UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM | ||||||||

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the Quarterly Period Ended June 30, 2022

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

Commission File Number: | ||||||||

(Exact name of Registrant as specified in its charter)

| (State of incorporation) | (I.R.S. employer identification no.) | |||||||||||||

| (Address of principal executive offices) | (Zip code) | |||||||||||||

| (Registrant's telephone number, including area code) | |||||||||||

| Securities registered pursuant to Section 12(b) of the Act: | ||||||||||||||

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||||||||||||

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company or an emerging growth company. See definition of “large accelerated filer”, “accelerated filer”, “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act): (Check one):

| Large accelerated filer | ☐ | ☒ | Non-accelerated filer | ☐ | Smaller reporting company | Emerging growth company | |||||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ☒ No ☐

As of August 5, 2022, 44,962,919 shares of common stock, par value $0.01 per share, of the Registrant were outstanding.

AMBAC FINANCIAL GROUP, INC. AND SUBSIDIARIES

TABLE OF CONTENTS

| Cautionary Statement Pursuant to the Private Securities Litigation Reform Act of 1995 | ||||||||||||||||||||

| Item Number | Page | Item Number | Page | |||||||||||||||||

| PART I. FINANCIAL INFORMATION | PART I (CONTINUED) | |||||||||||||||||||

| 1 | Unaudited Consolidated Financial Statements of Ambac Financial Group, Inc. and Subsidiaries | U.S. Insurance Statutory Basis Financial Results | ||||||||||||||||||

| 3 | ||||||||||||||||||||

| 4 | ||||||||||||||||||||

| 2 | PART II. OTHER INFORMATION | |||||||||||||||||||

| 1 | ||||||||||||||||||||

| 1A | ||||||||||||||||||||

| 2 | ||||||||||||||||||||

| 3 | ||||||||||||||||||||

| 5 | Other Information | |||||||||||||||||||

| 6 | Exhibits | |||||||||||||||||||

| Ambac Financial Group, Inc. i 2022 Second Quarter FORM 10-Q |

CAUTIONARY STATEMENT PURSUANT TO THE PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995

Management has included in Parts I and II of this Quarterly Report on Form 10-Q, including this MD&A, statements that may constitute “forward-looking statements” within the meaning of the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Words such as “estimate,” “project,” “plan,” “believe,” “anticipate,” “intend,” “planned,” “potential” and similar expressions, or future or conditional verbs such as “will,” “should,” “would,” “could,” and “may,” or the negative of those expressions or verbs, identify forward-looking statements. We caution readers that these statements are not guarantees of future performance. Forward-looking statements are not historical facts but instead represent only our beliefs regarding future events, which may by their nature be inherently uncertain and some of which may be outside our control. These statements may relate to plans and objectives with respect to the future, among other things which may change. We are alerting you to the possibility that our actual results may differ, possibly materially, from the expected objectives or anticipated results that may be suggested, expressed or implied by these forward-looking statements. Important factors that could cause our results to differ, possibly materially, from those indicated in the forward-looking statements include, among others, those discussed under “Risk Factors” in Part I, Item 1A of the 2021 Annual Report on Form 10-K and in Part II, Item 1A of this quarterly Report on Form 10-Q.

Any or all of management’s forward-looking statements here or in other publications may turn out to be incorrect and are based on management’s current belief or opinions. Ambac Financial Group’s (“AFG”) and its subsidiaries’ (collectively, “Ambac” or the “Company”) actual results may vary materially, and there are no guarantees about the performance of Ambac’s securities. Among events, risks, uncertainties or factors that could cause actual results to differ materially are: (1) the highly speculative nature of AFG’s common stock and volatility in the price of AFG’s common stock; (2) uncertainty concerning the Company’s ability to achieve value for holders of its securities, whether from Ambac Assurance Corporation (“AAC”) and its subsidiaries or from the specialty property and casualty program insurance business, the distribution business, or related businesses; (3) the inability of AAC to realize the expected recoveries, including RMBS litigation recoveries, included in its financial statements, or changes in estimated RMBS litigation recoveries over time; (4) failure to recover claims paid on Puerto Rico exposures or realization of losses in amounts higher than expected; (5) inadequacy of reserves established for losses and loss expenses and possibility that changes in loss reserves may result in further volatility of earnings or financial results; (6) potential for rehabilitation proceedings or other regulatory intervention against AAC; (7) credit risk throughout Ambac’s business, including but not limited to credit risk related to insured residential mortgage-backed securities, student loan and other asset securitizations, public finance obligations (including risks associated with Chapter 9 and other restructuring proceedings), issuers of securities in our investment portfolios, and exposures to reinsurers; (8) our inability to effectively reduce insured financial guarantee exposures or achieve recoveries or investment objectives; (9) our inability to generate the significant amount of cash needed to service our debt and financial obligations, including through litigation recoveries or disposition of assets, and our inability to refinance our indebtedness; (10) Ambac’s substantial indebtedness could adversely affect its financial condition and operating flexibility; (11) Ambac may not be able to obtain financing or raise capital on acceptable terms or at all due to its substantial indebtedness and financial condition; (12) the impact of catastrophic public health, environmental or natural events, including events like the COVID-19 pandemic, or global or regional conflicts, on significant portions of our insured portfolio; (13) credit risks related to large single risks, risk concentrations and correlated risks; (14) risks associated with adverse selection as Ambac’s financial guarantee insurance portfolio runs

off; (15) the risk that Ambac’s risk management policies and practices do not anticipate certain risks and/or the magnitude of potential for loss; (16) restrictive covenants in agreements and instruments that impair Ambac’s ability to pursue or achieve its business strategies; (17) adverse effects on operating results or the Company’s financial position resulting from measures taken to reduce financial guarantee risks in its insured portfolio; (18) disagreements or disputes with Ambac's insurance regulators; (19) loss of control rights in transactions for which we provide financial guarantee insurance; (20) adverse tax consequences or other costs resulting from the characterization of the AAC’s surplus notes or other obligations as equity; (21) risks attendant to the change in composition of securities in the Ambac’s investment portfolio; (22) adverse impacts from changes in prevailing interest rates; (23) events or circumstances that result in the impairment of our intangible assets and/or goodwill that was recorded in connection with Ambac’s acquisition of 80% of the membership interests of Xchange Benefits, LLC; (24) risks associated with the expected discontinuance of the London Inter-Bank Offered Rate; (25) factors that may negatively influence the amount of installment premiums paid to Ambac; (26) risks relating to determinations of amounts of impairments taken on investments; (27) the risk of litigation and regulatory inquiries or investigations, and the risk of adverse outcomes in connection therewith; (28) actions of stakeholders whose interests are not aligned with broader interests of Ambac's stockholders; (29) system security risks, data protection breaches and cyber attacks; (30) regulatory oversight of Ambac Assurance UK Limited (“Ambac UK”) and applicable regulatory restrictions may adversely affect our ability to realize value from Ambac UK or the amount of value we ultimately realize; (31) failures in services or products provided by third parties; (32) our inability to attract and retain qualified executives, senior managers and other employees, or the loss of such personnel; (33) fluctuations in foreign currency exchange rates; (34) failure to realize our business expansion plans or failure of such plans to create value; (35) greater competition for our specialty property & casualty program insurance business; (36) loss or lowering of the AM Best rating for our property and casualty insurance company subsidiaries; (37) disintermediation within the insurance industry or greater competition that negatively impacts our managing general agency/underwriting business; (38) changes in law or in the functioning of the healthcare market that impair the business model of our accident and health managing general underwriter; and (39) other risks and uncertainties that have not been identified at this time.

| Ambac Financial Group, Inc. 1 2022 Second Quarter FORM 10-Q |

PART I. FINANCIAL INFORMATION

Item 1. Unaudited Financial Statements of Ambac Financial Group, Inc. and Subsidiaries

AMBAC FINANCIAL GROUP, INC. AND SUBSIDIARIES

Consolidated Balance Sheets

| June 30, | December 31, | ||||||||||

| (Dollars in millions, except share data) (June 30, 2022 (Unaudited)) | 2022 | 2021 | |||||||||

| Assets: | |||||||||||

| Investments: | |||||||||||

Fixed maturity securities - available-for-sale, at fair value (amortized cost of $ | $ | $ | |||||||||

Fixed maturity securities pledged as collateral, at fair value (amortized cost of $ | |||||||||||

Fixed maturity securities - trading (includes $ | — | ||||||||||

Short-term investments, at fair value (amortized cost of $ | |||||||||||

Short-term investments pledged as collateral, at fair value (amortized cost of $ | |||||||||||

