|

Summary Prospectus April 14, 2016 |

Schwab

Massachusetts Municipal Money

Fund™

| Ticker Symbol: | Sweep Shares: SWDXX |

Before you invest, you may want to review the

fund’s prospectus, which contains more information about the fund and its risks. You can find the fund’s prospectus, Statement of Additional Information (SAI) and other information about the fund online at

www.csimfunds.com/schwabfunds_prospectus. You can also obtain this information at no cost by calling 1-866-414-6349 or by sending an email request to orders@mysummaryprospectus.com. If you purchase or hold fund shares through a financial intermediary, the fund’s prospectus, SAI, and other information about the fund are available from your financial

intermediary.

The fund’s

prospectus and SAI, both dated April 14, 2016, include a more detailed discussion of fund investment policies and the risks associated with various fund investments. The prospectus and SAI are incorporated by reference into the summary prospectus,

making them legally a part of the summary prospectus.

Investment objective

The fund’s goal is to seek current

income that is exempt from federal income and Massachusetts personal income tax, consistent with preservation of capital and liquidity. The fund’s investment objective is not fundamental and therefore may be changed by the fund’s

board of trustees without shareholder approval.

Fund fees and expenses

This table describes the fees and expenses you

may pay if you buy and hold Sweep Shares of the fund.

| Shareholder fees (fees paid directly from your investment) | |

| None | |

| Annual fund operating expenses (expenses that you pay each year as a % of the value of your investment) | |

| Management fees | 0.35 |

| Distribution (12b-1) fees | None |

| Other expenses | 0.41 |

| Total annual fund operating expenses | 0.76 |

| Less expense reduction | (0.11) |

| Total annual fund operating expenses after expense reduction1 | 0.65 |

| 1 | The investment adviser and its affiliates have agreed to limit the total annual fund operating expenses (excluding interest, taxes and certain non-routine expenses) of the Sweep Shares to 0.65% for so long as the investment adviser serves as the adviser to the fund (contractual expense limitation agreement). This contractual expense limitation agreement may only be amended or terminated with the approval of the fund’s Board of Trustees. The total annual fund operating expenses shown do not include proxy related expenses. If such expenses had been included, total annual fund operating expenses after expense reduction would have been 0.66%. |

Example

This example is intended to help you compare

the cost of investing in the fund’s Sweep Shares with the cost of investing in other mutual funds. The example assumes that you invest $10,000 in the fund for the time periods indicated and then redeem all of your shares at the end of

those time periods. The example also assumes that your investment has a 5% return each year and that the Sweep Shares’ operating expenses remain the same. The figures are based on total annual fund operating expenses after expense

reduction. The expenses would be the same whether you stayed in

the fund or sold your shares at the end of each period. Your

actual costs may be higher or lower.

Expenses on a $10,000 investment

| 1 year | 3 years | 5 years | 10 years |

| $66 | $208 | $362 | $810 |

Principal investment

strategies

To pursue its goal, the fund

invests in money market securities from Massachusetts issuers and from municipal agencies, U.S. territories and possessions. These securities may include general obligation issues, which typically are backed by the

issuer’s ability to levy taxes; revenue bonds, which typically are backed by a stream of revenue from a given source, such as a public water system or hospital; municipal commercial paper and municipal notes; and municipal leases, which may be

used to finance construction or equipment purchases. The fund may invest more than 25% of its total assets in municipal securities financing similar projects such as those relating to education, health care, transportation, utilities, industrial

development and housing. Under normal circumstances, the fund will invest at least 80% of its net assets in municipal money market securities the interest from which is exempt from federal income and Massachusetts personal income tax. The fund

may also invest in municipal securities of issuers located outside of Massachusetts.

The fund may purchase certain variable-rate

demand securities issued by closed-end municipal bond funds, which, in turn, invest primarily in portfolios of Massachusetts tax-exempt municipal bonds. It is anticipated that the interest on the variable-rate demand securities will be exempt from

federal and Massachusetts personal income tax. These securities are considered “municipal money market securities” for purposes of the fund’s 80% investment policy stated above.

Many of the fund’s securities will be

subject to credit or liquidity enhancements from U.S. and/or non-U.S. entities, which are designed to provide incremental levels of creditworthiness or liquidity. Some municipal securities have been structured to resemble variable- and floating-rate

securities so that they meet the requirements for being considered money market instruments.

In choosing securities, the fund’s

manager seeks to maximize current income within the limits of the fund’s investment objective

1 of 4

and credit, maturity and diversification policies. Some of these

policies may be stricter than the federal regulations that apply to all money funds.

The investment adviser’s credit research

department analyzes and monitors the securities that the fund owns or is considering buying. The manager may adjust the fund’s holdings or its average maturity based on actual or anticipated changes in interest rates or credit quality. To

preserve its investors’ capital, the fund seeks to maintain a stable $1.00 share price by operating, on or before October 14, 2016, as a “retail money market fund,” as such term is defined or interpreted under the rules governing

money market funds.

During unusual

market conditions, the fund may invest in taxable money market securities as a temporary defensive measure. When the fund engages in such activities, it may not achieve its investment goal.

Principal risks

The fund is subject to risks, any of which

could cause an investor to lose money. The fund’s principal risks include:

Investment Risk. You could lose money by investing in the fund. Although the fund seeks to preserve the value of your investment at $1.00 per share, it cannot guarantee it will do so. Effective October 14, 2016, the fund may impose a fee

upon the sale of your shares or may temporarily suspend your ability to sell shares if the fund’s liquidity falls below required minimums because of market conditions or other factors. An investment in the fund is not insured or guaranteed by

the Federal Deposit Insurance Corporation or any other government agency. The fund’s sponsor has no legal obligation to provide financial support to the fund, and you should not expect that the sponsor will provide financial support to the

fund at any time.

Retail Money

Market Fund Risk. On or before October 14, 2016, the fund intends to qualify as a “retail money market fund,” as such term is defined or interpreted under the rules governing money market funds. A

“retail money market fund” is a money market fund that has policies and procedures reasonably designed to limit all beneficial owners of the fund to natural persons. Prior to and upon conversion to a “retail money market

fund,” the fund may involuntarily redeem any investor who is not a natural person. The fund will provide advance notice of its intent to make any such involuntary redemption. Neither the fund nor the investment adviser will be responsible for

any loss or tax liability in an investor’s account resulting from such involuntary redemption. As a “retail money market fund,” the fund will be permitted to continue to value its securities using the amortized cost method to

seek to maintain a stable $1.00 share price. However, on or after October 14, 2016, the fund may be subject to liquidity fees and/or redemption gates on fund redemptions if the fund’s liquidity falls below required minimums because of

market conditions or other factors.

Interest Rate Risk. Interest rates rise and fall over time. As with any investment whose yield reflects current interest rates, the fund’s yield will change over time. During periods when interest rates are low, the fund’s

yield (and total return) also will be low or may even be negative, which may make it difficult for the fund to pay expenses out of fund assets or maintain a stable $1.00 share price. Because interest rates in the United States are near

historically low levels, a change in a central bank’s monetary policy or improving

economic conditions may result in an increase in interest rates.

A sudden or unpredictable rise in interest rates may cause volatility in the market and may decrease liquidity in the money market securities markets, making it more difficult for the fund to sell its money market investments at a time when the

investment adviser might wish to sell such investments. Decreased market liquidity also may make it more difficult to value some or all of the fund’s money market securities holdings.

Stable Net Asset Value Risk. If the fund or another money market fund fails to maintain a stable net asset value (or such perception exists in the market place), the fund could experience increased redemptions, which may adversely impact the

fund’s share price. The fund is permitted, among other things, to reduce or withhold any income and/or gains generated from its portfolio to maintain a stable $1.00 share price.

Credit Risk.

The fund is subject to the risk that a decline in the credit quality of a portfolio investment could cause the fund to lose money or underperform. The fund could lose money if the issuer of a portfolio investment fails to make timely principal or

interest payments or if a guarantor or liquidity provider of a portfolio investment fails to honor its obligations. For fixed-rate investments, negative perceptions of the ability of an issuer, guarantor or liquidity provider to make payments or

otherwise honor its obligations, as applicable, could also cause the price of that investment to decline. The credit quality of the fund’s portfolio holdings can change rapidly in certain market environments and any downgrade or default on the

part of a single portfolio investment could cause the fund’s share price or yield to fall. The fund’s investments in securities with credit or liquidity enhancements provided by foreign entities may involve certain risks that are greater

than those associated with investments in securities with credit or liquidity enhancements provided by U.S. entities. These include risks of adverse changes in foreign economic, political, regulatory and other conditions; the imposition of economic

sanctions or other government restrictions; differing accounting, auditing, financial reporting and legal standards and practices; differing securities market structures; and higher transaction costs. In addition, sovereign risk, or the risk that a

government may become unwilling or unable to meet its loan obligations or guarantees, could increase the credit risk of financial institutions connected to that particular country.

Credit and Liquidity Enhancements Risk. The fund may invest in securities with credit or liquidity enhancements provided by a bank or other financial institution, and the existence and nature of such enhancements may be a significant

factor in the investment adviser’s decision-making process. Generally, these enhancements are employed by the issuers of the securities to reduce credit risk and provide enhanced or back-up liquidity for a purchaser, such as the fund.

Adverse developments affecting these banks and financial institutions could therefore have a negative effect on the value of the fund’s holdings. For example, a rating agency downgrade of a credit or liquidity enhancement provider may

adversely affect the value of securities held by the fund. Any decline in the value of the securities held by the fund could cause the fund’s share price or yield to fall. To the extent that a portion of the fund’s underlying

investments are enhanced by the same bank or financial institution, these risks may be increased.

2 of 4

Management Risk. Any actively managed mutual fund is subject to the risk that its investment adviser will select investments or allocate assets in a manner that could cause the fund to underperform or otherwise not meet its

investment objective. The fund’s investment adviser applies its own investment techniques and risk analyses in making investment decisions for the fund, but there can be no guarantee that they will produce the desired results. The investment

adviser’s maturity decisions will also affect the fund’s yield, and potentially could affect its share price. To the extent that the investment adviser anticipates interest rate trends imprecisely, the fund’s yield at times could

lag the yields of other money market funds.

State Risk.

The fund invests primarily in securities issued by the Commonwealth of Massachusetts and its municipalities. Any reduction in the credit ratings of obligations of these issuers could adversely affect the market values and marketability of such

securities, and, consequently, the value of the fund’s portfolio. Further, the fund’s share price and performance could be affected by local, state and regional factors, including erosion of the tax base and changes in the economic

climate. Certain Massachusetts constitutional amendments, legislative measures, executive orders, administrative regulations and voter initiatives could result in adverse consequences affecting Massachusetts and/or its municipalities. National

governmental actions, such as the elimination of tax-exempt status, also could affect performance. In addition, a municipality or municipal project that relies directly or indirectly on national governmental funding mechanisms may be negatively

affected by the national government’s current budgetary constraints.

Investment Concentration Risk. To the extent that the fund invests a substantial portion of its assets in municipal securities financing similar projects, the fund may be more sensitive to adverse economic, business or political developments

affecting those projects. A change that affects one project, such as proposed legislation on the financing of the project, a shortage of materials needed for the project, or a declining need for the project, would likely affect all similar projects

and the overall municipal securities market.

Taxable Determinations Risk. Some of the fund’s income could be taxable. If certain types of investments the fund buys as tax-exempt are later ruled to be taxable, a portion of the fund’s income could become taxable. This risk, although

generally considered low, is somewhat higher for investments that have been structured as municipal money market securities than for investments in other types of municipal money market securities. Any investments in municipal securities from

issuers located in states other than Massachusetts could be subject to Massachusetts state tax. Any defensive investments in taxable securities could generate taxable income. Also, some types of municipal securities produce income that is subject to

the federal alternative minimum tax (AMT).

Liquidity Risk. Liquidity risk exists when particular investments are difficult to purchase, sell or value, especially during stressed market conditions. The market for certain investments may become illiquid due to specific

adverse changes in the conditions of a particular issuer or under adverse market or economic conditions independent of the issuer. In addition, dealer inventories of certain securities – an indication of the ability of dealers to engage

in “market making” – are at, or near, historic lows in relation to

market size, which could potentially lead to decreased

liquidity. In such cases, the fund, due to limitations on investments in illiquid securities and the difficulty in readily purchasing and selling such securities at favorable times or prices, may decline in value, experience lower returns

and/or be unable to achieve its desired level of exposure to a certain issuer or sector. Further, transactions in illiquid securities may entail transaction costs that are higher than those for transactions in liquid securities.

Redemption Risk. The fund may experience periods of heavy redemptions that could cause the fund to liquidate its assets at inopportune times or at a loss or depressed value, particularly during periods of declining or illiquid markets.

Redemptions by a few large investors in the fund may have a significant adverse effect on the fund’s ability to maintain a stable $1.00 share price. In the event any money market fund fails to maintain a stable net asset value, other money

market funds, including the fund, could face a market-wide risk of increased redemption pressures, potentially jeopardizing the stability of their $1.00 share prices.

Money Market Fund Risk. The fund is not designed to offer capital appreciation. In exchange for their emphasis on stability and liquidity, money market investments may offer lower long-term performance than stock or bond

investments.

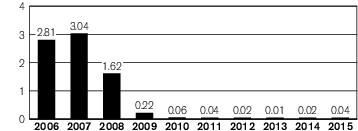

Performance

The bar chart below shows how the

fund’s Sweep Shares investment results have varied from year to year, and the following table shows the fund’s Sweep Shares average annual total returns for various periods. This information provides some indication of the

risks of investing in the fund. All figures assume distributions were reinvested. Keep in mind that future performance may differ from past performance. For current performance information, please see www.csimfunds.com/schwabfunds_prospectus or call

toll-free1-800-435-4000 for the fund’s current seven-day yield.

Annual total returns (%) as of 12/31

Best Quarter: 0.78% Q2 2007

Worst Quarter: 0.00% Q3 2015

Average annual total returns (%) as of 12/31/15

| 1 year | 5 years | 10 years | |

| Sweep Shares | 0.04% | 0.03% | 0.78% |

Investment adviser

Charles Schwab Investment Management,

Inc.

3 of 4

Schwab Massachusetts Municipal Money Fund™; Ticker

Symbol: Sweep Shares: SWDXX

Purchase and sale of fund shares

The fund is open for business each day that

the New York Stock Exchange (NYSE) is open except when the following federal holidays are observed: Columbus Day and Veterans Day. If the NYSE is closed due to weather or other extenuating circumstances on a day it would typically be open for

business, or the NYSE has an unscheduled early closing on a day it has opened for business, the fund reserves the right to treat such day as a business day and accept purchase and redemption orders and calculate its share price as of the normally

scheduled close of regular trading on the NYSE for that day.

Investments in the fund are intended to be

limited to accounts beneficially owned by natural persons. On or before October 14, 2016, the fund will adopt policies and procedures reasonably designed to limit all beneficial owners of the fund to natural persons. The fund reserves the right

to involuntarily redeem shares in any account that are not beneficially owned by natural persons, after providing notice.

Eligible Investors (as determined by the fund

and which are limited to natural persons) may invest in Sweep Shares as noted below. The Sweep Shares are designed for use in conjunction with certain accounts held at Charles Schwab & Co., Inc. (Schwab) and are subject to the terms and

conditions of your Schwab account agreement, as amended from time to time. If you designate the fund as the sweep fund on your Schwab account, your uninvested cash balances will be invested in the fund according to the terms

and conditions of your account agreement. Similarly, when you

use your account to purchase other investments or make payments, shares of the fund will be sold to cover these transactions according to the terms and conditions of your account agreement. You may make purchase, exchange and redemption requests in

accordance with your account agreement.

Tax

information

Distributions received from

the fund are typically intended to be exempt from federal income and Massachusetts personal income tax. While interest from municipal securities is generally exempt from federal income tax, some municipal securities in which the fund may invest may

produce income that is subject to the AMT. The fund may invest a portion of its assets in securities that generate income that is not exempt from federal income and Massachusetts personal income tax. Further, any of the fund’s

defensive investments in taxable securities also could generate taxable income.

Payments to financial intermediaries

The fund pays Schwab for shareholder and sweep

administration services. These payments may create a conflict of interest by influencing Schwab and your salesperson to recommend the fund over another investment. Ask your salesperson or visit Schwab’s website for more information.

REG54664-18 00164121

4 of 4