OAKMARK FUNDS

THIRD QUARTER REPORT | JUNE 30, 2018

OAKMARK FUND

OAKMARK SELECT FUND

OAKMARK EQUITY AND INCOME FUND

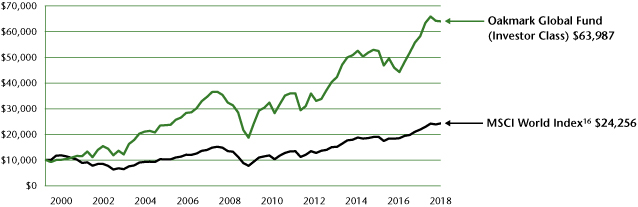

OAKMARK GLOBAL FUND

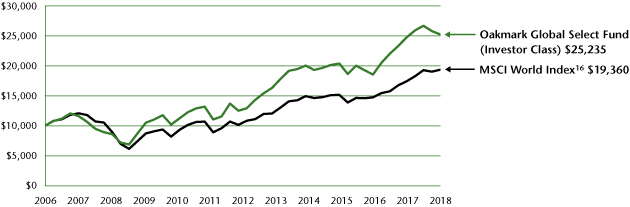

OAKMARK GLOBAL SELECT FUND

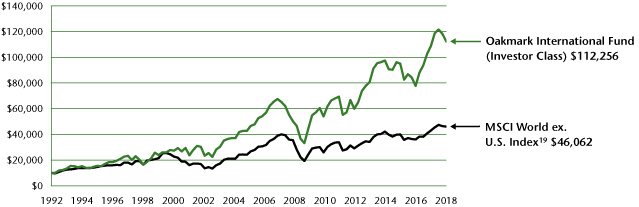

OAKMARK INTERNATIONAL FUND

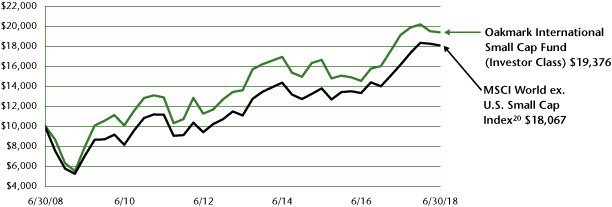

OAKMARK INTERNATIONAL SMALL CAP FUND

Oakmark Funds

2018 Third Quarter Report

TABLE OF CONTENTS

|

Commentary on Oakmark and Oakmark Select Funds |

1 |

||||||

|

Oakmark Fund |

|||||||

|

Summary Information |

4 |

||||||

|

Portfolio Manager Commentary |

5 |

||||||

|

Schedule of Investments |

6 |

||||||

|

Oakmark Select Fund |

|||||||

|

Summary Information |

10 |

||||||

|

Portfolio Manager Commentary |

11 |

||||||

|

Schedule of Investments |

12 |

||||||

|

Oakmark Equity and Income Fund |

|||||||

|

Summary Information |

14 |

||||||

|

Portfolio Manager Commentary |

15 |

||||||

|

Schedule of Investments |

17 |

||||||

|

Oakmark Global Fund |

|||||||

|

Summary Information |

24 |

||||||

|

Portfolio Manager Commentary |

25 |

||||||

|

Schedule of Investments |

27 |

||||||

|

Oakmark Global Select Fund |

|||||||

|

Summary Information |

30 |

||||||

|

Portfolio Manager Commentary |

31 |

||||||

|

Schedule of Investments |

32 |

||||||

|

Commentary on Oakmark International and Oakmark International Small Cap Funds |

34 |

||||||

|

Oakmark International Fund |

|||||||

|

Summary Information |

36 |

||||||

|

Portfolio Manager Commentary |

37 |

||||||

|

Schedule of Investments |

38 |

||||||

|

Oakmark International Small Cap Fund |

|||||||

|

Summary Information |

42 |

||||||

|

Portfolio Manager Commentary |

43 |

||||||

|

Schedule of Investments |

44 |

||||||

|

Disclosures and Endnotes |

47 |

||||||

|

Trustees and Officers |

49 |

||||||

FORWARD-LOOKING STATEMENT DISCLOSURE

One of our most important responsibilities as mutual fund managers is to communicate with shareholders in an open and direct manner. Some of our comments in our letters to shareholders are based on current management expectations and are considered "forward-looking statements." Actual future results, however, may prove to be different from our expectations. You can identify forward-looking statements by words such as "estimate", "may", "will", "expect", "believe",

"plan" and other similar terms. We cannot promise future returns. Our opinions are a reflection of our best judgment at the time this report is compiled, and we disclaim any obligation to update or alter forward-looking statements as a result of new information, future events, or otherwise.

Oakmark.com

Oakmark and Oakmark Select Funds June 30, 2018

Portfolio Manager Commentary

William C. Nygren, CFA

Portfolio Manager

oakmx@oakmark.com

oaklx@oakmark.com

oakwx@oakmark.com

At Oakmark, we are long-term investors. We attempt to identify growing businesses that are managed to benefit their shareholders. We will purchase stock in those businesses only when priced substantially below our estimate of intrinsic value. After purchase, we patiently wait for the gap between stock price and intrinsic value to close.

"My own thinking has changed drastically from 35 years ago when I was taught to favor tangible assets and to shun businesses whose value depended largely on economic goodwill."

-Warren Buffett1

If you were paging through Value Line2 in February looking for cheap stocks, it would have been easy to skip right past Gartner. Value Line says, "Gartner Inc. is the world's leading information technology research and advisory company..." You would have quickly seen that it is a database-driven, asset-light business that would be expected to command a higher than market P/E ratio.3 Despite the stock falling from $142 to $119, its P/E was still 31 times expected 2018 earnings and its book value was only $2 per share. Gartner didn't look like a value stock and, in fact, it was even included in the Russell 1000 Growth Index.4 But last quarter we bought it for the Oakmark Fund. So, it's fair to ask: has Oakmark changed, or does Gartner somehow meet our value criteria?

A closer look reveals that Gartner stock fell when management opted to substantially increase selling and marketing expenses to pursue accelerated organic growth, which in turn decreased the company's reported earnings. The way GAAP (generally accepted accounting principles) works, because the future benefit of a marketing expense is uncertain, the cost is immediately expensed. But at a company like Gartner, these marketing expenses could easily be seen as long-term investments in company growth. That's because a Gartner customer tends to remain with the company for a long time—a little more than six years, on average. So we adjusted the sales and marketing expenses to reflect a six-year life, just like GAAP would treat the purchase of a machine that was expected to last six years. With that one adjustment, Gartner's expected EPS5 increased by almost $3. Using our adjusted earnings, which we believe reflect a more realistic view of those intangible assets, Gartner appears to be priced as just an ordinary company. And, as we have said many times, buying an extraordinary company at an ordinary price is value investing at its finest.

Throughout Oakmark's history, we've been on the lookout for situations where GAAP obscures economic value. Though value investing has always implied buying at a discount to value, the early descriptions of value relied more on assets than earnings. In 1934, Ben Graham and David Dodd wrote Security Analysis,6 which was quickly adopted as the Bible of value investing. In it, Graham explains his idea of only investing when he had a "margin of safety:" he only purchases a stock when it is priced at a large discount to a company's intrinsic value. The concept remains a core principle of value investing today, even though the idea is almost 100 years old. Then, influenced by just having been through a depression, a company's intrinsic value was defined as its liquidation value, and Graham proposed the following formula for computing it: start with cash; add accounts

receivables, discounted by 10-25%; add inventory, discounted by 25-50%; add all other assets, discounted by 50-100%; and then deduct all liabilities. A stock passed his margin of safety test only if it sold for a large discount to this estimated liquidation value.

Over the next 40 years, stock prices were generally quite tightly tied to their book values and patient investors could often find companies that were out of favor, trading below estimated liquidation value. It was an asset-heavy economy, which made it appropriate to value businesses based on their tangible assets. In fact, as recently as 1975, 83% of the stock market value of the average company was represented by its tangible book value. In an economy where value was derived from fixed assets, it was hard to maintain competitive advantage: If you earned unusually high returns, others would duplicate your fixed assets and your advantage disappeared. That made it difficult for companies temporarily trading at large premiums to book value to sustain their high stock prices. So, an effective investment approach was to buy the stocks priced at discounts to book value and then patiently wait for reversion to the mean.

But, as the economy has become more asset-light, intangible assets—such as brand names, customer lists, R&D spending and patents—have become more important. Today, the relative importance of tangible assets compared to intangibles has completely flip-flopped from what it was 40 years ago. Intangibles now account for over 80% of the average company's market value. But much like Graham, GAAP doesn't even attempt to value those assets.

By the early 1980s, the Berkshire Hathaway investment portfolio, managed by Warren Buffett, looked nothing like the low price-to-book investments favored by his teacher Ben Graham. The portfolio included General Foods, RJ Reynolds, Time Inc. and Washington Post Co. When asked about the apparently high prices he paid for those companies relative to their book value, Buffett was fond of saying that their most valuable assets—their brand names—were not even on their balance sheets. The Buffett quote above, citing the decreasing importance of tangible assets in determining business value, sounds as timely today as it did when it appeared in Berkshire's 1983 Annual Report. What Buffett figured out earlier than most value investors was that conservative accounting rules overlooked the value of intangible assets. In turn, book value didn't fully reflect the economic value of businesses with strong brands.

