UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

|

Investment Company Act file number |

811-06292 | |||||||

|

| ||||||||

|

UBS Investment Trust | ||||||||

|

(Exact name of registrant as specified in charter) | ||||||||

|

| ||||||||

|

1285 Avenue of the Americas, New York, New York |

|

10019-6028 | ||||||

|

(Address of principal executive offices) |

|

(Zip code) | ||||||

|

| ||||||||

|

Keith A. Weller, Esq. UBS Asset Management One North Wacker Drive Chicago, IL 60606 | ||||||||

|

(Name and address of agent for service) | ||||||||

|

| ||||||||

|

Copy to: | ||||||||

|

Stephen H. Bier, Esq. Dechert LLP 1095 Avenue of the Americas New York, NY 10036-6797 | ||||||||

|

| ||||||||

|

Registrant’s telephone number, including area code: |

212-821 3000 |

| ||||||

|

| ||||||||

|

Date of fiscal year end: |

August 31 |

| ||||||

|

| ||||||||

|

Date of reporting period: |

August 31, 2019 |

| ||||||

Item 1. Reports to Stockholders.

(a) Copy of the report transmitted to shareholders:

UBS U.S. Allocation Fund

Annual Report | August 31, 2019

UBS U.S. Allocation Fund

October 1, 2019

Dear shareholder,

We present you with the annual report for UBS U.S. Allocation Fund (the "Fund") for the 12 months ended August 31, 2019.

Performance

Over the 12 months ended August 31, 2019, the Fund's Class A shares returned 0.84% before deducting the maximum sales charge and returned -4.71% after deducting the maximum sales charge. During the same period, the Fund's primary benchmark, the S&P 500 Index,1 which tracks large cap US equities, returned 2.92%. Since the Fund invests in both stocks and bonds, we believe it is appropriate to also compare its performance to the UBS U.S. Allocation Fund Benchmark (the Fund's secondary benchmark),2 which returned 4.59% during the period. (Returns for all share classes over various time periods and descriptions of the indices are shown in "Performance at a glance" on page 6; please note that the returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares.)

Market commentary

In July 2019, the US economy reached a new record for the longest expansion on record, exceeding the previous mark of 120 months.3 However, trade conflicts, less robust manufacturing activity and several other factors have led to moderating global growth. Looking back, the US Commerce Department reported that gross domestic product ("GDP") grew at 3.4% and 2.2% seasonally adjusted annualized rates during the third and fourth quarters of 2018, respectively. GDP growth then bounced back to 3.1% during the first quarter of 2019. Finally, the US Commerce Department's final reading for second quarter 2019 GDP growth—released after the reporting period ended—was 2.0%.4

Headwinds facing the economy were acknowledged by the US Federal Reserve Board (the "Fed"). After raising interest rates four times in 2018, in July 2019 the Fed started to reverse course, saying it would pause from additional rate hikes as it monitored incoming economic data. At its meeting that concluded on March 20, 2019, most Federal Open Market Committee ("FOMC")5 members indicated that they did not feel additional rate hikes would be needed in 2019. After its June 2019 meeting, Fed Chair Jerome Powell said, "The case for somewhat more accommodative policy has strengthened" and the market anticipated one or two rate cuts by the end of the year. At its meeting in July 2019, the Fed lowered its target rate from a range between 2.25% and 2.50% to a range

UBS U.S. Allocation Fund

Investment Objective:

Total return, consisting of long-term capital appreciation and current income

Portfolio Managers:

Alan Zlatar

Paul Lang

UBS Asset Management

(Americas) Inc.

Commencement:

Class A—May 10, 1993

Class P (formerly Class Y)—May 10, 1993

Dividend payments:

Annually, if any

1 The S&P 500 Index is an unmanaged, weighted index composed of 500 widely held common stocks varying in composition and is not available for direct investment. Investors should note that indices do not reflect the deduction of fees and expenses.

2 The UBS U.S. Allocation Fund Benchmark is an unmanaged benchmark compiled by the Advisor, constructed as follows: from July 22, 1992 (the Fund's inception) until February 29, 2004: 100% S&P 500 Index; from March 1, 2004 until May 31, 2005: 65% Russell 3000 Index, 30% Blomberg Barclays US Aggregate Index and 5% BofA Merrill Lynch US High Yield Cash Pay Index; and from June 1, 2005 until present: 65% Russell 3000 Index, 30% Bloomberg Barclays US Aggregate Index and 5% BofA Merrill Lynch US High Yield Cash Pay Constrained Index. Investors should note that indices do not reflect the deduction of fees and expenses.

3 Source: The National Bureau of Economic Research, 7/19

4 Based on the Commerce Department's final reading announced on September 26, 2019.

5 The Federal Open Market Committee ("FOMC") is a policy-making body of the Federal Reserve System responsible for the formulation of a policy designed to promote economic growth, full employment, stable prices and a sustainable pattern of international trade and payments.

1

UBS U.S. Allocation Fund

between 2.00% and 2.25%. This marked the first rate cut since 2008. Finally, the Fed again lower rates at its meeting in September 2019 (after the reporting period ended), pushing the target rate to a range between 1.75% and 2.00%.

The US equity market posted a modest gain during the reporting period. US equities experienced several periods of elevated volatility over the period. This was driven by a variety of issues, including the ongoing trade conflict between the US and China, signs of slowing global growth, questions regarding future Fed policy actions and a host of geopolitical issues. Collectively, these factors largely offset a number of sharp rallies and periods of robust investor risk appetite. All told, the S&P 500 Index6 gained 2.92% during the 12 months ended August 31, 2019.

The global fixed income market posted solid results during the reporting period. In the US, both short- and long-term Treasury yields declined (bond yields and prices move in the opposite direction). Periods of investor risk aversion, the Fed's monetary policy reversal and modest inflation helped to push yields lower. For the 12 month reporting period as a whole, the yield on the US 10-year Treasury fell from 2.86% to 1.50%. Government bond yields outside the US also generally moved lower, as the European Central Bank, the Bank of Japan and the Bank of England largely maintained their accommodative monetary policies. The overall US bond market, as measured by the Bloomberg Barclays US Aggregate Index,7 returned 10.17% for the 12 months ended August 31, 2019. Returns of riskier fixed income securities were also positive. High yield bonds, as measured by the ICE BofAML US High Yield Cash Pay Constrained Index,8 returned 6.62% during the reporting period. Elsewhere, emerging markets debt, as measured by the J.P. Morgan Emerging Markets Bond Index Global (EMBI Global),9 gained 13.11%.

Portfolio commentary

What worked

• In the US Equity Core portion of the Fund, stock selection in the financials and information technology sectors were the largest contributors to performance. On an individual stock basis, the largest contributors included:

• Universal Display Corp. outperformance was driven by a strong quarterly earnings reports coupled with better than expected guidance for 2019. The company saw 2019 as a year of growth after a sluggish 2018 in the adoption of OLED displays in smartphones, TVs and some laptop computers. Particularly exciting is the launch of foldable smartphones which dramatically increase the display area of phones and, correspondingly, Universal Displays sales of its organic phosphors for those displays.

• Marsh and McLennan outperformed the broader market over the past year. We believe the stock's outperformance is a result of Marsh and McLennan's solid organic growth and margin expansion, supplemented by additional acquisition-fueled earnings and high levels of free cash flow distribution to shareholders from a global franchise that has a below-average correlation with growing global GDP growth concerns. The

6 The S&P 500 Index is an unmanaged, weighted index composed of 500 widely held common stocks varying in composition and is not available for direct investment. Investors should note that indices do not reflect the deduction of fees and expenses.

7 The Bloomberg Barclays US Aggregate Index is an unmanaged broad based index designed to measure the US dollar-denominated, investment-grade, taxable bond market. The index includes bonds from the Treasury, government-related, corporate, mortgage-backed, asset-backed and commercial mortgage-backed sectors. Investors should note that indices do not reflect the deduction of fees and expenses.

8 The ICE BofAML US High Yield Cash Pay Constrained Index is an unmanaged index of publicly placed, non-convertible, coupon-bearing US dollar denominated, below investment grade corporate debt with a term to maturity of at least one year. The index is market capitalization weighted, so that larger bond issuers have a greater effect on the index's return. However, the representation of any single bond issuer is restricted to a maximum of 2% of the total index. Investors should note that indices do not reflect the deduction of fees and expenses.

9 The J.P. Morgan Emerging Markets Bond Index Global (EMBI Global) is an unmanaged index which is designed to track total returns for US dollar denominated debt instruments issued by emerging market sovereign and quasi-sovereign entities: Brady bonds, loans and Eurobonds. Investors should note that indices do not reflect the deduction of fees and expenses.

2

UBS U.S. Allocation Fund

acquisition of JLT, a mid-sized UK-based competitor, further reinforces our thesis that MMC can grow its core EPS by ~10% through most economic cycles and will, therefore, remain a secular winner relative to the rest of the market.

• Shares of AGCO benefited as the company continued to deliver strong quarterly reports. We believe that company's valuation continues to be attractive and see the potential to exceeded consensus profitability estimates through a combination of new product launches, the creation of a global production platform and cost savings.

• In the US Equity Core portion of the Fund, an overweight in the real estate sector was positive for performance.

• In the US growth equity portion of the Fund, an overweight to communication services contributed to performance. Security selection within information technology, health care and consumer discretionary was also a positive for performance. Several holdings were additive to performance on a relative basis including:

• Shares of Dollar General outperformed as it is considered a defensive growth asset with minimal exposure to tariffs and less sensitivity to weaker consumer environments due to trade-related effects.

• Shares of Universal Display Corp. rallied given strong earnings results and improved full year guidance amid a broad rebound in the display and smartphone sector in 2019 from a weak fourth quarter of 2018. We continue to believe that the company remains well positioned to benefit from continued penetration of organic light-emitting diode ("OLED") screens in handsets and TVs.

• Marvell Technology Group outperformed on improving sentiment around the company's 5G position, with wins announced at Samsung and another large provider, as well as a bright outlook. These wins could provide a material revenue tailwind to Marvell Technology Group over the next several years. Given this, and the potential for improved cyclical storage performance later in 2019, we continue to view the risk reward profile favorably.

What didn't work

• Overall, asset allocation detracted from performance during the reporting period.10

– We began the reporting period overweight equities and underweight fixed income versus the Index, with a 68.5% and 23.5% allocation, respectively, and an 8.0% target weight to cash.

– At the end of the reporting period, the Fund was allocated as follows: US equities—64.0%; US investment grade bonds—27.0%; US high yield bonds—2.5%; US TIPS—0.0%; cash—6.5%. For comparison purposes, neutral Index weights for the Fund are 65.0% equities and 35.0% fixed income.

We tactically adjusted the portfolio during the 12-month reporting period given the changing economic and market environment. We increased our overweight to equities and slightly reduced our underweight to fixed income by reducing the Fund's high yield underweight at the beginning of the period, as we felt that risk assets were oversold. This weighed on performance in fourth quarter of 2018 given the dramatic selloff witnessed in risk assets. Then, in the first quarter of 2019, we started to trim the Fund's overweight to equities and increase the underweight to US investment grade bonds by reducing our exposure to US 10 year Treasuries. The proceeds were used to raise cash given the rally witnessed across US equities and given the low interest rates of US bonds.

10 Allocations include derivative exposure.

3

UBS U.S. Allocation Fund

Our preference for equites over the first quarter of 2019 was additive for performance, but was offset by the Fund's overweight to cash. Over the remainder of the period, the Fund became underweight US equities, hurting relative performance as the asset class continued to outperform. The Fund's underweight to 10 year US Treasuries was closed at the end of the reporting period in August 2019.

• From a market allocation perspective, a long position in oil & gas, which was closed in November 2018, detracted from performance. An overweight to cash over the period was also detrimental to relative performance.

• Overall, US security selection detracted from results during the reporting period. The US growth equity portion of the Fund delivered positive security selection results, but this was offset by the US equity core portion.

• In the US growth equity portion of the Fund, a cash position, an underweight to consumer staples and an overweight to consumer discretionary detracted from relative performance. Security selection within communication services and industrials was also a headwind for performance. On an individual stock basis the largest detractors for relative performance included:

• Nvidia's shares declined as the company posted disappointing quarterly results on the back of weaker demand, in particular from its crypto business. We have since exited our position in the stock.

• Mohawk Industries underperformed amid weaker guidance as the company seeks to reduce inventory related to softer end markets. We have since exited our position in the stock in the US growth equity portion of the Fund.

• Activision Blizzard underperformed as the company posted disappointing results that pointed to weakening trends in the company's portfolio across multiple gaming properties. Execution issues and a perceived weaker game pipeline for calendar 2019 also pressured it shares. We have since exited our position in the stock in the US growth equity portion of the Fund.

• In the US equity core portion of the Fund, underweight in the utilities and overweight in financials sector had a negative impact on performance relative to the benchmark.

• Securities selection in health care and real estate sectors detracted the most from returns in the US Equity Core portion of the Fund. On an individual stock basis, the largest detractors included:

• Shares of Concho Resources fell sharply because the company reduced production guidance while holding capital expenditure spending flat. This raised questions about its ability to sustain free cash flow. In addition, a test of tighter spacing yielded poor results which reignited basic fears about the underlying intrinsic value of the asset. Our thesis on Concho Resources was based on an attractive valuation, a strong balance sheet and management team. We believed that the company would benefit from new pipeline capacity in the second half of 2019 that would yield better realized prices. We sold out of the holding on the basis of thesis violation.

• Shares of Ironwood underperformed following the spin out of R&D-Co. (now known as CYCN) on concerns around the growth prospects for the company's flagship product, Linzess. These concerns further intensified when ABBV announced plans to acquire IRWD's partner, AGN. This raised concerns that the Linzess franchise could be impacted by merger-related reorganizations/reprioritizations. We continue to hold this stock.

• Alnylam's shares underperformed on concerns around the durability of the company's TTR-franchise (Onpattro/TTRsc02) and following Sanofi's decision to terminate their collaboration and sell down their equity

4

UBS U.S. Allocation Fund

stake. At currently levels we believe the Street underappreciates the potential of inclisiran (discovered by ALNY and out licensed to MDCO) and of the recently announced CNS/ophthalmology collaboration with REGN. We continue to hold this stock.

• Relative to the benchmark, the use of fixed income and equity derivatives (futures, options, and swaps) detracted from the Fund's results. These derivative instruments, which were utilized to manage the Fund's fixed income and equity exposure, were a headwind for performance.

We thank you for your continued support and welcome any comments or questions you may have. For additional information on the UBS family of funds,* please contact your financial advisor or visit us at www.ubs.com/am-us.

Sincerely,

|

|

|

||||||

|

Igor Lasun President UBS U.S. Allocation Fund Executive Director UBS Asset Management (Americas) Inc. |

Alan Zlatar Portfolio Manager UBS U.S. Allocation Fund Managing Director UBS Asset Management (Americas) Inc. |

||||||

|

|

|||

|

Paul Lang Portfolio Manager UBS U.S. Allocation Fund Director UBS Asset Management (Americas) Inc. |

|||

This letter is intended to assist shareholders in understanding how the Fund performed during the 12 months ended August 31, 2019. The views and opinions in the letter were current as of October 1, 2019. They are not guarantees of future performance or investment results and should not be taken as investment advice. Investment decisions reflect a variety of factors, and we reserve the right to change our views about individual securities, sectors and markets at any time. As a result, the views expressed should not be relied upon as a forecast of the Fund's future investment intent. We encourage you to consult your financial advisor regarding your personal investment program.

* Mutual funds are sold by prospectus only. You should read it carefully and consider a fund's investment objectives, risks, charges, expenses and other important information contained in the prospectus before investing. The prospectus contains this and other information about the fund. Prospectuses for most of our funds can be obtained from your Financial Advisor, by calling UBS Funds at 800-647 1568 or by visiting our website at www.ubs.com/am-us.

5

UBS U.S. Allocation Fund

Performance at a glance (unaudited)

|

Average annual total returns for periods ended 08/31/2019 |

1 year |

5 years |

10 years |

||||||||||||

|

Before deducting maximum sales charge |

|||||||||||||||

|

Class A1 |

0.84 |

% |

5.96 |

% |

9.43 |

% |

|||||||||

|

Class P2 |

1.08 |

6.25 |

9.74 |

||||||||||||

|

After deducting maximum sales charge |

|||||||||||||||

|

Class A1 |

(4.71 |

) |

4.77 |

8.81 |

|||||||||||

|

S&P 500 Index.3 |

2.92 |

10.11 |

13.45 |

||||||||||||

|

UBS U.S. Allocation Fund Benchmark4 |

4.59 |

7.64 |

10.41 |

||||||||||||

|

Lipper Flexible Portfolio Funds median |

1.49 |

3.31 |

6.52 |

||||||||||||

Most recent calendar quarter-end returns (unaudited)

|

Average annual total returns for periods ended 09/30/2019 |

1 year |

5 years |

10 years |

||||||||||||

|

Before deducting maximum sales charge |

|||||||||||||||

|

Class A1 |

2.40 |

% |

6.58 |

% |

9.06 |

% |

|||||||||

|

Class P2 |

2.69 |

6.87 |

9.37 |

||||||||||||

|

After deducting maximum sales charge |

|||||||||||||||

|

Class A1 |

(3.22 |

) |

5.38 |

8.45 |

|||||||||||

The annualized gross and net expense ratios, respectively, for each class of shares as in the December 29, 2018 prospectuses, were as follows: Class A—1.02% and 1.02%; and Class P—0.76% and 0.76%.

Net expenses reflect fee waivers and/or expense reimbursements, if any, pursuant to an agreement that is in effect to cap the expenses. The Fund and UBS Asset Management (Americas) Inc. have entered into a written agreement, separate from UBS AM's investment advisory agreement with the Fund, whereby UBS AM has agreed to permanently reduce its management fees based on the Fund's average daily net assets to the following rates: $0 to $250 million: 0.50%; in excess of $250 million up to $500 million: 0.45%; in excess of $500 million up to $2 billion: 0.40%; over $2 billion: 0.35%. Effective December 29, 2018, UBS AM has contractually undertaken to waive fees/reimburse a portion of the Fund's expenses, when necessary, so that the ordinary total annual operating expenses of each class through December 31, 2019 (excluding dividend expense, borrowing costs and interest expense relating to short sales, and expenses attributable to investments in other investment companies, interest, taxes, brokerage commissions and extraordinary expenses, if any) would not exceed 1.15% for Class A and 0.90% for Class P.

1 Maximum sales charge for Class A shares is 5.5%. Class A shares bear ongoing 12b-1 service fees.

2 Class P shares do not bear initial or contingent deferred sales charges or ongoing 12b-1 service and distribution fees, but Class P shares held through advisory programs may be subject to a program fee, which, if included, would have reduced performance.

3 The S&P 500 Index is an unmanaged, weighted index comprising 500 widely held common stocks varying in composition and is not available for direct investment. Investors should note that indices do not reflect the deduction of fees and expenses.

4 The UBS U.S. Allocation Fund Benchmark is an unmanaged benchmark compiled by the Advisor, constructed as follows: from June 1, 2005 until present: 65% Russell 3000 Index, 30% Bloomberg Barclays US Aggregate Bond Index, and 5% ICE BofAML US High Yield Cash Pay Constrained Index. Investors should note that indices do not reflect the deduction of fees and expenses.

Past performance does not predict future performance, and the performance information provided does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The return and principal value of an investment will fluctuate, so that an investor's shares, when redeemed, may be worth more or less than their original cost. Performance results assume reinvestment of all dividends and capital gain distributions at net asset value on the ex-dividend dates. Current performance may be higher or lower than the performance data quoted. For month-end performance figures, please visit http://www.ubs.com/us-mutualfundperformance.

Lipper peer group data calculated by Lipper Inc.; used with permission. The Lipper median is the return of the fund that places in the middle of a Lipper peer group.

6

UBS U.S. Allocation Fund

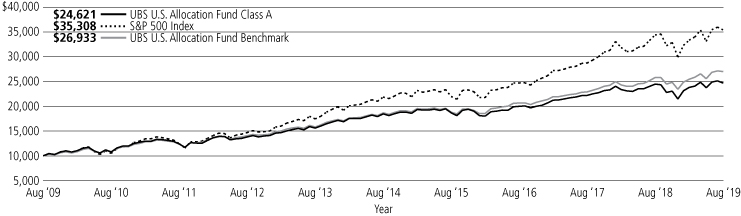

Illustration of an assumed investment of $10,000 in Class A shares of the Fund (unaudited)

The following graph depicts the performance of UBS U.S. Allocation Fund Class A shares versus the S&P 500 Index and the UBS U.S. Allocation Fund Benchmark over the 10 years ended August 31, 2019. The performance of the other classes will vary based upon the different class specific expenses and sales charges. The performance provided does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Past performance is no guarantee of future results. Share price and returns will vary with market conditions; investors may realize a gain or loss upon redemption. It is important to note that the Fund is a professionally managed portfolio while the Indices are not available for investment and are unmanaged. The comparison is shown for illustration purposes only.

UBS U.S. Allocation Fund Class A

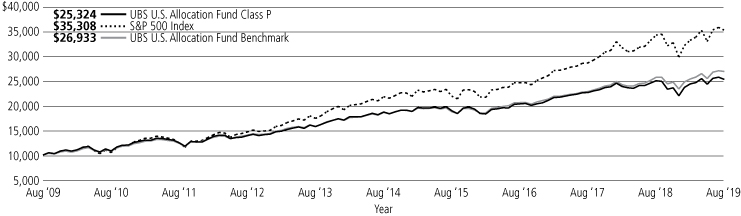

Illustration of an assumed investment of $10,000 in Class P shares of the Fund (unaudited)

The following graph depicts the performance of UBS U.S. Allocation Fund Class P shares versus the S&P 500 Index and the UBS U.S. Allocation Fund Benchmark over the 10 years ended August 31, 2019. The performance of the other classes will vary based upon the different class specific expenses and sales charges. The performance provided does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Past performance is no guarantee of future results. Share price and returns will vary with market conditions; investors may realize a gain or loss upon redemption. It is important to note that the Fund is a professionally managed portfolio while the Indices are not available for investment and are unmanaged. The comparison is shown for illustration purposes only.

UBS U.S. Allocation Fund Class P

7

UBS U.S. Allocation Fund

Understanding your Fund's expenses (unaudited)

As a shareholder of the Fund, you incur two types of costs: (1) transactional costs (as applicable), including sales charges (loads); and (2) ongoing costs, including management fees; service and/or distribution (12b-1) fees (if applicable); and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example below is based on an investment of $1,000 invested at the beginning of the period and held for the entire period, March 1, 2019 to August 31, 2019.

Actual expenses (unaudited)

The first line for each class of shares in the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over a period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line for each class of shares under the heading entitled "Expenses paid during period" to estimate the expenses you paid on your account during this period.

Hypothetical example for comparison purposes (unaudited)

The second line for each class of shares in the table below provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratios for each class of shares and an assumed rate of return of 5% per year before expenses, which is not the Fund's actual return for each class of shares. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing Fund costs only and do not reflect any transactional costs (as applicable), such as sales charges (loads). Therefore, the second line in the table for each class of shares is useful in comparing ongoing Fund costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

|

Beginning account value March 1, 2019 |

Ending account value August 31, 2019 |

Expenses paid during period1 03/01/19 to 08/31/19 |

Expense ratio during the period |

||||||||||||||||||||

|

Class A |

Actual |

$ |

1,000.00 |

$ |

1,036.50 |

$ |

5.03 |

0.98 |

% |

||||||||||||||

|

Hypothetical (5% annual return before expenses) |

1,000.00 |

1,020.27 |

4.99 |

0.98 |

|||||||||||||||||||

|

Class P |

Actual |

1,000.00 |

1,037.80 |

3.60 |

0.70 |

||||||||||||||||||

|

Hypothetical (5% annual return before expenses) |

1,000.00 |

1,021.68 |

3.57 |

0.70 |

|||||||||||||||||||

1 Expenses are equal to the Fund's annualized net expense ratio, multiplied by the average account value over the period, multiplied by 184 divided by 365 (to reflect the one-half year period).

8

UBS U.S. Allocation Fund

Portfolio statistics—August 31, 2019 (unaudited)

|

Top ten equity holdings1 |

Percentage of net assets |

||||||

|

Amazon.com, Inc. |

2.2 |

% |

|||||

|

Microsoft Corp. |

1.4 |

||||||

|

Visa, Inc., Class A |

1.4 |

||||||

|

Walt Disney Co./The |

1.1 |

||||||

|

Marsh & McLennan Cos., Inc. |

1.1 |

||||||

|

UnitedHealth Group, Inc. |

1.0 |

||||||

|

Alphabet, Inc., Class A |

1.0 |

||||||

|

Facebook, Inc., Class A |

1.0 |

||||||

|

Salesforce.com, Inc. |

0.9 |

||||||

|

JPMorgan Chase & Co. |

0.8 |

||||||

|

Total |

11.9 |

% |

|||||

|

Top ten long-term fixed income holdings1 |

Percentage of net assets |

||||||

|

US Treasury Note, 2.250% due 04/30/24 |

2.1 |

% |

|||||

|

Federal National Mortgage Association Certificate, 3.500% due 06/01/49 |

1.1 |

||||||

|

US Treasury Note, 2.375% due 05/15/29 |

0.9 |

||||||

|

Federal National Mortgage Association Certificate, 3.500% due 02/01/48 |

0.9 |

||||||

|

US Treasury Note, 1.625% due 08/15/29 |

0.7 |

||||||

|

US Treasury Bond, 2.875% due 05/15/49 |

0.6 |

||||||

|

US Treasury Inflation Index Note (TIPS), 0.500% due 04/15/24 |

0.6 |

||||||

|

US Treasury Bond, 3.125% due 05/15/48 |

0.6 |

||||||

|

US Treasury Note, 2.750% due 09/15/21 |

0.6 |

||||||

|

Federal National Mortgage Association Certificate, 4.000% due 06/01/47 |

0.6 |

||||||

|

Total |

8.7 |

% |

|||||

|

Top five issuer breakdown by country or territory of origin1 |

Percentage of net assets |

||||||

|

United States |

96.9 |

% |

|||||

|

United Kingdom |

0.7 |

||||||

|

Netherlands |

0.5 |

||||||

|

Canada |

0.4 |

||||||

|

Germany |

0.3 |

||||||

|

Total |

98.8 |

% |

|||||

1 The Fund's portfolio is actively managed and its composition will vary over time.

9

UBS U.S. Allocation Fund

Portfolio statistics—August 31, 2019 (unaudited) (concluded)

|

Asset allocation1 |

Percentage of net assets |

||||||

|

Common stocks |

43.2 |

% |

|||||

|

Corporate bonds |

12.8 |

||||||

|

Short-term US government obligations |

9.8 |

||||||

|

US government obligations |

8.0 |

||||||

|

Mortgage & agency debt securities |

7.7 |

||||||

|

Exchange traded fund |

4.2 |

||||||

|

Commercial mortgage-backed securities |

3.0 |

||||||

|

Asset-backed securities |

2.6 |

||||||

|

Non-US government obligations |

0.6 |

||||||

|

Municipal bonds |

0.2 |

||||||

|

Preferred stock |

0.0 |

* |

|||||

|

Options purchased, futures and swaps |

(0.5 |

) |

|||||

|

Cash equivalents and other assets less liabilities |

8.4 |

||||||

|

Total |

100.0 |

% |

|||||

* Weighting represents less than 0.05% of the Fund's net assets as of the dates indicated.

1 The Fund's portfolio is actively managed and its composition will vary over time.

10

UBS U.S. Allocation Fund

Portfolio of investments—August 31, 2019

|

Number of shares |

Value |

||||||||||

|

Common stocks—43.2% |

|||||||||||

|

Aerospace & defense—0.6% |

|||||||||||

|

Spirit AeroSystems Holdings, Inc., Class A |

16,555 |

$ |

1,334,333 |

||||||||

|

Airlines—0.7% |

|||||||||||

|

Delta Air Lines, Inc. |

29,273 |

1,693,736 |

|||||||||

|

Auto components—0.3% |

|||||||||||

|

Aptiv PLC |

9,268 |

770,820 |

|||||||||

|

Banks—1.5% |

|||||||||||

|

JPMorgan Chase & Co. |

17,178 |

1,887,175 |

|||||||||

|

Wells Fargo & Co. |

35,525 |

1,654,399 |

|||||||||

|

3,541,574 |

|||||||||||

|

Beverages—0.2% |

|||||||||||

|

PepsiCo, Inc. |

3,768 |

515,199 |

|||||||||

|

Biotechnology—1.5% |

|||||||||||

|

Alexion Pharmaceuticals, Inc.* |

6,135 |

618,162 |

|||||||||

|

Alnylam Pharmaceuticals, Inc.* |

3,207 |

258,773 |

|||||||||

|

Bluebird Bio, Inc.*,1 |

2,212 |

228,522 |

|||||||||

|

Coherus Biosciences, Inc.*,1 |

13,156 |

291,932 |

|||||||||

|

Cyclerion Therapeutics, Inc.* |

6,174 |

58,715 |

|||||||||

|

Incyte Corp.* |

12,580 |

1,029,295 |

|||||||||

|

Ironwood Pharmaceuticals, Inc.*,1 |

88,628 |

825,127 |

|||||||||

|

Mirati Therapeutics, Inc.* |

2,179 |

178,613 |

|||||||||

|

3,489,139 |

|||||||||||

|

Building products—0.8% |

|||||||||||

|

Allegion PLC |

8,300 |

799,041 |

|||||||||

|

Masco Corp. |

24,307 |

990,024 |

|||||||||

|

1,789,065 |

|||||||||||

|

Capital markets—0.6% |

|||||||||||

|

Ameriprise Financial, Inc. |

10,909 |

1,407,043 |

|||||||||

|

Chemicals—0.6% |

|||||||||||

|

FMC Corp. |

6,421 |

554,325 |

|||||||||

|

Westlake Chemical Corp. |

15,012 |

879,553 |

|||||||||

|

1,433,878 |

|||||||||||

|

Commercial services & supplies—0.5% |

|||||||||||

|

MSA Safety, Inc. |

7,996 |

844,618 |

|||||||||

|

Stericycle, Inc.*,1 |

9,388 |

421,427 |

|||||||||

|

1,266,045 |

|||||||||||

|

Communications equipment—0.4% |

|||||||||||

|

Arista Networks, Inc.* |

4,094 |

927,782 |

|||||||||

|

Consumer finance—1.0% |

|||||||||||

|

American Express Co. |

5,644 |

679,368 |

|||||||||

|

Synchrony Financial |

52,660 |

1,687,753 |

|||||||||

|

2,367,121 |

|||||||||||

|

Distributors—0.4% |

|||||||||||

|

LKQ Corp.* |

32,305 |

848,652 |

|||||||||

|

Electrical equipment—0.3% |

|||||||||||

|

Rockwell Automation, Inc. |

3,867 |

590,839 |

|||||||||

|

Number of shares |

Value |

||||||||||

|

Common stocks—(continued) |

|||||||||||

|

Electronic equipment, instruments & components—0.7% |

|||||||||||

|

IPG Photonics Corp.* |

6,281 |

$ |

777,148 |

||||||||

|

Trimble, Inc.* |

22,151 |

831,106 |

|||||||||

|

1,608,254 |

|||||||||||

|

Entertainment—2.4% |

|||||||||||

|

Activision Blizzard, Inc. |

20,679 |

1,046,357 |

|||||||||

|

Electronic Arts, Inc.* |

5,104 |

478,143 |

|||||||||

|

Netflix, Inc.* |

2,540 |

746,125 |

|||||||||

|

Take-Two Interactive Software, Inc.* |

5,622 |

741,935 |

|||||||||

|

Walt Disney Co./The |

18,983 |

2,605,607 |

|||||||||

|

5,618,167 |

|||||||||||

|

Equity real estate investment trusts—1.4% |

|||||||||||

|

Crown Castle International Corp. |

3,200 |

464,544 |

|||||||||

|

Digital Realty Trust, Inc. |

9,680 |

1,196,739 |

|||||||||

|

Simon Property Group, Inc. |

10,215 |

1,521,422 |

|||||||||

|

3,182,705 |

|||||||||||

|

Food products—0.7% |

|||||||||||

|

Mondelez International, Inc., Class A |

28,732 |

1,586,581 |

|||||||||

|

Health care equipment & supplies—1.4% |

|||||||||||

|

Abbott Laboratories |

7,008 |

597,923 |

|||||||||

|

Align Technology, Inc.* |

7,411 |

1,357,028 |

|||||||||

|

Cooper Cos., Inc./The |

1,276 |

395,241 |

|||||||||

|

LivaNova PLC* |

4,700 |

364,861 |

|||||||||

|

Zimmer Biomet Holdings, Inc. |

3,116 |

433,747 |

|||||||||

|

3,148,800 |

|||||||||||

|

Health care providers & services—1.5% |

|||||||||||

|

Laboratory Corp. of America Holdings* |

6,197 |

1,038,369 |

|||||||||

|

UnitedHealth Group, Inc. |

10,273 |

2,403,882 |

|||||||||

|

3,442,251 |

|||||||||||

|

Hotels, restaurants & leisure—0.9% |

|||||||||||

|

Carnival Corp. |

18,938 |

834,787 |

|||||||||

|

Domino's Pizza, Inc. |

3,083 |

699,348 |

|||||||||

|

Las Vegas Sands Corp. |

8,115 |

450,139 |

|||||||||

|

1,984,274 |

|||||||||||

|

Household durables—0.3% |

|||||||||||

|

Mohawk Industries, Inc.* |

6,882 |

818,201 |

|||||||||

|

Insurance—2.4% |

|||||||||||

|

Marsh & McLennan Cos., Inc. |

24,437 |

2,441,012 |

|||||||||

|

MetLife, Inc. |

30,351 |

1,344,549 |

|||||||||

|

Progressive Corp./The |

24,097 |

1,826,553 |

|||||||||

|

5,612,114 |

|||||||||||

|

Interactive media & services—2.2% |

|||||||||||

|

Alphabet, Inc., Class A* |

1,931 |

2,298,913 |

|||||||||

|

Facebook, Inc., Class A* |

12,260 |

2,276,314 |

|||||||||

|

IAC/InterActiveCorp.* |

2,462 |

626,924 |

|||||||||

|

5,202,151 |

|||||||||||

11

UBS U.S. Allocation Fund

Portfolio of investments—August 31, 2019

|

Number of shares |

Value |

||||||||||

|

Common stocks—(continued) |

|||||||||||

|

Internet & direct marketing retail—2.6% |

|||||||||||

|

Alibaba Group Holding Ltd., ADR* |

1,590 |

$ |

278,298 |

||||||||

|

Amazon.com, Inc.* |

2,868 |

5,094,400 |

|||||||||

|

Expedia Group, Inc. |

4,377 |

569,447 |

|||||||||

|

5,942,145 |

|||||||||||

|

IT services—2.1% |

|||||||||||

|

Fidelity National Information Services, Inc. |

4,097 |

558,093 |

|||||||||

|

GoDaddy, Inc., Class A* |

15,167 |

960,678 |

|||||||||

|

Visa, Inc., Class A |

17,883 |

3,233,604 |

|||||||||

|

4,752,375 |

|||||||||||

|

Life sciences tools & services—0.4% |

|||||||||||

|

Bio-Rad Laboratories, Inc., Class A* |

2,778 |

938,158 |

|||||||||

|

Machinery—1.3% |

|||||||||||

|

AGCO Corp. |

20,002 |

1,382,538 |

|||||||||

|

Caterpillar, Inc. |

4,345 |

517,055 |

|||||||||

|

Gardner Denver Holdings, Inc.* |

36,951 |

1,059,755 |

|||||||||

|

2,959,348 |

|||||||||||

|

Metals & mining—0.4% |

|||||||||||

|

Steel Dynamics, Inc. |

34,118 |

921,186 |

|||||||||

|

Multiline retail—0.4% |

|||||||||||

|

Dollar General Corp. |

5,556 |

867,236 |

|||||||||

|

Oil, gas & consumable fuels—0.8% |

|||||||||||

|

Apache Corp. |

43,067 |

928,955 |

|||||||||

|

Hess Corp. |

14,728 |

927,128 |

|||||||||

|

1,856,083 |

|||||||||||

|

Pharmaceuticals—1.4% |

|||||||||||

|

Allergan PLC |

1,232 |

196,775 |

