UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number [811-06111

The Mexico Equity and Income Fund, Inc.

(Exact name of registrant as specified in charter)

615 E. Michigan Street

Milwaukee, WI 53202

(Address of principal executive offices) (Zip code)

Mr. Gerald Hellerman

c/o U.S. Bancorp Fund Services, LLC

615 E. Michigan Street

Milwaukee, WI 53202

(Name and address of agent for service)

(866) 700-6104

Registrant's telephone number, including area code

Date of fiscal year end: July 31, 2011

Date of reporting period: July 31, 2011

Item 1. Reports to Stockholders.

The Mexico Equity

and Income Fund, Inc.

Annual Report

July 31, 2011

The Mexico Equity and Income Fund Inc.

September 27, 2011

Dear Fellow Stockholders:

As I said in my last letter, if one can live with inevitable and unpredictable stomach churning declines, it is possible for an investor to earn good returns over the long term by investing in a volatile market like Mexico. Over the last five fiscal years, our Fund’s return based on market value has been at least 26.09% on the upside or at least 28.38% on the downside. Over the two year stretch of 2008 - 2009 the market return was down almost 60%. Yet, for the five years ending July 31, 2011, shareholders experienced a total return on their investment of about 70%.

Management’s ability to dampen the Fund’s volatility is limited given our mandate to invest in Mexican securities. Hopefully, good stock picking will generate good long term returns for stockholders as has been the case over the past five fiscal years and since the Fund’s inception. One thing the Board can do to enhance shareholder value is to have the Fund opportunistically repurchase its shares when they are trading at a discount to net asset value. These repurchases are accretive to the net asset value and may have the effect of narrowing the discount. We are now posting the number of shares repurchased every month on the Fund’s website at www.mxefund.com.

Sincerely yours,

Phillip Goldstein

Chairman

1

THE MEXICO EQUITY AND INCOME FUND, INC.

The Mexico Equity and Income Fund Inc.

Report of Pichardo Asset Management (“PAM”),

The Investment Adviser.

I. INTRODUCTION

For the Mexico Equity and Income Fund’s fiscal year ended July 31, 2011, the global economy experienced a large bout of volatility due to the lack of a clear path for resolving Europe’s sovereign debt crisis and the persistence of U.S. budgetary and unemployment problems. S&P downgraded the U.S. sovereign credit risk rating in August 2011, as negotiations over the debt ceiling confirmed the prevalence of a difficult political climate that restricts economic policy options.

As the global economy outlook grows ever gloomier and pro-growth steps either pay off or prove futile, Mexico must find ways to increase its meager 1.9% 10-year average economic growth soon, while continuing to decouple from its high correlation to the U.S. economy.

Labor market indicators have been characterized by healthy job growth during the period 2008-2009, but the unemployment rate has remained stubbornly high as the labor force in Mexico has increased in numbers. Economists (Source: UBS Mexico) believe that a reversal in migration flows to the U.S. is the single most important factor why the labor market remains soft, with quarterly average household income still showing a drop of -12.3% at the end of 2010 from 2008 levels. The biggest source of income contraction comes from compensation obtained from independent work, which points to ongoing weakness in the informal sector of the economy, specifically from self-employed activities. Real wages in the formal sector have remained largely stagnant; falling by more than 10% relative to their pre-crisis level.

The second challenge for Mexico is undoubtedly the ongoing crime-related problems that the country faces, and as UBS remarks if household incomes were to remain constrained, this would negatively impact domestic demand growth. A comprehensive labor reform in Mexico is urgent, not only as one of the best tools to keep youths from enlarging the ranks of organized crime but also to prevent higher unemployment rates as the estimated prolonged reversal of migration flows to the U.S. continues.

Amid a difficult external environment, Mexican GDP is still expected to grow between 3.5-4.0% year-over-year in 2011. Main factors driving economic activity are:

|

i.

|

a low fiscal deficit and debt as a percentage of GDP (30%), with a monetary policy conducive to price stability,

|

||

|

ii.

|

a flexible foreign exchange rate regime that has led to a relative undervalued Mexican currency, which is key to maintaining the competitiveness of Mexican exports despite the surge of capital flows to emerging markets,

|

||

|

iii.

|

a solid banking system with a capitalization level double that of the regulatory minimum and the commitment of Mexican development banks to continue granting credit to infrastructure,

|

2

THE MEXICO EQUITY AND INCOME FUND, INC.

|

iv.

|

contained inflationary pressures that are also determined by Mexico’s labor market difficulties, while on the positive side leaving Mexico in a good position to cut rates if the international environment deteriorates further.

|

The Mexican Stock Exchange performance during the Fund’s fiscal year, ended July 31, 2011 has been relatively one of the best performing markets in the Latam region.

The price to earnings (P/E) ratio for the Mexican market shows an inverse correlation with the level of Mexican Sovereign Risk, implying a lower cost of capital for investors reflected in higher valuation multiples. Regarding country risk premiums for the main Latam economies as of September 15, 2011, Argentina has the largest spread at 864 basis points (bps), with 233 bps for Brazil, 204 bps for Mexico and 164 for Chile.

MXE’s 26.75% net asset dollar gain per share outperformed the MSCI Mexico Index’s 22.03% by 472 basis points for the fund’s fiscal year period ended July 31, 2011.

The MXE’s net asset dollar per share posted a 14.53% annual average dollar return (with dividends reinvested) for the last 20 years since the Fund’s inception on August 30, 1990, through July 31, 2011. (Source: Thomson).

|

Common Shares

|

|||||

|

Average Annual Total Returns

|

|||||

|

As of July 31, 2011

|

|||||

|

MXE

|

Mexico

|

||||

|

NAV

|

Market Price

|

MSCI

|

|||

|

Year-to-date

|

3.43%

|

2.74%

|

-0.71%

|

||

|

1 Year

|

26.75%

|

26.09%

|

22.03%

|

||

|

5 Year

|

11.77%

|

14.60%

|

8.24%

|

||

|

10 Year

|

17.47%

|

17.97%

|

13.86%

|

||

|

Source:

|

MXE- U.S.Bancorp (1 and 5 yr),Bloomberg (10-yr).

|

||||

|

MSCI Mexico – Bloomberg.

|

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate such that an investor’s shares, when redeemed, may be worth more or less than the original costs. Current performance of the fund may be lower or higher than the performance quoted. Performance data to the most recent month end may be obtained by calling U.S. Bancorp Fund Services, LLC, (414)877-785-0376.

We believe that adherence and discipline in following a de-indexed investment strategy during the Fund’s fiscal year, ended July 31, 2011 -supported by earnings per share and discounted cash flow (DCF) investment models- has enabled PAM’s investment management team to refrain from investing in the housing, cement and commodity (copper) sectors, where companies were affected by changing accounting standards, financial reengineering with high debt and no investment edge visibility and commodity high dollar prices.

At the end of July 31, 2011, the Fund had an approximate 37% in the so called Alpha (not academic) stocks, classified by PAM as: Defensive companies with dividend + buybacks, solid financials and Net Debt to Ebitda ratios that are either negative or less than 1.

3

THE MEXICO EQUITY AND INCOME FUND, INC.

The Beta–growth companies approximately 31% of total assets added the most value to the Fund during its fiscal year period, ended July 31, 2011. By sectors, consumption and commodities –silver and copper- as well infrastructure -toll road concessions- sectors contributed the most.

We are now pleased to report that during the Fund’s fiscal year ended 2010 and 2011 we have managed to consistently outperform the Mexbol and the MSCI Mexico Indexes by adhering to the 2008 established investment strategy, asset class categories, stock specific metrics -including small stocks within the special situations asset category, as well as an active management.

The Fund has also managed to place its discount to NAV at levels of approximately 12% at the Fund’s fiscal year ended July 31, 2011.

II.MEXICO’S ECONOMIC REVIEW

During the period of August to December, 2010 (first half of the Fund’s fiscal year ended July 31, 2011), there was renewed hope among investors that the expansive monetary and fiscal policies put in place by U.S. authorities would lead to a favorable economic recovery, renewed job creation and improvement in consumer and business confidence.

From January to July, 2011 (the second half of the Fund’s 2011 fiscal year), as economic reports remained below the market consensus, it became clear that the U.S. economy was not experiencing a healthy rebound from the depths of the 2008-2009 recession, but rather a much slower pace of growth than originally forecasted.

The evolution of the Mexican economy has been favorable as of the second half of the Fund’s 2011 fiscal year, as Mexico’s Gross Domestic Product (GDP) increased 3.3% year-over-year (y/y) in 2Q11 (7.6% y/y in 2Q10 and -8.7% y/y in 2Q09), despite a deceleration of the U.S. economy. As of 2Q11, the main economic highlights are:

|

i.

|

Growth in primary activities decreased -3.7% y/y in 2Q11, utilities (waterworks, electricity and natural gas) surged 7.6% over the same period. These activities have benefitted from a strong rebound in infrastructure spending, as evidenced by an increase in Construction of 3.44% y/y in 2Q11. (Source: Mexico National Institute of Statistics, Geography, and Informatics, “INEGI”).

|

||

|

ii.

|

Gross fixed investment has undergone a substantial improvement of 11.5% y/y in 2Q11, primarily linked to the machinery and equipment component, which surged 27.3% y/y. Manufacturing activity was up 4.75% y/y, as industrial production increased 3.2% y/y. (Source: INEGI).

|

||

|

iii.

|

Strong performers in the industrial sector have been tobacco and beverages with a growth rate of 7.39% y/y and Commerce and Services +5.39% y/y. (Source: INEGI). The external sector offers signs of strong growth as imports and exports increased 19.59% and 21.63% y/y, respectively. (Source: INEGI). Trade figures for June 2011 show a surplus of US$107.9 million (-US$340.5 million in June 2010).

|

||

|

iv.

|

Retail sales grew 4.8% y/y in June 2011, averaging a growth rate of 2.9% year-to-date through June 2011 (1.5% y-t-d through June 2010) (source: Bloomberg).

|

||

|

v.

|

Based on Mexican Social Security Institute data, 43,329 new jobs were added in July 2011, for a total of 425,819 new jobs created year to date, through July 2011 (source: IMSS).

|

Amid the current negative environment, Banco de México, in July Mexico’s central bank and private analysts revised down expected 2011 GDP growth to 3.5%-4% from 4%-4.5% earlier this year.

4

THE MEXICO EQUITY AND INCOME FUND, INC.

Banco de México’s discount rate was maintained at 4.5% at the writing of this report where its members signaled that contained inflationary pressures (3.55% y/y in July 2011) along with a global environment of low growth leave the door open for future benchmark rate cuts.

The Mexican Peso has maintained its relative undervaluation since the 2008 global financial crisis ($10.90 pesos per Dollar at end 2007) closing July 2011 at $11.73 pesos per Dollar, which is an approximate appreciation of 7.24% for the one-year period ($12.64 pesos per Dollar at end July 2010).

Regarding PEMEX, the state oil company informed in its 2010 Annual Report that it has raised its proven reserves replenishment rate to 86% and expects it to reach 100% by 2012. It has also set a goal to produce 3 million barrels of oil per day by 2016, up from 2.55 million barrels per day in 2010. Pemex has also started assigning oil production contracts with incentives for private companies to exploit mature oil fields in the Gulf of Mexico.

III.THE MEXICAN STOCK EXCHANGE

Global equities have experienced strong corrections in 2011. At the time of writing, European stock markets have recorded the largest drops in dollar terms (-20% and UK -10%, approximately) linked to a problem of solvency; U.S. stock markets have lost below 10% on structural risk factors; major stock markets in Asia have retraced 15% while the Thai stock market has gained 4.31%. The Mexican Bolsa Index has lost approximately 10%.

The MSCI Mexico Index’s return of 22.03% for the fund’s 2011 fiscal year ranked it as the second best performing Latam related equity market after MSCI Argentina (+36.60%). The other MSCI related Indexes registered the following gains: Chile (+18.84%), Colombia (+14.19%), Peru (+7.68%) and Brazil (+4.23%). (Source: Bloomberg).

We reiterate that the performance of the MSCI-Mexico Index is characterized by illiquid constituent stocks which skyrocketed more than 80% during the Fund’s fiscal year ended July 31, 2011; and it has an approximate 60% concentration in five stocks with AMX weighing 31% and Walmex 10% as of the last rebalancing in September 2011 compared to MXE’s weight of approximately 18% in AMX and 6% in Walmex.

For the Fund’s fiscal year, ended July 31, the MSCI Mexico Index’s 22.03% dollar gain ranked it as the second best performing Latam related equity market after MSCI Argentina (36.60%). The other MSCI related Indexes registered the following gains: Chile (18.84%), Colombia (14.19%), Peru (7.68%) and Brazil (4.23%). (Source: Bloomberg).

The Mexican Stock Market had a market cap of approximately US $500 Bn as of the Fund’s fiscal year, ended July 31, 2011. Its main valuation metrics are: P/E = 20x, EV/EBITDA = 11x, P/BV = 2.98x, P/Cash Flow = 14x. In terms of the P/BV ratio, the Mexican market is still above the minimum level of 2.55x observed at the height of the 2008 crisis.

IV.THE FUND’S PERFORMANCE

We are pleased to report that MXE’s net asset dollar gain per share, as of July 31, 2011, reflects a dollar return position outperforming the Morgan Stanley Capital International Mexico Index by:

|

i.

|

248 basis points for the month of July gaining 1.69% (source: U.S. Bancorp).

|

||

|

ii.

|

414 basis points for the six month-period (January-July), registering a gain of 3.43% (source: U.S. Bancorp).

|

5

THE MEXICO EQUITY AND INCOME FUND, INC.

|

iii.

|

472 basis points for the one-year period through July 2011, gaining 26.75% in dollar terms (source: U.S. Bancorp).

|

At the MXE’s fiscal year ended July 31, 2011, the Fund’s market share price registered a 26.09% return, (source: U.S. Bancorp).

The main reasons why the MXE has outperformed its benchmark are, in our opinion: i) our continuous adherence to our investment strategy supported by our valuation and rating models, giving preference to companies with what we believe are solid balance sheets, a high free cash flow yield and strong corporate governance, ii) strict compliance with a fundamental analysis approach that prevents us from taking speculative positions, and iii) defensive positions, reflected in asset class diversification among private equity, REITS, small & mid caps and large caps.

The BETA asset class category, as classified by PAM, was the biggest contributor to the MXE’s net asset dollar gain per share of 26.75% for the one-year period through July 31, 2011, primarily toll road concessions, over-the-counter/generics, and the coke bottlers-related stocks.

PAM’s management team has generated a positive Alpha for MXE investors equivalent to 2% since the Fund’s inception (Source: PAM calculations). This calculation was performed using yearly return figures (Source: Bloomberg), considering reinvested dividends for the MXE starting in 1991 and starting in 2003 for the MSCI Mexico Index.

The volatility of MXE’s portfolio was 15.54% during the fund’s fiscal year ended July 31, 2011. This level is in line with 15.63%.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate such that investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data to the most recent month end may be obtained by calling U.S. Bancorp Fund Services, LLC, (414)877-785-0376.

V.PORTFOLIO STRATEGY

For the Fund’s fiscal year ended July 31, 2011, PAM has continued to adhere to its investment strategy established in December 2008. This investment strategy classifies assets as follows: i) Alpha-defensive stocks: annual dividend + share buybacks; ii) Beta-free cash flow-growth stocks; iii) Special situations: discount to Book Value. PAM’s company rating, P/E, and DCF valuation models provide us with an additional investment decision-making tool.

For the Fund’s fiscal year ended July 31, 2011 the MXE’s non-indexed investment strategy registered its largest weighted sectors as follows: consumption, wireless telecom, petrochemicals and metals & mining.

6

THE MEXICO EQUITY AND INCOME FUND, INC.

MXE’S TOP TEN HOLDINGS

As of July 31, 2011

|

MXE

|

2Q11 Sales

|

EBITDA

|

||||

|

WEIGHT

|

Growth

|

Margin

|

Net

|

|||

|

PORTFOLIO

|

SECTOR

|

%

|

YoY %

|

ROE %

|

%

|

Debt/EBITDA

|

|

AMERICA MOVIL

|

Telcos.

|

17.5

|

58.3

|

33.2

|

38.2

|

0.8x

|

|

LIVERPOOL

|

Department Stores

|

9.4

|

12.6

|

16.1

|

18.4

|

0.7x

|

|

MEXICHEM

|

Petrochemical

|

9.2

|

38.1

|

25.3

|

24.3

|

1.4x

|

|

GENOMMA LAB

|

Over-the-counter/generics

|

8.8

|

27.7

|

29.4

|

23.9

|

0.0x

|

|

WALMEX

|

Retailing

|

6.1

|

9.2

|

17.1

|

8.7

|

0.0x

|

|

CIDMEGA

|

Real Estate

|

4.4

|

(7.9)

|

3.5

|

26.60

|

3.4x

|

|

GFREGIO

|

Banking

|

4.2

|

9.2*

|

18.5

|

na

|

na

|

|

QUALITAS

|

Insurance

|

4.2

|

14.4*

|

15.5

|

na

|

na

|

|

FEMSA

|

Beverages

|

3.70

|

16.1

|

12.5

|

15.4

|

-0.1x

|

|

ARCA/CONTAL

|

Beverages

|

3.5

|

54.7

|

11.0

|

20.5

|

0.8x

|

* In the case of Banregio interest income, and for Qualitas retained premiums.

Source : Bloomberg

The MXE’s diversified portfolio also includes 4% in the Mexican Real Estate Investment Trust (REIT), 3% in Private Equity, 2% in dollar-denominated corporate bonds, and 1% in cash and equivalents.

For the last twenty years we have had the privilege of advising the MXE’s asset portfolio and have been disciplined throughout our learning curve in monitoring companies through one-on-one meetings and diverse local institutional analyst and investor forums. The investment management team is comprised of Kathia Reynoso, Juan Carlos Maussan, CFA, and Eugenia Pichardo.

Sincerely yours,

Eugenia Pichardo

Portfolio Manager

Disclosures

The fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. The prospectus contains this and other important information about the investment company, and it may be obtained by calling U.S. Bancorp Fund Services, LLC, (414) 765-4255/or visiting www.themexicoequityandincomefund.com. Read it carefully before investing.

Mutual fund investing involves risk. Principal loss is possible.

7

THE MEXICO EQUITY AND INCOME FUND, INC.

Diversification does not assure a profit or protect against loss in a declining market.

Investing in Foreign Securities

Investment in Mexican securities involves special considerations and risks that are not normally associated with investments in U.S. securities, including (1) relatively higher price volatility, lower liquidity and the small market capitalization of the Mexican securities markets; (2) currency fluctuations and the cost of converting Mexican pesos into U.S. dollars; (3) restrictions on foreign investment and potential restrictions on repatriation of capital invested in Mexico and remittance of profits and dividends accruing thereto; (4) political, economic and social risks and uncertainties, including risks of confiscatory taxation and expropriation or nationalization of assets; (5) higher rates of inflation, unemployment and interest rates than in the United States; and (6) less stringent disclosure requirements, less available information regarding Mexican public companies and less active regulatory oversight of Mexican public companies.

Mexican Economic and Political Factors. Although Mexico’s economy has strengthened in recent years and Mexico’s sovereign debt was recently upgraded to “investment-grade” rating by the three most prominent rating agencies, including Standard and Poor’s, Mexico continues to be characterized as a developing economy and investments in developing countries are subject to certain economic risks. Mexico has experienced widespread bank failures, currency devaluations, high levels of inflation and interest rates. Mexico is also dependent on certain industries and exports for economic health. The Portfolio Securities are denominated in pesos. As a result, the Portfolio Securities must increase in market value at a rate in excess of the rate of any decline in the value of the peso against the U.S. dollar in order to avoid a decline in their equivalent U.S. dollar value.

Mexican Securities Laws and Accounting Rules. There is less publicly available information about the issuers of Mexican securities, such as the Portfolio Securities, than is regularly published by issuers in the United States. Information provided by Mexican public companies may not be current, accurate or easily obtainable and, to the extent available, is likely to be in Spanish. Also, there is generally less governmental supervision and regulation of exchanges, brokers and issuers in Mexico than there is in the United States. U.S. holders of Portfolio Securities may also experience difficulties enforcing U.S. laws or obtaining service of process against the issuers of the Portfolio Securities.

The information provided herein represents the opinion of Pichardo Asset Management and is not intended to be a forecast of future events, a guarantee of future results, or investment advice.

Fund holdings and sector allocations are subject to change at any time, and should not be considered recommendations to buy or sell any security. Current and future portfolio holdings are subject to risk. Please see the Schedule of Investments on pages 13-15 for the fund holdings as of the most recent quarter-end.

8

THE MEXICO EQUITY AND INCOME FUND, INC.

Definitions

|

•

|

MEXBOL-Mexico Bolsa Index: The Mexican Bolsa Index, or the IPC (Indice de Precios y Cotizaciones) is a capitalization-weighted index of the leading stocks traded on the Mexican Stock Exchange. The index was developed with a base level of 0.78 as of October 30, 1978.

|

|

•

|

MSCI MEXICO: The Morgan Stanley Capital International Index Mexico is a capitalization weighted index that monitors the performance of stocks from Mexico.

|

|

•

|

Mexbol-total return index. The Mexican Bolsa index that calculates the performance of their constituents assuming that all dividends and distributions are reinvested.

|

|

•

|

IPSA-Chile Stock Market Select: The IPSA Index (Indice de Precios Selectivo de Acciones) comprises the 40 stocks with the highest average annual trading volume in the Santiago Stock Exchange (Bolsa de Comercio de Santiago). On the last trading day of the year, the index is re-based back to 1000. The index has been calculated since 1977 and is revised on a quarterly basis. MERVAL-Argentina Merval Index: The Argentin Merval Index, a basket weighted index, is the market value of a stock portfolio, selected according to participation in the Buenos Aires Stock Exchange, number of transactions and trading value. The index has a base value of $0.01 as of June 30,1986. The index is revised every 3 months, taking into account trading volumes over the past 6 months.

|

|

•

|

IBOV-Brazil Bovespa Stock Exchange Index: The Bovespa Index is a total return index weighted by traded volume and is comprised of the most liquid stocks traded on the Sao Paulo Stock Exchange. The Bovespa Index has been divided 10 times by a factor of 10 since January 1, 1985, those dates are: 12/02/85, 04/14/89, 05/28/91, 01/26/93, 02/10/94, 08/29/88, 01/12/90, 01/21/92, 08/27/93, 03/03/97.

|

|

•

|

IBVC-Venezuela Stock Market Index: The IBC Index from the Caracas Stock Exchange (Venezuela), also known as the General Index, is a capitalization-weighted index of the 15 most liquid and highest capitalized stocks traded on the Caracas Stock Exchange (Bolsa de Valores de Caracas). The index was modified from a previous existing index on August 28, 1997, but essentially continues to be the same.

|

|

•

|

IGBVL-Peru Lima General Index: The IGBVL Index is a value weighted index that tracks the performance of the largest and most actively traded stocks on the Lima Exchange. The index was developed with a base value of 100 as of December 31, 1981.

|

|

•

|

IGBC-IGBC General Index: The IGBC Index from the Colombia Stock Exchange, also known as the General Index, is a Price-weighted index of the most liquid and highest capitalized stocks traded on the Colombia Stock Exchange (Bolsa de Valores de Colombia). This index was merged with Medellin and Occidente on 7/3/01.

|

|

•

|

The Dow Jones Industrial Average is an unmanaged index of common stocks comprised of major industrial companies and assumes reinvestment of dividends.

|

|

•

|

The S&P 500 Index is a broad based unmanaged index of 500 stocks, which is widely recognized as representative of the equity market in general.

|

You cannot invest directly in an index.

|

•

|

Basis point (bps) is one hundredth of a percentage point (0.01%).

|

9

THE MEXICO EQUITY AND INCOME FUND, INC.

|

•

|

The net asset value per share (NAV) is calculated as the total market value of all the securities and other assets held by a fund minus the total liabilities, divided by the total number of common shares outstanding. The NAV of an investment company will fluctuate with the changes in the market prices of the underlying securities. However, the market price of a closed-end fund is determined in the open market by buyers and sellers. This public market price is the price at which investors may purchase or sell shares of a closed-end fund. The market price of a closed-end fund fluctuates throughout the day and may differ from its underlying NAV, based on supply and demand for a fund’s shares on the open market. Shares of a closed-end fund may trade at a premium to (higher than) or a discount to (lower than) NAV. The difference between the market price and NAV is expressed as a percentage that is either a discount or a premium to the NAV, or underlying value.

|

|

•

|

Alpha-defensive companies: an asset classification created by PAM based on the following criteria: high total annual yield, clean balance sheet, market share dominance and pricing power.

|

|

•

|

Beta-growth companies: an asset classification created by PAM based on the following criteria: oversold stocks with consistent sales and EBITDA (Earnings before Interest, Tax, Depreciation and Amortization) growth, especially in the infrastructure and housing sectors.

|

|

•

|

Special Situation companies: an asset classification created by PAM and based on the following criteria: High discount to companies’ valuation.

|

|

•

|

INEGI -National Statistics, Geography and Information Institute-: provides geographic, demographic and economic information for Mexico. It also coordinates the Information Development Program and provides the public service of statistical and geographic information.

|

|

•

|

EPS: Earnings per share is the portion of a company’s profit allocated to each outstanding share of common stock. Earnings per share serves as an indicator of a company’s profitability.

|

|

•

|

CAGR: Compound Annual Growth Rate. The year-over-year growth rate of an investment over a specified period of time. The compound annual growth rate is calculated by taking the nth root of the total percentage growth rate, where n is the number of years in the period being considered.

|

|

•

|

The Price to Earnings (P/E) Ratio reflects the multiple of earnings at which a stock sells.

|

|

•

|

The correlation coefficient is a measure of the interdependence of two random variables that ranges in value from -1 to +1, indicating perfect negative correlation at -1 , absence of correlation at zero and perfect positive correlation at +1.

|

|

•

|

Cash flow measures the cash generating capability of a company by adding non-cash charges (e.g. depreciation) and interest expense to pretax income.

|

|

•

|

Book value is the net asset value of a company, calculated by subtracting total liabilities from total assets.

|

|

•

|

Free cash flow is revenue less operating expenses including interest expenses and maintenance capital spending. It is the discretionary cash that a company has after all expenses and is available for purposes such as dividend payments, investing back into the business or share repurchases.

|

|

•

|

Return on equity is a measure of a corporation’s profitability. It represents the average return on equity on the securities in the portfolio, not the actual return on equity on the portfolio.

|

References to other mutual funds should not be interpreted as an offer of these securities.

10

THE MEXICO EQUITY AND INCOME FUND, INC.

RELEVANT ECONOMIC INFORMATION for the years ended December 31

|

Real Activity (million US$)

|

2006

|

2007

|

2008

|

2009

|

2010

|

|||||||||||||||

|

Real GDP Growth (y-o-y)

|

4.80 | % | 3.30 | % | 1.30 | % | -6.50 | % | 5.50 | % | ||||||||||

|

Industrial Production (y-o-y Average)

|

5.78 | % | 2.03 | % | -0.04 | % | 7.29 | % | 6.06 | % | ||||||||||

|

Trade Balance (US billions)

|

-$6.10 | -$11.20 | $15.53 | -$4.70 | -$3.12 | |||||||||||||||

|

Exports

|

$253.90 | $249.99 | $291.81 | $229.70 | $298.36 | |||||||||||||||

|

Export growth (y-o-y)

|

10.30 | % | 5.80 | % | 7.30 | % | -18.10 | % | 28.20 | % | ||||||||||

|

Imports

|

$260.00 | $283.00 | $308.65 | $234.40 | $301.48 | |||||||||||||||

|

Import growth (y-o-y)

|

13.10 | % | 8.30 | % | 9.50 | % | -19.90 | % | 25.00 | % | ||||||||||

|

Financial Variables and Prices

|

||||||||||||||||||||

|

28-Day CETES (T-bills) Average

|

7.10 | % | 7.04 | % | 7.97 | % | 4.51 | % | 4.40 | % | ||||||||||

|

Exchange rate (Pesos/US$) Average

|

10.90 | 10.93 | 11.16 | 13.09 | 12.63 | |||||||||||||||

|

Inflation IPC, 12 month trailing

|

3.80 | % | 4.00 | % | 6.53 | % | 3.57 | % | 4.40 | % | ||||||||||

|

Mexbol Index

|

||||||||||||||||||||

|

USD Return

|

45.77 | % | 10.56 | % | -40.48 | % | 55.34 | % | 28.79 | % | ||||||||||

|

Market Cap- (US billions)

|

$343.48 | $441.04 | $172.14 | $257.88 | $281.56 | |||||||||||||||

|

EV/EBITDA

|

10.60 | x | 9.8 | x | 7.4 | x | 7.86 | x | 9.48 | x | ||||||||||

|

Fund’s NAV & Common Share

|

||||||||||||||||||||

|

Market Price Performance

|

||||||||||||||||||||

|

NAV’s per share

|

59.29 | % | 30.68 | % | -52.89 | % | 52.27 | % | 41.91 | % | ||||||||||

|

Share Price

|

75.54 | % | 24.39 | % | -47.46 | % | 22.20 | % | 48.41 | % | ||||||||||

Sources: Banamex, Banco de Mexico, Bloomberg, INEGI

11

THE MEXICO EQUITY AND INCOME FUND, INC.

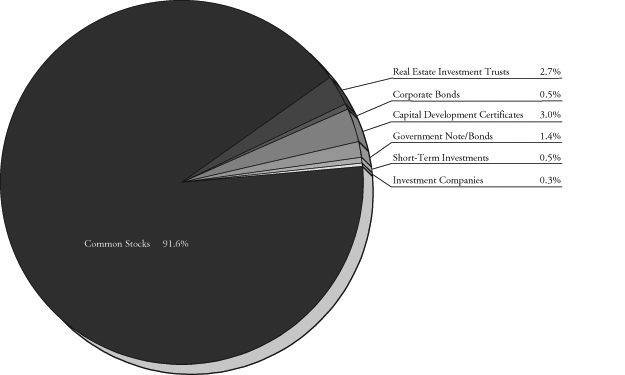

July 31, 2011

Allocation of Portfolio Assets

(Calculated as a percentage of Total Investments)

The accompanying notes are an integral part of these financial statements.

12

THE MEXICO EQUITY AND INCOME FUND, INC.

July 31, 2011

Schedule of Investments

|

MEXICO – 99.75%

|

Shares

|

Value

|

||||||

|

COMMON STOCKS – 91.66%

|

||||||||

|

Beverages – 7.21%

|

||||||||

|

Arca Continental S.A.B. de C.V.

|

575,289 | $ | 3,152,074 | |||||

|

Fomento Economico Mexicano, S.A.B. de C.V.

|

462,000 | 3,338,265 | ||||||

| 6,490,339 | ||||||||

|

Chemicals – 9.17%

|

||||||||

|

Mexichem, S.A. de C.V.

|

1,911,659 | 8,247,758 | ||||||

|

Commercial Banks – 4.25%

|

||||||||

|

Banregio Grupo Financiero S.A. de C.V. (a)

|

1,406,200 | 3,821,814 | ||||||

|

Construction & Engineering – 4.48%

|

||||||||

|

Carso Infraestructura y Construccion, S.A. de C.V. (a)

|

1,680,000 | 1,023,404 | ||||||

|

Promotora y Operadora de Infraestructura, S.A. de C.V. (a)

|

599,900 | 3,007,346 | ||||||

| 4,030,750 | ||||||||

|

Consumer Finance – 0.40%

|

||||||||

|

Financiera Independencia S.A.B. de C.V.

|

429,231 | 358,018 | ||||||

|

Diversified Telecommunication Services – 0.74%

|

||||||||

|

Telefonos De Mexico S.A.B. de C.V.

|

820,000 | 662,998 | ||||||

|

Food & Staples Retailing – 6.80%

|

||||||||

|

Grupo Comercial Chedraui, S.A. de C.V.

|

205,300 | 623,563 | ||||||

|

Wal-Mart de Mexico, S.A. de C.V. – Class V

|

1,991,000 | 5,492,624 | ||||||

| 6,116,187 | ||||||||

|

Food Products – 1.14%

|

||||||||

|

Grupo Bimbo, S.A.B. de C.V.

|

426,000 | 1,024,958 | ||||||

|

Health Care Providers & Services – 2.08%

|

||||||||

|

Medica Sur S.A.B. de C.V.

|

905,000 | 1,874,413 | ||||||

|

Hotels, Restaurants & Leisure – 6.49%

|

||||||||

|

Alsea, S.A. de C.V. – Class A

|

1,647,500 | 1,865,444 | ||||||

|

Grupe, S.A. de C.V. (a)

|

2,978,486 | 3,971,382 | ||||||

| 5,836,826 | ||||||||

The accompanying notes are an integral part of these financial statements.

13

THE MEXICO EQUITY AND INCOME FUND, INC.

July 31, 2011

Schedule of Investments (continued)

|

COMMON STOCKS (CONTINUED)

|

Shares

|

Value

|

||||||

|

Industrial Conglomerates – 3.62%

|

||||||||

|

Alfa, S.A. – Class A

|

108,600 | $ | 1,596,621 | |||||

|

Industrias CH, S.A. – Class B (a)

|

468,400 | 1,660,129 | ||||||

| 3,256,750 | ||||||||

|

Insurance – 4.16%

|

||||||||

|

Qualita Compania de Seguros

|

4,139,651 | 3,738,535 | ||||||

|

Metals & Mining – 5.33%

|

||||||||

|

Grupo Mexico, S.A. – Series B

|

538,498 | 1,983,358 | ||||||

|

Industrias Penoles, S.A.

|

65,110 | 2,807,974 | ||||||

| 4,791,332 | ||||||||

|

Multiline Retail – 9.38%

|

||||||||

|

El Puerto De Liver

|

1,044,600 | 8,442,381 | ||||||

|

Pharmaceuticals – 8.84%

|

||||||||

|

Genomma Lab Internacional SA (a)

|

3,463,700 | 7,950,046 | ||||||

|

Wireless Telecommunication Services – 17.57%

|

||||||||

|

America Movil, S.A. de C.V. – Class L

|

12,265,798 | 15,800,812 | ||||||

|

TOTAL COMMON STOCKS (Cost $76,820,822)

|

82,443,917 | |||||||

|

REAL ESTATE INVESTMENT TRUSTS – 2.70%

|

||||||||

|

Fibra Uno Administracion S.A. de C.V.

|

1,294,500 | 2,426,367 | ||||||

|

TOTAL REAL ESTATE INVESTMENT TRUSTS (Cost $2,095,703)

|

2,426,367 | |||||||

|

CORPORATE BONDS – 0.53%

|

Principal

|

|||||||

|

Urbi, Desarrollos Urbanos, S.A. de C.V.

|

||||||||

|

8.500%, 04/19/2016

|

$ | 461,300 | 479,752 | |||||

|

TOTAL CORPORATE BONDS (Cost $394,500)

|

479,752 | |||||||

The accompanying notes are an integral part of these financial statements.

14

THE MEXICO EQUITY AND INCOME FUND, INC.

July 31, 2011

Schedule of Investments (concluded)

|

MEXICAN GOVERNMENT NOTE/BONDS – 1.37%

|

Principal

|

Value

|

||||||

|

Mexico-united Mexican Sts

|

||||||||

|

8.125%, 12/30/2019

|

$ | 865,000 | $ | 1,228,300 | ||||

|

TOTAL FOREIGN GOVERNMENT NOTE/BONDS (Cost $1,152,294)

|

1,228,300 | |||||||

|

CAPITAL DEVELOPMENT CERTIFICATES – 2.99%

|

||||||||

|

Atlas Discovery Trust II (b)

|

300,000 | 2,686,760 | ||||||

|

TOTAL CAPITAL DEVELOPMENT CERTIFICATES (Cost $2,317,515)

|

2,686,760 | |||||||

|

SHORT-TERM INVESTMENTS – 0.50%

|

||||||||

|

Mexican INAFIN

|

||||||||

|

0.000% Coupon, 4.613% Effective Yield, 08/02/2011 (c)

|

5,232,628 | * | 445,739 | |||||

|

TOTAL SHORT-TERM INVESTMENTS (Cost $448,327)

|

445,739 | |||||||

|

TOTAL MEXICO (Cost $83,229,161)

|

89,710,835 | |||||||

|

UNITED STATES – 0.33%

|

Shares

|

|||||||

|

INVESTMENT COMPANIES – 0.33%

|

||||||||

|

First American Treasury Obligation – Class A, 0.000%

|

299,971 | 299,971 | ||||||

|

TOTAL INVESTMENT COMPANIES (Cost $299,971)

|

299,971 | |||||||

|

TOTAL UNITED STATES (Cost $299,971)

|

299,971 | |||||||

|

TOTAL INVESTMENTS (Cost $83,529,132) – 100.08%

|

90,010,806 | |||||||

|

LIABILITIES IN EXCESS OF OTHER ASSETS – (0.08)%

|

(62,628 | ) | ||||||

|

TOTAL NET ASSETS – 100.00%

|

$ | 89,948,178 | ||||||

Footnotes

Percentages are stated as a percent of net assets.

|

(a)

|

Non-income producing security.

|

|

(b)

|

Fair Valued Security.

|

|

(c)

|

Effective Yield based on the purchase price. The calculation assumes the security is held to maturity.

|

|

*

|

Principal amount in Mexican Pesos.

|

The accompanying notes are an integral part of these financial statements.

15

(This Page Intentionally Left Blank.)

16

THE MEXICO EQUITY AND INCOME FUND, INC.

July 31, 2011

Statement of Assets & Liabilities

|

ASSETS:

|

|||||

|

Investments, at value (Cost $83,529,132)

|

$ | 90,010,806 | |||

|

Cash

|

11,403 | ||||

|

Receivables for investments sold

|

9,470,497 | ||||

|

Dividends and interest receivable

|

16,760 | ||||

|

Other assets

|

10,182 | ||||

|

Total Assets

|

99,519,648 | ||||

|

LIABILITIES:

|

|||||

|

Payable for securities purchased

|

9,384,589 | ||||

|

Advisory fees payable

|

60,622 | ||||

|

Administration fees payable

|

18,023 | ||||

|

Custody fees payable

|

18,485 | ||||

|

Fund accounting fees payable

|

7,802 | ||||

|

Legal fees payable

|

7,989 | ||||

|

CCO fees payable

|

4,128 | ||||

|

Accrued expenses and other liabilities

|

69,832 | ||||

|

Total Liabilities

|

9,571,470 | ||||

|

Net Assets

|

$ | 89,948,178 | |||

|

Net Asset Value Per Preferred Share

|

|||||

| ($764,506 / 57,639) | $ | 13.26 | |||

|

Net Asset Value Per Common Share

|

|||||

| ($89,183,672 / 6,723,882) | $ | 13.26 | |||

|

NET ASSETS CONSIST OF:

|

|||||

|

Preferred stock, $0.001 par value; 57,639 shares outstanding

|

|||||

|

(1,855,128 shares authorized)

|

$ | 58 | |||

|

Common stock, $0.001 par value; 6,723,882 shares outstanding

|

|||||

|

(98,144,872 shares authorized)

|

6,724 | ||||

|

Paid-in capital

|

88,996,871 | ||||

|

Accumulated net realized loss on investments and foreign currency

|

(5,536,664 | ) | |||

|

Net unrealized appreciation on investments and foreign currency

|

6,481,189 | ||||

|

Net Assets

|

$ | 89,948,178 | |||

The accompanying notes are an integral part of these financial statements.

17

THE MEXICO EQUITY AND INCOME FUND, INC.

For the Year Ended

July 31, 2011

Statement of Operations

|

INVESTMENT INCOME

|

||||

|

Dividends

|

$ | 990,017 | ||

|

Interest

|

135,630 | |||

|

Total Investment Income

|

1,125,647 | |||

|

EXPENSES

|

||||

|

Advisory fees (Note B)

|

$ | 686,118 | ||

|

Directors’ fees and expenses (Note B)

|

142,469 | |||

|

Administration fees (Note B)

|

103,428 | |||

|

Custodian fees (Note B)

|

75,504 | |||

|

Legal fees

|

47,554 | |||

|

Fund accounting fees (Note B)

|

47,057 | |||

|

Printing and mailing

|

43,337 | |||

|

CCO fees (Note B)

|

34,741 | |||

|

NYSE fees

|

34,235 | |||

|

Insurance expense

|

32,987 | |||

|

Audit fees

|

29,880 | |||

|

Transfer agent fees & expenses

|

19,535 | |||

|

Miscellaneous fees

|

284 | |||

|

Total expenses

|

1,297,129 | |||

|

NET INVESTMENT LOSS

|

(171,482 | ) | ||

|

NET REALIZED AND UNREALIZED GAIN ON INVESTMENTS

|

||||

|

Net realized gain from investments and foreign currency transactions

|

11,258,224 | |||

|

Net change in unrealized appreciation on

|

||||

|

investments and foreign currency transactions

|

7,990,303 | |||

|

Net gain from investments and foreign currency transactions

|

19,248,527 | |||

|

Net increase in net assets resulting from operations

|

$ | 19,077,045 | ||

The accompanying notes are an integral part of these financial statements.

18

THE MEXICO EQUITY AND INCOME FUND, INC.

Statements of Changes in Net Assets

|

For the

|

For the

|

|||||||

|

Year Ended

|

Year Ended

|

|||||||

|

July 31, 2011

|

July 31, 2010

|

|||||||

|

INCREASE (DECREASE) IN NET ASSETS

|

||||||||

|

Operations:

|

||||||||

|

Net investment loss

|

$ | (171,482 | ) | $ | (13,975 | ) | ||

|

Net realized gain (loss) on investments and foreign currency transactions

|

||||||||

|

Unaffiliated Issuers

|

11,258,224 | 20,483,899 | ||||||

|

Affiliated Issuers

|

— | (8,023 | ) | |||||

|

Net realized gain from in-kind redemptions (Note A)

|

||||||||

|

Unaffiliated Issuers

|

— | 146,639 | ||||||

|

Affiliated Issuers

|

— | 27,250 | ||||||

|

Net change in unrealized appreciation in value

|

||||||||

|

of investments and foreign currency transactions

|

7,990,303 | 2,602,190 | ||||||

|

Net increase in net assets resulting from operations

|

19,077,045 | 23,237,980 | ||||||

|

Distributions to Shareholders from:

|

||||||||

|

Net investment income

|

||||||||

|

Common stock

|

(160,267 | ) | — | |||||

|

Preferred stock

|

(1,586 | ) | — | |||||

|

Decrease in net assets from distributions

|

(161,853 | ) | — | |||||

|

Capital Share Transactions:

|

||||||||

|

Purchase of common stock for dividend

|

(8,775 | ) | — | |||||

|

Issuance of common stock for dividend

|

8,775 | — | ||||||

|

Repurchase of common stock through Repurchase Plan (Note D)

|

(4,314,588 | ) | (5,501,792 | ) | ||||

|

Repurchase of preferred stock for in-kind tender offer

|

— | (3,813,379 | ) | |||||

|

Increase in net assets from capital share transactions

|

(4,314,588 | ) | (9,315,171 | ) | ||||

|

Total increase in net assets

|

14,600,604 | 13,922,809 | ||||||

|

Net Assets:

|

||||||||

|

Beginning of year

|

75,347,574 | 61,424,765 | ||||||

|

End of year*

|

$ | 89,948,178 | $ | 75,347,574 | ||||

|

* Including accumulated net investment loss of

|

$ | — | $ | (260,079 | ) | |||

The accompanying notes are an integral part of these financial statements.

19

THE MEXICO EQUITY AND INCOME FUND, INC.

Financial Highlights

For a Common Share Outstanding Throughout Each Year

|

For the Year Ended July 31,

|

||||||||||||||||||||

|

2011

|

2010

|

2009

|

2008

|

2007

|

||||||||||||||||

|

Per Share Operating Performance

|

||||||||||||||||||||

|

Net asset value, beginning of period

|

$ | 10.48 | $ | 7.37 | $ | 28.29 | $ | 38.18 | $ | 22.18 | ||||||||||

|

Net investment income (loss)

|

(0.03 | ) | (0.01 | ) | 0.07 | 0.03 | (0.14 | ) | ||||||||||||

|

Net realized and unrealized gains (losses)

|

||||||||||||||||||||

|

on investments and foreign currency transactions

|

2.75 | 3.00 | (13.95 | ) | (2.57 | ) | 19.17 | |||||||||||||

|

Net increase (decrease) from investment operations

|

2.72 | 2.99 | (13.88 | ) | (2.54 | ) | 19.03 | |||||||||||||

|

Less: Distributions

|

||||||||||||||||||||

|

Dividends from net investment income

|

(0.02 | ) | — | (0.25 | ) | — | (0.13 | ) | ||||||||||||

|

Distributions from net realized gains

|

— | — | (6.52 | ) | (7.41 | ) | (2.90 | ) | ||||||||||||

|

Total dividends and distributions

|

(0.02 | ) | — | (6.77 | ) | (7.41 | ) | (3.03 | ) | |||||||||||

|

Capital Share Transactions

|

||||||||||||||||||||

|

Anti-dilutive effect of

|

||||||||||||||||||||

|

Common Share Repurchase Program

|

0.08 | 0.12 | 0.04 | 0.15 | — | |||||||||||||||

|

Anti-dilutive effect of Common Rights Offering

|

— | — | — | 0.06 | — | |||||||||||||||

|

Anti-dilutive effect of Preferred In-Kind Tender Offer

|

— | — | — | 0.02 | — | |||||||||||||||

|

Dilutive effect of Preferred In-Kind Tender Offer

|

— | (0.00 | )(3) | (0.02 | ) | — | — | |||||||||||||

|

Dilutive effect of Reinvestment of

|

||||||||||||||||||||

|

Distributions by Common Stockholders

|

— | — | (0.29 | ) | (0.17 | ) | — | |||||||||||||

|

Total capital share transactions

|

0.08 | 0.12 | (0.27 | ) | 0.06 | — | ||||||||||||||

|

Net Asset Value, end of period

|

$ | 13.26 | $ | 10.48 | $ | 7.37 | $ | 28.29 | $ | 38.18 | ||||||||||

|

Per share market value, end of period

|

$ | 11.64 | $ | 9.25 | $ | 6.08 | $ | 24.39 | $ | 44.23 | ||||||||||

|

Total Investment Return Based on

|

||||||||||||||||||||

|

Market Value, end of period(1)

|

26.09 | % | 52.14 | % | (43.10 | )% | (28.38 | )% | 152.78 | % | ||||||||||

The accompanying notes are an integral part of these financial statements.

20

THE MEXICO EQUITY AND INCOME FUND, INC.

Financial Highlights (continued)

For a Common Share Outstanding Throughout Each Year

|

For the Year Ended July 31,

|

||||||||||||||||||||

|

2011

|

2010

|

2009

|

2008

|

2007

|

||||||||||||||||

|

Ratios/Supplemental Data

|

||||||||||||||||||||

|

Net assets, end of period (000’s)

|

$ | 89,184 | $ | 74,609 | $ | 56,980 | $ | 106,484 | $ | 100,251 | ||||||||||

|

Ratios of expenses to average net assets:

|

1.51 | % | 1.68 | % | 1.82 | % | 1.50 | % | 1.42 | % | ||||||||||

|

Ratios of net investment income (loss)

|

||||||||||||||||||||

|

to average net assets:

|

(0.20 | )% | (0.02 | )% | 0.97 | % | 0.09 | % | (0.47 | )% | ||||||||||

|

Portfolio turnover rate

|

253.20 | %(2) | 365.58 | %(2) | 335.64 | %(2) | 224.10 | %(2) | 135.49 | %(2) | ||||||||||

|

(1)

|

Total investment return is calculated assuming a purchase of common stock at the current market price on the first day and a sale at the current market price on the last day of each period reported. Dividends and distributions, if any, are assumed for purposes of this calculation to be reinvested at prices obtained under the Fund’s dividend reinvestment plan. Total investment does not reflect brokerage commissions.

|

|

(2)

|

Calculated on the basis of the Fund as a whole without distinguishing between shares issued.

|

|

(3)

|

Less than 0.5 cent per share.

|

The accompanying notes are an integral part of these financial statements.

21

THE MEXICO EQUITY AND INCOME FUND, INC.

Financial Highlights

For a Preferred Share Outstanding Throughout Each Year

|

For the Year Ended July 31,

|

||||||||||||||||||||

|

2011

|

2010

|

2009

|

2008

|

2007

|

||||||||||||||||

|

Per Share Operating Performance

|

||||||||||||||||||||

|

Net asset value, beginning of period

|

$ | 10.48 | $ | 7.37 | $ | 28.29 | $ | 38.18 | $ | 22.18 | ||||||||||

|

Net investment income

|

(0.03 | ) | (0.01 | ) | 0.07 | 0.03 | (0.14 | ) | ||||||||||||

|

Net realized and unrealized gains (losses)

|

||||||||||||||||||||

|

on investments and foreign currency transactions

|

2.75 | 3.00 | (13.95 | ) | (2.57 | ) | 19.17 | |||||||||||||

|

Net increase (decrease) from investment operations

|

2.72 | 2.99 | (13.88 | ) | (2.54 | ) | 19.03 | |||||||||||||

|

Less: Distributions

|

||||||||||||||||||||

|

Dividends from net investment income

|

(0.02 | ) | — | (0.25 | ) | — | (0.13 | ) | ||||||||||||

|

Distributions from net realized gains

|

— | — | (6.52 | ) | (7.41 | ) | (2.90 | ) | ||||||||||||

|

Total dividends and distributions

|

(0.02 | ) | — | (6.77 | ) | (7.41 | ) | (3.03 | ) | |||||||||||

|

Capital Share Transactions

|

||||||||||||||||||||

|

Anti-dilutive effect of

|

||||||||||||||||||||

|

Common Share Repurchase Program

|

0.08 | 0.12 | 0.04 | 0.15 | — | |||||||||||||||

|

Anti-dilutive effect of Common Rights Offering

|

— | — | — | 0.06 | — | |||||||||||||||

|

Anti-dilutive effect of Preferred In-Kind Tender Offer

|

— | — | — | 0.02 | — | |||||||||||||||

|

Dilutive effect of Preferred In-Kind Tender Offer

|

— | (0.00 | )(3) | (0.02 | ) | — | ||||||||||||||

|

Dilutive effect of Reinvestment of

|

||||||||||||||||||||

|

Distributions by Common Stockholders

|

— | — | (0.29 | ) | (0.17 | ) | — | |||||||||||||

|

Total capital share transactions

|

0.08 | 0.12 | (0.27 | ) | 0.06 | — | ||||||||||||||

|

Net Asset Value, end of period

|

$ | 13.26 | $ | 10.48 | $ | 7.37 | $ | 28.29 | $ | 38.18 | ||||||||||

|

Per share market value, end of period

|

$ | 11.93 | * | $ | 9.17 | * | $ | 6.85 | $ | 25.50 | $ | 36.10 | ||||||||

|

Total Investment Return Based on

|

||||||||||||||||||||

|

Market Value, end of period(1)

|

30.36 | %* | 33.87 | %* | (38.67 | )% | (8.25 | )% | 110.66 | % | ||||||||||

The accompanying notes are an integral part of these financial statements.

22

THE MEXICO EQUITY AND INCOME FUND, INC.

Financial Highlights (continued)

For a Preferred Share Outstanding Throughout Each Year

|

For the Year Ended July 31,

|

||||||||||||||||||||

|

2011

|

2010

|

2009

|

2008

|

2007

|

||||||||||||||||

|

Ratios/Supplemental Data

|

||||||||||||||||||||

|

Net assets, end of period (000’s)

|

$ | 764 | $ | 739 | $ | 4,444 | $ | 22,742 | $ | 54,567 | ||||||||||

|

Ratios of expenses to average net assets:

|

1.51 | % | 1.68 | % | 1.82 | % | 1.50 | % | 1.42 | % | ||||||||||

|

Ratios of net investment income (loss)

|

||||||||||||||||||||

|

to average net assets:

|

(0.20 | )% | (0.02 | )% | 0.97 | % | 0.09 | % | (0.47 | )% | ||||||||||

|

Portfolio turnover rate

|

253.20 | %(2) | 365.58 | %(2) | 335.64 | %(2) | 224.10 | %(2) | 135.49 | %(2) | ||||||||||

|

(1)

|

Total investment return is calculated assuming a purchase of preferred stock at the current market price on the first day and a sale at the current market price on the last day of each period reported. Dividends and distributions, if any, are assumed for purposes of this calculation to be reinvested at prices obtained under the Fund’s dividend reinvestment plan. Total investment does not reflect brokerage commissions.

|

|

(2)

|

Calculated on the basis of the Fund as a whole without distinguishing between shares issued.

|

|

(3)

|

Less than 0.5 cent per share.

|

|

*

|

Based on the mean of the bid and ask.

|

The accompanying notes are an integral part of these financial statements.

23

THE MEXICO EQUITY AND INCOME FUND, INC.

July 31, 2011

Notes to Financial Statements

NOTE A: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The Mexico Equity and Income Fund, Inc. (the “Fund”) was incorporated in Maryland on May 24, 1990, and commenced operations on August 21, 1990. The Fund is registered under the Investment Company Act of 1940, as amended, as a closed-end, non-diversified management investment company.

The preparation of financial statements in accordance with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts and disclosures in the financial statements. Actual results could differ from those estimates.

Significant accounting policies are as follows:

Portfolio Valuation. Investments are stated at value in the accompanying financial statements. All securities for which market quotations are readily available are valued at the last sales price prior to the time of determination of net asset value, or, if no sales price is available at that time, at the closing price last quoted for the securities (but if bid and asked quotations are available, at the mean between the current bid and asked prices, rather than the quoted closing price). Securities that are traded over-the-counter are valued, if bid and asked quotations are available, at the mean between the current bid and asked prices. Investments in short-term debt securities having a maturity of 60 days or less are valued at amortized cost if their term to maturity from the date of purchase was less than 60 days, or by amortizing their value on the 61st day prior to maturity if their term to maturity from the date of purchase when acquired by the Fund was more than 60 days. Other assets and securities for which no quotations are readily available will be valued in good faith at fair value using methods determined by the Board of Directors. These methods include, but are not limited to, the fundamental analytical data relating to the investment; the nature and duration of restrictions in the market in which they are traded (including the time needed to dispose of the security, methods of soliciting offers and mechanics of transfer); the evaluation of the forces which influence the market in which these securities may be purchased or sold, including the economic outlook and the condition of the industry in which the issuer participates. The Fund has a Valuation Committee which oversees the valuation of portfolio securities.

Investment Transactions and Investment Income. The cost of investments sold is determined by use of the specific identification method for both financial reporting and income tax purposes. Interest income, including the accretion of discount and amortization of premium on investments, is recorded on an accrual basis; dividend income is recorded on the ex-dividend date or, using reasonable diligence, when known to the Fund. The collectibility of income receivable from foreign securities is evaluated periodically, and any resulting allowances for uncollectible amounts are reflected currently in the determination of investment income.

Tax Status. No provision is made for U.S. Federal income or excise taxes as it is the Fund’s intention to continue to qualify as a regulated investment company and to make the requisite distributions to its

24

THE MEXICO EQUITY AND INCOME FUND, INC.

July 31, 2011

Notes to Financial Statements (continued)

shareholders that will be sufficient to relieve it from all or substantially all U.S. Federal income and excise taxes.

The Fund is subject to the following withholding taxes on income from Mexican sources:

Dividends distributed by Mexican companies are subject to withholding tax at an effective rate of 0.00%.

Interest income on debt issued by the Mexican federal government is generally not subject to withholding. Withholding tax on interest from other debt obligations such as publicly traded bonds and loans by banks or insurance companies is at a rate of 4.9% under the tax treaty between Mexico and the United States.

Gains realized from the sale or disposition of debt securities may be subject to a 4.9% withholding tax. Gains realized by the Fund from the sale or disposition of equity securities that are listed and traded on the Mexican Stock Exchange (“MSE”) are exempt from Mexican withholding tax if sold through the stock exchange. Gains realized on transactions outside of the MSE may be subject to withholding at a rate of 25% (20% rate prior to January 1, 2002) of the value of the shares sold or, upon the election of the Fund, at 35% (40% rate prior to January 1, 2002) of the gain. If the Fund has owned less than 25% of the outstanding stock of the issuer of the equity securities within the 12 month period preceding the disposition, then such disposition will not be subject to capital gains taxes as provided for in the treaty to avoid double taxation between Mexico and the United States.

New Tax Law. On December 22, 2010, The Regulated Investment Company Modernization Act of 2010 (the “Modernization Act”) was signed by The President. The Modernization Act is the first major piece of legislation affecting Regulated Investment Companies (“RICs”) since 1986 and it modernizes several of the federal income and excise tax provisions related to RICs. Some highlights of the enacted provisions are as follows:

New capital losses may now be carried forward indefinitely, and retain the character of the original loss. Under pre-enactment law, capital losses could be carried forward for eight years, and carried forward as short-term capital, irrespective of the character of the original loss.

The Modernization Act contains simplification provisions, which are aimed at preventing disqualification of a RIC for “inadvertent” failures of the asset diversification and/or qualifying income tests. Additionally, the Modernization Act exempts RICs from the preferential dividend rule, and repealed the 60-day designation requirement for certain types of pay-through income and gains.

Finally, the Modernization Act contains several provisions aimed at preserving the character of distributions made by a fiscal year RIC during the portion of its taxable year ending after October 31 or December 31, reducing the circumstances under which a RIC might be required to file amended Forms 1099 to restate previously reported distributions.

25

THE MEXICO EQUITY AND INCOME FUND, INC.

July 31, 2011

Notes to Financial Statements (continued)

Except for the simplification provisions related to RIC qualification, the Modernization Act is effective for taxable years beginning after December 22, 2010. The provisions related to RIC qualification are effective for taxable years for which the extended due date of the tax return is after December 22, 2010.

New Accounting Pronouncement. In May 2011, the Financial Accounting Standards Board issued Accounting Standards Update (“ASU”) No. 2011-04 “Amendments to Achieve Common Fair Value Measurement and Disclosure Requirements in U.S. GAAP and IFRSs.” ASU No. 2011-04 requires additional disclosures regarding fair value measurements. Effective for fiscal years beginning after December 15, 2011, and for interim periods within those fiscal years, entities will need to disclose the following:

1)the amounts of any transfers between Level 1 and Level 2 and the reasons for those transfers, and

2)for Level 3 fair value measurements, quantitative information about the significant unobservable inputs used, a description of the entity’s valuation processes, and a narrative description of the sensitivity of the fair value measurement to changes in the unobservable inputs and the interrelationship between inputs.

Management is currently evaluating the impact ASU No. 2011-04 will have on the Fund’s financial statement disclosures.

Summary of Fair Value Exposure at July 31, 2011. The Fund has adopted Statement of Financial Accounting Standard, “Fair Value Measurements and Disclosures” (“Fair Value Measurements”) and FASB Staff Position “Determining Fair Value when the Volume and Level of Activity for the Asset or Liability Have Significantly Decreased and Identified Transactions that are not Orderly” (“Determining Fair Value”). Determining Fair Value clarifies Fair Value Measurements and requires an entity to evaluate certain factors to determine whether there has been a significant decrease in volume and level of activity for the security such that recent transactions and quoted prices may not be determinative of fair value and further analysis and adjustment may be necessary to estimate fair value. Determining Fair Value also requires enhanced disclosure regarding the inputs and valuation techniques used to measure fair value in those instances as well as expanded disclosure of valuation levels for major security types. Fair Value Measurements requires the Fund to classify its securities based on valuation method. These inputs are summarized in the three broad levels listed below:

|

Level 1 –

|

Unadjusted quoted prices in active markets for identical assets or liabilities that the company has the ability to access.

|

|

Level 2 –

|

Observable inputs other than quoted prices included in level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data.

|

26

THE MEXICO EQUITY AND INCOME FUND, INC.

July 31, 2011

Notes to Financial Statements (continued)

|

Level 3 –

|

Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the company’s own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available.

|

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in level 3.

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety, is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. The following is a summary of the inputs used to value the Fund’s investments carried at fair value as of July 31, 2011:

27

THE MEXICO EQUITY AND INCOME FUND, INC.

July 31, 2011

Notes to Financial Statements (continued)

|

Level 1*

|

Level 2*

|

Level 3

|

Total

|

|||||||||||||

|

Equity

|

||||||||||||||||

|

Beverages

|

$ | 6,490,339 | $ | — | $ | — | $ | 6,490,339 | ||||||||

|

Capital Development Certificates

|

— | — | 2,686,760 | 2,686,760 | ||||||||||||

|

Chemicals

|

8,247,758 | — | — | 8,247,758 | ||||||||||||

|

Commercial Banks

|

3,821,814 | — | — | 3,821,814 | ||||||||||||

|

Construction & Engineering

|

4,030,750 | — | — | 4,030,750 | ||||||||||||

|

Consumer Finance

|

358,018 | — | — | 358,018 | ||||||||||||

|

Diversified Telecommunication Services

|

662,998 | — | — | 662,998 | ||||||||||||

|

Food & Staples Retailing

|

6,116,187 | — | — | 6,116,187 | ||||||||||||

|

Food Products

|

1,024,958 | — | — | 1,024,958 | ||||||||||||

|

Health Care Providers & Services

|

1,874,413 | — | — | 1,874,413 | ||||||||||||

|

Hotels, Restaurants & Leisure

|

1,865,444 | 3,971,382 | — | 5,836,826 | ||||||||||||

|

Industrial Conglomerates

|

3,256,750 | — | — | 3,256,750 | ||||||||||||

|

Insurance

|

3,738,535 | — | — | 3,738,535 | ||||||||||||

|

Metals & Mining

|

4,791,332 | — | — | 4,791,332 | ||||||||||||

|

Multiline Retail

|

8,442,381 | — | — | 8,442,381 | ||||||||||||

|

Pharmaceuticals

|

7,950,046 | — | — | 7,950,046 | ||||||||||||

|

Wireless Telecommunication Services

|

15,800,812 | — | — | 15,800,812 | ||||||||||||

|

Total Equity

|

78,472,535 | 3,971,382 | 2,686,760 | 85,130,677 | ||||||||||||

|

Real Estate Investment Trusts

|

$ | 2,426,367 | $ | — | $ | — | $ | 2,426,367 | ||||||||

|

Corporate Bonds

|

$ | — | $ | 479,752 | $ | — | $ | 479,752 | ||||||||

|

Mexican Government Bonds

|

$ | — | $ | 1,228,300 | $ | — | $ | 1,228,300 | ||||||||

|

Short-Term Investments

|

$ | 299,971 | $ | 445,739 | $ | — | $ | 745,710 | ||||||||

|

Total Investment in Securities

|

$ | 81,198,873 | $ | 6,125,173 | $ | 2,686,760 | $ | 90,010,806 | ||||||||

|

*

|

There were no significant transfers between levels 1 and 2 during the period. Transfers between levels are recognized at the end of the reporting period.

|

28

THE MEXICO EQUITY AND INCOME FUND, INC.

July 31, 2011

Notes to Financial Statements (continued)

Level 3 Reconciliation Disclosure

Following is a reconciliation of Level 3 assets for which significant unobservable inputs were used to determine fair value.

|

Description

|

Investments in Securities

|

|||

|

Balance as of July 31, 2010

|

$ | 2,370,277 | ||

|

Acquisition/Purchase

|

||||

|

Sales

|

— | |||

|

Realized gain

|

— | |||

|

Change in unrealized appreciation (depreciation)(1)

|

316,483 | |||

|

Balance as of July 31, 2011

|

$ | 2,686,760 | ||

(1) Included in the net change of unrealized appreciation (depreciation) on investments in the Statement of Operations.

Federal Income Taxes. The Fund intends to comply with the requirements of the Internal Revenue Code necessary to qualify as a regulated investment company and to make the requisite distributions of income and capital gains to its shareholders sufficient to relieve it from all or substantially all federal income taxes. Therefore, no federal income tax provision is required. Accounting principles generally accepted in the United States of America require that permanent differences between financial reporting and tax reporting be reclassified between various components of net assets.

The Fund recognizes the tax benefits of uncertain tax positions only where the position is “more-likely-than-not” to be sustained assuming examination by tax authorities. The Adviser has analyzed the Fund’s tax positions, and has concluded that no liability for unrecognized tax benefits should be recorded related to uncertain tax positions taken on returns filed for open tax years (2008-2010), or expected to be taken in the Fund’s 2011 tax returns. The Fund identifies its major tax jurisdictions as U.S. Federal, New York State and foreign jurisdictions where the Fund makes significant investments; however the Fund is not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will change materially in the next twelve months.

The Fund intends to utilize provisions of the federal income tax laws which allow it to carry a realized capital loss forward and offset such losses against any future realized capital gains. At July 31, 2011, the Fund had accumulated capital loss carryforwards for tax purposes as follows:

|

Date of Expiration

|

Amount

|

|

July 31, 2017

|

$1,330,397

|

As of July 31, 2011, the Fund deferred post-October losses of $2,371,184, which will be recognized in the fiscal year ending July 31, 2012.

29

THE MEXICO EQUITY AND INCOME FUND, INC.

July 31, 2011

Notes to Financial Statements (continued)

Reclassification of Capital Accounts. Accounting Principles generally accepted in the United States of America require certain components of net assets relating to permanent differences be reclassified between financial and tax reporting. These reclassifications have no effect on net assets or net asset value per shares. The permanent differences are primarily attributed to foreign currency gain reclassifications. For the year ended July 31, 2011, the Fund decreased undistributed net investment loss by $593,414, increased accumulated realized loss by $94,240 and decreased paid in capital by $499,174.

Foreign Currency Translation. The books and records of the Fund are maintained in U.S. dollars. Foreign currency amounts are translated into U.S. dollars on the following basis:

|

(i)

|

market value of investment securities, assets and liabilities at the current Mexican peso exchange rate on the valuation date, and

|

|

(ii)

|

purchases and sales of investment securities, income and expenses at the Mexican peso exchange rate prevailing on the respective dates of such transactions. Fluctuations in foreign currency rates, however, when determining the gain or loss upon the sale of foreign currency denominated debt obligations pursuant to U.S. Federal income tax regulations; such amounts are categorized as foreign exchange gain or loss for income tax reporting purposes.

|

The Fund reports realized foreign exchange gains and losses on all other foreign currency related transactions as components of realized gains and losses for financial reporting purposes, whereas such gains and losses are treated as ordinary income or loss for Federal income tax purposes.

Securities denominated in currencies other than U.S. dollars are subject to changes in value due to fluctuations in the foreign exchange rate. Foreign security and currency transactions may involve certain considerations and risks not typically associated with those of domestic origin as a result of, among other factors, the level of governmental supervision and regulation of foreign securities markets and the possibilities of political or economic instability.