For companies in the S&P 5007 today, the correlation between stock price and tangible book value has become quite small, just 14%. This is a very big change from 25 years ago, when that correlation was 71%—or 5x stronger than it is now. Unlike 25 years ago, knowing the book value of a company today gives little clue as to its stock price. Investors who have relied primarily on a price-to-book mean reversion strategy have had disappointing performance for the past decade. Some even feel

See accompanying Disclosures and Endnotes on page 47.

Oakmark.com 1

Oakmark and Oakmark Select Funds June 30, 2018

Portfolio Manager Commentary (continued)

they "are due" for an extended positive run. That would indeed be the case if irrational exuberance were the reason that book value is currently disconnected from stock prices.

But we don't see anything irrational about it. If book value still determined earnings power, we would expect P/E ratios to be as widely distributed as price-to-book ratios. However, that isn't the case. Today, the P/E distribution is narrower than it was 25 years ago. That shows that intangible assets are producing earnings and, therefore, investors have been acting rationally by attributing significant value to them. At Oakmark, we believe that the relative importance of intangible assets is more likely to continue than to reverse. As such, we think a portfolio of strictly low price-to-book stocks will continue to produce disappointing results.

Most value investors have come to realize that although book value can still be a useful metric in certain situations, such as analyzing a bank or a utility, it does not offer much insight for most companies. For this reason, book value is no longer used by most investors as a definitive indicator of economic value. Despite that, in our view, many investors have not yet considered what this means for the income statement. Back when GAAP book value was still closely tied to economic value, a company's annual income statement provided a pretty good approximation of the economic value added in that year. But now that economic value is not closely tied to book value, the income statement no longer provides a reliable indication of the value a company created in a particular year.

Since Oakmark's 1991 inception, we have sought out investments whose economic value was not easily seen in the simple GAAP metrics of net income and book value. Over that time, like Buffett, we've owned a lot of packaged food companies when we thought increased brand advertising was understating earnings. (Interestingly, the opposite condition is present today: Some companies have slashed advertising, increasing their GAAP earnings, but still benefit from historical spending that was previously expensed.) We owned cable TV distributors that reported net losses and negative book value while rapidly increasing their subscribers. (As with Gartner, customer acquisition costs were an immediate hit to their income, but their customers were long-lived.) We owned high-growth biotech companies that were selling at lower P/Es than mature pharmaceutical companies—once we treated their R&D expenditures as long-term investments.

As intangibles have grown in importance, so has the number of our holdings for which we adjust earnings to better reflect our view of intangible values. That has led Oakmark to invest in more companies generally owned by growth investors, such as Alphabet, Facebook, Gartner, Netflix and Regeneron. The thought process is no different than what led us to own food and cable stocks early in Oakmark's life. Today, it simply applies to more companies.

Regardless of the changing metrics that determine a company's value, the main concepts of value investing are the same today as 84 years ago when Security Analysis was first published:

-Investors still follow fads, get emotional and overreact,

-Which means stock prices sometimes decouple from intrinsic value,

-Allowing patient investors to invest when price is below value,

-Which creates a margin of safety.

So how can investors today determine which mutual funds are rigorously applying a disciplined value investing process and which ones are simply following trends? The relevant metrics for that have evolved, too. Because we rarely find price-to-book a useful statistic for estimating intrinsic value, our portfolios often don't look cheap on that metric. Low P/E ratios are frequently, but certainly not always, an indication of value. Though our portfolios still typically have a lower P/E than the market, we are more frequently investing in "exceptions" where the GAAP P/E looks expensive.

For those "exceptions," true value investors should be able to explain how they're calculating their margin of safety: What are they getting that they don't think they're paying for? As an example, let's look at the largest holding in both Oakmark and Oakmark Select, Alphabet, a stock that is primarily owned by growth managers. Alphabet's 2018 P/E is 26 times consensus estimates, which to us seems to be in the right ballpark given the expected growth from its search business. However, the company's $115 billion in cash, YouTube and other bets (including Waymo), in total, contribute nothing to our estimate of current earnings, despite having tremendous value. That's what we're getting for free, which creates our margin of safety.

At Oakmark, we commit time to writing these pieces because we want to help our shareholders understand how we think about investing. In a world where business value rests primarily on intangible assets, it's getting harder to use a style box to understand a mutual fund's investment approach. That's why it's more important than ever to spend time reading commentaries or watching interviews. They can explain a fund's investment philosophy far better than a price-to-book ratio ever will.

See accompanying Disclosures and Endnotes on page 47.

2 OAKMARK FUNDS

This page intentionally left blank.

Oakmark.com 3

Oakmark Fund June 30, 2018

Summary Information

VALUE OF A $10,000 INVESTMENT

Since Inception - 08/05/91 (Unaudited)

PERFORMANCE

|

Average Annual Total Returns (as of 06/30/18) |

|||||||||||||||||||||||||||||||

| (Unaudited) |

Total Return Last 3 Months |

1-year |

3-year |

5-year |

10-year |

Since Inception |

Inception Date |

||||||||||||||||||||||||

|

Oakmark Fund (Investor Class) |

2.13 |

% |

13.46 |

% |

11.82 |

% |

13.07 |

% |

12.48 |

% |

12.84 |

% |

08/05/91 |

||||||||||||||||||

|

S&P 500 Index |

3.43 |

% |

14.37 |

% |

11.93 |

% |

13.42 |

% |

10.17 |

% |

9.76 |

% |

|||||||||||||||||||

|

Dow Jones Industrial Average8 |

1.26 |

% |

16.31 |

% |

14.07 |

% |

12.96 |

% |

10.78 |

% |

10.70 |

% |

|||||||||||||||||||

|

Lipper Large-Cap Value Fund Index9 |

1.89 |

% |

9.25 |

% |

8.95 |

% |

10.60 |

% |

8.26 |

% |

8.87 |

% |

|||||||||||||||||||

|

Oakmark Fund (Advisor Class) |

2.16 |

% |

13.60 |

% |

N/A |

N/A |

N/A |

15.08 |

% |

11/30/16 |

|||||||||||||||||||||

|

Oakmark Fund (Institutional Class) |

2.18 |

% |

13.64 |

% |

N/A |

N/A |

N/A |

15.10 |

% |

11/30/16 |

|||||||||||||||||||||

|

Oakmark Fund (Service Class) |

2.07 |

% |

13.15 |

% |

11.49 |

% |

12.71 |

% |

12.15 |

% |

8.49 |

% |

04/05/01 |

||||||||||||||||||

The graph and table above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Past performance is no guarantee of future results. The performance data quoted represents past performance. Current performance may be lower or higher than the performance data quoted. Total return includes change in share prices and, in each case, includes reinvestment of dividends and capital gain distributions. The investment return and principal value vary so that an investor's shares when redeemed may be worth more or less than the original cost. To obtain the most recent month-end performance, please visit Oakmark.com.

|

TOP TEN EQUITY HOLDINGS10 |

% of Net Assets | ||||||

|

Citigroup, Inc. |

3.1 |

||||||

|

Alphabet Inc., Class C |

3.0 |

||||||

|

American International Group, Inc. |

2.5 |

||||||

|

Apple, Inc. |

2.5 |

||||||

|

Fiat Chrysler Automobiles N.V. |

2.5 |

||||||

|

Netflix, Inc. |

2.5 |

||||||

|

Bank of America Corp. |

2.5 |

||||||

|

CVS Health Corp. |

2.5 |

||||||

|

General Electric Co. |

2.3 |

||||||

|

Ally Financial, Inc. |

2.2 |

||||||

|

FUND STATISTICS |

|||||||

|

Ticker* |

OAKMX |

||||||

|

Number of Equity Holdings |

56 |

||||||

|

Net Assets |

$20.5 billion | ||||||

|

Weighted Average Market Cap |

$148.5 billion | ||||||

|

Median Market Cap |

$57.3 billion | ||||||

|

Gross Expense Ratio - Investor Class (as of 09/30/17)* |

0.90% | ||||||

|

Net Expense Ratio - Investor Class (as of 09/30/17)*† |

0.86% | ||||||

* This information is related to the Investor Class. Please visit Oakmark.com for information related to the Advisor, Institutional and Service Classes.

† The net expense ratio reflects a contractual advisory fee waiver agreement through January 28, 2019.

|

SECTOR ALLOCATION |

% of Net Assets | ||||||

|

Information Technology |

22.8 |

||||||

|

Financials |

22.4 |

||||||

|

Consumer Discretionary |

16.5 |

||||||

|

Health Care |

13.4 |

||||||

|

Industrials |

8.4 |

||||||

|

Consumer Staples |

5.9 |

||||||

|

Energy |

5.7 |

||||||

|

Short-Term Investments and Other |

4.9 |

||||||

See accompanying Disclosures and Endnotes on page 47.

4 OAKMARK FUNDS

Oakmark Fund June 30, 2018

Portfolio Manager Commentary

William C. Nygren, CFA

Portfolio Manager

oakmx@oakmark.com

Kevin Grant, CFA

Portfolio Manager

oakmx@oakmark.com

The Oakmark Fund increased 2.1% for the second quarter, which lagged behind the 3.4% gain for the S&P 500,7 the Fund's benchmark. Rapid corporate earnings growth, combined with stagnant share prices since the beginning of the calendar year, has brought broad market valuation multiples back down to historical levels. We believe equities remain the most attractive asset class, and due to the increased number of undervalued companies with misunderstood intangible assets (see Bill Nygren's market commentary), our research team has produced an impressive number of new investment ideas. The Oakmark Fund has added 10 new names to the portfolio over the past four quarters.

The Oakmark Fund's best contributing sectors during the second quarter were information technology (with double-digit gains from ADP, MasterCard, Apple, Visa, Facebook and Gartner) and energy (helped by rising commodity prices and improving asset productivity). Our lowest contributing sectors were industrials and financials. The Fund's best contributing individual securities were Netflix and Anadarko, both up over 20%, and the worst contributing securities were American Airlines and MGM Resorts International, down 27% and 17%, respectively. American Airlines was weak due to near-term profitability concerns, following a period of rapidly rising fuel costs. During the quarter, we added new positions in Bristol-Myers Squibb Company, Gartner and Hilton Worldwide Holdings. We eliminated our position in Aflac as the share price approached our estimate of intrinsic value, and we eliminated our position in Harley-Davidson due to deteriorating demand and profitability trends.

Bristol-Myers Squibb Company (BMY-$55)

Bristol-Myers Squibb is a global biopharmaceutical company with leading franchises in oncology, immunoscience and cardiovascular drugs. Long-time shareholders may recall a successful Bristol-Myers Squibb investment that we sold in 2013. We got another opportunity to own this company during the past quarter when investors became fearful that a competing drug would take share in the cancer market. We believe these fears are overstated because cancer remains a dangerous disease that is difficult to treat. The company's two most valuable drugs Opdivo and Yervoy should continue to grow revenue as they maintain effectiveness with new tumor types. Bristol Myers Squibb also has the most new molecular agents and the highest number of combinations of agents in trials. Moreover, the company's R&D and marketing prowess also make it a desired partner for promising academic and small biotech innovators. Collectively, these assets should assure Bristol-Myers Squibb's oncology leadership for many years. We believe intrinsic value is closer to the $70 level it traded for earlier this year than its more recent price in the low $50s.

Gartner, Inc. (IT-$133)

Gartner is the world's leading provider of information technology research and advice for information technology executives. The company's research reports and benchmarking data are used by information technology executives across industries to make mission-critical decisions with potential multi-million dollar ramifications, and the subscription price represents just a fraction of the typical information technology budget. In other words, Gartner is the Consumer Reports of the information technology industry. However, while the Gartner brand has been among the most recognizable in information technology research for more than 35 years, most sizeable enterprises are still not Gartner subscribers. The company is investing heavily in sales and marketing to grow its customer base and based on the excellent long-term track record of Gartner management, we believe these investments are likely to drive years of double-digit growth. While the company trades at a high multiple of GAAP earnings, that multiple falls significantly after adjusting sales and marketing expenses to account for the multi-year life of new customers. (See Bill Nygren's market commentary). On our adjusted earnings estimates, Gartner's price-to-earnings ratio is in line with the S&P 500. We believe this is a bargain price for a high-return, high-growth business with an excellent management team.

Hilton Worldwide Holdings Inc. (HLT-$79)

Hilton Worldwide is a high-quality, well-managed company that was the target of a successful leveraged buyout by Blackstone in 2007. We believe the company's transformation into an asset-light, fee-driven business with a more resilient earnings profile is underappreciated. After spinning off most of the company's owned hotels and timeshare businesses early last year, Hilton now generates over 90% of its profits from fees (requiring minimal capital investment) and produces substantial free cash flow (greater than 100% of net income). The company should generate high single-digit operating income growth for several years. We became interested in Hilton after we determined that its competitive moat is widening. The company's unit growth leads the industry and its global pipeline share is almost 22%—over four times larger than its current share of existing rooms (approximately 5%). We initiated our position at a particularly attractive price due to the temporary pressure created by HNA's sale of its 26% stake in the company for non-fundamental reasons.

See accompanying Disclosures and Endnotes on page 47.

Oakmark.com 5

Oakmark Fund June 30, 2018 (Unaudited)

Schedule of Investments (in thousands)

|

Shares |

Value |

||||||||||

|

COMMON STOCKS - 95.1% |

|||||||||||

|

INFORMATION TECHNOLOGY - 22.8% |

|||||||||||

|

SOFTWARE & SERVICES - 14.3% |

|||||||||||

|

Alphabet, Inc., Class C (a) |

558 |

$ |

622,818 |

||||||||

|

MasterCard, Inc., Class A |

2,320 |

455,926 |

|||||||||

|

Visa, Inc., Class A |

3,435 |

454,966 |

|||||||||

|

Automatic Data Processing, Inc. |

3,320 |

445,345 |

|||||||||

|

Oracle Corp. |

8,765 |

386,186 |

|||||||||

|

Facebook, Inc., Class A (a) |

1,200 |

233,184 |

|||||||||

|

Gartner, Inc. (a) |

1,600 |

212,640 |

|||||||||

|

Alphabet, Inc., Class A (a) |

93 |

105,120 |

|||||||||

|

2,916,185 |

|||||||||||

|

TECHNOLOGY HARDWARE & EQUIPMENT - 5.4% |

|||||||||||

|

Apple, Inc. |

2,787 |

515,902 |

|||||||||

|

TE Connectivity, Ltd. |

4,936 |

444,504 |

|||||||||

|

Flex, Ltd. (a) |

10,000 |

141,100 |

|||||||||

|

1,101,506 |

|||||||||||

|

SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT - 3.1% |

|||||||||||

|

Intel Corp. |

6,755 |

335,791 |

|||||||||

|

Texas Instruments, Inc. |

2,720 |

299,880 |

|||||||||

|

635,671 |

|||||||||||

|

4,653,362 |

|||||||||||

|

FINANCIALS - 22.4% |

|||||||||||

|

DIVERSIFIED FINANCIALS - 10.9% |

|||||||||||

|

Ally Financial, Inc. |

17,435 |

458,017 |

|||||||||

|

Capital One Financial Corp. |

4,963 |

456,081 |

|||||||||

|

State Street Corp. |

4,700 |

437,523 |

|||||||||

|

The Bank of New York Mellon Corp. |

6,320 |

340,818 |

|||||||||

|

Moody's Corp. |

1,706 |

291,056 |

|||||||||

|

The Goldman Sachs Group, Inc. |

1,105 |

243,730 |

|||||||||

|

2,227,225 |

|||||||||||

|

BANKS - 7.7% |

|||||||||||

|

Citigroup, Inc. |

9,530 |

637,748 |

|||||||||

|

Bank of America Corp. |

18,000 |

507,420 |

|||||||||

|

Wells Fargo & Co. |

7,910 |

438,530 |

|||||||||

|

1,583,698 |

|||||||||||

|

INSURANCE - 3.8% |

|||||||||||

|

American International Group, Inc. |

9,780 |

518,536 |

|||||||||

|

Aon PLC |

1,890 |

259,251 |

|||||||||

|

777,787 |

|||||||||||

|

4,588,710 |

|||||||||||

|

CONSUMER DISCRETIONARY - 16.5% |

|||||||||||

|

AUTOMOBILES & COMPONENTS - 5.0% |

|||||||||||

|

Fiat Chrysler Automobiles N.V. |

27,276 |

515,251 |

|||||||||

|

General Motors Co. |

6,850 |

269,890 |

|||||||||

|

Aptiv PLC |

2,200 |

201,586 |

|||||||||

|

Delphi Technologies PLC |

733 |

33,337 |

|||||||||

|

1,020,064 |

|||||||||||

|

Shares |

Value |

||||||||||

|

MEDIA - 4.9% |

|||||||||||

|

Charter Communications, Inc., Class A (a) |

1,300 |

$ |

381,173 |

||||||||

|

Comcast Corp., Class A |

11,438 |

375,294 |

|||||||||

|

News Corp., Class A |

15,401 |

238,711 |

|||||||||

|

995,178 |

|||||||||||

|

RETAILING - 4.8% |

|||||||||||

|

Netflix, Inc. (a) |

1,300 |

508,859 |

|||||||||

|

Qurate Retail, Inc. (a) |

12,115 |

257,089 |

|||||||||

|

Booking Holdings, Inc. (a) |

110 |

222,980 |

|||||||||

|

988,928 |

|||||||||||

|

CONSUMER SERVICES - 1.8% |

|||||||||||

|

MGM Resorts International |

9,400 |

272,882 |

|||||||||

|

Hilton Worldwide Holdings, Inc. |

1,279 |

101,254 |

|||||||||

|

374,136 |

|||||||||||

|

3,378,306 |

|||||||||||

|

HEALTH CARE - 13.4% |

|||||||||||

|

HEALTH CARE EQUIPMENT & SERVICES - 9.5% |

|||||||||||

|

CVS Health Corp. |

7,865 |

506,115 |

|||||||||

|

HCA Healthcare, Inc. |

4,316 |

442,770 |

|||||||||

|

Baxter International, Inc. |

5,300 |

391,352 |

|||||||||

|

UnitedHealth Group, Inc. |

1,345 |

329,982 |

|||||||||

|

Medtronic PLC |

3,190 |

273,096 |

|||||||||

|

1,943,315 |

|||||||||||

|

PHARMACEUTICALS, BIOTECHNOLOGY & LIFE SCIENCES - 3.9% |

|||||||||||

|

Regeneron Pharmaceuticals, Inc. (a) |

1,262 |

435,307 |

|||||||||

|

Bristol-Myers Squibb Co. |

6,500 |

359,710 |

|||||||||

|

795,017 |

|||||||||||

|

2,738,332 |

|||||||||||

|

INDUSTRIALS - 8.4% |

|||||||||||

|

CAPITAL GOODS - 5.7% |

|||||||||||

|

General Electric Co. |

34,050 |

463,420 |

|||||||||

|

Parker-Hannifin Corp. |

2,439 |

380,159 |

|||||||||

|

Cummins, Inc. |

1,520 |

202,160 |

|||||||||

|

Caterpillar, Inc. |

850 |

115,319 |

|||||||||

|

1,161,058 |

|||||||||||

|

TRANSPORTATION - 2.7% |

|||||||||||

|

American Airlines Group, Inc. |

7,700 |

292,292 |

|||||||||

|

FedEx Corp. |

1,130 |

256,578 |

|||||||||

|

548,870 |

|||||||||||

|

1,709,928 |

|||||||||||

|

CONSUMER STAPLES - 5.9% |

|||||||||||

|

FOOD, BEVERAGE & TOBACCO - 4.0% |

|||||||||||

|

Diageo PLC (b) |

3,000 |

432,030 |

|||||||||

|

Nestlé SA (b) |

4,965 |

384,440 |

|||||||||

|

816,470 |

|||||||||||

|

HOUSEHOLD & PERSONAL PRODUCTS - 1.9% |

|||||||||||

|

Unilever PLC (b) |

7,163 |

395,971 |

|||||||||

|

1,212,441 |

|||||||||||

6 OAKMARK FUNDS

Oakmark Fund June 30, 2018 (Unaudited)

Schedule of Investments (in thousands) (continued)

|

Shares |

Value |

||||||||||

|

COMMON STOCKS - 95.1% (continued) |

|||||||||||

|

ENERGY - 5.7% |

|||||||||||

|

Anadarko Petroleum Corp. |

5,600 |

$ |

410,200 |

||||||||

|

Apache Corp. |

8,540 |

399,240 |

|||||||||

|

National Oilwell Varco, Inc. |

5,929 |

257,314 |

|||||||||

|

Chesapeake Energy Corp. (a) |

20,000 |

104,800 |

|||||||||

|

1,171,554 |

|||||||||||

|

TOTAL COMMON STOCKS - 95.1% (COST $12,253,097) |

19,452,633 |

||||||||||

|

Par Value |

Value |

||||||||||

|

SHORT-TERM INVESTMENTS - 5.5% |

|||||||||||

|

U.S. GOVERNMENT BILL - 3.9% |

|||||||||||

|

United States Treasury Bills, 1.84% - 1.88%, due 07/26/18 - 08/23/18 (c) (Cost $798,381) |

$ |

800,000 |

798,381 |

||||||||

|

GOVERNMENT AND AGENCY SECURITIES - 1.2% |

|||||||||||

|

Federal National Mortgage Association, 1.78%, due 07/02/18 (c) (Cost $249,988) |

250,000 |

249,988 |

|||||||||

|

REPURCHASE AGREEMENT - 0.4% |

|||||||||||

|

Fixed Income Clearing Corp. Repurchase Agreement, 1.10% dated 06/29/18 due 07/02/18, repurchase price $86,996, collateralized by a Federal Home Loan Bank Bond, 2.150% due 02/14/20, value plus accrued interest of $88,733 (Cost: $86,988) |

86,988 |

86,988 |

|||||||||

|

TOTAL SHORT-TERM INVESTMENTS - 5.5% (COST $1,135,357) |

1,135,357 |

||||||||||

|

TOTAL INVESTMENTS - 100.6% (COST $13,388,454) |

20,587,990 |

||||||||||

|

Foreign Currencies (Cost $0) - 0.0% (d) |

0 |

(e) |

|||||||||

|

Liabilities In Excess of Other Assets - (0.6)% |

(122,230 |

) |

|||||||||

|

TOTAL NET ASSETS - 100.0% |

$ |

20,465,760 |

|||||||||

(a) Non-income producing security

(b) Sponsored American Depositary Receipt

(c) The rate shown represents the annualized yield at the time of purchase; not a coupon rate.

(d) Amount rounds to less than 0.1%.

(e) Amount rounds to less than $1,000.

Oakmark.com 7

Oakmark Fund June 30, 2018 (Unaudited)

Schedule of Investments (in thousands) (continued)

WRITTEN OPTIONS

|

Description |

Counterparty |

Exercise Price |

Expiration Date |

Number of Contracts |

Notional Amount |

Market Value |

Premiums Received by Fund |

Unrealized Gain/(Loss) |

|||||||||||||||||||||||||||

|

CALLS |

|||||||||||||||||||||||||||||||||||

|

Netflix, Inc. |

Pershing LLC |

$ |

350.00 |

9/21/2018 |

1,000 |

$ |

(39,143 |

) |

$ |

(5,983 |

) |

$ |

3,254 |

$ |

(2,729 |

) |

|||||||||||||||||||

8 OAKMARK FUNDS

This page intentionally left blank.

Oakmark.com 9

Oakmark Select Fund June 30, 2018

Summary Information

VALUE OF A $10,000 INVESTMENT

Since Inception - 11/01/96 (Unaudited)

PERFORMANCE

|

Average Annual Total Returns (as of 06/30/18) |

|||||||||||||||||||||||||||||||

| (Unaudited) |

Total Return Last 3 Months |

1-year |

3-year |

5-year |

10-year |

Since Inception |

Inception Date |

||||||||||||||||||||||||

|

Oakmark Select Fund (Investor Class) |

-0.41 |

% |

5.55 |

% |

7.58 |

% |

11.13 |

% |

11.94 |

% |

12.40 |

% |

11/01/96 |

||||||||||||||||||

|

S&P 500 Index |

3.43 |

% |

14.37 |

% |

11.93 |

% |

13.42 |

% |

10.17 |

% |

8.46 |

% |

|||||||||||||||||||

|

Lipper Multi-Cap Value Fund Index11 |

1.03 |

% |

7.15 |

% |

7.08 |

% |

9.68 |

% |

7.91 |

% |

7.61 |

% |

|||||||||||||||||||

|

Oakmark Select Fund (Advisor Class) |

-0.37 |

% |

5.72 |

% |

N/A |

N/A |

N/A |

8.62 |

% |

11/30/16 |

|||||||||||||||||||||

|

Oakmark Select Fund (Institutional Class) |

-0.37 |

% |

5.75 |

% |

N/A |

N/A |

N/A |

8.64 |

% |

11/30/16 |

|||||||||||||||||||||

|

Oakmark Select Fund (Service Class) |

-0.53 |

% |

5.21 |

% |

7.22 |

% |

10.77 |

% |

11.62 |

% |

9.17 |

% |

12/31/99 |

||||||||||||||||||

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Past performance is no guarantee of future results. The performance data quoted represents past performance. Current performance may be lower or higher than the performance data quoted. Total return includes change in share prices and, in each case, includes reinvestment of dividends and capital gain distributions. The investment return and principal value vary so that an investor's shares when redeemed may be worth more or less than the original cost. To obtain the most recent month-end performance, please visit Oakmark.com.

|

TOP TEN EQUITY HOLDINGS10 |

% of Net Assets | ||||||

|

Alphabet, Inc., Class C |

8.2 |

||||||

|

CBRE Group, Inc., Class A |

7.3 |

||||||

|

TE Connectivity, Ltd. |

6.3 |

||||||

|

Citigroup, Inc. |

5.7 |

||||||

|

Fiat Chrysler Automobiles N.V. |

5.5 |

||||||

|

Ally Financial, Inc. |

5.0 |

||||||

|

Apache Corp. |

4.7 |

||||||

|

MasterCard, Inc., Class A |

4.7 |

||||||

|

American International Group, Inc. |

4.6 |

||||||

|

General Electric Co. |

4.1 |

||||||

|

FUND STATISTICS |

|||||||

|

Ticker* |

OAKLX |

||||||

|

Number of Equity Holdings |

22 |

||||||

|

Net Assets |

$6.0 billion | ||||||

|

Weighted Average Market Cap |

$138.4 billion | ||||||

|

Median Market Cap |

$34.4 billion | ||||||

|

Gross Expense Ratio - Investor Class (as of 09/30/17)* |

1.03% | ||||||

|

Net Expense Ratio - Investor Class (as of 09/30/17)*† |

0.96% | ||||||

* This information is related to the Investor Class. Please visit Oakmark.com for information related to the Advisor, Institutional and Service Classes.

† The net expense ratio reflects a contractual advisory fee waiver agreement through January 28, 2019.

|

SECTOR ALLOCATION |

% of Net Assets | ||||||

|

Information Technology |

24.4 |

||||||

|

Financials |

22.5 |

||||||

|

Consumer Discretionary |

19.2 |

||||||

|

Energy |

11.7 |

||||||

|

Real Estate |

7.3 |

||||||

|

Industrials |

7.2 |

||||||

|

Health Care |

3.4 |

||||||

|

Short-Term Investments and Other |

4.3 |

||||||

See accompanying Disclosures and Endnotes on page 47.

10 OAKMARK FUNDS

Oakmark Select Fund June 30, 2018

Portfolio Manager Commentary

William C. Nygren, CFA

Portfolio Manager

oaklx@oakmark.com

Anthony P. Coniaris, CFA

Portfolio Manager

oaklx@oakmark.com

Win Murray

Portfolio Manager

oaklx@oakmark.com

For the quarter, the Oakmark Select Fund declined 0.4%, compared to a 3.4% increase in the S&P 500 Index,7 the Fund's benchmark. Year to date, the Fund declined 4.3%, compared to a 2.7% increase for the S&P 500.

Most of this quarter's underperformance was driven by our consumer discretionary holdings, although the reasons for the decline of individual companies within that sector varied. The largest detractors were American Airlines (–27%), MGM Resorts (–17%) and Adient (–18%). American Airlines shares were hurt by rising oil prices, which we believe will only have a temporary impact on profits as the airline industry adjusts its prices and capacity throughout the rest of this year. During the quarter, MGM modestly lowered its annual profit forecast due to financial issues that we believe are temporary and somewhat immaterial, related to the renovation of the Monte Carlo Resort and a slow resumption of occupancy at the Mandalay Bay Resort, following the tragic shooting. Adient's fundamentals continue to be damaged by a non-core segment, its seating structures business, but its board is acting with appropriate urgency. On the positive side, the largest contributors to performance were Chesapeake Energy (+72%), Apache (+22%) and Weatherford (+46%). Whereas higher oil prices negatively impacted American Airlines, it was a distinct positive for our energy holdings.

We eliminated the final portion of our Harley-Davidson position for reasons discussed in last quarter's letter. We initiated a new position in Regeneron Pharmaceuticals—a biotech company with industry-leading research and development (R&D) productivity and a proven management team. The company is led by its founder Len Schleifer who maintains a culture focused on internal development of novel drugs. Schleifer also holds a significant equity stake in the company. Over the past decade, Regeneron has received approval for six drugs, all of which were developed in-house. Furthermore, Regeneron has a reputation for responsible drug pricing. Recent approvals of some of its new drugs provide a strong path for long-term growth. Meanwhile, its largest drug, Eylea, has additional opportunities for growth and retains patent protection through 2027. Regeneron spends significantly more on R&D than its peers, and, due to several recent drug launches, Regeneron's selling, general and administrative (SG&A) spending is relatively high, too. We believe Regeneron's R&D spending provides a great return on investment, and we

expect launch costs to normalize over time. Although the company's consensus P/E3 multiple appears high, if its R&D and SG&A costs are adjusted to average levels, Regeneron would trade at a low-teens P/E. We believe this is a compelling valuation for a growing business with a strong management team that is aligned with its shareholders.

Thank you, our fellow shareholders, for your continued investment in the Oakmark Select Fund.

See accompanying Disclosures and Endnotes on page 47.

Oakmark.com 11

Oakmark Select Fund June 30, 2018 (Unaudited)

Schedule of Investments (in thousands)

|

Shares |

Value |

||||||||||

|

COMMON STOCKS - 95.7% |

|||||||||||

|

INFORMATION TECHNOLOGY - 24.4% |

|||||||||||

|

SOFTWARE & SERVICES - 18.0% |

|||||||||||

|

Alphabet, Inc., Class C (a) |

444 |

$ |

494,958 |

||||||||

|

MasterCard, Inc., Class A |

1,439 |

282,792 |

|||||||||

|

Oracle Corp. |

5,167 |

227,658 |

|||||||||

|

Alphabet, Inc., Class A (a) |

73 |

82,514 |

|||||||||

|

1,087,922 |

|||||||||||

|

TECHNOLOGY HARDWARE & EQUIPMENT - 6.4% |

|||||||||||

|

TE Connectivity, Ltd. |

4,243 |

382,119 |

|||||||||

|

1,470,041 |

|||||||||||

|

FINANCIALS - 22.5% |

|||||||||||

|

BANKS - 9.4% |

|||||||||||

|

Citigroup, Inc. |

5,112 |

342,095 |

|||||||||

|

Bank of America Corp. |

8,001 |

225,537 |

|||||||||

|

567,632 |

|||||||||||

|

DIVERSIFIED FINANCIALS - 8.5% |

|||||||||||

|

Ally Financial, Inc. |

11,500 |

302,105 |

|||||||||

|

Capital One Financial Corp. |

2,285 |

209,982 |

|||||||||

|

512,087 |

|||||||||||

|

INSURANCE - 4.6% |

|||||||||||

|

American International Group, Inc. |

5,195 |

275,450 |

|||||||||

|

1,355,169 |

|||||||||||

|

CONSUMER DISCRETIONARY - 19.2% |

|||||||||||

|

AUTOMOBILES & COMPONENTS - 8.8% |

|||||||||||

|

Fiat Chrysler Automobiles N.V. |

17,434 |

329,330 |

|||||||||

|

Adient PLC |

4,116 |

202,453 |

|||||||||

|

531,783 |

|||||||||||

|

CONSUMER SERVICES - 3.6% |

|||||||||||

|

MGM Resorts International |

7,584 |

220,178 |

|||||||||

|

MEDIA - 3.5% |

|||||||||||

|

Charter Communications, Inc., Class A (a) |

720 |

211,111 |

|||||||||

|

RETAILING - 3.3% |

|||||||||||

|

Qurate Retail, Inc. (a) |

9,293 |

197,195 |

|||||||||

|

1,160,267 |

|||||||||||

|

ENERGY - 11.7% |

|||||||||||

|

Apache Corp. |

6,071 |

283,819 |

|||||||||

|

Chesapeake Energy Corp. (a) |

44,860 |

235,069 |

|||||||||

|

Weatherford International PLC (a) |

57,380 |

188,781 |

|||||||||

|

707,669 |

|||||||||||

|

REAL ESTATE - 7.3% |

|||||||||||

|

CBRE Group, Inc., Class A (a) |

9,248 |

441,476 |

|||||||||

|

INDUSTRIALS - 7.2% |

|||||||||||

|

CAPITAL GOODS - 4.2% |

|||||||||||

|

General Electric Co. |

18,268 |

248,627 |

|||||||||

|

Shares |

Value |

||||||||||

|

TRANSPORTATION - 3.0% |

|||||||||||

|

American Airlines Group, Inc. |

4,800 |

$ |

182,208 |

||||||||

|

430,835 |

|||||||||||

|

HEALTH CARE - 3.4% |

|||||||||||

|

PHARMACEUTICALS, BIOTECHNOLOGY & LIFE SCIENCES - 3.4% |

|||||||||||

|

Regeneron Pharmaceuticals, Inc. (a) |

600 |

206,994 |

|||||||||

|

TOTAL COMMON STOCKS - 95.7% (COST $3,894,470) |

5,772,451 |

||||||||||

|

Par Value |

Value |

||||||||||

|

SHORT-TERM INVESTMENTS - 4.2% |

|||||||||||

|

GOVERNMENT AND AGENCY SECURITIES - 3.3% |

|||||||||||

|

Federal National Mortgage Association, 1.78%, due 07/02/18 (b) (Cost $199,990) |

$ |

200,000 |

199,990 |

||||||||

|

REPURCHASE AGREEMENT - 0.9% |

|||||||||||

|

Fixed Income Clearing Corp. Repurchase Agreement, 1.10% dated 06/29/18 due 07/02/18, repurchase price $55,947, collateralized by a Federal National Mortgage Association, 1.500% due 06/22/20 and a United States Treasury Note, 1.375% due 05/31/20, aggregate value plus accrued interest of $57,061 (Cost: $55,942) |

55,942 |

55,942 |

|||||||||

|

TOTAL SHORT-TERM INVESTMENTS - 4.2% (COST $255,932) |

255,932 |

||||||||||

|

TOTAL INVESTMENTS - 99.9% (COST $4,150,402) |

6,028,383 |

||||||||||

|

Other Assets In Excess of Liabilities - 0.1% |

6,522 |

||||||||||

|

TOTAL NET ASSETS - 100.0% |

$ |

6,034,905 |

|||||||||

(a) Non-income producing security

(b) The rate shown represents the annualized yield at the time of purchase; not a coupon rate.

12 OAKMARK FUNDS

Oakmark Select Fund June 30, 2018 (Unaudited)

Schedule of Investments (in thousands) (continued)

WRITTEN OPTIONS

|

Description |

Counterparty |

Exercise Price |

Expiration Date |

Number of Contracts |

Notional Amount |

Market Value |

Premiums Received by Fund |

Unrealized Gain/(Loss) |

|||||||||||||||||||||||||||

|

PUTS |

|||||||||||||||||||||||||||||||||||

|

Charter Communications, Inc., Class A |

Pershing LLC |

$ |

285.00 |

7/18/2018 |

4,000 |

$ |

117,284 |

$ |

(1,780 |

) |

$ |

3,992 |

$ |

2,212 |

|||||||||||||||||||||

Oakmark.com 13

Oakmark Equity and Income Fund June 30, 2018

Summary Information

VALUE OF A $10,000 INVESTMENT

Since Inception - 11/01/95 (Unaudited)

PERFORMANCE

|

Average Annual Total Returns (as of 06/30/18) |

|||||||||||||||||||||||||||||||

| (Unaudited) |

Total Return Last 3 Months |

1-year |

3-year |

5-year |

10-year |

Since Inception |

Inception Date |

||||||||||||||||||||||||

|

Oakmark Equity and Income Fund (Investor Class) |

0.22 |

% |

6.56 |

% |

5.77 |

% |

8.16 |

% |

6.47 |

% |

10.08 |

% |

11/01/95 |

||||||||||||||||||

|

Lipper Balanced Fund Index |

1.13 |

% |

7.01 |

% |

6.37 |

% |

7.60 |

% |

6.44 |

% |

6.88 |

% |

|||||||||||||||||||

|

S&P 500 Index |

3.43 |

% |

14.37 |

% |

11.93 |

% |

13.42 |

% |

10.17 |

% |

9.07 |

% |

|||||||||||||||||||

|

Barclays U.S. Govt./Credit Index |

-0.33 |

% |

-0.63 |

% |

1.83 |

% |

2.29 |

% |

3.78 |

% |

5.04 |

% |

|||||||||||||||||||

|

Oakmark Equity and Income Fund (Advisor Class) |

0.28 |

% |

6.76 |

% |

N/A |

N/A |

N/A |

9.17 |

% |

11/30/16 |

|||||||||||||||||||||

|

Oakmark Equity and Income Fund (Institutional Class) |

0.25 |

% |

6.74 |

% |

N/A |

N/A |

N/A |

9.18 |

% |

11/30/16 |

|||||||||||||||||||||

|

Oakmark Equity and Income Fund (Service Class) |

0.19 |

% |

6.33 |

% |

5.47 |

% |

7.84 |

% |

6.14 |

% |

8.43 |

% |

07/12/00 |

||||||||||||||||||

The graph and table above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Past performance is no guarantee of future results. The performance data quoted represents past performance. Current performance may be lower or higher than the performance data quoted. Total return includes change in share prices and, in each case, includes reinvestment of dividends and capital gain distributions. The investment return and principal value vary so that an investor's shares when redeemed may be worth more or less than the original cost. To obtain the most recent month-end performance, please visit Oakmark.com.

|

TOP TEN EQUITY HOLDINGS10 |

% of Net Assets | ||||||

|

General Motors Co. |

5.2 |

||||||

|

Bank of America Corp. |

4.6 |

||||||

|

TE Connectivity, Ltd. |

3.8 |

||||||

|

MasterCard, Inc., Class A |

3.2 |

||||||

|

Nestlé SA |

2.8 |

||||||

|

UnitedHealth Group, Inc. |

2.4 |

||||||

|

Citigroup, Inc. |

2.2 |

||||||

|

National Oilwell Varco, Inc. |

2.1 |

||||||

|

Philip Morris International, Inc. |

2.1 |

||||||

|

Diageo PLC |

2.0 |

||||||

|

FUND STATISTICS |

|||||||

|

Ticker* |

OAKBX |

||||||

|

Number of Equity Holdings |

45 |

||||||

|

Net Assets |

$15.5 billion | ||||||

|

Weighted Average Market Cap |

$116.2 billion | ||||||

|

Median Market Cap |

$31.5 billion | ||||||

|

Gross Expense Ratio - Investor Class (as of 09/30/17)* |

0.88% | ||||||

|

Net Expense Ratio - Investor Class (as of 09/30/17)*† |

0.78% | ||||||

* This information is related to the Investor Class. Please visit Oakmark.com for information related to the Advisor, Institutional and Service Classes.

† The net expense ratio reflects a contractual advisory fee waiver agreement through January 28, 2019.

|

SECTOR ALLOCATION |

% of Net Assets | ||||||

|

Equity Investments |

|||||||

|

Consumer Discretionary |

12.5 |

||||||

|

Financials |

12.2 |

||||||

|

Information Technology |

12.1 |

||||||

|

Consumer Staples |

6.9 |

||||||

|

Health Care |

6.8 |

||||||

|

Industrials |

4.9 |

||||||

|

Energy |

4.6 |

||||||

|

Materials |

1.1 |

||||||

|

Real Estate |

0.9 |

||||||

|

Total Equity Investments |

62.0 |

||||||

|

Preferred Stocks |

0.1 |

||||||

|

Fixed Income Investments |

|||||||

|

Corporate Bonds |

14.5 |

||||||

|

Government and Agency Securities |

13.5 |

||||||

|

Convertible Bond |

0.1 |

||||||

|

Total Fixed Income Investments |

28.1 |

||||||

|

Short-Term Investments and Other |

9.8 |

||||||

See accompanying Disclosures and Endnotes on page 47.

14 OAKMARK FUNDS

Oakmark Equity and Income Fund June 30, 2018

Portfolio Manager Commentary

Clyde S. McGregor, CFA

Portfolio Manager

oakbx@oakmark.com

M. Colin Hudson, CFA

Portfolio Manager

oakbx@oakmark.com

Edward J. Wojciechowski, CFA

Portfolio Manager

oakbx@oakmark.com

Fund Fundamentals

Each year at the end of June, the investment industry experiences a curious phenomenon: the reconstitution of the Russell Indexes. Russell is a large investment industry consultant that began constructing broad market indexes in the 1980s, of which the best known may be the Russell 2000 Index.14 Russell constructs these indexes in an objective and transparent manner, basically using market capitalization as the guide. Over time, approximately $1 trillion has been committed to passively investing in line with the Russell Indexes and Keefe, Bruyette & Woods estimates they are used as benchmarks for $8.5 trillion in managed assets. Rather than changing its indexes every time a company outgrows its classification or ceases to exist, Russell chooses to reconstitute each index once per year at the end of June.

A sort of cottage industry has grown up around these reclassifications. As the end of June nears, investors begin anticipating index changes. This works to push up the prices of companies likely to move into a higher valuation index, while depressing the prices of those likely to move down or out from their current index. This has the effect of making the valuation characteristics of the actual indexes slightly higher than they otherwise would have been if the changes had taken place more organically. In a June 23 article titled "Rise in Passive Funds Sees Tail Wagging the Dog in Index World," Financial Times columnist John Authers notes, "Indices no longer merely measure markets. They move them...Generally, new additions to the Russell 2000 handily beat the market in the days leading up to the reconstitution."15

As we have often written, we fundamental investors are glad that this sort of trading is a regular market feature. We are happy to purchase shares from market participants who are selling a stock due to factors that have nothing to do with the business's intrinsic value. And again to repeat ourselves, we have seldom met the investor whose economic goal was to match or beat an index. One cannot live on relative returns. Investors instead want positive absolute returns like what we strive to obtain for the Equity and Income Fund. Observing non-fundamental activity in the securities market suggests that now would be an appropriate time to review our guiding principles for managing the Fund.

The Equity and Income Fund is a balanced fund—i.e., a fund invested in several asset classes—that has the goal of producing income while preserving and growing capital. Over time, the Fund's equity allocation has tended to constitute about 60% of the total portfolio with various types of fixed income investments making up the remainder. Many decades of experience have shown that this 60:40 asset allocation buffers volatility such that investors may adhere to a long-term strategy rather than buckling in times of adversity. As well, this allocation has

proven sufficient to mediate between the need for current income and long-term growth. Many balanced funds have similar asset allocations, so what are the factors that make Oakmark Equity and Income distinctive?

The most distinctive factor for any fund in the Oakmark Family is the investment philosophy that we at Harris Associates have employed for more than 40 years. For any security we ask, "What is it worth?" and "What is its price?" If a security can be purchased at a sufficient discount to our estimate of its value such that we have a margin of safety, we consider it for investment. For our equity investments, we attempt to determine whether the company shows persistent growth in intrinsic value per share and whether its managers think and act like owners and treat their shareholder-partners appropriately.

Our concept of a balanced fund is also somewhat idiosyncratic. In our industry today, you often hear or see the word "sleeves." Many target-date funds, for example, are composed of independent asset pools (sleeves) that are mixed together in whatever way the investment manager thinks is appropriate to achieve a particular purpose. Such a fund might be categorized as "balanced," since it, like our Fund, holds multiple types of assets. We, however, understand a balanced fund to be an integrated portfolio where every holding competes for space with every other holding, actual or potential. We do not have an equity sleeve and a bond sleeve. Instead, the portfolio asset allocation itself will fluctuate depending on our ability to populate the portfolio with dominant investments. Although 60:40 is the typical ratio for the equity/fixed income allocations, equities have at times comprised as much as 75% and as little as 45% of the total portfolio.

Other Distinguishing Characteristics:

Our investment horizon is very long term. The ability to think and act with a long-term horizon is a great advantage. We can also be relatively inactive for long periods. In our view, sometimes the best course of action is to do nothing.

The Fund's diversification is an outcome of our bottom-up investing process. Our Fund is typically more focused in its holdings than other balanced funds are. Outstanding investment opportunities are scarce, in our opinion.

Although income is always desirable, value is determinative. Income itself is a factor to which we assign value, and like other characteristics, it can be over-priced or undervalued. We have generally found income to be overvalued in the current decade and this has significantly influenced our approach to investing in fixed income securities.

Quality, like income, is a factor to which we ascribe value. We can and will own low-grade fixed income investments in

See accompanying Disclosures and Endnotes on page 47.

Oakmark.com 15

Oakmark Equity and Income Fund June 30, 2018

Portfolio Manager Commentary (continued)

the Fund, but only when we perceive their potential return to be competitive with equities. Similarly, with highly leveraged equities, we demand a substantially higher discount to value before investing.

We are relatively indifferent to the size or domicile of an opportunity. We have the ability to invest the Fund in small-cap, medium-cap and large-cap company shares, and we can invest as much as 35% of the portfolio in international securities.

Finally, benchmarks do not drive our investing. Investors in the Fund should expect results to differ from benchmarks, especially over short time periods.

For investors in mutual funds, the question of "fit" is of paramount importance. Investors make the best decisions when they have invested with funds whose style and philosophy mesh well with their own character and needs. Perhaps the most useful advice we can give fund investors is that they should often check to see if they understand their funds and, if so, consider whether they still fit.

Quarter Review

The Equity and Income Fund earned 0.2% in the quarter, while the Lipper Balanced Fund Index,12 the Fund's performance benchmark, gained 1.1%. (Although we are not benchmark driven, we are required to have one.) For the calendar six months, the Fund lost 1.4% compared to a 0.1% increase for the Lipper. The Fund's nine-month fiscal year return was 2.8%, compared to 3.7% for the Lipper. The annualized compound rate of return since the Fund's inception in 1995 is 10.1%, while the corresponding return to the Lipper Index is 6.9%.

General Motors, UnitedHealth Group, Mastercard, National Oilwell Varco and Foot Locker led the list of contributors for the quarter. The largest detractors were TE Connectivity, Philip Morris International, Arconic, Bank of America and CommScope Holding. Short-term earnings concerns hurt Philip Morris International, Arconic and CommScope, while banks in general retreated as the fixed income yield curve flattened. Trade war fears also roiled markets and individual stocks. For the calendar six months, Mastercard, National Oilwell Varco, UnitedHealth Group, HCA Healthcare and Foot Locker contributed most while Arconic, Philip Morris International, Nestlé, CVS Health and Citigroup were the biggest detractors from return. For the nine months of the Fund's fiscal year, Mastercard, Bank of America, UnitedHealth Group, Foot Locker and National Oilwell Varco led the contributors list and Philip Morris International, CVS Health, Arconic, Baker Hughes and Oracle detracted.

Transaction Activity

During the quarter, the Fund added three new positions and exited four holdings. The three new positions are Apergy, American Airlines and Charter. Apergy was obtained through a spin-off from long-time holding Dover. Apergy provides equipment and technologies that help companies drill for and produce oil and gas. The company's two main product segments manufacture polycrystalline diamond cutters and equipment for artificial lift, both of which are crucial for non-conventional exploration and production. Apergy has generated free cash flow throughout the downturn and we expect a rapid recovery

in earnings and free cash flow as North American drilling activity rebounds. Trading at less than 15x our estimate of normalized earnings per share, this high-quality equipment company offers an attractive valuation, in our view.

Our investment in American Airlines is predicated on an evolution and improvement in the industry. Historically, airlines have not made for good investments, despite the usefulness of their services. At issue was the lack of pricing power and poor corporate cultures. However, after years of consolidation, capped by the merger of US Airways and American Airlines in 2013, the industry is now becoming more mature and rational. The three major hub-and-spoke carriers each have strength in their respective hubs and their management teams are all behaving in a healthier manner in terms of capacity additions and capital allocation. Our choice in the sector is American Airlines, due to the unusually large opportunity still in front of the company as it finishes off its merger integration. Also, CEO Doug Parker is in the process of improving the culture and restoring credibility with employees. Parker believes that American Airlines has around $5 billion of pre-tax earnings power and he has bought back 37% of the company's shares since the merger closed. With the stock selling for a single-digit multiple of normal earnings power, we believe that it is an attractive investment.

Charter gives us the opportunity to invest in what we believe is a strong business with exceptional management at an attractive price. Because of their valuable infrastructure, U.S. cable companies are benefiting from strong demand for high-speed internet access. In many markets, Charter has the only fiber-rich network capable of providing consumers with the high internet speeds they demand. We believe that new competitors are unlikely to enter the market as they will have to invest massive amounts of capital for fractional penetration. This should provide a long runway for continued growth at Charter. The stock has lagged behind the broader market as investors appear to be frustrated with the pace of operational improvement at recently acquired Time Warner Cable. Our experience investing in turnarounds reminds us that it takes more than a couple of quarters to make meaningful progress. We take a more positive, longer term view of the business, and believe Charter is valued at a discount to peer companies and private market transactions.

Besides being an attractive investment, the purchase of Charter also allowed us to lower our capital gain position as we sold Liberty Broadband at a loss. The main asset of Liberty Broadband is Charter stock, so we were able to effectively keep our economic position in Charter, while recognizing a tax loss. We have always actively managed the tax position of the Fund with a goal of maximizing after-tax returns.

The four positions eliminated during the quarter were Fidelity National Financial, Jones Lang LaSalle, and Liberty Broadband A and C shares. Both Fidelity National Financial and Jones Lang LaSalle were strong performers and reached our sell targets. As described above, the two classes of Liberty stock were sold to realize tax losses and we used the proceeds to purchase Charter stock.

As always, we thank our shareholders for entrusting their assets to the Fund and welcome your questions and comments.

See accompanying Disclosures and Endnotes on page 47.

16 OAKMARK FUNDS

Oakmark Equity and Income Fund June 30, 2018 (Unaudited)

Schedule of Investments (in thousands)

|

Shares |

Value |

||||||||||

|

COMMON STOCKS - 62.0% |

|||||||||||

|

CONSUMER DISCRETIONARY - 12.5% |

|||||||||||

|

AUTOMOBILES & COMPONENTS - 8.0% |

|||||||||||

|

General Motors Co. |

20,307 |

$ |

800,111 |

||||||||

|

Lear Corp. |

1,400 |

260,103 |

|||||||||

|

BorgWarner, Inc. |

4,282 |

184,807 |

|||||||||

|

1,245,021 |

|||||||||||

|

MEDIA - 1.9% |

|||||||||||

|

Charter Communications, Inc., Class A (a) |

749 |

219,703 |

|||||||||

|

Comcast Corp., Class A |

2,120 |

69,557 |

|||||||||

|

289,260 |

|||||||||||

|

RETAILING - 1.7% |

|||||||||||

|

Foot Locker, Inc. |

4,066 |

214,096 |

|||||||||

|

Qurate Retail, Inc. (a) |

2,327 |

49,389 |

|||||||||

|

263,485 |

|||||||||||

|

CONSUMER DURABLES & APPAREL - 0.5% |

|||||||||||

|

Carter's, Inc. |

664 |

72,004 |

|||||||||

|

CONSUMER SERVICES - 0.4% |

|||||||||||

|

MGM Resorts International |

2,351 |

68,256 |

|||||||||

|

1,938,026 |

|||||||||||

|

FINANCIALS - 12.2% |

|||||||||||

|

BANKS - 7.2% |

|||||||||||

|

Bank of America Corp. |

25,084 |

707,104 |

|||||||||

|

Citigroup, Inc. |

5,165 |

345,635 |

|||||||||

|

Wells Fargo & Co. |

1,203 |

66,716 |

|||||||||

|

1,119,455 |

|||||||||||

|

DIVERSIFIED FINANCIALS - 3.7% |

|||||||||||

|

Ally Financial, Inc. |

9,973 |

261,978 |

|||||||||

|

The Bank of New York Mellon Corp. |

3,030 |

163,389 |

|||||||||

|

State Street Corp. |

1,551 |

144,401 |

|||||||||

|

569,768 |

|||||||||||

|

INSURANCE - 1.3% |

|||||||||||

|

American International Group, Inc. |

3,646 |

193,295 |

|||||||||

|

1,882,518 |

|||||||||||

|

INFORMATION TECHNOLOGY - 12.1% |

|||||||||||

|

SOFTWARE & SERVICES - 7.4% |

|||||||||||

|

MasterCard, Inc., Class A |

2,502 |

491,771 |

|||||||||

|

Oracle Corp. |

6,705 |

295,427 |

|||||||||

|

Alphabet, Inc., Class C (a) |

263 |

293,193 |

|||||||||

|

CoreLogic, Inc. (a) |

1,293 |

67,107 |

|||||||||

|

1,147,498 |

|||||||||||

|

TECHNOLOGY HARDWARE & EQUIPMENT - 4.4% |

|||||||||||

|

TE Connectivity, Ltd. |

6,483 |

583,868 |

|||||||||

|

CommScope Holding Co., Inc. (a) |

3,280 |

95,798 |

|||||||||

|

679,666 |

|||||||||||

|

SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT - 0.3% |

|||||||||||

|

Qorvo, Inc. (a) |

609 |

48,856 |

|||||||||

|

1,876,020 |

|||||||||||

|

Shares |

Value |

||||||||||

|

CONSUMER STAPLES - 6.9% |

|||||||||||

|

FOOD, BEVERAGE & TOBACCO - 6.9% |

|||||||||||

|

Nestlé SA (b) |

5,623 |

$ |

435,389 |

||||||||

|

Philip Morris International, Inc. |

3,956 |

319,432 |

|||||||||

|

Diageo PLC (b) |

2,198 |

316,548 |

|||||||||

|

1,071,369 |

|||||||||||

|

HEALTH CARE - 6.8% |

|||||||||||

|

HEALTH CARE EQUIPMENT & SERVICES - 6.2% |

|||||||||||

|

UnitedHealth Group, Inc. |

1,506 |

369,590 |

|||||||||

|

CVS Health Corp. |

4,911 |

316,045 |

|||||||||

|

HCA Healthcare, Inc. |

2,186 |

224,253 |

|||||||||

|

LivaNova PLC (a) |

567 |

56,576 |

|||||||||

|

966,464 |

|||||||||||

|

PHARMACEUTICALS, BIOTECHNOLOGY & LIFE SCIENCES - 0.6% |

|||||||||||

|

Regeneron Pharmaceuticals, Inc. (a) |

271 |

93,527 |

|||||||||

|

1,059,991 |

|||||||||||

|

INDUSTRIALS - 4.9% |

|||||||||||

|

CAPITAL GOODS - 4.2% |

|||||||||||

|

Dover Corp. |

3,545 |

259,457 |

|||||||||

|

Johnson Controls International plc |

5,047 |

168,809 |

|||||||||

|

Arconic, Inc. |

7,096 |

120,701 |

|||||||||

|

Carlisle Cos., Inc. |

560 |

60,632 |

|||||||||

|

WESCO International, Inc. (a) |

682 |

38,919 |

|||||||||

|

648,518 |

|||||||||||

|

TRANSPORTATION - 0.7% |

|||||||||||

|

American Airlines Group, Inc. |

2,907 |

110,335 |

|||||||||

|

758,853 |

|||||||||||

|

ENERGY - 4.6% |

|||||||||||

|

National Oilwell Varco, Inc. |

7,573 |

328,677 |

|||||||||

|

PDC Energy, Inc. (a) |

1,900 |

114,879 |

|||||||||

|

Anadarko Petroleum Corp. |

1,417 |

103,773 |

|||||||||

|

Baker Hughes a GE Co. |

2,682 |

88,570 |

|||||||||

|

Apergy Corp. (a) |

1,772 |

73,992 |

|||||||||

|

709,891 |

|||||||||||

|

MATERIALS - 1.1% |

|||||||||||

|

Glencore PLC |

35,440 |

168,262 |

|||||||||

|

REAL ESTATE - 0.9% |

|||||||||||

|

The Howard Hughes Corp. (a) |

555 |

73,479 |

|||||||||

|

Gaming and Leisure Properties, Inc. REIT |

1,833 |

65,607 |

|||||||||

|

139,086 |

|||||||||||

|

TOTAL COMMON STOCKS - 62.0% (COST $5,659,761) |

9,604,016 |

||||||||||

|

PREFERRED STOCKS - 0.1% |

|||||||||||

|

FINANCIALS - 0.1% |

|||||||||||

|

GMAC Capital Trust I (c), 8.13% (3 mo. USD LIBOR + 5.785%), |

498 |

13,084 |

|||||||||

|

TOTAL PREFERRED STOCKS - 0.1% (COST $13,007) |

13,084 |

||||||||||

Oakmark.com 17

Oakmark Equity and Income Fund June 30, 2018 (Unaudited)

Schedule of Investments (in thousands) (continued)

|

Par Value |

Value |

||||||||||

|

FIXED INCOME - 28.1% |

|||||||||||

|

CORPORATE BONDS - 14.5% |

|||||||||||

|

CONSUMER DISCRETIONARY - 3.8% |

|||||||||||

|

Adient Global Holdings, Ltd., 144A 4.875%, due 08/15/26 (d) |

$ |

7,000 |

$ |

6,282 |

|||||||

|

Amazon.com, Inc. 3.15%, due 08/22/27 |

9,950 |

9,529 |

|||||||||

|

Booking Holdings, Inc. 3.60%, due 06/01/26 |

14,730 |

14,334 |

|||||||||

|

3.55%, due 03/15/28 |

9,950 |

9,471 |

|||||||||

|

2.75%, due 03/15/23 |

6,965 |

6,720 |

|||||||||

|

BorgWarner, Inc. 4.625%, due 09/15/20 |

10,810 |

11,082 |

|||||||||

|

Boyd Gaming Corp, 144A 6.00%, due 08/15/26 (d) |

4,975 |

4,925 |

|||||||||

|

Caesars Resort Collection LLC / CRC Finco, Inc., 144A 5.25%, due 10/15/25 (d) |

25,870 |

24,479 |

|||||||||

|

CCO Holdings LLC / CCO Holdings Capital Corp., 144A 5.125%, due 05/01/27 (d) |

250 |

234 |

|||||||||

|

Charter Communications Operating LLC / Charter Communications Operating Capital 3.579%, due 07/23/20 |

29,148 |

29,111 |

|||||||||

|

4.20%, due 03/15/28 |

9,950 |

9,315 |

|||||||||

|

4.50%, due 02/01/24 |

2,985 |

2,982 |

|||||||||

|

Dana, Inc. 6.00%, due 09/15/23 |

3,925 |

4,053 |

|||||||||

|

Delphi Technologies PLC, 144A 5.00%, due 10/01/25 (d) |

1,000 |

954 |

|||||||||

|

Dollar Tree, Inc. 3.055% (3 mo. USD LIBOR + 0.70%), due 04/17/20 (c) |

6,965 |

6,979 |

|||||||||

|

EMI Music Publishing Group North America Holdings, Inc., 144A 7.625%, due 06/15/24 (d) |

4,910 |

5,313 |

|||||||||

|

Expedia Group, Inc. 5.00%, due 02/15/26 |

28,360 |

28,887 |

|||||||||

|

Foot Locker, Inc. 8.50%, due 01/15/22 |

4,340 |

4,958 |

|||||||||

|

General Motors Co. 4.875%, due 10/02/23 |

41,400 |

42,561 |

|||||||||

|

3.50%, due 10/02/18 |

29,525 |

29,581 |

|||||||||

|

General Motors Financial Co., Inc. 3.50%, due 07/10/19 |

4,975 |

5,000 |

|||||||||

|

3.10%, due 01/15/19 |

4,915 |

4,920 |

|||||||||

|

International Game Technology PLC, 144A 6.50%, due 02/15/25 (d) |

19,600 |

20,237 |

|||||||||

|

6.25%, due 02/15/22 (d) |

14,800 |

15,170 |

|||||||||

|

5.625%, due 02/15/20 (d) |

9,800 |

9,922 |

|||||||||

|

KFC Holding Co/Pizza Hut Holdings LLC/ Taco Bell of America LLC, 144A 5.00%, due 06/01/24 (d) |

1,000 |

987 |

|||||||||

|

5.25%, due 06/01/26 (d) |

1,000 |

985 |

|||||||||

|

Lear Corp. 5.25%, due 01/15/25 |

11,060 |

11,375 |

|||||||||

|

5.375%, due 03/15/24 |

10,512 |

10,904 |

|||||||||

|

Lithia Motors, Inc., 144A 5.25%, due 08/01/25 (d) |

1,990 |

1,940 |

|||||||||

|

Par Value |

Value |

||||||||||

|