Other investments (includes $ | |||||||||||

Total investments (net of allowance for credit losses of $ | |||||||||||

| Cash and cash equivalents | |||||||||||

| Restricted cash | |||||||||||

Premium receivables (net of allowance for credit losses of $ | |||||||||||

Reinsurance recoverable on paid and unpaid losses (net of allowance for credit losses of $0 and $0) | |||||||||||

| Deferred ceded premium | |||||||||||

| Subrogation recoverable | |||||||||||

| Derivative assets | |||||||||||

| Intangible assets | |||||||||||

| Goodwill | |||||||||||

| Other assets | |||||||||||

| Variable interest entity assets: | |||||||||||

| Fixed maturity securities, at fair value | |||||||||||

| Restricted cash | |||||||||||

| Loans, at fair value | |||||||||||

| Derivative assets | |||||||||||

| Other assets | |||||||||||

| Total assets | $ | $ | |||||||||

| Liabilities and Stockholders’ Equity: | |||||||||||

| Liabilities: | |||||||||||

| Unearned premiums | $ | $ | |||||||||

| Loss and loss expense reserves | |||||||||||

| Ceded premiums payable | |||||||||||

| Long-term debt | |||||||||||

| Accrued interest payable | |||||||||||

| Derivative liabilities | |||||||||||

| Other liabilities | |||||||||||

| Variable interest entity liabilities: | |||||||||||

Long-term debt (includes $ | |||||||||||

| Derivative liabilities | |||||||||||

| Total liabilities | |||||||||||

| Commitments and contingencies (See Note 14) | |||||||||||

| Redeemable noncontrolling interest | |||||||||||

| Stockholders’ equity: | |||||||||||

Preferred stock, par value $ | |||||||||||

Common stock, par value $ | |||||||||||

| Additional paid-in capital | |||||||||||

| Accumulated other comprehensive income (loss) | ( | ||||||||||

| Retained earnings | |||||||||||

Treasury stock, shares at cost: | ( | ( | |||||||||

| Total Ambac Financial Group, Inc. stockholders’ equity | |||||||||||

| Nonredeemable noncontrolling interest | |||||||||||

| Total stockholders’ equity | |||||||||||

| Total liabilities, redeemable noncontrolling interest and stockholders’ equity | $ | $ | |||||||||

See accompanying Notes to Unaudited Consolidated Financial Statements

| Ambac Financial Group, Inc. 2 2022 Second Quarter FORM 10-Q |

AMBAC FINANCIAL GROUP, INC. AND SUBSIDIARIES

Consolidated Statements of Total Comprehensive Income (Loss) (Unaudited)

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||||||||||||

| (Dollars in millions, except share data) | 2022 | 2021 | 2022 | 2021 | ||||||||||||||||||||||

| Revenues: | ||||||||||||||||||||||||||

| Net premiums earned | $ | $ | $ | |||||||||||||||||||||||

| Net investment income (loss) | ( | ( | ||||||||||||||||||||||||

| Net investment gains (losses), including impairments | ( | |||||||||||||||||||||||||

| Net gains (losses) on derivative contracts | ( | |||||||||||||||||||||||||

| Net realized gains (losses) on extinguishment of debt | ||||||||||||||||||||||||||

| Commission income | ||||||||||||||||||||||||||

| Other income (expense) | ( | |||||||||||||||||||||||||

| Income (loss) on variable interest entities | ( | |||||||||||||||||||||||||

| Total revenues | ||||||||||||||||||||||||||

| Expenses: | ||||||||||||||||||||||||||

| Losses and loss expenses (benefit) | ( | ( | ( | |||||||||||||||||||||||

| Intangible amortization | ||||||||||||||||||||||||||

| Operating expenses | ||||||||||||||||||||||||||

| Interest expense | ||||||||||||||||||||||||||

| Total expenses | ||||||||||||||||||||||||||

| Pre-tax income (loss) | ( | |||||||||||||||||||||||||

| Provision (benefit) for income taxes | ||||||||||||||||||||||||||

| Net income (loss) | ( | ( | ||||||||||||||||||||||||

| Less: net (gain) loss attributable to noncontrolling interest | ||||||||||||||||||||||||||

| Net income (loss) attributable to common stockholders | $ | $ | ( | $ | $ | ( | ||||||||||||||||||||

| Other comprehensive income (loss), after tax: | ||||||||||||||||||||||||||

| Net income (loss) | $ | $ | ( | $ | $ | ( | ||||||||||||||||||||

Unrealized gains (losses) on securities, net of income tax provision (benefit) of $( | ( | ( | ||||||||||||||||||||||||

Gains (losses) on foreign currency translation, net of income tax provision (benefit) of $ | ( | ( | ||||||||||||||||||||||||

Credit risk changes of fair value option liabilities, net of income tax provision (benefit) of $ | ( | |||||||||||||||||||||||||

Changes to postretirement benefit, net of income tax provision (benefit) of $ | ( | |||||||||||||||||||||||||

| Total other comprehensive income (loss), net of income tax | ( | ( | ||||||||||||||||||||||||

| Total comprehensive income (loss) | ( | ( | ( | ( | ||||||||||||||||||||||

| Less: comprehensive (gain) loss attributable to the noncontrolling interest | ||||||||||||||||||||||||||

| Total comprehensive income (loss) attributable to common stockholders | $ | ( | $ | ( | $ | ( | $ | ( | ||||||||||||||||||

| Net income (loss) per share attributable to common stockholders: | ||||||||||||||||||||||||||

| Basic | $ | $ | ( | $ | $ | ( | ||||||||||||||||||||

| Diluted | $ | $ | ( | $ | $ | ( | ||||||||||||||||||||

| Weighted average number of common shares outstanding: | ||||||||||||||||||||||||||

| Basic | ||||||||||||||||||||||||||

| Diluted | ||||||||||||||||||||||||||

See accompanying Notes to Unaudited Consolidated Financial Statements

| Ambac Financial Group, Inc. 3 2022 Second Quarter FORM 10-Q |

AMBAC FINANCIAL GROUP, INC. AND SUBSIDIARIES

Consolidated Statements of Stockholders’ Equity (Unaudited)

| Three months ended June 30, 2022 and 2021 | |||||||||||||||||||||||||||||||||||||||||||||||

| Ambac Financial Group, Inc. | |||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in millions) | Total | Retained Earnings | Accumulated Other Comprehensive Income | Preferred Stock | Common Stock | Additional Paid-in Capital | Common Stock Held in Treasury, at Cost | Nonredeemable Noncontrolling Interest | |||||||||||||||||||||||||||||||||||||||

| Balance at March 31, 2022 | $ | $ | $ | ( | $ | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||||||||||

| Total comprehensive income (loss) | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||

| Stock-based compensation | |||||||||||||||||||||||||||||||||||||||||||||||

| Cost of shares repurchased | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||

| Sale of minority interest in subsidiary | |||||||||||||||||||||||||||||||||||||||||||||||

| Balance at June 30, 2022 | $ | $ | $ | ( | $ | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||||||||||

| Balance at March 31, 2021 | $ | $ | $ | $ | $ | $ | $ | ( | $ | ||||||||||||||||||||||||||||||||||||||

| Total comprehensive income (loss) | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||

| Stock-based compensation | |||||||||||||||||||||||||||||||||||||||||||||||

| Changes to redeemable NCI | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||

| Balance at June 30, 2021 | $ | $ | $ | $ | $ | $ | $ | ( | $ | ||||||||||||||||||||||||||||||||||||||

| Six months ended June 30, 2022 and 2021 | |||||||||||||||||||||||||||||||||||||||||||||||

| Ambac Financial Group, Inc. | |||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in millions) | Total | Retained Earnings | Accumulated Other Comprehensive Income | Preferred Stock | Common Stock | Additional Paid-in Capital | Common Stock Held in Treasury, at Cost | Noncontrolling Interest | |||||||||||||||||||||||||||||||||||||||

| Balance at January 1, 2022 | $ | $ | $ | $ | $ | $ | $ | ( | $ | ||||||||||||||||||||||||||||||||||||||

| Total comprehensive income (loss) | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||

| Stock-based compensation | |||||||||||||||||||||||||||||||||||||||||||||||

| Cost of shares repurchased | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||

| Sale of minority interest in subsidiary | |||||||||||||||||||||||||||||||||||||||||||||||

| Cost of shares (acquired) issued under equity plan | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||

| Balance at June 30, 2022 | $ | $ | $ | ( | $ | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||||||||||

| Balance at January 1, 2021 | $ | $ | $ | $ | $ | $ | $ | ( | $ | ||||||||||||||||||||||||||||||||||||||

| Total comprehensive income (loss) | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||

| Stock-based compensation | |||||||||||||||||||||||||||||||||||||||||||||||

| Cost of shares (acquired) issued under equity plan | ( | ( | ( | ||||||||||||||||||||||||||||||||||||||||||||

| Changes to redeemable NCI | ( | ( | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||

| Balance at June 30, 2021 | $ | $ | $ | $ | $ | $ | $ | ( | $ | ||||||||||||||||||||||||||||||||||||||

See accompanying Notes to Unaudited Consolidated Financial Statements

| Ambac Financial Group, Inc. 4 2022 Second Quarter FORM 10-Q |

AMBAC FINANCIAL GROUP, INC. AND SUBSIDIARIES

Consolidated Statements of Cash Flows (Unaudited)

| Six Months Ended June 30, | ||||||||||||||

| (Dollars in millions) | 2022 | 2021 | ||||||||||||

| Cash flows from operating activities: | ||||||||||||||

| Net income (loss) attributable to common stockholders | $ | $ | ( | |||||||||||

| Redeemable noncontrolling interest | ||||||||||||||

| Net income (loss) | ( | |||||||||||||

| Adjustments to reconcile net income to net cash used in operating activities: | ||||||||||||||

| Depreciation and amortization | ||||||||||||||

| Amortization of bond premium and discount | ( | ( | ||||||||||||

| Share-based compensation | ||||||||||||||

| Unearned premiums, net | ( | ( | ||||||||||||

| Losses and loss expenses, net | ( | ( | ||||||||||||

| Ceded premiums payable | ||||||||||||||

| Premium receivables | ||||||||||||||

| Accrued interest payable | ||||||||||||||

| Amortization of intangible assets | ||||||||||||||

| Net investment gains (losses), including impairments | ( | ( | ||||||||||||

| (Gain) loss on extinguishment of debt | ( | ( | ||||||||||||

| Variable interest entity activities | ( | ( | ||||||||||||

| Derivative assets and liabilities | ( | ( | ||||||||||||

| Other, net | ( | |||||||||||||

| Net cash provided by (used in) operating activities | ( | |||||||||||||

| Cash flows from investing activities: | ||||||||||||||

| Proceeds from sales of bonds | ||||||||||||||

| Proceeds from matured bonds | ||||||||||||||

| Purchases of bonds | ( | ( | ||||||||||||

| Proceeds from sales of other invested assets | ||||||||||||||

| Purchases of other invested assets | ( | ( | ||||||||||||

| Change in short-term investments | ( | |||||||||||||

| Change in cash collateral receivable | ||||||||||||||

| Proceeds from paydowns of consolidated VIE assets | ||||||||||||||

| Other, net | ||||||||||||||

| Net cash provided by investing activities | ||||||||||||||

| Cash flows from financing activities: | ||||||||||||||

| Paydowns of LSNI Ambac Note | ( | |||||||||||||

| Payments for purchases of common stock | ( | — | ||||||||||||

| Payments for extinguishment of surplus notes | ( | — | ||||||||||||

| Tax payments related to shares withheld for share-based compensation plans | ( | ( | ||||||||||||

| Distributions to noncontrolling interest holders | ( | |||||||||||||

| Payments of consolidated VIE liabilities | ( | ( | ||||||||||||

| Net cash used in financing activities | ( | ( | ||||||||||||

| Effect of foreign exchange on cash, cash equivalents and restricted cash | ( | |||||||||||||

| Net cash flow | ( | |||||||||||||

| Cash, cash equivalents, and restricted cash at beginning of period | ||||||||||||||

| Cash, cash equivalents, and restricted cash at end of period | $ | $ | ||||||||||||

See accompanying Notes to Unaudited Consolidated Financial Statements

| Ambac Financial Group, Inc. 5 2022 Second Quarter FORM 10-Q |

AMBAC FINANCIAL GROUP, INC. AND SUBSIDIARIES

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

| Note 1. Background and Business Description | Note 8. Intangible Assets | |||||||||||||||||||

| Note 2. Basis of Presentation and Significant Accounting Policies | Note 9. Variable Interest Entities | |||||||||||||||||||

| Note 3. Segment Information | Note 10. Revenues From Contracts with Customers | |||||||||||||||||||

| Note 4. Investments | Note 11. Comprehensive Income | |||||||||||||||||||

| Note 5. Fair Value Measurements | Note 12. Net Income Per Share | |||||||||||||||||||

| Note 6. Insurance Contracts | Note 13. Income Taxes | |||||||||||||||||||

| Note 7. Derivative Instruments | Note 14. Commitments and Contingencies | |||||||||||||||||||

| Ambac Financial Group, Inc. 6 2022 Second Quarter FORM 10-Q |

AMBAC FINANCIAL GROUP, INC. AND SUBSIDIARIES

Notes to Unaudited Consolidated Financial Statements

(Dollar Amounts in Millions, Except Share Amounts)

1. BACKGROUND AND BUSINESS DESCRIPTION

The following description provides an update of Note 1. Background and Business Description in the Notes to the Consolidated Financial Statements included in Part II, Item 8 in the Company’s Annual Report on Form 10-K for the year ended December 31, 2021, and should be read in conjunction with the complete descriptions provided in the Form 10-K. Capitalized terms used, but not defined herein, and in the other footnotes to the Consolidated Financial Statements included in this Quarterly Report on Form 10-Q shall have the meanings ascribed thereto in the Company’s Annual Report on Form 10-K for the year ended December 31, 2021.

Ambac Financial Group, Inc. (“AFG”), headquartered in New York City, is a financial services holding company incorporated in the state of Delaware on April 29, 1991 . References to “Ambac,” the “Company,” “we,” “our,” and “us” are to AFG and its subsidiaries, as the context requires. Ambac's business operations include:

•Legacy Financial Guarantee Insurance — Ambac's financial guarantee business includes the activities of Ambac Assurance Corporation ("AAC") and its wholly owned subsidiaries, including Ambac Assurance UK Limited (“Ambac UK”) and Ambac Financial Services LLC ("AFS"). Both AAC and Ambac UK (the "Legacy Financial Guarantee Companies") have financial guarantee insurance portfolios that have been in runoff since 2008. AFS uses derivatives to hedge interest rate risk in AAC's insurance and investment portfolios.

•Specialty Property & Casualty Insurance — Ambac's hybrid fronting Specialty Property & Casualty Insurance business. Currently includes five admitted carriers (Everspan Insurance Company, Providence Washington Insurance Company, Greenwood Insurance Company (formerly 21st Century Indemnity Insurance Company), Consolidated National Specialty Insurance Company (formerly 21st Century Pacific Insurance Company) and 21st Century Auto Insurance Company of New Jersey and an excess and surplus lines (“E&S” or “nonadmitted”) insurer, Everspan Indemnity Insurance Company (collectively, “Everspan”). The 21st Century companies were acquired in 2022. Everspan carriers have an AM Best rating of 'A-' (Excellent).

•Insurance Distribution — Ambac's specialty property and casualty ("P&C") insurance distribution business, which could include Managing General Agents and Underwriters (collectively "MGAs"), insurance wholesalers, and other distribution businesses, currently includes Xchange Benefits, LLC (“Xchange”) a P&C MGA specializing in accident and health products, 80 % of which was acquired by AFG on December 31, 2020. Refer to Note 3. Business Combination in the Notes to Consolidated Financial Statements included Part II, Item 8 in the Company’s Annual Report on Form 10-K for the year ended December 31, 2021, for further information relating to this acquisition.

Beginning in the first quarter of 2022, the Company began reporting these three business operations as segments; see Note 3. Segment Information for further information.

Strategies to Enhance Shareholder Value

The Company's primary goal is to maximize shareholder value through the execution of key strategies for both its (i) Specialty P&C Insurance Platform and (ii) Legacy Financial Guarantee Companies.

Specialty P&C Insurance Platform strategic priorities include:

•Growing and diversifying the Specialty Property & Casualty insurance business with existing and new program partners.

•Building a leading insurance Distribution business through additional acquisitions and de novo builds, supported by a centralized business services unit including core technology solutions.

•Making opportunistic investments that are strategic to the overall Specialty P&C Insurance Platform.

Legacy Financial Guarantee Companies’ strategic priorities include:

•Actively managing, de-risking and mitigating insured portfolio risk.

•Pursuing loss recovery through active litigation and other means, particularly residential mortgage back security representation and warranty litigation.

•Improving operating efficiency and optimizing our asset and liability profile.

•Exploring, at the appropriate time, strategic options to further maximize value for AFG.

The execution of Ambac’s strategy to increase the value of its investment in AAC is subject to the restrictions set forth in the Settlement Agreement, dated as of June 7, 2010 (the "Settlement Agreement"), by and among AAC, Ambac Credit Products LLC ("ACP"), AFG and certain counterparties to credit default swaps with ACP that were guaranteed by AAC; as well as the Stipulation and Order among the Office of the Commissioner of Insurance for the State of Wisconsin (“OCI”), AFG and AAC that became effective on February 12, 2018, as amended (the “Stipulation and Order”); and the indenture for the Tier 2 Notes (as defined below), each of which requires OCI and, under certain circumstances, holders of the debt instruments benefiting from such restrictions, to approve certain actions taken by or in respect of AAC. In exercising its approval rights, OCI will act for the benefit of policyholders, and will not take into account the interests of AFG.

Opportunities for remediating losses on poorly performing insured transactions also depend on market conditions, including the perception of AAC’s creditworthiness, the structure of the underlying risk and associated policy as well as other counterparty specific factors. AAC's ability to commute policies or purchase certain investments may also be limited by available liquidity.

| Ambac Financial Group, Inc. 7 2022 Second Quarter FORM 10-Q |

AMBAC FINANCIAL GROUP, INC. AND SUBSIDIARIES

Notes to Unaudited Consolidated Financial Statements

(Dollar Amounts in Millions, Except Share Amounts)

2. BASIS OF PRESENTATION AND SIGNIFICANT ACCOUNTING POLICIES

The Company has disclosed its significant accounting policies in Note 2. Basis of Presentation and Significant Accounting Policies in the Notes to Consolidated Financial Statements included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2021. The following significant accounting policies provide an update to those included in the Company’s Annual Report on Form 10-K.

Basis of Presentation:

The accompanying unaudited consolidated financial statements have been prepared in accordance with U.S. generally accepted accounting principles ("GAAP") for interim financial reporting and with the instructions to Form 10-Q and Article 10 of Regulation S-X. Accordingly, they do not include all of the information and disclosures required by GAAP for annual periods. These consolidated financial statements should be read in conjunction with the consolidated financial statements and notes thereto included in the Annual Report on Form 10-K for the year ended December 31, 2021. The accompanying consolidated financial statements have not been audited by an independent registered public accounting firm in accordance with the standards of the Public Company Accounting Oversight Board (U.S.), but in the opinion of management such financial statements include all adjustments necessary for the fair presentation of the Company’s consolidated financial position and results of operations. The results of operations for the three and six months ended June 30, 2022, may not be indicative of the results that may be expected for the year ending December 31, 2022. The December 31, 2021, consolidated balance sheet was derived from audited financial statements.

Redeemable Noncontrolling Interest:

The acquisition by AFG of 80 % of the ownership interests of Xchange is further described in Note 3. Business Combinations in the Notes to Consolidated Financial Statements included in Part II, Item 8 in the Company’s Annual Report on Form 10-K for the year ended December 31, 2021. Under the terms of the acquisition agreement, Ambac received a call option to purchase the remaining 20 % of Xchange from the minority owners (i.e., noncontrolling interests) and the minority owners received a put option to sell the remaining 20 % to Ambac. The call and put options are exercisable after different time periods elapse. Because the exercise of the put option is outside the control of Ambac, in accordance with the Distinguishing Liabilities from Equity Topic of the ASC, Ambac reports redeemable noncontrolling interests in the mezzanine section of its consolidated balance sheet.

The redeemable noncontrolling interest is remeasured each period as the greater of:

i.the carrying value under ASC 810, which attributes a portion of consolidated net income (loss) to the redeemable noncontrolling interest; and

ii.the redemption value of the put option under ASC 480 as if it were exercisable at the end of the reporting period.

Any increase (decrease) in the carrying amount of the redeemable noncontrolling interest as a result of adjusting to the redemption value of the put option is recorded as an offset to retained earnings. The impact of such differences on earnings per share are presented in Note 12. Net Income Per Share.

Following is a rollforward of redeemable noncontrolling interest.

| Six Months Ended June 30, | 2022 | 2021 | ||||||||||||

| Beginning balance | $ | $ | ||||||||||||

| Net income attributable to redeemable noncontrolling interest (ASC 810) | ||||||||||||||

| Adjustment to redemption value (ASC 480) | ||||||||||||||

| Ending balance | $ | $ | ||||||||||||

| Ambac Financial Group, Inc. 8 2022 Second Quarter FORM 10-Q |

AMBAC FINANCIAL GROUP, INC. AND SUBSIDIARIES

Notes to Unaudited Consolidated Financial Statements

(Dollar Amounts in Millions, Except Share Amounts)

Supplemental Disclosure of Cash Flow Information | Six Months Ended June 30, | |||||||||||||

| 2022 | 2021 | |||||||||||||

Cash paid during the period for: | ||||||||||||||

| Income taxes | $ | $ | ||||||||||||

Interest on long-term debt | ||||||||||||||

Non-cash investing and financing activities: | ||||||||||||||

| Decrease in long-term debt as a result of surplus notes exchanges | $ | $ | ||||||||||||

| Exchange of investments in Puerto Rico bonds for new securities issued in the restructuring transactions | — | |||||||||||||

| June 30, | ||||||||||||||

| 2022 | 2021 | |||||||||||||

| Reconciliation of cash, cash equivalents, and restricted cash reported within the Consolidated Balance Sheets to the Consolidated Statements of Cash Flows: | ||||||||||||||

Cash and cash equivalents | $ | $ | ||||||||||||

| Restricted cash | ||||||||||||||

| Variable Interest Entity restricted cash | ||||||||||||||

| Total cash, cash equivalents, and restricted cash shown on the Consolidated Statements of Cash Flows | $ | $ | ||||||||||||

Reclassifications and Rounding

Reclassifications may have been made to prior years' amounts to conform to the current year's presentation. Certain amounts and tables in the consolidated financial statements and associated notes may not add due to rounding.

Adopted Accounting Standards:

Effective January 1, 2022, the Company adopted the following accounting standard:

Equity-classified Written Call Options

In May 2021, the FASB issued ASU 2021-04, Issuer's Accounting for Certain Modifications or Exchanges of Freestanding Equity-Classified Written Call Options. The ASU clarifies and reduces diversity in practice for an issuer's accounting for modifications or exchanges of equity-classified written call options (e.g. warrants) that remain equity-classified after the modification or exchange. The ASU requires an issuer to account for the modification or exchange based on the economic substance of the transaction. For example, if the modification or exchange is related to the issuance of debt or equity, any change in the fair value of the written call option would be accounted for as part of the debt issuance cost in accordance with the debt guidance or equity issuance cost in accordance with the equity guidance, respectively. The ASU did not have a consequential impact on Ambac's financial statements.

Convertible Instruments and Contracts in an Entity's Own Equity

In August 2020, the FASB issued ASU 2020-06, Accounting for Convertible Instruments and Contracts in an Entity's Own Equity. The ASU i) simplifies the accounting for convertible debt and convertible preferred stock by reducing the number of accounting

models, and amends certain disclosures, ii) amends and simplifies the derivative scope exception guidance for contracts in an entity's own equity, including share-based compensation, and iii) amends the diluted earnings per share calculations for convertible instruments and contracts in an entity's own equity. The ASU did not have a consequential impact on Ambac's financial statements.

Future Application of Accounting Standards:

Reference Rate Reform

In March 2020, the FASB issued ASU 2020-04, Reference Rate Reform (Topic 848) - Facilitation of the Effects of Reference Rate Reform on Financial Reporting. The ASU provides companies with optional guidance to ease the potential accounting burden related to transitioning away from reference rates, such as LIBOR, that are expected to be discontinued as a result of initiatives undertaken by various jurisdictions around the world. For example, under current GAAP, contract modifications which change a reference rate are required to be evaluated in determining whether the modifications result in the establishment of new contracts or the continuation of existing contracts. The amendments in this ASU provide optional expedients and exceptions for applying GAAP to contracts, hedging relationships, and other transactions affected by reference rate reform if certain criteria are met. The ASU can be applied prospectively as of the beginning of the interim period that includes or is subsequent to March 12, 2020, or any date thereafter, but does not apply to contract modifications and other transactions entered into or evaluated after December 31, 2022. On April 20, 2022, the FASB issued a proposed ASU that would extend the sunset date to December 31, 2024 and make certain definitional changes, with feedback required by June 6, 2022. Management has not determined when it will adopt this ASU, and the impact on Ambac's financial statements is being evaluated.

| Ambac Financial Group, Inc. 9 2022 Second Quarter FORM 10-Q |

AMBAC FINANCIAL GROUP, INC. AND SUBSIDIARIES

Notes to Unaudited Consolidated Financial Statements

(Dollar Amounts in Millions, Except Share Amounts)

3. SEGMENT INFORMATION

The following tables summarize the components of the Company’s total revenues and expenses, pretax income (loss), net income (loss), net income (loss) attributable to common shareholders and total assets by reportable business segment. Information provided below for “Corporate and Other” primarily relates to the operations of AFG, which will include investment income on its investment portfolio and costs to maintain the operations of AFG, including public company reporting, capital management and business development costs for the acquisition and development of new business initiatives.

