000087688312/312023FYFALSEP3YP10YP3MP1YP1Yhttp://fasb.org/us-gaap/2022#OtherNonoperatingIncomeExpensehttp://fasb.org/us-gaap/2022#OtherNonoperatingIncomeExpensehttp://fasb.org/us-gaap/2022#OtherNonoperatingIncomeExpense00008768832023-01-012023-12-3100008768832023-12-31iso4217:USD0000876883us-gaap:CommonClassAMember2024-03-01xbrli:shares0000876883us-gaap:CommonClassCMember2024-03-0100008768832022-01-012022-12-3100008768832021-01-012021-12-310000876883stgw:ReputationDefenderMember2021-01-012021-12-31iso4217:USDxbrli:shares00008768832022-12-310000876883stgw:CommonClassAAndCommonClassBMember2023-12-310000876883stgw:CommonClassAAndCommonClassBMember2022-12-310000876883us-gaap:CommonClassCMember2023-12-310000876883us-gaap:CommonClassCMember2022-12-3100008768832021-12-3100008768832020-12-310000876883us-gaap:CommonStockMemberstgw:CommonClassAAndBMember2022-12-310000876883us-gaap:CommonStockMemberus-gaap:CommonClassCMember2022-12-310000876883us-gaap:AdditionalPaidInCapitalMember2022-12-310000876883us-gaap:RetainedEarningsMember2022-12-310000876883us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-12-310000876883us-gaap:ParentMember2022-12-310000876883us-gaap:NoncontrollingInterestMember2022-12-310000876883us-gaap:RetainedEarningsMember2023-01-012023-12-310000876883us-gaap:ParentMember2023-01-012023-12-310000876883us-gaap:NoncontrollingInterestMember2023-01-012023-12-310000876883us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-01-012023-12-310000876883us-gaap:AdditionalPaidInCapitalMember2023-01-012023-12-310000876883us-gaap:CommonStockMemberstgw:CommonClassAAndBMember2023-01-012023-12-310000876883us-gaap:CommonStockMemberstgw:CommonClassAAndCommonClassBMember2023-01-012023-12-310000876883us-gaap:CommonStockMemberus-gaap:CommonClassCMember2023-01-012023-12-310000876883us-gaap:CommonStockMemberstgw:CommonClassAAndBMember2023-12-310000876883us-gaap:CommonStockMemberus-gaap:CommonClassCMember2023-12-310000876883us-gaap:AdditionalPaidInCapitalMember2023-12-310000876883us-gaap:RetainedEarningsMember2023-12-310000876883us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-12-310000876883us-gaap:ParentMember2023-12-310000876883us-gaap:NoncontrollingInterestMember2023-12-310000876883us-gaap:CommonStockMemberstgw:CommonClassAAndBMember2021-12-310000876883us-gaap:CommonStockMemberus-gaap:CommonClassCMember2021-12-310000876883us-gaap:AdditionalPaidInCapitalMember2021-12-310000876883us-gaap:RetainedEarningsMember2021-12-310000876883us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-12-310000876883us-gaap:ParentMember2021-12-310000876883us-gaap:NoncontrollingInterestMember2021-12-310000876883us-gaap:RetainedEarningsMember2022-01-012022-12-310000876883us-gaap:ParentMember2022-01-012022-12-310000876883us-gaap:NoncontrollingInterestMember2022-01-012022-12-310000876883us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-01-012022-12-310000876883us-gaap:AdditionalPaidInCapitalMember2022-01-012022-12-310000876883stgw:CommonClassAAndBMember2022-01-012022-12-310000876883us-gaap:CommonStockMemberstgw:CommonClassAAndBMember2022-01-012022-12-310000876883us-gaap:CommonStockMemberus-gaap:CommonClassCMember2022-01-012022-12-310000876883us-gaap:MemberUnitsMember2020-12-310000876883us-gaap:ParentMember2020-12-310000876883us-gaap:NoncontrollingInterestMember2020-12-310000876883us-gaap:MemberUnitsMember2021-01-012021-08-020000876883us-gaap:ParentMember2021-01-012021-08-020000876883us-gaap:NoncontrollingInterestMember2021-01-012021-08-0200008768832021-01-012021-08-020000876883us-gaap:NoncontrollingInterestMember2021-08-032021-12-310000876883us-gaap:PreferredStockMember2021-01-012021-08-020000876883us-gaap:CommonStockMemberstgw:CommonClassAAndBMember2021-01-012021-08-020000876883us-gaap:CommonStockMemberus-gaap:CommonClassCMember2021-01-012021-08-020000876883us-gaap:AdditionalPaidInCapitalMember2021-01-012021-08-020000876883us-gaap:NoncontrollingInterestMember2021-01-012021-12-310000876883us-gaap:RetainedEarningsMember2021-08-032021-12-310000876883us-gaap:ParentMember2021-08-032021-12-3100008768832021-08-032021-12-310000876883us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-08-032021-12-310000876883us-gaap:CommonStockMemberstgw:CommonClassAAndBMember2021-08-032021-12-310000876883us-gaap:AdditionalPaidInCapitalMember2021-08-032021-12-310000876883us-gaap:PreferredStockMember2021-08-032021-12-310000876883stgw:AccumulatedOtherComprehensiveIncomeLossNetOfTaxMember2023-01-012023-03-310000876883stgw:IncomeTaxExpenseMember2023-01-012023-03-310000876883stgw:IncomeTaxPayableMember2023-01-012023-03-310000876883stgw:DeferredTaxAssetMember2023-01-012023-03-3100008768832023-04-012023-06-300000876883stgw:IncomeTaxReceivableAndPayableMember2023-04-012023-06-3000008768832023-01-012023-03-3100008768832023-10-012023-12-310000876883stgw:TaxReceivableAgreementMember2023-10-012023-12-310000876883us-gaap:SubsequentEventMemberstgw:TeamEpiphanyMember2024-01-022024-01-020000876883us-gaap:SubsequentEventMemberstgw:TeamEpiphanyMemberus-gaap:CommonClassAMember2024-01-022024-01-020000876883us-gaap:SubsequentEventMemberstgw:TeamEpiphanyMember2024-01-020000876883us-gaap:SubsequentEventMemberstgw:SidekickLiveLimitedMember2024-03-012024-03-01iso4217:GBP0000876883us-gaap:SubsequentEventMemberstgw:SidekickLiveLimitedMemberus-gaap:CommonClassAMember2024-03-012024-03-010000876883us-gaap:SubsequentEventMemberstgw:SidekickLiveLimitedMember2024-03-010000876883srt:MinimumMember2023-01-012023-12-310000876883srt:MaximumMember2023-01-012023-12-310000876883stgw:MoversAndShakersLLCMember2023-11-012023-11-010000876883us-gaap:CommonClassAMemberstgw:MoversAndShakersLLCMember2023-11-012023-11-010000876883stgw:MoversAndShakersLLCMember2023-11-010000876883stgw:LeftFieldLabsMember2023-10-022023-10-020000876883us-gaap:CommonClassAMemberstgw:LeftFieldLabsMember2023-10-022023-10-020000876883stgw:LeftFieldLabsMember2023-10-020000876883stgw:TinselMember2023-07-032023-07-030000876883stgw:TinselMember2023-07-030000876883stgw:HuskiesMember2023-04-252023-04-25iso4217:EUR0000876883stgw:HuskiesMember2023-04-250000876883stgw:BrandNewGalaxyMember2022-04-192022-04-190000876883stgw:BrandNewGalaxyMember2022-04-19xbrli:pure0000876883us-gaap:CustomerRelationshipsMemberstgw:TMADirectMember2022-04-190000876883stgw:BrandNewGalaxyMemberus-gaap:CustomerRelationshipsMember2022-04-192022-04-190000876883us-gaap:TradeNamesMemberstgw:BrandNewGalaxyMember2022-04-190000876883us-gaap:TradeNamesMemberstgw:TMADirectMember2022-04-192022-04-190000876883us-gaap:OtherIntangibleAssetsMemberstgw:TMADirectMember2022-04-190000876883us-gaap:OtherIntangibleAssetsMemberstgw:TMADirectMember2022-04-192022-04-190000876883stgw:TMADirectMember2022-04-190000876883stgw:BrandNewGalaxyMember2022-01-012022-12-310000876883stgw:BrandNewGalaxyMember2021-01-012021-12-310000876883stgw:BrandNewGalaxyMember2023-01-012023-12-310000876883stgw:TMADirectMember2022-05-310000876883stgw:TMADirectMember2022-05-312022-05-310000876883us-gaap:TradeNamesMemberstgw:TMADirectMember2022-05-310000876883us-gaap:TradeNamesMemberstgw:TMADirectMember2022-05-312022-05-310000876883us-gaap:CustomerRelationshipsMemberstgw:TMADirectMember2022-05-310000876883us-gaap:CustomerRelationshipsMemberstgw:TMADirectMember2022-05-312022-05-310000876883stgw:TMADirectMember2022-01-012022-12-310000876883stgw:TMADirectMember2021-01-012021-12-310000876883stgw:TMADirectMember2023-01-012023-12-310000876883stgw:MaruGroupMember2022-10-030000876883stgw:MaruGroupMember2022-10-032022-10-030000876883stgw:MaruGroupMemberus-gaap:CustomerRelationshipsMember2022-10-030000876883stgw:MaruGroupMemberus-gaap:CustomerRelationshipsMember2022-10-032022-10-030000876883stgw:MaruGroupMemberus-gaap:TradeNamesMember2022-10-030000876883stgw:MaruGroupMemberus-gaap:TradeNamesMember2022-10-032022-10-030000876883stgw:MaruGroupMemberus-gaap:OtherIntangibleAssetsMember2022-10-030000876883stgw:MaruGroupMembersrt:MinimumMemberus-gaap:OtherIntangibleAssetsMember2022-10-032022-10-030000876883stgw:MaruGroupMemberus-gaap:OtherIntangibleAssetsMembersrt:MaximumMember2022-10-032022-10-030000876883stgw:MaruGroupMember2022-01-012022-12-310000876883stgw:MaruGroupMember2021-01-012021-12-310000876883stgw:MaruGroupMember2023-01-012023-12-310000876883stgw:WolfgangMember2022-10-030000876883stgw:WolfgangMember2022-10-032022-10-030000876883us-gaap:CommonClassAMemberstgw:WolfgangMember2022-10-032022-12-310000876883us-gaap:CommonClassAMemberstgw:WolfgangMember2022-10-032022-10-030000876883stgw:WolfgangMember2022-01-012022-12-310000876883stgw:WolfgangMember2021-01-012021-12-310000876883stgw:WolfgangMember2023-01-012023-12-310000876883stgw:EpicenterMember2022-10-032022-10-030000876883stgw:EpicenterMember2022-10-030000876883stgw:EpicenterMember2022-01-012022-12-310000876883stgw:EpicenterMember2021-01-012021-12-310000876883stgw:EpicenterMember2023-01-012023-12-310000876883stgw:StagwellOpCoMemberstgw:MDCMemberstgw:CommonUnitsMember2021-08-020000876883us-gaap:CommonClassCMemberstgw:MDCMemberstgw:StagwellMediaMember2021-08-022021-08-020000876883stgw:StagwellMediaMember2021-08-020000876883stgw:MDCMember2021-08-020000876883stgw:MDCMember2021-08-022021-08-020000876883us-gaap:CommonClassBMemberstgw:MDCMember2021-08-020000876883stgw:IntegratedAgenciesNetworkMemberstgw:MDCMember2021-08-020000876883stgw:BrandPerformanceNetworkMemberstgw:MDCMember2021-08-020000876883stgw:CommunicationsNetworkMemberstgw:MDCMember2021-08-020000876883stgw:MDCMember2021-12-310000876883us-gaap:TradeNamesMemberstgw:MDCMember2021-08-020000876883us-gaap:TradeNamesMemberstgw:MDCMember2021-08-022021-08-020000876883stgw:MDCMemberus-gaap:CustomerRelationshipsMember2021-08-020000876883srt:MinimumMemberstgw:MDCMemberus-gaap:CustomerRelationshipsMember2021-08-022021-08-020000876883stgw:MDCMembersrt:MaximumMemberus-gaap:CustomerRelationshipsMember2021-08-022021-08-020000876883stgw:MDCMember2020-01-012020-12-310000876883stgw:MDCMember2021-08-032021-12-310000876883stgw:MDCMember2021-01-012021-12-310000876883stgw:GoodstuffHoldingsLimitedMember2021-12-312021-12-310000876883stgw:GoodstuffHoldingsLimitedMember2021-12-310000876883stgw:GoodstuffHoldingsLimitedMembersrt:MaximumMember2021-12-310000876883stgw:GoodstuffHoldingsLimitedMember2021-08-022021-08-020000876883stgw:GoodstuffHoldingsLimitedMemberus-gaap:TradeNamesMember2021-12-310000876883stgw:GoodstuffHoldingsLimitedMemberus-gaap:TradeNamesMember2021-12-312021-12-310000876883stgw:GoodstuffHoldingsLimitedMemberus-gaap:CustomerRelationshipsMember2021-12-310000876883stgw:GoodstuffHoldingsLimitedMemberus-gaap:CustomerRelationshipsMember2021-12-312021-12-310000876883stgw:GoodstuffHoldingsLimitedMember2021-01-012021-12-310000876883stgw:GoodstuffHoldingsLimitedMember2020-01-012020-12-310000876883stgw:PEPGroupMember2022-07-122022-07-120000876883stgw:PEPGroupMember2022-07-120000876883stgw:ApolloMember2022-07-152022-07-150000876883us-gaap:DisposalGroupDisposedOfBySaleNotDiscontinuedOperationsMemberstgw:ConcentricLifeMember2023-10-310000876883us-gaap:OtherNonoperatingIncomeExpenseMemberus-gaap:DisposalGroupDisposedOfBySaleNotDiscontinuedOperationsMemberstgw:ConcentricLifeMember2023-10-312023-10-310000876883us-gaap:DisposalGroupDisposedOfBySaleNotDiscontinuedOperationsMemberstgw:ReputationDefenderMember2021-09-150000876883us-gaap:OtherNonoperatingIncomeExpenseMemberus-gaap:DisposalGroupDisposedOfBySaleNotDiscontinuedOperationsMemberstgw:ReputationDefenderMember2021-09-152021-09-150000876883stgw:HelloDesignMember2022-04-012022-04-010000876883stgw:HelloDesignMember2022-04-010000876883stgw:TargetedVictoryMember2021-10-010000876883stgw:TargetedVictoryMember2023-07-310000876883stgw:TargetedVictoryMember2021-10-012021-10-010000876883stgw:TargetedVictoryMemberus-gaap:CommonClassAMember2021-10-012021-10-010000876883stgw:ConcentricLifeMember2021-12-010000876883stgw:ConcentricLifeMember2021-12-012021-12-010000876883stgw:ConcentricLifeMember2021-10-010000876883stgw:InstrumentHoldingsInc.Member2021-12-310000876883stgw:InstrumentHoldingsInc.Member2021-12-312021-12-310000876883stgw:InstrumentHoldingsInc.Member2021-12-012021-12-010000876883stgw:InstrumentHoldingsInc.Memberus-gaap:CommonClassAMember2021-12-312021-12-310000876883stgw:InstrumentHoldingsInc.Memberus-gaap:CommonClassAMember2021-12-310000876883stgw:PrincipalCapabilityMember2023-01-012023-12-310000876883stgw:DigitalTransformationMember2023-01-012023-12-310000876883stgw:DigitalTransformationMember2022-01-012022-12-310000876883stgw:DigitalTransformationMember2021-01-012021-12-310000876883stgw:CreativityAndCommunicationsMember2023-01-012023-12-310000876883stgw:CreativityAndCommunicationsMember2022-01-012022-12-310000876883stgw:CreativityAndCommunicationsMember2021-01-012021-12-310000876883stgw:PerformanceMediaAndDataMember2023-01-012023-12-310000876883stgw:PerformanceMediaAndDataMember2022-01-012022-12-310000876883stgw:PerformanceMediaAndDataMember2021-01-012021-12-310000876883stgw:ConsumerInsightsAndStrategyMember2023-01-012023-12-310000876883stgw:ConsumerInsightsAndStrategyMember2022-01-012022-12-310000876883stgw:ConsumerInsightsAndStrategyMember2021-01-012021-12-310000876883stgw:StagwellMarketingCloudGroupMember2023-01-012023-12-310000876883stgw:StagwellMarketingCloudGroupMember2022-01-012022-12-310000876883stgw:StagwellMarketingCloudGroupMember2021-01-012021-12-310000876883stgw:NonUSAndUKMember2023-12-31stgw:country0000876883stgw:ByLocationMember2023-01-012023-12-310000876883country:US2023-01-012023-12-310000876883country:US2022-01-012022-12-310000876883country:US2021-01-012021-12-310000876883country:GB2023-01-012023-12-310000876883country:GB2022-01-012022-12-310000876883country:GB2021-01-012021-12-310000876883stgw:OtherGeographicalLocationMember2023-01-012023-12-310000876883stgw:OtherGeographicalLocationMember2022-01-012022-12-310000876883stgw:OtherGeographicalLocationMember2021-01-012021-12-3100008768832024-01-012023-12-3100008768832025-01-012023-12-3100008768832026-01-012023-12-310000876883stgw:StagwellMediaMember2023-01-012023-12-310000876883stgw:StagwellGlobalMember2023-01-012023-12-310000876883us-gaap:StockAppreciationRightsSARSMember2023-01-012023-12-310000876883us-gaap:RestrictedStockUnitsRSUMember2023-01-012023-12-310000876883us-gaap:EmployeeStockMember2023-01-012023-12-310000876883us-gaap:CommonClassCMember2023-01-012023-12-310000876883stgw:StockAppreciationRightsAndRestrictedAwardsMember2023-01-012023-12-310000876883stgw:StagwellMediaMember2022-01-012022-12-310000876883stgw:StagwellGlobalMember2022-01-012022-12-310000876883us-gaap:StockAppreciationRightsSARSMember2022-01-012022-12-310000876883us-gaap:RestrictedStockUnitsRSUMember2022-01-012022-12-310000876883us-gaap:CommonClassCMember2022-01-012022-12-310000876883us-gaap:CommonClassAMember2022-01-012022-12-310000876883us-gaap:CommonClassCMember2021-01-012021-12-310000876883stgw:StockAppreciationRightsAndRestrictedAwardsMember2021-01-012021-12-3100008768832021-09-230000876883stgw:Series6ConvertiblePreferredSharesMemberstgw:StagwellAgencyHoldingsLLCMember2021-09-230000876883us-gaap:CommonClassAMember2021-10-072021-10-070000876883stgw:Series8PreferredStockMemberstgw:TheGoldmanSachsGroupIncMember2021-12-310000876883us-gaap:CommonClassAMember2021-11-082021-11-080000876883stgw:ComputersFurnitureAndFixturesMember2023-12-310000876883stgw:ComputersFurnitureAndFixturesMember2022-12-310000876883us-gaap:LeaseholdImprovementsMember2023-12-310000876883us-gaap:LeaseholdImprovementsMember2022-12-310000876883stgw:IntegratedAgenciesNetworkMemberus-gaap:OperatingSegmentsMember2020-12-310000876883us-gaap:OperatingSegmentsMemberstgw:BrandPerformanceNetworkMember2020-12-310000876883stgw:CommunicationsNetworkMemberus-gaap:OperatingSegmentsMember2020-12-310000876883stgw:AllOtherMemberus-gaap:OperatingSegmentsMember2020-12-310000876883stgw:IntegratedAgenciesNetworkMemberus-gaap:OperatingSegmentsMember2021-01-012021-12-310000876883us-gaap:OperatingSegmentsMemberstgw:BrandPerformanceNetworkMember2021-01-012021-12-310000876883stgw:CommunicationsNetworkMemberus-gaap:OperatingSegmentsMember2021-01-012021-12-310000876883stgw:AllOtherMemberus-gaap:OperatingSegmentsMember2021-01-012021-12-310000876883stgw:IntegratedAgenciesNetworkMemberus-gaap:OperatingSegmentsMember2021-12-310000876883us-gaap:OperatingSegmentsMemberstgw:BrandPerformanceNetworkMember2021-12-310000876883stgw:CommunicationsNetworkMemberus-gaap:OperatingSegmentsMember2021-12-310000876883stgw:AllOtherMemberus-gaap:OperatingSegmentsMember2021-12-310000876883stgw:IntegratedAgenciesNetworkMemberus-gaap:OperatingSegmentsMember2022-01-012022-12-310000876883us-gaap:OperatingSegmentsMemberstgw:BrandPerformanceNetworkMember2022-01-012022-12-310000876883stgw:CommunicationsNetworkMemberus-gaap:OperatingSegmentsMember2022-01-012022-12-310000876883stgw:AllOtherMemberus-gaap:OperatingSegmentsMember2022-01-012022-12-310000876883stgw:IntegratedAgenciesNetworkMemberus-gaap:OperatingSegmentsMember2022-12-310000876883us-gaap:OperatingSegmentsMemberstgw:BrandPerformanceNetworkMember2022-12-310000876883stgw:CommunicationsNetworkMemberus-gaap:OperatingSegmentsMember2022-12-310000876883stgw:AllOtherMemberus-gaap:OperatingSegmentsMember2022-12-310000876883stgw:IntegratedAgenciesNetworkMemberus-gaap:OperatingSegmentsMember2023-01-012023-12-310000876883us-gaap:OperatingSegmentsMemberstgw:BrandPerformanceNetworkMember2023-01-012023-12-310000876883stgw:CommunicationsNetworkMemberus-gaap:OperatingSegmentsMember2023-01-012023-12-310000876883stgw:AllOtherMemberus-gaap:OperatingSegmentsMember2023-01-012023-12-310000876883stgw:IntegratedAgenciesNetworkMemberus-gaap:OperatingSegmentsMember2023-12-310000876883us-gaap:OperatingSegmentsMemberstgw:BrandPerformanceNetworkMember2023-12-310000876883stgw:CommunicationsNetworkMemberus-gaap:OperatingSegmentsMember2023-12-310000876883stgw:AllOtherMemberus-gaap:OperatingSegmentsMember2023-12-310000876883us-gaap:CustomerRelationshipsMember2023-12-310000876883us-gaap:CustomerRelationshipsMember2022-12-310000876883us-gaap:TrademarksMember2023-12-310000876883us-gaap:TrademarksMember2022-12-310000