Table of Contents

As filed with the U.S. Securities and Exchange Commission on April 23, 2020

Registration Nos. 333-147508

811-06025

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-6

Registration Statement

Under

| the Securities Act of 1933 | ☐ | |||

| Pre-Effective Amendment No. | ☐ | |||

| Post-Effective Amendment No. 12 | ||||

| Registration Statement Under | ||||

| the Investment Company Act of 1940 | ☐ | |||

| Amendment No. 96 | ||||

Metropolitan Life Separate Account UL

(Exact Name of Registrant)

Metropolitan Life Insurance Company

(Name of Depositor)

200 Park Avenue

New York, NY 10166

(Address of depositor’s principal executive offices)

Depositor’s Telephone Number, including Area Code: (212) 578-9500

Stephen Gauster, Esq.

Executive Vice President and General Counsel

Metropolitan Life Insurance Company

200 Park Avenue

New York, NY 10166

(Name and Address of Agent for Service)

Copy to:

W. Thomas Conner, Esquire

Vedder Price P.C.

1401 I Street, N.W.

Suite 1100

Washington, D.C. 20005

It is proposed that this filing will become effective (check appropriate box)

| ☐ | immediately upon filing pursuant to paragraph (b) |

| ☒ | on May 1, 2020 pursuant to paragraph (b) |

| ☐ | 60 days after filing pursuant to paragraph (a)(1) |

| ☐ | on (date) pursuant to paragraph (a)(1) of Rule 485 |

| ☐ | this post-effective amendment designates a new effective date for a previously filed post-effective amendment |

| Title | of Securities Being Registered: Flexible Premium Variable Universal Life Insurance Policies. |

Table of Contents

EQUITY ADVANTAGE VUL

Flexible Premium

Variable Life Insurance Policies

Issued by

Metropolitan Life Separate Account UL of

Metropolitan Life Insurance Company

May 1, 2020

This prospectus describes individual flexible premium variable life insurance policies (the “Policies”) issued by Metropolitan Life Insurance Company (“MetLife”). The Policies are no longer offered for sale.

You allocate net premiums among the Divisions of Metropolitan Life Separate Account UL (the “Separate Account”). Each Division of the Separate Account invests in shares of one of the following “Portfolios” (Divisions may be referred to as “Investment Divisions” in your Policy):

Table of Contents

You may also allocate net Premiums to our Fixed Account. Special limits may apply to Fixed Account transfers and withdrawals.

You receive Fixed Account performance until 20 days after we apply your initial premium payment to the Policy. Thereafter, we invest the Policy’s Cash Value according to your instructions.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these policies or determined if this prospectus is accurate or complete. Any representation to the contrary is a criminal offense.

We do not guarantee how any of the Divisions or Portfolios will perform. The Policies and the Portfolios are not deposits or obligations of, or guaranteed or endorsed by, any financial institution and are not federally insured by the Federal Deposit Insurance Corporation, the Federal Reserve Board or any other government agency.

IMPORTANT INFORMATION

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of a Portfolio’s shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from us. Instead, the shareholder reports will be made available on www.metlife.com, and you will be notified by mail each time a shareholder report is posted and provided with a website link to access the shareholder report.

If you already elected to receive your shareholder report electronically, you will not be affected by this change, and you need not take any action. You may elect to receive shareholder reports and other communications, including Portfolio prospectuses and other information we send you by contacting our Administrative Office.

If you wish to continue to receive shareholder reports in paper on and after January 1, 2021, we will continue to send you all future reports in paper, free of charge. Please contact us at our Administrative Office if you wish to continue receiving paper copies of the Portfolios’ shareholder reports. Your election to receive shareholder reports in paper will apply to all Portfolios available under your Policy.

Table of Contents

| PAGE | ||||

| A-5 | ||||

| A-5 | ||||

| A-6 | ||||

| A-8 | ||||

| A-9 | ||||

| A-9 | ||||

| A-10 | ||||

| A-13 | ||||

| A-18 | ||||

| A-18 | ||||

| A-18 | ||||

| A-18 | ||||

| A-24 | ||||

| A-24 | ||||

| A-25 | ||||

| A-25 | ||||

| A-26 | ||||

| A-26 | ||||

| A-26 | ||||

| A-26 | ||||

| A-27 | ||||

| A-27 | ||||

| A-27 | ||||

| A-28 | ||||

| A-28 | ||||

| A-28 | ||||

| A-29 | ||||

| A-29 | ||||

| RECEIPT OF COMMUNICATIONS AND PAYMENTS AT METLIFE’S DESIGNATED OFFICE |

A-29 | |||

| A-31 | ||||

| A-31 | ||||

| A-32 | ||||

| A-33 | ||||

| A-34 | ||||

| A-34 | ||||

| A-35 | ||||

| A-35 | ||||

| A-36 | ||||

| A-36 | ||||

| A-36 | ||||

| A-38 | ||||

| A-38 | ||||

| A-41 | ||||

| A-42 | ||||

| A-43 | ||||

| A-43 | ||||

| A-44 | ||||

| A-45 | ||||

A-3

Table of Contents

| PAGE | ||||

| A-46 | ||||

| A-46 | ||||

| A-46 | ||||

| A-46 | ||||

| A-47 | ||||

| A-48 | ||||

| A-48 | ||||

| A-49 | ||||

| A-49 | ||||

| A-49 | ||||

| A-50 | ||||

| A-52 | ||||

| Charges Against the Portfolios and the Divisions of the Separate Account |

A-52 | |||

| A-53 | ||||

| A-53 | ||||

| A-53 | ||||

| A-53 | ||||

| A-58 | ||||

| A-58 | ||||

| A-59 | ||||

| A-60 | ||||

| A-60 | ||||

| A-61 | ||||

| APPENDIX A: GUIDELINE PREMIUM TEST AND CASH VALUE ACCUMULATION TEST |

A-62 | |||

A-4

Table of Contents

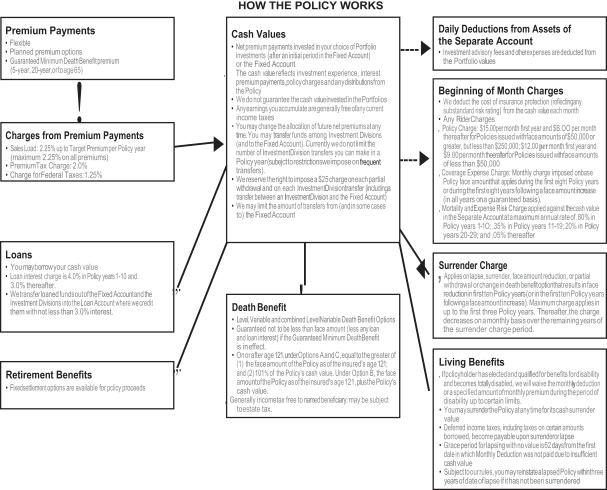

This summary describes the Policy’s important benefits and risks. The sections in the prospectus following this summary discuss the Policy in more detail. The Glossary at the end of the prospectus defines certain words and phrases used in this prospectus.

Death Proceeds. The Policy is designed to provide insurance protection. Upon receipt of satisfactory proof of the death of the insured, we pay death proceeds to the beneficiary of the Policy. Death proceeds generally equal the death benefit on the date of the insured’s death plus any additional insurance provided by rider, less any outstanding loan and accrued loan interest.

Choice of Death Benefit Option. You may choose among three death benefit options:

| — | a level death benefit that equals the Policy’s face amount; |

| — | a variable death benefit that equals the Policy’s face amount plus the Policy’s cash value; and |

| — | a combination variable and level death benefit that equals the Policy’s face amount plus the Policy’s cash value until the insured attains age 65 and equals the Policy’s face amount thereafter. |

The death benefit under any option could increase to satisfy Federal tax law requirements if the cash value reaches certain levels. After the first Policy year you may change your death benefit option, subject to our underwriting rules. A change in death benefit option may have tax consequences.

Premium Flexibility. You can make premium payments based on a schedule you determine, subject to some limits. You may change your payment schedule at any time or make a payment that does not correspond to your schedule. We can, however, limit or prohibit payments in some situations.

Right to Examine the Policy. During the first ten days following your receipt of the Policy, you have the right to return the Policy to us. If you exercise this right, we will refund the premiums you paid.

Investment Options. You can allocate your net Premiums and Cash Value among your choice of Divisions available in the Separate Account, each of which corresponds to a mutual fund portfolio, or “Portfolio.” The Portfolios available under the Policy include several common stock funds, including funds which invest primarily in foreign securities, as well as bond funds, balanced funds, asset allocation funds and funds that invest in exchange-traded funds. You may also allocate Premiums and Cash Value to our Fixed Account which provides guarantees of interest and principal. You may change your allocation of future premiums at any time.

We currently limit the amount of Cash Value You may transfer to or from any one Division to a maximum of $2.5 million per day. If You own more than one Equity Advantage VUL Policy on the same insured, this limit will be applied to the cumulative transfers You make to or from the Division under all such Policies.

