OAKMARK FUNDS

FIRST QUARTER REPORT | DECEMBER 31, 2015

OAKMARK FUND

OAKMARK SELECT FUND

OAKMARK EQUITY AND INCOME FUND

OAKMARK GLOBAL FUND

OAKMARK GLOBAL SELECT FUND

OAKMARK INTERNATIONAL FUND

OAKMARK INTERNATIONAL SMALL CAP FUND

Oakmark Funds

2016 First Quarter Report

TABLE OF CONTENTS

|

President's Letter |

1 |

||||||

|

Commentary on Oakmark and Oakmark Select Funds |

2 |

||||||

|

Oakmark Fund |

|||||||

|

Summary Information |

4 |

||||||

|

Portfolio Manager Commentary |

5 |

||||||

|

Schedule of Investments |

6 |

||||||

|

Oakmark Select Fund |

|||||||

|

Summary Information |

8 |

||||||

|

Portfolio Manager Commentary |

9 |

||||||

|

Schedule of Investments |

10 |

||||||

|

Oakmark Equity and Income Fund |

|||||||

|

Summary Information |

12 |

||||||

|

Portfolio Manager Commentary |

13 |

||||||

|

Schedule of Investments |

15 |

||||||

|

Oakmark Global Fund |

|||||||

|

Summary Information |

20 |

||||||

|

Portfolio Manager Commentary |

21 |

||||||

|

Schedule of Investments |

23 |

||||||

|

Oakmark Global Select Fund |

|||||||

|

Summary Information |

26 |

||||||

|

Portfolio Manager Commentary |

27 |

||||||

|

Schedule of Investments |

28 |

||||||

|

Commentary on Oakmark International and Oakmark Int'l Small Cap Funds |

30 |

||||||

|

Oakmark International Fund |

|||||||

|

Summary Information |

32 |

||||||

|

Portfolio Manager Commentary |

33 |

||||||

|

Schedule of Investments |

34 |

||||||

|

Oakmark International Small Cap Fund |

|||||||

|

Summary Information |

38 |

||||||

|

Portfolio Manager Commentary |

39 |

||||||

|

Schedule of Investments |

40 |

||||||

|

Disclosures and Endnotes |

42 |

||||||

|

Trustees and Officers |

44 | ||||||

FORWARD-LOOKING STATEMENT DISCLOSURE

One of our most important responsibilities as mutual fund managers is to communicate with shareholders in an open and direct manner. Some of our comments in our letters to shareholders are based on current management expectations and are considered "forward-looking statements." Actual future results, however, may prove to be different from our expectations. You can identify forward-looking statements by words such as "estimate", "may", "will", "expect", "believe",

"plan" and other similar terms. We cannot promise future returns. Our opinions are a reflection of our best judgment at the time this report is compiled, and we disclaim any obligation to update or alter forward-looking statements as a result of new information, future events, or otherwise.

OAKMARK FUNDS

Oakmark Funds December 31, 2015

President's Letter

Kristi L. Rowsell

President of Oakmark Funds

President of Harris Associates L.P.

Dear Shareholders,

The year 2015 proved to be challenging for U.S.-based stock investors. While the fourth quarter's performance was strongly positive, the calendar year ended with most benchmark indexes in negative territory. Market participants encountered a full mix of negative headlines during the year, such as slowing global growth, declining commodity prices, volatile currencies and reduced monetary stimulus in the United States. However, not all of the news today is negative. The U.S. unemployment rate continues to fall. Global inflation and interest rates remain low. And both households and companies around the world benefit from today's lower energy prices. These factors, plus significant monetary stimulation from many non-U.S. countries, lead most estimates of global growth to be between two and three percent.

Your Oakmark Funds also had a challenging performance year. Our managers discuss the factors and individual companies that impacted the portfolios in their letters this quarter. They provide valuable context for our shareholders, reflecting on their experience through full market cycles and their long tenure as managers for the Funds. We have always believed that the key to capturing equity market returns is to stay disciplined and focused. We invest in companies that we believe are priced below our estimate of intrinsic value. Our research teams use fundamental analysis to identify companies that we believe offer excellent business models, good management teams, strong balance sheets and attractive valuations. Our conviction in this philosophy is unwavering and has been repeatedly affirmed over our company's 40-year history as investment managers. Experience tells us that in weak performance periods like last year, good opportunities often arise and that our patience is typically rewarded.

One of our central investment tenets is to invest in companies that have management teams whose interests are aligned with their shareholders. This principle applies at Harris Associates with respect to the Oakmark Funds as well. Each year, we voluntarily report the level of personal assets the employees of the firm and trustees of the Funds collectively invest in the Oakmark Funds because we believe it demonstrates our commitment to our investing philosophy. This alignment of our interests with yours fosters stewardship of the Funds, a responsibility that we take very seriously. We are proud to tell you that, as of December 31, 2015, the employees of Harris Associates, our families and the Funds' trustees have more than $440 million invested in the Oakmark Funds, reflecting significant share purchases during the year. We hope that this level of investment demonstrates to you our confidence that the Funds remain attractive investments for the future.

Happy New Year to you all! We wish you a healthy and prosperous 2016.

Oakmark.com 1

Oakmark and Oakmark Select Funds December 31, 2015

Portfolio Manager Commentary

William C. Nygren, CFA

Portfolio Manager

oakmx@oakmark.com

oaklx@oakmark.com

At Oakmark, we are long-term investors. We attempt to identify growing businesses that are managed to benefit their shareholders. We will purchase stock in those businesses only when priced substantially below our estimate of intrinsic value. After purchase, we patiently wait for the gap between stock price and intrinsic value to close.

"Don't keep all your eggs in one basket."

-Old Italian Proverb

"Put all your eggs in one basket and watch that basket."

-Mark Twain

Active managers had a disappointing 2015. Following 2014, when 90% of actively managed mutual funds underperformed the S&P 5001, there was little improvement in 2015. The majority of mutual funds lost money this past year despite a small gain in the S&P. Most stocks declined, and that created a tough environment for active managers to make money. Unfortunately, the list of declining funds included most of the Oakmark Funds.

The poor mutual fund industry results led to an acceleration of investors redeeming shares from their actively managed funds and reinvesting in index funds. In my March commentary, I wrote that the inevitability of index funds outperforming the average actively managed fund didn't imply that identifying superior funds was destined to fail. In fact, we concluded that the long-term rewards from active management can be as high as they have ever been.

Disappointments during the year also included some high profile funds suffering substantial setbacks due to a lack of succession planning, poor tax management or excessive concentration in top holdings. Many mutual fund industry observers highlighted those issues, threw their hands up in frustration and hopped on the indexing bandwagon.

When we launched the Oakmark Select Fund in 1996, I wrote a paper outlining our belief that a more concentrated fund of our best stock selections was likely to produce better long-term returns, albeit with higher short-term volatility, than our more diversified funds. To conclude that paper, I selected a quote that Warren Buffett had used in his 1991 annual report to the shareholders of Berkshire Hathaway:

"John Maynard Keynes, whose brilliance as a practicing investor matched his brilliance in thought, wrote a letter to a business associate, F.C. Scott, on August 15, 1934, that says it all: 'As time goes on, I get more and more convinced that the right method in investment is to put fairly large sums into enterprises which one thinks one knows something about and in the management of which one thoroughly believes. It is a mistake to think that one limits one's risk by spreading too much between enterprises about which one knows little and has no reason for special confidence.'"

Is the more than 80-year-old quote from Keynes and nearly 25-year-old quote from Buffett, two of the greatest investors of all time, still valid today? In 2016, we will celebrate the 20th anniversary of Oakmark Select and the 10th of Oakmark Global Select. As one of the early advocates for concentrated investing

in mutual funds, we at Oakmark thought this would be a good opportunity to revisit the case for concentration.

Academic theory states there is no such thing as over-diversification. If all stocks are always priced appropriately—meaning there is no way to increase return without increasing risk—then diversification is a free good. The more stocks you add to your portfolio, the less risky the portfolio is. According to that theory, it makes sense that investors should own lots of stocks. Effectively, your eggs should be spread across as many baskets as you can find. And that is why most mutual fund portfolios own well over 100 stocks. The problem with this line of thinking is that if stock selection doesn't add value, then active management doesn't add value either, and low-cost index funds become a superior choice.

But what if stocks aren't always appropriately priced? What if, because investors occasionally are confused or overcome by emotions, some stocks get mispriced and offer a different risk-return tradeoff than other stocks? Then diversification theory gets stood on its head. Then some stocks are superior to others. Then there is a difference between one's favorite stocks and all the other stocks. Then diversifying away from those favorite stocks reduces expected return. Instead of more diversification always being better, it becomes a trade-off of risk versus return: Holding more stocks in a portfolio lowers risk, but at the cost of also lowering expected return. You still wouldn't want all your eggs in just one basket, but you'd recognize there is a cost for using too many baskets.

At Oakmark, we believe that the academic view on stocks is largely, but not completely, correct: We think that most of the time, most stocks are priced about right—but not always, and never each and every stock. We believe that misunderstood and "out of favor" stocks exist and that by using a disciplined approach to finding them and having the patience to hold them long-term, we can reap the excess rewards those stocks offer.

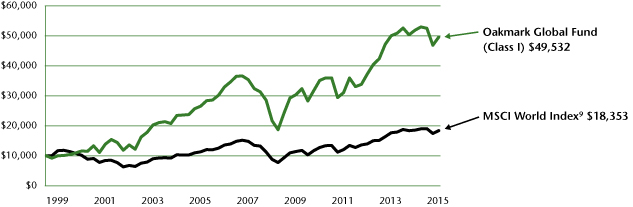

If you don't think that is possible, I encourage you to look at the performance graphs showing how a $10,000 investment has fared in each of our Funds. Then compare that performance to the relevant benchmark index shown on each graph. All Oakmark Funds use the same long-term value philosophy. But these Funds were started at different times, and they invest in different geographies and varied asset classes. The graphs show actual returns to shareholders, meaning they already deduct all expenses.

Because we believe our stock selection adds value, we own fewer stocks than most other mutual funds. Our diversified funds (Oakmark, Oakmark International, Oakmark Global, Oakmark Equity and Income, and Oakmark International Small Cap) generally own 40-60 stocks each. Typical mutual funds own two to three times that many. We believe adding more stocks to our

2 OAKMARK FUNDS

Oakmark and Oakmark Select Funds December 31, 2015

Portfolio Manager Commentary (continued)

portfolios would decrease their expected returns and only slightly reduce their volatility.

When I started in the investment business, in the days before Morningstar made information on mutual funds so easily accessible, many fund investors picked just one fund and invested most of their assets in that one fund. Today, most mutual fund investors build portfolios of mutual funds. When we started Oakmark Select, I used to bring a prop when I spoke to investors. It answered a simple question: What would the portfolio look like for an individual who put $10,000 into the top-rated fund in each of Morningstar's nine style boxes? And I didn't mean just a listing of nine funds. I wanted to show the portfolio of all the stocks held through ownership of the nine funds. So I printed out that portfolio, listing each stock and showing how much of the $90,000 was invested in it. For those of you too young to remember, computer printers back then didn't use regular paper; they used a continuous roll of paper with perforations for page breaks rather than separate pages. In any event, that printout showed a portfolio with over 1,000 stocks, and it was more than 30 feet long. Over-diversifying is not a good recipe for beating the market!

I don't think the mutual fund industry has changed to reflect how most investors now use funds. Because investors are diversifying their assets across multiple funds, their ability to outperform the market is lessened if each fund holds over 100 securities. That's why our diversified funds generally hold only 40-60 stocks, and our two Select funds generally own only 20 stocks. That magnifies the importance, both good and bad, of our stock selection. It also makes our Select funds great complements to holdings that are primarily indexed or to an investor's portfolio of funds. Because the Select funds have higher volatility, they are not as appropriate for "one-stop shopping" as our other funds are.

Nearly 20 years ago, in the first quarterly report I wrote introducing the Oakmark Select Fund, I said, "By concentrating in my favorite stocks, I hope to increase the probability of achieving our outperformance goal. The downside is that the short-term results will show more ups and downs." We've delivered on both goals. Our shareholders have definitely endured bigger ups and downs, but in return, they have enjoyed results that exceeded the Oakmark Fund in 14 of 19 calendar years and achieved significantly greater cumulative returns.

In that same report I also said, "We currently plan that at most times the Oakmark Select Fund will own 20 or fewer stocks, with about half of its assets in its five largest positions." Almost 20 years later, we still aim to own about 20 stocks. But we have made one change. Graphs of portfolio volatility at the time of the Fund's inception showed that most of the benefit of diversification was obtained by owning just 7-10 independent securities, implying weightings of 10-15% each. Now, because stocks have become more correlated with each other and somewhat more volatile, today's graphs show that 10-15 securities are needed to get the same reduction in portfolio volatility. Based on that, we believe somewhat smaller position sizes are prudent, so we now generally limit our largest positions to 7-10% of assets. The result is that our top five positions account for about 35% of assets instead of 50%.

In 2006, when David Herro and I started the Oakmark Global Select Fund, we wrote the following in our introductory shareholder letter. I'll quote at length because it still accurately explains how we manage the Fund today:

"As with all Oakmark Funds, we believe that we can add value via our stock selection and therefore believe that we can magnify that value via concentration. We expect the portfolio to generally contain about 20 stocks, and we expect that, over time, about half will be U.S.-based businesses and half will be based outside the U.S. When we find it easier to identify cheap stocks in the U.S., we will invest more heavily there, and we will shift to more international stocks when we believe non-U.S. opportunities are more abundant... We are not going to be benchmark sensitive and we will not attempt to minimize tracking error—the amount our performance differs from index performance. To us, that just isn't a useful measure of risk. We will attempt to select securities that provide undervaluation, growing values, and managements that work to maximize business value. We believe those features lessen what we define as risk—which is the chance of losing money. Our goal will be to maximize the long-term, after-tax growth of shareholder capital. And as with all other Oakmark Funds, 'shareholder capital' includes our own."

The Oakmark Global Select Fund has outperformed the average of Oakmark and Oakmark International in six of the nine ensuing calendar years and has also achieved a higher cumulative return. When stock selection is good, concentration makes it better.

We know it is painful to lose money. The past two years, during which most of our Funds have underperformed their respective indexes, have been difficult, and the first week of 2016 wasn't any better. But if you again look at the performance graphs I referenced earlier, you'll see that all of our Funds have endured periods, sometimes for several years, when they have either lost money or lost ground relative to their benchmarks. Though these times are frustrating for our shareholders—and, remember, that includes all of the portfolio managers—these periods of weak performance have been opportunities for additional investment rather than reasons to give up on our investment philosophy.

We are invested side-by-side with you, we share your frustration with recent results and we appreciate your patience. We believe that our Funds are positioned to continue delivering on their dual long-term goals of growing investor capital and performing better than index funds. You might be interested to know that every portfolio manager of every Oakmark Fund purchased more shares in the past twelve months. Actions speak louder than words.

Oakmark.com 3

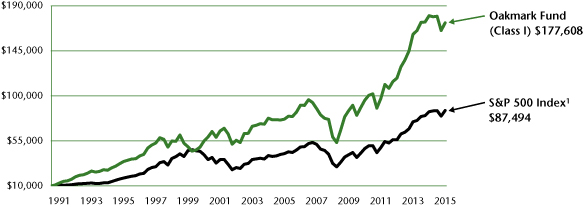

Oakmark Fund December 31, 2015

Summary Information

VALUE OF A $10,000 INVESTMENT

Since Inception - 08/05/91 (Unaudited)

PERFORMANCE

|

Average Annual Total Returns (as of 12/31/15) |

|||||||||||||||||||||||||||||||

|

(Unaudited) |

Total Return Last 3 Months |

1-year |

3-year |

5-year |

10-year |

Since Inception |

Inception Date |

||||||||||||||||||||||||

|

Oakmark Fund (Class I) |

4.64 |

% |

-3.95 |

% |

13.71 |

% |

12.61 |

% |

8.49 |

% |

12.51 |

% |

08/05/91 |

||||||||||||||||||

|

S&P 500 Index |

7.04 |

% |

1.38 |

% |

15.13 |

% |

12.57 |

% |

7.31 |

% |

9.29 |

% |

|||||||||||||||||||

|

Dow Jones Industrial Average2 |

7.70 |

% |

0.21 |

% |

12.66 |

% |

11.30 |

% |

7.75 |

% |

10.07 |

% |

|||||||||||||||||||

|

Lipper Large Cap Value Funds Index3 |

5.64 |

% |

-3.65 |

% |

12.53 |

% |

10.07 |

% |

5.71 |

% |

8.50 |

% |

|||||||||||||||||||

|

Oakmark Fund (Class II) |

4.58 |

% |

-4.26 |

% |

13.36 |

% |

12.26 |

% |

8.15 |

% |

7.30 |

% |

04/05/01 |

||||||||||||||||||

The graph and table above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Past performance is no guarantee of future results. The performance data quoted represents past performance. Current performance may be lower or higher than the performance data quoted. Total return includes change in share prices and, in each case, includes reinvestment of dividends and capital gain distributions. The investment return and principal value vary so that an investor's shares when redeemed may be worth more or less than the original cost. To obtain the most recent month-end performance, please visit Oakmark.com.