| Legacy Financial Guarantee Insurance | Specialty Property & Casualty Insurance | Insurance Distribution | Corporate & Other | Consolidated (2) | ||||||||||||||||||||||||||||

| Three Months Ended June 30, 2022 | ||||||||||||||||||||||||||||||||

| Revenues: | ||||||||||||||||||||||||||||||||

| Net premiums earned | $ | $ | $ | |||||||||||||||||||||||||||||

| Net investment income (loss) | ( | $ | ( | |||||||||||||||||||||||||||||

| Net gains on derivative contracts | ||||||||||||||||||||||||||||||||

| Net realized gains on extinguishment of debt | ||||||||||||||||||||||||||||||||

| Commission income | $ | |||||||||||||||||||||||||||||||

Other (1) | ||||||||||||||||||||||||||||||||

Total revenues (2) | ||||||||||||||||||||||||||||||||

| Expenses: | ||||||||||||||||||||||||||||||||

| Loss and loss expenses (benefit) | ( | ( | ||||||||||||||||||||||||||||||

Operating expenses (3) | ||||||||||||||||||||||||||||||||

Depreciation expense (3) | ||||||||||||||||||||||||||||||||

| Intangible amortization | ||||||||||||||||||||||||||||||||

Sub-producer commissions (3) | ||||||||||||||||||||||||||||||||

| Interest expense | ||||||||||||||||||||||||||||||||

Total expenses (2) | ||||||||||||||||||||||||||||||||

| Pretax income (loss) | $ | $ | ( | $ | $ | $ | ||||||||||||||||||||||||||

Total assets (2) | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||

| Six Months Ended June 30, 2022 | ||||||||||||||||||||||||||||||||

| Revenues: | ||||||||||||||||||||||||||||||||

| Net premiums earned | $ | $ | $ | |||||||||||||||||||||||||||||

| Net investment income (loss) | ( | $ | ( | |||||||||||||||||||||||||||||

| Net gains on derivative contracts | — | |||||||||||||||||||||||||||||||

| Net realized gains on extinguishment of debt | — | |||||||||||||||||||||||||||||||

| Commission income | $ | |||||||||||||||||||||||||||||||

Other (1) | ||||||||||||||||||||||||||||||||

Total revenues (2) | ||||||||||||||||||||||||||||||||

| Expenses: | ||||||||||||||||||||||||||||||||

| Loss and loss expenses (benefit) | ||||||||||||||||||||||||||||||||

Operating expenses (3) | ||||||||||||||||||||||||||||||||

Depreciation expense (3) | ||||||||||||||||||||||||||||||||

| Intangible amortization | ||||||||||||||||||||||||||||||||

Sub-producer commissions (3) | ||||||||||||||||||||||||||||||||

| Interest expense | ||||||||||||||||||||||||||||||||

Total expenses (2) | ||||||||||||||||||||||||||||||||

| Pretax income (loss) | $ | $ | ( | $ | $ | ( | $ | |||||||||||||||||||||||||

| Ambac Financial Group, Inc. 10 2022 Second Quarter FORM 10-Q |

AMBAC FINANCIAL GROUP, INC. AND SUBSIDIARIES

Notes to Unaudited Consolidated Financial Statements

(Dollar Amounts in Millions, Except Share Amounts)

| Legacy Financial Guarantee Insurance | Specialty Property & Casualty Insurance | Insurance Distribution | Corporate & Other | Consolidated (2) | ||||||||||||||||||||||||||||

| Three Months Ended June 30, 2021 | ||||||||||||||||||||||||||||||||

| Revenues: | ||||||||||||||||||||||||||||||||

| Net premiums earned | $ | $ | $ | |||||||||||||||||||||||||||||

| Net investment income | $ | |||||||||||||||||||||||||||||||

| Net gains (losses) on derivative contracts | ( | ( | ||||||||||||||||||||||||||||||

| Net realized gains on extinguishment of debt | ||||||||||||||||||||||||||||||||

| Commission income | $ | |||||||||||||||||||||||||||||||

Other (1) | ||||||||||||||||||||||||||||||||

Total revenues (2) | ||||||||||||||||||||||||||||||||

| Expenses: | ||||||||||||||||||||||||||||||||

| Loss and loss expenses (benefit) | ( | ( | ||||||||||||||||||||||||||||||

Operating expenses (3) | ||||||||||||||||||||||||||||||||

Depreciation expense (3) | ||||||||||||||||||||||||||||||||

| Intangible amortization | ||||||||||||||||||||||||||||||||

Sub-producer commissions (3) | ||||||||||||||||||||||||||||||||

| Interest expense | ||||||||||||||||||||||||||||||||

| Total expenses | ||||||||||||||||||||||||||||||||

Pretax income (loss) (2) | $ | ( | $ | ( | $ | $ | $ | ( | ||||||||||||||||||||||||

Total assets (2) | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||

| Six Months Ended June 30, 2021 | ||||||||||||||||||||||||||||||||

| Revenues: | ||||||||||||||||||||||||||||||||

| Net premiums earned | $ | $ | $ | |||||||||||||||||||||||||||||

| Net investment income | $ | |||||||||||||||||||||||||||||||

| Net gains on derivative contracts | — | |||||||||||||||||||||||||||||||

| Net realized gains on extinguishment of debt | ||||||||||||||||||||||||||||||||

| Commission income | $ | |||||||||||||||||||||||||||||||

Other revenues (1) | ( | |||||||||||||||||||||||||||||||

Total revenues (2) | ||||||||||||||||||||||||||||||||

| Expenses: | ||||||||||||||||||||||||||||||||

| Loss and loss expenses (benefit) | ( | ( | ||||||||||||||||||||||||||||||

Operating expenses (3) | ||||||||||||||||||||||||||||||||

Depreciation expense (3) | ||||||||||||||||||||||||||||||||

| Intangible amortization | ||||||||||||||||||||||||||||||||

Sub-producer commissions (3) | ||||||||||||||||||||||||||||||||

| Interest expense | ||||||||||||||||||||||||||||||||

| Total expenses | ||||||||||||||||||||||||||||||||

Pretax income (loss) (2) | $ | $ | ( | $ | $ | ( | $ | |||||||||||||||||||||||||

(1)Other revenues include the following line items on the Consolidated Statements of Total Comprehensive Income: Net investment gains (losses), including impairments, income (loss) on variable interest entities and other income (expense).

(2)Inter-segment revenues and inter-segment pre-tax income (loss) amounts are insignificant and are not presented separately. Total assets noted in the Corporate and Other Column is net of AFG's investment in surplus notes issued by the Legacy Financial Guarantee Segment with fair values of $61 and $116 at June 30, 2022 and 2021.

(3)The Consolidated Statements of Comprehensive Income presents the sum of these items as Operating Expenses.

| Ambac Financial Group, Inc. 11 2022 Second Quarter FORM 10-Q |

AMBAC FINANCIAL GROUP, INC. AND SUBSIDIARIES

Notes to Unaudited Consolidated Financial Statements

(Dollar Amounts in Millions, Except Share Amounts)

4. INVESTMENTS

Ambac’s non-VIE invested assets are primarily comprised of fixed maturity securities classified as either available-for-sale or trading securities, and interests in pooled investment funds, which are reported within Other investments on the Consolidated Balance Sheets. Interests in pooled investment funds in the form of common stock or in-substance common stock are classified as trading securities, while limited partner interests in such funds are

reported using the equity method. Fixed maturity securities classified as trading are unrated municipal bond obligations of Puerto Rico issuing entities that are part of the the PROMESA restructuring process as described further in Note 6. Insurance Contracts.

Fixed Maturity Securities:

The amortized cost and estimated fair value of available-for-sale investments, excluding VIE investments, at June 30, 2022 and December 31, 2021, were as follows:

| Amortized Cost | Allowance for Credit Losses | Gross Unrealized Gains | Gross Unrealized Losses | Estimated Fair Value | ||||||||||||||||||||||||||||

| June 30, 2022: | ||||||||||||||||||||||||||||||||

| Fixed maturity securities: | ||||||||||||||||||||||||||||||||

| Municipal obligations | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||

| Corporate obligations | ||||||||||||||||||||||||||||||||

| Foreign obligations | ||||||||||||||||||||||||||||||||

| U.S. government obligations | ||||||||||||||||||||||||||||||||

| Residential mortgage-backed securities | ||||||||||||||||||||||||||||||||

| Collateralized debt obligations | ||||||||||||||||||||||||||||||||

Other asset-backed securities (1) | ||||||||||||||||||||||||||||||||

| Short-term | ||||||||||||||||||||||||||||||||

| Fixed maturity securities pledged as collateral: | ||||||||||||||||||||||||||||||||

| U.S. government obligations | ||||||||||||||||||||||||||||||||

| Short-term | ||||||||||||||||||||||||||||||||

| Total available-for-sale investments | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||

| December 31, 2021: | ||||||||||||||||||||||||||||||||

| Fixed maturity securities: | ||||||||||||||||||||||||||||||||

| Municipal obligations | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||

| Corporate obligations | ||||||||||||||||||||||||||||||||

| Foreign obligations | ||||||||||||||||||||||||||||||||

| U.S. government obligations | ||||||||||||||||||||||||||||||||

| Residential mortgage-backed securities | ||||||||||||||||||||||||||||||||

| Collateralized debt obligations | ||||||||||||||||||||||||||||||||

Other asset-backed securities (1) | ||||||||||||||||||||||||||||||||

| Short-term | ||||||||||||||||||||||||||||||||

| Fixed maturity securities pledged as collateral: | ||||||||||||||||||||||||||||||||

| U.S. government obligations | ||||||||||||||||||||||||||||||||

| Short-term | ||||||||||||||||||||||||||||||||

| Total available-for-sale investments | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||

| Ambac Financial Group, Inc. 12 2022 Second Quarter FORM 10-Q |

AMBAC FINANCIAL GROUP, INC. AND SUBSIDIARIES

Notes to Unaudited Consolidated Financial Statements

(Dollar Amounts in Millions, Except Share Amounts)

The amortized cost and estimated fair value of available-for-sale investments, excluding VIE investments, at June 30, 2022, by contractual maturity, were as follows:

| Amortized Cost | Estimated Fair Value | |||||||||||||

| Due in one year or less | $ | $ | ||||||||||||

| Due after one year through five years | ||||||||||||||

| Due after five years through ten years | ||||||||||||||

| Due after ten years | ||||||||||||||

| Residential mortgage-backed securities | ||||||||||||||

| Collateralized debt obligations | ||||||||||||||

| Other asset-backed securities | ||||||||||||||

| Total | $ | $ | ||||||||||||

Expected maturities will differ from contractual maturities because borrowers may have the right to call or prepay certain obligations with or without call or prepayment penalties.

Unrealized Losses on Fixed Maturity Securities:

The following table shows gross unrealized losses and fair values of Ambac’s available-for-sale investments, excluding VIE investments, which at June 30, 2022 and December 31, 2021, did not have an allowance for credit losses under the CECL standard. This information is aggregated by investment category and length of time that the individual securities have been in a continuous unrealized loss position, at June 30, 2022 and December 31, 2021:

| Less Than 12 Months | 12 Months or More | Total | ||||||||||||||||||||||||||||||||||||

| Fair Value | Gross Unrealized Loss | Fair Value | Gross Unrealized Loss | Fair Value | Gross Unrealized Loss | |||||||||||||||||||||||||||||||||

| June 30, 2022: | ||||||||||||||||||||||||||||||||||||||

| Fixed maturity securities: | ||||||||||||||||||||||||||||||||||||||

| Municipal obligations | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||

| Corporate obligations | ||||||||||||||||||||||||||||||||||||||

| Foreign obligations | ||||||||||||||||||||||||||||||||||||||

| U.S. government obligations | ||||||||||||||||||||||||||||||||||||||

| Residential mortgage-backed securities | ||||||||||||||||||||||||||||||||||||||

| Collateralized debt obligations | ||||||||||||||||||||||||||||||||||||||

| Other asset-backed securities | ||||||||||||||||||||||||||||||||||||||

| Short-term | ||||||||||||||||||||||||||||||||||||||

| Fixed income securities, pledged as collateral: | ||||||||||||||||||||||||||||||||||||||

| Short-term | ||||||||||||||||||||||||||||||||||||||

| Total collateralized investments | ||||||||||||||||||||||||||||||||||||||

| Total temporarily impaired securities | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||

| Ambac Financial Group, Inc. 13 2022 Second Quarter FORM 10-Q |

AMBAC FINANCIAL GROUP, INC. AND SUBSIDIARIES

Notes to Unaudited Consolidated Financial Statements

(Dollar Amounts in Millions, Except Share Amounts)

| Less Than 12 Months | 12 Months or More | Total | ||||||||||||||||||||||||||||||||||||

| Fair Value | Gross Unrealized Loss | Fair Value | Gross Unrealized Loss | Fair Value | Gross Unrealized Loss | |||||||||||||||||||||||||||||||||

| December 31, 2021: | ||||||||||||||||||||||||||||||||||||||

| Fixed maturity securities: | ||||||||||||||||||||||||||||||||||||||

| Municipal obligations | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||

| Corporate obligations | ||||||||||||||||||||||||||||||||||||||

| Foreign obligations | ||||||||||||||||||||||||||||||||||||||

| U.S. government obligations | ||||||||||||||||||||||||||||||||||||||

| Residential mortgage-backed securities | ||||||||||||||||||||||||||||||||||||||

| Collateralized debt obligations | ||||||||||||||||||||||||||||||||||||||

| Other asset-backed securities | ||||||||||||||||||||||||||||||||||||||

| Short-term | ||||||||||||||||||||||||||||||||||||||

| Fixed income securities, pledged as collateral: | ||||||||||||||||||||||||||||||||||||||

| U. S. government obligations | ||||||||||||||||||||||||||||||||||||||

| Total collateralized investments | ||||||||||||||||||||||||||||||||||||||

| Total temporarily impaired securities | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||

Management has determined that the securities in the above table do not have credit impairment as of June 30, 2022 and December 31, 2021, based upon (i) no actual or expected principal and interest payment defaults on these securities; (ii) analysis of the creditworthiness of the issuer and financial guarantor, as applicable, and (iii) for debt securities that are non-highly rated beneficial interests in securitized financial assets, analysis of whether there was an adverse change in projected cash flows. Management's evaluation as of June 30, 2022, includes the expectation that all principal and interest payments on securities guaranteed by AAC or Ambac UK will be made timely and in full.

Ambac’s assessment about whether a security is credit impaired reflects management’s current judgment regarding facts and circumstances specific to the security and other factors. If that judgment changes, Ambac may record a charge for credit impairment in future periods.

Investment Income (Loss)

Net investment income (loss) was comprised of the following for the affected periods:

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||||||||||||

| 2022 | 2021 | 2022 | 2021 | |||||||||||||||||||||||

| Fixed maturity securities | $ | $ | $ | $ | ||||||||||||||||||||||

| Short-term investments | ||||||||||||||||||||||||||

| Investment expense | ( | ( | ( | ( | ||||||||||||||||||||||

| Securities available-for-sale and short-term | ||||||||||||||||||||||||||

| Fixed maturity securities - trading | ( | ( | ||||||||||||||||||||||||

| Other investments | ( | ( | ||||||||||||||||||||||||

| Total net investment income (loss) | $ | ( | $ | $ | ( | $ | ||||||||||||||||||||

Net investment income (loss) from Other investments primarily represents changes in fair value on equity securities, including certain pooled investment funds, and income from investment limited partnerships and other equity interests accounted for under the equity method.

| Ambac Financial Group, Inc. 14 2022 Second Quarter FORM 10-Q |

AMBAC FINANCIAL GROUP, INC. AND SUBSIDIARIES

Notes to Unaudited Consolidated Financial Statements

(Dollar Amounts in Millions, Except Share Amounts)

Net Investments Gains (Losses), including Impairments:

The following table details amounts included in net investment gains (losses) and impairments included in earnings for the affected periods:

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||||||||||||

| 2022 | 2021 | 2022 | 2021 | |||||||||||||||||||||||

| Gross realized gains on securities | $ | $ | $ | $ | ||||||||||||||||||||||

| Gross realized losses on securities | ( | ( | ( | ( | ||||||||||||||||||||||

| Foreign exchange gains (losses) | ( | ( | ||||||||||||||||||||||||

| Credit impairments | ||||||||||||||||||||||||||

| Intent / requirement to sell impairments | ||||||||||||||||||||||||||

| Net investment gains (losses), including impairments | $ | $ | ( | $ | $ | |||||||||||||||||||||

Ambac had an allowance for credit losses of $— and $— at June 30, 2022 and 2021, respectively.

Ambac did not purchase any financial assets with credit deterioration for the three and six months ended June 30, 2022 and 2021.

Counterparty Collateral, Deposits with Regulators and Other Restrictions:

Ambac routinely pledges and receives collateral related to certain transactions. Securities held directly in Ambac’s investment portfolio with a fair value of $85 and $120 at June 30, 2022 and December 31, 2021, respectively, were pledged to derivative counterparties. Ambac’s derivative counterparties have the right to re-pledge the investment securities and as such, these pledged securities are separately classified on the Consolidated Balance

Sheets as “Fixed maturity securities pledged as collateral, at fair value” and "Short-term investments pledged as collateral, at fair value." Refer to Note 7. Derivative Instruments for further information on cash collateral. There was no cash or securities received from other counterparties that were re-pledged by Ambac.

Securities carried at $22 and $17 at June 30, 2022 and December 31, 2021, respectively, were deposited by Ambac's insurance subsidiaries with governmental authorities or designated custodian banks as required by laws affecting insurance companies. Invested assets carried at $1 and $1 at June 30, 2022 and December 31, 2021, were deposited as security in connection with a letter of credit issued for an office lease.

Securities with a fair value of $587 and $669 at June 30, 2022 and December 31, 2021, respectively, were held by Ambac UK, the capital stock of which was pledged as collateral for the Sitka AAC Note. Refer to Note 12. Long-term Debt in the Notes to the Consolidated Financial Statements included in Part II, Item 8 in the Company’s Annual Report on Form 10-K for the year ended December 31, 2021 for further information about the Sitka AAC Note.

Guaranteed Securities:

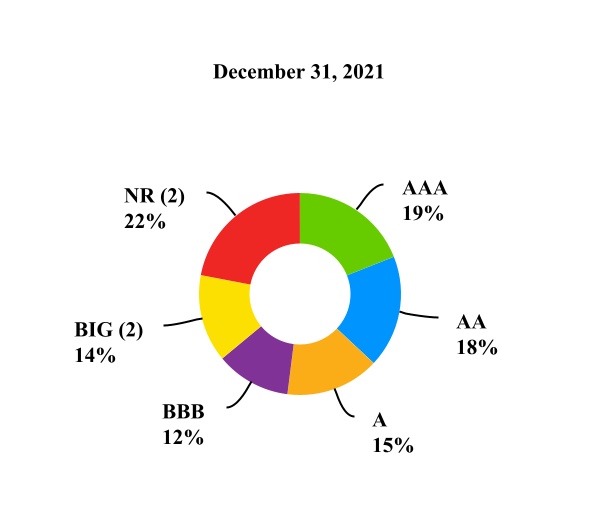

Ambac’s fixed maturity portfolio includes securities covered by guarantees issued by AAC and other financial guarantors (“insured securities”). The published rating agency ratings on these securities reflect the higher of the financial strength rating of the financial guarantor or the rating of the underlying issuer. Rating agencies do not always publish separate underlying ratings (those ratings excluding the insurance by the financial guarantor). In the event these underlying ratings are not available from the rating agencies, Ambac will assign an internal rating. The following table represents the fair value and weighted-average underlying rating of insured securities in Ambac's investment portfolio at June 30, 2022 and December 31, 2021, respectively:

| Municipal Obligations | Corporate Obligations (2) | Mortgage and Asset- backed Securities | Total | Weighted Average Underlying Rating (1) | ||||||||||||||||||||||||||||

| June 30, 2022: | ||||||||||||||||||||||||||||||||

| Ambac Assurance Corporation | $ | $ | $ | $ | B | |||||||||||||||||||||||||||

| Assured Guaranty Municipal Corporation | — | A | ||||||||||||||||||||||||||||||

| Total | $ | $ | $ | $ | B | |||||||||||||||||||||||||||

| December 31, 2021: | ||||||||||||||||||||||||||||||||

| Ambac Assurance Corporation | $ | $ | — | $ | $ | B | ||||||||||||||||||||||||||

| National Public Finance Guarantee Corporation | — | BBB- | ||||||||||||||||||||||||||||||

| Assured Guaranty Municipal Corporation | — | A- | ||||||||||||||||||||||||||||||

| Total | $ | $ | $ | $ | B | |||||||||||||||||||||||||||

(1)Ratings are based on the lower of Standard & Poor’s or Moody’s rating. If unavailable, Ambac’s internal rating is used.

| Ambac Financial Group, Inc. 15 2022 Second Quarter FORM 10-Q |

AMBAC FINANCIAL GROUP, INC. AND SUBSIDIARIES

Notes to Unaudited Consolidated Financial Statements

(Dollar Amounts in Millions, Except Share Amounts)

Other Investments:

Ambac's investment portfolio includes interests in various pooled investment funds. Fair value and additional information about investments in pooled funds, by investment type, is summarized in the table below. Except as noted in the table, fair value as reported is determined using net asset value ("NAV") as a practical expedient. Redemption of certain funds valued using NAV may be subject to withdrawal limitations and/or redemption fees which vary with the timing and notification of withdrawal provided by the investor. In addition to these investments, Ambac has unfunded commitments of $65 to private credit and private equity funds at June 30, 2022.

| Fair Value | ||||||||||||||||||||||||||

| Class of Funds | June 30, 2022 | December 31, 2021 | Redemption Frequency | Redemption Notice Period | ||||||||||||||||||||||

Real estate properties (1) | $ | $ | quarterly | 10 business days | ||||||||||||||||||||||

Hedge funds (2) | quarterly or semi-annually | 90 days | ||||||||||||||||||||||||

High yields and leveraged loans (3) | daily | 0 - 30 days | ||||||||||||||||||||||||

Private credit (4) | quarterly if permitted | 180 days if permitted | ||||||||||||||||||||||||

Insurance-linked investments (5) | see footnote (9) | see footnote (9) | ||||||||||||||||||||||||

Equity market investments (6) (11) | daily or quarterly | 0 - 90 days | ||||||||||||||||||||||||

Investment grade floating rate income (7) | weekly | 0 days | ||||||||||||||||||||||||

Private equity (8) | quarterly if permitted | 90 days if permitted | ||||||||||||||||||||||||

Emerging markets debt (9) (11) | daily | 0 days | ||||||||||||||||||||||||

Convertible bonds (10) | 8 | — | daily | 0 days | ||||||||||||||||||||||

| Total equity investments in pooled funds | $ | $ | ||||||||||||||||||||||||

(1)Investments consist of UK property to generate income and capital growth.

(2)This class seeks to generate superior risk-adjusted returns through selective asset sourcing, active trading and hedging strategies across a range of asset types.

(3)This class of funds includes investments in a range of instruments including high-yield bonds, leveraged loans, CLOs, ABS and floating rate notes to generate income and capital appreciation.

(4)This class aims to obtain high long-term returns primarily through credit and preferred equity investments with low liquidity and defined term.

(5)This class seeks to generate returns from insurance markets through investments in catastrophe bonds, life insurance and other insurance linked investments. This investment is restricted in connection with the unwind of certain insurance linked exposures. Ambac has redeemed its investment to the extent permitted by the fund.

(6)This class of funds aim to achieve long term growth through diversified exposure to global equity-markets.

(7)This class of funds includes investments in high quality floating rate debt securities including ABS and corporate floating rate notes.

(8)This class seeks to generate long-term capital appreciation through investments in private equity, equity-related and other instruments.

(9)This class seeks long-term income and growth through investments in the bonds of issuers in emerging markets.

(10)This class seeks to generate total returns from portfolios focused primarily on convertible securities.

The portion of net unrealized gains (losses) related to securities classified as trading and equity securities, excluding those reported using the equity method, still held at the end of each period is as follows:

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||||||||||||

| 2022 | 2021 | 2022 | 2021 | |||||||||||||||||||||||

| Net gains (losses) recognized during the period on trading and equity securities | $ | ( | $ | $ | ( | $ | ||||||||||||||||||||

| Less: net gains (losses) recognized during the reporting period on trading and equity securities sold during the period | ( | ( | ||||||||||||||||||||||||

| Unrealized gains (losses) recognized during the reporting period on trading and equity securities still held at the reporting date | $ | ( | $ | $ | ( | $ | ||||||||||||||||||||

| Ambac Financial Group, Inc. 16 2022 Second Quarter FORM 10-Q |

AMBAC FINANCIAL GROUP, INC. AND SUBSIDIARIES

Notes to Unaudited Consolidated Financial Statements

(Dollar Amounts in Millions, Except Share Amounts)

5. FAIR VALUE MEASUREMENTS

The Fair Value Measurement Topic of the ASC establishes a framework for measuring fair value and disclosures about fair value measurements.

Fair Value Hierarchy:

The Fair Value Measurement Topic of the ASC specifies a fair value hierarchy based on whether the inputs to valuation techniques used to measure fair value are observable or unobservable. Observable inputs reflect market data obtained from independent sources, while unobservable inputs reflect Company-based assumptions. The fair value hierarchy has three broad levels as follows:

| l | Level 1 | Quoted prices for identical instruments in active markets. Assets and liabilities classified as Level 1 include US Treasury and other foreign government obligations traded in highly liquid and transparent markets, certain highly liquid pooled fund investments, exchange traded futures contracts, variable rate demand obligations and money market funds. | |||||||||

| l | Level 2 | Quoted prices for similar instruments in active markets; quoted prices for identical or similar instruments in markets that are not active; and model-derived valuations in which all significant inputs and significant value drivers are observable in active markets. Assets and liabilities classified as Level 2 generally include investments in fixed maturity securities representing municipal, asset-backed and corporate obligations, certain interest rate swap contracts and most long-term debt of variable interest entities consolidated under the Consolidation Topic of the ASC. | |||||||||

| l | Level 3 | Model derived valuations in which one or more significant inputs or significant value drivers are unobservable. This hierarchy requires the use of observable market data when available. Assets and liabilities classified as Level 3 include credit derivative contracts, certain warrants, certain uncollateralized interest rate swap contracts, certain equity investments and certain investments in fixed maturity securities. Additionally, Level 3 assets and liabilities generally include loan receivables, and certain long-term debt of variable interest entities consolidated under the Consolidation Topic of the ASC. | |||||||||

The Fair Value Measurement Topic of the ASC permits, as a practical expedient, the estimation of fair value of certain investments in funds using the net asset value per share of the investment or its equivalent (“NAV”). Investments in funds valued using NAV are not categorized as Level 1, 2 or 3 under the fair value hierarchy. The Investments — Equity Securities Topic of the ASC permits the measurement of certain equity securities without a readily determinable fair value at cost, less impairment, and adjusted to fair value when observable price changes in identical or similar investments from the same issuer occur (the "measurement alternative"). The fair values of investments measured under this measurement alternative are not included in the below disclosures of fair value of financial instruments. The following table sets forth the carrying amount and fair value of Ambac’s financial assets and liabilities as of June 30, 2022 and December 31, 2021, including the level within the fair value hierarchy at which fair value measurements are categorized. As required by the Fair Value Measurement Topic of the ASC, financial assets and liabilities are classified in their entirety based on the lowest level of input that is significant to the fair value measurement.

| Ambac Financial Group, Inc. 17 2022 Second Quarter FORM 10-Q |

AMBAC FINANCIAL GROUP, INC. AND SUBSIDIARIES

Notes to Unaudited Consolidated Financial Statements

(Dollar Amounts in Millions, Except Share Amounts)

| Carrying Amount | Total Fair Value | Fair Value Measurements Categorized as: | ||||||||||||||||||||||||||||||

| June 30, 2022: | Level 1 | Level 2 | Level 3 | |||||||||||||||||||||||||||||

| Financial assets: | ||||||||||||||||||||||||||||||||

| Fixed maturity securities: | ||||||||||||||||||||||||||||||||

| Municipal obligations | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||

| Corporate obligations | ||||||||||||||||||||||||||||||||

| Foreign obligations | ||||||||||||||||||||||||||||||||

| U.S. government obligations | ||||||||||||||||||||||||||||||||

| Residential mortgage-backed securities | ||||||||||||||||||||||||||||||||

| Collateralized debt obligations | ||||||||||||||||||||||||||||||||

| Other asset-backed securities | ||||||||||||||||||||||||||||||||

| Fixed maturity securities, pledged as collateral: | ||||||||||||||||||||||||||||||||

| U.S. government obligations | ||||||||||||||||||||||||||||||||

| Short-term | ||||||||||||||||||||||||||||||||

| Short term investments | ||||||||||||||||||||||||||||||||

Other investments (1) | ||||||||||||||||||||||||||||||||

| Cash, cash equivalents and restricted cash | ||||||||||||||||||||||||||||||||

| Derivative assets: | ||||||||||||||||||||||||||||||||

| Interest rate swaps—asset position | ||||||||||||||||||||||||||||||||

| Warrants | ||||||||||||||||||||||||||||||||

| Other assets-Loans | ||||||||||||||||||||||||||||||||

| Variable interest entity assets: | ||||||||||||||||||||||||||||||||

| Fixed maturity securities: Corporate obligations, fair value option | ||||||||||||||||||||||||||||||||

| Fixed maturity securities: Municipal obligations, available-for-sale | ||||||||||||||||||||||||||||||||

| Restricted cash | ||||||||||||||||||||||||||||||||

| Loans | ||||||||||||||||||||||||||||||||

| Derivative assets: Currency swaps-asset position | ||||||||||||||||||||||||||||||||

| Total financial assets | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||

| Financial liabilities: | ||||||||||||||||||||||||||||||||

| Long term debt, including accrued interest | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||

| Derivative liabilities: | ||||||||||||||||||||||||||||||||

| Interest rate swaps—asset position | ( | ( | ( | |||||||||||||||||||||||||||||

| Interest rate swaps—liability position | ||||||||||||||||||||||||||||||||

| Futures contracts | ||||||||||||||||||||||||||||||||

Liabilities for net financial guarantees written (2) | ( | ( | ( | |||||||||||||||||||||||||||||

| Variable interest entity liabilities: | ||||||||||||||||||||||||||||||||

Long-term debt (includes $ | ||||||||||||||||||||||||||||||||

| Derivative liabilities: Interest rate swaps—liability position | ||||||||||||||||||||||||||||||||

| Total financial liabilities | $ | $ | $ | $ | $ | ( | ||||||||||||||||||||||||||

| Ambac Financial Group, Inc. 18 2022 Second Quarter FORM 10-Q |

AMBAC FINANCIAL GROUP, INC. AND SUBSIDIARIES

Notes to Unaudited Consolidated Financial Statements

(Dollar Amounts in Millions, Except Share Amounts)

| Carrying Amount | Total Fair Value | Fair Value Measurements Categorized as: | ||||||||||||||||||||||||||||||

| December 31, 2021: | Level 1 | Level 2 | Level 3 | |||||||||||||||||||||||||||||

| Financial assets: | ||||||||||||||||||||||||||||||||

| Fixed maturity securities: | ||||||||||||||||||||||||||||||||

| Municipal obligations | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||

| Corporate obligations | ||||||||||||||||||||||||||||||||

| Foreign obligations | ||||||||||||||||||||||||||||||||

| U.S. government obligations | ||||||||||||||||||||||||||||||||

| Residential mortgage-backed securities | ||||||||||||||||||||||||||||||||

| Collateralized debt obligations | ||||||||||||||||||||||||||||||||

| Other asset-backed securities | ||||||||||||||||||||||||||||||||

| Fixed maturity securities, pledged as collateral: | ||||||||||||||||||||||||||||||||

| U.S. government obligations | ||||||||||||||||||||||||||||||||

| Short-term | ||||||||||||||||||||||||||||||||

| Short term investments | ||||||||||||||||||||||||||||||||

Other investments (1) | ||||||||||||||||||||||||||||||||

| Cash, cash equivalents and restricted cash | ||||||||||||||||||||||||||||||||

| Derivative assets: | ||||||||||||||||||||||||||||||||

| Interest rate swaps—asset position | ||||||||||||||||||||||||||||||||

| Other assets-loans | ||||||||||||||||||||||||||||||||

| Variable interest entity assets: | ||||||||||||||||||||||||||||||||

| Fixed maturity securities: Corporate obligations, fair value option | ||||||||||||||||||||||||||||||||

| Fixed maturity securities: Municipal obligations, available-for-sale | ||||||||||||||||||||||||||||||||

| Restricted cash | ||||||||||||||||||||||||||||||||

| Loans | ||||||||||||||||||||||||||||||||

| Derivative assets: Currency swaps—asset position | ||||||||||||||||||||||||||||||||

| Total financial assets | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||

| Financial liabilities: | ||||||||||||||||||||||||||||||||

| Long term debt, including accrued interest | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||

| Derivative liabilities: | ||||||||||||||||||||||||||||||||

| Interest rate swaps—liability position | ||||||||||||||||||||||||||||||||

Liabilities for net financial guarantees written (2) | ( | ( | ( | |||||||||||||||||||||||||||||

| Variable interest entity liabilities: | ||||||||||||||||||||||||||||||||

Long-term debt (includes $ | ||||||||||||||||||||||||||||||||

| Derivative liabilities: Interest rate swaps—liability position | ||||||||||||||||||||||||||||||||

| Total financial liabilities | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||

(1)Excluded from the fair value measurement categories in the table above are investment funds of $518 and $577 as of June 30, 2022 and December 31, 2021, respectively, which are measured using NAV as a practical expedient. Also excluded from the fair value measurements in the table above are equity securities with a carrying value of $8 and $8 as of June 30, 2022 and December 31, 2021, respectively, that do not have readily determinable fair values and have carrying amounts determined using the measurement alternative.

(2)The carrying value of net financial guarantees written includes financial guarantee amounts in the following balance sheet items: Premium receivables; Reinsurance recoverable on paid and unpaid losses; Deferred ceded premium; Subrogation recoverable; Insurance intangible asset; Unearned premiums; Loss and loss expense reserves; Ceded premiums payable, premiums taxes payable and other deferred fees recorded in Other liabilities.

Determination of Fair Value:

When available, Ambac uses quoted active market prices specific to the financial instrument to determine fair value, and classifies such items within Level 1. The determination of fair value for financial instruments categorized in Level 2 or 3 involves judgment due to the complexity of factors contributing to the valuation. Third-party sources from which we obtain independent market quotes also use assumptions, judgments and estimates in

determining financial instrument values and different third parties may use different methodologies or provide different values for financial instruments. In addition, the use of internal valuation models may require assumptions about hypothetical or inactive markets. As a result of these factors, the actual trade value of a financial instrument in the market, or exit value of a financial instrument position by Ambac, may be significantly different from its recorded fair value.

| Ambac Financial Group, Inc. 19 2022 Second Quarter FORM 10-Q |

AMBAC FINANCIAL GROUP, INC. AND SUBSIDIARIES

Notes to Unaudited Consolidated Financial Statements

(Dollar Amounts in Millions, Except Share Amounts)