the Company when you enroll your email address by visiting http://ir.virtus.com. Information contained on the website is not incorporated by reference or otherwise considered part of this document.

8

| Item 1A. | Risk Factors. | ||||

This section describes some of the potential risks relating to our business. The risks described below are some of the more important factors that could affect our business. You should carefully consider the risks described below, together with all of the other information included in this Annual Report on Form 10-K, in evaluating the Company and our common stock. If any of the risks described below actually occur, our business, revenues, profitability, results of operations, financial condition, cash flows, reputation and stock price could be materially adversely affected.

RISKS RELATED TO OUR INDUSTRY, BUSINESS AND OPERATIONS

We earn substantially all of our revenues based on assets under management that fluctuate based on many factors, and any reduction would negatively impact our revenues and profitability.

The majority of our revenues are generated from asset-based fees from investment management products and services to individuals and institutions. Therefore, if assets under management decline, our fee revenues would decline, reducing profitability as certain of our expenses are fixed or have contractual terms. Assets under management could decline due to a variety of factors including, but not limited to, the following:

▪General domestic and global economic, political and public health conditions. Capital, equity and credit markets can experience substantial volatility. Changes in interest rates, the availability and cost of credit, inflation rates, economic uncertainty, changes in laws, trade barriers, commodity prices, currency exchange rates, national and international political circumstances and conflicts, public health issues and other conditions may impact the capital, equity and credit markets. Employment rates, economic weakness and budgetary challenges in parts of the world, uncertainty regarding governmental regulations and international trade policies, conflicts such as in Ukraine and the Middle East, concern over prospects in China and emerging markets, and growing debt for certain countries all indicate that economic and political conditions remain unpredictable. The occurrence of public health issues such as a major epidemic or pandemic that affect public health and public perception of health risk, as well as local, state and/or national government restrictive measures implemented to control such issues, could adversely affect the global financial markets, our employees and the systems we rely on. Any of the conditions listed herein, among others, may impact our assets under management.

Past volatility in the markets has highlighted the interconnection of the global economies and markets and has demonstrated how deteriorating financial condition of one institution may adversely impact the performance of other institutions. Our assets under management have exposure to many different industries and counterparties and may be exposed to credit, operational or other risk due to the default by a counterparty or client or in the event of a market failure or disruption. Negative, uncertain or diminishing investor confidence in the markets and/or adverse market conditions could result in a decrease in investor risk tolerance. Such a decrease could prompt investors to reduce their rate of investment or to partially or fully withdraw from markets, which could reduce our overall assets under management and have an adverse effect on our revenues, earnings and growth prospects. In the event of extreme circumstances, including economic, political or business or health crises, such as a widespread systemic failure in the global financial system, failures of firms that have significant obligations as counterparties, political conflicts or global pandemics, we may suffer significant declines in assets under management and severe liquidity or valuation issues.

▪Price declines in individual securities, market segments or geographic areas. Portfolios that we manage that are focused on certain geographic markets or industry sectors are particularly vulnerable to political, social and economic events in those markets and sectors. If those markets or industries decline or experience volatility, this could have a negative impact on our assets under management and our revenues. For example, certain non-U.S. markets, particularly emerging markets, are not as developed or as efficient as the U.S. financial markets and, as a result, may be less liquid, less regulated and significantly more volatile than the U.S. financial markets. In addition, certain industry sectors can experience significant volatility, such as the technology or oil sector. Liquidity or values in such markets or sectors may be adversely impacted by factors including political or economic events, government policies, expropriation, volume trading limits by foreign investors, social or civil unrest, etc. These factors may negatively impact the market value of a security or our ability to dispose of it.

▪Real or perceived negative absolute or relative performance. Sales and redemptions of our investment strategies can be affected by investment performance relative to established benchmarks or other competing investment strategies. Our investment management strategies are rated, ranked or assessed by independent third-parties, distribution partners and industry periodicals and services. These assessments often influence the investment decisions of clients. If the performance of our investment strategies is perceived to be underperforming relative to peers, it could result in

9

increased withdrawals of assets by existing clients and the inability to attract additional investments from new and existing clients.

We may engage in significant transactions that may not achieve the anticipated benefits or could expose us to additional or increased risks.

We have executed several inorganic transactions over the past years and we regularly evaluate potential transactions, including acquisitions, consolidations, joint ventures, strategic partnerships, or similar transactions, some of which could be significant. Our past acquisitions and strategic transactions have led to a significant increase in our assets under management and an expansion of our product and service offerings. We cannot provide assurance that we will continue to be successful in closing on transactions or achieving anticipated financial benefits, including such things as revenue or cost synergies.

Any transaction may also involve a number of other risks, including additional demands on our staff, unanticipated problems regarding integration of operating facilities, technologies and new employees, and the existence of liabilities or contingencies not disclosed to, or otherwise unknown by, us prior to closing a transaction. In addition, any business we acquire may underperform relative to expectations or may lose customers or employees.

Our investment management agreements are subject to renegotiation or termination on short notice, which could negatively impact our business.

Our clients include our sponsored fund investors, represented by boards of trustees or directors (the "fund boards"), managed account program sponsors, individual private clients, and institutional clients. Our investment management agreements with these clients may be terminated on short notice and without penalty. As a result, there would be little impediment for these clients to terminate our agreements. Our clients may renegotiate their investment contracts, or reduce the assets we manage for them, due to a number of reasons including, but not limited to: poor investment performance; loss of key investment personnel; a change in the client's or third-party distributors' decision makers; and reputational, regulatory or compliance issues. The fund boards may deem it to be in the best interests of a fund's shareholders to make decisions adverse to us, such as reducing the compensation paid to us, requesting that we subsidize fund expenses over certain thresholds, or imposing restrictions on our management of the fund. Under the Investment Company Act, investment management agreements automatically terminate in the event of an assignment, which may occur if, among other events, the Company undergoes a change in control, such as any person acquiring 25% of the voting rights of our common stock. If an assignment were to occur, we cannot be certain that the funds' boards and shareholders would approve a new investment management agreement. In addition, investment management agreements for the separate accounts we manage may not be assigned without the consent of the client. If an assignment occurs, we cannot be certain that the Company will be able to obtain the necessary approvals or client consents. The withdrawal, renegotiation or termination of any investment management agreement relating to a material portion of assets under management would have an adverse impact on our results of operations and financial condition.

Our business could be harmed by any damage to our reputation and lead to a reduction in our revenues and profitability.

Maintaining a positive reputation with existing and potential clients, the investment community and other constituencies is critical to our success. Our reputation is vulnerable to many threats that can be difficult or impossible to control, and costly or impossible to remediate even if they are without merit or satisfactorily addressed. Our reputation may be impacted by many factors including, but not limited to: poor performance; litigation; conflicts of interests; regulatory inquiries, investigations or findings; operational failures (including cyber breaches); intentional or unintentional misrepresentation of our products or services by us or our third-party service providers; material weaknesses in our internal controls; or employee misconduct or rumors. Any damage to our reputation could impede our ability to attract and retain clients and key personnel, adversely impact relationships with clients, third-party distributors and other business partners, and lead to a reduction in the amount of our assets under management, any of which could adversely affect our results of operations and financial condition.

Our debt agreements contain covenants, required principal repayments and other provisions that could adversely affect our financial condition or results of operations.

We incur indebtedness for a variety of business reasons, including in relation to financing acquisitions and transactions. The indebtedness we incur can take many forms including, but not limited to, term loans or revolving lines of credit that customarily contain covenants.

10

At December 31, 2023, we had $258.8 million of total debt outstanding under its credit agreement, excluding debt of consolidated investment products ("CIP"), and had no borrowings outstanding under our $175.0 million revolving credit facility. Under our credit agreement, we are required to use a portion of our cash flow to service interest and make required annual principal payments, which may restrict our cash flow available for other purposes. The credit agreement also contains covenants that may limit our ability to return capital to shareholders. We cannot provide assurances that at all times in the future we will satisfy all such covenants or obtain any required waiver or amendment, in which event all indebtedness could become immediately due. Any or all of the above factors could adversely affect our financial condition or results of operations.

We may need to obtain additional capital that may not be available to us in sufficient amounts or on acceptable terms, which could have an adverse impact on our business.

Our ability to meet our future cash needs is dependent upon our ability to generate or have short-term access to cash. Although we have generated sufficient cash in the past, we may not do so in the future. We had unused capacity under our revolving credit facility of $175.0 million as of December 31, 2023. Our ability to access capital markets efficiently depends on a number of factors, including the state of credit and equity markets, interest rates and credit spreads. At December 31, 2023, we had $258.8 million in debt outstanding, excluding the notes payable of our CIP for which risk of loss to the Company is limited to our $95.5 million investment in such products. (See Note 20 of our consolidated financial statements for additional information on the notes payable of the CIP). We may need to raise capital to fund new business initiatives in the future, and financing may not be available to us in sufficient amounts, on acceptable terms, or at all. If we are unable to access sufficient capital on acceptable terms, our business could be adversely impacted.

Our business relies on the ability to attract and retain key employees, and the loss of such employees could negatively affect our financial performance.

The success of our business is dependent to a large extent on our ability to attract and retain key employees, such as senior executives, portfolio managers, securities analysts and sales personnel. There is significant competition in the job market for these professionals and compensation levels in the industry are highly competitive. Our industry is also characterized by the movement of investment professionals among different firms.

If we are unable to continue to attract and retain key employees, or if compensation costs required to attract and retain key employees increase, our performance, including our competitive position, could be adversely affected. Additionally, we utilize equity awards as part of our compensation plans and as a means for recruiting and retaining key employees. Declines in our stock price would result in deterioration of the value of equity awards granted, thus lessening the effectiveness of using stock-based awards to retain key employees.

In certain circumstances, the departure of key investment personnel could cause higher redemption rates in certain strategies or the loss of certain client accounts. Any inability to retain key employees, attract qualified employees or replace key employees in a timely manner could lead to a reduction in the amount of our assets under management, which would have an adverse effect on our revenues and profitability. In addition, there could be additional costs to replace, retain or attract new talent that could result in a decrease in our profitability and have an adverse impact on our results of operations and financial condition.

We operate in a highly competitive industry that may require us to reduce our fees or increase amounts paid to financial intermediaries, which could result in a reduction of our revenues and profitability.

We face significant competition from a wide variety of financial institutions, including other investment management companies, as well as from proprietary products offered by our distribution partners such as banks, broker-dealers and financial planning firms. Competition in our businesses is based on several factors, including investment performance, fees charged, access to distribution channels and service to financial advisors. Our competitors, many of which are larger, often offer similar products, use the same distribution sources, offer less expensive products, maintain greater access to key distribution channels, and have greater resources, geographic footprints and name recognition. Additionally, certain products and asset classes that we do not currently offer, such as passive or index-based products, are popular with investors. Existing clients may withdraw their assets in order to invest in these products, and we may be unable to attract additional investments from existing and new clients, which would lead to a decline in our assets under management and market share.

11

Our profits are highly dependent on the fees we earn for our products and services. Competition could cause us to reduce the fees that we charge. If our clients, including our fund boards, were to view our fees as being inappropriately high relative to the market or the returns generated by our investment products, we may choose, or be required, to reduce our fee levels, or we may experience significant redemptions in our assets under management, which could have an adverse impact on our results of operations and financial condition.

We utilize unaffiliated firms to provide investment management services and any matters that adversely impact them or any change in our relationships with them could adversely affect our revenues and profitability.

We utilize unaffiliated subadvisers as investment managers for certain of our retail funds. Because we have no ownership interests in these firms, we do not control their business activities. Problems stemming from the business activities of those firms may negatively impact or disrupt their operations or expose them to disciplinary action or reputational harm. Furthermore, any such matters at these unaffiliated firms may have an adverse impact on our business or reputation or expose us to regulatory scrutiny, including with respect to our oversight of such firms.

We periodically negotiate provisions and renewals of these relationships, and we cannot provide assurance that such terms will remain acceptable to us or the unaffiliated firms. These relationships can also be terminated upon short notice without penalty. In addition, the departure of key employees at unaffiliated subadvisers could cause higher redemption rates for certain assets under management. An interruption or termination of unaffiliated firm relationships could affect our ability to market our products and result in a reduction in assets under management, which would have an adverse impact on our results of operations and financial condition.

We distribute our products through intermediaries and changes in key distribution relationships could reduce our revenues, increase our costs and adversely affect our profitability.

Our primary source of distribution for retail products is through intermediaries that include third-party financial institutions such as: major wire-houses; national, regional and independent broker-dealers and financial advisors; banks and financial planners; and registered investment advisers. We are highly dependent on access to these distribution systems to raise and maintain assets under management. These distributors are generally not contractually required to distribute our products and typically offer their clients various investment products and services, including proprietary products and services, in addition to, and in competition with, our products and services. While we compensate these intermediaries pursuant to contractual agreements, we may not be able to retain access to these channels at all or at similar pricing. Increasing competition for these distribution channels could cause our distribution costs to rise, which could have an adverse effect on our business, revenues and profitability. To the extent that existing or future intermediaries prefer to do business with our competitors, the sales of our products as well as our market share, revenues and profitability could decline.

We and our third-party service providers rely on numerous technology systems and any business interruption, security breach, or system failure could negatively impact our business and profitability.

Our technology systems, and those of third-party service providers, are critical to our operations. The ability to consistently and reliably obtain accurate securities pricing information, process client portfolio and fund shareholder transactions, and provide reports and other services to clients is an essential part of our business. Any delays or inaccuracies in obtaining pricing information, processing such transactions or reports, other breaches and errors, and any inadequacies in other client service could result in reimbursement obligations or other liabilities or alienate clients and potentially give rise to claims against us. Any failure or interruption of third-party systems, whether resulting from technology or infrastructure breakdowns, defects or external causes such as fire, natural disaster, computer viruses, acts of terrorism or power disruptions, or public health events could result in financial loss, negatively impact our reputation and negatively affect our ability to do business. Although we and our third-party service providers have disaster recovery plans in place, we may nonetheless experience interruptions if a natural or man-made disaster or prolonged power outage were to occur, which could have an adverse impact on our business and profitability.

In addition, our computer systems are regularly the target of viruses or other malicious codes, unauthorized access, cyber-attacks or other computer-related penetrations. The sophistication of cyber threats continues to increase, including through the use of "ransomware" and phishing attacks, and our controls and the preventative actions we take to reduce the risk of cyber incidents and protect our information systems may be insufficient to detect or prevent unauthorized access, cyber-attacks or other security breaches to our systems or those of third parties with whom we do business. Our third-party service providers' systems may also be affected by, or fail, as a result of, catastrophic events, such as fires, floods, hurricanes and tornadoes. A breach of our systems, or of those of third-party service providers, through cyber-attacks or failure to manage and sufficiently secure our technology environment could result in interruptions or malfunctions in the operations of our business, loss of valuable information, liability for stolen assets or information, remediation costs to repair damage caused by a breach or to recover access to our systems, additional costs to mitigate against future incidents, and litigation

12

costs resulting from an incident. Any of these conditions could have an adverse impact on our business and profitability.

We and certain of our third-party service providers receive and store personal information as well as non-public business information. Although we and our third-party service providers take precautions, we may still be vulnerable to hacking or other unauthorized use. A breach of the systems or hardware could result in unauthorized access to our proprietary business or client data or release of this type of data, which could subject us to legal liability or regulatory action under data protection and privacy laws, which may result in fines or penalties, the termination of existing client contracts, costly mitigation activities and harm to our reputation. The occurrence of any of these risks could have an adverse impact on our business and profitability.

We have significant capital invested in marketable securities, which exposes us to earnings volatility as the value of these investments fluctuate, as well as risk of capital loss.

We use capital to incubate new investment strategies, introduce new products or to enhance distribution access of existing products. At December 31, 2023, we had $275.6 million of such investments, comprising $180.1 million of marketable securities and $95.5 million of net investments in CLOs. These investments are in a variety of asset classes, including alternatives, fixed income and equity strategies and first-loss tranches of CLO equity. Many of these investments employ a long-term investment strategy with an optimal investment period spanning several years. Accordingly, during this investment period, the capital held in these investments may not be available for other corporate purposes without significantly diminishing our investment return. We cannot provide assurance that these investments will perform as expected. Increases or decreases in the value of these investments could increase the volatility of our earnings, and an other-than-temporary or permanent decline in the value of these investments could result in the loss of capital and have an adverse impact on our results of operations and financial condition.

LEGAL AND REGULATORY RISKS

We are subject to an extensive and complex regulatory environment and changes in regulations or failure to comply with them could adversely affect our revenues and profitability.

The investment management industry in which we operate is subject to extensive and frequently changing regulation. We are subject to regulation by the SEC, other federal and state agencies, certain international regulators, as well as FINRA and other self-regulatory organizations. Each of our affiliated investment managers and unaffiliated subadvisers is registered with the SEC under the Investment Advisers Act. There are various regulatory reform initiatives in the U.S. and other jurisdictions and new regulations or interpretations of existing laws may result in enhanced disclosure obligations which could negatively affect us or materially increase our regulatory burden. Increased regulations generally increase our costs, and we could continue to experience higher costs if new laws require us to spend more time, hire additional personnel, or purchase new technology to comply effectively.

