Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended January 29, 2011

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File No. 1-10738

ANNTAYLOR STORES CORPORATION

(Exact name of registrant as specified in its charter)

| DELAWARE | 13-3499319 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification Number) | |

| 7 Times Square, New York, NY | 10036 | |

| (Address of principal executive offices) | (Zip Code) | |

(212) 541-3300

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class |

Name of each exchange on which registered | |

| Common Stock, $.0068 Par Value | The New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x.

Indicate by check mark whether registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨.

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨.

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨ Smaller reporting company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x.

The aggregate market value of the registrant’s voting stock held by non-affiliates of the registrant as of July 30, 2010 was $1,000,992,916.

The number of shares of the registrant’s common stock outstanding as of February 25, 2011 was 54,324,666.

Documents Incorporated by Reference:

Portions of the Registrant’s Proxy Statement for the Registrant’s 2011 Annual Meeting of Stockholders to be held on May 18, 2011 are incorporated by reference into Part III.

Table of Contents

ANNUAL REPORT ON FORM 10-K INDEX

| Page No. | ||||||||

| ITEM 1. |

2 | |||||||

| ITEM 1A. |

8 | |||||||

| ITEM 1B. |

14 | |||||||

| ITEM 2. |

15 | |||||||

| ITEM 3. |

15 | |||||||

| ITEM 4. |

15 | |||||||

| ITEM 5. |

16 | |||||||

| ITEM 6. |

18 | |||||||

| ITEM 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

20 | ||||||

| ITEM 7A. |

35 | |||||||

| ITEM 8. |

36 | |||||||

| ITEM 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

36 | ||||||

| ITEM 9A. |

36 | |||||||

| ITEM 9B. |

36 | |||||||

| ITEM 10. |

37 | |||||||

| ITEM 11. |

37 | |||||||

| ITEM 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

37 | ||||||

| ITEM 13. |

Certain Relationships and Related Transactions, and Director Independence |

37 | ||||||

| ITEM 14. |

37 | |||||||

| ITEM 15. |

38 | |||||||

| 39 | ||||||||

| 40 | ||||||||

| 77 | ||||||||

1

Table of Contents

Statement Regarding Forward-Looking Disclosures

This Annual Report on Form 10-K (this “Report”) includes, and incorporates by reference, certain forward-looking statements made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. The forward-looking statements may use the words “expect”, “anticipate”, “plan”, “intend”, “project”, “may”, “believe” and similar expressions. These forward-looking statements reflect the current expectations of AnnTaylor Stores Corporation concerning future events and actual results may differ materially from current expectations or historical results. Any such forward-looking statements are subject to various risks and uncertainties, including without limitation those discussed in the sections of this Report entitled “Business”, “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations”. AnnTaylor Stores Corporation does not assume any obligation to publicly update or revise any forward-looking statements at any time for any reason.

| ITEM 1. | Business. |

General

AnnTaylor Stores Corporation, through its wholly-owned subsidiaries, is a leading national specialty retailer of women’s apparel, shoes and accessories sold primarily under the “Ann Taylor” and “LOFT” brands. As used in this report, all references to “we”, “our”, “us” and “the Company” refer to AnnTaylor Stores Corporation and its wholly-owned subsidiaries.

We believe “Ann Taylor” and “LOFT” are highly recognized national brands with distinct fashion points of view, though both are equally committed to providing clients with feminine, fashionable, high-quality merchandise that is relevant to all aspects of their lifestyles. Ann Taylor is an aspirational luxury brand that offers modern style while remaining true to its legacy as a destination for every generation of working women, with timeless wear-now and wear-to-work fashion of impeccable quality at compelling prices. LOFT is the go-to destination for accessible and affordable fashion with a relaxed casual appeal that is distinctly feminine.

Our Ann Taylor and LOFT brands offer a full range of career and casual separates, dresses, tops, weekend wear, shoes and accessories, coordinated as part of a strategy to provide modern styles that are versatile across all occasions and needs. We offer updated past season best sellers from the Ann Taylor and LOFT merchandise collections at our Ann Taylor Factory and LOFT Outlet stores, respectively, and our clients can also shop online at www.anntaylor.com and www.LOFT.com (together, our “Online Stores”) or by phone at 1-800-DIAL-ANN and 1-888-LOFT-444.

We were incorporated in the State of Delaware in 1988 and, as of January 29, 2011, operated 896 retail stores in 46 states, the District of Columbia and Puerto Rico, comprised of 266 Ann Taylor stores, 502 LOFT stores, 92 Ann Taylor Factory stores and 36 LOFT Outlet stores. See “Stores and Expansion” for further discussion.

We are dedicated to maintaining the right merchandise mix in our stores and plan the timing of our merchandise offerings to address clients’ needs, anticipating fabric and yarn preferences on a regional and seasonal basis. Our direct marketing efforts are planned to support this merchandising strategy. Our merchandise, marketing and distribution strategies are reinforced by an emphasis on client service, as our sales associates are trained to assist clients in merchandise selection and wardrobe coordination.

Merchandise Design and Production

Substantially all of our merchandise is developed by our in-house product design and development teams, who design merchandise exclusively for us. Our merchandising groups determine inventory needs for the upcoming season, edit the assortments developed by the design teams, plan monthly merchandise flows and arrange for the production of merchandise by independent manufacturers, primarily through our in-house sourcing group. A small percentage of our merchandise is purchased through branded vendors, which is selected to complement our in-house assortment.

2

Table of Contents

Our production management and quality assurance departments establish the technical specifications for all merchandise and inspect our merchandise for quality, including periodic in-line inspections while goods are in production, to identify potential problems prior to shipment. Upon receipt, merchandise is inspected on a test basis for uniformity of size and color, as well as for conformity with specifications and overall quality of manufacturing.

In Fiscal 2010, we sourced merchandise from approximately 145 manufacturers and vendors in 19 countries, and no single supplier accounted for more than 10% of merchandise purchased on either a unit or cost basis. Approximately 42% of our merchandise unit purchases originated in China (representing approximately 50% of total merchandise cost), 16% in the Philippines (15% of total merchandise cost), 13% in Indonesia (12% of total merchandise cost), 12% in India (11% of total merchandise cost), and 9% in Vietnam (5% of total merchandise cost). Any event causing a sudden disruption of manufacturing or imports from any of these countries, including the imposition of additional import restrictions, could have a material adverse effect on our operations. We generally do not maintain any long-term or exclusive commitments or arrangements to purchase merchandise with any single supplier, but we have taken steps to mitigate sourcing pressures from rising raw material costs by making advance commitments on key core fabrics, leveraging our strong vendor relationships and using country sourcing flexibility. Our foreign purchases are negotiated and paid for in U.S. dollars.

We have a social compliance program that requires our suppliers, factories and subcontractors to comply with our Global Supplier Principles and Guidelines as well as the local laws and regulations in the country of manufacture. We conduct unannounced third-party audits to confirm manufacturer compliance with our compliance standards. We are also a certified and validated member of the United States Customs and Border Protection’s Customs-Trade Partnership Against Terrorism (“C-TPAT”) program and expect all of our suppliers shipping to the United States to adhere to our C-TPAT requirements. These include standards relating to facility security, procedural security, personnel security, cargo security and the overall protection of the supply chain. Audits are conducted to confirm supplier compliance with our compliance standards.

We believe we have solid relationships with our suppliers and that, subject to the discussion in “Statement Regarding Forward-Looking Disclosures”, “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Liquidity and Capital Resources”, we will continue to have adequate sources to produce a sufficient supply of quality merchandise in a timely manner and on satisfactory economic terms.

Inventory Control and Merchandise Allocation

Our planning departments analyze relevant historical product demand data (i.e., sales, margins, sales and inventory history of store clusters, etc.) by brand, size and store location, including our Online Stores, to assist in determining the quantity of merchandise to be purchased for, and the allocation of merchandise to, our channels. Merchandise is allocated to achieve an emphasis that is suited to each store’s client base, including our Online Stores. Merchandise is typically sold at its original marked price for several weeks, with the length of time varying by individual style or color choice and dependent on client acceptance. We review inventory levels on an ongoing basis to identify slow-moving merchandise styles and broken assortments (items no longer in stock in a sufficient range of sizes) and use markdowns to clear this merchandise. Markdowns may also be used if inventory exceeds client demand for reasons of design, seasonal adaptation or changes in client preference, or if it is determined that the inventory will not sell at its currently marked price. Most inventory is cleared in-store, including through our Online Stores.

Our core merchandising system is the central repository for inventory data and related business activities that affect inventory levels such as purchasing, receiving, allocation and distribution. Our primary distribution center is located in Louisville, Kentucky. See “Properties” for further discussion of our Louisville distribution center. The vast majority of our merchandise is processed through our Louisville facility, which is owned and operated by us. Additionally, we contract with a third-party fulfillment vendor and utilize their Bolingbrook, IL facility to fulfill orders for our Online Stores. We also utilize a third-party distribution center bypass facility in Santa Fe Springs, CA. Only select product is processed through this bypass facility, which primarily serves as a disaster recovery facility.

3

Table of Contents

Stores and Expansion

Our business strategy includes a real estate expansion program designed to reach new clients through the opening of new stores. We open new stores in markets that we believe have a sufficient concentration of our target clients. We also add stores, or optimize the size of existing stores, in markets where we already have a presence, as demographic conditions warrant and sites become available. In addition, we reinvest in our current store base to elevate and modernize the in-store experience we provide to our clients.

Store locations are determined on the basis of various factors, including geographic location, demographic studies, anchor tenants in a mall location, other specialty stores in a mall or specialty center location or in the vicinity of a village location and the proximity to professional offices in a downtown or village location. We open our Ann Taylor Factory and LOFT Outlet stores in outlet centers with co-tenants that generally include a significant number of outlet or discount stores operated under nationally recognized upscale brand names. Store size is determined on the basis of various factors, including merchandise needs, geographic location, demographic studies and space availability.

At Ann Taylor, our focus in 2010 was on optimizing store productivity and enhancing the in-store environment of our existing store fleet, while preparing for future store growth through the testing of prototype stores that are approximately 30-40% smaller in size than the fleet average. We converted four existing Ann Taylor stores to this new format during the second half of Fiscal 2010 in various markets. At LOFT, we moved forward with the planned expansion of the brand by opening 10 new LOFT stores and 14 new LOFT Outlet stores. During Fiscal 2011, we expect to further accelerate our planned store growth in the factory outlet channel during the first half of Fiscal 2011 through the opening of 44 stores in premium factory outlet centers across the United States.

In January 2008, we initiated a multi-year, strategic restructuring program (the “Restructuring Program”), a component of which provided for the closing of approximately 225 underperforming stores, of which 137 were closed during the three-year period ending January 29, 2011. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Liquidity and Capital Resources” for further discussion of our Restructuring Program. In addition, during the past two years, we significantly scaled back our new store growth and aggressively pursued renegotiating or extending existing leases at more favorable occupancy rates. During Fiscal 2011, we plan to open approximately 78 stores, which represents a return to more aggressive store growth than we undertook during the economic downturn experienced over the past two years.

As of January 29, 2011, we operated 896 retail stores throughout the United States, the District of Columbia and Puerto Rico, comprised of 266 Ann Taylor stores, 502 LOFT stores, 92 Ann Taylor Factory stores and 36 LOFT Outlet stores.

An average Ann Taylor store is approximately 5,500 square feet in size. We operate two larger Ann Taylor flagship stores, one located in New York City and one located in Chicago. We converted four existing Ann Taylor stores into a new prototype format during the second half of Fiscal 2010 in various markets. Based on the early success of this format, we plan to open approximately 20 new Ann Taylor stores using this new, smaller format during Fiscal 2011. These stores are expected to average 4,000 square feet.

LOFT stores average approximately 5,800 square feet. We also operate one LOFT flagship store on the ground floor of 7 Times Square, our corporate headquarters, in New York City. In Fiscal 2010, we opened 10 LOFT stores that averaged approximately 5,500 square feet and converted six Ann Taylor stores to LOFT stores that averaged 5,000 square feet. In Fiscal 2011, we plan to open approximately 14 LOFT stores, which are expected to average 5,200 square feet.

Ann Taylor Factory stores average approximately 7,300 square feet. As planned, we did not open any Ann Taylor Factory stores in Fiscal 2010. In Fiscal 2011, we plan to open approximately six Ann Taylor Factory stores, which are expected to average 5,600 square feet.

LOFT Outlet stores average approximately 6,500 square feet. In Fiscal 2010, we continued to grow our fleet of LOFT Outlet stores by opening 14 new stores that averaged approximately 6,000 square feet and converting four existing LOFT stores to LOFT Outlet stores. In Fiscal 2011, we plan to open approximately 38 LOFT Outlet stores in leading factory outlet centers across the United States. These stores are expected to average 7,600 square feet.

Our stores typically have approximately 25% of their total square footage allocated to stockroom and other non-selling space.

4

Table of Contents

We believe that our stores are located in some of the most productive retail centers in the United States and that our existing store base is a significant strategic asset of our business. During the past five years, we have invested approximately $370 million in our store base and approximately 56% of our stores are either new, expanded or have been remodeled or refurbished in the last five years.

The following table sets forth certain information regarding store openings, expansions and closings for Ann Taylor stores (“ATS”), LOFT stores (“LOFT”), Ann Taylor Factory stores (“ATF”) and LOFT Outlet stores (“LOS”) over the past five years:

| Fiscal Year |

Total Stores Open at Beginning of Fiscal Year |

No. Stores Opened During Fiscal Year |

No. Stores Closed During Fiscal Year |

No.

Stores Converted During Fiscal Year |

No. Stores Open at End of Fiscal Year |

No. Stores Expanded During Fiscal Year |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ATS | LOFT | ATF | LOS | ATS | LOFT | ATF | ATS | LOFT | LOS | ATS | LOFT | ATF | LOS | Total | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2006 |

824 | 11 | 52 | 7 | — | 20 | 4 | 1 | — | — | — | 348 | 464 | 57 | — | 869 | 16 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 2007 |

869 | 14 | 52 | 11 | — | 13 | 4 | — | — | — | — | 349 | 512 | 68 | — | 929 | 14 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 2008 |

929 | 4 | 25 | 23 | 14 | 33 | 27 | — | — | — | — | 320 | 510 | 91 | 14 | 935 | 5 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 2009 |

935 | — | 9 | 1 | 4 | 18 | 24 | — | -11 | 11 | — | 291 | 506 | 92 | 18 | 907 | 1 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 2010 |

907 | — | 10 | 0 | 14 | 19 | 16 | — | -6 | 2 | 4 | 266 | 502 | 92 | 36 | 896 | 1 | |||||||||||||||||||||||||||||||||||||||||||||||||||

In Fiscal 2010, our total square footage decreased by approximately 64,000 square feet, or approximately 1%, from Fiscal 2009, but remained relatively constant at approximately 5.3 million square feet. During Fiscal 2011, we plan to open 78 stores, close approximately 30 stores, and optimize the size of existing stores primarily through the roll-out of the new, smaller Ann Taylor store format, resulting in a net increase in total square footage of approximately 230,000 square feet, or approximately 4%.

