Table of Contents

As filed with the Securities and Exchange Commission on June 15, 2017

Registration Statement No. 333-217914

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C.

AMENDMENT NO. 2

TO

REGISTRATION STATEMENT

UNDER

SCHEDULE B

OF

THE SECURITIES ACT OF 1933

THE KOREA DEVELOPMENT BANK

(Name of Registrant)

THE REPUBLIC OF KOREA

(Co-Registrant and Guarantor)

Names and Addresses of Authorized Representatives in the United States:

| Nak Joo Seong or Young Eun Ban Duly Authorized Representatives of The Korea Development Bank 320 Park Avenue, 32nd Floor New York, NY 10022 |

Seong-wook Kim Duly Authorized Representative of The Republic of Korea 460 Park Avenue, 9th Floor New York, NY 10022 |

Copies to:

Jinduk Han, Esq.

Cleary Gottlieb Steen & Hamilton LLP

c/o 19F, Ferrum Tower

19, Eulji-ro 5-gil, Jung-gu

Seoul 04539, Korea

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

The securities registered hereby will be offered on a delayed or continuous basis pursuant to the procedures set forth in Securities Act Release Nos. 33-6240 and 33-6424.

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of each class of securities being registered |

Amount to be registered(2) |

Amount of registration fee | ||

| Debt securities, with or without warrants to purchase debt securities, and guarantees(1) |

US$6,000,000,000 | US$695,400 | ||

| Guarantees of The Republic of Korea |

— (3) | — (3) | ||

|

| ||||

|

| ||||

| (1) | Consists of guarantees to be issued by The Korea Development Bank in respect of obligations of other parties. |

| (2) | Or an equivalent amount in another currency or currencies or in composite currencies or as determined by reference to an index or, if the debt securities are to be offered at a discount, the approximate proceeds to The Korea Development Bank. Includes the maximum principal amount of the obligations to be guaranteed by the Registrants under the guarantees registered hereby. |

| (3) | The Republic of Korea may irrevocably guarantee the debt securities being registered hereby. Pursuant to Rule 457(n) of the Securities Act of 1933, no registration fee is required with respect to the guarantees. |

Pursuant to Rule 429 under the Securities Act of 1933, the Prospectus contained in this Registration Statement and supplements to such Prospectus will also be used in connection with US$1,847,380,000 of debt securities with or without warrants to purchase debt securities registered under Registration Statement No. 333-203739.

The Registrants hereby amend this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrants shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

| * | This Registration Statement also constitutes Post-Effective Amendment No. 9 to Registration Statement No. 333-203739. |

Table of Contents

EXPLANATORY NOTE

This registration statement relates to US$6,000,000,000 aggregate amount of (i) debt securities (with or without warrants) of The Korea Development Bank to be offered from time to time as separate issues on terms and in the manner to be specified in a prospectus supplement to be delivered in connection with each such offering, (ii) guarantees that may be issued by The Korea Development Bank in respect of obligations of other parties on terms and in the manner to be specified in a prospectus supplement to be delivered in connection with each such issuance and (iii) guarantees that may be issued by The Republic of Korea in respect of debt securities of The Korea Development Bank on terms and in the manner to be specified in a prospectus supplement to be delivered in connection with each such issuance. The prospectus constituting a part of this registration statement relates to (i) the debt securities (with or without warrants) and guarantees to be issued by The Korea Development Bank, registered hereunder, (ii) guarantees to be issued by The Republic of Korea, registered hereunder and (iii) US$1,847,380,000 aggregate principal amount of debt securities (with or without warrants) and guarantees registered under Registration Statement No. 333-203739 (including an aggregate principal amount of US$200,000,000 of debt securities that may be sold by us from time to time in a continuous offering designated Medium-Term Notes, Series C, Due Not Less Than Nine Months From Date of Issue (the “Series C Notes”)).

This registration statement contains a form of prospectus supplement filed as Exhibit K-1 to this registration statement, together with the supplement to that prospectus supplement filed as Exhibit K-2 to this registration statement, to be used in connection with the sale by us of the Series C Notes in a continuous offering.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED JUNE 15, 2017

PROSPECTUS

$7,847,380,000

The Korea Development Bank

Debt Securities

Warrants to Purchase Debt Securities

Guarantees

The Republic of Korea

Guarantees

We will provide the specific terms of these securities in supplements to this prospectus. You should read this prospectus and any prospectus supplement carefully before you invest.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

This prospectus is dated , 2017

Table of Contents

| Page | ||||

| 1 | ||||

| 2 | ||||

| 3 | ||||

| 3 | ||||

| 7 | ||||

| 7 | ||||

| 9 | ||||

| 16 | ||||

| 23 | ||||

| 24 | ||||

| 26 | ||||

| 26 | ||||

| 26 | ||||

| 27 | ||||

| 32 | ||||

| 158 | ||||

| 158 | ||||

| 160 | ||||

| 163 | ||||

| 171 | ||||

| 178 | ||||

| 183 | ||||

| 187 | ||||

| 195 | ||||

| 198 | ||||

| 200 | ||||

| 203 | ||||

| 203 | ||||

| 209 | ||||

| 210 | ||||

| 211 | ||||

| Description of Guarantees to be Issued by The Republic of Korea |

211 | |||

| LIMITATIONS ON ISSUANCE OF BEARER DEBT SECURITIES AND BEARER WARRANTS |

213 | |||

| 214 | ||||

| 214 | ||||

| 216 | ||||

| 224 | ||||

| 225 | ||||

| 225 | ||||

| 225 | ||||

| 225 | ||||

| 226 | ||||

| 228 | ||||

i

Table of Contents

CERTAIN DEFINED TERMS AND CONVENTIONS

All references to the “Bank”, “we”, “our” or “us” mean The Korea Development Bank. All references to “Korea” or the “Republic” contained in this prospectus mean The Republic of Korea. All references to the “Government” mean the government of Korea.

Unless otherwise indicated,

all references to “won”, “Won” or “W” contained in this prospectus are to the currency of Korea, references to “U.S. dollars”, “Dollars”, “$”, “USD” or

“US$” are to the currency of the United States of America, references to “Euro”, “EUR” or “€” are to the currency of the European Union, references to “Japanese yen”, “JPY” or

“¥” are to the currency of Japan, references to “Singapore dollar” or “SGD” are to the currency of Singapore, references to “Swiss franc” or “CHF” are to the currency of Switzerland, references

to “pound sterling”, “GBP” or “£” are to the currency of the United Kingdom, references to “Chinese offshore renminbi” or “CNH” are to the currency of the People’s Republic of China traded

outside of mainland China, references to “Hong Kong dollar” or “HKD” are to the currency of Hong Kong, S.A.R., references to “Malaysian ringgit” or “MYR” are to the currency of Malaysia, references to

“Mexican Peso” or “MXN” are to the currency of the United Mexican States, references to “New Zealand Dollar” or “NZD” are to the currency of New Zealand, references to “Australian dollar” or

“AUD” are to the currency of Australia, references to “South African Rand” or “ZAR” are to the currency of South Africa, references to “Turkish Lira” or “TRY” are to the currency of Turkey,

references to “Norwegian krone” or “NOK” are to the currency of Norway and references to “Brazilian real” or “BRL” are to the currency of the Federative Republic of Brazil.

All discrepancies in any table between totals and the sums of the amounts listed are due to rounding.

Our separate financial information as of and for the years ended December 31, 2016 and 2015 included in this prospectus has been prepared in accordance with International Financial Reporting Standards as adopted in Korea (“Korean IFRS” or “K-IFRS”). References in this prospectus to “separate” financial statements and information are to financial statements and information prepared on a non-consolidated basis. Unless specified otherwise, our financial and other information included in this prospectus is presented on a separate basis in accordance with Korean IFRS and does not include such information with respect to our subsidiaries. KDB Financial Group (or KDBFG), a financial holding company, and Korea Finance Corporation (or KoFC), a public policy financing vehicle and the parent company of KDBFG, both of which had originally been established by spinning off a portion of our assets, liabilities and equity in October 2009, merged with and into us on December 31, 2014.

1

Table of Contents

Unless otherwise specified in the applicable prospectus supplement, we will use the net proceeds from the sale of the securities for our general operations.

2

Table of Contents

We were established in 1954 as a government-owned financial institution pursuant to The Korea Development Bank Act, as amended (the “KDB Act”). Since our establishment, we have been the leading bank in the Republic with respect to the provision of long-term financing for projects designed to assist the nation’s economic growth and development. The Government directly owns all of our paid-in capital. Our registered office is located at 14, Eunhaeng-ro, Youngdeungpo-gu, Seoul, The Republic of Korea.

In June 2008, the Financial Services Commission announced the Government’s preliminary plan for our privatization and, in May 2009, the KDB Act was amended to facilitate our privatization. The preliminary plan reflected the Government’s intention to nurture a more competitive corporate and investment banking sector and trigger reorganization and further advancement of the Korean financial industry.

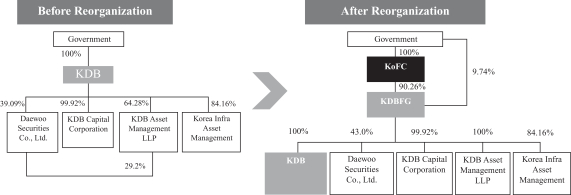

To implement our privatization, the Government established KDB Financial Group, or KDBFG, a financial holding company, and Korea Finance Corporation, or KoFC, a public policy financing vehicle, in October 2009, by spinning off a portion of our assets, liabilities and equity. In the spin-off, our interests in Daewoo Securities Co., Ltd., KDB Asset Management Co., Ltd. and KDB Capital Corp. were transferred to KDBFG, and our equity holdings in certain government-controlled companies, including Korea Electric Power Corporation, or KEPCO, and certain companies under restructuring programs, including Hyundai Engineering & Construction Co., Ltd., were transferred to KoFC. The Government transferred its ownership interest in us to KDBFG in exchange for all of KDBFG’s share capital on November 24, 2009.

The following diagram shows our ownership structure before and after the spin-off and the share transfer.

In April 2013, in light of continued uncertainties surrounding the global economy and the prolonged effects of the global financial crisis that commenced in the second half of 2008 on the Korean economy, as well as certain overlap of financial policy roles among different Government-owned banks and financial corporations, the Government launched a task force (the “Task Force”) to consider the reorganization of the financial policy roles of Government-owned banks and financial corporations, including the Government’s plan for our privatization. The Task Force, composed of representatives from various government branches responsible for overseeing such Government-owned entities as well as members of the academia, held a series of closed meetings, considered various reorganization options with respect to policy financing functions and reported their findings to the Financial Services Commission. In August 2013, pursuant to the findings of the Task Force, the Financial Services Commission announced the Government’s plan to reorganize Government-owned policy banks and financial corporations in order to streamline their overlapping functions and reinforce their policy financing roles for start-ups and small- and medium-sized enterprises, new growth industries and overseas projects. The plan called for, among other things, (i) the merger of KoFC and KDBFG into us and the transfer of

3

Table of Contents

KoFC’s overseas assets of approximately W2 trillion to The Export-Import Bank of Korea, or KEXIM, (ii) the sale of our subsidiaries that do not have policy

financing roles and (iii) the gradual reduction of our retail banking services.

In May 2014, the National Assembly amended the KDB Act to largely reflect the plan announced by the Financial Services Commission and halt our privatization and streamline the financial policy roles among

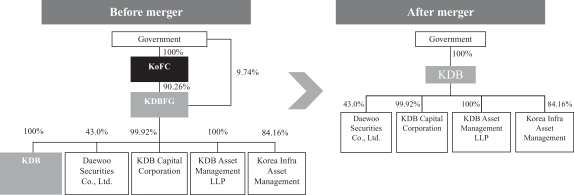

Government-owned banks and financial corporations in order to better respond systematically to rapidly changing domestic and international economic conditions. Under the amended KDB Act, which was amended in May 2014, the public policy financing

role was consolidated and strengthened, and KDBFG and KoFC (together with its subsidiaries) were merged into us on December 31, 2014 in order to utilize our rich experience and expertise in public policy financing, and we took over KoFC’s

role of providing public policy financial support to Korean companies, including managing and operating the Financial Market Stabilization Fund established pursuant to the Act on the Structural Improvement of the Financial Industry enacted in 2009,

while KoFC’s overseas assets of approximately W2 trillion were transferred to KEXIM. On December 31, 2014, the Government transferred all of its ownership interest in KoFC and KDBFG to us and in return received

3,036,079,768 new shares of us with an aggregate par value of W15,180.4 billion. As a newly merged entity, we have an authorized share capital of up to W30,000 billion and our paid-in capital was W15,180.4 billion. As of the date of this prospectus, the Government owns 100% of our share capital.

The following diagram shows our ownership structure before and after the merger was effected under the amended KDB Act. Our ownership structure returned to our original ownership structure that existed prior to the spin-off and reorganization in October 2009.

While the Government has halted its plan for our privatization, it has expressed its intention to privatize our subsidiaries that do not have policy financing roles, subject to market conditions.

Our primary purpose, as stated in the KDB Act, the KDB Decree and our Articles of Incorporation, is to “furnish funds in order to expedite the development of the national economy.” We make loans available to major industries for equipment, capital investment and the development of high technology, as well as for working capital.

As of

December 31, 2016, we had W141,321.2 billion of loans outstanding (including loans, call loans, domestic usance, bills of exchange bought, local letters of credit negotiation and loan-type suspense accounts pursuant to the

applicable guidelines without adjusting for allowance for possible loan losses, present value discounts and deferred loan fees), total assets of W219,075.9 billion and total equity of W22,565.0 billion, as

compared to W140,968.3 billion of loans outstanding, W224,460.7 billion of total assets and W25,255.6 billion of total equity as of December 31, 2015. In 2016, we recorded

interest income of W5,014.0 billion, interest expense of W3,589.6 billion and net loss of W3,641.1 billion, as compared to W5,490.4 billion of interest income,

W3,912.2 billion of interest expense and W1,895.1 billion of net loss in 2015. See “—Selected Financial Statement Data.”

4

Table of Contents

Currently, the Government directly holds all of our paid-in capital. In addition to contributions to our capital, the Government provides direct financial support for our financing activities, in the form of loans or guarantees. The Government has the power to elect or dismiss our Chairman and Chief Executive Officer, members of our Board of Directors and Auditor. The Government may dismiss each such person if he/she (i) violates the KDB Act, an order issued thereunder, or the Articles of Incorporation or (ii) is unable to perform his/her duties due to physical or mental disability. The Chairman may be dismissed by the President of the Republic at the recommendation of the chairman of the Financial Services Commission. The Chief Executive Officer and members of the Board of Directors may be dismissed by the chairman of the Financial Services Commission at the recommendation of the Chairman and the Auditor may be dismissed by the Financial Services Commission. There is no prescribed timeline for dismissal. Pursuant to the KDB Act, the Financial Services Commission has supervisory power and authority over matters relating to our general business including, but not limited to, capital adequacy and managerial soundness.

The Government supports our operations pursuant to Article 32 of the KDB Act. Article 32 provides that “the annual net losses of the Korea Development Bank shall be offset each year by the reserve, and if the reserve be insufficient, the deficit shall be replenished by the Government.” As a result of the KDB Act, the Government is generally responsible for our operations and is legally obligated to replenish any deficit that arises if our reserve, consisting of our surplus and capital surplus items, is insufficient to cover our annual net losses. In light of the above, if we had insufficient funds to make any payment under any of our obligations, including the debt securities and guarantees covered by this prospectus, the Government would take appropriate steps, such as by making a capital contribution, by allocating funds or by taking other action, to enable us to make such payment when due. The provisions of Article 32 do not, however, constitute a direct guarantee by the Government of our obligations under the debt securities or the guarantees, and the provisions of the KDB Act, including Article 32, may be amended at any time by action of the National Assembly.

In January 1998, the Government amended the KDB Act to:

| • | subordinate our borrowings from the Government to other indebtedness incurred in our operations; |

| • | allow the Government to offset any deficit that arises if our reserve fails to cover our annual net losses by transferring Government-owned property, including securities held by the Government, to us; and |

| • | allow direct injections of capital by the Government without prior National Assembly approval. |

The Government amended the KDB Act in May 1999 and the KDB Decree in March 2000, to allow the Financial Services Commission to supervise and regulate us in terms of capital adequacy and managerial soundness.

In March 2002, the Government amended the KDB Act to enable us, among other things, to:

| • | obtain low-cost funds from The Bank of Korea and from the issuance of debt securities (in addition to already permitted Industrial Finance Bonds), which funds may be used for increased levels of lending to small and medium size enterprises; |

| • | broaden the scope of borrowers to which we may extend working capital loans to include companies in the manufacturing industry, enterprises which are “closely related” to enhancing the corporate competitiveness of the manufacturing industry and leading-edge high-tech companies; and |

| • | extend credits to mergers and acquisitions projects intended to facilitate corporate restructuring efforts. |

In July 2005 and May 2009, the Government amended the KDB Act to provide that:

| (1) | our annual net profit, after adequate allowances are made for depreciation in assets, shall be distributed as follows: |

| (i) | forty percent or more of the net profit shall be credited to reserve, until the reserve amounts equal the total amount of paid-in capital; and |

| (ii) | any net profit remaining following the apportionment required under subparagraph (i) above shall be distributed in accordance with the resolution of our Board of Directors and the approval of our shareholders; |

5

Table of Contents

| (2) | accumulated amounts in reserve may be capitalized after offsetting any net losses; and |

| (3) | any distributions made in accordance with paragraph (1)(ii) above may be in the form of cash dividends or dividends in kind, provided that any distributions of dividends in kind must be made in accordance with applicable provisions of the KDB Decree. |

In February 2008, the Government further amended the KDB Act, primarily to transfer most of the Government’s supervisory authority over us from the Ministry of Strategy and Finance (formerly the Ministry of Finance and Economy) to the Financial Services Commission.

In May 2009, the Government amended the KDB Act to facilitate our privatization. The amendment provided for, among others:

| • | the preparation for the transformation of us from a special statutory entity into a corporation, including the application of the Banking Act as applicable; |

| • | the expansion of our operation scope that enables us to engage in commercial banking activities, including retail banking (which was subsequently adjusted due to a change in the Government’s decision to halt its plan for our privatization and to consolidate and strengthen our public financing role, utilizing our rich experience and expertise in public policy financing); |

| • | the provision of government guarantees for our mid-to-long term foreign currency debt outstanding at the time of initial sale of the Government’s stake in KDBFG (subject to the National Assembly’s authorization of the Government guarantee amount) and possible guarantees for our foreign currency debt incurred for the refinancing of such mid-to-long term foreign currency debt with the government guarantee during the period when the Government owns more than 50% of our shares; and |

| • | the establishment of KDBFG and KoFC and application of the Financial Holding Company Act to KDBFG. |

In May 2014, the Government and the National Assembly amended the KDB Act to streamline the financial policy roles among Government-owned banks and financial corporations in order to better respond systematically to rapidly changing domestic and international economic conditions by merging KDBFG and KoFC into us. The amended KDB Act provides, among others, that:

| • | the Government will halt its plan for our privatization; |

| • | public policy financing will be consolidated and strengthened through the newly merged entity; |

| • | we will comprehensively succeed to the properties, rights and obligations of KDBFG and KoFC upon the consummation of the merger; |

| • | the bonds issued by KDBFG and the policy bank bonds issued by the KoFC shall be deemed as the industrial financial bonds issued by us; |

| • | the business engaged in by KoFC in accordance with the Korea Finance Corporation Act or other laws and decrees will be continuously performed by us; and |

| • | the repayment of the principal of and interest on foreign currency debt (with an original maturity of one year or more at the time of issuance) incurred by KoFC and us before this amended KDB Act comes into force shall be guaranteed by the Government at the time of initial sale by the Government of its equity interest in us, subject to the approval by the National Assembly. |

The Minister of Strategy and Finance of the Republic has, on behalf of the Republic, signed the registration statement of which this prospectus forms a part.

6

Table of Contents

As of December 31, 2016, our authorized capital was W30,000 billion and

capitalization was as follows:

| December

31, 2016(1) |

||||

| (billions of won) | ||||

| Long-term debt: |

||||

| Won currency borrowings |

||||

| Industrial finance bonds |

109,912.7 | |||

| Foreign currency borrowings |

6,843.2 | |||

|

|

|

|||

| Total long-term debt |

120,586.1 | (2)(3) | ||

|

|

|

|||

| Capital: |

||||

| Paid-in capital |

17,543.1 | |||

| Capital surplus |

2,499.9 | |||

| Retained earnings(4) |

1,308.5 | |||

| Accumulated other comprehensive income |

1,213.5 | |||

|

|

|

|||

| Total capital |

22,565.0 | |||

|

|

|

|||

| Total capitalization |

||||

|

|

|

|||

| (1) | Except as disclosed in this prospectus, there has been no material adverse change in our capitalization since December 31, 2016. |

| (2) | We have translated borrowings in foreign currencies into Won at the rate of |

| (3) | As of December 31, 2016, we had contingent liabilities totaling |

| (4) | Includes regulatory reserve for loan losses of |

Purpose and Authority

Since our establishment, we have been the leading bank in the Republic in providing long-term financing for projects designed to assist the nation’s economic growth and development.

Under the KDB Act, the KDB Decree and our Articles of Incorporation, our primary purpose is to “contribute to the sound development of the financial industry and the national economy by supplying and managing funds necessary for the development and promotion of industries, expansion of social infrastructure, development of regions, stabilization of the financial markets and facilitation of sustainable growth.” Since we serve the public policy objectives of the Government, we do not seek to maximize profits. We do, however, strive to maintain a level of profitability to strengthen our equity base and support growth in the volume of our business.

Under the KDB Act, we may:

| • | carry out activities necessary to accomplish the expansion of the national economy, subject to the approval of the Financial Services Commission; |

| • | provide loans or discount notes; |

7

Table of Contents

| • | subscribe to, underwrite or invest in securities; |

| • | guarantee or assume indebtedness; |

| • | raise funds by accepting demand deposits and time and savings deposits from the general public, issuing securities, borrowing from the Government, The Bank of Korea or other financial institutions, and borrowing from overseas; |

| • | execute foreign exchange transactions, including currency and interest swap transactions; |

| • | provide planning, management, research and other support services at the request of the Government, public bodies, financial institutions or enterprises; and |

| • | carry out other businesses incidental to the foregoing (subject to the approval of the Financial Services Commission). |

Government Support and Supervision

The Government owns directly all of our paid-in capital. On February 20, 2000, the Government contributed W100 billion in cash to our capital. On December 29, 2000, we reduced our

paid-in capital by W959.8 billion to offset our expected net loss for the year. To compensate for the resulting deficit under the KDB Act, on June 20, 2001, the Government

contributed W3 trillion in the form of shares of common stock of KEPCO to our capital. On December 29, 2001, the Government contributed W50 billion in cash to our capital. On August 13, 2003, the

Government contributed W80 billion in cash to our capital to support our existing fund for facilitating the Republic’s regional economies. On April 30, 2004, the Government contributed W1 trillion in

the form of shares of common stock of KEPCO and Korea Water Resources Corporation to our capital to support our lending to small-and medium-sized companies and to

compensate for our contribution to LG Card Ltd. in the form of loans, cash injections and debt-for-equity swaps. On December 19, 2008, the Government contributed

W500 billion in the form of shares of common stock of Korea Expressway Corporation to our capital and, in January 2009, the Government contributed W900 billion in cash to our capital, in each case to

bolster our capital base in order to stabilize the Korean financial market by supporting small and medium-sized enterprises and providing increased liquidity to corporations. In October 2009, our paid-in capital decreased by W400.0 billion in connection with the establishment by the Government of KDBFG and KoFC by spinning off a portion of our assets, liabilities and equity (including paid-in capital). In March 2010, the Government, through KDBFG, made a further capital contribution of W10 billion in cash to our capital. In December 2013, the Government contributed

W10 billion in cash to our capital. In December 2014, our paid-in capital increased by W5,918.5 billion in connection with the merger of KDBFG and KoFC into us as

described under the heading “Overview” in this prospectus. .” In April, July and September 2015, the Government contributed W2 trillion in the form of shares of common stock of Korea Land & Housing

Corporation and KEPCO, W40 billion in cash and W15 billion in cash, respectively, to our capital to support our fund for infrastructure projects, new growth engine, high-tech and new renewable energy

industries and business enterprises in general. The Government further contributed to our capital W50 billion in cash in July 2016, W247.7 billion in cash in September 2016 and

W10 billion in cash in November 2016. Taking into account these capital contributions, reduction and merger, as of December 31, 2016, our total paid-in capital was

W17,543.1 billion. See “—Financial Statements and the Auditors—Notes to Separate Financial Statements of December 31, 2016 and 2015—Note 23.”

In addition to capital contributions, the Government directly supports our financing activities by:

| • | lending us funds to on-lend; |

| • | allowing us to administer Government loans made from a range of special Government funds; |

| • | allowing us to administer some of The Bank of Korea’s surplus foreign exchange holdings; and |

| • | allowing us to receive credit from The Bank of Korea. |

The Government also supports our operations pursuant to Articles 31 and 32 of the KDB Act. Article 31 provides that “40% or more of the annual net profit of the Korea Development Bank shall be transferred to

8

Table of Contents

reserve, until the reserve amounts equal the total amount of authorized capital” and that accumulated amounts in reserve may be capitalized. Article 32 provides that “the net losses of the Korea Development Bank shall be offset each fiscal year by the reserve, and if the reserve be insufficient, the deficit shall be replenished by the Government.”

As a result of the KDB Act, the Government is generally responsible for our operations and is legally obligated to replenish any deficit that arises if our reserve, consisting of our surplus and capital surplus items, is insufficient to cover our annual net losses. In light of the above, if we had insufficient funds to make any payment under any of our obligations, including the debt securities and the guarantees covered by this prospectus, the Government would take appropriate steps, such as by making a capital contribution, by allocating funds or by taking other action, to enable us to make such payment when due. The provisions of Article 32 do not, however, constitute a direct guarantee by the Government of our obligations under the debt securities or the guarantees, and the provisions of the KDB Act, including Article 32, may be amended at any time by action of the National Assembly.

The Government closely supervises our operations in the following ways:

| • | the Government has the power to elect or dismiss our Chairman and Chief Executive Officer, members of our Board of Directors and Auditor; |

| • | within three months after the end of each fiscal year, we must submit our financial statements for the fiscal year to the Financial Services Commission; |

| • | the Financial Services Commission has broad authority to require reports from us on any matter and to examine our books, records and other documents. On the basis of the reports and examinations, the Financial Services Commission may issue any orders deemed necessary to enforce the KDB Act; |

| • | the Financial Services Commission must approve our operating manual, which sets out the guidelines for all principal operating matters; |

| • | the Financial Services Commission may supervise our operations to ensure managerial soundness based upon the KDB Decree and the Bank Supervisory Regulations of the Financial Services Commission and may issue orders deemed necessary for such supervision; and |

| • | we may amend our Articles of Incorporation only with the approval of the Financial Services Commission. |

In addition, the conditions of the IMF aid package stated that domestic banks in the Republic, including us, should undergo external audits from internationally recognized accounting firms. Accordingly, we have had our annual financial statements for years commencing 1998 audited by an external auditor. See “—Financial Statements and the Auditors” and “Experts.”

Pursuant to our most recently approved program of operations, we expect to support the reform and restructuring of the Republic’s economic and industrial structure, including financing of promising small and medium sized enterprises, providing export finance and encouraging investments in infrastructure necessary to promote consumer demand and industrial reorganization.

Selected Financial Statement Data

Unless specified otherwise, the information provided below is stated on a separate basis in accordance with Korean IFRS.

9

Table of Contents

Consolidated Statements of Financial Position Data

The following table presents selected statements of financial position data regarding our assets, liabilities and shareholders’ equity on a consolidated basis as of December 31, 2015 and 2016, which have been derived from our audited consolidated financial statements as of and for the years ended December 31, 2015 and 2016.

| As of December 31, | ||||||||

| 2015(1) | 2016 | |||||||

| (billions of won) | ||||||||

| Statements of Financial Position Data |

||||||||

| Total Loans(2) |

147,018.1 | 147,855.5 | ||||||

| Total Borrowings(3) |

198,247.4 | 194,384.6 | ||||||

| Total Assets |

309,316.3 | 272,837.8 | ||||||

| Total Liabilities |

275,202.5 | 241,818.4 | ||||||

| Equity |

34,113.8 | 31,019.5 | ||||||

| (1) | Daewoo Shipbuilding & Marine Engineering Co., Ltd., our associate, restated its consolidated financial statements as of and for the year ended

December 31, 2015, primarily due to errors in estimating construction costs, which affected our statements of financial position data as of December 31, 2015 (including a decrease in our assets by |

| (2) | Gross amount, which includes loans for facility development, loans for working capital, inter-bank loans, private loans, off-shore loan receivables, loans borrowed from overseas financial institutions, bills bought in foreign currencies, advance payments on acceptances and guarantees and other loans without adjusting for allowance for loan losses, present value discounts and deferred loan fees. |

| (3) | Total Borrowings include deposits, financial liabilities designated at fair value through profit or loss, borrowings and debt issued. |

Consolidated Income Statement Data

Our selected income statement data included in the following table have been derived from our audited consolidated financial statements as of and for the years ended December 31, 2015 and 2016.

| Year Ended December 31, |

||||||||

| 2015(1) | 2016 | |||||||

| (billions of Won) | ||||||||

| Income Statement Data |

||||||||

| Total Interest Income |

6,304.6 | 5,777.7 | ||||||

| Total Interest Expense |

4,053.6 | 3,734.0 | ||||||

| Net Interest Income |

2,251.0 | 2,043.7 | ||||||

| Operating Income (Loss) |

(1,091.7 | ) | (3,154.3 | ) | ||||

| Non-operating Income (Loss) |

4,158.8 | 1,916.3 | ||||||

| Income (Loss) before Income Tax |

3,067.2 | (1,238.0 | ) | |||||

| Income Tax Benefit (Expense) |

(1,035.8 | ) | (1,118.4 | ) | ||||

| Income from discontinued operations |

56.7 | 294.8 | ||||||

| Net Income (Loss) |

2,088.1 | (2,061.6 | ) | |||||

| (1) | Daewoo Shipbuilding & Marine Engineering Co., Ltd., our associate, has restated its consolidated financial statements as of and for the year

ended December 31, 2015, primarily due to errors in estimating construction costs, which affected our income statement data in 2015 (including an increase in net income by |

10

Table of Contents

| strengthen the supervision of accounting, particularly in the shipbuilding and construction industries, to achieve enhanced transparency and ensure fair operation of the external audit system and prevent accounting firms that fail to meet certain requirements from auditing listed companies. |

Separate Financial Statement Data

The following tables present selected separate financial information as of and for the years ended December 31, 2015 and 2016, which has been derived from our audited separate financial statements as of and for the years ended December 31, 2015 and 2016 included in this prospectus. You should read the following financial statement data together with the financial statements and notes included in this prospectus.

| As of December 31, | ||||||||

| 2015 | 2016 | |||||||

| (billions of won) | ||||||||

| Statements of Financial Position Data |

||||||||

| Total Loans(1) |

140,968.3 | 141,321.2 | ||||||

| Total Borrowings(2) |

182,852.1 | 180,357.7 | ||||||

| Total Assets |

224,460.7 | 219,075.9 | ||||||

| Total Liabilities |

199,205.1 | 196,510.9 | ||||||

| Equity |

25,255.6 | 22,565.0 | ||||||

| (1) | Gross amount, which includes loans for facility development, loans for working capital, inter-bank loans, private loans, off-shore loan receivables, loans borrowed from overseas financial institutions, bills bought in foreign currencies, advance payments on acceptances and guarantees and other loans without adjusting for allowance for loan losses, present value discounts and deferred loan fees. |

| (2) | Total Borrowings include deposits, financial liabilities designated at fair value through profit or loss, borrowings and debt issued. |

As of December 31, 2016, our total assets decreased by

2.4% to W219,075.9 billion from W224,460.7 billion as of December 31, 2015, primarily due to a decrease in

available-for-sale financial assets to W36,680.1 billion from W41,291.6 billion and a decrease in investments in subsidiaries

and associates to W22,776.4 billion from W25,167.8 billion, which more than offset an increase in loans to W141,321.2 billion from W140,968.3 billion.

As of December 31, 2016, our total

liabilities decreased by 1.4% to W196,510.9 billion from W199,205.1 billion as of December 31, 2015, primarily due to a decrease in deposits to W37,677.8 billion from

W39,934.9 billion and a decrease in borrowings to W23,600.0 billion from W24,400.6 billion, which more than offset an increase in bonds to W117,186.9 billion

from W116,894.0 billion.

As

of December 31, 2016, our total shareholders’ equity decreased by 10.7% to W22,565.0 billion from W25,255.6 billion as of December 31, 2015, primarily due to a decrease in retained earnings

to W1,308.5 billion from W4,949.6 billion, which more than offset an increase in accumulated other comprehensive income to W1,213.5 billion from W569.2 billion

and an increase in paid-in capital to W17,543.1 billion from W17,235.4 billion.

11

Table of Contents

Our selected income statement data included in the following table have been derived from our audited separate financial statements as of and for the years ended December 31, 2015 and 2016 included in this prospectus.

| Year Ended December 31, |

||||||||

| 2015 | 2016 | |||||||

| (billions of Won) | ||||||||

| Income Statement Data |

||||||||

| Total Interest Income |

5,490.4 | 5,014.0 | ||||||

| Total Interest Expense |

3,912.2 | 3,589.6 | ||||||

| Net Interest Income |

1,578.2 | 1,424.4 | ||||||

| Operating Income (Loss) |

(1,219.3 | ) | (1,270.5 | ) | ||||

| Income (Loss) before Income Tax |

(2,360.8 | ) | (3,894.1 | ) | ||||

| Income Tax Benefit (Expense) |

465.7 | 253.0 | ||||||

| Net Income (Loss) |

(1,895.1 | ) | (3,641.1 | ) | ||||

2016

We had net loss of

W3,641.1 billion in 2016 compared to net loss of W1,895.1 billion in 2015, on a separate basis.

Principal factors for the increase in net loss in 2016 compared to 2015 included:

| • | an increase in impairment losses on investments in subsidiaries and associates to |

| • | an increase in provision for loan losses to |

The above factors were partially offset by an increase in dividend income to W1,197.4 billion in 2016 from

W615.3 billion in 2015, primarily due to increased dividends from investments in associates (including Korea Electric Power Corporation, or KEPCO).

We recorded a net cash outflow from operating activities of

W6,070.0 billion for 2016. The primary reasons for the net cash outflow during the period were outflows of W4,369.3 billion due to an increase in loans, W3,641.1 billion from our net loss and

W2,275.4 billion due to a decrease in deposits. These outflows were partially offset by an inflow of W3,249.7 billion from provision for loan losses.

2015

We had net loss of W1,895.1 billion in 2015 compared to net income of W183.5 billion in 2014,

on a separate basis.

Principal factors for the

net loss of W1,895.1 billion in 2015 compared to the net income of W183.5 billion in 2014 included:

| • | an increase in provision for loan losses to |

12

Table of Contents

| • | an increase in impairment losses on investments in subsidiaries and associates to |

| • | a decrease in net interest income to |

| • | an increase in provision for other allowances to |

The above factors were partially offset by an increase in dividend income to W615.3 billion in 2015 from

W158.2 billion in 2014, primarily due to an increase in dividend income from KEPCO.

We recorded a net cash outflow from operating activities of W1,156.3 billion for 2015. The primary reasons for the net

cash outflow during the period were outflows of W6,031.0 billion due to an increase in loans, W2,701.2 billion due to a decrease in derivative financial liabilities and W1,895.1 billion from our net

loss. These outflows were partially offset by inflows of W2,810.1 billion from provision for loan losses, W2,622.3 billion due to an increase in other liabilities and W2,396.7 billion due to an

increase in deposits.

Provisions for Possible Loan Losses and Loans in Arrears

We establish provisions for possible losses from problem loans, including guarantees and other extensions of credit, based on the length

of the delinquent periods and the nature of the loans, including guarantees and other extensions of credit. As of December 31, 2016, we established provisions of W3,313.4 billion for possible loan losses, 20.3% lower than

the provisions as of December 31, 2015 of W4,159.3 billion, primarily due to the write-off of certain non-performing loans and debt-to-equity

swaps. The provisions for possible loan losses under Korean IFRS are recorded for those loans for which objective evidence of impairment exists as a result of one or more events that occurred after initial recognition and, if our provision for

possible loan losses is deemed insufficient for regulatory purposes, we compensate for the difference by recording a regulatory reserve for possible loan losses, which will be deducted from retained earnings. See “—Financial Statements and

the Auditors—Notes to Separate Financial Statements of December 31, 2016 and 2015—Notes 3(26), 23(4) and 23(5).”

Certain of our customers have restructured loans with their creditor banks. As of December 31, 2016, we have provided loans of

W4,723.5 billion for companies under workout, court receivership, court mediation and other restructuring procedures. In addition, as of such date, we held equity securities of such companies in the amount of

W148.7 billion following debt-for-equity swaps. As of December 31, 2016, we had established provisions of W1,870.4 billion for such loans. We cannot assure you that actual results of the credit loss

from the loans to these customers will not exceed the provisions reserved.

13

Table of Contents

The following table provides information on our loan loss provisions.

| As of December 31, 2015(1) | As of December 31, 2016(1) | |||||||||||||||||

| Loan Amount |

Loan Loss Provisions |

Loan Amount |

Loan Loss Provisions |

|||||||||||||||

| (billions of won) | ||||||||||||||||||

| Loan Classification |

Normal(2) | |||||||||||||||||

| Precautionary | 3,559.5 | 434.8 | 5,147.5 | 1,097.3 | ||||||||||||||

| Substandard | 4,768.1 | 2,536.2 | 2,056.8 | 505.1 | ||||||||||||||

| Doubtful | 827.1 | 566.8 | 664.6 | 416.3 | ||||||||||||||

| Expected Loss | 447.1 | 292.7 | 1,359.9 | 988.8 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||

| Total |

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||

| (1) | These figures include loans for facility development, loans for working capital, inter-bank loans, private loans, off-shore loan receivables, loans borrowed from overseas financial institutions, bills bought in foreign currencies, advance payments on acceptances and guarantees and other loans. |

| (2) | Includes loans guaranteed by the Government. Under Korean IFRS, we establish loan loss provisions for all loans including loans guaranteed by the Government. |

As of December 31, 2016, our non-performing loans totaled W4,081.2 billion, representing 2.9% of our outstanding loans as of such date. Non-performing loans are defined as loans that

are classified as substandard or below. On December 31, 2016, our legal reserve was W3,578.8 billion, representing 2.5% of our outstanding loans as of such date.

Loans to Financially Troubled Companies

We have credit exposure (including loans, guarantees and equity investments) to a number of financially

troubled Korean companies including DSME, STX Offshore & Shipbuilding, Dongbu Steel Co., Ltd. Hanjin Heavy Industries and Construction Co., Ltd., Hyundai Merchant Marine Co., Ltd., Daehan Shipbuilding Co., Ltd., Hanjin Shipping Co.,

Ltd., and STX Heavy Industries Co., Ltd. As of December 31, 2016, our credit extended to these companies totaled W14,182.2 billion, accounting for 6.5% of our total assets as of such date.

As of December 31, 2016, our exposure (including loans

classified as substandard or below and equity investment classified as estimated loss or below) to DSME increased to W7,634.4 billion from W6,485.3 billion as of December 31, 2015, primarily due to

the extension of new guarantees. As of December 31, 2016, our exposure to STX Offshore & Shipbuilding was W1,422.8 billion, a decrease from W4,876.5 billion as of December 31, 2015,

primarily due to debt-to-equity swaps. As of December 31, 2016, our exposure to Dongbu Steel decreased to W1,325.2 billion from

W1,407.7 billion as of December 31, 2015, primarily due to the redemption of certain existing loans. As of December 31, 2016, our exposure to Hanjin Heavy Industries and Construction increased to

W1,242.2 billion from W1,216.5 billion as of December 31, 2015, primarily due to the extension of new loans. As of December 31, 2016, our exposure to Hyundai Merchant Marine increased to

W1,080.4 billion from W1,039.1 billion as of December 31, 2015, primarily due to debt-to-equity swaps. As of December 31, 2016, our exposure to Daehan Shipbuilding decreased to

W769.2 billion from W1,453.4 billion as of December 31, 2015, primarily due to a decrease in guarantees. As of December 31, 2016, our exposure to Hanjin Shipping decreased to

W439.5 billion from W1,117.0 billion as of December 31, 2015, primarily due to the write-off of certain existing loans. As of December 31, 2016, our

exposure to STX Heavy Industries decreased to W268.7 billion from W538.3 billion as of December 31, 2015, primarily due to the write-off of certain existing

loans.

As of December 31, 2016, we

established provisions of W1,049.2 billion for our exposure to DSME, W991.0 billion for STX Offshore & Shipbuilding, W165.9 billion for Dongbu Steel,

W102.9 billion for Hanjin Heavy Industries and Construction, W210.9 billion for Hyundai Merchant Marine, W61.9 billion for Daehan Shipbuilding, W200.2 billion for

Hanjin Shipping and W128.7 billion for STX Heavy Industries.

14

Table of Contents

Companies in the STX Group, a large Korean conglomerate primarily engaged in shipbuilding and trading, have faced financial difficulties for the past several years due to prolonged slowdowns in the Korean construction, shipbuilding and shipping industries. STX Pan Ocean had been in court receivership since June 2013 and was sold to Harim Group in June 2015. STX Construction has been in court receivership since April 2013. STX Offshore & Shipbuilding filed for court receivership in May 2016 and executed debt-to-equity swaps with their creditors, including us, in December 2016 under a rehabilitation plan through which we increased our equity interest to 43.9% and became its largest shareholder. In August 2016, STX Heavy Industries filed for court receivership, and in January 2017, the Seoul Central District Court approved its rehabilitation plan, which includes debt-to-equity swaps. The remaining troubled companies (including STX Corporation and STX Engine) are in voluntary out-of-court debt restructuring programs with their creditors. Companies in the Dongbu Group, a large Korean conglomerate providing industrial, chemical, shipping, insurance and financial products and services, have also been facing financial difficulties for the past several years due to the prolonged slowdown in the Korean construction industry and in the Korean economy in general. Certain troubled companies in the Dongbu Group are in voluntary out-of-court debt restructuring programs with their creditors, and Dongbu Steel entered into a voluntary workout agreement with its creditors in October 2015. We are the main creditor bank of STX Group and Dongbu Group.

In May 2016, Hanjin Shipping, Korea’s largest container operator, submitted itself to joint management with us, as its largest creditor, and other creditors in an effort to revive itself from financial difficulties. In August 2016, we and the other creditors rejected Hanjin Shipping’s last funding plan, and Hanjin Shipping entered into court receivership in September 2016 and was declared bankrupt in February 2017. In July 2016, Hyundai Merchant Marine executed a debt-to-equity swap with us and other creditors, as part of its continued restructuring led by us as its largest creditor, and affiliates of the Hyundai group reduced their shareholdings in Hyundai Merchant Marine, which resulted in us becoming the largest shareholder of Hyundai Merchant Marine with a 14% equity interest.

During 2015, DSME, one of the largest shipbuilding and offshore construction companies in Korea, suffered from financial difficulties

primarily due to significant losses incurred in connection with the construction of offshore plants resulting from a prolonged slowdown in the global shipbuilding industry. In October 2015, we announced that we, along with The Export-Import Bank of

Korea, would extend additional financing of up to W4.2 trillion to DSME by the end of 2016 in the form of debt-to-equity swaps, extension of additional loans and provision of other forms of liquidity support. In this connection, in

December 2015, we acquired W382.9 billion of new equity shares of DSME, which increased our equity interest in DSME from 31.5% to 49.7%, and we became its largest shareholder. In December 2016, we increased our equity interest

in DSME to 79.0% through an additional debt for equity swap. In March 2017, we and The Export-Import Bank of Korea announced a second joint plan pursuant to which, among others, (i) we, along with The Export-Import Bank of Korea, will

provide an additional W2.9 trillion in financial support to DSME, (ii) we will provide additional debt-to-equity swaps of W 0.3 trillion and (iii) The Export-Import Bank of Korea will exchange a term loan

in the amount of W1.28 trillion provided by it to DSME for perpetual bonds to be issued by DSME, which would be contingent on other creditors agreeing to debt-to-equity swaps for up to 80% of their debt with DSME and rescheduling

the maturities of the remainder. In April 2017, the other creditors approved the second joint plan.

In January 2016, the prosecutors’ office of Korea began investigating allegations of mismanagement and accounting irregularities at DSME, including our dealings with and oversight of DSME. Concurrent with the prosecutors’ investigation, in June 2016, the Board of Audit and Inspection, the audit agency of the Government, submitted to financial regulators its reports showing DSME had overstated its operating profit in 2013 and 2014 and criticized us, as the lead creditor bank and largest shareholder of DSME, for alleged mismanagement and loose oversight of DSME, which allegedly led to the failure to uncover the alleged accounting irregularities contributing to further losses at DSME. In December 2016, the prosecutors indicted our former chief executive officer, who had served from 2011 to 2013, for alleged malpractice, bribery and abuse of power. Although we believe our dealings regarding DSME were carried out in compliance with relevant guidelines and procedures, we cannot predict whether the outcome of the investigation by the prosecutors into DSME may be adverse to us.

15

Table of Contents

In addition, further investigations may be launched by other governmental authorities with respect to our dealings with DSME, including those by our other former officers. An adverse determination by the prosecutors or other governmental authorities may result in regulatory sanctions and/or financial penalties as well as reputational harm to us.

In the event that the financial condition of these companies or other large corporations to which we extended credits deteriorate in the future, we may be required to record additional provisions for credit losses, as well as charge-offs and valuation or impairment losses or losses on disposal, which may have a material adverse effect on our financial condition and results of operations.

In 2016, we sold non-performing loans worth W747.5 billion to Cyrus Capital Partners, Eugene Asset Management and UAMCO Ltd.

Loan Operations

We mainly provide equipment capital loans, project loans and working capital loans to private Korean enterprises that undertake major industrial projects either directly or indirectly through on-lending. The loans generally cover over 50%, and in some cases as much as 100%, of the total project cost. Equipment capital loans include loans to major industries for development of high technology and for acquisition, improvement or repair of machinery and equipment. We disburse loan proceeds in installments to ensure that the borrower uses the loan for its intended purpose.

Before approving a loan, we consider:

| • | the economic benefits of the project to the Republic; |

| • | the extent to which the project serves priorities established by the Government’s industrial policy; |

| • | the project’s operational feasibility; |

| • | the loan’s and the project’s profitability; and |

| • | the quality of the borrower’s management. |

We charge, on average, interest of 1.8% over our prime rate, although we provide a discount between 0.2% and 0.7% to small- and medium-sized companies. We adjust the prime rate monthly. The spread depends on the purpose of the loan, maturity date and the borrower’s credit ratings. Certain loans bear interest at below market rates. Equipment capital loans generally have original maturities of three to five years, although we occasionally make equipment capital loans with longer maturities. Working capital loans usually mature within two years.

The Business Planning Department functions as our centralized policy-making and planning division with respect to our lending activities. The Business Planning Department formulates and revises our internal regulations on loan programs as well as setting basic lending guidelines.

We have multiple levels of loan approval authority, depending on the loan amount and other factors such as the availability of collateral or guarantee, debt repayment ability and business prospects. The Credit Review Committee, Division Credit Review Committee, Division Credit Review Sub-Committee, General Manager each has authority to approve loans up to a specified amount. The amount differs depending on the type of loan and certain other factors, for example, whether a loan is collateralized or guaranteed.

Our overall risk management policy is set by the Risk Management Committee. For detailed information regarding our risk management policy and procedures, see “—Financial Statements and Auditors—Notes to Separate Financial Statements of December 31, 2016 and 2015—Note 48.”

16

Table of Contents

The following table sets out, by currency and category of loan, our total outstanding loans:

Loans(1)

| December 31, | ||||||||

| 2015 | 2016 | |||||||

| (billions of won) | ||||||||

| Equipment Capital Loans: |

||||||||

| Domestic Currency |

||||||||

| Foreign Currency(2) |

8,689.5 | 8,307.3 | ||||||

|

|

|

|

|

|||||

| 60,309.8 | 58,723.5 | |||||||

| Working Capital Loans: |

||||||||

| Domestic Currency(3) |

48,760.1 | 47,931.6 | ||||||

| Foreign Currency(2) |

6,290.8 | 6,718.1 | ||||||

|

|

|

|

|

|||||

| 55,050.9 | 54,649.7 | |||||||

| Other Loans(4) |

25,607.6 | 27,948.0 | ||||||

|

|

|

|

|

|||||

| Total Loans |

||||||||

|

|

|

|

|

|||||

| (1) | Includes loans extended to affiliates. |

| (2) | Includes loans disbursed and repayable in Won, the amounts of which are based upon an equivalent amount of foreign currency. This type of loan totaled

|

| (3) | Includes loans on households. |

| (4) | Includes inter-bank loans, private loans, off-shore loan receivables, loans borrowed from overseas financial institutions, bills bought in foreign currencies, advance payments on acceptances and guarantees and other loans. |

As of December 31, 2016, we had W141,321.2 billion in outstanding loans, which represents a 0.3% increase from

W140,968.3 billion of outstanding loans as of December 31, 2015.

Maturities of Outstanding Loans

The following table categorizes our outstanding equipment capital and working capital loans by their remaining maturities:

Outstanding Equipment Capital and Working Capital Loans by Remaining Maturities(1)

| December 31, | As % of December 31, 2016 Total |

|||||||||||

| 2015 | 2016 | |||||||||||

| (billions of won, except percentages) | ||||||||||||

| Loans with Remaining Maturities of One Year or Less |

39.6 | % | ||||||||||

| Loans with Remaining Maturities of More Than One Year |

71,875.9 | 68,457.4 | 60.4 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total |

100.0 | % | ||||||||||

|

|

|

|

|

|

|

|||||||

| (1) | Includes loans extended to affiliates. |

17

Table of Contents

Loans by Industrial Sector

The following table sets out the total amount of our outstanding equipment capital and working capital loans, categorized by industry sector:

Outstanding Equipment Capital and Working Capital Loans by Industry Sector(1)

| December 31, | As % of December 31, 2016 Total |

|||||||||||

| 2015 | 2016 | |||||||||||

| (billions of won, except percentages) | ||||||||||||

| Manufacturing |

48.7 | % | ||||||||||

| Banking and Insurance |

25,132.3 | 24,042.3 | 21.2 | |||||||||

| Transportation |

6,805.6 | 7,130.1 | 6.3 | |||||||||

| Public Administration |

862.2 | 855.5 | 0.8 | |||||||||

| Electric, Gas and Water Supply Industry |

3,227.8 | 3,498.2 | 3.1 | |||||||||

| Others(2) |

23,333.2 | 22,612.4 | 19.9 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total |

100.0 | % | ||||||||||

|

|

|

|

|

|

|

|||||||

| Percentage increase from previous period |

2.9 | % | (1.7 | )% | ||||||||

| (1) | Includes loans extended to affiliates. |

| (2) | Includes wholesale and retail trade, real estate and leasing, and construction. |

The manufacturing sector accounted for 48.7% of our outstanding equipment capital and working capital loans as of December 31, 2016. As of December 31, 2016, loans to the transportation equipment manufacturing businesses and the metal product manufacturing businesses accounted for 18.6% and 13.5%, respectively, of our outstanding equipment capital and working capital loans to the manufacturing sector.

Industrial Bank of Korea was our single largest borrower as of December 31, 2016, accounting for 4.7% of our outstanding equipment capital and working capital loans. As of December 31, 2016, our five largest borrowers and 20 largest borrowers accounted for 11.2% and 24.0%, respectively, of our outstanding equipment capital and working capital loans.

The following table breaks down the equipment capital and working capital loans to our 20 largest borrowers outstanding as of December 31, 2016 by industry sector:

20 Largest Borrowers by Industry Sector

| As % of

December 31, 2016 Total Outstanding Equipment Capital and Working Capital Loans to Our 20 Largest Borrowers |

||||

| Manufacturing |

34.7 | % | ||

| Banking and Insurance |

52.4 | |||

| Transportation |

4.6 | |||

| Public Administration |

2.0 | |||

| Others(1) |

6.3 | |||

|

|

|

|||

| Total |

100.0 | % | ||

|

|

|

|||

| (1) | Includes wholesale and retail trade, real estate and leasing, and construction. |

18

Table of Contents

The following table categorizes the new loans made by us by industry sector:

New Loans by Industry Sector

|

Year Ended December 31, |

As % of Year Ended December 31, 2016 Total |

|||||||||||

| 2015 | 2016 | |||||||||||

| (billions of won, except percentages) | ||||||||||||

| Manufacturing |

60.4 | % | ||||||||||

| Banking and Insurance |

4,301.4 | 3,162.6 | 7.2 | |||||||||

| Transportation |

2,787.2 | 3,130.7 | 7.1 | |||||||||

| Electric, Gas and Water Supply Industry |

1,326.0 | 912.0 | 2.1 | |||||||||

| Others(1) |

12,098.6 | 10,216.4 | 23.2 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total |

100.0 | % | ||||||||||

|

|

|

|

|

|

|

|||||||

| Percentage increase (decrease) from previous period |

6.7 | % | (8.4 | )% | ||||||||

| (1) | Includes wholesale and retail trade, real estate and leasing, and construction. |

Loans by Categories

In addition to dividing our loans into equipment capital and working capital loans, we classify loans into several groupings, the most important being:

| • | industrial fund loans; |

| • | on-lending loans; |

| • | foreign currency loans; |

| • | local currency loans denominated in foreign currencies; |

| • | offshore loans in foreign countries; and |

| • | government fund loans. |

The following table sets out equipment capital and working capital loans by categories as of December 31, 2016:

| Equipment Capital Loans(1) |

Working Capital Loans(1) |

|||||||||||||||

| December 31, 2016 |

% | December 31, 2016 |

% | |||||||||||||

| (billions of won, except percentages) | ||||||||||||||||

| Industrial fund loans |

73.9 | % | 64.2 | % | ||||||||||||

| On-lending loans |

4,359.5 | 7.4 | 9,514.2 | 17.4 | ||||||||||||

| Foreign currency loans |

5,433.7 | 9.3 | 1,201.5 | 2.2 | ||||||||||||

| Local currency loans denominated in foreign currencies |

73.3 | 0.1 | 70.0 | 0.1 | ||||||||||||

| Offshore loans in foreign currencies |

1,180.2 | 2.0 | 3,715.7 | 6.8 | ||||||||||||

| Government fund loans |

320.2 | 0.5 | — | — | ||||||||||||

| Overdraft |

— | — | 165.2 | 0.3 | ||||||||||||

| Others(1) |

3,938.5 | 6.8 | 4,921.5 | 9.0 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

100.0 | % | 100.0 | % | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| (1) | Includes loans on households and loans extended to affiliates. |

19

Table of Contents

Industrial Fund Loans. Industrial fund loans are equipment capital and working capital loans denominated in Won to borrowers in major industries to finance equipment and facilities.

We currently make equipment capital industrial fund loans at floating or fixed rates for terms of up to 10 years and for up to 100% of the equipment cost being financed. We make working capital industrial fund loans at floating or fixed rates and in amounts constituting up to 40% of the borrower’s estimated annual sales.

On-lending Loans. On-lending is a form of indirect financing that involves intermediary financial institutions which on-lend the funds provided by us to industrial borrowers and are responsible for repayment to us. Most of the funds provided by us through on-lending are ultimately lent to small- and medium-sized enterprises for their equipment purchases and working capital. We explicitly set detailed guidelines (including scope of borrowers, maturity and interest rates) for intermediary financial institutions to be followed when on-lending to the ultimate borrowers. We monitor our exposure to, and the credit standing of, each financial institution to which we lend. Borrowers do not apply directly to us and may only apply for our on-lending loans through their regular bank or another bank of their choice. The intermediary bank appraises the financial and business situation of the applicant and generally assumes liability for repayment to us. Although the processing of individual loans requires two formally separate loan approvals for each borrower, first by the intermediary bank and then by us, the ultimate borrower need only apply to the intermediary bank for approval.

Foreign Currency Loans. We extend loans denominated in U.S. dollars, Japanese yen or other foreign currencies principally to finance the purchase of industrial equipment from abroad or the implementation of overseas industrial development projects by Korean companies. We make these loans at floating interest rates with original maturities, in the case of equipment capital foreign currency loans, of up to 10 years and, in the case of working capital foreign currency loans, of up to three years.

Local Currency Loans Denominated in Foreign Currencies. We make local currency loans denominated in foreign currencies for the same purposes, and to the same borrowers, as foreign currency loans. Although we denominate the loans in foreign currency, the borrower receives and repays the loans in Won based on foreign exchange rates at the time of receipt and repayment. We currently make loans of this type at floating interest rates, with original maturities, in the case of equipment capital loans, of up to 10 years and, in the case of working capital loans, of up to three years.

Offshore Loans in Foreign Currencies. We extend offshore loans in foreign currencies to finance:

| • | the purchase of industrial equipment and the implementation of overseas industrial projects by overseas subsidiaries and branches of Korean companies; and |

| • | the overseas industrial development projects of foreign government entities, international organizations and foreign companies. |

We make these loans at floating interest rates with original maturities, in the form of equipment capital foreign currency loans, of up to 10 years and, working capital foreign currency loans, of up to three years.

Government Fund Loans. We make government fund loans primarily to finance:

| • | water supply and drainage facilities; |

| • | the Seoul subway system; |

| • | freight terminal facilities; |

| • | hospitals; and |

| • | other facilities. |

Government fund loans that are equipment capital loans require approval by the appropriate Government ministry. We currently make government fund loans in Won at floating interest rates with original maturities of 10 to 20 years.

20

Table of Contents

Other Loans. We also make special purpose fund loans for particular industries or projects using funds lent to us by the Government and foreign financial institutions. The Government funds that finance these loans include, among others:

| • | the Tourism Promotion Fund (hotel and resort projects); |

| • | the Rational Use of Energy Fund (energy conservation projects and collective energy supply projects); and |

| • | the Small- and Medium-sized Enterprises Promotion Fund (small- and medium-sized enterprises). |

For further information relating to such loans, see “—Sources of Funds.”

Guarantee Operations

We extend guarantees to our clients to facilitate their other borrowings and to finance major industrial projects. We guarantee Won-denominated corporate debentures, local currency loans, and other Won liabilities and foreign currency loans from domestic and overseas Korean financial institutions and from foreign institutions. The KDB Act and our Articles of Incorporation limit the aggregate amount of our industrial finance bond obligations and guarantee obligations. See “—Sources of Funds.”

We generally obtain collateral valued in excess of the original guarantee. We appraise the value of our collateral at least once a year. Depending on the borrower, the collateral may be industrial plants, real estate and/or marketable securities.

The following table shows our outstanding guarantees:

Guarantees Outstanding

| As of December 31, | ||||||||

| 2015 | 2016 | |||||||

| (billions of won) | ||||||||

| Acceptances |

||||||||

| Guarantees on local borrowing |

1,057.0 | 812.8 | ||||||

| Guarantees on foreign borrowing |

8,099.8 | 8,584.6 | ||||||

| Letter of guarantee for importers |

32.7 | 46.6 | ||||||

|

|

|

|

|

|||||

| Total |

||||||||

|

|

|

|

|

|||||

Investments

We invest in a range of Korean private

and Government-owned enterprises but we will not take a controlling interest in a company unless the acquisition is necessary for the corporate restructuring of the company. Although generally a long-term investor, we sell investments from time to

time. In recent years, sales resulted principally from the Government’s privatization program, and we expect to continue such sales in the future. The Government plans to sell its direct or indirect interest in certain private sector companies

acquired during previous restructuring programs, including Daewoo Engineering & Construction Co., Ltd., depending on market conditions. In accordance with such plan, we expect to sell our equity holdings in certain private sector companies

if favorable opportunities for sale arise. Our equity investments decreased to W32,602.2 billion as of December 31, 2016 from W35,696.8 billion as of December 31, 2015.

The KDB Act and our Articles of Incorporation provide that the cost basis of our total equity investments may not exceed twice the sum of our paid-in capital and our reserve from profit. In addition, pursuant to the KDB Decree, we may not acquire equity securities of a single company in excess of 15% of its entire voting shares. The 15% limit, however, does not apply to certain investments, including those in Government-controlled

21

Table of Contents

companies financed by capital contributions from the Government. As of December 31, 2016, the cost basis of our equity investments subject to restriction under the KDB Act and our Articles

of Incorporation totaled W11,583.1 billion, equal to 25.7% of our equity investment ceiling. For a discussion of Korean accounting principles relating to our equity investments, see “—Financial Statements and the

Auditors.”

The following table sets out our equity investments by industry sector on a book value basis as of December 31, 2016:

Equity Investments

| Book Value as of December 31, 2016 |

||||

| (billions of won) | ||||

| Electric, Gas and Water Supply Industry |

||||

| Construction |

1,005.1 | |||

| Banking and Insurance |

8,183.5 | |||

| Real Estate Business |

2,599.1 | |||

| Manufacturing |

749.3 | |||

| Transportation |

1,404.1 | |||

| Others |

613.3 | |||

|

|

|

|||

| Total |

||||

|

|

|

|||

As of December 31, 2016,

we held total equity investments, on a book value basis, of W577.8 billion in one of our five largest borrowers and W1,239.4 billion in four of our 20 largest borrowers. We have not established a policy

addressing loans to enterprises in which we hold equity interests or equity interests in enterprises to which we have extended loans.

When possible, we use the prevailing market price of a security to determine the value of our interest. However, if no readily ascertainable market value exists for our holdings, we record these investments at the cost of acquisition. With respect to our equity interests in enterprises in which we hold more than 15% of interest, we value these investments annually, with certain exceptions, on a net asset value basis when the investee company releases its financial statements. As of December 31, 2016, the aggregate value of our equity investments accounted for approximately 101.3% of their aggregate cost basis.

As part of our investment activities, we underwrite straight and convertible bond issuances in Won for domestic corporations. We also invest in municipal bonds, extending funds to municipalities at subsidized interest rates, mostly to finance water supply and drainage infrastructure projects.

Other Activities

We engage in a range of industrial development activities in addition to providing loans and guarantees, including:

| • | conducting economic and industrial research; |

| • | performing engineering surveys; |

| • | providing business analyzes and managerial assistance; and |

| • | offering trust services. |

As of December 31, 2016, we held in trust cash and other assets totaling W36,058.0 billion, and we generated in

2016 trust fee income equaling W133.8 billion. As of December 31, 2015, we held in trust cash and

22

Table of Contents

other assets totaling W32,630.9 billion, and we generated in 2015 trust fee income equaling W184.0 billion. Pursuant to Korean law, we segregate trust

assets from our other assets; trust assets are not available to satisfy claims of our depositors or other creditors. Accordingly, we account for our trust accounts separately from our banking accounts. However, if our trust operations fail to

preserve the principal of our clients’ trust assets, we are responsible for covering the deficit either from previously established provisions in our trust accounts or by a transfer from our banking accounts. In 2015 and 2016, we did not