|||||||||

|

Elanco Animal Health, Inc.* |

35,159 |

914,837 |

|||||||||

|

GlaxoSmithKline PLC, ADR |

10,400 |

432,432 |

|||||||||

|

Johnson & Johnson |

13,622 |

1,748,520 |

|||||||||

|

3,292,564 |

|||||||||||

|

Professional services—0.2% |

|||||||||||

|

TransUnion |

4,706 |

393,657 |

|||||||||

|

Road & rail—0.4% |

|||||||||||

|

Lyft, Inc., Class A* |

2,852 |

139,663 |

|||||||||

|

Union Pacific Corp. |

4,921 |

797,005 |

|||||||||

|

936,668 |

|||||||||||

|

Semiconductors & semiconductor equipment—2.9% |

|||||||||||

|

Cree, Inc.* |

9,347 |

401,267 |

|||||||||

|

KLA Corp. |

3,348 |

495,169 |

|||||||||

|

Lam Research Corp. |

3,137 |

660,370 |

|||||||||

|

Marvell Technology Group Ltd. |

24,203 |

580,146 |

|||||||||

|

Micron Technology, Inc.* |

24,315 |

1,100,740 |

|||||||||

|

Monolithic Power Systems, Inc. |

2,822 |

424,880 |

|||||||||

|

NXP Semiconductors N.V. |

9,122 |

931,721 |

|||||||||

|

ON Semiconductor Corp.* |

22,315 |

397,207 |

|||||||||

|

Qorvo, Inc.* |

5,934 |

423,866 |

|||||||||

|

Skyworks Solutions, Inc. |

5,593 |

420,985 |

|||||||||

|

Number of shares |

Value |

||||||||||

|

Common stocks—(concluded) |

|||||||||||

|

Semiconductors & semiconductor equipment—(concluded) |

|||||||||||

|

Teradyne, Inc. |

7,871 |

$ |

416,927 |

||||||||

|

Universal Display Corp. |

2,168 |

445,459 |

|||||||||

|

6,698,737 |

|||||||||||

|

Software—3.3% |

|||||||||||

|

Autodesk, Inc.* |

5,463 |

780,226 |

|||||||||

|

LogMeIn, Inc. |

5,920 |

395,693 |

|||||||||

|

Microsoft Corp. |

24,233 |

3,340,761 |

|||||||||

|

Palo Alto Networks, Inc.* |

2,060 |

419,457 |

|||||||||

|

Salesforce.com, Inc.* |

12,778 |

1,994,262 |

|||||||||

|

ServiceNow, Inc.* |

2,402 |

628,940 |

|||||||||

|

7,559,339 |

|||||||||||

|

Specialty retail—1.5% |

|||||||||||

|

Burlington Stores, Inc.* |

7,308 |

1,479,797 |

|||||||||

|

Carvana Co.*,1 |

4,115 |

333,973 |

|||||||||

|

Lowe's Cos., Inc. |

6,208 |

696,538 |

|||||||||

|

TJX Cos., Inc./The |

16,320 |

897,110 |

|||||||||

|

3,407,418 |

|||||||||||

|

Technology hardware, storage & peripherals—1.4% |

|||||||||||

|

Apple, Inc. |

8,400 |

1,753,416 |

|||||||||

|

NetApp, Inc. |

8,953 |

430,281 |

|||||||||

|

Western Digital Corp. |

17,556 |

1,005,432 |

|||||||||

|

3,189,129 |

|||||||||||

|

Textiles, apparel & luxury goods—0.4% |

|||||||||||

|

NIKE, Inc., Class B |

11,396 |

962,962 |

|||||||||

|

Wireless telecommunication services—0.4% |

|||||||||||

|

T-Mobile US, Inc.* |

12,544 |

979,059 |

|||||||||

|

Total common stocks (cost—$87,798,754) |

99,834,788 |

||||||||||

|

Exchange traded fund—4.2% |

|||||||||||

|

iShares Russell 1000 Value ETF1 (cost—$8,305,506) |

77,650 |

9,673,637 |

|||||||||

|

Preferred stock—0.0%† |

|||||||||||

|

Financial services—0.0%† |

|||||||||||

|

Squaretwo Financial Corp.2,3 (cost—$0) |

35,000 |

0 |

|||||||||

|

Face amount |

|||||||||||

|

US government obligations—8.0% |

|||||||||||

|

US Treasury Bonds 2.250%, due 08/15/49 |

$ |

280,000 |

297,773 |

||||||||

|

2.875%, due 05/15/49 |

1,235,000 |

1,488,127 |

|||||||||

|

3.000%, due 08/15/48 |

360,000 |

442,223 |

|||||||||

|

3.125%, due 02/15/43 |

260,000 |

318,927 |

|||||||||

|

3.125%, due 05/15/48 |

1,110,000 |

1,392,833 |

|||||||||

|

3.375%, due 11/15/48 |

445,000 |

585,349 |

|||||||||

|

3.750%, due 11/15/43 |

395,000 |

534,623 |

|||||||||

|

US Treasury Inflation Index Notes (TIPS) 0.500%, due 04/15/24 |

1,386,280 |

1,414,453 |

|||||||||

|

0.875%, due 01/15/29 |

131,873 |

142,720 |

|||||||||

12

UBS U.S. Allocation Fund

Portfolio of investments—August 31, 2019

|

Face amount |

Value |

||||||||||

|

US government obligations—(concluded) |

|||||||||||

|

US Treasury Notes 1.625%, due 08/15/29 |

$ |

1,555,000 |

$ |

1,572,676 |

|||||||

|

1.875%, due 07/31/26 |

775,000 |

796,434 |

|||||||||

|

2.125%, due 05/31/21 |

560,000 |

565,228 |

|||||||||

|

2.250%, due 04/30/24 |

4,595,000 |

4,767,851 |

|||||||||

|

2.375%, due 02/29/24 |

700,000 |

729,367 |

|||||||||

|

2.375%, due 05/15/29 |

1,850,000 |

1,994,531 |

|||||||||

|

2.750%, due 09/15/21 |

1,340,000 |

1,373,134 |

|||||||||

|

Total US government obligations (cost—$17,504,056) |

18,416,249 |

||||||||||

|

Mortgage & agency debt securities—7.7% |

|||||||||||

|

Federal Home Loan Mortgage Corporation Certificates, 3.000%, due 11/01/46 |

273,588 |

281,018 |

|||||||||

|

3.000%, due 07/01/47 |

428,509 |

439,861 |

|||||||||

|

3.000%, due 08/01/47 |

370,411 |

380,485 |

|||||||||

|

4.000%, due 05/01/47 |

607,014 |

636,906 |

|||||||||

|

4.000%, due 08/01/47 |

78,488 |

82,339 |

|||||||||

|

4.000%, due 11/01/47 |

273,295 |

286,277 |

|||||||||

|

4.000%, due 12/01/47 |

456,092 |

477,566 |

|||||||||

|

4.500%, due 06/01/47 |

285,664 |

302,519 |

|||||||||

|

5.000%, due 03/01/38 |

21,725 |

24,206 |

|||||||||

|

5.500%, due 05/01/37 |

175,230 |

197,146 |

|||||||||

|

5.500%, due 08/01/40 |

22,213 |

24,977 |

|||||||||

|

6.500%, due 08/01/28 |

51,908 |

58,232 |

|||||||||

|

Federal National Mortgage Association Certificates, 1.875%, due 09/24/26 |

200,000 |

204,984 |

|||||||||

|

2.375%, due 01/19/23 |

590,000 |

607,233 |

|||||||||

|

2.500%, due 08/01/34 |

843,710 |

854,904 |

|||||||||

|

3.000%, due 07/01/49 |

1,214,148 |

1,237,642 |

|||||||||

|

3.500%, due 12/01/47 |

366,236 |

377,657 |

|||||||||

|

3.500%, due 02/01/48 |

1,926,148 |

1,990,603 |

|||||||||

|

3.500%, due 03/01/48 |

829,815 |

855,304 |

|||||||||

|

3.500%, due 06/01/49 |

2,524,118 |

2,597,480 |

|||||||||

|

4.000%, due 12/01/39 |

78,348 |

83,662 |

|||||||||

|

4.000%, due 02/01/41 |

43,910 |

46,910 |

|||||||||

|

4.000%, due 08/01/45 |

216,047 |

230,662 |

|||||||||

|

4.000%, due 06/01/47 |

1,265,063 |

1,322,883 |

|||||||||

|

4.000%, due 11/01/47 |

202,230 |

211,930 |

|||||||||

|

4.500%, due 09/01/37 |

210,834 |

227,468 |

|||||||||

|

4.500%, due 07/01/47 |

219,435 |

232,208 |

|||||||||

|

5.000%, due 10/01/39 |

8,830 |

9,763 |

|||||||||

|

5.000%, due 05/01/40 |

14,244 |

15,679 |

|||||||||

|

5.500%, due 08/01/39 |

56,377 |

61,667 |

|||||||||

|

7.000%, due 08/01/32 |

134,455 |

159,092 |

|||||||||

|

7.500%, due 02/01/33 |

2,196 |

2,384 |

|||||||||

|

Government National Mortgage Association Certificate I, 4.000%, due 07/15/42 |

63,365 |

67,576 |

|||||||||

|

Government National Mortgage Association Certificates II, 3.000%, due 08/20/46 |

