UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

____________________________________

FORM 10-Q

____________________________________

(Mark One)

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the quarterly period ended March 31, 2024

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from ____________ to ______________

Commission file number 001-13958

____________________________________

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

(Address of principal executive offices) (Zip Code)

(860 ) 547-5000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

1

| Indicate by check mark: | ||||||||||||||

• whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | ☑ | No | ☐ | |||||||||||

• whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). | ☑ | No | ☐ | |||||||||||

| • whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act. | ||||||||||||||

| ☑ | Accelerated filer | ☐ | ||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||

| Emerging growth company | ||||||||||||||

| • | If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. | ☐ | |||||||||||||||

| • | whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). | Yes | No | ☑ | |||||||||||||

As of April 24, 2024, there were outstanding 295,755,372 shares of Common Stock, $0.01 par value per share, of the registrant.

2

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

QUARTERLY REPORT ON FORM 10-Q

FOR THE QUARTERLY PERIOD ENDED MARCH 31, 2024

TABLE OF CONTENTS

| Item | Description | Page | ||||||

| PART I. FINANCIAL INFORMATION | ||||||||

| 1. | ||||||||

| 2. | ||||||||

| 3. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | [a] | ||||||

| 4. | ||||||||

| PART II. OTHER INFORMATION | ||||||||

| 1. | ||||||||

| 1A. | ||||||||

| 2. | ||||||||

5.. | ||||||||

| 6. | ||||||||

[a]The information required by this item is set forth in the Enterprise Risk Management section of Item 2, Management's Discussion and Analysis of Financial Condition and Results of Operations and is incorporated herein by reference.

3

Forward-looking Statements

Certain of the statements contained herein are forward-looking statements made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements can be identified by words such as “anticipates,” “intends,” “plans,” “seeks,” “believes,” “estimates,” “expects,” “projects,” and similar references to future periods.

Forward-looking statements are based on management's current expectations and assumptions regarding future economic, competitive, legislative and other developments and their potential effect upon The Hartford Financial Services Group, Inc. and its subsidiaries (collectively, the "Company" or "The Hartford"). Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict. Actual results could differ materially from expectations depending on the evolution of various factors, including the risks and uncertainties identified below, as well as factors described in such forward-looking statements, the Risk Factors of The Hartford's 2023 Form 10-K Annual Report, and our other filings with the Securities and Exchange Commission.

•Risks Relating to Economic, Political and Global Market Conditions:

◦challenges related to the Company’s current operating environment, including global political, economic and market conditions, and the effect of financial market disruptions, economic downturns, changes in trade regulation including tariffs and other barriers or other potentially adverse macroeconomic developments on the demand for our products and returns in our investment portfolios;

◦market risks associated with our business, including changes in credit spreads, equity prices, interest rates, inflation rate, foreign currency exchange rates and market volatility;

◦the impact on our investment portfolio if our investment portfolio is concentrated in any particular segment of the economy;

◦the impacts of changing climate and weather patterns on our businesses, operations and investment portfolio including on claims, demand and pricing of our products, the availability and cost of reinsurance, our modeling data used to evaluate and manage risks of catastrophes and severe weather events, the value of our investment portfolios and credit risk with reinsurers and other counterparties;

•Insurance Industry and Product-Related Risks:

◦the possibility of unfavorable loss development, including with respect to long-tailed exposures;

◦the significant uncertainties that limit our ability to estimate the ultimate reserves necessary for asbestos and environmental claims;

◦the possibility of another pandemic, civil unrest, earthquake, or other natural or man-made disaster that may adversely affect our businesses;

◦weather and other natural physical events, including the intensity and frequency of thunderstorms, tornadoes, hail, wildfires, flooding, winter storms, hurricanes and tropical storms, as well as climate change and its potential impact on weather patterns;

◦the possible occurrence of terrorist attacks and the Company’s inability to contain its exposure as a result of, among other factors, the inability to exclude coverage for terrorist attacks from workers' compensation policies and limitations on reinsurance coverage from the federal government under applicable laws;

◦the Company’s ability to effectively price its products and policies, including its ability to obtain regulatory consents to pricing actions or to non-renewal or withdrawal of certain product lines;

◦actions by competitors that may be larger or have greater financial resources than we do;

◦technological changes, including usage-based methods of determining premiums, advancements in certain emerging technologies, including machine learning, predictive analytics, “big data” analysis or other artificial intelligence functions, advancements in automotive safety features, the development of autonomous vehicles, and platforms that facilitate ride sharing;

◦the Company's ability to market, distribute and provide insurance products and investment advisory services through current and future distribution channels and advisory firms;

◦the uncertain effects of emerging claim and coverage issues;

◦political instability, politically motivated violence or civil unrest, which may increase the frequency and severity of insured losses;

◦the ongoing effects of COVID-19, including exposure to COVID-19 business interruption property claims and the possibility of a resurgence of COVID-19 related losses in Group Benefits;

•Financial Strength, Credit and Counterparty Risks:

◦risks to our business, financial position, prospects and results associated with negative rating actions or downgrades in the Company’s financial strength and credit ratings or negative rating actions or downgrades relating to our investments;

◦capital requirements which are subject to many factors, including many that are outside the Company’s control, such as National Association of Insurance Commissioners ("NAIC") risk based capital formulas, rating agency capital models, Funds at Lloyd's

4

and Solvency Capital Requirement, which can in turn affect our credit and financial strength ratings, cost of capital, regulatory compliance and other aspects of our business and results;

◦losses due to nonperformance or defaults by others, including credit risk with counterparties associated with investments, derivatives, premiums receivable, reinsurance recoverables and indemnifications provided by third parties in connection with previous dispositions;

◦the potential for losses due to our reinsurers' unwillingness or inability to meet their obligations under reinsurance contracts and the availability, pricing and adequacy of reinsurance to protect the Company against losses;

◦state and international regulatory limitations on the ability of the Company and certain of its subsidiaries to declare and pay dividends;

•Risks Relating to Estimates, Assumptions and Valuations:

◦risks associated with the use of analytical models in making decisions in key areas such as underwriting, pricing, capital management, reserving, investments, reinsurance and catastrophe risk management;

◦the potential for differing interpretations of the methodologies, estimations and assumptions that underlie the Company’s fair value estimates for its investments and the evaluation of intent-to-sell impairments and allowance for credit losses on available-for-sale securities and mortgage loans;

◦the potential for impairments of our goodwill;

•Strategic and Operational Risks:

◦the Company’s ability to maintain the availability of its systems and safeguard the security of its data in the event of a disaster, cyber or other information security incident or other unanticipated event;

◦the potential for difficulties arising from outsourcing and similar third-party relationships;

◦the risks, challenges and uncertainties associated with capital management plans, expense reduction initiatives and other actions;

◦risks associated with acquisitions and divestitures, including the challenges of integrating acquired companies or businesses, which may result in our inability to achieve the anticipated benefits and synergies and may result in unintended consequences;

◦difficulty in attracting and retaining talented and qualified personnel, including key employees, such as executives, managers and employees with strong technological, analytical and other specialized skills;

◦the Company’s ability to protect its intellectual property and defend against claims of infringement;

•Regulatory and Legal Risks:

◦the cost and other potential effects of increased federal, state and international regulatory and legislative developments, including those that could adversely impact the demand for the Company’s products, operating costs and required capital levels;

◦unfavorable judicial or legislative developments;

◦the impact of changes in federal, state or foreign tax laws;

◦regulatory requirements that could delay, deter or prevent a takeover attempt that stockholders might consider in their best interests; and

◦the impact of potential changes in accounting principles and related financial reporting requirements.

Any forward-looking statement made by the Company in this document speaks only as of the date of the filing of this Form 10-Q. Factors or events that could cause the Company’s actual results to differ may emerge from time to time, and it is not possible for the Company to predict all of them. The Company undertakes no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments or otherwise.

5

Part I - Item 1. Financial Statements

Item 1. | ||||||||||||||

FINANCIAL STATEMENTS

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors and Stockholders of

The Hartford Financial Services Group, Inc.

Hartford, Connecticut

Results of Review of Interim Financial Information

We have reviewed the accompanying condensed consolidated balance sheet of The Hartford Financial Services Group, Inc. and subsidiaries (the "Company") as of March 31, 2024, the related condensed consolidated statements of operations, comprehensive income, changes in stockholders' equity, and cash flows for the three-month periods ended March 31, 2024 and 2023, and the related notes (collectively referred to as the "interim financial information"). Based on our reviews, we are not aware of any material modifications that should be made to the accompanying interim financial information for it to be in conformity with accounting principles generally accepted in the United States of America.

We have previously audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States) (PCAOB), the consolidated balance sheet of the Company as of December 31, 2023, and the related consolidated statements of operations, comprehensive income (loss), changes in stockholders' equity, and cash flows for the year then ended (not presented herein); and in our report dated February 23, 2024, we expressed an unqualified opinion on those consolidated financial statements and included an explanatory paragraph regarding a change in accounting principle for the measurement and disclosure of long-duration contracts issued by insurance companies. In our opinion, the information set forth in the accompanying condensed consolidated balance sheet as of December 31, 2023, is fairly stated, in all material respects, in relation to the consolidated balance sheet from which it has been derived.

Basis for Review Results

This interim financial information is the responsibility of the Company's management. We are a public accounting firm registered with the PCAOB and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our reviews in accordance with standards of the PCAOB. A review of interim financial information consists principally of applying analytical procedures and making inquiries of persons responsible for financial and accounting matters. It is substantially less in scope than an audit conducted in accordance with the standards of the PCAOB, the objective of which is the expression of an opinion regarding the financial statements taken as a whole. Accordingly, we do not express such an opinion.

/s/ DELOITTE & TOUCHE LLP

Hartford, Connecticut

April 25, 2024

6

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

Condensed Consolidated Statements of Operations

| Three Months Ended March 31, | ||||||||

| (in millions, except for per share data) | 2024 | 2023 | ||||||

| (Unaudited) | ||||||||

| Revenues | ||||||||

| Earned premiums | $ | $ | ||||||

| Fee income | ||||||||

| Net investment income | ||||||||

| Net realized gains (losses) | ( | |||||||

| Other revenues | ||||||||

| Total revenues | ||||||||

| Benefits, losses and expenses | ||||||||

| Benefits, losses and loss adjustment expenses | ||||||||

Amortization of deferred policy acquisition costs ("DAC") | ||||||||

| Insurance operating costs and other expenses | ||||||||

| Interest expense | ||||||||

| Amortization of other intangible assets | ||||||||

| Restructuring and other costs | ||||||||

| Total benefits, losses and expenses | ||||||||

| Income before income taxes | ||||||||

| Income tax expense | ||||||||

| Net income | ||||||||

| Preferred stock dividends | ||||||||

| Net income available to common stockholders | $ | $ | ||||||

| Net income available to common stockholders per common share | ||||||||

| Basic | $ | $ | ||||||

| Diluted | $ | $ | ||||||

See Notes to Condensed Consolidated Financial Statements.

7

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

Condensed Consolidated Statements of Comprehensive Income

| Three Months Ended March 31, | ||||||||

| (in millions) | 2024 | 2023 | ||||||

| (Unaudited) | ||||||||

| Net income | $ | $ | ||||||

Other comprehensive income (loss) ("OCI"): | ||||||||

| Change in net unrealized gain (loss) on fixed maturities, available-for-sale ("AFS") | ( | |||||||

| Change in unrealized losses on fixed maturities with an allowance for credit losses ("ACL") | ( | |||||||

| Change in net gain (loss) on cash flow hedging instruments | ||||||||

| Change in foreign currency translation adjustments | ( | |||||||

| Change in liability for future policy benefits adjustments | ( | |||||||

| Change in pension and other postretirement plan adjustments | ||||||||

| Other comprehensive income (loss), net of tax | ( | |||||||

| Comprehensive income | $ | $ | ||||||

See Notes to Condensed Consolidated Financial Statements.

8

| (in millions, except for share and per share data) | March 31, 2024 | December 31, 2023 | ||||||

| (Unaudited) | ||||||||

| Assets | ||||||||

| Investments: | ||||||||

Fixed maturities, AFS, at fair value (amortized cost of $ | $ | $ | ||||||

Fixed maturities, at fair value using the fair value option ("FVO Securities") | ||||||||

| Equity securities, at fair value | ||||||||

Mortgage loans (net of ACL of $ | ||||||||

| Limited partnerships and other alternative investments | ||||||||

| Other investments | ||||||||

| Short-term investments | ||||||||

| Total investments | ||||||||

| Cash | ||||||||

| Restricted cash | ||||||||

Accrued investment income | ||||||||

Premiums receivable and agents' balances (net of ACL of $ | ||||||||

Reinsurance recoverables (net of allowance for uncollectible reinsurance of $ | ||||||||

| Deferred policy acquisition costs | ||||||||

| Deferred income taxes, net | ||||||||

| Goodwill | ||||||||

| Property and equipment, net | ||||||||

| Other intangible assets, net | ||||||||

| Other assets | ||||||||

| Total assets | $ | $ | ||||||

| Liabilities | ||||||||

| Unpaid losses and loss adjustment expenses | $ | $ | ||||||

| Reserve for future policy benefits | ||||||||

| Other policyholder funds and benefits payable | ||||||||

| Unearned premiums | ||||||||

| Long-term debt | ||||||||

| Other liabilities | ||||||||

| Total liabilities | ||||||||

| Commitments and Contingencies (Note 13) | ||||||||

| Stockholders’ Equity | ||||||||

Preferred stock, $ | ||||||||

Common stock, $ | ||||||||

| Additional paid-in capital | ||||||||

| Retained earnings | ||||||||

Treasury stock, at cost | ( | ( | ||||||

Accumulated other comprehensive income (loss) ("AOCI"), net of tax | ( | ( | ||||||

| Total stockholders’ equity | ||||||||

| Total liabilities and stockholders’ equity | $ | $ | ||||||

See Notes to Condensed Consolidated Financial Statements.

9

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

Condensed Consolidated Statements of Changes in Stockholders' Equity

| Three Months Ended March 31, | ||||||||

| (in millions, except for share and per share data) | 2024 | 2023 | ||||||

| (Unaudited) | ||||||||

| Preferred Stock | $ | $ | ||||||

| Common Stock | ||||||||

| Additional Paid-in Capital | ||||||||

| Additional Paid-in Capital, beginning of period | ||||||||

| Issuance of shares under incentive and stock compensation plans and other | ( | ( | ||||||

| Stock-based compensation plans expense | ||||||||

| Additional Paid-in Capital, end of period | ||||||||

| Retained Earnings | ||||||||

| Retained Earnings, beginning of period | ||||||||

| Net income | ||||||||

| Dividends declared on preferred stock | ( | ( | ||||||

| Dividends declared on common stock | ( | ( | ||||||

| Retained Earnings, end of period | ||||||||

| Treasury Stock, at cost | ||||||||

| Treasury Stock, at cost, beginning of period | ( | ( | ||||||

| Treasury stock acquired | ( | ( | ||||||

| Issuance of shares under incentive and stock compensation plans from treasury stock and other | ||||||||

| Net shares acquired related to employee incentive and stock compensation plans | ( | ( | ||||||

| Treasury Stock, at cost, end of period | ( | ( | ||||||

| Accumulated Other Comprehensive Income (Loss), net of tax | ||||||||

| Accumulated Other Comprehensive Income, net of tax, beginning of period | ( | ( | ||||||

| Total other comprehensive income (loss) | ( | |||||||

| Accumulated Other Comprehensive Income (Loss), net of tax, end of period | ( | ( | ||||||

| Total Stockholders’ Equity | $ | $ | ||||||

| Preferred Shares Outstanding | ||||||||

| Common Shares Outstanding (in thousands) | ||||||||

| Common Shares Outstanding, beginning of period | ||||||||

| Treasury stock acquired | ( | ( | ||||||

| Issuance of shares under incentive and stock compensation plans and other | ||||||||

| Return of shares under incentive and stock compensation plans to treasury stock | ( | ( | ||||||

| Common Shares Outstanding, at end of period | ||||||||

| Cash dividends declared per common share | $ | $ | ||||||

| Cash dividends declared per preferred share | $ | $ | ||||||

See Notes to Condensed Consolidated Financial Statements.