|

TOP TEN EQUITY HOLDINGS4 |

% of Net Assets |

||||||

|

Bank of America Corp. |

3.5 |

||||||

|

General Electric Co. |

2.8 |

||||||

|

Citigroup, Inc. |

2.7 |

||||||

|

American International Group, Inc. |

2.7 |

||||||

|

JPMorgan Chase & Co. |

2.6 |

||||||

|

MasterCard, Inc., Class A |

2.5 |

||||||

|

Visa, Inc., Class A |

2.4 |

||||||

|

Intel Corp. |

2.3 |

||||||

|

Alphabet Inc., Class C |

2.3 |

||||||

|

Microsoft Corp. |

2.2 |

||||||

|

FUND STATISTICS |

|||||||

|

Ticker |

OAKMX |

||||||

|

Inception |

08/05/1991 |

||||||

|

Number of Equity Holdings |

55 |

||||||

|

Net Assets |

$17.1 billion | ||||||

|

Benchmark |

S&P 500 Index |

||||||

|

Weighted Average Market Cap |

$120.4 billion | ||||||

|

Median Market Cap |

$45.1 billion | ||||||

|

Portfolio Turnover (for the 12-months ended 09/30/15) |

33% | ||||||

|

Expense Ratio - Class I (as of 09/30/14) |

0.87% | ||||||

|

Expense Ratio - Class I (as of 09/30/15) |

0.85% | ||||||

|

SECTOR ALLOCATION |

% of Net Assets |

||||||

|

Financials |

30.5 |

||||||

|

Information Technology |

25.3 |

||||||

|

Industrials |

10.9 |

||||||

|

Consumer Discretionary |

9.8 |

||||||

|

Energy |

5.9 |

||||||

|

Consumer Staples |

5.8 |

||||||

|

Health Care |

5.1 |

||||||

|

Materials |

1.7 |

||||||

|

Short-Term Investments and Other |

5.0 |

||||||

4 OAKMARK FUNDS

Oakmark Fund December 31, 2015

Portfolio Manager Commentary

William C. Nygren, CFA

Portfolio Manager

oakmx@oakmark.com

Kevin Grant, CFA

Portfolio Manager

oakmx@oakmark.com

The Oakmark Fund returned 5% during the fourth quarter of 2015, bringing the calendar year to a loss of 4%. These results lagged behind the S&P 5001, which was up 7% for the fourth quarter and up 1% for the calendar year. We are disappointed with the Fund's full-year results, which were hurt by significant declines in energy-related shares and relative underperformance from financials. As portfolio managers and large shareholders of the Fund, we're not satisfied with losses, but we remain confident in our time-tested philosophy, investment process and our research team. As we have said in the past, our analysts look for three characteristics in every investment: (1) businesses selling at a discount to fair value, (2) businesses that produce sustainable value growth over time and (3) management teams that think and act like value-maximizing owners. We typically buy businesses that are trading at a significant discount to our estimate of a company's intrinsic value and sell when the price approaches intrinsic value. With recent underperformance in several of our sectors, the valuation of the Oakmark Fund portfolio is attractively positioned toward the "buy" end of the range.

Our biggest contributing sectors for the fourth quarter were information technology and financials, with General Electric and Amazon being the best individual contributors. Our worst contributing sectors for the quarter were energy and healthcare, and our worst individual securities were Anadarko and Cummins. For the calendar year, the highest contributing securities were Amazon and Alphabet (formerly known as Google), and the worst contributing securities were Chesapeake and Qualcomm. Chesapeake was affected by another 30% drop in crude oil prices in 2015, to what we feel is an unsustainable level, and Qualcomm was pressured by foreign disputes in their highly profitable wireless royalty business.

During the quarter, we added a new position in Ally Financial (see below), and we eliminated positions in Accenture, Amazon and Omnicom Group. Amazon has been a great holding for the Fund, and with the share price more than doubling in 2015, we believe the business is now fairly valued. With minimal reported earnings and a very high P/E5 ratio, Amazon may have looked like an unusual purchase for a value-based fund when we initiated a position in April 2014. We looked past reported earnings, which were tempered by large investments for future growth, and found that the scale and core earnings power of Amazon's business were quite impressive and under-appreciated. Omnicom Group has also been a strong performer for the Fund. We have held Omnicom since late 2008, and we eliminated the position in the fourth quarter as the share price approached our estimate of fair value.

Ally Financial (ALLY-$18.79)

Ally was founded nearly a century ago as General Motors Acceptance Corporation. Its purpose then was to provide financing to GM dealers and retail customers. Today, Ally's

business is largely the same except that it is no longer owned by GM and now serves dealers and customers of many other automobile manufacturers, such as Ford, Chrysler and Toyota. Since Ally's initial public offering in spring 2014, its shares have fallen over 20% while the S&P 500 has returned over 15%. Over this period, some investors have grown concerned that the business is at a cyclical peak, as U.S. auto sales are near record levels and credit losses are below long-term averages; as a result, some believe Ally's earnings have nowhere to go but down. We believe cyclical pressures will be offset by continued internal improvements, such as funding cost reductions (as "legacy" liabilities are replaced with lower cost borrowings) and improving their capital structure. With Ally's stock trading at just 80% of tangible book value, we believe Ally is a compelling addition to the Oakmark Fund.

Oakmark.com 5

Oakmark Fund December 31, 2015 (Unaudited)

Schedule of Investments (in thousands)

|

Shares |

Value |

||||||||||

|

COMMON STOCKS - 95.0% |

|||||||||||

|

FINANCIALS - 30.5% |

|||||||||||

|

DIVERSIFIED FINANCIALS - 12.5% |

|||||||||||

|

State Street Corp. Asset Management & Custody Banks |

5,180 |

$ |

343,745 |

||||||||

|

American Express Co. Consumer Finance |

4,800 |

333,840 |

|||||||||

|

The Goldman Sachs Group, Inc. Investment Banking & Brokerage |

1,740 |

313,600 |

|||||||||

|

Capital One Financial Corp. Consumer Finance |

4,113 |

296,862 |

|||||||||

|

Bank of New York Mellon Corp. Asset Management & Custody Banks |

6,450 |

265,854 |

|||||||||

|

Franklin Resources, Inc. Asset Management & Custody Banks |

5,339 |

196,564 |

|||||||||

|

Ally Financial, Inc. (a) Consumer Finance |

10,456 |

194,909 |

|||||||||

|

T Rowe Price Group, Inc. Asset Management & Custody Banks |

2,547 |

182,069 |

|||||||||

|

2,127,443 |

|||||||||||

|

BANKS - 10.5% |

|||||||||||

|

Bank of America Corp. Diversified Banks |

35,500 |

597,465 |

|||||||||

|

Citigroup, Inc. Diversified Banks |

9,030 |

467,303 |

|||||||||

|

JPMorgan Chase & Co. Diversified Banks |

6,740 |

445,042 |

|||||||||

|

Wells Fargo & Co. Diversified Banks |

5,290 |

287,564 |

|||||||||

|

1,797,374 |

|||||||||||

|

INSURANCE - 7.5% |

|||||||||||

|

American International Group, Inc. Multi-line Insurance |

7,305 |

452,691 |

|||||||||

|

Aflac, Inc. Life & Health Insurance |

5,670 |

339,633 |

|||||||||

|

Aon PLC Insurance Brokers |

3,080 |

284,007 |

|||||||||

|

Principal Financial Group, Inc. Life & Health Insurance |

4,609 |

207,327 |

|||||||||

|

1,283,658 |

|||||||||||

|

5,208,475 |

|||||||||||

|

Shares |

Value |

||||||||||

|

INFORMATION TECHNOLOGY - 25.3% |

|||||||||||

|

SOFTWARE & SERVICES - 14.6% |

|||||||||||

|

MasterCard, Inc., Class A Data Processing & Outsourced Services |

4,450 |

$ |

433,252 |

||||||||

|

Visa, Inc., Class A Data Processing & Outsourced Services |

5,280 |

409,464 |

|||||||||

|

Alphabet, Inc., Class C (a) Internet Software & Services |

524 |

397,274 |

|||||||||

|

Microsoft Corp. Systems Software |

6,650 |

368,942 |

|||||||||

|

Automatic Data Processing, Inc. Data Processing & Outsourced Services |

4,320 |

365,990 |

|||||||||

|

Oracle Corp. Systems Software |

9,445 |

345,026 |

|||||||||

|

Alphabet, Inc., Class A (a) Internet Software & Services |

217 |

168,515 |

|||||||||

|

2,488,463 |

|||||||||||

|

SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT - 5.4% |

|||||||||||

|

Intel Corp. Semiconductors |

11,580 |

398,931 |

|||||||||

|

Texas Instruments, Inc. Semiconductors |

6,365 |

348,866 |

|||||||||

|

Applied Materials, Inc. Semiconductor Equipment |

9,260 |

172,884 |

|||||||||

|

920,681 |

|||||||||||

|

TECHNOLOGY HARDWARE & EQUIPMENT - 5.3% |

|||||||||||

|

Apple, Inc. Technology Hardware, Storage & Peripherals |

3,307 |

348,095 |

|||||||||

|

TE Connectivity, Ltd. Electronic Manufacturing Services |

5,036 |

325,353 |

|||||||||

|

QUALCOMM, Inc. Communications Equipment |

4,845 |

242,177 |

|||||||||

|

915,625 |

|||||||||||

|

4,324,769 |

|||||||||||

|

INDUSTRIALS - 10.9% |

|||||||||||

|

CAPITAL GOODS - 7.6% |

|||||||||||

|

General Electric Co. Industrial Conglomerates |

15,500 |

482,825 |

|||||||||

|

Caterpillar, Inc. Construction Machinery & Heavy Trucks |

4,400 |

299,024 |

|||||||||

|

Cummins, Inc. Construction Machinery & Heavy Trucks |

3,000 |

264,030 |

|||||||||

|

Parker-Hannifin Corp. Industrial Machinery |

2,539 |

246,257 |

|||||||||

|

1,292,136 |

|||||||||||

|

TRANSPORTATION - 3.3% |

|||||||||||

|

FedEx Corp. Air Freight & Logistics |

2,200 |

327,778 |

|||||||||

|

Union Pacific Corp. Railroads |

2,950 |

230,690 |

|||||||||

|

558,468 |

|||||||||||

|

1,850,604 |

|||||||||||

6 OAKMARK FUNDS

Oakmark Fund December 31, 2015 (Unaudited)

Schedule of Investments (in thousands) (continued)

|

Shares |

Value |

||||||||||

|

COMMON STOCKS - 95.0% (continued) |

|||||||||||

|

CONSUMER DISCRETIONARY - 9.8% |

|||||||||||

|

AUTOMOBILES & COMPONENTS - 3.7% |

|||||||||||

|

General Motors Co. Automobile Manufacturers |

7,850 |

$ |

266,978 |

||||||||

|

Fiat Chrysler Automobiles N.V. (a) Automobile Manufacturers |

16,000 |

223,840 |

|||||||||

|

Harley-Davidson, Inc. Motorcycle Manufacturers |

3,102 |

140,800 |

|||||||||

|

631,618 |

|||||||||||

|

MEDIA - 2.5% |

|||||||||||

|

News Corp., Class A Publishing |

19,704 |

263,247 |

|||||||||

|

Comcast Corp., Class A Cable & Satellite |

2,944 |

166,141 |

|||||||||

|

429,388 |

|||||||||||

|

RETAILING - 1.9% |

|||||||||||

|

Liberty Interactive Corp. QVC Group, Class A (a) Catalog Retail |

11,891 |

324,860 |

|||||||||

|

CONSUMER DURABLES & APPAREL - 1.7% |

|||||||||||

|

Whirlpool Corp. Household Appliances |

2,000 |

293,740 |

|||||||||

|

1,679,606 |

|||||||||||

|

ENERGY - 5.9% |

|||||||||||

|

Apache Corp. Oil & Gas Exploration & Production |

8,274 |

367,940 |

|||||||||

|

Anadarko Petroleum Corp. Oil & Gas Exploration & Production |

4,900 |

238,042 |

|||||||||

|

Halliburton Co. Oil & Gas Equipment & Services |

6,801 |

231,506 |

|||||||||

|

National Oilwell Varco, Inc. Oil & Gas Equipment & Services |

3,580 |

119,894 |

|||||||||

|

Chesapeake Energy Corp. Oil & Gas Exploration & Production |

12,000 |

54,000 |

|||||||||

|

1,011,382 |

|||||||||||

|

CONSUMER STAPLES - 5.8% |

|||||||||||

|

FOOD, BEVERAGE & TOBACCO - 4.4% |

|||||||||||

|

Nestle SA (b) Packaged Foods & Meats |

3,540 |

263,447 |

|||||||||

|

Diageo PLC (b) Distillers & Vintners |

2,250 |

245,407 |

|||||||||

|

General Mills, Inc. Packaged Foods & Meats |

4,066 |

234,447 |

|||||||||

|

743,301 |

|||||||||||

|

HOUSEHOLD & PERSONAL PRODUCTS - 1.4% |

|||||||||||

|

Unilever PLC (b) Personal Products |

5,613 |

242,032 |

|||||||||

|

985,333 |

|||||||||||

|

Shares |

Value |

||||||||||

|

HEALTH CARE - 5.1% |

|||||||||||

|

HEALTH CARE EQUIPMENT & SERVICES - 3.7% |

|||||||||||

|

Medtronic PLC Health Care Equipment |

4,190 |

$ |

322,295 |

||||||||

|

UnitedHealth Group, Inc. Managed Health Care |

2,590 |

304,687 |

|||||||||

|

626,982 |

|||||||||||

|

PHARMACEUTICALS, BIOTECHNOLOGY & LIFE SCIENCES - 1.4% |

|||||||||||

|

Sanofi (b) Pharmaceuticals |

5,670 |

241,826 |

|||||||||

|

868,808 |

|||||||||||

|

MATERIALS - 1.7% |

|||||||||||

|

Monsanto Co. Fertilizers & Agricultural Chemicals |

3,000 |

295,560 |

|||||||||

|

TOTAL COMMON STOCKS - 95.0% (COST $12,634,021) |

16,224,537 |

||||||||||

|

Par Value |

Value |

||||||||||

|

SHORT TERM INVESTMENTS - 5.0% |

|||||||||||

|

REPURCHASE AGREEMENT - 3.8% |

|||||||||||

|

Fixed Income Clearing Corp. Repurchase Agreement, 0.08% dated 12/31/15 due 01/04/16, repurchase price $648,078, collateralized by United States Treasury Notes, 1.375% - 1.750%, due 07/31/20 - 12/31/20, aggregate value plus accrued interest of $661,037 (Cost: $648,073) |

$ |

648,073 |

648,073 |

||||||||

|

GOVERNMENT AND AGENCY SECURITIES - 0.6% |

|||||||||||

|

United States Treasury Note, 0.02%, due 01/31/16 (c) (Cost $100,161) |

100,000 |

100,161 |

|||||||||

|

U.S. GOVERNMENT BILLS - 0.6% |

|||||||||||

|

United States Treasury Bills, 0.26%, due 03/10/16 (c) (Cost $99,950) |

100,000 |

99,978 |

|||||||||

|

TOTAL SHORT TERM INVESTMENTS - 5.0% (COST $848,184) |

848,212 |

||||||||||

|

TOTAL INVESTMENTS - 100.0% (COST $13,482,205) |

17,072,749 |

||||||||||

|

Other Assets In Excess of Liabilities - 0.0% (d) |

681 |

||||||||||

|

TOTAL NET ASSETS - 100.0% |

$ |

17,073,430 |

|||||||||

(a) Non-income producing security

(b) Sponsored American Depositary Receipt

(c) The rate shown represents the annualized yield at the time of purchase; not a coupon rate.

(d) Amount rounds to less than 0.1%.

Oakmark.com 7

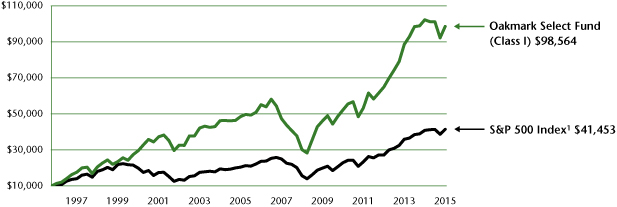

Oakmark Select Fund December 31, 2015

Summary Information

VALUE OF A $10,000 INVESTMENT

Since Inception - 11/01/96 (Unaudited)

PERFORMANCE

|

Average Annual Total Returns (as of 12/31/15) |

|||||||||||||||||||||||||||||||

|

(Unaudited) |

Total Return Last 3 Months |

1-year |

3-year |

5-year |

10-year |

Since Inception |

Inception Date |

||||||||||||||||||||||||

|

Oakmark Select Fund (Class I) |

6.90 |

% |

-3.58 |

% |

14.95 |

% |

13.56 |

% |

7.34 |

% |

12.68 |

% |

11/01/96 |

||||||||||||||||||

|

S&P 500 Index |

7.04 |

% |

1.38 |

% |

15.13 |

% |

12.57 |

% |

7.31 |

% |

7.70 |

% |

|||||||||||||||||||

|

Lipper Multi-Cap Value Funds Index6 |

3.76 |

% |

-4.53 |

% |

12.24 |

% |

9.71 |

% |

5.23 |

% |

7.16 |

% |

|||||||||||||||||||

|

Oakmark Select Fund (Class II) |

6.80 |

% |

-3.94 |

% |

14.60 |

% |

13.22 |

% |

7.04 |

% |

9.05 |

% |

12/31/99 |

||||||||||||||||||

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Past performance is no guarantee of future results. The performance data quoted represents past performance. Current performance may be lower or higher than the performance data quoted. Total return includes change in share prices and, in each case, includes reinvestment of dividends and capital gain distributions. The investment return and principal value vary so that an investor's shares when redeemed may be worth more or less than the original cost. To obtain the most recent month-end performance, please visit Oakmark.com.

|

TOP TEN EQUITY HOLDINGS4 |

% of Net Assets |

||||||

|

Alphabet Inc., Class C |

8.0 |

||||||

|

General Electric Co. |

7.7 |

||||||

|

American International Group, Inc. |

6.5 |

||||||

|

Bank of America Corp. |

6.1 |

||||||

|

TE Connectivity, Ltd. |

6.0 |

||||||

|

JPMorgan Chase & Co. |

5.9 |

||||||

|

Citigroup, Inc. |

5.8 |

||||||

|

CBRE Group, Inc. Class A |

5.3 |

||||||

|

MasterCard, Inc., Class A |

5.1 |

||||||

|

FNF Group |

4.7 |

||||||

|

FUND STATISTICS |

|||||||

|

Ticker |

OAKLX |

||||||

|

Inception |

11/01/96 |

||||||

|

Number of Equity Holdings |

19 |

||||||

|

Net Assets |

$5.8 billion | ||||||

|

Benchmark |

S&P 500 Index |

||||||

|

Weighted Average Market Cap |

$140.1 billion | ||||||

|

Median Market Cap |

$43.3 billion | ||||||

|

Portfolio Turnover (for the 12-months ended 09/30/15) |

46% | ||||||

|

Expense Ratio - Class I (as of 09/30/14) |

0.95% | ||||||

|

Expense Ratio - Class I (as of 09/30/15) |

0.95% | ||||||

|

SECTOR ALLOCATION |

% of Net Assets |

||||||

|

Financials |

38.1 |

||||||

|

Information Technology |

27.0 |

||||||

|

Consumer Discretionary |

8.2 |

||||||

|

Industrials |

7.8 |

||||||

|

Energy |

6.4 |

||||||

|

Materials |

3.4 |

||||||

|

Utilities |

3.2 |

||||||

|

Short-Term Investments and Other |

5.9 |

||||||

8 OAKMARK FUNDS

Oakmark Select Fund December 31, 2015

Portfolio Manager Commentary

William C. Nygren, CFA

Portfolio Manager

oaklx@oakmark.com

Anthony P. Coniaris, CFA

Portfolio Manager

oaklx@oakmark.com

Win Murray

Portfolio Manager

oaklx@oakmark.com

The Oakmark Select Fund returned 7% for the quarter which matched the S&P 500 Index's1 return. For all of calendar 2015, the Oakmark Select Fund declined by 4%, compared to a 1% gain for the S&P 500 Index.

Our top performers in the quarter, each up by at least 24%, were Alphabet (formerly known as Google), General Electric (GE), and Amazon. Alphabet and GE ended the quarter as the two largest positions in the Fund, and we believe both investments remain substantively undervalued, possess strong fundamentals, and are run by excellent management teams. We've always believed that Alphabet's highly valuable search business makes more money than investors give it credit for, and the company's new reporting structure should better highlight this profit stream. General Electric, meanwhile, is completing its portfolio transformation by selling off finance assets, acquiring what we believe is a quality industrial asset at a great price (Alstom), and buying back stock with proceeds from its Synchrony share exchange. We expect the newly refocused GE to have significant margin expansion potential over the next few years.

We eliminated our Amazon stake during the quarter, as the stock's rapid climb in 2015 brought the shares up to our estimate of intrinsic value. While our holding period for Amazon (first purchased in the Fund in the second quarter of 2014) was much shorter than is typical for us, we've always said that turnover is simply a byproduct of the length of time required for price to converge with value. We'll happily show high turnover when it is the result of rapid stock price appreciation. We reinvested the Amazon proceeds across existing holdings, ending the quarter with investments in 19 companies; the Fund generally holds about 20 positions.

Our worst quarterly performer by far was Chesapeake Energy, down 39%, while only two other positions declined—FNF Group down 2% and Calpine down 1%. In our opinion, commodity prices have fallen to levels which, if permanent, would bankrupt much of the exploration and production sector of the oil and gas industry. However, we believe commodity prices will rise and that many investments made today in this industry will prove quite rewarding. That said, given Chesapeake's financial obligations, it is without question a much riskier investment than we normally hold. Securities across Chesapeake's capital structure have all declined sharply and, in our opinion, are now all attractively priced. We've shifted some of our position from common stock to somewhat less risky preferred stock, which we believe reduces risk without forfeiting upside potential.

While the Fund's full-year performance wasn't as strong as we would've liked, it's worth noting that our pre-tax and after-tax returns were very similar, despite realizing large gains throughout the year in investments such as FedEx, Medtronic, and Amazon. We actively monetized losses, where appropriate, so that we could eliminate the need for capital gains distributions this year.

Thank you, our fellow shareholders, for your continued investment in our Fund. Best wishes for a happy and prosperous 2016.

Oakmark.com 9

Oakmark Select Fund December 31, 2015 (Unaudited)

Schedule of Investments (in thousands)

|

Shares |

Value |

||||||||||

|

COMMON STOCKS - 93.1% |

|||||||||||

|

FINANCIALS - 38.1% |

|||||||||||

|

BANKS - 17.8% |

|||||||||||

|

Bank of America Corp. Diversified Banks |

20,979 |

$ |

353,070 |

||||||||

|

JPMorgan Chase & Co. Diversified Banks |

5,230 |

345,337 |

|||||||||

|

Citigroup, Inc. Diversified Banks |

6,577 |

340,360 |

|||||||||

|

1,038,767 |

|||||||||||

|

INSURANCE - 11.2% |

|||||||||||

|

American International Group, Inc. Multi-line Insurance |

6,145 |

380,818 |

|||||||||

|

FNF Group Property & Casualty Insurance |

7,821 |

271,161 |

|||||||||

|

651,979 |

|||||||||||

|

REAL ESTATE - 5.3% |

|||||||||||

|

CBRE Group, Inc., Class A (a) Real Estate Services |

8,964 |

309,975 |

|||||||||

|

DIVERSIFIED FINANCIALS - 3.8% |

|||||||||||

|

Capital One Financial Corp. Consumer Finance |

3,050 |

220,149 |

|||||||||

|

2,220,870 |

|||||||||||

|

INFORMATION TECHNOLOGY - 27.0% |

|||||||||||

|

SOFTWARE & SERVICES - 17.2% |

|||||||||||

|

Alphabet, Inc., Class C (a) Internet Software & Services |

616 |

467,205 |

|||||||||

|

MasterCard, Inc., Class A Data Processing & Outsourced Services |

3,075 |

299,382 |

|||||||||

|

Oracle Corp. Systems Software |

6,540 |

238,906 |

|||||||||

|

1,005,493 |

|||||||||||

|

TECHNOLOGY HARDWARE & EQUIPMENT - 6.0% |

|||||||||||

|

TE Connectivity, Ltd. Electronic Manufacturing Services |

5,394 |

348,502 |

|||||||||

|

SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT - 3.8% |

|||||||||||

|

Intel Corp. Semiconductors |

6,447 |

222,099 |

|||||||||

|

1,576,094 |

|||||||||||

|

INDUSTRIALS - 7.8% |

|||||||||||

|

CAPITAL GOODS - 7.8% |

|||||||||||

|

General Electric Co. Industrial Conglomerates |

14,500 |

451,675 |

|||||||||

|

CONSUMER DISCRETIONARY - 7.3% |

|||||||||||

|

RETAILING - 4.3% |

|||||||||||

|

Liberty Interactive Corp. QVC Group, Class A (a) Catalog Retail |

9,214 |

251,723 |

|||||||||

|

Shares |

Value |

||||||||||

|

AUTOMOBILES & COMPONENTS - 3.0% |

|||||||||||

|

Fiat Chrysler Automobiles N.V. (a) Automobile Manufacturers |

12,470 |

$ |

174,462 |

||||||||

|

426,185 |

|||||||||||

|

ENERGY - 6.3% |

|||||||||||

|

Apache Corp. Oil & Gas Exploration & Production |

5,310 |

236,136 |

|||||||||

|

Chesapeake Energy Corp. (b) Oil & Gas Exploration & Production |

29,075 |

130,837 |

|||||||||

|

366,973 |

|||||||||||

|

MATERIALS - 3.4% |

|||||||||||

|

Monsanto Co. Fertilizers & Agricultural Chemicals |

2,000 |

197,040 |

|||||||||

|

UTILITIES - 3.2% |

|||||||||||

|

Calpine Corp. (a) Independent Power Producers & Energy Traders |

13,004 |

188,174 |

|||||||||

|

TOTAL COMMON STOCKS - 93.1% (COST $3,934,205) |

5,427,011 |

||||||||||

|

PREFERRED STOCKS - 0.1% |

|||||||||||

|

ENERGY - 0.1% |

|||||||||||

|

Chesapeake Energy Corp., 5.75% Oil & Gas Exploration & Production |

37 |

7,021 |

|||||||||

|

TOTAL PREFERRED STOCKS - 0.1% (COST $7,522) |

7,021 |

||||||||||

|

Par Value |

Value |

||||||||||

|

FIXED INCOME - 0.9% |

|||||||||||

|

CONVERTIBLE BOND - 0.9% |

|||||||||||

|

Fiat Chrysler Automobiles N.V., 7.875%, due 12/15/16 (Cost $57,052) |

$ |

45,779 |

53,029 |

||||||||

|

TOTAL FIXED INCOME - 0.9% (COST $57,052) |

53,029 |

||||||||||

|

SHORT TERM INVESTMENTS - 5.8% |

|||||||||||

|

REPURCHASE AGREEMENT - 5.8% |

|||||||||||

|

Fixed Income Clearing Corp. Repurchase Agreement, 0.08% dated 12/31/15 due 01/04/16, repurchase price $337,837, collateralized by United States Treasury Notes, 1.625% - 3.125%, due 10/31/16 - 07/31/20, aggregate value plus accrued interest of $344,594 (Cost: $337,834) |

337,834 |

337,834 |

|||||||||

|

TOTAL SHORT TERM INVESTMENTS - 5.8% (COST $337,834) |

337,834 |

||||||||||

|

TOTAL INVESTMENTS - 99.9% (COST $4,336,613) |

5,824,895 |

||||||||||

|

Other Assets In Excess of Liabilities - 0.1% |

4,463 |

||||||||||

|

TOTAL NET ASSETS - 100.0% |

$ |

5,829,358 |

|||||||||

(a) Non-income producing security

(b) A portion of the security out on loan.