1,221,254 |

1,264,914 |

|||||||||

|

3.000%, due 01/20/47 |

148,902 |

154,211 |

|||||||||

|

3.000%, due 07/20/47 |

461,483 |

476,898 |

|||||||||

|

3.000%, due 08/20/47 |

349,745 |

361,272 |

|||||||||

|

Face amount |

Value |

||||||||||

|

Mortgage & agency debt securities—(concluded) |

|||||||||||

|

3.500%, due 04/20/47 |

$ |

457,899 |

$ |

477,773 |

|||||||

|

4.500%, due 08/20/48 |

328,985 |

345,005 |

|||||||||

|

6.000%, due 11/20/28 |

486 |

545 |

|||||||||

|

6.000%, due 02/20/29 |

1,149 |

1,288 |

|||||||||

|

6.000%, due 02/20/34 |

239,526 |

261,512 |

|||||||||

|

Total mortgage & agency debt securities (cost—$17,560,780) |

17,932,641 |

||||||||||

|

Asset-backed securities—2.6% |

|||||||||||

|

AmeriCredit Automobile Receivables Trust, Series 2018-1, Class D, |

|||||||||||

|

3.820%, due 03/18/24 |

175,000 |

180,871 |

|||||||||

|

Capital Auto Receivables Asset Trust, Series 2015-4, Class D, 3.620%, due 05/20/21 |

125,000 |

125,476 |

|||||||||

|

Series 2016-3, Class D, 2.650%, due 01/20/24 |

125,000 |

125,258 |

|||||||||

|

Capital One Multi-Asset Execution Trust, Series 2005-B3, Class B3, 3 mo. USD LIBOR + 0.550%, 2.853%, due 05/15/284 |

350,000 |

346,187 |

|||||||||

|

Dell Equipment Finance Trust, Series 2018-1, Class C, 3.530%, due 06/22/235 |

331,000 |

337,893 |

|||||||||

|

Series 2018-1, Class D, 3.850%, due 06/24/245 |

210,000 |

214,274 |

|||||||||

|

Drive Auto Receivables Trust, Series 2015-BA, Class D, 3.840%, due 07/15/215 |

65,548 |

65,662 |

|||||||||

|

Series 2015-DA, Class D, 4.590%, due 01/17/235 |

151,075 |

151,662 |

|||||||||

|

Series 2017-1, Class D, 3.840%, due 03/15/23 |

125,000 |

126,623 |

|||||||||

|

Series 2017-2, Class C, 2.750%, due 09/15/23 |

58,500 |

58,545 |

|||||||||

|

Series 2018-2, Class D, 4.140%, due 08/15/24 |

350,000 |

360,438 |

|||||||||

|

Series 2018-4, Class D, 4.090%, due 01/15/26 |

250,000 |

257,874 |

|||||||||

|

Exeter Automobile Receivables Trust, Series 2018-1, Class AD, 3.530%, due 11/15/235 |

150,000 |

153,225 |

|||||||||

|

Invitation Homes Trust, Series 2018-SFR1, Class C, 1 mo. USD LIBOR + 1.250%, 3.432%, due 03/17/374,5 |

150,000 |

149,376 |

|||||||||

|

OneMain Direct Auto Receivables Trust, Series 2019-1A, Class A, 3.630%, due 09/14/275 |

550,000 |

578,779 |

|||||||||

|

Santander Drive Auto Receivables Trust, Series 2017-2, Class D, 3.490%, due 07/17/23 |

150,000 |

151,953 |

|||||||||

|

Series 2017-3, Class D, 3.200%, due 11/15/23 |

325,000 |

328,938 |

|||||||||

|

Series 2018-2, Class C, 3.350%, due 07/17/23 |

225,000 |

227,624 |

|||||||||

|

Series 2018-2, Class D, 3.880%, due 02/15/24 |

225,000 |

231,230 |

|||||||||

13

UBS U.S. Allocation Fund

Portfolio of investments—August 31, 2019

|

Face amount |

Value |

||||||||||

|

Asset-backed securities—(concluded) |

|||||||||||

|

Sofi Consumer Loan Program Trust, Series 2018-1, Class B, 3.650%, due 02/25/275 |

$ |

175,000 |

$ |

179,695 |

|||||||

|

Series 2018-2, Class A2, 3.350%, due 04/26/275 |

300,000 |

302,753 |

|||||||||

|

Series 2018-2, Class B, 3.790%, due 04/26/275 |

200,000 |

205,526 |

|||||||||

|

Series 2018-3, Class B, 4.020%, due 08/25/275 |

200,000 |

208,260 |

|||||||||

|

Series 2019-1, Class A, 3.240%, due 02/25/285 |

396,002 |

400,769 |

|||||||||

|

Tesla Auto Lease Trust, Series 2018-B, Class A, 3.710%, due 08/20/215 |

264,707 |

269,413 |

|||||||||

|

World Financial Network Credit Card Master Trust, Series 2016-A, Class A, 2.030%, due 04/15/25 |

225,000 |

225,477 |

|||||||||

|

Total asset-backed securities (cost—$5,845,441) |

5,963,781 |

||||||||||

|

Commercial mortgage-backed securities—3.0% |

|||||||||||

|

Angel Oak Mortgage Trust I LLC, Series 2018-3, Class A1, 3.649%, due 09/25/485,6 |

265,893 |

268,827 |

|||||||||

|

Series 2019-4, Class A1, 2.993%, due 07/26/495,6 |

462,233 |

463,966 |

|||||||||

|

Ashford Hospitality Trust, Series 2018-ASHF, Class D, 1 mo. USD LIBOR + 2.100%, 4.295%, due 04/15/354,5 |

200,000 |

200,563 |

|||||||||

|

Bank, Series 2017-BNK7, Class C, 4.187%, due 09/15/606 |

200,000 |

214,298 |

|||||||||

|

Series 2018-BNK14, Class E, 3.000%, due 09/15/605,6 |

350,000 |

301,252 |

|||||||||

|

BBCMS Trust, Series 2015-SRCH, Class A2, 4.197%, due 08/10/355 |

350,000 |

397,659 |

|||||||||

|

BENCHMARK Mortgage Trust, Series 2019-B10, Class C, 3.750%, due 03/15/62 |

250,000 |

265,486 |

|||||||||

|

CHT Mortgage Trust, Series 2017-COSMO, Class D, 1 mo. USD LIBOR + 2.250%, 4.445%, due 11/15/364,5 |

375,000 |

375,233 |

|||||||||

|

Citigroup Commercial Mortgage Trust, Series 2017-C4, Class D, 3.000%, due 10/12/505 |

300,000 |

283,655 |

|||||||||

|

Series 2017-P8, Class D, 3.000%, due 09/15/505 |

450,000 |

387,487 |

|||||||||

|

COMM Mortgage Trust, Series 2015-CCRE24, Class D, 3.463%, due 08/10/486 |

150,000 |

142,987 |

|||||||||

|

Series 2016-DC2, Class A5, 3.765%, due 02/10/49 |

160,000 |

174,831 |

|||||||||

|

Series 2017-COR2, Class C, 4.714%, due 09/10/506 |

500,000 |

546,053 |

|||||||||

|

Face amount |

Value |

||||||||||

|

Commercial mortgage-backed securities—(concluded) |

|||||||||||

|

Series 2018-COR3, Class C, 4.713%, due 05/10/516 |

$ |

127,000 |

$ |

141,022 |

|||||||

|

FREMF Mortgage Trust, Series 2017-K64, Class B, 4.117%, due 05/25/505,6 |

50,000 |

53,858 |

|||||||||

|

Hilton USA Trust, Series 2016-SFP, Class B, 3.323%, due 11/05/355 |

425,000 |

425,857 |

|||||||||

|

J.P. Morgan Chase Commercial Mortgage Securities Trust, Series 2018-ASH8, Class D, 1 mo. USD LIBOR + 2.050%, 4.245%, due 02/15/354,5 |

150,000 |

150,138 |

|||||||||

|

JPMBB Commercial Mortgage Securities Trust, Series 2014-C26, Class AS, 3.800%, due 01/15/48 |

250,000 |

267,548 |

|||||||||

|

Series 2015-C29, Class D, 3.795%, due 05/15/486 |

150,000 |

129,408 |

|||||||||

|

JPMDB Commercial Mortgage Securities Trust, Series 2016-C2, Class D, 3.553%, due 06/15/495,6 |

300,000 |

275,987 |

|||||||||

|

Morgan Stanley Bank of America Merrill Lynch Trust, Series 2016-C32, Class AS, 3.994%, due 12/15/496 |

260,000 |

285,984 |

|||||||||

|

Series 2017-C34, Class C, 4.325%, due 11/15/526 |

150,000 |

160,865 |

|||||||||

|

Morgan Stanley Capital I, Series 2017-HR2, Class C, 4.367%, due 12/15/506 |

250,000 |

271,246 |

|||||||||

|

Series 2017-HR2, Class D, 2.730%, due 12/15/50 |

125,000 |

114,371 |

|||||||||

|

RETL, Series 2019-RVP, Class C, 1 mo. USD LIBOR + 2.100%, 4.295%, due 03/15/364,5 |

