UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-06279

Harris Associates Investment Trust

(Exact name of Registrant as specified in charter)

111 South Wacker Drive, Suite 4600

Chicago, Illinois 60606-4319

(Address of principal executive offices) (Zip code)

| Rana J. Wright | Ndenisarya M. Bregasi, Esq. | |

| Harris Associates L.P. | K&L Gates LLP | |

| 111 South Wacker Drive, Suite 4600 | 1601 K Street, N.W. | |

| Chicago, Illinois 60606-4319 | Washington, D.C. 20006-1600 | |

| (Name and address of agents for service) | ||

Registrant's telephone number, including area code: (312) 646-3600

Date of fiscal year end: 09/30/21

Date of reporting period: 03/31/22

Item 1. Reports to Shareholders.

| (a) | Following is a copy of the semi-annual report transmitted to shareholders pursuant to Rule 30e-1 under the Act. |

OAKMARK FUNDS

SEMI-ANNUAL REPORT | MARCH 31, 2022

OAKMARK FUND

OAKMARK SELECT FUND

OAKMARK GLOBAL FUND

OAKMARK GLOBAL SELECT FUND

OAKMARK INTERNATIONAL FUND

OAKMARK INTERNATIONAL SMALL CAP FUND

OAKMARK EQUITY AND INCOME FUND

OAKMARK BOND FUND

Oakmark Funds

2022 Semi-Annual Report

TABLE OF CONTENTS

|

Fund Expenses |

1 |

||||||

|

Commentary on Oakmark and Oakmark Select Funds |

2 |

||||||

|

Oakmark Fund |

|||||||

|

Summary Information |

4 |

||||||

|

Portfolio Manager Commentary |

5 |

||||||

|

Schedule of Investments |

7 |

||||||

|

Oakmark Select Fund |

|||||||

|

Summary Information |

10 |

||||||

|

Portfolio Manager Commentary |

11 |

||||||

|

Schedule of Investments |

12 |

||||||

|

Oakmark Global Fund |

|||||||

|

Summary Information |

14 |

||||||

|

Portfolio Manager Commentary |

15 |

||||||

|

Schedule of Investments |

17 |

||||||

|

Oakmark Global Select Fund |

|||||||

|

Summary Information |

20 |

||||||

|

Portfolio Manager Commentary |

21 |

||||||

|

Schedule of Investments |

22 |

||||||

|

Commentary on Oakmark International and Oakmark International Small Cap Funds |

24 |

||||||

|

Oakmark International Fund |

|||||||

|

Summary Information |

26 |

||||||

|

Portfolio Manager Commentary |

27 |

||||||

|

Schedule of Investments |

29 |

||||||

|

Oakmark International Small Cap Fund |

|||||||

|

Summary Information |

32 |

||||||

|

Portfolio Manager Commentary |

33 |

||||||

|

Schedule of Investments |

34 |

||||||

|

Oakmark Equity and Income Fund |

|||||||

|

Summary Information |

38 |

||||||

|

Portfolio Manager Commentary |

39 |

||||||

|

Schedule of Investments |

42 |

||||||

|

Oakmark Bond Fund |

|||||||

|

Summary Information |

48 |

||||||

|

Portfolio Manager Commentary |

49 |

||||||

|

Schedule of Investments |

52 |

||||||

|

Financial Statements |

|||||||

|

Statements of Assets and Liabilities |

55 |

||||||

|

Statements of Operations |

58 |

||||||

|

Statements of Changes in Net Assets |

61 |

||||||

|

Notes to Financial Statements |

77 |

||||||

|

Financial Highlights |

88 |

||||||

|

Disclosure Regarding Investment Advisory Agreements Approval |

96 |

||||||

|

Disclosures and Endnotes |

100 |

||||||

|

Trustees and Officers |

105 |

||||||

|

As permitted by regulations adopted by the U.S. Securities and Exchange Commission, paper copies of the Oakmark Funds' annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on Oakmark.com, and you will be notified by mail each time a report is posted and provided with a website link to access the report. If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Funds electronically anytime by contacting your financial intermediary (such as a broker-dealer or bank) or, if you hold your shares directly with the Funds, by calling 1-800-OAKMARK (625-6275) or visiting Oakmark.com. |

|||

You may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you hold your shares directly with the Funds, you can call 1-800-OAKMARK (625-6275) to let the Funds know you wish to continue receiving paper copies of your shareholder reports. Your election to receive reports in paper will apply to all Funds you hold directly or all Funds you hold through your financial intermediary, as applicable.

FORWARD-LOOKING STATEMENT DISCLOSURE

One of our most important responsibilities as mutual fund managers is to communicate with shareholders in an open and direct manner. Some of our comments in our letters to shareholders are based on current management expectations and are considered "forward-looking statements." Actual future results, however, may prove to be different from our expectations. You can identify forward-looking statements by words such as "estimate," "may," "will," "expect," "believe,"

"plan" and other similar terms. We cannot promise future returns. Our opinions are a reflection of our best judgment at the time this report is compiled, and we disclaim any obligation to update or alter forward-looking statements as a result of new information, future events or otherwise.

Oakmark.com

Expense Example

A shareholder of each Fund incurs ongoing costs, including investment advisory fees, transfer agent fees and other Fund expenses. The examples below are intended to help shareholders understand the ongoing costs (in dollars) of investing in each Fund and to compare these costs with the ongoing costs of investing in other funds.

The following table provides information about actual account values and actual Fund expenses as well as hypothetical account values and hypothetical fund expenses for shares of each Fund.

ACTUAL EXPENSES

The following table shows the expenses a shareholder would have paid on a $1,000 investment in each Fund from October 1, 2021 to March 31, 2022, as well as how much a $1,000 investment would be worth at the close of the period, assuming actual Fund returns and expenses. A shareholder can estimate expenses incurred for the period by dividing the account value at March 31, 2022, by $1,000 and multiplying the result by the number in the "Actual—Expenses Paid During Period" column shown below.

HYPOTHETICAL EXAMPLE FOR COMPARISON PURPOSES

The following table provides information about hypothetical account values and hypothetical expenses for shares of each Fund based on actual expense ratios and an assumed rate of return of 5% per year before expenses, which are not the Funds' actual returns. The hypothetical account values and expenses may not be used to estimate the actual ending account balances or actual expenses shareholders paid for the period. Shareholders may use this information to compare the ongoing costs of investing in a Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs, such as redemption fees. Therefore, the "Hypothetical—Expenses Paid During Period" column of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. If these transaction costs were included, the total costs would have been higher.

|

ACTUAL |

HYPOTHETICAL (5% annual return before expenses) |

||||||||||||||||||||||||||

|

Beginning Account Value (10/01/21) |

Ending Account Value (03/31/22) |

Expenses Paid During Period* |

Ending Account Value (03/31/22) |

Expenses Paid During Period* |

Annualized Expense Ratio |

||||||||||||||||||||||

|

Oakmark Fund |

|||||||||||||||||||||||||||

|

Investor Class |

$ |

1,000.00 |

$ |

1,019.80 |

$ |

4.53 |

$ |

1,020.44 |

$ |

4.53 |

0.90 |

% |

|||||||||||||||

|

Advisor Class |

$ |

1,000.00 |

$ |

1,021.00 |

$ |

3.38 |

$ |

1,021.59 |

$ |

3.38 |

0.67 |

% |

|||||||||||||||

|

Institutional Class |

$ |

1,000.00 |

$ |

1,021.00 |

$ |

3.38 |

$ |

1,021.59 |

$ |

3.38 |

0.67 |

% |

|||||||||||||||

|

R6 Class |

$ |

1,000.00 |

$ |

1,021.30 |

$ |

3.12 |

$ |

1,021.84 |

$ |

3.13 |

0.62 |

% |

|||||||||||||||

|

Oakmark Select Fund |

|||||||||||||||||||||||||||

|

Investor Class |

$ |

1,000.00 |

$ |

971.60 |

$ |

4.82 |

$ |

1,020.04 |

$ |

4.94 |

0.98 |

% |

|||||||||||||||

|

Advisor Class |

$ |

1,000.00 |

$ |

972.40 |

$ |

4.18 |

$ |

1,020.69 |

$ |

4.28 |

0.85 |

% |

|||||||||||||||

|

Institutional Class |

$ |

1,000.00 |

$ |

972.80 |

$ |

3.84 |

$ |

1,021.04 |

$ |

3.93 |

0.78 |

% |

|||||||||||||||

|

R6 Class |

$ |

1,000.00 |

$ |

972.80 |

$ |

3.59 |

$ |

1,021.29 |

$ |

3.68 |

0.73 |

% |

|||||||||||||||

|

Oakmark Global Fund |

|||||||||||||||||||||||||||

|

Investor Class |

$ |

1,000.00 |

$ |

981.90 |

$ |

5.48 |

$ |

1,019.40 |

$ |

5.59 |

1.11 |

% |

|||||||||||||||

|

Advisor Class |

$ |

1,000.00 |

$ |

982.70 |

$ |

4.50 |

$ |

1,020.39 |

$ |

4.58 |

0.91 |

% |

|||||||||||||||

|

Institutional Class |

$ |

1,000.00 |

$ |

982.90 |

$ |

4.35 |

$ |

1,020.54 |

$ |

4.43 |

0.88 |

% |

|||||||||||||||

|

R6 Class |

$ |

1,000.00 |

$ |

982.80 |

$ |

4.20 |

$ |

1,020.69 |

$ |

4.28 |

0.85 |

% |

|||||||||||||||

|

Oakmark Global Select Fund |

|||||||||||||||||||||||||||

|

Investor Class |

$ |

1,000.00 |

$ |

950.10 |

$ |

5.25 |

$ |

1,019.55 |

$ |

5.44 |

1.08 |

% |

|||||||||||||||

|

Advisor Class |

$ |

1,000.00 |

$ |

951.10 |

$ |

4.43 |

$ |

1,020.39 |

$ |

4.58 |

0.91 |

% |

|||||||||||||||

|

Institutional Class |

$ |

1,000.00 |

$ |

951.20 |

$ |

4.23 |

$ |

1,020.59 |

$ |

4.38 |

0.87 |

% |

|||||||||||||||

|

R6 Class |

$ |

1,000.00 |

$ |

951.50 |

$ |

3.99 |

$ |

1,020.84 |

$ |

4.13 |

0.82 |

% |

|||||||||||||||

|

Oakmark International Fund |

|||||||||||||||||||||||||||

|

Investor Class |

$ |

1,000.00 |

$ |

922.10 |

$ |

4.98 |

$ |

1,019.75 |

$ |

5.24 |

1.04 |

% |

|||||||||||||||

|

Advisor Class |

$ |

1,000.00 |

$ |

923.10 |

$ |

4.12 |

$ |

1,020.64 |

$ |

4.33 |

0.86 |

% |

|||||||||||||||

|

Institutional Class |

$ |

1,000.00 |

$ |

923.40 |

$ |

3.79 |

$ |

1,020.99 |

$ |

3.98 |

0.79 |

% |

|||||||||||||||

|

R6 Class |

$ |

1,000.00 |

$ |

923.60 |

$ |

3.60 |

$ |

1,021.19 |

$ |

3.78 |

0.75 |

% |

|||||||||||||||

|

Oakmark International Small Cap Fund |

|||||||||||||||||||||||||||

|

Investor Class |

$ |

1,000.00 |

$ |

896.20 |

$ |

6.29 |

$ |

1,018.30 |

$ |

6.69 |

1.33 |

% |

|||||||||||||||

|

Advisor Class |

$ |

1,000.00 |

$ |

896.50 |

$ |

5.44 |

$ |

1,019.20 |

$ |

5.79 |

1.15 |

% |

|||||||||||||||

|

Institutional Class |

$ |

1,000.00 |

$ |

897.10 |

$ |

5.11 |

$ |

1,019.55 |

$ |

5.44 |

1.08 |

% |

|||||||||||||||

|

R6 Class |

$ |

1,000.00 |

$ |

897.30 |

$ |

4.97 |

$ |

1,019.70 |

$ |

5.29 |

1.05 |

% |

|||||||||||||||

|

Oakmark Equity and Income Fund |

|||||||||||||||||||||||||||

|

Investor Class |

$ |

1,000.00 |

$ |

997.30 |

$ |

4.13 |

$ |

1,020.79 |

$ |

4.18 |

0.83 |

% |

|||||||||||||||

|

Advisor Class |

$ |

1,000.00 |

$ |

998.10 |

$ |

2.89 |

$ |

1,022.04 |

$ |

2.92 |

0.58 |

% |

|||||||||||||||

|

Institutional Class |

$ |

1,000.00 |

$ |

998.10 |

$ |

2.89 |

$ |

1,022.04 |

$ |

2.92 |

0.58 |

% |

|||||||||||||||

|

R6 Class |

$ |

1,000.00 |

$ |

998.30 |

$ |

2.69 |

$ |

1,022.24 |

$ |

2.72 |

0.54 |

% |

|||||||||||||||

|

Oakmark Bond Fund |

|||||||||||||||||||||||||||

|

Investor Class |

$ |

1,000.00 |

$ |

966.10 |

$ |

1.24 |

(a) |

$ |

1,021.24 |

$ |

3.73 |

0.74 |

% |

||||||||||||||

|

Advisor Class |

$ |

1,000.00 |

$ |

947.50 |

$ |

2.62 |

$ |

1,022.24 |

$ |

2.72 |

0.54 |

% |

|||||||||||||||

|

Institutional Class |

$ |

1,000.00 |

$ |

947.50 |

$ |

2.52 |

$ |

1,022.34 |

$ |

2.62 |

0.52 |

% |

|||||||||||||||

|

R6 Class |

$ |

1,000.00 |

$ |

947.90 |

$ |

2.14 |

$ |

1,022.74 |

$ |

2.22 |

0.44 |

% |

|||||||||||||||

* Expenses are calculated using the Annualized Expense Ratio, multiplied by the average account value over the period, multiplied by 182 and divided by 365 (to reflect one-half year period)

(a) Expenses are calculated using the Annualized Expense Ratio, multiplied by the average account value over the period, multiplied by 62 and divided by 365 (to reflect number of days the class was open)

Oakmark.com 1

Oakmark and Oakmark Select Funds March 31, 2022

Portfolio Manager Commentary

William C. Nygren, CFA

Portfolio Manager

oakmx@oakmark.com

oaklx@oakmark.com

oakwx@oakmark.com

At Oakmark, we are long-term investors. We attempt to identify growing businesses that are managed to benefit their shareholders. We will purchase stock in those businesses only when priced substantially below our estimate of intrinsic value. After purchase, we patiently wait for the gap between stock price and intrinsic value to close.

"Fear and pessimism bring opportunities."

-Michael Price (1951-2022)

The commentary I wrote in 2016 for Oakmark's 25-year anniversary looked back at the investment performance of the Fund and the stock market in the context of the many events in the world that investors worried about. The conclusion was that investors did just fine despite one crisis after another—and this conclusion still holds true today.

The Oakmark Fund was launched in 1991 shortly after Operation Desert Storm, in which the United States led a multi-nation coalition that prevented Iraq from annexing Kuwait. Today we remember that conflict mostly for how fast victory was achieved—six weeks of bombing followed by only four days of armed combat. But before the fighting began, there was tremendous fear that we could lose to Iraq's highly trained Republican Army, that losing access to Middle Eastern oil could cause a global depression and that Iraqi use of weapons of mass destruction could kill people across the world. I remember one of Harris Associates' founding partners, Myron Szold, saying, "Betting that the world is going to end is the worst bet you can make. You're unlikely to win, and even if you do, you can't collect."

They say history doesn't repeat; it rhymes. Many of today's concerns about the tragedy in Ukraine seem analogous to the concerns investors had about war in Iraq when we were preparing to launch the Oakmark Fund in 1991. One analyst report last month grabbed headlines when it predicted a 10% probability that Russia's attack on Ukraine would spread and end civilization. It may sound cavalier to ignore that risk, but using Myron's logic, there is no payoff to structuring a portfolio for the end of civilization. We believe it is reassuring to put current events into context as we determine how to invest our assets today.

Here is an update to the list I used in 2016 of troubling events we've been through since we started the Oakmark Fund in 1991. We've experienced the following, roughly by year:

• Operation Desert Storm

• Global Recession

• Hillarycare

• Fed Increasing Interest Rates

• Oklahoma City Bombing

• U.S. Government Shutdown

• Mad Cow Disease

• Asian Flu

• Clinton Impeachment

• Y2K

• Tech Bubble

• 9/11

• Afghan War

• Recession

• Iraq War

• SARS

• Hurricane Katrina

• Subprime Mortgage Crisis

• Lehman Bros. Bankruptcy

• Obamacare

• Real Estate Collapse

• Global Financial Crisis

• Greek Bailout

• S&P Downgrading U.S. Debt

• Oil Price Collapse

• Ebola

• Ukraine/Crimea/Russia

• Syrian Migrant Crisis

• Brexit

• Divisive Presidential Election

• Trump Impeachment

• China Trade War

• Covid-19

• Inflation Acceleration

• Ukraine/Russia

That's an intimidating list. In 2016, I wrote that despite all that went wrong in the world, an investor who bought the S&P 500 in 1991 and held their position through 2016 would have accumulated more than nine times their initial capital. And that return is despite experiencing eight corrections and three bear markets. (Corrections are defined as a drop of at least 10% in the S&P 500, a level reached in the past quarter; and bear markets are declines of over 20%.) Though it is tempting to use world events to try to profitably move in and out of the market, it's hard to improve on that buy-and-hold record by picking the right periods to sit out. Likewise, during those 25 years, the Oakmark Fund had periods of both good and bad returns relative to the S&P 500, but an investor who bought at the

See accompanying Disclosures and Endnotes on page 100.

2 OAKMARK FUNDS

Oakmark and Oakmark Select Funds March 31, 2022

Portfolio Manager Commentary (continued)

beginning in 1991 and held through 2016 ended with more than 19 times their starting capital. Those 25 years included many frustrating times when fundamental value investing was out of favor, but the 25-year return of over twice the S&P 500 would have been difficult to improve on by trying to guess when our investment style was going to be in favor.

Updating those numbers through the end of March 2022 shows that over the past six years the S&P 500 investor more than doubled their capital, going from nine times to more than 20 times the original value. That return was despite experiencing four corrections and two bear markets. And even though the Oakmark Fund hasn't quite kept pace with the S&P 500 since 2016, our investors have grown their capital from 19 times to nearly 40 times the original value, roughly double the return of the S&P 500.

When confronted with global uncertainty, it can be difficult to imagine what the next year or even the next month will bring, and that can be scary. But at Oakmark, we are anchored by an investment philosophy that exploits deviations between current prices and long-term values. We only own stocks that are selling at unusually large discounts to what we believe those businesses will be worth roughly seven years from now. The events investors worry about might lead to significant reductions in current earnings, but that is usually transitory. It is rare for such issues to cause meaningful reductions in estimates of long-term business value. That is why in periods of high volatility, as occurred this past quarter, we see opportunity and often make more portfolio changes than usual.

My favorite sporting event is March Madness. The David versus Goliath early-round matchups are the most fun. Every couple of years a huge favorite gets knocked off by a small school we've barely heard of. In this year's first round, oddsmakers gave perennial favorite and number-2 seed Kentucky a 95% chance of beating number-15 seed St. Peter's. And though it ruined my bracket, watching the kids from St. Peter's celebrate their win is what makes March Madness must-see TV.

We don't know which game will produce the huge March Madness upset, but we've come to expect them. There are eight matchups annually between 1- or 2-seeds and 15- or 16-seeds. If each underdog has a 5% chance of winning, there is a 34% chance that a major upset happens in any given year. I wish investors could think about stock market corrections like March Madness upsets. They are to be expected, happening about every two years. And just like the winning bracket is not the one that anticipates the most upsets, the best long-term investment record is not the one that anticipates the most corrections. I'm not going to take the analogy so far as to say that you can actually enjoy the corrections as much as you enjoy the upsets, but you can use them to your advantage.

We encourage shareholders to have a target for the percentage of their assets they want to have invested in the stock market. When stock prices fall, stocks will fall below that percentage target. But individual investors often sell after stock prices fall. This not only hurts their returns, but it moves their portfolios further away from their targets. If you buy after your percentage in stocks has fallen below your target and sell after it has risen above the target, you can avoid the trap of buying high and selling low.

When world events cause the stock market to fall, don't join in the panic. Check your portfolio. And if stocks have fallen

meaningfully under your target weighting, take advantage of the cheaper prices. It won't be as much fun as watching St. Peter's celebrate, but it may ease the pain and boost your returns.

See accompanying Disclosures and Endnotes on page 100.

Oakmark.com 3

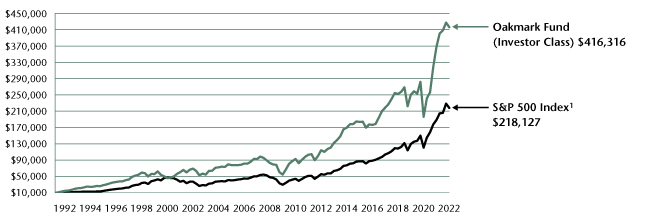

Oakmark Fund March 31, 2022

Summary Information

VALUE OF A $10,000 INVESTMENT

Since Inception - 08/05/91 (Unaudited)

PERFORMANCE

|

Average Annual Total Returns (as of 03/31/22) |

|||||||||||||||||||||||||||||||

| (Unaudited) |

Total Return Last 3 Months |

1-year |

3-year |

5-year |

10-year |

Since Inception |

Inception Date |

||||||||||||||||||||||||

|

Oakmark Fund (Investor Class) |

-2.63 |

% |

13.12 |

% |

18.41 |

% |

13.73 |

% |

13.80 |

% |

12.94 |

% |

08/05/91 |

||||||||||||||||||

|

S&P 500 Index |

-4.60 |

% |

15.65 |

% |

18.92 |

% |

15.99 |

% |

14.64 |

% |

10.58 |

% |

|||||||||||||||||||

|

Dow Jones Industrial Average2 |

-4.10 |

% |

7.11 |

% |

12.57 |

% |

13.40 |

% |

12.77 |

% |

10.91 |

% |

|||||||||||||||||||

|

Lipper Large-Cap Value Funds Index3 |

-0.93 |

% |

11.73 |

% |

14.09 |

% |

11.41 |

% |

11.82 |

% |

9.27 |

% |

|||||||||||||||||||

|

Oakmark Fund (Advisor Class) |

-2.56 |

% |

13.37 |

% |

18.59 |

% |

13.88 |

% |

N/A |

14.18 |

% |

11/30/16 |

|||||||||||||||||||

|

Oakmark Fund (Institutional Class) |

-2.56 |

% |

13.39 |

% |

18.65 |

% |

13.94 |

% |

N/A |

14.23 |

% |

11/30/16 |

|||||||||||||||||||

|

Oakmark Fund (R6 Class) |

-2.56 |

% |

13.43 |

% |

N/A |

N/A |

N/A |

25.19 |

% |

12/15/20 |

|||||||||||||||||||||

The graph and table above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Past performance is no guarantee of future results. The performance data quoted represents past performance. Current performance may be lower or higher than the performance data quoted. Total return includes change in share prices and, in each case, includes reinvestment of dividends and capital gain distributions. The investment return and principal value vary so that an investor's shares, when redeemed, may be worth more or less than the original cost. To obtain the most recent month-end performance, please visit Oakmark.com.

|

TOP TEN EQUITY HOLDINGS4 |

% of Net Assets | ||||||

|

EOG Resources, Inc. |

3.5 |

||||||

|

Alphabet, Inc., Class A |

3.2 |

||||||

|

Ally Financial, Inc. |

3.2 |

||||||

|

APA Corp. |

2.9 |

||||||

|

The Charles Schwab Corp. |

2.7 |

||||||

|

Capital One Financial Corp. |

2.6 |

||||||

|

ConocoPhillips |

2.6 |

||||||

|

American International Group, Inc. |

2.2 |

||||||

|

Citigroup, Inc. |

2.2 |

||||||

|

Charter Communications, Inc., Class A |

2.2 |

||||||

|

FUND STATISTICS |

|||||||

|

Ticker* |

OAKMX |

||||||

|

Number of Equity Holdings |

56 |

||||||

|

Net Assets |

$18 billion | ||||||

|

Weighted Average Market Cap |

$149.3 billion | ||||||

|

Median Market Cap |

$57.9 billion | ||||||

|

Gross Expense Ratio - Investor Class*^ |

0.93% | ||||||

|

Net Expense Ratio - Investor Class*†^ |

0.91% | ||||||

* This information is related to the Investor Class. Please visit Oakmark.com for information related to the Advisor, Institutional and R6 Classes.

† The net expense ratio reflects a contractual advisory fee waiver agreement through January 27, 2023.

^ The Gross Expense Ratio and Net Expense Ratio are from the Fund's Prospectus dated January 28, 2022.

|

SECTOR ALLOCATION |

% of Net Assets | ||||||

|

Financials |

29.7 |

||||||

|

Communication Services |

14.8 |

||||||

|

Information Technology |

10.5 |

||||||

|

Energy |

10.4 |

||||||

|

Consumer Discretionary |

9.0 |

||||||

|

Health Care |

7.1 |

||||||

|

Consumer Staples |

5.8 |

||||||

|

Industrials |

4.9 |

||||||

|

Real Estate |

1.2 |

||||||

|

Short-Term Investments and Other |

6.6 |

||||||

See accompanying Disclosures and Endnotes on page 100.

4 OAKMARK FUNDS

Oakmark Fund March 31, 2022

Portfolio Manager Commentary

William C. Nygren, CFA

Portfolio Manager

oakmx@oakmark.com

Michael A. Nicolas, CFA

Portfolio Manager

oakmx@oakmark.com

The Oakmark Fund generated a –3% return during the first quarter, outperforming the S&P 500 Index's1 return of –5%. Our holdings in the energy sector were the biggest contributor to our outperformance during the period, whereas our holdings in the communication services sector detracted the most. Our highest contributing securities during the period were EOG Resources and APA Corp, while our largest detractors were Netflix and Meta Platforms. We continue to own each of these investments given their significant discounts to our estimates of business value, and we added exposure to both Meta Platforms and Netflix.