10

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

Condensed Consolidated Statements of Cash Flows

| Three Months Ended March 31, | ||||||||

| (in millions) | 2024 | 2023 | ||||||

| Operating Activities | (Unaudited) | |||||||

| Net income | $ | $ | ||||||

| Adjustments to reconcile net income to net cash provided by operating activities: | ||||||||

| Net realized losses (gains) | ( | |||||||

| Amortization of deferred policy acquisition costs | ||||||||

| Additions to deferred policy acquisition costs | ( | ( | ||||||

| Depreciation and amortization | ||||||||

| Other operating activities, net | ||||||||

| Change in assets and liabilities: | ||||||||

| Decrease in reinsurance recoverables | ||||||||

| Net change in accrued and deferred income taxes | ||||||||

| Increase in insurance liabilities | ||||||||

| Net change in premiums receivable and agents' balances | ( | ( | ||||||

| Net change in other assets and other liabilities | ( | ( | ||||||

| Net cash provided by operating activities | ||||||||

| Investing Activities | ||||||||

| Proceeds from the sale/maturity/prepayment of: | ||||||||

| Fixed maturities, AFS | ||||||||

| Fixed maturities, at fair value using the fair value option | ||||||||

| Equity securities, at fair value | ||||||||

| Mortgage loans | ||||||||

| Limited partnership and other alternative investments | ||||||||

| Payments for the purchase of: | ||||||||

| Fixed maturities, AFS | ( | ( | ||||||

| Fixed maturities, at fair value using the fair value option | ||||||||

| Equity securities, at fair value | ( | ( | ||||||

| Mortgage loans | ( | ( | ||||||

| Limited partnership and other alternative investments | ( | ( | ||||||

| Net proceeds from derivatives | ||||||||

| Net additions of property and equipment | ( | ( | ||||||

| Net proceeds from (payments for) short-term investments | ( | |||||||

| Other investing activities, net | ( | |||||||

| Net cash used for investing activities | ( | ( | ||||||

| Financing Activities | ||||||||

| Deposits and other additions to investment and universal life-type contracts | ||||||||

| Withdrawals and other deductions from investment and universal life-type contracts | ( | ( | ||||||

| Net return of shares under incentive and stock compensation plans | ( | ( | ||||||

| Treasury stock acquired | ( | ( | ||||||

| Dividends paid on preferred stock | ( | ( | ||||||

| Dividends paid on common stock | ( | ( | ||||||

| Net cash used for financing activities | ( | ( | ||||||

| Foreign exchange rate effect on cash | ( | |||||||

| Net increase (decrease) in cash and restricted cash | ( | |||||||

| Cash and restricted cash – beginning of period | ||||||||

| Cash and restricted cash– end of period | $ | $ | ||||||

| Supplemental Disclosure of Cash Flow Information | ||||||||

| Income tax paid | $ | $ | ||||||

| Interest paid | $ | $ | ||||||

See Notes to Condensed Consolidated Financial Statements.

11

|

| Note 1 - Basis of Presentation and Significant Accounting Policies | ||||||||

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Dollar amounts in millions, except for per share data, unless otherwise stated)

(Unaudited)

Basis of Presentation

The Hartford Financial Services Group, Inc. is a holding company for insurance and financial services subsidiaries that provide property and casualty insurance, group benefits insurance and services and mutual funds and exchange-traded funds ("ETF") to individual and business customers in the United States as well as in the United Kingdom and other international locations (collectively, “The Hartford”, the “Company”, “we” or “our”).

The Condensed Consolidated Financial Statements have been prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”) for interim financial information, which differ materially from the accounting practices prescribed by various insurance regulatory authorities. These Condensed Consolidated Financial Statements and Notes should be read in conjunction with the Consolidated Financial Statements and Notes thereto included in the Company's 2023 Form 10-K Annual Report. The results of operations for interim periods are not necessarily indicative of the results that may be expected for the full year.

The accompanying Condensed Consolidated Financial Statements and Notes are unaudited. These financial statements reflect all adjustments (generally consisting only of normal accruals) which are, in the opinion of management, necessary for the fair statement of the financial position, results of operations and cash flows for the interim periods.

Consolidation

The Condensed Consolidated Financial Statements include the accounts of The Hartford Financial Services Group, Inc., and entities in which the Company directly or indirectly has a controlling financial interest. Entities in which the Company has significant influence over the operating and financing decisions but does not control are reported using the equity method. Intercompany transactions and balances between The Hartford and its subsidiaries and affiliates have been eliminated.

Use of Estimates

The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

The most significant estimates include those used in determining property and casualty and group long-term disability ("LTD") insurance product reserves, net of reinsurance; evaluation of goodwill for impairment; valuation of investments and derivative instruments; and contingencies relating to corporate litigation and regulatory matters.

Reclassifications

2. EARNINGS PER COMMON SHARE

| Computation of Basic and Diluted Earnings per Common Share | ||||||||

| Three Months Ended March 31, | ||||||||

| (In millions, except for per share data) | 2024 | 2023 | ||||||

| Earnings | ||||||||

| Net income | $ | $ | ||||||

| Less: Preferred stock dividends | ||||||||

| Net income available to common stockholders | $ | $ | ||||||

| Shares | ||||||||

| Weighted average common shares outstanding, basic | ||||||||

| Dilutive effect of stock-based awards under compensation plans | ||||||||

| Weighted average common shares outstanding and dilutive potential common shares | ||||||||

| Net income available to common stockholders per common share | ||||||||

| Basic | $ | $ | ||||||

| Diluted | $ | $ | ||||||

12

|

Note 3 - Segment Information | ||||||||

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

3. SEGMENT INFORMATION

The Company currently conducts business principally in five reporting segments including Commercial Lines, Personal Lines, Property & Casualty ("P&C") Other Operations, Group Benefits and Hartford Funds, as well as a Corporate category.