Partial Withdrawals. You may withdraw cash surrender value from your Policy at any time after the first Policy anniversary. The minimum amount you may withdraw is $500. We reserve the right to limit partial withdrawals to no more than 90% of the Policy’s cash surrender value. We may limit the number of partial withdrawals to 12 per Policy year or impose a processing charge of $25 for each partial withdrawal. Partial withdrawals may have tax consequences.

Transfers and Automated Investment Strategies. You may transfer your Policy’s Cash Value among the Divisions or between the Divisions and the Fixed Account. The minimum amount you may transfer is $50, or if less, the total amount in the Division or the Fixed Account. We may limit the number of transfers among the

A-5

Table of Contents

Divisions and the Fixed Account to no more than four per Policy year. We may impose a processing charge of $25 for each transfer. We may also impose restrictions on frequent transfers. (See “Transfers” for additional information on such restrictions.) We offer five automated investment strategies that allow you to periodically transfer or reallocate your cash value among the Divisions and the Fixed Account. (See “Automated Investment Strategies.”)

Loans. You may borrow from the Cash Value of your Policy. The minimum amount you may borrow is $500. The maximum amount you may borrow is an amount equal to the Policy’s Cash Value net of the Surrender Charge, reduced by Monthly Deductions and interest charges through the next Policy anniversary, increased by interest credits through the next Policy anniversary, less any existing Policy loans. We charge you a maximum annual interest rate of 4.0% for the first ten Policy years and 3.0% thereafter. We credit interest at an annual rate of at least 3.0% on amounts we hold as collateral to support your loan. Loans may have tax consequences. (See “Loans” for additional information.)

Surrenders. You may surrender the Policy for its cash surrender value at any time. Cash surrender value equals the Cash Value reduced by any Policy loan and accrued loan interest and by any applicable Surrender Charge. A surrender may have tax consequences.

Tax Benefits. We anticipate that the Policy should be deemed to be a life insurance contract under Federal tax law. Accordingly, undistributed increases in Cash Value should not be taxable to you. As long as your Policy is not a modified endowment contract, partial withdrawals should be non-taxable until you have withdrawn an amount equal to your total investment in the Policy. However, different rules apply in the first fifteen Policy years, as distributions accompanied by benefit reductions may be taxable prior to a complete withdrawal of your investment in the Policy. Always confirm in advance the tax consequences of a particular withdrawal with a qualified tax adviser. Death benefits paid to your beneficiary should generally be free of Federal income tax. Death benefits may be subject to estate taxes. Under current Federal income tax law, the taxable portion of distributions from variable life policies is taxed at ordinary income tax rates and does not qualify for the reduced tax rate applicable to long-term capital gains and dividends.

Conversion Right. During the first two Policy years, you may convert the Policy to fixed benefit coverage by exchanging the Policy for a fixed benefit life insurance policy that we agree to, and that is issued by us or an affiliate that we name. We will make the exchange without evidence of insurability.

Supplemental Benefits and Riders. We offer a variety of riders that provide supplemental benefits under the Policy. We generally deduct any monthly charges for these riders as part of the Monthly Deduction. Your registered representative can help you determine whether any of these riders are suitable for you.

Personalized Illustrations. You will receive personalized illustrations in connection with the purchase of this Policy that reflect your own particular circumstances. These hypothetical illustrations may help you to understand the long-term effects of different levels of investment performance, the possibility of lapse, and the charges and deductions under the Policy. They will also help you to compare this Policy to other life insurance policies. The personalized illustrations are based on hypothetical rates of return and are not a representation or guarantee of investment returns or Cash Value.

Investment Risk. If you invest your Policy’s Cash Value in one or more of the Divisions, then you will be subject to the risk that investment performance will be unfavorable and that your Cash Value will decrease. In addition, we deduct Policy fees and charges from your Policy’s Cash Value, which can significantly reduce your Policy’s Cash Value. During times of poor investment performance, this deduction will have an even greater impact on your Policy’s Cash Value. It is possible to lose your full investment and your Policy could lapse without value, unless you pay additional premium. If you allocate Cash Value to the Fixed Account, then we

A-6

Table of Contents

credit such Cash Value with a declared rate of interest. You assume the risk that the rate may decrease, although it will never be lower than the guaranteed minimum annual effective rate of 3%.

Surrender and Withdrawal Risks. The Policies are designed to provide lifetime insurance protection. They are not offered primarily as an investment, and should not be used as a short-term savings vehicle. If you surrender the Policy within the first ten (10) Policy years (or within the first ten (10) Policy years following a face amount increase), you will be subject to a Surrender Charge as well as income tax on any gain that is distributed or deemed to be distributed from the Policy. You will also be subject to a Surrender Charge if you make a partial withdrawal from the Policy within the first ten (10) Policy years (or the first ten (10) Policy years following the face amount increase) if the partial withdrawal reduces the face amount (or the face amount increase). If you surrender the Policy in the first Policy year (or in the first year following a face amount increase) we will also deduct an amount equal to the remaining first year Coverage Expense Charges.

You should purchase the Policy only if you have the financial ability to keep it in force for a substantial period of time. You should not purchase the Policy if you intend to surrender all or part of the Policy’s Cash Value in the near future. Even if you do not ask to surrender your Policy, surrender charges may play a role in determining whether your Policy will lapse (terminate without value), because surrender charges determine the cash surrender value, which is a measure we use to determine whether your Policy will enter the grace period (and possibly lapse).

Risk of Lapse. Your Policy may lapse if you have paid an insufficient amount of Premiums or if the investment experience of the Divisions is poor. If your cash surrender value is not enough to pay the Monthly Deduction, your Policy may enter a 62-day grace period. We will notify you that the Policy will lapse unless you make a sufficient payment of additional Premium during the grace period. Your Policy generally will not lapse if you pay certain required Premium amounts and you are therefore protected by a Guaranteed Minimum Death Benefit. If your Policy does lapse, your insurance coverage will terminate, although you will be given an opportunity to reinstate it. Lapse of a Policy on which there is an outstanding loan may have adverse tax consequences.

Tax Risks. We anticipate that the Policy should be deemed to be a life insurance contract under Federal tax law. However, the rules are not entirely clear in certain circumstances, for example, if your Policy is issued on a substandard basis. The death benefit under the Policy will never be less than the minimum amount required for the Policy to be treated as life insurance under section 7702 of the Internal Revenue Code, as in effect on the date the Policy was issued. If your Policy is not treated as a life insurance contract under Federal tax law, increases in the Policy’s Cash Value will be taxed currently.

Even if your Policy is treated as a life insurance contract for Federal tax purposes, it may become a modified endowment contract due to the payment of excess Premiums or unnecessary Premiums, due to a material change or due to a reduction in your death benefit. If your Policy becomes a modified endowment contract, surrenders, partial withdrawals, loans, and use of the Policy as collateral for a loan will be treated as a distribution of the earnings in the Policy and will be taxable as ordinary income to the extent thereof. In addition, if the Policy Owner is under age 591⁄2 at the time of the surrender, partial withdrawal or loan, the amount that is included in income will generally be subject to a 10% penalty tax.

If the Policy is not a modified endowment contract, distributions generally will be treated first as a return of basis or investment in the Policy and then as taxable income. However, different rules apply in the first fifteen Policy years, as distributions accompanied by benefit reductions may be taxable prior to a complete withdrawal of your investment in the Policy. Moreover, loans will generally not be treated as distributions prior to termination of your Policy, whether by lapse, surrender or exchange. Finally, neither distributions nor loans from a Policy that is not a modified endowment contract are subject to the 10% penalty tax.

See “Tax Considerations.” You should consult a qualified tax adviser for assistance in all Policy-related tax matters.

A-7

Table of Contents

Loan Risks. A Policy loan, whether or not repaid, will affect the Cash Value of your Policy over time because we subtract the amount of the loan from the Divisions and/or Fixed Account as collateral, and hold it in our Loan Account. This loan collateral does not participate in the investment experience of the Divisions or receive any higher current interest rate credited to the Fixed Account.

We also reduce the amount we pay on the insured’s death by the amount of any outstanding loan and accrued loan interest. Your Policy may lapse if your outstanding loan and accrued loan interest reduce the cash surrender value to zero.

If you surrender your Policy or your Policy lapses while there is an outstanding loan, there will generally be Federal income tax payable on the amount by which loans and partial withdrawals exceed the premiums paid. Since loans and partial withdrawals reduce your Policy’s Cash Value, any remaining Cash Value may be insufficient to pay the income tax due.

Limitations on Cash Value in the Fixed Account. Transfers to and from the Fixed Account must generally be in amounts of $50 or more. Partial withdrawals from the Fixed Account must be in amounts of $500 or more. The total amount of transfers and withdrawals from the Fixed Account in a Policy year may generally not exceed the greater of 25% of the Policy’s cash surrender value in the Fixed Account at the beginning of the year, or the maximum transfer amount for the preceding Policy year. We may also limit the number of transfers and partial withdrawals and may impose a processing charge for transfers and partial withdrawals. We are not currently imposing the maximum limit on transfers and withdrawals from the Fixed Account, but we reserve the right to do so. It is important to note that if we impose the maximum limit on transfers and withdrawals from the Fixed Account, it could take a number of years to fully transfer or withdraw a current balance from the Fixed Account. You should keep this in mind when considering whether an allocation of Cash Value to the Fixed Account is consistent with your risk tolerance and time horizon.

Tax Law Changes. Tax laws, regulations, and interpretations have often been changed in the past and such changes continue to be proposed. To the extent that you purchase a Policy based on expected tax benefits, relative to other financial or investment products or strategies, there is no certainty that such advantages will always continue to exist.

Other Matters. The novel coronavirus COVID-19 pandemic is causing illnesses and deaths. This pandemic, other pandemics, and their related major public health issues are having a major impact on the global economy and financial markets. Governmental and non-governmental organizations may not effectively combat the spread and severity of such a pandemic, increasing its harm to the Company. Any of these events could materially adversely affect the Company’s operations, business, financial results, or financial condition.

A comprehensive discussion of the risks associated with each of the Portfolios can be found in the Portfolio prospectuses, which you can obtain by calling 1-800-638-5000. There is no assurance that any of the Portfolios will achieve its stated investment objective.

A-8

Table of Contents

The following tables describe the fees and expenses that a Policy Owner will pay when buying, owning and surrendering the Policy. The first table describes the fees and expenses that a Policy Owner will pay at the time he or she buys the Policy, surrenders the Policy or transfers Cash Value among accounts.

| Charge |

When Charge is Deducted |

Current Amount Deducted |

Maximum Amount Deductible | |||

| Sales Charge Imposed on Premiums |

On payment of premium | 2.25% of premiums paid up to the Target Premium per Policy year1 | 2.25% of each premium paid | |||

| Premium Tax Imposed on Premiums |

On payment of premium | 2.0% in all Policy years | 2.0% in all Policy years | |||

| Federal Tax Imposed on Premiums |

On payment of premium | 1.25% in all Policy years | 1.25% in all Policy years | |||

| 1 | The target premium varies based on individual characteristics, including the insured’s issue age, risk class and (except for unisex Policies) sex. |

| Charge |

When Charge is Deducted |

Current Amount Deducted |

Maximum Amount Deductible | |||

| Surrender Charge1 |

On surrender, lapse, or face amount reduction in the first ten (10) Policy years (and, with respect to a face amount increase, in the first ten (10) Policy years after the increase) | |||||

| Minimum and Maximum Charge |

In Policy year 1, $3.75 to $38.25 per $1,000 of base Policy face amount2 |

In Policy year 1, $3.75 to $38.25 per $1,000 of base Policy face amount2 | ||||

| Charge in the first Policy year for a Representative Insured 3 |

$14.00 per $1,000 of base Policy face amount | $14.00 per $1,000 of base Policy face amount | ||||

| Transfer Charge4 |

On transfer of cash value among the Divisions and to and from the Fixed Account | Not currently charged | $25 for each transfer | |||

| Partial Withdrawal Charge |

On partial withdrawal of cash value | Not currently charged | $25 for each partial withdrawal5 | |||

| Illustration of Benefits Charge |

On provision of each illustration in excess of one per year | Not currently charged | $25 per illustration | |||

| 1 | The Surrender Charge varies based on individual characteristics, including the insured’s issue age, risk class, sex (except for unisex Policies), smoker status, and the Policy’s face amount. The Surrender Charge |

A-9

Table of Contents

| may not be representative of the charge that a particular Policy Owner would pay. You can obtain more information about the Surrender Charge that would apply for a particular insured by contacting your registered representative. |

| 2 | No Surrender Charge will apply on up to 10% of cash surrender value withdrawn each year. The Surrender Charge will remain level for one to three Policy years, and will then begin to decline on a monthly basis until it reaches zero in the last month of the tenth Policy year. The Surrender Charge applies to requested face amount reductions as well as to face amount reductions resulting from a change in death benefit option. |

| 3 | The Representative Insured is a male, age 35, in the preferred nonsmoker risk class, under a Policy with a base Policy face amount of $375,000. |

| 4 | The Portfolios in which the Divisions invest may impose a redemption fee on shares held for a relatively short period. |

| 5 | If imposed, the partial withdrawal charge would be in addition to any Surrender Charge that is imposed. |

The next table describes the fees and expenses that a Policy Owner will pay periodically during the time that he or she owns the Policy, not including Portfolio fees and expenses.

Periodic Charges other than Portfolio Operating Expenses

| Charge |

When Charge is Deducted |

Current Amount Deducted |

Maximum Amount Deductible | |||

| Cost of Insurance1 |

||||||

| Minimum and Maximum Charge |

Monthly | $.01 to $83.33 per $1,000 of net amount at risk2 | $.02 to $83.33 per $1,000 of net amount at risk2 | |||

| Charge in the first Policy year for a Representative Insured 3 |

Monthly | $.02 per $1,000 of net amount at risk | $.09 per $1,000 of net amount at risk | |||

| Policy Charge4 |

||||||

| Policy face amount less than $50,000 |

Monthly | $12 | $12 | |||

| Policy face amount between $50,000 and $249,999 |

Monthly | $15 | $15 | |||

| Mortality and Expense Risk Charge (annual rate imposed on Cash Value in the Separate Account)5 |

Monthly | .60% | .80% | |||

| Coverage Expense Charge6 |

||||||

| Minimum and Maximum Charge |

Monthly | $.04 to $2.30 per $1,000 of base Policy face amount7 | $.04 to $2.30 per $1,000 of base Policy face amount | |||

| Charge for a Representative Insured 3 |

Monthly | $.16 per $1,000 of base Policy face amount7 | $.16 per $1,000 of base Policy face amount | |||

| Loan Interest Spread8 |

Annually (or on loan termination, if earlier) | 1.00% of loan collateral | 1.00% of loan collateral | |||

A-10

Table of Contents

| 1 | The cost of insurance charge varies based on individual characteristics, including the Policy’s face amount and the insured’s age, risk class, and (except for unisex Policies) sex. The cost of insurance charge may not be representative of the charge that a particular Policy Owner would pay. You can obtain more information about the cost of insurance charge that would apply for a particular insured by contacting your registered representative. |

| 2 | The net amount at risk is the difference between the death benefit (generally discounted at the monthly equivalent of 3% per year) and the Policy’s Cash Value. |

| 3 | The Representative Insured is a male, age 35, in the preferred nonsmoker risk class, under a Policy with a base Policy face amount of $375,000. |

| 4 | After the first Policy Year, the Policy Charge declines to $9 for a Policy with a face amount of less than $50,000, and to $8 for a Policy with a face amount between $50,000 and $249,999. No Policy Charge applies if a Policy is issued with a face amount equal to or greater than $250,000. |

| 5 | The Mortality and Expense Risk Charge declines over time in accordance with the following schedule: |

| Current Charge | Maximum Charge | |||||||

| Policy years 1 - 10 |

.60 | % | .80 | % | ||||

| Policy years 11 - 19 |

.35 | % | .35 | % | ||||

| Policy years 20 - 29 |

.20 | % | .20 | % | ||||

| Policy years 30+ |

.05 | % | .05 | % | ||||

The Current Charge Percentages shown above apply if the Policy’s net Cash Value is less than the equivalent of five Target Premiums. The percentages decrease as the Policy’s net Cash Value, measured as a multiple of Target Premiums, increases, as shown below:

| Less than 5 target premiums |

At least 5 but less than 10 target premiums |

At least 10 but less than 20 target premiums |

20 or more target premiums |

|||||||||||||

| Policy years 1- 10 |

.60 | % | .55 | % | .30 | % | .15 | % | ||||||||

| Policy years 11- 19 |

.35 | % | .30 | % | .15 | % | .10 | % | ||||||||

| Policy years 20- 29 |

.20 | % | .15 | % | .10 | % | .05 | % | ||||||||

| Policy years 30+ |

.05 | % | .05 | % | .05 | % | .05 | % | ||||||||

| 6 | The Coverage Expense Charge varies based on individual characteristics, including the Policy’s face amount and the Insured’s age, risk class, and (except for unisex Policies) sex. The Coverage Expense Charge may not be representative of the charge that a particular Policy Owner would pay. You can obtain more information about the Coverage Expense Charge that would apply to a particular insured by contacting your registered representative. |

| 7 | The Coverage Expense Charge is imposed in Policy years 1-8 and, with respect to a requested face amount increase, during the first eight years following the increase. If you surrender the Policy in the first Policy year (or in the first year following a face amount increase), we will deduct from the surrender proceeds an amount equal to the Coverage Expense Charges due for the remainder of the first Policy year (or the first year following the face amount increase). If the Policy’s face amount is reduced in the first year following a face amount increase, we will deduct from the Cash Value an amount equal to the Coverage Expense Charges due for the remainder of the first year following the face amount increase. |

| 8 | The loan interest spread is the difference between the interest rates we charge on Policy loans and the interest earned on Cash Value we hold as security for the loan (“loan collateral”). We charge interest on Policy loans at an effective rate of 4.0% per year in Policy years 1-10 and 3.0% thereafter. Loan collateral earns interest at an effective rate of not less than 3.0% per year. |

A-11

Table of Contents

Charges for Optional Features (Riders):

| Charge |

When Charge is Deducted | Current Amount Deducted |

Maximum Amount Deductible | |||||

| Guaranteed Survivor Income Benefit Rider1 |

||||||||

| Minimum and Maximum Charge |

Monthly | $.01 to $1.08 per $1,000 of Eligible Death Benefit | $.01 to $83.33 per $1,000 of Eligible Death Benefit | |||||

| Charge for a Representative Insured2 |

Monthly | $.02 per $1,000 of Eligible Death Benefit | $.02 per $1,000 of Eligible Death Benefit | |||||

| Children’s Term Insurance Rider |

Monthly | $.40 per $1,000 of rider face amount | $.40 per $1,000 of rider face amount | |||||

| Waiver of Monthly Deduction Rider3 |

||||||||

| Minimum and Maximum Charge |

Monthly | $.00 to $61.44 per $100 of Monthly Deduction | $.00 to $61.44 per $100 of Monthly Deduction | |||||

| Charge in the first Policy year for a Representative insured4 |

Monthly | $6.30 per $100 of Monthly Deduction | $6.30 per $100 of Monthly Deduction | |||||

| Waiver of Specified Premium Rider |

||||||||

| Minimum and Maximum Charge |

Monthly | $.00 to $21.75 per $100 of Specified Premium | $.00 to $21.75 per $100 of Specified Premium | |||||

| Charge in the first Policy year for a Representative Insured4 |

Monthly | $3.00 per $100 of Specified Premium | $3.00 per $100 of Specified Premium | |||||

| 1 | The charge for the Guaranteed Survivor Income Benefit Rider varies based on individual characteristics, including the rider’s Eligible Death Benefit and the insured’s age, risk class, and (except for unisex Policies) sex. The rider change may not be representative of the charge that a particular Policy Owner would pay. You can obtain more information about the rider charge that would apply for a particular insured by contacting your registered representative. |

| 2 | The Representative Insured is a male, age 35, in the preferred nonsmoker risk class, under a Policy with an Eligible Death Benefit of $375,000. |

| 3 | The charge for this rider varies based on individual characteristics, including the insured’s age, risk class, and (except for unisex Policies) sex. The rider charge may not be representative of the charge that a particular Policy Owner would pay. You can obtain more information about the rider charge that would apply for a particular insured by contacting your registered representative. |

| 4 | The Representative Insured is a male, age 35, in the preferred nonsmoker risk class. |

A-12

Table of Contents

| Charge |

When Charge is Deducted | Current Amount Deducted |

Maximum Amount Deductible | |||

| Options to Purchase Additional Insurance Coverage Rider1 |

||||||

| Minimum and Maximum Charge |

Monthly | $.02 to $.25 per $1,000 of Option amount | $.02 to $.25 per $1,000 of Option amount | |||

| Charge for a Representative Insured2 |

Monthly | $.03 per $1,000 of Option amount | $.03 per $1,000 of Option amount | |||

| Accidental Death Benefit Rider1 |

||||||

| Minimum and Maximum Charge |

Monthly | $.00 to $.34 per $1,000 of rider face amount | $.00 to $83.33 per $1,000 of rider face amount | |||

| Charge in the first Policy year for a Representative Insured2 |

Monthly | $.05 per $1,000 of rider face amount | $.08 per $1,000 of rider face amount | |||

| Guaranteed Minimum Death Benefit Rider1,3 |

||||||

| Minimum and Maximum Charge |

Monthly | $.03 to $.14 per $1,000 of net amount at risk | $.03 to $83.33 per $1,000 of net amount at risk | |||

| Charge for a Representative Insured4 |

Monthly | $.03 per $1,000 of net amount at risk | $.03 per $1,000 of net amount at risk | |||

| Acceleration of Death Benefit Rider |

At time of benefit payment | Not currently charged | One-time fee of $150 | |||

| Overloan Protection Rider |

At time of exercise | One-time fee of 3.5% of Policy cash value | One-time fee of 3.5% of Policy cash value | |||

| 1 | The charge for this rider varies based on individual characteristics, including the insured’s age, risk class, and (except for unisex Policies) sex. The rider charge may not be representative of the charge that a particular Policy Owner would pay. You can obtain more information about the rider charge that would apply for a particular insured by contacting your registered representative. |

| 2 | The Representative Insured is a male, age 35, in the preferred nonsmoker risk class. |

| 3 | The charge shown applicable to both the Guaranteed Minimum Death Benefit to Age 85 Rider and the Guaranteed Minimum Death Benefit to Age 121 Rider. |

| 4 | The Representative Insured is a female, age 45, in the preferred nonsmoker risk class. |

Annual Portfolio Operating Expenses

The next table describes the Portfolio fees and expenses that a Policy Owner may pay periodically during the time that he or she owns the Policy. The table shows the minimum and maximum total operating expenses charged by the Portfolios for the fiscal year ended December 31, 2019. Expenses of the Portfolios may be higher or lower in the future. More detail concerning each Portfolio’s fees and expenses is contained in the table that follows and in the prospectus for each Portfolio.

A-13

Table of Contents

Annual Operating Expenses

(as a percentage of average net assets)

Minimum and Maximum Total Annual Portfolio Operating Expenses

| Minimum | Maximum | |||||||

| Total Annual Portfolio Operating Expenses |

||||||||

| (expenses that are deducted from Portfolio assets, including management fees, distribution and/or service (12b-1) fees, and other expenses) |

0.28 | % | 1.42 | % | ||||

Portfolio Fees and Expenses

(as a percentage of average daily net assets)

The following table is a summary. For more complete information on Portfolio fees and expenses, please refer to the prospectus for each Portfolio.

| Portfolio |

Management Fee |

Distribution and/or Service (12b-1) Fees |

Other Expenses |

Acquired Fund Fees and Expenses |

Total Annual Operating Expenses |

Fee Waiver and/or Expense Reimbursement |

Net Total Annual Operating Expenses |

|||||||||||||||||||||

| American Funds Insurance Series® — Class 2 |

||||||||||||||||||||||||||||

| American Funds Bond Fund |

0.36 | % | 0.25 | % | 0.04 | % | — | 0.65 | % | — | 0.65 | % | ||||||||||||||||

| American Funds Global Small Capitalization Fund |

0.70 | % | 0.25 | % | 0.06 | % | — | 1.01 | % | — | 1.01 | % | ||||||||||||||||

| American Funds Growth Fund |

0.32 | % | 0.25 | % | 0.04 | % | — | 0.61 | % | — | 0.61 | % | ||||||||||||||||

| American Funds Growth-Income Fund |

0.26 | % | 0.25 | % | 0.04 | % | — | 0.55 | % | — | 0.55 | % | ||||||||||||||||

| Brighthouse Funds Trust I |

||||||||||||||||||||||||||||

| AB Global Dynamic Allocation Portfolio — Class B |

0.61 | % | 0.25 | % | 0.04 | % | 0.01 | % | 0.91 | % | 0.02 | % | 0.89 | % | ||||||||||||||

| American Funds® Balanced Allocation Portfolio — Class B |

0.06 | % | 0.25 | % | 0.01 | % | 0.42 | % | 0.74 | % | — | 0.74 | % | |||||||||||||||

| American Funds® Growth Allocation Portfolio — Class B |

0.06 | % | 0.25 | % | 0.01 | % | 0.43 | % | 0.75 | % | — | 0.75 | % | |||||||||||||||

| American Funds® Moderate Allocation Portfolio — Class B |

0.06 | % | 0.25 | % | 0.02 | % | 0.41 | % | 0.74 | % | — | 0.74 | % | |||||||||||||||

| AQR Global Risk Balanced Portfolio — Class B |

0.62 | % | 0.25 | % | 0.03 | % | 0.05 | % | 0.95 | % | 0.01 | % | 0.94 | % | ||||||||||||||

| BlackRock Global Tactical Strategies Portfolio — Class B |

0.66 | % | 0.25 | % | 0.02 | % | 0.07 | % | 1.00 | % | 0.05 | % | 0.95 | % | ||||||||||||||

| Brighthouse Asset Allocation 100 Portfolio — Class A |

0.07 | % | — | 0.02 | % | 0.66 | % | 0.75 | % | — | 0.75 | % | ||||||||||||||||

| Brighthouse Balanced Plus Portfolio — Class B |

0.24 | % | 0.25 | % | 0.01 | % | 0.45 | % | 0.95 | % | 0.01 | % | 0.94 | % | ||||||||||||||

| Brighthouse/Aberdeen Emerging Markets Equity Portfolio — Class A |

0.92 | % | — | 0.09 | % | — | 1.01 | % | 0.10 | % | 0.91 | % | ||||||||||||||||

| Brighthouse/Templeton International Bond Portfolio — Class A |

0.60 | % | — | 0.08 | % | — | 0.68 | % | — | 0.68 | % | |||||||||||||||||

| Brighthouse/Wellington Large Cap Research Portfolio — Class A |

0.56 | % | — | 0.03 | % | — | 0.59 | % | 0.04 | % | 0.55 | % | ||||||||||||||||

A-14

Table of Contents

| Portfolio |

Management Fee |

Distribution and/or Service (12b-1) Fees |

Other Expenses |

Acquired Fund Fees and Expenses |

Total Annual Operating Expenses |

Fee Waiver and/or Expense Reimbursement |

Net Total Annual Operating Expenses |

|||||||||||||||||||||

| Clarion Global Real Estate Portfolio — Class A |

0.62 | % | — | 0.05 | % | — | 0.67 | % | 0.04 | % | 0.63 | % | ||||||||||||||||

| Harris Oakmark International Portfolio — Class A |

0.77 | % | — | 0.05 | % | — | 0.82 | % | 0.03 | % | 0.79 | % | ||||||||||||||||

| Invesco Balanced-Risk Allocation Portfolio — Class B |

0.63 | % | 0.25 | % | 0.04 | % | 0.02 | % | 0.94 | % | 0.02 | % | 0.92 | % | ||||||||||||||

| Invesco Global Equity Portfolio — Class A |

0.66 | % | — | 0.04 | % | — | 0.70 | % | 0.11 | % | 0.59 | % | ||||||||||||||||

| Invesco Small Cap Growth Portfolio — Class A |

0.85 | % | — | 0.04 | % | — | 0.89 | % | 0.08 | % | 0.81 | % | ||||||||||||||||

| JPMorgan Global Active Allocation Portfolio — Class B |

0.72 | % | 0.25 | % | 0.05 | % | — | 1.02 | % | 0.06 | % | 0.96 | % | |||||||||||||||

| JPMorgan Small Cap Value Portfolio — Class A |

0.78 | % | — | 0.07 | % | — | 0.85 | % | 0.10 | % | 0.75 | % | ||||||||||||||||

| Loomis Sayles Global Allocation Portfolio — Class A |

0.70 | % | — | 0.08 | % | — | 0.78 | % | 0.01 | % | 0.77 | % | ||||||||||||||||

| Loomis Sayles Growth Portfolio — Class A |

0.57 | % | — | 0.02 | % | — | 0.59 | % | 0.02 | % | 0.57 | % | ||||||||||||||||

| MetLife Multi-Index Targeted Risk Portfolio — Class B |

0.17 | % | 0.25 | % | 0.01 | % | 0.22 | % | 0.65 | % | — | 0.65 | % | |||||||||||||||

| MFS® Research International Portfolio — Class A |

0.70 | % | — | 0.04 | % | — | 0.74 | % | 0.10 | % | 0.64 | % | ||||||||||||||||

| Morgan Stanley Discovery Portfolio — Class A |

0.64 | % | — | 0.04 | % | — | 0.68 | % | 0.02 | % | 0.66 | % | ||||||||||||||||

| PanAgora Global Diversified Risk Portfolio — Class B |

0.65 | % | 0.25 | % | 0.20 | % | 0.02 | % | 1.12 | % | — | 1.12 | % | |||||||||||||||

| PIMCO Inflation Protected Bond Portfolio — Class A |

0.48 | % | — | 0.94 | % | — | 1.42 | % | — | 1.42 | % | |||||||||||||||||

| PIMCO Total Return Portfolio — Class A |

0.48 | % | — | 0.38 | % | — | 0.86 | % | 0.03 | % | 0.83 | % | ||||||||||||||||

| Schroders Global Multi-Asset Portfolio — Class B |

0.63 | % | 0.25 | % | 0.04 | % | 0.02 | % | 0.94 | % | 0.01 | % | 0.93 | % | ||||||||||||||

| SSGA Growth and Income ETF Portfolio — Class A |

0.31 | % | — | 0.01 | % | 0.20 | % | 0.52 | % | — | 0.52 | % | ||||||||||||||||

| SSGA Growth ETF Portfolio — Class A |

0.32 | % | — | 0.03 | % | 0.21 | % | 0.56 | % | — | 0.56 | % | ||||||||||||||||

| T. Rowe Price Mid Cap Growth Portfolio — Class A |

0.75 | % | — | 0.03 | % | — | 0.78 | % | — | 0.78 | % | |||||||||||||||||

| Victory Sycamore Mid Cap Value Portfolio — Class A |

0.65 | % | — | 0.04 | % | — | 0.69 | % | 0.09 | % | 0.60 | % | ||||||||||||||||

| Brighthouse Funds Trust II — Class A |

||||||||||||||||||||||||||||

| Baillie Gifford International Stock Portfolio |

0.79 | % | — | 0.05 | % | — | 0.84 | % | 0.12 | % | 0.72 | % | ||||||||||||||||

| BlackRock Bond Income Portfolio |

0.34 | % | — | 0.05 | % | — | 0.39 | % | — | 0.39 | % | |||||||||||||||||

| BlackRock Capital Appreciation Portfolio |

0.70 | % | — | 0.02 | % | — | 0.72 | % | 0.09 | % | 0.63 | % | ||||||||||||||||

A-15

Table of Contents

| Portfolio |

Management Fee |

Distribution and/or Service (12b-1) Fees |

Other Expenses |

Acquired Fund Fees and Expenses |

Total Annual Operating Expenses |

Fee Waiver and/or Expense Reimbursement |

Net Total Annual Operating Expenses |

|||||||||||||||||||||

| Brighthouse Asset Allocation 20 Portfolio |

0.10 | % | — | 0.03 | % | 0.63 | % | 0.76 | % | 0.03 | % | 0.73 | % | |||||||||||||||

| Brighthouse Asset Allocation 40 Portfolio |

0.06 | % | — | — | 0.63 | % | 0.69 | % | — | 0.69 | % | |||||||||||||||||

| Brighthouse Asset Allocation 60 Portfolio |

0.05 | % | — | — | 0.64 | % | 0.69 | % | — | 0.69 | % | |||||||||||||||||

| Brighthouse Asset Allocation 80 Portfolio |

0.05 | % | — | 0.01 | % | 0.65 | % | 0.71 | % | — | 0.71 | % | ||||||||||||||||

| Brighthouse/Artisan Mid Cap Value Portfolio |

0.82 | % | — | 0.04 | % | — | 0.86 | % | 0.08 | % | 0.78 | % | ||||||||||||||||

| Brighthouse/Wellington Balanced Portfolio |

0.46 | % | — | 0.07 | % | — | 0.53 | % | — | 0.53 | % | |||||||||||||||||

| Brighthouse/Wellington Core Equity Opportunities Portfolio |

0.70 | % | — | 0.02 | % | — | 0.72 | % | 0.12 | % | 0.60 | % | ||||||||||||||||

| Frontier Mid Cap Growth Portfolio |

0.71 | % | — | 0.04 | % | — | 0.75 | % | 0.02 | % | 0.73 | % | ||||||||||||||||

| Jennison Growth Portfolio |

0.60 | % | — | 0.02 | % | — | 0.62 | % | 0.08 | % | 0.54 | % | ||||||||||||||||

| Loomis Sayles Small Cap Core Portfolio |

0.90 | % | — | 0.07 | % | 0.01 | % | 0.98 | % | 0.09 | % | 0.89 | % | |||||||||||||||

| Loomis Sayles Small Cap Growth Portfolio |

0.90 | % | — | 0.08 | % | — | 0.98 | % | 0.09 | % | 0.89 | % | ||||||||||||||||

| MetLife Aggregate Bond Index Portfolio |

0.25 | % | — | 0.03 | % | — | 0.28 | % | 0.01 | % | 0.27 | % | ||||||||||||||||

| MetLife Mid Cap Stock Index Portfolio |

0.25 | % | — | 0.05 | % | 0.01 | % | 0.31 | % | — | 0.31 | % | ||||||||||||||||

| MetLife MSCI EAFE® Index Portfolio |

0.30 | % | — | 0.07 | % | 0.01 | % | 0.38 | % | — | 0.38 | % | ||||||||||||||||

| MetLife Russell 2000® Index Portfolio |

0.25 | % | — | 0.06 | % | — | 0.31 | % | — | 0.31 | % | |||||||||||||||||

| MetLife Stock Index Portfolio |

0.25 | % | — | 0.03 | % | — | 0.28 | % | 0.01 | % | 0.27 | % | ||||||||||||||||

| MFS® Total Return Portfolio |

0.57 | % | — | 0.06 | % | — | 0.63 | % | — | 0.63 | % | |||||||||||||||||

| MFS® Value Portfolio |

0.61 | % | — | 0.02 | % | — | 0.63 | % | 0.06 | % | 0.57 | % | ||||||||||||||||

| Neuberger Berman Genesis Portfolio |

0.82 | % | — | 0.04 | % | — | 0.86 | % | 0.01 | % | 0.85 | % | ||||||||||||||||

| T. Rowe Price Large Cap Growth Portfolio |

0.60 | % | — | 0.03 | % | — | 0.63 | % | 0.05 | % | 0.58 | % | ||||||||||||||||

| T. Rowe Price Small Cap Growth Portfolio |

0.47 | % | — | 0.03 | % | — | 0.50 | % | — | 0.50 | % | |||||||||||||||||

| VanEck Global Natural Resources Portfolio |

0.78 | % | — | 0.03 | % | 0.01 | % | 0.82 | % | 0.06 | % | 0.76 | % | |||||||||||||||

| Western Asset Management Strategic Bond Opportunities Portfolio |

|

0.57 |

% |

|

— |

|

|

0.03 |

% |

|

— |

|

|

0.60 |

% |

|

0.06 |

% |

|

0.54 |

% | |||||||

| Western Asset Management U.S. Government Portfolio |

0.48 | % | — | 0.02 | % | — | 0.50 | % | 0.03 | % | 0.47 | % | ||||||||||||||||

The information shown in the table above was provided by the Portfolios. Certain Portfolios and their investment adviser have entered into expense reimbursement and/or fee waiver arrangements that will continue through April 30, 2021. These arrangements can be terminated with respect to these Portfolios only with the approval of the Portfolio’s board of directors or trustees. Please see the Portfolios’ prospectuses for additional information regarding these arrangements.

A-16

Table of Contents

Certain Portfolios that have “Acquired Fund Fees and Expenses” may be “funds of funds.” A fund of funds invests substantially all of its assets in other underlying funds. Because the Portfolio invests in other funds, it will bear its pro rata portion of the operating expenses of those underlying funds, including the management fee.

None of the Portfolios are affiliated with Metropolitan Life Insurance Company, however, Metropolitan Life Investors (MLI) serves as a sub-adviser to some of the Portfolios available in the Brighthouse Funds Trust I and the Brighthouse Funds Trust II. MLI receives an advisory fee for those Portfolios for which it serves as a sub-adviser. For information concerning compensation paid for the sale of the Policies, see “Distribution of the Policies.”

A-17

Table of Contents

THE COMPANY, THE SEPARATE ACCOUNT AND THE PORTFOLIOS

Metropolitan Life Insurance Company is a provider of insurance, annuities, employee benefits and asset management. We are also one of the largest institutional investors in the United States with a $280.6 billion general account portfolio invested primarily in fixed income securities (corporate, structured products, municipals, and government and agency) and mortgage loans, as well as real estate, real estate joint ventures, other limited partnerships and equity securities, at December 31, 2019. The Company was incorporated under the laws of New York in 1868. The Company’s office is located at 200 Park Avenue, New York, New York 10166-0188. The Company is a wholly-owned subsidiary of MetLife, Inc.. We are obligated to pay all benefits under the Policies.

Metropolitan Life Separate Account UL is the funding vehicle for the Policies and other variable life insurance policies that we issue. Income and realized and unrealized capital gains and losses of the Separate Account are credited to the Separate Account without regard to any of our other income or capital gains or losses. Although we own the assets of the Separate Account, applicable law provides that the portion of the Separate Account assets equal to the reserves and other liabilities of the Separate Account may not be charged with liabilities that arise out of any other business we conduct. This means that the assets of the Separate Account are not available to meet the claims of our general creditors, and may only be used to support the Cash Values of the variable life insurance policies issued by the Separate Account.

We are obligated to pay the death benefit under the Policy even if that amount exceeds the Policy’s Cash Value in the Separate Account. The amount of the death benefit that exceeds the Policy’s Cash Value in the Separate Account is paid from our general account. Death benefits paid from the general account are subject to the financial strength and claims-paying ability of the Company. For other life insurance policies and annuity contracts that we issue, we pay all amounts owed under the policies and contracts from the general account. MetLife is regulated as an insurance company under state law. State law generally imposes restrictions on the amount and type of investments in the general account. However, there is no guarantee that we will be able to meet our claims-paying obligations. There are risks to purchasing any insurance product.

The investment adviser to certain of the Portfolios offered with the Policy or with other variable life insurance policies issued through the Separate Account may be regulated as a Commodity Pool Operator. While it does not concede that the Separate Account is a commodity pool, MetLife has claimed an exclusion from the definition of the term “commodity pool operator” under the Commodities Exchange Act (“CEA”), and is not subject to registration or regulation as a pool operator under the CEA.

Each Division of the Separate Account invests in a corresponding Portfolio. Each Portfolio is part of an open-end management investment company, more commonly known as a mutual fund, that serves as an investment vehicle for variable life insurance and variable annuity separate accounts of various insurance companies. The Trusts that offer the Portfolios are the American Funds Insurance Series®, Brighthouse Funds Trust I, Brighthouse Funds Trust II and the Franklin Templeton Variable Insurance Products Trust. Each of these Trusts has an investment adviser responsible for overall management of each portfolio available in the Trust. Some investment advisers have contracted with sub-advisers to make the day-to-day investment decisions for the Portfolios.

A-18

Table of Contents

The adviser, sub-adviser and investment objective of each Portfolio are as follows:

| Portfolio |

Investment Objective |

Investment Adviser/Subadviser | ||

| American Funds Insurance Series® — Class 2 |

||||

| American Funds Bond Fund |

Seeks as high a level of current income as is consistent with the preservation of capital. | Capital Research and Management CompanySM | ||

| American Funds Global Small Capitalization Fund |

Seeks long-term growth of capital. | Capital Research and Management CompanySM | ||

| American Funds Growth Fund |

Seeks growth of capital. | Capital Research and Management CompanySM | ||

| American Funds Growth-Income Fund |

Seeks long-term growth of capital and income. | Capital Research and Management CompanySM | ||

| Brighthouse Funds Trust I |

||||

| AB Global Dynamic Allocation Portfolio — Class B |

Seeks capital appreciation and current income. | Brighthouse Investment Advisers, LLC Subadviser: AllianceBernstein L.P. | ||

| American Funds® Balanced Allocation Portfolio — Class B |

Seeks a balance between a high level of current income and growth of capital, with a greater emphasis on growth of capital. | Brighthouse Investment Advisers, LLC | ||

| American Funds® Growth Allocation Portfolio — Class B |

Seeks growth of capital. | Brighthouse Investment Advisers, LLC | ||

| American Funds® Moderate Allocation Portfolio — Class B |

Seeks a high total return in the form of income and growth of capital, with a greater emphasis on income. | Brighthouse Investment Advisers, LLC | ||

| AQR Global Risk Balanced Portfolio — Class B |

Seeks total return. | Brighthouse Investment Advisers, LLC Subadviser: AQR Capital Management, LLC | ||

| BlackRock Global Tactical Strategies Portfolio — Class B |

Seeks capital appreciation and current income. | Brighthouse Investment Advisers, LLC Subadviser: BlackRock Financial Management, Inc. | ||

| Brighthouse Asset Allocation 100 Portfolio — Class A |

Seeks growth of capital. | Brighthouse Investment Advisers, LLC | ||

| Brighthouse Balanced Plus Portfolio — Class B |

Seeks a balance between a high level of current income and growth of capital, with a greater emphasis on growth of capital. | Brighthouse Investment Advisers, LLC Subadviser: Overlay Portion: Pacific Investment Management Company LLC | ||

| Brighthouse/Aberdeen Emerging Markets Equity Portfolio — Class A |

Seeks capital appreciation. | Brighthouse Investment Advisers, LLC Subadviser: Aberdeen Asset Managers Limited | ||

| Brighthouse/Templeton International Bond Portfolio — Class A |

Seeks current income with capital appreciation and growth of income. | Brighthouse Investment Advisers, LLC Subadviser: Franklin Advisers, Inc. | ||

| Brighthouse/Wellington Large Cap Research Portfolio — Class A |

Seeks long-term capital appreciation. | Brighthouse Investment Advisers, LLC Subadviser: Wellington Management Company LLP | ||

A-19

Table of Contents

| Portfolio |

Investment Objective |

Investment Adviser/Subadviser | ||

| Clarion Global Real Estate Portfolio — Class A |

Seeks total return through investment in real estate securities, emphasizing both capital appreciation and current income. | Brighthouse Investment Advisers, LLC Subadviser: CBRE Clarion Securities LLC | ||

| Harris Oakmark International Portfolio — Class A |

Seeks long-term capital appreciation. | Brighthouse Investment Advisers, LLC Subadviser: Harris Associates L.P. | ||

| Invesco Balanced-Risk Allocation Portfolio — Class B |

Seeks total return. | Brighthouse Investment Advisers, LLC Subadviser: Invesco Advisers, Inc. | ||

| Invesco Global Equity Portfolio — Class A (formerly Oppenheimer Global Equity Portfolio) |

Seeks capital appreciation. | Brighthouse Investment Advisers, LLC Subadviser: Invesco Advisers, Inc. | ||

| Invesco Small Cap Growth Portfolio — Class A |

Seeks long-term growth of capital. | Brighthouse Investment Advisers, LLC Subadviser: Invesco Advisers, Inc. | ||

| JPMorgan Global Active Allocation Portfolio — Class B |

Seeks capital appreciation and current income. | Brighthouse Investment Advisers, LLC Subadviser: J.P. Morgan Investment Management Inc. | ||

| JPMorgan Small Cap Value Portfolio — Class A |

Seeks long-term capital growth. | Brighthouse Investment Advisers, LLC Subadviser: J.P. Morgan Investment Management Inc. | ||

| Loomis Sayles Global Allocation Portfolio — Class A |

Seeks high total investment return through a combination of capital appreciation and income. | Brighthouse Investment Advisers, LLC Subadviser: Loomis, Sayles & Company, L.P. | ||

| Loomis Sayles Growth Portfolio — Class A (formerly ClearBridge Aggressive Growth Portfolio) |

Seeks long-term growth of capital. | Brighthouse Investment Advisers, LLC Subadviser: Loomis, Sayles & Company, L.P. | ||

| MetLife Multi-Index Targeted Risk Portfolio — Class B |

Seeks a balance between growth of capital and current income, with a greater emphasis on growth of capital. | Brighthouse Investment Advisers, LLC Subadviser: Overlay Portion: MetLife Investment Advisors, LLC | ||

| MFS® Research International Portfolio — Class A |

Seeks capital appreciation. | Brighthouse Investment Advisers, LLC Subadviser: Massachusetts Financial Services Company | ||

| Morgan Stanley Discovery Portfolio — Class A |

Seeks capital appreciation. | Brighthouse Investment Advisers, LLC Subadviser: Morgan Stanley Investment Management Inc. | ||

| PanAgora Global Diversified Risk Portfolio — Class B |

Seeks total return. | Brighthouse Investment Advisers, LLC Subadviser: PanAgora Asset Management, Inc. | ||

| PIMCO Inflation Protected Bond Portfolio — Class A |

Seeks maximum real return, consistent with preservation of capital and prudent investment management. | Brighthouse Investment Advisers, LLC Subadviser: Pacific Investment Management Company LLC | ||

| PIMCO Total Return Portfolio — Class A |

Seeks maximum total return, consistent with the preservation of capital and prudent investment management. | Brighthouse Investment Advisers, LLC Subadviser: Pacific Investment Management Company LLC | ||

A-20

Table of Contents

| Portfolio |

Investment Objective |

Investment Adviser/Subadviser | ||

| Schroders Global Multi-Asset Portfolio — Class B |

Seeks capital appreciation and current income. | Brighthouse Investment Advisers, LLC Subadvisers: Schroder Investment Management North America Inc.; Schroder Investment Management North America Limited | ||

| SSGA Growth and Income ETF Portfolio — Class A |

Seeks growth of capital and income. | Brighthouse Investment Advisers, LLC Subadviser: SSGA Funds Management, Inc. | ||

| SSGA Growth ETF Portfolio — Class A |

Seeks growth of capital. | Brighthouse Investment Advisers, LLC Subadviser: SSGA Funds Management, Inc. | ||

| T. Rowe Price Mid Cap Growth Portfolio — Class A |

Seeks long-term growth of capital. | Brighthouse Investment Advisers, LLC Subadviser: T. Rowe Price Associates, Inc. | ||

| Victory Sycamore Mid Cap Value Portfolio — Class A |

Seeks high total return by investing in equity securities of mid-sized companies. | Brighthouse Investment Advisers, LLC Subadviser: Victory Capital Management Inc. | ||

| Brighthouse Funds Trust II — Class A |

||||

| Baillie Gifford International Stock Portfolio |

Seeks long-term growth of capital. | Brighthouse Investment Advisers, LLC Subadviser: Baillie Gifford Overseas Limited | ||

| BlackRock Bond Income Portfolio |

Seeks a competitive total return primarily from investing in fixed-income securities. | Brighthouse Investment Advisers, LLC Subadviser: BlackRock Advisors, LLC | ||

| BlackRock Capital Appreciation Portfolio |

Seeks long-term growth of capital. | Brighthouse Investment Advisers, LLC Subadviser: BlackRock Advisors, LLC | ||

| Brighthouse Asset Allocation 20 Portfolio |

Seeks a high level of current income, with growth of capital as a secondary objective. | Brighthouse Investment Advisers, LLC | ||

| Brighthouse Asset Allocation 40 Portfolio |

Seeks high total return in the form of income and growth of capital, with a greater emphasis on income. | Brighthouse Investment Advisers, LLC | ||

| Brighthouse Asset Allocation 60 Portfolio |

Seeks a balance between a high level of current income and growth of capital, with a greater emphasis on growth of capital. | Brighthouse Investment Advisers, LLC | ||

| Brighthouse Asset Allocation 80 Portfolio |

Seeks growth of capital. | Brighthouse Investment Advisers, LLC | ||

| Brighthouse/Artisan Mid Cap Value Portfolio |

Seeks long-term capital growth. | Brighthouse Investment Advisers, LLC Subadviser: Artisan Partners Limited Partnership | ||

A-21

Table of Contents

| Portfolio |

Investment Objective |

Investment Adviser/Subadviser | ||

| Brighthouse/Wellington Balanced Portfolio |

Seeks long-term capital appreciation with some current income. | Brighthouse Investment Advisers, LLC Subadviser: Wellington Management Company LLP | ||

| Brighthouse/Wellington Core Equity Opportunities Portfolio |

Seeks to provide a growing stream of income over time and, secondarily, long-term capital appreciation and current income. | Brighthouse Investment Advisers, LLC Subadviser: Wellington Management Company LLP | ||

| Frontier Mid Cap Growth Portfolio |

Seeks maximum capital appreciation. | Brighthouse Investment Advisers, LLC Subadviser: Frontier Capital Management Company, LLC | ||

| Jennison Growth Portfolio |

Seeks long-term growth of capital. | Brighthouse Investment Advisers, LLC Subadviser: Jennison Associates LLC | ||

| Loomis Sayles Small Cap Core Portfolio |

Seeks long-term capital growth from investments in common stocks or other equity securities. | Brighthouse Investment Advisers, LLC Subadviser: Loomis, Sayles & Company, L.P. | ||

| Loomis Sayles Small Cap Growth Portfolio |

Seeks long-term capital growth. | Brighthouse Investment Advisers, LLC Subadviser: Loomis, Sayles & Company, L.P. | ||

| MetLife Aggregate Bond Index Portfolio |

Seeks to track the performance of the Bloomberg Barclays U.S. Aggregate Bond Index. | Brighthouse Investment Advisers, LLC Subadviser: MetLife Investment Advisors, LLC | ||

| MetLife Mid Cap Stock Index Portfolio |

Seeks to track the performance of the Standard & Poor’s MidCap 400® Composite Stock Price Index. | Brighthouse Investment Advisers, LLC Subadviser: MetLife Investment Advisors, LLC | ||

| MetLife MSCI EAFE® Index Portfolio |

Seeks to track the performance of the MSCI EAFE® Index. | Brighthouse Investment Advisers, LLC Subadviser: MetLife Investment Advisors, LLC | ||

| MetLife Russell 2000® Index Portfolio |

Seeks to track the performance of the Russell 2000® Index. | Brighthouse Investment Advisers, LLC Subadviser: MetLife Investment Advisors, LLC | ||

| MetLife Stock Index Portfolio |

Seeks to track the performance of the Standard & Poor’s 500® Composite Stock Price Index. | Brighthouse Investment Advisers, LLC Subadviser: MetLife Investment Advisors, LLC | ||

| MFS® Total Return Portfolio |

Seeks a favorable total return through investment in a diversified portfolio. | Brighthouse Investment Advisers, LLC Subadviser: Massachusetts Financial Services Company | ||

| MFS® Value Portfolio |

Seeks capital appreciation. | Brighthouse Investment Advisers, LLC Subadviser: Massachusetts Financial Services Company | ||

| Neuberger Berman Genesis Portfolio |

Seeks high total return, consisting principally of capital appreciation. | Brighthouse Investment Advisers, LLC Subadviser: Neuberger Berman Investment Advisers LLC | ||

| T. Rowe Price Large Cap Growth Portfolio |

Seeks long-term growth of capital. | Brighthouse Investment Advisers, LLC Subadviser: T. Rowe Price Associates, Inc. | ||

A-22

Table of Contents

| Portfolio |

Investment Objective |

Investment Adviser/Subadviser | ||

| T. Rowe Price Small Cap Growth Portfolio |

Seeks long-term capital growth. | Brighthouse Investment Advisers, LLC Subadviser: T. Rowe Price Associates, Inc. | ||

| VanEck Global Natural Resources Portfolio |

Seeks long-term capital appreciation with income as a secondary consideration. | Brighthouse Investment Advisers, LLC Subadviser: VanEck Associates Corporation | ||

| Western Asset Management Strategic Bond Opportunities Portfolio |

Seeks to maximize total return consistent with preservation of capital. | Brighthouse Investment Advisers, LLC Subadviser: Western Asset Management Company | ||

| Western Asset Management U.S. Government Portfolio |

Seeks to maximize total return consistent with preservation of capital and maintenance of liquidity. | Brighthouse Investment Advisers, LLC Subadviser: Western Asset Management Company | ||

For more information regarding the Portfolios and their investment advisers and subadvisers, see the Portfolio prospectuses and their Statements of Additional Information, which you can obtain by calling 1-800-638-5000.

The Portfolios’ investment objectives may not be met. The investment objectives and policies of certain Portfolios are similar to the investment objectives and policies of other funds that may be managed by the same investment adviser or sub-adviser. The investment results of the Portfolios may be higher or lower than the results of these funds. There is no assurance, and no representation is made, that the investment results of any of the Portfolios will be comparable to the investment results of any other fund.