250,000 |

251,016 |

|||||||||

|

Verus Securitization Trust, Series 2019-3, Class A1, 2.784%, due 07/25/595,7 |

297,380 |

297,959 |

|||||||||

|

Wells Fargo Commercial Mortgage Trust, Series 2018-C44, Class C, 4.997%, due 05/15/516 |

150,000 |

166,439 |

|||||||||

|

Total commercial mortgage-backed securities (cost—$6,690,483) |

7,013,995 |

||||||||||

|

Corporate bonds—12.8% |

|||||||||||

|

Aerospace & defense—0.1% |

|||||||||||

|

TransDigm, Inc. 6.250%, due 03/15/265 |

20,000 |

21,575 |

|||||||||

|

6.500%, due 07/15/24 |

20,000 |

20,650 |

|||||||||

|

6.500%, due 05/15/25 |

55,000 |

57,338 |

|||||||||

|

United Technologies Corp. 4.125%, due 11/16/28 |

150,000 |

171,645 |

|||||||||

|

271,208 |

|||||||||||

14

UBS U.S. Allocation Fund

Portfolio of investments—August 31, 2019

|

Face amount |

Value |

||||||||||

|

Corporate bonds—(continued) |

|||||||||||

|

Auto loans—0.0%† |

|||||||||||

|

General Motors Financial Co., Inc. 2.350%, due 10/04/19 |

$ |

50,000 |

$ |

49,997 |

|||||||

|

3.700%, due 11/24/20 |

60,000 |

60,862 |

|||||||||

|

110,859 |

|||||||||||

|

Automobile OEM—0.2% |

|||||||||||

|

Ford Motor Credit Co. LLC 8.125%, due 01/15/20 |

150,000 |

153,130 |

|||||||||

|

General Motors Co. 6.600%, due 04/01/36 |

100,000 |

116,110 |

|||||||||

|

6.750%, due 04/01/46 |

100,000 |

119,025 |

|||||||||

|

388,265 |

|||||||||||

|

Automotive parts—0.0%† |

|||||||||||

|

Allison Transmission, Inc. 5.000%, due 10/01/245 |

40,000 |

41,154 |

|||||||||

|

5.875%, due 06/01/295 |

15,000 |

16,087 |

|||||||||

|

Meritor, Inc. 6.250%, due 02/15/24 |

40,000 |

40,950 |

|||||||||

|

Panther BF Aggregator 2 LP/Panther Finance Co., Inc. 6.250%, due 05/15/265 |

5,000 |

5,188 |

|||||||||

|

8.500%, due 05/15/275 |

5,000 |

4,875 |

|||||||||

|

108,254 |

|||||||||||

|

Banking-non-US—0.6% |

|||||||||||

|

Australia & New Zealand Banking Group Ltd. MTN 2.700%, due 11/16/20 |

50,000 |

50,427 |

|||||||||

|

Barclays PLC 4.337%, due 01/10/28 |

305,000 |

321,428 |

|||||||||

|

Credit Suisse Group Funding Guernsey Ltd. 4.550%, due 04/17/26 |

250,000 |

277,013 |

|||||||||

|

Deutsche Bank AG 4.250%, due 02/04/21 |

150,000 |

151,689 |

|||||||||

|

HSBC Holdings PLC 6.500%, due 09/15/37 |

200,000 |

271,267 |

|||||||||

|

Lloyds Banking Group PLC 4.582%, due 12/10/25 |

200,000 |

209,923 |

|||||||||

|

Royal Bank of Scotland Group PLC (fixed, converts to FRN on 09/30/31), 7.648%, due 09/30/318 |

25,000 |

33,500 |

|||||||||

|

Standard Chartered PLC (fixed, converts to FRN on 07/30/37), 7.014%, due 07/30/375,8 |

100,000 |

112,750 |

|||||||||

|

1,427,997 |

|||||||||||

|

Banking-US—1.2% |

|||||||||||

|

BB&T Corp. MTN 2.625%, due 06/29/20 |

140,000 |

140,606 |

|||||||||

|

Capital One Bank USA N.A. 3.375%, due 02/15/23 |

70,000 |

72,232 |

|||||||||

|

Citigroup, Inc. 4.125%, due 07/25/28 |

100,000 |

109,074 |

|||||||||

|

5.500%, due 09/13/25 |

425,000 |

487,101 |

|||||||||

|

(fixed, converts to FRN on 01/30/23), 5.950%, due 01/30/238 |

65,000 |

68,413 |

|||||||||

|

6.675%, due 09/13/43 |

50,000 |

74,137 |

|||||||||

|

Face amount |

Value |

||||||||||

|

Corporate bonds—(continued) |

|||||||||||

|

Banking-US—(concluded) |

|||||||||||

|

Goldman Sachs Group, Inc./The 5.150%, due 05/22/45 |

$ |

210,000 |

$ |

256,086 |

|||||||

|

5.750%, due 01/24/22 |

200,000 |

216,546 |

|||||||||

|

JPMorgan Chase & Co. |

|||||||||||

|

(fixed, converts to FRN on 07/24/47), 4.032%, due 07/24/48 |

150,000 |

174,637 |

|||||||||

|

4.625%, due 05/10/21 |

260,000 |

270,957 |

|||||||||

|

Series R, (fixed, converts to FRN on 08/01/23), 6.000%, due 08/01/238 |

50,000 |

53,250 |

|||||||||

|

Series V, 3 mo. USD LIBOR + 3.320%, 5.639%, due 10/01/194,8 |

75,000 |

74,850 |

|||||||||

|

Morgan Stanley 4.300%, due 01/27/45 |

75,000 |

88,772 |

|||||||||

|

4.875%, due 11/01/22 |

170,000 |

182,877 |

|||||||||

|

Morgan Stanley GMTN 4.350%, due 09/08/26 |

365,000 |

399,670 |

|||||||||

|

Wells Fargo & Co. MTN (fixed, converts to FRN on 06/17/26), 3.196%, due 06/17/27 |

95,000 |

98,968 |

|||||||||

|

2,768,176 |

|||||||||||

|

Beverages—0.1% |

|||||||||||

|

Anheuser-Busch Cos. LLC/Anheuser-Busch InBev Worldwide, Inc. 4.700%, due 02/01/36 |

150,000 |

174,605 |

|||||||||

|

4.900%, due 02/01/46 |

30,000 |

35,845 |

|||||||||

|

210,450 |

|||||||||||

|

Building materials—0.2% |

|||||||||||

|

Boise Cascade Co. 5.625%, due 09/01/245 |

40,000 |

41,500 |

|||||||||

|

Builders FirstSource, Inc. 5.625%, due 09/01/245 |

68,000 |

70,805 |

|||||||||

|

6.750%, due 06/01/275 |

5,000 |

5,463 |

|||||||||

|

JELD-WEN, Inc. 4.625%, due 12/15/255 |

10,000 |

9,800 |

|||||||||

|

4.875%, due 12/15/275 |

15,000 |

14,513 |

|||||||||

|

Masco Corp. 4.450%, due 04/01/25 |

80,000 |

87,146 |

|||||||||

|

New Enterprise Stone & Lime Co., Inc. 6.250%, due 03/15/265 |

35,000 |

35,892 |

|||||||||

|

10.125%, due 04/01/225 |

75,000 |

76,687 |

|||||||||

|

Summit Materials LLC/Summit Materials Finance Corp. 6.500%, due 03/15/275 |

15,000 |

16,125 |

|||||||||

|

357,931 |

|||||||||||

|

Chemicals—0.3% |

|||||||||||

|

CF Industries, Inc. 5.375%, due 03/15/44 |

50,000 |

50,529 |

|||||||||

|

DuPont de Nemours, Inc. 4.725%, due 11/15/28 |

150,000 |

173,462 |

|||||||||

|

Kraton Polymers LLC/Kraton Polymers Capital Corp. 7.000%, due 04/15/255 |

60,000 |

62,175 |

|||||||||

15

UBS U.S. Allocation Fund

Portfolio of investments—August 31, 2019

|

Face amount |

Value |

||||||||||

|

Corporate bonds—(continued) |

|||||||||||

|

Chemicals—(concluded) |

|||||||||||

|

NOVA Chemicals Corp. 5.250%, due 06/01/275 |

$ |

75,000 |

$ |

78,281 |

|||||||

|

Sherwin-Williams Co./The 3.450%, due 06/01/27 |

80,000 |

84,508 |

|||||||||

|

4.200%, due 01/15/22 |

60,000 |

62,753 |

|||||||||

|

Tronox, Inc. 6.500%, due 04/15/265 |

25,000 |

23,750 |

|||||||||

|

W.R. Grace & Co.-Conn. 5.625%, due 10/01/245 |

50,000 |

54,000 |

|||||||||

|

589,458 |

|||||||||||

|

Commercial services—0.2% |

|||||||||||

|

AECOM 5.125%, due 03/15/27 |

55,000 |

57,448 |

|||||||||

|

5.875%, due 10/15/24 |

20,000 |

21,600 |

|||||||||

|

Booz Allen Hamilton, Inc. 5.125%, due 05/01/255 |

50,000 |

51,375 |

|||||||||

|

Brand Industrial Services, Inc. 8.500%, due 07/15/255 |

15,000 |

13,219 |

|||||||||

|

Garda World Security Corp. 8.750%, due 05/15/255 |

40,000 |

41,262 |

|||||||||

|

Harsco Corp. 5.750%, due 07/31/275 |

15,000 |

15,544 |

|||||||||

|

Herc Holdings, Inc. 5.500%, due 07/15/275 |

30,000 |

30,937 |

|||||||||

|

Hertz Corp./The 7.125%, due 08/01/265 |

25,000 |

25,513 |

|||||||||

|

Prime Security Services Borrower LLC/Prime Finance, Inc. 9.250%, due 05/15/235 |

25,000 |

26,290 |

|||||||||

|

RR Donnelley & Sons Co. 7.875%, due 03/15/21 |

10,000 |

10,000 |

|||||||||

|

Service Corp. International 5.125%, due 06/01/29 |

35,000 |

37,450 |

|||||||||

|

Weight Watchers International, Inc. 8.625%, due 12/01/255 |

25,000 |

25,062 |

|||||||||

|

355,700 |

|||||||||||

|

Communications equipment—0.0%† |

|||||||||||

|

QUALCOMM, Inc. 3.250%, due 05/20/27 |

80,000 |

83,922 |

|||||||||

|

Consumer products—0.1% |

|||||||||||

|

Avon International Capital PLC 6.500%, due 08/15/225 |

60,000 |

61,800 |

|||||||||

|

Avon International Operations, Inc. 7.875%, due 08/15/225 |

25,000 |

26,098 |

|||||||||

|

Kimberly-Clark Corp. 3.625%, due 08/01/20 |

45,000 |

45,643 |

|||||||||

|

Party City Holdings, Inc. 6.625%, due 08/01/265 |

85,000 |

80,962 |

|||||||||

|

Prestige Brands, Inc. 6.375%, due 03/01/245 |

25,000 |

26,187 |

|||||||||

|

240,690 |

|||||||||||

|

Distribution/wholesale—0.0%† |

|||||||||||

|

IAA, Inc. 5.500%, due 06/15/275 |

35,000 |

37,275 |

|||||||||

|

Face amount |

Value |

||||||||||

|

Corporate bonds—(continued) |

|||||||||||

|

Diversified manufacturing—0.2% |

|||||||||||

|

Amsted Industries, Inc. 5.625%, due 07/01/275 |

$ |

15,000 |

$ |

16,013 |

|||||||

|

Bombardier, Inc. 7.875%, due 04/15/275 |

35,000 |

33,906 |

|||||||||

|

Eaton Corp. 2.750%, due 11/02/22 |

70,000 |

71,380 |

|||||||||

|

Illinois Tool Works, Inc. 2.650%, due 11/15/26 |

110,000 |

114,487 |

|||||||||

|

3.500%, due 03/01/24 |

110,000 |

116,471 |

|||||||||

|

Terex Corp. 5.625%, due 02/01/255 |

35,000 |

35,615 |

|||||||||

|

387,872 |

|||||||||||

|

Electric-generation—0.1% |

|||||||||||

|

Calpine Corp. 5.375%, due 01/15/23 |

70,000 |

70,957 |

|||||||||

|

NRG Energy, Inc. 5.250%, due 06/15/295 |

10,000 |

10,670 |

|||||||||

|

6.625%, due 01/15/27 |

40,000 |

43,200 |

|||||||||

|

7.250%, due 05/15/26 |

35,000 |

38,369 |

|||||||||

|

163,196 |

|||||||||||

|

Electric-integrated—0.8% |

|||||||||||

|

Alabama Power Co. 6.000%, due 03/01/39 |

30,000 |

42,675 |

|||||||||

|

Berkshire Hathaway Energy Co. 3.750%, due 11/15/23 |

80,000 |

85,052 |

|||||||||

|

4.450%, due 01/15/49 |

100,000 |

122,259 |

|||||||||

|

Covanta Holding Corp. 5.875%, due 07/01/25 |

55,000 |

57,337 |

|||||||||

|

Dominion Energy, Inc. 3.900%, due 10/01/25 |

150,000 |

161,711 |

|||||||||

|

DTE Electric Co. 3.700%, due 03/15/45 |

50,000 |

55,846 |

|||||||||

|

Duke Energy Ohio, Inc. 4.300%, due 02/01/49 |

200,000 |

245,226 |

|||||||||

|

Energizer Holdings, Inc. 6.375%, due 07/15/265 |

25,000 |

26,344 |

|||||||||

|

Exelon Corp. 3.400%, due 04/15/26 |

270,000 |

286,144 |

|||||||||

|

Exelon Generation Co. LLC 2.950%, due 01/15/20 |

170,000 |

170,329 |

|||||||||

|

Florida Power & Light Co. 5.950%, due 02/01/38 |

45,000 |

64,520 |

|||||||||

|

Georgia Power Co., Series C, 2.000%, due 09/08/20 |

100,000 |

100,034 |

|||||||||

|

Indiana Michigan Power Co., Series K, 4.550%, due 03/15/46 |

100,000 |

123,313 |

|||||||||

|

Northern States Power Co. 2.600%, due 05/15/23 |

50,000 |

50,963 |

|||||||||

|

Oncor Electric Delivery Co. LLC 3.750%, due 04/01/45 |

40,000 |

45,397 |

|||||||||

|

Southern Power Co. 5.250%, due 07/15/43 |

60,000 |

70,492 |

|||||||||

16

UBS U.S. Allocation Fund

Portfolio of investments—August 31, 2019

|

Face amount |

Value |

||||||||||

|

Corporate bonds—(continued) |

|||||||||||

|

Electric-integrated—(concluded) |

|||||||||||

|

Talen Energy Supply LLC 6.625%, due 01/15/285 |

$ |

10,000 |

$ |

9,675 |

|||||||

|

7.250%, due 05/15/275 |

5,000 |

4,963 |

|||||||||

|

10.500%, due 01/15/265 |

35,000 |

31,815 |

|||||||||

|

Vistra Operations Co. LLC 5.000%, due 07/31/275 |

65,000 |

67,112 |

|||||||||

|

5.500%, due 09/01/265 |

85,000 |

89,250 |

|||||||||

|

Waste Pro USA, Inc. 5.500%, due 02/15/265 |

25,000 |

26,000 |

|||||||||

|

1,936,457 |

|||||||||||

|

Energy-independent—0.4% |

|||||||||||

|

Apache Corp. 4.375%, due 10/15/28 |

150,000 |

154,157 |

|||||||||

|

Ascent Resources Utica Holdings LLC/ARU Finance Corp. 7.000%, due 11/01/265 |

20,000 |

16,519 |

|||||||||

|

10.000%, due 04/01/225 |

24,000 |

24,060 |

|||||||||

|

California Resources Corp. 8.000%, due 12/15/225 |

15,000 |

8,625 |

|||||||||

|

Canadian Natural Resources Ltd. 3.850%, due 06/01/27 |

200,000 |

211,845 |

|||||||||

|

Carrizo Oil & Gas, Inc. 6.250%, due 04/15/23 |

40,000 |

38,260 |

|||||||||

|

Centennial Resource Production LLC 6.875%, due 04/01/275 |

20,000 |

20,000 |

|||||||||

|

Chesapeake Energy Corp. 7.500%, due 10/01/26 |

15,000 |

10,275 |

|||||||||

|

8.000%, due 06/15/27 |

20,000 |

14,450 |

|||||||||

|

Continental Resources, Inc. 5.000%, due 09/15/22 |

80,000 |

80,712 |

|||||||||

|

Gulfport Energy Corp. 6.375%, due 05/15/25 |

40,000 |

28,800 |

|||||||||

|

Hilcorp Energy I LP/Hilcorp Finance Co. 5.750%, due 10/01/255 |

40,000 |

37,300 |

|||||||||

|

6.250%, due 11/01/285 |

10,000 |

9,200 |

|||||||||

|

MEG Energy Corp. 6.500%, due 01/15/255 |

45,000 |

45,225 |

|||||||||

|

Oasis Petroleum, Inc. 6.250%, due 05/01/265 |

25,000 |

20,156 |

|||||||||

|

Occidental Petroleum Corp. 3.400%, due 04/15/26 |

50,000 |

50,859 |

|||||||||

|

Parsley Energy LLC/Parsley Finance Corp. 5.375%, due 01/15/255 |

60,000 |

61,200 |

|||||||||

|

QEP Resources, Inc. 5.250%, due 05/01/23 |

25,000 |

21,875 |

|||||||||

|

SM Energy Co. 6.125%, due 11/15/22 |

38,000 |

35,340 |

|||||||||

|

6.625%, due 01/15/27 |

10,000 |

8,500 |

|||||||||

|

Whiting Petroleum Corp. 6.250%, due 04/01/23 |

35,000 |

27,475 |

|||||||||

|

WPX Energy, Inc. 5.250%, due 09/15/24 |

20,000 |

20,300 |

|||||||||

|

5.750%, due 06/01/26 |

35,000 |

36,312 |

|||||||||

|

981,445 |

|||||||||||

|

Face amount |

Value |

||||||||||

|

Corporate bonds—(continued) |

|||||||||||

|

Energy-integrated—0.0%† |

|||||||||||