UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant x Filed by a Party other than the Registrant ¨

Check the appropriate box:

| ¨Preliminary | Proxy Statement |

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| x | Definitive Proxy Statement |

| ¨ | Definitive Additional Materials |

| ¨ | Soliciting Material under §240.14a-12 |

MANPOWER INC

(Name of registrant as specified in its

charter)

(Name of person(s) filing proxy statement, if other than the registrant)

Payment of Filing Fee (Check the appropriate box):

| x | No fee required. |

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

| (1) | Title of each class of securities to which the transaction applies: |

| (2) | Aggregate number of securities to which the transaction applies: |

| (3) | Per unit price or other underlying value of the transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| (4) | Proposed maximum aggregate value of the transaction: |

| (5) | Total fee paid: |

| ¨ | Fee paid previously with preliminary materials. |

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| (1) | Amount Previously Paid: |

| (2) | Form, Schedule or Registration Statement No.: |

| (3) | Filing Party: |

| (4) | Date Filed: |

MANPOWER INC.

(d/b/a ManpowerGroup)

100 MANPOWER PLACE

MILWAUKEE, WISCONSIN 53212

NOTICE OF ANNUAL MEETING OF SHAREHOLDERS

May 2, 2012

To the Shareholders of ManpowerGroup:

The 2012 Annual Meeting of Shareholders of Manpower Inc. (d/b/a ManpowerGroup) will be held at the International Headquarters of ManpowerGroup, 100 Manpower Place, Milwaukee, Wisconsin, on May 2, 2012, at 10:00 a.m., local time, for the following purposes:

| (1) | To elect four individuals nominated by the Board of Directors of ManpowerGroup to serve until 2015 as Class I directors; |

| (2) | To approve the proposed amendment to the Amended and Restated Articles of Incorporation of Manpower Inc. to change the name of the corporation to ManpowerGroup Inc.; |

| (3) | To ratify the appointment of Deloitte & Touche LLP as our independent auditors for 2012; |

| (4) | To hold an advisory vote on approval of the compensation of our named executive officers; |

| (5) | To transact such other business as may properly come before the meeting. |

Shareholders of record at the close of business on March 2, 2012 are entitled to notice of and to vote at the annual meeting and at all adjournments of the annual meeting.

Holders of a majority of the outstanding shares must be present in person or by proxy in order for the annual meeting to be held. Therefore, whether or not you expect to attend the annual meeting in person, you are urged to vote by a telephone vote, by voting electronically via the Internet or by completing and returning the accompanying proxy in the enclosed envelope. Instructions for telephonic voting and electronic voting via the Internet are contained on the accompanying proxy card. If you attend the meeting and wish to vote your shares personally, you may do so by revoking your proxy at any time prior to the voting thereof. In addition, you may revoke your proxy at any time before it is voted by advising the Secretary of ManpowerGroup in writing (including executing a later-dated proxy or voting via the Internet) or by telephone of such revocation.

Important Notice Regarding the Availability of Proxy Materials for the Annual Meeting of Shareholders to be held on May 2, 2012: The annual report and proxy statement of ManpowerGroup are available at www.manpowergroup.com/annualmeeting.

Kenneth C. Hunt, Secretary

March 16, 2012

MANPOWER INC.

(d/b/a ManpowerGroup)

100 Manpower Place

Milwaukee, Wisconsin 53212

March 16, 2012

PROXY STATEMENT

The enclosed proxy is solicited by the board of directors of Manpower Inc. (d/b/a ManpowerGroup) for use at the annual meeting of shareholders to be held at 10:00 a.m., local time, on May 2, 2012, or at any postponement or adjournment of the annual meeting, for the purposes set forth in this proxy statement and in the accompanying notice of annual meeting of shareholders. The annual meeting will be held at ManpowerGroup’s International Headquarters, 100 Manpower Place, Milwaukee, Wisconsin.

The expenses of printing and mailing proxy material, including expenses involved in forwarding materials to beneficial owners of stock, will be paid by us. No solicitation other than by mail is contemplated, except that our officers or employees may solicit the return of proxies from certain shareholders by telephone. In addition, we have retained Georgeson Shareholder Communications Inc. to assist in the solicitation of proxies for a fee of approximately $9,500 plus expenses.

Only shareholders of record at the close of business on March 2, 2012 are entitled to notice of and to vote the shares of our common stock, $.01 par value, registered in their name at the annual meeting. As of the record date, we had outstanding 80,153,480 shares of common stock. The presence, in person or by proxy, of a majority of the shares of the common stock outstanding on the record date will constitute a quorum at the annual meeting. Abstentions and broker non-votes, which are proxies from brokers or nominees indicating that such persons have not received instructions from the beneficial owners or other persons entitled to vote shares, will be treated as present for purposes of determining the quorum. Each share of common stock entitles its holder to cast one vote on each matter to be voted upon at the annual meeting. With respect to the proposals to elect the individuals nominated by our Board of Directors to serve as Class I directors, to ratify the appointment of Deloitte & Touche LLP as our independent auditors for 2012, as well as the advisory vote on approval of the compensation of our named executive officers, abstentions and broker non-votes will not be counted as voting on the proposals. With respect to the proposal to approve the proposed amendment to the Amended and Restated Articles of Incorporation of Manpower Inc. to change the name of the corporation to ManpowerGroup Inc., abstentions and broker non-votes will have the effect of votes against the proposal.

This proxy statement, notice of annual meeting of shareholders and the accompanying proxy card, together with our annual report to shareholders, including financial statements for our fiscal year ended December 31, 2011, are being mailed to shareholders commencing on or about March 26, 2012.

If the accompanying proxy card is properly signed and returned to us and not revoked, it will be voted in accordance with the instructions contained in the proxy card. Each shareholder may revoke a previously granted proxy at any time before it is exercised by advising the secretary of ManpowerGroup in writing (either by submitting a duly executed proxy bearing a later date or voting via the Internet) or by telephone of such revocation. Attendance at the annual meeting will not, in itself, constitute revocation of a proxy. Unless otherwise directed, all proxies will be voted for the election of each of the individuals nominated by our board of directors to serve as Class I directors, will be voted for approval of the amendment to the Amended and Restated Articles of Incorporation of Manpower Inc. to change the name of the corporation to ManpowerGroup Inc., will be voted for the appointment of Deloitte & Touche LLP as our independent auditors for 2012, and will be voted for approval of the compensation of our named executive officers.

CORPORATE GOVERNANCE DOCUMENTS

Certain documents relating to corporate governance matters are available in print by writing to Mr. Kenneth C. Hunt, Secretary, Manpower Inc., 100 Manpower Place, Milwaukee, Wisconsin 53212 and on Manpower’s web site at www.manpowergroup.com/about/corporategovernance.cfm. These documents include the following:

| • | Amended and Restated Articles of Incorporation; |

| • | Amended and Restated By-Laws; |

| • | Corporate governance guidelines; |

| • | Code of business conduct and ethics; |

| • | Charter of the nominating and governance committee, including the guidelines for selecting board candidates; |

| • | Categorical standards for relationships deemed not to impair independence of non-employee directors; |

| • | Charter of the audit committee; |

| • | Policy on services provided by independent auditors; |

| • | Charter of the executive compensation and human resources committee; |

| • | Executive officer stock ownership guidelines; |

| • | Outside director stock ownership guidelines; and |

| • | Foreign Corrupt Practices Act Compliance Policy. |

Information contained on ManpowerGroup’s web site is not deemed to be a part of this proxy statement.

2

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS

The following table lists as of the record date information as to the persons believed by us to be beneficial owners of more than 5% of our outstanding common stock:

| Name and Address of Beneficial Owners |

Amount and Nature of Beneficial Ownership |

Percent of Class(1) |

||||||

| T. Rowe Price Associates, Inc. 100 East Pratt Street Baltimore, Maryland 21202 |

9,980,527 | (2) | 12.5 | % | ||||

| BlackRock, Inc. 40 East 52nd Street New York, New York 10022 |

7,658,821 | (3) | 9.6 | % | ||||

| Wellington Management Company, LLP. 280 Congress Street Boston, Massachusetts 02210 |

6,528,972 | (4) | 8.1 | % | ||||

| FMR LLC 82 Devonshire Street Boston, Massachusetts 02109 |

4,461,488 | (5) | 5.6 | % | ||||

| (1) | Based on 80,153,480 shares of common stock outstanding as of the record date. |

| (2) | This information is based on a Schedule 13G filed on February 10, 2012. According to this Schedule 13G, these securities are owned by various individual and institutional investors for which T.Rowe Price Associates, Inc. (“Price Associates”) serves as investment adviser. Price Associates has sole voting power with respect to 2,035,885 shares held and sole dispositive power with respect to 9,980,527 shares held. |

| (3) | This information is based on a Schedule 13G filed on February 9, 2012, by BlackRock, Inc. on its behalf and on behalf of its following affiliates: BlackRock Advisors LLC, BlackRock Advisors (UK) Limited, BlackRock Asset Management Australia Limited, BlackRock Asset Management Canada Limited, BlackRock Japan Co. Ltd., BlackRock Capital Management, Inc. , BlackRock Financial Management, Inc., BlackRock Fund Advisors, BlackRock Institutional Trust Company, N.A., BlackRock Investment Management, LLC, BlackRock Investment Management (Australia) Limited, BlackRock Asset Management Ireland Limited, BlackRock (Luxembourg) S.A., BlackRock (Netherlands) B.V., BlackRock International Ltd, BlackRock Investment Management UK Ltd and BlackRock Fund Managers Limited. According to this Schedule 13G, these securities are owned of record by BlackRock, Inc. BlackRock, Inc. has sole voting power with respect to 7,658,821 shares held and sole dispositive power with respect to 7,658,821 shares held. |

| (4) | This information is based on a Schedule 13G filed on February 14, 2012. According to this Schedule 13G, these securities are owned of record by clients of Wellington Management Company, LLP. Wellington Management Company, LLP has shared voting power with respect to 4,860,412 shares held and shared dispositive power with respect to 6,528,972 shares held. |

| (5) | This information is based on a Schedule 13G filed on February 14, 2012, filed by FMR LLC (“FMR”) and Edward C. Johnson 3d, Chairman of FMR, on their behalf and on the behalf of the following affiliates of FMR: Fidelity Management & Research Company’ Strategic Advisers, Inc.; and FIL Limited. FMR and Edward C. Johnson 3d have sole voting power with respect to 782,568 shares held and sole dispositive power with respect to 4,461,488 shares held. |

3

1. ELECTION OF DIRECTORS

ManpowerGroup’s directors are divided into three classes, designated as Class I, Class II and Class III, with staggered terms of three years each. The term of office of directors in Class I expires at the annual meeting. The board of directors proposes that the nominees described below, all of whom are currently serving as Class I directors, be elected as Class I directors for a new term of three years ending at the 2015 annual meeting of shareholders and until their successors are duly elected, except as otherwise provided in the Wisconsin Business Corporation Law. Mr. Joerres, Mr. Walter, Mr. Bolland and Mr. Payne are all standing for re-election.

In accordance with our articles of incorporation and by-laws, a nominee will be elected as a director if the number of votes cast in favor of the election exceeds the number of votes cast against the election of that nominee. Abstentions and broker non-votes will not be counted as votes cast. If the number of votes cast in favor of the election of an incumbent director is less than the number of votes cast against the election of the director, the director is required to tender his or her resignation from the board of directors to the nominating and governance committee. Any such resignation will be effective only upon its acceptance by the board of directors. The nominating and governance committee will recommend to the board of directors whether to accept or reject the tendered resignation or whether other action should be taken. The board of directors will act on the recommendation of the nominating and governance committee and publicly disclose its decision, and the rationale behind its decision, within 90 days from the date of the announcement of the final results of balloting for the election.

| Name |

Age | Principal Occupation and Directorships | ||||

| Class I Directors (term expiring in 2012) | ||||||

| Jeffrey A. Joerres |

52 | Chairman of ManpowerGroup since May 2001, and President and Chief Executive Officer of ManpowerGroup since April 1999. Senior Vice President European Operations and Marketing and Major Account Development of ManpowerGroup from July 1998 to April 1999. A director of Johnson Controls, Inc. and the Federal Reserve Bank of Chicago. Formerly a director of Artisan Funds, Inc. from August 2001 to April 2011. A director of ManpowerGroup for more than five years. An employee of ManpowerGroup since July 1993. | ||||

| John R. Walter |

65 | Retired President and Chief Operating Officer of AT&T Corp. from November 1996 to July 1997. Chairman, President and Chief Executive Officer of R.R. Donnelley & Sons Company, a print and digital information management, reproduction and distribution company, from 1989 through 1996. Currently a director of InnerWorkings, Inc. Served as Non-Executive Chairman of the Board of InnerWorkings, Inc. from May 2004 to June 2010. Also a director of Vasco Data Securities, Inc. and Echo Global Logistics. A director of ManpowerGroup for more than five years. Previously, a director of Abbott Laboratories from 1997 to 2007, Deere & Company from 1991 to 2007 and SNP Corporation of Singapore from 2002 to 2009. | ||||

| Marc J. Bolland |

52 | Chief Executive Officer of Marks and Spencer Group plc. since May 2010. Chief Executive Officer of Wm Morrisons Supermarket Plc from September 2006 to April 2010. Executive Board Member of Heineken N.V., a Dutch beer brewing and bottling company, from 2001 to August 2006. Previously, a Managing Director of Heineken Export Group Worldwide, a subsidiary of Heineken N.V., from 1999 | ||||

4

| to 2001, and Heineken Slovensko, Slovakia, a subsidiary of Heineken N.V., from 1995 to 1998. A director of ManpowerGroup for more than five years. No other public directorships in the past five years. | ||||||

| Ulice Payne, Jr. |

56 | President of Addison-Clifton, LLC, a provider of global trade compliance advisory services, from May 2004 to present. President and Chief Executive Officer of the Milwaukee Brewers Baseball Club from 2002 to 2003. Partner with Foley & Lardner LLP, a national law firm, from 1998 to 2002. A trustee of The Northwestern Mutual Life Insurance Company and Wisconsin Energy Corporation. A director of ManpowerGroup since October 2007. Previously, a director of Midwest Air Group, Inc. from 1998 to 2008 and Badger Meter, Inc. from 2000 to 2010. | ||||

| Class II Directors (term expiring in 2013) | ||||||

| Gina R. Boswell |

49 | Executive Vice President, Personal Care, North America at Unilever since July 2011. President, Global Brands, of Alberto-Culver Company from January 2008 to July 2011. Senior Vice President and Chief Operating Officer — North America of Avon Products, Inc. from February 2005 to May 2007. Senior Vice President — Corporate Strategy and Business Development of Avon Products, Inc. from 2003 to February 2005. Prior thereto, an executive with Ford Motor Company, serving in various positions from 1999 to 2003. A director of ManpowerGroup since February 2007. Previously, a director of Applebee’s International, Inc. (now DineEquity) from 2005 to 2007. | ||||

| William Downe |

59 | President and Chief Executive Officer of BMO Financial Group since March 2007. Chief Operating Officer of BMO Financial Group from 2006 to March 2007. Deputy Chair of BMO Financial Group and Chief Executive Officer, BMO Nesbitt Burns and Head of Investment Banking Group from 2001 to 2006. Vice Chair of Bank of Montreal, 1999 to 2001. Prior thereto, held various senior management positions at Bank of Montreal in Canada and the United States. A director of ManpowerGroup since May 2011. A director of BMO Financial Group. No other public directorships in the past five years. | ||||

| Jack M. Greenberg |

69 | Non-Executive Chairman of The Western Union Company since 2006. Also Non-Executive Chairman of InnerWorkings, Inc. since June 2010. Retired Chairman and Chief Executive Officer of McDonald’s Corporation from May 1999 to December 2002 and Chief Executive Officer and President from August 1998 to May 1999. Director of The Allstate Corporation, InnerWorkings, Inc., Hasbro, Inc. and The Western Union Company. A director of ManpowerGroup for more than five years. Previously, a director of Abbott Laboratories from 2000 to 2007 and First Data Corporation from 2003 to 2006. | ||||

| Patricia A. Hemingway Hall |

59 | President and Chief Executive Officer of Health Care Service Corporation since November 2008. President and Chief Operating Officer of Health Care Service Corporation from November 2007 to November 2008. Executive Vice President of Internal Operations of Health Care Service Corporation from 2006 to 2007. Prior thereto | ||||

5

| held other senior management positions within Health Care Service Corporation since 1998. A director of ManpowerGroup since May 2011. No other public directorships in the past five years. | ||||||

| Terry A. Hueneke |

69 | Retired Executive Vice President of ManpowerGroup from 1996 until February 2002. Senior Vice President — Group Executive of ManpowerGroup’s former principal operating subsidiary from 1987 until 1996. A director of ManpowerGroup for more than five years. No other public directorships in the past five years. | ||||

| Class III Directors (term expiring in 2014) | ||||||

| Cari M. Dominguez |

62 | Chair of the U.S. Equal Employment Opportunity Commission from 2001 to 2006. President, Dominguez & Associates, a consulting firm, from 1999 to 2001. Partner, Heidrick & Struggles, a consulting firm, from 1995 to 1998. Director, Spencer Stuart, a consulting firm, from 1993 to 1995. Assistant Secretary for Employment Standards Administration and Director of the Office of Federal Contract Compliance Programs, U.S. Department of Labor, from 1989 to 1993. Prior thereto, held senior management positions with Bank of America. A trustee of Calvert SAGE Funds since September 2008. A director of ManpowerGroup since May 2007. No other public directorships in the past five years. | ||||

| Roberto Mendoza |

63 | Senior Managing Director of Atlas Advisors LLC, an independent global investment banking firm, since March 2010. Partner of Deming Mendoza & Co. LLC, a corporate finance advisory firm, from January 2009 to March 2010. Non-executive Chairman of Trinsum Group, Inc., an international strategic and financial advisory firm, from February 2007 to November 2008. Chairman of Integrated Finance Limited, a financial advisory firm, from June 2001 to January 2007. Managing Director of Goldman Sachs & Co. from September 2000 to March 2001. Director and Vice Chairman of J.P. Morgan & Co. Inc., from January 1990 to June 2000. A director of ManpowerGroup since April 2009. A director of The Western Union Company, PartnerRe Limited, a reinsurance company and Rocco Forte & Family Limited, a hotel management company. Also a member of the Council on Foreign Relations. Previously a director of Egg plc. from 2000 to 2006, Prudential plc. from 2000 to 2007 and Paris Re Holdings Limited from 2007 to 2009. | ||||

| Elizabeth P. Sartain |

57 | Independent Human Resource Advisor and Consultant since April 2008. Executive Vice President and Chief People Yahoo at Yahoo! Inc. from August 2001 to April 2008. Prior thereto, an executive with Southwest Airlines serving in various positions from 1988 to 2001. Director of Peets Tea and Coffee, Inc. A director of ManpowerGroup since August 2010. No other public directorships in the past five years. | ||||

| Edward J. Zore |

66 | Retired Chairman and Chief Executive Officer of The Northwestern Mutual Life Insurance Company (“Northwestern Mutual”) from March 2009 to July 2010. President and Chief Executive Officer of Northwestern Mutual from June 2001 to March 2009. President of Northwestern Mutual from March 2000 to June 2001. Executive Vice President, Life and Disability Income Insurance, of | ||||

6

| Northwestern Mutual from 1998 to 2000. Executive Vice President, Chief Financial Officer and Chief Investment Officer of Northwestern Mutual from 1995 to 1998. Prior thereto, Chief Investment Officer and Senior Vice President of Northwestern Mutual. Also a trustee of Northwestern Mutual. A director of ManpowerGroup for more than five years. A director of RenaissanceRe Holdings Ltd. since August 2010. Previously, a director of Mason Street Funds from 2000 to 2007 and a director of the Northwestern Mutual Series Fund, Inc. from 2000 to May 2010. |

Each director attended at least 75% of the board meetings and meetings of committees on which he or she served in 2011. The board of directors held seven meetings during 2011. The board of directors did not take action by written consent during 2011.

Under ManpowerGroup’s by-laws, nominations, other than those made by the board of directors or the nominating and governance committee, must be made pursuant to timely notice in proper written form to the secretary of ManpowerGroup. To be timely, a shareholder’s request to nominate a person for election to the board of directors at an annual meeting of shareholders, together with the written consent of such person to serve as a director, must be received by the secretary of ManpowerGroup not less than 90 days nor more than 150 days prior to the anniversary of the annual meeting of shareholders held in the prior year. To be in proper written form, the notice must contain certain information concerning the nominee and the shareholder submitting the nomination, including the disclosure of any hedging, derivative or other complex transactions involving the Company’s common stock to which a shareholder proposing a director nomination is a party.

The board of directors has adopted categorical standards for relationships deemed not to impair independence of non-employee directors to assist it in making determinations of independence. The categorical standards are available on ManpowerGroup’s website at http://www.manpowergroup.com/about/corporategovernance.cfm. The board of directors has determined that twelve of thirteen of the current directors of ManpowerGroup are independent under the listing standards of the New York Stock Exchange after taking into account the categorical standards and the following:

| • | Mr. Walter is a director and shareholder of Echo Global Logistics, a public company that entered into an agreement to provide logistics support to ManpowerGroup. |

| • | Mr. Walter and Mr. Greenberg are directors of InnerWorkings, Inc., a public company, which provides print management services to ManpowerGroup. |

| • | Mr. Greenberg is the Non-Executive Chairman of the Western Union Company, a public company, which has engaged ManpowerGroup to provide services to the company. |

| • | Mr. Zore and Mr. Payne are trustees of Northwestern Mutual. Northwestern Mutual and certain of its affiliates have engaged ManpowerGroup, Experis and Right Management to provide contingent staffing, accounting and other services. In addition, ManpowerGroup and certain of its affiliates have from time to time leased space from joint venture and limited liability companies in which Northwestern Mutual has an equity interest. |

| • | Ms. Boswell is Executive Vice President, Personal Care at Unilever, which has engaged ManpowerGroup to provide services to the company. |

| • | Ms. Hemingway Hall is President and Chief Executive Officer of Health Care Service Corporation, which has engaged ManpowerGroup to provide services to the company. |

| • | Mr. Downe is the President and Chief Executive Officer of BMO Financial Group, and one of its subsidiaries, BMO Harris Bank, is a party to the syndicate of banks in ManpowerGroup’s $800 million revolving credit facility, which was entered into in the ordinary course of business. |

7

The independent directors are Mr. Bolland, Ms. Boswell, Ms. Dominguez, Mr. Downe, Mr. Greenberg, Ms. Hemingway Hall, Mr. Hueneke, Mr. Mendoza, Mr. Payne, Ms. Sartain, Mr. Walter and Mr. Zore.

The nominating and governance committee will evaluate eligible shareholder-nominated candidates for election to the board of directors in accordance with the procedures described in ManpowerGroup’s Amended and Restated By-Laws and in accordance with the guidelines and considerations relating to the selection of candidates for membership on the board of directors described under “Board Composition and Qualifications of Board Members” below.

ManpowerGroup does not have a policy regarding board members’ attendance at the annual meeting of shareholders. Twelve of the thirteen directors attended the 2011 annual meeting of shareholders.

Any interested party who wishes to communicate directly with the lead director or with the non-management directors as a group may do so by calling 1-800-210-3458. The third-party service provider that monitors this telephone number will forward a summary of all communications directed to the non-management directors to the lead director.

Committees of the Board

The board of directors has standing audit, executive compensation and human resources, and nominating and governance committees. The board of directors has adopted written charters for the audit, executive compensation and human resources and nominating and governance committees. These charters are available on ManpowerGroup’s web site at http://www.manpowergroup.com/about/corporategovernance.cfm.

The audit committee consists of Mr. Zore (Chairman), Ms. Boswell, Mr. Hueneke, Mr. Payne, Mr. Mendoza and Ms. Hemingway-Hall. Ms. Hemingway Hall was appointed to the audit committee on December 12, 2011. Each member of the audit committee is “independent” within the meaning of the applicable listing standards of the New York Stock Exchange. The board of directors has determined that Mr. Zore is an “audit committee financial expert” and “independent” as defined under the applicable rules of the Securities and Exchange Commission.

The functions of the audit committee include: (i) appointing the independent auditors for the annual audit and approving the fee arrangements with the independent auditors; (ii) monitoring the independence, qualifications and performance of the independent auditors; (iii) reviewing the planned scope of the annual audit; (iv) reviewing the financial statements to be included in our quarterly reports on Form 10-Q and our annual report on Form 10-K, and our disclosures under “Management’s Discussion and Analysis of Financial Condition and Results of Operations”; (v) reviewing compliance with and reporting under Section 404 of the Sarbanes-Oxley Act of 2002; (vi) reviewing our accounting management and controls and any significant audit adjustments proposed by the independent auditors; (vii) making a recommendation to the board of directors regarding inclusion of the audited financial statements in our annual report on Form 10-K; (viii) reviewing recommendations, if any, by the independent auditors resulting from the audit to ensure that appropriate actions are taken by management; (ix) reviewing matters of disagreement, if any, between management and the independent auditors; (x) periodically reviewing our Policy Regarding the Retention of Former Employees of Independent Auditors; (xi) overseeing compliance with our Policy on Services Provided by Independent Auditors; (xii) meeting privately on a periodic basis with the independent auditors, internal audit staff and management to review the adequacy of our internal controls; (xiii) monitoring our internal audit department, including our internal audit plan; (xiv) monitoring our policies and procedures regarding compliance with the Foreign Corrupt Practices Act and compliance by our employees with our code of business conduct and ethics; (xv) assisting the board of directors with its oversight of the performance of the Company’s risk management function; (xvi) reviewing current tax matters affecting us; (xvii) periodically discussing with management our risk management framework; (xviii) serving as our qualified legal compliance committee; and (xix) monitoring any litigation involving ManpowerGroup, which may have a material financial impact on ManpowerGroup or relate to matters entrusted to the audit committee. In addition, the charter of the audit committee provides that the

8

audit committee shall review and approve all related party transactions that are material to ManpowerGroup’s financial statements or that otherwise require disclosure to ManpowerGroup’s shareholders, provided that the audit committee shall not be responsible for reviewing and approving related party transactions that are reviewed and approved by the board of directors or another committee of the board of directors. The audit committee held five meetings during 2011. The audit committee did not take action by written consent during 2011.

The executive compensation and human resources committee consists of Mr. Greenberg (Chairman), Mr. Bolland, Ms. Dominguez, Mr. Downe, Ms. Sartain and Mr. Walter. Mr. Downe was appointed to the committee on December 12, 2011. Each member of the executive compensation and human resources committee is “independent” within the meaning of the applicable listing standards of the New York Stock Exchange and qualifies as an “outside director” under Section 162(m) of the Internal Revenue Code. The functions of this committee are to: (i) establish the compensation of the president and chief executive officer and the chief financial officer of ManpowerGroup, subject to ratification by the board of directors; (ii) approve the compensation, based on the recommendations of the president and chief executive officer of ManpowerGroup, of certain other senior executives of ManpowerGroup and its subsidiaries; (iii) determine the terms of any agreements concerning employment, compensation or employment termination, as well as monitor the application of ManpowerGroup’s retirement and other fringe benefit plans, with respect to the individuals listed in (i) and (ii); (iv) monitor the development of ManpowerGroup’s key executive officers; (v) administer ManpowerGroup’s equity incentive plans and employee stock purchase plans and oversee ManpowerGroup’s employee retirement and welfare plans; (vi) administer ManpowerGroup’s corporate senior management annual incentive plan; and (vii) act as the compensation committee of outside directors under Section 162(m) of the Internal Revenue Code. The executive compensation and human resources committee held six meetings during 2011. The executive compensation and human resources committee did not take action by written consent during 2011.

The nominating and governance committee consists of Mr. Walter (Chairman), Ms. Boswell, Mr. Greenberg, Mr. Payne, and Mr. Zore. Each member of the nominating and governance committee is “independent” within the meaning of the applicable listing standards of the New York Stock Exchange. The functions of this committee are to: (i) recommend nominees to stand for election at annual meetings of shareholders, to fill vacancies on the board of directors and to serve on committees of the board of directors; (ii) establish procedures and assist in identifying candidates for board membership; (iii) review the qualifications of candidates for board membership; (iv) periodically review the compensation arrangements in effect for the non-management members of the board of directors and recommend any changes deemed appropriate; (v) coordinate the annual self- evaluation of the performance of the board of directors and each of its committees; (vi) establish and review, for recommendation to the board of directors, guidelines and policies on the size and composition of the board, the structure, composition and functions of the board committees, and other significant corporate governance principles and procedures; (vii) oversee the content and format of our code of business conduct and ethics; (vii) monitor compliance by the non-management directors with our code of business conduct and ethics; and (viii) develop and periodically review succession plans for the directors. The nominating and governance committee has from time to time engaged director search firms to assist it in identifying and evaluating potential board candidates. The nominating and governance committee met four times during 2011. The nominating and governance committee did not take action by written consent during 2011.

Board Composition and Qualifications of Board Members

The nominating and governance committee has adopted, and the board of directors has approved, guidelines for selecting board candidates that the committee considers when evaluating candidates for nomination as directors. The guidelines call for the following with respect to the composition of the board:

| • | a variety of experience and backgrounds |

| • | a core of business executives having substantial senior management and financial experience |

9

| • | individuals who will represent the best interests of the shareholders as a whole rather than special interest constituencies |

| • | the independence of at least a majority of the directors |

| • | individuals who represent a diversity of gender, race and age |

In connection with its consideration of possible candidates for board membership, the committee also has identified areas of experience that members of the board should as a goal collectively possess. These areas include:

| • | previous board experience |

| • | active or former CEO/COO/Chairperson |

| • | human resources experience |

| • | accounting or financial oversight experience |

| • | international business experience |

| • | sales experience |

| • | marketing and branding experience |

| • | operations experience |

| • | corporate governance experience |

| • | government relations experience |

| • | technology experience |

The Company believes that the present composition of the board of directors satisfies the guidelines for selecting board candidates set out above; specifically, the board is composed of individuals who have a variety of experience and backgrounds, the board has a core of business executives having substantial experience in management as well as one member having government experience, board members represent the best interests of all of the shareholders rather than special interests, and twelve of thirteen directors are independent under the rules of the New York Stock Exchange. The composition of the board also reflects diversity of country of origin, gender, race and age, an objective that the nominating and governance committee continually strives to enhance when searching for and considering new directors. Based on the composition of our board of directors, we believe this objective has been achieved.

In addition, the particular areas of desired experience identified above that are possessed by each director with significant or some experience is as follows:

M. Bolland — Active CEO/COO/Chairman, Human Resources, Financial Oversight/Accounting, International Business, Sales, Marketing/Branding, Operations and Government Relations

G. Boswell — Previous Board Experience, Human Resources, Financial Oversight/Accounting, International Business, Sales, Marketing/Branding, Operations, Governance and Technology

C. Dominguez — Human Resources, International Business, Operations, Governance and Government Relations

W. Downe — Previous Board Experience, Active CEO/COO/Chairman, International Business, Operations

J. Greenberg — Previous Board Experience, Active CEO/COO/Chairman, Former CEO, Human Resources, Financial Oversight/Accounting, International Business, Marketing/Branding, Operations, Governance, Government Relations and Technology

10

P. Hemingway Hall — Active CEO/COO/Chairman, Human Resources, Sales, Marketing/Branding, Operations, Government Relations

T. Hueneke — Human Resources, Financial Oversight/Accounting, International Business, Sales, Marketing/Branding and Operations

R. Mendoza — Previous Board Experience, Human Resources, Financial Oversight/Accounting, International Business, Sales, Operations and Governance

U. Payne — Previous Board Experience, Active CEO/COO/Chairman, Former CEO, Human Resources, Financial Oversight/Accounting, International Business, Sales, Marketing/Branding, Operations, Governance and Government Relations

E. Sartain — Previous Board Experience, Human Resources, International Business, Marketing/Branding and Operations

J. Walter — Previous Board Experience, Former CEO, Human Resources, Financial Oversight/Accounting, International Business, Sales, Marketing/Branding, Operations, Governance, Government Relations and Technology

E. Zore — Previous Board Experience, Former CEO, Human Resources, Financial Oversight/Accounting, Sales, Marketing/Branding, Operations, Governance, Government Relations and Technology

Mr. Joerres has experience in many of these areas as well, however his position on the board is due to his position as CEO of the Company, as the board of directors has determined the CEO should also be chairman of the board of directors. For more information on how each of the board of directors meets these objectives, see their occupations and directorships disclosed previously under “Election of Directors”.

Prior to 2011, ManpowerGroup’s corporate governance guidelines stated that it is the policy of the board of directors that no individual who would be age 70 or older at the time of his or her election will be eligible to stand for election to the board of directors. In 2011, the Board amended the corporate governance guidelines and has established a general retirement age of 72. An individual cannot be nominated for election to the Board of Directors after his or her 72nd birthday. A director that is standing for election who will turn age 72 during his or her normal term must submit a resignation effective as of his or her 72nd birthday as a condition to having the Board recommend the director for election. If the Board of Directors rejects the resignation for any reason, the director shall continue in office until the expiration of his or her current term.

Board Leadership Structure

The board of directors has appointed the chief executive officer of the Company to the position of chairman of the board. Combining the roles of chairman of the board and chief executive officer (1) enhances alignment between the board of directors and management in strategic planning and execution as well as operational matters, (2) avoids the confusion over roles, responsibilities and authority that can result from separating the positions, and (3) streamlines board process in order to conserve time for the consideration of the important matters the board needs to address. At the same time, the combination of a completely independent board (except for the chairman of the board) and the lead director arrangement maintained by the board facilitate effective oversight of the performance of senior management.

11

The board of directors has established an arrangement under which the chairman of one of the principal board committees serves as lead director on a rotating basis for each calendar year in the following order: executive compensation and human resources committee, audit committee, and nominating and governance committee. The lead director’s duties as specified in the Company’s corporate governance guidelines are as follows:

| • | Preside at executive sessions of the non-employee directors and all other meetings of directors where the chairman of the board is not present; |

| • | Serve as liaison between the chairman of the board and the non-employee directors; |

| • | Approve what information is sent to the board; |

| • | Approve the meeting agendas for the board; |

| • | Approve meeting schedules to assure that there is sufficient time for discussion on all agenda items; |

| • | Have the authority to call meetings of the non-employee directors; and |

| • | If requested by major shareholders, ensure that he or she is available for consultation and direct communication. |

Mr. Greenberg, the chairman of the executive compensation and human resources committee, will serve as lead director in 2012.

Board Oversight of Risk

The audit committee is responsible for assisting the board of directors with its oversight of the performance of the Company’s risk management functions including:

| • | Periodically reviewing and discussing with management the Company’s policies, practices and procedures regarding risk assessment and management; |

| • | Periodically receiving, reviewing and discussing with management reports on selected risk topics as the committee or management deems appropriate from time to time; and |

| • | Periodically reporting to the board of directors on its activities in this oversight role. |

In this oversight capacity, the committee’s role is one of informed oversight rather than direct management of risk. In addition, it is not intended that the committee be involved in the day-to-day risk management activities. Instead, the committee is expected to engage in reviews and discussions with management (and others if considered appropriate) as necessary to be reasonably assured that the Company’s risk management processes (1) are adequate to identify the material risks that we face in a timely manner, (2) include strategies for the management of risk that are responsive to our risk profile and specific material risk exposure, (3) serve to integrate risk management considerations into business decision-making throughout the Company, and (4) include policies and procedures that are reasonably effective in facilitating the transmission of information with respect to material risks to the senior executives of the Company and the committee.

Compensation Consultant

The executive compensation and human resources committee directly retains Mercer (US) Inc. to advise it on executive compensation matters. Mercer reports to the chairman of the committee. On an annual basis, the Company and Mercer enter into an engagement letter, which sets out the services to be performed by Mercer for the committee during the ensuing year. Mercer’s primary role is to provide objective analysis, advice and information and otherwise to support the committee in the performance of its duties. Mercer’s fees for executive compensation consulting to the committee in 2011 were $142,475.

12

The committee requests information and recommendations from Mercer as it deems appropriate in order to assist it in structuring and evaluating ManpowerGroup’s executive compensation programs and practices. The committee’s decisions about executive compensation, including the specific amounts paid to executive officers, are its own and may reflect factors and considerations other than the information and recommendations provided by Mercer.

Mercer was engaged by the committee to perform the following services for the period from June 1, 2011 through May 31, 2012:

| • | Evaluate the competitiveness of our total executive compensation and benefits program for the CEO, CFO and senior management team, including base salary, annual incentive, total cash compensation, long-term incentive awards, total direct compensation, retirement benefits and total remuneration against the market; |

| • | Assess how well the compensation and benefits programs are aligned with the committee’s stated philosophy to align pay with performance, including analyzing our performance against comparator companies; |

| • | Review the companies included in our industry peer group; |

| • | Provide advice and assistance to the committee on the levels of total compensation and the principal elements of compensation for our senior executives; |

| • | Brief the executive compensation and human resources committee on executive compensation trends in executive compensation and benefits among large public companies and on regulatory, legislative and other developments; |

| • | Advise the executive compensation and human resources committee on salary, target incentive opportunities and equity grants; and |

| • | Assist with the preparation of the Compensation Discussion and Analysis and other executive compensation disclosures to be included in this proxy statement. |

In connection with the engagement, ManpowerGroup and Mercer have agreed on written guidelines for minimizing potential conflicts of interest. These guidelines are as follows:

| • | The committee has the authority to retain and dismiss Mercer at any time; |

| • | Mercer reports directly to the committee and has direct access to the committee through the chairman; |

| • | Mercer does not consult with or otherwise interact with our executives except to discuss our business and compensation strategies and culture, obtain compensation and benefits data along with financial projections and operational data, consult about the nature and scope of the various executive jobs for benchmarking purposes, confirm factual and data analyses to ensure accuracy, and consult with the CEO about the compensation of the other executives of ManpowerGroup; |

| • | Mercer’s main contacts with management are the CFO and executive vice president, global strategy and talent; |

| • | Mercer’s written reports may be distributed to committee members as part of the committee meeting mailings, except any findings and recommendation regarding the CEO are sent in a separate document directly to committee members; |

| • | Each engagement of Mercer by the committee is documented in an engagement letter that includes a description of the agreed upon services, fees and other matters considered appropriate; and |

| • | Prior to the Mercer consultant performing any services, whether related to compensation or other consulting services, for ManpowerGroup in addition to those performed for the committee, the consultant must inform the committee chairman and obtain approval. |

13

Ultimately, the consultant provides recommendations and advice to the committee in an executive session where management is not present, which is when critical pay decisions are made. This approach protects the committee’s ability to receive objective advice from the consultant so that the committee may make independent decisions about executive pay at our company.

Besides Mercer’s involvement with the committee, it and its affiliates also provide other non-executive compensation services to us. The total amount paid for these other services provided in 2011 was $674,719.

The committee believes the advice it receives from the individual executive compensation consultant is objective and not influenced by Mercer’s or its affiliates’ relationships with us because of the procedures Mercer and the committee have in place, including the following:

| • | The consultant receives no incentive or other compensation based on the fees charged to us for other services provided by Mercer or any of its affiliates; |

| • | The consultant is not responsible for selling other Mercer or affiliate services to us; |

| • | Mercer’s professional standards prohibit the individual consultant from considering any other relationships Mercer or any of its affiliates may have with us in rendering his or her advice and recommendations; and |

| • | The committee evaluates the quality and objectivity of the services provided by the consultant each year and determines whether to continue to retain the consultant. |

14

2. APPROVE THE PROPOSED AMENDMENT TO THE AMENDED AND RESTATED ARTICLES OF INCORPORATION OF MANPOWER INC. TO CHANGE THE NAME OF THE CORPORATION TO MANPOWERGROUP INC.

On February 15, 2012, our Board of Directors unanimously approved and recommended that our shareholders approve an amendment to the Company’s Amended and Restated Articles of Incorporation to the change the name of the Company from “Manpower Inc.” to “ManpowerGroup Inc. “ (the “Amendment”).

On March 30, 2011, we began doing business as ManpowerGroup to reflect our global leadership in providing innovative workforce solutions for clients. This evolution creates a stronger, more connected family of brands and allows us to tell the world that the umbrella of solutions that we provide is much bigger than what people may have previously thought. This name change strengthens and better articulates our family of brands and suite of solutions and differentiates our organization in a way that clearly defines what each of the ManpowerGroup brands stand for individually, while also strengthening the combined assets, that makes it easier to provide clients with dynamic and flexible solutions across ManpowerGroup.

If the proposal to amend our Amended and Restated Articles of Incorporation to change our name to “ManpowerGroup Inc.” is approved by our shareholders, the new name will become effective upon the filing of articles of amendment that include the Amendment and other required information with the Wisconsin Department of Financial Institutions. This Amendment will change Article I of the Amended and Restated Articles of Incorporation to read in its entirety as follows:

“ARTICLE I.

The name of the Corporation is ManpowerGroup Inc.”

If the name change becomes effective, the rights of shareholders holding shares represented by outstanding stock certificates and the number of shares represented by those certificates will remain unchanged. The name change will not affect the validity or transferability of any currently outstanding stock certificates nor will it be necessary for shareholders with certificated shares to surrender or exchange any stock certificates they currently hold as a result of the name change.

The affirmative vote of the holders of not less than two-thirds of the outstanding total shares of stock entitled to vote at the annual meeting is required to approve the Amendment. Abstentions and broker non-votes will have the effect of votes against approval of the Amendment.

The board of directors recommends that you vote FOR approval of the amendment to the Company’s Amended and Restated Articles of Incorporation and your proxy will be so voted unless you specify otherwise.

15

SECURITY OWNERSHIP OF MANAGEMENT

Set forth in the table below, as of March 2, 2012, are the shares of ManpowerGroup common stock beneficially owned by each director and nominee, each of the executive officers named in the table under the heading “Executive and Director Compensation — Summary Compensation Table,” who we refer to as the named executive officers, and all directors and executive officers of ManpowerGroup as a group and the shares of ManpowerGroup common stock that could be acquired within 60 days of March 2, 2012 by such persons.

| Name of Beneficial Owner |

Common Stock Beneficially Owned(1) |

Right to Acquire Common Stock(1)(2) |

Percent of Class(3) |

|||||||||

| Jeffrey A. Joerres |

1,251,629 | (4)(5) | 943,884 | 1.6 | % | |||||||

| Michael J. Van Handel |

391,910 | (5) | 290,208 | * | ||||||||

| Marc J. Bolland |

20,196 | (5) | 6,250 | * | ||||||||

| Gina R. Boswell |

12,298 | (5) | 0 | * | ||||||||

| Cari M. Dominguez |

7,176 | (5) | 0 | * | ||||||||

| William Downe |

6,000 | 0 | * | |||||||||

| Darryl Green |

94,108 | 70,968 | * | |||||||||

| Jack M. Greenberg |

25,126 | (5) | 10,000 | * | ||||||||

| Françoise Gri |

116,572 | 93,733 | * | |||||||||

| Patricia Hemingway Hall |

0 | 0 | * | |||||||||

| Terry A. Hueneke |

25,975 | (5) | 8,750 | * | ||||||||

| Hans Leentjes |

30,587 | 30,587 | * | |||||||||

| Roberto Mendoza |

0 | 0 | * | |||||||||

| Ulice Payne, Jr |

7,026 | 0 | * | |||||||||

| Jonas Prising |

134,839 | (5) | 104,983 | * | ||||||||

| Elizabeth P. Sartain |

5,454 | 0 | * | |||||||||

| Owen J. Sullivan |

169,492 | (5) | 155,753 | * | ||||||||

| John R. Walter |

39,506 | 18,028 | * | |||||||||

| Edward J. Zore |

50,865 | (5) | 15,000 | * | ||||||||

| All directors and executive officers as a group (21 persons) |

2,602,042 | 1,938,066 | 3.2 | % | ||||||||

| (1) | Except as indicated below, all shares shown in this column are owned with sole voting and dispositive power. Amounts shown in the Right to Acquire Common Stock column are also included in the Common Stock Beneficially Owned column. |

| The table does not include vested shares of deferred stock, which will be settled in shares of ManpowerGroup common stock on a one-for-one basis, held by the following directors that were issued under the 2003 Equity Incentive Plan and the Terms and Conditions Regarding the Grant of Awards to Non-Employee Directors under the 2003 Equity Incentive Plan and the 2011 Equity Incentive Plan and the Terms and Conditions Regarding the Grant of Awards to Non-Employee Directors under the 2011 Equity Incentive Plan: |

| Director | Vested Deferred Stock | |||||||||||

| 2003 Plan | 2011 Plan | Total | ||||||||||

| Marc J. Bolland |

1,882 | 1,573 | 3,455 | |||||||||

| William Downe |

0 | 2,127 | 2,127 | |||||||||

| Jack M. Greenberg |

1,586 | 0 | 1,586 | |||||||||

| Patricia Hemingway Hall |

0 | 1,058 | 1,058 | |||||||||

| Terry A. Hueneke |

3,244 | 0 | 3,244 | |||||||||

| Roberto Mendoza |

6,172 | 1,573 | 7,745 | |||||||||

| Ulice Payne, Jr. |

1,692 | 0 | 1,692 | |||||||||

| Elizabeth P. Sartain |

2,026 | 0 | 2,026 | |||||||||

| John R. Walter |

12,695 | 0 | 12,695 | |||||||||

| Edward J. Zore |

3,308 | 948 | 4,256 | |||||||||

16

| The table does not include 2,937 unvested shares of deferred stock, which will be settled in shares of ManpowerGroup common stock on a one-for-one basis, held by each of Ms. Dominguez, Mr. Downe, Ms. Hall, Mr. Mendoza and Mr. Payne that were issued under the 2011 Plan and the Terms and Conditions on January 1, 2012. These shares of deferred stock vest in equal quarterly installments during 2012. |

| The table does not include unvested restricted stock units, which will be settled in shares of ManpowerGroup common stock on a one-for-one basis, held by the following executive officers that were issued under the 2003 Plan and 2011 Plan: |

| Officer | Unvested Restricted Stock Units |

|||||||||||

| 2003 Plan | 2011 Plan | Total | ||||||||||

| Jeffrey A. Joerres |

21,218 | 31,244 | 52,462 | |||||||||

| Michael J. Van Handel |

7,578 | 11,159 | 18,737 | |||||||||

| Darryl Green |

10,998 | 4,910 | 15,908 | |||||||||

| Francoise Gri |

8,270 | 4,910 | 13,180 | |||||||||

| Hans Leentjes |

2,425 | 4,464 | 6,889 | |||||||||

| Jonas Prising |

20,281 | 4,910 | 25,191 | |||||||||

| Owen J. Sullivan |

23,096 | 4,910 | 28,006 | |||||||||

| Of these amounts, (i) the following restricted stock units vest on February 17, 2013: Mr. Green — 5,239, Ms. Gri — 5,239 and Mr. Prising — 2,095, (ii) the following restricted stock units vest on February 16, 2014: Mr. Joerres — 21,218; Mr. Van Handel — 7,578; Mr. Green — 5,759; Ms. Gri — 3,031; Mr. Leentjes — 2,425; Mr. Prising — 3,031; and Mr. Sullivan – 3,031, (iii) the following restricted stock units vest on February 15, 2015: Mr. Joerres — 31,244; Mr. Van Handel — 11,159; Mr. Green — 4,910; Ms. Gri — 4,910; Mr. Leentjes — 4,464; Mr. Prising — 4,910; and Mr. Sullivan – 4,910, and (iv) 15,155 shares of restricted stock held by each of Mr. Prising and Mr. Sullivan will vest on February 16, 2016 , except as otherwise provided in the 2003 and 2011 Plan. |

| (2) | Common stock that may be acquired within 60 days of the record date through the exercise of stock options and the settlement of restricted stock units. |

| (3) | No person named in the table, other than Mr. Joerres, beneficially owns more than 1% of the outstanding shares of common stock. The percentage is based on the column entitled Common Stock Beneficially Owned. |

| (4) | Includes 300 shares held by Mr. Joerres’ spouse. |

| (5) | Includes the following number of shares of unvested restricted stock as of the record date: |

| Officer or Director | Unvested Restricted Stock |

|||

| Jeffrey A. Joerres |

40,000 | |||

| Jonas Prising |

2,500 | |||

| Owen J. Sullivan |

2,500 | |||

| Marc J. Bolland |

2,937 | |||

| Gina R. Boswell |

2,937 | |||

| Jack M. Greenberg |

2,937 | |||

| Terry A. Hueneke |

2,937 | |||

| Elizabeth P. Sartain |

2,937 | |||

| John R. Walter |

2,937 | |||

| Edward J. Zore |

2,937 | |||

| The holders of the restricted stock have sole voting power with respect to all shares held and no dispositive power with respect to all shares held. |

17

EXECUTIVE AND DIRECTOR COMPENSATION

Compensation Discussion and Analysis

Background

This compensation discussion and analysis provides information about ManpowerGroup’s compensation policies and decisions regarding the company’s CEO, CFO and the five executive officers who are the leaders of the company’s business operating units. In the discussion below, we refer to this group of executives as the named executive officers (“NEOs”). This group includes the executive officers for whom disclosure is required under the rules of the Securities and Exchange Commission.

ManpowerGroup is the world leader in innovative workforce solutions and services with over 85% percent of its revenues coming from outside the United States. We do business in 80 countries and territories, have nearly 3,800 offices and over 31,000 staff employees globally, and placed approximately 3.5 million people in jobs in 2011. The variations in laws around the world, the variety of services offered, and the increasing multiregional and global solutions that clients need make the business increasingly complex. None of our competitors can match our global reach or breadth of service offerings.

Executive Summary

2011 Financial Highlights

ManpowerGroup’s performance in 2011 was strong. We were able to improve our operating leverage by effectively using our office network to support revenue growth with a minimal increase in expenses. Our ability to gain such operating leverage was a result of strategic cost reductions made during the economic downturn, which minimized the adverse impact of the economy on our business during the downturn, yet preserved capacity within our office network to handle the increased demand that we expected and subsequently experienced during 2011. This improvement in our markets and operating leverage allowed us to significantly improve our operating results. Highlights of our 2011 performance compared to 2010 include:

| • | Revenue of $22.0 billion, an increase of 16.6%; |

| • | Operating Profit Margin(1) of 2.49%, an increase of 36.8%, |

| • | Diluted Earnings Per Share(1) (“EPS”) of $3.04, a 106.8% increase; and |

| • | Economic Profit(1) (net operating profit after taxes less a capital charge, referred to as “EP”) of -$6.1 million, a 95.8% improvement. |

| (1) | Operating Profit Margin, EPS and EP have been calculated for 2011 and 2010 in accordance with our compensation plans. |

Compensation Philosophy

The amount of compensation earned by our executives is directly tied to our ability to deliver financial and operating performance that provides long-term increases in shareholder value. A significant component of pay is variable based on performance and our guiding principles are as follows (see page 24 for further detail regarding these principles):

| • | Pay for results, |

| • | Not pay for failure, |

| • | Align compensation with shareholder interests, |

| • | Pay competitively, |

18

| • | Balance cash and equity, |

| • | Use internal and external performance reference points, |

| • | Recognize the global and cyclical nature of our business, |

| • | Retain executives, |

| • | Assure total compensation is affordable, and |

| • | Clearly communicate plans so that they are understood. |

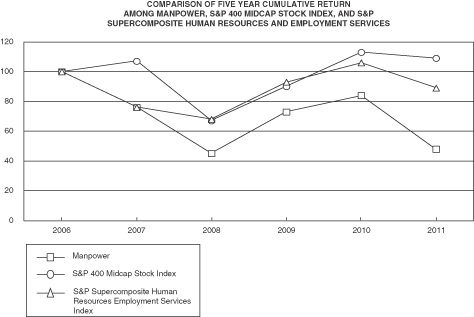

Total Shareholder Return

The following is a graph for the periods ending December 31, 2006-2011 comparing the cumulative total shareholder return on our common stock with the cumulative total return of companies in the Standard & Poor’s 400 Midcap Stock Index and the Standard & Poor’s Supercomposite Human Resources and Employment Services Index, of which we are included. The graph assumes a $100 investment on December 31, 2006 in our common stock, the Standard & Poor’s 400 Midcap Stock Index and the Standard & Poor’s Supercomposite Human Resources and Employment Services Index and assumes the reinvestment of all dividends.

The Company’s Total Shareholder Return (TSR) has underperformed against both the S&P 400 Midcap Stock Index and the S&P Supercomposite Human Resources Employment Services Index over this period. Although we took the actions necessary to minimize the adverse impact of the economy on our business during the economic downturn, it is widely recognized that the volatility in stock prices over the last part of 2011 was largely driven by global macro issues such as the European debt crisis, and not by company specific performance. Given that approximately 66% of our business is in Europe, we were disproportionately affected by these issues and as a result our stock price was negatively affected. For example, our Revenue for 2011 increased 16.6% over prior year, while EPS increased 106.8% from 2010. However, the TSR for 2011 declined 42%.

19

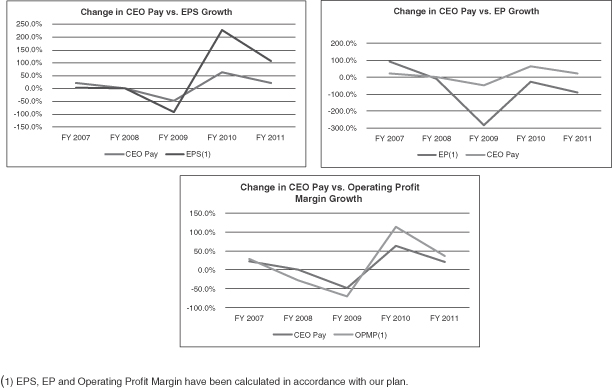

Alignment with Shareholder Interests

Due to the cyclicality of our business, we look at pay for performance on an annual basis as well as over the long term. We pay for performance based on the Company’s financial performance, typically using EP, EPS and Operating Profit Margin, which align with long-term shareholder value. EPS keeps Mr. Joerres, as well as the other NEOs, focused on producing financial results that align with shareholders goals, while EP promotes our business strategy of producing returns in excess of our cost of capital. Operating Profit Margin is a strong measure of the long-term profitability of our company. The higher our operating profit margin, the more valuable our business becomes, which over time, provides greater value to our shareholders. Typically, when the Company experiences weak EP, EPS and Operating Profit Margin performance, Mr. Joerres’ total compensation declines. Accordingly, when the Company has strong EP, EPS and Operating Profit Margin performance, Mr. Joerres total compensation increases. The following graph demonstrates the alignment between Mr. Joerres’ change in total compensation as reported in the Summary Compensation Table and company performance, using EPS, EP and Operating Profit Margin growth over the last five years.

The decline in stock price also has an impact on the value of the CEO’s long-term compensation. For example, the value at target of the RSUs and PSUs granted to our CEO in February 2011 was $2.6 million on December 31, 2011 compared to $4.9 million on February 16, 2011, a decline of $2.3 million or 47%. Furthermore, the value realized from Mr. Joerres’ 2010 grant of PSUs was reduced by 15% as a result of the decline in stock price from the date the shares were granted to the date the shares were received.

20

Actions Taken to Strengthen Compensation and Other Governance Practices

The Committee reviews the Company’s executive compensation program and is continually looking to align the program within the committee’s philosophy, and with best compensation practices that are in the best interests of our shareholders. As a result, the committee implemented the following changes to the Company’s executive compensation program in 2011:

| • | Elimination of tax gross-ups: Consistent with best governance practices within the committee’s philosophy, we entered into new severance agreements with our CEO and CFO that eliminated the right they had under their previous agreements to receive tax gross up payments for any amounts considered excess parachute payments under Section 280G of the Internal Revenue Code and subject to the 20% excise tax imposed on such payments under Section 4999 of the Internal Revenue Code. None of the other NEOs severance agreements contained this feature. |

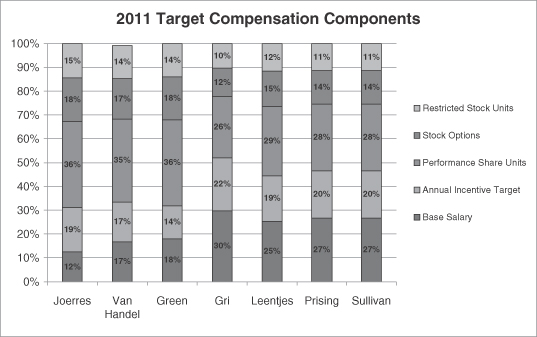

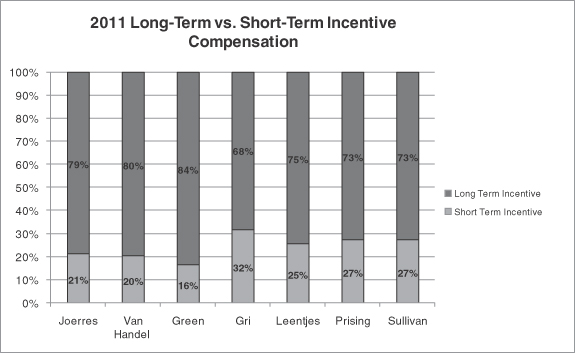

| • | Modification to long-term equity incentive awards: The committee believes performance share units (PSUs) should represent a significant portion of the NEOs equity compensation because pay for performance is a significant component of the Company’s compensation philosophy. Under our PSU program, NEOs will receive a certain number of shares of stock at the end of a period based on achievement of a pre-established performance metric for that period, typically operating profit margin. Beginning in 2011, PSUs comprised approximately 50% of the long-term compensation grants for the NEOs, while stock options and restricted stock units comprised approximately 30% and 20%, respectively. The committee included RSUs in 2011 as part of the long-term incentive compensation grants to provide a retention incentive to NEOs that are payable in stock provided the executive remains with the Company through the vesting date. The committee believes restricted stock units directly align the economic interests of our NEOs with those of our shareholders as they provide both upside potential and downside risk in our stock price. Prior to 2011, PSUs comprised approximately 40% of the long-term equity incentive awards to the NEOs, while stock options were approximately 60%. |

In addition, the following are key pay practices and policies of the Company’s executive compensation program that the committee has adopted over the past several years to align our executive compensation program with best governance practices:

Pay Practices

| • | Double triggers in equity and severance agreements –– Double triggers are in place in our severance agreements and most of our equity awards. In order for NEOs to receive a number of benefits in the event of a change in control their employment generally must be terminated. |

| • | No tax gross ups — In 2011 the committee eliminated any tax gross up payments for any amounts considered excess parachute payments. |

| • | Limited perquisites — Our executives are provided very limited perquisites including financial planning reimbursement and broad-based automobile benefits and selected benefits for expatriate services. |

| • | Stock ownership guidelines —The Company has stock ownership guidelines for its executive officers, including the NEOs to reinforce the alignment of their economic interests with other ManpowerGroup shareholders. |

Program Policies

| • | Independent compensation consultant — The committee engages an independent compensation consultant who performs services solely in support of the committee. The committee has also adopted guidelines for minimizing potential conflicts of interest involving the independent compensation consultant. |

21

| • | Competitive market — The Company benchmarks its executive compensation program for the NEOs against the competitive market. For NEOs, target performance is intended to result in compensation levels which approximate median compensation results in the competitive market. The Company’s goal is to only pay above the median of the competitive market for exceptional financial and individual performance. |

| • | Hedging policy — ManpowerGroup has a policy prohibiting executives from engaging in short-selling of ManpowerGroup securities and buying and selling puts and calls on ManpowerGroup securities without advance approval. |

In addition to the compensation practices and policies described above, the Company has adopted the following improvements in corporate governance:

| • | Adoption of a majority voting requirement in non-contested election of directors, |

| • | Implementation of comprehensive lead director appointment and responsibilities, and |

| • | Significant expansion in the Company’s code of business conduct and ethics policy. |

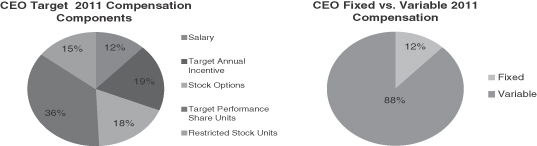

Summary of 2011 CEO Compensation Components and Results

The discussion below provides details regarding the components of the CEO’s 2011 compensation as well as the performance results related to those components.

Approximately 73% of our CEO’s 2011 compensation is tied to performance and 88% of his total pay is variable. The following charts show the components of our CEO’s 2011 target compensation and the mix between fixed and variable pay. For the 2011 target compensation components and results for our other NEOs, please see the discussion beginning on page 29.

Base Pay

The following table illustrates the CEO’s increase in base pay over the last five years:

| 2007 | 2008 | 2009 | 2010 | 2011 | ||||||||||||||||

| Base Pay ($) |

1,000,000 | 1,000,000 | 1,000,000 | 1,000,000 | 1,200,000 | |||||||||||||||

| % increase YOY |

0 | % | 0 | % | 0 | % | 0 | % | 20 | % | ||||||||||

Because Mr. Joerres had not received an increase in base salary since 2005, his salary fell below the market median Given his performance over past years and throughout the economic crisis, the committee determined it was appropriate to give Mr. Joerres a 20% raise in 2011 to bring his salary within a suitable range of the market median. The 20% increase Mr. Joerres received in 2011 equates to an average effective increase of approximately 3% per year for the past six years.

22

Annual Incentive

The following table shows the metrics used and annual incentive payable to the CEO as a percentage of his base salary for achieving threshold, target and maximum levels under those metrics as well as the actual payout for 2011 compared to 2010:

| Threshold | Target | Outstanding | 2011 Actual Payout |

2010 Actual Payout |

||||||||||||||||

| EPS Goal (40% of total opportunity) |

15.0 | % | 60.0 | % | 120.0 | % | 103.2 | % | 86.4 | % | ||||||||||

| EP Goal (40% of total opportunity) |

15.0 | % | 60.0 | % | 120.0 | % | 103.9 | % | 97.8 | % | ||||||||||

| Operating Objective (20% of total opportunity) |

7.5 | % | 30.0 | % | 60.0 | % | 35.5 | % | 48.0 | % | ||||||||||

| Total % of base salary |

37.5 | % | 150 | % | 300 | % | 242.6 | % | 232.2 | % | ||||||||||

| Adjustment Related to 2009 Restatement(1) |

-0.9 | % | -1.7 | % | ||||||||||||||||

| Total ($) |

450,000 | 1,800,000 | 3,600,000 | 2,900,000 | 2,305,521 | |||||||||||||||

| (1) | Mr. Joerres’ 2011 and 2010 incentive was reduced by 0.9% and 1.7% , respectively, related to our 2009 restatement of earnings for a workforce solution contract in which the Company prematurely recorded revenues. This adjustment reflects the reduction in 2010 and 2011 earnings attributable to the restated revenues from this contract for which an incentive had previously been paid to Mr. Joerres. |

Long Term Incentive

Mr. Joerres’ 2011 compensation package consisted of three long-term components:

| • | Approximately 50% of long-term awards in the form of PSUs. Mr. Joerres earned a certain number of shares of stock at the end of the 2011 performance period based on achievement of operating profit margin, with payout of these shares over the next two years based on continued service; |

| • | Approximately 30% of long-term awards in the form of stock options which vest over a four year period and have a ten year expiration; |

| • | Approximately 20% of long-term awards in the form of restricted stock units (RSUs) which are settled in stock at the end of a three year retention period. |

We believe it is important that the executive compensation program is heavily weighted towards long-term incentives that are linked to performance to appropriately focus Mr. Joerres’ and the other NEOs’ attention on the long-term impact of their decisions. The results of the performance share units granted to Mr. Joerres in 2011 and 2010 are as follows:

| • | The following table shows the 2010 operating profit margin goals at threshold, target and maximum levels, including the payout levels and actual level achieved: |

| Threshold | Target | Outstanding | 2010 Level Achieved(1) |

|||||||||||||

| Operating Profit Margin Goals |

0.60 | % | 0.95 | % | 2.00 | % | 1.82 | %(2) | ||||||||

| Vesting % |

50 | % | 100 | % | 200 | % | 183 | % | ||||||||

| PSUs |

20,500 | 41,000 | 82,000 | 75,030 | ||||||||||||

| (1) | In order to receive his vested shares, the threshold operating profit margin had to be maintained in 2011. Operating profit margin was 2.49% in 2011. These PSUs were awarded in the form of common stock in February 2012. |

| (2) | Actual operating profit margin has been adjusted to exclude certain non-recurring costs, as defined in the plan. |

23

Although Mr. Joerres received 183% of the target level of shares, because of the stock price decline over the performance period, Mr. Joerres only received 156% of the long-term grant value reported in the Summary Compensation Table for 2010.

| • | The following table shows the 2011 operating profit margin goals at threshold, target and maximum levels, including the payout levels and the actual level achieved based on the Company’s performance during the performance period: |

| Threshold | Target | Outstanding | 2011 Level Achieved(1) |

|||||||||||||

| Operating Profit Margin Goals |

1.50 | % | 2.20 | % | 2.70 | % | 2.49 | %(2) | ||||||||

| Vesting % |

50 | % | 100 | % | 200 | % | 158 | % | ||||||||

| PSUs |

26,073 | 52,146 | 104,292 | 82,391 | ||||||||||||

| (1) | An operating profit “gate” of $308.5 million was also established. If operating profit did not exceed this level, Mr. Joerres could not receive more than 100% of the target level payout. Because this level was achieved, Mr. Joerres will receive 50% of the total PSUs earned at the end of 2012 and the remaining 50% at the end of 2013 as long as he is still employed on those dates. |

| (2) | Actual operating profit margin has been adjusted to exclude non-recurring costs, as defined in the plan. |

| Although Mr. Joerres will receive 158% of the target number of PSUs, the ultimate value of his award will depend on the closing stock price on the date these shares are received. |

Other Compensation

As described in the All Other Compensation Table on page 45, Mr. Joerres receives an automobile under our broad-based auto program, in which ManpowerGroup pays for 75% of the cost of a leased car, and is also reimbursed for financial planning assistance. In addition, Mr. Joerres received a company match and profit sharing contribution under the terms of our Nonqualified Savings Plan, which is a plan maintained for “highly compensated” employees. For more information regarding the company’s non-qualified savings plan, see page 40.

Objectives of Compensation Program

In making decisions regarding compensation elements, program features and compensation award levels, ManpowerGroup is guided by a series of principles, listed below. Within the framework of these principles, ManpowerGroup considers governance trends, the competitive market, corporate, business unit and individual results, and various individual factors.

ManpowerGroup’s executive compensation guiding principles are to: