As filed with the Securities and Exchange Commission on May 15, 2019

Registration No. 333-222572

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

Post-Effective Amendment No.2 to

FORM S-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

BIOLARGO, INC.

(Exact name of registrant as specified in its charter)

|

Delaware |

|

2800 |

|

65-0159115 |

|

(State or other jurisdiction of |

|

(Primary Standard Industrial |

|

(I.R.S. Employer |

|

incorporation or organization) |

|

Classification Code Number) |

|

Identification No.) |

|

BioLargo, Inc. |

|

14921 Chestnut St. Westminster, CA 92683 |

|

(949) 643-9540 |

|

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices) |

|

Copy to: |

|

Christopher A. Wilson, Esq. |

|

Wilson Bradshaw & Cao, LLP |

|

18818 Teller Avenue, Suite 115 |

|

Irvine, CA 92612 |

|

Tel: (949) 752-1100 cwilson@wbc-law.com |

Agents and Corporations, Inc.

1201 Orange Street, Suite 600

Wilmington, DE 19801

(302) 575-0877

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Approximate date of commencement of proposed sale to the public:

From time to time after this registration statement is declared effective.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: ☐

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer: ☐ |

Accelerated filer: ☐ |

Non-accelerated filer: ☐ |

Smaller reporting company: X |

|

Emerging growth company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided to Section 7(a)(2)(B) of the Securities Act. ☐

CALCULATION OF REGISTRATION FEE

|

Title of Each Class of Securities to be Registered |

Amount to be Registered |

Proposed Maximum Offering Price Per Share(1) |

Proposed Maximum Aggregate Offering Price(1) |

Amount of Registration Fee(2) |

|

Shares of Common Stock, par value $0.00067 per share, to be sold by the Selling Stockholders |

13,801,119 |

$0.159 |

$2,193,160 |

$273.05 |

|

(1) Estimated solely for purposes of calculating the registration fee in accordance with Rule 457(a) and (c) under the Securities Act of 1933, as amended. |

|

(2) A registration fee of $220.51 was paid when the Company filed the Registration Statement on Form S-1 on February 8, 2018, and an additional $52.54 was paid with respect to the filing of Amendment No. 1 to this registration statement. These fees are transferred and carried forward to this amendment pursuant to Rule 429 under the Securities Act. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

EXPLANATORY NOTE

BioLargo, Inc. (the “Company,” “we,” or “us”) filed a Registration Statement on Form S-1 with the Securities and Exchange Commission (“SEC”) on February 8, 2018 (the “Registration Statement”). The Registration Statement was declared effective on February 8, 2018. The Company filed post-effective Amendment No. 1 to the Registration Statement on August 28, 2018, and it was declared effective on September 6, 2018.

The Company is submitting this post-effective Amendment No. 2 (“Amendment”) to its Registration Statement for the purpose of (i) providing information from its Annual Report on Form 10-K for the period ended December 31, 2018 filed with the SEC March 29, 2019, and as amended on April 30, 2019; (ii) incorporating by reference the Current Reports on Form 8-K filed since March 29, 2018 to the date of this Amendment; (iii) increasing the number of shares purchasable by two selling stockholders pursuant to stock purchase warrants resulting from reductions in the exercise price of said warrants.

The contents of the Registration Statement as previously filed which are not modified and revised by this Amendment are hereby incorporated by reference.

The information in this prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

PROSPECTUS (Subject to Completion)

Dated: May 15, 2019

PROSPECTUS

13,801,119 shares of common stock

This prospectus relates to the offer and sale of up to 13,801,119 shares of common stock, par value $0.00067, of BioLargo, Inc., a Delaware corporation, by (i) Vista Capital Investments, LLC (“Vista Capital”), (ii) FirstFire Global Opportunities Fund, LLC (“FirstFire”), (iii) Black Mountain Equities, Inc., (“Black Mountain”), and (iv) Gemini Master Fund, L.P. (“Gemini”). In this prospectus, we sometimes refer to Vista Capital, FirstFire, Black Mountain, and Gemini collectively as the “selling stockholders,” or individually as a “selling stockholder.”

The shares of common stock being offered by Vista Capital have been or may be issued pursuant to the purchase agreement dated December 14, 2017 that we entered into with Vista Capital. (See “The Vista Capital Transaction” below for a description of that agreement and “Selling Stockholders” for additional information regarding Vista Capital.)

The shares of common stock being offered by FirstFire have been or may be issued pursuant to the purchase agreement dated January 16, 2018 that we entered into with FirstFire. (See “The FirstFire Transaction” below for a description of that agreement and “Selling Stockholders” for additional information regarding FirstFire.)

The shares of common stock being offered by Black Mountain and Gemini may be issued pursuant to stock purchase warrants issued pursuant to Securities Purchase Agreements dated July 8, 2016, December 30, 2016 and July 18, 2017. See “The Black Mountain/Gemini Transactions” below for a description of those agreements and “Selling Stockholders” for additional information regarding Black Mountain and Gemini.

We are not selling any securities under this prospectus and will not receive any of the proceeds from the sale of shares by the selling stockholders. We may receive up to $820,000 aggregate gross proceeds in the event the warrants are exercised.

The selling stockholders may sell the shares of common stock described in this prospectus in a number of different ways and at varying prices. See “Plan of Distribution” for more information about how the selling stockholders may sell the shares of common stock being registered pursuant to this prospectus. Each selling stockholder may be considered “underwriter” within the meaning of Section 2(a)(11) of the Securities Act of 1933, as amended.

We will pay the expenses incurred in registering the shares, including legal and accounting fees. See “Plan of Distribution”.

Since January 23, 2008, our common stock has been quoted on the OTC Markets “OTCQB” marketplace (formerly known as the “OTC Bulletin Board”, and referred to in this prospectus as the “OTC Markets”) under the trading symbol “BLGO.” On May 10, 2019, the last reported sale price of our common stock on the OTC Markets was $0.18.

The securities offered in this prospectus involve a high degree of risk. You should consider the risk factors beginning on page 3 before purchasing our common stock.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is May 15, 2019

Unless otherwise specified, the information in this prospectus is set forth as of May 15, 2019, and we anticipate that changes in our affairs will occur after such date. We have not authorized any person to give any information or to make any representations, other than as contained in this prospectus, in connection with the offer contained in this prospectus. If any person gives you any information or makes representations in connection with this offer, do not rely on it as information we have authorized. This prospectus is not an offer to sell our common stock in any state or other jurisdiction to any person to whom it is unlawful to make such offer.

The following summary highlights selected information from this prospectus and may not contain all the information that is important to you. You should read this entire prospectus, including the section titled “Risk Factors,” and our financial statements and the notes included in the Annual Report on Form 10-K for year ended December 31, 2018, incorporated herein by reference, before deciding to invest in our Common Stock. When we refer in this prospectus to “BioLargo,” the “company,” “our company,” “we,” “us” and “our,” we mean BioLargo, Inc., a Delaware corporation, and its wholly owned subsidiaries, BioLargo Life Technologies, Inc., a California corporation, Odor-No-More, Inc., a California corporation, BioLargo Water, Inc., a Canadian corporation, BioLargo Development Corp., a California corporation, BioLargo Engineering, Science & Technologies, LLC, Tennessee limited liability company, and its partially owned subsidiary Clyra Medical Technologies, Inc., a California corporation. This prospectus contains forward-looking statements and information relating to BioLargo. See “Cautionary Note Regarding Forward Looking Statements” on page 12.