Net Income (Loss) | ||||||||

| Three Months Ended March 31, | ||||||||

| 2024 | 2023 | |||||||

| Commercial Lines | $ | $ | ||||||

| Personal Lines | ( | |||||||

| Property & Casualty Other Operations | ||||||||

| Group Benefits | ||||||||

| Hartford Funds | ||||||||

| Corporate | ( | ( | ||||||

| Net income | ||||||||

| Preferred stock dividends | ||||||||

| Net income available to common stockholders | $ | $ | ||||||

13

|

Note 3 - Segment Information | ||||||||

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

Revenues

| Three Months Ended March 31, | ||||||||

| 2024 | 2023 | |||||||

| Earned premiums and fee income: | ||||||||

Commercial Lines | ||||||||

| Workers’ compensation | $ | $ | ||||||

| Liability | ||||||||

| Marine | ||||||||

| Package business | ||||||||

| Property | ||||||||

| Professional liability | ||||||||

| Bond | ||||||||

| Assumed reinsurance | ||||||||

| Automobile | ||||||||

| Total Commercial Lines | ||||||||

Personal Lines | ||||||||

| Automobile | ||||||||

| Homeowners | ||||||||

| Total Personal Lines [1] | ||||||||

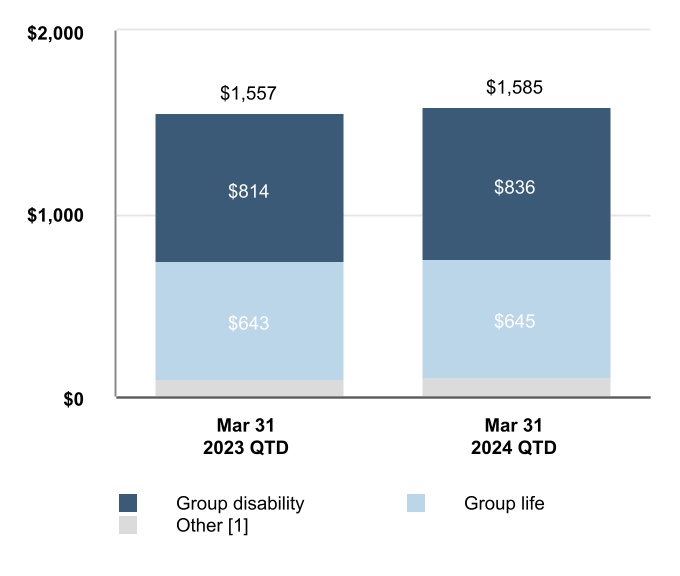

Group Benefits | ||||||||

| Group disability | ||||||||

| Group life | ||||||||

| Other | ||||||||

| Total Group Benefits | ||||||||

Hartford Funds | ||||||||

| Mutual fund and ETF | ||||||||

| Third-party life and annuity separate accounts | ||||||||

| Total Hartford Funds | ||||||||

Corporate | ||||||||

| Total earned premiums and fee income | ||||||||

| Net investment income | ||||||||

| Net realized gains (losses) | ( | |||||||

| Other revenues | ||||||||

Total revenues | $ | $ | ||||||

14

|

Note 3 - Segment Information | ||||||||

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

Non-Insurance Revenue from Contracts with Customers

| Three Months Ended March 31, | |||||||||||

| Revenue Line Item | 2024 | 2023 | |||||||||

| Commercial Lines | |||||||||||

| Installment billing fees | Fee income | $ | $ | ||||||||

| Personal Lines | |||||||||||

| Installment billing fees | Fee income | ||||||||||

| Insurance servicing revenues | Other revenues | ||||||||||

| Group Benefits | |||||||||||

| Administrative services | Fee income | ||||||||||

| Hartford Funds | |||||||||||

| Advisory, servicing and distribution fees | Fee income | ||||||||||

| Corporate | |||||||||||

| Investment management and other fees | Fee income | ||||||||||

| Total non-insurance revenues with customers | $ | $ | |||||||||

4. FAIR VALUE MEASUREMENTS

The Company carries certain financial assets and liabilities at estimated fair value. Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in the principal or most advantageous market in an orderly transaction between market participants. Our fair value framework includes a hierarchy that gives the highest priority to the use of quoted prices in active markets, followed by the use of market observable inputs, followed by the use of unobservable inputs. The fair value hierarchy levels are as follows:

Level 1 Fair values based primarily on unadjusted quoted prices for identical assets or liabilities, in active markets that the Company has the ability to access at the measurement date.

Level 2 Fair values primarily based on observable inputs, other than quoted prices included in Level 1, or based on prices for similar assets and liabilities.

Level 3 Fair values derived when one or more of the significant inputs are unobservable (including assumptions about risk). With little or no observable market, the determination of fair values uses considerable judgment and represents the Company’s best estimate of an amount that could be realized in a market exchange for the asset or liability. Also included are securities that are traded within illiquid markets and/or priced by independent brokers.

The Company will classify the financial asset or liability by level based upon the lowest level input that is significant to the determination of the fair value. In most cases, both observable inputs (e.g., changes in interest rates) and unobservable inputs (e.g., changes in risk assumptions) are used to determine fair values that the Company has classified within Level 3.

15

|

Note 4 - Fair Value Measurements | ||||||||

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

| Assets and (Liabilities) Carried at Fair Value by Hierarchy Level as of March 31, 2024 | ||||||||||||||

| Total | Quoted Prices in Active Markets for Identical Assets (Level 1) | Significant Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | |||||||||||

| Assets accounted for at fair value on a recurring basis | ||||||||||||||

| Fixed maturities, AFS | ||||||||||||||

Asset backed securities ("ABS") | $ | $ | $ | $ | ||||||||||

Collateralized loan obligations ("CLO") | ||||||||||||||

Commercial mortgage-backed securities ("CMBS") | ||||||||||||||

| Corporate | ||||||||||||||

| Foreign government/government agencies | ||||||||||||||

| Municipal | ||||||||||||||

Residential mortgage-backed securities ("RMBS") | ||||||||||||||

| U.S. Treasuries | ||||||||||||||

| Total fixed maturities, AFS | ||||||||||||||

| FVO securities | ||||||||||||||

| Equity securities, at fair value [1] | ||||||||||||||

| Derivative assets | ||||||||||||||

| Credit derivatives | ||||||||||||||

| Foreign exchange derivatives | ||||||||||||||

| Interest rate derivatives | ||||||||||||||

| Total derivative assets [2] | ||||||||||||||

| Short-term investments | ||||||||||||||

| Total assets accounted for at fair value on a recurring basis | $ | $ | $ | $ | ||||||||||

| Liabilities accounted for at fair value on a recurring basis | ||||||||||||||

| Derivative liabilities | ||||||||||||||

| Credit derivatives | $ | ( | $ | $ | ( | $ | ||||||||

| Foreign exchange derivatives | ||||||||||||||

| Interest rate derivatives | ( | ( | ||||||||||||

| Total derivative liabilities [3] | ( | ( | ||||||||||||

| Total liabilities accounted for at fair value on a recurring basis | $ | ( | $ | $ | ( | $ | ||||||||

16

|

Note 4 - Fair Value Measurements | ||||||||

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

| Assets and (Liabilities) Carried at Fair Value by Hierarchy Level as of December 31, 2023 | ||||||||||||||

| Total | Quoted Prices in Active Markets for Identical Assets (Level 1) | Significant Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | |||||||||||

| Assets accounted for at fair value on a recurring basis | ||||||||||||||

| Fixed maturities, AFS | ||||||||||||||

| ABS | $ | $ | $ | $ | ||||||||||

| CLO | ||||||||||||||

| CMBS | ||||||||||||||

| Corporate | ||||||||||||||

| Foreign government/government agencies | ||||||||||||||

| Municipal | ||||||||||||||

| RMBS | ||||||||||||||

| U.S. Treasuries | ||||||||||||||

| Total fixed maturities, AFS | ||||||||||||||

| FVO securities | ||||||||||||||

| Equity securities, at fair value [1] | ||||||||||||||

| Derivative assets | ||||||||||||||

| Credit derivatives | ( | ( | ||||||||||||

| Foreign exchange derivatives | ||||||||||||||

| Total derivative assets [2] | ( | ( | ||||||||||||

| Short-term investments | ||||||||||||||

| Total assets accounted for at fair value on a recurring basis | $ | $ | $ | $ | ||||||||||

| Liabilities accounted for at fair value on a recurring basis | ||||||||||||||

| Derivative liabilities | ||||||||||||||

| Credit derivatives | $ | $ | $ | $ | ||||||||||

| Foreign exchange derivatives | ||||||||||||||

| Interest rate derivatives | ( | ( | ||||||||||||

| Total derivative liabilities [3] | ||||||||||||||

| Total liabilities accounted for at fair value on a recurring basis | $ | $ | $ | $ | ||||||||||

[1]Level 3 includes investments that have contractual sales restrictions that require consent to sell and are in place for the duration that the securities are held by the Company.

[2]Includes derivative instruments in a net positive fair value position after consideration of the accrued interest and impact of collateral posting requirements which may be imposed by agreements and applicable law. See footnote 3 to this table for derivative liabilities.

[3]Includes derivative instruments in a net negative fair value position (derivative liability) after consideration of the accrued interest and impact of collateral posting requirements which may be imposed by agreements and applicable law.

The Company has overseas deposits included in other investments of $75

Fixed Maturities, Equity Securities, Short-term Investments, and Derivatives

Valuation Techniques

The Company generally determines fair values using valuation techniques that use prices, rates, and other relevant information evident from market transactions involving identical or similar

instruments. Valuation techniques also include, where appropriate, estimates of future cash flows that are converted into a single discounted amount using current market expectations. The Company uses a "waterfall" approach comprised of the following pricing sources and techniques, which are listed in priority order:

•Quoted prices, unadjusted, for identical assets or liabilities in active markets, which are classified as Level 1.

•Prices from third-party pricing services, which primarily utilize a combination of techniques. These services utilize recently reported trades of identical, similar, or benchmark securities making adjustments for market observable inputs available through the reporting date. If there are no recently reported trades, they may use a discounted cash flow

17

|

Note 4 - Fair Value Measurements | ||||||||

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

technique to develop a price using expected cash flows based upon the anticipated future performance of the underlying collateral discounted at an estimated market rate. Both techniques develop prices that consider the time value of future cash flows and provide a margin for risk, including liquidity and credit risk. Most prices provided by third-party pricing services are classified as Level 2 because the inputs used in pricing the securities are observable. However, some securities that are less liquid or trade less actively are classified as Level 3. Additionally, certain long-dated securities include benchmark interest rate or credit spread assumptions that are not observable in the marketplace and are thus classified as Level 3.

