Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended December 31, 2010

-OR-

| ¨ | TRANSITION REPORT FILED PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

COMMISSION FILE NUMBER 1-12291

The AES Corporation

(Exact name of registrant as specified in its charter)

| Delaware |

54 1163725 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| 4300 Wilson Boulevard Arlington, Virginia |

22203 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (703) 522-1315

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class |

Name of Each Exchange on Which Registered | |

| Common Stock, par value $0.01 per share | New York Stock Exchange | |

| AES Trust III, $3.375 Trust Convertible Preferred Securities | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15 (d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer x |

Accelerated filer ¨ | Non-accelerated filer ¨ | Smaller reporting company ¨ | |||

| (Do not check if a smaller reporting company) |

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the voting and non-voting common equity held by non-affiliates on June 30, 2010, the last business day of the Registrant’s most recently completed second fiscal quarter (based on the closing sale price of $9.24 of the Registrant’s Common Stock, as reported by the New York Stock Exchange on such date) was approximately $7.350 billion.

The number of shares outstanding of the Registrant’s Common Stock, par value $0.01 per share, on February 23, 2011, was 788,253,071.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of Registrant’s Proxy Statement for its 2011 annual meeting of stockholders are incorporated by reference in Parts II and III

Table of Contents

THE AES CORPORATION

FISCAL YEAR 2010 FORM 10-K

| 1 | ||||

| 3 | ||||

| 3 | ||||

| 6 | ||||

| 19 | ||||

| 19 | ||||

| 19 | ||||

| 20 | ||||

| 21 | ||||

| 73 | ||||

| 97 | ||||

| 97 | ||||

| 107 | ||||

| 108 | ||||

| 108 | ||||

| 108 | ||||

| Purchases of Equity Securities by the Issuer and Affiliated Purchasers |

108 | |||

| 109 | ||||

| 110 | ||||

| 110 | ||||

| 111 | ||||

| ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

113 | |||

| 113 | ||||

| 117 | ||||

| 120 | ||||

| 129 | ||||

| 149 | ||||

| 153 | ||||

| 154 | ||||

| 164 | ||||

| ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK |

165 | |||

| 168 | ||||

| ITEM 9. CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE |

277 | |||

| 277 | ||||

| 280 | ||||

| 280 | ||||

| ITEM 10. DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE |

280 | |||

| 280 | ||||

| 280 | ||||

| ITEM 13. CERTAIN RELATIONSHIPS AND RELATED PARTY TRANSACTIONS AND DIRECTOR INDEPENDENCE |

282 | |||

| 282 | ||||

| 283 | ||||

| 283 | ||||

| 288 |

Table of Contents

In this Annual Report the terms “AES,” “the Company,” “us,” or “we” refer to The AES Corporation and all of its subsidiaries and affiliates, collectively. The term “The AES Corporation” and “Parent Company” refers only to the parent, publicly-held holding company, The AES Corporation, excluding its subsidiaries and affiliates.

FORWARD-LOOKING INFORMATION

In this filing we make statements concerning our expectations, beliefs, plans, objectives, goals, strategies, and future events or performance. Such statements are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Although we believe that these forward-looking statements and the underlying assumptions are reasonable, we cannot assure you that they will prove to be correct.

Forward-looking statements involve a number of risks and uncertainties, and there are factors that could cause actual results to differ materially from those expressed or implied in our forward-looking statements. Some of those factors (in addition to others described elsewhere in this report and in subsequent securities filings) include:

| • | the economic climate, particularly the state of the economy in the areas in which we operate, including the fact that the global economy faces considerable uncertainty for the foreseeable future, which further increases many of the risks discussed in this Form 10-K; |

| • | changes in inflation, demand for power, interest rates and foreign currency exchange rates, including our ability to hedge our interest rate and foreign currency risk; |

| • | changes in the price of electricity at which our Generation businesses sell into the wholesale market and our Utility businesses purchase to distribute to their customers, and the success of our risk management practices, such as our ability to hedge our exposure to such market price risk; |

| • | changes in the prices and availability of coal, gas and other fuels (including our ability to have fuel transported to our facilities) and the success of our risk management practices, such as our ability to hedge our exposure to such market price risk, and our ability to meet credit support requirements for fuel and power supply contracts; |

| • | changes in and access to the financial markets, particularly changes affecting the availability and cost of capital in order to refinance existing debt and finance capital expenditures, acquisitions, investments and other corporate purposes; |

| • | our ability to manage liquidity and comply with covenants under our recourse and non-recourse debt, including our ability to manage our significant liquidity needs and to comply with covenants under our senior secured credit facility and other existing financing obligations; |

| • | changes in our or any of our subsidiaries’ corporate credit ratings or the ratings of our or any of our subsidiaries’ debt securities or preferred stock, and changes in the rating agencies’ ratings criteria; |

| • | our ability to purchase and sell assets at attractive prices and on other attractive terms; |

| • | our ability to compete in markets where we do business; |

| • | our ability to manage our operation and maintenance costs; |

| • | the performance and reliability of our generating plants, including our ability to reduce unscheduled down-times; |

| • | our ability to locate and acquire attractive “greenfield” projects and our ability to finance, construct and begin operating our “greenfield” projects on schedule and within budget; |

1

Table of Contents

| • | our ability to enter into long-term contracts, which limit volatility in our results of operations and cash flow, such as power purchase agreements, fuel supply, and other agreements and to manage counterparty credit risks in these agreements; |

| • | variations in weather, especially mild winters and cooler summers in the areas in which we operate, low levels of wind or sunlight for our wind and solar businesses, and the occurrence of difficult hydrological conditions for our hydro-power plants, as well as hurricanes and other storms and disasters; |

| • | our ability to meet our expectations in the development, construction, operation and performance of our wind businesses, which rely, in part, on actual wind conditions and wind turbine performance being in line with our expectations; |

| • | the success of our initiatives in other renewable energy projects, as well as greenhouse gas emissions reduction projects and energy storage projects; |

| • | our ability to keep up with advances in technology; |

| • | the potential effects of threatened or actual acts of terrorism and war; |

| • | the expropriation or nationalization of our businesses or assets by foreign governments, whether with or without adequate compensation; |

| • | our ability to achieve expected rate increases in our Utility businesses; |

| • | changes in laws, rules and regulations affecting our international businesses; |

| • | changes in laws, rules and regulations affecting our North America business, including, but not limited to, deregulation of wholesale power markets and its effects on competition, the ability to recover net utility assets and other potential stranded costs by our utilities, the establishment of a regional transmission organization that includes our utility service territory, the application of market power criteria by the Federal Energy Regulatory Commission, changes in law resulting from new federal energy legislation, including the effects of the repeal of Public Utility Holding Company Act of 1935, and changes in political or regulatory oversight or incentives affecting our wind business, our solar joint venture, our other renewables projects and our initiatives in greenhouse gas reductions and energy storage including tax incentives; |

| • | changes in environmental laws, including requirements for reduced emissions of sulfur, nitrogen, carbon, mercury, coal ash, hazardous air pollutants and other substances, including potential greenhouse gas legislation, regulation and/or treaties; |

| • | changes in tax laws and the effects of our strategies to reduce tax payments; |

| • | the effects of litigation and government and regulatory investigations; |

| • | our ability to maintain adequate insurance; |

| • | decreases in the value of pension plan assets, increases in pension plan expenses and our ability to fund defined benefit pension and other post-retirement plans at our subsidiaries; |

| • | losses on the sale or write-down of assets due to impairment events or changes in management intent with regard to either holding or selling certain assets; |

| • | changes in accounting standards, corporate governance and securities law requirements; |

| • | our ability to maintain effective internal controls over financial reporting; and |

| • | our ability to attract and retain talented directors, management and other personnel, including, but not limited to, financial personnel in our foreign businesses that have extensive knowledge of accounting principles generally accepted in the United States. |

2

Table of Contents

These factors in addition to others described elsewhere in this Form 10-K, including those described under Item 1A.—Risk Factors, and in subsequent securities filings, should not be construed as a comprehensive listing of factors that could cause results to vary from our forward looking information.

We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise. If one or more forward-looking statements are updated, no inference should be drawn that additional updates will be made with respect to those or other forward-looking statements.

| ITEM 1. | BUSINESS |

We are a global power company. We own a portfolio of electricity generation and distribution businesses on five continents in 28 countries, with total capacity of approximately 40,500 Megawatts (“MW”) and distribution networks serving over 12 million people as of December 31, 2010. In addition, we have more than 2,000 MW under construction in six countries. Our global workforce of approximately 29,000 people helps provide electricity to people in diverse markets ranging from urban centers in the United States to remote villages in India. We were incorporated in Delaware in 1981 and for three decades we have been committed to providing safe and reliable energy.