We took advantage of the market's heightened volatility during the quarter by adding six new positions to the portfolio. (See descriptions below.) We also eliminated our holdings in ADP, Mastercard, and S&P Global. Each of these successful investments approached our estimate of intrinsic value and was sold to pursue more attractive alternatives.

A close look at the portfolio shows an increase in options positions. We use options for two reasons. We frequently use them as part of our tax-loss selling to reduce taxable capital gain distributions. What you see this quarter, however, is different. When other investors believe our companies are substantially riskier than we do, options prices will be higher than our estimate of their intrinsic value. When opportunities like this surface, we'll sell puts or calls as an alternative to purchasing or selling shares, respectively. During the quarter, we took advantage of elevated volatility by selling calls against a small portion of our energy holdings instead of trimming them. We also sold puts on Meta Platforms (rather than adding to it) and Amazon (to initiate a new position).

The following is a brief description of our new holdings:

Amazon is the leading e-commerce and cloud-computing provider in the world. In e-commerce, two-thirds of U.S. households are Amazon Prime subscribers, and over half of all online product searches now start on Amazon. We believe the company's strong customer loyalty and massive infrastructure are significant barriers to entry in a growing e-commerce market. Separately, Amazon Web Services (AWS) controls nearly half of the market in cloud computing. We believe AWS has become utility-like in nature and scale, and we expect healthy growth moving forward as IT workloads continue moving to the cloud. More recently, concerns about rising investment spending have weighed on the stock—as they have in times past—providing us another opportunity to purchase shares at an attractive multiple of normalized earnings and a discount to its peer-weighted enterprise value-to-sales multiple.

Equifax is one of the leading U.S. credit bureaus. The company competes in a triopoly with TransUnion and Experian, all of which are great businesses due to their entrenched competitive position, valuable data sets, deep client integration and pricing

power. In our view, what separates Equifax from its peers is its proprietary Workforce Solutions database, which is now its largest and most differentiated business. Workforce Solutions is an income and employment database used to evaluate the creditworthiness of a consumer in real-time. Furthermore, Equifax's collection of alternative data is becoming increasingly important to lenders so they can assess the creditworthiness of consumers with thin or even nonexistent credit files. We were able to purchase this well-managed company at an attractive valuation due to concerns that rising interest rates would adversely affect credit inquiries. Despite these near-term headwinds, Equifax recently reiterated full-year guidance and continues to expect significant market outgrowth. Longer term, the company anticipates 7-10% organic sales growth, an outlook that we believe is not properly reflected in today's stock price.

Global Payments is a leading provider of merchant acquiring services. The company is also one of the largest providers of payment processing and related technology solutions to credit card issuers. We believe Global Payments' merchant acquiring business is well positioned given its strength in software-driven payments. This is one of the fastest growing parts of the industry as small business customers are increasingly recognizing the efficiency benefits of having payments seamlessly integrated into the software they use to run their businesses. In addition, Global Payments benefits from the broader secular shift away from cash and toward electronic payment methods. Together, these tailwinds have the potential to drive low-double-digit revenue growth and even faster earnings growth. With this strong outlook and with management returning a significant portion of free cash flow to shareholders via repurchase, we think the stock looks attractive at its current valuation of just 12.5x next year's expected EPS.5

We previously had an opportunity to own Pinterest when the stock sold off during the Covid-19-related downturn, and we were pleased to be able to invest in the company once again at an attractive price during the quarter. Pinterest is an online personal discovery tool that people use to find ideas based on their tastes and interests. Unlike most social media companies, the objectives of users and advertisers are fundamentally aligned on Pinterest. Users find a positive and useful product discovery experience, and advertisers find an audience with high commercial intent and the ability to integrate ads naturally. Although Pinterest had more than 430 million global users as of year-end, the company is still in the early days of monetizing its platform. We believe that its shares trade well below fair value on conventional metrics, such as enterprise value to revenue, as well as when we benchmark its ultimate revenue and margin potential against more mature internet companies.

Pulte is one of the nation's largest homebuilders. While demographic tailwinds are expected to support healthy housing

See accompanying Disclosures and Endnotes on page 100.

Oakmark.com 5

Oakmark Fund March 31, 2022

Portfolio Manager Commentary (continued)

demand for years to come, more important to our thesis is the company's operational transformation over the past decade. Having adopted a more rigorous, returns-driven approach to land acquisition and manufacturing, Pulte now consistently earns returns on equity near the high end of its peer group. We expect the company to generate approximately 15% of its market cap in free cash flow this year, and management is putting that cash to good use by strengthening its balance sheet and returning capital to shareholders. While we recognize that the recent surge in home prices is producing a level of profitability that's above what we would consider "normal," we still find the stock attractive relative to our more tempered estimate of mid-cycle earnings.

Over the past 20 years, Salesforce has become a dominant global player in sales, customer service, commerce and marketing software. CRM earns 80% gross margins, grows 20% organically and virtually all of its revenue is recurring. It's a great business that we've admired from afar for a long time. More recently, the organization has made some changes at the top that prompted us to take a closer look at the stock. New CEO Bret Taylor and CFO Amy Weaver are bringing a culture of financial discipline. We believe this renewed focus on profitability, combined with Salesforce's strong underlying business characteristics, will yield strong results. The current valuation of 5x next year's revenues represents a significant discount compared to publicly traded comparables and private market values in the software space. We view this discount as an opportunity to invest in a great business at a good value.

We thank you, our fellow shareholders, for your investment and continued support of the Oakmark Fund.

See accompanying Disclosures and Endnotes on page 100.

6 OAKMARK FUNDS

Oakmark Fund March 31, 2022 (Unaudited)

Schedule of Investments (in thousands)

|

Shares |

Value |

||||||||||

|

COMMON STOCKS - 93.4% |

|||||||||||

|

FINANCIALS - 29.7% |

|||||||||||

|

DIVERSIFIED FINANCIALS - 19.0% |

|||||||||||

|

Ally Financial, Inc. |

13,243 |

$ |

575,810 |

||||||||

|

The Charles Schwab Corp. |

5,709 |

481,326 |

|||||||||

|

Capital One Financial Corp. |

3,597 |

472,250 |

|||||||||

|

The Goldman Sachs Group, Inc. |

1,105 |

364,760 |

|||||||||

|

American Express Co. |

1,804 |

337,404 |

|||||||||

|

Intercontinental Exchange, Inc. |

2,400 |

317,088 |

|||||||||

|

State Street Corp. |

3,568 |

310,827 |

|||||||||

|

KKR & Co., Inc. |

4,030 |

235,634 |

|||||||||

|

The Bank of New York Mellon Corp. |

4,335 |

215,123 |

|||||||||

|

Moody's Corp. |

330 |

111,302 |

|||||||||

|

3,421,524 |

|||||||||||

|

INSURANCE - 5.5% |

|||||||||||

|

American International Group, Inc. |

6,293 |

394,999 |

|||||||||

|

Willis Towers Watson PLC |

1,350 |

318,897 |

|||||||||

|

Reinsurance Group of America, Inc. |

2,519 |

275,733 |

|||||||||

|

989,629 |

|||||||||||

|

BANKS - 5.2% |

|||||||||||

|

Citigroup, Inc. |

7,324 |

391,112 |

|||||||||

|

Wells Fargo & Co. |

7,000 |

339,220 |

|||||||||

|

Bank of America Corp. |

4,946 |

203,854 |

|||||||||

|

934,186 |

|||||||||||

|

5,345,339 |

|||||||||||

|

COMMUNICATION SERVICES - 14.8% |

|||||||||||

|

MEDIA & ENTERTAINMENT - 13.4% |

|||||||||||

|

Alphabet, Inc., Class A (a) |

210 |

583,569 |

|||||||||

|

Charter Communications, Inc., Class A (a) |

711 |

387,592 |

|||||||||

|

Netflix, Inc. (a) |

903 |

338,105 |

|||||||||

|

Meta Platforms, Inc., Class A (a) (b) |

1,330 |

295,828 |

|||||||||

|

Comcast Corp., Class A |

6,261 |

293,144 |

|||||||||

|

Take-Two Interactive Software, Inc. (a) |

1,700 |

261,358 |

|||||||||

|

Pinterest, Inc., Class A (a) |

10,000 |

246,100 |

|||||||||

|

2,405,696 |

|||||||||||

|

TELECOMMUNICATION SERVICES - 1.4% |

|||||||||||

|

T-Mobile US, Inc. (a) |

2,000 |

256,700 |

|||||||||

|

2,662,396 |

|||||||||||

|

ENERGY - 10.5% |

|||||||||||

|

EOG Resources, Inc. (b) |

5,259 |

626,978 |

|||||||||

|

APA Corp. (b) |

12,824 |

530,008 |

|||||||||

|

ConocoPhillips (b) |

4,706 |

470,570 |

|||||||||

|

Diamondback Energy, Inc. (b) |

1,960 |

268,677 |

|||||||||

|

1,896,233 |

|||||||||||

|

Shares |

Value |

||||||||||

|

INFORMATION TECHNOLOGY - 10.4% |

|||||||||||

|

SOFTWARE & SERVICES - 9.6% |

|||||||||||

|

Fiserv, Inc. (a) |

3,800 |

$ |

385,320 |

||||||||

|

Gartner, Inc. (a) |

1,177 |

349,969 |

|||||||||

|

Workday, Inc., Class A (a) |

1,207 |

288,980 |

|||||||||

|

salesforce.com, Inc. (a) |

1,000 |

212,320 |

|||||||||

|

DXC Technology Co. (a) |

6,458 |

210,716 |

|||||||||

|

Global Payments, Inc. |

1,400 |

191,576 |

|||||||||

|

Visa, Inc., Class A |

435 |

96,403 |

|||||||||

|

1,735,284 |

|||||||||||

|

TECHNOLOGY HARDWARE & EQUIPMENT - 0.8% |

|||||||||||

|

TE Connectivity, Ltd. |

1,123 |

147,057 |

|||||||||

|

1,882,341 |

|||||||||||

|

CONSUMER DISCRETIONARY - 9.0% |

|||||||||||

|

CONSUMER SERVICES - 3.5% |

|||||||||||

|

Booking Holdings, Inc. (a) |

157 |

367,767 |

|||||||||

|

Hilton Worldwide Holdings, Inc. (a) |

1,722 |

261,312 |

|||||||||

|

629,079 |

|||||||||||

|

AUTOMOBILES & COMPONENTS - 3.0% |

|||||||||||

|

General Motors Co. (a) |

7,762 |

339,510 |

|||||||||

|

BorgWarner, Inc. |

5,000 |

194,500 |

|||||||||

|

534,010 |

|||||||||||

|

RETAILING - 1.5% |

|||||||||||

|

eBay, Inc. |

4,598 |

263,264 |

|||||||||

|

Qurate Retail, Inc., Class A |

3,792 |

18,050 |

|||||||||

|

281,314 |

|||||||||||

|

CONSUMER DURABLES & APPAREL - 1.0% |

|||||||||||

|

Pulte Homes, Inc. |

4,200 |

175,980 |

|||||||||

|

1,620,383 |

|||||||||||

|

HEALTH CARE - 7.1% |

|||||||||||

|

HEALTH CARE EQUIPMENT & SERVICES - 5.3% |

|||||||||||

|

HCA Healthcare, Inc. |

1,500 |

375,929 |

|||||||||

|

Humana, Inc. |

823 |

358,145 |

|||||||||

|

CVS Health Corp. |

2,103 |

212,862 |

|||||||||

|

946,936 |

|||||||||||

|

PHARMACEUTICALS, BIOTECHNOLOGY & LIFE SCIENCES - 1.8% |

|||||||||||

|

Regeneron Pharmaceuticals, Inc. (a) |

468 |

326,788 |

|||||||||

|

1,273,724 |

|||||||||||

|

CONSUMER STAPLES - 5.8% |

|||||||||||

|

FOOD, BEVERAGE & TOBACCO - 5.8% |

|||||||||||

|

Altria Group, Inc. |

7,000 |

365,750 |

|||||||||

|

Constellation Brands, Inc., Class A |

1,535 |

353,518 |

|||||||||

|

Keurig Dr Pepper, Inc. |

8,578 |

325,103 |

|||||||||

|

1,044,371 |

|||||||||||

See accompanying Notes to Financial Statements.

Oakmark.com 7

Oakmark Fund March 31, 2022 (Unaudited)

Schedule of Investments (in thousands) (continued)

|

Shares |

Value |

||||||||||

|

COMMON STOCKS - 93.4% (continued) |

|||||||||||

|

INDUSTRIALS - 4.9% |

|||||||||||

|

CAPITAL GOODS - 3.8% |

|||||||||||

|

General Electric Co. |

2,127 |

$ |

194,621 |

||||||||

|

PACCAR, Inc. |

2,000 |

176,140 |

|||||||||

|

General Dynamics Corp. |

650 |

156,767 |

|||||||||

|

Cummins, Inc. |

722 |

148,089 |

|||||||||

|

675,617 |

|||||||||||

|

COMMERCIAL & PROFESSIONAL SERVICES - 1.1% |

|||||||||||

|

Equifax, Inc. |

850 |

201,535 |

|||||||||

|

877,152 |

|||||||||||

|

REAL ESTATE - 1.2% |

|||||||||||

|

CBRE Group, Inc., Class A (a) |

2,368 |

216,719 |

|||||||||

|

TOTAL COMMON STOCKS - 93.4% (COST $10,255,082) |

16,818,658 |

||||||||||

|

Par Value |

Value |

||||||||||

|

SHORT-TERM INVESTMENT - 6.4% |

|||||||||||

|

REPURCHASE AGREEMENT - 6.4% |

|||||||||||

|

Fixed Income Clearing Corp. Repurchase Agreement, 0.28% dated 03/31/22 due 04/01/22, repurchase price $1,148,725, collateralized by United States Treasury Notes, 0.125% - 2.500% due 02/28/26 - 03/31/27, aggregate value plus accrued interest of $1,171,691 (Cost: $1,148,716) |

$ |

1,148,716 |

1,148,716 |

||||||||

|

TOTAL SHORT-TERM INVESTMENTS - 6.4% (COST $1,148,716) |

1,148,716 |

||||||||||

|

TOTAL INVESTMENTS - 99.8% (COST $11,403,798) |

17,967,374 |

||||||||||

|

Other Assets In Excess of Liabilities - 0.2% |

27,685 |

||||||||||

|

TOTAL NET ASSETS - 100.0% |

$ |

17,995,059 |

|||||||||

(a) Non-income producing security

(b) All or a portion of this investment is held in connection with one or more options within the Fund.

See accompanying Notes to Financial Statements.

8 OAKMARK FUNDS

Oakmark Fund March 31, 2022 (Unaudited)

Schedule of Investments (in thousands) (continued)

WRITTEN OPTIONS

|

Description |

Exercise Price |

Expiration Date |

Number of Contracts |

Notional Amount |

Market Value |

Premiums (Received) by Fund |

Unrealized Gain/(Loss) |

||||||||||||||||||||||||

|

CALLS |

|||||||||||||||||||||||||||||||

|

ConocoPhillips |

$ |

105.00 |

8/19/22 |

(5,000 |

) |

$ |

(50,000 |

) |

$ |

(3,175 |

) |

$ |

(5,154 |

) |

$ |

1,979 |

|||||||||||||||

|

APA Corp. |

$ |

40.00 |

7/15/22 |

(13,000 |

) |

$ |

(53,729 |

) |

$ |

(6,857 |

) |

$ |

(7,232 |

) |

$ |

375 |

|||||||||||||||

|

Diamondback Energy, Inc. |

$ |

140.00 |

6/17/22 |

(2,000 |

) |

$ |

(27,416 |

) |

$ |

(2,260 |

) |

$ |

(3,091 |

) |

$ |

831 |

|||||||||||||||

|

EOG Resources, Inc. |

$ |

124.00 |

7/15/22 |

(5,500 |

) |

$ |

(65,577 |

) |

$ |

(4,249 |

) |

$ |

(5,763 |

) |

$ |

1,514 |

|||||||||||||||

|

$ |

(196,722 |

) |

$ |

(16,541 |

) |

$ |

(21,240 |

) |

$ |

4,699 |

|||||||||||||||||||||

|

PUTS |

|||||||||||||||||||||||||||||||

|

Amazon.com, Inc. |

$ |

3,070.00 |

6/17/22 |

(680 |

) |

$ |

(221,677 |

) |

$ |

(7,834 |

) |

$ |

(13,705 |

) |

$ |

5,871 |

|||||||||||||||

|

Amazon.com, Inc. |

$ |

3,200.00 |

6/17/22 |

(680 |

) |

$ |

(221,677 |

) |

$ |

(11,109 |

) |

$ |

(10,810 |

) |

$ |

(299 |

) |

||||||||||||||

|

Meta Platforms, Inc. |

$ |

200.00 |

4/14/22 |

(8,000 |

) |

$ |

(177,888 |

) |

$ |

(604 |

) |

$ |

(8,628 |

) |

$ |

8,024 |

|||||||||||||||

|

$ |

(621,242 |

) |

$ |

(19,547 |

) |

$ |

(33,143 |

) |

$ |

13,596 |

|||||||||||||||||||||

See accompanying Notes to Financial Statements.

Oakmark.com 9

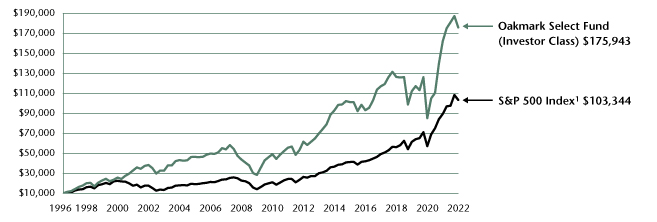

Oakmark Select Fund March 31, 2022

Summary Information

VALUE OF A $10,000 INVESTMENT

Since Inception - 11/01/96 (Unaudited)

PERFORMANCE

|

Average Annual Total Returns (as of 03/31/22) |

|||||||||||||||||||||||||||||||

| (Unaudited) |

Total Return Last 3 Months |

1-year |

3-year |

5-year |

10-year |

Since Inception |

Inception Date |

||||||||||||||||||||||||

|

Oakmark Select Fund (Investor Class) |

-6.07 |

% |

8.47 |

% |

16.21 |

% |

8.49 |

% |

11.06 |

% |

11.95 |

% |

11/01/96 |

||||||||||||||||||

|

S&P 500 Index |

-4.60 |

% |

15.65 |

% |

18.92 |

% |

15.99 |

% |

14.64 |

% |

9.63 |

% |

|||||||||||||||||||

|

Lipper Multi-Cap Value Fund Index6 |

-1.16 |

% |

11.06 |

% |

13.17 |

% |

9.41 |

% |

10.68 |

% |

8.01 |

% |

|||||||||||||||||||

|

Oakmark Select Fund (Advisor Class) |

-6.04 |

% |

8.62 |

% |

16.36 |

% |

8.63 |

% |

N/A |

9.23 |

% |

11/30/16 |

|||||||||||||||||||

|

Oakmark Select Fund (Institutional Class) |

-6.02 |

% |

8.71 |

% |

16.44 |

% |

8.70 |

% |

N/A |

9.28 |

% |

11/30/16 |

|||||||||||||||||||

|

Oakmark Select Fund (R6 Class) |

-6.02 |

% |

8.71 |

% |

N/A |

N/A |

N/A |

20.58 |

% |

12/15/20 |

|||||||||||||||||||||

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Past performance is no guarantee of future results. The performance data quoted represents past performance. Current performance may be lower or higher than the performance data quoted. Total return includes change in share prices and, in each case, includes reinvestment of dividends and capital gain distributions. The investment return and principal value vary so that an investor's shares, when redeemed, may be worth more or less than the original cost. To obtain the most recent month-end performance, please visit Oakmark.com.

|

TOP TEN EQUITY HOLDINGS4 |

% of Net Assets | ||||||

|

Alphabet, Inc., Class A |

9.0 |

||||||

|

CBRE Group, Inc., Class A |

6.9 |

||||||

|

Ally Financial, Inc. |

5.7 |

||||||

|

Netflix, Inc. |

4.5 |

||||||

|

Charter Communications, Inc., Class A |

4.4 |

||||||

|

Fiserv, Inc. |

4.4 |

||||||

|

APA Corp. |

4.3 |

||||||

|

American International Group, Inc. |

4.0 |

||||||

|

Citigroup, Inc. |

3.9 |

||||||

|

Lithia Motors, Inc. |

3.9 |

||||||

|

FUND STATISTICS |

|||||||

|

Ticker* |

OAKLX |

||||||

|

Number of Equity Holdings |

25 |

||||||

|

Net Assets |

$5.3 billion | ||||||

|

Weighted Average Market Cap |

$257 billion | ||||||

|

Median Market Cap |

$55.2 billion | ||||||

|

Gross Expense Ratio - Investor Class*^ |

1.00% | ||||||

|

Net Expense Ratio - Investor Class*†^ |

0.98% | ||||||

* This information is related to the Investor Class. Please visit Oakmark.com for information related to the Advisor, Institutional and R6 Classes.

† The net expense ratio reflects a contractual advisory fee waiver agreement through January 27, 2023.

^ The Gross Expense Ratio and Net Expense Ratio are from the Fund's Prospectus dated January 28, 2022.

|

SECTOR ALLOCATION |

% of Net Assets | ||||||

|

Financials |

23.7 |

||||||

|

Communication Services |

21.0 |

||||||

|

Consumer Discretionary |

11.2 |

||||||

|

Energy |

7.9 |

||||||

|

Health Care |

7.0 |

||||||

|

Real Estate |

6.9 |

||||||

|

Industrials |

6.3 |

||||||

|

Information Technology |

4.4 |

||||||

|

Consumer Staples |

3.9 |

||||||

|

Short-Term Investments and Other |

7.7 |

||||||

See accompanying Disclosures and Endnotes on page 100.

10 OAKMARK FUNDS

Oakmark Select Fund March 31, 2022

Portfolio Manager Commentary

William C. Nygren, CFA

Portfolio Manager

oaklx@oakmark.com

Anthony P. Coniaris, CFA

Portfolio Manager

oaklx@oakmark.com

The Oakmark Select Fund declined 6% in the first quarter of 2022 compared to a 5% decline in the S&P 500.1 While the portfolio is well positioned for rising interest rates and higher oil prices—both of which were front and center to start the year—two company-specific earnings reports put a damper on what otherwise would have been a solid relative performance quarter. Concentration is a double-edged sword, and we felt the negative side of the blade this quarter.

Netflix (–38%) and Meta Platforms (–34%) were the most significant detractors in the first quarter—detracting twice as much as the next closest stock. Netflix is experiencing what we would describe as a Covid-19-induced hangover. The pandemic pulled forward subscriber growth while content spend was limited due to health restrictions pushing out production timelines. This led to a perfect storm of accelerated revenue and margin growth, which the Fund benefited from in 2020 and into 2021 when Netflix was one of our top performers. Now the reverse is occurring. Looking at Netflix's business performance with a longer term lens, one hardly sees any disruption in the franchise. We used the price strength in 2021 to reduce our position and have used the current weakness to add to our exposure to Netflix. Meta reported a disappointing outlook for the first quarter of this year as well, but for different reasons. The company's targeted advertising business has been negatively impacted by Apple's new privacy policies, and the franchise also appears to be maturing somewhat. The stock was pummeled on news that the first quarter of 2022 could see revenue growth in the 5-10% plus range. While most companies would kill for an outlook like that, Meta shareholders were accustomed to more. Now shares are valued as if the company won't grow much at all going forward, which we believe is misguided. We sold put options to add to our economic exposure in Meta to take advantage of the price weakness. Please see the Oakmark Fund letter for a more thorough description of why we have elected to use options to increase our exposure to certain names in the Fund.

Our two oil holdings, APA Corporation (+54%) and EOG Resources (+36%), were our top contributors in the quarter as oil prices rallied due to tight supplies, which were then exacerbated by the Russian invasion of Ukraine. Although their share prices have increased considerably, both companies still look quite undervalued even using longer term oil prices in the $65-70 dollar range. Meanwhile, if times are good over the next couple of years, we expect these companies to return significant percentages of their market caps to shareholders.

As is typical during periods of significant volatility, we added a new name to the portfolio. Lithia Motors is the largest franchised auto dealer group in the United States. The company has a long history of creating shareholder value through best-in-class operations and consistent acquisitions of smaller dealers at

attractive returns. There is a long runway for management to continue creating value through such acquisitions. Management believes this will drive earnings per share to more than $50 by 2025, even as car prices return to pre-pandemic levels. Meanwhile, Lithia has a significant opportunity to further accelerate growth through Driveway, its online auto retailing platform. We believe Lithia's existing nationwide infrastructure provides Driveway with significant competitive advantages in e-commerce, which smaller dealers will struggle to replicate. Driveway is not generating any earnings today, but it could become a major contributor over the next five to seven years. With the stock priced at less than 7x management's 2025 EPS5 target and with substantial future growth potential from Driveway, we believe Lithia shares are a bargain today.

Humana and Hilton were reduced to minimal positions in the portfolio as the discount to value narrowed considerably during the quarter. Our CIT shares were converted to First Citizens Bancshares as the merger was completed.

Thank you, our fellow shareholders, for your continued investment in the Fund.

See accompanying Disclosures and Endnotes on page 100.

Oakmark.com 11

Oakmark Select Fund March 31, 2022 (Unaudited)

Schedule of Investments (in thousands)

|

Shares |

Value |

||||||||||

|

COMMON STOCKS - 92.3% |

|||||||||||

|

FINANCIALS - 23.7% |

|||||||||||

|

BANKS - 10.3% |

|||||||||||

|

Citigroup, Inc. |

3,942 |

$ |

210,503 |

||||||||

|

First Citizens BancShares, Inc., Class A |

290 |

193,046 |

|||||||||

|

Bank of America Corp. |

3,362 |

138,578 |

|||||||||

|

First Citizens BancShares, Inc., Class B |

14 |

8,795 |

|||||||||

|

550,922 |

|||||||||||

|

DIVERSIFIED FINANCIALS - 9.4% |

|||||||||||

|

Ally Financial, Inc. |

7,000 |

304,364 |

|||||||||

|

Capital One Financial Corp. |

1,479 |

194,191 |

|||||||||

|

498,555 |

|||||||||||

|

INSURANCE - 4.0% |

|||||||||||

|

American International Group, Inc. |

3,410 |

214,033 |

|||||||||

|

1,263,510 |

|||||||||||

|

COMMUNICATION SERVICES - 21.0% |

|||||||||||

|

MEDIA & ENTERTAINMENT - 21.0% |

|||||||||||

|

Alphabet, Inc., Class A (a) |

172 |

477,866 |

|||||||||

|

Netflix, Inc. (a) |

641 |

240,150 |

|||||||||

|

Charter Communications, Inc., Class A (a) |

429 |

233,973 |

|||||||||

|

Meta Platforms, Inc., Class A (a) (b) |

760 |

168,994 |

|||||||||

|

1,120,983 |

|||||||||||

|

CONSUMER DISCRETIONARY - 11.2% |

|||||||||||

|

CONSUMER SERVICES - 4.2% |

|||||||||||

|

Booking Holdings, Inc. (a) |

82 |

192,573 |

|||||||||

|

Hilton Worldwide Holdings, Inc. (a) |

196 |

29,813 |

|||||||||

|

222,386 |

|||||||||||

|

RETAILING - 3.9% |

|||||||||||

|

Lithia Motors, Inc. |

700 |

210,084 |

|||||||||

|

AUTOMOBILES & COMPONENTS - 3.1% |

|||||||||||

|

Lear Corp. |

1,150 |

163,979 |

|||||||||

|

596,449 |

|||||||||||

|

ENERGY - 7.9% |

|||||||||||

|

APA Corp. (b) |

5,550 |

229,381 |

|||||||||

|

EOG Resources, Inc. (b) |

1,640 |

195,494 |

|||||||||

|

424,875 |

|||||||||||

|

HEALTH CARE - 7.0% |

|||||||||||

|

HEALTH CARE EQUIPMENT & SERVICES - 4.1% |

|||||||||||

|

HCA Healthcare, Inc. |

703 |

176,122 |

|||||||||

|

Humana, Inc. |

97 |

42,212 |

|||||||||

|

218,334 |

|||||||||||

|

PHARMACEUTICALS, BIOTECHNOLOGY & LIFE SCIENCES - 2.9% |

|||||||||||

|

Regeneron Pharmaceuticals, Inc. (a) |

224 |

156,446 |

|||||||||

|

374,780 |

|||||||||||

|

REAL ESTATE - 6.9% |

|||||||||||

|

CBRE Group, Inc., Class A (a) (b) |

4,017 |

367,605 |

|||||||||

|

Shares |

Value |

||||||||||

|

INDUSTRIALS - 6.3% |

|||||||||||

|

CAPITAL GOODS - 6.3% |

|||||||||||

|

Allison Transmission Holdings, Inc. |

4,490 |

$ |

176,278 |

||||||||

|

General Electric Co. |

1,753 |

160,372 |

|||||||||

|

336,650 |

|||||||||||

|

INFORMATION TECHNOLOGY - 4.4% |

|||||||||||

|

SOFTWARE & SERVICES - 4.4% |

|||||||||||

|

Fiserv, Inc. (a) |

2,300 |

233,220 |

|||||||||

|

CONSUMER STAPLES - 3.9% |

|||||||||||

|

FOOD, BEVERAGE & TOBACCO - 3.9% |

|||||||||||

|

Constellation Brands, Inc., Class A |

910 |

209,499 |

|||||||||

|

TOTAL COMMON STOCKS - 92.3% (COST $2,960,329) |

4,927,571 |

||||||||||

|

Par Value |

Value |

||||||||||

|

SHORT-TERM INVESTMENTS - 8.2% |

|||||||||||

|

REPURCHASE AGREEMENT - 8.2% |

|||||||||||

|

Fixed Income Clearing Corp. Repurchase Agreement, 0.28% dated 03/31/22 due 04/01/22, repurchase price $437,124, collateralized by United States Treasury Notes, 0.125% - 0.625% due 10/15/25 - 01/31/26, aggregate value plus accrued interest of $445,863 (Cost: $437,120) |

$ |

437,120 |

437,120 |

||||||||

|

TOTAL SHORT-TERM INVESTMENTS - 8.2% (COST $437,120) |

437,120 |

||||||||||

|

TOTAL INVESTMENTS - 100.5% (COST $3,397,449) |

5,364,691 |

||||||||||

|

Liabilities In Excess of Other Assets - (0.5)% |

(26,113 |

) |

|||||||||

|

TOTAL NET ASSETS - 100.0% |

$ |

5,338,578 |

|||||||||

(a) Non-income producing security

(b) All or a portion of this investment is held in connection with one or more options within the Fund.

See accompanying Notes to Financial Statements.

12 OAKMARK FUNDS

Oakmark Select Fund March 31, 2022 (Unaudited)

Schedule of Investments (in thousands) (continued)

WRITTEN OPTIONS

|

Description |

Exercise Price |

Expiration Date |

Number of Contracts |

Notional Amount |

Market Value |

Premiums (Received) by Fund |

Unrealized Gain/(Loss) |

||||||||||||||||||||||||

|

CALLS |

|||||||||||||||||||||||||||||||

|

APA Corp. |

$ |

40.00 |

7/15/22 |

(6,000 |

) |

$ |

(24,798 |

) |

$ |

(3,165 |

) |

$ |

(3,337 |

) |

$ |

172 |

|||||||||||||||

|

EOG Resources, Inc. |

$ |

124.00 |

7/15/22 |

(2,000 |

) |

$ |

(23,846 |

) |

$ |

(1,545 |

) |

$ |

(2,096 |

) |

$ |

551 |

|||||||||||||||

|

CBRE Group, Inc. |

$ |

95.00 |

6/17/22 |

(18,000 |

) |

$ |

(164,736 |

) |

$ |

(6,750 |

) |

$ |

(17,441 |

) |

$ |

10,691 |

|||||||||||||||

|

$ |

(213,380 |

) |

$ |

(11,460 |

) |

$ |

(22,874 |

) |

$ |

11,414 |

|||||||||||||||||||||

|

PUTS |

|||||||||||||||||||||||||||||||

|

Meta Platforms, Inc. |

$ |

215.00 |

6/17/22 |

(4,000 |

) |

$ |

(88,944 |

) |

$ |

(5,240 |

) |

$ |

(6,386 |

) |

$ |

1,146 |

|||||||||||||||

|

$ |

(88,944 |

) |

$ |

(5,240 |

) |

$ |

(6,386 |

) |

$ |

1,146 |

|||||||||||||||||||||

See accompanying Notes to Financial Statements.

Oakmark.com 13

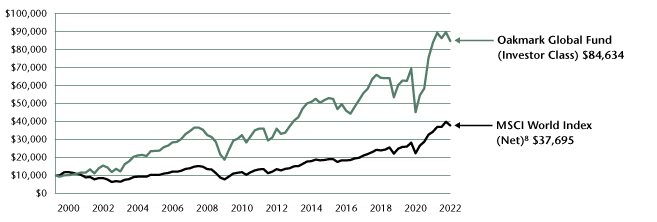

Oakmark Global Fund March 31, 2022

Summary Information

VALUE OF A $10,000 INVESTMENT

Since Inception - 08/04/99 (Unaudited)

PERFORMANCE

|

Average Annual Total Returns (as of 03/31/22) |

|||||||||||||||||||||||||||||||

| (Unaudited) |

Total Return Last 3 Months |

1-year |

3-year |

5-year |

10-year |

Since Inception |

Inception Date |

||||||||||||||||||||||||

|

Oakmark Global Fund (Investor Class) |

-5.53 |

% |

1.07 |

% |

12.09 |

% |

8.70 |

% |

8.96 |

% |

9.89 |

% |

08/04/99 |

||||||||||||||||||

|

MSCI World Index (Net) |

-5.15 |

% |

10.12 |

% |

14.98 |

% |

12.42 |

% |

10.88 |

% |

6.03 |

% |

|||||||||||||||||||

|

Lipper Global Fund Index9 |

-8.23 |

% |

2.23 |

% |

12.03 |

% |

9.93 |

% |

9.42 |

% |

6.13 |

% |

|||||||||||||||||||

|

Oakmark Global Fund (Advisor Class) |

-5.48 |

% |

1.26 |

% |

12.26 |

% |

8.85 |

% |

N/A |

10.41 |

% |

11/30/16 |

|||||||||||||||||||

|

Oakmark Global Fund (Institutional Class) |

-5.48 |

% |

1.28 |

% |

12.31 |

% |

8.91 |

% |

N/A |

10.47 |

% |

11/30/16 |

|||||||||||||||||||

|

Oakmark Global Fund (R6 Class) |

-5.48 |

% |

1.30 |

% |

N/A |

N/A |

N/A |

11.12 |

% |

12/15/20 |

|||||||||||||||||||||

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Past performance is no guarantee of future results. The performance data quoted represents past performance. Current performance may be lower or higher than the performance data quoted. Total return includes change in share prices and, in each case, includes reinvestment of dividends and capital gain distributions. The investment return and principal value vary so that an investor's shares, when redeemed, may be worth more or less than the original cost. To obtain the most recent month-end performance, please visit Oakmark.com.

|

TOP TEN EQUITY HOLDINGS4 |

% of Net Assets | ||||||

|

Alphabet, Inc., Class A |

6.7 |

||||||

|

Bayer AG |

4.8 |

||||||

|

TE Connectivity, Ltd. |

4.4 |

||||||

|

Lloyds Banking Group PLC |

4.0 |

||||||

|

General Motors Co |

3.9 |

||||||

|

Allianz SE |

3.6 |

||||||

|

Tenet Healthcare Corp. |

3.6 |

||||||

|

Credit Suisse Group AG |

3.5 |

||||||

|

Alibaba Group Holding, Ltd. |

3.3 |

||||||

|

Bank of America Corp. |

3.3 |

||||||

|

FUND STATISTICS |

|||||||

|

Ticker* |

OAKGX |

||||||

|

Number of Equity Holdings |

47 |

||||||

|

Net Assets |

$1.4 billion | ||||||

|

Weighted Average Market Cap |

$221.5 billion | ||||||

|

Median Market Cap |

$42.6 billion | ||||||

|

Gross Expense Ratio - Investor Class*^ |

1.15% | ||||||

|

Net Expense Ratio - Investor Class*†^ |

1.13% | ||||||

* This information is related to the Investor Class. Please visit Oakmark.com for information related to the Advisor, Institutional and R6 Classes.

† The net expense ratio reflects a contractual advisory fee waiver agreement through January 27, 2023.

^ The Gross Expense Ratio and Net Expense Ratio are from the Fund's Prospectus dated January 28, 2022.

|

SECTOR ALLOCATION |

% of Net Assets | ||||||

|

Equity Investments |

|||||||

|

Financials |

20.5 |

||||||

|

Consumer Discretionary |

17.3 |

||||||

|

Communication Services |

15.1 |

||||||

|

Information Technology |

12.6 |

||||||

|

Health Care |

12.5 |

||||||

|

Industrials |

10.5 |

||||||

|

Consumer Staples |

3.3 |

||||||

|

Materials |

3.2 |

||||||

|

Energy |

2.0 |

||||||

|

Total Equity Investments |

97.0 |

||||||

|

Preferred Stocks |

0.7 |

||||||

|

Short-Term Investments and Other |

2.3 |

||||||

|

GEOGRAPHIC ALLOCATION |

|||||||

|

% of Equity |

|||||||

|

North America |

50.1 |

||||||

|

United States |

50.1 |

||||||

|

Europe |

43.9 |

||||||

|

Germany* |

16.8 |

||||||

|

Switzerland |

10.6 |

||||||

|

United Kingdom |

10.1 |

||||||

|

Netherlands* |

3.1 |

||||||

|

Belgium* |

2.1 |

||||||

|

Ireland* |

1.2 |

||||||

|

% of Equity |

|||||||

|

Asia |

4.8 |

||||||

|

China |

3.4 |

||||||

|

India |

0.7 |

||||||

|

South Korea |

0.7 |

||||||

|

Latin America |

1.2 |

||||||

|

Mexico |

1.2 |

||||||

* Euro currency countries comprise 23.2% of equity investments.

See accompanying Disclosures and Endnotes on page 100.

14 OAKMARK FUNDS

Oakmark Global Fund March 31, 2022

Portfolio Manager Commentary

David G. Herro, CFA

Portfolio Manager

oakgx@oakmark.com

Clyde S. McGregor, CFA

Portfolio Manager

oakgx@oakmark.com

Anthony P. Coniaris, CFA

Portfolio Manager

oakgx@oakmark.com

Jason E. Long, CFA

Portfolio Manager

oakgx@oakmark.com

The Oakmark Global Fund declined by 5.53% for the quarter ended March 31, 2022, compared to a decline of 5.15% for the MSCI World Index (Net)8 and a decline of 8.23% for the Lipper Global Fund Index.9 Since its inception in 1999, the Fund has achieved a compound annual rate of return18 of 9.89%, which compares to 6.03% for the MSCI World Index (Net) and 6.13% for the Lipper Global Fund Index.

For the quarter, the countries that contributed the most to the Fund's return were Mexico, India, Australia and Japan, while the U.S., Netherlands, U.K., Germany and Switzerland were the most significant detractors. From an individual security perspective, Bayer (Germany), Glencore (Switzerland), NOV (U.S.), Flowserve (U.S.) and Grupo Televisa (Mexico) were the strongest contributors. The Fund holdings that detracted most were Prosus (Netherlands), General Motors (U.S.), Continental (Germany), TE Connectivity (U.S.) and Credit Suisse (Switzerland). We discuss a few of the key contributors and detractors in further detail below.

Bayer (Germany), a life science company with pharmaceuticals, consumer health and crop science divisions, was a top contributor to the Fund's performance for the quarter. The company reported strong earnings results for 2021, in our view, with growth exceeding expectations across divisions. Notably, the crop science division delivered 11% growth, staging a robust recovery following two years of an agriculture downcycle and competitive challenges. Management's increased guidance for crop science in 2022 calls for 7% organic growth and a 25-26% margin, which we believe is a key positive for the segment as it signals a long-awaited favorable transition toward profitable growth. In the pharmaceuticals division, revenue growth of more than 7% also bested expectations, supported by a strong recovery of Eylea, the continued growth of Xarelto and the slate of new products. Moreover, Bayer's pipeline enjoyed notable successes in the period, including a favorable read-out for the cancer drug Nubeqa. We spoke with Bayer CFO Wolfgang Nickl during the quarter, who noted that tailwinds are robust in the business today. Notably, he expressed confidence in both the pricing and competitive backdrop in the crop science business as rate increases are layering into sales growth and cost cuts begin to come through. Nickl also reiterated Bayer's expectations for continued growth in pharmaceuticals, driven largely by new launches and technologies.

In our view, Glencore (Switzerland) delivered a solid fiscal-year 2021 earnings report due to significantly improved year-over-year financial metrics, driven by both the mining business, where higher prices supported strong profitability, and the marketing business, which benefited from rising prices, supply constraints

and inventory drawdowns. Glencore's free-cash-flow generation was quite robust and resulted in net debt of just $6 billion, which is a record low 0.3x EBITDA10 and well below the $10-$16 billion range targeted by the company. Back in mid-February, guidance already suggested significantly higher earnings and cash flow, compared to 2022, due to significantly higher commodity prices across the board. This has been further amplified by additional price surges for most of the commodities that Glencore mines, including copper, cobalt, zinc, nickel and thermal coal. As a result, Glencore should report a substantial amount of free cash flow and incremental shareholder returns for the year. We recently met with CEO Gary Nagle and CFO Steve Kalmin and discussed the massive impact the crisis in Ukraine is having on Glencore's markets. In many cases, realized prices significantly exceed index prices due to very tight physical markets. Management reiterated its commitment to pay out all excess cash below $10 billion of net debt to shareholders and noted that the company now has 27 assets that are either in the process of being sold or are under consideration for sale. This is in addition to the nine assets already sold under the portfolio simplification. We appreciate Nagle's focus on efficiency and returns, and we believe the company continues to trade at a large discount to our perception of its intrinsic value.

Prosus (Netherlands), owing to its 29% stake in Tencent and the impact of the Russian invasion of Ukraine, was a notable detractor for the first quarter. Tencent was negatively impacted by fears for increased regulation and a poor macro backdrop that have negatively impacted fundamentals. We have spoken with numerous contacts on the changing regulatory landscape in China. Although we believe structural growth at Tencent will be lower in the future due to the new regulatory environment, it remains an excellent business with a high degree of innovation. Later during the quarter, Russia's invasion of Ukraine weighed on companies with exposure to Russia. In Prosus' case, its two Russian assets, Avito (the largest online classifieds company in Russia) and Mail.ru (the largest social media company in Russia), are now valueless in our estimation and resulted in a small reduction of our estimate of Prosus' intrinsic value. While we monitor any new developments closely, we continue to believe Prosus remains extremely undervalued relative to its sum of the parts.