•Internal matrix pricing is a valuation process internally developed for private placement securities for which the Company is unable to obtain a price from a third-party pricing service. Internal pricing matrices determine credit spreads that, when combined with risk-free rates, are applied to contractual cash flows to develop a price. The Company develops credit spreads using market based data for public securities adjusted for credit spread differentials between public and private securities, which are obtained from a survey of multiple private placement brokers. The market-based reference credit spread considers the issuer’s sector, financial strength, and term to maturity, using an independent public security index, while the credit spread differential considers the non-public nature of the security. Securities priced using internal matrix pricing are classified as Level 2 because the significant inputs are observable or can be corroborated with observable data.

•Independent broker quotes, which are typically non-binding, use inputs that can be difficult to corroborate with observable market-based data. Brokers may use present value techniques using assumptions specific to the security types, or they may use recent transactions of similar securities. Due to the lack of transparency in the process that brokers use to develop prices, valuations that are based on independent broker quotes are classified as Level 3.

The fair value of derivative instruments is determined primarily using a discounted cash flow model or option model technique and incorporates counterparty credit risk. In some cases, quoted market prices for exchange-traded and over-the-counter ("OTC") cleared derivatives may be used and in other cases independent broker quotes may be used. The pricing valuation models primarily use inputs that are observable in the market or can be corroborated by observable market data. The valuation of certain derivatives may include significant inputs that are unobservable, such as volatility levels, and reflect the Company’s view of what other market participants would use when pricing such instruments.

Valuation Controls

The process for determining the fair value of investments is monitored by the Valuation Committee, which is a cross-functional group of senior management within the Company. The purpose of the Valuation Committee is to provide oversight of the pricing policy, procedures, and controls, including approval of valuation methodologies and pricing sources. The Valuation Committee reviews market data trends, pricing statistics and trading statistics to ensure that prices are reasonable and consistent with our fair value framework. Controls and procedures used to assess third-party pricing services are reviewed by the Valuation Committee, including the results of annual due-diligence reviews. Controls include, but are not limited to, reviewing daily and monthly price changes, stale prices, and missing prices and comparing new trade prices to third-party pricing services, weekly price changes to published bond index prices, and daily OTC derivative market valuations to counterparty valuations. The Company has a dedicated pricing group that works with trading and investment professionals to challenge prices received by a third-party pricing source if the Company believes that the valuation received does not accurately reflect the fair value. New valuation models and changes to current models require approval by the Valuation Committee. In addition, the Company’s enterprise-wide Operational Risk Management function provides an independent review of the suitability and reliability of model inputs, as well as an analysis of significant changes to current models.

Valuation Inputs

Quoted prices for identical assets in active markets are considered Level 1 and consist of on-the-run U.S. Treasuries, money market funds, exchange-traded equity securities, open-ended mutual funds, certain short-term investments, and exchange traded derivative instruments.

18

|

Note 4 - Fair Value Measurements | ||||||||

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

| Valuation Inputs Used in Levels 2 and 3 Measurements for Securities and Derivatives | |||||||||||

Level 2 Primary Observable Inputs | Level 3 Primary Unobservable Inputs | ||||||||||

| Fixed Maturity Investments | |||||||||||

| Structured securities (includes ABS, CLO, CMBS and RMBS) | |||||||||||

| • Benchmark yields and spreads • Monthly payment information • Collateral performance, which varies by vintage year and includes delinquency rates, loss severity rates and refinancing assumptions • Credit default swap indices Other inputs for ABS, CLO, and RMBS: • Estimate of future principal prepayments, derived from the characteristics of the underlying structure • Prepayment speeds previously experienced at the interest rate levels projected for the collateral | • Independent broker quotes • Credit spreads beyond observable curve • Interest rates beyond observable curve Other inputs for less liquid securities or those that trade less actively, including subprime RMBS: • Estimated cash flows • Credit spreads, which include illiquidity premium • Constant prepayment rates • Constant default rates • Loss severity | ||||||||||

| Corporates | |||||||||||

• Benchmark yields and spreads • Reported trades, bids, offers of the same or similar securities • Issuer spreads and credit default swap curves Other inputs for investment grade privately placed securities that utilize internal matrix pricing: • Credit spreads for public securities of similar quality, maturity, and sector, adjusted for non-public nature | • Independent broker quotes • Credit spreads beyond observable curve • Interest rates beyond observable curve Other inputs for below investment grade privately placed securities and private bank loans: • Credit spreads for public securities of similar quality, maturity, and sector, adjusted for non-public nature | ||||||||||

| U.S. Treasuries, Municipals, and Foreign government/government agencies | |||||||||||

| • Benchmark yields and spreads • Issuer credit default swap curves • Political events in emerging market economies • Municipal Securities Rulemaking Board reported trades and material event notices • Issuer financial statements | • Credit spreads beyond observable curve • Interest rates beyond observable curve | ||||||||||

| Equity Securities | |||||||||||

| • Quoted prices in markets that are not active | • For privately traded equity securities, internal discounted cash flow models utilizing earnings multiples or other cash flow assumptions that are not observable | ||||||||||

| Short-term Investments | |||||||||||

• Benchmark yields and spreads • Reported trades, bids, offers • Issuer spreads and credit default swap curves • Material event notices and new issue money market rates | • Independent broker quotes • For privately traded investments, credit spreads for public securities of similar quality, maturity, and sector, adjusted for non-public nature | ||||||||||

| Derivatives | |||||||||||

| Credit derivatives | |||||||||||

• Swap yield curve • Credit default swap curves | • Not applicable | ||||||||||

| Foreign exchange derivatives | |||||||||||

• Swap yield curve • Currency spot and forward rates • Cross currency basis curves | • Not applicable | ||||||||||

| Interest rate derivatives | |||||||||||

| • Swap yield curve | • Not applicable | ||||||||||

19

|

Note 4 - Fair Value Measurements | ||||||||

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

| Significant Unobservable Inputs for Level 3 - Securities | |||||||||||||||||||||||

| Assets accounted for at fair value on a recurring basis | Fair Value | Predominant Valuation Technique | Significant Unobservable Input | Minimum | Maximum | Weighted Average [1] | Impact of Increase in Input on Fair Value [2] | ||||||||||||||||

| As of March 31, 2024 | |||||||||||||||||||||||

| CLO [3] | $ | Discounted cash flows | Spread | Decrease | |||||||||||||||||||

| CMBS [3] | $ | Discounted cash flows | Spread (encompasses prepayment, default risk and loss severity) | Decrease | |||||||||||||||||||

| Corporate [4] | $ | Discounted cash flows | Spread | Decrease | |||||||||||||||||||

| RMBS | $ | Discounted cash flows | Spread [6] | Decrease | |||||||||||||||||||

| Constant prepayment rate [6] | Decrease [5] | ||||||||||||||||||||||

| Constant default rate [6] | Decrease | ||||||||||||||||||||||

| Loss severity [6] | Decrease | ||||||||||||||||||||||

| Short-term investments [3] | $ | Discounted cash flows | Spread | Decrease | |||||||||||||||||||

| As of December 31, 2023 | |||||||||||||||||||||||

| CLO [3] | $ | Discounted cash flows | Spread | Decrease | |||||||||||||||||||

| CMBS [3] | $ | Discounted cash flows | Spread (encompasses prepayment, default risk and loss severity) | Decrease | |||||||||||||||||||

| Corporate [4] | $ | Discounted cash flows | Spread | Decrease | |||||||||||||||||||

| RMBS | $ | Discounted cash flows | Spread [6] | Decrease | |||||||||||||||||||

| Constant prepayment rate [6] | Decrease [5] | ||||||||||||||||||||||

| Constant default rate [6] | Decrease | ||||||||||||||||||||||

| Loss severity [6] | Decrease | ||||||||||||||||||||||

| Short-term investments [3] | $ | Discounted cash flows | Spread | Decrease | |||||||||||||||||||

[1]The weighted average is determined based on the fair value of the securities.

[2]Conversely, the impact of a decrease in input would have the opposite impact to the fair value as that presented in the table.

[3]Excludes securities for which the Company bases fair value on broker quotations.

[4]Excludes securities for which the Company bases fair value on broker quotations; however, included are broker priced lower-rated private placement securities for which the Company receives spread and yield information to corroborate the fair value.