10 OAKMARK FUNDS

This page intentionally left blank.

Oakmark.com 11

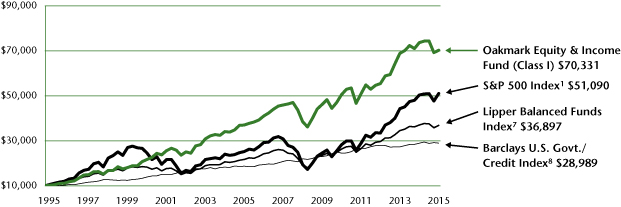

Oakmark Equity and Income Fund December 31, 2015

Summary Information

VALUE OF A $10,000 INVESTMENT

Since Inception - 11/01/95 (Unaudited)

PERFORMANCE

|

Average Annual Total Returns (as of 12/31/15) |

|||||||||||||||||||||||||||||||

|

(Unaudited) |

Total Return Last 3 Months |

1-year |

3-year |

5-year |

10-year |

Since Inception |

Inception Date |

||||||||||||||||||||||||

|

Oakmark Equity and Income Fund (Class I) |

1.55 |

% |

-4.60 |

% |

8.22 |

% |

6.82 |

% |

6.62 |

% |

10.16 |

% |

11/01/95 |

||||||||||||||||||

|

Lipper Balanced Funds Index |

2.98 |

% |

-0.42 |

% |

7.51 |

% |

6.98 |

% |

5.43 |

% |

6.69 |

% |

|||||||||||||||||||

|

S&P 500 Index |

7.04 |

% |

1.38 |

% |

15.13 |

% |

12.57 |

% |

7.31 |

% |

8.42 |

% |

|||||||||||||||||||

|

Barclays U.S. Govt./Credit Index |

-0.74 |

% |

0.15 |

% |

1.21 |

% |

3.39 |

% |

4.47 |

% |

5.42 |

% |

|||||||||||||||||||

|

Oakmark Equity and Income Fund (Class II) |

1.46 |

% |

-4.90 |

% |

7.87 |

% |

6.48 |

% |

6.27 |

% |

8.32 |

% |

07/12/00 |

||||||||||||||||||

The graph and table above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Past performance is no guarantee of future results. The performance data quoted represents past performance. Current performance may be lower or higher than the performance data quoted. Total return includes change in share prices and, in each case, includes reinvestment of dividends and capital gain distributions. The investment return and principal value vary so that an investor's shares when redeemed may be worth more or less than the original cost. To obtain the most recent month-end performance, please visit Oakmark.com.

|

TOP TEN EQUITY HOLDINGS4 |

% of Net Assets |

||||||

|

General Motors Co. |

4.2 |

||||||

|

Bank of America Corp. |

4.1 |

||||||

|

Oracle Corp. |

3.7 |

||||||

|

Nestle ADR |

3.4 |

||||||

|

TE Connectivity, Ltd. |

2.8 |

||||||

|

CVS Health Corp. |

2.8 |

||||||

|

Foot Locker, Inc. |

2.4 |

||||||

|

Dover Corp. |

2.2 |

||||||

|

MasterCard, Inc., Class A |

2.0 |

||||||

|

TD Ameritrade Holding Corp. |

1.9 |

||||||

|

FUND STATISTICS |

|||||||

|

Ticker |

OAKBX |

||||||

|

Inception |

11/01/95 |

||||||

|

Number of Equity Holdings |

49 |

||||||

|

Net Assets |

$17.6 billion | ||||||

|

Benchmark |

Lipper Balanced Funds Index |

||||||

|

Weighted Average Market Cap |

$74.5 billion | ||||||

|

Median Market Cap |

$13.2 billion | ||||||

|

Portfolio Turnover (for the 12-months ended 09/30/15) |

25% | ||||||

|

Expense Ratio - Class I (as of 09/30/14) |

0.74% | ||||||

|

Expense Ratio - Class I (as of 09/30/15) |

0.75% | ||||||

|

SECTOR ALLOCATION |

% of Net Assets |

||||||

|

Equity Investments |

|||||||

|

Financials |

16.3 |

||||||

|

Consumer Discretionary |

10.8 |

||||||

|

Industrials |

10.3 |

||||||

|

Consumer Staples |

9.5 |

||||||

|

Information Technology |

9.1 |

||||||

|

Energy |

2.7 |

||||||

|

Health Care |

2.2 |

||||||

|

Materials |

0.4 |

||||||

|

Total Equity Investments |

61.3 |

||||||

|

Fixed Income Investments |

|||||||

|

Corporate Bonds |

9.2 |

||||||

|

Government and Agency Securities |

8.9 |

||||||

|

Asset Backed Securities |

0.1 |

||||||

|

Total Fixed Income Investments |

18.2 |

||||||

|

Short-Term Investments and Other |

20.5 |

||||||

12 OAKMARK FUNDS

Oakmark Equity and Income Fund December 31, 2015

Portfolio Manager Commentary

Clyde S. McGregor, CFA

Portfolio Manager

oakbx@oakmark.com

M. Colin Hudson, CFA

Portfolio Manager

oakbx@oakmark.com

Matthew A. Logan, CFA

Portfolio Manager

oakbx@oakmark.com

Edward J. Wojciechowski, CFA

Portfolio Manager

oakbx@oakmark.com

A Very Narrow Year

2015 was a year that market technicians describe as having bad breadth. Simply put, this means that the capitalization-weighted averages earned positive returns, but the majority of stocks lost money. This phenomenon occurs occasionally (see 1999, for example), but 2015 was probably a more extreme case in that a very small number of stocks succeeded in holding the market up. If one owned equal amounts of the 10 largest companies as of the end of the calendar year, the return was approximately 20%. Owning the remaining 490 issues in the S&P 5001 resulted in a loss (before dividends) of roughly 3%. The composite outcome in this circumstance was a very tight return range for the year, and momentum and growth factors trounced traditional value characteristics.

After the market's decline in the September quarter, the December quarter experienced a recovery, albeit with the momentum-versus-value dichotomy still firmly in place. Perhaps the defining event of the quarter (in financial terms) was the Federal Reserve's decision to increase short-term interest rates. This was the first rate increase since 2006. A prominent bank CEO noted that the majority of his employees had never seen a rate increase during their professional careers.

The Equity and Income Fund earned 2% in the quarter, which contrasts to a 3% gain for the Lipper Balanced Fund Index7, the Fund's performance benchmark. For calendar 2015 as a whole, the Fund showed a loss of 5%, compared to a small loss for the Lipper Index. We are pleased to report that the annualized compound rate of return since the Fund's inception in 1995 is 10% while the corresponding return to the Lipper Index is 7%.

As noted above, for investors to thrive in 2015, they needed to own a small group of the largest companies. We did not, finding those companies' valuations to be inconsistent with the Equity and Income Fund's mandate. Weak energy and commodity markets hurt a wide range of companies in the Fund, including companies with rather indirect exposure. In our opinion, these share price declines were out of proportion with any actual reduction in business value.

General Motors, Bank of America, TE Connectivity, Lear and Bruker led the list of contributors to return in the quarter. Foot Locker led the detractors (despite reporting strong earnings). Other detractors included Baker Hughes, Union Pacific, HSN and Reinsurance Group of America. For calendar 2015, Glencore, National Oilwell Varco, Oracle, Union Pacific and Flowserve detracted most from return. The largest contributors to annual portfolio return were Lear, United Health Group,

Omnicare (which CVS Health purchased for cash during the year), Foot Locker and MasterCard Class A.

20-Year Retrospective

For the writer of this section, it is hard to believe that the Equity and Income Fund opened for business just over 20 years ago. In the first quarterly report for the Fund, I stated objectives of producing attractive rates of return with attention to preservation of capital and current income. As noted above, the Fund has generated a compound rate of return of 10% over its 20-year history. While I certainly would like to have done better, I am satisfied that clients could meet their economic needs with that rate of return, particularly given that price inflation in the general economy has stayed low. Compared to my expectations in 1995, both the volatility of this return stream and the equity contribution to portfolio return have been higher. Perhaps the key macro factor that I did not foresee was the long-term suppression of interest rates that began nine years ago. Back in 1995, I naively believed that fixed income investments could be expected to produce yields of 6% over the Fund's life. I also did not predict the shift in emphasis at many companies from dividends to share repurchases. Although share repurchase has been helpful to the total return of many of the Fund's equity holdings, it does nothing for the Fund's current income generation. As I look back, it is this shortfall of current income that has disappointed me most.

