EXHIBIT 99.2

BLOOMIA B.V. AND SUBSIDIARIES

CONSOLIDATED FINANCIAL STATEMENTS

Years ended June 30, 2023 and 2022

| 1 |

Index to the Consolidated Financial Statements

| Pages |

| ||

|

| 3 |

| |

|

|

|

|

|

| 5 |

| ||

|

|

|

|

|

| Consolidated Statements of Operations and Comprehensive Income |

| 6 |

|

|

|

|

|

|

| 7 |

| ||

|

|

|

|

|

| 8 |

| ||

|

|

|

|

|

|

| 9-23 |

|

| 2 |

| Table of Contents |

To the Stockholders

Bloomia B.V. and Subsidiaries

Opinion

We have audited the accompanying consolidated financial statements of Bloomia B.V. and Subsidiaries (the Company), which comprise the consolidated balance sheets as of June 30, 2023 and 2022, and the related consolidated statements of operations and comprehensive income, changes in shareholders' equity and cash flows for the years then ended, and the related notes to the consolidated financial statements.

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of Bloomia B.V. and Subsidiaries as of June 30, 2023 and 2022, and the results of its operations and its cash flows for the years then ended in accordance with accounting principles generally accepted in the United States of America.

Basis for Opinion

We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Our responsibilities under those standards are further described in the Auditor's Responsibilities for the Audit of the Consolidated Financial Statements section of our report. We are required to be independent of Bloomia B.V. and Subsidiaries and to meet our other ethical responsibilities in accordance with the relevant ethical requirements relating to our audit. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Responsibilities of Management for the Consolidated Financial Statements

Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with accounting principles generally accepted in the United States of America and for the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the consolidated financial statements, management is required to evaluate whether there are conditions or events, considered in the aggregate, that raise substantial doubt about Bloomia B.V. and Subsidiaries’ ability to continue as a going concern within one year after the date that the consolidated financial statements are available to be issued.

Auditor's Responsibilities for the Audit of the Consolidated Financial Statements

Our objectives are to obtain reasonable assurance about whether the consolidated financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor's report that includes our opinion. Reasonable assurance is a high level of assurance but is not absolute assurance and therefore is not a guarantee that an audit conducted in accordance with generally accepted auditing standards will always detect a material misstatement when it exists. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control. Misstatements are considered material if there is a substantial likelihood that, individually or in aggregate, they would influence the judgment made by a reasonable user based on the consolidated financial statements.

| 3 |

| Table of Contents |

In performing an audit in accordance with generally accepted auditing standards, we:

|

| · | Exercise professional judgment and maintain professional skepticism throughout the audits. |

|

| · | Identify and assess the risks of material misstatement of the consolidated financial statements, whether due to fraud or error, and design and perform audit procedures responsive to those risks. Such procedures include examining, on a test basis, evidence regarding the amounts and disclosures in the consolidated financial statements. |

|

| · | Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control. Accordingly, no such opinion is expressed. |

|

| · | Evaluate the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluate the overall presentation of the consolidated financial statements. |

|

| · | Conclude whether, in our judgment, there are conditions or events, considered in the aggregate, that raise substantial doubt about the Company’s ability to continue as a going concern for a reasonable period of time. |

We are required to communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit, significant audit findings, and certain internal control related matters that we identified during the audits.

/s/Boulay PLLP

We have served as the Company’s auditor since 2023.

Minneapolis, Minnesota

May 17, 2024

| 4 |

| Table of Contents |

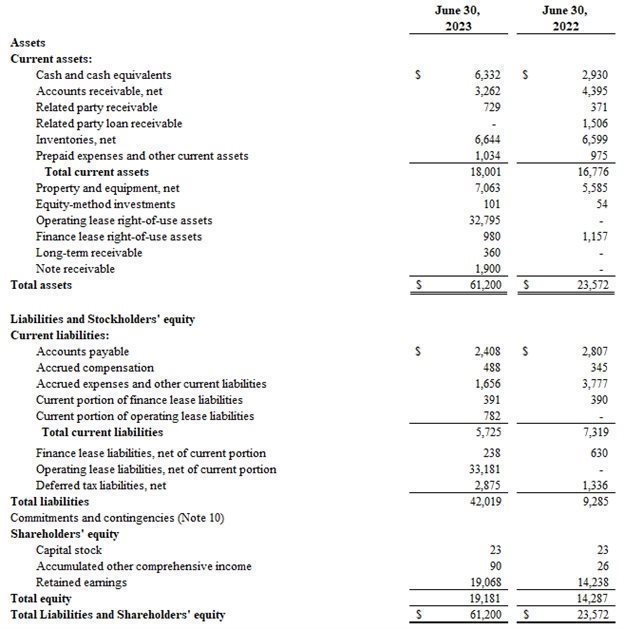

Consolidated Balance Sheets

(Amounts in thousands of U.S. dollars)

The accompanying notes are an integral part of these consolidated financial statements.

| 5 |

| Table of Contents |

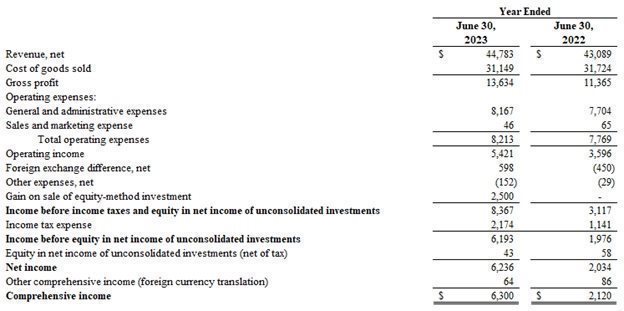

Consolidated Statements of Operations and Comprehensive Income

(Amounts in thousands of U.S. dollars)

The accompanying notes are an integral part of these consolidated financial statements.

| 6 |

| Table of Contents |

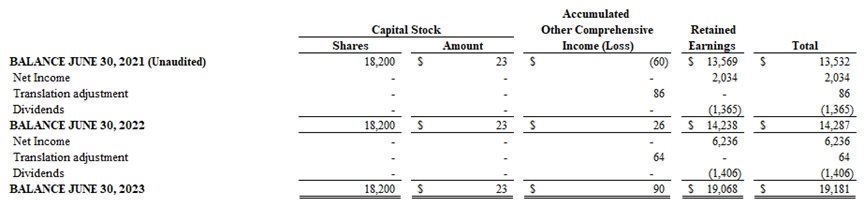

Consolidated Statements of Changes in Shareholders’ Equity

(Amounts in thousands of U.S. dollars, except share data)

The accompanying notes are an integral part of these consolidated financial statements.

| 7 |

| Table of Contents |

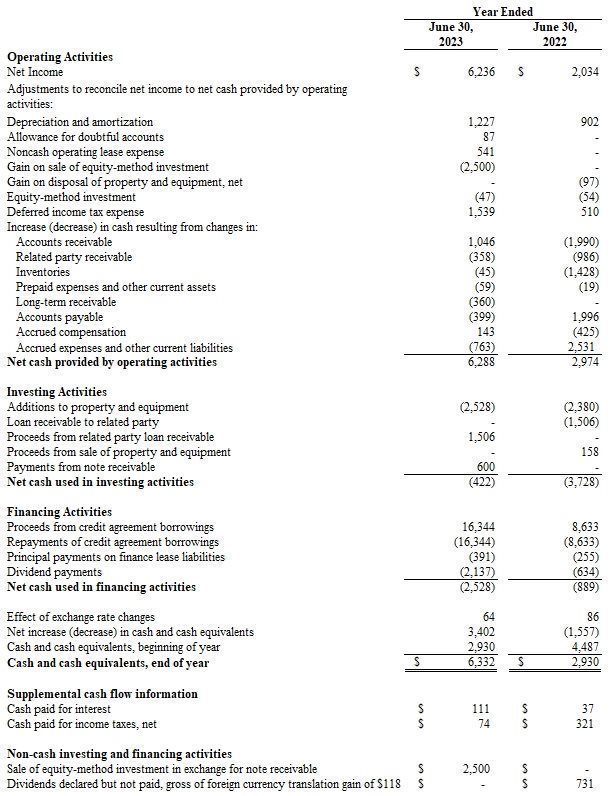

Consolidated Statements of Cash Flow

(Amounts in thousands of U.S. dollars)

The accompanying notes are an integral part of these consolidated financial statements.

| 8 |

| Table of Contents |

Notes to Consolidated Financial Statements

(U.S Dollars in thousands)

Note 1 — Organization and Business Operations

Bloomia B.V (“Bloomia”) is a limited liability company incorporated under the laws of the Netherlands. Bloomia is one of the largest producers of fresh cut tulips in the United States of America (“USA”), nurturing over 75 million stems annually. Operations are primarily in the USA with a presence in the Netherlands and South Africa. Bloomia purchases tulip bulbs, hydroponically grows tulips from the bulbs, and sells the stems to retail stores.

At June 30, 2023, Bloomia had two wholly owned subsidiaries, Bloomia PTY Ltd and Fresh Tulips USA, LLC (“Fresh Tulips”) and a 30% ownership stake in Bloomia Araucania Flowers SA (“Araucania”), together (the “Company”).

Note 2 — Summary of Significant Accounting Policies

Basis of Presentation

The accompanying consolidated financial statements have been prepared in accordance with generally accepted accounting principles in the Unites States of America (“U.S. GAAP”) and includes the accounts of the Company and its wholly owned subsidiaries. Entities for which the Company owns an interest, but does not consolidate, are accounted for under the equity method and are included in equity-method investments within the consolidated balance sheets. All intercompany transactions and accounts have been eliminated in consolidation.

On February 22, 2024, the Company was acquired by Tulp 24.1 LLC, a subsidiary of Lendway, Inc. (“Lendway”).

Use of Estimates

The preparation of consolidated financial statements in conformity with U.S. GAAP requires management to make certain estimates and assumptions that affect the reported amounts and disclosures of assets and liabilities at the date of the consolidated financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. Significant estimates include the assumptions used in the measurement of right-of-use assets and liabilities and estimated lives of depreciable and amortizable assets.

Foreign Currency Transactions

Transactions and balances that are denominated in currencies that differ from the functional currencies have been remeasured into US dollars in accordance with principles set forth in ASC 830, Foreign Currency Matters. At each balance sheet date, monetary items denominated in foreign currencies are translated at exchange rates in effect at the balance sheet date, while income and expenses are translated at average exchange rates for the periods presented. All exchange gains and losses from the remeasurement mentioned above are reflected in the consolidated statement of operations as foreign exchange expenses or income, as appropriate.

The revenues of the Company and most of its subsidiaries are generated in US dollars. In addition, most of the costs of the Company and most of its subsidiaries are incurred in US dollars. The Company’s management has established that the US dollar is the primary currency of the economic environment in which the Company and most of its subsidiaries operate. Thus, the functional currency of the Company and most of its subsidiaries is the US dollar.

For subsidiaries whose functional currency has been determined to be other than the US dollar, assets and liabilities are translated at year-end exchange rates, the consolidated statement of operations items are translated at average exchange rates prevailing during the year, and equity is translated at blended historical rates. Resulting translation differences are recorded as a separate component of accumulated other comprehensive income (loss) in equity.

| 9 |

| Table of Contents |

Cash and Cash Equivalents

The Company considers all highly liquid investments with a maturity of three months or less at the time of purchase to be cash equivalents. Cash and cash equivalents consist of demand deposits with banks and negotiable order of withdrawal accounts.

Accounts Receivable, net

Accounts receivable are presented in the balance sheets at their outstanding balances net of the allowance for doubtful accounts. The allowance for doubtful accounts is determined through an evaluation of the aging of the Company’s accounts receivable balances, and considers such factors as the customer’s creditworthiness, the customer’s payment history and current economic conditions. Bad debt written-off and any recovery of bad debt write-off is applied to the allowance for doubtful accounts. At June 30, 2023 and 2022, the Company had an allowance for doubtful accounts of $60 and $12, respectively.

Inventories

Raw materials consist primarily of tulip bulbs, including freight, and packaging supplies. Work-in-process consists of tulip stems and bulbs that have rooted. Inventories are stated at the lower of cost, as determined on the first-in, first-out method, or net realizable value. Finished goods and work-in-process include the inventory costs of raw materials, direct labor and normal manufacturing overhead. Abnormal amounts of spoilage are expensed as incurred and not included in overhead.

Property and Equipment, net

Property and equipment, net are stated at historical cost, less accumulated depreciation and amortization. Depreciation and amortization are computed using the straight-line method over the estimated useful lives of the assets. Bushes refer to peony plants, which accumulate planting and development costs that are capitalized into their basis until they become commercially productive, at which point the asset begins depreciating, and future maintenance costs are expensed as incurred. Planting costs consist primarily of the costs to purchase and plant nursery stock. Development costs consist of cultivation, pruning, irrigation, labor, spraying and fertilization, and interest costs during the development period. Amortization of leasehold improvements is computed using the straight-line method over the shorter of the remaining lease term (including renewals that are reasonably certain to occur) or the estimated useful lives of the improvements. The estimated useful lives of property and equipment are as follows:

| Estimated Useful life | |

| Leasehold improvements | 15 years |

| Bushes | 7-10 years |

| Machinery and equipment | 5-20 years |

| Vehicles | 5 years |

| Furniture and fixtures | 5-7 years |

Long-Lived Assets Impairment

The Company reviews long-lived assets with finite lives for impairment in accordance with ASC 360, “Property, Plant, and Equipment.” The analysis to determine whether or not an asset is impaired requires significant judgment that is dependent on internal forecasts, including estimated future cash flows, estimates of long-term growth rates for the business, and the expected life over which cash flows will be realized. Changes in these estimates and assumptions could materially affect the determination of fair value and any impairment charge. While the gross undiscounted future cash flows of these assets exceeds their carrying value based on the Company’s current estimates and assumptions, materially different estimates and assumptions in the future in response to changing economic conditions, changes in the business, increased competition or loss of market share, product innovation or obsolescence, product claims that result in a significant loss of sales or profitability over the product life or for other reasons could result in the recognition of impairment losses.

| 10 |

| Table of Contents |

For assets to be held and used, including long-lived assets subject to amortization, the Company initiates a review of each individual asset-group whenever events or changes in circumstances indicate that the carrying amount of these assets may not be recoverable. Recoverability of an asset is measured by comparison of its carrying amount, to the future undiscounted cash flows that the asset is expected to generate. Any impairment to be recognized is measured by the amount by which the carrying amount of the asset exceeds its fair value. Significant management judgment is required in this process. During the years ended June 30, 2023 and 2022, no impairment losses were identified.

Investments

Investments are accounted for using the equity method of accounting if the investment gives the Company the ability to exercise significant influence, but not control, over the investee. Under the equity method of accounting, the Company records its investments in equity-method investees in the consolidated balance sheets as equity method investments and its share of investees’ earnings or losses together with other-than-temporary impairments in value, are recorded in equity in net income of unconsolidated investments. Basis differences between the carrying amount and our ownership interest in the underlying net assets of the investee, and any gain or loss from the sale of an equity-method investment is reported as Gain on sale of equity investment in net income of unconsolidated investments in the consolidated statements of operations. The Company evaluates its equity-method investments for impairment whenever events or changes in circumstances indicate that the carrying amounts of such investments may be impaired. If a decline in the value of an equity-method investment is determined to be other than temporary, a loss is recorded in earnings in the current period.

Investments in joint ventures of immaterial entities are estimated based upon the overall performance of the entity where financial results are not available on a timely basis.

Fair Value

ASC 820, Fair Value Measurements and Disclosures, establishes a fair value hierarchy which requires an entity to maximize the use of observable inputs and minimize the use of unobservable inputs when measuring fair value. The standard describes three levels of inputs that may be used to measure fair value:

|

| · | Level 1: Quoted prices (unadjusted) for identical assets or liabilities in active markets that the entity has the ability to access as of the measurement date. |

|

|

|

|

|

| · | Level 2: Significant other observable inputs other than Level 1 prices such as quoted prices for similar assets or liabilities; quoted prices in markets that are not active; or other inputs that are observable or can be corroborated by observable market data. |

|

|

|

|

|

| · | Level 3: Significant unobservable inputs that reflect a reporting entity’s own assumptions about the assumptions that market participants would use in pricing an asset or liability. |

The carrying amounts of certain financial instruments, which include cash and cash equivalents, receivables, accounts payable, and accrued expenses approximate their fair values at June 30, 2023 and 2022 due to their short-term nature and management’s belief that their carrying amounts approximate the amount for which the assets could be sold or the liabilities could be settled. See Note 13 – Derivative Financial Instruments for the fair value of derivative financial instruments.

Revenue Recognition

The Company accounts for revenue in accordance with FASB Topic 606, “Revenue from Contracts with Customers,” (ASC 606), using the following steps:

|

| · | Identify the contract or contracts, with a customer; |

|

|

|

|

|

| · | Identify the performance obligations in the contract; |

|

|

|

|

|

| · | Determine the transaction price; |

|

|

|

|

|

| · | Allocate the transaction price to performance obligations in the contract; and |

|

|

|

|

|

| · | Recognize revenue when or as the Company satisfies a performance obligation. |

| 11 |

| Table of Contents |

Revenues from the sale of stems

The Company recognizes revenue when obligations under the terms of a contract with its customer are satisfied; this occurs with the transfer of control of its tulips. Revenue is measured as the amount of consideration expected to be received in exchange for transferring products. Revenue from product sales is governed primarily by customer pricing and related purchase orders (“contracts”) which specify shipping terms and the transaction price. Contracts are at standalone pricing. The performance obligation in these contracts is determined by each of the individual purchase orders and the respective stated quantities, with revenue being recognized at a point in time when obligations under the terms of the agreement are satisfied. This generally occurs with the transfer of control of stems to the customer when the product is delivered, with payments from customers being collected between 30-60 days following the transfer of control.

The Company expenses the incremental costs of obtaining a contract, if the amortization period is one year or less. These costs are included in sales and marketing expense on the Consolidated Statement of Operations and Other Comprehensive Income.

The Company had opening contract asset balances of $4,395 and $2,405 for the years ended June 30, 2023 and 2022, respectively.

The following table presents revenue disaggregated by customer, as determined by the operational nature of their industry:

|

|

| Year Ended |

| |||||

|

|

| June 30, |

| |||||

|

|

| 2023 |

|

| 2022 |

| ||

| Supermarket |

| $ | 42,504 |

|

| $ | 41,299 |

|

| Wholesaler |

|

| 1,738 |

|

|

| 1,111 |

|

| Other |

|

| 541 |

|

|

| 679 |

|

| Total |

| $ | 44,783 |

|

| $ | 43,089 |

|

Cost of Sales

Cost of sales consists primarily of costs to procure, sort, pick, cool and transport bulbs. Additionally, cost of sales includes labor and facility costs related to production operations.

Shipping and Handling

The Company’s shipping and handling costs include costs incurred with third-party carriers to transport products to customers. The costs of out-bound freight are included in the cost of goods sold in the Consolidated Statement of Operations and Comprehensive Income. For the years ended June 30, 2023 and 2022, the costs of out-bound freight were $3,232 and $3,298, respectively.

Advertising Costs

The Company expenses advertising costs as incurred. These costs are included within sales and marketing expenses in the Consolidated Statement of Operations and Comprehensive Income. Total advertising expense was approximately $46 and $65 for the years ended June 30, 2023 and 2022, respectively.

Income Taxes

The Company uses the liability method to account for income taxes as prescribed by ASC 740. Deferred tax assets and liabilities are determined based on the difference between the financial statement and tax bases of assets and liabilities as measured by the enacted tax rates which will be in effect when these differences reverse. Deferred tax expense (benefit) is the result of changes in deferred tax assets and liabilities. Deferred income tax assets and liabilities are adjusted to recognize the effects of changes in tax laws or enacted tax rates in the period during which they are signed into law. In determining the Company’s ability to realize its deferred tax assets, the Company considers any available tax planning strategies that could be implemented. Under ASC 740 a valuation allowance is required when it is more likely than not that all or some portion of the deferred tax assets will not be realized due to the inability to generate sufficient future taxable income of the correct character. Failure to achieve previously forecasted taxable income could affect the ultimate realization of deferred tax assets and could negatively impact the Company’s effective tax rate on future earnings.

The Company recognizes the tax benefit from an uncertain tax position only if it is more likely than not that the tax position will be sustained on examination by the taxing authorities, based on the technical merits of the position. The tax benefits recognized in the consolidated financial statements from such a position should be measured based on the largest benefit that has a greater than 50% likelihood of being realized upon ultimate settlement.

| 12 |

| Table of Contents |

Interest income or expense/penalties attributable to the overpayment or underpayment, respectively, of income taxes is recognized as an element of the Company’s provision for income taxes.

As a multinational corporation, we are subject to taxation in many jurisdictions, and the calculation of our tax liabilities involves dealing with uncertainties in the application of complex tax laws and regulations in various taxing jurisdictions. If we ultimately determine that the payment of these liabilities will be unnecessary, the liability will be reversed, and we will recognize a tax benefit during the period in which it is determined the liability no longer applies. Conversely, the Company records additional tax charges in a period in which it is determined that a recorded tax liability is less than the ultimate assessment is expected to be.

The application of tax laws and regulations is subject to legal and factual interpretation, judgment and uncertainty. Tax laws and regulations themselves are subject to change as a result of changes in fiscal policy, changes in legislation, the evolution of regulations and court rulings. Therefore, the actual liability for U.S. or foreign taxes may be materially different from management’s estimates, which could result in the need to record additional tax liabilities or potentially reverse previously recorded tax liabilities.

New Accounting Pronouncements

Recently Adopted Accounting Standards

In February 2016, the FASB issued ASU 2016-02, Leases (Topic 842), which requires the recognition of right-of-use assets and lease liabilities by lessees for certain leases classified as operating leases and also requires expanded disclosures regarding leasing activities. The Company has adopted the standard effective July 1, 2022, using the modified retrospective approach. All comparative periods prior to July 1, 2022 are not adjusted and continue to be reported in accordance with ASC 840, Leases.

The Company has elected the package of practical expedients permitted under the transition guidance within the new standard, which among other things, allows the Company to carry forward the historical lease classification and initial direct costs treatment at transition. The Company has also made an accounting policy election to exclude leases with an initial term of 12 months or less from the consolidated balance sheet. The Company will recognize those lease payments in the consolidated statements of operations and other comprehensive loss on a straight-line basis over the lease term.

Lease payments may include future escalations based on an index or other rate (such as the consumer price index), which the Company initially measures using the index or rate at lease commencement. Subsequent changes or other periodic market-rate adjustments to base rent are recorded as variable lease expense in the period incurred. Residual value guarantees or payments for terminating the lease are included in the lease liability only when it is probable they will be incurred. Lease liabilities and their corresponding right-of-use assets (“ROU”) are recorded based on the present value of lease payments over the expected lease term. The interest rate implicit in lease contracts is sometimes not readily determinable. In such cases, the Company utilizes the appropriate incremental borrowing rate, which is the rate incurred to borrow on a collateralized basis over a similar term an amount equal to the lease payments in a similar economic environment. The ROU assets are also adjusted for any initial direct costs incurred and lease payments made at or before the commencement date and are reduced by lease incentives received.

The Company’s leases may include a non-lease component representing additional services transferred to the Company, such as common area maintenance for real estate. The Company has made an accounting policy election to account for lease and non-lease components in its contracts as a single lease component for real estate asset related leases. The Company has elected to separate all lease and non-lease components for all other asset classes. The non-lease components, which are typically variable in nature, are recorded in variable lease expense in the period incurred.

The adoption of the standard resulted in recording operating lease right-of-use assets and operating lease liabilities of $33,952 and $34,579, respectively on July 1, 2022. The adoption of the new standard did not have a material impact on the Company’s consolidated statement of operations and comprehensive income or consolidated statement of cash flows.

| 13 |

| Table of Contents |

In December 2019, the FASB issued ASU 2019-12, Income Taxes (Topic 740): Simplifying the Accounting for Income Taxes, which removes certain exceptions for recognizing deferred taxes for investments, performing intraperiod allocation and calculating income taxes in interim periods. The ASU also adds guidance to reduce complexity in certain areas, including recognizing deferred taxes for tax goodwill and allocating taxes to members of a consolidated group. ASU 2019-12 is effective for the Company’s annual periods beginning after December 15, 2021. The adoption of ASU 2019-12 on July 1, 2022 did not have a material impact on the Company’s consolidated financial statements.

Recently Issued Accounting Standards Not Yet Adopted

In June 2016, the FASB issued ASU 2016-13, Measurement of Credit Losses on Financial Instruments (Topic 326). This standard requires a new method for recognizing credit losses that is referred to as the current expected credit loss (“CECL”) method. The CECL method requires the recognition of all losses expected over the life of a financial instrument upon origination or purchase of the instrument unless the Company elects to recognize such instruments at fair value with changes in profit and loss (the fair value option). This standard is effective for the Company for fiscal years beginning after December 15, 2022. The Company believes the adoption of ASC 2016-13 will not have a material impact on the Company’s consolidated financial statements.

In December 2023, the FASB issued Accounting Standards Update ASU 2023-09, Income Taxes (Topic 740)—Improvements to Income Tax Disclosures. The ASU requires that an entity disclose specific categories in the effective tax rate reconciliation as well as provide additional information for reconciling items that meet a quantitative threshold. Further, the ASU requires certain disclosures of state versus federal income tax expense and taxes paid. The amendments in this ASU are required to be adopted for fiscal years beginning after December 15, 2024. Early adoption is permitted for annual financial statements that have not yet been issued. The amendments should be applied on a prospective basis although retrospective application is permitted. The Company is currently evaluating the impact of the ASU 2023-09 adoption on its consolidated financial statements.

Note 3 — Inventories

Inventories consisted of the following:

|

|

| June 30, |

| |||||

|

|

| 2023 |

|

| 2022 |

| ||

| Finished goods |

| $ | 555 |

|

| $ | 631 |

|

| Work-in-process |

|

| 1,864 |

|

|

| 1,603 |

|

| Raw materials and packaging supplies |

|

| 4,225 |

|

|

| 4,365 |

|

| Total inventories |

| $ | 6,644 |

|

| $ | 6,599 |

|

Note 4 — Prepaid Expenses and Other Current Assets

Prepaid expenses and other current assets consisted of the following:

|

|

| June 30, |

| |||||

|

|

| 2023 |

|

| 2022 |

| ||

| Prepaid cultivation costs |

| $ | 316 |

|

| $ | 74 |

|

| Prepaid costs |

|

| 190 |

|

|

| 259 |

|

| Prepaid VAT |

|

| 112 |

|

|

| 168 |

|

| Other receivables |

|

| 416 |

|

|

| 474 |

|

| Total prepaid expenses and other current assets |

| $ | 1,034 |

|

| $ | 975 |

|

| 14 |

| Table of Contents |

Note 5 — Property and Equipment

|

|

| June 30, |

| |||||

|

|

| 2023 |

|

| 2022 |

| ||

| Machinery and equipment |

| $ | 12,243 |

|

| $ | 9,939 |

|

| Leasehold improvements |

|

| 316 |

|

|

| 316 |

|

| Bushes |

|

| 430 |

|

|

| 252 |

|

| Vehicles |

|

| 401 |

|

|

| 371 |

|

| Furniture and fixtures |

|

| 137 |

|

|

| 121 |

|

| Property and equipment, gross |

|

| 13,527 |

|

|

| 10,999 |

|

| Less: accumulated depreciation |

|

| (6,464 | ) |

|

| (5,414 | ) |

| Property and equipment, net |

| $ | 7,063 |

|

| $ | 5,585 |

|

Depreciation and amortization expense of property and equipment was $1,050 for the year ended June 30, 2023, of which $908 and $142 were recorded within cost of sales, and general and administrative expenses, respectively. Depreciation and amortization expense of property and equipment was $869 for the year ended June 30, 2022, of which $752 and $117 were recorded within cost of sales, and general and administrative expenses, respectively.

Note 6 — Equity-method Investments

The following summarizes the Company’s equity-method investments:

|

|

| June 30, 2023 |

|

| June 30, 2022 |

| ||||||||||

|

|

| Carrying Amount |

|

| Economic Interest |

|

| Carrying Amount |

|

| Economic Interest |

| ||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

| Araucanía Flowers SA |

| $ | 101 |

|

|

| 30.0 | % |

| $ | 54 |

|

|

| 30.0 | % |

| Horti-Group USA LLC |

|

| - |

|

| -% |

|

|

| - |

|

|

| 50.0 | % | |

| Total Investments |

| $ | 101 |

|

|

|

|

|

| $ | 54 |

|

|

|

|

|

At June 30, 2023 and 2022, there was not a material difference between the amount at which the Company’s equity-method investments are carried and the amount of underlying equity in the net assets of the equity-method investments, excluding equity-method investments that have had accumulated losses in excess of the equity-method investment’s carrying amount.

The following summarizes the equity in net income (loss) of unconsolidated investments (net of tax) reflected in the consolidated statements of operations (in thousands):

|

|

| Year Ended June 30, |

| |||||

|

|

| 2023 |

|

| 2022 |

| ||

| Entity |

|

|

|

|

|

| ||

| Araucanía Flowers SA |

| $ | 43 |

|

| $ | 58 |

|

| Horti-Group USA LLC |

|

| - |

|

|

| - |

|

| Total |

| $ | 43 |

|

| $ | 58 |

|

The Company owns a 30% interest in Araucanía Flowers SA (“Araucanía”), which is a closed private corporation that was incorporated and is domiciled in Pucón Chile. Araucanía serves as a marketing arm for the Company to export its crops to Latin America countries. Araucanía supplies tulips primarily to Latin America countries via wholesale and online sales. Araucanía has two other shareholders that hold 70% of its aggregate issued and outstanding shares. In 2019, the Company entered into a debt agreement with Araucanía in exchange for the cumulative balance of unpaid invoices. The debt agreement with Araucanía was for the principal amount of approximately $274 bearing interest rate at 4% per annum. The debt agreement has a repayment term of five years with monthly principal payments. In 2022, Araucanía borrowed an additional $153 from the company in exchange for unpaid invoices; resulting in the increase to the principal amount owed on the loan. As of June 30, 2023 and 2022, the loan to Araucanía had a balance of approximately $202 and $284, respectively. As of June 30, 2023 and 2022, the Company had trade receivables from Araucanía of approximately $241 and $221, respectively; for the fiscal years ended June 30, 2023 and 2022, the Company had sales to Araucanía of approximately $100 and $149, respectively.

| 15 |

| Table of Contents |

The Company owned a 100% interest in Viridus Fortuna LLC (“Viridus”). Viridus is a single member limited liability company whose sole member was Fresh Tulips. Viridus was a pass-through entity that held the Company’s 50% ownership interest in Horti-Group USA LLC (“Horti-Group”) and had no significant assets or operations of its own. Horti-Group is a limited liability company (treated as a partnership for US income taxes) whose two members were Viridus and V-Maxx LLC (“V-Maxx”) (the managing member and unrelated entity). Horti-Group operates a 45 acre facility near Washington D.C. that the Company utilizes to grow and distribute its tulips to North American customers. On July 1, 2021, Fresh Tulips entered into a lease with Horti-Group for the greenhouse facility. The initial lease term is 7.5 years commencing July 1, 2021, and terminating on December 31, 2028; Fresh Tulips has the option to extend the lease for an additional 10 years. The monthly rent expense was initially $272 and increases 2% each year. On July 1, 2022, as amended, Fresh Tulips issued a loan to Horti-Group for an amount of $1,500, bearing interest of 5.0% per annum. The purpose of the loan was to provide Horti-Group capital to invest in a container system in its greenhouses. The loan was repaid during the twelve months ended June 30, 2023 via reductions to Fresh Tulips monthly rent payable.

Pursuant to a purchase agreement on July 1, 2021, as amended on July 1, 2022, and as addended on January 1, 2023, Fresh Tulips agreed to sell, convey, and transfer to V-Maxx its membership interest in Viridus and its ownership interest in Horti-Group with the sale to be effective on March 31, 2023, or such earlier date as agreed. At such time, V-Maxx would become the sole, absolute and unconditional owner of Viridus and thus its ownership interest in Horti-Group together with any and all other rights or interests Bloomia had in Viridus. On February 9, 2023 the sale was consummated and Bloomia sold and conveyed its ownership interest in Viridus and Horti-Group to V-Maxx for a purchase price of $2,500. The purchase price was seller-financed via the issuance of an interest-free loan from Fresh Tulips to V-Maxx with an original principal amount $2,500. The loan to V-Maxx is to be repaid in 17 monthly instalments of $150 for the first 16 months and $100 for the last month, with the first payment on April 1, 2023 and the last payment on August 1, 2024. At June 30, 2023, the balance of the loan was $1,900. Due to the Company’s significant influence, but not controlling interest, in Horti-Group, the Company’s investment in Horti-Group was accounted for using the equity method. The Company recorded a gain on the sale of the equity-method investment of $2,500 on the consolidated statements of operations for the year ended June 30, 2023.

Note 7 — Accrued Expenses and Other Current Liabilities

Accrued expenses and other current liabilities consisted of the following:

|

|

| June 30, |

| |||||

|

|

| 2023 |

|

| 2022 |

| ||

| Accrued income taxes |

| $ | 1,071 |

|

| $ | 486 |

|

| Derivative liability |

|

| 11 |

|

|

| 903 |

|

| Goods received not invoiced |

|

| 205 |

|

|

| 663 |

|

| Dividend payable |

|

| - |

|

|

| 629 |

|

| Deferred rent |

|

| - |

|

|

| 627 |

|

| Accrued professional fees |

|

| 56 |

|

|

| - |

|

| Other |

|

| 313 |

|

|

| 469 |

|

| Total accrued expenses and other current liabilities |

| $ | 1,656 |

|

| $ | 3,777 |

|

| 16 |

| Table of Contents |

Note 8 — Long-term Debt

On September 6, 2023, the Company entered into a credit agreement (“2023 Credit Agreement”) with Coöperatieve Rabobank U.A. (“Rabobank”) to finance business activities. This credit agreement was executed to replace a line of credit (“2022 Credit Agreement”) from the prior year that was set to expire in August of 2023. Available borrowing limits (translated from Euros at the spot rate as of June 30, 2023) are as follows:

| - | September 23, 2023 to January 31, 2024: $ 4,987,800 |

| - | February 1, 2024 to February 29, 2024: $ 4,081,500 |

| - | March 1, 2024 to March 31, 2024: $ 3,537,300 |

| - | April 1, 2024 to April 30, 2024: $ 1,360,500 |

| - | May 1, 2024 to August 31, 2024: $ 272,100 |

Under the 2023 Credit Agreement, interest payments are due monthly, and interest on the borrowings consist of the average one-month Euro Interbank Offered Rate (“EURIBOR”) as determined during a month and a surcharge of 3.00%. At June 30, 2023 and June 30, 2022, there were no borrowings outstanding, and interest expense for the years ended June 30, 2023 and 2022 were $111 and $37, respectively.

On September 7, 2022, the Company entered into a Credit Agreement (the “2022 Credit Agreement”) with Rabobank that provided for a € 4.9 million line of credit, that reduced to € 250,000 on April 1, 2023, and matured on September 6, 2023. Interest payments were due monthly, and interest on the borrowings consisted of the average one-month EURIBOR rate as determined during a month plus a surcharge of 3.55%.

To obtain these loans the Company was required to pledge the following collateral: accounts receivable, inventory, legal claims, bank accounts, and equity of Bloomia B.V.

Note 9 — Leases

The Company is party to leasing contracts in which the Company is the lessee. These lease contracts are classified as either operating or finance leases. The Company’s lease contracts include land, buildings, and equipment. Remaining lease terms range from 2 to 6 years with various term extension options available. The Company includes optional extension periods and early termination options in its lease term if it is reasonably likely that the Company will exercise an option to extend or terminate early.

Operating lease ROU assets and operating lease liabilities are recognized based on the present value of lease payments over the lease term, at the later of the commencement date or the date of initial adoption. Because most of the Company’s leases do not provide an implicit rate of return, the discount rate is based on the collateralized borrowing rate of the Company, on a portfolio basis.

The balances for operating and finance leases where the Company is the lessee are presented as follows within the consolidated balance sheets:

|

|

| June 30, |

| |

|

|

| 2023 |

| |

| Finance lease: |

|

|

| |

| Finance right-of-use assets, net |

| $ | 980 |

|

|

|

|

|

|

|

| Current portion of finance lease obligations |

|

| 391 |

|

| Finance lease obligations, net of current portion |

|

| 238 |

|

| Total finance lease liabilities |

| $ | 629 |

|

|

|

|

|

|

|

| Operating lease: |

|

|

|

|

| Operating lease right-of-use assets, net |

| $ | 32,795 |

|

|

|

|

|

|

|

| Current portion of operating lease obligations |

|

| 782 |

|

| Operating lease obligations, net of current portion |

|

| 33,181 |

|

| Total operating lease liabilities |

| $ | 33,963 |

|

| 17 |

| Table of Contents |

The Company is party to an operating lease agreement with Horti-Group for land and greenhouses in King George, Virginia, United States. The lease commenced on July 1, 2021 and ends on December 31, 2038. The Company recognized the following related party balances in the consolidated balance sheets:

|

|

| June 30, |

| |

|

|

| 2023 |

| |

| Operating lease right-of-use assets, net |

| $ | 32,017 |

|

|

|

|

|

|

|

| Current portion of operating lease obligations |

|

| 636 |

|

| Operating lease obligations, net of current portion |

|

| 32,524 |

|

| Total operating lease liabilities |

| $ | 33,160 |

|

The total amount of equipment capitalized under capital lease obligations as of June 30, 2022 was $1,157.

The components of lease expense are as follows within the consolidated statement of operations:

|

|

| June 30, |

| |

|

|

| 2023 |

| |

| Finance lease expense: |

|

|

| |

| Amortization of leased assets |

| $ | 179 |

|

| Interest on lease liabilities |

|

| 38 |

|

| Operating lease expense: |

|

|

|

|

| Operating lease cost |

|

| 4,103 |

|

| Short-term and variable lease cost |

|

| 225 |

|

| Total lease expense |

| $ | 4,545 |

|

Operating lease expense for the year ended June 30, 2022 totaled $4,425. Operating lease expense is included in cost of goods sold and in general and administrative expenses on the consolidated statements of operations and comprehensive income.

The weighted average remaining lease term and weighted average discount rate is as follows:

|

|

| June 30, |

| |

|

|

| 2023 |

| |

| Weighted average remaining lease term (years) |

|

|

| |

| Finance leases |

|

| 1.56 |

|

| Operating leases |

|

| 15.34 |

|

|

|

|

|

|

|

| Weighted average discount rate applied |

|

|

|

|

| Finance leases |

|

| 4.45 | % |

| Operating leases |

|

| 8.56 | % |

Supplemental cash flow information related to leases where the Company is the lessee is as follows:

|

|

| June 30, |

| |

|

|

| 2023 |

| |

| Operating cash outflows from operating leases |

| $ | 3,562 |

|

| Operating cash outflows from finance leases (interest payments) |

|

| 38 |

|

| Financing cash outflows from finance leases |

|

| 391 |

|

| Leased assets obtained in exchange for finance lease liabilities |

|

| - |

|

| Leased assets obtained in exchange for operating lease liabilities |

|

| - |

|

| 18 |

| Table of Contents |

As of June 30, 2023, the maturities of the operating and finance lease liabilities were as follows:

|

|

| Operating |

|

| Finance |

| ||

| Year ending June 30, |

| Leases |

|

| Leases |

| ||

| 2024 |

| $ | 3,633 |

|

| $ | 429 |

|

| 2025 |

|

| 3,704 |

|

|

| 222 |

|

| 2026 |

|

| 3,776 |

|

|

| 4 |

|

| 2027 |

|

| 3,850 |

|

|

| - |

|

| 2028 |

|

| 3,852 |

|

|

| - |

|

| Thereafter |

|

| 43,784 |

|

|

| - |

|

| Total minimum lease payments |

| $ | 62,599 |

|

| $ | 655 |

|

| Less: imputed interest |

|

| (28,636 | ) |

|

| (26 | ) |

| Total: present value of lease liabilities |

| $ | 33,963 |

|

| $ | 629 |

|

| Less: current portion |

|

| (782 | ) |

|

| (391 | ) |

| Long-term portion of lease liabilities |

| $ | 33,181 |

|

| $ | 238 |

|

As of June 30, 2022, future minimum lease payments under operating leases were as follows:

| Year ending June 30, |

|

|

| |

| 2023 |

| $ | 3,557 |

|

| 2024 |

|

| 3,626 |

|

| 2025 |

|

| 3,697 |

|

| 2026 |

|

| 3,769 |

|

| 2027 |

|

| 3,842 |

|

| Thereafter |

|

| 47,630 |

|

| Total minimum lease payments |

| $ | 66,121 |

|

As of June 30, 2022, the maturities of the finance lease liabilities are as follows:

| Year ending June 30, |

|

|

| |

| 2023 |

| $ | 428 |

|

| 2024 |

|

| 428 |

|

| 2025 |

|

| 222 |

|

| 2026 |

|

| 4 |

|

| Thereafter |

|

| - |

|

| Total minimum lease payments |

| $ | 1,082 |

|

| Less: imputed interest |

|

| (62 | ) |

| Total: present value of lease liabilities |

| $ | 1,020 |

|

| Less: current portion |

|

| (390 | ) |

| Long-term portion of lease liabilities |

| $ | 630 |

|

| 19 |

| Table of Contents |

Note 10 — Commitments and Contingencies

Litigation

Liabilities for loss contingencies arising from claims, assessments, litigation, fines, and penalties and other sources are recorded when it is probable that a liability has been incurred and the amount can be reasonably estimated. Legal costs incurred in connection with loss contingencies are expensed as incurred.

In the ordinary course of the business, the Company is subject to periodic legal or administrative proceedings. As of June 30, 2023, the Company was not involved in any material claims or legal actions which, in the opinion of management, the ultimate disposition would have a material adverse effect on the Company’s consolidated financial position, results of operations, or liquidity.

Purchase Obligation

On July 1, 2023 the Company entered into an obligation with a third-party to purchase 25% of their annual production of tulip bulbs through 2028 for an annual obligation of $1.65 million, totaling $8.0 million over the duration of the agreement. In addition, the Company entered into a separate agreement with the same party to supply tulips to that party over a three-year period for a total of $360. The Company will be paid in three sums of $120 beginning on March 1, 2026, with the final payment to be received on March 1, 2028.

Other than these obligations, the Company has not had any material service or supply agreements that obligate the Company to make payments to vendors for an extended period of time.

As of June 30, 2023, the Company has committed to purchase machinery from a third-party for a total amount of $485.

Note 11 — Taxes

The components of income upon which domestic and foreign income taxes have been provided are as follows:

|

|

| Year Ended |

| |||||

|

|

| June 30, |

| |||||

|

|

| 2023 |

|

| 2022 |

| ||

| U.S. income before income taxes |

| $ | 6,667 |

|

| $ | 2,430 |

|

| Foreign income before income taxes |

|

| 1,700 |

|

|

| 687 |

|

| Total income before income taxes |

| $ | 8,367 |

|

| $ | 3,117 |

|

| 20 |

| Table of Contents |

Income tax expense (benefit) is comprised of the following:

|

|

| Year Ended |

| |||||

|

|

| June 30, |

| |||||

| Current: |

| 2023 |

|

| 2022 |

| ||

|

|

|

|

|

| ||||

| Federal |

| $ | 335 |

|

| $ | 16 |

|

| State and local |

|

| 192 |

|

|

| 85 |

|

| Foreign |

|

| 108 |

|

|

| 530 |

|

| Total current income tax expense |

| $ | 635 |

|

| $ | 631 |

|

|

|

|

|

|

|

|

|

|

|

| Deferred: |

|

|

|

|

|

|

|

|

| Federal |

| $ | 1,033 |

|

| $ | 476 |

|

| State and local |

|

| 200 |

|

|

| 144 |

|

| Foreign |

|

| 306 |

|

|

| (110 | ) |

| Total deferred income tax expense |

|

| 1,539 |

|

|

| 510 |

|

|

|

|

|

|

|

|

|

|

|

| Tax provision |

| $ | 2,174 |

|

| $ | 1,141 |

|

The reconciliation between the statutory U.S. federal tax rate and our effective tax rate from continuing operations is as follows:

|

|

| Year Ended |

| |||||

|

|

| June 30, |

| |||||

|

| 2023 |

|

| 2022 |

| |||

| US Federal statutory tax rate |

|

| 21.0 | % |

|

| 21.0 | % |

| Foreign tax rate differential |

|

| 0.7 | % |

|

| 0.8 | % |

| State income taxes – net of federal income tax benefits |

|

| 3.7 | % |

|

| 2.7 | % |

| Participation exemption |

| (0.4 | %) |

| (4.5 | %) | ||

| Other permanent differences |

|

| 0.3 | % |

|

| 12.0 | % |

| Return to provision |

|

| 0.0 | % |

|

| 2.5 | % |

| Other |

|

| 0.6 | % |

|

| 1.4 | % |

| Effective tax rate |

|

| 25.9 | % |

|

| 35.9 | % |

| 21 |

| Table of Contents |

The significant components of deferred tax assets and liabilities are reflected in the following table:

|

|

| June 30, |

| |||||

|

|

| 2023 |

|

| 2022 |

| ||

| Deferred tax assets: |

|

|

|

|

|

| ||

| Net operating loss |

| $ | - |

|

| $ | 688 |

|

| Other |

|

| - |

|

|

| 159 |

|

| Total deferred tax assets |

|

| - |

|

|

| 847 |

|

|

|

|

|

|

|

|

|

|

|

| Accrual to cash |

|

| (499 | ) |

|

| (627 | ) |

| Inventory |

|

| (1,033 | ) |

|

| (987 | ) |

| Fixed assets |

|

| (1,181 | ) |

|

| (314 | ) |

| Investment in partnership |

|

| (67 | ) |

|

| (255 | ) |

| Other |

|

| (95 | ) |

|

| - |

|

| Total deferred tax liabilities |

|

| (2,875 | ) |

|

| (2,183 | ) |

|

|

|

|

|

|

|

|

|

|

| Total net deferred tax assets/(liabilities) |

| $ | (2,875 | ) |

| $ | (1,336 | ) |

The realization of deferred tax assets, including net operating loss (NOL) carryforwards, is dependent on the generation of future taxable income of sufficient to realize the tax deductions, carryforwards and credits. Management must evaluate the ability to rely on expectations of future income in evaluating the ability to realize the Company's deferred tax assets. Valuation allowances on deferred tax assets are recognized if it is determined that it is more likely than not that the asset will not be realized. As of June 30, 2023 and June 30, 2022, the Company does not have a valuation allowance on any of its deferred tax assets.

As of June 30, 2023, Bloomia has no federal, state or foreign operating loss carryforwards.

The Company recognizes interest and penalties related to income tax filings within the provision for income taxes in the accompanying consolidated statements of operations and comprehensive income. Accrued interest and penalties are recorded along with tax liabilities. Interest and penalties related to income taxes are immaterial for the years ended June 30, 2023 and June 30, 2022.

The Company is no longer subject to U.S. federal income tax examinations for years before June 30, 2020, with few exceptions, and is no longer subject to state and local or non-U.S. income tax examinations by tax authorities for years before June 30, 2020.

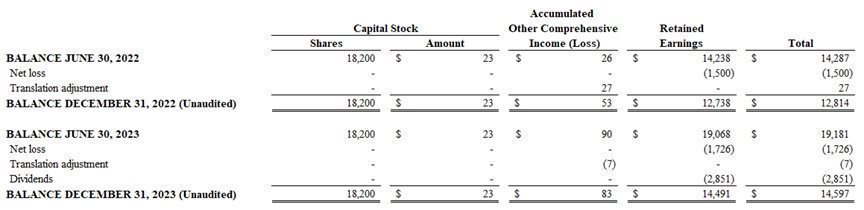

Note 12 — Shareholders’ Equity

Capital Stock

The Company’s authorized, issued and outstanding shares of capital stock of $23 were comprised of 18.2 thousand shares of ordinary shares, with a par value $1.27. As of June 30, 2023 and June 30, 2022 Botman Bloembollen B.V. held 93% and 100% of the ordinary shares, respectively.

Dividends

In November 2021, the Company declared a dividend of $1.36 million, of which $629 was still payable as of June 30, 2022. In December 2022, the Company declared a dividend of $1.41 million, which was paid out in May 2023.

Subsequent to June 30, 2023, the Company declared a dividend of $2.85 million which was paid in September 2023.

| 22 |

| Table of Contents |

Note 13 — Derivative Financial Instruments

The Company is exposed to certain risks to its ongoing business operations. The primary risk managed by using derivative instruments is foreign currency exchange rate risk. The Company has entered into certain financial derivative instruments to manage the risk.

The derivative financial instruments the Company has entered into are forward exchange contracts which have terms of less than a year to economically hedge foreign currency exchange rate risk on recognized nonfunctional currency monetary accounts. The purpose of the Company’s foreign currency hedging activities is to economically hedge the Company’s risk from changes in the fair value of non-functional currency denominated monetary accounts.

The Company records all derivative financial instruments at their fair value in its Consolidated Balance Sheets. None of the derivative financial instruments that the Company holds are designated as either a fair value hedge or cash flow hedge and the gain or loss on the derivative instrument is recorded in earnings. The Company has determined that the fair value of its derivative financial instruments are determined using level 2 inputs (inputs other than quoted prices in active markets for identical assets and liabilities that are observable either directly or indirectly for substantially the full term of the asset or liability) in the fair value hierarchy as the fair value is based on publicly available foreign exchange rates at each financial reporting date. At June 30, 2023 and 2022, the fair value of the Company’s foreign currency forward contracts totaled a liability of $11 and $903, respectively. Derivative liabilities are included in accrued expenses and other current liabilities in the accompanying Consolidated Balance Sheets. For the years ended June 30, 2023 and 2022 the Company recorded a loss of $872 and $1,157, respectively related to changes in fair value. All gains and losses were included in foreign exchange difference, net in the accompanying Consolidated Statement of Operations. The notional principal associated with those contracts was $3,445 and $13,694 million as of June 30, 2023 and 2022.

Note 14 – Pension Plan

For all Dutch employees, the Company participates in defined contribution pension plans with an independent insurance company. Defined contributions are expensed in the year in which the related employee services are rendered. The Company makes contributions on behalf of all Dutch employees of which $62 and $53 were made for the years ended June 30, 2023 and 2022, respectively. These expenses are included in general and administrative expenses in the Consolidated Statements of Operations and Other Comprehensive Income.

Note 15 — Related Parties

On January 1, 2018, the Company entered into an Inter-Company Service Agreement (the “Agreement”) with Botman Bloembollen B.V. (the “Parent”). Per the agreement, the Parent will provide administrative, financial and accounting services, corporate governance and compliance services, legal services, treasury services, regulatory services, human resources services, payroll processing services, procurement management services, tax services and related services. The Agreement was terminated on February 22, 2024.

The net balance between the Company and the Parent was a $729 receivable and a $371 receivable as of June 30, 2023 and 2022, respectively.

The Company is party to an operating lease agreement with Horti-Group for land and greenhouses in King George, Virginia, United States. The lease commenced on July 1, 2021 and ends on December 31, 2038. The Company made rental payments to Horti-Group under the lease agreement during the years ended June 30, 2023 and 2022 totaling $3,365 and $3,299, respectively. The Company recorded expenses under the lease agreement of $3,904 and $3,904 during the years ended June 30, 2023 and 2022. The Company had no balance payable to Horti-Group as of June 30, 2023 and 2022.

Note 16 – Significant Customers

For the years ended June 30, 2023 and 2022, the Company had three customers that accounted for 10% or more of the total revenues. These three customers accounted for 40%, 17%, and 11%, for the year ended June 30, 2023 and 31%, 22%, and 12%, for the year ended June 30, 2022. As of June 30, 2023 and 2022, $1,150 and $2,693 was due from these three customers. The loss of a major customer could adversely affect the Company's operating results and financial condition.

Note 17 — Subsequent Events

The Company has evaluated all events through May 17, 2024, which was the date that the consolidated financial statements were issued. Except as otherwise disclosed in the notes to the consolidated financial statements, there were no other events requiring disclosure in these consolidated financial statements.

| 23 |

| Table of Contents |

BLOOMIA B.V. AND SUBSIDIARIES

CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

FOR THE SIX MONTHS ENDED DECEMBER 31, 2023 AND 2022

| 24 |

Index to the Condensed Consolidated Financial Statements

Six months ended December 31, 2023 and 2022

(Unaudited)

| Pages |

| ||

|

|

| ||

| 26 |

| ||

|

|

|

|

|

| Condensed Consolidated Statements of Operations and Comprehensive Loss |

| 27 |

|

|

|

|

|

|

| Condensed Consolidated Statements of Changes in Shareholders’ Equity | 27 |

| |

|

|

|

|

|

| 29 |

| ||

|

|

|

|

|

|

| 30-40 |

|

| 25 |

| Table of Contents |

Condensed Consolidated Balance Sheets

(Amounts in thousands of U.S. dollars)

The accompanying notes are an integral part of these condensed consolidated financial statements.

| 26 |

| Table of Contents |

Condensed Consolidated Statements of Operations and Comprehensive Loss

(Unaudited)

(Amounts in thousands of U.S. dollars)

The accompanying notes are an integral part of these condensed consolidated financial statements.

| 27 |

| Table of Contents |

Condensed Consolidated Statements of Changes in Shareholders’ Equity

(Amounts in thousands of U.S. dollars, except share data)

The accompanying notes are an integral part of these condensed consolidated financial statements.

| 28 |

| Table of Contents |

Condensed Consolidated Statements of Cash Flows

(Amounts in thousands of U.S. dollars)

(Unaudited)

The accompanying notes are an integral part of these condensed consolidated financial statements.

| 29 |

| Table of Contents |

Notes to Condensed Consolidated Financial Statements

(Unaudited)

(U.S Dollars in thousands)

Note 1 — Organization and Business Operations

Bloomia B.V (“Bloomia”) is a limited liability company incorporated under the laws of the Netherlands. Bloomia is one of the largest producers of fresh cut tulips in the United States of America (“USA”), nurturing over 75 million stems annually. Operations are primarily in the USA with a presence in the Netherlands and South Africa. Bloomia purchases tulip bulbs, hydroponically grows tulips from the bulbs, and sells the stems to retail stores.

As of December 31, 2023, Bloomia had two wholly owned subsidiaries, Bloomia PTY Ltd and Fresh Tulips USA, LLC (“Fresh Tulips”) and a 31% ownership stake in Bloomia Araucania Fowers (“AF”), together (the “Company”).

Note 2 — Summary of Significant Accounting Policies

Basis of Presentation

The accompanying consolidated financial statements have been prepared in accordance with generally accepted accounting principles in the Unites States of America (“U.S. GAAP”) and includes the accounts of the Company and its wholly owned subsidiaries. Entities for which the Company owns an interest, but does not consolidate, are accounted for under the equity method and are included in equity-method investments within the consolidated balance sheets. All intercompany transactions and accounts have been eliminated in consolidation.

On February 22, 2024, the Company was acquired by Tulp 24.1 LLC, a subsidiary of Lendway, Inc. (“Lendway”).

Unaudited Condensed Consolidated Financial Statements

The condensed consolidated balance sheet as of December 31, 2023, the condensed consolidated statements of operations and comprehensive loss, shareholders’ equity, and cash flows for the six months ended December 31, 2023 and 2022, are unaudited. These unaudited interim condensed consolidated financial statements have been prepared on the same basis as the annual consolidated financial statements and reflect, in the opinion of management, all adjustments of a normal and recurring nature that are necessary for the fair statement of the Company’s financial position as of December 31, 2023 and the results of operations and cash flows for the periods presented.

Certain information and footnote disclosures normally included in financial statements prepared in accordance with U.S. GAAP have been condensed or omitted. These interim condensed consolidated financial statements should be read in conjunction with the Company’s audited consolidated financial statements for the year ended June 30, 2023. The financial data and the other financial information disclosed in these notes to the condensed consolidated financial statements related to the six months ended December 31, 2023 and 2022, are also unaudited. The condensed consolidated balance sheet as of June 30, 2023, included herein was derived from the audited consolidated financial statements as of that date. The condensed consolidated results of operations and comprehensive loss for the six months ended December 31, 2023, are not necessarily indicative of results to be expected for the fiscal year ending June 30, 2024, nor for any other future annual or interim period. The tulip sales business tends to be seasonal with spring being the strongest sales season.

Use of Estimates

The preparation of consolidated financial statements in conformity with U.S. GAAP requires management to make certain estimates and assumptions that affect the reported amounts and disclosures of assets and liabilities at the date of the consolidated financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. Significant estimates include the assumptions used in the measurement of right-of-use assets and liabilities and estimated lives of depreciable and amortizable assets.

| 30 |

| Table of Contents |

Foreign Currency Transactions

Transactions and balances that are denominated in currencies that differ from the functional currencies have been remeasured into US dollars in accordance with principles set forth in ASC 830, Foreign Currency Matters. At each balance sheet date, monetary items denominated in foreign currencies are translated at exchange rates in effect at the balance sheet date, while income and expenses are translated at average exchange rates for the periods presented. All exchange gains and losses from the remeasurement mentioned above are reflected in the condensed consolidated statement of operations and comprehensive loss as foreign exchange expenses or income, as appropriate.

The revenues of the Company and most of its subsidiaries are generated in US dollars. In addition, most of the costs of the Company and most of its subsidiaries are incurred in US dollars. The Company’s management has established that the US dollar is the primary currency of the economic environment in which the Company and most of its subsidiaries operate. Thus, the functional currency of the Company and most of its subsidiaries is the US dollar.

For subsidiaries whose functional currency has been determined to be other than the US dollar, assets and liabilities are translated at year-end exchange rates, consolidated statement of operations items are translated at average exchange rates prevailing during the year, and equity is translated at blended historical rates. Resulting translation differences are recorded as a separate component of accumulated other comprehensive income (loss) in equity.

Accounts Receivable, net

Accounts receivable are presented in the balance sheets at their outstanding balances net of the for credit losses. These receivables are generally trade receivables due in one year or less or expected to be billed and collected in one year. The Company estimates credit losses on accounts receivables in accordance with ASC 326 Financial Instruments - Credit Losses. The Company adopted this accounting standard on July 1, 2023 using the modified retrospective approach. The adoption of this ASU did not have a material impact on its condensed consolidated financial statements and related disclosures.

The Company measures the allowance for credit losses on trade receivables on a collective (pool) basis when similar risk characteristics exist. The estimate for allowance for credit losses is based on a historical loss rate for each pool. Management considers qualitative factors such as change in economic factors, regulatory matters, and industry trends to determine if an allowance should be further adjusted. The allowance for credit losses was $60 as of December 31, 2023 and June 30, 2023.

Inventories

Raw materials consist primarily of tulip bulbs, including freight, and packaging supplies. Work-in-process consists of tulip stems and bulbs that have rooted. Inventories are stated at the lower of cost, as determined on the first-in, first-out method, or net realizable value. Finished goods and work-in-process include the inventory costs of raw materials, direct labor and normal manufacturing overhead. Abnormal amounts of spoilage are expensed as incurred and not included in overhead.

Revenue Recognition

The Company accounts for revenue in accordance with FASB Topic 606, “Revenue from Contracts with Customers,” (ASC 606), using the following steps:

|

| · | Identify the contract or contracts, with a customer; |

|

| · | Identify the performance obligations in the contract; |

|

| · | Determine the transaction price; |

|

| · | Allocate the transaction price to performance obligations in the contract; and |

|

| · | Recognize revenue when or as the Company satisfies a performance obligation. |

Revenues from the sale of tulips

The Company recognizes revenue when obligations under the terms of a contract with its customer are satisfied; this occurs with the transfer of control of its tulips. Revenue is measured as the amount of consideration expected to be received in exchange for transferring products. Revenue from product sales is governed primarily by customer pricing and related purchase orders (“contracts”) which specify shipping terms and the transaction price. Contracts are at standalone pricing. The performance obligation in these contracts is determined by each of the individual purchase orders and the respective stated quantities, with revenue being recognized at a point in time when obligations under the terms of the agreement are satisfied. This generally occurs with the transfer of control of tulips to the customer when the product is delivered, with payments from customers being collected between 30-60 days following the transfer of control.

| 31 |

| Table of Contents |

The Company expenses the incremental costs of obtaining a contract, if the amortization period is one year or less. These costs are included in sales and marketing expense on the condensed consolidated statement of operations and other comprehensive loss.

The following table presents revenue disaggregated by customer, as determined by the operational nature of their industry:

|

|

| Six Months Ended December 31, |

| |||||

|

|

| 2023 |

|

| 2022 |

| ||

| Supermarket |

| $ | 9,781 |

|

| $ | 11,651 |

|

| Wholesaler |

|

| 1,902 |

|

|

| 225 |

|

| Other |

|

| 1 |

|

|

| 10 |

|

| Total |

| $ | 11,684 |

|

| $ | 11,886 |

|

Cost of Sales

Cost of sales consists primarily of costs to procure, sort, pick, cool and transport bulbs. Additionally, cost of sales includes labor and facility costs related to production operations.

Shipping and handling

The Company’s shipping and handling costs include costs incurred with third-party carriers to transport products to customers. The costs of out-bound freight are included in the cost of goods sold in the condensed consolidated statement of operations and other comprehensive loss. For the six months ended December 31, 2023 and 2022, the costs of out-bound freight were $1,186 and $1,238, respectively.

Advertising costs

The Company expenses advertising costs as incurred. These costs are included within sales and marketing expenses in the condensed consolidated statement of operations and other comprehensive loss. Total advertising expense was approximately $21 and $27 for the six months ended December 31, 2023 and 2022, respectively.

New Accounting Pronouncements

Recently Adopted Accounting Standards

In February 2016, the FASB issued ASU 2016-02, Leases (Topic 842), which requires the recognition of right-of-use assets and lease liabilities by lessees for certain leases classified as operating leases and also requires expanded disclosures regarding leasing activities. The Company has adopted the standard effective July 1, 2022, using the modified retrospective approach. All comparative periods prior to July 1, 2022 are not adjusted and continue to be reported in accordance with ASC 840, Leases.

The Company has elected the package of practical expedients permitted under the transition guidance within the new standard, which among other things, allows the Company to carry forward the historical lease classification and initial direct costs treatment at transition. The Company has also made an accounting policy election to exclude leases with an initial term of 12 months or less from the consolidated balance sheet. The Company will recognize those lease payments in the condensed consolidated statements of operations and other comprehensive loss on a straight-line basis over the lease term.

| 32 |

| Table of Contents |

Lease payments may include future escalations based on an index or other rate (such as the consumer price index), which the Company initially measures using the index or rate at lease commencement. Subsequent changes or other periodic market-rate adjustments to base rent are recorded as variable lease expense in the period incurred. Residual value guarantees or payments for terminating the lease are included in the lease liability only when it is probable they will be incurred. Lease liabilities and their corresponding right-of-use assets (“ROU”) are recorded based on the present value of lease payments over the expected lease term. The interest rate implicit in lease contracts is sometimes not readily determinable. In such cases, the Company utilizes the appropriate incremental borrowing rate, which is the rate incurred to borrow on a collateralized basis over a similar term an amount equal to the lease payments in a similar economic environment. The ROU assets are also adjusted for any initial direct costs incurred and lease payments made at or before the commencement date and are reduced by lease incentives received.

The Company’s leases may include a non-lease component representing additional services transferred to the Company, such as common area maintenance for real estate. The Company has made an accounting policy election to account for lease and non-lease components in its contracts as a single lease component for real estate asset related leases. The Company has elected to separate all lease and non-lease components for all other asset classes. The non-lease components, which are typically variable in nature, are recorded in variable lease expense in the period incurred.

The adoption of the standard resulted in recording operating lease right-of-use assets and operating lease liabilities of $33,952 and $34,579, respectively on July 1, 2022. The adoption of the new standard did not have a material impact on the Company’s condensed consolidated statement of operations and other comprehensive loss or consolidated statement of cash flows.

In December 2019, the FASB issued ASU 2019-12, Income Taxes (Topic 740): Simplifying the Accounting for Income Taxes, which removes certain exceptions for recognizing deferred taxes for investments, performing intraperiod allocation and calculating income taxes in interim periods. The ASU also adds guidance to reduce complexity in certain areas, including recognizing deferred taxes for tax goodwill and allocating taxes to members of a consolidated group. ASU 2019-12 is effective for the Company’s annual periods beginning after December 15, 2021. The adoption of ASU 2019-12 on July 1, 2022 did not have a material impact on the Company’s consolidated financial statements.