SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the Fiscal Year Ended December 31, 2010

|

Commission File No. 0-22750

|

ROYALE ENERGY, INC.

(Name of registrant in its charter)

|

California

|

33-0224120

|

|

(State or other jurisdiction of

incorporation or organization)

|

(I.R.S. Employer

Identification No.)

|

7676 Hazard Center Drive, Suite 1500

San Diego, CA 92108

(Address of principal executive offices)

Issuer's telephone number: 619-881-2800

Securities registered pursuant to Section 12(b) of the Act:

None

Securities to be registered pursuant to Section 12(g) of the Act:

Common Stock, no par value per share

(Title of Class)

Indicate by check mark if the registrant is a well known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ]; No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act.

Yes [ ]; No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] ; No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-B is not contained herein, and will not be contained, to the best or registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company.

Large accelerated filer [ ] Accelerated filer [ ]

Non-accelerated filer [ ] Smaller Reporting Company [X]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

Yes [ ]; No [X]

At June 30, 2010, the end of the registrant’s most recently completed second fiscal quarter, the aggregate market value of common equity held by non-affiliates was $15,203,305.

At December 31, 2010, 10,274,731 shares of registrant's Common Stock were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE: The issuer’s proxy statement for its annual meeting of

stockholders, to be filed within 120 days after December 31, 2010, will contain the information required by Part III, Items 10, 11, 12, 13 and 14, which information is hereby incorporated by reference into this Form 10-K.

|

CONTENTS

|

|||

|

PART I

|

1

|

||

|

Item 1

|

Description of Business

|

1

|

|

|

Plan of Business

|

2

|

||

|

Competition, Markets and Regulation

|

3

|

||

|

Item 1A

|

Risk Factors

|

3

|

|

|

Item 2

|

Description of Property

|

7

|

|

|

Northern California

|

8

|

||

|

Developed and Undeveloped Leasehold Acreage

|

8

|

||

|

Drilling Activities

|

8

|

||

|

Production

|

9

|

||

|

Net Proved Oil and Natural Gas Reserves

|

9

|

||

|

Item 3

|

Legal Proceedings

|

9

|

|

|

PART II

|

9

|

||

|

Item 5

|

Market for Common Equity and Related Stockholder Matters

|

9

|

|

|

Dividends

|

10

|

||

|

Recent Sales of Unregistered Securities

|

10

|

||

|

Performance Graph

|

10

|

||

|

Item 6

|

Selected Financial Data

|

11

|

|

|

Item 7

|

Management’s Discussion and Analysis of financial Condition and Results of Operations

|

11

|

|

|

Critical Accounting Policies

|

11

|

||

|

Results of Operations for the Twelve Months Ended December 31, 2010, as Compared to the Twelve Months Ended December 31, 2009

|

13

|

||

|

Results of Operations for the Twelve Months Ended December 31, 2009, as Compared to the Twelve Months Ended December 31, 2008

|

14

|

||

|

Capital Resources and Liquidity

|

16

|

||

|

Changes in Reserve Estimates

|

18

|

||

|

Item 7A

|

Qualitative and Quantitative Disclosures About Market Risk

|

19

|

|

|

Item 8

|

Financial Statements

|

19

|

|

|

Item 9A

|

Controls and Procedures

|

||

|

Disclosure Controls

|

19

|

||

|

Management Report on Internal Control over Financial Reporting

|

19

|

||

|

Changes in Internal Control over Financial Reporting

|

20

|

||

|

Limitations on Effectiveness of Controls

|

20

|

||

|

PART III

|

20

|

||

|

Item 10

|

Directors and Executive Officers of the Registrant

|

20

|

|

|

Item 11

|

Executive Compensation

|

21

|

|

|

Item 12

|

Security ownership of Certain Beneficial Owners and Management

|

21

|

|

|

Item 13

|

Certain Relationships and Related Transactions

|

21

|

|

|

Item 14

|

Principal Accountant Fees and Services

|

21

|

|

|

PART IV

|

21

|

||

|

Item 15

|

Exhibits and Financial Statement Schedules

|

21

|

|

|

SIGNATURES

FINANCIAL STATEMENTS

|

23

|

||

|

F-1

|

|||

ROYALE ENERGY, INC.

PART I

Item 1 Description of Business

Royale Energy, Inc. ("Royale Energy") is an independent oil and natural gas producer. Royale Energy's principal lines of business are the production and sale of natural gas, acquisition of oil and gas lease interests and proved reserves, drilling of both exploratory and development wells, and sales of fractional working interests in wells to be drilled by Royale Energy. Royale Energy was incorporated in California in 1986 and began operations in 1988. Royale Energy's common stock is traded on the NASDAQ Capital Market System (symbol ROYL). On December 31, 2010, Royale Energy had 22 full time employees.

Royale Energy owns wells and leases located mainly in the Sacramento Basin and San Joaquin Basin in California as well as in Utah, Texas, Oklahoma, and Louisiana. Royale Energy usually sells a portion of the working interest in each lease that it acquires to third party investors and retains a portion of the prospect for its own account. Selling part of the working interest to others allows Royale Energy to reduce its drilling risk by owning a diversified inventory of properties with less of its own funds invested in each drilling prospect, than if Royale Energy owned the whole working interest and paid all drilling and development costs of each prospect itself. Royale Energy generally sells working interests in its prospects to accredited investors in exempt securities offerings. The prospects are bundled into multi-well investments, which permit the third party investors to diversify their investments by investing in several wells at once instead of investing in single well prospects.

During its fiscal year ended December 31, 2010, Royale Energy continued to explore and develop natural gas properties with a concentration in California. We also own proved developed producing and non-producing reserves of oil and natural gas in Utah, Texas, Oklahoma, and Louisiana. In 2010, Royale Energy drilled nine wells in northern and central California; five were commercially productive wells, one was not commercially productive and the remaining three were dry holes. Royale Energy's estimated total reserves increased from approximately 4.8 BCFE (billion cubic feet equivalent) at December 31, 2009 to approximately 5.9 BCFE at December 31, 2010. According to the reserve reports furnished to Royale Energy by Netherland, Sewell & Associates, Inc., and Source Energy, LLC, Royale Energy's independent petroleum engineers, the net reserve value of its proved developed and undeveloped reserves was approximately $15.7 million at December 31, 2010, based on natural gas prices ranging from $3.82 per MCF to $4.32 per MCF. Source Energy, LLC, supplied reserve value estimates for Royale Energy’s Utah properties, and Netherland, Sewell & Associates, Inc. provided reserve information for the Company’s California, Texas, Oklahoma, and Louisiana properties.

Of course, net reserve value does not represent the fair market value of our reserves on that date, and we cannot be sure what return we will eventually receive on our reserves. Net reserve value of proved developed and undeveloped reserves was calculated by subtracting estimated future development costs, future production costs and other operating expenses from estimated net future cash flows from our developed and undeveloped reserves.

Our standardized measure of discounted future net cash flows at December 31, 2010, was estimated to be $8,689,821. This figure was calculated by subtracting our estimated future income tax expense from the net reserve value of proved developed and undeveloped reserves, and by further applying a 10% annual discount for estimated timing of cash flows. A detailed calculation of our standardized measure of discounted future net cash flow is contained in Supplemental Information About Oil and Gas Producing Activities – Changes in Standardized Measure of Discounted Future Net Cash Flow from Proved Reserve Quantities, page F-30.

Royale Energy reported gross revenues in connection with the drilling of wells on a "turnkey contract" basis, or sales of fractional interests in undeveloped wells, in the amount of $7,868,273 for the year ended December 31, 2010, which represents approximately 68% of its total revenues for the year. In 2009, Royale Energy reported $5,061,804 gross revenues from turnkey drilling operations for the year, representing 59% of Royale Energy's total revenues for that year.

These amounts are offset by drilling expenses and development costs of $2,560,068 in 2010, and $2,146,904 in 2009. In addition to Royale Energy's own geological, land, and engineering staff, Royale Energy hires independent contractors to drill, test, complete and equip the wells that it drills.

1

Approximately 26% of Royale Energy's total revenue for the year ended December 31, 2010, came from sales of oil and natural gas from production of its wells in the amount of $3,047,201. In 2009, this amount was $2,800,557, which represented 32% of Royale Energy's total revenues.

Plan of Business

Royale Energy acquires interests in oil and natural gas reserves and sponsors private joint ventures. Royale Energy believes that its stockholders are better served by diversification of its investments among individual drilling prospects. Through its sale of joint ventures, Royale Energy can acquire interests and develop oil and natural gas properties with greater diversification of risk and still receive an interest in the revenues and reserves produced from these properties. By selling some of its working interest in most projects, Royale Energy decreases the amount of its investment in the projects and diversifies its oil and gas property holdings, to reduce the risk of concentrating a large amount of its capital in a few projects that may not be successful.

After acquiring the leases or lease participation, Royale Energy drills or participates in the drilling of development and exploratory oil and natural gas wells on its property. Royale Energy pays its proportionate share of the actual cost of drilling, testing, and completing the project to the extent that it retains all or any portion of the working interest.

Royale Energy also may sell fractional interests in undeveloped wells to finance part of the drilling cost. A drilling contract that calls for a company to drill a well, for a fixed price, to a specified depth or geological formation is called a "turnkey contract." When Royale Energy sells fractional interests to raise capital to drill oil and natural gas wells, generally it agrees to drill these wells on a turnkey contract basis, so that the holders of the fractional interests prepay a fixed amount for the drilling and completion of a specified number of wells. Under a turnkey contract, Royale Energy recognizes gross revenue for the amount paid by the purchaser and agrees to pay the expense of drilling and development of the well for the participants. Sometimes the actual drilling and development costs are less than the fixed amount that Royale Energy received from the fractional interest sale.

When Royale Energy authorizes a turnkey drilling project for sale, a calculation is made to estimate the pre-drilling costs and the drilling costs. A percentage for each is calculated. The turnkey drilling project is then sold to investors who execute a contract with Royale Energy. In this agreement, the investor agrees to share in the pre-drilling costs, which include lease costs, geological and geophysical costs, and other costs as required so that the drilling of the project can proceed. As stated in the contract, the percentage of the pre-drilling costs that the investor contributes is non-refundable, and thus on its financial statements, Royale Energy recognizes these non-refundable payments as revenue since the pre-drilling costs have commenced. The remaining investment is held and reported by Royale Energy as deferred turnkey drilling until drilling is complete.

Once drilling has commenced, it is generally completed within 10-30 days. See Note 1 to Royale Energy's Financial Statements, at page F-11. Royale Energy maintains internal records of the expenditure of each investor's funds for drilling projects.

Royale Energy generally operates the wells it completes. As operator, it receives fees set by industry standards from the owners of fractional interests in the wells and from expense reimbursements. For the year ended December 31, 2010, Royale Energy earned gross revenues from operation of the wells in the amount of $394,483, representing 3.4% of its total revenues on a consolidated basis for that year. In 2009, the amount was $388,736, which represented about 4.5% of total revenues. At December 31, 2010, Royale Energy operated 53 natural gas wells in California. Royale also owns an interest and operates seven natural gas wells in Utah and has non-operating interests in 12 oil and gas wells in Texas, three in Oklahoma, one in California, and two in Louisiana.

Royale Energy currently sells most of its California natural gas production through PG&E pipelines to independent customers on a monthly contract basis, while some gas is delivered through privately owned pipelines to independent customers. Since many users are willing to make such purchase arrangements, the loss of any one customer would not affect our overall sales operations.

All oil and natural gas properties are depleting assets in which production naturally decreases over time as the finite amount of existing reserves are produced and sold. It is Royale Energy’s business as an oil and natural gas exploration and production company to continually search for new development properties. The company’s success will ultimately depend on its ability to continue locating and developing new oil and natural gas resources.

2

Natural gas demand and the prices paid for gas are seasonal. In recent years, natural gas demand and prices in Northern California have fluctuated unpredictably throughout the year.

Royale Energy had no subsidiaries in 2010.

Competition, Markets and Regulation

Competition

The exploration and production of oil and natural gas is an intensely competitive industry. The sale of interests in oil and gas projects, like those Royale Energy sells, is also very competitive. Royale Energy encounters competition from other oil and natural gas producers, as well as from other entities which invest in oil and gas for their own account or for others, and many of these companies are substantially larger than Royale Energy.

Markets

Market factors affect the quantities of oil and natural gas production and the price Royale Energy can obtain for the production from its oil and natural gas properties. Such factors include: the extent of domestic production; the level of imports of foreign oil and natural gas; the general level of market demand on a regional, national and worldwide basis; domestic and foreign economic conditions that determine levels of industrial production; political events in foreign oil-producing regions; and variations in governmental regulations including environmental, energy conservation, and tax laws or the imposition of new regulatory requirements upon the oil and natural gas industry.

Regulation

Federal and state laws and regulations affect, to some degree, the production, transportation, and sale of oil and natural gas from Royale Energy’s operations. States in which Royale Energy operates have statutory provisions regulating the production and sale of oil and natural gas, including provisions regarding deliverability. These statutes, along with the regulations interpreting the statutes, generally are intended to prevent waste of oil and natural gas, and to protect correlative rights to produce oil and natural gas by assigning allowable rates of production to each well or proration unit.

The exploration, development, production and processing of oil and natural gas are subject to various federal and state laws and regulations to protect the environment. Various federal and state agencies are considering, and some have adopted, other laws and regulations regarding environmental controls that could increase the cost of doing business. These laws and regulations may require: the acquisition of a permit by operators before drilling commences; the prohibition of drilling activities on certain lands lying within wilderness areas or where pollution arises; and the imposition of substantial liabilities for pollution resulting from drilling operations, particularly operations in offshore waters or on submerged lands. The cost of oil and natural gas development and production also may increase because of the cost of compliance with such legislation and regulations, together with any penalties resulting from failing to comply with the legislation and regulations. Ultimately, Royale Energy may bear some of these costs.

Presently, Royale Energy does not anticipate that compliance with federal, state and local environmental regulations will have a material adverse effect on capital expenditures, earnings, or its competitive position in the oil and natural gas industry; however, changes in the laws, rules or regulations, or the interpretation thereof, could have a materially adverse effect on Royale Energy’s financial condition or results of operation.

Royale Energy files quarterly, yearly and other reports with the Securities Exchange Commission. You may obtain a copy of any materials filed by Royale Energy with the SEC at 450 Fifth Street, N.W., Washington, D.C. 20549, by calling 1-800-SEC-0300. The SEC also maintains an Internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC at http://www.sec.gov. Royale Energy also provides access to its SEC reports and other public announcements on its website, http://www.royl.com.

Item 1A Risk Factors

In addition to the other information contained in this report, the following risk factors should be considered in evaluating our business.

3

We Depend on Market Conditions and Prices in the Oil and Gas Industry.

Our success depends heavily upon our ability to market oil and gas production at favorable prices. In recent decades, there have been both periods of worldwide overproduction and underproduction of hydrocarbons and periods of increased and relaxed energy conservation efforts. As a result the world has experienced periods of excess supply of, and reduced demand for, crude oil on a worldwide basis and for natural gas on a domestic basis; these periods have been followed by periods of short supply of, and increased demand for, crude oil and, to a lesser extent, natural gas. The excess or short supply of oil and gas has placed pressures on prices and has resulted in dramatic price fluctuations.

Natural gas demand and the prices paid for gas are seasonal. The fluctuations in gas prices and possible new regulations create uncertainty about whether we can continue to produce gas for a profit.

Prices for oil and natural gas affect the amount of cash flow available for capital expenditures and our ability to borrow and raise additional capital. Lower prices may also reduce the amount of oil and natural gas that we can economically produce. Any substantial and extended decline in the price of oil or natural gas would decrease our cash flows, as well as the carrying value of our proved reserves, our borrowing capacity and our ability to obtain additional capital.

Variance in Estimates of Oil and Gas Reserves could be Material.

The process of estimating oil and gas reserves is complex, requiring significant decisions and assumptions in the evaluation of available geological, geophysical, engineering and economic data for each reservoir. As a result, such estimates are inherently imprecise. Actual future production, oil and gas prices, revenues, taxes, development expenditures, operating expenses and quantities of recoverable oil and gas reserves may vary substantially from those estimated in reserve reports that we periodically obtain from independent reserve engineers.

You should not construe the standardized measure of proved reserves contained in our annual report as the current market value of the estimated proved reserves of oil and gas attributable to our properties. In accordance with Securities and Exchange Commission requirements, we have based the standardized measure of future net cash flows from the standardized measure of proved reserves on the average price during the 12-month period before the ending date of the period covered by the report, whereas actual future prices and costs may vary significantly. The following factors may also affect actual future net cash flows:

|

·

|

the timing of both production and related expenses;

|

|

·

|

changes in consumption levels; and

|

|

·

|

governmental regulations or taxation.

|

In addition, the calculation of the standardized measure of the future net cash flows using a 10% discount as required by the Securities and Exchange Commission is not necessarily the most appropriate discount rate based on interest rates in effect from time to time and risks associated with our reserves or the oil and gas industry in general. Furthermore, we may need to revise our reserves downward or upward based upon actual production, results of future development, supply and demand for oil and gas, prevailing oil and gas prices and other factors.

Any significant variance in these assumptions could materially affect the estimated quantities and present value of our reserves. In addition, our standardized measure of proved reserves may be revised downward or upward, based upon production history, results of future exploration and development, prevailing oil and gas prices and other factors, many of which are beyond our control. Actual production, revenues, taxes, development expenditures and operating expenses with respect to our reserves will likely vary from the estimates used, and such variances may be material.

Future Acquisitions and Development Activities May Not Result in Additional Proved Reserves, and We May Not be Able to Drill Productive Wells at Acceptable Costs.

In general, the volume of production from oil and gas properties declines as reserves are depleted. Except to the extent that we acquire properties containing proved reserves or conduct successful development and exploration

4

activities, or both, our proved reserves will decline as reserves are produced. Our future oil and gas production is, therefore, highly dependent upon our ability to find or acquire additional reserves.

The business of acquiring, enhancing or developing reserves is capital intensive. We require cash flow from operations as well as outside investments to fund our acquisition and development activities. If our cash flow from operations is reduced and external sources of capital become limited or unavailable, our ability to make the necessary capital investment to maintain or expand our asset base of oil and gas reserves would be impaired.

The Oil and Gas Industry has Mechanical and Environmental Risks.

Oil and gas drilling and production activities are subject to numerous risks. These risks include the risk that no commercially productive oil or gas reservoirs will be encountered, that operations may be curtailed, delayed or canceled, and that title problems, weather conditions, compliance with governmental requirements, mechanical difficulties or shortages or delays in the delivery of drilling rigs and other equipment may limit our ability to develop, produce or market our reserves. New wells we drill may not be productive and we may not recover all or any portion of our investment in the well. Drilling for oil and gas may involve unprofitable efforts, not only from dry wells but also from wells that are productive but do not produce sufficient net revenues to return a profit after drilling, operating and other costs. In addition, our properties may be susceptible to hydrocarbon drainage from production by other operators on adjacent properties.

Industry operating risks include the risks of fire, explosions, blow outs, pipe failure, abnormally pressured formations and environmental hazards, such as oil spills, natural gas leaks, ruptures or discharges of toxic gases, the occurrence of any of which could result in substantial losses due to injury or loss of life, severe damage to or destruction of property, natural resources and equipment, pollution or other environmental damage, clean up responsibilities, regulatory investigation and penalties and suspension of operations. In accordance with customary industry practice, we maintain insurance for these kinds of risks, but we cannot be sure that our level of insurance will cover all losses in the event of a drilling or production catastrophe. Insurance is not available for all operational risks, such as risks that we will drill a dry hole, fail in an attempt to complete a well or have problems maintaining production from existing wells.

Drilling is a Speculative Activity Even With Newer Technology.

Assessing drilling prospects is uncertain and risky for many reasons. We have grown in the past several years by using 3-D seismic technology to acquire and develop exploratory projects in northern California, as well as by acquiring producing properties for further development. The successful acquisition of such properties depends on our ability to assess recoverable reserves, future oil and gas prices, operating costs, potential environmental and other liabilities and other factors.

Nevertheless, exploratory drilling remains a speculative activity. Even when fully utilized and properly interpreted, 3-D seismic data and other advanced technologies assist geoscientists in identifying subsurface structures but do not enable the interpreter to know whether hydrocarbons are in fact present. In addition, 3-D seismic and other advanced technologies require greater pre-drilling expenditures than traditional drilling strategies, and we could incur losses as a result of these costs.

Therefore, our assessment of drilling prospects are necessarily inexact and their accuracy inherently uncertain. In connection with such an assessment, we perform a review of the subject properties that we believe to be generally consistent with industry practices. Such a review, however, will not reveal all existing or potential problems, nor will it permit us to become sufficiently familiar with the properties to fully assess their deficiencies and capabilities.

Breaches of Contract by Sellers of Properties Could Adversely Affect Operations.

In most cases, we are not entitled to contractual indemnification for pre closing liabilities, including environmental liabilities, and we generally acquire interests in the properties on an "as is" basis with limited remedies for breaches of representations and warranties. In those circumstances in which we have contractual indemnification rights for pre-closing liabilities, the seller may not fulfill those obligations and leave us with the costs.

5

We May Not be Able to Acquire Producing Oil and Gas Properties Which Contain Economically Recoverable Reserves.

Competition for producing oil and gas properties is intense and many of our competitors have substantially greater financial and other resources than we do. Acquisitions of producing oil and gas properties may be at prices that are too high to be acceptable.

We Require Substantial Capital for Exploration and Development.

We make substantial capital expenditures for our exploration and development projects. We will finance these capital expenditures with cash flow from operations and sales of direct working interests to third party investors. We will need additional financing in the future to fund our developmental and exploration activities. Additional financing that may be required may not be available or continue to be available to us. If additional capital resources are not available to us, our developmental and other activities may be curtailed, which would harm our business, financial condition and results of operations.

Profit Depends on the Marketability of Production.

The marketability of our natural gas production depends in part upon the availability, proximity and capacity of natural gas gathering systems, pipelines and processing facilities. Most of our natural gas is delivered through natural gas gathering systems and natural gas pipelines that we do not own. Federal, state and local regulation of oil and gas production and transportation, tax and energy policies, and/or changes in supply and demand and general economic conditions could adversely affect our ability to produce and market its oil and gas. Any dramatic change in market factors could have a material adverse effect on our financial condition and results of operations.

We Depend on Key Personnel.

Our business will depend on the continued services of our co-presidents and co-chief executive officers, Donald H. Hosmer and Stephen M. Hosmer. Stephen Hosmer is also the chief financial officer. We do not have employment agreements with either Donald or Stephen Hosmer. The loss of the services of either of these individuals would be particularly detrimental to us because of their background and experience in the oil and gas industry.

The Hosmer Family Exerts Significant Influence Over Stockholder Matters.

The control positions held by members of the Hosmer family may discourage others from making bids to buy Royale Energy or change its management without their consent. Donald H. Hosmer is the co-president of the company. Stephen M. Hosmer is the co-president and chief financial officer. Harry E. Hosmer is the chairman of the board. Together, they make up three of the eight members of our board of directors. At December 31, 2010, these individuals owned or controlled the following amounts of Royale Energy common stock, including shares they had the right to acquire on the exercise of outstanding stock options:

|

Name

|

Number of Shares (1)

|

Percent (2), (3)

|

|

Donald H. Hosmer

|

977,159

|

9.42%

|

|

Stephen M. Hosmer (4)

|

1,254,256

|

12.11%

|

|

Harry E. Hosmer

|

794,626

|

7.67%

|

|

Total

|

3,026,041

|

28.74%

|

|

(1)

|

Includes the following options to purchase shares of stock: Donald H. Hosmer – 95,000, Stephen M. Hosmer – 80,000, and Harry E. Hosmer – 80,000.

|

|

(2)

|

Based on total of 10,274,731 outstanding shares on December 31, 2010.

|

|

(3)

|

Calculated pursuant to Rule 13d-3 of the Securities and Exchange Commission.

|

|

(4)

|

Includes 24,000 shares of stock owned by the minor children of Stephen M. Hosmer. Mr. Hosmer disclaims beneficial ownership of the shares owned by his children.

|

The amounts of stock owned by Hosmer family members make it quite likely that they could control the outcome of any contested vote of the stockholders on matters related to management of the corporation.

6

The Oil and Gas Industry is Highly Competitive.

The oil and gas industry is highly competitive in all its phases. Competition is particularly intense with respect to the acquisition of desirable producing properties, the acquisition of oil and gas prospects suitable for enhanced production efforts, and the hiring of experienced personnel. Our competitors in oil and gas acquisition, development, and production include the major oil companies in addition to numerous independent oil and gas companies, individual proprietors and drilling programs.

Many of our competitors possess and employ financial and personnel resources far greater than those which are available to us. They may be able to pay more for desirable producing properties and prospects and to define, evaluate, bid for, and purchase a greater number of producing properties and prospects than we can. We must compete against these larger companies for suitable producing properties and prospects, to generate future oil and gas reserves.

Governmental Regulations Can Hinder Production.

Domestic oil and gas exploration, production and sales are extensively regulated at both the federal and state levels. Legislation affecting the oil and gas industry is under constant review for amendment or expansion, frequently increasing the regulatory burden. Also, numerous departments and agencies, both federal and state, have legal authority to issue, and have issued, rules and regulations affecting the oil and gas industry which often are difficult and costly to comply with and which carry substantial penalties for noncompliance. State statutes and regulations require permits for drilling operations, drilling bonds, and reports concerning operations. Most states where we operate also have statutes and regulations governing conservation matters, including the unitization or pooling of properties. Our operations are also subject to numerous laws and regulations governing plugging and abandonment, discharging materials into the environment or otherwise relating to environmental protection. The heavy regulatory burden on the oil and gas industry increases its costs of doing business and consequently affects its profitability. Changes in the laws, rules or regulations, or the interpretation thereof, could have a materially adverse effect on our financial condition or results of operation.

Minority or Royalty Interest Purchases Do Not Allow Us to Control Production Completely.

We sometimes acquire less than the controlling working interest in oil and gas properties. In such cases, it is likely that these properties would not be operated by us. When we do not have controlling interest, the operator or the other co-owners might take actions we do not agree with and possibly increase costs or reduce production income in ways we do not agree with.

Environmental Regulations Can Hinder Production.

Oil and gas activities can result in liability under federal, state and local environmental regulations for activities involving, among other things, water pollution and hazardous waste transport, storage, and disposal. Such liability can attach not only to the operator of record of the well, but also to other parties that may be deemed to be current or prior operators or owners of the wells or the equipment involved. We have inspections performed on our properties to assure environmental law compliance, but inspections may not always be performed on every well, and structural and environmental problems are not necessarily observable even when an inspection is undertaken.

Item 2 Description of Property

Since 1993, Royale Energy has concentrated on development of properties in the Sacramento Basin and the San Joaquin Basin of Northern and Central California. In 2010, Royale Energy drilled nine wells in northern and central California, five of which were commercially productive wells, four are currently producing and one is awaiting pipeline hookup.

Following industry standards, Royale Energy generally acquires oil and natural gas acreage without warranty of title except as to claims made by, through, or under the transferor. In these cases, Royale Energy attempts to conduct due diligence as to title before the acquisition, but it cannot assure that there will be no losses resulting from title defects or from defects in the assignment of leasehold rights. Title to property most often carries encumbrances, such as royalties, overriding royalties, carried and other similar interests, and contractual obligations, all of which are customary within the oil and natural gas industry.

7

During 2010, Royale Energy maintained a revolving credit agreement with Texas Capital Bank, N.A.. Under the terms of the agreement, Royale Energy may borrow, repay, and reborrow money from Texas Capital Bank with a total credit line of $14,250,000. The maximum allowable amount of each credit request is governed by a formula in the agreement. The maximum allowable amount at December 31, 2010, was $3,200,000. At December 31, 2010, Royale Energy owed $3,200,000 under this credit line. Royale uses advances under this credit line to finance lease acquisition operations and for temporary working capital. Following is a discussion of Royale Energy's significant oil and natural gas properties. Reserves at December 31, 2010, for each property discussed below, have been determined by Netherland, Sewell & Associates, Inc., and Source Energy, LLC, registered professional petroleum engineers, in accordance with reports submitted to Royale Energy on February 18, 2011 and February 23, 2011, respectively.

Northern California

Royale Energy owns lease interests in eleven gas fields with locations ranging from Tehama County in the north to Kern County in the south, in the Sacramento and San Joaquin Basins in California. At December 31, 2010, Royale operated 53 wells in California with estimated total proven, developed, and undeveloped reserves at approximately 5.1 BCF, according to Royale’s independently prepared reserve report as of December 31, 2010.

Developed and Undeveloped Leasehold Acreage

As of December 31, 2010, Royale Energy owned leasehold interests in the following developed and undeveloped properties in both gross and net acreage.

|

Developed

|

Undeveloped

|

|||

|

Gross Acres

|

Net Acres

|

Gross Acres

|

Net Acres

|

|

|

California

|

13,606.94

|

9,032.93

|

12,430.17

|

11,555.48

|

|

All Other States

|

4,275.30

|

1,794.83

|

19,322.43

|

13,988.75

|

|

Total

|

17,882.24

|

10,827.76

|

31,752.60

|

25,544.23

|

Drilling Activities

The following table sets forth Royale Energy's drilling activities during the years ended December 31, 2008, 2009 and 2010. All wells are located in the Continental U.S., in California, Texas, Louisiana and Utah.

|

Year

|

Type of Well(a)

|

Gross Wells(e)

|

Net Wells(b)

|

|||

|

Total

|

Producing(c)

|

Dry(d)

|

Producing(c)

|

Dry(d)

|

||

|

2008

|

Exploratory

|

2

|

1

|

1

|

0.4985

|

0.1238

|

|

Developmental

|

5

|

4

|

1

|

1.9441

|

0.0000

|

|

|

2009

|

Exploratory

|

3

|

2

|

1

|

0.9715

|

0.2468

|

|

Developmental

|

2

|

1

|

1

|

0.4982

|

0.5369

|

|

|

2010

|

Exploratory

|

7

|

5

|

2

|

2.0087

|

0.5686

|

|

Developmental

|

2

|

1

|

1

|

0.7599

|

0.5003

|

|

|

a)

|

An exploratory well is one that is drilled in search of new oil and natural gas reservoirs, or to test the boundary limits of a previously discovered reservoir. A developmental well is one drilled on a previously known productive area of an oil and natural gas reservoir with the objective of completing that reservoir.

|

|

b)

|

Gross wells represent the number of actual wells in which Royale Energy owns an interest. Royale Energy's interest in these wells may range from 1% to 100%.

|

|

c)

|

A producing well is one that produces oil and/or natural gas that is being purchased on the market.

|

|

d)

|

A dry well is a well that is not deemed capable of producing hydrocarbons in paying quantities.

|

|

e)

|

One "net well" is deemed to exist when the sum of fractional ownership working interests in gross wells or acres equals one. The number of net wells is the sum of the fractional working interests owned in gross wells expressed as a whole number or a fraction.

|

8

Production

The following table summarizes, for the periods indicated, Royale Energy's net share of oil and natural gas production, average sales price per barrel (BBL), per thousand cubic feet (MCF) of natural gas, and the MCF equivalent (MCFE) for the barrels of oil based on a 10 to 1 ratio of the price per barrel of oil to the price per MCF of natural gas. "Net" production is production that Royale Energy owns either directly or indirectly through partnership or joint venture interests produced to its interest after deducting royalty, limited partner or other similar interests. Royale Energy generally sells its oil and natural gas at prices then prevailing on the "spot market" and does not have any material long term contracts for the sale of natural gas at a fixed price.

|

2010

|

2009

|

2008

|

||||

|

Net volume

|

||||||

|

Oil (BBL)

|

6,511

|

8,364

|

11,089

|

|||

|

Gas (MCF)

|

603,330

|

575,995

|

714,230

|

|||

|

MCFE

|

668,440

|

659,635

|

825,120

|

|||

|

Average sales price

|

||||||

|

Oil (BBL)

|

$

|

70.95

|

$

|

52.92

|

$

|

95.04

|

|

Gas (MCF)

|

$

|

4.28

|

$

|

4.09

|

$

|

8.32

|

|

Net production costs and taxes

|

$

|

1,221,904

|

$

|

1,415,970

|

$

|

2,906,325

|

|

Lifting costs (per MCFE)

|

$

|

1.83

|

$

|

2.15

|

$

|

3.52

|

Net Proved Oil and Natural Gas Reserves

As of December 31, 2010, Royale Energy had proved developed reserves of 5,041 MMCF and total proved reserves of 5,734 MMCF of natural gas on all of the properties Royale Energy leases. For the same period, Royale Energy also had proved developed oil reserves of 17 MBBL and total proved oil reserves of 17 MBBL.

Oil and gas reserve estimates and the discounted present value estimates associated with the reserve estimates are based on numerous engineering, geological and operational assumptions that generally are derived from limited data.

Item 3 Legal Proceedings

National Fuel Corporation (“NFC”) v. Royale Energy, Inc., No. 080800735, Uintah County, Utah. NFC filed the current lawsuit seeking to challenge a settlement agreement from a prior lawsuit over management of property in which Royale is the 75% owner and operator and NFC is a non-operator with a 25% ownership. The last actions taken were depositions performed by each party. The case remains active and the Company intends to defend itself vigorously.

Mountain West Oil Field Services and Supplies, Inc. (Mountain West) v. Royale Energy, Inc., No. 2:10-cv-00865DN, United States District Court in Salt Lake City, Utah. The litigation involves actions for breach of contract for alleged failure to timely pay Mountain West, an oilfield service company, breach of implied covenant of good faith and fair dealing, unjust enrichment, promissory estoppels, and attorney’s fees and costs. Plaintiff has specified the amount of damages to be $355,850, together with interest, court costs and attorney’s fees as provided for by law. The case has been pending since August 31, 2010 and remains active. The Company intends to defend itself vigorously, but has set aside a portion of the claimed amount.

Douglas Jones v. Royale Energy, Inc., et.al.

On July 1, 2010, Douglas Jones filed a lawsuit against the Company in the Circuit Court, 17th Judicial District, Broward County, Florida. Mr. Jones was an independent contractor handling certain aspects of sales for the Company prior to July 2, 2008. He asserts that he is entitled to an unspecified amount for commissions and

9

expenses. The Company denies that any money is owed to Mr. Jones, and intends to defend the lawsuit vigorously. On August 16, 2010, the Company filed a motion to dismiss the lawsuit for lack of jurisdiction in the Florida courts. No date has been set for a hearing on the motion, and no opposition has been filed. Nothing further has occurred in the action, and no discovery has taken place.

PART II

Item 5 Market for Common Equity and Related Stockholder Matters

Since 1997 Royale Energy's Common Stock has been traded on the Nasdaq National Market System under the symbol "ROYL." On April 1, 2009, Nasdaq notified Royale that it was not in compliance with the requirement that companies listed on the Nasdaq Global Market are required by Marketplace Rule 4450(a)(3) to maintain a minimum of $10 million in stockholders’ equity for continued listing. Effective July 31, 2009, Royale transferred its securities listing from the Nasdaq Global Market to the Nasdaq Capital Market. Royale complies with the Capital Market listing requirements. As of December 31, 2010, 10,274,731 shares of Royale Energy's Common Stock were held by approximately 4,850 stockholders. The following table reflects high and low quarterly closing sales prices from January 2009 through December 2010. Share prices in this table have been adjusted to give effect to the issuance of stock dividends in 2003, 2004 and 2005, and a stock split in 2004.

|

1st Qtr

|

2nd Qtr

|

3rd Qtr

|

4th Qtr

|

||||||||

|

High

|

Low

|

High

|

Low

|

High

|

Low

|

High

|

Low

|

||||

|

2010

|

3.06

|

2.07

|

2.50

|

1.92

|

2.26

|

1.83

|

2.42

|

1.98

|

|||

|

2009

|

3.36

|

1.40

|

3.77

|

1.88

|

2.55

|

1.89

|

3.69

|

1.99

|

|||

Dividends

The Board of Directors did not issue cash or stock dividends in 2010 or 2009.

Recent Sales of Unregistered Securities

In March 2008, Royale Energy awarded options to purchase 45,000 shares of common stock at $3.50 per share (the fair market value of Royale’s common stock on the date of grant) to each of its eight directors (a total of 360,000 shares). In June 2008, three directors exercised their options to acquire a total of 36,844 shares during 2008. The options were issued and the stock was purchased in reliance on the exemption from registrations requirements of the Securities Act of 1933 contained in Section 4(2) thereof.

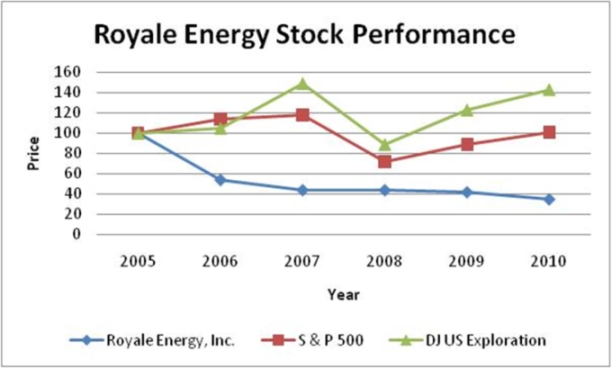

Performance Graph

The following stock price performance graph is included in accordance with the SEC’s executive compensation disclosure rules and is intended to allow stockholders to review Royale Energy’s executive compensation policies in light of corresponding stockholder returns, expressed in terms of the appreciation of Royale Energy’s common stock relative to two broad-based stock performance indices. The information is included for historical comparative purposes only and should not be considered indicative of future stock performance. The graph compares total return on $100 value of Royale Energy’s common stock on December 31, 2005, with the cumulative total return of the Standard & Poor’s Composite 500 Stock Index and the Dow Jones U.S. Exploration and Production Index from December 31, 2005 through December 31, 2010.

|

2005

|

2006

|

2007

|

2008

|

2009

|

2010

|

|

|

Royale Energy, Inc.

|

100

|

54

|

44

|

44

|

42

|

35

|

|

S & P Composite 500 Stock Index

|

100

|

114

|

118

|

72

|

89

|

101

|

|

DJ US Exploration and Production Index

|

100

|

105

|

149

|

89

|

123

|

143

|

Item 6 Selected Financial Data

(In thousands, except earnings per share data)

As of December 31,

|

2010

|

2009

|

2008

|

2007

|

2006

|

|

|

Income Statement Data:

|

|||||

|

Revenues

|

$ 11,598

|

$ 8,626

|

$ 19,174

|

$ 16,557

|

$ 24,896

|

|

Operating Income (Loss)

|

1,153

|

(3,147)

|

(14,362)

|

(3,885)

|

(3,189)

|

|

Net Income (Loss)

|

1,308

|

(2,197)

|

(8,778)

|

(2,779)

|

(2,650)

|

|

Basic Earnings Per Share

|

0.12

|

(0.24)

|

(1.06)

|

(0.35)

|

(0.33)

|

|

Balance Sheet Date:

|

|||||

|

Oil & Gas Properties,

Equipment & Fixtures

|

$ 10,258

|

$ 8,800

|

$ 10,264

|

$ 23,390

|

$ 20,526

|

|

Total Assets

|

23,820

|

23,564

|

24,191

|

32,571

|

33,715

|

|

Long Term Obligations

|

3,781

|

2,954

|

2,470

|

6,159

|

5,757

|

|

Total Stockholders’ Equity

|

10,938

|

10,127

|

7,394

|

12,385

|

15,548

|

Item 7 Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion should be read in conjunction with Royale Energy’s Financial Statements and Notes thereto and other financial information relating to Royale Energy included elsewhere in this document.

For the past seventeen years, Royale Energy has primarily acquired and developed producing and non-producing natural gas properties in California. In 2004, Royale Energy began developing leases in Utah. The most significant factors affecting the results of operations are (i) changes in oil and natural gas production levels and reserves, (ii) recording of turnkey drilling revenues and the associated drilling expense, and (iii) the change in commodities price of natural gas and oil reserves owned by Royale Energy.

11

Critical Accounting Policies

Revenue Recognition

Royale Energy’s financial statements include its pro rata ownership of wells. Royale Energy usually sells a portion of the working interest in each lease that it acquires to third party investors and retains a portion of the prospect for its own account. Royale Energy generally retains about a 50% working interest. All results, successful or not, are included at its pro rata ownership amounts: revenue, expenses, assets, and liabilities.

Royale Energy has developed two profit-oriented segments of business: marketing direct working interests (DWI), and producing and selling oil and gas.

Royale Energy derives DWI revenue from sales of working interests to high net worth individuals. The DWI revenue is divided into payments for pre-drilling costs and for drilling costs. DWI investments are non-refundable. Royale Energy recognizes the pre-drilling revenue portion when the investor deposits money with Royale Energy. The company holds the remaining investment in trust as deferred turnkey drilling until drilling is complete. Occasionally, drilling is delayed due to the permitting process or drilling rig availability. At December 31, 2010 and 2009, Royale Energy had deferred turnkey drilling of $3,866,319 and $4,979,605, respectively.

The primary business segment is oil and gas production. Northern and central California account for approximately 98% of the company’s successful natural gas production in 2010. Natural gas flows from the wells into gathering line systems, which are equipped occasionally with compressor systems, which in turn flow into metered transportation and customer pipelines. Monthly, price data and daily production are used to invoice customers for amounts due to Royale Energy and other working interest owners. Royale Energy operates virtually all of its own wells and receives industry standard operator fees.

Oil and Gas Property and Equipment

Royale Energy follows the successful efforts method of accounting for oil and gas properties. Costs are accumulated on a field-by-field basis. These costs include pre-drilling activities such as leasing rents paid, drilling costs, and post-drilling tangible costs. Costs of unproved properties are excluded from amortization until the properties are evaluated. Royale Energy regularly evaluates its unproved properties on a field-by-field basis for possible impairment. Due to the unpredictable nature of exploration drilling activities, the amount and timing of impairment expenses are difficult to predict with any certainty.

Depletion

The units of production method of accounting uses proved reserves in the calculation of depletion, depreciation and amortization. Proved reserves are estimated quantities of crude oil, natural gas, and natural gas liquids which geological and engineering data demonstrate with reasonable certainty to be recoverable from known reservoirs under existing economic and operating conditions. Proved reserves cannot be measured exactly, and the estimation of reserves involves judgment determinations. Independent engineering reserve estimates must be reviewed and adjusted periodically to reflect additional information gained from reservoir performance, new geological and geophysical data and economic changes. The estimates are based on current technology and economic conditions, and Royale Energy considers such estimates to be reasonable and consistent with current knowledge of the characteristics and extent of production. The independent engineering estimates include only those amounts considered to be proved reserves and do not include additional amounts which may result from new discoveries in the future, or from application of secondary and tertiary recovery processes where facilities are not in place or for which transportation and/or marketing contracts are not in place. Changes in previous estimates of proved reserves result from new information obtained from production history and changes in economic factors.

Impairment Of Assets

Producing property costs are evaluated for impairment and reduced to fair value if the sum of expected undiscounted future cash flows is less than net book value pursuant to the Extractive Activities Topic of the Financial Accounting Standard Board’s (FASB) Accounting Standards Codification. Impairment of non-producing leasehold costs and undeveloped mineral and royalty interests are assessed periodically on a property-by-property basis and any impairment in value is charged to expense. We periodically review for impairment of proved properties on a field

12

by-field basis. Unamortized capital costs are measured on a field basis and are reduced to fair value if it is determined that the sum of expected future net cash flows are less than the net book value. We determine if impairment has occurred through either adverse changes or as a result of its periodic review for impairment. Impairment is measured on undiscounted cash flows. We regard impairment costs of undeveloped properties as a component of our turnkey drilling overhead, since impairment costs amount to a write-down of previously acquired property inventory that we were unable to successfully develop as part of our turnkey drilling program.

Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. The most significant estimates pertain to proved oil, plant products and gas reserve volumes and the future development costs. Actual results could differ from those estimates.

Deferred Income Taxes

Deferred income taxes reflect the net tax effects, calculated at currently enacted rates, of (a) future deductible/taxable amounts attributable to events that have been recognized on a cumulative basis in the financial statements or income tax returns, and (b) operating loss and tax credit carry forwards. A valuation allowance for deferred tax assets is recorded when it is more likely than not that the benefit from the deferred tax asset will not be realized.

Results of Operations for the Twelve Months Ended December 31, 2010, as Compared to the Twelve Months Ended December 31, 2009

For the year ended December 31, 2010, we achieved a net profit of $1,308,028, a $3,505,171 improvement when compared to our net loss of $2,197,143 during 2009. This improvement was primarily due to higher turnkey drilling revenues due to an increase in the number of wells drilled during 2010. Total revenues from operations for the year in 2010 were $11,598,440, an increase of $2,972,855, or 34.5%, from the total revenues of $8,625,585 in 2009, also the result of higher turnkey drilling revenues.

In 2010, revenues from oil and gas production increased by 8.8% to $3,047,201 from $2,800,557 in 2009, due to slight increases in both production and the commodity prices received for our oil and natural gas production. The net sales volume of natural gas for the year ended December 31, 2010, was approximately 603,330 MCF with an average price of $4.28 per MCF, versus 575,995 MCF with an average price of $4.09 per MCF for 2009. This represents an increase in net sales volume of 27,335 MCF or 4.7%. This increase was due to higher production volumes of wells drilled and put online during the later part of the year. The net sales volume for oil and condensate (natural gas liquids) production was approximately 6,511 barrels with an average price of $70.95 per barrel for the year ended December 31, 2010, compared to 8,364 barrels at an average price of $52.92 per barrel for the year in 2009. This represents a decrease in net sales volume of 1,853 barrels, or 22.2%.

Oil and gas lease operating expenses decreased by $194,066, or 13.7%, to $1,221,904 for the year ended December 31, 2010, from $1,415,970 for the year in 2009. This decrease was mainly due to continuing cost control measures, lower workover costs and other reduced lease operating costs during 2010. When measuring lease operating costs on a production or lifting cost basis, in 2010, the $1,221,904 equates to a $1.83 per MCFE lifting cost versus a $2.15 per MCFE lifting cost in 2009, a 14.9% decrease.

For the year ended December 31, 2010, turnkey drilling revenues increased $2,806,469 to $7,868,273 from $5,061,804 in 2009, or 55.4%. We also had a $413,164 or 19.2% increase in turnkey drilling and development costs to $2,560,068 in 2010 from $2,146,904 in 2009. In 2010 we drilled nine wells, seven exploratory wells and two developmental wells versus five wells, three exploratory wells and two developmental wells in 2009. Our gross margins, or profits, on drilling depend on our ability to accurately estimate the costs associated with the development of projects in which we sell working interests and to acquire viable properties that can be successfully developed. Costs associated with contract drilling depend on location, well depth, weather, and availability of drilling contractors and equipment. Our gross margin on drilling increased to 67.5% from 57.6% for the years ended December 31, 2010 and 2009, respectively. Gross margin is calculated as the difference between turnkey drilling revenue and turnkey drilling expense. However, management believes that a portion of its impairment losses should

13

also be considered as a cost of drilling in determining the profitability of this segment, because impairment costs are incurred in the selection of higher quality prospects for ultimate development.

Impairment losses of $500,144 and $1,935,861 were recorded in 2010 and 2009, respectively. In both years, we recorded impairments in fields where year end reserve values were less than the net book values of wells or where lease and land costs that were no longer viable. In 2010, the River Island field was impaired $233,521 due to lower proved producing reserves than current book values. Additionally, two other California fields, Dunnigan Hills, and Rio Vista were impaired $22,118 and $17,931, respectively, also due to lower proved producing reserves than current book values. Our Bowerbank field in California was impaired $24,680 due to lower proved undeveloped reserves than current book values. In 2009, the majority of the impairment, $1,124,293, was recorded in our Utah fields, where various recently drilled wells had significantly lower proved developed nonproducing reserves than originally estimated. Much of these were costs carried over from wells drilled in 2008. Our Elkhorn Slough and East Rice Creek fields, both in California, were impaired $341,098 and $205,173, respectively, due to lower proved producing reserves than their current book values. Two other California fields, the Rio Vista and Bowerbank, were impaired $74,124 and $71,975, respectively, due to lower proved undeveloped reserves than originally estimated. Additionally in 2010 and 2009, we recorded lease impairments of $201,883 and $112,165, respectively, on various capitalized lease and land costs that were no longer viable.

Bad debt expense for 2010 and 2009 were $43,153 and $255,478, respectively. These expenses arose from identified uncollectable receivables relating to our oil and natural gas properties either plugged and abandoned or scheduled for plugging and abandonment. In 2010 and 2009, approximately 79% and 78%, respectively, of these expenses arose from two of our California wells. We periodically review our accounts receivable from working interest owners to determine whether collection of any of these charges where doubtful. By contract, the Company may not collect some charges from its Direct Working Interest owners for certain wells that ceased production or had been sold during the year, to the extent that these charges exceed production revenue. As a result of those reviews in 2009 we increased the allowance $49,699 for receivables from these Direct Working Interest owners. There were no such increases in 2010.

The aggregate of supervisory fees and other income was $682,966 for the year ended December 31, 2010, a decrease of $80,258 (10.5%) from $763,224 during the year in 2009. This decrease was mainly due to the 2009 granting of a seismic license to an industry member for which we were compensated. Supervisory fees are charged in accordance with the Council for Petroleum Accountants Societies (COPAS) policy for reimbursement of expenses associated with the joint accounting for billing, revenue disbursement, and payment of taxes and royalties. These charges are reevaluated each year and adjusted up or down as deemed appropriate by a published report to the industry by Ernst & Young, LLP, Certified Public Accountants. Supervisory fees increased $5,747 or 1.5%, to $394,483 in 2010 from $388,736 in 2009.

Depreciation, depletion and amortization expense decreased to $919,355 from $989,716 a decrease of $70,361 (7.1%) for the year ended December 31, 2010, as compared to 2009. The depletion rate is calculated using production as a percentage of reserves. This decrease in depletion expense was mainly due to the decrease in our oil and gas asset base from our 2009 impairments.

General and administrative expenses increased by $454,554 or 12.8%, from $3,546,816 for the year ended December 31, 2009, to $4,001,370 for the year in 2010. This increase was primarily due to higher employee related expenses such as salaries, taxes and insurances. Legal and accounting expense decreased to $574,384 for the year, compared to $717,173 for 2009, a $142,789 or 19.9% decrease. This decrease stems from higher legal fees incurred during the first two quarters of 2009 pertaining to the Pioneer litigation.

Marketing expense for the year ended December 31, 2010, decreased $188,616 or 23.3%, to $621,531, compared to $810,147 for the year in 2009. Marketing expense usually varies from period to period according to the number of marketing events attended by personnel and their associated costs. In 2010, our cost containment measures led to decreases primarily in exhibition costs.

In 2010, we recorded a loss of $3,310 on the sales of non-oil and gas assets. In 2009, we recorded a gain on the sales of assets of $45,611 that can be primarily attributable to a reconciling adjustment gain of $170,713 from our 2008 Rio Bravo sale and a loss from the sale of marketable securities of $120,219.

During the second quarter of 2010, we received title to securities stemming from a litigation settlement received approximately 10 years ago; the securities at that time had an undeterminable value. In June 2010, Royale began to

14

liquidate its position and during the third quarter had fully liquidated its position. For 2010, the Company has recognized a net unrealized holding loss of $676,563 in the other comprehensive income section of the Statement of Operations, and a realized gain of $907,679 from the complete liquidation of these securities in the other income section of the Statement of Operations.

During 2010, interest expense decreased to $46,613 from $101,675 in 2009, a $55,062 or 54.2% decrease. This was due to a decrease in the usage of our bank line of credit. Further details concerning Royale’s line of credit usage can be found in the Capital Resources and Liquidity section below.

In 2010, we had income tax expense of $706,259 due to our net profit before taxes of $2,014,287. In 2009, we had an income tax benefit of $1,051,401 due to our net loss before taxes of $3,248,544. For 2009, the use of percentage depletion created from the current operations, and from utilization of unused percentage depletion carryforwards, results in an effective tax rate less than the normal federal rate of 34% plus the relevant state rates (mostly California, 9.3%).

Results of Operations for the Twelve Months Ended December 31, 2009, as Compared to the Twelve Months Ended December 31, 2008

For the year ended December 31, 2009, we had a net loss of $2,197,143, a $6,580,471 improvement when compared to the net loss of $8,777,614 during 2008. This improvement was due to Company wide efforts to control and reduce costs. Total revenues from operations for the year in 2009 were $8,625,585, a decrease of $10,548,529, or 55%, from the total revenues of $19,174,114 in 2008. This decrease in revenues was due to several factors, including the industry wide decline in oil and natural gas commodity prices which affected our oil and natural gas production revenues, and decreased turnkey drilling revenues due to lower direct working interest sales. Although revenues decreased expenses also decreased. Total costs and expenses fell from $36,084,449 in 2008 to $11,818,065 in 2009, a $24,266,384 or 67% decrease. The decreased costs and expenses also translated into a 78% decrease in the Company’s loss from operations from $14,362,885 in 2008 to $3,146,869 in 2009, an $11,216,016 decrease.

In 2009, revenues from oil and gas production decreased by 60% to $2,800,557 from $6,999,022 in 2008, due to lower commodity prices received for our oil and natural gas production. The net sales volume of natural gas for the year ended December 31, 2009, was approximately 575,995 MCF with an average price of $4.09 per MCF, versus 714,230 MCF with an average price of $8.32 per MCF for 2008. This represents a decrease in net sales volume of 138,235 MCF or 19.4%. This decrease in production was due to a natural decline in production from existing oil and gas wells. The net sales volume for oil and condensate (natural gas liquids) production was approximately 8,364 barrels with an average price of $52.92 per barrel for the year ended December 31, 2009, compared to 11,089 barrels at an average price of $95.04 per barrel for the year in 2008. This represents a decrease in net sales volume of 2,725 barrels, or 24.6%.

Oil and gas lease operating expenses decreased by $1,490,355, or 51.3%, to $1,415,970 for the year ended December 31, 2009, from $2,906,325 for the year in 2008. This decrease was mainly due to lower workover and plugging and abandonment costs, as cost reduction measures were implemented in 2009. When measuring lease operating costs on a production or lifting cost basis, in 2009, the $1,415,970 equates to a $2.15 per MCFE lifting cost versus a $3.52 per MCFE lifting cost in 2008, a 39% decrease.

For the year ended December 31, 2009, turnkey drilling revenues decreased $6,410,261 to $5,061,804 in 2009 from $11,472,065 in 2008, or 55.9%. We also had a $3,868,486 or 64.3% decrease in turnkey drilling and development costs to $2,146,904 in 2009 from $6,015,390 in 2008. In 2009 we drilled five wells, three exploratory wells and two developmental wells versus two exploratory wells and five developmental wells in 2008. Our gross margins, or profits, on drilling depend on our ability to accurately estimate the costs associated with the development of projects in which we sell working interests and to acquire viable properties that can be successfully developed. Costs associated with contract drilling depend on location, well depth, weather, and availability of drilling contractors and equipment. Our gross margin on drilling increased to 57.6% from 47.6% for the years ended December 31, 2009 and 2008, respectively. Gross margin is calculated as the difference between turnkey drilling revenue and turnkey drilling expense. However, management believes that a portion of its impairment losses should also be considered as a cost of drilling in determining the profitability of this segment, because impairment costs are incurred in the selection of higher quality prospects for ultimate development.

15

Impairment losses of $1,935,861 and $15,691,348 were recorded in 2009 and 2008, respectively. In both years, we recorded impairments in fields where year end reserve values were less than the net book values of wells or where lease and land costs that were no longer viable. In 2009, the majority of the impairment, $1,124,293, was recorded in our Utah fields, where various recently drilled wells had significantly lower proved developed nonproducing reserves than originally estimated. Much of these were costs carried over from wells drilled in 2008. Our Elkhorn Slough and East Rice Creek fields, both in California, were impaired $341,098 and $205,173, respectively, due to lower proved producing reserves than their current book values. Two other California fields, the Rio Vista and Bowerbank, were impaired $74,124 and $71,975, respectively, due to lower proved undeveloped reserves than originally estimated. In 2008, $9,508,294 of this impairment was recorded in our Utah field where the weather delays caused lower than expected production to support the proved reserves values that were lower than their current net book values. The Texas and Gulf Coast fields were impaired $4,950,417, of which $1,936,390 was due to wells which had lower proved reserve values than their current net book values and $3,014,027 was due to previously capitalized lease and land costs which were not expected to be developed within the current year. We impaired two wells in California. One drilled in 2008 was impaired for $348,376, and the other a workover was impaired $340,129, due to lower reserves. Two fields in California, the Elkhorn Slough and Bowerbank, were impaired $284,379 and $100,436, respectively due to lower proved reserves than their current book values. Additionally in 2009 and 2008, we recorded lease impairments of $112,165 and $827,888, respectively, on various capitalized lease and land costs that were no longer viable.

Bad debt expense for 2009 and 2008 was $255,478 and $567,521, respectively. These expenses arose from identified uncollectable receivables relating to our oil and natural gas properties either plugged and abandoned or scheduled for plugging and abandonment. In 2009, approximately 78% of these expenses stem from one of our California wells. We periodically review our accounts receivable from working interest owners to determine whether collection of any of these charges where doubtful. By contract, the Company may not collect some charges from its Direct Working Interest owners for certain wells that ceased production or had been sold during the year, to the extent that these charges exceed production revenue. As a result of those reviews in 2009 and 2008, we increased the allowance from $973,319 at December 31, 2008 to $1,019,018 at December 31, 2009, for receivables from these Direct Working Interest owners.

The aggregate of supervisory fees and other income was $763,224 for the year ended December 31, 2009, an increase of $60,197 (8.6%) from $703,027 during the year in 2008. This increase was mainly due to the granting of a seismic license to an industry member for which we were compensated. Supervisory fees are charged in accordance with the Council for Petroleum Accountants Societies (COPAS) policy for reimbursement of expenses associated with the joint accounting for billing, revenue disbursement, and payment of taxes and royalties. These charges are reevaluated each year and adjusted up or down as deemed appropriate by a published report to the industry by Ernst & Young, LLP, Public Accountants. Supervisory fees decreased $3,582 or 1%, to $388,736 in 2009 from $392,318 in 2008.

Depreciation, depletion and amortization expense decreased to $989,716 from $4,148,415 a decrease of $3,158,699 (76.1%) for the year ended December 31, 2009, as compared to 2008. The depletion rate is calculated using production as a percentage of reserves. This decrease in depletion expense was mainly due to the decrease in our oil and gas asset base from our 2008 impairments.

General and administrative expenses decreased by $835,646 or 19.1%, from $4,382,462 for the year ended December 31, 2008 to $3,546,816 for the year in 2009. This decrease was primarily due to reductions in employee related expenses such as salaries, taxes and insurances, implemented in our cost control measures. Legal and accounting expense decreased to $717,173 for the year, compared to $1,211,989 for 2008, a $494,816 or 40.8% decrease. This decrease was a result of lower legal fees due to litigation defending property rights in 2008, which culminated in a trial and a successful outcome for the company in April of 2008.

Marketing expense for the year ended December 31, 2009, decreased $350,852 or 30.2%, to $810,147, compared to $1,160,999 for the year in 2008. Marketing expense usually varies from period to period according to the number of marketing events attended by personnel and their associated costs. In 2009, our cost containment measures led to decreases primarily in marketing related travel and exhibition costs.