UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-6452

Fidelity Union Street Trust II

(Exact name of registrant as specified in charter)

245 Summer St., Boston, MA 02210

(Address of principal executive offices) (Zip code)

Marc Bryant, Secretary

245 Summer St.

Boston, Massachusetts 02210

(Name and address of agent for service)

Registrant's telephone number, including area code:

617-563-7000

| Date of fiscal year end: | August 31 |

| | |

| Date of reporting period: | February 28, 2018 |

Item 1.

Reports to Stockholders

|

Fidelity® Arizona Municipal Income Fund Fidelity® Arizona Municipal Money Market Fund Semi-Annual Report February 28, 2018 |

|

Contents

|

Board Approval of Investment Advisory Contracts and Management Fees |

To view a fund's proxy voting guidelines and proxy voting record for the 12-month period ended June 30, visit http://www.fidelity.com/proxyvotingresults or visit the Securities and Exchange Commission's (SEC) web site at http://www.sec.gov.

You may also call 1-800-544-8544 to request a free copy of the proxy voting guidelines.

Standard & Poor's, S&P and S&P 500 are registered service marks of The McGraw-Hill Companies, Inc. and have been licensed for use by Fidelity Distributors Corporation.

Other third-party marks appearing herein are the property of their respective owners.

All other marks appearing herein are registered or unregistered trademarks or service marks of FMR LLC or an affiliated company. © 2018 FMR LLC. All rights reserved.

This report and the financial statements contained herein are submitted for the general information of the shareholders of the Fund. This report is not authorized for distribution to prospective investors in the Fund unless preceded or accompanied by an effective prospectus.

A fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. Forms N-Q are available on the SEC’s web site at http://www.sec.gov. A fund's Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information regarding the operation of the SEC's Public Reference Room may be obtained by calling 1-800-SEC-0330.

For a complete list of a fund's portfolio holdings, view the most recent holdings listing, semiannual report, or annual report on Fidelity's web site at http://www.fidelity.com, http://www.institutional.fidelity.com, or http://www.401k.com, as applicable.

NOT FDIC INSURED •MAY LOSE VALUE •NO BANK GUARANTEE

Neither the Fund nor Fidelity Distributors Corporation is a bank.

Fidelity® Arizona Municipal Income Fund

Investment Summary (Unaudited)

Top Five Sectors as of February 28, 2018

| % of fund's net assets | |

| Education | 25.2 |

| General Obligations | 17.1 |

| Health Care | 15.1 |

| Special Tax | 10.5 |

| Transportation | 8.3 |

Quality Diversification (% of fund's net assets)

| As of February 28, 2018 | ||

| AAA | 1.6% | |

| AA,A | 88.2% | |

| BBB | 6.4% | |

| Not Rated | 1.9% | |

| Short-Term Investments and Net Other Assets | 1.9% | |

We have used ratings from Moody's Investors Service, Inc. Where Moody's® ratings are not available, we have used S&P® ratings. All ratings are as of the date indicated and do not reflect subsequent changes.

Fidelity® Arizona Municipal Income Fund

Schedule of Investments February 28, 2018 (Unaudited)

Showing Percentage of Net Assets

| Municipal Bonds - 98.1% | |||

| Principal Amount | Value | ||

| Arizona - 97.5% | |||

| Arizona Board of Regents Arizona State Univ. Rev.: | |||

| (Arizona State Univ. Revs. Proj.) Series 2017 B, 5% 7/1/43 | $1,200,000 | $1,362,636 | |

| Series 2012 A: | |||

| 5% 7/1/26 | 550,000 | 615,439 | |

| 5% 7/1/26 (Pre-Refunded to 7/1/22 @ 100) | 450,000 | 505,125 | |

| Series 2015 A, 5% 7/1/35 | 2,215,000 | 2,512,275 | |

| Series 2015 B, 5% 7/1/31 | 1,525,000 | 1,749,160 | |

| Series 2015 D: | |||

| 5% 7/1/34 | 500,000 | 568,520 | |

| 5% 7/1/35 | 900,000 | 1,020,789 | |

| 5% 7/1/41 | 485,000 | 545,329 | |

| 5% 7/1/46 | 3,000,000 | 3,362,730 | |

| Arizona Board of Regents Ctfs. of Prtn. (Univ. of Arizona Projs.) Series 2012 C, 5% 6/1/26 | 3,035,000 | 3,368,577 | |

| Arizona Ctfs. of Prtn.: | |||

| Series 2010 A, 5% 10/1/29 (FSA Insured) | 5,000,000 | 5,245,747 | |

| Series 2013 A, 5% 10/1/25 | 1,870,000 | 2,081,385 | |

| Series 2015, 5% 9/1/27 | 1,500,000 | 1,737,150 | |

| Series 2016, 5% 10/1/21 | 500,000 | 553,400 | |

| Arizona Game and Fish Dept. and Commission (AGF Administration Bldg. Proj.) Series 2006: | |||

| 5% 7/1/21 | 1,280,000 | 1,283,635 | |

| 5% 7/1/32 | 470,000 | 471,213 | |

| Arizona Health Facilities Auth. Hosp. Sys. Rev. Series 2012 A, 5% 2/1/23 | 1,285,000 | 1,407,563 | |

| Arizona Health Facilities Auth. Rev.: | |||

| (Banner Health Sys. Proj.) Series 2007 B, 3 month U.S. LIBOR + 0.810% 1.945%, tender 1/1/37 (a)(b) | 1,000,000 | 921,060 | |

| (Scottsdale Lincoln Hospitals Proj.) Series 2014 A: | |||

| 5% 12/1/26 | 2,000,000 | 2,277,960 | |

| 5% 12/1/42 | 2,020,000 | 2,226,101 | |

| Series 2011 B1, 5.25% 3/1/39 | 1,000,000 | 1,071,570 | |

| Series 2012 A, 5% 1/1/43 | 3,500,000 | 3,765,475 | |

| Arizona State Trans. Board: | |||

| Series 2017 A, 5% 7/1/32 | 1,500,000 | 1,758,510 | |

| Series 2017A, 5% 7/1/31 | 385,000 | 452,729 | |

| Arizona Wtr. Infrastructure Fin. Auth. Rev. Series A, 5% 10/1/28 | 2,000,000 | 2,309,480 | |

| Avondale Muni. Dev. Corp. Excise Tax Rev. 5% 7/1/28 (Pre-Refunded to 7/1/18 @ 100) | 500,000 | 505,955 | |

| Buckeye Excise Tax Rev. Series 2015: | |||

| 5% 7/1/27 | 350,000 | 406,231 | |

| 5% 7/1/28 | 500,000 | 577,440 | |

| 5% 7/1/29 | 455,000 | 522,204 | |

| Central Wtr. Conservation District (Central Arizona Proj.) Series 2016 A, 5% 1/1/36 | 500,000 | 565,580 | |

| Dysart Unified School District #89 Gen. Oblig. Series 2014: | |||

| 5% 7/1/23 | 700,000 | 797,300 | |

| 5% 7/1/27 | 1,300,000 | 1,471,262 | |

| Glendale Gen. Oblig.: | |||

| Series 2015, 5% 7/1/22 (FSA Insured) | 1,000,000 | 1,119,860 | |

| Series 2017, 5% 7/1/32 | 1,000,000 | 1,154,640 | |

| Glendale Indl. Dev. Auth. (Midwestern Univ. Proj.) Series 2007, 5.25% 5/15/19 | 1,000,000 | 1,040,600 | |

| Glendale Sr. Excise Tax Rev. Series 2015 A, 5% 7/1/28 | 1,000,000 | 1,147,700 | |

| Goodyear Pub. Impt. Corp. Facilities Rev. Series 2016 A, 5% 7/1/29 | 1,000,000 | 1,155,990 | |

| Maricopa County Indl. Dev. Auth. Health Facilities Rev. (Catholic Healthcare West Proj.) Series 2009 A, 6% 7/1/39 | 1,000,000 | 1,047,780 | |

| Maricopa County Indl. Dev. Auth. Rev. Series 2016 A: | |||

| 5% 1/1/34 | 3,000,000 | 3,414,900 | |

| 5% 1/1/38 | 1,215,000 | 1,363,145 | |

| Maricopa County Indl. Dev. Auth. Sr. Living Facilities Series 2016: | |||

| 5.75% 1/1/36 (c) | 250,000 | 252,215 | |

| 6% 1/1/48 (c) | 250,000 | 253,565 | |

| Maricopa County Phoenix Union High School District #210 Series E, 5% 7/1/22 | 1,000,000 | 1,124,710 | |

| Maricopa County School District #28 Kyrene Elementary: | |||

| Series 2010 B: | |||

| 5.25% 7/1/28 (Pre-Refunded to 7/1/23 @ 100) | 690,000 | 801,697 | |

| 5.5% 7/1/29 (Pre-Refunded to 7/1/23 @ 100) | 480,000 | 563,736 | |

| 5.5% 7/1/30 (Pre-Refunded to 7/1/23 @ 100) | 400,000 | 469,780 | |

| Series 2010 C, 4% 7/1/29 | 650,000 | 691,145 | |

| Maricopa County Unified School District #48 Scottsdale Series 2017 B, 5% 7/1/33 | 3,000,000 | 3,503,640 | |

| Maricopa School District # 214 (High School Inprovement Proj.) Series 2018 A, 5% 7/1/31 | 350,000 | 410,176 | |

