OAKMARK FUNDS

FIRST QUARTER REPORT | DECEMBER 31, 2019

OAKMARK FUND

OAKMARK SELECT FUND

OAKMARK EQUITY AND INCOME FUND

OAKMARK GLOBAL FUND

OAKMARK GLOBAL SELECT FUND

OAKMARK INTERNATIONAL FUND

OAKMARK INTERNATIONAL SMALL CAP FUND

Oakmark Funds

2020 First Quarter Report

TABLE OF CONTENTS

|

Commentary on Oakmark and Oakmark Select Funds |

1 |

||||||

|

Oakmark Fund |

|||||||

|

Summary Information |

4 |

||||||

|

Portfolio Manager Commentary |

5 |

||||||

|

Schedule of Investments |

6 |

||||||

|

Oakmark Select Fund |

|||||||

|

Summary Information |

8 |

||||||

|

Portfolio Manager Commentary |

9 |

||||||

|

Schedule of Investments |

10 |

||||||

|

Oakmark Equity and Income Fund |

|||||||

|

Summary Information |

12 |

||||||

|

Portfolio Manager Commentary |

13 |

||||||

|

Schedule of Investments |

15 |

||||||

|

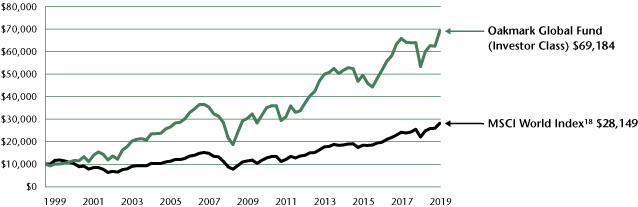

Oakmark Global Fund |

|||||||

|

Summary Information |

20 |

||||||

|

Portfolio Manager Commentary |

21 |

||||||

|

Schedule of Investments |

23 |

||||||

|

Oakmark Global Select Fund |

|||||||

|

Summary Information |

26 |

||||||

|

Portfolio Manager Commentary |

27 |

||||||

|

Schedule of Investments |

28 |

||||||

|

Commentary on Oakmark International and Oakmark International Small Cap Funds |

30 |

||||||

|

Oakmark International Fund |

|||||||

|

Summary Information |

32 |

||||||

|

Portfolio Manager Commentary |

33 |

||||||

|

Schedule of Investments |

34 |

||||||

|

Oakmark International Small Cap Fund |

|||||||

|

Summary Information |

38 |

||||||

|

Portfolio Manager Commentary |

39 |

||||||

|

Schedule of Investments |

40 |

||||||

|

Disclosures and Endnotes |

43 |

||||||

|

Trustees and Officers |

45 |

||||||

|

Beginning on January 1, 2021, as permitted by regulations adopted by the U.S. Securities and Exchange Commission, paper copies of the Oakmark Funds' annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on Oakmark.com, and you will be notified by mail each time a report is posted and provided with a website link to access the report. If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Funds electronically anytime by contacting your financial intermediary (such as a broker-dealer or bank) or, if you hold your shares directly with the Funds, by calling 1-800-OAKMARK (625-6275) or visiting Oakmark.com. |

|||

You may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you hold your shares directly with the Funds, you can call 1-800-OAKMARK (625-6275) to let the Funds know you wish to continue receiving paper copies of your shareholder reports. Your election to receive reports in paper will apply to all Funds you hold directly or all Funds you hold through your financial intermediary, as applicable.

FORWARD-LOOKING STATEMENT DISCLOSURE

One of our most important responsibilities as mutual fund managers is to communicate with shareholders in an open and direct manner. Some of our comments in our letters to shareholders are based on current management expectations and are considered "forward-looking statements." Actual future results, however, may prove to be different from our expectations. You can identify forward-looking statements by words such as "estimate", "may", "will", "expect", "believe",

"plan" and other similar terms. We cannot promise future returns. Our opinions are a reflection of our best judgment at the time this report is compiled, and we disclaim any obligation to update or alter forward-looking statements as a result of new information, future events, or otherwise.

Oakmark.com

Oakmark and Oakmark Select Funds December 31, 2019

Portfolio Manager Commentary

William C. Nygren, CFA

Portfolio Manager

oakmx@oakmark.com

oaklx@oakmark.com

oakwx@oakmark.com

At Oakmark, we are long-term investors. We attempt to identify growing businesses that are managed to benefit their shareholders. We will purchase stock in those businesses only when priced substantially below our estimate of intrinsic value. After purchase, we patiently wait for the gap between stock price and intrinsic value to close.

"What is smart at one price is stupid at another."

-Warren Buffett

The S&P 5001 returned 31% in 2019. With the exception of its 32% return in 2013, this was the S&P 500's largest annual gain in the past 20 years. The Oakmark Fund produced a return of 27% for the year and Oakmark Select returned 28%. Compared to almost anything other than the S&P 500, those are very good numbers and exceeded almost all beginning-of-the-year predictions for what a mutual fund would return in 2019. Still, for the third straight year, both Oakmark and Oakmark Select returned less than the S&P 500. We are encouraged that the past quarter showed signs of a turn—both funds outperformed a strong market. But given that we and our shareholders expect our Funds to outperform the S&P 500 over the long term, we wanted to focus this report on our relative performance as opposed to our strong absolute performance. We hope this will help our shareholders answer this important question: "Did Oakmark trail because value investing is, as a strategy, underperforming? Or is Oakmark doing a poor job of implementing its strategy?"

To answer these questions, let's first look at how value performed in 2019. You've probably heard of the "Dogs of the Dow" theory, which states that the 10 cheapest stocks in the Dow Jones Industrial Average2 (based on dividend yield) tend to outperform that index over the following year. And from 2000 through 2018, this held true: the "Dogs" outperformed the Dow by an average of 150 basis points per year. But in 2019, the 10 "Dogs" underperformed the other 20 stocks in the Dow by a whopping 1770 basis points, returning 13% versus 30%.

Using another value measure, if, at the beginning of 2019, you had bought the 50 cheapest S&P 500 stocks based on price-to-book3 value, you would have underperformed the rest of the S&P 500 by over 500 basis points for the year. Similarly, if you bought the 50 stocks with the lowest expected 2019 EPS4 growth, your portfolio would have underperformed the 50 highest expected growth stocks by 830 basis points over the year. Consistent with that, the Russell 1000 Value Index5, an index composed of lower priced stocks relative to earnings and book value, underperformed the Russell 1000 Growth Index6 by 990 basis points in 2019. Given these results, it's no surprise that Morningstar reports7 that large-cap value funds as an aggregate underperformed large-cap growth funds by 690 basis points in 2019.

Undoubtedly, we made our share of mistakes at Oakmark in 2019. But the data suggest that our much bigger problem was that investors were not very concerned about valuation levels. Though this can be frustrating, it also gives us the opportunity to start the year with a portfolio of stocks that our research suggests is at a larger discount to the market than is typical.

To examine these opportunities, let's take a step back and compare U.S. equities with the bond market. Many investors think a 10-year U.S. Treasury bond is a riskless investment because the U.S. Treasury not paying its debts is unthinkable. And if you rule out default, except for inflation risk, it would be risk-free—but only if it is held to maturity. However, if you hold that bond for a shorter period, its total return will be a combination of its coupon yield plus the change in value caused by interest rate changes. For example, if interest rates rise to just 2.1%, a 10-year Treasury bond that currently yields 1.9% will generate a negative one-year return. And good luck to those pension funds relying on 30-year Treasuries repeating their 7% annualized return from the past decade. That will only happen if their yield, starting at 2.3% today, goes to negative 1.2% a decade from now. I guess nothing is impossible, but this outcome seems highly unlikely. Fixed income investors who ignore the impact of interest rate changes have a lot in common with equity investors who ignore the impact that movement in P/E8 multiples have on stock prices.

I sometimes get frustrated with legal edits that don't allow me to say things like, "Alphabet is a great business." Despite the company's demonstrably superior financial metrics, that statement is an opinion, not a fact. So, when my writing comes back from editing, it is often filled with new insertions like, "we believe," "in our opinion," "it could be the case" and so on. At times, it feels as if I have to write, "Two plus two, in our opinion, equals four." (To be clear, our lawyers aren't to blame. Rather, it's our industry's history of bad actors who stretched the truth that have led to increased regulation.) Because of this, I'm excited that I can write something definitive about stock prices: a stock's price always equals its price-to-earnings ratio times its earnings-per-share, or P= P/E x EPS.

As value investors, we pay close attention to P/E and base most of our investments on the premise that a stock's current P/E ratio is too low. If a stock moves to what we believe is a fair multiple, the result is a higher price. Occasionally, we have a strong non-consensus view on earnings potential, such as when we believed that Baxter's new management team had an opportunity to nearly double margins. Likewise, as the 2008 recession came to a close, we believed that earnings would get back to "normal" over our seven-year time horizon—a decidedly more positive outlook than most investors had at the time.

Usually, however, we don't quarrel much with consensus earnings forecasts. Instead, we believe that our stocks will benefit from higher P/E multiples. That was our view in 2000 when we avoided technology stocks that were selling above the S&P 500's 30 times multiple and instead owned single-digit P/E stocks, such as consumer packaged goods, industrials and financials. Today, you can see this same logic at work in our bank and cyclical holdings, with many selling at single-digit P/Es, and our

See accompanying Disclosures and Endnotes on page 43.