Capital expenditures related to our Fiscal 2010 new stores totaled approximately $25.4 million and expenditures for store remodeling and refurbishment totaled approximately $14.2 million. We expect that capital expenditures for our Fiscal 2011 store expansion program will be approximately $85 million and expenditures for store renovations and refurbishment will be approximately $20 million.

Our store expansion and refurbishment plans are dependent upon, among other things, general economic and business conditions affecting consumer confidence and spending, the availability of desirable locations and the negotiation of acceptable lease terms. See “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Liquidity and Capital Resources”.

Information Systems

During Fiscal 2010, we continued our investment in information services and technology, enhancing the systems we use to support our online, merchandise sourcing, back office and in-store management functions. These enhancements are generally aimed at driving online sales and operational efficiencies while providing speed and flexibility in our supply chain.

Brand Building and Marketing

We believe that our Ann Taylor and LOFT brands are among our most important assets and that these brands and their relationship with our clients are key to our competitive advantage. We continuously evolve these brands to appeal to the changing needs of our target clients and to stay competitive in the market.

We control all aspects of brand development for our retail concepts, including product design, store merchandising and design, channels of distribution and marketing and advertising. We continue to invest in the development of these brands through, among other things, client research, advertising, in-store and direct marketing and our online sites and online marketing initiatives. We also make investments to enhance the overall client experience through the opening of new stores, the expansion and remodeling of existing stores and a focus on client service. In addition, we are strategically focusing on building a multi-channel brand strategy and are making investments to support this initiative.

We believe it is strategically important to communicate on a regular basis directly with our current client base and with potential clients, through national and regional advertising, as well as through direct mail marketing and in-store presentation. Marketing expenditures as a percentage of sales were 4.0% in Fiscal 2010, 3.3% in Fiscal 2009 and 2.8% in Fiscal 2008.

5

Table of Contents

Trademarks, Domain Names and Service Marks

The “AnnTaylor®”, “LOFT®” and “AnnTaylor Loft®” trademarks are registered with the United States Patent and Trademark Office and with the trademark registries of many foreign countries. Our rights in these marks are a significant part of our business, as we believe they are famous and well-known in the women’s apparel industry. Accordingly, we intend to maintain our trademarks and related registrations and vigorously protect them against infringement.

In 2009, we acquired the registered trademark in the People’s Republic of China (“PRC”) for the “Ann Taylor” mark (the “Mark”) in the apparel and footwear class pursuant to a Trademark Assignment Agreement, which assignment was subject to approval by the PRC Trademark Office. Until that approval was received, our existing trademark license agreement permitting our use of the Mark remained in effect. The assignment of the Mark was approved by the PRC Trademark Office in October 2010 and is subject to renewal with the PRC Trademark Office every ten years. The costs of renewal are immaterial, and we intend to renew the Mark indefinitely. In addition, during Fiscal 2010, we obtained ownership of the LOFT.com domain name. See “Statement Regarding Forward-Looking Disclosures” and “Risk Factors”.

Competition

The women’s retail apparel industry is highly competitive. We compete with certain departments in international, national and local department stores and with other specialty stores, catalog and internet businesses that offer similar categories of merchandise. We believe that our focused merchandise selection, versatile fashions and client service distinguish us from other apparel retailers. Our competitors range from smaller, growing companies to considerably larger players with substantially greater financial, marketing and other resources. There is no assurance that we will be able to compete successfully with them in the future. See “Risk Factors” and “Statement Regarding Forward-Looking Disclosures”.

Client Loyalty Programs

We have a credit card program that offers eligible clients the choice of a private label or a co-branded credit card. All new cardholders are automatically enrolled in our exclusive rewards program, which is designed to recognize and promote client loyalty. Both cards can be used at any Ann Taylor or LOFT store location, including Ann Taylor Factory and LOFT Outlet, as well as at our Online Stores. The co-branded credit card can also be used at any other business where the card is accepted. Both cards are offered in an Ann Taylor and LOFT version, depending upon where a client enrolls in the program; however, the core benefits offered to clients are the same for each.

To encourage clients to apply for a credit card, we provide a discount to approved cardholders on all purchases made with a new card in any of our stores on the day of application acceptance. Rewards points are earned on purchases made with the credit card at any of our brands through any of our channels. Co-branded cardholders also earn points on purchases made at other businesses where our card is accepted. Cardholders who accumulate the requisite number of points are issued a Rewards Card redeemable toward a future purchase at Ann Taylor, LOFT, Ann Taylor Factory, LOFT Outlet or either of our Online Stores. In addition to earning points, all participants in the credit card program receive exclusive offers throughout the year. These offers include a Birthday Bonus and exclusive access to shopping events and periodic opportunities to earn bonus points.

Employees

As of January 29, 2011, we had approximately 19,400 employees, of which approximately 1,900 were full-time salaried employees, 1,800 were full-time hourly employees and 15,700 were part-time hourly employees working less than 30 hours per week. None of our employees are represented by a labor union. We believe that our relationship with our employees is good.

6

Table of Contents

Available Information

We make available free of charge on our website, http://investor.anntaylor.com, copies of our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Sections 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, as soon as reasonably practicable after such reports are filed electronically with, or otherwise furnished to, the United States Securities and Exchange Commission. Copies of the charters of each of our Audit Committee, Compensation Committee and Nominating and Corporate Governance Committee, as well as our Corporate Governance Guidelines and Business Conduct Guidelines, are also available on our website.

7

Table of Contents

| ITEM 1A. | Risk Factors. |

The following risk factors should be considered carefully in evaluating our business and the forward-looking information in this document. Please also see “Statement Regarding Forward-Looking Disclosures” in the section immediately preceding Item 1 of this Report. The risks described below are not the only risks our business faces. We may also be adversely affected by additional risks not presently known to us or that we currently deem immaterial.

Our ability to anticipate and respond to changing client preferences and fashion trends in a timely manner

Our success largely depends on our ability to consistently gauge fashion trends and provide a balanced assortment of merchandise that satisfies client demands for each of our brands in a timely manner. Any missteps may affect inventory levels, since we enter into agreements to manufacture and purchase our merchandise well in advance of the applicable selling season. Our failure to anticipate, identify or react appropriately in a timely manner to changes in fashion trends and economic conditions could lead to lower sales, missed opportunities, excess inventories and more frequent markdowns, which could have a material adverse impact on our business. Merchandise missteps could also negatively impact our image with our clients and result in diminished brand loyalty.

The effect of fluctuations in sourcing costs

The raw materials, in particular cotton, silk and wool, used to manufacture our merchandise are subject to availability constraints and price volatility caused by high demand for fabrics, labor conditions, transportation or freight costs, currency fluctuations, weather conditions, supply conditions, government regulations, economic climate and other unpredictable factors. We have taken steps to mitigate sourcing pressures from rising raw material costs by making advance commitments on key core fabrics, leveraging our strong vendor relationships and using country sourcing flexibility. Despite these measures, an increase in the demand for, or the price of, and/or a decrease in the availability of the raw materials used to manufacture our merchandise could have a material adverse effect on our cost of sales or our ability to meet our clients’ needs. Increases in labor costs, especially in China, as well as a shortage of labor in certain areas of China, may also impact our sourcing costs. We may not be able to pass all or a portion of such higher sourcing costs onto our clients, which could negatively impact our profitability.

Our ability to successfully manage store growth and optimize the productivity and profitability of our store portfolio

Our continued growth and success depends, in part, on our ability to successfully open and operate new stores, enhance and remodel existing stores on a timely and profitable basis, and optimize store performance by closing under-performing stores. Accomplishing our store expansion goals depends upon a number of factors, including locating suitable sites and negotiating favorable lease terms. We must also be able to effectively renew and renegotiate lease terms for existing stores. Managing the profitability of our stores and optimizing store productivity will also depend in large part on the continued success and client acceptance of our new Ann Taylor and LOFT store prototypes, as well as our ability to open, achieve and accelerate planned store growth for LOFT Outlet in Fiscal 2011. Hiring and training qualified associates, particularly at the store management level, and maintaining overall good relations with our associates, is also important to our store operations. There is no assurance that we will achieve our store expansion goals, manage our growth effectively or operate our stores profitably.

Our ability to successfully upgrade and maintain our information systems to support the needs of the organization

We rely heavily on information systems to manage our operations, including a full range of retail, financial, sourcing and merchandising systems, and regularly make investments to upgrade, enhance or replace these systems. The reliability and capacity of our information systems is critical. Despite our preventative efforts, our systems are vulnerable from time to time to damage or interruption from, among other things, security breaches, computer viruses, power outages and other technical malfunctions. Any disruptions affecting our information systems, or any delays or difficulties in transitioning to new systems or in integrating them with current systems, could have a material adverse impact on our business. Any failure to maintain adequate system security controls to protect our computer assets and sensitive data, including client data, from unauthorized access, disclosure or use could also damage our reputation with our clients.

8

Table of Contents

We rely on third parties for the implementation and/or management of certain aspects of our information technology infrastructure. Failure by any of these third parties to implement and/or manage our information technology infrastructure effectively could disrupt our operations, adversely affect our customers’ shopping experience and negatively impact our profitability.

In addition, our ability to continue to operate our business without significant interruption in the event of a disaster or other disruption depends in part on the ability of our information systems to operate in accordance with our disaster recovery and business continuity plans.

Our reliance on key management and our ability to retain and attract qualified associates

Our success depends to a significant extent upon both the continued services of our current executive and senior management team, as well as our ability to attract, hire, motivate and retain qualified management talent in the future. Competition for key executives in the retail industry is intense, and our operations could be adversely affected if we cannot retain our key executives or if we fail to attract additional qualified individuals.

Our performance also depends in large part on the talents and contributions of engaged and skilled associates in all areas of our organization. If we are unable to identify, hire, develop, motivate and retain talented individuals, we may be unable to compete effectively and our business could be adversely impacted.

Our reliance on third-party manufacturers and key vendors

We do not own or operate any manufacturing facilities and depend on independent third parties to manufacture our merchandise. We cannot be certain that we will not experience operational difficulties with our manufacturers, such as reductions in the availability of production capacity, errors in complying with merchandise specifications, insufficient quality control and failure to meet production deadlines or increases in manufacturing costs. In addition, we source our merchandise from a select group of manufacturers and we continue to strengthen our relationship with these key vendors. While this strategy has benefits, it also has risks. If one or more of our key vendors were to cease working with us, the flow of merchandise to our stores could be impacted, which could have a material adverse effect on our sales and results of operations. In addition, world-wide economic conditions continue to negatively impact businesses around the world, and the impact of those conditions on our major suppliers cannot be predicted. Our suppliers may be unable to obtain adequate credit or access liquidity to finance their operations. A manufacturer’s failure to ship merchandise to us on a timely basis or to meet the required product safety and quality standards could cause supply shortages, failure to meet client expectations and damage to our brands.

Risks associated with Internet sales

We sell merchandise over the Internet through our Online Stores, www.anntaylor.com and www.LOFT.com. Our Internet operations are subject to numerous risks, including:

| • | the successful implementation of new systems and internet platforms; |

| • | reliance on third-party computer hardware/software; |

| • | reliance on third-party order fulfillment providers; |

| • | rapid technological change; |

| • | diversion of sales from our stores; |

| • | liability for online content; |

| • | violations of state or federal laws, including those relating to online privacy; |

| • | credit card fraud; |

| • | the failure of the computer systems that operate our websites and their related support systems, including computer viruses; and |

| • | telecommunications failures and electronic break-ins and similar disruptions. |

There is no assurance that our Internet operations will continue to achieve sales and profitability growth.

9

Table of Contents

Our reliance on foreign sources of production

We purchase a significant portion of our merchandise from foreign suppliers. As a result, we are subject to the various risks of doing business in foreign markets and importing merchandise from abroad, such as:

| • | fluctuation in the value of the U.S. dollar against foreign currencies or restrictions on the transfer of funds; |

| • | imposition of new legislation relating to import quotas or other restrictions that may limit the quantity of our merchandise that may be imported into the United States from countries in regions where we do business; |

| • | significant delays in the delivery of cargo due to port security considerations; |

| • | imposition of duties, taxes, and other charges on imports; |

| • | imposition of anti-dumping or countervailing duties in response to an investigation as to whether a particular product being sold in the United States at less than fair value may cause (or threaten to cause) material injury to the relevant domestic industry; |

| • | financial or political instability in any of the countries in which our merchandise is manufactured; |

| • | impact of natural disasters and public health concerns on our foreign sourcing offices and vendor manufacturing operations; |

| • | potential cancellation of orders or recalls of any merchandise that does not meet our quality standards; and |

| • | disruption of imports by labor disputes and local business practices. |

Any sudden disruptions in the manufacture or import of our merchandise caused by adverse changes in these or any other factors could increase the cost or reduce the supply of merchandise available to us and adversely affect our business, financial condition, results of operations and liquidity.

Our ability to maintain the value of our brands

Our success depends on the value of our Ann Taylor and LOFT brands. The Ann Taylor and LOFT names are integral to our business as well as to the implementation of our strategies for expanding our business. Maintaining, promoting and growing our brands will depend largely on the success of our design, merchandising, and marketing efforts and our ability to provide a consistent, high quality client experience. Our business could be adversely affected if we fail to achieve these objectives for one or both of our brands and our public image and reputation could be tarnished by negative publicity. Any of these events could negatively impact sales and profitability.

Our ability to manage inventory levels and changes in merchandise mix

The long lead times required for a substantial portion of our merchandise make client demand difficult to predict and responding quickly to changes challenging. Though we have the ability to source certain product categories with shorter lead times, we enter into contracts for a substantial portion of our merchandise well in advance of the applicable selling season. Our financial condition could be materially adversely affected if we are unable to manage inventory levels and respond to short-term shifts in client demand patterns. Inventory levels in excess of client demand may result in excessive markdowns and, therefore, lower than planned gross margin. If we underestimate demand for our merchandise, on the other hand, we may experience inventory shortages resulting in missed sales and lost revenues. Either of these events could significantly affect our operating results and brand image. In addition, our margins may be impacted by changes in our merchandise mix and a shift toward merchandise with lower selling prices. These changes could have a material adverse effect on our results of operations.

The effect of competitive pressures from other retailers

The specialty retail industry is highly competitive. We compete with local, national and international department stores, specialty and discount stores, catalogs and internet businesses offering similar categories of merchandise. Many of our competitors are companies with substantially greater financial, marketing and other resources. Increased levels of promotional activity by our competitors, some of which may be able to adopt more aggressive pricing policies than we can, both online and in stores, may negatively impact our sales and profitability. There is no assurance that we can compete successfully with these companies in the future.

10

Table of Contents

In addition to competing for sales, we compete for favorable store locations, lease terms and qualified associates. Increased competition in these areas may result in higher costs, which could reduce our sales and margins and adversely affect our results of operations.