The Portfolios listed below are managed in a way that is intended to minimize volatility of returns (referred to as a “managed volatility strategy”):

| • | AB Global Dynamic Allocation Portfolio |

| • | AQR Global Risk Balanced Portfolio |

| • | BlackRock Global Tactical Strategies Portfolio |

| • | Invesco Balanced-Risk Allocation Portfolio |

| • | JPMorgan Global Active Allocation Portfolio |

| • | Brighthouse Balanced Plus Portfolio |

| • | MetLife Multi-Index Targeted Risk Portfolio |

| • | PanAgora Global Diversified Risk Portfolio |

| • | Schroders Global Multi-Asset Portfolio |

Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors or general market conditions. Bond prices may fluctuate because they move in the opposite direction of interest rates. Foreign investing carries additional risks such as currency and market volatility. A managed volatility strategy is designed to reduce volatility of returns to the above Portfolios from investing in stocks and bonds. This strategy seeks to reduce such volatility by “smoothing” returns, which may result in a Portfolio outperforming the general securities market during periods of flat or negative market performance, and underperforming the general securities market during periods of positive market performance.

A-23

Table of Contents

This means that in periods of high market volatility, this managed volatility strategy could limit your participation in market gains; this may conflict with your investment objectives by limiting your ability to maximize potential growth of your Policy’s Cash Value and, in turn, the value of any guaranteed benefit that is tied to investment performance. Other Portfolios may offer the potential for higher returns.

Share Classes of the Portfolios

The Portfolios offer various classes of shares, each of which has a different level of expenses. The prospectuses for the Portfolios may provide information for share classes that are not available through the Policy. When you consult the prospectus for any Portfolio, you should be careful to refer to only the information regarding the class of shares that is available through the Policy. For the American Funds Insurance Series and the Franklin Templeton Variable Insurance Products Trust, we offer Class 2 shares only; for Brighthouse Funds Trust I, we offer Class A and Class B shares; and for Brighthouse Funds Trust II, we offer Class A shares only.

Certain Payments We Receive with Regard to the Portfolios

An investment adviser or subadviser of a Portfolio, or its affiliates, may make payments to us and/or certain of our affiliates. These payments may be used for a variety of purposes, including payment for expenses for certain administrative, marketing and support services with respect to the Policies and, in our role as intermediary, with respect to the Portfolios. We and our affiliates may profit from these payments. These payments may be derived, in whole or in part, from fees deducted from Portfolio assets. Policy Owners, through their indirect investment in the Portfolios, bear the costs of these fees (see the Portfolio prospectuses for more information). The amount of the payments we receive is based on a percentage of assets of the Portfolio attributable to the Policies and certain other variable insurance products that we and our affiliates issue. These percentages differ and some advisers or subadvisers (or other affiliates) may pay us more than others. These percentages currently range up to 0.50%. Additionally, an investment adviser or subadviser of a Portfolio or its affiliates may provide us with wholesaling services that assist in the distribution of the Policies and may pay us and/or certain of our affiliates amounts to participate in sales meetings. These amounts may be significant and may provide the adviser or subadviser (or their affiliates) with increased access to persons involved in the distribution of the Policies.

On August 4, 2017, MetLife, Inc. completed the separation of Brighthouse Financial, Inc. and its subsidiaries (“Brighthouse”) where MetLife, Inc. retained an ownership interest of 19.2% non-voting common stock outstanding of Brighthouse Financial, Inc. In June 2018, MetLife, Inc. sold Brighthouse Financial, Inc. common stock in exchange for MetLife, Inc. senior notes and Brighthouse was no longer considered a related party. At December 31, 2018, MetLife, Inc. no longer held any shares of Brighthouse Financial, Inc. for its own account; however, certain insurance company separate accounts managed by MetLife held shares of Brighthouse Financial, Inc. Brighthouse subsidiaries include Brighthouse Investment Advisers, LLC, which serves as the investment adviser for the Brighthouse Funds Trust I and Brighthouse Funds Trust II. We and Our affiliated companies have entered into agreements with Brighthouse Advisers, LLC, Brighthouse Funds Trust I and Brighthouse Funds trust II whereby We receive payments for certain administrative, marketing and support services described in the previous paragraphs. Currently, the Portfolios in Brighthouse Funds Trust I and Brighthouse Funds Trust II are only available in variable annuity contracts and variable life insurance policies issued by Metropolitan Life Insurance Company and its affiliates. As of December 31, 2019, approximately 89% of Portfolio assets held in Separate Accounts of Metropolitan Life Insurance Company and its affiliates were allocated to Portfolios in Brighthouse Funds Trust I and Brighthouse Funds Trust II. Should we or Brighthouse Investment Advisers, LLC decide to terminate the agreements, we would be required to find alternative Portfolios which could have higher or lower costs to the Contract Owner. In addition, the amount of payments we receive could cease or be substantially reduced which may have a material impact on our financial statements.

A-24

Table of Contents

Certain Portfolios have adopted a Distribution Plan under Rule 12b-1 of the Investment Company Act of 1940. A Portfolio’s 12b-1 Plan, if any, is described in more detail in the Portfolio’s prospectus. (See “Fee Tables—Annual Portfolio Expenses” and “Distribution of the Policies.”) Any payments we receive pursuant to those 12b-1 Plans are paid to us or our Distributor MetLife Investors Distribution Company (MLIDC). Payments under a Portfolio’s 12b-1 Plan decrease the Portfolio’s investment return.

For more specific information on the amounts we may receive on account of your investment in the Portfolios, you may call us toll free at 1-800-638-5000.

We select the Portfolios offered through the Policy based on a number of criteria, including asset class coverage, the strength of the adviser’s or subadviser’s reputation and tenure, brand recognition, performance, and the capability and qualification of each investment firm. Another factor we consider during the selection process is whether the Portfolio’s adviser or subadviser is one of our affiliates or whether the Portfolio, its adviser, its subadviser(s), or an affiliate will make payments to us or our affiliates. For additional information on these arrangements, see “Certain Payments We Receive with Regard to the Portfolios” above. In this regard, the profit distributions we receive from our affiliated investment advisers are a component of the total revenue that we consider in configuring the features and investment choices available in the variable insurance products that we and our affiliated insurance companies issue. Since we and our affiliated insurance companies may benefit more from the allocation of assets to Portfolios advised by our affiliates than those that are not, we may be more inclined to offer Portfolios advised by our affiliates in the variable insurance products we issue. We review the Portfolios periodically and may remove a Portfolio or limit its availability to new premium payments and/or transfers of Cash Value if we determine that the Portfolio no longer meets one or more of the selection criteria, and/or if the Portfolio has not attracted significant allocations from Policy Owners. We may include Portfolios based on recommendations from selling firms. In some cases, the selling firms may receive payments from the Portfolios they recommend and may benefit accordingly from the allocation of Cash Value to such Portfolios.

We do not provide any investment advice and do not recommend or endorse any particular Portfolio. You bear the risk of any decline in the Cash Value of your Policy resulting from the performance of the Portfolios you have chosen.

We own the Portfolio shares held in the Separate Account and have the right to vote those shares at meetings of the Portfolio shareholders. However, to the extent required by Federal securities law, we will give you, as Policy Owner, the right to instruct us how to vote the shares that are attributable to your Policy.

We will determine, as of the record date, if you are entitled to give voting instructions and the number of shares to which you have a right of instruction. If we do not receive timely instructions from you, we will vote your shares for, against, or withhold from voting on, any proposition in the same proportion as the shares held in that Division for all Policies for which we have received voting instructions. The effect of this proportional voting is that a small number of Policy Owners may control the outcome of a vote.

We will vote Portfolio shares held by our general account (or any unregistered separate account for which voting privileges were not extended) in the same proportion as the total of (i) shares for which voting instructions were received and (ii) shares that are voted in proportion to such voting instructions.

We may disregard voting instructions for changes in the investment policy, investment adviser or principal underwriter of a Portfolio if required by state insurance law, or if we (i) reasonably disapprove of the changes and (ii) in the case of a change in investment policy or investment adviser, make a good faith determination that the proposed change is prohibited by state authorities or inconsistent with a Division’s investment objectives. If we do disregard voting instructions, the next semi-annual report to Policy Owners will include a summary of that action and the reasons for it.

A-25

Table of Contents

We and our affiliates may change the voting procedures and vote Portfolio shares without Policy Owner instructions, if the securities laws change. We also reserve the right: (1) to add Divisions; (2) to combine Divisions; (3) to substitute shares of another registered open-end management investment company, which may have different fees and expenses, for shares of a Portfolio; (4) to substitute or close a Division to allocations of Premium payments or Cash Value or both, and to existing investments or the investment of future Premiums, or both, for any class of Policy or Policy Owner, at any time in our sole discretion; (5) to operate the Separate Account as a management investment company under the Investment Company Act of 1940 or in any other form; (6) to deregister the Separate Account under the Investment Company Act of 1940; (7) to combine it with other Separate Accounts; and (8) to transfer assets supporting the Policies from one Division to another or from the Separate Account to other Separate Accounts, or to transfer assets to our general account as permitted by applicable law. We will exercise these rights in accordance with applicable law, including approval of Policy Owners if required. We will notify you if exercise of any of these rights would result in a material change in the Separate Account or its investments.

We will not make any changes without receiving any necessary approval of the SEC and applicable state insurance departments. We will notify you of any changes.