| McAllister Academic Village LLC Rev.: | |||

| (Arizona State Univ. Hassayampa Academic Village Proj.) Series 2016: | |||

| 5% 7/1/37 | 2,000,000 | 2,269,160 | |

| 5% 7/1/38 | 3,850,000 | 4,362,127 | |

| Series 2016, 5% 7/1/39 | 2,270,000 | 2,568,392 | |

| Mesa Util. Sys. Rev. Series 2017, 4% 7/1/25 | 2,000,000 | 2,206,800 | |

| Northern Arizona Univ. Ctfs. of Prtn.: | |||

| (Univ. Proj.) Series 2013, 5% 9/1/24 | 1,000,000 | 1,101,690 | |

| Series 2015, 5% 9/1/20 (FSA Insured) | 440,000 | 473,224 | |

| Northern Arizona Univ. Revs.: | |||

| Series 2012: | |||

| 5% 6/1/36 | 860,000 | 918,299 | |

| 5% 6/1/41 | 1,250,000 | 1,333,538 | |

| Series 2013, 5% 8/1/27 | 1,000,000 | 1,118,310 | |

| Series 2014, 5% 6/1/29 | 500,000 | 558,675 | |

| Series 2015, 5% 6/1/30 | 1,000,000 | 1,139,840 | |

| Phoenix Civic Impt. Board Arpt. Rev.: | |||

| Series 2013: | |||

| 5% 7/1/26 (d) | 1,100,000 | 1,228,260 | |

| 5% 7/1/29 (d) | 500,000 | 555,145 | |

| Series 2015 A, 5% 7/1/45 | 4,100,000 | 4,564,489 | |

| Series 2017 A, 5% 7/1/35 (d) | 2,425,000 | 2,751,575 | |

| Series 2017 D, 5% 7/1/31 | 2,000,000 | 2,321,600 | |

| Phoenix Civic Impt. Corp. District Rev. (Plaza Expansion Proj.) Series 2005 B, 5.5% 7/1/38 (Nat'l. Pub. Fin. Guarantee Corp. Insured) | 2,000,000 | 2,511,120 | |

| Phoenix Civic Impt. Corp. Wastewtr. Sys. Rev. Series 2016, 5% 7/1/33 | 1,000,000 | 1,151,990 | |

| Phoenix Gen. Oblig. Series 2014, 4% 7/1/26 | 2,000,000 | 2,185,620 | |

| Phoenix-Mesa Gateway Arpt. Auth. (Mesa Proj.) Series 2012: | |||

| 5% 7/1/24 (d) | 380,000 | 421,386 | |

| 5% 7/1/27 (d) | 400,000 | 437,004 | |

| Pima County Ctfs. of Prtn.: | |||

| Series 2013 A, 5% 12/1/22 | 1,000,000 | 1,121,690 | |

| Series 2014, 5% 12/1/27 | 1,745,000 | 1,946,443 | |

| Pima County Swr. Sys. Rev.: | |||

| Series 2011 B, 5% 7/1/22 | 1,050,000 | 1,158,476 | |

| Series 2012 A: | |||

| 5% 7/1/23 | 30,000 | 33,689 | |

| 5% 7/1/25 | 1,600,000 | 1,790,368 | |

| 5% 7/1/26 | 1,000,000 | 1,117,660 | |

| Salt River Proj. Agricultural Impt. & Pwr. District Elec. Sys. Rev.: | |||

| (Arizona Salt River Proj.) Series A: | |||

| 5% 1/1/31 | 3,000,000 | 3,520,770 | |

| 5% 1/1/38 | 1,000,000 | 1,149,920 | |

| Series 2015 A: | |||

| 5% 12/1/34 | 1,500,000 | 1,711,860 | |

| 5% 12/1/45 | 1,035,000 | 1,163,143 | |

| Series 2017 A, 5% 1/1/33 | 1,000,000 | 1,180,340 | |

| Salt Verde Finl. Corp. Sr. Gas Rev. Series 2007: | |||

| 5% 12/1/37 | 1,500,000 | 1,755,240 | |

| 5.5% 12/1/29 | 3,000,000 | 3,592,890 | |

| Scottsdale Gen. Oblig. Series 2017, 4% 7/1/32 | 400,000 | 429,632 | |

| Scottsdale Indl. Dev. Auth. Hosp. Rev. (Scottsdale Healthcare Proj.): | |||

| Series 2006 C, 5% 9/1/35 (FSA Insured) | 420,000 | 448,211 | |

| Series 2008 A, 5% 9/1/23 | 355,000 | 360,364 | |

| Scottsdale Muni. Property Corp. Excise Tax Rev.: | |||

| Series 2015, 5% 7/1/34 | 1,355,000 | 1,547,410 | |

| Series 2017, 5% 7/1/31 | 4,320,000 | 5,118,898 | |

| Surprise Pledged Rev. Series 2015, 5% 7/1/26 | 1,010,000 | 1,176,660 | |

| Tempe Excise Tax Rev.: | |||

| Series 2012, 5% 7/1/25 | 1,090,000 | 1,225,934 | |

| Series 2016: | |||

| 5% 7/1/28 | 315,000 | 368,204 | |

| 5% 7/1/29 | 500,000 | 582,020 | |

| 5% 7/1/30 | 325,000 | 376,740 | |

| 5% 7/1/31 | 375,000 | 433,196 | |

| Tempe Indl. Dev. Auth. Rev. (Mirabella At Asu, Inc. Proj.) Series 2017 B, 6% 10/1/37 (c) | 500,000 | 510,930 | |

| Tempe Transit Excise Tax Rev. Series 2008: | |||

| 4.75% 7/1/38 | 35,000 | 35,347 | |

| 4.75% 7/1/38 (Pre-Refunded to 7/1/18 @ 100) | 25,000 | 25,286 | |

| Tucson Ctfs. of Prtn.: | |||

| Series 2014: | |||

| 4% 7/1/20 (FSA Insured) | 500,000 | 525,335 | |

| 5% 7/1/28 (FSA Insured) | 1,000,000 | 1,127,400 | |

| Series 2015, 5% 7/1/23 (FSA Insured) | 555,000 | 630,652 | |

| Series 2016, 5% 7/1/27 (FSA Insured) | 1,245,000 | 1,437,216 | |

| Tucson Wtr. Rev.: | |||

| Series 2015, 5% 7/1/31 | 1,000,000 | 1,146,990 | |

| Series 2017, 5% 7/1/34 | 1,000,000 | 1,163,450 | |

| 5% 7/1/27 | 1,000,000 | 1,165,010 | |

| 5% 7/1/28 | 2,000,000 | 2,319,860 | |

| Univ. Med. Ctr. Corp. Hosp. Rev. 5.625% 7/1/36 (Pre-Refunded to 7/1/23 @ 100) | 1,000,000 | 1,172,450 | |

| Univ. of Arizona Univ. Revs.: | |||

| Series 2012 A, 5% 6/1/37 | 2,225,000 | 2,457,201 | |

| Series 2014, 5% 8/1/28 | 1,000,000 | 1,139,020 | |

| Series 2015 A 5% 6/1/30 | 2,500,000 | 2,870,750 | |

| 5% 6/1/38 | 2,000,000 | 2,269,900 | |

| 5% 6/1/39 | 1,910,000 | 2,164,794 | |

| Yavapai County Indl. Dev. Auth.: | |||

| (Northern Healthcare Sys. Proj.) Series 2011, 5% 10/1/20 | 1,000,000 | 1,081,000 | |

| Series 2012 A, 5.25% 8/1/33 | 2,000,000 | 2,200,180 | |

| Series 2016, 5% 8/1/36 | 1,305,000 | 1,410,000 | |

| Yuma Indl. Dev. Auth. Hosp. Rev. Series 2014 A, 5% 8/1/27 | 2,000,000 | 2,260,400 | |

| TOTAL ARIZONA | 166,135,982 | ||

| Guam - 0.6% | |||

| Guam Int'l. Arpt. Auth. Rev. Series 2013 C: | |||

| 5% 10/1/18 (d) | 300,000 | 304,575 | |

| 6.375% 10/1/43 (d) | 200,000 | 227,382 | |

| Guam Pwr. Auth. Rev. Series 2012 A, 5% 10/1/21 (FSA Insured) | 400,000 | 436,636 | |

| TOTAL GUAM | 968,593 | ||

| TOTAL MUNICIPAL BONDS | |||

| (Cost $164,911,686) | 167,104,575 | ||

| TOTAL INVESTMENT IN SECURITIES - 98.1% | |||

| (Cost $164,911,686) | 167,104,575 | ||

| NET OTHER ASSETS (LIABILITIES) - 1.9% | 3,317,534 | ||

| NET ASSETS - 100% | $170,422,109 |

Legend

(a) Coupon rates for floating and adjustable rate securities reflect the rates in effect at period end.

(b) Coupon is indexed to a floating interest rate which may be multiplied by a specified factor and/or subject to caps or floors.

(c) Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers. At the end of the period, the value of these securities amounted to $1,016,710 or 0.6% of net assets.

(d) Private activity obligations whose interest is subject to the federal alternative minimum tax for individuals.

Investment Valuation

All investments are categorized as Level 2 under the Fair Value Hierarchy. The inputs or methodology used for valuing securities may not be an indication of the risk associated with investing in those securities. For more information on valuation inputs please refer to the Investment Valuation section in the accompanying Notes to Financial Statements.

Other Information

The distribution of municipal securities by revenue source, as a percentage of total Net Assets, is as follows (Unaudited):

| Education | 25.2% |

| General Obligations | 17.1% |

| Health Care | 15.1% |

| Special Tax | 10.5% |

| Transportation | 8.3% |

| Water & Sewer | 8.3% |

| Electric Utilities | 6.8% |

| Others* (Individually Less Than 5%) | 8.7% |

| 100.0% |

* Includes net other assets

See accompanying notes which are an integral part of the financial statements.

Fidelity® Arizona Municipal Income Fund

Financial Statements

Statement of Assets and Liabilities

| February 28, 2018 (Unaudited) | ||

| Assets | ||

| Investment in securities, at value — See accompanying schedule: Unaffiliated issuers (cost $164,911,686) | $167,104,575 | |

| Cash | 2,594,147 | |

| Receivable for fund shares sold | 7,009 | |

| Interest receivable | 1,530,481 | |

| Other receivables | 443 | |

| Total assets | 171,236,655 | |

| Liabilities | ||

| Payable for investments purchased | $410,536 | |

| Payable for fund shares redeemed | 203,695 | |

| Distributions payable | 121,112 | |

| Accrued management fee | 79,203 | |

| Total liabilities | 814,546 | |

| Net Assets | $170,422,109 | |

| Net Assets consist of: | ||

| Paid in capital | $168,072,067 | |

| Undistributed net investment income | 23,675 | |

| Accumulated undistributed net realized gain (loss) on investments | 133,478 | |

| Net unrealized appreciation (depreciation) on investments | 2,192,889 | |

| Net Assets, for 14,475,751 shares outstanding | $170,422,109 | |

| Net Asset Value, offering price and redemption price per share ($170,422,109 ÷ 14,475,751 shares) | $11.77 |

See accompanying notes which are an integral part of the financial statements.

Statement of Operations

| Six months ended February 28, 2018 (Unaudited) | ||

| Investment Income | ||

| Interest | $2,687,861 | |

| Expenses | ||

| Management fee | $491,040 | |

| Independent trustees' fees and expenses | 339 | |

| Miscellaneous | 260 | |

| Total expenses before reductions | 491,639 | |

| Expense reductions | (1,145) | 490,494 |

| Net investment income (loss) | 2,197,367 | |

| Realized and Unrealized Gain (Loss) | ||

| Net realized gain (loss) on: | ||

| Investment securities: | ||

| Unaffiliated issuers | 540,166 | |

| Total net realized gain (loss) | 540,166 | |

| Change in net unrealized appreciation (depreciation) on investment securities | (5,872,008) | |

| Net gain (loss) | (5,331,842) | |

| Net increase (decrease) in net assets resulting from operations | $(3,134,475) |

See accompanying notes which are an integral part of the financial statements.

Statement of Changes in Net Assets

| Six months ended February 28, 2018 (Unaudited) | Year ended August 31, 2017 | |

| Increase (Decrease) in Net Assets | ||

| Operations | ||

| Net investment income (loss) | $2,197,367 | $4,591,618 |

| Net realized gain (loss) | 540,166 | 1,044,744 |

| Change in net unrealized appreciation (depreciation) | (5,872,008) | (5,535,598) |

| Net increase (decrease) in net assets resulting from operations | (3,134,475) | 100,764 |

| Distributions to shareholders from net investment income | (2,195,026) | (4,576,975) |

| Distributions to shareholders from net realized gain | (1,204,002) | (370,311) |

| Total distributions | (3,399,028) | (4,947,286) |

| Share transactions | ||

| Proceeds from sales of shares | 12,646,706 | 33,452,973 |

| Reinvestment of distributions | 2,178,203 | 3,162,383 |

| Cost of shares redeemed | (19,609,304) | (42,753,902) |

| Net increase (decrease) in net assets resulting from share transactions | (4,784,395) | (6,138,546) |

| Redemption fees | – | 71 |

| Total increase (decrease) in net assets | (11,317,898) | (10,984,997) |

| Net Assets | ||

| Beginning of period | 181,740,007 | 192,725,004 |

| End of period | $170,422,109 | $181,740,007 |

| Other Information | ||

| Undistributed net investment income end of period | $23,675 | $21,334 |

| Shares | ||

| Sold | 1,050,192 | 2,771,855 |

| Issued in reinvestment of distributions | 181,656 | 262,497 |

| Redeemed | (1,635,986) | (3,572,932) |

| Net increase (decrease) | (404,138) | (538,580) |

See accompanying notes which are an integral part of the financial statements.

Financial Highlights

Fidelity Arizona Municipal Income Fund

| Six months ended (Unaudited) February 28, | Years endedAugust 31, | |||||

| 2018 | 2017 | 2016 | 2015 | 2014 | 2013 | |

| Selected Per–Share Data | ||||||

| Net asset value, beginning of period | $12.21 | $12.50 | $12.12 | $12.11 | $11.31 | $12.19 |

| Income from Investment Operations | ||||||

| Net investment income (loss)A | .148 | .311 | .335 | .375 | .399 | .382 |

| Net realized and unrealized gain (loss) | (.359) | (.267) | .498 | .018 | .831 | (.855) |

| Total from investment operations | (.211) | .044 | .833 | .393 | 1.230 | (.473) |

| Distributions from net investment income | (.148) | (.310) | (.335) | (.375) | (.398) | (.382) |

| Distributions from net realized gain | (.081) | (.024) | (.118) | (.008) | (.032) | (.025) |

| Total distributions | (.229) | (.334) | (.453) | (.383) | (.430) | (.407) |

| Redemption fees added to paid in capitalA | – | –B | –B | –B | –B | –B |

| Net asset value, end of period | $11.77 | $12.21 | $12.50 | $12.12 | $12.11 | $11.31 |

| Total ReturnC,D | (1.75)% | .43% | 7.01% | 3.28% | 11.06% | (4.03)% |

| Ratios to Average Net AssetsE | ||||||

| Expenses before reductions | .55%F | .55% | .55% | .55% | .55% | .55% |

| Expenses net of fee waivers, if any | .55%F | .55% | .55% | .55% | .55% | .55% |

| Expenses net of all reductions | .55%F | .55% | .55% | .55% | .55% | .55% |

| Net investment income (loss) | 2.48%F | 2.58% | 2.73% | 3.08% | 3.40% | 3.16% |

| Supplemental Data | ||||||

| Net assets, end of period (000 omitted) | $170,422 | $181,740 | $192,725 | $150,985 | $145,784 | $156,049 |

| Portfolio turnover rate | 15%F | 18% | 7% | 17% | 8% | 20% |

A Calculated based on average shares outstanding during the period.

B Amount represents less than $.0005 per share.

C Total returns for periods of less than one year are not annualized.

D Total returns would have been lower if certain expenses had not been reduced during the applicable periods shown.

E Expense ratios reflect operating expenses of the Fund. Expenses before reductions do not reflect amounts reimbursed by the investment adviser or reductions from expense offset arrangements and do not represent the amount paid by the Fund during periods when reimbursements or reductions occur. Expenses net of fee waivers reflect expenses after reimbursement by the investment adviser but prior to reductions from expense offset arrangements. Expenses net of all reductions represent the net expenses paid by the Fund.

F Annualized

See accompanying notes which are an integral part of the financial statements.

Fidelity® Arizona Municipal Money Market Fund

Investment Summary/Performance (Unaudited)

Effective Maturity Diversification as of February 28, 2018

| Days | % of fund's investments 2/28/18 |

| 1 - 7 | 93.1 |

| 8 - 30 | 0.2 |

| 31 - 60 | 1.3 |

| 61 - 90 | 0.2 |

| 91 - 180 | 4.9 |

| > 180 | 0.3 |

Effective maturity is determined in accordance with the requirements of Rule 2a-7 under the Investment Company Act of 1940.

Asset Allocation (% of fund's net assets)

| As of February 28, 2018 | ||

| Variable Rate Demand Notes (VRDNs) | 67.5% | |

| Tender Option Bond | 14.2% | |

| Other Municipal Security | 6.7% | |

| Investment Companies | 11.5% | |

| Net Other Assets (Liabilities) | 0.1% | |

Current 7-Day Yield

| 2/28/18 | |

| Fidelity® Arizona Municipal Money Market Fund | 0.63% |

Yield refers to the income paid by the Fund over a given period. Yield for money market funds is usually for seven-day periods, as it is here, though it is expressed as an annual percentage rate. Past performance is no guarantee of future results. Yield will vary and it's possible to lose money investing in the Fund.

Fidelity® Arizona Municipal Money Market Fund

Schedule of Investments February 28, 2018 (Unaudited)

Showing Percentage of Net Assets

| Variable Rate Demand Note - 67.5% | |||

| Principal Amount | Value | ||

| Alabama - 0.2% | |||

| Decatur Indl. Dev. Board Exempt Facilities Rev. (Nucor Steel Decatur LLC Proj.) Series 2003 A, 1.43% 3/7/18, VRDN (a)(b) | $300,000 | $300,000 | |

| Arizona - 65.5% | |||

| Arizona Health Facilities Auth. Rev. (Catholic Healthcare West Proj.) Series 2009 F, 1.16% 3/7/18, LOC Mizuho Corporate Bank Ltd., VRDN (a) | 15,600,000 | 15,600,000 | |

| Coconino County Poll. Cont. Corp. Rev. (Tucson Elec. Pwr. Co. Navajo Proj.) Series 2010 A, 1.17% 3/7/18, LOC JPMorgan Chase Bank, VRDN (a)(b) | 5,700,000 | 5,700,000 | |

| Maricopa County Poll. Cont. Rev. (Arizona Pub. Svc. Co. Palo Verde Proj.) Series 2009 A, 1.17% 3/7/18, VRDN (a) | 12,500,000 | 12,500,000 | |

| Phoenix Indl. Dev. Auth. Rev. (Independent Newspaper, Inc. Proj.) Series 2000, 1.32% 3/7/18, LOC Wells Fargo Bank NA, VRDN (a)(b) | 375,000 | 375,000 | |

| FHLMC Phoenix Indl. Dev. Auth. Multi-family Hsg. Rev. (Del Mar Terrace Apts. Proj.) Series 1999 A, 1.15% 3/7/18, LOC Freddie Mac, VRDN (a) | 6,200,000 | 6,200,000 | |