876883us-gaap:SoftwareAndSoftwareDevelopmentCostsMember2023-12-310000876883us-gaap:SoftwareAndSoftwareDevelopmentCostsMember2022-12-310000876883us-gaap:OtherIntangibleAssetsMember2023-12-310000876883us-gaap:OtherIntangibleAssetsMember2022-12-310000876883stgw:IntegratedAgenciesNetworkAndBrandPerformanceNetworkMember2021-01-012021-12-310000876883us-gaap:CustomerRelationshipsMember2023-01-012023-12-310000876883us-gaap:TrademarksMember2023-01-012023-12-310000876883us-gaap:SoftwareAndSoftwareDevelopmentCostsMember2023-01-012023-12-310000876883us-gaap:OtherIntangibleAssetsMember2023-01-012023-12-310000876883srt:WeightedAverageMember2023-01-012023-12-3100008768832023-01-012023-06-300000876883us-gaap:CommonClassAMember2023-01-012023-12-310000876883us-gaap:CommonClassAMember2023-01-012023-06-300000876883stgw:ContingentPaymentMember2023-12-310000876883stgw:FixedpaymentsMember2023-12-310000876883stgw:ContingentPaymentMember2022-12-310000876883stgw:FixedpaymentsMember2022-12-310000876883us-gaap:CommonClassAMember2023-12-310000876883us-gaap:CommonClassAMember2022-12-31stgw:lease0000876883stgw:CombinedCreditAgreementMember2023-12-310000876883stgw:CombinedCreditAgreementMember2022-12-310000876883us-gaap:SeniorNotesMemberstgw:FivePointSixTwoFivePercentSeniorNotesMember2021-08-200000876883us-gaap:SeniorNotesMemberstgw:FivePointSixTwoFivePercentSeniorNotesMember2023-12-310000876883us-gaap:SeniorNotesMemberstgw:FivePointSixTwoFivePercentSeniorNotesMember2022-12-310000876883stgw:InterestAndDebtExpenseMember2023-01-012023-12-310000876883stgw:InterestAndDebtExpenseMember2022-01-012022-12-310000876883stgw:InterestAndDebtExpenseMember2021-01-012021-12-310000876883us-gaap:SecuredDebtMemberus-gaap:RevolvingCreditFacilityMemberstgw:CombinedCreditAgreementMember2021-08-0200008768832023-06-300000876883currency:GBPus-gaap:SecuredDebtMemberus-gaap:RevolvingCreditFacilityMemberstgw:CombinedCreditAgreementMember2021-08-020000876883currency:EURus-gaap:SecuredDebtMemberus-gaap:RevolvingCreditFacilityMemberstgw:CombinedCreditAgreementMember2021-08-020000876883us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMemberstgw:CombinedCreditAgreementMember2021-08-020000876883us-gaap:SecuredDebtMemberus-gaap:RevolvingCreditFacilityMemberstgw:FederalFundsMemberstgw:CombinedCreditAgreementMember2023-01-012023-12-310000876883stgw:AdjustedTermSOFRRateMemberus-gaap:SecuredDebtMemberus-gaap:RevolvingCreditFacilityMemberstgw:CombinedCreditAgreementMember2023-01-012023-12-310000876883us-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMemberus-gaap:SecuredDebtMemberus-gaap:RevolvingCreditFacilityMemberstgw:CombinedCreditAgreementMember2023-01-012023-12-310000876883us-gaap:StandbyLettersOfCreditMemberus-gaap:RevolvingCreditFacilityMemberstgw:CombinedCreditAgreementMember2021-08-020000876883us-gaap:LetterOfCreditMemberus-gaap:RevolvingCreditFacilityMemberstgw:CombinedCreditAgreementMember2023-12-310000876883us-gaap:LetterOfCreditMemberus-gaap:RevolvingCreditFacilityMemberstgw:CombinedCreditAgreementMember2022-12-310000876883us-gaap:SeniorNotesMemberus-gaap:DebtInstrumentRedemptionPeriodTwoMemberstgw:FivePointSixTwoFivePercentSeniorNotesMember2021-08-202021-08-200000876883us-gaap:SeniorNotesMemberus-gaap:DebtInstrumentRedemptionPeriodThreeMemberstgw:FivePointSixTwoFivePercentSeniorNotesMember2021-08-202021-08-200000876883us-gaap:SeniorNotesMemberstgw:FivePointSixTwoFivePercentSeniorNotesMemberus-gaap:DebtInstrumentRedemptionPeriodFourMember2021-08-202021-08-200000876883us-gaap:DebtInstrumentRedemptionPeriodOneMemberus-gaap:SeniorNotesMemberstgw:FivePointSixTwoFivePercentSeniorNotesMember2021-08-202021-08-200000876883us-gaap:SeniorNotesMemberstgw:FivePointSixTwoFivePercentSeniorNotesMember2021-08-202021-08-200000876883us-gaap:SeniorNotesMemberstgw:DebtInstrumentRedemptionWithEquityOfferingProceedsPeriodOneMemberstgw:FivePointSixTwoFivePercentSeniorNotesMember2021-08-202021-08-200000876883us-gaap:DividendDeclaredMember2023-12-310000876883us-gaap:MoneyMarketFundsMember2023-12-310000876883us-gaap:MutualFundMember2023-12-310000876883us-gaap:MoneyMarketFundsMember2022-12-310000876883us-gaap:MutualFundMember2022-12-310000876883us-gaap:EquitySecuritiesMember2023-12-310000876883us-gaap:EquitySecuritiesMember2022-12-310000876883us-gaap:DebtSecuritiesMember2023-12-310000876883us-gaap:DebtSecuritiesMember2022-12-310000876883us-gaap:CashAndCashEquivalentsMember2023-12-310000876883us-gaap:CashAndCashEquivalentsMember2022-12-310000876883stgw:StagwellMediaMember2021-01-012021-12-310000876883stgw:StagwellGlobalMember2021-01-012021-12-310000876883stgw:StagwellMediaMember2023-12-310000876883stgw:StagwellMediaMember2022-12-310000876883stgw:StagwellGlobalMember2023-12-310000876883stgw:StagwellGlobalMember2022-12-3100008768832023-01-012023-09-300000876883stgw:VestingoverperiodMember2023-12-310000876883stgw:TerminationdisabilityordeathMember2023-12-310000876883us-gaap:CommonClassAMember2023-12-31stgw:vote00008768832023-05-1100008768832023-03-0100008768832023-05-232023-05-2300008768832023-05-230000876883us-gaap:CommonClassAMember2023-01-012023-12-3100008768832023-09-300000876883us-gaap:CommonClassAMember2023-09-300000876883stgw:StockCompensationAwardMember2023-01-012023-12-310000876883stgw:StockCompensationAwardMember2022-01-012022-12-310000876883stgw:StockCompensationAwardMember2021-01-012021-12-310000876883stgw:TimeBasedAwardsMember2022-12-310000876883us-gaap:PerformanceSharesMember2022-12-310000876883stgw:TimeBasedAwardsMember2023-01-012023-12-310000876883us-gaap:PerformanceSharesMember2023-01-012023-12-310000876883stgw:TimeBasedAwardsMember2023-12-310000876883us-gaap:PerformanceSharesMember2023-12-310000876883stgw:TimeBasedAwardsMember2022-01-012022-12-310000876883stgw:TimeBasedAwardsMember2021-01-012021-12-310000876883us-gaap:PerformanceSharesMember2022-01-012022-12-310000876883us-gaap:PerformanceSharesMember2021-01-012021-12-310000876883stgw:RestrictedStockAndRestrictedStockUnitsMember2023-01-012023-12-310000876883stgw:RestrictedStockAndRestrictedStockUnitsMember2022-01-012022-12-310000876883stgw:RestrictedStockAndRestrictedStockUnitsMember2021-01-012021-12-310000876883us-gaap:StockAppreciationRightsSARSMember2022-12-310000876883us-gaap:StockAppreciationRightsSARSMember2023-01-012023-12-310000876883us-gaap:StockAppreciationRightsSARSMember2023-12-310000876883us-gaap:StockAppreciationRightsSARSMember2021-01-012021-12-310000876883srt:MinimumMemberus-gaap:StockAppreciationRightsSARSMember2021-12-310000876883us-gaap:StockAppreciationRightsSARSMembersrt:MaximumMember2021-12-310000876883srt:MinimumMemberus-gaap:StockAppreciationRightsSARSMember2021-01-012021-12-310000876883us-gaap:StockAppreciationRightsSARSMembersrt:MaximumMember2021-01-012021-12-310000876883srt:MinimumMemberstgw:StockAppreciationRightsGrantedIn2023Member2023-12-310000876883stgw:StockAppreciationRightsGrantedIn2023Membersrt:MaximumMember2023-12-310000876883srt:MinimumMemberstgw:StockAppreciationRightsGrantedIn2023Member2023-01-012023-12-310000876883stgw:StockAppreciationRightsGrantedIn2023Membersrt:MaximumMember2023-01-012023-12-310000876883stgw:StockAppreciationRightsGrantedIn2023Member2023-01-012023-12-310000876883srt:MinimumMemberus-gaap:StockAppreciationRightsSARSMember2023-01-012023-12-310000876883us-gaap:StockAppreciationRightsSARSMembersrt:MaximumMember2023-01-012023-12-310000876883us-gaap:StockAppreciationRightsSARSMember2022-01-012022-12-310000876883stgw:OtherAwardsMember2023-12-310000876883stgw:OtherAwardsMember2022-12-310000876883us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2021-12-310000876883us-gaap:AccumulatedTranslationAdjustmentMember2021-12-310000876883us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2022-01-012022-12-310000876883us-gaap:AccumulatedTranslationAdjustmentMember2022-01-012022-12-310000876883us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2022-12-310000876883us-gaap:AccumulatedTranslationAdjustmentMember2022-12-310000876883us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2023-01-012023-12-310000876883us-gaap:AccumulatedTranslationAdjustmentMember2023-01-012023-12-310000876883us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2023-12-310000876883us-gaap:AccumulatedTranslationAdjustmentMember2023-12-310000876883us-gaap:DomesticCountryMember2023-01-012023-12-310000876883us-gaap:DomesticCountryMember2022-01-012022-12-310000876883us-gaap:DomesticCountryMember2021-01-012021-12-310000876883us-gaap:ForeignCountryMember2023-01-012023-12-310000876883us-gaap:ForeignCountryMember2022-01-012022-12-310000876883us-gaap:ForeignCountryMember2021-01-012021-12-3100008768832022-09-3000008768832022-02-010000876883us-gaap:GeneralBusinessMember2023-12-310000876883us-gaap:DomesticCountryMember2023-12-310000876883us-gaap:StateAndLocalJurisdictionMembersrt:SubsidiariesMember2023-12-310000876883us-gaap:ForeignCountryMembersrt:SubsidiariesMember2022-12-310000876883us-gaap:DomesticCountryMembersrt:SubsidiariesMember2023-12-310000876883us-gaap:ForeignCountryMembersrt:SubsidiariesMember2023-12-310000876883srt:MinimumMember2023-12-310000876883srt:MaximumMember2023-12-310000876883us-gaap:SeniorNotesMemberus-gaap:CarryingReportedAmountFairValueDisclosureMember2023-12-310000876883us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:SeniorNotesMember2023-12-310000876883us-gaap:SeniorNotesMemberus-gaap:CarryingReportedAmountFairValueDisclosureMember2022-12-310000876883us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:SeniorNotesMember2022-12-310000876883srt:MinimumMemberus-gaap:FairValueInputsLevel3Member2023-12-310000876883srt:DirectorMemberstgw:TechnologicalServicesMember2023-12-310000876883stgw:MarketingAndAdvertisingServicesMembersrt:DirectorMember2023-01-012023-12-310000876883stgw:MarketingAndAdvertisingServicesMembersrt:DirectorMember2022-01-012022-12-310000876883stgw:MarketingAndAdvertisingServicesMembersrt:DirectorMember2023-12-310000876883stgw:MarketingAndAdvertisingServicesMembersrt:DirectorMember2022-12-310000876883stgw:MarketingAndAdvertisingServicesMembersrt:AffiliatedEntityMember2023-12-310000876883stgw:MarketingAndAdvertisingServicesMembersrt:AffiliatedEntityMember2023-01-012023-12-310000876883stgw:MarketingAndAdvertisingServicesMembersrt:AffiliatedEntityMember2022-01-012022-12-310000876883stgw:MarketingAndAdvertisingServicesMembersrt:AffiliatedEntityMember2021-01-012021-12-310000876883stgw:MarketingAndAdvertisingServicesMembersrt:AffiliatedEntityMember2022-12-310000876883stgw:MarketingAndWebsiteDevelopmentServicesMemberus-gaap:BeneficialOwnerMemberstgw:StagwellAffiliateMember2023-12-310000876883stgw:MarketingAndWebsiteDevelopmentServicesMemberus-gaap:BeneficialOwnerMemberstgw:StagwellAffiliateMember2023-01-012023-12-310000876883stgw:MarketingAndWebsiteDevelopmentServicesMemberus-gaap:BeneficialOwnerMemberstgw:StagwellAffiliateMember2022-01-012022-12-310000876883stgw:MarketingAndWebsiteDevelopmentServicesMemberus-gaap:BeneficialOwnerMemberstgw:StagwellAffiliateMember2021-01-012021-12-310000876883stgw:MarketingAndWebsiteDevelopmentServicesMemberus-gaap:BeneficialOwnerMemberstgw:StagwellAffiliateMember2022-12-310000876883stgw:PollingServicesMemberus-gaap:ImmediateFamilyMemberOfManagementOrPrincipalOwnerMember2023-12-310000876883stgw:PollingServicesMemberus-gaap:ImmediateFamilyMemberOfManagementOrPrincipalOwnerMember2023-01-012023-12-310000876883stgw:PollingServicesMemberus-gaap:ImmediateFamilyMemberOfManagementOrPrincipalOwnerMember2022-01-012022-12-310000876883stgw:PollingServicesMemberus-gaap:ImmediateFamilyMemberOfManagementOrPrincipalOwnerMember2021-01-012021-12-310000876883stgw:PollingServicesMemberus-gaap:ImmediateFamilyMemberOfManagementOrPrincipalOwnerMember2022-12-310000876883stgw:ImmediateFamilyMemberOfCompanysPresidentMemberstgw:PollingServicesMember2023-12-310000876883stgw:ImmediateFamilyMemberOfCompanysPresidentMemberstgw:PollingServicesMember2023-01-012023-12-310000876883stgw:ImmediateFamilyMemberOfCompanysPresidentMemberstgw:PollingServicesMember2022-01-012022-12-310000876883stgw:ImmediateFamilyMemberOfCompanysPresidentMemberstgw:PollingServicesMember2022-12-310000876883stgw:PollingServicesMembersrt:AffiliatedEntityMember2023-12-310000876883stgw:PollingServicesMembersrt:AffiliatedEntityMember2023-01-012023-12-310000876883stgw:PollingServicesMembersrt:AffiliatedEntityMember2022-01-012022-12-310000876883stgw:PollingServicesMembersrt:AffiliatedEntityMember2022-12-310000876883srt:AffiliatedEntityMemberstgw:LoanAgreementRelatedPartyMember2023-12-310000876883srt:AffiliatedEntityMemberstgw:LoanAgreementRelatedPartyMember2022-12-310000876883srt:AffiliatedEntityMemberstgw:LoanAgreementRelatedPartyMember2023-01-012023-12-310000876883srt:AffiliatedEntityMemberstgw:LoanAgreementRelatedPartyMember2022-01-012022-12-310000876883srt:AffiliatedEntityMemberstgw:LoanAgreementRelatedPartyMember2021-01-012021-12-310000876883stgw:SalesAndManagementServicesMembersrt:AffiliatedEntityMember2023-01-012023-12-310000876883stgw:SalesAndManagementServicesMembersrt:AffiliatedEntityMember2022-01-012022-12-310000876883stgw:SalesAndManagementServicesMembersrt:AffiliatedEntityMember2021-01-012021-12-310000876883stgw:SalesAndManagementServicesMembersrt:AffiliatedEntityMember2023-12-310000876883stgw:SalesAndManagementServicesMembersrt:AffiliatedEntityMember2022-12-310000876883stgw:MarketingAndAdvertisingServicesMemberstgw:DirectorInBrandMember2023-01-012023-12-310000876883stgw:MarketingAndAdvertisingServicesMemberstgw:DirectorInBrandMember2022-01-012022-12-310000876883stgw:MarketingAndAdvertisingServicesMemberstgw:DirectorInBrandMember2021-01-012021-12-310000876883stgw:MarketingAndAdvertisingServicesMemberstgw:DirectorInBrandMember2022-12-310000876883stgw:MarketingAndAdvertisingServicesMemberstgw:DirectorInBrandMember2023-12-310000876883stgw:EmployeeOfSubsidiaryMember2023-01-012023-12-31stgw:reportable_segment0000876883stgw:IntegratedAgenciesNetworkMemberus-gaap:OperatingSegmentsMember2023-01-012023-12-310000876883stgw:IntegratedAgenciesNetworkMemberus-gaap:OperatingSegmentsMember2022-01-012022-12-310000876883stgw:IntegratedAgenciesNetworkMemberus-gaap:OperatingSegmentsMember2021-01-012021-12-310000876883stgw:BrandPerformanceNetworkMemberus-gaap:OperatingSegmentsMember2023-01-012023-12-310000876883stgw:BrandPerformanceNetworkMemberus-gaap:OperatingSegmentsMember2022-01-012022-12-310000876883stgw:BrandPerformanceNetworkMemberus-gaap:OperatingSegmentsMember2021-01-012021-12-310000876883stgw:CommunicationsNetworkMemberus-gaap:OperatingSegmentsMember2023-01-012023-12-310000876883stgw:CommunicationsNetworkMemberus-gaap:OperatingSegmentsMember2022-01-012022-12-310000876883stgw:CommunicationsNetworkMemberus-gaap:OperatingSegmentsMember2021-01-012021-12-310000876883stgw:AllOtherMemberus-gaap:OperatingSegmentsMember2023-01-012023-12-310000876883stgw:AllOtherMemberus-gaap:OperatingSegmentsMember2022-01-012022-12-310000876883stgw:AllOtherMemberus-gaap:OperatingSegmentsMember2021-01-012021-12-310000876883us-gaap:CorporateNonSegmentMember2023-01-012023-12-310000876883us-gaap:CorporateNonSegmentMember2022-01-012022-12-310000876883us-gaap:CorporateNonSegmentMember2021-01-012021-12-310000876883country:US2023-12-310000876883stgw:AllOtherCountriesMember2023-12-310000876883country:US2022-12-310000876883stgw:AllOtherCountriesMember2022-12-310000876883srt:ScenarioPreviouslyReportedMember2022-01-012022-12-310000876883srt:RestatementAdjustmentMember2022-01-012022-12-310000876883srt:ScenarioPreviouslyReportedMember2022-12-310000876883srt:RestatementAdjustmentMember2022-12-3100008768832023-07-012023-09-300000876883srt:ScenarioPreviouslyReportedMember2023-01-012023-03-310000876883srt:RestatementAdjustmentMember2023-01-012023-03-310000876883srt:ScenarioPreviouslyReportedMember2023-04-012023-06-300000876883srt:RestatementAdjustmentMember2023-04-012023-06-300000876883srt:ScenarioPreviouslyReportedMember2023-01-012023-06-300000876883srt:RestatementAdjustmentMember2023-01-012023-06-300000876883srt:ScenarioPreviouslyReportedMember2023-01-012023-09-300000876883srt:RestatementAdjustmentMember2023-01-012023-09-300000876883srt:ScenarioPreviouslyReportedMemberus-gaap:RetainedEarningsMember2023-01-012023-03-310000876883srt:RestatementAdjustmentMemberus-gaap:RetainedEarningsMember2023-01-012023-03-310000876883us-gaap:RetainedEarningsMember2023-01-012023-03-310000876883us-gaap:NoncontrollingInterestMembersrt:ScenarioPreviouslyReportedMember2023-01-012023-03-310000876883srt:RestatementAdjustmentMemberus-gaap:NoncontrollingInterestMember2023-01-012023-03-310000876883us-gaap:NoncontrollingInterestMember2023-01-012023-03-310000876883us-gaap:AccumulatedOtherComprehensiveIncomeMembersrt:ScenarioPreviouslyReportedMember2023-01-012023-03-310000876883srt:RestatementAdjustmentMemberus-gaap:AccumulatedOtherComprehensiveIncomeMember2023-01-012023-03-310000876883us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-01-012023-03-310000876883us-gaap:AllowanceForCreditLossMember2022-12-310000876883us-gaap:AllowanceForCreditLossMember2023-01-012023-12-310000876883us-gaap:AllowanceForCreditLossMember2023-12-310000876883us-gaap:AllowanceForCreditLossMember2021-12-310000876883us-gaap:AllowanceForCreditLossMember2022-01-012022-12-310000876883us-gaap:AllowanceForCreditLossMember2020-12-310000876883us-gaap:AllowanceForCreditLossMember2021-01-012021-12-310000876883us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2022-12-310000876883us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2023-01-012023-12-310000876883us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2023-12-310000876883us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2021-12-310000876883us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2022-01-012022-12-310000876883us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2020-12-310000876883us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2021-01-012021-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| | | | | | | | |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended December 31, 2023