The Fund's first report set three guiding principles for investing that are still in force today:

1. A balanced fund such as the Equity and Income Fund is an integrated unit. We understand the portfolio in its entirety, not as an aggregation of different types of securities. All securities appropriate for the objectives of this Fund compete for space within the portfolio. A word sometimes used in our industry that we find objectionable is "silo." In this Fund, there are no silos.

2. Our ability to identify attractive investment opportunities drives the Fund's asset allocation. At Harris Associates, our investing process has always moved from the bottom up, and this is a key differentiating factor for the Equity and Income Fund. If attractive stocks are plentiful, the Fund's equity allocation will approach its maximum. Or, should expected returns from bonds become compelling, we will move the Fund in that direction. Accordingly, the Fund's asset allocation to equities has ranged from a high of 75% (the prospectus maximum) to a low of around 48% over the Fund's history. Investors should

Oakmark.com 13

Oakmark Equity and Income Fund December 31, 2015

Portfolio Manager Commentary (continued)

expect consistency of investing philosophy and style, not a stable asset allocation.

3. We do not equate volatility with risk. For us, fluctuations in share prices do not define the riskiness of an issue. We think of risk as the probability of losing money in an investment. For all 20 years, we have focused on minimizing downside risk while positioning the portfolio to capture upside volatility.

We still believe that this sort of multi-asset class fund offers considerable utility to investors. It can be a complete investing program or the core holding of a more complex portfolio.

To close this retrospective, I must thank the scores of colleagues who have helped this Fund to be successful. Harris Associates' research department originates all of the ideas that eventually populate the Fund. I am deeply grateful for the many good recommendations that our team of analysts has provided over the past 20 years. I also thank my team of co-managers for the past 21/2 years, and I look forward to more years of collaboration. Finally, I must again express my deep gratitude to my retired co-manager of the Fund, Edward A. Studzinski, for his many years of contributing to the Fund's success.

Transaction Activity

We initiated three new holdings in the quarter: Ally Financial, Gaming and Leisure Properties, and Oshkosh. Ally was originally founded nearly a century ago as General Motors Acceptance Corporation. Its purpose then was to provide financing to GM dealers and retail customers. Today, Ally's purpose is largely the same except that it is no longer owned by GM and now serves dealers and customers of many other automobile manufacturers, such as Ford, Chrysler, and Toyota. Since Ally's initial public offering in spring 2014, its shares have fallen over 20% while the S&P 500 has increased by over 15%. Over this period, some investors have grown concerned that the business is at a cyclical peak, as U.S. auto sales are near record levels and credit losses are below long-term averages; as a result, some believe Ally's earnings have nowhere to go but down. But we believe cyclical pressures will be offset by continued internal improvements, such as funding cost reductions (as "legacy" liabilities are replaced with lower cost borrowings) and capital actions. With Ally's stock trading at just 80% of tangible book value, we believe Ally is a compelling investment opportunity.

Gaming and Leisure Properties (GLPI) is a triple net real estate investment trust (REIT), formed from the tax-free spin-off of the real estate assets of Penn National Gaming. It is currently trading at a sizable discount to our estimate of its intrinsic worth, as well as peer valuations. The discount stems from the newness of the regional gaming industry to the REIT category, interest rate concerns and the overhang created by an upcoming equity issuance associated with a recent acquisition. In our opinion, regional casinos' cash flows are well suited to the REIT structure, and we expect investors to appreciate this better in time. We believe that the equity financing will be completed in the first half of 2016, which will reduce investor uncertainty. GLPI is run by CEO Peter Carlino and CFO Bill Clifford—two proven value creators. With their leadership, GLPI should have significant consolidation opportunities ahead. Finally, GLPI pays an attractive dividend with a yield of 7.7%.

Oshkosh manufactures aerial work platforms (access equipment), fire and emergency vehicles, heavy-duty commercial vehicles, and military vehicles. Access equipment generates the majority of corporate profits. This business correlates closely with non-residential housing construction but also benefits from increasing housing starts. The defense business offers significant upside to Oshkosh. In August, the Department of Defense awarded Oshkosh the contract for its Joint Light Tactical Vehicle program, which will replace the Humvees currently used by the Army and Marines. Lockheed Martin has protested this contract award, so the ultimate outcome is uncertain. In the event that Oshkosh prevails, the large size of this program should prove quite rewarding.

As always, we thank our fellow shareholders for investing in the Equity and Income Fund. We especially thank those of you who have been with us for the past 20 years.

14 OAKMARK FUNDS

Oakmark Equity and Income Fund December 31, 2015 (Unaudited)

Schedule of Investments (in thousands)

|

Shares |

Value |

||||||||||

|

COMMON STOCKS - 61.3% |

|||||||||||

|

FINANCIALS - 16.3% |

|||||||||||

|

BANKS - 6.4% |

|||||||||||

|

Bank of America Corp. Diversified Banks |

42,798 |

$ |

720,282 |

||||||||

|

U.S. Bancorp Diversified Banks |

5,169 |

220,574 |

|||||||||

|

Wells Fargo & Co. Diversified Banks |

3,299 |

179,344 |

|||||||||

|

1,120,200 |

|||||||||||

|

DIVERSIFIED FINANCIALS - 5.4% |

|||||||||||

|

TD Ameritrade Holding Corp. Investment Banking & Brokerage |

9,880 |

342,937 |

|||||||||

|

The Goldman Sachs Group, Inc. Investment Banking & Brokerage |

1,568 |

282,637 |

|||||||||

|

Bank of New York Mellon Corp. Asset Management & Custody Banks |

5,340 |

220,134 |

|||||||||

|

Ally Financial, Inc. (a) Consumer Finance |

4,267 |

79,541 |

|||||||||

|

T Rowe Price Group, Inc. Asset Management & Custody Banks |

474 |

33,881 |

|||||||||

|

959,130 |

|||||||||||

|

INSURANCE - 4.0% |

|||||||||||

|

FNF Group Property & Casualty Insurance |

8,081 |

280,182 |

|||||||||

|

Principal Financial Group, Inc. Life & Health Insurance |

5,061 |

227,657 |

|||||||||

|

Reinsurance Group of America, Inc. Reinsurance |

2,402 |

205,500 |

|||||||||

|

713,339 |

|||||||||||

|

REAL ESTATE - 0.5% |

|||||||||||

|

The Howard Hughes Corp. (a) Real Estate Development |

479 |

54,209 |

|||||||||

|

Gaming and Leisure Properties, Inc. Specialized REIT's |

982 |

27,286 |

|||||||||

|

81,495 |

|||||||||||

|

2,874,164 |

|||||||||||

|

CONSUMER DISCRETIONARY - 10.8% |

|||||||||||

|

AUTOMOBILES & COMPONENTS - 6.9% |

|||||||||||

|

General Motors Co. Automobile Manufacturers |

21,666 |

736,874 |

|||||||||

|

BorgWarner, Inc. Auto Parts & Equipment |

7,718 |

333,662 |

|||||||||

|

Lear Corp. Auto Parts & Equipment |

1,161 |

142,634 |

|||||||||

|

1,213,170 |

|||||||||||

|

RETAILING - 3.1% |

|||||||||||

|

Foot Locker, Inc. Apparel Retail |

6,369 |

414,558 |

|||||||||

|

HSN, Inc. Catalog Retail |

2,491 |

126,231 |

|||||||||

|

540,789 |

|||||||||||

|

Shares |

Value |

||||||||||

|

CONSUMER DURABLES & APPAREL - 0.8% |

|||||||||||

|

Kate Spade & Co. (a) Apparel, Accessories & Luxury Goods |

4,691 |

$ |

83,364 |

||||||||

|

Carter's, Inc. Apparel, Accessories & Luxury Goods |

664 |

59,143 |

|||||||||

|

142,507 |

|||||||||||

|

1,896,466 |

|||||||||||

|

INDUSTRIALS - 10.3% |

|||||||||||

|

CAPITAL GOODS - 8.7% |

|||||||||||

|

Dover Corp. Industrial Machinery |

6,366 |

390,284 |

|||||||||

|

Flowserve Corp. Industrial Machinery |

7,338 |

308,775 |

|||||||||

|

Rockwell Automation, Inc. Electrical Components & Equipment |

2,145 |

220,099 |

|||||||||

|

Parker-Hannifin Corp. Industrial Machinery |

1,638 |

158,849 |

|||||||||

|

Precision Castparts Corp. Aerospace & Defense |

612 |

141,897 |

|||||||||

|

General Electric Co. Industrial Conglomerates |

3,834 |

119,432 |

|||||||||

|

The Manitowoc Co., Inc. Construction Machinery & Heavy Trucks |

6,243 |

95,827 |

|||||||||

|

WESCO International, Inc. (a) Trading Companies & Distributors |

1,118 |

48,817 |

|||||||||

|

Oshkosh Corp. Construction Machinery & Heavy Trucks |

912 |

35,589 |

|||||||||

|

Blount International, Inc. (a) Industrial Machinery |

1,913 |

18,771 |

|||||||||

|

1,538,340 |

|||||||||||

|

TRANSPORTATION - 1.4% |

|||||||||||

|

Union Pacific Corp. Railroads |

3,086 |

241,341 |

|||||||||

|

COMMERCIAL & PROFESSIONAL SERVICES - 0.2% |

|||||||||||

|

Herman Miller, Inc. Office Services & Supplies |

1,350 |

38,742 |

|||||||||

|

1,818,423 |

|||||||||||

|

CONSUMER STAPLES - 9.5% |

|||||||||||

|

FOOD, BEVERAGE & TOBACCO - 6.8% |

|||||||||||

|

Nestle SA (b) Packaged Foods & Meats |

7,993 |

594,839 |

|||||||||

|

Philip Morris International, Inc. Tobacco |

3,806 |

334,612 |

|||||||||

|

Diageo PLC (b) Distillers & Vintners |

2,441 |

266,288 |

|||||||||

|

1,195,739 |

|||||||||||

|

FOOD & STAPLES RETAILING - 2.7% |

|||||||||||

|

CVS Health Corp. Drug Retail |

4,993 |

488,122 |

|||||||||

|

1,683,861 |

|||||||||||

Oakmark.com 15

Oakmark Equity and Income Fund December 31, 2015 (Unaudited)

Schedule of Investments (in thousands) (continued)

|

Shares |

Value |

||||||||||

|

COMMON STOCKS - 61.3% (continued) |

|||||||||||

|

INFORMATION TECHNOLOGY - 9.1% |

|||||||||||

|

SOFTWARE & SERVICES - 6.1% |

|||||||||||

|

Oracle Corp. Systems Software |

17,795 |

$ |

650,052 |

||||||||

|

MasterCard, Inc., Class A Data Processing & Outsourced Services |

3,703 |

360,483 |

|||||||||

|

Broadridge Financial Solutions, Inc. Data Processing & Outsourced Services |

1,261 |

67,750 |

|||||||||

|

1,078,285 |

|||||||||||

|

TECHNOLOGY HARDWARE & EQUIPMENT - 3.0% |

|||||||||||

|

TE Connectivity, Ltd. Electronic Manufacturing Services |

7,641 |

493,685 |

|||||||||

|

Knowles Corp. (a) Electronic Components |

1,857 |

24,751 |

|||||||||

|

518,436 |

|||||||||||

|

1,596,721 |

|||||||||||

|

ENERGY - 2.7% |

|||||||||||

|

Baker Hughes, Inc. Oil & Gas Equipment & Services |

6,736 |

310,844 |

|||||||||

|

Oceaneering International, Inc. Oil & Gas Equipment & Services |

2,312 |

86,735 |

|||||||||

|

National Oilwell Varco, Inc. Oil & Gas Equipment & Services |

1,700 |

56,920 |

|||||||||

|

Rowan Cos. PLC Oil & Gas Drilling |

1,491 |

25,279 |

|||||||||

|

479,778 |

|||||||||||

|

HEALTH CARE - 2.2% |

|||||||||||

|

HEALTH CARE EQUIPMENT & SERVICES - 1.6% |

|||||||||||

|

UnitedHealth Group, Inc. Managed Health Care |

2,445 |

287,634 |

|||||||||

|

PHARMACEUTICALS, BIOTECHNOLOGY & LIFE SCIENCES - 0.6% |

|||||||||||

|

Bruker Corp. (a) Life Sciences Tools & Services |

4,077 |

98,941 |

|||||||||

|

386,575 |

|||||||||||

|

MATERIALS - 0.4% |

|||||||||||

|

Glencore PLC Diversified Metals & Mining |

55,555 |

74,103 |

|||||||||

|

Southern Copper Corp. Diversified Metals & Mining |

98 |

2,562 |

|||||||||

|

76,665 |

|||||||||||

|

TOTAL COMMON STOCKS - 61.3% (COST $7,639,331) |

10,812,653 |

||||||||||

|

Par Value |

Value |

||||||||||

|

FIXED INCOME - 18.2% |

|||||||||||

|

CORPORATE BONDS - 9.2% |

|||||||||||

|

Kinetic Concepts, Inc., 10.50%, due 11/01/18 |

$ |

47,940 |

46,742 |

||||||||

|

Par Value |

Value |

||||||||||

|

JPMorgan Chase & Co., 3.15%, due 07/05/16 |

$ |

44,592 |

$ |

45,053 |

|||||||

|

Mondelez International, Inc., 4.125%, due 02/09/16 |

43,567 |

43,679 |

|||||||||

|

General Motors Co., 4.875%, due 10/02/23 |

41,400 |

42,338 |

|||||||||

|

Omega Healthcare Investors, Inc., 5.875%, due 03/15/24 |

39,292 |

40,667 |

|||||||||

|

Zimmer Biomet Holdings, Inc., 1.45%, due 04/01/17 |

37,671 |

37,488 |

|||||||||

|

The Manitowoc Co., Inc., 8.50%, due 11/01/20 |

35,655 |

36,903 |

|||||||||

|

The William Carter Co., 5.25%, due 08/15/21 |

35,137 |

36,103 |

|||||||||

|

Credit Suisse Group AG, 144A, 7.50% (c) (d) (e) |

30,000 |

31,495 |

|||||||||

|

Bank of America Corp., 5.625%, due 10/14/16 |

29,855 |

30,800 |

|||||||||

|

Omnicom Group, Inc., 3.625%, due 05/01/22 |

30,425 |

30,712 |

|||||||||

|

CVS Health Corp., 4.00%, due 12/05/23 |

29,325 |

30,475 |

|||||||||

|

1011778 BC ULC / New Red Finance, Inc., 144A, 6.00%, due 04/01/22 (c) |

29,500 |

30,385 |

|||||||||

|

Live Nation Entertainment, Inc., 144A, 7.00%, due 09/01/20 (c) |

28,930 |

29,943 |

|||||||||

|

General Motors Co., 3.50%, due 10/02/18 |

29,525 |

29,821 |

|||||||||

|

Toyota Motor Credit Corp., 1.45%, due 01/12/18 |

29,495 |

29,439 |

|||||||||

|

Activision Blizzard, Inc., 144A, 5.625%, due 09/15/21 (c) |

26,745 |

28,015 |

|||||||||

|

Credit Suisse Group Funding Guernsey, Ltd., 144A, 3.125%, due 12/10/20 (c) |

25,000 |

24,886 |

|||||||||

|

Credit Suisse New York, 1.75%, due 01/29/18 |

24,700 |

24,631 |

|||||||||

|

Penn National Gaming, Inc., 5.875%, due 11/01/21 |

23,704 |

22,993 |

|||||||||

|

Whirlpool Corp., 7.75%, due 07/15/16 |

22,256 |

22,947 |

|||||||||

|

Expedia, Inc., 144A, 5.00%, due 02/15/26 (c) |

23,445 |

22,881 |

|||||||||

|

E*TRADE Financial Corp., 5.375%, due 11/15/22 |

20,605 |

21,584 |

|||||||||

|

Thermo Fisher Scientific, Inc., 2.25%, due 08/15/16 |

21,438 |

21,555 |

|||||||||

|

Delphi Corp., 5.00%, due 02/15/23 |

20,277 |

21,453 |

|||||||||

|

Anadarko Petroleum Corp., 5.95%, due 09/15/16 |

20,821 |

21,395 |

|||||||||

|

Bank of America Corp., 3.75%, due 07/12/16 |

20,295 |

20,549 |

|||||||||

|

JPMorgan Chase Bank NA, 0.902%, due 06/14/17 (d) |

19,750 |

19,672 |

|||||||||

|

CBRE Services, Inc., 4.875%, due 03/01/26 |

19,665 |

19,589 |

|||||||||

|

JPMorgan Chase & Co., 1.70%, due 03/01/18 |

19,665 |

19,570 |

|||||||||

|

Centene Corp., 4.75%, due 05/15/22 |

20,084 |

19,431 |

|||||||||

16 OAKMARK FUNDS

Oakmark Equity and Income Fund December 31, 2015 (Unaudited)

Schedule of Investments (in thousands) (continued)

|

Par Value |

Value |

||||||||||

|

FIXED INCOME - 18.2% (continued) |

|||||||||||

|

CORPORATE BONDS - 9.2% (continued) |

|||||||||||

|

Lam Research Corp., 2.75%, due 03/15/20 |

$ |

19,660 |

$ |

19,013 |

|||||||

|

DIRECTV Holdings LLC / DIRECTV Financing Co., Inc., 5.00%, due 03/01/21 |

16,710 |

18,020 |

|||||||||

|

Dollar General Corp., 4.125%, due 07/15/17 |

17,095 |

17,555 |

|||||||||

|

McGraw Hill Financial, Inc., 4.00%, due 06/15/25 |

17,150 |

17,192 |

|||||||||

|

Aon Corp., 5.00%, due 09/30/20 |

14,745 |

16,115 |

|||||||||

|

Anthem, Inc., 5.875%, due 06/15/17 |

15,150 |

16,014 |

|||||||||

|

CBRE Services, Inc., 5.25%, due 03/15/25 |

14,975 |

15,169 |

|||||||||