Our Company

BioLargo, Inc. is a Delaware corporation.

Our principal executive offices are located at 14921 Chestnut St., Westminster, California 92683. Our telephone number is (888) 400-2863.

The Offering

This prospectus covers 13,801,119 shares of stock, all of which are offered for sale by the selling stockholders.

Vista Capital Transaction

On December 18, 2017, we received $495,000 pursuant to a securities purchase agreement (the “Vista Agreement”) and a registration rights agreement (the “Vista RRA”) with Vista Capital and issued a convertible note (the “Vista Note”) to Vista Capital in the aggregate principal amount of $500,000 at 5% annual interest, which was initially convertible into shares of common stock of the Company at $0.394 per share, subject to the terms, and certain limitations and conditions, set forth in the Vista Agreement and Vista Note. The Vista Note was initially scheduled to mature on September 18, 2018. As set forth below, the Vista Note has been partially paid and the maturity date of the remaining principle amount has been extended.

Pursuant to the Vista Agreement, the Company issued 250,000 shares of common stock to Vista Capital as a commitment fee (the “Vista Commitment Shares”).

Under the Vista Note and Vista Agreement, the Company initially reserved 1,316,668 shares of common stock for issuance upon conversion of the Vista Note. Pursuant to the Vista RRA, we agreed and filed a registration statement with the Securities and Exchange Commission (the “SEC”) registering the 1,316,668 shares of common stock for conversion of the Vista Note, as well as the 250,000 Vista Commitment Shares. The Vista Agreement required the issuance of additional Vista Commitment Shares in the event the closing price of our common stock, on the earlier of the date the registration statement is deemed effective and 20 trading days following the six-month anniversary of the Vista Note, is lower than the closing price on December 18, 2017 (which was $0.41). On the effective date of the Registration Statement (February 8, 2018), the closing price of the Company’s common stock was $0.3147 per share. As a result, in February 2018, the Company issued 140,849 additional commitment shares to Vista Capital.

Vista Capital represented to the Company, among other things, that it was an “accredited investor” (as such term is defined in Rule 501(a) of Regulation D under the Securities Act of 1933, as amended). The Vista Note, the Vista Agreement, and the Vista RRA contain customary representations, warranties, agreements and conditions including indemnification rights and obligations of the parties.

The Company used the proceeds received by the Company of the Vista Note for working capital and general corporate purposes.

See “Subsequent Conversions of Vista Note, Changes to Conversion Price”, below.

FirstFire Transaction

On January 16, 2018, we entered into a securities purchase agreement (the “FirstFire Agreement”) and a registration rights agreement (the “FirstFire RRA”) with FirstFire.

In conjunction with the execution of the FirstFire Agreement, and receipt of funds, we issued a convertible promissory note (the “FirstFire Note”) to FirstFire in the aggregate principal amount of $150,000 at 5% annual interest, which was initially convertible into shares of common stock of the Company at $0.394 per share, subject to the terms, and certain limitations and conditions, set forth in the FirstFire Agreement and the FirstFire Note. FirstFire may convert the FirstFire Note at any time. The Company may require the conversion of the FirstFire Note in the event the Company’s common stock has traded at a price per share of $0.75 or above for the ten trading days immediately preceding the mandatory conversion, and the shares underlying the conversion are subject to an effective registration statement filed with the SEC. The FirstFire Note has been paid in full and would have matured on October 16, 2018.

Pursuant to the FirstFire Agreement, the Company issued 75,000 shares of common stock to FirstFire (the “FirstFire Commitment Shares”) as a commitment fee.

Under the FirstFire Note, the Company initially reserved 394,949 shares of common stock for issuance upon its conversion. Pursuant to the FirstFire RRA, we agreed to file a registration statement with the SEC registering all shares of common stock into which the FirstFire Note is convertible and the FirstFire Commitment Shares. The FirstFire Agreement required the issuance of additional FirstFire Commitment Shares in the event the closing price of our common stock, on the earlier of the date the registration statement is deemed effective and 20 trading days following the six-month anniversary of the FirstFire Note, is lower than the closing price on January 16, 2018. On February 8, 2018, the closing price of the Company’s common stock was $0.3147 per share. As a result, in February 2018, the Company issued 36,536 additional commitment shares to FirstFire.

FirstFire represented to the Company, among other things, that it was an “accredited investor” (as such term is defined in Rule 501(a) of Regulation D under the Securities Act of 1933, as amended). The FirstFire Note, the FirstFire Agreement, and the FirstFire RRA contain customary representations, warranties, agreements and conditions including indemnification rights and obligations of the parties.

The Company used the proceeds received by the Company of the FirstFire Note for working capital and general corporate purposes.

In June 2018, FirstFire elected to convert $95,761 of the outstanding principal balance of the FirstFire Note and we issued 383,047 shares. In July 2018, FirstFire elected to convert the remaining principal due on the note of $54,239. We issued an aggregate 217,960 shares at $0.25 per share, consisting of 216,950 shares for payment of principal, and 1,010 for payment of accrued interest. As of the date of this Prospectus, the FirstFire Note is paid in full.

Black Mountain and Gemini Transaction dated July 8, 2016

On July 8, 2016, we received $250,000 and issued convertible promissory notes (initially convertible at $0.45 per share) with a maturity date of July 8, 2017 to Black Mountain and Gemini in the aggregate principal amount of $280,000. Interest was charged upon issuance at 3% per annum. Concurrently, we issued these investors stock purchase warrants to purchase an aggregate 400,000 shares of our common stock, initially exercisable at $0.65 per share, which expire five years from the date of grant. Subject to certain exceptions, the exercise price of the stock purchase warrant may be adjusted downward in the event we sell our common stock or issue warrants at a lower price. Both Black Mountain and Gemini exercised their rights to convert their promissory notes to common stock, and on January 17, 2017, we issued an aggregate 640,889 shares in full payment of principal and interest due under the notes.

These warrants issued to Black Mountain and Gemini have since been repriced pursuant their terms (see “Warrant Reprice” below).

Black Mountain and Gemini Transaction dated December 30, 2016

On December 30, 2016, we received $250,000 and issued convertible promissory notes (initially convertible at $0.57 per share) with a maturity date of December 30, 2017 to Black Mountain and Gemini in the aggregate principal amount of $280,000. Interest was charged upon issuance at 3% per annum. Concurrently, we issued these investors stock purchase warrants to purchase an aggregate 400,000 shares of our common stock, initially exercisable at $0.75 per share, which expire five years from the date of grant. Subject to certain exceptions, the exercise price of the stock purchase warrant may be adjusted downward in the event we sell our common stock or issue warrants at a lower price. Both Black Mountain and Gemini exercised their rights to convert their promissory notes to common stock, and on July 20, 2017, we issued an aggregate 686,667 shares in full payment of principal and interest due under the notes.

These warrants issued to Black Mountain and Gemini have since been repriced pursuant their terms (see “Warrant Reprice” below).

Black Mountain and Gemini Transaction dated July 18, 2017

On July 18, 2017, we received $250,000 and issued convertible promissory notes (initially convertible at $0.42 per share) with a maturity date of July 8, 2018 to Black Mountain and Gemini in the aggregate principal amount of $280,000. Interest was charged upon issuance at 3% per annum. Concurrently, we issued these investors stock purchase warrants to purchase an aggregate 400,000 shares of our common stock, initially exercisable at $0.65 per share, which expire five years from the date of grant. Subject to certain exceptions, the exercise price of the stock purchase warrant may be adjusted downward in the event we sell our common stock or issue warrants at a lower price.

These warrants issued to Black Mountain and Gemini have since been repriced pursuant their terms (see “Warrant Reprice” below).

Warrant Reprice

Subsequent to the issuance of the warrants to Black Mountain and Gemini, we sold shares of our common stock at a price lower than the exercise price of the warrants. Pursuant to the terms of those warrants, the exercise price automatically reduced to the lowest price that we sold our shares, and the number of shares exercisable under the warrants increased such that the dollar amount required to fully exercise each warrant remained the same. Thus, for example, in July 2016 we issued warrants to purchase an aggregate 400,000 shares to Black Mountain and Gemini, exercisable at $0.65 per share. To purchase the 400,000 shares at $0.65 would require $260,000, payable to BioLargo. In February 2018, the exercise price of these warrants was reduced to $0.25 per share, and the number of shares issuable by BioLargo upon exercise of these warrants has been increased from 400,000 to 1,040,000. On March 30, 2019, we again notified Black Mountain and Gemini that we sold shares at a lower price than the $0.25 exercise price in the warrants, and issued notices that the exercise price of the warrants issued in July 2016 and December 2016 had decreased to $0.12 a share.1

|

1 |

The July 2017 warrants contain an exemption for shares issued in conversion of promissory notes, and thus the exercise price of the July 2017 warrants did not adjust. |

In the aggregate, the warrants originally issued to Black Mountain and Gemini provided for the purchase of 1,200,000 shares. Because the subsequent exercise price reductions, the number of shares purchasable under the warrants has increased to an aggregate of 5,706,666 shares.

As of May 10, 2019, there were 144,953,058 shares of our common stock outstanding, of which 106,447,090 shares were held by non-affiliates. If all of the 13,801,119 shares offered by the selling stockholders under this prospectus were issued and outstanding as of the date hereof, such shares would represent 7.7% of the total number of shares of our common stock outstanding and 10.2% of the total number of outstanding shares held by non-affiliates, in each case as of the date hereof.

Issuances of our common stock in this offering will not affect the rights or privileges of our existing stockholders, except that the economic and voting interests of each of our existing stockholders will be diluted as a result of any such issuance. Although the number of shares of common stock that our existing stockholders own will not decrease, the shares owned by our existing stockholders will represent a smaller percentage of our total outstanding shares after any such issuance to Vista Capital, Black Mountain, or Gemini.

Subsequent Conversions of Vista Note, Changes to Conversion Price

Subsequent to the filing of the Registration Statement, in February 2018, the conversion rate of the Vista Note was reduced to $0.25 pursuant to the price protection features in the Note.

In June 2018, Vista Capital elected to convert $52,025 of the outstanding principal balance of the Vista Note and we issued 208,100 shares, plus shares for interest that had accrued through the date of conversion. As of June 30, 2018, the outstanding balance on the Vista Note was $447,975. Through the September 18, 2018 maturity date, the note would have accrued additional interest, such that the amount due on the date of maturity would be $453,140.

On August 28, 2018, we filed Amendment No. 1 to the Registration Statement. At that time, we determined that the principal and interest due on the Vista Note at the September 18, 2018 maturity date would be $453,140. Therefore, Amendment No. 1 increased to 1,812,561 the shares registered to Vista Capital for conversion of the Vista Note.

On September 12, 2018, Vista Capital agreed to extend the maturity date of the Vista Note to December 18, 2018. In return, we increased the principal outstanding balance by 20% or $92,000. In addition, we issued Vista Capital a warrant to purchase 1,812,000 shares of our common stock at $0.25 per share.

On December 18, 2018, Vista Capital elected to convert $166,667 of the outstanding principal and interest of the Vista Note in conjunction with our agreement that the principal amount of the note had increased by $166,667 in accordance with the price protection features in the Vista Note and our issuance of a promissory note dated October 16, 2018 that contained an original issue discount. We issued Vista Capital 666,668 shares of our common stock as a result of this conversion. As of December 31, 2018, the outstanding balance on the Vista Note totaled $550,000.

On January 7, 2019, Vista Capital agreed to extend the maturity date of the Vista Note to April 15, 2019. We agreed to amend the note to (i) increase the principal amount of the note to $605,100, (ii) re-define the conversion price of the note to equal 80% of the lowest closing bid price of the Company’s common stock during the 25 consecutive trading days immediately preceding the conversion date, (iii) reduce the prepayment penalty from 20% to 15%, such that a prepayment requires the payment of an additional 15% of the then outstanding balance, and (iv) reduce the penalty for a default from 30% to 25% of the outstanding balance.

Subsequent to the January 7, 2019 amendment, Vista Capital has chosen to convert $275,000 of the Vista 2017 Note (credited to interest and then principal), and received an aggregate 2,158,353 shares of our common stock. We and Vista Capital have agreed to further extend the maturity date from April 15, 2019 to July 15, 2019, and as consideration have increased the principal balance of the note by 10%. Accounting for these conversions and the extension, the principal amount due on the note is $370,451.

SECURITIES OFFERED

| Common stock to be offered by the selling stockholder | 13,801,119 shares consisting of: | ||||

| ● | 3,704,510 shares issuable to Vista Capital upon conversion of the remaining balance on the Vista Note of $370,451 (assuming a $0.10 per share conversion rate); | ||||

| ● | 96,609 shares held by FirstFire issued pursuant to the FirstFire Agreement; | ||||

| ● | 6,000,000 shares issuable to Gemini when and if Gemini exercises its right to purchase shares under its three stock purchase warrants; and | ||||

| ● | 4,000,000 shares issuable to Black Mountain when and if Black Mountain exercises its right to purchase shares under its three stock purchase warrants. | ||||

|

|

|

|

|

Common stock outstanding prior to this offering |

|

144,953,058 shares, as of May 10, 2019. |

|

|

||

|

Common stock to be outstanding after giving effect to the issuance of 13,801,119 additional shares registered hereunder |

158,754,177 shares, which amount includes 144,953,058 shares outstanding as of May 10, 2019, and the 13,801,119 shares registered hereunder. |

|

|

Use of Proceeds |

We will receive no proceeds from the sale of shares of common stock by Vista Capital or FirstFire in this offering. We may receive up to $820,000 aggregate gross proceeds under the stock purchase warrants should Black Mountain and Gemini exercise their rights to purchase shares under the warrants. Any proceeds that we receive from sales to Black Mountain and Gemini under the warrants will be used for working capital requirements of the Company’s business divisions and for research and development. See “Use of Proceeds.” |

|

|

|

|

|

|

Risk factors |

This investment involves a high degree of risk. See “Risk Factors” for a discussion of factors you should consider carefully before making an investment decision. |

|

|

Symbol on the OTC Markets |

|

“BLGO” |

An investment in our common stock is highly speculative, involves a high degree of risk and should be made only by investors who can afford a complete loss. You should carefully consider the following risk factors, together with the other information in this prospectus, including our financial statements and the related notes, before you decide to buy our common stock. If any of the following risks actually occurs, then our business, financial condition or results of operations could be materially adversely affected, the trading of our common stock could decline, and you may lose all or part of your investment therein.

Risks Relating to our Business

Our limited operating history makes evaluation of our business difficult.

We have limited and only nominal historical financial data upon which to base planned operating expenses or forecast accurately our future operating results. Because our operations are not yet sufficient to fund our operational expenses, we rely on investor capital to fund operations. Our limited operational history make it difficult to forecast the need for future financing activities. Further, our limited operating history will make it difficult for investors and securities analysts to evaluate our business and prospects. Our failure to address these risks and difficulties successfully could seriously harm us.

We have never generated any significant revenues, have a history of losses, and cannot assure you that we will ever become or remain profitable.

We have not yet generated any significant revenue from operations, and, accordingly, we have incurred net losses every year since our inception. To date, we have dedicated most of our financial resources to research and development, general and administrative expenses, and initial sales and marketing activities. We have funded the majority of our activities through the issuance of convertible debt or equity securities. Although sale of our CupriDyne Clean products are increasing, and we are devoting more energy and money to our sales and marketing activities, we continue to anticipate net losses and negative cash flow for the foreseeable future. Our ability to reach positive cash flow depends on many factors, including our ability to fund sales and marketing activities, and the rate of client adoption. There can be no assurance that our revenues will be sufficient for us to become profitable in 2019 or future years, or thereafter maintain profitability. We may also face unforeseen problems, difficulties, expenses or delays in implementing our business plan, including generally the need for odor control products in solid waste handling operations, which we may not fully understand or be able to predict.

Our cash requirements are significant. We will require additional financing to sustain our operations and without it we may not be able to continue operations.

Our cash requirements and expenses will continue to be significant. Our net cash used in continuing operations for the year ended December 31, 2018 was almost $4,000,000, over $300,000 per month. During that same period, we generated only $1,364,000 in total gross revenues. Thus, in order to become profitable, we must significantly increase our revenues. Although our revenues are increasing through sales of our products and from our engineering division, we expect to continue to use cash in 2019 as it becomes available.

At December 31, 2018, we had working capital deficit of approximately $1,536,000. Our auditor’s report for the year ended December 31, 2018 includes an explanatory paragraph to their audit opinion stating that our recurring losses from operations and working capital deficiency raise substantial doubt about our ability to continue as a going concern. We do not currently have sufficient financial resources to fund our operations or those of our subsidiaries. Therefore, we need additional financing to continue these operations.

In August 2017, we entered into a three-year purchase agreement with Lincoln Park Capital Fund LLC (“Lincoln Park”) through which we may direct Lincoln Park to purchase shares of our common stock at prices that depend on the market price of our stock (the “LPC Agreement”). Over time, and subject to multiple limitations, we may direct Lincoln Park to purchase up to $10,000,000 of our common stock. Since inception of the LPC Agreement, through December 31, 2018, we directed Lincoln Park to purchase 4,025,733 shares of our common stock, and received $1,349,969 in proceeds. During the year ended December 31, 2018, we directed Lincoln Park to purchase 2,850,733 shares of our common stock, and received $838,884 in proceeds. The extent to which we rely on Lincoln Park as a source of funding in 2019 will depend on a number of factors, including the prevailing market price of our common stock, and the extent to which we are able to secure working capital from other sources. If obtaining sufficient funding from Lincoln Park were to prove unavailable or prohibitively dilutive, we will need to secure another source of funding in order to satisfy our working capital needs. Even if we were receive the full maximum commitment of $10,000,000 in aggregate gross proceeds from sales of our common stock to Lincoln Park during the three year term of the LPC Agreement, we may still need additional capital to fully implement our business, operating and development plans. Should the financing we require to sustain our working capital needs be unavailable or prohibitively expensive when we require it, the consequences could be a material adverse effect on our business, operating results, financial condition and prospects.

From time to time, we issue stock, instead of cash, to pay some of our operating expenses. These issuances are dilutive to our existing stockholders.

We are party to agreements that provide for the payment of, or permit us to pay at our option, securities rather than cash in consideration for services provided to us. We include these provisions in agreements to allow us to preserve cash. When we pay employees, vendors and consultants in stock or stock options, we do so at a premium. We anticipate that we will continue to do so in the future. All such issuances are dilutive to our stockholders because they increase (and will increase in the future) the total number of shares of our common stock issued and outstanding, even though such arrangements assist us with managing our cash flow. These issuances also increase the expense amount recorded.

Our stockholders face further potential dilution in any new financing.

Our private securities offerings typically provide for convertible securities, including notes and warrants. Any additional capital that we raise would dilute the interest of the current stockholders and any persons who may become stockholders before such financing. Given the low price of our common stock, such dilution in any financing of a significant amount could be substantial.

Our stockholders face further potential adverse effects from the terms of any preferred stock that may be issued in the future.

In order to raise capital to meet expenses or to acquire a business, our board of directors may issue additional stock, including preferred stock. Any preferred stock that we may issue may have voting rights, liquidation preferences, redemption rights and other rights, preferences and privileges. The rights of the holders of our common stock will be subject to, and in many respects subordinate to, the rights of the holders of any such preferred stock. Furthermore, such preferred stock may have other rights, including economic rights, senior to our common stock that could have a material adverse effect on the value of our common stock. Preferred stock, while providing desirable flexibility in connection with possible acquisitions and other corporate purposes, can also have the effect of making it more difficult for a third party to acquire a majority of our outstanding voting stock, thereby delaying, deferring or preventing a change in control of our company.

There are several specific business opportunities we are considering in further development of our business. None of these opportunities is yet the subject of a definitive agreement, and most or all of these opportunities will require additional funding obligations on our part, for which funding is not currently in place.

In furtherance of our business plan, we are presently considering a number of opportunities to promote our business, to further develop and broaden, and to license, our technology with third parties. While discussions are underway with respect to such opportunities, there are no definitive agreements in place with respect to any of such opportunities at this time. There can be no assurance that any of such opportunities being discussed will result in definitive agreements or, if definitive agreements are entered into, that they will be on terms that are favorable to us.

Moreover, should any of these opportunities result in definitive agreements being executed or consummated, we may be required to expend additional monies above and beyond our current operating budget to promote such endeavors. No such financing is in place at this time for such endeavors, and we cannot assure you that any such financing will be available, or if it is available, whether it will be on terms that are favorable to our company.

We expect to incur future losses and may not be able to achieve profitability.

Although we are generating limited revenue from the sale of our products, and we expect to generate revenue from new products we are introducing, and eventually from other license or supply agreements, we anticipate net losses and negative cash flow to continue for the foreseeable future until our products are expanded in the marketplace and they gain broader acceptance by resellers and customers. Our current level of sales is not sufficient to support the financial needs of our business. We cannot predict when or if sales volumes will be sufficiently large to cover our operating expenses. We intend to expand our marketing efforts of our products as financial resources are available, and we intend to continue to expand our research and development efforts. Consequently, we will need to generate significant additional revenue or seek additional financings to fund our operations. This has put a proportionate corresponding demand on capital. Our ability to achieve profitability is dependent upon our efforts to deliver a viable product and our ability to successfully bring it to market, which we are currently pursuing. Although our management is optimistic that we will succeed in licensing our technology, we cannot be certain as to timing or whether we will generate sufficient revenue to be able to operate profitably. If we cannot achieve or sustain profitability, then we may not be able to fund our expected cash needs or continue our operations. If we are not able to devote adequate resources to promote commercialization of our technology, then our business plans will suffer and may fail.

Because we have limited resources to devote to sales, marketing and licensing efforts with respect to our technology, any delay in such efforts may jeopardize future research and development of technologies and commercialization of our technology. Although our management believes that it can finance commercialization efforts through sales of our securities and possibly other capital sources, if we do not successfully bring our technology to market, our ability to generate revenues will be adversely affected.

Our internal controls are not effective.

We have determined that our disclosure controls and procedures and our internal control over financial reporting are currently not effective. The lack of effective internal controls could materially adversely affect our financial condition and ability to carry out our business plan.

Our management team for financial reporting, under the supervision and with the participation of our chief executive officer and our chief financial officer, conducted an evaluation of the effectiveness of the design and operation of our internal controls. Recognizing the dynamic nature and growth of the Company’s business in the year ended December 31, 2018, including the growth of the core operations and the increase in the number of employees, management has recognized the strain on the overall internal control environment. As a result, management has concluded that its internal controls over financial reporting are not effective. Management identified a material weakness with respect to deficiencies in its financial closing and reporting procedures. Management believes this is due to a lack of resources. Management intends to add accounting personnel and operating staff and more sophisticated systems in order to improve its reporting procedures and internal controls, subject to available capital. Until we have adequate resources to increase address these issues, any material weaknesses may materially adversely affect our ability to report accurately our financial condition and results of operations in the future in a timely and reliable manner. In addition, although we continually review and evaluate internal control systems to allow management to report on the sufficiency of our internal controls, we cannot assure you that we will not discover additional weaknesses in our internal control over financial reporting. Any such additional weakness or failure to remediate the existing weakness could materially adversely affect our financial condition or ability to comply with applicable financial reporting requirements and the requirements of the Company’s various financing agreements.

If we are not able to manage our anticipated growth effectively, we may not become profitable.

We anticipate that expansion will continue to be required to address potential market opportunities for our technology and our products. Our existing infrastructure is limited. While we believe our current manufacturing processes as well as our office and warehousing provide the basic resources to expand as we grow sales of CupriDyne Clean to more than $2 million per month, our infrastructure will need more staffing to support manufacturing, customer service, administration as well as sales/account executive functions. There can be no assurance that we will have the financial resources to create new infrastructure, or that any such infrastructure will be sufficiently scalable to manage future growth, if any. There also can be no assurance that, if we invest in additional infrastructure, we will be effective in expanding our operations or that our systems, procedures or controls will be adequate to support such expansion. In addition, we will need to provide additional sales and support services to our partners if we achieve our anticipated growth with respect to the sale of our technology for various applications. Failure to properly manage an increase in customer demands could result in a material adverse effect on customer satisfaction, our ability to meet our contractual obligations, and our operating results.

Some of the products incorporating our technology will require regulatory approval.

The products in which our technology may be incorporated have both regulated and non-regulated applications. The regulatory approvals for certain applications may be difficult, impossible, time consuming and/or expensive to obtain. While our management believes such approvals can be obtained for the applications contemplated, until those approvals from the FDA or the EPA or other regulatory bodies, at the federal and state levels, as may be required are obtained, we may not be able to generate commercial revenues for regulated products. Certain specific regulated applications and their use require highly technical analysis and additional third-party validation and will require regulatory approvals from organizations like the FDA. Certain applications may also be subject to additional state and local agency regulations, increasing the cost and time associated with commercial strategies. Additionally, most products incorporating our technology that may be sold in the European Union (“EU”) will require EU and possibly also individual country regulatory approval. All such approvals, including additional testing, are time-consuming, expensive and do not have assured outcomes of ultimate regulatory approval.

We need to outsource and rely on third parties for the manufacture of the chemicals, material components or delivery apparatus used in our technology, and part of our future success will be dependent on the timeliness and effectiveness of the efforts of these third parties.

We do not have the required financial and human resources or capability to manufacture the chemicals necessary to make our odor control products. Our business model calls for the outsourcing of the manufacture of these chemicals in order to reduce our capital and infrastructure costs as a means of potentially improving our financial position and the profitability of our business. Accordingly, we must enter agreements with other companies that can assist us and provide certain capabilities, including sourcing and manufacturing, which we do not possess. We may not be successful in entering into such alliances on favorable terms or at all. Even if we do succeed in securing such agreements, we may not be able to maintain them. Furthermore, any delay in entering into agreements could delay the development and commercialization of our technology or reduce its competitiveness even if it reaches the market. Any such delay related to such future agreements could adversely affect our business.

If any party to which we have outsourced certain functions fails to perform its obligations under agreements with us, the commercialization of our technology could be delayed or curtailed.

To the extent that we rely on other companies to manufacture the chemicals used in our technology, or sell or market products incorporating our technology, we will be dependent on the timeliness and effectiveness of their efforts. If any of these parties does not perform its obligations in a timely and effective manner, the commercialization of our technology could be delayed or curtailed because we may not have sufficient financial resources or capabilities to continue such efforts on our own.

We rely on a small number of key supply ingredients in order to manufacture our products.

All of the supply ingredients used to manufacture our products are readily available from multiple suppliers. However, commodity prices for these ingredients can vary significantly, and the margins that we are able to generate could decline if prices rise. If our manufacturing costs rise significantly, we may be forced to raise the prices for our products, which may reduce their acceptance in the marketplace.

If our technology or products incorporating our technology do not gain market acceptance, it is unlikely that we will become profitable.

The potential markets for products into which our technology can be incorporated are rapidly evolving, and we have many successful competitors including some of the largest and most well-established companies in the world. (see, herein: “Description At this time, our technology is unproven in all but one industry – waste management – and the use of our technology by others, and the sales of our products, is relatively nominal. The commercial success of products incorporating our technology will depend on the adoption of our technology by commercial and consumer end users in various fields.

Market acceptance may depend on many factors, including:

|

● |

the willingness and ability of consumers and industry partners to adopt new technologies from a company with little or no history in the industry; |

|

● |

our ability to convince potential industry partners and consumers that our technology is an attractive alternative to other competing technologies; |

|

● |

our ability to license our technology in a commercially effective manner; |

|

● |

our ability to continue to fund operations while our products move through the process of gaining acceptance, before the time in which we are able to scale up production to obtain economies of scale; and |

|

● |

our ability to overcome brand loyalties. |

If products incorporating our technology do not achieve a significant level of market acceptance, then demand for our technology itself may not develop as expected, and, in such event, it is unlikely that we will become profitable.

Any revenues that we may earn in the future are unpredictable, and our operating results are likely to fluctuate from quarter to quarter.

We believe that our future operating results will fluctuate due to a variety of factors, including:

|

● |

delays in product development by us or third parties; |

|

● |

market acceptance of products incorporating our technology; |

|

● |

changes in the demand for, and pricing of, products incorporating our technology; |

|

● |

competition and pricing pressure from competitive products; and |

|

● |

expenses related to, and the results of, proceedings relating to our intellectual property. |

We expect our operating expenses will continue to fluctuate significantly in 2019 and beyond, as we continue our research and development and increase our marketing and licensing activities. Although we expect to generate revenues from licensing our technology in the future, revenues may decline or not grow as anticipated, and our operating results could be substantially harmed for a particular fiscal period. Moreover, our operating results in some quarters may not meet the expectations of stock market analysts and investors. In that case, our stock price most likely would decline.

Some of our revenue is dependent on the award of new contracts from the U.S. government, which we do not directly control.

A substantial portion of our revenue and is generated from sales to the U.S. defense logistics agency through a bid process in response to request for bids. The timing and size of requests for bids is unpredictable and outside of our control. The number of other companies competing for these bids is also unpredictable and outside of our control. In the event of more competition for these awards, we may have to reduce our margins. These variables make it difficult to predict when or if we will sell more products to the US government, which in turns makes it difficult to stock inventory and purchase raw materials.

We have limited product distribution experience, and we rely in part on third parties who may not successfully sell our products.

We have limited product distribution experience and rely in part on product distribution arrangements with third parties. In our future product offerings, we may rely solely on third parties for product sales and distribution. We also plan to license our technology to certain third parties for commercialization of certain applications. We expect to enter into additional distribution agreements and licensing agreements in the future, and we may not be able to enter into these additional agreements on terms that are favorable to us, if at all. In addition, we may have limited or no control over the distribution activities of these third parties. These third parties could sell competing products and may devote insufficient sales efforts to our products. As a result, our future revenues from sales of our products, if any, will depend on the success of the efforts of these third parties.

We may not be able to attract or retain qualified senior personnel.

We believe we are currently able to manage our current business with our existing management team. However, as we expand the scope of our operations, we will need to obtain the full-time services of additional senior management and other personnel. Competition for highly-skilled personnel is intense, and there can be no assurance that we will be able to attract or retain qualified senior personnel. Our failure to do so could have an adverse effect on our ability to implement our business plan. As we add full-time senior personnel, our overhead expenses for salaries and related items will increase from current levels and, depending upon the number of personnel we hire and their compensation packages, these increases could be substantial.

If we lose our key personnel or are unable to attract and retain additional personnel, we may be unable to achieve profitability.

Our future success is substantially dependent on the efforts of our senior management, particularly Dennis P. Calvert, our president and chief executive officer. The loss of the services of Mr. Calvert or other members of our senior management may significantly delay or prevent the achievement of product development and other business objectives. Because of the scientific nature of our business, we depend substantially on our ability to attract and retain qualified marketing, scientific and technical personnel. There is intense competition among specialized and technologically-oriented companies for qualified personnel in the areas of our activities. If we lose the services of, or do not successfully recruit, key marketing, scientific and technical personnel, then the growth of our business could be substantially impaired. At present, we do not maintain key man insurance for any of our senior management, although management is evaluating the potential of securing this type of insurance in the future as may be available.

Nondisclosure agreements with employees and others may not adequately prevent disclosure of trade secrets and other proprietary information.

In order to protect our proprietary technology and processes, we rely in part on nondisclosure agreements with our employees, potential licensing partners, potential manufacturing partners, testing facilities, universities, consultants, agents and other organizations to which we disclose our proprietary information. These agreements may not effectively prevent disclosure of confidential information and may not provide an adequate remedy in the event of unauthorized disclosure of confidential information. In addition, others may independently discover trade secrets and proprietary information, and in such cases we could not assert any trade secret rights against such parties. Costly and time-consuming litigation could be necessary to enforce and determine the scope of our proprietary rights, and failure to obtain or maintain trade secret protection could adversely affect our competitive business position. Since we rely on trade secrets and nondisclosure agreements, in addition to patents, to protect some of our intellectual property, there is a risk that third parties may obtain and improperly utilize our proprietary information to our competitive disadvantage. We may not be able to detect unauthorized use or take appropriate and timely steps to enforce our intellectual property rights.

We may become subject to product liability claims.

As a business that manufactures and markets products for use by consumers and institutions, we may become liable for any damage caused by our products, whether used in the manner intended or not. Any such claim of liability, whether meritorious or not, could be time-consuming and/or result in costly litigation. Although we maintain general liability insurance, our insurance may not cover potential claims of the types described above and may not be adequate to indemnify for all liabilities that may be imposed. Any imposition of liability that is not covered by insurance or is in excess of insurance coverage could harm our business and operating results, and you may lose some or all of any investment you have made, or may make, in our company.

Litigation or the actions of regulatory authorities may harm our business or otherwise distract our management.

Substantial, complex or extended litigation could cause us to incur major expenditures and distract our management. For example, lawsuits by employees, former employees, investors, stockholders, partners, customers or others, or actions taken by regulatory authorities, could be very costly and substantially disrupt our business. As a result of our financing activities over time, and by virtue of the number of people that have invested in our company, we face increased risk of lawsuits from investors. Such lawsuits or actions could from time to time be filed against our company and/or our executive officers and directors. Such lawsuits and actions are not uncommon, and we cannot assure you that we will always be able to resolve such disputes or actions on terms favorable to our company.

If we suffer negative publicity concerning the safety or efficacy of our products, our sales may be harmed.

If concerns should arise about the safety or efficacy of any of our products that are marketed, regardless of whether or not such concerns have a basis in generally accepted science or peer-reviewed scientific research, such concerns could adversely affect the market for those products. Similarly, negative publicity could result in an increased number of product liability claims, whether or not those claims are supported by applicable law.

The licensing of our technology or the manufacture, use or sale of products incorporating our technology may infringe on the patent rights of others, and we may be forced to litigate if an intellectual property dispute arises.

If we infringe or are alleged to have infringed another party’s patent rights, we may be required to seek a license, defend an infringement action or challenge the validity of the patents in court. Patent litigation is costly and time consuming. We may not have sufficient resources to bring these actions to a successful conclusion. In addition, if we do not obtain a license, do not successfully defend an infringement action or are unable to have infringed patents declared invalid, we may:

|

● |

incur substantial monetary damages; |

|

● |

encounter significant delays in marketing our current and proposed product candidates; |

|

● |

be unable to conduct or participate in the manufacture, use or sale of product candidates or methods of treatment requiring licenses; |

|

● |

lose patent protection for our inventions and products; or |

|

● |

find our patents are unenforceable, invalid or have a reduced scope of protection |

Parties making such claims may be able to obtain injunctive relief that could effectively block our company’s ability to further develop or commercialize our current and proposed product candidates in the United States and abroad and could result in the award of substantial damages. Defense of any lawsuit or failure to obtain any such license could substantially harm our company. Litigation, regardless of outcome, could result in substantial cost to, and a diversion of efforts by, our company.

Our patents are expensive to maintain, our patent applications are expensive to prosecute, and thus we are unable to file for patent protection in many countries.

Our ability to compete effectively will depend in part on our ability to develop and maintain proprietary aspects of our technology and either to operate without infringing the proprietary rights of others or to obtain rights to technology owned by third parties. Pending patent applications relating to our technology may not result in the issuance of any patents or any issued patents that will offer protection against competitors with similar technology. We must employ patent attorneys to prosecute our patent applications both in the United States and internationally. International patent protection requires the retention of patent counsel and the payment of patent application fees in each foreign country in which we desire patent protection, on or before filing deadlines set forth by the International Patent Cooperation Treaty (“PCT”). We therefore choose to file patent applications only in foreign countries where we believe the commercial opportunities require it, considering our available financial resources and the needs for our technology. This has resulted, and will continue to result, in the irrevocable loss of patent rights in all but a few foreign jurisdictions.

Patents we receive may be challenged, invalidated or circumvented in the future, or the rights created by those patents may not provide a competitive advantage. We also rely on trade secrets, technical know-how and continuing invention to develop and maintain our competitive position. Others may independently develop substantially equivalent proprietary information and techniques or otherwise gain access to our trade secrets.

We are subject to risks related to future business outside of the United States.

Over time, we may develop business relationships outside of North America, and as those efforts are pursued, we will face risks related to those relationships such as:

|

● |

foreign currency fluctuations; |

|

● |

unstable political, economic, financial and market conditions; |

|

● |

import and export license requirements; |

|

● |

trade restrictions; |

|

● |

increases in tariffs and taxes; |

|

● |

high levels of inflation; |

|

● |

restrictions on repatriating foreign profits back to the United States; |

|

● |

greater difficulty collecting accounts receivable and longer payment cycles; |

|

● |

less favorable intellectual property laws, and the lack of intellectual property legal protection; |

|

● |

regulatory requirements; |

|

● |

unfamiliarity with foreign laws and regulations; and |

|

● |

changes in labor conditions and difficulties in staffing and managing international operations. |

The volatility of certain raw material costs may adversely affect operations and competitive price advantages for products that incorporate our technology.

Most of the chemicals and other key materials that we use in our business, such as minerals, fiber materials and packaging materials, are neither generally scarce nor price sensitive, but prices for such chemicals and materials can be cyclical. Super Absorbent Polymer (SAP) beads, which are a petrochemical derivative, have been subject to periodic scarcity and price volatility from time to time during recent years, although prices are relatively stable at present. Should the volume of our sales increase dramatically, we may have difficulty obtaining SAP beads or other raw materials at a favorable price. Supply and demand factors, which are beyond our control, generally affect the price of our raw materials. We try to minimize the effect of price increases through production efficiency and the use of alternative suppliers, but these efforts are limited by the size of our operations. If we are unable to minimize the effects of increased raw material costs, our business, financial condition, results of operations and cash flows may be materially adversely affected.

Certain of our products sales historically have been highly impacted by fluctuations in seasons and weather.

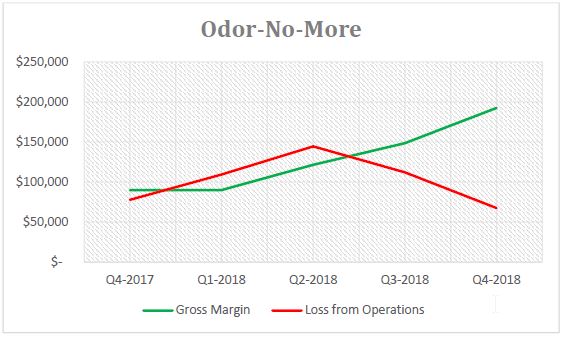

Industrial odor control products have proven highly effective in controlling volatile organic compounds that are released as vapors produced by decomposing waste material. Such vapors are produced with the highest degree of intensity in temperatures between 40 degrees Fahrenheit (5 degrees Celsius) and 140 degrees Fahrenheit (60 degrees Celsius). When weather patterns are cold or in times of precipitation, our clients are less prone to use our odor control products, presumably because such vapors are less noticeable or, in the case of precipitation, can be washed away or altered. This leads to unpredictability in use and sales patterns for, especially, our CupriDyne Clean product line which accounts for over one-half our total sales.

The cost of maintaining our public company reporting obligations is high.

We are obligated to maintain our periodic public filings and public reporting requirements, on a timely basis, under the rules and regulations of the SEC. In order to meet these obligations, we will need to continue to raise capital. If adequate funds are not available, we will be unable to comply with those requirements and could cease to be qualified to have our stock traded in the public market. As a public company, we incur significant legal, accounting and other expenses. In addition, the Sarbanes-Oxley Act of 2002, as well as related rules adopted by the SEC, has imposed substantial requirements on public companies, including certain corporate governance practices and requirements relating to internal control over financial reporting under Section 404 of the Sarbanes-Oxley Act.

Risks Relating to our Common Stock

The sale or issuance of our common stock to Lincoln Park may cause dilution, and the sale of the shares of common stock acquired by Lincoln Park, or the perception that such sales may occur, could cause the price of our common stock to fall.

On August 25, 2017, we entered into the LPC Agreement with Lincoln Park, pursuant to which Lincoln Park has committed to purchase up to $10,000,000 of our common stock, noted above in our Risks Related to our Business. We generally have the right to control the timing and amount of any sales of our shares to Lincoln Park. Sales of our common stock, if any, to Lincoln Park will depend on market conditions and other factors to be determined by us. We may ultimately decide to sell to Lincoln Park all, some or none of the shares of our common stock that may be available for us to sell pursuant to the LPC Agreement. If and when we do sell shares to Lincoln Park, after Lincoln Park has acquired the shares, Lincoln Park may resell all, some or none of those shares at any time or from time to time in its discretion. Therefore, sales to Lincoln Park by us could result in substantial dilution to the interests of other holders of our common stock, as well as sales of our stock by Lincoln Park into the open market causing reductions in the price of our common stock. Additionally, the sale of a substantial number of shares of our common stock to Lincoln Park, or the anticipation of such sales, could make it more difficult for us to sell equity or equity-related securities in the future at a time and at a price that we might otherwise desire to effect sales.

Our common stock is thinly traded and largely illiquid.

Our stock is currently quoted on the OTC Markets (OTCQB). Being quoted on the OTCQB has made it more difficult to buy or sell our stock and from time to time has led to a significant decline in the frequency of trades and trading volume. Continued trading on the OTCQB will also likely adversely affect our ability to obtain financing in the future due to the decreased liquidity of our shares and other restrictions that certain investors have for investing in OTCQB traded securities. While we intend to seek listing on the Nasdaq Stock Market (“Nasdaq”) or another national stock exchange when our company is eligible, there can be no assurance when or if our common stock will be listed on Nasdaq or another national stock exchange.

The market price of our stock is subject to volatility.

|

● |

Because our stock is thinly traded, its price can change dramatically over short periods, even in a single day. An investment in our stock is subject to such volatility and, consequently, is subject to significant risk. The market price of our common stock could fluctuate widely in response to many factors, including: |

|

● |

developments with respect to patents or proprietary rights; |

|

● |

announcements of technological innovations by us or our competitors; |

|

● |

announcements of new products or new contracts by us or our competitors; |

|

● |

actual or anticipated variations in our operating results due to the level of development expenses and other factors; |

|

● |

changes in financial estimates by securities analysts and whether any future earnings of ours meet or exceed such estimates; |

|

● |

conditions and trends in our industry; |

|

● |

new accounting standards; |

|

● |

general economic, political and market conditions and other factors; and |

|

● |

the occurrence of any of the risks described in this Annual Report. |

You may have difficulty selling our shares because they are deemed “penny stocks”.

Because our common stock is not quoted on the Nasdaq National Market or Nasdaq Capital Market or listed on a national securities exchange, if the trading price of our common stock remains below $5.00 per share, which we expect for the foreseeable future, trading in our common stock will be subject to the requirements of certain rules promulgated under the Securities Exchange Act of 1934, as amended (the “Exchange Act”), which require additional disclosure by broker-dealers in connection with any trades involving a stock defined as a penny stock (generally, any non-Nasdaq equity security that has a market price of less than $5.00 per share, subject to certain exceptions). Such rules require the delivery, before any penny stock transaction, of a disclosure schedule explaining the penny stock market and the risks associated therewith and impose various sales practice requirements on broker-dealers who sell penny stocks to persons other than established customers and accredited investors (generally defined as an investor with a net worth in excess of $1,000,000 or annual income exceeding $200,000 individually or $300,000 together with a spouse). For these types of transactions, the broker-dealer must make a special suitability determination for the purchaser and have received the purchaser’s written consent to the transaction before the sale. The broker-dealer also must disclose the commissions payable to the broker-dealer and current bid and offer quotations for the penny stock and, if the broker-dealer is the sole market-maker, the broker-dealer must disclose this fact and the broker-dealer’s presumed control over the market. Such information must be provided to the customer orally or in writing before or with the written confirmation of trade sent to the customer. Monthly statements must be sent disclosing recent price information for the penny stock held in the account and information on the limited market in penny stocks. The additional burdens imposed on broker-dealers by such requirements could discourage broker-dealers from effecting transactions in our common stock, which could severely limit the market liquidity of our common stock and the ability of holders of our common stock to sell their shares.

Because our shares are deemed “penny stocks,” new rules make it more difficult to remove restrictive legends.

Rules put in place by the Financial Industry Regulatory Authority (FINRA) require broker-dealers to perform due diligence before depositing unrestricted common shares of penny stocks, and as such, some broker-dealers, including many national firms (such as eTrade and Charles Schwab), are refusing to deposit previously restricted common shares of penny stocks. As such, it may be more difficult for purchases of shares in our private securities offerings to deposit the shares with broker-dealers and sell those shares on the open market.

Because we will not pay dividends in the foreseeable future, stockholders will only benefit from owning common stock if it appreciates.

We have never declared or paid a cash dividend to stockholders. We intend to retain any earnings that may be generated in the future to finance operations. Accordingly, any potential investor who anticipates the need for current dividends from his investment should not purchase our common stock.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

All statements, other than statements of historical fact, included in this prospectus regarding our strategy, future operations, future financial position, future revenues, projected costs, prospects and plans and objectives of management are forward-looking statements. The words “anticipates,” “believes,” “estimates,” “expects,” “intends,” “may,” “plans,” “projects,” “will,” “would” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain these identifying words.

We have based these forward-looking statements on our current expectations and projections about future events. Although we believe that the expectations underlying our forward-looking statements are reasonable, these expectations may prove to be incorrect, and all of these statements are subject to risks and uncertainties. Therefore, you should not place undue reliance on our forward-looking statements. We have included important risks and uncertainties in the cautionary statements included in this prospectus, particularly the section titled “Risk Factors” incorporated by reference herein. We believe these risks and uncertainties could cause actual results or events to differ materially from the forward-looking statements that we make. Should one or more of these risks and uncertainties materialize, or should underlying assumptions, projections or expectations prove incorrect, actual results, performance or financial condition may vary materially and adversely from those anticipated, estimated or expected. Our forward-looking statements do not reflect the potential impact of future acquisitions, mergers, dispositions, joint ventures or investments that we may make. We do not assume any obligation to update any of the forward-looking statements contained herein, whether as a result of new information, future events or otherwise, except as required by law. In the light of these risks and uncertainties, the forward-looking events and circumstances discussed in this prospectus may not occur, and actual results could differ materially from those anticipated or implied in the forward-looking statements. Any forward-looking statement made by us in this prospectus is based only on information currently available to us and speaks only as of the date on which it is made.

This prospectus relates to shares of our common stock that may be offered and sold from time to time by selling stockholders Vista Capital, FirstFire, Black Mountain, and Gemini. We will receive no proceeds from the sale of shares of common stock by Vista Capital or FirstFire in this offering. We may receive up to $820,000 aggregate gross proceeds under the warrants should Black Mountain and/or Gemini choose to exercise their rights to purchase shares under the warrants. See “Plan of Distribution” elsewhere in this prospectus for more information.

We expect to use any proceeds that we receive under the exercise of the warrants to help fund general working capital for our corporate operations.

We have never declared or paid a cash dividend to stockholders. We intend to retain any earnings that may be generated in the future to finance operations.

The following table sets forth our actual cash and cash equivalents and our capitalization as of December 31, 2018, and as adjusted to give effect to the sale of the shares offered hereby and the use of proceeds, as described in the section titled “Use of Proceeds” above.

You should read this information in conjunction with “Managements’ Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes appearing in our Annual Report on Form 10-K for the periods ended December 31, 2018.

|

As of December 31, 2018 (in thousands) |

||||||||

|

Actual (unaudited) |

As Adjusted(1) |

|||||||

|

CASH AND CASH EQUIVALENTS |

$ | 655 | $ | 1,475 | ||||

|

STOCKHOLDERS’ DEFICIT: |

||||||||

| Convertible Preferred Series A, $.00067 Par Value, 50,000,000 Shares Authorized, -0- Shares Issued and Outstanding, at December 31, 2018 and as adjusted. | — | — | ||||||

|

Common stock, $.00067 Par Value, 400,000,000 Shares Authorized, 141,466,071 Shares Issued at December 31, 2018, and 155,267,190 as adjusted |

95 | 104 | ||||||

|

Additional paid-in capital |

110,222 | 111,033 | ||||||

|

Accumulated deficit |

(111,723 | ) | (111,723 | ) | ||||

|

Accumulated other comprehensive loss |

(90 | ) | (90 | ) | ||||

|

Total BioLargo stockholders’ deficit |

(1,496 | ) | (676 | ) | ||||

|

Non-controlling interest (Note 6) |

373 | 373 | ||||||

|

Total stockholders’ (deficit) equity |

(1,123 | ) | (303 | ) | ||||

|

Total liabilities and stockholders’ equity |

$ | 3,185 | $ | 4,005 | ||||

|

(1) |

The “as adjusted” column assumes Black Mountain and Gemini both purchase all shares pursuant to their warrants for an aggregate exercise price of $820,000, and that all shares registered hereunder are issued. |

The net tangible book value of our company as of December 31, 2018 was negative $1,123,000 or approximately $(0.008) per share of common stock. Net tangible book value per share is determined by dividing the net tangible book value of our company (total tangible assets less total liabilities) by the number of outstanding shares of our common stock.

Assuming all warrants issued to Black Mountain and Gemini are exercised and the exercise price is received by the Company, and the Vista Note is converted to our common stock, our adjusted net tangible book value as of December 31, 2018 would have been negative $303,000 or approximately $(0.002) per share. This represents an immediate increase in net tangible book value of approximately $0.006 per share to existing stockholders.

MARKET PRICE OF AND DIVIDENDS ON COMMON EQUITY

AND RELATED STOCKHOLDER MATTERS

Market Information

Since January 23, 2008, our common stock has been quoted on the OTC Markets “OTCQB” marketplace (formerly known as the “OTC Bulletin Board”) under the trading symbol “BLGO”.