Oakmark.com 1

Oakmark and Oakmark Select Funds December 31, 2019

Portfolio Manager Commentary (continued)

avoidance of utilities, consumer packaged goods and REITs9 that trade at P/Es in the 20s.

Although the formula P=P/E x EPS highlights that estimating future P/E is just as important as forecasting EPS, investors typically alternate being obsessed with one factor and then the other. The collapse of the tech bubble in 2000 was a time when investors stopped paying higher and higher prices for the fastest growers and quickly pivoted to low P/E stocks. And today, just like during the height of the tech bubble, analysts are focusing much more on a company's earnings than on the company's appropriate P/E multiple. It's not the analysts' fault. After all, their job is to earn commissions from their clients, and today, most of their clients are paying them to focus on earnings predictions.

But this focus on earnings instead of valuation has led to some very—shall we say—interesting analyst reports, including the following "takes" we've seen on our own holdings:

• One analyst wrote that he believed, as we do, that DXC's new CEO will restructure the company and largely eliminate the quality gap between DXC and its public peers over the next three years. Yet, in the same report, the analyst set the company's target P/E at a 30% discount to its peers—unchanged from its historical average, despite its improved competitive stance.

• An in-depth report on Lear highlighted the company's many advantages compared to other auto parts businesses that sell for between 5 and 11 times EBITDA10. But then the analyst computed Lear's new target price using a multiple of 4.8 times EBITDA. Why? That was left to the reader's imagination.

• A report on CBRE Group touted the company's improved business mix. Over the past few years, CBRE's maintenance outsourcing segment has grown rapidly compared to its more cyclical brokerage segment—historically the larger part of the business. Importantly, the market tends to value recurring income, like that from service businesses, at a much higher P/E than businesses based on one-time transactions. Nevertheless, this still concluded that CBRE is fairly priced because its current P/E is approximately at its 15-year average.

• A report on Constellation Brands kept the company's target P/E the same—at 17 times—despite the company's recent purchase of a large interest in Canopy Growth Corporation. Canopy's losses reduce Constellation's reported EPS by about $0.85 so the analyst is inadvertently valuing Constellation's Canopy investment at negative $14 per Constellation share, despite its market value being positive $14.

• Another report noted that big banks are safer and more competitively advantaged today than at any time in recent history. Yet it concluded that these banks are fully valued at their current price of 10 times earnings—which is a P/E roughly the same as their 30-year average. The report never explained why the improved business fundamentals shouldn't be rewarded with a higher P/E multiple.

The largest industry weighting in our portfolios, financials, demonstrates why we believe our Funds will benefit when

valuations become a bigger determinant of prices. In the Oakmark Fund, for example, we own 10 stocks in the financials sector, comprising about 30% of the portfolio. Their median P/E on expected 2021 earnings is 9 times, compared to the S&P 500 at 16 times. Median price-to-book is 1.2 times and dividend yield is 2.3%, compared to the S&P 500 at 3.6 times book and a 1.9% yield. So, on earnings, assets and yield, the banks appear much cheaper than the S&P 500. Normally, stocks that look that cheap are expected to grow much slower than the market or even experience declining earnings. In this case, however, we expect our median financial stock to have annual EPS growth of 8%, which exceeds the consensus expectation for the S&P 500. To us, faster growth, higher yield and cheaper price translate to win, win and win. We believe that the market will eventually reflect our view by narrowing the gap between the S&P 500's and the financials sector's P/E ratios.

Our portfolio is filled with stocks whose stories sound similar and our research leads us to believe are selling at bargain prices—relative to both other stocks and to the absolute returns we expect in assets other than equities.

One year ago in this commentary, after the market fell 14% in the fourth quarter, I wrote:

"The stock market looks more attractive to us than it usually does, and the divergence among individual stocks allowed us to structure a portfolio that we believe is more undervalued relative to the market than it usually is. Though the decline has made watching the market painful, we are all gritting our teeth and adding to our personal holdings."

With hindsight, we were right about the market being unusually attractive, but we have yet to prove that our portfolio was more attractive than the market.

It is frustrating when market performance doesn't reflect our estimates of business value, but that's what creates opportunity. Since our longest tenured mutual fund, the Oakmark Fund, started in 1991, its annualized return has been 12.5% versus 10.0% for the S&P 500. Yet during those 28 years, our trailing three-year return has lagged behind the market 49% of the time. That number falls to 35% for 5-year and just 22% for 10-year time periods.

We understand that patience is in short supply when a fund underperforms. In addition to our strong long-term record, consider a few other issues when evaluating our recent returns. First, most value funds have underperformed over the past three years at least in part because investors have shown little concern for valuation as some high growth stocks have surged. Second, the relative values that are available today in sectors like financials (our largest exposure) seem historically unusual. And, finally, our investment philosophy and team have been remarkably consistent throughout our history. In our view, this consistency is a major factor behind our long-term outperformance. We believe our long-term returns have been higher because we have applied our value approach consistently as opposed to following current market trends. Based on what we've seen in the past, we believe today's market offers the opportunity to profit from a potential narrowing of the gap between business value and stock price. That's exactly what we've been exploiting for the past 28 years.

See accompanying Disclosures and Endnotes on page 43.

2 OAKMARK FUNDS

This page intentionally left blank.

Oakmark.com 3

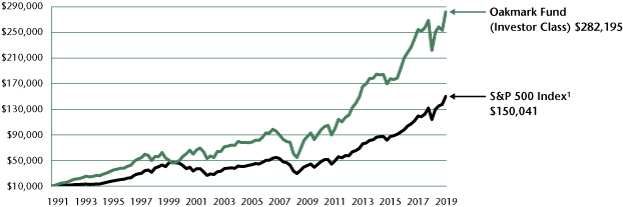

Oakmark Fund December 31, 2019

Summary Information

VALUE OF A $10,000 INVESTMENT

Since Inception - 08/05/91 (Unaudited)

PERFORMANCE

|

Average Annual Total Returns (as of 12/31/19) |

|||||||||||||||||||||||||||||||

| (Unaudited) |

Total Return Last 3 Months |

1-year |

3-year |

5-year |

10-year |

Since Inception |

Inception Date |

||||||||||||||||||||||||

|

Oakmark Fund (Investor Class) |

11.33 |

% |

26.98 |

% |

10.32 |

% |

8.82 |

% |

12.43 |

% |

12.48 |

% |

08/05/91 |

||||||||||||||||||

|

S&P 500 Index |

9.07 |

% |

31.49 |

% |

15.27 |

% |

11.70 |

% |

13.56 |

% |

10.00 |

% |

|||||||||||||||||||

|

Dow Jones Industrial Average2 |

6.67 |

% |

25.34 |

% |

15.73 |

% |

12.59 |

% |

13.40 |

% |

10.87 |

% |

|||||||||||||||||||

|

Lipper Large Cap Value Fund Index11 |

7.92 |

% |

26.19 |

% |

10.62 |

% |

8.70 |

% |

11.14 |

% |

8.99 |

% |

|||||||||||||||||||

|

Oakmark Fund (Advisor Class) |

11.38 |

% |

27.09 |

% |

10.44 |

% |

N/A |

N/A |

10.72 |

% |

11/30/16 |

||||||||||||||||||||

|

Oakmark Fund (Institutional Class) |

11.38 |

% |

27.19 |

% |

10.50 |

% |

N/A |

N/A |

10.76 |

% |

11/30/16 |

||||||||||||||||||||

|

Oakmark Fund (Service Class) |

11.27 |

% |

26.65 |

% |

10.02 |

% |

8.50 |

% |

12.09 |

% |

8.28 |

% |

04/05/01 |

||||||||||||||||||

The graph and table above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Past performance is no guarantee of future results. The performance data quoted represents past performance. Current performance may be lower or higher than the performance data quoted. Total return includes change in share prices and, in each case, includes reinvestment of dividends and capital gain distributions. The investment return and principal value vary so that an investor's shares, when redeemed, may be worth more or less than the original cost. To obtain the most recent month-end performance, please visit Oakmark.com.

|

TOP TEN EQUITY HOLDINGS12 |

% of Net Assets | ||||||

|

Citigroup, Inc. |

3.6 |

||||||

|

Bank of America Corp. |

3.6 |

||||||

|

Capital One Financial Corp. |

3.1 |

||||||

|

Netflix, Inc. |

3.1 |

||||||

|

Regeneron Pharmaceuticals, Inc. |

2.9 |

||||||

|

Ally Financial, Inc. |

2.9 |

||||||

|

State Street Corp. |

2.8 |

||||||

|

Charter Communications, Inc., Class A |

2.7 |

||||||

|

Alphabet, Inc., Class A |

2.6 |

||||||

|

The Charles Schwab Corp. |

2.6 |

||||||

|

FUND STATISTICS |

|||||||

|

Ticker* |

OAKMX |

||||||

|

Number of Equity Holdings |

51 |

||||||

|

Net Assets |

$16.8 billion | ||||||

|

Weighted Average Market Cap |

$152.6 billion | ||||||

|

Median Market Cap |

$48.5 billion | ||||||

|

Gross Expense Ratio - Investor Class (as of 09/30/19)* |

0.92% | ||||||

|

Net Expense Ratio - Investor Class (as of 09/30/19)*† |

0.88% | ||||||

* This information is related to the Investor Class. Please visit Oakmark.com for information related to the Advisor, Institutional and Service Classes.

† The net expense ratio reflects a contractual advisory fee waiver agreement through January 27, 2021.

|

SECTOR ALLOCATION |

% of Net Assets | ||||||

|

Financials |

29.7 |

||||||

|

Communication Services |

14.4 |

||||||

|

Consumer Discretionary |

13.6 |

||||||

|

Information Technology |

13.3 |

||||||

|

Industrials |

10.2 |

||||||

|

Health Care |

7.6 |

||||||

|

Energy |

5.5 |

||||||

|

Consumer Staples |

1.8 |

||||||

|

Short-Term Investments and Other |

3.9 |

||||||

See accompanying Disclosures and Endnotes on page 43.

4 OAKMARK FUNDS

Oakmark Fund December 31, 2019

Portfolio Manager Commentary

William C. Nygren, CFA

Portfolio Manager

oakmx@oakmark.com

Kevin Grant, CFA

Portfolio Manager

oakmx@oakmark.com

The Oakmark Fund generated an 11% return during the fourth quarter, outperforming the S&P 500 Index's1 return of 9% over the same time period. We were encouraged that investors rewarded several of our key holdings within the financials sector, our largest and top contributing sector during the fourth quarter. As discussed in this quarter's market commentary, we continue to believe that our holdings within the financials sector offer an attractive risk/reward proposition, given their safer balance sheets and stronger competitive positions relative to recent history. We believe the prices of our financial holdings do not accurately reflect this dynamic. For the calendar year 2019, the Oakmark Fund returned 27% versus the 31% return for the S&P 500. Despite our strong absolute performance for the year, our long-term followers will know that we take little solace in this result, given our expectation to generate market-beating returns.

During the fourth quarter, we eliminated positions in Chesapeake Energy and Halliburton. These sales do not reflect a change in our view of the energy sector's overall attractiveness. Instead, they were executed to recognize a tax loss and deploy the proceeds from the sales into more attractive holdings in the industry that offers stronger cash flow profiles, better balance sheets and more compelling risk-adjusted expected returns. The energy sector has significantly underperformed the price of oil over the past several years. Since early 2016, the price of oil has risen over 100%, while the returns from the S&P Oil & Gas Exploration and Production ETF (ticker: XOP) have dropped. Yet demand for oil has continued to grow and we expect a more balanced global supply outlook. Therefore, we believe that attractive opportunities remain in this out-of-favor industry.

We did not add any names to the portfolio during the fourth quarter, but we did take advantage of the relative price differential within Alphabet's dual share class structure by swapping a portion of our non-voting Class C shares for voting Class A shares, which were offered at a slight discount to the non-voting shares. We believe that the voting rights afforded to the Class A shares should trade at a modest premium to the non-voting C shares—not a discount. We were happy to express this view by performing a like-kind exchange that didn't trigger a taxable event.

Regeneron Pharmaceuticals and State Street were the best individual contributors for the quarter and the lowest contributors were Ally Financial and American International Group. No single position cost the Fund more than 28 basis points during the period. Our strongest contributing sectors were financials and health care and our lowest contributing sectors were energy and consumer staples, the latter of which is among our smallest sector allocations. For the calendar year, our best individual contributors were Citigroup and Apple, while our biggest detractors were Qurate Retail Class A and DXC Technology.

We thank our fellow shareholders for your investment and continued support of the Oakmark Fund.

See accompanying Disclosures and Endnotes on page 43.

Oakmark.com 5

Oakmark Fund December 31, 2019 (Unaudited)

Schedule of Investments (in thousands)

|

Shares |

Value |

||||||||||

|

COMMON STOCKS - 96.1% |

|||||||||||

|

FINANCIALS - 29.7% |

|||||||||||

|

DIVERSIFIED FINANCIALS - 18.2% |

|||||||||||

|

Capital One Financial Corp. |

5,031 |

$ |

517,699 |

||||||||

|

Ally Financial, Inc. |

15,923 |

486,610 |

|||||||||

|

State Street Corp. |

5,857 |

463,297 |

|||||||||

|

The Charles Schwab Corp. |

9,180 |

436,591 |

|||||||||

|

Moody's Corp. |

1,471 |

349,294 |

|||||||||

|

The Bank of New York Mellon Corp. |

6,158 |

309,908 |

|||||||||

|

The Goldman Sachs Group, Inc. |

1,105 |

254,073 |

|||||||||

|

S&P Global, Inc. |

842 |

229,794 |

|||||||||

|

3,047,266 |

|||||||||||

|

BANKS - 9.4% |

|||||||||||

|

Citigroup, Inc. |

7,591 |

606,453 |

|||||||||

|

Bank of America Corp. |

17,174 |

604,858 |

|||||||||

|

Wells Fargo & Co. |

6,944 |

373,560 |

|||||||||

|

1,584,871 |

|||||||||||

|

INSURANCE - 2.1% |

|||||||||||

|

American International Group, Inc. |

6,908 |

354,573 |

|||||||||

|

4,986,710 |

|||||||||||

|

COMMUNICATION SERVICES - 14.4% |

|||||||||||

|

MEDIA & ENTERTAINMENT - 14.4% |

|||||||||||

|

Netflix, Inc. (a) |

1,586 |

513,182 |

|||||||||

|

Charter Communications, Inc., Class A (a) |

941 |

456,315 |

|||||||||

|

Alphabet, Inc., Class A (a) |

332 |

444,357 |

|||||||||

|

Comcast Corp., Class A |

8,873 |

399,028 |

|||||||||

|

Facebook, Inc., Class A (a) |

1,927 |

395,537 |

|||||||||

|

Alphabet, Inc., Class C (a) |

154 |

205,935 |

|||||||||

|

2,414,354 |

|||||||||||

|

CONSUMER DISCRETIONARY - 13.6% |

|||||||||||

|

AUTOMOBILES & COMPONENTS - 5.7% |

|||||||||||

|

Fiat Chrysler Automobiles N.V. |

24,924 |

366,131 |

|||||||||

|

General Motors Co. |

9,229 |

337,770 |

|||||||||

|

Aptiv PLC |

2,149 |

204,043 |

|||||||||

|

Delphi Technologies PLC (a) |

3,646 |

46,777 |

|||||||||

|

954,721 |

|||||||||||

|

RETAILING - 4.3% |

|||||||||||

|

Booking Holdings, Inc. (a) |

191 |

391,235 |

|||||||||

|

eBay, Inc. |

6,348 |

229,219 |

|||||||||

|

Qurate Retail, Inc., Class A (a) |

12,406 |

104,584 |

|||||||||

|

725,038 |

|||||||||||

|

CONSUMER SERVICES - 3.6% |

|||||||||||

|

MGM Resorts International |

9,180 |

305,412 |

|||||||||

|

Hilton Worldwide Holdings, Inc. |

2,714 |

301,010 |

|||||||||

|

606,422 |

|||||||||||

|

2,286,181 |

|||||||||||

|

Shares |

Value |

||||||||||

|

INFORMATION TECHNOLOGY - 13.3% |

|||||||||||

|

SOFTWARE & SERVICES - 6.3% |

|||||||||||

|

Gartner, Inc. (a) |

1,758 |

$ |

270,892 |

||||||||

|

DXC Technology Co. |

6,900 |

259,371 |

|||||||||

|

Automatic Data Processing, Inc. |

1,065 |

181,497 |

|||||||||

|

Visa, Inc., Class A |

929 |

174,616 |

|||||||||

|

MasterCard, Inc., Class A |

572 |

170,853 |

|||||||||

|

1,057,229 |

|||||||||||

|

TECHNOLOGY HARDWARE & EQUIPMENT - 4.1% |

|||||||||||

|

TE Connectivity, Ltd. |

4,301 |

412,174 |

|||||||||

|

Apple, Inc. |

938 |

275,561 |

|||||||||

|

687,735 |

|||||||||||

|

SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT - 2.9% |

|||||||||||

|

Intel Corp. |

5,053 |

302,434 |

|||||||||

|

Texas Instruments, Inc. |

1,504 |

192,948 |

|||||||||

|

495,382 |

|||||||||||

|

2,240,346 |

|||||||||||

|

INDUSTRIALS - 10.2% |

|||||||||||

|

CAPITAL GOODS - 7.8% |

|||||||||||

|

Parker-Hannifin Corp. |

1,900 |

391,008 |

|||||||||

|

General Electric Co. |

32,589 |

363,690 |

|||||||||

|

Cummins, Inc. |

1,680 |

300,617 |

|||||||||

|

Caterpillar, Inc. |

1,709 |

252,400 |

|||||||||

|

1,307,715 |

|||||||||||

|

TRANSPORTATION - 2.4% |

|||||||||||

|

American Airlines Group, Inc. |

8,080 |

231,737 |

|||||||||

|

FedEx Corp. |

1,104 |

166,876 |

|||||||||

|

398,613 |

|||||||||||

|

1,706,328 |

|||||||||||

|

HEALTH CARE - 7.6% |

|||||||||||

|

HEALTH CARE EQUIPMENT & SERVICES - 4.7% |

|||||||||||

|

CVS Health Corp. |

4,356 |

323,605 |

|||||||||

|

Humana, Inc. |

684 |

250,590 |

|||||||||

|

HCA Healthcare, Inc. |

1,459 |

215,698 |

|||||||||

|

789,893 |

|||||||||||

|

PHARMACEUTICALS, BIOTECHNOLOGY & LIFE SCIENCES - 2.9% |

|||||||||||

|

Regeneron Pharmaceuticals, Inc. (a) |

1,301 |

488,348 |

|||||||||

|

1,278,241 |

|||||||||||

|

ENERGY - 5.5% |

|||||||||||

|

Apache Corp. |

11,391 |

291,485 |

|||||||||

|

Concho Resources, Inc. |

2,616 |

229,118 |

|||||||||

|

EOG Resources, Inc. |

2,553 |

213,856 |

|||||||||

|

Diamondback Energy, Inc. |

2,008 |

186,454 |

|||||||||

|

920,913 |

|||||||||||

6 OAKMARK FUNDS

Oakmark Fund December 31, 2019 (Unaudited)

Schedule of Investments (in thousands) (continued)

|

Shares |

Value |

||||||||||

|

COMMON STOCKS - 96.1% (continued) |

|||||||||||

|

CONSUMER STAPLES - 1.8% |

|||||||||||

|

FOOD, BEVERAGE & TOBACCO - 1.8% |

|||||||||||

|

Constellation Brands, Inc., Class A |

1,611 |

$ |

305,763 |

||||||||

|

TOTAL COMMON STOCKS - 96.1% (COST $9,656,107) |

16,138,836 |

||||||||||

|

Par Value |

Value |

||||||||||

|

SHORT-TERM INVESTMENT - 3.9% |

|||||||||||

|

REPURCHASE AGREEMENT - 3.9% |

|||||||||||

|

Fixed Income Clearing Corp. Repurchase Agreement, 1.55% dated 12/31/19 due 01/02/20, repurchase price $647,928, collateralized by United States Treasury Notes, 1.875% - 2.875% due 11/15/21 - 12/15/21, aggregate value plus accrued interest of $660,830 (Cost: $647,872) |

$ |

647,872 |

647,872 |

||||||||

|

TOTAL SHORT-TERM INVESTMENTS - 3.9% (COST $647,872) |

647,872 |

||||||||||

|

TOTAL INVESTMENTS - 100.0% (COST $10,303,979) |

16,786,708 |

||||||||||

|

Foreign Currencies (Cost $0) - 0.0% (b) |

0 |

(c) |

|||||||||

|

Liabilities In Excess of Other Assets - 0.0% (b) |

(880 |

) |

|||||||||

|

TOTAL NET ASSETS - 100.0% |

$ |

16,785,828 |

|||||||||

(a) Non-income producing security

(b) Amount rounds to less than 0.1%.

(c) Amount rounds to less than $1,000.

Oakmark.com 7

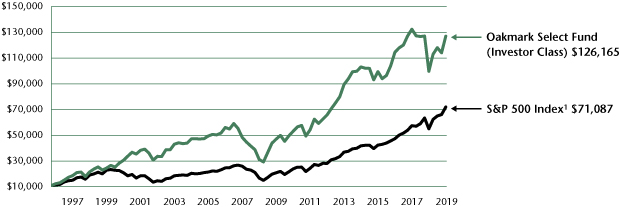

Oakmark Select Fund December 31, 2019

Summary Information

VALUE OF A $10,000 INVESTMENT

Since Inception - 11/01/96 (Unaudited)

PERFORMANCE

|

Average Annual Total Returns (as of 12/31/19) |

|||||||||||||||||||||||||||||||

| (Unaudited) |

Total Return Last 3 Months |

1-year |

3-year |

5-year |

10-year |

Since Inception |

Inception Date |

||||||||||||||||||||||||

|

Oakmark Select Fund (Investor Class) |

11.47 |

% |

27.69 |

% |

3.54 |

% |

4.30 |

% |

10.60 |

% |

11.56 |

% |

11/01/96 |

||||||||||||||||||

|

S&P 500 Index |

9.07 |

% |

31.49 |

% |

15.27 |

% |

11.70 |

% |

13.56 |

% |

8.84 |

% |

|||||||||||||||||||

|

Lipper Multi-Cap Value Fund Index13 |

7.59 |

% |

25.02 |

% |

7.59 |

% |

6.71 |

% |

10.19 |

% |

7.60 |

% |

|||||||||||||||||||

|

Oakmark Select Fund (Advisor Class) |

11.52 |

% |

27.82 |

% |

3.69 |

% |

N/A |

N/A |

4.47 |

% |

11/30/16 |

||||||||||||||||||||

|

Oakmark Select Fund (Institutional Class) |

11.51 |

% |

27.87 |

% |

3.72 |

% |

N/A |

N/A |

4.50 |

% |

11/30/16 |

||||||||||||||||||||

|

Oakmark Select Fund (Service Class) |

11.40 |

% |

27.40 |

% |

3.29 |

% |

4.00 |

% |

10.27 |

% |

8.45 |

% |

12/31/99 |

||||||||||||||||||

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Past performance is no guarantee of future results. The performance data quoted represents past performance. Current performance may be lower or higher than the performance data quoted. Total return includes change in share prices and, in each case, includes reinvestment of dividends and capital gain distributions. The investment return and principal value vary so that an investor's shares, when redeemed, may be worth more or less than the original cost. To obtain the most recent month-end performance, please visit Oakmark.com.

|

TOP TEN EQUITY HOLDINGS12 |

% of Net Assets | ||||||

|

CBRE Group, Inc., Class A |

9.0 |

||||||

|

Citigroup, Inc. |

7.3 |

||||||

|

Alphabet, Inc., Class A |

7.1 |

||||||

|

Ally Financial, Inc. |

6.5 |

||||||

|

Bank of America Corp. |

5.4 |

||||||

|

Charter Communications, Inc., Class A |

4.9 |

||||||

|

Regeneron Pharmaceuticals, Inc. |

4.8 |

||||||

|

Capital One Financial Corp |

4.7 |

||||||

|

Fiat Chrysler Automobiles N.V. |

4.7 |

||||||

|

TE Connectivity, Ltd. |

4.3 |

||||||

|

FUND STATISTICS |

|||||||

|

Ticker* |

OAKLX |

||||||

|

Number of Equity Holdings |

22 |

||||||

|

Net Assets |

$4.9 billion | ||||||

|

Weighted Average Market Cap |

$161.6 billion | ||||||

|

Median Market Cap |

$36.6 billion | ||||||

|

Gross Expense Ratio - Investor Class (as of 09/30/19)* |

1.08% | ||||||

|

Net Expense Ratio - Investor Class (as of 09/30/19)*† |

1.00% | ||||||

* This information is related to the Investor Class. Please visit Oakmark.com for information related to the Advisor, Institutional and Service Classes.

† The net expense ratio reflects a contractual advisory fee waiver agreement through January 27, 2021.

|

SECTOR ALLOCATION |

% of Net Assets | ||||||

|

Financials |

28.0 |

||||||

|

Communication Services |

18.7 |

||||||

|

Consumer Discretionary |

15.8 |

||||||

|

Real Estate |

9.0 |

||||||

|

Industrials |

7.4 |

||||||

|

Energy |

6.3 |

||||||

|

Information Technology |

5.3 |

||||||

|

Health Care |

4.8 |

||||||

|

Short-Term Investments and Other |

4.7 |

||||||

See accompanying Disclosures and Endnotes on page 43.

8 OAKMARK FUNDS

Oakmark Select Fund December 31, 2019

Portfolio Manager Commentary

William C. Nygren, CFA

Portfolio Manager

oaklx@oakmark.com

Anthony P. Coniaris, CFA

Portfolio Manager

oaklx@oakmark.com

Win Murray

Portfolio Manager

oaklx@oakmark.com

What a difference a year can make! The Oakmark Select Fund returned 11.5% in the fourth quarter compared to the S&P 500's1 9.1% return. Unlike one year ago when fear ruled the day, the fourth quarter of 2019 was a welcome return to a market where business fundamentals mattered. For calendar year 2019, the Oakmark Select Fund increased 27.7% versus 31.5% for the S&P 500. While we still have to make up some ground due to a few years of below-market returns, we are encouraged by these much stronger results.

The largest contributors to performance during the quarter were Regeneron Pharmaceuticals, CBRE Group and Citigroup. After lagging the market considerably despite strong underlying fundamentals, Regeneron (REGN) management announced a large share repurchase authorization to take advantage of a growing gap between the market price and underlying value of REGN. We applaud management's opportunism and, somewhat oddly, the same market that undervalued REGN seems to agree. The largest detractors were Ally Financial, American International Group and Qurate Retail. There was no identifiable news to explain the relative contribution or detraction from the other aforementioned holdings.

A year ago, we took advantage of the spike in market volatility and added four new names to the portfolio. The market environment of 2019 was quite different as was our activity. We didn't add or remove any companies from the portfolio in the fourth quarter of 2019. We did, however, swap more than 70% of our non-voting Alphabet Class C shares for voting Class A shares as they were offered at a small discount to non-voting shares. We believe there should be a modest premium for the higher voting rights of the Class A shares and the swaps were done via like-kind exchange so there wasn't a corresponding capital gain.

Speaking of taxes, despite a portfolio return of nearly 30% this year, we were able to offset all capital gains in 2019 with losses such that there was no capital gains distribution in 2019.

Thank you, our fellow shareholders, for you continued investment in the Oakmark Select Fund.

See accompanying Disclosures and Endnotes on page 43.

Oakmark.com 9

Oakmark Select Fund December 31, 2019 (Unaudited)

Schedule of Investments (in thousands)

|

Shares |

Value |

||||||||||

|

COMMON STOCKS - 95.3% |

|||||||||||

|

FINANCIALS - 28.0% |

|||||||||||

|

BANKS - 12.7% |

|||||||||||

|

Citigroup, Inc. |

4,412 |

$ |

352,475 |

||||||||

|

Bank of America Corp. |

7,501 |

264,171 |

|||||||||

|

616,646 |

|||||||||||

|

DIVERSIFIED FINANCIALS - 11.2% |

|||||||||||

|

Ally Financial, Inc. |

10,280 |

314,157 |

|||||||||

|

Capital One Financial Corp. |

2,235 |

229,993 |

|||||||||

|

544,150 |

|||||||||||

|

INSURANCE - 4.1% |

|||||||||||

|

American International Group, Inc. |

3,885 |

199,427 |

|||||||||

|

1,360,223 |

|||||||||||

|

COMMUNICATION SERVICES - 18.7% |

|||||||||||

|

MEDIA & ENTERTAINMENT - 18.7% |

|||||||||||

|

Alphabet, Inc., Class A (a) |

257 |

344,269 |

|||||||||

|

Charter Communications, Inc., Class A (a) |

494 |

239,629 |

|||||||||

|

Netflix, Inc. (a) |

576 |

186,441 |

|||||||||

|

Alphabet, Inc., Class C (a) |

102 |

136,209 |

|||||||||

|

906,548 |

|||||||||||

|

CONSUMER DISCRETIONARY - 15.8% |

|||||||||||

|

AUTOMOBILES & COMPONENTS - 8.1% |

|||||||||||

|

Fiat Chrysler Automobiles N.V. |

15,434 |

226,727 |

|||||||||

|

Lear Corp. |

1,200 |

164,640 |

|||||||||

|

391,367 |

|||||||||||

|

CONSUMER SERVICES - 6.2% |

|||||||||||

|

MGM Resorts International |

5,147 |

171,240 |

|||||||||

|

Hilton Worldwide Holdings, Inc. |

1,166 |

129,374 |

|||||||||

|

300,614 |

|||||||||||

|

RETAILING - 1.5% |

|||||||||||

|

Qurate Retail, Inc., Class A (a) |

8,717 |

73,484 |

|||||||||

|

765,465 |

|||||||||||

|

REAL ESTATE - 9.0% |

|||||||||||

|

CBRE Group, Inc., Class A (a) |

7,118 |

436,232 |

|||||||||

|

INDUSTRIALS - 7.4% |

|||||||||||

|

CAPITAL GOODS - 4.3% |

|||||||||||

|

General Electric Co. |

18,640 |

208,022 |

|||||||||

|

TRANSPORTATION - 3.1% |

|||||||||||

|

American Airlines Group, Inc. |

5,239 |

150,263 |

|||||||||

|

358,285 |

|||||||||||

|

ENERGY - 6.3% |

|||||||||||

|

Apache Corp. |

6,100 |

156,099 |

|||||||||

|

Concho Resources, Inc. |

1,710 |

149,745 |

|||||||||

|

305,844 |

|||||||||||

|

Shares |

Value |

||||||||||

|

INFORMATION TECHNOLOGY - 5.3% |

|||||||||||

|

TECHNOLOGY HARDWARE & EQUIPMENT - 4.3% |

|||||||||||

|

TE Connectivity, Ltd. |

2,188 |

$ |

209,692 |

||||||||

|

SOFTWARE & SERVICES - 1.0% |

|||||||||||

|

MasterCard, Inc., Class A |

155 |

46,281 |

|||||||||

|

255,973 |

|||||||||||

|

HEALTH CARE - 4.8% |

|||||||||||

|

PHARMACEUTICALS, BIOTECHNOLOGY & LIFE SCIENCES - 4.8% |

|||||||||||

|

Regeneron Pharmaceuticals, Inc. (a) |

620 |

232,798 |

|||||||||

|

TOTAL COMMON STOCKS - 95.3% (COST $2,701,670) |

4,621,368 |

||||||||||

|

Par Value |

Value |

||||||||||

|

SHORT-TERM INVESTMENTS - 4.7% |

|||||||||||

|

REPURCHASE AGREEMENT - 4.7% |

|||||||||||

|

Fixed Income Clearing Corp. Repurchase Agreement, 1.55% dated 12/31/19 due 01/02/20, repurchase price $230,210, collateralized by a United States Treasury Note, 1.625% due 12/31/21, value plus accrued interest of $234,798 (Cost: $230,191) |

$ |

230,191 |

230,191 |

||||||||

|

TOTAL SHORT-TERM INVESTMENTS - 4.7% (COST $230,191) |

230,191 |

||||||||||

|

TOTAL INVESTMENTS - 100.0% (COST $2,931,861) |

4,851,559 |

||||||||||

|

Liabilities In Excess of Other Assets - 0.0% (b) |

(850 |

) |

|||||||||

|

TOTAL NET ASSETS - 100.0% |

$ |

4,850,709 |

|||||||||

(a) Non-income producing security

(b) Amount rounds to less than 0.1%.

10 OAKMARK FUNDS

This page intentionally left blank.

Oakmark.com 11

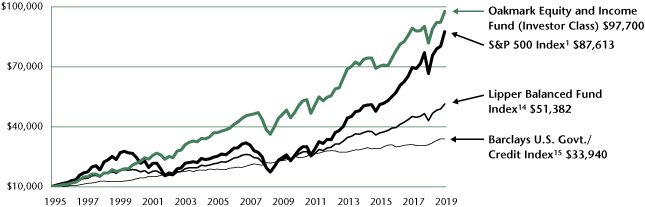

Oakmark Equity and Income Fund December 31, 2019

Summary Information

VALUE OF A $10,000 INVESTMENT

Since Inception - 11/01/95 (Unaudited)

PERFORMANCE

|

Average Annual Total Returns (as of 12/31/19) |

|||||||||||||||||||||||||||||||

| (Unaudited) |

Total Return Last 3 Months |

1-year |

3-year |

5-year |

10-year |

Since Inception |

Inception Date |

||||||||||||||||||||||||

|

Oakmark Equity and Income Fund (Investor Class) |

5.84 |

% |

19.31 |

% |

7.77 |

% |

5.79 |

% |

7.78 |

% |

9.89 |

% |

11/01/95 |

||||||||||||||||||

|

Lipper Balanced Fund Index |

5.12 |

% |

19.44 |

% |

9.11 |

% |

6.76 |

% |

8.12 |

% |

7.01 |

% |

|||||||||||||||||||

|

S&P 500 Index |

9.07 |

% |

31.49 |

% |

15.27 |

% |

11.70 |

% |

13.56 |

% |

9.40 |

% |

|||||||||||||||||||

|

Barclays U.S. Govt./Credit Index |

-0.01 |

% |

9.71 |

% |

4.35 |

% |

3.23 |

% |

3.96 |

% |

5.19 |

% |

|||||||||||||||||||

|

Oakmark Equity and Income Fund (Advisor Class) |

5.88 |

% |

19.43 |

% |

7.92 |

% |

N/A |

N/A |

8.23 |

% |

11/30/16 |

||||||||||||||||||||

|

Oakmark Equity and Income Fund (Institutional Class) |

5.87 |

% |

19.50 |

% |

7.96 |

% |

N/A |

N/A |

8.27 |

% |

11/30/16 |

||||||||||||||||||||

|

Oakmark Equity and Income Fund (Service Class) |

5.76 |

% |

18.99 |

% |

7.49 |

% |

5.49 |

% |

7.46 |

% |

8.31 |

% |

07/12/00 |

||||||||||||||||||

The graph and table above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Past performance is no guarantee of future results. The performance data quoted represents past performance. Current performance may be lower or higher than the performance data quoted. Total return includes change in share prices and, in each case, includes reinvestment of dividends and capital gain distributions. The investment return and principal value vary so that an investor's shares, when redeemed, may be worth more or less than the original cost. To obtain the most recent month-end performance, please visit Oakmark.com.

|

TOP TEN EQUITY HOLDINGS12 |

% of Net Assets | ||||||

|

Bank of America Corp. |

5.3 |

||||||

|

General Motors Co. |

4.7 |

||||||

|

TE Connectivity, Ltd. |

4.3 |

||||||

|

MasterCard, Inc., Class A |

3.3 |

||||||

|

Alphabet, Inc., Class C |

3.2 |

||||||

|

Nestlé SA |

3.0 |

||||||

|

CVS Health Corp. |

2.9 |

||||||

|

Citigroup, Inc. |

2.9 |

||||||

|

Philip Morris International, Inc. |

2.7 |

||||||

|

Charter Communications, Inc., Class A |

2.4 |

||||||

|

FUND STATISTICS |

|||||||

|

Ticker* |

OAKBX |

||||||

|

Number of Equity Holdings |

43 |

||||||

|

Net Assets |

$11.6 billion | ||||||

|

Weighted Average Market Cap |

$155.0 billion | ||||||

|

Median Market Cap |

$31.4 billion | ||||||

|

Gross Expense Ratio - Investor Class (as of 09/30/19)* |

0.91% | ||||||

|

Net Expense Ratio - Investor Class (as of 09/30/19)*† |

0.81% | ||||||

* This information is related to the Investor Class. Please visit Oakmark.com for information related to the Advisor, Institutional and Service Classes.

† The net expense ratio reflects a contractual advisory fee waiver agreement through January 27, 2021.

|

SECTOR ALLOCATION |

% of Net Assets | ||||||

|

Equity Investments |

|||||||

|

Financials |

11.8 |

||||||

|

Consumer Discretionary |

11.6 |

||||||

|

Information Technology |

9.1 |

||||||

|

Health Care |

7.7 |

||||||

|

Consumer Staples |

7.3 |

||||||

|

Communication Services |

6.4 |

||||||

|

Industrials |

4.6 |

||||||

|

Energy |

2.5 |

||||||

|

Real Estate |

1.5 |

||||||

|

Materials |

0.9 |

||||||

|

Total Equity Investments |

63.4 |

||||||

|

Preferred Stocks |

0.1 |

||||||

|

Fixed Income Investments |

|||||||

|

Corporate Bonds |

18.0 |

||||||

|

Government and Agency Securities |

11.3 |

||||||

|

Total Fixed Income Investments |

29.3 |

||||||

|

Short-Term Investments and Other |

7.2 |

||||||

See accompanying Disclosures and Endnotes on page 43.

12 OAKMARK FUNDS

Oakmark Equity and Income Fund December 31, 2019

Portfolio Manager Commentary

Clyde S. McGregor, CFA

Portfolio Manager

oakbx@oakmark.com

M. Colin Hudson, CFA

Portfolio Manager

oakbx@oakmark.com

Edward J. Wojciechowski, CFA

Portfolio Manager

oakbx@oakmark.com

Market Inequality

In this politically fraught time, it seems that advocates call out inequality in almost every social and economic endeavor, and now it is the stock market's turn. Many commentators have noted the increasing gap in profit margins favoring the largest U.S. companies over all the rest, a reversal of the outcome in the first decade of this century. Superior profitability has led to superior equity performance for many of the largest companies. The Equity and Income Fund has implicitly recognized this development: we now maintain a higher proportion of large capitalization stocks in the equity allocation of the portfolio than we did in the Fund's early years.

But Hendrik Bessembinder of the Carey School of Business at Arizona State University16 recently discovered an even greater inequality. According to Bessembinder, since 1990, 56% of U.S. stocks have failed to beat the return on cash (as represented by the return on one-month Treasury bills). He also found that the top 1.3% of companies account for almost all of the net increase in global stock market wealth creation over the 30 years he included in his study. Overall, Bessembinder's work shows that the stock market earns returns well in excess of Treasury bills, but it accomplishes this through very large returns to few stocks rather than excess returns to average stocks.

We do not have the ability to study all of Bessembinder's data, but we do consider its implications for our equity portfolio. To review quickly, we are value investors. We attempt to identify companies selling at a discount to our estimate of their intrinsic value per share, that persistently grow their intrinsic value per share, and that have managers who act and think like owners of the business.

Bessembinder's work suggests that our focus on determining whether a company is growing its intrinsic value per share is vital. We well know the danger of "value traps," i.e., businesses that are priced cheaply because their business value is deteriorating over time. Long before Harris Associates introduced the Oakmark family of mutual funds, the firm developed its three-part definition of value, in part to mitigate the risk of potential value traps. Our value discipline might seem at odds with an investing environment where the winners are generating a disproportionate share of return, but this is not necessarily the case. For example, Fund holding Mastercard has increased in price roughly 13 times from our initial purchase. We have been able to maintain a position in the company because our understanding of the growth in its intrinsic value has grown commensurate with its price. Two other long-held names that demonstrate this attribute are Nestlé and UnitedHealth Group. It is our job to seek the issues that can produce this sort of outcome for the portfolio. Although the extreme outcome

inequality that Bessembinder describes makes this search more difficult, it is our challenge.

Year/Quarter Review

2019 proved to be a strong year for U.S. stocks and bonds. Of course, this followed a roughly 20% drop in stock indexes during the fourth quarter of 2018. In 2018, the Federal Reserve increased interest rates four times. Old-timers may remember investment strategist Edson Gould who coined the phrase "three steps and stumble" to describe the stock market's response to a series of Fed interest rate hikes, and 2018 demonstrated the wisdom in that rubric. In the second half of 2019, the Fed apparently took the stock market's message to heart and reversed course by cutting rates three times.

During the year, recession fears and forecasts waxed, and investors began to keep a tally of the number of times the word "recession" appeared in news articles. The Treasury yield curve inverted in the spring, meaning that long-term interest rates fell below short-term rates. This seemed to buttress the recession case because the historic record shows that inverted yield curves have preceded economic downturns. But, later in the year, the economic clouds began to dissipate, the yield curve lost its inversion and economic sentiment rebounded, especially when it appeared that U.S./China trade talks were developing favorably. The renewed confidence helped to support a particularly good fourth quarter for U.S. equities.

The Equity and Income Fund earned 6% in the quarter, which contrasts to a 5% gain for the Lipper Balanced Fund Index14, the Fund's performance benchmark. For calendar 2019 as a whole, the Fund showed a gain of 19%, which matches the return for the Lipper Index. We are pleased to report that the annualized compound rate of return since the Fund's inception in 1995 is 9.9%, while the corresponding return to the Lipper Index is 7.0%.

The largest contributors to portfolio return in the quarter were Bank of America, UnitedHealth Group, CVS Health, Citigroup and Charter Communications. Ally Financial, TD Ameritrade (sold), Foot Locker, American International Group and General Motors detracted most. For all of calendar 2019, Bank of America, Mastercard, Charter Communications, TE Connectivity and Citigroup led the contributors, while Foot Locker, TD Ameritrade, National Oilwell Varco, Diamondback Energy and Qurate Retail (sold) detracted most from return.

Transaction Activity

We made no significant changes to the total asset allocation of the Fund during the quarter. The equity percentage increased somewhat because of the strong rally in share prices. As noted above, the yield curve became "uninverted" in the quarter as short-term rates declined below intermediate and longer term rates. The Fund's fixed income duration, the measure of

See accompanying Disclosures and Endnotes on page 43.

Oakmark.com 13

Oakmark Equity and Income Fund December 31, 2019

Portfolio Manager Commentary (continued)

sensitivity to changes in interest rates, increased modestly in the period. As always, our fixed income team continually works to identify opportunities to improve the Fund's bond allocation.

We initiated one new equity holding while eliminating one in the quarter. The elimination, TD Ameritrade, proved to be badly timed as the company announced a merger agreement not long after our sale. We sold Ameritrade as part of our tax-loss harvesting process that helps moderate the Fund's capital gains' distributions. The company's share price declined after its competitor Charles Schwab announced it was eliminating commissions on equity trades. We took the Ameritrade loss at that time to offset previously realized gains. We regret the infelicitous timing of the sale.

Our new purchase was EOG Resources, the largest independent oil production company in the U.S. onshore region. The company has built a unique decentralized and returns-focused corporate culture, which has produced returns in excess of peers through multiple commodity cycles. This relentless focus on returns has resulted in leading capabilities in land acquisition cost, well design, operating cost efficiency and technology innovation. EOG expects that over 90% of the wells it will drill over the next 10-12 years will generate economic returns at a $40 per barrel oil price. (The price per barrel for West Texas Intermediate was $61 as of January 2.) This low position on the cost curve should allow EOG to grow oil production at a sustained mid-teens rate at today's oil prices, even though its shares trade at just 6x EV/EBITDA17. This compares favorably to the S&P 5001, which historically grows earnings at a mid-single digits pace and trades in a 10-14x EV/EBITDA range. Shares of energy companies performed poorly in 2019, despite the robust stock market rally. We believe that this industry may offer unusual attraction today.

We thank our fellow shareholders for investing in the Equity and Income Fund and invite your comments and questions.

See accompanying Disclosures and Endnotes on page 43.

14 OAKMARK FUNDS

Oakmark Equity and Income Fund December 31, 2019 (Unaudited)

Schedule of Investments (in thousands)

|

Shares |

Value |

||||||||||

|

COMMON STOCKS - 63.4% |

|||||||||||

|

FINANCIALS - 11.8% |

|||||||||||

|

BANKS - 8.2% |

|||||||||||

|

Bank of America Corp. |

17,561 |

$ |

618,495 |

||||||||

|

Citigroup, Inc. |

4,153 |

331,775 |

|||||||||

|

950,270 |

|||||||||||

|

DIVERSIFIED FINANCIALS - 2.7% |

|||||||||||

|

Ally Financial, Inc. |

7,050 |

215,451 |

|||||||||

|

State Street Corp. |

1,239 |

97,997 |

|||||||||

|

313,448 |

|||||||||||

|

INSURANCE - 0.9% |

|||||||||||

|

American International Group, Inc. |

2,077 |

106,595 |

|||||||||

|

1,370,313 |

|||||||||||

|

CONSUMER DISCRETIONARY - 11.6% |

|||||||||||

|

AUTOMOBILES & COMPONENTS - 8.4% |

|||||||||||

|

General Motors Co. |

14,856 |

543,726 |

|||||||||

|

BorgWarner, Inc. |

5,386 |

233,627 |

|||||||||

|

Lear Corp. |

1,433 |

196,544 |

|||||||||

|

973,897 |

|||||||||||

|

RETAILING - 1.9% |

|||||||||||

|

Foot Locker, Inc. |

3,520 |

137,229 |

|||||||||

|

Booking Holdings, Inc. (a) |

41 |

83,258 |

|||||||||

|

220,487 |

|||||||||||

|

CONSUMER SERVICES - 0.7% |

|||||||||||

|

MGM Resorts International |

2,351 |

78,225 |

|||||||||

|

CONSUMER DURABLES & APPAREL - 0.6% |

|||||||||||

|

Carter's, Inc. |

664 |

72,635 |

|||||||||

|

1,345,244 |

|||||||||||

|

INFORMATION TECHNOLOGY - 9.1% |

|||||||||||

|

SOFTWARE & SERVICES - 4.8% |

|||||||||||

|

MasterCard, Inc., Class A |

1,290 |

385,092 |

|||||||||

|

Oracle Corp. |

2,026 |

107,327 |

|||||||||

|

CoreLogic, Inc. (a) |

1,293 |

56,517 |

|||||||||

|

548,936 |

|||||||||||

|

TECHNOLOGY HARDWARE & EQUIPMENT - 4.3% |

|||||||||||

|

TE Connectivity, Ltd. |

5,241 |

502,326 |

|||||||||

|

1,051,262 |

|||||||||||

|

HEALTH CARE - 7.7% |

|||||||||||

|

HEALTH CARE EQUIPMENT & SERVICES - 6.2% |

|||||||||||

|

CVS Health Corp. |

4,585 |

340,646 |

|||||||||

|

UnitedHealth Group, Inc. |

736 |

216,234 |

|||||||||

|

HCA Healthcare, Inc. |

736 |

108,758 |

|||||||||

|

LivaNova PLC (a) |

757 |

57,137 |

|||||||||

|

722,775 |

|||||||||||

|

PHARMACEUTICALS, BIOTECHNOLOGY & LIFE SCIENCES - 1.5% |

|||||||||||

|

Agilent Technologies, Inc. |

998 |

85,114 |

|||||||||

|

Regeneron Pharmaceuticals, Inc. (a) |

219 |

82,230 |

|||||||||

|

167,344 |

|||||||||||

|

890,119 |

|||||||||||

|

Shares |

Value |

||||||||||

|

CONSUMER STAPLES - 7.3% |

|||||||||||

|

FOOD, BEVERAGE & TOBACCO - 7.3% |

|||||||||||

|

Nestlé SA (b) |

3,187 |

$ |

345,035 |

||||||||

|

Philip Morris International, Inc. |

3,642 |

309,923 |

|||||||||

|

Diageo PLC (b) |

960 |

161,683 |

|||||||||

|

Constellation Brands, Inc., Class A |

174 |

32,941 |

|||||||||

|

849,582 |

|||||||||||

|

COMMUNICATION SERVICES - 6.4% |

|||||||||||

|

MEDIA & ENTERTAINMENT - 6.4% |

|||||||||||

|

Alphabet, Inc., Class C (a) |

275 |

367,012 |

|||||||||

|

Charter Communications, Inc., Class A (a) |

577 |

279,746 |

|||||||||

|

Comcast Corp., Class A |

2,120 |

95,336 |

|||||||||

|

742,094 |

|||||||||||

|

INDUSTRIALS - 4.6% |

|||||||||||

|

CAPITAL GOODS - 3.7% |

|||||||||||

|

Arconic, Inc. |

5,364 |

165,057 |

|||||||||

|

Carlisle Cos., Inc. |

718 |

116,233 |

|||||||||

|

Johnson Controls International plc |

2,519 |

102,529 |

|||||||||

|

WESCO International, Inc. (a) |

890 |

52,835 |

|||||||||

|

436,654 |

|||||||||||

|

TRANSPORTATION - 0.9% |

|||||||||||

|

American Airlines Group, Inc. |

2,147 |

61,573 |

|||||||||

|

Southwest Airlines Co. |

755 |

40,749 |

|||||||||

|

102,322 |

|||||||||||

|

538,976 |

|||||||||||

|

ENERGY - 2.5% |

|||||||||||

|

Apergy Corp. (a) |

2,398 |

80,999 |

|||||||||

|

Diamondback Energy, Inc. |

774 |

71,846 |

|||||||||

|

EOG Resources, Inc. |

678 |

56,806 |

|||||||||

|

National Oilwell Varco, Inc. |

2,012 |

50,400 |

|||||||||

|

PDC Energy, Inc. (a) |

1,082 |

28,319 |

|||||||||

|

288,370 |

|||||||||||

|

REAL ESTATE - 1.5% |

|||||||||||

|

The Howard Hughes Corp. (a) |

735 |

93,217 |

|||||||||

|

Gaming and Leisure Properties, Inc. REIT |

1,833 |

78,893 |

|||||||||

|

172,110 |

|||||||||||

|

MATERIALS - 0.9% |

|||||||||||

|

Glencore PLC |

35,440 |

110,483 |

|||||||||

|

TOTAL COMMON STOCKS - 63.4% (COST $3,944,118) |

7,358,553 |

||||||||||

|

PREFERRED STOCKS - 0.1% |

|||||||||||

|

FINANCIALS - 0.1% |

|||||||||||

|

GMAC Capital Trust I (c), 7.69% (3 mo. USD LIBOR + 5.785%), |

498 |

12,960 |

|||||||||

|

TOTAL PREFERRED STOCKS - 0.1% (COST $13,007) |

12,960 |

||||||||||

Oakmark.com 15

Oakmark Equity and Income Fund December 31, 2019 (Unaudited)

Schedule of Investments (in thousands) (continued)

|

Par Value |

Value |

||||||||||

|

FIXED INCOME - 29.3% |

|||||||||||

|

CORPORATE BONDS - 18.0% |

|||||||||||

|

CONSUMER DISCRETIONARY - 4.3% |

|||||||||||

|

Adient US LLC, 144A 7.00%, due 05/15/26 (d) |

$ |

15,965 |

$ |

17,402 |

|||||||

|

Amazon.com, Inc. 3.15%, due 08/22/27 |

9,950 |

10,545 |

|||||||||

|

Booking Holdings, Inc. 3.60%, due 06/01/26 |

14,730 |

15,725 |

|||||||||

|

3.55%, due 03/15/28 |

9,950 |

10,603 |

|||||||||

|

2.75%, due 03/15/23 |

6,965 |

7,117 |

|||||||||

|

BorgWarner, Inc. 4.625%, due 09/15/20 |

10,810 |

10,981 |

|||||||||

|

Boyd Gaming Corp. 6.00%, due 08/15/26 |

4,975 |

5,336 |

|||||||||

|

Caesars Resort Collection LLC / CRC Finco, Inc., 144A 5.25%, due 10/15/25 (d) |

25,870 |

26,775 |

|||||||||

|

CCO Holdings LLC / CCO Holdings Capital Corp., 144A 4.75%, due 03/01/30 (d) |

2,980 |

3,034 |

|||||||||

|

5.125%, due 05/01/27 (d) |

250 |

264 |

|||||||||

|

Charter Communications Operating LLC / Charter Communications Operating Capital 3.579%, due 07/23/20 |

29,148 |

29,334 |

|||||||||

|

4.20%, due 03/15/28 |

9,950 |

10,607 |

|||||||||

|

4.50%, due 02/01/24 |

2,985 |

3,213 |

|||||||||

|

Choice Hotels International, Inc. 3.70%, due 12/01/29 |

9,935 |

10,007 |

|||||||||

|

Delphi Technologies PLC, 144A 5.00%, due 10/01/25 (d) |

20,826 |

19,264 |

|||||||||

|

Dollar Tree, Inc. 2.702% (3 mo. USD LIBOR + 0.700%), due 04/17/20 (c) |

6,965 |

6,966 |

|||||||||

|

Expedia Group, Inc. 5.00%, due 02/15/26 |

28,360 |

31,288 |

|||||||||

|

Expedia Group, Inc., 144A 3.25%, due 02/15/30 (d) |

10,830 |

10,423 |

|||||||||

|

Foot Locker, Inc. 8.50%, due 01/15/22 |

4,340 |

4,807 |

|||||||||

|

General Motors Co. 4.875%, due 10/02/23 |

41,400 |

44,433 |

|||||||||

|

Hasbro, Inc. 3.55%, due 11/19/26 |

4,970 |

5,005 |

|||||||||

|

International Game Technology PLC, 144A 6.50%, due 02/15/25 (d) |

19,600 |

22,001 |

|||||||||

|

6.25%, due 02/15/22 (d) |

14,800 |

15,614 |

|||||||||

|

6.25%, due 01/15/27 (d) |

200 |

225 |

|||||||||

|

KFC Holding Co/Pizza Hut Holdings LLC/Taco Bell of America LLC, 144A 5.25%, due 06/01/26 (d) |

1,000 |

1,055 |

|||||||||

|

5.00%, due 06/01/24 (d) |

1,000 |

1,036 |

|||||||||

|

Lear Corp. 5.25%, due 01/15/25 |

11,060 |

11,370 |

|||||||||

|

4.25%, due 05/15/29 |

7,955 |

8,223 |

|||||||||

|

Lithia Motors, Inc., 144A 4.625%, due 12/15/27 (d) |

2,980 |

3,063 |

|||||||||

|

5.25%, due 08/01/25 (d) |

1,990 |

2,082 |

|||||||||

|

Par Value |

Value |

||||||||||

|

Marriott International, Inc. 4.00%, due 04/15/28 |

$ |

9,761 |

$ |

10,549 |

|||||||

|

3.60%, due 04/15/24 |

6,960 |

7,331 |

|||||||||

|

Penn National Gaming, Inc., 144A 5.625%, due 01/15/27 (d) |

9,950 |

10,515 |

|||||||||

|

Penske Automotive Group, Inc. 5.50%, due 05/15/26 |

11,343 |

11,882 |

|||||||||

|

5.375%, due 12/01/24 |

3,580 |

3,683 |

|||||||||

|

Sands China, Ltd. 5.40%, due 08/08/28 |

5,000 |

5,641 |

|||||||||

|

5.125%, due 08/08/25 |

3,000 |

3,292 |

|||||||||

|

4.60%, due 08/08/23 |

2,000 |

2,111 |

|||||||||

|

Scientific Games International, Inc., 144A 5.00%, due 10/15/25 (d) |

19,910 |

20,831 |

|||||||||

|

Starbucks Corp. 3.80%, due 08/15/25 |

9,950 |

10,722 |

|||||||||

|

4.00%, due 11/15/28 |

2,985 |

3,328 |

|||||||||

|

Station Casinos LLC, 144A 5.00%, due 10/01/25 (d) |

1,990 |

2,025 |

|||||||||

|

Tapestry, Inc. 3.00%, due 07/15/22 |

12,145 |

12,301 |

|||||||||

|

4.125%, due 07/15/27 |

4,975 |

5,085 |

|||||||||

|

Tempur Sealy International, Inc. 5.50%, due 06/15/26 |

3,125 |

3,293 |

|||||||||

|

The Gap, Inc. 5.95%, due 04/12/21 |

1,965 |

2,039 |

|||||||||

|

The William Carter Co., 144A 5.625%, due 03/15/27 (d) |

1,750 |

1,881 |

|||||||||

|

Under Armour, Inc. 3.25%, due 06/15/26 |

12,565 |

12,227 |

|||||||||

|

Wolverine World Wide, Inc., 144A 5.00%, due 09/01/26 (d) |

12,140 |

12,322 |

|||||||||

|

Yum! Brands, Inc. 3.875%, due 11/01/23 |

6,329 |

6,519 |

|||||||||

|

495,375 |

|||||||||||

|

FINANCIALS - 4.2% |

|||||||||||

|

Ally Financial, Inc. 3.875%, due 05/21/24 |

7,950 |

8,328 |

|||||||||

|

American Express Credit Corp. 2.60%, due 09/14/20 |

2,945 |

2,956 |

|||||||||

|

American International Group, Inc. 3.30%, due 03/01/21 |

14,665 |

14,878 |

|||||||||

|

Aon Corp. 5.00%, due 09/30/20 |

14,745 |

15,061 |

|||||||||

|

Bank of America Corp. 4.45%, due 03/03/26 |

5,000 |

5,492 |

|||||||||

|

BNP Paribas SA, 144A 7.625% (USD 5 Year Swap rate + 6.314%) (c) (d) (e) |

5,000 |

5,275 |

|||||||||

|

Citigroup, Inc. 3.352% (3 mo. USD LIBOR + 0.897%), due 04/24/25 (c) |

22,860 |

23,793 |

|||||||||

|

3.40%, due 05/01/26 |

15,000 |

15,760 |

|||||||||

|

4.05%, due 07/30/22 |

13,338 |

13,940 |

|||||||||

|

CNO Financial Group, Inc. 5.25%, due 05/30/25 |

5,895 |

6,529 |

|||||||||

|

Credit Suisse Group AG, 144A 7.50%(USD 5 Year Swap rate + 4.598%) (c) (d) (e) |

30,000 |

33,713 |

|||||||||

|

6.25%(USD 5 Year Swap rate + 3.455%) (c) (d) (e) |

7,000 |

7,614 |

|||||||||

16 OAKMARK FUNDS

Oakmark Equity and Income Fund December 31, 2019 (Unaudited)

Schedule of Investments (in thousands) (continued)

|

Par Value |

Value |

||||||||||

|

FIXED INCOME - 29.3% (continued) |

|||||||||||

|

CORPORATE BONDS - 18.0% (continued) |

|||||||||||

|

Credit Suisse Group Funding Guernsey, Ltd. 3.125%, due 12/10/20 |

$ |

25,000 |

$ |

25,223 |

|||||||

|

3.80%, due 06/09/23 |

14,750 |

15,444 |

|||||||||

|

E*TRADE Financial Corp. 2.95%, due 08/24/22 |

11,965 |

12,190 |

|||||||||

|

3.80%, due 08/24/27 |

4,975 |

5,173 |

|||||||||

|

JPMorgan Chase & Co. 2.972%, due 01/15/23 |

29,765 |

30,328 |

|||||||||

|

3.514%(3 mo. USD LIBOR + 0.610%), due 06/18/22 (c) |

24,870 |

25,409 |

|||||||||

|

3.166%(3 mo. USD LIBOR + 1.230%), due 10/24/23 (c) |

19,910 |

20,249 |

|||||||||

|

Moody's Corp. 4.50%, due 09/01/22 |

13,040 |

13,789 |

|||||||||

|

2.625%, due 01/15/23 |

12,201 |

12,386 |

|||||||||

|

MSCI, Inc., 144A 5.25%, due 11/15/24 (d) |

9,311 |

9,566 |

|||||||||

|

5.375%, due 05/15/27 (d) |

6,965 |

7,505 |

|||||||||

|

4.75%, due 08/01/26 (d) |

5,925 |

6,206 |

|||||||||

|

5.75%, due 08/15/25 (d) |

2,950 |

3,094 |

|||||||||

|

Principal Life Global Funding II, 144A 2.15%, due 01/10/20 (d) |

19,910 |

19,909 |

|||||||||

|

2.375%, due 11/21/21 (d) |

6,970 |

7,010 |

|||||||||

|

Reinsurance Group of America, Inc. 3.95%, due 09/15/26 |

4,905 |

5,205 |

|||||||||

|

S&P Global, Inc. 4.00%, due 06/15/25 |

17,150 |

18,656 |

|||||||||

|

2.95%, due 01/22/27 |

9,810 |

10,134 |

|||||||||

|

4.40%, due 02/15/26 |

1,970 |

2,185 |

|||||||||

|

The Charles Schwab Corp. 3.25%, due 05/21/21 |

19,895 |

20,283 |

|||||||||

|

The Goldman Sachs Group, Inc. 2.35%, due 11/15/21 |

14,616 |

14,674 |

|||||||||

|

3.20%, due 02/23/23 |

7,000 |

7,197 |

|||||||||

|

3.686%(3 mo. USD LIBOR + 1.750%), due 10/28/27 (c) |

2,975 |

3,103 |

|||||||||

|

2.625%, due 04/25/21 |

2,000 |

2,018 |

|||||||||

|

2.875%, due 02/25/21 |

1,000 |

1,010 |

|||||||||

|

Wells Fargo & Co. 3.069%, due 01/24/23 |

14,930 |

15,238 |

|||||||||

|

3.157%(3 mo. USD LIBOR + 1.230%), due 10/31/23 (c) |

8,603 |

8,756 |

|||||||||

|

Wells Fargo Bank NA 3.625%, due 10/22/21 |

10,000 |

10,292 |

|||||||||

|

485,571 |

|||||||||||

|

INDUSTRIALS - 1.9% |

|||||||||||

|

Bacardi, Ltd., 144A 4.45%, due 05/15/25 (d) |

14,900 |

16,069 |

|||||||||

|

BAT Capital Corp. 3.557%, due 08/15/27 |

6,965 |

7,111 |

|||||||||

|

Delta Air Lines, Inc. 3.40%, due 04/19/21 |

11,590 |

11,750 |

|||||||||

|

3.80%, due 04/19/23 |

9,425 |

9,780 |

|||||||||

|

Fortune Brands Home & Security, Inc. 4.00%, due 06/15/25 |

13,430 |

14,394 |

|||||||||

|

4.00%, due 09/21/23 |

9,945 |

10,510 |

|||||||||

|

Par Value |

Value |

||||||||||

|

Hilton Domestic Operating Co., Inc. 5.125%, due 05/01/26 |

$ |

16,915 |

$ |

17,803 |

|||||||

|

Southwest Airlines Co. 2.65%, due 11/05/20 |

12,148 |

12,213 |

|||||||||

|

Stanley Black & Decker, Inc. 4.25%, due 11/15/28 |

6,965 |