Although we spend extensive time and resources to ensure compliance with all applicable laws and regulations, if we fail to properly adhere to our policies or modify and update our compliance procedures in a timely manner in this changing and highly complex regulatory environment, we may be subject to various legal proceedings, including civil litigation, governmental investigations and enforcement actions that could result in fines, penalties, suspensions of individual employees, or limitations on particular business activities, any of which could have an adverse impact on our revenues and profitability.

We manage assets under agreements that have investment guidelines or other contractual requirements and failure to comply could result in claims, losses, or regulatory sanctions, which could negatively impact our revenues and profitability.

The agreements under which we manage client assets often have established investment guidelines or other contractual requirements with which we are required to comply in providing our investment management services. Although we maintain various compliance procedures and other controls to prevent, detect and correct such errors, any failure or allegation of a failure to comply with these guidelines or other requirement could result in client claims, reputational damage, withdrawal of assets and potential regulatory sanctions, any of which could have an adverse impact on our revenues and profitability.

We could be subject to civil litigation and government investigations or proceedings, which could adversely affect our business.

Many aspects of our business involve substantial risks of liability, and there have been substantial incidences of litigation and regulatory investigations in the financial services industry in recent years, including customer claims as well as class action suits seeking substantial damages. From time to time, we and/or our sponsored funds may be named as defendants or co-defendants in lawsuits or be involved in disputes that involve the threat of lawsuits seeking substantial

13

damages. We and/or our sponsored funds are also involved from time to time in governmental and self-regulatory organization investigations and proceedings. (See Item 3. "Legal Proceedings" for further information.)

Any lawsuits, investigations or proceedings could result in reputational damage, loss of clients and assets, settlements, awards, injunctions, fines, penalties, increased costs and expenses in resolving a claim, diversion of employee resources and resultant financial losses. Predicting the outcome of such matters is inherently difficult, particularly where claims are brought on behalf of various classes of claimants or by a large number of claimants, when claimants seek substantial or unspecified damages, or when investigations or legal proceedings are at an early stage. A substantial judgment, settlement, fine or penalty could be material to our operating results or cash flows for a particular period, depending on our results for that period, or could cause us significant reputational harm, which could harm our business prospects.

We depend to a large extent on our business relationships and our reputation to attract and retain clients. As a result, allegations of improper conduct by private litigants, including investors in our funds, or regulators, whether the ultimate outcome is favorable or unfavorable to us, as well as negative publicity and press speculation about us, our investment activities or the asset management industry in general, whether or not valid, may harm our reputation. We may incur substantial legal expenses in defending against proceedings commenced by a client, regulatory authority or other private litigant. Substantial legal liability levied on us could cause significant reputational harm and have an adverse impact on our results of operations and financial condition.

We are subject to multiple tax jurisdictions and any changes in tax laws or unanticipated tax obligations could have an adverse impact on our financial condition, results of operations and cash flow.

We are subject to income as well as non-income-based taxes and are subject to ongoing tax audits, in various jurisdictions in which we operate. Tax authorities may disagree with certain positions we have taken that may result in the assessment of additional taxes. We regularly assess the appropriateness of our tax positions and reporting. We cannot provide assurance that we will accurately predict the outcomes of audits and the actual outcomes of these audits could be unfavorable. Any changes to tax laws could impact our estimated effective tax rate and tax expense and could result in adjustments to our treatment of deferred taxes, including the realization or value thereof, which could have an adverse effect on our business, financial condition and results of operations.

RISKS RELATED TO OWNERSHIP OF OUR COMMON STOCK

We may not pay dividends as intended or at all.

The declaration, payment and determination of the amount of our quarterly dividends may change at any time. In making decisions regarding our dividends, we consider general economic and business conditions as well as our strategic plans and prospects, business and investment opportunities, financial condition and operating results, working capital requirements and anticipated cash needs, contractual and regulatory restrictions (including under the terms of our credit agreement) and other obligations, that may have implications on the payment of distributions by us to our shareholders or by our subsidiaries to us, and such other factors as we may deem relevant. Our ability to pay or increase our dividends maybe subject to restrictions under the terms of our credit agreement. We cannot make any assurances that any dividends, whether quarterly or otherwise, will continue to be paid in the future.

We have corporate governance provisions that may make an acquisition of us more difficult.

Certain provisions of our certificate of incorporation and bylaws could discourage, delay or prevent a merger, acquisition or other change in control that stockholders may consider favorable, including transactions by which stockholders might otherwise receive a premium for their shares. These provisions also could limit the price that investors might be willing to pay in the future for shares of our common stock, thereby depressing the market price of our common stock. Stockholders who wish to participate in these transactions may not have the opportunity to do so. In addition, the provisions of Section 203 of the Delaware General Corporation Law also restrict certain business combinations with interested stockholders.

GENERAL RISK FACTORS

Our insurance policies may not cover all losses and costs to which we may be exposed, which could adversely impact our results of operations and financial condition.

We carry insurance in amounts and under terms that we believe are appropriate. Our insurance may not cover all liabilities and losses to which we may be exposed. Certain insurance coverage may not be available or may be prohibitively expensive in future periods. As our insurance policies come up for renewal, we may need to assume higher deductibles or pay higher premiums, which could have an adverse impact on our results of operations and financial condition.

14

We have goodwill and other intangible assets on our balance sheet that could become impaired, which could impact our results of operations and financial condition.

As of December 31, 2023, the Company had $829.2 million in intangible assets and goodwill. We cannot be certain that we will realize the value of such intangible assets. Our intangible assets may become impaired as a result of a variety of factors which could adversely affect our financial condition and results of operations.

SPECIAL NOTE ABOUT FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains statements that are, or may be considered to be, forward-looking statements within the meaning of The Private Securities Litigation Reform Act of 1995, as amended, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended (the "Exchange Act"). All statements that are not historical facts, including statements about our beliefs or expectations, are "forward-looking statements." These statements may be identified by such forward-looking terminology as "expect," "estimate," "intent," "plan," "intend," "believe," "anticipate," "may," "will," "should," "could," "continue," "project," "opportunity," "predict," "would," "potential," "future," "forecast," "guarantee," "assume," "likely," "target" or similar statements or variations of such terms.

Our forward-looking statements are based on a series of expectations, assumptions and projections about the Company and the markets in which we operate, are not guarantees of future results or performance, and involve substantial risks and uncertainty, including assumptions and projections concerning our assets under management, net asset inflows and outflows, operating cash flows, business plans and ability to borrow, for all future periods. All forward-looking statements contained in this Annual Report on Form 10-K are as of the date of this Annual Report on Form 10-K only.

We can give no assurance that such expectations or forward-looking statements will prove to be correct. Actual results may differ materially. We do not undertake or plan to update or revise any such forward-looking statements to reflect actual results, changes in plans, assumptions, estimates or projections, or other circumstances occurring after the date of this Annual Report on Form 10-K, even if such results, changes or circumstances make it clear that any forward-looking information will not be realized. If there are any future public statements or disclosures by us that modify or impact any of the forward-looking statements contained in or accompanying this Annual Report on Form 10-K, such statements or disclosures will be deemed to modify or supersede such statements in this Annual Report on Form 10-K.

Our business and our forward-looking statements involve substantial known and unknown risks and uncertainties, including those discussed under "Risk Factors" and "Management's Discussion and Analysis of Financial Condition and Results of Operations" in this Annual Report on Form 10-K, resulting from: (i) any reduction in our assets under management; (ii) inability to achieve the expected benefits of strategic transactions; (iii) withdrawal, renegotiation or termination of investment management agreements; (iv) damage to our reputation; (v) inability to satisfy financial debt covenants and required payments; (vi) inability to attract and retain key personnel; (vii) challenges from competition; (viii) adverse developments related to unaffiliated subadvisers; (ix) negative changes in key distribution relationships; (x) interruptions, breaches, or failures of technology systems; (xi) loss on our investments; (xii) lack of sufficient capital on satisfactory terms; (xiii) adverse regulatory and legal developments; (xiv) failure to comply with investment guidelines or other contractual requirements; (xv) adverse civil litigation, government investigations, or proceedings; (xvi) unfavorable changes in tax laws or limitations; (xvii) inability to make common stock dividend payments; (xviii) impediments from certain corporate governance provisions; (xix) losses or costs not covered by insurance; (xx) impairment of goodwill or other intangible assets; and other risks and uncertainties. Any occurrence of, or any material adverse change in, one or more risk factors or risks and uncertainties referred to in this Annual Report on Form 10-K and our other periodic reports filed with the SEC could materially and adversely affect our operations, financial results, cash flows, prospects and liquidity.

Certain other factors that may impact our continuing operations, prospects, financial results and liquidity, or that may cause actual results to differ from such forward-looking statements, are discussed or included in the Company's periodic reports filed with the SEC and are available on our website at www.virtus.com under "Investor Relations." You are urged to carefully consider all such factors.

| Item 1B. | Unresolved Staff Comments. | ||||

None.

15

| Item 1C. | Cybersecurity | ||||

Cybersecurity Strategy and Risk Management

We maintain a cybersecurity and information protection program that is supported by policies and procedures designed to protect our systems and assets and the Company’s sensitive or confidential business information, including that entrusted to us by our clients and business partners. Identifying and assessing cybersecurity risk is integrated into our overall enterprise risk management (“ERM”) processes. Our ERM processes consider cybersecurity threat risks alongside other company risks as part of our overall management activities. Cybersecurity risks related to our business are identified and managed though a multi-faceted approach utilizing various systems, controls, and processes.

We maintain a layered security architecture as a key part of our infrastructure design and utilize our employees and managed third-party service providers to help ensure a secure environment and safeguard against a variety of threats including malware, systems intrusions, unauthorized access, data loss and other security risks. We have implemented various technology products and associated procedures, including, among others, the following:

▪Firewall protection, operating system security patches, and multi-factor authentication;

▪System security agent software, which includes encryption, malware protection, patches and virus definitions;

▪Monitoring of computer systems for unauthorized use of or access to sensitive information;

▪Web content filtering;

▪Web and network vulnerability assessments and penetration testing;

▪Monitoring emerging laws and regulations related to data protection and information security;

▪Hosting in-house production systems in geographically dispersed locations that are backed up to alternate locations; and

▪Employee cybersecurity awareness training that includes regular phishing simulations.

As part of the above processes, we engage various professional services firms that use external third-party tools to assess our internal cybersecurity programs and compliance with applicable practices and standards. Our use of these third parties allows us to leverage specialized knowledge, insights and industry best practices.

The Company’s processes to identify material risks from cybersecurity threats associated with our use of third-party service providers are included within our service provider management policy. The policy provides guidelines in performing cyber risk assessments on our critical and material third party service providers during onboarding and periodically thereafter.

The assessment of cybersecurity incidents are integrated as part of the Company's business continuity and disaster recovery program (“BCDR”). Our BCDR includes an incident response protocol that provides a framework for the assessment, response, and recovery phases for any business disruption, including cybersecurity incidents. It also incorporates various event, incident and response teams that comprise the Company's information security, risk management, compliance, legal and other functions as needed in response to any cybersecurity incidents. Our incident response protocol also provides for reporting mechanisms to senior management and our Board of Directors in the event of a material cybersecurity incident.

We have not had a cybersecurity incident that has materially affected, or was reasonably likely to, materially affect, our business strategy, results of operations or financial condition. There are risks from cybersecurity threats that if they were to occur could materially affect our business strategy, results of operations or financial condition which are further discussed in Item 1A. “Risk Factors—Risks Related to our Industry, Business and Operations—We and our third-party service providers rely on numerous technology systems and any business interruption, security breach, or system failure could negatively impact our business and profitability” of this Annual Report on Form 10-K, which should be read in conjunction with the information in this section.

Cybersecurity Governance

Our Board of Directors ("Board") oversees our risk management processes, including our risks from cybersecurity threats. As part of its ongoing responsibilities, the Board receives recurring reports from management on the Company’s cybersecurity risk environment and regularly meets with management to review the risk landscape and discuss the steps taken by management to monitor and mitigate cyber exposures. In addition, from time to time, our Chief Technology Officer and Chief Information Security Officer (“CISO”) brief the Board on the cyber-threat landscape, our information security program and other related information technology topics.

The Company maintains an Enterprise Risk Committee (“ERC”), comprising the Company executives who lead day-to-day risk management, and whose efforts are supplemented by specific risk-related committees or teams. The ERC is a cross-

16

functional committee that focuses on identifying and managing operational risk throughout the organization, including cybersecurity threats. The ERC has integrated cybersecurity into key elements of the Company’s ERM framework, including our BCDR planning program and service provider management policy, and personnel from our information security, risk management, compliance and legal groups are a part of the assessment and response team for cybersecurity incidents and the evaluation of third-party cybersecurity risk.

Our cybersecurity systems, controls and processes are overseen by our cybersecurity information technology team which is managed by our CISO. Our CISO has over 25 years of experience in the information technology and cybersecurity field and is a Certified Information Systems Security Professional.

| Item 2. | Properties. | ||||

We lease our principal offices, which are located at One Financial Plaza, Hartford, CT 06103. In addition, we lease office space in California, Connecticut, Florida, Georgia, Illinois, Massachusetts, New Jersey, New York, Texas, Singapore and the UK.

| Item 3. | Legal Proceedings. | ||||

The information set forth in response to Item 103 of Regulation S-K under "Legal Proceedings" is incorporated by reference from Part II, Item 8. "Financial Statements and Supplementary Data," Note 12 "Commitments and Contingencies" of this Annual Report on Form 10-K.

| Item 4. | Mine Safety Disclosures. | ||||

Not applicable.

17

PART II

| Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. | ||||

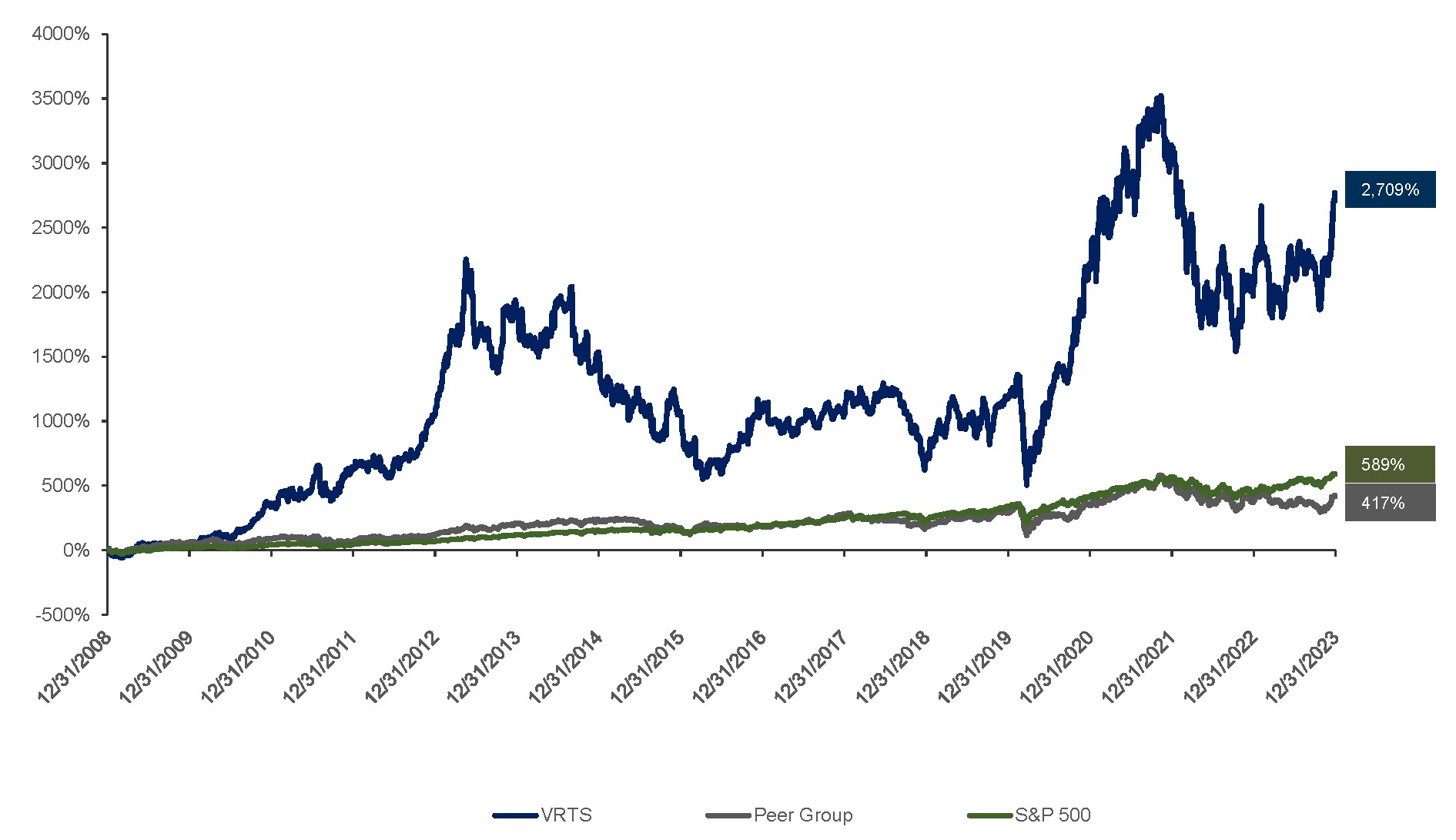

Our common stock is traded on the New York Stock Exchange under the trading symbol "VRTS." As of February 9, 2024, we had 7,087,728 shares of common stock outstanding that were held by approximately 39,000 holders of record.