| FNMA: | |||

| Arizona Hsg. Fin. Auth. Multi-family Hsg. Rev. (Santa Carolina Apts. Proj.) Series 2005, 1.15% 3/7/18, LOC Fannie Mae, VRDN (a)(b) | 3,645,000 | 3,645,000 | |

| Maricopa County Indl. Dev. Auth. Multi-family Hsg. Rev.: | |||

| (Glenn Oaks Apts. Proj.) Series 2001, 1.2% 3/7/18, LOC Fannie Mae, VRDN (a)(b) | 4,520,000 | 4,520,000 | |

| (Ranchwood Apts. Proj.) Series 2001 A, 1.2% 3/7/18, LOC Fannie Mae, VRDN (a)(b) | 1,250,000 | 1,250,000 | |

| (San Angelin Apts. Proj.) Series 2004, 1.17% 3/7/18, LOC Fannie Mae, VRDN (a)(b) | 8,900,000 | 8,900,000 | |

| (San Martin Apts. Proj.) Series A2, 1.17% 3/7/18, LOC Fannie Mae, VRDN (a)(b) | 4,300,000 | 4,300,000 | |

| (San Remo Apts. Proj.) Series 2002, 1.17% 3/7/18, LOC Fannie Mae, VRDN (a)(b) | 7,000,000 | 7,000,000 | |

| (Village Square Apts. Proj.) Series 2004, 1.17% 3/7/18, LOC Fannie Mae, VRDN (a)(b) | 3,500,000 | 3,500,000 | |

| Pima County Indl. Dev. Auth. Multi-family Hsg. Rev.: | |||

| (River Point Proj.) Series 2001, 1.2% 3/7/18, LOC Fannie Mae, VRDN (a)(b) | 4,895,000 | 4,895,000 | |

| Series A, 1.16% 3/7/18, LOC Fannie Mae, VRDN (a)(b) | 3,030,000 | 3,030,000 | |

| 81,415,000 | |||

| Arkansas - 0.2% | |||

| Osceola Solid Waste Disp. Rev. (Plum Point Energy Associates, LLC Proj.) Series 2006, 1.3% 3/7/18, LOC Royal Bank of Scotland PLC, VRDN (a)(b) | 300,000 | 300,000 | |

| Indiana - 1.0% | |||

| Indiana Dev. Fin. Auth. Envir. Rev. (PSI Energy Proj.) Series 2003 B, 1.26% 3/7/18, VRDN (a)(b) | 1,180,000 | 1,180,000 | |

| Nebraska - 0.2% | |||

| Stanton County Indl. Dev. Rev. (Nucor Corp. Proj.) Series 1996, 1.43% 3/7/18, VRDN (a)(b) | 200,000 | 200,000 | |

| North Carolina - 0.1% | |||

| Hertford County Indl. Facilities Poll. Cont. Fing. Auth. (Nucor Corp. Proj.) Series 2000 A, 1.36% 3/7/18, VRDN (a)(b) | 100,000 | 100,000 | |

| West Virginia - 0.3% | |||

| West Virginia Econ. Dev. Auth. Solid Waste Disp. Facilities Rev. (Appalachian Pwr. Co.- Mountaineer Proj.) Series 2008 A, 1.32% 3/7/18, VRDN (a)(b) | 400,000 | 400,000 | |

| TOTAL VARIABLE RATE DEMAND NOTE | |||

| (Cost $83,895,000) | 83,895,000 | ||

| Tender Option Bond - 14.2% | |||

| Arizona - 12.1% | |||

| Arizona Board of Regents Arizona State Univ. Rev. Participating VRDN Series 33 85X, 1.12% 3/7/18 (Liquidity Facility Morgan Stanley Bank, West Valley City Utah) (a)(c) | 5,665,000 | 5,665,000 | |

| Mesa Util. Sys. Rev.: | |||

| Bonds Series Solar 17 0026, SIFMA Municipal Swap Index + 0.050% 1.14%, tender 3/1/18 (Liquidity Facility U.S. Bank NA, Cincinnati) (a)(c)(d) | 1,890,000 | 1,890,000 | |

| Participating VRDN Series ROC II R 11959X, 1.12% 3/7/18 (Liquidity Facility Citibank NA) (a)(c) | 1,500,000 | 1,500,000 | |

| Rowan Univ. Participating VRDN Series 2016 XF 2337, 1.13% 3/7/18 (Liquidity Facility Barclays Bank PLC) (a)(c) | 3,400,000 | 3,400,000 | |

| Salt River Proj. Agricultural Impt. & Pwr. District Elec. Sys. Rev. Participating VRDN Series Floaters XF 21 92, 1.12% 3/7/18 (Liquidity Facility Morgan Stanley Bank, West Valley City Utah) (a)(c) | 2,600,000 | 2,600,000 | |

| 15,055,000 | |||

| Colorado - 0.1% | |||

| Colorado Health Facilities Auth. Rev. Participating VRDN Series Floaters XF 22 41, 1.19% 3/7/18 (Liquidity Facility Citibank NA) (a)(c) | 100,000 | 100,000 | |

| Florida - 0.6% | |||

| Central Fla Expwy Auth. Rev. Participating VRDN Series Floaters 004, 1.27% 4/11/18 (Liquidity Facility Barclays Bank PLC) (a)(c)(e) | 500,000 | 500,000 | |

| Central Florida Expressway Bonds Series RBC E 62, SIFMA Municipal Swap Index + 0.170% 1.26%, tender 5/1/18 (Liquidity Facility Royal Bank of Canada) (a)(c)(d)(e) | 300,000 | 300,000 | |

| 800,000 | |||

| Illinois - 0.5% | |||

| Chicago Board of Ed. Participating VRDN Series Floaters 003, 1.34% 4/11/18 (Liquidity Facility Barclays Bank PLC) (a)(c)(e) | 600,000 | 600,000 | |

| Montana - 0.5% | |||

| Missoula Mont Wtr. Sys. Rev. Participating VRDN Series Floaters 011, 1.27% 4/11/18 (Liquidity Facility Barclays Bank PLC) (a)(c)(e) | 600,000 | 600,000 | |

| New Jersey - 0.1% | |||

| New Jersey St. Trans. Trust Fund Auth. Participating VRDN Series Floaters 16 XF1059, 1.26% 3/7/18 (Liquidity Facility Deutsche Bank AG New York Branch) (a)(c) | 100,000 | 100,000 | |

| Ohio - 0.1% | |||

| Middletown Hosp. Facilities Rev. Participating VRDN Series Floaters 00 31 44, 1.27% 4/11/18 (Liquidity Facility Barclays Bank PLC) (a)(c)(e) | 95,000 | 95,000 | |

| Ohio Higher Edl. Facility Commission Rev. Participating VRDN Series 2017, 1.27% 4/11/18 (Liquidity Facility Barclays Bank PLC) (a)(c)(e) | 100,000 | 100,000 | |

| 195,000 | |||

| Pennsylvania - 0.2% | |||

| Berks County Muni. Auth. Rev. Participating VRDN Series Floaters 001, 1.27% 4/11/18 (Liquidity Facility Barclays Bank PLC) (a)(c)(e) | 100,000 | 100,000 | |

| Pennsylvania Higher Edl. Facilities Auth. Bonds Series 2016 E75, SIFMA Municipal Swap Index + 0.170% 1.26%, tender 4/2/18 (Liquidity Facility Royal Bank of Canada) (a)(c)(d)(e) | 100,000 | 100,000 | |

| 200,000 | |||

| TOTAL TENDER OPTION BOND | |||

| (Cost $17,650,000) | 17,650,000 | ||

| Other Municipal Security - 6.7% | |||

| Arizona - 6.3% | |||

| Arizona Board of Regents Ctfs. of Prtn. Bonds (Univ. of Arizona Univ. Revs.) Series 2018A, 5% 6/1/18 | 1,000,000 | 1,009,094 | |

| Arizona Health Facilities Auth. Rev. Bonds (Banner Health Sys. Proj.) Series 2015 A, 5% 1/1/19 | 400,000 | 411,725 | |

| Phoenix Civic Impt. Board Arpt. Rev. Bonds: | |||

| Series 2008 A: | |||

| 5% 7/1/18 (Pre-Refunded to 7/1/18 @ 100) | 1,000,000 | 1,011,875 | |

| 5% 7/1/18 (Pre-Refunded to 7/1/18 @ 100) | 1,300,000 | 1,315,485 | |

| Series 2017, 5% 7/1/18 (b) | 1,760,000 | 1,782,478 | |

| Salt River Proj. Agricultural Impt. & Pwr. District Elec. Sys. Rev. Series C, 1.13% 3/5/18, CP | 1,300,000 | 1,300,000 | |

| Scottsdale Gen. Oblig. Bonds Series 2014, 3% 7/1/18 | 1,000,000 | 1,006,202 | |

| 7,836,859 | |||

| Kentucky - 0.1% | |||

| Jefferson County Poll. Cont. Rev. Bonds Series 2001 A, 1.32% tender 4/6/18, CP mode | 100,000 | 100,000 | |

| New Hampshire - 0.1% | |||

| New Hampshire Bus. Fin. Auth. Poll. Cont. Rev. Bonds (New England Pwr. Co. Proj.) Series B, 1.45% tender 3/1/18, CP mode | 200,000 | 200,000 | |

| West Virginia - 0.2% | |||

| Grant County Cmnty. Solid Waste Disp. Rev. Bonds Series 96, 1.3% tender 3/28/18, CP mode (b) | 200,000 | 200,000 | |

| TOTAL OTHER MUNICIPAL SECURITY | |||

| (Cost $8,336,859) | 8,336,859 | ||

| Shares | Value | ||

| Investment Company - 11.5% | |||

| Fidelity Municipal Cash Central Fund, 1.18%(f)(g) | |||

| (Cost $14,374,869) | 14,373,460 | 14,374,869 | |

| TOTAL INVESTMENT IN SECURITIES - 99.9% | |||

| (Cost $124,256,728) | 124,256,728 | ||

| NET OTHER ASSETS (LIABILITIES) - 0.1% | 86,913 | ||

| NET ASSETS - 100% | $124,343,641 |

Security Type Abbreviations

CP – COMMERCIAL PAPER

VRDN – VARIABLE RATE DEMAND NOTE (A debt instrument that is payable upon demand, either daily, weekly or monthly)

Legend

(a) Coupon rates for floating and adjustable rate securities reflect the rates in effect at period end.

(b) Private activity obligations whose interest is subject to the federal alternative minimum tax for individuals.

(c) Provides evidence of ownership in one or more underlying municipal bonds.

(d) Coupon is indexed to a floating interest rate which may be multiplied by a specified factor and/or subject to caps or floors.

(e) Restricted securities - Investment in securities not registered under the Securities Act of 1933 (excluding 144A issues). At the end of the period, the value of restricted securities (excluding 144A issues) amounted to $2,395,000 or 1.9% of net assets.

(f) Information in this report regarding holdings by state and security types does not reflect the holdings of the Fidelity Municipal Cash Central Fund.

(g) Affiliated fund that is available only to investment companies and other accounts managed by Fidelity Investments. The rate quoted is the annualized seven-day yield of the fund at period end. A complete unaudited listing of the fund's holdings as of its most recent quarter end is available upon request. In addition, each Fidelity Central Fund's financial statements are available on the SEC's website or upon request.

Additional information on each restricted holding is as follows:

| Security | Acquisition Date | Cost |

| Berks County Muni. Auth. Rev. Participating VRDN Series Floaters 001, 1.27% 4/11/18 (Liquidity Facility Barclays Bank PLC) | 1/18/18 | $100,000 |

| Central Fla Expwy Auth. Rev. Participating VRDN Series Floaters 004, 1.27% 4/11/18 (Liquidity Facility Barclays Bank PLC) | 1/18/18 | $500,000 |

| Central Florida Expressway Bonds Series RBC E 62, SIFMA Municipal Swap Index + 0.170% 1.26%, tender 5/1/18 (Liquidity Facility Royal Bank of Canada) | 2/14/18 | $300,000 |

| Chicago Board of Ed. Participating VRDN Series Floaters 003, 1.34% 3/1/18 (Liquidity Facility Barclays Bank PLC) | 2/1/18 | $600,000 |

| Middletown Hosp. Facilities Rev. Participating VRDN Series Floaters 00 31 44, 1.27% 4/11/18 (Liquidity Facility Barclays Bank PLC) | 9/14/17 | $95,000 |

| Missoula Mont Wtr. Sys. Rev. Participating VRDN Series Floaters 011, 1.27% 4/11/18 (Liquidity Facility Barclays Bank PLC) | 7/20/17 - 2/2/18 | $600,000 |

| Ohio Higher Edl. Facility Commission Rev. Participating VRDN Series 2017, 1.27% 4/11/18 (Liquidity Facility Barclays Bank PLC) | 3/9/17 | $100,000 |

| Pennsylvania Higher Edl. Facilities Auth. Bonds Series 2016 E75, 1.26%, tender 4/2/18 (Liquidity Facility Royal Bank of Canada) | 2/2/18 | $100,000 |

Affiliated Central Funds

Information regarding fiscal year to date income earned by the Fund from investments in Fidelity Central Funds is as follows:

| Fund | Income earned |

| Fidelity Municipal Cash Central Fund | $61,613 |

| Total | $61,613 |

Amounts in the income column in the above table exclude any capital gain distributions from underlying funds, which are presented in the corresponding line-item in the Statement of Operations if applicable.

Investment Valuation

All investments are categorized as Level 2 under the Fair Value Hierarchy. The inputs or methodology used for valuing securities may not be an indication of the risk associated with investing in those securities. For more information on valuation inputs please refer to the Investment Valuation section in the accompanying Notes to Financial Statements.

See accompanying notes which are an integral part of the financial statements.

Fidelity® Arizona Municipal Money Market Fund

Financial Statements

Statement of Assets and Liabilities

| February 28, 2018 (Unaudited) | ||

| Assets | ||

| Investment in securities, at value — See accompanying schedule: Unaffiliated issuers (cost $109,881,859) | $109,881,859 | |

| Fidelity Central Funds (cost $14,374,869) | 14,374,869 | |

| Total Investment in Securities (cost $124,256,728) | $124,256,728 | |

| Cash | 186,097 | |

| Receivable for investments sold | 100,000 | |

| Receivable for fund shares sold | 339,967 | |

| Interest receivable | 136,905 | |

| Distributions receivable from Fidelity Central Funds | 10,121 | |

| Other receivables | 33 | |

| Total assets | 125,029,851 | |

| Liabilities | ||

| Payable for investments purchased | $123 | |

| Payable for fund shares redeemed | 630,533 | |

| Distributions payable | 3,284 | |

| Accrued management fee | 52,270 | |

| Total liabilities | 686,210 | |

| Net Assets | $124,343,641 | |

| Net Assets consist of: | ||

| Paid in capital | $124,343,103 | |

| Distributions in excess of net investment income | (8) | |

| Accumulated undistributed net realized gain (loss) on investments | 546 | |

| Net Assets, for 124,208,663 shares outstanding | $124,343,641 | |

| Net Asset Value, offering price and redemption price per share ($124,343,641 ÷ 124,208,663 shares) | $1.00 |

See accompanying notes which are an integral part of the financial statements.

Statement of Operations

| Six months ended February 28, 2018 (Unaudited) | ||

| Investment Income | ||

| Interest | $657,868 | |

| Income from Fidelity Central Funds | 61,613 | |

| Total income | 719,481 | |

| Expenses | ||

| Management fee | $330,276 | |

| Independent trustees' fees and expenses | 254 | |

| Total expenses before reductions | 330,530 | |

| Expense reductions | (290) | 330,240 |

| Net investment income (loss) | 389,241 | |

| Realized and Unrealized Gain (Loss) | ||

| Net realized gain (loss) on: | ||

| Investment securities: | ||

| Unaffiliated issuers | (202) | |

| Fidelity Central Funds | 269 | |

| Capital gain distributions from Fidelity Central Funds | 341 | |

| Total net realized gain (loss) | 408 | |

| Net increase in net assets resulting from operations | $389,649 |

See accompanying notes which are an integral part of the financial statements.

Statement of Changes in Net Assets

| Six months ended February 28, 2018 (Unaudited) | Year ended August 31, 2017 | |

| Increase (Decrease) in Net Assets | ||

| Operations | ||

| Net investment income (loss) | $389,241 | $532,579 |

| Net realized gain (loss) | 408 | 19,768 |

| Net increase in net assets resulting from operations | 389,649 | 552,347 |

| Distributions to shareholders from net investment income | (389,249) | (532,572) |

| Distributions to shareholders from net realized gain | – | (343,231) |

| Total distributions | (389,249) | (875,803) |

| Share transactions at net asset value of $1.00 per share | ||

| Proceeds from sales of shares | 9,455,711 | 15,739,222 |

| Reinvestment of distributions | 365,572 | 828,727 |

| Cost of shares redeemed | (28,731,150) | (115,036,936) |

| Net increase (decrease) in net assets and shares resulting from share transactions | (18,909,867) | (98,468,987) |

| Total increase (decrease) in net assets | (18,909,467) | (98,792,443) |

| Net Assets | ||

| Beginning of period | 143,253,108 | 242,045,551 |

| End of period | $124,343,641 | $143,253,108 |

| Other Information | ||

| Distributions in excess of net investment income end of period | $(8) | $– |

See accompanying notes which are an integral part of the financial statements.

Financial Highlights

Fidelity Arizona Municipal Money Market Fund

| Six months ended (Unaudited) February 28, | Years endedAugust 31, | |||||

| 2018 | 2017 | 2016 | 2015 | 2014 | 2013 | |

| Selected Per–Share Data | ||||||

| Net asset value, beginning of period | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 |

| Income from Investment Operations | ||||||

| Net investment income (loss) | .003 | .003 | –A | –A | –A | –A |

| Net realized and unrealized gain (loss) | –A | .002 | –A | –A | –A | –A |

| Total from investment operations | .003 | .005 | –A | –A | –A | –A |

| Distributions from net investment income | (.003) | (.003) | –A | –A | –A | –A |

| Distributions from net realized gain | – | (.002) | –A | – | – | –A |

| Total distributions | (.003) | (.005) | –A | –A | –A | –A |

| Net asset value, end of period | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 |

| Total ReturnB,C | .30% | .48% | .02% | .01% | .01% | .02% |

| Ratios to Average Net AssetsD,E | ||||||

| Expenses before reductions | .50%F | .50% | .50% | .50% | .50% | .50% |

| Expenses net of fee waivers, if any | .50%F | .50% | .20% | .06% | .09% | .16% |

| Expenses net of all reductions | .50%F | .50% | .20% | .06% | .09% | .16% |

| Net investment income (loss) | .59%F | .29% | .01% | .01% | .01% | .01% |

| Supplemental Data | ||||||

| Net assets, end of period (000 omitted) | $124,344 | $143,253 | $242,046 | $400,132 | $417,266 | $408,028 |

A Amount represents less than $.0005 per share.

B Total returns for periods of less than one year are not annualized.

C Total returns would have been lower if certain expenses had not been reduced during the applicable periods shown.

D Fees and expenses of any underlying Fidelity Central Funds are not included in the Fund's expense ratio. The Fund indirectly bears its proportionate share of the expenses of any underlying Fidelity Central Funds.

E Expense ratios reflect operating expenses of the Fund. Expenses before reductions do not reflect amounts reimbursed or waived or reductions from expense offset arrangements and do not represent the amount paid by the Fund during periods when reimbursements, waivers or reductions occur. Expenses net of fee waivers reflect expenses after reimbursement and waivers but prior to reductions from expense offset arrangements. Expenses net of all reductions represent the net expenses paid by the Fund.

F Annualized

See accompanying notes which are an integral part of the financial statements.

Notes to Financial Statements (Unaudited)

For the period ended February 28, 2018

1. Organization.

Fidelity Arizona Municipal Income Fund (the Income Fund) is a fund of Fidelity Union Street Trust. Fidelity Arizona Municipal Money Market Fund (the Money Market Fund) is a fund of Fidelity Union Street Trust II. Each Trust is registered under the Investment Company Act of 1940, as amended (the 1940 Act), as an open-end management investment company. Fidelity Union Street Trust and Fidelity Union Street Trust II (the Trusts) are organized as a Massachusetts business trust and a Delaware statutory trust, respectively. The Income Fund is a non-diversified fund. Each Fund is authorized to issue an unlimited number of shares. Shares of the Money Market Fund are only available for purchase by retail shareholders. Share transactions on the Statement of Changes in Net Assets may contain exchanges between affiliated funds. Each Fund may be affected by economic and political developments in the state of Arizona.

2. Investments in Fidelity Central Funds.

The Funds may invest in Fidelity Central Funds, which are open-end investment companies generally available only to other investment companies and accounts managed by the investment adviser and its affiliates. The Funds' Schedules of Investments list each of the Fidelity Central Funds held as of period end, if any, as an investment of each Fund, but does not include the underlying holdings of each Fidelity Central Fund. As an Investing Fund, each Fund indirectly bears its proportionate share of the expenses of the underlying Fidelity Central Funds.

The Money Market Central Funds seek preservation of capital and current income and are managed by Fidelity Investments Money Management, Inc. (FIMM), an affiliate of the investment adviser. Annualized expenses of the Money Market Central Funds as of their most recent shareholder report date are less than .005%.

A complete unaudited list of holdings for each Fidelity Central Fund is available upon request or at the Securities and Exchange Commission (the SEC) website at www.sec.gov. In addition, the financial statements of the Fidelity Central Funds are available on the SEC website or upon request.

3. Significant Accounting Policies.

Each Fund is an investment company and applies the accounting and reporting guidance of the Financial Accounting Standards Board (FASB) Accounting Standards Codification Topic 946 Financial Services – Investments Companies. The financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America (GAAP), which require management to make certain estimates and assumptions at the date of the financial statements. Actual results could differ from those estimates. Subsequent events, if any, through the date that the financial statements were issued have been evaluated in the preparation of the financial statements. The following summarizes the significant accounting policies of the Funds:

Investment Valuation. Investments are valued as of 4:00 p.m. Eastern time on the last calendar day of the period. The Board of Trustees (the Board) has delegated the day to day responsibility for the valuation of the Income Fund's investments to the Fair Value Committee (the Committee) established by the Fund's investment adviser. In accordance with valuation policies and procedures approved by the Board, the Income Fund attempts to obtain prices from one or more third party pricing vendors or brokers to value its investments. When current market prices, quotations or currency exchange rates are not readily available or reliable, investments will be fair valued in good faith by the Committee, in accordance with procedures adopted by the Board. Factors used in determining fair value vary by investment type and may include market or investment specific events, changes in interest rates and credit quality. The frequency with which these procedures are used cannot be predicted and they may be utilized to a significant extent. The Committee oversees the Income Fund's valuation policies and procedures and reports to the Board on the Committee's activities and fair value determinations. The Board monitors the appropriateness of the procedures used in valuing the Income Fund's investments and ratifies the fair value determinations of the Committee.

Each Fund categorizes the inputs to valuation techniques used to value its investments into a disclosure hierarchy consisting of three levels as shown below:

- Level 1 – quoted prices in active markets for identical investments

- Level 2 – other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, etc.)

- Level 3 – unobservable inputs (including the Fund's own assumptions based on the best information available)

Valuation techniques used to value each Fund's investments by major category are as follows:

For the Income Fund, debt securities, including restricted securities, are valued based on evaluated prices received from third party pricing vendors or from brokers who make markets in such securities. Municipal securities are valued by pricing vendors who utilize matrix pricing which considers yield or price of bonds of comparable quality, coupon, maturity and type or by broker-supplied prices. When independent prices are unavailable or unreliable, debt securities may be valued utilizing pricing methodologies which consider similar factors that would be used by third party pricing vendors. Debt securities are generally categorized as Level 2 in the hierarchy but may be Level 3 depending on the circumstances.

For the Money Market Fund, as permitted by compliance with certain conditions under Rule 2a-7 of the 1940 Act, securities are valued at amortized cost, which approximates fair value. The amortized cost of an instrument is determined by valuing it at its original cost and thereafter amortizing any discount or premium from its face value at a constant rate until maturity. Securities held by a money market fund are generally high quality and liquid; however, they are reflected as Level 2 because the inputs used to determine fair value are not quoted prices in an active market.

For the Income Fund, changes in valuation techniques may result in transfers in or out of an assigned level within the disclosure hierarchy.

Investment Transactions and Income. For financial reporting purposes, the Funds' investment holdings and net asset value (NAV) include trades executed through the end of the last business day of the period. The NAV per share for processing shareholder transactions is calculated as of the close of business of the New York Stock Exchange (NYSE), normally 4:00 p.m. Eastern time and includes trades executed through the end of the prior business day for the Income Fund and trades executed through the end of the current business day for the Money Market Fund. Gains and losses on securities sold are determined on the basis of identified cost. Income and capital gain distributions from Fidelity Central Funds, if any, are recorded on the ex-dividend date. Interest income is accrued as earned and includes coupon interest and amortization of premium and accretion of discount on debt securities as applicable.

Expenses. Expenses directly attributable to a fund are charged to that fund. Expenses attributable to more than one fund are allocated among the respective funds on the basis of relative net assets or other appropriate methods. Expense estimates are accrued in the period to which they relate and adjustments are made when actual amounts are known.

Income Tax Information and Distributions to Shareholders. Each year, each Fund intends to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code, including distributing substantially all of its taxable income and realized gains. As a result, no provision for U.S. Federal income taxes is required. Each Fund files a U.S. federal tax return, in addition to state and local tax returns as required. Each Fund's federal income tax returns are subject to examination by the Internal Revenue Service (IRS) for a period of three fiscal years after they are filed. State and local tax returns may be subject to examination for an additional fiscal year depending on the jurisdiction.

Dividends are declared and recorded daily and paid monthly from net investment income. Distributions from realized gains, if any, are declared and recorded on the ex-dividend date. Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from GAAP.

Capital accounts within the financial statements are adjusted for permanent book-tax differences. These adjustments have no impact on net assets or the results of operations. Capital accounts are not adjusted for temporary book-tax differences which will reverse in a subsequent period.

Book-tax differences are primarily due to market discount.

The Funds purchase municipal securities whose interest, in the opinion of the issuer, is free from federal income tax. There is no assurance that the IRS will agree with this opinion. In the event the IRS determines that the issuer does not comply with relevant tax requirements, interest payments from a security could become federally taxable, possibly retroactively to the date the security was issued.

As of period end, the cost and unrealized appreciation (depreciation) in securities, and derivatives if applicable, for federal income tax purposes were as follows for each Fund:

| Tax cost | Gross unrealized appreciation | Gross unrealized depreciation | Net unrealized appreciation (depreciation) | |

| Fidelity Arizona Municipal Income Fund | $164,835,532 | $4,175,226 | $(1,906,183) | $2,269,043 |

| Fidelity Arizona Municipal Money Market Fund | 124,256,728 | – | – | – |

Restricted Securities. The Funds may invest in securities that are subject to legal or contractual restrictions on resale. These securities generally may be resold in transactions exempt from registration or to the public if the securities are registered. Disposal of these securities may involve time-consuming negotiations and expense, and prompt sale at an acceptable price may be difficult. Information regarding restricted securities is included at the end of each applicable Fund's Schedule of Investments.

New Accounting Pronouncement. In March 2017, the Financial Accounting Standards Board (FASB) issued an Accounting Standards Update (ASU), ASU 2017-08, which amends the amortization period for certain callable debt securities that are held at a premium. The amendment requires the premium to be amortized to the earliest call date. The amendments do not require an accounting change for securities held at a discount. The ASU is effective for annual periods beginning after December 15, 2018. Management is currently evaluating the potential impact of these changes to the financial statements.

4. Purchases and Sales of Investments.

Purchases and sales of securities, other than short-term securities, for the Income Fund aggregated $12,944,851 and $20,455,913, respectively.

5. Fees and Other Transactions with Affiliates.

Management Fee. Fidelity Management & Research Company (the investment adviser) and its affiliates provides the Funds with investment management related services for which the Funds pay a monthly management fee. The investment adviser pays all other expenses, except the compensation of the independent Trustees and certain other expenses such as interest expense, including commitment fees. The management fee is reduced by an amount equal to the fees and expenses paid by the Fund to the independent Trustees. Each Fund's management fee is equal to the following annual rate of average net assets:

| Fidelity Arizona Municipal Income Fund | .55% |

| Fidelity Arizona Municipal Money Market Fund | .50% |

Interfund Trades. The Funds may purchase from or sell securities to other Fidelity Funds under procedures adopted by the Board. The procedures have been designed to ensure these interfund trades are executed in accordance with Rule 17a-7 of the 1940 Act. For the Income Fund, interfund trades are included within the respective purchases and sales amounts shown in the Purchases and Sales of Investments note.

6. Committed Line of Credit.

The Income Fund participates with other funds managed by the investment adviser or an affiliate in a $4.25 billion credit facility (the "line of credit") to be utilized for temporary or emergency purposes to fund shareholder redemptions or for other short-term liquidity purposes. The participating funds have agreed to pay commitment fees on their pro-rata portion of the line of credit, which are reflected in Miscellaneous expenses on the Statement of Operations, and are as follows:

| Fidelity Arizona Municipal Income Fund | $260 |

During the period, the Income Fund did not borrow on this line of credit.

7. Expense Reductions.

Through arrangements with each applicable Fund's custodian, credits realized as a result of certain uninvested cash balances were used to reduce each applicable Fund's management fee. During the period, these credits reduced management fee by the following amounts:

| Fidelity Arizona Municipal Income Fund | $1,145 |

| Fidelity Arizona Municipal Money Market Fund | 290 |

8. Other.

The Funds' organizational documents provide former and current trustees and officers with a limited indemnification against liabilities arising in connection with the performance of their duties to the Funds. In the normal course of business, the Funds may also enter into contracts that provide general indemnifications. The Funds' maximum exposure under these arrangements is unknown as this would be dependent on future claims that may be made against the Funds. The risk of material loss from such claims is considered remote.

Shareholder Expense Example

As a shareholder of a Fund, you incur two types of costs: (1) transaction costs and (2) ongoing costs, including management fees and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (September 1, 2017 to February 28, 2018).

Actual Expenses

The first line of the accompanying table for each fund provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000.00 (for example, an $8,600 account value divided by $1,000.00 = 8.6), then multiply the result by the number in the first line for a fund under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period. A small balance maintenance fee of $12.00 that is charged once a year may apply for certain accounts with a value of less than $2,000. This fee is not included in the table below. If it was, the estimate of expenses you paid during the period would be higher, and your ending account value lower, by this amount. In addition, each Fund, as a shareholder in the underlying Fidelity Central Funds, will indirectly bear its pro-rata share of the fees and expenses incurred by the underlying Fidelity Central Funds. These fees and expenses are not included in the Fund's annualized expense ratio used to calculate the expense estimate in the table below.

Hypothetical Example for Comparison Purposes

The second line of the accompanying table for each fund provides information about hypothetical account values and hypothetical expenses based on a fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. A small balance maintenance fee of $12.00 that is charged once a year may apply for certain accounts with a value of less than $2,000. This fee is not included in the table below. If it was, the estimate of expenses you paid during the period would be higher, and your ending account value lower, by this amount. In addition, each Fund, as a shareholder in the underlying Fidelity Central Funds, will indirectly bear its pro-rata share of the fees and expenses incurred by the underlying Fidelity Central Funds. These fees and expenses are not included in the Fund's annualized expense ratio used to calculate the expense estimate in the table below.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds.

| Annualized Expense Ratio-A | Beginning Account Value September 1, 2017 | Ending Account Value February 28, 2018 | Expenses Paid During Period-B September 1, 2017 to February 28, 2018 |

|

| Fidelity Arizona Municipal Income Fund | .55% | |||

| Actual | $1,000.00 | $982.50 | $2.70 | |

| Hypothetical-C | $1,000.00 | $1,022.07 | $2.76 | |

| Fidelity Arizona Municipal Money Market Fund | .50% | |||

| Actual | $1,000.00 | $1,003.00 | $2.48 | |

| Hypothetical-C | $1,000.00 | $1,022.32 | $2.51 |

A Annualized expense ratio reflects expenses net of applicable fee waivers.

B Expenses are equal to each Fund's annualized expense ratio, multiplied by the average account value over the period, multiplied by 181/ 365 (to reflect the one-half year period).

C 5% return per year before expenses

Board Approval of Investment Advisory Contracts and Management Fees

Fidelity Arizona Municipal Income Fund / Fidelity Arizona Municipal Money Market Fund

Each year, the Board of Trustees, including the Independent Trustees (together, the Board), votes on the renewal of the management contract with Fidelity Management & Research Company (FMR) and the sub-advisory agreements (together, the Advisory Contracts) for each fund. FMR and the sub-advisers are referred to herein as the Investment Advisers. The Board, assisted by the advice of fund counsel and Independent Trustees' counsel, requests and considers a broad range of information relevant to the renewal of the Advisory Contracts throughout the year.

The Board meets regularly and, at each of its meetings, covers an extensive agenda of topics and materials and considers factors that are relevant to its annual consideration of the renewal of each fund's Advisory Contracts, including the services and support provided to each fund and its shareholders. The Board has established four standing committees (Committees) — Operations, Audit, Fair Valuation, and Governance and Nominating — each composed of and chaired by Independent Trustees with varying backgrounds, to which the Board has assigned specific subject matter responsibilities in order to enhance effective decision-making by the Board. The Operations Committee, of which all of the Independent Trustees are members, meets regularly throughout the year and considers, among other matters, information specifically related to the annual consideration of the renewal of each fund's Advisory Contracts. The Board, acting directly and through its Committees, requests and receives information concerning the annual consideration of the renewal of each fund's Advisory Contracts. The Board also meets as needed to review matters specifically related to the Board's annual consideration of the renewal of the Advisory Contracts. Members of the Board may also meet with trustees of other Fidelity funds through ad hoc joint committees to discuss certain matters relevant to all of the Fidelity funds.

At its September 2017 meeting, the Board unanimously determined to renew each fund's Advisory Contracts. In reaching its determination, the Board considered all factors it believed relevant, including (i) the nature, extent, and quality of the services to be provided to each fund and its shareholders (including the investment performance of each fund); (ii) the competitiveness of each fund's management fee and total expense ratio relative to peer funds; (iii) the total costs of the services to be provided by and the profits to be realized by Fidelity from its relationships with each fund; and (iv) the extent to which, if any, economies of scale exist and would be realized as each fund grows, and whether any economies of scale are appropriately shared with fund shareholders.

In considering whether to renew the Advisory Contracts for each fund, the Board reached a determination, with the assistance of fund counsel and Independent Trustees' counsel and through the exercise of its business judgment, that the renewal of the Advisory Contracts was in the best interests of each fund and its shareholders and that the compensation payable under the Advisory Contracts was fair and reasonable. The Board's decision to renew the Advisory Contracts was not based on any single factor, but rather was based on a comprehensive consideration of all the information provided to the Board at its meetings throughout the year. The Board, in reaching its determination to renew the Advisory Contracts, was aware that shareholders of each fund have a broad range of investment choices available to them, including a wide choice among funds offered by Fidelity's competitors, and that each fund's shareholders, who have the opportunity to review and weigh the disclosure provided by the fund in its prospectus and other public disclosures, have chosen to invest in that fund, which is part of the Fidelity family of funds.

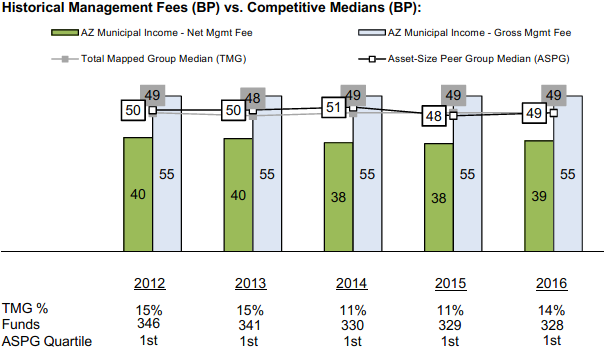

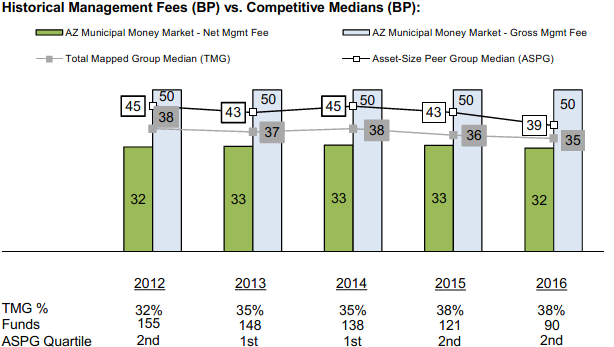

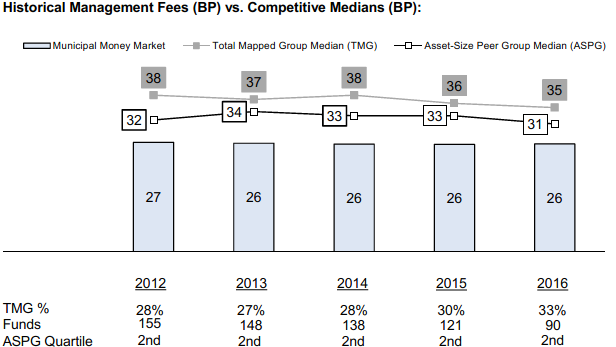

Nature, Extent, and Quality of Services Provided. The Board considered Fidelity's staffing as it relates to the funds, including the backgrounds of investment personnel of Fidelity, and also considered the funds' investment objectives, strategies, and related investment philosophies. The Independent Trustees also had discussions with senior management of Fidelity's investment operations and investment groups. The Board considered the structure of the investment personnel compensation program and whether this structure provides appropriate incentives to act in the best interests of each fund. Additionally, the Board considered the portfolio managers' investments, if any, in the funds that they manage. Resources Dedicated to Investment Management and Support Services. The Board reviewed the general qualifications and capabilities of Fidelity's investment staff, including its size, education, experience, and resources, as well as Fidelity's approach to recruiting, managing, and compensating investment personnel. The Board noted that Fidelity has continued to increase the resources devoted to non-U.S. offices, including expansion of Fidelity's global investment organization. The Board also noted that Fidelity's analysts have extensive resources, tools and capabilities that allow them to conduct sophisticated quantitative and fundamental analysis, as well as credit analysis of issuers, counterparties and guarantors. Further, the Board considered that Fidelity's investment professionals have sufficient access to global information and data so as to provide competitive investment results over time, and that those professionals also have access to sophisticated tools that permit them to assess portfolio construction and risk and performance attribution characteristics continuously, as well as to transmit new information and research conclusions rapidly around the world. Additionally, in its deliberations, the Board considered Fidelity's trading, risk management, compliance, and technology and operations capabilities and resources, which are integral parts of the investment management process. Shareholder and Administrative Services. The Board considered (i) the nature, extent, quality, and cost of advisory, administrative, and shareholder services performed by the Investment Advisers and their affiliates under the Advisory Contracts and under separate agreements covering transfer agency and pricing and bookkeeping services for each fund; (ii) the nature and extent of the supervision of third party service providers, principally custodians, subcustodians, and pricing vendors; and (iii) the resources devoted to, and the record of compliance with, each fund's compliance policies and procedures.The Board noted that the growth of fund assets over time across the complex allows Fidelity to reinvest in the development of services designed to enhance the value or convenience of the Fidelity funds as investment vehicles. These services include 24-hour access to account information and market information through telephone representatives and over the Internet, investor education materials and asset allocation tools, and the expanded availability of Fidelity Investor Centers. Investment in a Large Fund Family. The Board considered the benefits to shareholders of investing in a Fidelity fund, including the benefits of investing in a fund that is part of a large family of funds offering a variety of investment disciplines and providing a large variety of mutual fund investor services. The Board noted that Fidelity had taken, or had made recommendations that resulted in the Fidelity funds taking, a number of actions over the previous year that benefited particular funds, including: (i) continuing to dedicate additional resources to Fidelity's investment research process, which includes meetings with management of issuers in which the funds invest, and to the support of the senior management team that oversees asset management; (ii) continuing efforts to enhance Fidelity's global research capabilities; (iii) launching new funds and making other enhancements to meet client needs; (iv) launching new share classes of existing funds; (v) eliminating purchase minimums and broadening eligibility requirements for certain lower-priced share classes; (vi) reducing management fees and total expenses for certain growth equity funds and index funds; (vii) lowering expense caps for certain existing funds and classes to reduce expenses borne by shareholders; (viii) eliminating short-term redemption fees for certain funds; (ix) introducing a new pricing structure for certain funds of funds that is expected to reduce overall expenses paid by shareholders; (x) rationalizing product lines and gaining increased efficiencies through proposals for fund mergers and share class consolidations; (xi) continuing to develop, acquire and implement systems and technology to improve services to the funds and shareholders, strengthen information security, and increase efficiency; and (xii) implementing enhancements to further strengthen Fidelity's product line to increase investors' probability of success in achieving their investment goals, including retirement income goals. Investment Performance (for Fidelity Arizona Municipal Income Fund). The Board considered whether the fund has operated in accordance with its investment objective, as well as its record of compliance with its investment restrictions and its performance history.The Board took into account discussions with representatives of the Investment Advisers about fund investment performance that occur at Board meetings throughout the year. In this regard the Board noted that as part of regularly scheduled fund reviews and other reports to the Board on fund performance, the Board considers annualized return information for the fund for different time periods, measured against a securities market index ("benchmark index") and a peer group of funds with similar objectives ("peer group"), if any. In its evaluation of fund investment performance at meetings throughout the year, the Board gave particular attention to information indicating underperformance of certain Fidelity funds for specific time periods and discussed with the Investment Advisers the reasons for such underperformance.In addition to reviewing absolute and relative fund performance, the Independent Trustees periodically consider the appropriateness of fund performance metrics in evaluating the results achieved. In general, the Independent Trustees believe that fund performance should be evaluated based on gross performance (before fees and expenses but after transaction costs) compared to appropriate benchmark indices, over appropriate time periods that may include full market cycles, and on net performance (after fees and expenses) compared to peer groups, as applicable, over the same periods, taking into account relevant factors including the following: general market conditions; expectations for interest rate levels and credit conditions; issuer-specific information including credit quality; the potential for incremental return versus the fund's benchmark index weighed against the risks involved in obtaining that incremental return, including the risk of diminished or negative total returns; and fund cash flows and other factors. Depending on the circumstances, the Independent Trustees may be satisfied with a fund's performance notwithstanding that it lags its benchmark index or peer group for certain periods.The Independent Trustees recognize that shareholders evaluate performance on a net basis over their own holding periods, for which one-, three-, and five-year periods are often used as a proxy. For this reason, the performance information reviewed by the Board also included net cumulative calendar year total return information for the fund and an appropriate benchmark index and peer group for the most recent one-, three-, and five-year periods. Investment Performance (for Fidelity Arizona Municipal Money Market Fund). The Board considered whether the fund has operated in accordance with its investment objective, as well as its record of compliance with its investment restrictions and its performance history.The Board took into account discussions with representatives of the Investment Advisers about fund investment performance that occur at Board meetings throughout the year. In this regard the Board noted that as part of regularly scheduled fund reviews and other reports to the Board on fund performance, the Board considers annualized return information for the fund for different time periods, measured against a peer group of funds with similar objectives ("peer group").In addition to reviewing absolute and relative fund performance, the Independent Trustees periodically consider the appropriateness of fund performance metrics in evaluating the results achieved. In general, the Independent Trustees believe that fund performance should be evaluated based on gross performance (before fees and expenses but after transaction costs) compared to the gross performance of appropriate peer groups, over appropriate time periods that may include full market cycles, taking into account relevant factors including the following: general market conditions; expectations for interest rate levels and credit conditions; issuer-specific information including credit quality; the fund's market value NAV over time and its resilience under various stressed conditions; and fund cash flows and other factors.The Board recognizes that in interest rate environments where many competitors waive fees to maintain a minimum yield, relative money market fund performance on a net basis (after fees and expenses) may not be particularly meaningful due to miniscule performance differences among competitor funds. Depending on the circumstances, the Independent Trustees may be satisfied with a fund's performance notwithstanding that it lags its peer group for certain periods.The Independent Trustees recognize that shareholders evaluate performance on a net basis over their own holding periods, for which one-, three-, and five-year periods are often used as a proxy. For this reason, the performance information reviewed by the Board also included net cumulative calendar year total return information for the fund and an appropriate peer group for the most recent one-, three-, and five-year periods.Based on its review, the Board concluded that the nature, extent, and quality of services provided to each fund under the Advisory Contracts should continue to benefit the shareholders of each fund. Competitiveness of Management Fee and Total Expense Ratio. The Board considered each fund's management fee and total expense ratio compared to "mapped groups" of competitive funds and classes created for the purpose of facilitating the Trustees' competitive analysis of management fees and total expenses. Fidelity creates "mapped groups" by combining similar Lipper investment objective categories that have comparable investment mandates. Combining Lipper investment objective categories aids the Board's management fee and total expense ratio comparisons by broadening the competitive group used for comparison. Management Fee. The Board considered two proprietary management fee comparisons for the 12-month periods shown in basis points (BP) in the charts below. The group of Lipper funds used by the Board for management fee comparisons is referred to below as the "Total Mapped Group" and, for the reasons explained above, is broader than the Lipper peer group used by the Board for performance comparisons. The Total Mapped Group comparison focuses on a fund's standing in terms of gross management fees before expense reimbursements or caps relative to the total universe of funds with comparable investment mandates, regardless of whether their management fee structures also are comparable. Funds with comparable investment mandates offer exposure to similar types of securities. Funds with comparable management fee structures have similar management fee contractual arrangements (e.g., flat rate charged for advisory services, all-inclusive fee rate, etc.). "TMG %" represents the percentage of funds in the Total Mapped Group that had management fees that were lower than a fund's. For example, a hypothetical TMG % of 20% would mean that 80% of the funds in the Total Mapped Group had higher, and 20% had lower, management fees than a fund. The funds' actual TMG %s and the number of funds in the Total Mapped Group are in the charts below. The "Asset-Size Peer Group" (ASPG) comparison focuses on a fund's standing relative to a subset of non-Fidelity funds within the Total Mapped Group that are similar in size and management fee structure. For example, if a fund is in the first quartile of the ASPG, the fund's management fee ranks in the least expensive or lowest 25% of funds in the ASPG. The ASPG represents at least 15% of the funds in the Total Mapped Group with comparable asset size and management fee structures, subject to a minimum of 50 funds (or all funds in the Total Mapped Group if fewer than 50). Additional information, such as the ASPG quartile in which a fund's management fee rate ranked, is also included in the charts and considered by the Board. Because the vast majority of competitor funds' management fees do not cover non-management expenses, for a more meaningful comparison of management fees, each fund is compared on the basis of a hypothetical "net management fee," which is derived by subtracting payments made by FMR for non-management expenses (including transfer agent fees, pricing and bookkeeping fees, and fees paid to non-affiliated custodians) from the fund's all-inclusive fee. In this regard, the Board considered that net management fees can vary from year to year because of differences in non-management expenses.Fidelity Arizona Municipal Income Fund

Fidelity Arizona Municipal Money Market Fund

![]()

Corporate Headquarters

245 Summer St.

Boston, MA 02210

www.fidelity.com

AZI-SPZ-SANN-0418

1.700927.120

|

Fidelity® Municipal Money Market Fund Semi-Annual Report February 28, 2018 |

|

|

Contents

|

Board Approval of Investment Advisory Contracts and Management Fees |