or

| | | | | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ______________ to ______________

Commission File Number: 001-13718

Stagwell Inc.

(Exact name of registrant as specified in its charter)

| | | | | | | | | | | |

| Delaware | | 86-1390679 |

(State or other jurisdiction of

incorporation or organization) | | (IRS Employer Identification No.) |

| | | | |

One World Trade Center, Floor 65

| | |

| New York, | New York | | 10007 |

| (Address of principal executive offices) | | (Zip Code) |

(646) 429-1800

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Class A Common Stock, par value $0.001 per share | STGW | NASDAQ |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | |

| Large accelerated Filer | ☐ | Accelerated Filer | ☒ |

| Non-accelerated Filer | ☐ | Smaller reporting company | ☐ |

| Emerging growth company | ☐ | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☒

Indicate by check mark whether any of those error corrections are restatements that required recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the voting and non-voting common stock of the registrant held by non-affiliates as of June 30, 2023, the last business day of the registrant’s most recently completed second fiscal quarter, was approximately $628.9 million, computed upon the basis of the closing sales price of $7.21 of the Class A Common Stock on that date.

The number of shares of common stock outstanding as of March 1, 2024 was 116,906,352 shares of Class A Common Stock and 151,648,741 shares of Class C Common Stock.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s Proxy Statement relating to the 2024 Annual Meeting of Stockholders are incorporated by reference in Part III of this Annual Report on Form 10-K where indicated.

STAGWELL INC.

TABLE OF CONTENTS

| | | | | | | | |

| | | Page |

| | PART I | |

| Item 1. | | |

| Item 1A. | | |

| Item 1B. | | |

Item 1C. | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| | PART II | |

| Item 5. | | |

| Item 6. | [Reserved] |

|

| Item 7. | | |

| Item 7A. | | |

| Item 8. | | |

| Item 9. | | |

| Item 9A. | | |

| Item 9B. | | |

| Item 9C. | | |

| PART III | |

| Item 10. | | |

| Item 11. | | |

| Item 12. | | |

| Item 13. | | |

| Item 14. | | |

| PART IV | |

| Item 15. | | |

| Item 16. | | |

| | |

EXPLANATORY NOTE

On December 21, 2020, MDC Partners Inc. (“MDC”) and Stagwell Media LP (“Stagwell Media”) announced that they had entered into an agreement, providing for the combination of MDC with the operating businesses and subsidiaries of Stagwell Media (the “Stagwell Subject Entities”) (the “Transaction Agreement”). The Stagwell Subject Entities comprised Stagwell Marketing Group LLC (“Stagwell Marketing” or “SMG”) and its direct and indirect subsidiaries.

On August 2, 2021 (the “Closing Date”), we completed the combination of MDC and the Stagwell Subject Entities and a series of steps and related transactions (such combination and transactions, the “Transactions”). In connection with the Transactions, among other things, (i) MDC completed a series of transactions pursuant to which it emerged as a wholly owned subsidiary of the Company, converted into a Delaware limited liability company and changed its name to Midas OpCo Holdings LLC (“OpCo”) which was subsequently renamed Stagwell Global LLC; (ii) Stagwell Media contributed the equity interests of Stagwell Marketing and its direct and indirect subsidiaries to OpCo; and (iii) the Company converted into a Delaware corporation, succeeded MDC as the publicly-traded company and changed its name to Stagwell Inc.

The Transactions were treated as a reverse acquisition for financial reporting purposes, with MDC treated as the legal acquirer and Stagwell Marketing treated as the accounting acquirer. As a result of the Transactions and the change in our business and operations, under applicable accounting principles, the historical financial results of Stagwell Marketing prior to August 2, 2021 are considered our historical financial results. Accordingly, historical information presented in this Annual Report on Form 10-K (this “Form 10-K”) for events occurring or periods ending before August 2, 2021 does not reflect the impact of the Transactions or the financial results of MDC and may not be comparable with historical information for events occurring or periods ending on or after August 2, 2021.

References in this Form 10-K to “Stagwell,” “we,” “us,” “our” and the “Company” refer (i) with respect to events occurring or periods ending before August 2, 2021, to Stagwell Marketing and its direct and indirect subsidiaries and (ii) with respect to events occurring or periods ending on or after August 2, 2021, to Stagwell Inc. and its direct and indirect subsidiaries.

All dollar amounts are stated in U.S. dollars unless otherwise stated.

Forward-Looking Statements

This document contains forward-looking statements. within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). The Company’s representatives may also make forward-looking statements orally or in writing from time to time. Statements in this document that are not historical facts, including, statements about the Company’s beliefs and expectations, future financial performance, growth, and future prospects, the Company’s strategy, business and economic trends and growth, technological leadership and differentiation, potential acquisitions, anticipated operating efficiencies and synergies and estimates of amounts for redeemable noncontrolling interests and deferred acquisition consideration, constitute forward-looking statements. Forward-looking statements, which are generally denoted by words such as “aim,” “anticipate,” “assume,” “believe,” “continue,” “could,” “create,” “estimate,” “expect,” “focus,” “forecast,” “foresee,” “future,” “goal,” “guidance,” “in development,” “intend,” “likely,” “look,” “maintain,” “may,” “ongoing,” “opportunity,” “outlook,” “plan,” “possible,” “potential,” “predict,” “project,” “should,” “target,” “will,” “would” or the negative of such terms or other variations thereof and terms of similar substance used in connection with any discussion of current plans, estimates and projections are subject to change based on a number of factors, including those outlined in this section.

Forward-looking statements in this document are based on certain key expectations and assumptions made by the Company. Although the management of the Company believes that the expectations and assumptions on which such forward-looking statements are based are reasonable, undue reliance should not be placed on the forward-looking statements because the Company can give no assurance that they will prove to be correct. The material assumptions upon which such forward-looking statements are based include, among others, assumptions with respect to general business, economic and market conditions, the competitive environment, anticipated and unanticipated tax consequences and anticipated and unanticipated costs. These forward-looking statements are based on current plans, estimates and projections, and are subject to change based on a number of factors, including those outlined in this section. These forward-looking statements are subject to various risks and uncertainties, many of which are outside the Company’s control. Therefore, you should not place undue reliance on such statements. Forward-looking statements speak only as of the date they are made, and the Company undertakes no obligation to update publicly any of them in light of new information or future events, if any.

Forward-looking statements involve inherent risks and uncertainties. A number of important factors could cause actual results to differ materially from those contained in any forward-looking statements. Such risk factors include, but are not limited to, the following:

•risks associated with international, national and regional unfavorable economic conditions that could affect the Company or its clients;

•demand for the Company’s services, which may precipitate or exacerbate other risks and uncertainties;

•inflation and actions taken by central banks to counter inflation;

•the Company’s ability to attract new clients and retain existing clients;

•the impact of a reduction in client spending and changes in client advertising, marketing and corporate communications requirements;

•financial failure of the Company’s clients;

•the Company’s ability to retain and attract key employees;

•the Company’s ability to compete in the markets in which it operates;

•the Company’s ability to achieve its cost saving initiatives;

•the Company’s implementation of strategic initiatives;

•the Company’s ability to remain in compliance with its debt agreements and the Company’s ability to finance its contingent payment obligations when due and payable, including but not limited to those relating to redeemable noncontrolling interests and deferred acquisition consideration;

•the Company’s ability to manage its growth effectively, including the successful completion and integration of acquisitions that complement and expand the Company’s business capabilities;

•the Company’s ability to develop products incorporating new technologies, including augmented reality, artificial intelligence, and virtual reality, and realize benefits from such products;

•the Company’s use of artificial intelligence, including generative artificial intelligence

•adverse tax consequences for the Company, its operations and its stockholders, that may differ from the expectations of the Company, including that future changes in tax laws, potential increases to corporate tax rates in the United States and disagreements with tax authorities on the Company’s determinations that may result in increased tax costs;

•adverse tax consequences in connection with the Transactions, including the incurrence of material Canadian federal income tax (including material “emigration tax”);

•the Company’s unremediated material weaknesses in internal control over financial reporting and its ability to establish and maintain an effective system of internal control over financial reporting; including the risk that the Company’s internal controls will fail to detect misstatements in its financial statements;

•the Company’s ability to accurately forecast its future financial performance and provide accurate guidance;

•the Company’s ability to protect client data from security incidents or cyberattacks;

•economic disruptions resulting from war and other geopolitical tensions (such as the ongoing military conflicts between Russia and Ukraine and in Israel and Gaza), terrorist activities and natural disasters;

•stock price volatility; and

•foreign currency fluctuations.

Investors should carefully consider these risk factors, the additional risk factors outlined under the caption “Risk Factors” in this Form 10-K, and in the Company’s other filings with the Securities and Exchange Commission (the “SEC”) which are accessible on the SEC’s website at www.sec.gov.

SUPPLEMENTARY FINANCIAL INFORMATION

The Company reports its financial results in accordance with accounting principles generally accepted in the United States (“GAAP”). However, the Company has included certain non-GAAP financial measures and ratios, which it believes, provide useful information to both management and readers of this report in measuring the financial performance and financial condition of the Company. These measures do not have a standardized meaning prescribed by GAAP and, therefore, may not be comparable to similarly titled measures presented by other publicly traded companies, nor should they be construed as an alternative to other titled measures determined in accordance with GAAP.

PART I

Item 1. Business

About Us

Stagwell Inc. is the challenger network built to transform marketing. Stagwell delivers scaled creative performance for some of the world’s most ambitious brands, connecting creativity with leading-edge technology to harmonize the art and science of marketing. Led by entrepreneurs, we employ approximately 13,000 people, including contractors, in over 34 countries across the globe who drive effectiveness and improve business results for our more than 4,000 blue-chip customers as of December 31, 2023. In addition, as of December 31, 2023, our Global Affiliate Network added coverage in over 30 additional countries.

Stagwell offers the capabilities marketers need in the digital age: Digital Transformation, Performance Media & Data, Consumer Insights & Strategy, Creativity & Communications, and “software as a service” (“SaaS”) and “data as a

service” (“DaaS”) technology tools within the Stagwell Marketing Cloud Group. Our global scale allows us to compete for many of the largest marketing contracts available, including multi-regional contracts with annual fees of more than $10 million. Stagwell operates in a highly competitive and fragmented industry, but we believe we have a distinct advantage given our digital composition and its alignment with the broader marketplace. Additionally, the Stagwell Marketing Cloud, our proprietary suite of SaaS and DaaS technology solutions is designed for modern marketers and includes applications across the marketing value chain—research and insights, communications technology, media studios and advanced media platforms (including augmented reality (“AR”). Stagwell provides a suite of marketing services that serve marketers’ needs as well as self-service technology-driven solutions for in-house marketers. Through the Stagwell Marketing Cloud, Stagwell is investing in the frontiers of marketing, with technology products that fuel artificial intelligence (“AI”) for content creation, “instant” market research, and for communications professionals and AR experiences for stadium goers and live events. This is a key part of the future strategy for the company.

Stagwell has grown through a combination of organic growth and investment. Beginning with a single company in 2015, Stagwell focused on the fastest-growing area of marketing: digital services. Between 2015 and 2021, we acquired companies including digital transformation and digital media groups like Code and Theory and ForwardPMX. In 2019, Stagwell Media made a $100 million investment into MDC, the parent company of creative powerhouses including 72andSunny, Anomaly, Crispin, Porter & Bogusky, Doner and Forsman & Bodenfors. Recognizing the potential of those companies, Stagwell’s reorganization and careful management of the portfolio turned MDC around. In August 2021, Stagwell Media completed the Transactions with MDC to become Stagwell Inc.

Stagwell’s unified corporate team is the foundation of a powerful value creation platform focused on scaling our portfolio of marketing services firms, which we refer to as “Brands,” and driving continual network evolution. We plan to continue investing in our core digital platforms, developing our suite of digital products in the Stagwell Marketing Cloud, increasing our technology leadership through investment and innovation, and further expanding our international footprint both organically and via our Global Affiliate Network to deliver value for our clients, employees, and shareholders.

Our Market

Industry Trends

The digital revolution has changed where and how brands relate to consumers and created an entirely new, highly complex content and commerce ecosystem. Historically, marketing was characterized by television and brand advertising targeted to broad audiences: everyone saw the same advertisement at the same time. Over the last two decades, digital innovation has created new, personalized ways to reach targeted consumers and spurred a fundamental shift in the marketing services landscape. Growth now comes primarily from digital marketing, helping brands meet customers across the entire online ecosystem. We believe every company today at its core is a digital marketing company.

We believe five key trends describe the industry today:

First, online advertising now accounts for more than half of global advertising spend, and two-thirds of spend in the United States alone, with the shift further accelerating as new media channels like connected television and platforms diversify the digital channels dominating content and commerce. Online now means virtually everywhere: website, mobile, social media, television, out-of-home, and immersive in-person experiences.

Second, advertising is commerce. Digital platforms provide ways for brands to reach consumers directly through e-commerce. Platforms as diverse as TikTok, Instacart, and LinkedIn have created new ways for brands to interact with their customers. Brands can sell their products directly on their sites, via digital platforms such as Amazon or through interactive experiences enabled by social media. Digital platforms also allow advocacy groups and political campaigns to reach constituents to mobilize support or raise funds online. Retail media networks add complexity and opportunity to brands’ consumer engagement strategies.

Third, data is everywhere. Platform and channel growth has created an explosion of addressable data that can be used to better understand consumer desires, habits, and needs in real-time, allowing the delivery of content that consumers want, when they want it, and where they want it. Sources of online data include web, mobile, email, social, and connected TV – in addition to emerging products, apps and wearables that enhance day-to-day experiences. The emergence of vast amounts of data spans behavioral, transactional, demographic, psychographic and geographic categories. As connectivity grows, the value of raw data declines – but we believe the ability to derive actionable insights from the data, as Stagwell businesses do, increases.

Fourth, frontier technologies such as AI and AR are gaining critical foothold among mass consumers, reshaping how businesses connect. Both technologies have evolved past initial niche or enterprise use cases and are now reaching lay consumers, and businesses now are investing in making them widely accessible to consumer audiences, as seen with generative AI tools like ChatGPT and AR tools like Stagwell Marketing Cloud’s ARound. Stagwell is at the forefront of innovating with this technology, implementing these innovations across our client work, and incubating original and proprietary technology to drive business results and sits on what we refer to as the next frontier of marketing. As AI in particular drives cross-sector transformation, we are delivering solutions around the “Three Es” of AI: enablement across operations, efficiency in marketing, and engagement with consumers.

Finally, marketing technology is transforming the industry. SaaS and DaaS products are increasing the efficiency of marketing campaigns and in-house marketing operations, utilizing cutting edge technologies such as AI and automated media modeling, scaled consumer insights, campaign and asset management, brand reputation tracking, and more.

Competitive Landscape

Stagwell operates in a highly competitive and fragmented industry. Stagwell’s Brands compete for business and talent with the operating subsidiaries of large global holding companies such as Omnicom Group Inc., Interpublic Group of Companies, Inc., WPP plc, Publicis Groupe SA, Dentsu Inc. and Havas SA, as well as with numerous independent agencies that operate in multiple markets. Our Brands also face competition from consultancies, like Accenture and Deloitte, tech platforms, media companies and other services firms that offer related services. Stagwell’s Brands must compete with these other companies to maintain and grow existing client relationships and to obtain new clients and assignments. Individual products within the Stagwell Marketing Cloud also typically compete with offerings that may be provided within broader service offerings at large global holding companies or provided on a standalone basis by technology startups or other industry participants such as Infosys, Wipro and Cognizant.

During the decades when marketing was dominated by television, the marketing services industry experienced significant consolidation as legacy advertising holding companies built substantial portfolios of often overlapping creative, communications, PR, and media businesses to achieve financial efficiencies by centralizing administrative operations. These holding companies grew significantly in size and market share.

The rapid rise of digital channels, convergence of advertising and commerce, explosion in addressable data and marketing technology created a paradigm shift in the industry. While legacy models still accounted for a significant share of the market in 2022, we believe they are largely underexposed to the digital areas of the market experiencing the highest levels of client demand growth. In recent years, a number of large consulting firms with information technology implementation backgrounds have entered the marketing services market and, collectively, achieved significant market share. However, we believe these firms’ lack of creative and media expertise limits their long-term growth potential as true challengers to the legacy marketing holding companies.

With a combination of talent and technology, we believe that Stagwell is well positioned to take advantage of the continued transformation sweeping the marketing ecosystem and to disrupt the marketing services landscape. Stagwell was born digital and now has a global network of entrepreneurial companies that deliver the right combination of creativity and technology for the modern, digital marketer through a model that emphasizes flexibility and integration. In addition, as AI drives transformation across marketing sectors, we believe our additional focus on AI-enabled product development in the Stagwell Marketing Cloud sets us apart.

Our Offering

Principal Capabilities

Stagwell’s Brands provide differentiated, digital-first marketing and related services to a diverse client base across many industries.

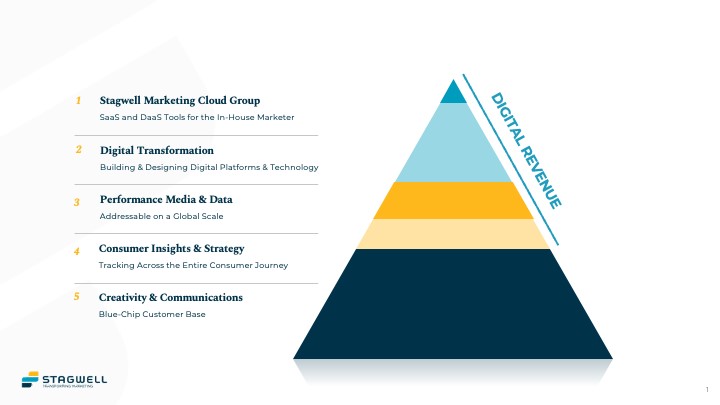

Our principal capabilities fall into five categories: 1) Stagwell Marketing Cloud Group 2) Digital Transformation 3) Performance Media & Data 4) Consumer Insights & Strategy and 5) Creativity & Communications. Taken together, these capabilities provide an integrated suite of marketing services for our blue-chip customer base.

Digital Transformation. We build digital services and products for clients. We design and build digital platforms and experiences that support the delivery of content, commerce, services and sales. We create websites, mobile applications, back-end systems, content and data management systems, and other digital environments enabling clients to engage with consumers across the digital ecosystem. We steer significant digital transformations for businesses, blending data, analytics & research and organizational consulting to drive impact with technology. We design and implement technology and data strategies to support digital services needed for our clients. We also implement technology and strategies for utilizing digital channels to mobilize and raise funds from proponents and constituents to support political candidates, non-profit groups and issue organizations in the public arena. As businesses across every sector are likely to grapple with the impact of AI, we implement AI to enable stronger operations for our clients, more efficient marketing, and new engagement methods with consumers.

Performance Media & Data. We develop omnichannel media strategies and provide coordinated execution for the placement of advertisements across the media funnel including digital channels, performance marketing and analog placements globally. Unlike legacy holding companies that own large amounts of television inventory and therefore must sell it, we take a media-agnostic approach leveraging digital technologies and media in addition to analog advertising. Our media services include media solutions such as audience analysis, and media buying and planning, ranging across the platforms a modern marketer needs to engage consumers.

Consumer Insights & Strategy. We perform large-scale online surveys, specialized research, and data analytics across the consumer journey to provide strategic insights and guidance that informs business content, product, communications and media strategies for many of the world’s largest companies, including numerous Fortune 100 clients. We have differentiated specialization in brand and corporate reputation tracking, theatrical and streaming content and strategy, and technology product design and marketing, and we believe our Brands are at the forefront of innovation in the field.

Creativity & Communications. We develop holistic, creativity-based content strategies and campaigns from concept to execution through to optimization. These services include strategy development, advertising creation, live events, immersive digital experiences, cross platform engagement, and social media content. We also provide strategic communications, public relations and public affairs services including media relations, thought leadership, investor and financial relations, social media, executive positioning and visibility.

Stagwell Marketing Cloud Group. We develop proprietary, in-house software and related technology products, including AI-enabled communications, research, and media technology, cookie-less data platforms for advanced targeting and activation, software tools for e-commerce applications, specialty media solutions in the fast-growing augmented reality space, and innovative applications of text-messaging for consumer engagement, which we license to clients using subscription-based SaaS and DaaS models.

We group our Brands into these principal capability categories based on the source of most of their revenue. We also classify Digital Transformation, Performance Media & Data, Consumer Insights & Strategy, and Stagwell Marketing Cloud Group as “Digital” though Brands categorized as Creativity & Communications generate a significant portion of revenue from creativity and content delivered on digital channels and some, such as 72andSunny and Anomaly, do meaningful amounts of digital work that fluctuates as a percentage of revenue. We believe our concentration of digital capabilities today provides a competitive advantage in the marketplace and positions us to benefit from continued digital disruption in the marketing services industry. We plan to continue to invest in our core digital platforms as well as emerging technologies to effectively support marketing transformation for our clients.

Network Structure & Reportable Segments

Stagwell maintains a 100% ownership position in substantially all of its Brands, and the remainder are majority owned with management of the Brands owning the remaining equity. Stagwell generally has rights to increase ownership of non-wholly owned subsidiaries to 100% over a defined period of time.

The Company organizes its Brands into three reportable segments: “Integrated Agencies Network,” “Brand Performance Network” and the “Communications Network.” In addition, the Company combines and discloses operating segments that do not meet the aggregation criteria as “All Other.” The Company also reports corporate expenses, as further detailed below, as “Corporate.”

The reportable segments are:

•The Integrated Agencies Network includes five operating segments: the Anomaly Alliance, Constellation, the Doner Partner Network, Code and Theory, and National Research Group. The operating segments offer an array of complementary services spanning our core capabilities of Digital Transformation, Performance Media & Data, Consumer Insights & Strategy, and Creativity & Communications. The Brands included in the operating segments that comprise the Integrated Agencies Network reportable segment are as follows: Anomaly Alliance (Anomaly), Constellation (72andSunny, Colle McVoy, Hunter, Instrument, Redscout, Team Enterprises, Harris Insights, Left Field Labs, and Movers and Shakers), the Doner Partner Network (Doner, KWT Global, Harris X, Veritas, Doner North, and Yamamoto (Brands)), Code and Theory, and National Research Group. ConcentricLife, which was part of Anomaly Alliance was sold on October 31, 2023.

These operating segments share similar characteristics related to (i) the nature of their services; (ii) the type of clients and the methods used to provide services; and (iii) the extent to which they may be impacted by global economic and geopolitical risks. In addition, these operating segments may occasionally compete with each other for new business or have business move between them.

•The Brand Performance Network (“BPN”) is comprised of a single operating segment. BPN includes a unified media and data management structure with omnichannel media placement, creative media consulting, influencer and business-to-business marketing capabilities. Our Brands in this segment aim to provide scaled creative performance through developing and executing sophisticated omnichannel campaign strategies leveraging significant amounts of consumer data. BPN’s Brands provide media solutions such as audience analysis, media planning, and buying across a range of digital and traditional platforms (out-of-home, paid search, social media, lead generation, programmatic, television, broadcast, among others) and includes multichannel Brands Assembly, Brand New Galaxy, Crispin Porter Bogusky, Forsman & Bodenfors, Goodstuff, Bruce Mau, digital creative & transformation consultancy Gale, B2B specialist Multiview, CX specialists Kenna, and travel media experts Ink.

•The Communications Network reportable segment is comprised of a single operating segment, our specialist network that provides advocacy, strategic corporate communications, investor relations, public relations, online fundraising and other services to both corporations and political and advocacy organizations and consists of our Allison brands, SKDK brands, and Targeted Victory brands.

•All Other consists of the Company’s digital innovation group and Stagwell Marketing Cloud Group, including Maru and Epicenter, and products such as ARound, PRophet and SmartAssets.

•Corporate consists of corporate office expenses incurred in connection with the strategic resources provided to the operating segments, as well as certain other centrally managed expenses that are not fully allocated to the operating segments. These office and general expenses include (i) salaries and related expenses for corporate office employees, including employees dedicated to supporting the operating segments, (ii) occupancy expenses relating to properties occupied by all corporate office employees, (iii) other office and general expenses including professional fees for the financial statement audits and other public company costs, and (iv) certain other professional fees managed by the corporate office. Additional expenses managed by the corporate office that are directly related to the operating segments are allocated to the appropriate reportable segment and the All Other category.

Go-To-Market Strategy

Our global go-to-market strategy is key to our objective of providing our clients with a balanced combination of leading-edge technology and creative talent. We go to market in four main ways: as individual Brands, as networks where collaboration across services is needed, as Stagwell Global when we create multi-region, Stagwell-wide teams, and as the Stagwell Marketing Cloud, which delivers SaaS and DaaS products for in-house marketers.

Unlike legacy holding companies who have focused on achieving cost synergies by consolidating brands within their networks, Stagwell focuses on collaboration. We believe it is important for our Brands to maintain their individual identities to attract the highest quality talent within their capabilities of expertise. Maintaining strong brand identities within our integrated Brands and specialist networks provides a structure supporting both individual and joint go-to-market approaches. Maintaining separate Brands with flexibility to integrate also enables effective management of potential conflicts of interest. Go-to-market collaboration typically occurs on larger engagements requiring services across multiple capabilities or geographies.

To further support collaboration, Stagwell provides financial incentives for Brands to collaborate with one another through referrals and the sharing of both services and expertise. Network and Brand leaders have components of incentive compensation that are based on Stagwell’s overall performance and the overall performance of their integrated or specialist networks to incentivize go-to-market collaboration.

In addition to our owned Brands, we maintain a network of go-to-market alliances with like-minded independent brands, tech companies and marketing services firms in key markets around the world. These partners, which we refer to as Global Affiliates, enable us to increase our local-market reach and qualify for business opportunities that require enhanced capabilities in specific local markets without taking on additional costs. As of December 31, 2023, the Global Affiliate Network included more than 80 affiliates.

Our distinct Brand structure enables us to work with multiple clients within the same business sector, and many of our largest clients are served by multiple Brands within our portfolio. The Brands’ work is supported by a centralized marketing and new business team that fosters collaboration, sources new business opportunities and communicates across industries to drive awareness of our offerings. Additionally, a centralized corporate innovation team develops and invests in proprietary digital marketing products that are distributed by Brands across the network, further enhancing the value proposition Stagwell’s Brands offer to clients.

Our Strategy

The key components of the Stagwell strategy are Digital, Integrated, Global, and Strategic (“DIGS”). We believe the DIGS model gives us a sustainable, long-term path to significant growth and supports our primary objectives which are achieving strong levels of organic growth, increasing our digital revenue mix, increasing international scale, expanding the average client relationship size, and improving strong margins and free cash flow. We believe pursuing these objectives will increase value for our shareholders.

Our strategy is focused on six specific initiatives: 1) Investing in Digital Capabilities, 2) Expanding Addressable Markets, 3) Effective Integration at Scale, 4) Strategic Value Creation Platform, 5) Maintaining a Highly Variable Cost Structure, and 6) Efficient Capital Allocation.

Investing in Digital Capabilities

Our digital businesses serve the areas where we expect the fastest growth in the marketing space and position us to lead the wave of transformation in the industry. By investing in our core digital platforms and introducing proprietary SaaS and DaaS marketing technology (“martech”) products, we aim to increase the digital proportion of our net revenue. We aim to expand our digital capabilities in three main ways:

•First, we intend to continue to invest in our leading digital Brands like Code and Theory, Instrument and Left Field Labs. This planned investment includes funding new capabilities and supporting cross-selling via our Integrated Agencies Network, which has already created additional opportunities. We intend to invest in these Brands’ emerging technologies, including AI solutions, to remain at the forefront of the transformation of marketing services.

•Second, we intend to pursue complementary acquisition opportunities to bolster our existing assets in areas such as digital transformation and digital media buying. We have built a successful track record of “bolt-on” acquisitions such as TrueLogic Software, LLC, Ramenu S.A., Polar Bear Development S.R.L., a Latin America engineering shop, and Kettle Solutions, LLC (“Kettle”), a content and digital design firm.

•Third, we intend to continue to invest in the Stagwell Marketing Cloud, a suite of technology products in development or early-stage commercialization. These include AI-enabled solutions in communications technology, research and insights, media, and advanced media solutions. These products are licensed to our clients using subscription-based

SaaS and DaaS models and distributed by Brands across our network. We believe the Stagwell Marketing Cloud positions us to serve in-house marketing departments and create recurring, high-value revenue streams in the future. We have also made strategic acquisitions for the Stagwell Marketing Cloud, including The People Platform (formerly Epicenter Experience), an enterprise software company that leverages mobile and location data to map and sequence complex consumer behavior patterns, and Maru Group, a leading software experience and insights data platform.

Expanding Addressable Markets

We are focused on expanding our addressable markets through investments that increase our global footprint as well as adding emerging marketing technologies in areas expected to have strong secular growth. We believe increasing our geographic presence and breadth of capabilities will allow us to significantly grow our average client relationship size over time.

•International Markets: Our strategy for growing our international operations is focused on expanding our media buying, content creation and digital capabilities in new markets, which will improve our qualifications for large multi-regional contracts with the largest global marketers. For example, in April 2022, we acquired Brand New Galaxy, a scaled provider of end-to-end e-commerce services such as DTC strategy, digital content production, automation, and complex technology implementations. The acquisition bolsters Stagwell’s broad e-commerce capabilities to service more global clients and provides significant scale in Europe. Further, in April 2023, we acquired In the Company of Huskies, a Dublin-based creative shop with services such as creative and brand marketing, strategy, and insights, which functionally expanded Stagwell’s footprint to Ireland under the Forsman & Bodenfors brand.

•We maintain a Global Affiliate network that enables us to deliver creative, performance, media and technology capabilities at the scale required to serve the world’s largest marketers. Our affiliates provide local talent and insights for regional engagements without requiring investment capital. We believe our Global Affiliates will be a valuable source for acquisitions, allowing Stagwell to vet companies before formal investment. Brand New Galaxy was our first affiliate and affiliate acquisition. As of December 31, 2023, we had over 80 Global Affiliate partners in our network.

•Emerging Marketing Technologies: In addition to the advertising and marketing services market, we believe our investments in the Stagwell Marketing Cloud will position us to address new, rapidly expanding market opportunities, including marketing data, campaign martech, the metaverse, and AR and VR applications. For example, Stagwell’s AI-enabled instant research tool Harris Quest is now operating in over a dozen countries, and signed its 150th client in 2023, and Stagwell’s shared AR product ARound has launched stadium-level experiences with professional sporting teams in Major League Baseball and the National Football League, namely the Minnesota Twins and the Los Angeles Rams. We expect to expand app integrations for ARound further in 2024.

Effective Integration at Scale