We own and operate two primary types of businesses. The first is our Generation business, where we own and/or operate power plants to generate and sell power to wholesale customers such as utilities and other intermediaries. The second is our Utilities business, where we own and/or operate utilities to distribute, transmit and sell electricity to end-user customers in the residential, commercial, industrial and governmental sectors within a defined service area.

Our assets are diverse with respect to fuel source and type of market, which helps reduce certain types of operating risk. Our portfolio employs a broad range of fuels, including coal, gas, fuel oil, biomass and renewable sources such as hydroelectric power, wind and solar, which reduces the risks associated with dependence on any one fuel source. Our presence in mature markets helps reduce the volatility associated with our businesses in faster-growing emerging markets. In addition, our Generation portfolio is largely contracted, which reduces the risk related to market prices of electricity and fuel. We also attempt to limit risk by hedging some of our interest rate and commodity risk, and by matching the currency of most of our subsidiary debt to the revenue of the underlying business. However, our business is still subject to these and other risks, which are further described in Item 1A.—Risk Factors of this Form 10-K.

Our goal is to maximize value for our shareholders through continued focus on increasing the profitability of our existing portfolio and increasing cash flow while managing our risk and employing rigorous capital allocation. We will continue to seek prudent expansion of our traditional Generation and Utilities lines of business, along with expansion of wind, solar and energy storage, through acquisitions or greenfield developments. Portfolio management remains an area of focus through which we have sold and expect to continue to sell or monetize a portion of certain businesses or assets when market values appear attractive. Furthermore, we will continue to focus on improving our business operations and management processes, including our internal controls over financial reporting.

Key Lines of Business

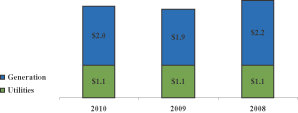

AES’ primary sources of revenue and gross margin today are from Generation and Utilities. These businesses are distinguished by the nature of the customers, operational differences, cost structure, regulatory environment and risk exposure. The breakout of revenue and gross margin between Generation and Utilities for the years ended December 31, 2010, 2009 and 2008, respectively, is shown below. Operating results for integrated utilities, which have both Generation and Utilities, are reflected in the Utilities amounts below.

3

Table of Contents

Revenue

($ in billions)

Gross Margin

($ in billions)

| (1) | Utilities gross margin includes the margin from generation businesses owned by the Company and from whom the utility purchases energy. |

Generation

We currently own or operate a generation portfolio of approximately 34,100 MW, excluding the generation capabilities of our integrated utilities, consisting of 100 Generation facilities in 25 countries on five continents at our generation businesses. We also have approximately 1,700 MW of capacity currently under construction in four countries. We are a major power source in many countries, such as Panama where we are the largest generator of electricity, and Chile, where AES Gener (“Gener”) is the second largest electricity generation company in terms of capacity. Our Generation business uses a wide range of technologies and fuel types including coal, combined-cycle gas turbines, hydroelectric power and biomass. Generation revenue was $7.5 billion, $6.1 billion and $7.4 billion for the years ended December 31, 2010, 2009 and 2008, respectively.

Performance drivers for our Generation businesses include, among other factors, plant reliability, fuel costs, power prices, volume and fixed-cost management. Growth in the Generation business is largely tied to securing new power purchase agreements (“PPAs”), expanding capacity in our existing facilities and building or acquiring new power plants.

4

Table of Contents

The majority of the electricity produced by our Generation businesses is sold under long-term PPAs, to wholesale customers. In 2010, approximately 64% of the revenue from our Generation business was from plants that operate under PPAs of three years or longer for 75% or more of their output capacity. These businesses often reduce their exposure to fuel supply risks by entering into long-term fuel supply contracts or fuel tolling arrangements where the customer assumes full responsibility for purchasing and supplying the fuel to the power plant. These long-term contractual agreements help reduce the volatility of our cash flows and earnings and also reduce exposure to volatility in the market price for electricity and fuel; however, the amount of earnings and cash flow predictability varies from business to business based on the degree to which its exposure is limited by the contracts it has negotiated.

Our Generation businesses with long-term contracts face most of their competition from other utilities and independent power producers (“IPPs”) prior to the execution of a power sales agreement during the development phase of a project or upon expiration of an existing agreement. Once a project is operational, we traditionally have faced limited competition due to the long-term nature of the generation contracts. However, as our existing contracts expire, the introduction of new power markets has increased competition to attract new customers and maintain our current customer base.

The balance of our Generation business sells power through competitive markets under short-term contracts, directly in the spot market or, in some cases, at regulated prices. As a result, the cash flows and earnings associated with these businesses are more sensitive to fluctuations in the market price for electricity, natural gas, coal and other fuels. Competitive factors for these facilities include price, reliability, operational cost and third-party credit requirements.

Utilities

AES utility businesses distribute power to over 12 million people in seven countries on five continents and consist primarily of 14 companies owned or operated under management agreements, each of which operate in defined service areas. These businesses also include 15 generation plants in two countries with generation capacity totaling approximately 4,600 MW. These businesses have a variety of structures ranging from pure distribution businesses to fully integrated utilities, which generate, transmit and distribute power. For instance, our wholly owned subsidiary in the U.S., Indianapolis Power & Light (“IPL”), has the exclusive right to provide retail services to approximately 470,000 customers in Indianapolis, Indiana. Eletropaulo Metropolitana Electricidad de São Paulo S.A (“AES Eletropaulo” or “Eletropaulo”), serving the São Paulo metropolitan region for over 100 years, has approximately six million customers and is the largest electricity distribution company in Brazil in terms of revenue and electricity distributed. In Cameroon, we are the primary generator and distributor of electricity and in El Salvador we provide distribution services to serve more than 77% of the country’s electricity customers. Utilities revenue was $9.1 billion, $7.8 billion and $7.8 billion for the years ended December 31, 2010, 2009 and 2008, respectively.

Performance drivers for Utilities include, but are not limited to, reliability of service, management of working capital, negotiation of tariff adjustments, compliance with extensive regulatory requirements, and in developing countries, reduction of commercial and technical losses. The results of operations of our Utilities businesses are sensitive to changes in economic growth, regulations and variations in weather conditions in the areas in which they operate.

Utilities face relatively little direct competition due to significant barriers to entry which are present in these markets. In certain locations, our distribution businesses face increased competition as a result of changes in laws and regulations which allow wholesale and retail services to be provided on a competitive basis. Competition is a factor in efforts to acquire existing businesses. In this arena, we compete against a number of other market participants, some of which have greater financial resources, have been engaged in distribution related businesses for longer periods of time and/or have accumulated more significant portfolios. Relevant competitive factors for our power distribution businesses include financial resources, governmental assistance, regulatory restrictions and access to non-recourse financing.

5

Table of Contents

Renewables and Other Initiatives

In recent years, as demand for renewable sources of energy has grown, we have placed increasing emphasis on developing projects in wind, solar and other renewable initiatives including energy storage. In 2005, we started a wind generation business (“AES Wind Generation”), which currently has 20 plants in operation in five countries totaling approximately 1,800 MW in generation capacity and is one of the largest producers of wind power in the U.S. In addition, 264 MW are under construction in four countries. In March 2008, we formed AES Solar Energy LLC (“AES Solar”), a joint venture with Riverstone Holdings, LLC (“Riverstone”), a private equity firm, which has since commenced commercial operations of nine plants totaling 37 MW of solar projects in France, Greece and Spain. We have a few projects producing GHG credits in Asia, Europe and Latin America. We also have a line of business to develop and implement utility scale energy storage systems (such as batteries), which store and release power when needed. While none of these initiatives are currently material to our operations, we believe that as these businesses grow, they may become a material contributor to our operations. However, there are risks associated with these initiatives, which are further described in Item 1A.—Risk Factors of this Form 10-K. As further described in “Our Organization and Segments” below, some of these projects are managed within the region in which they are located, while others are managed as separate business units and reported as set forth below.

Risks

We routinely encounter and address risks, some of which may cause our future results to be different, sometimes materially different, than we presently anticipate. The categories of risk we have identified in Item 1A.—Risk Factors of this Form 10-K include the following:

| • | risks associated with our disclosure controls and internal controls over financial reporting; |

| • | risks related to our high level of indebtedness; |

| • | risks associated with our ability to raise needed capital; |

| • | external risks associated with revenue and earnings volatility; |

| • | risks associated with our operations; and |

| • | risks associated with governmental regulation and laws. |

The categories of risk identified above are discussed in greater detail in Item 1A.—Risk Factors of this Form 10-K. These risk factors should be read in conjunction with Item 7.—Management’s Discussion and Analysis of Financial Condition and Results of Operations, and the Consolidated Financial Statements and related notes included elsewhere in this report.

We believe our broad geographic footprint allows us to focus development in targeted markets with opportunities for new investment, and provides stability through our presence in more developed regions. In addition, our presence in each region affords us important relationships and helps us identify local markets with attractive opportunities for new investment. As a result, we have structured our organization into geographic regions, and each region is led by a regional president or other senior executive responsible for managing those businesses. The regional presidents report to our Chief Operating Officer (“COO”), who in turn reports to our Chief Executive Officer (“CEO”). Both our CEO and COO are based in Arlington, Virginia.

The Company’s segment reporting structure is organized along our two lines of business (Generation and Utilities) and three regions: (1) Latin America & Africa; (2) North America; and (3) Europe, Middle East & Asia (collectively, “EMEA”), which reflects how we manage the business internally. Additionally, AES Wind Generation is managed within our North America region. For financial reporting purposes, the Company has six reportable segments which include:

| • | Latin America—Generation; |

| • | Latin America—Utilities; |

6

Table of Contents

| • | North America—Generation; |

| • | North America—Utilities; |

| • | Europe—Generation; |

| • | Asia—Generation. |

Corporate and Other—The Company’s Europe Utilities, Africa Utilities, Africa Generation and AES Wind Generation businesses as well as the Company’s renewables initiatives are reported within “Corporate and Other” because they do not require separate disclosure under segment reporting accounting guidance. See Item 7.—Management’s Discussion and Analysis of Financial Condition and Results of Operations for further discussion of the Company’s segment structure used for financial reporting purposes.

The following describes our businesses as they are aligned in our segment reporting structure for financial reporting purposes.

Latin America

Our Latin America operations accounted for 69%, 70% and 68% of consolidated AES revenue in 2010, 2009 and 2008, respectively. The following table provides highlights of our Latin America operations:

| Countries |

Argentina, Brazil, Chile, Colombia, Dominican Republic, El Salvador and Panama | |

| Generation Capacity |

11,907 Gross MW | |

| Utilities Penetration |

8.6 million customers (49,280 Gigawatt Hours (“GWh”)) | |

| Generation Facilities |

55 (including 3 under construction) | |

| Utilities Businesses |

8 | |

| Key Generation Businesses |

Gener, Tietê and Alicura | |

| Key Utilities Businesses |

Eletropaulo and Sul |

The graph below shows the breakdown between our Latin America Generation and Utilities segments as a percentage of total Latin America revenue and gross margin for the years ended December 31, 2010, 2009, and 2008. See Note 15—Segment and Geographic Information in the Consolidated Financial Statements in Item 8 of this Form 10-K for information on revenue from external customers, Adjusted Gross Margin (a non-GAAP measure) and total assets by segment.

| Revenue ($ in billions)

|

Gross Margin ($ in billions)

|

Latin America Generation. Our largest generation business in Latin America, AES Tietê (“Tietê”), located in Brazil, represents approximately 18% of the total generation capacity in the state of São Paulo and is the tenth largest generator in Brazil. AES holds a 24% economic interest in Tietê. In Argentina, we are the third largest

7

Table of Contents

private power generator contributing 11% of the country’s total power generation capacity. In Chile, we are the second largest generator of power. We currently have three new generation plants under construction—two coal plants in Chile and one hydro plant in Panama with a combined generation capacity of 1,011 MW.

Set forth below is a list of our Latin America Generation facilities:

Generation

| Business |

Location | Fuel | Gross MW |

AES Equity Interest (Percent, Rounded) |

Year Acquired or Began Operation |

|||||||||||

| Alicura |

Argentina | Hydro | 1,050 | 99 | % | 2000 | ||||||||||

| Central Dique |

Argentina | Gas/Diesel | 68 | 51 | % | 1998 | ||||||||||

| Gener—TermoAndes |

Argentina | Gas/Diesel | 643 | 71 | % | 2000 | ||||||||||

| Los Caracoles(1) |

Argentina | Hydro | 125 | 0 | % | 2009 | ||||||||||

| Paraná-GT |

Argentina | Gas/Diesel | 845 | 99 | % | 2001 | ||||||||||

| Quebrada de Ullum(1) |

Argentina | Hydro | 45 | 0 | % | 2004 | ||||||||||

| Rio Juramento—Cabra Corral |

Argentina | Hydro | 102 | 99 | % | 1995 | ||||||||||

| Rio Juramento—El Tunal |

Argentina | Hydro | 10 | 99 | % | 1995 | ||||||||||

| San Juan—Sarmiento |

Argentina | Gas/Diesel | 33 | 99 | % | 1996 | ||||||||||

| San Juan—Ullum |

Argentina | Hydro | 45 | 99 | % | 1996 | ||||||||||

| San Nicolás |

Argentina | Coal/Gas/Oil | 675 | 99 | % | 1993 | ||||||||||

| Tietê(2) |

Brazil | Hydro | 2,657 | 24 | % | 1999 | ||||||||||

| Uruguaiana |

Brazil | Gas | 639 | 46 | % | 2000 | ||||||||||

| Gener—Electrica Santiago(3) |

Chile | Gas/Diesel | 479 | 64 | % | 2000 | ||||||||||

| Gener—Electrica Ventanas(4) |

Chile | Coal | 272 | 71 | % | 2010 | ||||||||||

| Gener—Energía Verde(5) |

Chile | Biomass/Diesel | 49 | 71 | % | 2000 | ||||||||||

| Gener—Gener(6) |

Chile | Hydro/Coal/Diesel | 953 | 71 | % | 2000 | ||||||||||

| Gener—Guacolda(7),(8) |

Chile | Coal/Pet Coke | 608 | 35 | % | 2000 | ||||||||||

| Gener—Norgener |

Chile | Coal/Pet Coke | 277 | 71 | % | 2000 | ||||||||||

| Chivor |

Colombia | Hydro | 1,000 | 71 | % | 2000 | ||||||||||

| Andres |

Dominican Republic | Gas | 319 | 100 | % | 2003 | ||||||||||

|

Itabo(9) |

Dominican Republic | Coal | 295 | 50 | % | 2000 | ||||||||||

| Los Mina |

Dominican Republic | Gas | 236 | 100 | % | 1996 | ||||||||||

| Bayano |

Panama | Hydro | 260 | 49 | % | 1999 | ||||||||||

| Chiriqui—Esti |

Panama | Hydro | 120 | 49 | % | 2003 | ||||||||||

| Chiriqui—La Estrella |

Panama | Hydro | 48 | 49 | % | 1999 | ||||||||||

| Chiriqui—Los Valles |

Panama | Hydro | 54 | 49 | % | 1999 | ||||||||||

| 11,907 | ||||||||||||||||

| (1) | AES operates these facilities through management or operations and maintenance (“O&M”) agreements and owns no equity interest in these businesses. |

| (2) | Tietê plants: Água Vermelha, Bariri, Barra Bonita, Caconde, Euclides da Cunha, Ibitinga, Limoeiro, Mog-Guaçu, Nova Avanhandava, Promissão and seven other small hydroelectric plants below Tietê’s wholly-owned subsidiary “PCH Minas Ltda”. |

| (3) | Gener—Electrica Santiago plants: Nueva Renca and Renca. |

| (4) | Gener—Electrica Ventanas plant: Nueva Ventanas. |

| (5) | Gener—Energia Verde Plants: Constitución, Laja and San Francisco de Mostazal. |

| (6) | Gener—Gener plants: Alfalfal, Laguna Verde, Laguna Verde Turbogas, Los Vientos, Maitenas, Queltehues, Santa Lidia, Ventanas and Volcán. |

| (7) | Gener—Guacolda plants: Guacolda 1, Guacolda 2, Guacolda 3 and Guacolda 4. |

| (8) | Unconsolidated entities, the results of operations of which are reflected in Equity in Earnings of Affiliates. |

| (9) | Itabo plants: Itabo complex (two coal-fired steam turbines and one gas-fired steam turbine). |

8

Table of Contents

Generation under construction

| Business |

Location |

Fuel |

Gross MW |

AES Equity Interest (Percent, Rounded) |

Expected Year of Commercial Operations |

|||||||||||

| Angamos |

Chile | Coal | 518 | 71 | % | 2011 | ||||||||||

| Campiche |

Chile | Coal | 270 | 71 | % | 2013 | ||||||||||

| Changuinola I |

Panama | Hydro | 223 | 100 | % | 2011 | ||||||||||

| 1,011 | ||||||||||||||||

Latin America Utilities. Each of our Utilities businesses in Latin America sells electricity under regulated tariff agreements and has transmission and distribution capabilities but none of them has generation capability. AES Eletropaulo, a consolidated subsidiary of which AES owns a 16% economic interest and which has served the São Paulo, Brazil area for over 100 years, has approximately six million customers and is the largest electricity distribution company in Brazil in terms of revenue and electricity distributed. Pursuant to its concession agreement, AES Eletropaulo is entitled to distribute electricity in its service area until 2028. AES Eletropaulo’s service territory consists of 24 municipalities in the greater São Paulo metropolitan area and adjacent regions that account for approximately 17% of Brazil’s GDP and 40% of the population in the State of São Paulo. AES Sul (“Sul”), a wholly-owned subsidiary, serves over one million customers. In El Salvador, our Utilities businesses provide electricity to over 81% of the country, serving more than one million customers.

Set forth below is a list of our Latin America Utilities facilities:

Distribution

| Business |

Location | Approximate Number of Customers Served as of 12/31/2010 |

GWh Sold in 2010 |

AES Equity Interest (Percent, Rounded) |

Year Acquired |

|||||||||||||||

| Edelap |

Argentina | 329,000 | 2,776 | 90 | % | 1998 | ||||||||||||||

| Edes |

Argentina | 172,000 | 894 | 90 | % | 1997 | ||||||||||||||

| Eletropaulo |

Brazil | 5,832,000 | 33,860 | 16 | % | 1998 | ||||||||||||||

| Sul |

Brazil | 1,181,474 | 8,320 | 100 | % | 1997 | ||||||||||||||

| CAESS |

El Salvador | 516,000 | 2,060 | 75 | % | 2000 | ||||||||||||||

| CLESA |

El Salvador | 304,000 | 786 | 64 | % | 1998 | ||||||||||||||

| DEUSEM |

El Salvador | 62,000 | 108 | 74 | % | 2000 | ||||||||||||||

| EEO |

El Salvador | 229,000 | 476 | 89 | % | 2000 | ||||||||||||||

| 8,625,474 | 49,280 | |||||||||||||||||||

North America

Our North America operations accounted for 19%, 22% and 22% of consolidated revenue in 2010, 2009 and 2008, respectively. The following table provides highlights of our North America operations:

| Countries |

U.S., Puerto Rico and Mexico | |

| Generation Capacity |

13,396 Gross MW | |

| Utilities Penetration |

470,000 customers (16,537 GWh) | |

| Generation Facilities |

19 | |

| Utilities Businesses |

1 integrated utility (includes 4 generation plants) | |

| Key Generation Businesses |

Eastern Energy, Southland and TEG/TEP | |

| Key Utilities Business |

IPL |

9

Table of Contents

The graph below shows the breakdown between our North America Generation and Utilities segments as a percentage of total North America revenue and gross margin for the years ended December 31, 2010, 2009 and 2008. See Note 15—Segment and Geographic Information in the Consolidated Financial Statements in Item 8 of this Form 10-K for information on revenue from external customers, Adjusted Gross Margin (a non-GAAP measure) and total assets by segment.

| Revenue ($ in billions) |

Gross Margin ($ in millions) | |

|

|

North America Generation. Approximately 86% of the generation capacity is supported by long-term power purchase or tolling agreements. Our North America Generation business consists of six gas-fired, ten coal-fired and three petroleum coke-fired plants in the United States, Puerto Rico and Mexico.

Our largest generation business is AES Southland. This business operates three gas-fired plants, representing generation capacity of 4,327 MW, in the Los Angeles basin under a long-term tolling agreement. In addition, in the Western New York power market, AES Eastern Energy operates four of our coal-fired plants, Cayuga, Greenidge, Somerset and Westover, representing generation capacity of 1,169 MW, providing power to this market under short-term contracts, as well as in the spot electricity market.

10

Table of Contents

Set forth below is a list of our North America Generation facilities:

Generation

| Business |

Location | Fuel | Gross MW |

AES Equity Ownership (Percent, Rounded) |

Year Acquired or Began Operation |

|||||||||||

| Mérida III |

Mexico | Gas | 484 | 55 | % | 2000 | ||||||||||

| Termoelectrica del Golfo (TEG) |

Mexico | Pet Coke | 230 | 99 | % | 2007 | ||||||||||

| Termoelectrica del Peñoles (TEP) |

Mexico | Pet Coke | 230 | 99 | % | 2007 | ||||||||||

| Southland—Alamitos |

USA—CA | Gas | 2,047 | 100 | % | 1998 | ||||||||||

| Southland—Huntington Beach |

USA—CA | Gas | 904 | 100 | % | 1998 | ||||||||||

| Southland—Redondo Beach |

USA—CA | Gas | 1,376 | 100 | % | 1998 | ||||||||||

| Thames |

USA—CT | Coal | 208 | 100 | % | 1990 | ||||||||||

| Hawaii |

USA—HI | Coal | 203 | 100 | % | 1992 | ||||||||||

| Warrior Run |

USA—MD | Coal | 205 | 100 | % | 2000 | ||||||||||

| Red Oak |

USA—NJ | Gas | 832 | 100 | % | 2002 | ||||||||||

| Cayuga |

USA—NY | Coal | 306 | 100 | % | 1999 | ||||||||||

| Greenidge |

USA—NY | Coal | 106 | 100 | % | 1999 | ||||||||||

| Somerset |

USA—NY | Coal | 675 | 100 | % | 1999 | ||||||||||

| Westover |

USA—NY | Coal | 82 | 100 | % | 1999 | ||||||||||

| Shady Point |

USA—OK | Coal | 360 | 100 | % | 1991 | ||||||||||

| Beaver Valley |

USA—PA | Coal | 125 | 100 | % | 1985 | ||||||||||

| Ironwood |

USA—PA | Gas | 710 | 100 | % | 2001 | ||||||||||

| Puerto Rico |

USA—PR | Coal | 454 | 100 | % | 2002 | ||||||||||

| Deepwater |

USA—TX | Pet Coke | 160 | 100 | % | 1986 | ||||||||||

| 9,697 | ||||||||||||||||

North America Utilities. AES has one integrated utility in North America, IPL, which it owns through IPALCO Enterprises Inc. (“IPALCO”), the parent holding company of IPL. IPL generates, transmits, distributes and sells electricity to approximately 470,000 customers in the city of Indianapolis and neighboring areas within the state of Indiana. IPL owns and operates four generation facilities that provide more than 96% of the electricity it distributes. Two of the generation facilities are coal-fired plants. The third facility has a combination of units that use coal (base load capacity) and natural gas and/or oil (peaking capacity). The fourth facility is a small peaking station that uses gas-fired combustion turbine technology. IPL’s gross generation capacity is 3,699 MW. Approximately 45% of IPL’s coal is provided by one supplier with which IPL has long-term contracts. A key driver for the business is tariff recovery for environmental projects through the rate adjustment process. IPL’s customers include residential, industrial, commercial and all other which made up 37%, 40%, 15% and 8%, respectively, of North America Utilities revenue for 2010.

IPL’s generation facilities

| Business |

Location | Fuel | Gross MW |

AES Equity Interest (Percent, Rounded) |

Year Acquired or Began Operation |

|||||||||

|

IPL(1) |

USA—IN | Coal/Gas/Oil | 3,699 | 100 | % | 2001 | ||||||||

| (1) | IPL plants: Eagle Valley, Georgetown, Harding Street and Petersburg. |

11

Table of Contents

Distribution

| Business |

Location | Approximate Number of Customers Served as of 12/31/2010 |

GWh Sold in 2010 |

AES Equity Interest (Percent, Rounded) |

Year Acquired |

|||||||||||||

| IPL |

USA—IN | 470,000 | 16,537 | 100 | % | 2001 | ||||||||||||

Europe

The following table provides highlights of our Europe operations:

| Countries |

Czech Republic, Hungary, Jordan, Kazakhstan, Netherlands, Spain, Turkey, Ukraine and the United Kingdom | |

| Generation Capacity |

7,986 Gross MW | |

| Utilities Penetration |

1.8 million customers (9,904 GWh) | |

| Generation Facilities |

21 (including 3 under construction) | |

| Utilities Businesses |

4 | |

| Key Generation Businesses |

Ballylumford, Cartagena, Kilroot, Tisza II | |

| Key Utilities Businesses |

Kievoblenergo and Rivneenergo |

Our Utilities operations in Europe are discussed further under Corporate and Other below.

Europe Generation. Our Generation operations in Europe accounted for 8%, 6% and 8% of our consolidated revenue in 2010, 2009 and 2008, respectively. In 2007, we began commercial operation of AES Cartagena (“Cartagena”), our first power plant in Spain, with capacity of 1,199 MW. As a result of the new accounting guidance for variable interest entities, the Company consolidated Cartagena effective January 1, 2010. In prior periods, the results of operations for Cartagena were included in the Equity in Earnings of Affiliates line item on the Consolidated Statements of Operations. Today, AES operates four power plants in Kazakhstan which account for 8% of the country’s total installed generation capacity. In September 2009, AES completed construction and launched commercial operation of the 380 MW combined-cycle Amman East power plant in Jordan. See Note 15—Segment and Geographic Information in the Consolidated Financial Statements in Item 8 of this Form 10-K for revenue, Adjusted Gross Margin (a non-GAAP measure) and total assets by segment. Key business drivers of this segment are: foreign currency exchange rates, new legislation and regulations including those related to the environment.

12

Table of Contents

Set forth below is a list of our Europe Generation facilities:

Generation

| Business |

Location | Fuel | Gross MW |

AES Equity Interest (Percent, Rounded) |

Year Acquired or Began Operation |

|||||||||||||||

| Bohemia |

Czech Republic | Coal/Biomass | 50 | 100 | % | 2001 | ||||||||||||||

| Borsod |

Hungary | Biomass/Coal | 71 | 100 | % | 1996 | ||||||||||||||

| Tisza II |

Hungary | Gas/Oil | 900 | 100 | % | 1996 | ||||||||||||||

| Tiszapalkonya |

Hungary | Coal/Biomass | 90 | 100 | % | 1996 | ||||||||||||||

| Amman East |

Jordan | Gas | 380 | 37 | % | 2008 | ||||||||||||||

| Shulbinsk HPP(1) |

Kazakhstan | Hydro | 702 | 0 | % | 1997 | ||||||||||||||

| Sogrinsk CHP |

Kazakhstan | Coal | 301 | 100 | % | 1997 | ||||||||||||||

| Ust—Kamenogorsk HPP(1) |

Kazakhstan | Hydro | 331 | 0 | % | 1997 | ||||||||||||||

| Ust—Kamenogorsk CHP |

Kazakhstan | Coal | 1,354 | 100 | % | 1997 | ||||||||||||||

|

Elsta(2) |

Netherlands | Gas | 630 | 50 | % | 1998 | ||||||||||||||

| Cartagena |

Spain | Gas | 1,199 | 71 | % | 2006 | ||||||||||||||

| Damlapinar(2)(3) |

Turkey | Hydro | 16 | 51 | % | 2010 | ||||||||||||||

| Girlevik II-Mercan(2) |

Turkey | Hydro | 12 | 51 | % | 2007 | ||||||||||||||

| Kepezkaya(2)(3) |

Turkey | Hydro | 28 | 51 | % | 2010 | ||||||||||||||

| Yukari-Mercan(2) |

Turkey | Hydro | 14 | 51 | % | 2007 | ||||||||||||||

| Ballylumford |

United Kingdom | Natural Gas | 1,246 | 100 | % | 2010 | ||||||||||||||

| Kilroot(4) |

United Kingdom | Coal/Gas/Oil | 662 | 99 | % | 1992 | ||||||||||||||

| 7,986 | ||||||||||||||||||||

| (1) | AES operates these facilities under concession agreements until 2017. |

| (2) | Unconsolidated entities, the results of operations of which are reflected in Equity in Earnings of Affiliates. |

| (3) | Joint Venture with I.C. Energy. |

| (4) | Includes Kilroot Open Cycle Gas Turbine (“OCGT”). |

Generation under construction

| Business |

Location | Fuel | Gross MW |

AES Equity Interest (Percent, Rounded) |

Expected Year of Commercial Operation |

|||||||||||||||

| Maritza East(1) |

Bulgaria | Coal | 670 | 100 | % | 2011 | ||||||||||||||

| Kumkoy(2) |

Turkey | Hydro | 18 | 51 | % | 2011 | ||||||||||||||

| Niksar(2) |

Turkey | Hydro | 40 | 51 | % | 2011 | ||||||||||||||

| 728 | ||||||||||||||||||||

| (1) | Construction of the Maritza East facility is currently on hold. For further discussion please see Item 7.—Management’s Discussion and Analysis—Key Trends and Uncertainties and Item 1A.—Risk Factors, “Our business is subject to substantial development uncertainties.” |

| (2) | Joint Venture with I.C. Energy. The joint venture is an unconsolidated entity, the results of operations of which are reflected in Equity in Earnings of Affiliates. |

13

Table of Contents

Asia

Our Asia operations accounted for 4%, 3% and 2% of consolidated revenue in 2010, 2009 and 2008, respectively. Asia’s Generation business operates 9 power plants with a total capacity of 4,103 MW in four countries. In Asia, AES operates generation facilities only. See Note 15—Segment and Geographic Information in the Consolidated Financial Statements in Item 8 of this Form 10-K for revenue, Adjusted Gross Margin (a non-GAAP measure) and total assets by segment. The following table provides highlights of our Asia operations:

| Countries |

China, India, the Philippines and Sri Lanka | |

| Generation Capacity |

4,103 Gross MW | |

| Utilities Penetration |

None | |

| Generation Facilities |

9 | |

| Utilities Businesses |

None | |

| Key Businesses |

Yangcheng and Masinloc |

Asia Generation. In 2010, the Company closed the sales of our businesses in Oman, Pakistan and Qatar. See Note 21—Discontinued Operations and Held for Sale Businesses in Item 8 of this Form 10-K for further information on these sales. More than half of our remaining generation capacity in Asia is located in China. In 1996, AES joined with Chinese partners to build Yangcheng, the first “coal-by-wire” power plant with the generation capacity of 2,100 MW. In April 2008, the Company completed the purchase of a 92% interest in a 660 MW coal-fired thermal power generation facility in Masinloc, Philippines (“Masinloc”).

Set forth below is a list of our generation facilities in Asia:

Generation

| Business |

Location | Fuel | Gross MW |

AES Equity Interest (Percent, Rounded) |

Year Acquired or Began Operation |

|||||||||||||||

| Aixi |

China | Coal | 51 | 71 | % | 1998 | ||||||||||||||

| Chengdu(1) |

China | Gas | 50 | 35 | % | 1997 | ||||||||||||||

| Cili |

China | Hydro | 25 | 51 | % | 1994 | ||||||||||||||

|

JHRH(1) |

China | Hydro | 379 | 35 | % | 2010 | ||||||||||||||

|

Wuhu(1),(2) |

China | Coal | 250 | 25 | % | 1996 | ||||||||||||||

| Yangcheng(1) |

China | Coal | 2,100 | 25 | % | 2001 | ||||||||||||||

|

OPGC(1) |

India | Coal | 420 | 49 | % | 1998 | ||||||||||||||

| Masinloc |

Philippines | Coal | 660 | 92 | % | 2008 | ||||||||||||||

| Kelanitissa |

Sri Lanka | Diesel | 168 | 90 | % | 2003 | ||||||||||||||

| 4,103 | ||||||||||||||||||||

| (1) | Unconsolidated entities, the results of operations of which are reflected in Equity in Earnings of Affiliates. |

| (2) | AES agreed to sell its 25% equity interest in this business on August 11, 2010. The disposal was approved by the government authority on December 6, 2010. |

Corporate and Other

“Corporate and Other” includes the net operating results from our Utilities businesses in Africa and Europe, Africa Generation and AES Wind Generation and other renewables projects. These operations do not require separate segment disclosure. The following provides additional details about our Utilities businesses in Africa and Europe, Africa generation and AES Wind Generation, which are reported within “Corporate and Other” for financial reporting purposes.

14

Table of Contents

Europe Utilities. Our distribution businesses in the Ukraine and Kazakhstan together serve approximately 1.8 million customers.

Distribution

| Business |

Location | Approximate Number of Customers Served as of 12/31/2010 |

GWh Sold in 2010 |

AES Equity Interest (Percent, Rounded) |

Year Acquired |

|||||||||||||||

| Eastern Kazakhstan REC(1)(2) |

Kazakhstan | 459,000 | 3,444 | 0 | % | |||||||||||||||

| Ust-Kamenogorsk Heat Nets(1)(3) |

Kazakhstan | 96,000 | — | 0 | % | |||||||||||||||

| Kievoblenergo |

Ukraine | 861,828 | 4,557 | 89 | % | 2001 | ||||||||||||||

| Rivneenergo |

Ukraine | 405,934 | 1,903 | 84 | % | 2001 | ||||||||||||||

| 1,822,762 | 9,904 | |||||||||||||||||||

| (1) | AES operates these businesses through management agreements and owns no equity interest in these businesses. |

| (2) | Shygys Energo Trade, a retail electricity company, is 100% owned by Eastern Kazakhstan REC (“EK REC”) and purchases distribution service from EK REC and electricity in the wholesale electricity market and resells to the distribution customers of EK REC. |

| (3) | Ust-Kamenogorsk Heat Nets provide transmission and distribution of heat with a total heat generating capacity of 224 Gcal. |

Africa Utilities. AES owns a 56% interest in an integrated utility, Société Nationale d’Electricité (“Sonel”). Sonel generates, transmits and distributes electricity to over half a million people and is the sole distributor of electricity in Cameroon.

Set forth below is a list of the generation and distribution facilities of Sonel:

Sonel’s generation facilities

| Business |

Location | Fuel | Gross MW |

AES Equity Interest (Percent, Rounded) |

Year Acquired or Began Operation |

|||||||||||||||

|

Sonel(1) |

Cameroon | Hydro/ Diesel/Heavy Fuel Oil | 936 | 56 | % | 2001 | ||||||||||||||

| (1) | Sonel plants: Bafoussam, Bassa, Djamboutou, Edéa, Lagdo, Limbé, Logbaba I, Logbaba II, Oyomabang I, Oyomabang II, Song Loulou, and other small remote network units. |

Sonel’s distribution facility

| Business |

Location | Approximate Number of Customers Served as of 12/31/2010 |

GWh Sold in 2010 |

AES Equity Interest (Percent, Rounded) |

Year Acquired |

|||||||||||||

| Sonel |

Cameroon | 660,484 | 3,345 | 56 | % | 2001 | ||||||||||||

15

Table of Contents

Africa Generation. Set forth below is a list of our generation facilities in Africa.

Generation

| Business |

Location | Fuel | Gross MW |

AES Equity Interest (Percent, Rounded) |

Year Acquired or Began Operation |

|||||||||||||||

| Dibamba |

Cameroon | Heavy Fuel Oil | 86 | 56 | % | 2009 | ||||||||||||||

| Ebute |

Nigeria | Gas | 294 | 95 | % | 2001 | ||||||||||||||

| 380 | ||||||||||||||||||||

Wind Generation. We own and operate 1,538 MW of wind generation capacity and operate an additional 215 MW of capacity through operating and management agreements. Our wind business is located primarily in North America where we operate wind generation facilities that have generation capacity of 1,269 MW.

Set forth below is a list of AES Wind Generation facilities:

Generation

| Business |

Location | Power Source |

Gross MW |

AES Equity Interest (Percent, Rounded) |

Year Acquired or Began Operation |

|||||||||||||||

| St. Nikola |

Bulgaria | Wind | 156 | 89 | % | 2010 | ||||||||||||||

| Dong Qi(1),(3) |

China | Wind | 49 | 49 | % | 2010 | ||||||||||||||

| Huanghua I(1),(3) |

China | Wind | 49 | 49 | % | 2009 | ||||||||||||||

| Huanghua II(1),(3) |

China | Wind | 49 | 49 | % | 2010 | ||||||||||||||

| Hulunbeier(1),(3) |

China | Wind | 49 | 49 | % | 2008 | ||||||||||||||

| InnoVent(2),(3) |

France | Wind | 75 | 40 | % | 2003-2009 | ||||||||||||||

| St. Patrick |

France | Wind | 35 | 100 | % | 2010 | ||||||||||||||

| North Rhins |

Scotland | Wind | 22 | 100 | % | 2010 | ||||||||||||||

| Altamont |

USA—CA | Wind | 40 | 100 | % | 2005 | ||||||||||||||

| Mountain View I & II(4) |

USA—CA | Wind | 67 | 100 | % | 2008 | ||||||||||||||

| Palm Springs |

USA—CA | Wind | 30 | 100 | % | 2005 | ||||||||||||||

| Tehachapi |

USA—CA | Wind | 58 | 100 | % | 2007 | ||||||||||||||

| Storm Lake II(4) |

USA—IA | Wind | 78 | 100 | % | 2007 | ||||||||||||||

| Lake Benton I(4) |

USA—MN | Wind | 106 | 100 | % | 2007 | ||||||||||||||

| Condon(4) |

USA—OR | Wind | 50 | 100 | % | 2005 | ||||||||||||||

| Armenia Mountain(4) |

USA—PA | Wind | 101 | 100 | % | 2009 | ||||||||||||||

| Buffalo Gap I(4) |

USA—TX | Wind | 121 | 100 | % | 2006 | ||||||||||||||

| Buffalo Gap II(4) |

USA—TX | Wind | 233 | 100 | % | 2007 | ||||||||||||||

| Buffalo Gap III(4) |

USA—TX | Wind | 170 | 100 | % | 2008 | ||||||||||||||

| Wind generation facilities(5) |

USA | Wind | 215 | 0 | % | 2005 | ||||||||||||||

| 1,753 | ||||||||||||||||||||

| (1) | Joint Venture with Guohua Energy Investment Co. Ltd. |

| (2) | InnoVent plants: Bignan, Chepy, Croixrault-Moyencourt, Frenouville, Gapree, Grand Fougeray, Guehenno, Hargicourt, Hescamps, LePortal, Les Diagots, Nibas, Plechatel, Saint-Hilaire la Croix and Valhoun. InnoVent owns various percentages of underlying projects. |

| (3) | Unconsolidated entities, the results of operations of which are reflected in Equity in Earnings of Affiliates. |

16

Table of Contents

| (4) | AES owns these assets together with third party tax equity investors with variable ownership interests. The tax equity investors receive a portion of the economic attributes of the facilities, including tax attributes that vary over the life of the projects. The proceeds from the issuance of tax equity are recorded as Noncontrolling Interest in the Company’s Consolidated Balance Sheets. |

| (5) | AES operates these facilities through management or O&M agreements and owns no equity interest in these businesses. |

AES Wind Generation projects under construction

| Business |

Location | Power Source |

Gross MW |

AES Equity Interest (Percent, Rounded) |

Expected Year of Commercial Operation |

|||||||||||||||

| Chen Qi(1) |

China | Wind | 49 | 49 | % | 2011 | ||||||||||||||

| InnoVent(2) |

France | Wind | 29 | 40 | % | 2011 | ||||||||||||||

| Saurashtra |

India | Wind | 39 | 100 | % | 2011 | ||||||||||||||

| Mountain View IV |

US-CA | Wind | 49 | 100 | % | 2011 | ||||||||||||||

| Laurel Mountain |

US-WV | Wind | 98 | 100 | % | 2011 | ||||||||||||||

| 264 | ||||||||||||||||||||

| (1) | Joint Venture with Guohua Energy Investment Co. Ltd. |

| (2) | InnoVent plants: Allery, Audrieu, Lamballe, Lefaux and Vron. InnoVent owns various percentages of underlying projects. |

Other. AES Solar and certain other unconsolidated businesses are accounted for using the equity method of accounting. Therefore, their operating results are included in “Net Equity in Earnings of Affiliates” on the face of the Consolidated Statements of Operations, not in revenue and gross margin. AES Solar was formed in March 2008 to develop, own and operate solar installations. Since its launch, AES Solar has commenced commercial operations of 37 MW of solar projects in France, Greece and Spain, has 75 MW under construction in Italy, and has development potential in Bulgaria, India and the U.S.

“Corporate and Other” also includes general and administrative expenses related to corporate staff functions and initiatives, executive management, business development, finance, legal, human resources and information systems which are not allocable to our business segments and the effects of eliminating transactions, such as self insurance charges, between the operating segments and corporate. See Note 15—Segment and Geographic Information in the Consolidated Financial Statements in Item 8 of this Form 10-K for information on revenue from external customers, Adjusted Gross Margin (a non-GAAP measure) and total assets by segment.

17

Table of Contents

Financial Data by Country

The table below presents information, by country, about our consolidated operations for each of the three years ended December 31, 2010, 2009 and 2008, respectively, and property, plant and equipment as of December 31, 2010 and 2009, respectively. Revenue is recognized in the country in which it is earned and assets are reflected in the country in which they are located.

| Revenue | Property, Plant & Equipment, net | |||||||||||||||||||

| 2010 | 2009 | 2008 | 2010 | 2009 | ||||||||||||||||

| (in millions) | ||||||||||||||||||||

| United States |

$ | 2,615 | $ | 2,545 | $ | 2,745 | $ | 6,167 | $ | 7,016 | ||||||||||

| Non-U.S.: |

||||||||||||||||||||

| Brazil |

6,473 | 5,394 | 5,501 | 6,413 | 5,799 | |||||||||||||||

| Chile |

1,355 | 1,239 | 1,349 | 2,560 | 2,321 | |||||||||||||||

| Argentina |

887 | 684 | 949 | 459 | 448 | |||||||||||||||

| El Salvador |

648 | 619 | 484 | 261 | 254 | |||||||||||||||

| Dominican Republic |

535 | 429 | 601 | 625 | 634 | |||||||||||||||

| Philippines(1) |

501 | 250 | 148 | 784 | 765 | |||||||||||||||

| Cameroon |

422 | 370 | 379 | 823 | 742 | |||||||||||||||

|

Spain(2) |

411 | — | — | 667 | — | |||||||||||||||

| Mexico |

409 | 329 | 463 | 786 | 802 | |||||||||||||||

| Colombia |

393 | 347 | 291 | 387 | 390 | |||||||||||||||

| United Kingdom |

385 | 241 | 342 | 527 | 433 | |||||||||||||||

| Ukraine |

356 | 286 | 403 | 86 | 80 | |||||||||||||||

| Hungary |

296 | 317 | 466 | 80 | 196 | |||||||||||||||

| Puerto Rico |

253 | 267 | 251 | 596 | 609 | |||||||||||||||

| Panama |

194 | 168 | 210 | 921 | 834 | |||||||||||||||

| Kazakhstan |

138 | 123 | 234 | 63 | 48 | |||||||||||||||

| Jordan |

120 | 104 | 47 | 224 | 231 | |||||||||||||||

| Sri Lanka |

100 | 109 | 184 | 69 | 74 | |||||||||||||||

| Bulgaria(3) |

44 | — | — | 1,825 | 1,835 | |||||||||||||||

|

Qatar(4) |

— | — | — | — | — | |||||||||||||||

| Pakistan(5) |

— | — | — | — | — | |||||||||||||||

|

Oman(6) |

— | — | — | — | — | |||||||||||||||

| Other Non-U.S. |

112 | 133 | 150 | 298 | 285 | |||||||||||||||

| Total Non-U.S. |

14,032 | 11,409 | 12,452 | 18,454 | 16,780 | |||||||||||||||

| Total |

$ | 16,647 | $ | 13,954 | $ | 15,197 | $ | 24,621 | $ | 23,796 | ||||||||||

| (1) | Masinloc was acquired in April 2008; 2008 revenue represents results for a partial year. |

| (2) | Cartagena was consolidated effective January 1, 2010 upon implementation of the variable interest entity accounting guidance. |

| (3) | Maritza East and our wind project in Bulgaria were under development and therefore not operational as of December 31, 2009. Our wind project in Bulgaria started operations in 2010. |

| (4) | Excludes revenue of $129 million, $163 million and $161 million for the years ended December 31, 2010, 2009 and 2008, respectively, and property, plant and equipment of $501 million as of December 31, 2009 related to Ras Laffan, which was reflected as discontinued operations and businesses held for sale in the accompanying Consolidated Statements of Operations and Consolidated Balance Sheets. |

| (5) | Excludes revenue of $299 million, $470 million and $607 million for the years ended December 31, 2010, 2009 and 2008, respectively, and property, plant and equipment of $36 million as of December 31, 2009 related to Lal Pir and Pak Gen, which were reflected as discontinued operations and businesses held for sale in the accompanying Consolidated Statements of Operations and Consolidated Balance Sheets. |

18

Table of Contents

| (6) | Excludes revenue of $62 million, $101 million and $105 million for the years ended December 31, 2010, 2009 and 2008, respectively, and property, plant and equipment of $311 million as of December 31, 2009, related to Barka, which was reflected as discontinued operations and businesses held for sale in the accompanying Consolidated Statements of Operations and Consolidated Balance Sheets. |

We sell to a wide variety of customers. No individual customer accounted for 10% or more of our 2010 total revenue. In our generation business, we own and/or operate power plants to generate and sell power to wholesale customers such as utilities and other intermediaries. Our utilities sell to end-user customers in the residential, commercial, industrial and governmental sectors in a defined service area.

As of December 31, 2010, we employed approximately 29,000 people.

The following individuals are our executive officers:

Paul Hanrahan, 53 years old, has been the President, CEO and a member of our Board of Directors since 2002. Prior to assuming his current position, Mr. Hanrahan was the Executive Vice President and COO. In this role, he was responsible for managing all aspects of business development activities and the operation of multiple electric utilities and generation facilities in Europe, Asia and Latin America. Mr. Hanrahan was previously the President and CEO of the AES China Generating Company, Ltd., a public company formerly listed on NASDAQ. Mr. Hanrahan also has managed other AES businesses in the United States, Europe and Asia. In March 2006, he was elected to the board of directors of Corn Products International, Inc. Prior to joining AES, Mr. Hanrahan served as a line officer on the U.S. fast attack nuclear submarine, USS Parche (SSN-683). Mr. Hanrahan is a graduate of Harvard Business School and the U.S. Naval Academy.

Andres R. Gluski, 53 years old, has been an Executive Vice President and COO of the Company since March 2007. Prior to becoming the COO of AES, Mr. Gluski was Executive Vice President and the Regional President of Latin America from 2006 to 2007. Mr. Gluski was Senior Vice President for the Caribbean and Central America from 2003 to 2006, CEO of La Electricidad de Caracas (“EDC”) from 2002 to 2003 and CEO of AES Gener (Chile) in 2001. Prior to joining AES in 2000, Mr. Gluski was Executive Vice President and CFO of EDC, Executive Vice President of Banco de Venezuela (Grupo Santander), Vice President for Santander Investment, and Executive Vice President and CFO of CANTV (subsidiary of GTE). Mr. Gluski has also worked with the International Monetary Fund in the Treasury and Latin American Departments and served as Director General of the Ministry of Finance of Venezuela. Mr. Gluski currently serves on the Board of Directors of Cliffs Natural Resources, The Council of Americas, US Spain Business Council and The Edison Electric Institute and is Chairman of AES Gener and AES Brasiliana. Mr. Gluski is a graduate of Wake Forest University and holds an M.A and a Ph.D in Economics from the University of Virginia.

Ned Hall, 51 years old, has been an Executive Vice President, Regional President for North America and Chairman, Global Wind Generation and Energy Storage since June 2008. In August of 2009, Mr. Hall joined the Board of AES Solar Energy, Ltd., a joint venture between AES and Riverstone Holdings LLC. Prior to his current position, Mr. Hall was Vice President of the Company and President, Global Wind Generation from April 2005 to June 2008, Managing Director of AES Global Development from September 2003 to April 2005, and was an AES Group Manager from April 2001 to September 2003. Mr. Hall joined AES in 1988 as a Project Manager working in the Development Group and has held a variety of development and operating roles for AES, including assignments in the U.S., Europe, Asia and Latin America. He is a registered professional engineer in the Commonwealth of Massachusetts. Mr. Hall holds a BSME degree from Tufts University and an MBA degree in finance/operations management from the MIT Sloan School of Management.

19

Table of Contents

Victoria D. Harker, 46 years old, has been an Executive Vice President and CFO since January 2006. Prior to joining the Company, Ms. Harker held the positions of Acting CFO, Senior Vice President and Treasurer of MCI from November 2002 to January 2006. Prior to that, Ms. Harker served as CFO of MCI Group, a unit of WorldCom Inc., from 1998 to 2002. Prior to 1998, Ms. Harker held several positions at MCI in the areas of finance, information technology and operations. In November of 2009, she was elected to the board of directors of Darden Restaurants, Inc. She has also been a member of the University of Virginia Board of Managers since 2007 and the board of the Wolf Trap Foundation for the Performing Arts since 2009. Ms. Harker received a Bachelor of Arts degree in English and Economics from the University of Virginia and a Masters in Business Administration, Finance from American University.

Brian A. Miller, 45 years old, is an Executive Vice President of the Company, General Counsel, and Corporate Secretary. Since November of 2010, Mr. Miller has also served as the co-head of the Company’s Development Steering Committee. Mr. Miller joined the Company in 2001 and has served in various positions including Vice President, Deputy General Counsel, Corporate Secretary, General Counsel for North America and Assistant General Counsel. In March of 2008, Mr. Miller joined the Board of AES Solar Energy, Ltd., a joint venture between AES and Riverstone Holdings LLC. In 2009, he joined the board of AgCert International Limited and AgCert Canada Holding Limited. Prior to joining AES, he was an attorney with the law firm Chadbourne & Parke, LLP. Mr. Miller received a bachelor’s degree in History and Economics from Boston College and holds a Juris Doctorate from the University of Connecticut School of Law.

Richard Santoroski, 46 years old, became an Executive Vice President in February 2010 and has led the Company’s Global Risk & Commodity Organization since February 2008. Since November of 2010, he has also served as co-head of the Company’s Development Steering Committee. Prior to his current position, Mr. Santoroski was Vice President, Energy & Natural Resources, a business development group, and Vice President, Risk Management. Mr. Santoroski joined AES in January 1999 to lead AES Eastern Energy’s commodity management. Prior to AES, Mr. Santoroski held various engineering, trading and risk management positions at New York State Electric & Gas, including leading the energy trading group. He graduated from Pennsylvania State University with a Bachelor of Science in Electrical Engineering, and earned an MBA and a Master of Science in Electrical Engineering from Syracuse University. Mr. Santoroski is a Licensed Professional Engineer in the State of New York.

Andrew Vesey, 55 years old, is Executive Vice President and Regional President of Latin America and Africa. He has held that position since April 2009. Prior to this, Mr. Vesey was Executive Vice President and Regional President for Latin America from March 2008 through March 2009 and Chief Operating Officer for Latin America from July 2007 through February 2008. Mr. Vesey also served as Vice President and Group Manager for AES Latin America, DR-CAFTA Region from 2006 to 2007, Vice President of the Global Business Transformation Group from 2005 to 2006, and Vice President of the Integrated Utilities Development Group from 2004 to 2005. Prior to joining the Company in 2004, Mr. Vesey was a Managing Director of the Utility Finance and Regulatory Advisory Practice at FTI Consulting Inc., a partner in the Energy, Chemicals and Utilities Practice of Ernst & Young LLP, and CEO and Managing Director of Citipower Pty of Melbourne, Australia. He received his BA in Economics and BS in Mechanical Engineering from Union College in Schenectady, New York and his MS from New York University.

How to Contact AES and Sources of Other Information

Our principal offices are located at 4300 Wilson Boulevard, Arlington, Virginia 22203. Our telephone number is (703) 522-1315. Our website address is http://www.aes.com. Our annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K and any amendments to such reports filed pursuant to Section 13(a) or Section 15(d) of the Securities Exchange Act of 1934 (the “Exchange Act”) are posted on our website. After the reports are filed with, or furnished to, the Securities and Exchange Commission (“SEC”), they are available from us free of charge. Material contained on our website is not part of and is not incorporated by reference in this Form 10-K. You may also read and copy any materials we file with the SEC at

20

Table of Contents

the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. You may obtain information about the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an internet website that contains the reports, proxy and information statements and other information that we file electronically with the SEC at www.sec.gov.

Our CEO and our CFO have provided certifications to the SEC as required by Section 302 of the Sarbanes-Oxley Act of 2002. These certifications are included as exhibits to this Annual Report on Form 10-K.

Our CEO provided a certification pursuant to Section 303A of the New York Stock Exchange Listed Company Manual on May 21, 2010.

Our Code of Business Conduct (“Code of Conduct”) and Corporate Governance Guidelines have been adopted by our Board of Directors. The Code of Conduct is intended to govern, as a requirement of employment, the actions of everyone who works at AES, including employees of our subsidiaries and affiliates. Our Ethics and Compliance Department provides training, information, and certification programs for AES employees related to the Code of Conduct. The Ethics and Compliance Department also has programs in place to prevent and detect criminal conduct, promote an organizational culture that encourages ethical behavior and a commitment to compliance with the law, and to monitor and enforce AES policies on corruption, bribery, money laundering and associations with terrorists groups. The Code of Conduct and the Corporate Governance Guidelines are located in their entirety on our website at http://www.aes.com. Any person may obtain a copy of the Code of Conduct or the Corporate Governance Guidelines without charge by making a written request to: Corporate Secretary, The AES Corporation, 4300 Wilson Boulevard, Arlington, VA 22203. If any amendments to, or waivers from, the Code of Conduct or the Corporate Governance Guidelines are made, we will disclose such amendments or waivers on our website.

Overview

In each country where we conduct business, we are subject to extensive and complex governmental regulations which affect most aspects of our business, such as regulations governing the generation and distribution of electricity and environmental regulations. These regulations affect the operation, development, growth and ownership of our businesses. Regulations differ on a country-by-country basis and are based upon the type of business we operate in a particular country.

Regulation of our Generation Businesses

Our Generation businesses operate in two different types of regulatory environments: Market Environments and Other Environments.

Market Environments. In market environments, sales of electricity may be made directly on the spot market, under negotiated bilateral contracts, or pursuant to PPAs. The spot markets are typically administered by a central dispatch or system operator who seeks to optimize the use of the generation resources throughout an interconnected system (the cost of the least expensive next-generation plant required to meet system demand). The spot price is usually set at the marginal cost of energy or based on bid prices. In addition, many of these wholesale markets include markets for ancillary services to support the reliable operation of the transmission system, such as regulation (a service that corrects for short-term changes in electricity use that could impact the stability of the power system). Most of our businesses in Europe, Latin America and the United States operate in these types of liberalized markets.

Other Environments. We operate Generation assets in certain countries that do not have a spot market. In these environments, electricity is sold only through PPAs with state-owned entities and/or industrial clients as the offtaker. Examples of countries where we operate in this type of environment include Jordan, Nigeria, Puerto Rico and Sri Lanka.

21

Table of Contents

Regulation of our Distribution Businesses

In general, our distribution companies sell electricity directly to end-users such as homes and businesses and bill customers directly. The amount our distribution companies can charge customers for electricity is governed by a regulated tariff. The tariff, in turn, is generally based upon a certain usage level that includes a pass-through to the customer of costs that are not controlled by the distribution company, including the costs of fuel (in the case of integrated utilities) and/or the costs of purchased energy, plus a margin for the value added by the distributor, which is usually calculated as a fair return on the fair value of the company’s assets. This regulated tariff is periodically reviewed and reset by the applicable regulatory agency. Components of the tariff that are directly passed through to the customer are usually adjusted through an automated process. In many instances, the tariffs can be adjusted between scheduled regulatory resets pursuant to an inflation adjustment or another index. Customers with demand above a certain level are often unregulated and can choose to contract with generation companies directly and pay a wheeling fee, which is a fee to the distribution company for use of the distribution system. Most of our utilities operate as monopolies within exclusive geographic areas set by the regulatory agency and face limited competition from other distributors.

Set forth below is a discussion of certain regulations we operate under in the countries where we do business. In each country, the regulatory environment can pose material risks to our business, operations or financial condition. For further discussion of those risks, see the Item 1A.—Risk Factors of this Form 10-K.

Latin America and Africa

Argentina

Structure of Electricity Market. The Argentine electricity market is divided into three separate lines of business: generation, transmission and distribution. AES Argentina operates 12% of the installed capacity of the Wholesale Electricity Market (“WEM”) and two distribution companies: one under federal jurisdiction–EDELAP; and the other under the jurisdiction of the Province of Buenos Aires–EDES. The law recognizes a category of large users made up of industrial companies and other consumers with substantial electricity supply needs.

The WEM is comprised of:

| • | A Term Contracts Market, with contracts freely agreed amongst producers and consumers; |

| • | A Spot Market, with prices sanctioned on an hourly basis considering the economic cost of production represented by the short-term marginal cost (spot prices); and |

| • | A Stabilization System on a quarterly basis of the prices forecasted for the spot market, created for the purchase of the distributors (seasonal prices). |

Principal Regulators. The National Electricity Regulating Agency (“ENRE”) is responsible for ensuring transmission and distribution companies comply with the concessions granted by the Argentine government and approving distribution tariffs. The WEM is managed by Compañía Administradora del Mercado Mayorista Eléctrico, Sociedad Anónima (“CAMMESA”), the independent system operator. CAMMESA also acts as the dispatch entity, or OED (Organismo Encargado de Desapacho), and manages the organization, dispatch and operations of the WEM at large according to the policies established by the Energy Secretariat, under the Ministry of Federal Planning, Public Investment and Services. In such capacity, CAMMESA is empowered to interpret the rules relating to the organization, dispatch and energy agreements in the WEM. In addition to these duties, CAMMESA manages the information on supply and demand in the WEM, which is used by the Energy Secretariat to fix the seasonal prices and the market’s operational rules. CAMMESA’s operating costs are borne by the WEM’s participants and agents.

In the Provincial Jurisdiction, the regulator is the Organismo de Control de la Electricidad de Buenos Aires and the Dirección Provincial de Energía under the Ministry of Infrastructure.

22

Table of Contents