As filed with the U.S. Securities and Exchange Commission on April 23, 2024

Registration Nos. 333-147508

811-06025

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-6

Registration

Statement

| Under the

Securities Act of 1933 |

☐ |

| Pre-Effective Amendment No. |

☐ |

| Post-Effective Amendment No. 20 |

☒ |

Registration

Statement

| Under the

Investment Company Act of 1940 |

☐ |

| Amendment No. 136 |

☒ |

Metropolitan Life Separate Account UL

(Exact Name of Registrant)

Metropolitan Life Insurance Company

(Name of Depositor)

(Name of Depositor)

200 Park Avenue

New York, NY 10166

(Address of depositor's principal executive offices)

New York, NY 10166

(Address of depositor's principal executive offices)

Depositor’s Telephone Number, including Area Code: (212) 578-9500

Monica Curtis

Executive Vice President and Chief Legal Officer

Metropolitan Life Insurance Company

200 Park Avenue

New York, NY 10166

(Name and Address of Agent for Service)

Executive Vice President and Chief Legal Officer

Metropolitan Life Insurance Company

200 Park Avenue

New York, NY 10166

(Name and Address of Agent for Service)

Copy to:

W. Thomas Conner, Esq.

Carlton Fields

1025 Thomas Jefferson Street, NW, Suite

400 West

Washington, DC 20007-5208

Carlton Fields

1025 Thomas Jefferson Street, NW, Suite

400 West

Washington, DC 20007-5208

Approximate Date of Proposed Public Offering:

April 29, 2024

It is proposed that this filing will become effective (check appropriate

box)

| ☐ |

immediately upon filing pursuant to paragraph (b) |

| ☒ |

on April 29, 2024 pursuant to paragraph (b) |

| ☐ |

60 days after filing pursuant to paragraph (a)(1) |

| ☐ |

on (date) pursuant to paragraph (a)(1) of Rule 485 |

| | |

| If appropriate, check the following box: | |

| ☐ |

this post-effective amendment designates a new effective date for a previously filed post-effective amendment |

April 29, 2024

Equity Advantage VUL

Flexible Premium Variable Life Insurance Policies

Issued by Metropolitan Life Separate Account UL of Metropolitan Life

Insurance Company

Prospectus

This Prospectus provides you with important information about MetLife’s Equity Advantage VUL Policy ("Policy"). However, this Prospectus is not the Policy. The Policy, rather, is a separate written agreement that Metropolitan Life Insurance Company (“Metropolitan Life”, “MetLife”, “we”, “us”, “our”) issued to you. There may be differences between the description of the

Policy contained in this Prospectus and the Policy issued to you due to differences in state law. Please consult your Policy for the provisions that apply in your state. The Policy is no longer available for sale.

You allocate net Premiums among the Divisions of Metropolitan Life

Separate Account UL (the “Separate Account”). Each Division of the Separate Account invests in shares of one of the “Portfolios” listed in Appendix A. (Divisions may be referred to as “Investment Divisions” in your Policy.)

You may also allocate net Premiums to our Fixed Account. Special limits

may apply to Fixed Account transfers and withdrawals.

Additional information about certain investment products, including variable life insurance, has been prepared by the Securities and Exchange Commission’s staff and is available at Investor.gov.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these policies or determined if this Prospectus is accurate or complete. Any representation to the contrary is a criminal offense.

We do not guarantee how any of the Divisions or Portfolios will

perform. Interests in the Separate Account, the Fixed

Account and the Portfolios are not deposits or obligations of, or guaranteed or endorsed by, any financial institution and are not federally insured by the U.S. Government, any bank or other depository institution including the Federal Deposit Insurance Corporation (“FDIC”), the Federal Reserve Board or any other agency or entity or person. We do not authorize any representations about this offering other than as contained in this Prospectus or its supplements or in our authorized supplemental sales material, the Federal Reserve Board or any other government agency.

TABLE OF CONTENTS

| 4 | |

| 6 | |

| 8 | |

| 12 | |

| 17 | |

| 17 | |

| 17 | |

| 18 | |

| 19 | |

| 19 | |

| 20 | |

| 20 | |

| 20 | |

| 21 | |

| 21 | |

| 21 | |

| 22 | |

| 22 | |

| 22 | |

| 23 | |

| 23 | |

| 24 | |

| 24 | |

| 24 | |

| 25 | |

| 26 | |

| 27 | |

| 28 | |

| 28 | |

| 29 | |

| 29 | |

| 30 | |

| 30 | |

| 31 | |

| 33 | |

| 33 | |

| 33 | |

| 36 | |

| 36 | |

| 37 | |

| 37 | |

| 38 | |

| 39 | |

| 45 | |

| 45 |

2

IMPORTANT INFORMATION YOU SHOULD CONSIDER ABOUT THE POLICY

| |

FEES AND EXPENSES |

LOCATION IN

PROSPECTUS | ||

| Charges for Early

Withdrawal |

If, during the first ten Policy years, or during the first ten Policy

years following a face amount increase, you surrender or

lapse your Policy, reduce the face amount, or make a

partial withdrawal or make a change in death benefit

option that reduces the face amount, then we will deduct

a Surrender Charge from the Cash Value.

The maximum surrender charge is 3.825% of specified face amount.

For example, the maximum surrender charge during the

first year after issue (or a specified face amount

increase), assuming an initial face amount (or subsequent

specified face amount increase) of $100,000, is

$3,825. |

“Charges -Surrender

Charge, Partial

Withdrawal Charge” | ||

| Transaction Charges |

In addition to surrender charges,

you also may be charged for other

transfer

Cash Value between investment options, make a partial

withdrawal or request an illustration if

you have requested more

than one illustration in a year). |

|||

| Ongoing Fees and

Expenses (annual

charges) |

In addition to surrender charges and transaction charges, an

investment in the Policy is subject to certain ongoing

fees and expenses, including fees and expenses covering

the cost of insurance under the Policy and optional

benefits added by rider, and such fees and expenses are

set based on characteristics of the insured (e.g., age, sex and risk classification). There is also a mortality and

expense risk charge deducted. You should review the

Policy specifications page of your Policy for rates

applicable to your Policy.

You will also bear expenses associated with the Portfolios available

under your Policy, as shown in the following table: |

|||

| ANNUAL FEE |

MIN. |

MAX. | ||

| Investment options (

Portfolio fees

and charges) |

0.28% |

1.06% | ||

| |

RISKS |

LOCATION IN

PROSPECTUS | ||

| Risk of Loss |

You can lose money by investing in this Policy, including loss of principal. |

“Principal Risks” | ||

| Not a Short- Term

Investment |

The Policies are designed to provide lifetime insurance protection.

They should not be used as a short-term investment or if

you need

surrendering the Policy. In addition, withdrawals may be subject to

ordinary income tax or tax penalties. |

“Principal Risks” | ||

| Risks Associated with

Investment Options |

An investment in this Policy is subject to the risk of poor investment

performance and can vary depending on the performance of

the investment options available under the Policy (e.g.,

Portfolios). Each investment option (including any Fixed Account investment option)

has its own unique risks.

You should review the investment options

before making an investment decision. |

“Principal Risks” | ||

4

| |

RISKS |

LOCATION IN

PROSPECTUS | ||

| Insurance Company

Risks |

Investments in the Policy are subject to the risks related to

Metropolitan Life, including any obligations (including

under any Fixed Account investment option), guarantees, and benefits of

the Policy, including any death benefit, which are

subject to the claims paying ability of Metropolitan

Life. If Metropolitan Life experiences financial

distress, it may not be able to meet its obligations to you. More information about Metropolitan Life, including its financial

strength ratings, is available upon request by calling 1-800-638-5000

or visiting:

https://www.metlife.com/about-us/corporate-profile/

ratings. |

“Prinicipal Risks” | ||

| Contract Lapse |

Your Policy may lapse if

you have not paid a sufficient amount of

Premiums

or if the investment experience of the Portfolios is poor,

you have taken partial withdrawals, and the

cash surrender value

under your Policy is insufficient to cover the monthly deduction.

Lapse of a Policy on which there is an outstanding loan

may have adverse tax consequences. If the Policy lapses,

no death benefit will be paid. A Policy may be reinstated

if the conditions for reinstatement are met including the

payment of required Premiums. |

“Prinicipal Risks” | ||

| |

RESTRICTIONS |

LOCATION IN

PROSPECTUS | ||

| Investments |

Policy Owners may transfer

Cash Value between and among the

Divisions

and the Fixed Account. There are limitations on transfers

from the

Fixed Account and limits on the minimum amount Policy

Owners may transfer. Metropolitan Life also reserves the

right to limit transfers to four (4) per Policy year and

to impose a charge of $25 per transfer. Restrictions may

apply to frequent transfers.

Metropolitan Life reserves the right to remove or substitute

Portfolios as investment options that are available under

the Policy. |

“Transfer Charge” and

“Transfers” | ||

| Optional Benefits |

The Option to Purchase Additional Insurance Coverage Rider,

Overloan Protection Rider, Guaranteed Survivor Income

Benefit Rider and Guaranteed Minimum Death Benefit Rider

were available to be elected at Policy issue only. You may not elect both the Waiver

of Monthly Deduction Rider and the Waiver of Specified

Premium

Rider. |

“Additional Benefits” | ||

| |

TAXES |

LOCATION IN

PROSPECTUS | ||

| Tax Implications |

Consult with a tax professional to determine the tax implications of

an investment in and payments received under this

Policy. Withdrawals may be subject to ordinary income tax,

and may be subject to tax penalties.

Lapse of a Policy on which there is an outstanding loan may have

adverse tax consequences. |

“Tax Considerations” | ||

| |

CONFLICTS OF INTEREST |

LOCATION IN

PROSPECTUS | ||

| Investment

Professional

Compensation |

Your investment professional may receive compensation relating to

your ownership of a Policy, both in the form of

commissions and continuing payments. This conflict of

interest may influence your investment professional when

advising you on your Policy. |

“Distribution of the Policies” | ||

5

| |

CONFLICTS OF INTEREST |

LOCATION IN

PROSPECTUS | ||

| Exchanges |

“The Policies-Replacing Existing Insurance” | |||

OVERVIEW OF THE POLICY

Purpose of the Policy

The Policy is designed to provide lifetime insurance coverage on the insured(s) named in the Policy, as well as maximum flexibility in connection with Premium payments and death benefits. This flexibility allows you to provide for changing insurance needs within the confines of a single insurance policy. The Policy also provides tax deferred accumulation of assets as well as favorable tax treatment of insurance proceeds. The Policy may be appropriate for an investor who has a longer time horizon, is not purchasing the Policy for short-term liquidity needs and desires life insurance coverage.

Payment of Premiums

A Policy Owner has considerable flexibility concerning the amount and frequency of Premium payments. The Policy Owner elected in the application when the Policy was first purchased. The Policy Owner could have elected to pay Premiums annually, on a monthly “check-o-matic” (or payroll deduction plan if provided by the employer of the Policy Owner) quarterly or semi-annual basis. The schedule will provide for a Premium payment of a level amount determined by the Policy Owner at fixed intervals over a specified period of time. A Policy Owner need not adhere to the planned periodic Premium payment schedule. Instead, generally, a Policy Owner may make Premium

payments in any amount above the $50 minimum and at any frequency up until the Policy anniversary when the insured reaches age 121. The Policy Owner may be required to make an unscheduled Premium payment in order to keep the Policy in force. The payment of a given Premium will not necessarily guarantee that your Policy will remain in force. Rather, this depends on the Policy’s cash surrender value. Insufficient Premiums may result in lapse of the Policy. Premiums may be allocated among the Divisions and the Fixed Account. If you terminate your participation in optional benefits which have allocations to specific Divisions, you will remain invested in the same Divisions until you request allocations to different Divisions. Additional information

about each Portfolio including its Portfolio type, advisers and any sub-advisers as well as current expenses and certain performance information is included in Appendix A.

Features of the Policy

The Policy has a number of features designed to provide lifetime insurance coverage as well as maximum flexibility in connection with Premium payments and death benefits, including flexibility to change the type and amount of the death benefit; flexibility in paying Premiums; loan privileges; surrender privileges; and optional insurance benefits.

Death Benefit. The Policy is designed to provide insurance protection. Upon receipt of

satisfactory proof of the death of the insured, we pay death proceeds to the beneficiary of the Policy. Death proceeds generally equal the death benefit on the date of the insured’s death plus any additional insurance provided by rider, less any outstanding loan and accrued loan interest.

6

Choice of Death Benefit Option. You may choose among three death benefit

options:

•

a level death benefit that equals the Policy’s face amount;

•

a variable death benefit that equals the Policy’s face amount plus the

Policy’s Cash Value; and

•

a combination variable and level death benefit that equals the Policy’s face

amount plus the Policy’s Cash Value until the insured attains age 65 and equals the Policy’s face amount thereafter.

The death benefit under

any option could increase to satisfy Federal tax law requirements if the Cash Value reaches certain levels. After the first Policy year you may change your death benefit

option, subject to our underwriting rules. A change in death benefit option may have tax consequences.

Investment Options. You can allocate your net Premiums and Cash Value among your choice of Divisions available in the

Separate Account, each of which corresponds to and invests in a mutual fund portfolio, or “Portfolio.” The Portfolios available under the Policy include

several common stock funds, including funds which invest primarily in foreign securities, as well as bond funds, balanced funds, asset allocation funds and funds that

invest in exchange-traded funds. You may also allocate Premiums and Cash Value to our Fixed Account which provides guarantees of interest and principal. You may change your allocation of future Premiums at any time.

Additional information about each Portfolio is provided

in Appendix A.

Partial Withdrawals. You may withdraw cash surrender value from your Policy at any time after the first Policy anniversary.

The minimum amount you may withdraw is $500. We reserve the right to limit partial withdrawals to no more than 90% of the Policy’s cash surrender value. We may

limit the number of partial withdrawals to 12 per Policy year or impose a processing charge of $25 for each partial withdrawal. Partial withdrawals may have tax consequences.

Transfers and Automated Investment Strategies. You may transfer your Policy’s

Cash Value among the Divisions or between the Divisions and the Fixed Account. The minimum amount you may transfer is $50, or if less, the total amount in the Division or the Fixed Account. We may limit the number of transfers among the Divisions and the Fixed Account to no more than four per Policy year. We may impose a processing charge of $25 for each transfer. We may also impose restrictions on frequent transfers. (See “Transfers” for additional information on such restrictions.) We offer five automated investment strategies that allow you to periodically transfer or reallocate your Cash Value among the Divisions and the Fixed Account. If You terminate your participation in optional

benefits which have allocations to specific Divisions, You will remain invested in the same Divisions until You request allocations to different Divisions. (See “Automated Investment Strategies”)

Loans. You may borrow from the Cash Value of your

Policy. The minimum amount you may borrow is $500. The maximum amount you may borrow is an amount equal to the Policy’s Cash Value net of the Surrender Charge,

reduced by Monthly Deductions and interest charges through the next Policy anniversary, increased by interest credits through the next Policy anniversary, less any existing Policy loans. We charge you a maximum annual interest rate of 4.0% for the first ten Policy years and 3.0% thereafter. We credit interest at an annual rate of at least 3.0% on amounts we hold as collateral to support your loan. Loans may have tax consequences. (See “Loans” for additional information.)

Surrenders. You may surrender the Policy for its cash surrender value at any time. Cash

surrender value equals the Cash Value reduced by any Policy loan and accrued loan interest and by any applicable Surrender Charge. A surrender may have tax consequences.

7

Supplemental Benefits and Riders. We offer a variety of riders that provide

supplemental benefits under the Policy. These include the Children's Term Insurance Rider, Waiver of Monthly Deduction Rider, Waiver of Specified Premium Rider, Options to Purchase Additional Insurance Coverage Rider, Accidental Death Benefit Rider,

Acceleration of Death Benefit Rider, Guaranteed Survivor Income Benefit Rider, Guaranteed Minimum Death Benefit Rider and Overloan Protection Rider. We generally deduct any monthly charges for these riders as part of the Monthly Deduction.

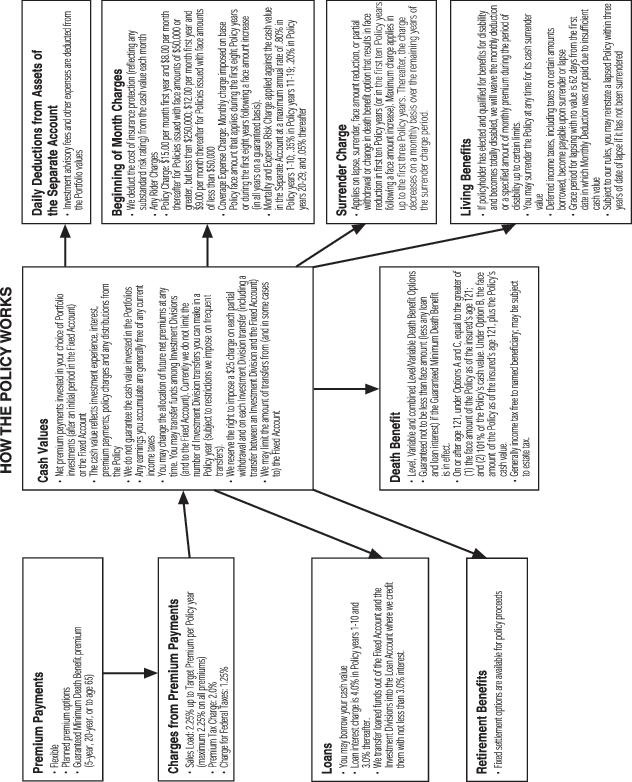

FEE TABLES

The following tables describe the fees and expenses that a Policy Owner will pay when buying, owning and surrendering or making withdrawals from the Policy. Please refer to your Policy’s specifications page for information about the specific fees you will pay each year based on the options that you have elected.

The first table describes the fees and expenses that you will

pay at the time you buy the Policy, surrender the Policy, make withdrawals from the Policy, or transfer Cash Value among Divisions or the Fixed

Account.

Transaction Fees

| Charge |

When Charge is

Deducted |

Maximum Amount

Deducted |

Current Amount

Deducted |

| Maximum Sales Charge Imposed on

Premiums ("loads") |

On payment of

Premium |

2.25% of each Premium

paid |

2.25% of Premiums paid up

to the Target Premium per

Policy year |

| State Premium Tax |

On payment of

Premium |

2.0% in all Policy years |

2.0% in all Policy years |

| Federal Premium Tax |

On payment of

Premium |

1.25% in all Policy years |

1.25% in all Policy years |

| Surrender Charge1 |

|

|

|

| Minimum and Maximum Charge |

On surrender, lapse,

or face amount

reduction in the first

ten (10) Policy years

(and, with respect to

a face amount

increase, in the first

ten (10) Policy years

after the increase) |

In Policy year 1, $3.75 to

$38.25 per $1,000 of base

Policy face amount2 |

In Policy year 1, $3.75 to

$38.25 per $1,000 of base

Policy face amount2 |

| Representative Insured3 |

$14.00 per $1,000 of base

Policy face amount |

$14.00 per $1,000 of base

Policy face amount | |

| Transfer Charge |

On transfer of Cash

Value among the

Divisions and to and

from the Fixed

Account |

$25 for each transfer |

Not currently charged |

| Partial Withdrawal Charge |

On partial

withdrawal of cash

value |

$25 for each partial

withdrawal4 |

Not currently charged |

| Illustration of Benefits Charge |

Charge for each

illustration in excess

of one per year |

$25 per illustration |

Not currently charged |

| Acceleration of Death Benefit Rider |

At time of benefit

payment |

One-time fee of $150 |

Not currently charged |

8

| Charge |

When Charge is

Deducted |

Maximum Amount

Deducted |

Current Amount

Deducted |

| Overloan Protection Rider |

At time of exercise |

One-time fee of 3.5% of

Policy cash value |

One-time fee of 3.5% of Policy cash value |

1

The Surrender Charge varies based on individual characteristics, including the

insured’s issue age, risk class, sex (except for unisex Policies), smoker status, and the Policy’s face amount. The Surrender Charge may not be representative

of the charge that a particular Policy Owner would pay. You can obtain more information about the Surrender Charge that would apply for a particular insured by contacting your registered representative.

2

No Surrender Charge will apply on up to 10% of cash surrender value withdrawn each

year. The Surrender Charge will remain level for one to three Policy years, and will then begin to decline on a monthly basis until it reaches zero in the last month of the tenth Policy year. The Surrender Charge applies to requested face amount reductions as well as to face amount reductions resulting from a change in death benefit option.

3

The representative insured is a male, age 35, in the preferred nonsmoker risk class,

under a Policy with a base Policy face amount of $375,000.

4

If imposed, the partial withdrawal charge would be in addition to any Surrender

Charge that is imposed.

The next table describes the fees and expenses that you will pay periodically during the time that you own the Policy, not including Portfolio fees and expenses.

Periodic Charges other than Portfolio Operating

Expenses

| Charge |

When Charge is

Deducted |

Maximum Amount

Deducted |

Current Amount

Deducted |

| Base Policy Charges: |

|

|

|

| Cost of Insurance (1) |

|

|

|

| •Minimum and Maximum Charge |

Monthly |

$0.02 to $83.33 per $1,000

of net amount at risk(2) |

$0.01 to $83.33 per $1,000

of net amount at risk(2) |

| •Charge for a representative insured (3) |

$0.09 per $1,000 of net

amount at risk |

$0.02 per $1,000 of net

amount at risk | |

| Policy Charge(4) |

|

|

|

| •Policy face amount less than $50,000 |

Monthly |

$12 |

$12 |

| •Policy face amount between $50,000 and $249,999 |

$15 |

$15 | |

| Mortality and Expense Risk Charge(5) |

Daily |

Effective annual rate of

0.80% |

Effective annual rate of

0.60% |

| Coverage Expense Charge (6),(7) |

|

|

|

| •Minimum and Maximum Charge |

Monthly |

$0.04 to $2.30 per $1,000 of

base Policy face amount |

$0.04 to $2.30 per $1,000 of

base Policy face amount |

| •Charge for a representative insured (3) |

$0.16 per $1,000 of base

Policy face amount |

$0.16 per $1,000 of base

Policy face amount | |

| Loan Interest Spread(8) |

Annually |

Annual rate of 1% of loan

collateral |

Annual rate of 1% of loan

collateral |

| Optional Benefit Charges: |

|

|

|

| Guaranteed Survivor Income Benefit

Rider(9)

|

|

|

|

| •Minimum and Maximum Charge |

Monthly |

$0.01 to $83.33 per $1,000

of Eligible Death Benefit |

$0.01 to $1.08 per $1,000 of

Eligible Death Benefit |

| •Charge for a representative insured(3)

|

$0.02 per $1,000 of Eligible

Death Benefit |

$0.02 per $1,000 of Eligible

Death Benefit | |

| Children’s Term Insurance Rider |

Monthly |

$0.40 per $1,000 of rider

face amount |

$0.40 per $1,000 of rider face amount |

9

| Charge |

When Charge is

Deducted |

Maximum Amount

Deducted |

Current Amount

Deducted |

| Waiver of Monthly Deduction Rider(10) |

|

|

|

| •Minimum and Maximum Charge |

Monthly |

$0.00 to $61.44 per $100 of

monthly deduction |

$0.00 to $61.44 per $100 of

monthly deduction |

| •Charge for a representative insured(3)

|

$6.30 per $100 of monthly

deduction |

$6.30 per $100 of monthly

deduction | |

| Waiver of Specified Premium Rider(10) |

|

|

|

| •Minimum and Maximum Charge |

Monthly |

$0.00 to $21.75 per $100 of

Specified Premium |

$0.00 to $21.75 per $100 of

Specified Premium |

| •Charge for a representative insured(3)

|

$3.00 per $100 of Specified

Premium |

$3.00 per $100 of Specified

Premium | |

| Option to Purchase Additional

Insurance Coverage Rider (10) |

|

|

|

| •Minimum and Maximum Charge |

Monthly |

$0.02 to $0.25 per $1,000 of

Option amount |

$0.02 to $0.25 per $1,000 of

Option amount |

| •Charge for a representative insured(3)

|

$0.03 per $1,000 of Option

amount |

$0.03 per $1,000 of Option

amount | |

| Accidental Death Benefit Rider(10) |

|

|

|

| •Minimum and Maximum Charge |

Monthly |

$0.00 to $83.33 per $1,000

of rider face amount |

$0.00 to $0.34 per $1,000 of

rider face amount |

| •Charge for a representative insured(3)

|

$0.08 per $1,000 of rider

face amount |

$0.05 per $1,000 of rider

face amount | |

| Guaranteed Minimum Death Benefit

(10), (11) |

|

|

|

| •Minimum and Maximum Charge |

Monthly |

$0.03 to $83.33 per $1,000

of net amount at risk |

$0.03 to $0.14 per $1,000 of

net amount at risk |

| •Charge for a representative insured(3)

|

$0.03 per $1,000 of net

amount at risk |

$0.03 per $1,000 of net amount at risk |

1

The cost of insurance charge varies based on individual characteristics, including

the Policy’s face amount and the insured’s age, risk class, and (except for unisex Policies) sex. The cost of insurance charge may not be representative of

the charge that a particular Policy Owner would pay. You can obtain more information about the cost of insurance charge that would apply for a particular insured by contacting your registered representative.

2

The net amount at risk is the difference between the death benefit (generally

discounted at the monthly equivalent of 3% per year) and the Policy’s Cash Value.

3

The representative insured is a male, age 35, in the preferred nonsmoker risk class,

under a Policy with a base Policy face amount of $375,000.

4

After the first Policy Year, the Policy Charge declines to $9 for a Policy with a

face amount of less than $50,000, and to $8 for a Policy with a face amount between $50,000 and $249,999. No Policy Charge applies if a Policy is issued with a face

amount equal to or greater than $250,000.

5

The Mortality and Expense Risk Charge declines over time in accordance with the

following schedule:

| |

Maximum

Charge |

Current

Charge |

| Policy years 1 - 10 |

.80% |

.60% |

| Policy years 11 - 19 |

.35% |

.35% |

| Policy years 20 –29 |

.20% |

.20% |

| Policy years 30+ |

.05% |

.05% |

The current charge percentages shown above apply if the Policy’s net Cash Value

is less than the equivalent of five Target Premiums. The percentages decrease as the Policy’s net Cash Value, measured as a multiple of Target Premiums, increases, as shown below:

10

| |

Less

than 5 target premiums |

At least

5 but less than 10 target premiums |

At least

10 but less than 20 target premiums |

20 or

more target premiums |

| Policy years 1- 10 |

0.60% |

0.55% |

0.30% |

0.15% |

| Policy years 11- 19 |

0.35% |

0.30% |

0.15% |

0.10% |

| Policy years 20- 29 |

0.20% |

0.15% |

0.10% |

0.05% |

| Policy years 30+ |

0.05% |

0.05% |

0.05% |

0.05% |

6

The Coverage Expense Charge varies based on individual characteristics, including

the Policy’s face amount and the insured’s age, risk class, and (except for unisex Policies) sex. The Coverage Expense Charge may not be representative of

the charge that a particular Policy Owner would pay. You can obtain more information about the Coverage Expense Charge that would apply to a particular insured by contacting your registered representative.

7

The Coverage Expense Charge is imposed in Policy years 1-8 and, with respect to a

requested face amount increase, during the first eight years following the increase. If you surrender the Policy in the first Policy year (or in the first year following a face amount increase), we will deduct from the surrender proceeds an amount equal to the Coverage Expense Charges due for the remainder of the first Policy year (or the first year following the face amount increase). If the Policy’s face amount is reduced in the first year following a face amount increase, we will deduct from the Cash Value an amount equal to the Coverage Expense Charges due for the remainder of the first year following the face amount increase.

8

The loan interest spread is the difference between the interest rates we charge on Policy loans and the interest earned on Cash Value we hold as security for the loan (“loan collateral”). We charge interest on Policy loans at an effective rate of 4.0% per year in Policy years 1-10 and 3.0% thereafter. Loan collateral earns interest at an effective rate of not less than 3.0% per year. The maximum loan interest spread is 1% per year of the loan collateral.

9

The charge for the Guaranteed Survivor Income Benefit Rider varies based on

individual characteristics, including the rider’s Eligible Death Benefit and the insured’s age, risk class, and (except for unisex Policies) sex. The rider

change may not be representative of the charge that a particular Policy Owner would pay. You can obtain more information about the rider charge that would apply for a particular insured by contacting your registered representative.

10

The charge for this rider varies based on individual characteristics, including the

insured’s age, risk class, and (except for unisex Policies) sex. The rider charge may not be representative of the charge that a particular Policy Owner would pay.

You can obtain more information about the rider charge that would apply for a particular insured by contacting your registered representative.

11

The charge shown applicable to both the Guaranteed Minimum Death Benefit to age 85

Rider and the Guaranteed Minimum Death Benefit to age 121 Rider.

The next table shows the minimum and maximum total operating

expenses charged by the Portfolios that you may pay periodically during the time that you own the Policy. A complete list of the Portfolios available

under the Policy, including their current expenses, may be found in Appendix A.

Annual Portfolio Expenses

| Annual Portfolio Expenses |

Minimum |

Maximum |

| Expenses that are deducted from Portfolio assets,

including management fees, distribution

and/or service (12b-1) fees, and other expenses |

0.28% |

1.06% |

11

PRINCIPAL RISKS

Investment Risk. We do not guarantee the investment performance of the Divisions and

you should consider your risk tolerance before selection Divisions. If you invest your Policy’s Cash Value in one or more of the Divisions, then you will be subject

to the risk that investment performance will be unfavorable and that your Cash Value will decrease. In addition, we deduct Policy fees and charges from your

Policy’s Cash Value, which can significantly reduce your Policy’s Cash Value. During times of poor investment performance, this deduction will have an even

greater impact on your Policy’s Cash Value. It is possible to lose your full investment and your Policy could lapse without value, unless you pay additional Premium.

If you allocate Cash Value to the Fixed Account, then we credit such Cash Value with a declared rate of interest. You assume the risk that the rate may decrease, although it will never be lower than the guaranteed minimum annual effective rate of 3%.

Surrender and Withdrawal Risks (Short-Term Investment Risk). The Policies are designed

to provide lifetime insurance protection. They are not offered primarily as an investment and should not be used as a short-term savings vehicle. Subject to the free withdrawal provision, if you surrender the Policy within the first ten (10) Policy years (or within the first ten (10) Policy years following a face amount increase), you will be subject to a Surrender Charge as well as income tax on any gain that is distributed or deemed to be distributed from the Policy. You will also be subject to a Surrender Charge if you make a partial withdrawal from the Policy within the first ten (10) Policy years (or the first ten (10) Policy years following the face amount increase) if the partial withdrawal reduces the face amount (or the face amount increase). If you surrender the Policy in the first Policy year (or in the first year following a face amount increase) we will also deduct an amount equal to the remaining first year Coverage Expense Charges.

You should purchase the Policy only if you have the financial ability to keep it in force for a substantial period of time. You should not purchase the Policy if you intend to surrender all or part of the Policy’s Cash Value in the near future. Even if you do not ask to surrender your Policy, surrender charges may play a role in determining whether your Policy will lapse (terminate without value), because surrender charges determine the cash surrender value, which is a measure we use to determine whether your Policy will enter the grace period (and possibly lapse).

Risk of Lapse. Your Policy may lapse if you have not paid a sufficient amount of Premiums or if the investment

experience of the Divisions is poor. If your cash surrender value is not enough to pay the Monthly Deduction, your Policy may enter a 62-day grace period. We will notify you that the Policy will lapse unless you make a sufficient payment of additional Premium during the grace period. Your Policy generally will not lapse if you pay certain required Premium amounts and you are therefore protected by a Guaranteed Minimum Death Benefit. If your

Policy does lapse, your insurance coverage will terminate, although you will be given an opportunity to reinstate it. Lapse of a Policy on which there is an outstanding loan may have adverse tax consequences.

Tax Treatment. We anticipate that the Policy should

be deemed to be a life insurance contract under Federal tax law. However, the rules are not entirely clear in certain circumstances, for example, if your Policy is issued

on a substandard basis. The death benefit under the Policy will never be less than the minimum amount required for the Policy to be treated as life insurance under section 7702 of the Internal Revenue Code (the “Code”), as in effect on the date the Policy was issued. If your Policy is not treated as a life insurance contract under Federal tax law, increases in the Policy’s Cash Value will be taxed currently.

Even if your Policy is treated as a life insurance contract for Federal tax purposes, it may become a modified endowment contract (“MEC”) due to the payment of excess Premiums or unnecessary Premiums, due to a material

12

change

or due to a reduction in your death benefit. If your Policy becomes a MEC, surrenders, partial withdrawals, loans, and use of the Policy as collateral for a loan will be

treated as a distribution of the earnings in the Policy and will be taxable as ordinary income to the extent thereof. In addition, if the Policy Owner is under age

59 1∕2 at the time of the

surrender, partial withdrawal or loan, the amount that is included in income will generally be subject to a 10% penalty tax.

If the Policy is not a modified endowment contract, distributions generally

will be treated first as a return of basis or investment in the Policy and then as taxable income. However, different rules apply in the first fifteen Policy years, as distributions accompanied by benefit reductions may be taxable prior to a complete withdrawal of your investment in the Policy. Moreover, loans will generally not be treated as distributions prior to termination of your Policy, whether by lapse, surrender or exchange.

See “Tax Considerations” You should consult a qualified tax adviser for

assistance in all Policy-related tax matters.

Loans. A Policy loan, whether or not repaid, will affect the Cash Value of your Policy over time because we subtract the amount of the loan from the Divisions and/or Fixed Account as collateral, and hold it in our Loan Account. This loan collateral does not participate in the investment experience of the Divisions or receive any higher current interest rate credited to the Fixed Account.

We also reduce the amount we pay on the insured’s death by the amount of any outstanding loan and accrued loan interest. Your Policy may lapse if your outstanding loan and accrued loan interest reduce the cash surrender value to zero.

If you surrender your Policy or your Policy lapses while there is an outstanding loan, there will generally be Federal income tax payable on the amount by which loans and partial withdrawals exceed the Premiums paid. Since loans and partial withdrawals reduce your Policy’s Cash Value, any remaining Cash Value may be insufficient to pay the income tax due.

Limitations on Transfers. Transfers to and from the Fixed Account must generally be in

amounts of $50 or more. Partial withdrawals must be in amounts of $500 or more. The total amount of transfers and withdrawals from the Fixed Account in a Policy year may generally not exceed the greater of 25% of the Policy’s cash surrender value in the Fixed Account at the beginning of the year, or the maximum transfer amount for the preceding Policy year. We reserve the right to only allow transfers and withdrawals from the Fixed Account during the 30-day period that follows the Policy anniversary. We may also limit the number of transfers and partial withdrawals and may impose a processing charge for transfers and partial withdrawals. We are not currently imposing the maximum limit on transfers and withdrawals from the Fixed Account, but we reserve the right to do so. It is important to note that if we impose the maximum limit on transfers and withdrawals from the Fixed Account, it could take a number of

years to fully transfer or withdraw a current balance from the Fixed Account. You should keep this in mind when considering whether an allocation of Cash Value to the Fixed Account is consistent with your risk tolerance and time horizon. In addition, we may limit transfers to four per Policy year. We do not currently charge for transfers, but we reserve the right to charge up to $25 per transfer, except for transfers under the Automated Investment Strategies. We have adopted procedures to limit excessive transfer activity. In addition, each Portfolio may restrict or refuse certain transfers among, or purchases of shares in their Portfolios as a result of certain market timing activities. You should read each Portfolio's prospectus for more details.

Limitations on Access to Cash Value. You may

withdraw cash surrender value from your Policy at any time after the first Policy anniversary. The minimum amount you may withdraw is $500. We reserve the right to limit

partial

13

withdrawals to no more than 90% of the Policy’s cash surrender value in addition to limitations on withdrawals from the Fixed Account. We may limit the number of partial withdrawals to 12 per Policy year or impose a processing charge of $25 for each partial withdrawal. Partial withdrawals may have tax consequences. You may borrow from the Cash Value of your Policy. The minimum amount you may borrow is $500. The maximum amount you may borrow is an amount equal to the Policy’s Cash Value net of the Surrender Charge, reduced by Monthly Deductions and interest charges through the next Policy anniversary, increased by interest credits through the next Policy anniversary, less any existing Policy loans.

Policy Charge and Expense Increase. We have the right to increase certain Policy

charges.

Tax Law Changes. Tax laws, regulations, and interpretations have often been changed in the past and such changes

continue to be proposed. To the extent that you purchase a Policy based on expected tax benefits, relative to other financial or investment products or strategies, there

is no certainty that such advantages will always continue to exist.

Pandemics and Other Public Health Issues. Pandemics

and other public health issues or other events, and governmental, business and consumer reactions to them, may affect economic conditions and may cause a large number of illnesses or deaths. Hurricanes, windstorms, earthquakes, tornadoes, explosions, severe winter weather, fires, floods and mudslides, blackouts and man-made events such as riot, insurrection, terrorist attacks or acts of war may also cause catastrophic losses and increased claims. Any such catastrophes may also result in changes in consumer or business confidence, behavior and investment and business activity, changes to interest rates and other market risk factors, and governmental or other restrictions on economic activity for prolonged periods.

Cybersecurity. Our business is highly dependent upon the effective operation of our information systems, and those of

our service providers, vendors, and other third parties. Cybersecurity breaches of such systems can be intentional or unintentional events, and can occur through

unauthorized access to computer systems, networks or devices; infection from computer viruses or other malicious software code; or attacks that shut down, disable, slow

or otherwise disrupt operations, business processes or website access or functionality and our disaster recovery systems may be insufficient to safeguard our ability to conduct business. Cybersecurity breaches can interfere with our processing of Policy transactions, including the processing of transfer orders from our website or with the Portfolios; impact our ability to calculate the net investment factor; cause the release and possible loss or destruction of confidential Policy Owner or business information; impede order processing or cause other

operational issues; and result in regulatory enforcement actions or new laws or regulations which could increase our compliance costs. Although we continually make efforts to identify and reduce our exposure to cybersecurity risk, and we require our critical vendors to implement effective cybersecurity and data protection measures, there is no guarantee that we will be able to successfully manage this risk at all times.

Insurance Company Risks. Policies are subject to

the risks related to Metropolitan Life. Any obligations (including under any Fixed Account investment options), guarantees, and benefits of the Policy, including any

death benefit, are subject to the claims paying ability of Metropolitan Life. If Metropolitan Life experiences financial distress, it may not be able to meet its obligations to you. More information about Metropolitan Life, including its financial strength ratings, is available upon request by calling 1-800-638-5000 or by visiting www.metlife.com/about-us/corporate-profile/ratings.

Terrorism and Security Risk. The continued threat of terrorism, ongoing or potential military conflict and other actions and

heightened security measures may cause economic uncertainty and result in loss of life, property damage, additional disruptions to commerce and reduced economic activity.

The value of MetLife's investment portfolio may be adversely affected by declines in the credit and equity markets and reduced economic activity

14

caused

by such threats. Companies in which we maintain investments may suffer losses as a result of financial, commercial or economic disruptions, and such disruptions might

affect the ability of those companies to pay interest or principal on their securities or mortgage loans. Terrorist or military actions also could disrupt our operations centers and result in higher than anticipated claims under our insurance policies.

15

THE COMPANY, THE SEPARATE ACCOUNT AND THE PORTFOLIOS

The Company

Metropolitan Life Insurance Company is a provider of insurance, annuities, employee benefits and asset

management. We are also one of the largest institutional investors in the United States with a general account portfolio invested primarily in fixed income securities (corporate, structured products, municipals, and government and agency) and mortgage loans, as well as real estate, real estate joint ventures, other limited partnerships and equity securities. Metropolitan Life Insurance Company was incorporated under the laws of New York in 1868. The Company’s office is located at 200 Park Avenue, New York, New York 10166-0188. The Company is a wholly-owned subsidiary of MetLife, Inc. We are obligated to pay all benefits under the Policies. We are obligated to pay all benefits under the Policies. Investments in the Policy are subject to the risks related to Metropolitan Life with respect to any death benefit or other guarantees (including Fixed Account guarantees) that MetLife make available under the Policy.

All obligations (including under the Fixed Account), and benefits of the Policy are subject to the claims paying ability of Metropolitan Life. If Metropolitan Life experiences financial distress, it may not be able to meet its obligations to you.

The Separate Account

Metropolitan Life Separate Account UL is the funding vehicle for the Policies and other variable life insurance policies that we issue. Income and realized and unrealized capital gains and losses of the Separate Account are credited to the Separate Account without regard to any of our other income or capital gains or losses. Although we own the assets of the Separate Account, applicable law provides that the portion of the Separate Account assets equal to the reserves and other liabilities of the Separate Account may not be charged with liabilities that arise out of any other business we conduct. This means that the assets of the Separate Account are not available to meet the claims of our general creditors, and may only be used to support the Cash Values of the variable life insurance policies issued by the Separate Account.

We are obligated to pay the death benefit and any optional benefits under the Policy even if that amount exceeds the Policy’s Cash Value in the Separate Account. The amount of the death benefit and any optional benefits that exceeds the Policy’s Cash Value in the Separate Account is paid from our general account. Death benefits and any optional benefits paid from the general account are subject to the financial strength and claims-paying ability of the Company. For other life insurance policies and annuity contracts that we issue, we pay all amounts owed under the policies and contracts from the general account. MetLife is regulated as an insurance company under state law. State law generally imposes restrictions on the amount and type of investments in the general account. However, there is no guarantee that we will be able to meet our claims-paying obligations. There are risks to purchasing any insurance product.

The investment adviser to certain of the Portfolios offered with the Policy or with other variable life insurance policies issued through the Separate Account may be regulated as a Commodity Pool Operator. While we do not concede that the Separate Account is a commodity pool, MetLife has claimed an exclusion from the definition of the term “commodity pool operator” under the Commodities Exchange Act (“CEA”), and is not subject to registration or regulation as a pool operator under the CEA.

17

The Portfolios

Each Division of the Separate Account invests in a corresponding Portfolio. Each Portfolio is part of an open-end management investment company, more commonly known as a mutual fund, that serves as an investment vehicle

for variable life insurance and variable annuity separate accounts of various insurance companies. The mutual funds that offer the Portfolios are the American Funds Insurance

Series®, Brighthouse Funds Trust I and Brighthouse Funds Trust II. Each of these mutual funds has an investment adviser responsible for overall

management of each Portfolio available in the mutual fund. Some investment advisers have contracted with sub-advisers to make the day-to-day investment decisions for the Portfolios.

Portfolios Available Under the Policy. Information regarding each

Portfolio, including (i) its name; (ii) its Portfolio type (iii) its investment adviser and any sub-investment adviser; (iv) current expenses; and (v) performance is available in Appendix A to the prospectus. Each Fund has issued a prospectus that contains more detailed information about the Portfolio, which you may obtain by calling 1-800-638-5000 or going on line to: dfinview.com/metlife/tahd/MET000252.

The Portfolios’ investment objectives may not be met. The investment

objectives and policies of certain Portfolios are similar to the investment objectives and policies of other funds that may be managed by the same investment adviser or sub-adviser. The investment results of the Portfolios may be higher or lower than the results of these funds. There is no assurance, and no representation is made, that the investment results of any of the Portfolios will be comparable to the investment results of any other fund.

The Portfolios listed below are managed in a way that is intended to minimize volatility of returns (referred to as a “managed volatility strategy”):

•

AB Global Dynamic Allocation Portfolio

•

BlackRock Global Tactical Strategies Portfolio

•

Invesco Balanced-Risk Allocation Portfolio

•

JPMorgan Global Active Allocation Portfolio

•

Brighthouse Balanced Plus Portfolio

•

MetLife Multi-Index Targeted Risk Portfolio

•

PanAgora Global Diversified Risk Portfolio

•

Schroders Global Multi-Asset Portfolio

Stock prices fluctuate,

sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors or general market conditions. Bond prices may

fluctuate because they move in the opposite direction of interest rates. Foreign investing carries additional risks such as currency and market volatility. A managed volatility strategy is designed to reduce volatility of returns to the above Portfolios from investing in stocks and bonds. This strategy seeks to reduce such volatility by “smoothing” returns, which may result in a Portfolio outperforming the general securities market during periods of flat or negative market performance, and underperforming the general securities market during periods of positive market performance. This means that in periods of high market volatility, this managed volatility strategy could limit your participation in market gains; this may conflict with your investment objectives by limiting your ability to maximize potential growth of your Policy’s Cash Value and, in turn, the value of any guaranteed benefit that is tied to investment performance. Other Portfolios may offer the potential for higher returns.

18

Share

Classes of the Portfolios

The Portfolios offer various classes of

shares, each of which has a different level of expenses. The prospectuses for the Portfolios may provide information for share classes that are not available through the

Policy. When you consult the prospectus for any Portfolio, you should be careful to refer to only the information regarding the class of shares that is available through the Policy. For the American Funds Insurance Series, we offer Class 2 shares only; for Brighthouse Funds Trust I, we offer Class A and Class B shares; and for Brighthouse Funds Trust II, we offer Class A shares only.

Certain Payments We Receive with Regard to the Portfolios

An investment adviser or subadviser of a Portfolio, or its affiliates, may make payments to us and/or certain of our affiliates. These payments may be used for a variety of purposes, including payment for expenses for certain administrative, marketing and support services with respect to the Policies and, in our role as intermediary, with respect to the Portfolios. We and our affiliates may profit from these payments.

These payments may be derived, in whole or in part, from

fees deducted from Portfolio assets. Policy Owners, through their indirect investment in the Portfolios, bear the costs of these fees (see the Portfolio prospectuses for

more information). The amount of the payments we receive is based on a percentage of assets of the Portfolio attributable to the Policies and certain other variable insurance products that we and our affiliates issue. These percentages differ and some advisers or subadvisers (or other affiliates) may pay us more than others. These percentages currently range up to 0.50%.

Additionally, an investment adviser or subadviser of a Portfolio or its affiliates may provide us with wholesaling services that assist in the distribution of the Policies and may pay us and/or certain of our affiliates amounts to participate in sales meetings. These amounts may be significant and may provide the adviser or subadviser (or their affiliates) with increased access to persons involved in the distribution of the Policies.

As of December 31, 2023, approximately 87% of Portfolio assets held in Separate Accounts of Metropolitan Life and its affiliates were allocated to Portfolios in Brighthouse Funds Trust I and Brighthouse Funds Trust II. We and certain of our affiliated companies have entered into agreements with Brighthouse Advisers, LLC, Brighthouse Funds Trust I and Brighthouse Funds trust II whereby we receive payments for certain administrative, marketing and support services described in the previous paragraphs. Currently, the Portfolios in Brighthouse Funds Trust I and Brighthouse Funds Trust II are only available in variable annuity contracts and variable life insurance policies issued by Metropolitan Life Insurance Company and its affiliates as well as Brighthouse Life Insurance Company and its affiliates. Should we or Brighthouse Investment Advisers, LLC decide to terminate the agreements, we would be required to find alternative Portfolios which could have higher or lower costs to the Policy Owner. In addition, the amount of payments we receive could cease or be substantially reduced which may have a material impact on our financial statements.

Certain Portfolios have adopted a Distribution Plan under Rule 12b-1 of the Investment Company Act of 1940. A Portfolio’s 12b-1 Plan, if any, is described in more detail in the Portfolio’s prospectus. (See “Distribution of the Policies.”) Any payments we receive pursuant to those 12b-1 Plans are paid to us or our Distributor MetLife Investors Distribution Company (MLIDC). Payments under a Portfolio’s 12b-1 Plan decrease the Portfolio’s investment return.

For more specific information on the amounts we may receive on account of your investment in the Portfolios, you may call us toll free at 1-800-638-5000.

19

Selection of the Portfolios

We select the Portfolios offered through the Policy based on a number of criteria, including asset class coverage, the strength of the adviser’s or subadviser’s reputation and tenure, brand recognition, performance, and the capability and qualification of each investment firm. Other factors we consider during the selection process are whether the Portfolio’s adviser or subadviser is one of our affiliates or whether the Portfolio, its adviser, its subadviser(s), or an affiliate will make payments to us or our affiliates. For additional information on these arrangements, see “Certain Payments We Receive with Regard to the Portfolios” above.

In this regard, the profit distributions we receive from our affiliated

investment advisers are a component of the total revenue that we consider in configuring the features and investment choices available in the variable insurance products that we and our affiliated insurance companies issue. Since we and our affiliated insurance companies may benefit more from the allocation of assets to Portfolios advised by our affiliates than those that are not, we may be more inclined to offer Portfolios advised by our affiliates in the variable insurance products we issue. We review the Portfolios periodically and may remove a Portfolio or limit its availability to new Premium payments and/or transfers of Cash Value if we determine that the Portfolio no longer meets one or more of the selection criteria, and/or if the Portfolio has not attracted significant allocations from Policy Owners. We may include Portfolios based on recommendations from selling firms. In some cases, the selling firms may receive payments from the Portfolios they recommend and may benefit accordingly from the allocation of Cash Value to such Portfolios.

We do not provide any investment advice and do not recommend or endorse any particular Portfolio. You bear the risk of any decline in the Cash Value of your Policy resulting from the performance of the Portfolios you have chosen.

Purchase and Redemption of Portfolio Shares by Our Separate Account

As of the end of each Valuation Period, we purchase and redeem Portfolio shares for the Separate Account at their net asset value without any sales or redemption charges. These purchases and redemptions reflect the amount of any of the following transactions that take effect at the end of the Valuation Period:

•

The allocation of net Premiums to the Separate Account.

•

Dividends and distributions on Portfolio shares, which are reinvested as of the

dates paid (which reduces the value of each share of the Fund and increases the number of Fund shares outstanding, but has no affect on the Cash Value in the Separate Account).

•

Policy loans and loan repayments allocated to the Separate Account.

•

Transfers to and among Divisions.

•

Withdrawals and surrenders taken from the Separate Account.

Voting Rights

We own the Portfolio shares held in the Separate Account and have the

right to vote those shares at meetings of the Portfolio shareholders. However, to the extent required by Federal securities law, we will give you, as Policy Owner,

the right to instruct us how to vote the shares that are attributable to your Policy.

We will determine, as of the record date, if you are entitled to give voting

instructions and the number of shares to which you have a right of instruction. If we do not receive timely instructions from you, we will vote your shares for,

20

against, or withhold from voting on, any proposition in the same proportion as the shares held in that Division for all Policies for which we have received voting instructions. The effect of this proportional voting is that a small number of Policy Owners may control the outcome of a vote.

We will vote Portfolio shares held by our general account (or any unregistered separate account for which voting privileges were not extended) in the same proportion as the total of (i) shares for which voting instructions were received and (ii) shares that are voted in proportion to such voting instructions.

We may disregard voting instructions for changes in the investment policy, investment adviser or principal underwriter of a Portfolio if required by state insurance law, or if we (i) reasonably disapprove of the changes and (ii) in the case of a change in investment policy or investment adviser, make a good faith determination that the proposed change is prohibited by state authorities or inconsistent with a Division’s investment objectives. If we do disregard voting instructions, the next semi-annual report to Policy Owners will include a summary of that action and the reasons for it.

Rights Reserved by MetLife

We and our affiliates may change the voting procedures and vote Portfolio shares without Policy Owner

instructions, if the securities laws change. We also reserve the right: (1) to add Divisions; (2) to combine Divisions; (3) to substitute shares of another registered open-end management investment company, which may have

different fees and expenses, for shares of a Portfolio; (4) to substitute or close a Division to allocations of Premium payments or Cash Value or both, and to existing investments or the investment of future Premiums, or both, for any class of Policy or Policy Owner, at any time in our sole discretion; (5) to operate the Separate Account as a management investment company under the Investment Company Act of 1940 or in any other form; (6) to

deregister the Separate Account under the Investment Company Act of 1940; (7) to combine it with other Separate Accounts; and (8) to transfer assets supporting the Policies from one Division to another or from the Separate Account to other separate accounts, or to transfer assets to our general account as permitted by applicable law. We will exercise these rights in accordance with applicable law, including approval of Policy Owners if required. We will notify you if exercise of any of these rights would result in a material change in the Separate Account or its investments.

We will not make any changes without receiving any necessary approval of the SEC and applicable state insurance departments. We will notify you of any changes.

THE POLICIES

Purchasing a Policy

The Policy is no longer offered for sale. To purchase a Policy, you must have submited a completed application and an initial Premium to us at our Designated Office. The minimum face amount for the base Policy is $50,000 unless we consented to a lower amount. For Policies acquired through a pension or profit sharing plan qualified under Section 401 of the Code, the minimum face amount is $25,000.

The Policies were available for insureds age 85 or younger. We reserve the right to modify our minimum face amount and underwriting requirements at any time. We must have received evidence of insurability that satisfies our underwriting standards before we will issue a Policy. We reserved the right to reject an application for any reason permitted by law.

21

We may offer other variable life insurance policies that have different death benefits, policy features, and optional programs. However, these other policies also have different charges that would affect your Division performance and Cash Values. To obtain more information about these other policies, including their eligibility requirements, contact our Designated Office or your registered representative.

Replacing Existing Insurance

It may not be in your best interest to surrender, lapse, change, or borrow from existing life insurance policies (including this Policy) or annuity contracts in connection with the purchase of a different policy. You should carefully compare your existing insurance and any new insurance that you are considering. You should replace your existing insurance only when you determine that the new insurance is better for you. You may have to pay a

surrender charge on your existing insurance, and the new insurance may impose a new surrender charge period. You should talk to your financial professional or tax adviser to make sure the exchange will be tax-free. If you surrender your existing Policy for cash and then buy a new policy, you may have to pay a tax, including possibly a penalty tax, on the surrendered Policy. We no longer sell this Policy and therefore you may not exchange an existing life insurance policy or annuity contract to purchase this Policy, but should consider these risks if you are thinking of replacing your Policy.

Policy Owner and Beneficiary

The Policy Owner is named in the application but may be changed from time to time. While the insured is living and the Policy is in force, the Policy Owner may exercise all the rights and options described in the Policy, subject to the terms of any beneficiary designation or assignment of the Policy. These rights include selecting and changing the beneficiary, changing the Policy Owner, changing the face amount of the Policy and assigning the Policy. At the death of the Policy Owner who is not the insured, his or her estate will become the Policy Owner unless a successor Policy Owner has been named. The Policy Owner’s rights (except for rights to payment of benefits) terminate at the death of the insured.

The beneficiary is also named in the application. You may change the beneficiary at any time before the death of the insured, unless the beneficiary designation is irrevocable. The beneficiary has no rights under the Policy until the death of the insured and must survive the insured in order to receive the death proceeds. If no named

beneficiary survives the insured, we pay proceeds to the Policy Owner.

A change of Policy Owner or beneficiary is subject to all payments made and actions taken by us under the Policy before we receive a signed change form. You can contact your registered representative or our Designated Office for the procedure to follow.

You may assign (transfer) your rights in the Policy to someone else. An absolute assignment of the Policy is a change of Policy Owner and beneficiary to the assignee. A collateral assignment of the Policy does not change the Policy Owner or beneficiary, but their rights will be subject to the terms of the assignment. Assignments are subject to all payments made and actions taken by us under the Policy before we receive a signed copy of the assignment form. We are not responsible for determining whether or not an assignment is valid. Changing the Policy Owner or assigning the Policy may have tax consequences. (See “Tax Considerations” below.)

Exchange Right

At least once each year you have the option to transfer all of your Cash Value to the Fixed Account and apply the cash surrender value to a new policy issued by us or an affiliate which provides paid-up insurance. Paid-up

22

insurance is permanent insurance with no further Premiums due. The face amount of the new Policy of paid-up insurance may be less than the face amount of the Policy.

PREMIUMS

Flexible Premiums

Subject to the limits described below, you choose the amount and frequency of Premium payments. You select a Planned Premium schedule, which consists of a first-year Premium amount and an amount for subsequent

Premium payments. This schedule appears in your Policy. Your Planned

Premiums will not necessarily keep your Policy in force. You may skip

Planned Premium payments or make additional payments. Additional payments could be subject to underwriting. No payment can be less than $50, except with our

consent.

You can pay Planned Premiums on an annual,

semi-annual or quarterly schedule, or on a monthly schedule if payments are drawn directly from your checking account under our pre-authorized checking arrangement. We

will send Premium notices for annual, semi-annual or quarterly Planned Premiums. You may make payments by check or through our pre-authorized checking arrangement. You can change your Planned Premium schedule by sending your request to us at our Designated Office. You may not make Premium payments on or after the Policy

anniversary when the insured reaches age 121, except for Premiums required during the grace period.

If any payments under the Policy exceed the “7-pay limit” under

Federal tax law, your Policy will become a modified endowment contract and you may have more adverse tax consequences with respect to certain distributions than would otherwise be the case if Premium payments did not exceed the “7-pay limit.” Information about your “7-pay limit” is found in your Policy illustration. If we receive a Premium payment 30 days or less before the anniversary of the 7-pay testing period that exceeds the “7-pay limit” and would cause the Policy to become a modified endowment contract, and waiting until the anniversary to apply that payment would prevent the Policy from

becoming a modified endowment contract, we may retain the Premium payment in a non-interest bearing account and apply the payment to the Policy on the anniversary. If we follow this procedure, we will notify you and give you the option of having the Premium payment applied to the Policy before the anniversary. Otherwise, if you make a Premium payment that exceeds the “7-pay limit,” we will apply the payment to the Policy according to our standard procedures described below and notify you that the Policy has become a modified endowment contract. In addition, if you have selected the guideline Premium test, Federal tax law limits the amount of Premiums that you can pay under the Policy. You need our consent if, because of tax law requirements, a payment would increase the Policy’s death benefit by more than it would increase Cash Value. We may require evidence of insurability before accepting the payment.

We allocate net Premiums to your Policy’s Divisions as of the date we receive the payments at our Designated Office, if they are received before the close of regular trading on the New York Stock Exchange, which is usually 4 p.m. Eastern Time. Payments received after that time, or on a day that the New York Stock Exchange is not open, will be allocated to your Policy’s Divisions on the next day that the New York Stock Exchange is open. (See “Sending Communications and Payments to Us.”)

Under our current processing, we treat any payment received by us as a Premium payment unless it is clearly marked as a loan repayment.

23

Amount Provided for Investment under the Policy

Investment Start Date. Your initial net Premium is credited with Fixed Account interest

as of the investment start date. The investment start date is the later of the Policy Date and the date we first receive a Premium payment for the Policy at our Designated Office.

Premium with Application. If you made a Premium payment with the application, unless

you requested otherwise, the Policy Date was the date the policy application is approved. Monthly Deductions begin on the Policy Date. You may only make one Premium payment with the application. The minimum amount you must pay is set forth in the application. If we decline an application, we refund the Premium payment made.

If you make a Premium payment with the application, we will cover the insured under a temporary insurance agreement beginning on the later of the date the application is signed or on the date of any required medical examination. (See “Death Benefits.”)

Premium on Delivery. If you pay the initial Premium upon delivery of the Policy, unless

you request otherwise, the Policy Date and the investment start date are the date your Premium payment is received at our Designated Office. Monthly Deductions begin on the Policy Date.

Backdating. We may sometimes backdate a Policy, if you request, by assigning a Policy

Date earlier than the date the Policy application is approved (but not earlier than six months prior to the date that the application is completed). You may wish to backdate so that you can obtain lower cost of insurance rates, based on a younger insurance age. For a backdated Policy, you must also pay the minimum Premiums due for the period between the Policy Date and the investment start date. As of the investment start date, we allocate the net Premiums to the Policy, adjusted for monthly Policy charges. For a backdated Policy, the investment start date is the later of the date the Policy application is approved and the date your Premium is received at our Designated Office.

Allocation of Net Premiums

You make the initial Premium allocation when you apply for a Policy. You can

change the allocation of future Premiums at any time thereafter. The change will be effective for Premiums applied on or after the date when we receive your request. You may request the change by telephone, by written request (which may be telecopied to us) or over the Internet. (See “Sending of Communications and Payments To Us.”)

When we allocate net Premiums to your Policy’s Divisions, we convert them into units of the Divisions. We determine the number of units by dividing the dollar amount of the net Premium by the unit value. For your initial Premium, we use the unit value on the investment start date. For subsequent Premiums, we use the unit value next determined after receipt of the payment. (See “Cash Value.”)

SENDING COMMUNICATIONS AND PAYMENTS TO US

We will treat your request for a Policy transaction, or your submission of a payment, as received by us if we receive a request conforming to our administrative procedures or a payment at our Designated Office before the close of regular trading on the New York Stock Exchange on that day (usually 4:00 p.m. Eastern Time). If we receive it after that time, or if the New York Stock Exchange is not open that day, then we will treat it as received on the next day when the New York Stock Exchange is open. These rules apply regardless of the reason we did not receive your request by the close of regular trading on the New York Stock Exchange — even if due to our delay (such as a delay in answering your telephone call).

24

The

Designated Office for Premium payments is printed on the billing statement we mail to you. If you do not have your billing statement you may call us at 1-800-638-5000 to

obtain the address. The Designated Office for other transactions and requests is included in your annual statement or other correspondence that we send to

you.

You may request a Cash Value transfer or reallocation of

future Premiums by written request (which may be telecopied) to us, by telephoning us or over the Internet (subject to our restrictions on frequent transfers). To request a transfer or reallocation by telephone, you should contact your registered representative or contact us at 1-800-638-5000. To request a transfer over the Internet, you may log on to our website at www.metlife.com. We use reasonable procedures to confirm that instructions communicated by telephone, facsimile or Internet are genuine. Any telephone, facsimile or Internet instructions that we reasonably believe to be genuine are your responsibility, including losses arising from any errors in the communication of instructions. However, because telephone and Internet transactions may be available to anyone who provides certain information about you and your Policy, you should protect that information. We may not be able to verify that you are the person providing telephone or Internet instructions, or that you have authorized any such person to act for you.

Telephone, facsimile, and computer systems (including the Internet) may not always be available. Any telephone, facsimile or computer system, whether it is yours, your service provider’s, your registered representative’s, or ours, can experience outages or slowdowns for a variety of reasons. These outages or slowdowns may delay or prevent our processing of your request. Although we have taken precautions to help our systems handle heavy use, we cannot promise complete reliability under all circumstances. If you are experiencing problems, you should make your request by writing to our Designated Office.