[5]Decrease for above market rate coupons and increase for below market rate coupons.

As of March 31, 2024 and December 31, 2023, the fair values of the Company's level 3 derivatives were less than $1

The table above excludes certain securities for which fair values are predominately based on independent broker quotes. While the Company does not have access to the significant unobservable inputs that independent brokers may use in their pricing process, the Company believes brokers likely use inputs similar to those used by the Company and third-party pricing services to price similar instruments. As such, in their pricing models, brokers likely use estimated loss severity rates, prepayment rates, constant default rates and credit spreads. Therefore, similar to non-broker priced securities, increases in these inputs would generally cause fair values to decrease. As of March 31, 2024, no significant adjustments were made by the Company to broker prices received.

Level 3 Assets and Liabilities Measured at Fair Value on a Recurring Basis Using Significant Unobservable Inputs

The Company uses derivative instruments to manage the risk associated with certain assets and liabilities. However, the derivative instrument may not be classified within the same fair value hierarchy level as the associated asset or liability.

20

|

Note 4 - Fair Value Measurements | ||||||||

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

| Fair Value Rollforwards for Financial Instruments Classified as Level 3 for the Three Months Ended March 31, 2024 | ||||||||||||||||||||||||||||||||

| Total realized/unrealized gains (losses) | ||||||||||||||||||||||||||||||||

| Fair value as of January 1, 2024 | Included in net income [1] | Purchases | Settlements | Sales | Transfers into Level 3 [3] | Transfers out of Level 3 [3] | Fair value as of March 31, 2024 | |||||||||||||||||||||||||

| Assets | ||||||||||||||||||||||||||||||||

| Fixed maturities, AFS | ||||||||||||||||||||||||||||||||

| ABS | $ | $ | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||

| CLO | ( | ( | ||||||||||||||||||||||||||||||

| CMBS | ( | |||||||||||||||||||||||||||||||

| Corporate | ( | ( | ( | |||||||||||||||||||||||||||||

| RMBS | ( | |||||||||||||||||||||||||||||||

| Total fixed maturities, AFS | ( | ( | ( | ( | ||||||||||||||||||||||||||||

| FVO securities | ( | |||||||||||||||||||||||||||||||

| Equity securities, at fair value | ||||||||||||||||||||||||||||||||

| Short-term investments | ||||||||||||||||||||||||||||||||

| Total Assets | $ | $ | $ | ( | $ | $ | ( | $ | ( | $ | $ | ( | $ | |||||||||||||||||||

| Fair Value Rollforwards for Financial Instruments Classified as Level 3 for the Three Months Ended March 31, 2023 | ||||||||||||||||||||||||||||||||

| Total realized/unrealized gains (losses) | ||||||||||||||||||||||||||||||||

| Fair value as of January 1, 2023 | Included in net income [1] | Purchases | Settlements | Sales | Transfers into Level 3 [3] | Transfers out of Level 3 [3] | Fair value as of March 31, 2023 | |||||||||||||||||||||||||

| Assets | ||||||||||||||||||||||||||||||||

| Fixed maturities, AFS | ||||||||||||||||||||||||||||||||

| ABS | $ | $ | $ | $ | $ | $ | $ | $ | ( | $ | ||||||||||||||||||||||

| CLO | ( | |||||||||||||||||||||||||||||||

| CMBS | ( | |||||||||||||||||||||||||||||||

| Corporate | ( | ( | ( | |||||||||||||||||||||||||||||

| RMBS | ( | ( | ||||||||||||||||||||||||||||||

| Total fixed maturities, AFS | ( | ( | ( | |||||||||||||||||||||||||||||

| FVO securities | ( | |||||||||||||||||||||||||||||||

| Equity securities, at fair value | ( | ( | ||||||||||||||||||||||||||||||

| Short-term investments | ( | |||||||||||||||||||||||||||||||

| Total Assets | $ | $ | ( | $ | $ | $ | ( | $ | ( | $ | $ | ( | $ | |||||||||||||||||||

[1]Amounts in these columns are generally reported in net realized gains (losses). All amounts are before income taxes.

[2]All amounts are before income taxes.

[3]Transfers into and/or (out of) Level 3 are primarily attributable to the availability of market observable information and the re-evaluation of the observability of pricing inputs.

21

|

Note 4 - Fair Value Measurements | ||||||||

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

| Changes in Unrealized Gains (Losses) for Financial Instruments Classified as Level 3 Still Held at End of Period | ||||||||||||||||||||

| Three Months Ended March 31, | ||||||||||||||||||||

| 2024 | 2023 | 2024 | 2023 | |||||||||||||||||

| Changes in Unrealized Gain/(Loss) included in Net Income [1] [2] | Changes in Unrealized Gain/(Loss) included in OCI [3] | |||||||||||||||||||

| Assets | ||||||||||||||||||||

| Fixed maturities, AFS | ||||||||||||||||||||

| CMBS | $ | $ | $ | $ | ( | |||||||||||||||

| Corporate | ( | |||||||||||||||||||

| Total fixed maturities, AFS | ( | |||||||||||||||||||

| FVO securities | ( | |||||||||||||||||||

| Total Assets | $ | $ | ( | $ | ( | $ | ||||||||||||||

[1]All amounts in these rows are reported in . All amounts are before income taxes.

[2]Amounts presented are for Level 3 only and therefore may not agree to other disclosures included herein.

[3]Changes in unrealized gains (losses) on fixed maturities, AFS are reported in changes in net unrealized gain (loss) on fixed maturities in the Condensed Consolidated Statements of Comprehensive Income.

Fair Value Option

The Company has elected the fair value option for certain investments in residual interests of securitizations and other securities that contain embedded credit derivatives with underlying credit risk related to residential real estate in order to reflect changes in fair value in earnings. These instruments are included within FVO securities on the Condensed Consolidated Balance Sheets and changes in the fair value of these investments are reported in net realized gains and losses.

As of March 31, 2024 and December 31, 2023, the fair value of assets using the fair value option was $292 and $327 , respectively, of which $167

For the three months ended March 31, 2024 and 2023, realized gains (losses) related to the change in fair value of assets using the fair value option were $4 and $(8 ), respectively.

Financial Instruments Not Carried at Fair Value

| Financial Assets and Liabilities Not Carried at Fair Value | |||||||||||||||||||||||

| March 31, 2024 | December 31, 2023 | ||||||||||||||||||||||

| Fair Value Hierarchy Level | Carrying Amount [1] | Fair Value | Fair Value Hierarchy Level | Carrying Amount [1] | Fair Value | ||||||||||||||||||

Assets | |||||||||||||||||||||||

| Mortgage loans | Level 3 | $ | $ | Level 3 | $ | $ | |||||||||||||||||

Liabilities | |||||||||||||||||||||||

| Other policyholder funds and benefits payable | Level 3 | $ | $ | Level 3 | $ | $ | |||||||||||||||||

| Senior notes [2] | Level 2 | $ | $ | Level 2 | $ | $ | |||||||||||||||||

| Junior subordinated debentures [2] | Level 2 | $ | $ | Level 2 | $ | $ | |||||||||||||||||

[1]As of March 31, 2024 and December 31, 2023, the carrying amount of mortgage loans is net of ACL of $48 and $51 , respectively.

[2]Included in long-term debt in the Condensed Consolidated Balance Sheets, except for any current maturities, which are included in short-term debt when applicable.

22

|

Note 5 - Investments | ||||||||

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

5. INVESTMENTS

| Net Realized Gains (Losses) | ||||||||

| Three Months Ended March 31, | ||||||||

| (Before tax) | 2024 | 2023 | ||||||

Gross gains on sales of fixed maturities | $ | $ | ||||||

Gross losses on sales of fixed maturities | ( | ( | ||||||

| Equity securities [1] | ||||||||

| Net realized gains (losses) on sales of equity securities | ( | |||||||

| Change in net unrealized gains (losses) of equity securities | ( | |||||||

| Net realized and unrealized gains (losses) on equity securities | ||||||||

| Net credit losses on fixed maturities, AFS | ( | ( | ||||||

| Change in ACL on mortgage loans | ||||||||

| Other, net [2] | ( | ( | ||||||

| Net realized gains (losses) | $ | $ | ( | |||||

[1]The change in net unrealized gains (losses) on equity securities still held as of the end of the period and included in net realized gains (losses) were $36 and $2 for the three months ended March 31, 2024, and 2023, respectively.

[2]For the three months ended March 31, 2024, and 2023 includes gains (losses) from transactional foreign currency revaluation of $2 and $(7 ), respectively, and gains (losses) on non-qualifying derivatives of $(2 ), and $5 , respectively.

Proceeds from the sales of fixed maturities, AFS totaled $0.4 billion and $1.4 billion for the three months ended March 31, 2024 and 2023, respectively.

Accrued Investment Income on Fixed Maturities, AFS and Mortgage Loans

As of March 31, 2024 and December 31, 2023, the Company reported accrued investment income related to fixed maturities, AFS of $381 and $371 , respectively, and accrued investment income related to mortgage loans of $21 and $20 , respectively. These amounts are not included in the carrying value of the fixed maturities or mortgage loans. Investment income on fixed maturities and mortgage loans is accrued unless it is past due over 90 days or management deems the interest uncollectible. The Company does not include the current accrued investment income balance when estimating the ACL. The Company has a policy to write-off accrued investment income balances that are more than 90 days past due. Write-offs of accrued investment income are recorded as a credit loss component of net realized gains and losses.

Recognition and Presentation of Intent-to-Sell Impairments and ACL on Fixed Maturities, AFS

The Company will record an "intent-to-sell impairment" as a reduction to the amortized cost of fixed maturities, AFS in an unrealized loss position if the Company intends to sell or it is more likely than not that the Company will be required to sell the fixed maturity before a recovery in value. A corresponding charge is recorded in net realized losses equal to the difference between the fair value on the impairment date and the amortized cost basis of the fixed maturity before recognizing the impairment.

Developing the Company’s best estimate of expected future cash flows is a quantitative and qualitative process that incorporates information received from third-party sources along with certain internal assumptions regarding the future performance. The Company's considerations include, but are not limited to, (a) changes in the financial condition of the issuer and/or the underlying collateral, (b) whether the issuer is current on contractually obligated interest and principal payments, (c) credit ratings, (d) payment structure of the security and (e) the extent to which the fair value has been less than the amortized cost of the security.

For non-structured securities, assumptions include, but are not limited to, economic and industry-specific trends and fundamentals, instrument-specific developments including changes in credit ratings, industry earnings multiples and the issuer’s ability to restructure, access capital markets, and execute asset sales.

23

|

Note 5 - Investments | ||||||||

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

For structured securities, assumptions include, but are not limited to, various performance indicators such as historical and projected default and recovery rates, credit ratings, current and projected delinquency rates, loan-to-value ("LTV") ratios, average cumulative collateral loss rates that vary by vintage year, prepayment speeds, and property value declines. These

assumptions require the use of significant management judgment and include the probability of issuer default and estimates regarding timing and amount of expected recoveries which may include estimating the underlying collateral value.

| ACL on Fixed Maturities, AFS by Type | |||||||||||||||||||||||

| Three Months Ended March 31, | |||||||||||||||||||||||

| 2024 | 2023 | ||||||||||||||||||||||

| (Before tax) | Corporate | CMBS | Total | Corporate | CMBS | Total | |||||||||||||||||

| Balance as of beginning of period | $ | $ | $ | $ | $ | $ | |||||||||||||||||

| Credit losses on fixed maturities where an allowance was not previously recorded | |||||||||||||||||||||||

| Net increases (decreases) on fixed maturities where an allowance was previously recorded | |||||||||||||||||||||||

| Write-offs charged against the allowance | ( | ( | |||||||||||||||||||||

| Balance as of end of period | $ | $ | $ | $ | $ | $ | |||||||||||||||||

Fixed Maturities, AFS

| Fixed Maturities, AFS, by Type | |||||||||||||||||||||||||||||||||||

| March 31, 2024 | December 31, 2023 | ||||||||||||||||||||||||||||||||||

Amortized Cost | ACL | Gross Unrealized Gains | Gross Unrealized Losses | Fair Value | Amortized Cost | ACL | Gross Unrealized Gains | Gross Unrealized Losses | Fair Value | ||||||||||||||||||||||||||

| ABS | $ | $ | $ | $ | ( | $ | $ | $ | $ | $ | ( | $ | |||||||||||||||||||||||

| CLO | ( | ( | |||||||||||||||||||||||||||||||||

| CMBS | ( | ( | ( | ( | |||||||||||||||||||||||||||||||

| Corporate | ( | ( | ( | ( | |||||||||||||||||||||||||||||||

| Foreign govt./govt. agencies | ( | ( | |||||||||||||||||||||||||||||||||

| Municipal | ( | ( | |||||||||||||||||||||||||||||||||

| RMBS | ( | ( | |||||||||||||||||||||||||||||||||

| U.S. Treasuries | ( | ( | |||||||||||||||||||||||||||||||||

| Total fixed maturities, AFS | $ | $ | ( | $ | $ | ( | $ | $ | $ | ( | $ | $ | ( | $ | |||||||||||||||||||||

| Fixed Maturities, AFS, by Contractual Maturity Year | |||||||||||||||||

| March 31, 2024 | December 31, 2023 | ||||||||||||||||

| Amortized Cost | Fair Value | Amortized Cost | Fair Value | ||||||||||||||

| One year or less | $ | $ | $ | $ | |||||||||||||

| Over one year through five years | |||||||||||||||||

| Over five years through ten years | |||||||||||||||||

| Over ten years | |||||||||||||||||

| Subtotal | |||||||||||||||||

| Mortgage-backed and asset-backed securities | |||||||||||||||||

| Total fixed maturities, AFS | $ | $ | $ | $ | |||||||||||||

24

|

Note 5 - Investments | ||||||||

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

Estimated maturities may differ from contractual maturities due to call or prepayment provisions. Due to the potential for variability in payment speeds (i.e., prepayments or extensions), mortgage-backed and asset-backed securities are not categorized by contractual maturity.

Concentration of Credit Risk

The Company aims to maintain a diversified investment portfolio including issuer, sector and geographic stratification, where

applicable, and has established certain exposure limits, diversification standards and review procedures to mitigate credit risk. The Company had no

Unrealized Losses on Fixed Maturities, AFS

| Unrealized Loss Aging for Fixed Maturities, AFS by Type and Length of Time as of March 31, 2024 | ||||||||||||||||||||||||||

| Less Than 12 Months | 12 Months or More | Total | ||||||||||||||||||||||||

| Fair Value | Unrealized Losses | Fair Value | Unrealized Losses | Fair Value | Unrealized Losses | |||||||||||||||||||||

| ABS | $ | $ | ( | $ | $ | ( | $ | $ | ( | |||||||||||||||||

| CLO | ( | ( | ( | |||||||||||||||||||||||

| CMBS | ( | ( | ( | |||||||||||||||||||||||

| Corporate | ( | ( | ( | |||||||||||||||||||||||

| Foreign govt./govt. agencies | ( | ( | ( | |||||||||||||||||||||||

| Municipal | ( | ( | ( | |||||||||||||||||||||||

| RMBS | ( | ( | ( | |||||||||||||||||||||||

| U.S. Treasuries | ( | ( | ( | |||||||||||||||||||||||

| Total fixed maturities, AFS in an unrealized loss position | $ | $ | ( | $ | $ | ( | $ | $ | ( | |||||||||||||||||

| Unrealized Loss Aging for Fixed Maturities, AFS by Type and Length of Time as of December 31, 2023 | ||||||||||||||||||||||||||

| Less Than 12 Months | 12 Months or More | Total | ||||||||||||||||||||||||

| Fair Value | Unrealized Losses | Fair Value | Unrealized Losses | Fair Value | Unrealized Losses | |||||||||||||||||||||

| ABS | $ | $ | ( | $ | $ | ( | $ | $ | ( | |||||||||||||||||

| CLO | ( | ( | ( | |||||||||||||||||||||||

| CMBS | ( | ( | ( | |||||||||||||||||||||||

| Corporate | ( | ( | ( | |||||||||||||||||||||||

| Foreign govt./govt. agencies | ( | ( | ||||||||||||||||||||||||

| Municipal | ( | ( | ( | |||||||||||||||||||||||

| RMBS | ( | ( | ( | |||||||||||||||||||||||

| U.S. Treasuries | ( | ( | ( | |||||||||||||||||||||||

| Total fixed maturities, AFS in an unrealized loss position | $ | $ | ( | $ | $ | ( | $ | $ | ( | |||||||||||||||||

As of March 31, 2024, fixed maturities, AFS in an unrealized loss position consisted of 4,002 instruments and were primarily depressed due to higher interest rates and/or wider credit spreads since the purchase date. As of March 31, 2024, 95 % of these fixed maturities were depressed less than 20% of cost or amortized cost. The increase in unrealized losses during the three months ended March 31, 2024, was primarily attributable to higher interest rates, partially offset by tighter credit spreads.

Most of the fixed maturities depressed for twelve months or more relate to the corporate sector, RMBS, municipal bonds, and CMBS which were primarily depressed because current rates are higher and/or market spreads are wider than at the

respective purchase dates. The Company neither has an intention to sell nor does it expect to be required to sell the fixed maturities outlined in the preceding discussion. The decision to record credit losses on fixed maturities, AFS in the form of an ACL requires us to make qualitative and quantitative estimates of expected future cash flows.

Mortgage Loans

ACL on Mortgage Loans

The Company reviews mortgage loans on a quarterly basis to estimate the ACL with changes in the ACL recorded in net

25

|

Note 5 - Investments | ||||||||

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

realized gains and losses. Apart from an ACL recorded on individual mortgage loans where the borrower is experiencing financial difficulties, the Company records an ACL on the pool of mortgage loans based on lifetime expected credit losses. The Company utilizes a third-party forecasting model to estimate lifetime expected credit losses at a loan level under multiple economic scenarios. The scenarios use macroeconomic data provided by an internationally recognized economics firm that generates forecasts of varying economic factors such as GDP growth, unemployment and interest rates. The economic scenarios are projected over 10 years. The first two to four years of the 10-year period assume a specific modeled economic scenario (including moderate upside, moderate recession and severe recession scenarios) and then revert to historical long-term assumptions over the remaining period. Using these economic scenarios, the forecasting model projects property-specific operating income and capitalization rates used to estimate the value of a future operating income stream. The operating income and the property valuations derived from capitalization rates are compared to loan payment and principal amounts to create debt service coverage ratios ("DSCRs") and LTVs over the forecast period. The Company's process also considers qualitative factors. The model overlays historical data about mortgage loan performance based on DSCRs and LTVs and projects the probability of default, amount of loss given a default and resulting expected loss through maturity for each loan under each economic scenario. Economic scenarios are probability-weighted based on a statistical analysis of the forecasted economic factors and qualitative analysis. The Company records the change in the ACL on mortgage loans based on the weighted-average expected credit losses across the selected economic scenarios.

When a borrower is experiencing financial difficulty, including when foreclosure is probable, the Company measures an ACL on individual mortgage loans. The ACL is established for any shortfall between the amortized cost of the loan and the fair value of the collateral less costs to sell. Estimates of collectibility from an individual borrower require the use of significant management judgment and include the probability and timing of borrower default and loss severity estimates. In addition, cash

flow projections may change based upon new information about the borrower's ability to pay and/or the value of underlying collateral such as changes in projected property value estimates. As of March 31, 2024, the Company did no t have any mortgage loans for which an ACL was established on an individual basis.

There were no no

| ACL on Mortgage Loans | ||||||||

| Three Months Ended March 31, | ||||||||

| 2024 | 2023 | |||||||

| ACL as of beginning of period | $ | $ | ||||||

| Current period provision (release) | ( | |||||||

| ACL as of December 31, | $ | $ | ||||||

The release in the allowance for the three months ended March 31, 2024 is primarily attributable to improved economic scenario forecasts and property specific reductions, partially offset by net additions of new loans.

The weighted-average LTV ratio of the Company’s mortgage loan portfolio was 55 % as of March 31, 2024, while the weighted-average LTV ratio at origination of these loans was 59 %. LTV ratios compare the loan amount to the value of the underlying property collateralizing the loan with property values based on appraisals updated no less than annually. Factors considered in estimating property values include, among other things, actual and expected property cash flows, geographic market data and the ratio of the property's net operating income to its value. DSCR compares a property’s net operating income to the borrower’s principal and interest payments and are updated no less than annually through reviews of underlying properties.

| Mortgage Loans LTV & DSCR by Origination Year as of March 31, 2024 | ||||||||||||||||||||||||||||||||||||||||||||

| 2024 | 2023 | 2022 | 2021 | 2020 | 2019 & Prior | Total | ||||||||||||||||||||||||||||||||||||||

| Loan-to-value | Amortized Cost | Avg. DSCR | Amortized Cost | Avg. DSCR | Amortized Cost | Avg. DSCR | Amortized Cost | Avg. DSCR | Amortized Cost | Avg. DSCR | Amortized Cost | Avg. DSCR | Amortized Cost [1] | Avg. DSCR | ||||||||||||||||||||||||||||||

| Greater than 80% | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||

| 65% - 80% | ||||||||||||||||||||||||||||||||||||||||||||

| Less than 65% | ||||||||||||||||||||||||||||||||||||||||||||

Total mortgage loans | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||

[1]Amortized cost of mortgage loans excludes ACL of $48 .

26

|

Note 5 - Investments | ||||||||

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

| Mortgage Loans LTV & DSCR by Origination Year as of December 31, 2023 | ||||||||||||||||||||||||||||||||||||||||||||

| 2023 | 2022 | 2021 | 2020 | 2019 | 2018 & Prior | Total | ||||||||||||||||||||||||||||||||||||||

| Loan-to-value | Amortized Cost | Avg. DSCR | Amortized Cost | Avg. DSCR | Amortized Cost | Avg. DSCR | Amortized Cost | Avg. DSCR | Amortized Cost | Avg. DSCR | Amortized Cost | Avg. DSCR | Amortized Cost [1] | Avg. DSCR | ||||||||||||||||||||||||||||||

| Greater than 80% | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||

| 65% - 80% | ||||||||||||||||||||||||||||||||||||||||||||

| Less than 65% | ||||||||||||||||||||||||||||||||||||||||||||

Total mortgage loans | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||

[1]Amortized cost of mortgage loans excludes ACL of $51 .

| Mortgage Loans by Region | |||||||||||||||||

| March 31, 2024 | December 31, 2023 | ||||||||||||||||

| Amortized Cost | Percent of Total | Amortized Cost | Percent of Total | ||||||||||||||

| East North Central | $ | % | $ | % | |||||||||||||

| Middle Atlantic | % | % | |||||||||||||||

| Mountain | % | % | |||||||||||||||

| New England | % | % | |||||||||||||||

| Pacific | % | % | |||||||||||||||

| South Atlantic | % | % | |||||||||||||||

| West North Central | % | % | |||||||||||||||

| West South Central | % | % | |||||||||||||||

| Other [1] | % | % | |||||||||||||||

| Total mortgage loans | % | % | |||||||||||||||

| ACL | ( | ( | |||||||||||||||

| Total mortgage loans, net of ACL | $ | $ | |||||||||||||||

[1]Primarily represents loans collateralized by multiple properties in various regions.

| Mortgage Loans by Property Type | |||||||||||||||||

| March 31, 2024 | December 31, 2023 | ||||||||||||||||

| Amortized Cost | Percent of Total | Amortized Cost | Percent of Total | ||||||||||||||

| Commercial | |||||||||||||||||

| Industrial | $ | % | $ | % | |||||||||||||

| Multifamily | % | % | |||||||||||||||

| Office | % | % | |||||||||||||||

| Retail [1] | % | % | |||||||||||||||

| Single Family | % | % | |||||||||||||||

| Total mortgage loans | % | % | |||||||||||||||

| ACL | ( | ( | |||||||||||||||

| Total mortgage loans, net of ACL | $ | $ | |||||||||||||||

[1]Primarily comprised of grocery-anchored retail centers, with no exposure to regional shopping malls.

Past-Due Mortgage Loans

Mortgage loans are considered past due if a payment of principal or interest is not received according to the contractual terms of the loan agreement, which typically includes a grace period. As of March 31, 2024 and December 31, 2023, the Company held no

27

|

Note 5 - Investments | ||||||||

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

Mortgage Servicing