| UNITED STATES | ||

| SECURITIES AND EXCHANGE COMMISSION | ||

| Washington, D.C. 20549 | ||

FORM | ||

| (Mark One) | ||||||||||||||||||||||||||||||||||||||

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||||||||||||||||||||||||||||||||

| For the quarterly period ended | ||||||||||||||||||||||||||||||||||||||

| or | ||||||||||||||||||||||||||||||||||||||

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||||||||||||||||||||||||||||||||

| For the transition period from | to | |||||||||||||||||||||||||||||||||||||

| Commission File No. | Exact Name of Registrant as Specified in its Charter, Address of Principal Executive Office and Telephone Number | State of Incorporation | I.R.S. Employer Identification No. | Former name, former address and former fiscal year, if changed since last report | |||||||||||||

| No change | ||||||||||||||||

| No change | ||||||||||||||||

| No change | ||||||||||||||||

| SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT: | ||||||||

| Title of Each Class | Trading Symbol | Name of Each Exchange on Which Registered | ||||||

| SEMPRA: | ||||||||

| SAN DIEGO GAS & ELECTRIC COMPANY: | ||||||||

| None | ||||||||

| SOUTHERN CALIFORNIA GAS COMPANY: | ||||||||

| None | ||||||||

(1) Sempra’s common shares are also registered with the National Securities Registry of the CNBV in Mexico. The registration of Sempra’s common shares with the National Securities Registry does not imply certification regarding the investment quality of the securities, the solvency of the issuer or the accuracy or completeness of the information included in the quarterly report, nor does it confirm acts that may have been performed in contravention of the law. This quarterly report has been filed in Mexico in accordance with the general provisions applicable to issuers and other securities market participants.

Indicate by check mark whether the Registrants (1) have filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrants were required to file such reports), and (2) have been subject to such filing requirements for the past 90 days. | ||||||||||||||

| ☒ | No | ☐ | ||||||||||||

Indicate by check mark whether the Registrants have submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the Registrants were required to submit such files). | ||||||||||||||

| ☒ | No | ☐ | ||||||||||||

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. | ||||||||||||||

| Sempra: | ||||||||||||||

☒ | ☐ Accelerated Filer | ☐ Non-accelerated Filer | ||||||||||||

| San Diego Gas & Electric Company: | ||||||||||||||

☐ Large Accelerated Filer | ☐ Accelerated Filer | ☒ | ||||||||||||

| Southern California Gas Company: | ||||||||||||||

☐ Large Accelerated Filer | ☐ Accelerated Filer | ☒ | ||||||||||||

| If an emerging growth company, indicate by check mark if the Registrants have elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. | ||||||||||||||

☐ | ||||||||||||||

| Indicate by check mark whether the Registrants are a shell company (as defined in Rule 12b-2 of the Exchange Act). | ||||||||||||||

Yes | No | ☒ | ||||||||||||

| Indicate the number of shares outstanding of each of the issuers’ classes of common stock, as of the latest practicable date. | ||||||||||||||

Common stock outstanding as of April 30, 2024: | ||||||||||||||

| Sempra | ||||||||

| San Diego Gas & Electric Company | Wholly owned by Enova Corporation, which is wholly owned by Sempra | |||||||

| Southern California Gas Company | Wholly owned by Pacific Enterprises, which is wholly owned by Sempra | |||||||

2

| TABLE OF CONTENTS | ||||||||

| Page | ||||||||

| PART I – FINANCIAL INFORMATION | ||||||||

| Item 1. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| PART II – OTHER INFORMATION | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

This combined Form 10-Q is separately filed by Sempra, San Diego Gas & Electric Company and Southern California Gas Company. Information contained herein relating to any one of these individual Registrants is filed by such entity on its own behalf. Each such Registrant makes statements herein only as to itself and its consolidated entities and makes no statement whatsoever as to any other entity.

You should read this report in its entirety as it pertains to each respective Registrant. No one section of the report deals with all aspects of the subject matter. A separate Part I – Item 1 is provided for each Registrant, except for the Notes to Condensed Consolidated Financial Statements, which are combined for all the Registrants. All Items other than Part I – Item 1 are combined for the three Registrants.

None of the website references in this report are active hyperlinks, and the information contained on or that can be accessed through any such website is not and shall not be deemed to be part of or incorporated by reference in this report or any other document that we file with or furnish to the SEC.

3

The following terms and abbreviations appearing in this report have the meanings indicated below.

| GLOSSARY | |||||

| AB | California Assembly Bill | ||||

| ADIA | Black Silverback ZC 2022 LP (assignee of Black River B 2017 Inc.), a wholly owned affiliate of Abu Dhabi Investment Authority | ||||

| AFUDC | allowance for funds used during construction | ||||

| amparo | an extraordinary constitutional appeal governed by Articles 103 and 107 of the Mexican Constitution and filed in Mexican federal court | ||||

| Annual Report | Annual Report on Form 10-K for the year ended December 31, 2023 | ||||

| AOCI | accumulated other comprehensive income (loss) | ||||

| ASEA | Agencia de Seguridad, Energía y Ambiente (Mexico’s National Agency for Industrial Safety and Environmental Protection) | ||||

| ASU | Accounting Standards Update | ||||

| Bcf | billion cubic feet | ||||

| bps | basis points | ||||

| Cameron LNG JV | Cameron LNG Holdings, LLC | ||||

| Cameron LNG Phase 1 facility | Cameron LNG JV liquefaction facility | ||||

| Cameron LNG Phase 2 project | Cameron LNG JV liquefaction expansion project | ||||

| CCA | Community Choice Aggregation | ||||

| CCM | cost of capital adjustment mechanism | ||||

| CFE | Comisión Federal de Electricidad (Mexico’s Federal Electricity Commission) | ||||

| CFIN | Cameron LNG FINCO, LLC, a wholly owned and unconsolidated affiliate of Cameron LNG JV | ||||

| CNBV | Comisión Nacional Bancaria y de Valores (Mexico’s National Banking and Securities Commission) | ||||

| CODM | chief operating decision maker as defined in Accounting Standards Codification 280 | ||||

| ConocoPhillips | ConocoPhillips Company | ||||

| CPUC | California Public Utilities Commission | ||||

| CRE | Comisión Reguladora de Energía (Mexico’s Energy Regulatory Commission) | ||||

| CRR | congestion revenue right | ||||

| DOE | U.S. Department of Energy | ||||

| ECA LNG | ECA LNG Phase 1 and ECA LNG Phase 2, collectively | ||||

| ECA LNG Phase 1 | ECA LNG Holdings B.V. | ||||

| ECA LNG Phase 2 | ECA LNG II Holdings B.V. | ||||

| ECA Regas Facility | Energía Costa Azul, S. de R.L. de C.V. LNG regasification facility | ||||

| Ecogas | Ecogas México, S. de R.L. de C.V. | ||||

| Edison | Southern California Edison Company, a subsidiary of Edison International | ||||

| EFH | Energy Future Holdings Corp. (renamed Sempra Texas Holdings Corp.) | ||||

| EPC | engineering, procurement and construction | ||||

| EPS | earnings per common share | ||||

| ETR | effective income tax rate | ||||

| Exchange Act | Securities Exchange Act of 1934, as amended | ||||

| FERC | Federal Energy Regulatory Commission | ||||

| Fitch | Fitch Ratings, Inc. | ||||

| FTA | Free Trade Agreement | ||||

| GCIM | Gas Cost Incentive Mechanism | ||||

| GHG | greenhouse gas | ||||

| GRC | General Rate Case | ||||

| HOA | Heads of Agreement | ||||

| IEnova | Infraestructura Energética Nova, S.A.P.I. de C.V. | ||||

| IMG | Infraestructura Marina del Golfo | ||||

| INEOS | INEOS Energy Trading Limited, a subsidiary of INEOS Limited | ||||

| IOU | investor-owned utility | ||||

| IRA | Inflation Reduction Act of 2022 | ||||

| IRS | U.S. Internal Revenue Service | ||||

4

| GLOSSARY (CONTINUED) | |||||

| ISO | Independent System Operator | ||||

| ITC | investment tax credit | ||||

| JV | joint venture | ||||

| KKR Denali | KKR Denali Holdco LLC, an affiliate of Kohlberg Kravis Roberts & Co. L.P. | ||||

| KKR Pinnacle | KKR Pinnacle Investor L.P. (as successor-in-interest to KKR Pinnacle Aggregator L.P.), an affiliate of Kohlberg Kravis Roberts & Co. L.P. | ||||

| Leak | the leak at the SoCalGas Aliso Canyon natural gas storage facility injection-and-withdrawal well, SS25, discovered by SoCalGas on October 23, 2015 | ||||

| LNG | liquefied natural gas | ||||

| MD&A | Management’s Discussion and Analysis of Financial Condition and Results of Operations | ||||

| MMBtu | million British thermal units (of natural gas) | ||||

| Moody’s | Moody’s Investors Service, Inc. | ||||

| MOU | Memorandum of Understanding | ||||

| Mtpa | million tonnes per annum | ||||

| MW | megawatt | ||||

| MWh | megawatt hour | ||||

| NCI | noncontrolling interest(s) | ||||

| NDT | nuclear decommissioning trusts | ||||

| NEIL | Nuclear Electric Insurance Limited | ||||

| O&M | operation and maintenance expense | ||||

| OCI | other comprehensive income (loss) | ||||

| OII | Order Instituting Investigation | ||||

| Oncor | Oncor Electric Delivery Company LLC | ||||

| Oncor Holdings | Oncor Electric Delivery Holdings Company LLC | ||||

| ORLEN | Polski Koncern Naftowy Orlen S.A. | ||||

| Other Sempra | All Sempra consolidated entities, except for SDG&E and SoCalGas | ||||

| PA LNG Phase 1 project | initial phase of the Port Arthur LNG liquefaction project | ||||

| PA LNG Phase 2 project | second phase of the Port Arthur LNG liquefaction project | ||||

| PBOP | postretirement benefits other than pension | ||||

| Port Arthur LNG | Port Arthur LNG, LLC, an indirect subsidiary of SI Partners that owns the PA LNG Phase 1 project | ||||

| PP&E | property, plant and equipment | ||||

| PPA | power purchase agreement | ||||

| PUCT | Public Utility Commission of Texas | ||||

| RBS Sempra Commodities | RBS Sempra Commodities LLP | ||||

| Registrants | has the meaning set forth in Rule 12b-2 under the Exchange Act and consists of Sempra, SDG&E and SoCalGas for purposes of this report | ||||

| ROE | return on equity | ||||

| RSU | restricted stock unit | ||||

| S&P | S&P Global Ratings, a division of S&P Global Inc. | ||||

| SB | California Senate Bill | ||||

| SDG&E | San Diego Gas & Electric Company | ||||

| SDSRA | Senior Debt Service Reserve Account | ||||

| SEC | U.S. Securities and Exchange Commission | ||||

| SEDATU | Secretaría de Desarrollo Agrario, Territorial y Urbano (Mexico’s agency in charge of agriculture, land and urban development) | ||||

| SENER | Secretaría de Energía de México (Mexico’s Ministry of Energy) | ||||

| series A preferred stock | Sempra’s 6% mandatory convertible preferred stock, series A | ||||

| series B preferred stock | Sempra’s 6.75% mandatory convertible preferred stock, series B | ||||

| series C preferred stock | Sempra’s 4.875% fixed-rate reset cumulative redeemable perpetual preferred stock, series C | ||||

| SI Partners | Sempra Infrastructure Partners, LP, the holding company for most of Sempra’s subsidiaries not subject to California or Texas utility regulation | ||||

| SoCalGas | Southern California Gas Company | ||||

| SOFR | Secured Overnight Financing Rate | ||||

5

| GLOSSARY (CONTINUED) | |||||

| SONGS | San Onofre Nuclear Generating Station | ||||

| SPA | sale and purchase agreement | ||||

| Support Agreement | support agreement, dated July 28, 2020 and amended on June 29, 2021, among Sempra and Sumitomo Mitsui Banking Corporation | ||||

| TAG Norte | TAG Norte Holding, S. de R.L. de C.V. | ||||

| TAG Pipelines | TAG Pipelines Norte, S. de R.L. de C.V. | ||||

| TCEQ | Texas Commission on Environmental Quality | ||||

| TdM | Termoeléctrica de Mexicali | ||||

| TO5 | Electric Transmission Owner Formula Rate, effective June 1, 2019 | ||||

| U.S. GAAP | generally accepted accounting principles in the United States of America | ||||

| VIE | variable interest entity | ||||

| Wildfire Fund | the fund established pursuant to AB 1054 | ||||

| Wildfire Legislation | AB 1054 and AB 111 | ||||

In this report, references to “Sempra” are to Sempra and its consolidated entities, collectively, and references to “we,” “our,” “us” and “our company” are to the applicable Registrant and its consolidated entities, collectively, in each case unless otherwise stated or indicated by the context. All references in this report to our reportable segments are not intended to refer to any legal entity with the same or similar name.

Throughout this report, we refer to the following as Condensed Consolidated Financial Statements and Notes to Condensed Consolidated Financial Statements when discussed together or collectively:

▪the Condensed Consolidated Financial Statements and related Notes of Sempra;

▪the Condensed Financial Statements and related Notes of SDG&E; and

▪the Condensed Financial Statements and related Notes of SoCalGas.

6

INFORMATION REGARDING FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements are based on assumptions about the future, involve risks and uncertainties, and are not guarantees. Future results may differ materially from those expressed or implied in any forward-looking statement. These forward-looking statements represent our estimates and assumptions only as of the filing date of this report. We assume no obligation to update or revise any forward-looking statement as a result of new information, future events or otherwise.

Forward-looking statements can be identified by words such as “believe,” “expect,” “intend,” “anticipate,” “contemplate,” “plan,” “estimate,” “project,” “forecast,” “envision,” “should,” “could,” “would,” “will,” “confident,” “may,” “can,” “potential,” “possible,” “proposed,” “in process,” “construct,” “develop,” “opportunity,” “preliminary,” “initiative,” “target,” “outlook,” “optimistic,” “poised,” “positioned,” “maintain,” “continue,” “progress,” “advance,” “goal,” “aim,” “commit,” or similar expressions, or when we discuss our guidance, priorities, strategy, goals, vision, mission, opportunities, projections, intentions or expectations.

Factors, among others, that could cause actual results and events to differ materially from those expressed or implied in any forward-looking statement include:

▪California wildfires, including potential liability for damages regardless of fault and any inability to recover all or a substantial portion of costs from insurance, the Wildfire Fund, rates from customers or a combination thereof

▪decisions, investigations, inquiries, regulations, denials or revocations of permits, consents, approvals or other authorizations, renewals of franchises, and other actions, including the failure to honor contracts and commitments, by the (i) CPUC, CRE, DOE, FERC, PUCT, IRS and other regulatory bodies and (ii) U.S., Mexico and states, counties, cities and other jurisdictions therein and in other countries where we do business

▪the success of business development efforts, construction projects, acquisitions, divestitures, and other significant transactions, including risks related to (i) being able to make a final investment decision, (ii) completing construction projects or other transactions on schedule and budget, (iii) realizing anticipated benefits from any of these efforts if completed, (iv) obtaining third-party consents and approvals and (v) third parties honoring their contracts and commitments

▪macroeconomic trends or other factors that could change our capital expenditure plans and their potential impact on rate base or other growth

▪litigation, arbitrations, property disputes and other proceedings, and changes to laws and regulations, including those related to tax and trade policy and the energy industry in Mexico

▪cybersecurity threats, including by state and state-sponsored actors, of ransomware or other attacks on our systems or the systems of third parties with which we conduct business, including the energy grid or other energy infrastructure

▪the availability, uses, sufficiency, and cost of capital resources and our ability to borrow money or otherwise raise capital on favorable terms and meet our obligations, including due to (i) actions by credit rating agencies to downgrade our credit ratings or place those ratings on negative outlook, (ii) instability in the capital markets, or (iii) rising interest rates and inflation

▪the impact on affordability of SDG&E’s and SoCalGas’ customer rates and their cost of capital and on SDG&E’s, SoCalGas’ and Sempra Infrastructure’s ability to pass through higher costs to customers due to (i) volatility in inflation, interest rates and commodity prices, (ii) with respect to SDG&E’s and SoCalGas’ businesses, the cost of meeting the demand for lower carbon and reliable energy in California, and (iii) with respect to Sempra Infrastructure’s business, volatility in foreign currency exchange rates

▪the impact of climate and sustainability policies, laws, rules, regulations, trends and required disclosures, including actions to reduce or eliminate reliance on natural gas, increased uncertainty in the political or regulatory environment for California natural gas distribution companies, the risk of nonrecovery for stranded assets, and uncertainty related to emerging technologies

▪weather, natural disasters, pandemics, accidents, equipment failures, explosions, terrorism, information system outages or other events, such as work stoppages, that disrupt our operations, damage our facilities or systems, cause the release of harmful materials or fires or subject us to liability for damages, fines and penalties, some of which may not be recoverable through regulatory mechanisms or insurance or may impact our ability to obtain satisfactory levels of affordable insurance

▪the availability of electric power, natural gas and natural gas storage capacity, including disruptions caused by failures in the transmission grid, pipeline system or limitations on the withdrawal of natural gas from storage facilities

▪Oncor’s ability to reduce or eliminate its quarterly dividends due to regulatory and governance requirements and commitments, including by actions of Oncor’s independent directors or a minority member director

▪other uncertainties, some of which are difficult to predict and beyond our control

7

We caution you not to rely unduly on any forward-looking statements. You should review and carefully consider the risks, uncertainties and other factors that affect our businesses as described herein, in our Annual Report and in other reports we file with the SEC.

8

PART I – FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

| SEMPRA | |||||||||||

| CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS | |||||||||||

| (Dollars in millions, except per share amounts; shares in thousands) | |||||||||||

| Three months ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| (unaudited) | |||||||||||

| REVENUES | |||||||||||

Utilities: | |||||||||||

Natural gas | $ | $ | |||||||||

Electric | |||||||||||

| Energy-related businesses | |||||||||||

| Total revenues | |||||||||||

| EXPENSES AND OTHER INCOME | |||||||||||

| Utilities: | |||||||||||

| Cost of natural gas | ( | ( | |||||||||

| Cost of electric fuel and purchased power | ( | ( | |||||||||

| Energy-related businesses cost of sales | ( | ( | |||||||||

| Operation and maintenance | ( | ( | |||||||||

| Depreciation and amortization | ( | ( | |||||||||

| Franchise fees and other taxes | ( | ( | |||||||||

Other income, net | |||||||||||

| Interest income | |||||||||||

| Interest expense | ( | ( | |||||||||

| Income before income taxes and equity earnings | |||||||||||

Income tax expense | ( | ( | |||||||||

| Equity earnings | |||||||||||

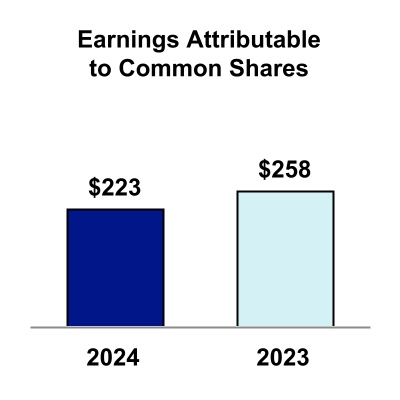

Net income | |||||||||||

Earnings attributable to noncontrolling interests | ( | ( | |||||||||

| Preferred dividends | ( | ( | |||||||||

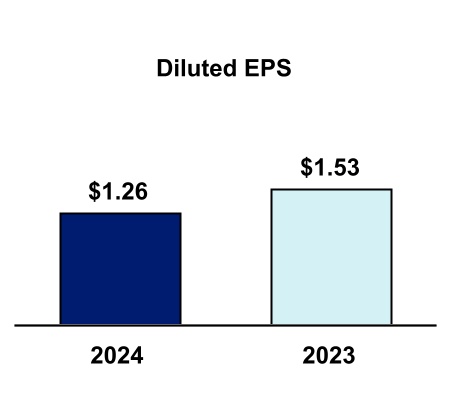

Earnings attributable to common shares | $ | $ | |||||||||

| Basic EPS: | |||||||||||

Earnings | $ | $ | |||||||||

| Weighted-average common shares outstanding | |||||||||||

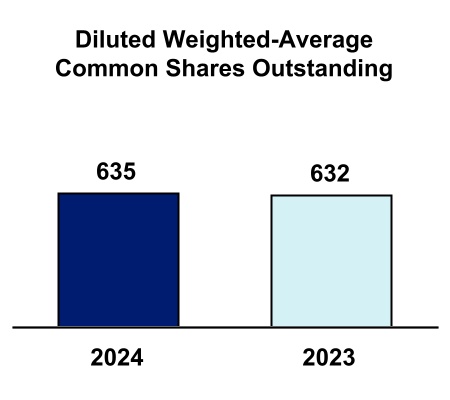

| Diluted EPS: | |||||||||||

Earnings | $ | $ | |||||||||

| Weighted-average common shares outstanding | |||||||||||

See Notes to Condensed Consolidated Financial Statements.

9

| SEMPRA | |||||||||||||||||||||||||||||

| CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS) | |||||||||||||||||||||||||||||

| (Dollars in millions) | |||||||||||||||||||||||||||||

| Sempra shareholders’ equity | |||||||||||||||||||||||||||||

| Pretax amount | Income tax (expense) benefit | Net-of-tax amount | Noncontrolling interests (after tax) | Total | |||||||||||||||||||||||||

| (unaudited) | |||||||||||||||||||||||||||||

| Three months ended March 31, 2024 and 2023 | |||||||||||||||||||||||||||||

| 2024: | |||||||||||||||||||||||||||||

| Net income | $ | $ | ( | $ | $ | $ | |||||||||||||||||||||||

| Other comprehensive income (loss): | |||||||||||||||||||||||||||||

| Foreign currency translation adjustments | |||||||||||||||||||||||||||||

| Financial instruments | ( | ||||||||||||||||||||||||||||

| Pension and other postretirement benefits | ( | ||||||||||||||||||||||||||||

| Total other comprehensive income | ( | ||||||||||||||||||||||||||||

| Comprehensive income | $ | $ | ( | $ | $ | $ | |||||||||||||||||||||||

| 2023: | |||||||||||||||||||||||||||||

| Net income | $ | $ | ( | $ | $ | $ | |||||||||||||||||||||||

| Other comprehensive income (loss): | |||||||||||||||||||||||||||||

| Foreign currency translation adjustments | |||||||||||||||||||||||||||||

| Financial instruments | ( | ( | ( | ( | |||||||||||||||||||||||||

| Pension and other postretirement benefits | ( | ( | ( | ||||||||||||||||||||||||||

| Total other comprehensive loss | ( | ( | ( | ( | |||||||||||||||||||||||||

| Comprehensive income | $ | $ | ( | $ | $ | $ | |||||||||||||||||||||||

See Notes to Condensed Consolidated Financial Statements.

10

| SEMPRA | |||||||||||

| CONDENSED CONSOLIDATED BALANCE SHEETS | |||||||||||

| (Dollars in millions) | |||||||||||

| March 31, | December 31, | ||||||||||

| 2024 | 2023(1) | ||||||||||

| (unaudited) | |||||||||||

| ASSETS | |||||||||||

| Current assets: | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Restricted cash | |||||||||||

| Accounts receivable – trade, net | |||||||||||

| Accounts receivable – other, net | |||||||||||

| Due from unconsolidated affiliates | |||||||||||

| Income taxes receivable | |||||||||||

| Inventories | |||||||||||

| Prepaid expenses | |||||||||||

| Regulatory assets | |||||||||||

| Fixed-price contracts and other derivatives | |||||||||||

| Greenhouse gas allowances | |||||||||||

| Other current assets | |||||||||||

| Total current assets | |||||||||||

| Other assets: | |||||||||||

| Restricted cash | |||||||||||

| Regulatory assets | |||||||||||

| Greenhouse gas allowances | |||||||||||

| Nuclear decommissioning trusts | |||||||||||

| Dedicated assets in support of certain benefit plans | |||||||||||

| Deferred income taxes | |||||||||||

| Right-of-use assets – operating leases | |||||||||||

| Investment in Oncor Holdings | |||||||||||

| Other investments | |||||||||||

| Goodwill | |||||||||||

| Other intangible assets | |||||||||||

| Wildfire fund | |||||||||||

| Other long-term assets | |||||||||||

| Total other assets | |||||||||||

| Property, plant and equipment: | |||||||||||

| Property, plant and equipment | |||||||||||

| Less accumulated depreciation and amortization | ( | ( | |||||||||

| Property, plant and equipment, net | |||||||||||

| Total assets | $ | $ | |||||||||

(1) Derived from audited financial statements.

See Notes to Condensed Consolidated Financial Statements.

11

| SEMPRA | |||||||||||

| CONDENSED CONSOLIDATED BALANCE SHEETS (CONTINUED) | |||||||||||

| (Dollars in millions) | |||||||||||

| March 31, | December 31, | ||||||||||

| 2024 | 2023(1) | ||||||||||

| (unaudited) | |||||||||||

| LIABILITIES AND EQUITY | |||||||||||

| Current liabilities: | |||||||||||

| Short-term debt | $ | $ | |||||||||

| Accounts payable – trade | |||||||||||

| Accounts payable – other | |||||||||||

| Due to unconsolidated affiliates | |||||||||||

| Dividends and interest payable | |||||||||||

| Accrued compensation and benefits | |||||||||||

| Regulatory liabilities | |||||||||||

| Current portion of long-term debt and finance leases | |||||||||||

| Greenhouse gas obligations | |||||||||||

| Other current liabilities | |||||||||||

| Total current liabilities | |||||||||||

| Long-term debt and finance leases | |||||||||||

| Deferred credits and other liabilities: | |||||||||||

| Due to unconsolidated affiliates | |||||||||||

| Regulatory liabilities | |||||||||||

| Greenhouse gas obligations | |||||||||||

| Pension and other postretirement benefit plan obligations, net of plan assets | |||||||||||

| Deferred income taxes | |||||||||||

| Asset retirement obligations | |||||||||||

| Deferred credits and other | |||||||||||

| Total deferred credits and other liabilities | |||||||||||

| Commitments and contingencies (Note 11) | |||||||||||

| Equity: | |||||||||||

Preferred stock ( | |||||||||||

Preferred stock, series C ( | |||||||||||

Common stock ( outstanding at March 31, 2024 and December 31, 2023, respectively; no par value) | |||||||||||

| Retained earnings | |||||||||||

| Accumulated other comprehensive income (loss) | ( | ( | |||||||||

| Total Sempra shareholders’ equity | |||||||||||

| Preferred stock of subsidiary | |||||||||||

| Other noncontrolling interests | |||||||||||

| Total equity | |||||||||||

| Total liabilities and equity | $ | $ | |||||||||

(1) Derived from audited financial statements.

See Notes to Condensed Consolidated Financial Statements.

12

| SEMPRA | |||||||||||

| CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS | |||||||||||

| (Dollars in millions) | |||||||||||

| Three months ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| (unaudited) | |||||||||||

| CASH FLOWS FROM OPERATING ACTIVITIES | |||||||||||

| Net income | $ | $ | |||||||||

| Adjustments to reconcile net income to net cash provided by operating activities: | |||||||||||

| Depreciation and amortization | |||||||||||

| Deferred income taxes and investment tax credits | |||||||||||

| Equity earnings | ( | ( | |||||||||

| Share-based compensation expense | |||||||||||

| Fixed-price contracts and other derivatives | ( | ||||||||||

| Bad debt expense | |||||||||||

| Other | |||||||||||

| Net change in working capital components | |||||||||||

| Distributions from investments | |||||||||||

| Changes in other noncurrent assets and liabilities, net | ( | ( | |||||||||

| Net cash provided by operating activities | |||||||||||

| CASH FLOWS FROM INVESTING ACTIVITIES | |||||||||||

| Expenditures for property, plant and equipment | ( | ( | |||||||||

| Expenditures for investments | ( | ( | |||||||||

| Purchases of nuclear decommissioning and other trust assets | ( | ( | |||||||||

| Proceeds from sales of nuclear decommissioning and other trust assets | |||||||||||

| Other | ( | ||||||||||

| Net cash used in investing activities | ( | ( | |||||||||

| CASH FLOWS FROM FINANCING ACTIVITIES | |||||||||||

| Common dividends paid | ( | ( | |||||||||

| Issuances of common stock | |||||||||||

| Repurchases of common stock | ( | ( | |||||||||

| Issuances of debt (maturities greater than 90 days) | |||||||||||

| Payments on debt (maturities greater than 90 days) and finance leases | ( | ( | |||||||||

| (Decrease) increase in short-term debt, net | ( | ||||||||||

| Advances from unconsolidated affiliates | |||||||||||

| Proceeds from sale of noncontrolling interests | |||||||||||

| Distributions to noncontrolling interests | ( | ( | |||||||||

| Contributions from noncontrolling interests | |||||||||||

| Settlement of cross-currency swaps | ( | ||||||||||

| Other | ( | ( | |||||||||

| Net cash provided by financing activities | |||||||||||

| Effect of exchange rate changes on cash, cash equivalents and restricted cash | |||||||||||

| Increase in cash, cash equivalents and restricted cash | |||||||||||

| Cash, cash equivalents and restricted cash, January 1 | |||||||||||

| Cash, cash equivalents and restricted cash, March 31 | $ | $ | |||||||||

See Notes to Condensed Consolidated Financial Statements.

13

| SEMPRA | |||||||||||

| CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (CONTINUED) | |||||||||||

| (Dollars in millions) | |||||||||||

| Three months ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| (unaudited) | |||||||||||

| SUPPLEMENTAL DISCLOSURE OF CASH FLOW INFORMATION | |||||||||||

| Interest payments, net of amounts capitalized | $ | $ | |||||||||

| Income tax payments, net of refunds | |||||||||||

| SUPPLEMENTAL DISCLOSURE OF NONCASH INVESTING AND FINANCING ACTIVITIES | |||||||||||

| Repayments of advances from unconsolidated affiliate in lieu of distributions | $ | $ | |||||||||

| Accrued capital expenditures | |||||||||||

| Increase in finance lease obligations for investment in PP&E | |||||||||||

| Preferred dividends declared but not paid | |||||||||||

| Common dividends issued in stock | |||||||||||

| Common dividends declared but not paid | |||||||||||

See Notes to Condensed Consolidated Financial Statements.

14

| SEMPRA | |||||||||||||||||||||||||||||||||||||||||

| CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY | |||||||||||||||||||||||||||||||||||||||||

| (Dollars in millions) | |||||||||||||||||||||||||||||||||||||||||

| Preferred stock | Common stock | Retained earnings | Accumulated other comprehensive income (loss) | Sempra shareholders' equity | Non- controlling interests | Total equity | |||||||||||||||||||||||||||||||||||

| (unaudited) | |||||||||||||||||||||||||||||||||||||||||

| Three months ended March 31, 2024 | |||||||||||||||||||||||||||||||||||||||||

| Balance at December 31, 2023 | $ | $ | $ | $ | ( | $ | $ | $ | |||||||||||||||||||||||||||||||||

| Net income | |||||||||||||||||||||||||||||||||||||||||

| Other comprehensive income | |||||||||||||||||||||||||||||||||||||||||

| Share-based compensation expense | |||||||||||||||||||||||||||||||||||||||||

| Dividends declared: | |||||||||||||||||||||||||||||||||||||||||

Series C preferred stock ($ | ( | ( | ( | ||||||||||||||||||||||||||||||||||||||

Common stock ($ | ( | ( | ( | ||||||||||||||||||||||||||||||||||||||

| Issuances of common stock | |||||||||||||||||||||||||||||||||||||||||

| Repurchases of common stock | ( | ( | ( | ||||||||||||||||||||||||||||||||||||||

| Noncontrolling interest activities: | |||||||||||||||||||||||||||||||||||||||||

| Contributions | |||||||||||||||||||||||||||||||||||||||||

| Distributions | ( | ( | |||||||||||||||||||||||||||||||||||||||

| Balance at March 31, 2024 | $ | $ | $ | $ | ( | $ | $ | $ | |||||||||||||||||||||||||||||||||

| Three months ended March 31, 2023 | |||||||||||||||||||||||||||||||||||||||||

| Balance at December 31, 2022 | $ | $ | $ | $ | ( | $ | $ | $ | |||||||||||||||||||||||||||||||||

| Net income | |||||||||||||||||||||||||||||||||||||||||

| Other comprehensive loss | ( | ( | ( | ( | |||||||||||||||||||||||||||||||||||||

| Share-based compensation expense | |||||||||||||||||||||||||||||||||||||||||

| Dividends declared: | |||||||||||||||||||||||||||||||||||||||||

Series C preferred stock ($ | ( | ( | ( | ||||||||||||||||||||||||||||||||||||||

Common stock ($ | ( | ( | ( | ||||||||||||||||||||||||||||||||||||||

| Repurchases of common stock | ( | ( | ( | ||||||||||||||||||||||||||||||||||||||

| Noncontrolling interest activities: | |||||||||||||||||||||||||||||||||||||||||

| Contributions | |||||||||||||||||||||||||||||||||||||||||

| Distributions | ( | ( | |||||||||||||||||||||||||||||||||||||||

| Sale | |||||||||||||||||||||||||||||||||||||||||

| Balance at March 31, 2023 | $ | $ | $ | $ | ( | $ | $ | $ | |||||||||||||||||||||||||||||||||

See Notes to Condensed Consolidated Financial Statements.

15

| SAN DIEGO GAS & ELECTRIC COMPANY | |||||||||||

| CONDENSED STATEMENTS OF OPERATIONS | |||||||||||

| (Dollars in millions) | |||||||||||

| Three months ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| (unaudited) | |||||||||||

| Operating revenues: | |||||||||||

| Electric | $ | $ | |||||||||

| Natural gas | |||||||||||

| Total operating revenues | |||||||||||

| Operating expenses: | |||||||||||

| Cost of electric fuel and purchased power | |||||||||||

| Cost of natural gas | |||||||||||

| Operation and maintenance | |||||||||||

| Depreciation and amortization | |||||||||||

| Franchise fees and other taxes | |||||||||||

| Total operating expenses | |||||||||||

| Operating income | |||||||||||

| Other income, net | |||||||||||

| Interest income | |||||||||||

| Interest expense | ( | ( | |||||||||

| Income before income taxes | |||||||||||

| Income tax expense | ( | ( | |||||||||

| Net income/Earnings attributable to common shares | $ | $ | |||||||||

See Notes to Condensed Financial Statements.

16

| SAN DIEGO GAS & ELECTRIC COMPANY | |||||||||||||||||

| CONDENSED STATEMENTS OF COMPREHENSIVE INCOME (LOSS) | |||||||||||||||||

| (Dollars in millions) | |||||||||||||||||

| Pretax amount | Income tax expense | Net-of-tax amount | |||||||||||||||

| (unaudited) | |||||||||||||||||

| Three months ended March 31, 2024 and 2023 | |||||||||||||||||

| 2024: | |||||||||||||||||

| Net income/Comprehensive income | $ | $ | ( | $ | |||||||||||||

| 2023: | |||||||||||||||||

| Net income/Comprehensive income | $ | $ | ( | $ | |||||||||||||

See Notes to Condensed Financial Statements.

17

| SAN DIEGO GAS & ELECTRIC COMPANY | |||||||||||

| CONDENSED BALANCE SHEETS | |||||||||||

| (Dollars in millions) | |||||||||||

| March 31, | December 31, | ||||||||||

| 2024 | 2023(1) | ||||||||||

| (unaudited) | |||||||||||

| ASSETS | |||||||||||

| Current assets: | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Accounts receivable – trade, net | |||||||||||

| Accounts receivable – other, net | |||||||||||

| Income taxes receivable, net | |||||||||||

| Inventories | |||||||||||

| Prepaid expenses | |||||||||||

| Regulatory assets | |||||||||||

| Greenhouse gas allowances | |||||||||||

| Other current assets | |||||||||||

| Total current assets | |||||||||||

| Other assets: | |||||||||||

| Regulatory assets | |||||||||||

| Greenhouse gas allowances | |||||||||||

| Nuclear decommissioning trusts | |||||||||||

| Right-of-use assets – operating leases | |||||||||||

| Wildfire fund | |||||||||||

| Other long-term assets | |||||||||||

| Total other assets | |||||||||||

| Property, plant and equipment: | |||||||||||

| Property, plant and equipment | |||||||||||

| Less accumulated depreciation and amortization | ( | ( | |||||||||

| Property, plant and equipment, net | |||||||||||

| Total assets | $ | $ | |||||||||

(1) Derived from audited financial statements.

See Notes to Condensed Financial Statements.

18

| SAN DIEGO GAS & ELECTRIC COMPANY | |||||||||||

| CONDENSED BALANCE SHEETS (CONTINUED) | |||||||||||

| (Dollars in millions) | |||||||||||

| March 31, | December 31, | ||||||||||

| 2024 | 2023(1) | ||||||||||

| (unaudited) | |||||||||||

| LIABILITIES AND SHAREHOLDER'S EQUITY | |||||||||||

| Current liabilities: | |||||||||||

| Accounts payable | $ | $ | |||||||||

| Due to unconsolidated affiliates | |||||||||||

| Interest payable | |||||||||||

| Accrued compensation and benefits | |||||||||||

| Accrued franchise fees | |||||||||||

| Regulatory liabilities | |||||||||||

| Current portion of long-term debt and finance leases | |||||||||||

| Greenhouse gas obligations | |||||||||||

| Asset retirement obligations | |||||||||||

| Other current liabilities | |||||||||||

| Total current liabilities | |||||||||||

| Long-term debt and finance leases | |||||||||||

| Deferred credits and other liabilities: | |||||||||||

| Regulatory liabilities | |||||||||||

| Greenhouse gas obligations | |||||||||||

| Pension obligation, net of plan assets | |||||||||||

| Deferred income taxes | |||||||||||

| Asset retirement obligations | |||||||||||

| Deferred credits and other | |||||||||||

| Total deferred credits and other liabilities | |||||||||||

| Commitments and contingencies (Note 11) | |||||||||||

| Shareholder's equity: | |||||||||||

Preferred stock ( | |||||||||||

Common stock ( no par value) | |||||||||||

| Retained earnings | |||||||||||

| Accumulated other comprehensive income (loss) | ( | ( | |||||||||

| Total shareholder’s equity | |||||||||||

| Total liabilities and shareholder's equity | $ | $ | |||||||||

(1) Derived from audited financial statements.

See Notes to Condensed Financial Statements.

19

| SAN DIEGO GAS & ELECTRIC COMPANY | |||||||||||

| CONDENSED STATEMENTS OF CASH FLOWS | |||||||||||

| (Dollars in millions) | |||||||||||

| Three months ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| (unaudited) | |||||||||||

| CASH FLOWS FROM OPERATING ACTIVITIES | |||||||||||

| Net income | $ | $ | |||||||||

| Adjustments to reconcile net income to net cash provided by operating activities: | |||||||||||

| Depreciation and amortization | |||||||||||

| Deferred income taxes and investment tax credits | ( | ||||||||||

| Bad debt expense | |||||||||||

| Other | ( | ( | |||||||||

| Net change in working capital components | ( | ( | |||||||||

| Changes in noncurrent assets and liabilities, net | ( | ||||||||||

| Net cash provided by operating activities | |||||||||||

| CASH FLOWS FROM INVESTING ACTIVITIES | |||||||||||

| Expenditures for property, plant and equipment | ( | ( | |||||||||

| Purchases of nuclear decommissioning trust assets | ( | ( | |||||||||

| Proceeds from sales of nuclear decommissioning trust assets | |||||||||||

| Net cash used in investing activities | ( | ( | |||||||||

| CASH FLOWS FROM FINANCING ACTIVITIES | |||||||||||

| Issuances of debt (maturities greater than 90 days) | |||||||||||

| Payments on debt (maturities greater than 90 days) and finance leases | ( | ( | |||||||||

| Decrease in short-term debt, net | ( | ||||||||||

| Debt issuance costs | ( | ( | |||||||||

| Net cash provided by financing activities | |||||||||||

| Increase in cash and cash equivalents | |||||||||||

| Cash and cash equivalents, January 1 | |||||||||||

| Cash and cash equivalents, March 31 | $ | $ | |||||||||

| SUPPLEMENTAL DISCLOSURE OF CASH FLOW INFORMATION | |||||||||||

| Interest payments, net of amounts capitalized | $ | $ | |||||||||

| SUPPLEMENTAL DISCLOSURE OF NONCASH INVESTING AND FINANCING ACTIVITIES | |||||||||||

| Accrued capital expenditures | $ | $ | |||||||||

| Increase in finance lease obligations for investment in PP&E | |||||||||||

See Notes to Condensed Financial Statements.

20

| SAN DIEGO GAS & ELECTRIC COMPANY | |||||||||||||||||||||||

| CONDENSED STATEMENTS OF CHANGES IN SHAREHOLDER’S EQUITY | |||||||||||||||||||||||

| (Dollars in millions) | |||||||||||||||||||||||

| Common stock | Retained earnings | Accumulated other comprehensive income (loss) | Total shareholder's equity | ||||||||||||||||||||

| (unaudited) | |||||||||||||||||||||||

| Three months ended March 31, 2024 | |||||||||||||||||||||||

| Balance at December 31, 2023 | $ | $ | $ | ( | $ | ||||||||||||||||||

| Net income | |||||||||||||||||||||||

| Balance at March 31, 2024 | $ | $ | $ | ( | $ | ||||||||||||||||||

| Three months ended March 31, 2023 | |||||||||||||||||||||||

| Balance at December 31, 2022 | $ | $ | $ | ( | $ | ||||||||||||||||||

| Net income | |||||||||||||||||||||||

| Balance at March 31, 2023 | $ | $ | ( | $ | |||||||||||||||||||

See Notes to Condensed Financial Statements.

21

| SOUTHERN CALIFORNIA GAS COMPANY | |||||||||||

| CONDENSED STATEMENTS OF OPERATIONS | |||||||||||

| (Dollars in millions) | |||||||||||

| Three months ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| (unaudited) | |||||||||||

| Operating revenues | $ | $ | |||||||||

| Operating expenses: | |||||||||||

| Cost of natural gas | |||||||||||

| Operation and maintenance | |||||||||||

| Depreciation and amortization | |||||||||||

| Franchise fees and other taxes | |||||||||||

| Total operating expenses | |||||||||||

| Operating income | |||||||||||

| Other income (expense), net | ( | ||||||||||

| Interest income | |||||||||||

| Interest expense | ( | ( | |||||||||

| Income before income taxes | |||||||||||

| Income tax expense | ( | ( | |||||||||

| Net income/Earnings attributable to common shares | $ | $ | |||||||||

See Notes to Condensed Financial Statements.

22

| SOUTHERN CALIFORNIA GAS COMPANY | |||||||||||||||||

| CONDENSED STATEMENTS OF COMPREHENSIVE INCOME (LOSS) | |||||||||||||||||

| (Dollars in millions) | |||||||||||||||||

| Pretax amount | Income tax expense | Net-of-tax amount | |||||||||||||||

| (unaudited) | |||||||||||||||||

| Three months ended March 31, 2024 and 2023 | |||||||||||||||||

| 2024: | |||||||||||||||||

| Net income | $ | $ | ( | $ | |||||||||||||

| Other comprehensive income (loss): | |||||||||||||||||

| Pension and other postretirement benefits | |||||||||||||||||

| Total other comprehensive income | |||||||||||||||||

| Comprehensive income | $ | $ | ( | $ | |||||||||||||

| 2023: | |||||||||||||||||

| Net income | $ | $ | ( | $ | |||||||||||||

| Other comprehensive income (loss): | |||||||||||||||||

| Pension and other postretirement benefits | |||||||||||||||||

| Total other comprehensive income | |||||||||||||||||

| Comprehensive income | $ | $ | ( | $ | |||||||||||||

See Notes to Condensed Financial Statements.

23

| SOUTHERN CALIFORNIA GAS COMPANY | |||||||||||

| CONDENSED BALANCE SHEETS | |||||||||||

| (Dollars in millions) | |||||||||||

| March 31, | December 31, | ||||||||||

| 2024 | 2023(1) | ||||||||||

| (unaudited) | |||||||||||

| ASSETS | |||||||||||

| Current assets: | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Accounts receivable – trade, net | |||||||||||

| Accounts receivable – other, net | |||||||||||

| Due from unconsolidated affiliates | |||||||||||

| Inventories | |||||||||||

| Regulatory assets | |||||||||||

| Greenhouse gas allowances | |||||||||||

| Other current assets | |||||||||||

| Total current assets | |||||||||||

| Other assets: | |||||||||||

| Regulatory assets | |||||||||||

| Greenhouse gas allowances | |||||||||||

| Right-of-use assets – operating leases | |||||||||||

| Other long-term assets | |||||||||||

| Total other assets | |||||||||||

| Property, plant and equipment: | |||||||||||

| Property, plant and equipment | |||||||||||

| Less accumulated depreciation and amortization | ( | ( | |||||||||

| Property, plant and equipment, net | |||||||||||

| Total assets | $ | $ | |||||||||

(1) Derived from audited financial statements.

See Notes to Condensed Financial Statements.

24

| SOUTHERN CALIFORNIA GAS COMPANY | |||||||||||

| CONDENSED BALANCE SHEETS (CONTINUED) | |||||||||||

| (Dollars in millions) | |||||||||||

| March 31, | December 31, | ||||||||||

| 2024 | 2023(1) | ||||||||||

| (unaudited) | |||||||||||

| LIABILITIES AND SHAREHOLDERS’ EQUITY | |||||||||||

| Current liabilities: | |||||||||||

| Short-term debt | $ | $ | |||||||||

| Accounts payable – trade | |||||||||||

| Accounts payable – other | |||||||||||

| Due to unconsolidated affiliates | |||||||||||

| Accrued compensation and benefits | |||||||||||

| Regulatory liabilities | |||||||||||

| Current portion of long-term debt and finance leases | |||||||||||

| Greenhouse gas obligations | |||||||||||

| Asset retirement obligations | |||||||||||

| Other current liabilities | |||||||||||

| Total current liabilities | |||||||||||

| Long-term debt and finance leases | |||||||||||

| Deferred credits and other liabilities: | |||||||||||

| Regulatory liabilities | |||||||||||

| Greenhouse gas obligations | |||||||||||

| Pension obligation, net of plan assets | |||||||||||

| Deferred income taxes | |||||||||||

| Asset retirement obligations | |||||||||||

| Deferred credits and other | |||||||||||

| Total deferred credits and other liabilities | |||||||||||

| Commitments and contingencies (Note 11) | |||||||||||

| Shareholders’ equity: | |||||||||||

Preferred stock ( | |||||||||||

Common stock ( no par value) | |||||||||||

| Retained earnings | |||||||||||

| Accumulated other comprehensive income (loss) | ( | ( | |||||||||

| Total shareholders’ equity | |||||||||||

| Total liabilities and shareholders’ equity | $ | $ | |||||||||

(1) Derived from audited financial statements.

See Notes to Condensed Financial Statements.

25

| SOUTHERN CALIFORNIA GAS COMPANY | |||||||||||

| CONDENSED STATEMENTS OF CASH FLOWS | |||||||||||

| (Dollars in millions) | |||||||||||

| Three months ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| (unaudited) | |||||||||||

| CASH FLOWS FROM OPERATING ACTIVITIES | |||||||||||

| Net income | $ | $ | |||||||||

| Adjustments to reconcile net income to net cash provided by operating activities: | |||||||||||

| Depreciation and amortization | |||||||||||

| Deferred income taxes and investment tax credits | |||||||||||

| Bad debt expense | |||||||||||

| Other | ( | ||||||||||

| Net change in working capital components | ( | ||||||||||

| Changes in noncurrent assets and liabilities, net | ( | ( | |||||||||

| Net cash provided by operating activities | |||||||||||

| CASH FLOWS FROM INVESTING ACTIVITIES | |||||||||||

| Expenditures for property, plant and equipment | ( | ( | |||||||||

| Net cash used in investing activities | ( | ( | |||||||||

| CASH FLOWS FROM FINANCING ACTIVITIES | |||||||||||

| Issuances of debt (maturities greater than 90 days) | |||||||||||

| Payments on finance leases | ( | ( | |||||||||

| (Decrease) increase in short-term debt, net | ( | ||||||||||

| Debt issuance costs | ( | ||||||||||

| Net cash (used in) provided by financing activities | ( | ||||||||||

| Increase (decrease) in cash and cash equivalents | ( | ||||||||||

| Cash and cash equivalents, January 1 | |||||||||||

| Cash and cash equivalents, March 31 | $ | $ | |||||||||

| SUPPLEMENTAL DISCLOSURE OF CASH FLOW INFORMATION | |||||||||||

| Interest payments, net of amounts capitalized | $ | $ | |||||||||

| SUPPLEMENTAL DISCLOSURE OF NONCASH INVESTING AND FINANCING ACTIVITIES | |||||||||||

| Accrued capital expenditures | $ | $ | |||||||||

| Increase in finance lease obligations for investment in PP&E | |||||||||||

See Notes to Condensed Financial Statements.

26

| SOUTHERN CALIFORNIA GAS COMPANY | |||||||||||||||||||||||||||||

| CONDENSED STATEMENTS OF CHANGES IN SHAREHOLDERS’ EQUITY | |||||||||||||||||||||||||||||

| (Dollars in millions) | |||||||||||||||||||||||||||||

| Preferred stock | Common stock | Retained earnings | Accumulated other comprehensive income (loss) | Total shareholders’ equity | |||||||||||||||||||||||||

| (unaudited) | |||||||||||||||||||||||||||||

| Three months ended March 31, 2024 | |||||||||||||||||||||||||||||

| Balance at December 31, 2023 | $ | $ | $ | $ | ( | $ | |||||||||||||||||||||||

| Net income | |||||||||||||||||||||||||||||

| Other comprehensive income | |||||||||||||||||||||||||||||

| Dividends declared: | |||||||||||||||||||||||||||||

Preferred stock ($ | |||||||||||||||||||||||||||||

| Balance at March 31, 2024 | $ | $ | $ | $ | ( | $ | |||||||||||||||||||||||

| Three months ended March 31, 2023 | |||||||||||||||||||||||||||||

| Balance at December 31, 2022 | $ | $ | $ | $ | ( | $ | |||||||||||||||||||||||

Net income | |||||||||||||||||||||||||||||

| Other comprehensive income | |||||||||||||||||||||||||||||

| Dividends declared: | |||||||||||||||||||||||||||||

Preferred stock ($ | |||||||||||||||||||||||||||||

| Balance at March 31, 2023 | $ | $ | $ | $ | ( | $ | |||||||||||||||||||||||

See Notes to Condensed Financial Statements.

27

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

NOTE 1. GENERAL INFORMATION AND OTHER FINANCIAL DATA

PRINCIPLES OF CONSOLIDATION

Sempra

Sempra’s Condensed Consolidated Financial Statements include the accounts of Sempra, a California-based holding company, and its consolidated entities, which invest in, develop and operate energy infrastructure in North America, and provide electric and gas services to customers.

Sempra has three separate reportable segments, which we describe in Note 12. In the fourth quarter of 2023, Sempra realigned its reportable segments to reflect changes in how the CODM oversees our three platforms: Sempra California, Sempra Texas Utilities and Sempra Infrastructure. Our former SDG&E and SoCalGas reportable segments were combined into one operating and reportable segment, Sempra California, which is consistent with how the CODM assesses performance due to the similarities of their operations, including geographic location and regulatory framework in California. Sempra’s historical segment disclosures have been restated to conform with the current presentation, so that all discussions reflect the revised segment information of its three reportable segments. All references in these Notes to our reportable segments are not intended to refer to any legal entity with the same or similar name.

SDG&E

SDG&E’s common stock is wholly owned by Enova Corporation, which is a wholly owned subsidiary of Sempra. SDG&E is a regulated public utility that provides electric service to San Diego and southern Orange counties and natural gas service to San Diego County. SDG&E has one reportable segment.

SoCalGas

SoCalGas’ common stock is wholly owned by Pacific Enterprises, which is a wholly owned subsidiary of Sempra. SoCalGas is a regulated public natural gas distribution utility, serving customers throughout most of Southern California and part of central California. SoCalGas has one reportable segment.

BASIS OF PRESENTATION

This is a combined report of Sempra, SDG&E and SoCalGas. We provide separate information for SDG&E and SoCalGas as required. We have eliminated intercompany accounts and transactions within the condensed consolidated financial statements of each Registrant.

We have prepared our Condensed Consolidated Financial Statements in conformity with U.S. GAAP and in accordance with the interim period reporting requirements of Form 10-Q and applicable rules of the SEC. The financial statements reflect all adjustments that are necessary for a fair presentation of the results for the interim periods. These adjustments are only of a normal, recurring nature. Results of operations for interim periods are not necessarily indicative of results for the entire year or for any other period. We evaluated events and transactions that occurred after March 31, 2024 through the date the financial statements were issued and, in the opinion of management, the accompanying statements reflect all adjustments necessary for a fair presentation.

All December 31, 2023 balance sheet information in the Condensed Consolidated Financial Statements has been derived from our audited 2023 Consolidated Financial Statements in the Annual Report. Certain information and note disclosures normally included in annual financial statements prepared in accordance with U.S. GAAP have been condensed or omitted pursuant to the interim period reporting provisions of U.S. GAAP and the SEC.

We describe our significant accounting policies in Note 1 of the Notes to Consolidated Financial Statements in the Annual Report and the impact of the adoption of new accounting standards on those policies in Note 2 below. We follow the same accounting policies for interim period reporting purposes.

The information contained in this report should be read in conjunction with the Annual Report.

28

REGULATED OPERATIONS

SDG&E, SoCalGas and Sempra Infrastructure’s natural gas distribution utility, Ecogas, prepare their financial statements in accordance with the provisions of U.S. GAAP governing rate-regulated operations. We discuss revenue recognition and the effects of regulation at our utilities in Notes 3 and 4 below and in Notes 1, 3 and 4 of the Notes to Consolidated Financial Statements in the Annual Report.

Our Sempra Texas Utilities segment is comprised of our equity method investments in holding companies that own interests in regulated electric transmission and distribution utilities in Texas.

Our Sempra Infrastructure segment includes the operating companies of our subsidiary, SI Partners, as well as certain holding companies and risk management activity. Certain business activities at Sempra Infrastructure are regulated by the CRE and the FERC and meet the regulatory accounting requirements of U.S. GAAP.

VARIABLE INTEREST ENTITIES

We consolidate a VIE if we are the primary beneficiary of the VIE. Our determination of whether we are the primary beneficiary is based on qualitative and quantitative analyses, which assess:

▪the purpose and design of the VIE;

▪the nature of the VIE’s risks and the risks we absorb;

▪the power to direct activities that most significantly impact the economic performance of the VIE; and

▪the obligation to absorb losses or the right to receive benefits that could be significant to the VIE.

SDG&E

SDG&E’s power procurement is subject to reliability requirements that may require SDG&E to enter into various PPAs that include variable interests. SDG&E evaluates the respective entities to determine if variable interests exist and, based on the qualitative and quantitative analyses described above, if SDG&E, and indirectly Sempra, is the primary beneficiary.

SDG&E has agreements under which it purchases power generated by facilities for which it supplies all of the natural gas to fuel the power plant (i.e., tolling agreements). SDG&E’s obligation to absorb natural gas costs may be a significant variable interest. In addition, SDG&E has the power to direct the dispatch of electricity generated by these facilities. Based on our analysis, the ability to direct the dispatch of electricity may have the most significant impact on the economic performance of the entity owning the generating facility because of the associated exposure to the cost of natural gas, which fuels the plants, and the value of electricity produced. To the extent that SDG&E (1) is obligated to purchase and provide fuel to operate the facility, (2) has the power to direct the dispatch, and (3) purchases all of the output from the facility for a substantial portion of the facility’s useful life, SDG&E may be the primary beneficiary of the entity owning the generating facility. SDG&E determines if it is the primary beneficiary in these cases based on a qualitative approach in which it considers the operational characteristics of the facility, including its expected power generation output relative to its capacity to generate and the financial structure of the entity, among other factors. If SDG&E determines that it is the primary beneficiary, SDG&E and Sempra consolidate the entity that owns the facility as a VIE.

In addition to tolling agreements, other variable interests involve various elements of fuel and power costs, and other components of cash flows expected to be paid to or received by our counterparties. In most of these cases, the expectation of variability is not substantial, and SDG&E generally does not have the power to direct activities, including the operation and maintenance activities of the generating facility, that most significantly impact the economic performance of the other VIEs. If our ongoing evaluation of these VIEs were to conclude that SDG&E becomes the primary beneficiary and consolidation by SDG&E becomes necessary, the effects could be significant to the financial position and liquidity of SDG&E and Sempra.

29

SDG&E determined that none of its PPAs and tolling agreements resulted in SDG&E being the primary beneficiary of a VIE at March 31, 2024 and December 31, 2023. PPAs and tolling agreements that relate to SDG&E’s involvement with VIEs are primarily accounted for as finance leases. The carrying amounts of the assets and liabilities under these contracts are included in PP&E, net, and finance lease liabilities with balances of $1,159 1,166

Other Sempra

Oncor Holdings

Oncor Holdings is a VIE. Sempra is not the primary beneficiary of this VIE because of the structural and operational ring-fencing and governance measures in place that prevent us from having the power to direct the significant activities of Oncor Holdings. As a result, we do not consolidate Oncor Holdings and instead account for our ownership interest as an equity method investment. See Note 6 of the Notes to Consolidated Financial Statements in the Annual Report for additional information about our equity method investment in Oncor Holdings and restrictions on our ability to influence its activities. Our maximum exposure to loss, which fluctuates over time, from our interest in Oncor Holdings does not exceed the carrying value of our investment, which was $14,545 million and $14,266 million at March 31, 2024 and December 31, 2023, respectively.

Cameron LNG JV

Cameron LNG JV is a VIE principally due to contractual provisions that transfer certain risks to customers. Sempra is not the primary beneficiary of this VIE because we do not have the power to direct the most significant activities of Cameron LNG JV, including LNG production and operation and maintenance activities at the liquefaction facility. Therefore, we account for our investment in Cameron LNG JV under the equity method. The carrying value of our investment, including amounts recognized in AOCI related to interest-rate cash flow hedges at Cameron LNG JV, was $1,025 million at March 31, 2024 and $1,008 million at December 31, 2023. Our maximum exposure to loss, which fluctuates over time, includes the carrying value of our investment and our obligation under the SDSRA, which we discuss in Note 5.

CFIN

As we discuss in Note 5, in July 2020, Sempra entered into a Support Agreement for the benefit of CFIN, which is a VIE. Sempra is not the primary beneficiary of this VIE because we do not have the power to direct the most significant activities of CFIN, including modification, prepayment, and refinance decisions related to the financing arrangement with external lenders and Cameron LNG JV’s four project owners as well as the ability to determine and enforce remedies in the event of default. The conditional obligations of the Support Agreement represent a variable interest that we measure at fair value on a recurring basis (see Note 8). Sempra’s maximum exposure to loss under the terms of the Support Agreement is $979 million.

ECA LNG Phase 1

ECA LNG Phase 1 is a VIE because its total equity at risk is not sufficient to finance its activities without additional subordinated financial support. We expect that ECA LNG Phase 1 will require future capital contributions or other financial support to finance the construction of the facility. Sempra is the primary beneficiary of this VIE because we have the power to direct the activities related to the construction and future operation and maintenance of the liquefaction facility. As a result, we consolidate ECA LNG Phase 1. Sempra consolidated $1,638 million and $1,580 million of assets at March 31, 2024 and December 31, 2023, respectively, consisting primarily of PP&E, net, attributable to ECA LNG Phase 1 that could be used only to settle obligations of this VIE and that are not available to settle obligations of Sempra, and $1,087 million and $1,029 million of liabilities at March 31, 2024 and December 31, 2023, respectively, consisting primarily of long-term debt, accounts payable and short-term debt attributable to ECA LNG Phase 1 for which creditors do not have recourse to the general credit of Sempra. Additionally, as we discuss in Note 6, IEnova and TotalEnergies SE have provided guarantees for 83.4 % and 16.6 %, respectively, of the loan facility supporting construction of the liquefaction facility.

30

Port Arthur LNG

Port Arthur LNG is a VIE because its total equity at risk is not sufficient to finance its activities without additional subordinated financial support. We expect that Port Arthur LNG will require future capital contributions or other financial support to finance the construction of the PA LNG Phase 1 project. Sempra is the primary beneficiary of this VIE because we have the power to direct the activities related to the construction and future operation and maintenance of the liquefaction facility. As a result, we consolidate Port Arthur LNG. Sempra consolidated $4,605 million and $3,927 million of assets at March 31, 2024 and December 31, 2023, respectively, consisting primarily of PP&E, net, and other long-term assets attributable to Port Arthur LNG that could be used only to settle obligations of this VIE and that are not available to settle obligations of Sempra, and $582 million and $600 million of liabilities at March 31, 2024 and December 31, 2023, respectively, consisting primarily of accounts payable and long-term debt attributable to Port Arthur LNG for which creditors do not have recourse to the general credit of Sempra.

CASH, CASH EQUIVALENTS AND RESTRICTED CASH

The following table provides a reconciliation of cash, cash equivalents and restricted cash reported on Sempra’s Condensed Consolidated Balance Sheets to the sum of such amounts reported on Sempra’s Condensed Consolidated Statements of Cash Flows. We provide information about the nature of restricted cash in Note 1 of the Notes to Consolidated Financial Statements in the Annual Report.

| RECONCILIATION OF CASH, CASH EQUIVALENTS AND RESTRICTED CASH | ||||||||

| (Dollars in millions) | ||||||||

| March 31, 2024 | December 31, 2023 | |||||||

| Sempra: | ||||||||

| Cash and cash equivalents | $ | $ | ||||||

| Restricted cash, current | ||||||||

| Restricted cash, noncurrent | ||||||||

Total cash, cash equivalents and restricted cash on the Condensed Consolidated Statements of Cash Flows | $ | $ | ||||||

CREDIT LOSSES

We are exposed to credit losses from financial assets measured at amortized cost, including trade and other accounts receivable, amounts due from unconsolidated affiliates, our net investment in sales-type leases and a note receivable. We are also exposed to credit losses from off-balance sheet arrangements through Sempra’s guarantee related to Cameron LNG JV’s SDSRA, which we discuss in Note 5.

We regularly monitor and evaluate credit losses and record allowances for expected credit losses, if necessary, for trade and other accounts receivable using a combination of factors, including past-due status based on contractual terms, trends in write-offs, the age of the receivables and customer payment patterns, historical and industry trends, counterparty creditworthiness, economic conditions and specific events, such as bankruptcies, pandemics and other factors. We write off financial assets measured at amortized cost in the period in which we determine they are not recoverable. We record recoveries of amounts previously written off when it is known that they will be recovered.

The implementation of customer assistance programs and higher 2023 winter season customer billings have resulted in certain SDG&E and SoCalGas customers exhibiting slower payment and higher levels of nonpayment than has been the case historically. In January 2024, the CPUC directed SDG&E and SoCalGas to offer long-term repayment plans to eligible residential customers with past-due balances until October 2026.

SDG&E and SoCalGas have regulatory mechanisms to recover credit losses and thus record changes in the allowances for credit losses related to Accounts Receivable – Trade that are probable of recovery in regulatory accounts. We discuss regulatory accounts in Note 4 below and in Note 4 of the Notes to Consolidated Financial Statements in the Annual Report.

31

Changes in allowances for credit losses for trade receivables and other receivables are as follows:

| CHANGES IN ALLOWANCES FOR CREDIT LOSSES | ||||||||

| (Dollars in millions) | ||||||||

| 2024 | 2023 | |||||||

| Sempra: | ||||||||

| Allowances for credit losses at January 1 | $ | $ | ||||||

| Provisions for expected credit losses | ||||||||

| Write-offs | ( | ( | ||||||

Allowances for credit losses at March 31 | $ | $ | ||||||

| SDG&E: | ||||||||

| Allowances for credit losses at January 1 | $ | $ | ||||||

| Provisions for expected credit losses | ||||||||

| Write-offs | ( | ( | ||||||

Allowances for credit losses at March 31 | $ | $ | ||||||

| SoCalGas: | ||||||||

| Allowances for credit losses at January 1 | $ | $ | ||||||

| Provisions for expected credit losses | ||||||||

| Write-offs | ( | ( | ||||||

Allowances for credit losses at March 31 | $ | $ | ||||||

Allowances for credit losses related to trade receivables and other receivables are included in the Condensed Consolidated Balance Sheets as follows:

| ALLOWANCES FOR CREDIT LOSSES | ||||||||

| (Dollars in millions) | ||||||||

| March 31, | December 31, | |||||||

| 2024 | 2023 | |||||||

| Sempra: | ||||||||

| Accounts receivable – trade, net | $ | $ | ||||||

| Accounts receivable – other, net | ||||||||

| Other long-term assets | ||||||||

| Total allowances for credit losses | $ | $ | ||||||

| SDG&E: | ||||||||

| Accounts receivable – trade, net | $ | $ | ||||||

| Accounts receivable – other, net | ||||||||

| Other long-term assets | ||||||||

| Total allowances for credit losses | $ | $ | ||||||

| SoCalGas: | ||||||||

| Accounts receivable – trade, net | $ | $ | ||||||

| Accounts receivable – other, net | ||||||||

Other long-term assets | ||||||||

| Total allowances for credit losses | $ | $ | ||||||

As we discuss below in “Note Receivable,” we have an interest-bearing promissory note due from KKR Pinnacle. On a quarterly basis, we evaluate credit losses and record allowances for expected credit losses on this note receivable, including compounded interest and unamortized transaction costs, based on published default rate studies, the maturity date of the instrument and an internally developed credit rating. At both March 31, 2024 and December 31, 2023, $6

As we discuss in Note 5, Sempra provided a guarantee for the benefit of Cameron LNG JV related to amounts withdrawn by Sempra Infrastructure from the SDSRA. On a quarterly basis, we evaluate credit losses and record liabilities for expected credit losses on this off-balance sheet arrangement based on external credit ratings, published default rate studies and the maturity date of the arrangement. At both March 31, 2024 and December 31, 2023, $5

32

TRANSACTIONS WITH AFFILIATES

We summarize amounts due from and to unconsolidated affiliates at the Registrants in the following table.

| AMOUNTS DUE FROM (TO) UNCONSOLIDATED AFFILIATES | |||||||||||

| (Dollars in millions) | |||||||||||

| March 31, 2024 | December 31, 2023 | ||||||||||

| Sempra: | |||||||||||

| Tax sharing arrangement with Oncor Holdings | $ | $ | |||||||||

| Various affiliates | |||||||||||

| Total due from unconsolidated affiliates – current | $ | $ | |||||||||

TAG Pipelines – | $ | $ | ( | ||||||||

| Total due to unconsolidated affiliates – current | $ | $ | ( | ||||||||

TAG Pipelines(1): | |||||||||||

| $ | $ | ( | |||||||||

| ( | |||||||||||

| ( | ( | ||||||||||

| ( | ( | ||||||||||

| ( | ( | ||||||||||

| ( | ( | ||||||||||

| ( | |||||||||||

TAG Norte – | ( | ( | |||||||||

| Total due to unconsolidated affiliates – noncurrent | $ | ( | $ | ( | |||||||

| SDG&E: | |||||||||||

| Sempra | $ | ( | $ | ( | |||||||

| SoCalGas | ( | ( | |||||||||

| Various affiliates | ( | ( | |||||||||

| Total due to unconsolidated affiliates – current | $ | ( | $ | ( | |||||||

Income taxes due from Sempra(2) | $ | $ | |||||||||

| SoCalGas: | |||||||||||

| SDG&E | $ | $ | |||||||||

| Various affiliates | |||||||||||

| Total due from unconsolidated affiliates – current | $ | $ | |||||||||

| Sempra | $ | ( | $ | ( | |||||||

| Total due to unconsolidated affiliates – current | $ | ( | $ | ( | |||||||

Income taxes due from Sempra(2) | $ | $ | |||||||||

(1) U.S. dollar-denominated loans at fixed interest rates. Amounts include principal balances plus accumulated interest outstanding and value added tax payable to the Mexican government.

(2) SDG&E and SoCalGas are included in the consolidated income tax return of Sempra, and their respective income tax expense is computed as an amount equal to that which would result from each company having always filed a separate return. Amounts include current and noncurrent income taxes due to/from Sempra.

33

The following table summarizes income statement information from unconsolidated affiliates.

| INCOME STATEMENT IMPACT FROM UNCONSOLIDATED AFFILIATES | |||||||||||

| (Dollars in millions) | |||||||||||

| Three months ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| Sempra: | |||||||||||

| Revenues | $ | $ | |||||||||

| Interest expense | |||||||||||

| SDG&E: | |||||||||||

| Revenues | $ | $ | |||||||||

| Cost of sales | |||||||||||

| SoCalGas: | |||||||||||

| Revenues | $ | $ | |||||||||

Cost of sales(1) | ( | ||||||||||

(1) Includes net commodity costs from natural gas transactions with unconsolidated affiliates.

Guarantees

Sempra provides guarantees related to Cameron LNG JV’s SDSRA and CFIN’s Support Agreement. We discuss these guarantees in Note 5.

INVENTORIES

The components of inventories are as follows:

| INVENTORY BALANCES | |||||||||||||||||||||||||||||||||||

| (Dollars in millions) | |||||||||||||||||||||||||||||||||||

| Sempra | SDG&E | SoCalGas | |||||||||||||||||||||||||||||||||

| March 31, 2024 | December 31, 2023 | March 31, 2024 | December 31, 2023 | March 31, 2024 | December 31, 2023 | ||||||||||||||||||||||||||||||

| Natural gas | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

| LNG | |||||||||||||||||||||||||||||||||||

| Materials and supplies | |||||||||||||||||||||||||||||||||||

| Total | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

DEDICATED ASSETS IN SUPPORT OF CERTAIN BENEFITS PLANS

In support of its Supplemental Executive Retirement, Cash Balance Restoration and Deferred Compensation Plans, Sempra maintains dedicated assets, including a Rabbi Trust and investments in life insurance contracts, which totaled $559 million and $549 million at March 31, 2024 and December 31, 2023, respectively.

NOTE RECEIVABLE

In November 2021, Sempra loaned $300 million to KKR Pinnacle in exchange for an interest-bearing promissory note that is due in full no later than October 2029 and bears compound interest at 5 % per annum, which may be paid quarterly or added to the outstanding principal at the election of KKR Pinnacle. At March 31, 2024 and December 31, 2023, Other Long-Term Assets includes $336 million and $332 million, respectively, of outstanding principal, compounded interest and unamortized transaction costs, net of allowance for credit losses, on Sempra’s Condensed Consolidated Balance Sheets.

34

PROPERTY, PLANT AND EQUIPMENT

Sempra Infrastructure’s Sonora natural gas pipeline consists of two segments, the Sasabe-Puerto Libertad-Guaymas segment and the Guaymas-El Oro segment. Each segment has its own service agreement with the CFE. Following the start of commercial operations of the Guaymas-El Oro segment, Sempra Infrastructure reported damage to the pipeline in the Yaqui territory that has made that section inoperable since August 2017. Sempra Infrastructure and the CFE have agreed to an amendment to their transportation services agreement and to re-route the portion of the pipeline that is in the Yaqui territory, whereby the CFE would pay for the re-routing with a new tariff. This amendment will terminate if certain conditions are not met, and Sempra Infrastructure retains the right to terminate the transportation services agreement and seek to recover its reasonable and documented costs and lost profit. Sempra Infrastructure continues to acquire and pursue the necessary rights-of-way and permits for the re-routed portion of the pipeline. At March 31, 2024, Sempra Infrastructure had $408 million in PP&E, net, related to the Guaymas-El Oro segment of the Sonora pipeline, which could be subject to impairment if Sempra Infrastructure is unable to re-route a portion of the pipeline and resume operations or if Sempra Infrastructure terminates the contract and is unable to obtain recovery.

CAPITALIZED FINANCING COSTS

Capitalized financing costs include capitalized interest costs and AFUDC related to both debt and equity financing of construction projects. We capitalize interest costs incurred to finance capital projects and interest at equity method investments that have not commenced planned principal operations.

The table below summarizes capitalized financing costs, comprised of AFUDC and capitalized interest.

| CAPITALIZED FINANCING COSTS | |||||||||||

| (Dollars in millions) | |||||||||||

| Three months ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| Sempra | $ | $ | |||||||||

| SDG&E | |||||||||||

| SoCalGas | |||||||||||

35

COMPREHENSIVE INCOME

The following tables present the changes in AOCI by component and amounts reclassified out of AOCI to net income, after amounts attributable to NCI.

CHANGES IN ACCUMULATED OTHER COMPREHENSIVE INCOME (LOSS) BY COMPONENT(1) | |||||||||||||||||||||||

| (Dollars in millions) | |||||||||||||||||||||||

| Foreign currency translation adjustments | Financial instruments | Pension and PBOP | Total accumulated other comprehensive income (loss) | ||||||||||||||||||||