The effect of general economic conditions and the recent financial crisis

Our financial performance is subject to world-wide economic conditions and the resulting impact on levels of consumer spending, which may remain depressed for the foreseeable future. Some of the factors impacting discretionary consumer spending include general economic conditions, wages and unemployment, consumer debt, reductions in net worth based on recent severe market declines, residential real estate and mortgage markets, taxation, fuel and energy prices, consumer confidence and other macroeconomic factors.

Although the recent global financial crisis eased somewhat in the United States during Fiscal 2010 from the unprecedented levels reached during Fiscal 2008 and Fiscal 2009, world-wide economic conditions remain challenging and consumer spending remains depressed as compared to pre-crisis levels. Consumer purchases of discretionary items, including our merchandise, generally decline during recessionary periods and other periods where disposable income is adversely affected. The downturn in the economy may continue to affect consumer purchases of our merchandise and adversely impact our results of operations and continued growth. It is difficult to predict whether recent improvements in the economic, capital and credit markets will continue or whether such conditions will further deteriorate, as well as the impact this might have on our business.

The impact of a privacy breach and the resulting effect on our business and reputation

As part of our normal course of business, we collect, process and retain sensitive and confidential customer information. Despite the robust security measures we have in place, our facilities and systems, and those of our third-party service providers, may be vulnerable to security breaches, acts of vandalism, computer viruses, misplaced or lost data, programming and/or human errors or other similar events. Any security breach involving the misappropriation, loss or other unauthorized disclosure of confidential information, whether by us or our third-party service providers, could severely damage our reputation and our relationships with our clients, expose us to risks of litigation and liability and adversely affect our business.

Our ability to execute brand extensions and new concepts

Part of our business strategy is to grow our existing brands and identify and develop new growth opportunities. Our success with new merchandise offerings or concepts requires significant capital expenditures and management oversight. Any such plan is subject to risks such as client acceptance, competition and product differentiation. In addition, we face challenges to economies of scale in merchandise sourcing and competition for qualified associates, including management and designers. There is no assurance that these merchandise offerings or concepts will be successful or that our overall profitability will increase as a result. Our failure to successfully execute our growth strategies may adversely impact our financial condition and results of operations.

Uncertain global economic conditions could have a material adverse effect on our liquidity and capital resources

The distress in the financial markets has resulted in extreme volatility in security prices and diminished liquidity and credit availability, and there can be no assurance that our liquidity will not be affected by further volatility in the financial markets and the global economy or that our capital resources will at all times be sufficient to satisfy our liquidity needs. Although we believe that our existing cash and cash equivalents, cash provided by operations and available borrowing capacity under our $250 million Third Amended and Restated Credit Agreement (the “Credit Facility”) will be adequate to satisfy our capital needs for the foreseeable future, any renewed tightening of the credit markets could make it more difficult for us to access funds, enter into agreements for new indebtedness or obtain funding through the issuance of our securities. Our Credit Facility also has financial covenants which, if not met, may further impede our ability to access funds under the Credit Facility.

In addition, we have significant amounts of cash and cash equivalents invested in deposit accounts at FDIC-insured banks. All of our deposit account balances are currently FDIC insured and will remain so through December 31, 2012 as a result of the Dodd-Frank Wall Street Reform and Consumer Protection Act. We also have a small amount of cash and cash equivalents invested in money market funds that are backed by U.S. Treasury Securities as of January 29, 2011. With the continued uncertainty surrounding financial institutions, we cannot be assured that we will not experience losses on any money market holdings.

11

Table of Contents

Manufacturer compliance with our social compliance program requirements

We require our independent manufacturers to comply with the Ann Taylor Global Supplier Principles and Guidelines that cover many areas including labor, health and safety and environmental standards. We monitor their compliance with these Guidelines using third-party monitoring firms. Although we have an active program to provide training for our independent manufacturers and monitor their compliance with these standards, we do not control the manufacturers or their practices. Any failure of our independent manufacturers to comply with our Global Supplier Principles and Guidelines or local laws in the country of manufacture could disrupt the shipment of merchandise to us, force us to locate alternative manufacturing sources, reduce demand for our merchandise or damage our reputation.

Our ability to secure and protect trademarks and other intellectual property rights

We believe that our “AnnTaylor”, “LOFT” and “AnnTaylor Loft” trademarks are important to our success. Even though we register and protect our trademarks and other intellectual property rights, there is no assurance that our actions will protect us from the prior registration by others or prevent others from infringing our trademarks and proprietary rights or seeking to block sales of our products as infringements of their trademarks and proprietary rights. Further, the laws of foreign countries may not protect proprietary rights to the same extent as do the laws of the United States. Because we have not registered all of our trademarks in all categories, or in all foreign countries in which we currently manufacture merchandise or may manufacture or sell merchandise in the future, our ability to pursue international expansion and our sourcing of merchandise from international suppliers could be impacted.

Failure to comply with legal and regulatory requirements

Our policies, procedures and internal controls are designed to comply with all applicable laws and regulations, including those imposed by the U.S. Securities and Exchange Commission and the New York Stock Exchange, as well as applicable employment laws. Any changes in regulations, the imposition of additional regulations or the enactment of any new legislation that affects employment and labor, trade, product safety, transportation and logistics, health care, tax, privacy, or environmental issues, among other things, may increase the complexity of the regulatory environment in which we operate and the related cost of compliance. Failure to comply with such laws and regulations could result in damage to our reputation and negatively impact our financial condition and the market price of our stock.

Our dependence on our Louisville distribution center and third-party transportation companies

Although we have contracted with a third-party distribution service to help manage the flow of inventory to our stores, we handle the majority of merchandise distribution to our stores primarily from our distribution center in Louisville, Kentucky. Independent third-party transportation companies deliver merchandise to our stores and our clients. Any significant interruption in the operation of our Louisville distribution center or the domestic transportation infrastructure due to natural disasters, accidents, inclement weather, system failures, work stoppages, slowdowns or strikes by employees of the transportation companies, or other unforeseen causes could delay or impair our ability to distribute merchandise to our stores, which could result in lower sales, a loss of loyalty to our brands and excess inventory. Furthermore, we are susceptible to increases in fuel and other transportation costs that we may not be able to pass onto our clients, which could adversely affect our results of operations.

The impact on our stock price of fluctuations in our level of sales and earnings growth

A variety of factors have historically affected, and will continue to affect, our comparable sales results and profit margins. These factors include fashion trends and client preferences, changes in our merchandise mix, competition, economic conditions, weather, effective inventory management and new store openings. There is no assurance that we will achieve positive levels of sales and earnings growth, and any decline in our future growth or performance could have a material adverse effect on the market price of our common stock.

Our stock price has experienced, and could continue to experience in the future, substantial volatility as a result of many factors, including global economic conditions, broad market fluctuations, our operating performance and public perception of the prospects for the women’s apparel industry. Failure to meet market expectations, particularly with respect to comparable sales, net revenue, operating margins and earnings per share, would likely result in a decline in the market value of our stock.

12

Table of Contents

Effects of war, terrorism, public health concerns or other catastrophes

Threat of terrorist attacks or actual terrorist events in the United States and world-wide could cause damage or disruption to international commerce and the global economy, disrupt the production, shipment or receipt of our merchandise or lead to lower client traffic in regional shopping centers. Natural disasters and public health concerns, including severe infectious diseases, could also impact our ability to open and run our stores in affected areas and negatively impact our foreign sourcing offices and the manufacturing operations of our vendors. Lower client traffic due to security concerns, war or the threat of war, natural disasters and public health concerns could result in decreased sales that could have a material adverse impact on our business, financial condition and results of operations.

Our ability to sustain the benefits of our restructuring program

Our multi-year, strategic restructuring program, which was initiated in January 2008, was designed to enhance our profitability and improve our overall operating effectiveness. While we have realized significant benefits from our restructuring program to date, our ability to sustain these benefits over time may depend on various factors, in particular our ability to maintain discipline in our approach to new store openings, variations in which could impose unexpected costs and/or delays. Further, to the extent we are unable to improve our financial performance, further restructuring measures may be required in the future. In addition, as part of our store fleet optimization plan, we have, and may continue to, sublease certain closing store locations to third parties. If our sub-lessees default in their rental payment obligations under the sublease agreements, we may be adversely impacted.

Our ability to realize deferred tax assets

If our business does not perform well, we may be required to establish a valuation allowance against our deferred tax assets, which could have a material adverse effect on our results of operations and financial condition. Deferred tax assets represent the tax effect of the differences between the book and tax basis of assets and liabilities. Deferred tax assets are assessed periodically by management to determine if they are realizable. Factors in management’s determination consist of the performance of the business, including the ability to generate taxable income from operations, and tax planning strategies. If, based on available information, it is more likely than not that a deferred tax asset will not be realized, then a valuation allowance would be required with a corresponding charge to income tax expense, thereby reducing net income.

The effect of external economic factors on our Pension Plan

Our future funding obligations with respect to our defined benefit Pension Plan, which was frozen in 2007, will depend upon the future performance of assets set aside for this Pension Plan, interest rates used to determine funding levels, actuarial data and experience and any changes in government laws and regulations. Our Pension Plan holds mutual funds which invest in equity securities. If the market values of these securities decline, our pension expense would increase and, as a result, could adversely affect our business. Decreases in interest rates or asset returns could also increase our obligations under the Pension Plan. Although no additional benefits have been earned under the Pension Plan since it was frozen, depending on the Pension Plan’s funded status, there may be ongoing contribution obligations and those obligations could be material.

Our dependence on shopping malls and other retail centers to attract customers to our stores

Many of our stores are located in shopping malls and other retail centers. Sales at these stores benefit from the ability of “anchor” retail tenants, generally large department stores, and other attractions to generate sufficient levels of consumer traffic in the vicinity of our stores. Any declines in the volume of consumer traffic at shopping centers, whether because of the slowdown in the economy, a falloff in the popularity of shopping centers or otherwise, may result in reduced sales at our stores and leave us with excess inventory. We may have to respond by increasing markdowns or initiating marketing promotions to reduce excess inventory, which could materially adversely impact our margins and operating results.

The impact of potential consolidation of commercial and retail landlords

Continued consolidation in the commercial retail real estate market could affect our ability to successfully negotiate favorable rental terms for our stores in the future. Should significant consolidation continue, a large proportion of our store base could be concentrated with one or a few entities that could then be in a position to dictate unfavorable terms to us due to their significant negotiating leverage. If we are unable to negotiate favorable rental terms with these entities, this could affect our ability to profitably operate our stores, which could adversely impact our business, financial condition and results of operations.

13

Table of Contents

| ITEM 1B. | Unresolved Staff Comments. |

None.

14

Table of Contents

| ITEM 2. | Properties. |

As of January 29, 2011, we operated 896 retail stores in 46 states, the District of Columbia and Puerto Rico, all of which were leased. Store leases typically provide for initial terms of ten years, although some leases have shorter or longer initial periods. Some of the leases grant us the right to extend the term for one or two additional five-year periods. Some leases also contain early termination options, which can be exercised by us under specific conditions. Most of the store leases require us to pay a specified minimum rent, plus a contingent rent based on a percentage of the store’s net sales in excess of a specified threshold. Most of the leases also require us to pay real estate taxes, insurance and certain common area and maintenance costs. The current terms of our leases expire as follows:

| Fiscal Years Lease Terms Expire |

Number of Stores |

|||

| 2011 - 2013 |

370 | |||

| 2014 - 2016 |

306 | |||

| 2017 - 2019 |

187 | |||

| 2020 and later |

33 | |||

We lease our corporate offices at 7 Times Square in New York City (approximately 297,000 square feet) under a lease expiring in 2020. In addition, in Milford, Connecticut, we maintain 42,000 square feet of office space under a lease which expires in 2019.

The Company’s wholly owned subsidiary, AnnTaylor Distribution Services, Inc., owns our 256,000 square foot distribution center located in Louisville, Kentucky. The distribution center is located on approximately 27 acres, which could accommodate possible future expansion of the facility. Nearly all our merchandise is distributed to stores, including our Online Stores, through this facility.

| ITEM 3. | Legal Proceedings. |

We are subject to various legal proceedings and claims that arise in the ordinary course of our business. Although the amount of any liability that could arise with respect to these actions cannot be determined with certainty, in our opinion, any such liability will not have a material adverse effect on our consolidated financial position, consolidated results of operations or liquidity.

| ITEM 4. | (Removed and Reserved). |

15

Table of Contents

| ITEM 5. | Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. |

Our common stock is listed and traded on the New York Stock Exchange under the symbol “ANN”. The number of holders of record of common stock at February 25, 2011 was 603. The following table sets forth the high and low sale prices per share of our common stock on the New York Stock Exchange for the periods indicated:

| Market Price | ||||||||

| High | Low | |||||||

| Fiscal Year 2010 |

||||||||

| Fourth quarter |

$ | 28.24 | $ | 20.97 | ||||

| Third quarter |

23.81 | 14.59 | ||||||

| Second quarter |

25.24 | 15.14 | ||||||

| First quarter |

24.75 | 12.57 | ||||||

| Fiscal Year 2009 |

||||||||

| Fourth quarter |

$ | 16.26 | $ | 11.59 | ||||

| Third quarter |

17.50 | 11.41 | ||||||

| Second quarter |

12.26 | 6.33 | ||||||

| First quarter |

7.58 | 2.41 | ||||||

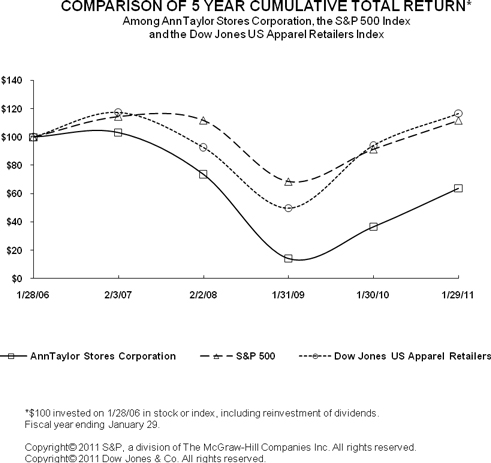

STOCK PERFORMANCE GRAPH

The following graph compares the percentage changes in the cumulative total stockholder return on the Company’s Common Stock for the five-year period ended January 29, 2011, with the cumulative total return on the Standard & Poor’s 500 Stock Index (“S&P 500”) and the Dow Jones U.S. Retailers, Apparel Index for the same period. In accordance with the rules of the Securities and Exchange Commission, the returns are indexed to a value of $100 at January 27, 2006 and assume that all dividends, if any, were reinvested. This performance graph shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), or otherwise subject to the liabilities under that Section, and shall not be deemed to be incorporated by reference into any filing of the Company under the Securities Act of 1933, as amended, or the Exchange Act.

16

Table of Contents

We have never paid cash dividends on our common stock. Any determination to pay cash dividends is at the discretion of our Board of Directors, which considers it on a periodic basis. In addition, as a holding company, our ability to pay dividends is dependent upon the receipt of dividends or other payments from our subsidiaries, including our wholly owned subsidiary AnnTaylor, Inc. The payment of dividends by AnnTaylor, Inc. to us is subject to certain restrictions under its Credit Facility. We are also subject to certain restrictions contained in the Credit Facility on the payment of cash dividends on our common stock. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations - Liquidity and Capital Resources”.

The following table sets forth information concerning purchases of our common stock for the periods indicated, which upon repurchase, are classified as treasury shares available for general corporate purposes:

| Total Number of Shares Purchased (1) |

Average Price Paid Per Share |

Total Number of Shares Purchased as Part of Publicly Announced Program (2) |

Approximate Dollar Value of Shares that May Yet Be Purchased Under Publicly Announced Program |

|||||||||||||

| (in thousands) | ||||||||||||||||

| October 31, 2010 to November 27, 2010 |

6,561 | $ | 23.48 | — | $ | 239,299 | ||||||||||

| November 28, 2010 to January 1, 2011 |

2,188,414 | 26.93 | 2,187,500 | 180,387 | ||||||||||||

| January 2, 2011 to January 29, 2011 |

814,631 | 26.18 | 813,504 | 159,083 | ||||||||||||

| 3,009,606 | 3,001,004 | |||||||||||||||

| (1) | Includes a total of 8,602 shares of restricted stock purchased in connection with employee tax withholding obligations under employee equity compensation plans, which are not purchases under the Company’s publicly announced program. |

| (2) | On August 19, 2010, our Board of Directors approved a $100 million expansion of our existing securities repurchase program (the “Repurchase Program”) to a total of $400 million, increasing the remaining amount then available for share repurchases under the Repurchase Program to approximately $259.1 million. The Repurchase Program will expire when we have repurchased all securities authorized for repurchase thereunder, unless terminated earlier by our Board of Directors. We repurchased 3,001,004 shares under the Repurchase Program during the fourth quarter of Fiscal 2010. On March 8, 2011, our Board of Directors approved an additional $200 million expansion of the Repurchase Program, bringing the total authorized under the Repurchase Program to $600 million. As of the date of this filing, approximately $259.1 million remained available under the Repurchase Program. |

The information called for by this item relating to “Securities Authorized for Issuance under Equity Compensation Plans” is provided in Item 12.

17

Table of Contents

| ITEM 6. | Selected Financial Data. |

The following historical Consolidated Statements of Operations and Consolidated Balance Sheet information has been derived from our audited consolidated financial statements. The information set forth below should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and notes thereto included elsewhere in this document. All references to years are to our fiscal year, which ends on the Saturday nearest January 31 in the following calendar year. All fiscal years for which financial information is set forth below contain 52 weeks, except for the fiscal year ended February 3, 2007, which includes 53 weeks.

| Fiscal Year Ended | ||||||||||||||||||||

| January 29, 2011 |

January 30, 2010 |

January 31, 2009 |

February 2, 2008 |

February 3, 2007 |

||||||||||||||||

| (in thousands, except per share, per square foot and number of stores data) | ||||||||||||||||||||

| Consolidated Statements of Operations Information: |

||||||||||||||||||||

| Net sales |

$ | 1,980,195 | $ | 1,828,523 | $ | 2,194,559 | $ | 2,396,510 | $ | 2,342,907 | ||||||||||

| Cost of sales |

876,201 | 834,188 | 1,139,753 | 1,145,246 | 1,085,897 | |||||||||||||||

| Gross margin |

1,103,994 | 994,335 | 1,054,806 | 1,251,264 | 1,257,010 | |||||||||||||||

| Selling, general and administrative expenses |

978,580 | 966,603 | 1,050,560 | 1,061,869 | 1,031,341 | |||||||||||||||

| Restructuring charges |

5,624 | 36,368 | 59,714 | 32,255 | — | |||||||||||||||

| Asset impairment charges |

— | 15,318 | 29,590 | 1,754 | 1,832 | |||||||||||||||

| Goodwill impairment charge |

— | — | 286,579 | — | — | |||||||||||||||

| Operating income/(loss) |

119,790 | (23,954 | ) | (371,637 | ) | 155,386 | 223,837 | |||||||||||||

| Interest income |

964 | 935 | 1,677 | 7,826 | 17,174 | |||||||||||||||

| Interest expense |

1,632 | 3,091 | 1,462 | 2,172 | 2,230 | |||||||||||||||

| Income/(loss) before income taxes |

119,122 | (26,110 | ) | (371,422 | ) | 161,040 | 238,781 | |||||||||||||

| Income tax provision/(benefit) |

45,725 | (7,902 | ) | (37,516 | ) | 63,805 | 95,799 | |||||||||||||

| Net income/(loss) |

$ | 73,397 | $ | (18,208 | ) | $ | (333,906 | ) | $ | 97,235 | $ | 142,982 | ||||||||

| Basic earnings/(loss) per share (1) |

$ | 1.26 | $ | (0.32 | ) | $ | (5.82 | ) | $ | 1.52 | $ | 1.98 | ||||||||

| Diluted earnings/(loss) per share (1) |

$ | 1.24 | $ | (0.32 | ) | $ | (5.82 | ) | $ | 1.51 | $ | 1.96 | ||||||||

| Weighted average shares outstanding |

57,203 | 56,782 | 57,366 | 62,753 | 70,993 | |||||||||||||||

| Weighted average shares outstanding, assuming dilution |

58,110 | 56,782 | 57,366 | 63,212 | 71,721 | |||||||||||||||

| Consolidated Operating Information: |

||||||||||||||||||||

| Percentage increase/(decrease) in comparable sales (2) |

10.7 | % | (17.4 | )% | (13.4 | )% | (2.2 | )% | 4.5 | % | ||||||||||

| Net sales per square foot (3) |

$ | 337 | $ | 311 | $ | 372 | $ | 435 | $ | 458 | ||||||||||

| Number of stores: |

||||||||||||||||||||

| Open at beginning of period |

907 | 935 | 929 | 869 | 824 | |||||||||||||||

| Opened during the period |

24 | 14 | 66 | 77 | 70 | |||||||||||||||

| Closed during the period |

35 | 42 | 60 | 17 | 25 | |||||||||||||||

| Open at the end of the period |

896 | 907 | 935 | 929 | 869 | |||||||||||||||

| Expanded during the period |

1 | 1 | 5 | 14 | 16 | |||||||||||||||

| Total store square footage at end of period |

5,284 | 5,348 | 5,492 | 5,410 | 5,079 | |||||||||||||||

| Capital expenditures (4) |

$ | 64,367 | $ | 35,736 | $ | 100,195 | $ | 145,852 | $ | 165,129 | ||||||||||

| Depreciation and amortization |

$ | 95,523 | $ | 104,351 | $ | 122,222 | $ | 116,804 | $ | 105,890 | ||||||||||

| Working capital turnover (5) |

8.0 | x | 10.5 | x | 14.0 | x | 8.2 | x | 5.8 | x | ||||||||||

| Inventory turnover (6) |

4.8 | x | 4.9 | x | 5.4 | x | 4.7 | x | 5.0 | x | ||||||||||

| Consolidated Balance Sheet Information: |

||||||||||||||||||||

| Working capital |

$ | 268,005 | $ | 229,521 | $ | 118,013 | $ | 195,015 | $ | 391,187 | ||||||||||

| Goodwill |

— | — | — | 286,579 | 286,579 | |||||||||||||||

| Total assets |

926,820 | 902,141 | 960,439 | 1,393,755 | 1,568,503 | |||||||||||||||

| Total debt |

5,180 | 2,642 | 7,039 | — | — | |||||||||||||||

| Total stockholders’ equity |

423,445 | 417,186 | 416,512 | 839,484 | 1,049,911 | |||||||||||||||

(Footnotes on following page)

18

Table of Contents

(Footnotes for preceding page)

| (1) | We adopted amendments to Accounting Standards Codification (“ASC”) 260-10 on February 1, 2009, which impacted the determination and reporting of earnings per share by requiring the inclusion of restricted stock and performance restricted stock as participating securities, since they have the right to share in dividends, if declared, equally with common shareholders. During periods of net income, participating securities are allocated a proportional share of net income determined by dividing total weighted average participating securities by the sum of total weighted average common shares and participating securities (“the two-class method”). During periods of net loss, no effect is given to the participating securities because they do not share in the losses of the Company. Including these shares in our earnings per share calculation during periods of net income has the effect of diluting both basic and diluted earnings per share. As a result of adopting the amendments to ASC 260-10, prior period basic and diluted shares outstanding, as well as the related per share amounts presented in the preceding table, were adjusted retroactively. |

The retroactive application of the two-class method resulted in a change to previously reported basic earnings per share for Fiscal 2007 and Fiscal 2006 from $1.55 to $1.52 and from $2.01 to $1.98, respectively. There was no change to previously reported basic earnings per share for Fiscal 2008 due to the net loss for the period.

The retroactive application of the two-class method resulted in a change to previously reported diluted earnings per share for Fiscal 2007 and Fiscal 2006 from $1.53 to $1.51 and from $1.98 to $1.96, respectively. There was no change to previously reported diluted earnings per share for Fiscal 2008 due to the net loss for the period.

| (2) | Comparable sales provides a measure of existing store sales performance. A store is included in comparable sales in its thirteenth month of operation. A store with a square footage change greater than 15% is treated as a new store for the first year following its reopening. In addition, in a year with 53 weeks, sales in the last week of that year are excluded from comparable sales. During Fiscal 2010, we began including sales from our Online Stores in comparable sales. All prior year comparable sales figures were adjusted retroactively. |

| (3) | Net sales per average gross square foot is determined by dividing net sales for the period by the average monthly gross square footage for the period. Unless otherwise indicated, references herein to square feet are to gross square feet, rather than net selling space. Sales from our Online Stores are excluded from the net sales per average gross square foot calculations. |

During Fiscal 2010, we revised the calculation of net sales per average gross square foot from one that calculated the average of the gross square feet at the beginning and end of each period to one using the average monthly gross square footage for the period. All prior period amounts have been adjusted to conform to the current period presentation.

| (4) | Capital expenditures are accounted for on the accrual basis and include net non-cash transactions totaling $3.2 million, $(2.8) million, $(10.1) million, $5.9 million, and $(0.8) million in Fiscal 2010, 2009, 2008, 2007 and 2006, respectively. The non-cash transactions are primarily related to the purchase of property and equipment on account. |

| (5) | Working capital turnover is determined by dividing net sales by the average of the amount of working capital at the beginning and end of the period. |

| (6) | Inventory turnover is determined by dividing cost of sales by the average of the cost of inventory at the beginning and end of the period. |

19

Table of Contents

| ITEM 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations. |

The following discussion and analysis should be read together with our consolidated financial statements and related notes thereto included elsewhere in this Annual Report on Form 10-K.

Management Overview

Our key priorities in Fiscal 2010 included delivering top-line growth at both our Ann Taylor and LOFT brands and maximizing gross margin performance. To drive this growth, we continued to focus on delivering compelling and relevant product assortments at both brands. In addition, we also developed and tested new store formats at both brands, designed to reflect our evolved product aesthetic, maximize store sales productivity and provide our clients with a more engaging in-store experience. These efforts paid off, and despite continued economic pressures, our results for Fiscal 2010 reflected substantial improvement in operating profit. This was due to the combined impact of profitable sales growth, particularly at Ann Taylor stores and in our e-commerce and factory outlet channels at both brands, as well as the benefit of increased SG&A cost leverage and continued expense management across the Company. Our focus on improving top-line productivity resulted in net sales growth of 8.3% to $1.98 billion, which contributed to a record gross margin rate of 55.8% for the fiscal year. Net income also increased significantly, to $73.4 million for Fiscal 2010.

At the Ann Taylor brand, we experienced building sales momentum throughout the year. Our merchandise assortments in 2010 leveraged the success and learnings from our 2009 evolution of the brand and, as a result, were chic, relevant and compelling. This, combined with a highly-effective marketing strategy, resulted in strong full-price sell-through and consistent double-digit comparable sales growth each quarter during Fiscal 2010, which contributed to strong gross margin performance throughout the year. Comparable sales for the brand increased 18.7% in Fiscal 2010, with a 19.3% increase at Ann Taylor stores, a 54.3% increase at anntaylor.com and a 9.3% increase at Ann Taylor Factory stores.

At LOFT, we continued to focus on delivering our client feminine, casual fashion at great value. Our merchandise assortments were well-received at LOFT.com and LOFT Outlet, which contributed to significant sales growth in these channels. At our LOFT stores channel, we experienced some pressure beginning in the second quarter, due to a merchandise mix that lacked balance between fashion and key items. In addition, consumers in the middle-income bracket continued to struggle under macroeconomic pressures and remained highly selective and more incentive-driven in their purchases, which further impacted our business. As a result of these factors, we were more promotional at LOFT stores, particularly in the latter half of Fiscal 2010, which impacted gross margin performance. Comparable sales for the brand were up 5.0% in Fiscal 2010, with a 0.5% increase at LOFT stores, a 65.3% increase at LOFTonline.com and a 21.2% increase at LOFT Outlet.

Throughout the year, we remained committed to maintaining a healthy balance sheet and cash position and, as a result, closed the year with $227 million in cash and no bank debt. In addition, during the second half of Fiscal 2010, we repurchased 4.2 million shares of our stock, at a cost of $100 million, to further return value to our shareholders. We also continued to closely manage our inventory levels throughout the year, with an intent to keep inventories approximately in-line with our comparable sales expectations. We were successful in this regard, and ended the year with total inventory per square foot up 14%, excluding e-commerce, in line with our comparable sales performance and also reflecting incremental inventory build to support our plans to open 44 factory outlet stores in the first half of Fiscal 2011. Fiscal 2010 also marked the last year of our multi-year strategic restructuring program, and our results reflect the benefit of approximately $125 million in ongoing, annualized cost savings, of which approximately $20 million were first realized in Fiscal 2010.

Our Fiscal 2010 real estate growth strategy remained focused on supporting our brand objectives, while we continued to enhance the overall productivity of our fleet through the execution of selective store closures associated with our restructuring program. At the Ann Taylor brand, our 2010 goals focused on optimizing store productivity and enhancing the in-store environment of our existing fleet. To this end, the brand opened four prototype stores during Fiscal 2010, which were approximately 30-40% smaller than the fleet average and had an updated aesthetic. At LOFT, we moved forward with the 2010 expansion of the LOFT brand store fleet, opening 10 new LOFT stores, 14 new LOFT Outlet stores, and converting 4 LOFT stores to LOFT Outlet stores.

Overall, our businesses experienced substantial improvement in both sales and profitability during Fiscal 2010 as compared to last year. Looking ahead, we expect our performance in Fiscal 2011 will benefit from continued momentum at the Ann Taylor brand and improved top-line and bottom-line results at the LOFT brand, mainly due to improvements to the merchandise mix at LOFT stores.

20

Table of Contents

Key Performance Indicators

In evaluating our performance, senior management reviews certain key performance indicators, including: