| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-226486-08 | ||

|

|

Free Writing Prospectus

Structural and Collateral Term Sheet

$900,240,222

(Approximate Initial Pool Balance)

Wells Fargo Commercial Mortgage Trust 2019-C52

as Issuing Entity

Wells Fargo Commercial Mortgage Securities, Inc.

as Depositor

Argentic Real Estate Finance LLC

Rialto Mortgage Finance, LLC

Barclays Capital Real Estate Inc.

Ladder Capital Finance LLC

BSPRT CMBS Finance, LLC

Wells Fargo Bank, National Association

as Sponsors and Mortgage Loan Sellers

Commercial

Mortgage Pass-Through Certificates

Series 2019-C52

July 25, 2019

WELLS FARGO SECURITIES Co-Lead Manager and Joint Bookrunner |

BARCLAYS Co-Lead Manager and Joint Bookrunner | |

Academy Securities Co-Manager |

Drexel Hamilton Co-Manager |

STATEMENT REGARDING THIS FREE WRITING PROSPECTUS

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (‘‘SEC’’) (SEC File No. 333-226486) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC Web site at www.sec.gov. Alternatively, the depositor, any underwriter, or any dealer participating in the offering will arrange to send you the prospectus after filing if you request it by calling toll free 1-800-745-2063 (8 a.m. – 5 p.m. EST) or by emailing wfs.cmbs@wellsfargo.com.

Nothing in this document constitutes an offer of securities for sale in any jurisdiction where the offer or sale is not permitted. The information contained herein is preliminary as of the date hereof, supersedes any such information previously delivered to you and will be superseded by any such information subsequently delivered and ultimately by the final prospectus relating to the securities. These materials are subject to change, completion, supplement or amendment from time to time.

This free writing prospectus has been prepared by the underwriters for information purposes only and does not constitute, in whole or in part, a prospectus for the purposes of Directive 2003/71/EC (as amended) and/or Part VI of the Financial Services and Markets Act 2000, as amended, or other offering document.

STATEMENT REGARDING ASSUMPTIONS AS TO SECURITIES, PRICING ESTIMATES AND OTHER INFORMATION

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) which have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected herein. As such, no assurance can be given as to the Computational Materials’ accuracy, appropriateness or completeness in any particular context; or as to whether the Computational Materials and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of these securities. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the attached Computational Materials. The specific characteristics of the securities may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any security described in the Computational Materials are subject to change prior to issuance. None of Wells Fargo Securities, LLC, Barclays Capital Inc., Academy Securities, Inc., Drexel Hamilton, LLC, or any of their respective affiliates, make any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the securities. The information in this presentation is based upon management forecasts and reflects prevailing conditions and management’s views as of this date, all of which are subject to change. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Mortgage Loan Sellers or which was otherwise reviewed by us.

This free writing prospectus contains certain forward-looking statements. If and when included in this free writing prospectus, the words “expects”, “intends”, “anticipates”, “estimates” and analogous expressions and all statements that are not historical facts, including statements about our beliefs or expectations, are intended to identify forward-looking statements. Any forward-looking statements are made subject to risks and uncertainties which could cause actual results to differ materially from those stated. Those risks and uncertainties include, among other things, declines in general economic and business conditions, increased competition, changes in demographics, changes in political and social conditions, regulatory initiatives and changes in customer preferences, many of which are beyond our control and the control of any other person or entity related to this offering. The forward-looking statements made in this free writing prospectus are made as of the date stated on the cover. We have no obligation to update or revise any forward-looking statement.

Wells Fargo Securities is the trade name for the capital markets and investment banking services of Wells Fargo & Company and its subsidiaries, including but not limited to Wells Fargo Securities, LLC, a member of NYSE, FINRA, NFA and SIPC, Wells Fargo Prime Services, LLC, a member of FINRA, NFA and SIPC, and Wells Fargo Bank, N.A. Wells Fargo Securities, LLC and Wells Fargo Prime Services, LLC are distinct entities from affiliated banks and thrifts.

IMPORTANT NOTICE REGARDING THE OFFERED CERTIFICATES

The information herein is preliminary and may be supplemented or amended prior to the time of sale. In addition, the Offered Certificates referred to in these materials and the asset pool backing them are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis.

The underwriters described in these materials may from time to time perform investment banking services for, or solicit investment banking business from, any company named in these materials. The underwriters and/or their affiliates or respective employees may from time to time have a long or short position in any security or contract discussed in these materials.

The information contained herein supersedes any previous such information delivered to any prospective investor and will be superseded by information delivered to such prospective investor prior to the time of sale.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY-GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of any email communication to which this free writing prospectus is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) any representation that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

2

| Wells Fargo Commercial Mortgage Trust 2019-C52 | Transaction Highlights |

A. Transaction Highlights

Mortgage Loan Sellers:

Mortgage Loan Seller |

Number

of |

Number

of |

Aggregate Cut-off Date Balance |

%

of Initial Pool | |||||

| Argentic Real Estate Finance LLC | 10 | 24 | $196,152,533 | 21.8 | % | ||||

| Rialto Mortgage Finance, LLC | 12 | 13 | 156,301,747 | 17.4 | |||||

| Barclays Capital Real Estate Inc. | 7 | 38 | 149,435,533 | 16.6 | |||||

| Ladder Capital Finance LLC | 16 | 20 | 140,673,066 | 15.6 | |||||

| BSPRT CMBS Finance, LLC | 9 | 14 | 131,071,354 | 14.6 | |||||

| Wells Fargo Bank, National Association | 13 | 17 | 126,605,989 | 14.1 | |||||

Total |

67 |

126 |

$900,240,222 |

100.0 |

% | ||||

Loan Pool:

| Initial Pool Balance: | $900,240,222 |

| Number of Mortgage Loans: | 67 |

| Average Cut-off Date Balance per Mortgage Loan: | $13,436,421 |

| Number of Mortgaged Properties: | 126 |

| Average Cut-off Date Balance per Mortgaged Property(1): | $7,144,764 |

| Weighted Average Mortgage Interest Rate: | 4.399% |

| Ten Largest Mortgage Loans as % of Initial Pool Balance: | 39.2% |

| Weighted Average Original Term to Maturity or ARD (months): | 116 |

| Weighted Average Remaining Term to Maturity or ARD (months): | 115 |

| Weighted Average Original Amortization Term (months)(2): | 357 |

| Weighted Average Remaining Amortization Term (months)(2): | 357 |

| Weighted Average Seasoning (months): | 1 |

| (1) | Information regarding mortgage loans secured by multiple properties is based on an allocation according to relative appraised values or the allocated loan amounts or property-specific release prices set forth in the related loan documents or such other allocation as the related mortgage loan seller deemed appropriate. |

| (2) | Excludes any mortgage loan that does not amortize. |

Credit Statistics:

| Weighted Average U/W Net Cash Flow DSCR(1): | 2.14x |

| Weighted Average U/W Net Operating Income Debt Yield(1): | 11.5% |

| Weighted Average Cut-off Date Loan-to-Value Ratio(1): | 61.6% |

| Weighted Average Balloon or ARD Loan-to-Value Ratio(1): | 55.8% |

| % of Mortgage Loans with Additional Subordinate Debt(2): | 9.4% |

| % of Mortgage Loans with Single Tenants(3): | 15.9% |

| (1) | With respect to any mortgage loan that is part of a whole loan, loan-to-value ratio, debt service coverage ratio and debt yield calculations include the related pari passu companion loan(s) but exclude any related subordinate companion loans (unless otherwise stated). The debt service coverage ratio, debt yield and loan-to-value ratio information do not take into account any subordinate debt (whether or not secured by the related mortgaged property), that currently exists or is allowed under the terms of any mortgage loan. See “Description of the Mortgage Pool—Mortgage Pool Characteristics” in the Preliminary Prospectus and Annex A-1 to the Preliminary Prospectus. |

| (2) | The percentage figure expressed as “% of Mortgage Loans with Additional Subordinate Debt” is determined as a percentage of the initial pool balance and does not take into account any future subordinate debt (whether or not secured by the mortgaged property), if any, that may be permitted under the terms of any mortgage loan or the pooling and servicing agreement. See “Description of the Mortgage Pool—Additional Indebtedness—Other Unsecured Indebtedness” in the Preliminary Prospectus. |

| (3) | Excludes mortgage loans that are secured by multiple single tenant properties. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

3

| Wells Fargo Commercial Mortgage Trust 2019-C52 | Characteristics of the Mortgage Pool |

| B. | Summary of the Whole Loans |

| Property Name | Mortgage Loan Seller in WFCM 2019-C52 |

Note(s)(1) | Original Balance | Holder of Note(1) | Lead Servicer for Whole Loan | Master Servicer Under Lead Securitization Servicing Agreement |

Special Servicer Under Lead Securitization Servicing Agreement | |

| Moffett Towers - Buildings 3 & 4 | Barclays | A-1-A, A-2-A, A-3-A | $5,000,000 | MFTII 2019-B3B4 | No | KeyBank National Association | Situs Holdings, LLC | |

| A-1-B(2) | $65,000,000 | Barclays Capital Real Estate Inc. | (2) | |||||

| A-1-C | $50,000,000 | BANK 2019-BNK19 | No | |||||

| A-1-D | $49,750,000 | WFCM 2019-C52 | No | |||||

| A-1-E | $25,000,000 | Barclays Capital Real Estate Inc. | No | |||||

| A-2-B. A-2-C | $77,625,000 | Deutsche Bank AG, New York Branch | No | |||||

| A-3-B. A-3-C | $77,625,000 | Goldman Sachs Bank USA | No | |||||

| B-1, B-2, B-3(2) | $155,000,000 | MFTII 2019-B3B4 | Yes | |||||

| SoCal Retail Portfolio-WF | AREF | A-1 | $40,000,000 | MSC 2019-H7 | Yes | Midland Loan Services | LNR Partners, LLC | |

| A-2, A-7, A-8 | $64,785,000 | MSC 2019-H6 | No | |||||

| A-3 | $40,000,000 | WFCM 2019-C52 | No | |||||

| A-4, A-6 | $50,000,000 | Argentic Real Estate Finance LLC | No | |||||

| A-5 | $20,000,000 | MSC 2019-H7 | No | |||||

| Embassy Suites at Centennial Olympic Park-WF | AREF | A-1 | $30,000,000 | MSC 2019-H7 | Yes | Midland Loan Services | LNR Partners, LLC | |

| A-2, A-4, A-5, A-6 | $38,500,000 | WFCM 2019-C52 | No | |||||

| A-3 | $15,000,000 | MSC 2019-H7 | No | |||||

| Inland Life Storage Portfolio | Barclays | A-1-A | $39,505,000 | KeyBank National Association | Yes | Wells

Fargo Bank, National Association(3) |

LNR Partners, LLC(3) | |

| A-1-B | $27,000,000 | KeyBank National Association | No | |||||

| A-1-C | $10,000,000 | KeyBank National Association | No | |||||

| A-2-A | $31,297,500 | Barclays Capital Real Estate Inc. | No | |||||

| A-2-B | $31,297,500 | WFCM 2019-C52 | No | |||||

| Renaissance Center VI | BSPRT | A-1 | $22,500,000 | WFCM 2019-C52 | Yes | Wells

Fargo Bank, National Association |

LNR Partners, LLC | |

| A-2 | $12,500,000 | BBCMS 2019-C4 | No | |||||

| 188 Spear Street | Barclays | A-1 | $60,000,000 | Barclays Capital Real Estate Inc | Yes | Wells

Fargo Bank, National Association |

C-III Asset Management LLC | |

| A-2 | $47,000,000 | WFCM 2019-C51 | No | |||||

| A-3 | $18,000,00 | WFCM 2019-C52 | No | |||||

| El Con Center | RMF | A-1 | $45,000,000 | WFCM 2019-C51 | Yes | Wells

Fargo Bank, National Association |

C-III Asset Management LLC | |

| A-2 | $18,000,000 | WFCM 2019-C52 | No | |||||

| Mount Kemble | BSPRT | A-1 | $17,000,000 | WFCM 2019-C52 | Yes | Wells

Fargo Bank, National Association |

LNR Partners, LLC | |

| A-2 | $14,000,000 | BBCMS 2019-C4 | No | |||||

| Shetland Park | RMF | A-1 | $45,000,000 | WFCM 2019-C51 | Yes | Wells

Fargo Bank, National Association |

C-III Asset Management LLC | |

| A-2 | $13,000,000 | WFCM 2019-C52 | No | |||||

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

4

| Wells Fargo Commercial Mortgage Trust 2019-C52 | Characteristics of the Mortgage Pool |

| Property Name | Mortgage

Loan Seller in WFCM 2019-C52 |

Note(s)(1) | Original Balance | Holder of Note(1) | Lead Servicer for Whole Loan | Master Servicer Under Lead Securitization Servicing Agreement |

Special Servicer Under Lead Securitization Servicing Agreement | |

| Smoke Tree Village and Smoke Tree Commons | RMF | A-1 | $25,000,000 | Rialto Mortgage Finance, LLC | Yes | Wells

Fargo Bank, National Association(3) |

LNR Partners, LLC(3) | |

| A-2 | $10,000,000 | WFCM 2019-C52 | No | |||||

| Del Mar Terrace Apartments | BSPRT | A-1 | $9,500,000 | WFCM 2019-C52 | Yes | Wells

Fargo Bank, National Association |

LNR Partners, LLC | |

| A-2 | $6,700,000 | BSPRT CMBS Finance, LLC | No | |||||

| (1) | Unless otherwise indicated, each note not currently held by a securitization trust is expected to be contributed to a future securitization. No assurance can be provided that any such note will not be split further. |

| (2) | The controlling note holder with respect to Moffett Towers – Buildings 3 & 4 Whole Loan will be (i) prior to a control appraisal period, the controlling class certificateholder under the MFTII 2019-B3B4 securitization, or (ii) during a control appraisal period, the holder of Note A-1-B or the directing certificateholder of the securitization trust that holds Note A-1-B. See “Description of the Mortgage Pool — The Whole Loans — The Non-Serviced AB Whole Loans” in the Preliminary Prospectus. |

| (3) | The related whole loan is expected to initially be serviced under the WFCM 2019-C52 pooling and servicing agreement until the securitization of the related “lead” pari passu note (namely, the related pari passu note marked “Yes” in the column entitled “Lead Servicer for Whole Loan”), after which the related whole loan will be serviced under the pooling and servicing agreement governing such securitization of the related “lead” pari passu note. The master servicer and special servicer for such securitization will be identified in a notice, report or statement to holders of the WFCM 2019-C52 certificates after the closing of such securitization. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

5

| Wells Fargo Commercial Mortgage Trust 2019-C52 | Characteristics of the Mortgage Pool |

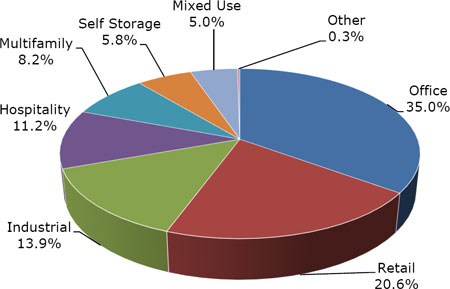

C. Property Type Distribution(1)

| Property Type | Number of Mortgaged Properties | Aggregate

Cut-off Date Balance ($) |

%

of Initial Pool Balance (%) |

Weighted Average Cut-off Date LTV Ratio (%) | Weighted Average Balloon or ARD LTV Ratio (%) |

Weighted Average U/W NCF DSCR (x) |

Weighted Average U/W NOI Debt Yield (%) | Weighted Average U/W NCF Debt Yield (%) | Weighted Average Mortgage Rate (%) | |||||||

| Office | 18 | $314,972,731 | 35.0 | % | 61.1 | % | 56.6 | % | 2.31 | x | 11.7 | % | 11.1 | % | 4.284 | % |

| Suburban | 16 | 266,972,731 | 29.7 | 61.6 | 56.2 | 2.30 | 11.9 | 11.2 | 4.258 | |||||||

| Medical | 1 | 30,000,000 | 3.3 | 59.2 | 59.2 | 2.07 | 10.7 | 10.4 | 4.950 | |||||||

| CBD | 1 | 18,000,000 | 2.0 | 57.6 | 57.6 | 2.82 | 10.5 | 10.2 | 3.570 | |||||||

| Retail | 28 | 185,685,711 | 20.6 | 63.2 | 58.7 | 2.01 | 10.5 | 9.9 | 4.444 | |||||||

| Anchored | 22 | 170,097,243 | 18.9 | 63.2 | 58.4 | 2.03 | 10.6 | 9.9 | 4.430 | |||||||

| Single Tenant | 3 | 8,431,000 | 0.9 | 67.3 | 67.3 | 1.78 | 8.5 | 8.5 | 4.707 | |||||||

| Unanchored | 1 | 4,875,000 | 0.5 | 59.8 | 54.9 | 1.77 | 11.8 | 11.0 | 4.650 | |||||||

| Shadow Anchored | 2 | 2,282,469 | 0.3 | 52.0 | 52.0 | 2.28 | 9.9 | 9.4 | 4.059 | |||||||

| Industrial | 20 | 124,934,433 | 13.9 | 60.6 | 53.8 | 1.86 | 11.1 | 10.4 | 4.272 | |||||||

| Flex | 4 | 46,540,000 | 5.2 | 62.0 | 55.7 | 1.79 | 9.4 | 8.9 | 4.176 | |||||||

| Warehouse Distribution | 8 | 35,531,519 | 3.9 | 63.0 | 55.2 | 1.83 | 11.6 | 11.0 | 4.416 | |||||||

| Manufacturing | 5 | 27,100,000 | 3.0 | 50.0 | 45.4 | 2.13 | 13.0 | 12.2 | 3.990 | |||||||

| Warehouse | 3 | 15,762,913 | 1.8 | 69.4 | 59.4 | 1.70 | 11.6 | 10.6 | 4.716 | |||||||

| Hospitality | 10 | 100,886,177 | 11.2 | 63.3 | 51.0 | 1.93 | 13.8 | 12.3 | 4.759 | |||||||

| Limited Service | 8 | 56,437,520 | 6.3 | 61.3 | 48.9 | 2.06 | 15.0 | 13.4 | 4.848 | |||||||

| Full Service | 1 | 38,455,033 | 4.3 | 68.4 | 55.5 | 1.72 | 11.7 | 10.6 | 4.590 | |||||||

| Select Service | 1 | 5,993,624 | 0.7 | 49.5 | 40.8 | 1.99 | 15.5 | 12.8 | 5.000 | |||||||

| Multifamily | 6 | 74,250,000 | 8.2 | 58.1 | 56.3 | 2.96 | 12.5 | 12.1 | 4.537 | |||||||

| Garden | 4 | 39,500,000 | 4.4 | 48.5 | 48.5 | 4.24 | 15.7 | 15.1 | 4.159 | |||||||

| Mid Rise | 1 | 18,750,000 | 2.1 | 67.4 | 67.4 | 1.49 | 7.9 | 7.8 | 5.150 | |||||||

| Student Housing | 1 | 16,000,000 | 1.8 | 71.1 | 62.6 | 1.52 | 9.7 | 9.5 | 4.750 | |||||||

| Self Storage | 37 | 52,286,813 | 5.8 | 60.0 | 53.2 | 1.88 | 10.2 | 10.1 | 4.087 | |||||||

| Self Storage | 37 | 52,286,813 | 5.8 | 60.0 | 53.2 | 1.88 | 10.2 | 10.1 | 4.087 | |||||||

| Mixed Use | 6 | 44,954,814 | 5.0 | 65.3 | 58.9 | 1.70 | 10.3 | 9.5 | 4.683 | |||||||

| Retail/Office | 3 | 20,975,000 | 2.3 | 62.6 | 53.9 | 1.51 | 9.3 | 8.9 | 4.644 | |||||||

| Industrial/Office/Self Storage | 1 | 12,957,960 | 1.4 | 72.8 | 67.5 | 1.52 | 11.5 | 10.0 | 5.150 | |||||||

| Office/Retail | 2 | 11,021,854 | 1.2 | 61.8 | 58.4 | 2.28 | 10.7 | 10.3 | 4.207 | |||||||

| Other | 1 | 2,269,542 | 0.3 | 41.0 | 33.5 | 1.49 | 9.7 | 9.3 | 4.730 | |||||||

| Leased Fee | 1 | 2,269,542 | 0.3 | 41.0 | 33.5 | 1.49 | 9.7 | 9.3 | 4.730 | |||||||

| Total/Weighted Average: | 126 | $900,240,222 | 100.0 | % | 61.6 | % | 55.8 | % | 2.14 | x | 11.5 | % | 10.8 | % | 4.399 | % |

| (1) | Because this table presents information relating to the mortgaged properties and not the mortgage loans, the information for mortgage loans secured by more than one mortgaged property is based on allocated amounts (allocating the principal balance of the mortgage loan to each of those properties according to the relative appraised values of the mortgaged properties or the allocated loan amounts or property-specific release prices set forth in the related mortgage loan documents or such other allocation as the related mortgage loan seller deemed appropriate). With respect to any mortgage loan that is part of a whole loan, the loan-to-value ratio, debt service coverage ratio and debt yield calculations include the related pari passu companion loan(s) but exclude any related subordinate companion loans (unless otherwise stated). With respect to each mortgage loan, debt service coverage ratio, debt yield and loan-to-value ratio information do not take into account any subordinate debt (whether or not secured by the related mortgaged property) that currently exists or is allowed under the terms of such mortgage loan. See Annex A-1 to the Preliminary Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

6

| Wells Fargo Commercial Mortgage Trust 2019-C52 | Certain Terms and Conditions |

D. Large Loan Summaries

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

7

| No. 1 – Moffett Towers II – Buildings 3 & 4 | |||||||

| Mortgage Loan Information | Mortgaged Property Information | ||||||

| Mortgage Loan Seller: | Barclays Capital Real Estate Inc. | Single Asset/Portfolio: | Single Asset | ||||

Credit Assessment (KBRA/Fitch/Moody’s): |

BBB/BBB-sf/NR | Property Type – Subtype: | Office – Suburban | ||||

| Original Principal Balance(1): | $49,750,000 | Location: | Sunnyvale, CA | ||||

| Cut-off Date Balance(1): | $49,750,000 | Size: | 701,266 SF | ||||

| % of Initial Pool Balance: | 5.5% | Cut-off Date Balance Per SF(1): | $499.10 | ||||

| Loan Purpose: | Refinance | Maturity Date Balance Per SF(1): | $499.10 | ||||

| Borrower Sponsor: | Jay Paul Company | Year Built/Renovated: | 2019/NAP | ||||

| Guarantor: | Paul Guarantor LLC | Title Vesting: | Fee | ||||

| Mortgage Rate: | 3.76386% | Property Manager: | Self-managed | ||||

| Note Date: | June 19, 2019 | Current Occupancy (As of): | 100.0% (8/1/2019) | ||||

| Seasoning: | 1 month | YE 2018 Occupancy(6): | NAP | ||||

| Anticipated Repayment Date(2): | July 6, 2029 | YE 2017 Occupancy(6): | NAP | ||||

| IO Period: | 120 months | YE 2016 Occupancy(6): | NAP | ||||

| Loan Term (Original): | 120 months | YE 2015 Occupancy(6): | NAP | ||||

| Amortization Term (Original): | NAP | Appraised Value(7): | $790,000,000 | ||||

| Loan Amortization Type: | Interest-only, ARD | Appraised Value Per SF(7): | $1,126.53 | ||||

| Call Protection(3): | L(24),GRTR 1% or YM(1), GRTR 1% or YM or D(88),O(7) | Appraisal Valuation Date(7): | Various | ||||

| Lockbox Type: | Hard/Upfront Cash Management | Underwriting and Financial Information | |||||

| Additional Debt(1): | Yes | TTM NOI(6): | NAP | ||||

| Additional Debt Type (Balance)(1): | Pari Passu ($300,250,000); Subordinate B-Notes ($155,000,000); Mezzanine Debt ($85,000,000) | YE 2018 NOI(6): | NAP | ||||

| YE 2017 NOI(6): | NAP | ||||||

| YE 2016 NOI(6): | NAP | ||||||

| U/W Revenues: | $57,629,637 | ||||||

| U/W Expenses: | $11,259,997 | ||||||

| Escrows and Reserves(4) | U/W NOI: | $46,369,641 | |||||

| Initial | Monthly | Cap | U/W NCF: | $46,224,616 | |||

| Taxes | $525,523 | $87,587 | NAP | U/W DSCR based on NOI/NCF(1): | 3.46x / 3.45x | ||

| Insurance | $0 | Springing | NAP | U/W Debt Yield based on NOI/NCF(1): | 13.2% / 13.2% | ||

| Replacement Reserve | $0 | Springing | NAP | U/W Debt Yield at Maturity based on NOI/NCF(1): | 13.2% / 13.2% | ||

| Free Rent Reserve | $16,127,329 | $0 | NAP | Cut-off Date LTV Ratio(1): | 44.3% | ||

| Outstanding TI/LC Reserve | $23,165,933 | $0 | NAP | LTV Ratio at Maturity or ARD(1): | 44.3% | ||

| Lease Sweep Reserve | $0 | Springing | (5) | ||||

| Sources and Uses | ||||||||||

| Sources | Uses | |||||||||

| Original whole loan amount(1) | $505,000,000 | 85.6 | % | Loan payoff(8) | $408,943,870 | 69.3 | % | |||

| Mezzanine loan | 85,000,000 | 14.4 | Upfront reserves | 39,818,785 | 6.7 | |||||

| Closing costs(9) | 26,972,612 | 4.6 | ||||||||

| Return of equity | 114,264,733 | 19.4 | ||||||||

| Total Sources | $590,000,000 | 100.0 | % | Total Uses | $590,000,000 | 100.0 | % | |||

| (1) | The Moffett Towers II – Buildings 3 & 4 Mortgage Loan (as defined below) is part of the Moffett Towers II – Buildings 3 & 4 Whole Loan (as defined below), which is evidenced by (i) eleven pari passu notes with an aggregate original balance of $350,000,000 (the “Moffett Towers II – Buildings 3 & 4 Senior Loan”) and (ii) three subordinate B-notes with an aggregate original principal balance of $155,000,000 (the “Moffett Towers II – Buildings 3 & 4 B Notes”). The Cut-off Date Balance Per SF, Maturity Date Balance Per SF, U/W NOI Debt Yield, U/W NCF Debt Yield, U/W NOI DSCR, U/W NCF DSCR, Cut-off Date LTV Ratio and LTV Ratio at Maturity or ARD numbers presented above are based on the aggregate principal balance of the promissory notes comprising the Moffett Towers II – Buildings 3 & 4 Senior Loan, without regard to the Moffett Towers II – Buildings 3 & 4 B Notes. The Cut-off Date Balance Per SF, Maturity or ARD Date Balance Per SF, U/W Debt Yield based on NOI/NCF, U/W DSCR based on NOI/NCF, Cut-off Date LTV Ratio and LTV Ratio at Maturity or ARD numbers presented above based on the combined balance of the entire Moffett Towers – Buildings 3 & 4 Whole Loan are $720, $720, 9.2%, 9.2%, 2.40x, 2.39x, 63.9% and 63.9%, respectively. |

| (2) | The Moffett Towers II – Buildings 3 & 4 Whole Loan is structured with an anticipated repayment date of July 6, 2029 (the “ARD”). If the Moffett Towers II – Buildings 3 & 4 Whole Loan is not paid off before the ARD, then the Moffett Towers II – Buildings 3 & 4 Whole Loan will accrue interest at the Adjusted Interest Rate (as defined below); however, interest accrued at the excess of the Adjusted Interest Rate over the initial interest rate will be deferred. In addition, from and after the ARD, all excess cash flow from the Moffett Towers II – Buildings 3 & 4 Property after the payment of the reserves for tax and insurance, and mortgage and mezzanine interest calculated at the initial interest rate will be applied (i) first, to repay the outstanding principal balance of the Moffett Towers II – Buildings 3 & 4 Senior Loan, in the amount required to fully amortize (based on a 30-year amortization schedule) the outstanding principal balance of the entire Moffett Towers II – Buildings 3 & 4 Whole Loan, (ii) second, if the Moffett Towers II – Buildings 3 & 4 Senior Loan has been repaid in full, to repay the outstanding principal balance of the Moffett Towers II – Buildings 3 & 4 B Notes, in the amount required to fully amortize (based on a 30-year amortization schedule) the outstanding principal balance of the Moffett Towers II – Buildings 3 & 4 B Notes, (iii) third, if lender elects, to make reserve payments for capital expenditures, (iv) fourth, to pay operating costs, (v) fifth, to repay the outstanding principal balance of the Moffett Towers II – Buildings 3 & 4 Senior Loan until the entire outstanding principal balance is paid, (vi) sixth, to repay the outstanding principal balance of the Moffett Towers II – Buildings 3 & 4 B Notes until the entire outstanding principal balance is paid, (vii) seventh, to the payment of accrued interest under the Moffett Towers II – Buildings 3 & 4 Senior Loan and |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

8

| Office - Suburban | Loan #1 | Cut-off Date Balance: | $49,750,000 | |

| 1190 Discovery Way & 900 5th Avenue | Moffett Towers II – Buildings 3 & 4 | Cut-off Date LTV: | 44.3% | |

| Sunnyvale, CA 94089 | U/W NCF DSCR: | 3.45x | ||

| U/W NOI Debt Yield: | 13.2% |

(viii) eighth, to the payment of accrued interest under the Moffett Towers II – Buildings 3 & 4 B Notes. The final maturity date of the Moffett Towers II – Buildings 3 & 4 Whole Loan is June 6, 2034. |

| (3) | Defeasance of the Moffett Towers II – Buildings 3 & 4 Whole Loan is permitted at any time after the earlier of (i) two years after the closing date that includes the last note to be securitized or (ii) June 19, 2022. The assumed defeasance lockout period of 25 payments is based on the WFCM 2019-C52 securitization trust closing date of August 2019. |

| (4) | See “Escrows” section. |

| (5) | See “Lockbox and Cash Management” section. |

| (6) | Historical occupancy and historical NOI are unavailable for the Moffett Towers II – Buildings 3 & 4 Property since it was built in 2019. |

| (7) | See “Appraisal” section. The appraised value is a prospective market value that assumes that any remaining construction costs have been paid and Facebook, the sole tenant, has taken occupancy, completed construction and commenced rental payments (expected January 1, 2020 for Building 3 and December 1, 2019 for Building 4, pursuant to its leases). The borrower reserved $23,165,933 for remaining construction costs and $16,127,329 representing 100% of the free rent. Facebook has taken possession of its space and is currently constructing its interior improvements. The as-is appraised value is $726.0 million as of May 3, 2019 and is inclusive of deductions for rent concessions and outstanding tenant improvements and leasing commissions, equating to a Cut-off Date LTV Ratio and LTV Ratio at Maturity or ARD of 48.2%. |

| (8) | In May 2018, Goldman Sachs Bank USA (“GS Bank”) funded a $795.0 million loan to an affiliate of the borrower to construct the Moffett Towers II – Buildings 3 & 4 Property. GS Bank subsequently syndicated $690.0 million of such loan to third parties, including one syndication partner who placed its $100.0 million allocation on a warehouse line with GS Bank. GS Bank retained $105.0 million of such loan on its balance sheet. The Moffett Towers II – Buildings 3 & 4 Whole Loan was used in part to pay off the existing GS Bank loan. |

| (9) | Approximately $18.4 million of closing costs are expenses associated with Level 10 Construction LP, an affiliate of the borrower. |

The Mortgage Loan. The mortgage loan (the “Moffett Towers II – Buildings 3 & 4 Mortgage Loan”) is part of a whole loan (the “Moffett Towers II – Buildings 3 & 4 Whole Loan”) evidenced by (i) eleven pari passu promissory notes with an aggregate original principal balance of $350,000,000 (the “Moffett Towers II – Buildings 3 & 4 Senior Loan”) and (ii) three B-notes with an aggregate original principal balance of $155,000,000 (the “Moffett Towers II – Buildings 3 & 4 B Notes”). The Moffett Towers II – Buildings 3 & 4 Whole Loan is secured by a first lien mortgage encumbering the borrower’s fee interest in 701,266 square feet of office buildings located in Sunnyvale, California (the “Moffett Towers II – Buildings 3 & 4 Property”). See “Description of the Mortgage Pool – The Whole Loans – The Non-Serviced AB Whole Loan” and “Pooling and Servicing Agreement – Servicing of the Non-Serviced Mortgage Loans” in the Preliminary Prospectus.

The Moffett Towers II– Buildings 3 & 4 Whole Loan requires interest-only payments through the ARD and accrues at a rate of 3.76386% per annum (the “Initial Interest Rate”) through the ARD. Following the ARD, to the extent that the loan is outstanding, the Moffett Towers II – Buildings 3 & 4 Whole Loan will accrue interest at a rate of the greater of (a) 5.26386% per annum, (b) the 10-year swap rate on the ARD plus 150 basis points or (c) the default rate as defined in the loan documents (the “Adjusted Interest Rate”). In addition, to the extent that there is excess cash flow after the payment of reserves, the excess cash flow will be applied as described in footnote 2 above.

Note Summary

| Notes | Original Principal Balance | Cut-off Date Balance | Note Holder | Controlling Interest |

| A-1-A | $2,750,000 | $2,750,000 | MFTII 2019-B3B4 | No |

| A-2-A | $1,125,000 | $1,125,000 | MFTII 2019-B3B4 | No |

| A-3-A | $1,125,000 | $1,125,000 | MFTII 2019-B3B4 | No |

| A-1-B | $65,000,000 | $65,000,000 | BBCMS 2019-C4 | (1) |

| A-1-C | $50,000,000 | $50,000,000 | BANK 2019-BNK19 | No |

| A-1-D | $49,750,000 | $49,750,000 | WFCM 2019-C52 | No |

| A-1-E | $25,000,000 | $25,000,000 | Barclays Capital Real Estate Inc. or an affiliate | No |

| A-2-B | $50,000,000 | $50,000,000 | Deutsche Bank AG, New York Branch | No |

| A-2-C | $27,625,000 | $27,625,000 | Deutsche Bank AG, New York Branch | No |

| A-3-B | $50,000,000 | $50,000,000 | Goldman Sachs Bank USA | No |

| A-3-C | $27,625,000 | $27,625,000 | Goldman Sachs Bank USA | No |

| B-1 | $85,250,000 | $85,250,000 | MFTII 2019-B3B4 | Yes(1) |

| B-2 | $34,875,000 | $34,875,000 | MFTII 2019-B3B4 | Yes(1) |

| B-3 | $34,875,000 | $34,875,000 | MFTII 2019-B3B4 | Yes(1) |

| Total | $505,000,000 | $505,000,000 |

| (1) | When a control appraisal period is no longer in effect, Note A-1-B will be the controlling note, and the directing certificateholder of the BBCMS 2019-C4 securitization trust will be entitled to exercise the related control rights. See “Description of the Mortgage Pool—The Whole Loans—The Non-Serviced AB Whole Loan” in the Preliminary Prospectus. |

The Borrower and Borrower Sponsor. The borrower is MT2 B3-4 LLC, a Delaware limited liability company and single purpose entity with two independent directors. Legal counsel to the borrower delivered a non-consolidation opinion in connection with the originationS of the Moffett Towers II – Buildings 3 & 4 Whole Loan. The non-recourse carve-out guarantor of the Moffett Towers II – Buildings 3 & 4 Whole Loan is Paul Guarantor LLC, and the borrower sponsor is The Jay Paul Company.

Founded in 1975, Jay Paul Company is a privately-held real estate firm based in San Francisco, California that concentrates on the acquisition, development, and management of commercial properties throughout California with a special focus on creating the best-

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

9

| Office - Suburban | Loan #1 | Cut-off Date Balance: | $49,750,000 | |

| 1190 Discovery Way & 900 5th Avenue | Moffett Towers II – Buildings 3 & 4 | Cut-off Date LTV: | 44.3% | |

| Sunnyvale, CA 94089 | U/W NCF DSCR: | 3.45x | ||

| U/W NOI Debt Yield: | 13.2% |

in-class projects for leading technology firms. According to the borrower sponsor, since 2000, Jay Paul Company has closed on more than $12.0 billion in debt and equity financings through a variety of large financial institutions. Jay Paul Company has developed over 13.0 million square feet of institutional quality space including projects for Apple, Google, Amazon, Facebook, Motorola, Microsoft, Boeing, Philips Electronics, Ariba, HP, Rambus, Synopsys, Nokia, DreamWorks and Tencent. Jay Paul Company is committed to green, sustainable development with over 11.0 million square feet of LEED certified office space and over 9.0 million square feet of LEED Platinum certified office space. Jay Paul Company has 25 office/R&D buildings in Moffett Park, totaling nearly 7.2 million square feet, including Moffett Place, Moffett Gateway, Technology Corners, Moffett Towers and Moffett Towers II.

The Property. The Moffett Towers II – Buildings 3 & 4 Property consists of two identical, newly-constructed eight-story buildings totaling 701,266 square feet of Class A office space that is 100.0% leased to Facebook through May 31, 2034 and is located in Sunnyvale, California. The Moffett Towers II - Buildings 3 & 4 Property is the third and final phase of the approximately 1.8 million square foot, five-building Moffett Towers II Campus and is situated on 13.4 acres of the 47.4 acre campus. In addition to approximately $80.5 million in allocated land acquisition costs, according to the borrower sponsor, the construction and development of the collateral buildings, exclusive of tenant-funded build outs, will result in approximately $506.2 million of capital improvements to the buildings, comprised of approximately $483.0 million in construction costs and approximately $23.2 million in tenant improvement allowances which were reserved at origination. The Moffett Towers II – Buildings 3 & 4 Property also features access to a 59,648 square foot non-collateral fitness/amenities building and separate parking structures with an overall parking ratio of 3.3 spaces per 1,000 square feet. With respect to the fitness/amenities space and parking structure, the borrower is subject to a declaration of covenants, conditions, restrictions and easement and charges agreement made by Moffett Towers II Association LLC, an affiliate of the borrower sponsor, and the owner of the common area non-collateral buildings at the Moffett Towers II Campus (see “Amenities and Common Areas” section). As of August 1, 2019, the Moffett Towers II – Buildings 3 & 4 Property was 100.0% leased to Facebook.

Sole Tenant.

Facebook, Inc. (701,266 square feet; 100.0% of net rentable area; 100.0% of underwritten base rent; 5/31/2034 lease expiration) –Facebook, Inc. (“Facebook”) is leasing both buildings on two separate 350,633 square-foot triple-net leases, each with two seven-year extension options and no termination options. Facebook is a global technology and media company focused on building products that enable people to connect and share with friends and family through mobile devices, personal computers and other digital platforms. Facebook’s products include Facebook, Instagram, Messenger, WhatsApp and Oculus. As of year end 2018, daily and monthly active users were 1.52 billion and 2.32 billion, respectively, representing a 9% increase year-over-year. Facebook’s 2018 revenue was $55.84 billion, up 37.4% from year end 2017. Facebook executed its leases at the Moffett Towers II – Buildings 3 & 4 Property in March 2018 and took possession of the spaces in May and June 2019. According to the borrower sponsor, Facebook is currently utilizing Level10 (Jay Paul Company’s related contracting company) to complete its build out of Building 5 (non-collateral) and is expected to move employees into that building by August 2019. Facebook is expected to begin its first phase of build out in August 2019 of Building 3 and move employees in by the end of 2019 or early 2020. The last building which Facebook will phase in will be Building 4.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

10

| Office - Suburban | Loan #1 | Cut-off Date Balance: | $49,750,000 | |

| 1190 Discovery Way & 900 5th Avenue | Moffett Towers II – Buildings 3 & 4 | Cut-off Date LTV: | 44.3% | |

| Sunnyvale, CA 94089 | U/W NCF DSCR: | 3.45x | ||

| U/W NOI Debt Yield: | 13.2% |

The following table presents certain information relating to the tenancy at the Moffett Towers II – Buildings 3 & 4 Property:

Major Tenant

| Tenant Name | Credit

Rating (Fitch/ Moody’s/ S&P) |

Tenant NRSF(1) |

%

of NRSF |

Annual U/W Rent PSF(2)(3) | Annual U/W Rent(2)(3) |

% of Total Annual U/W Rent | Lease

Expiration Date |

Extension Options | Termination Option (Y/N) |

| Major Tenant | |||||||||

| NR/NR/NR | 701,266 | 100.0% | $65.98(3) | $46,272,943(2) | 100.0% | 5/31/2034 | 2, 7-year(4) | N | |

| Vacant Space | 0 | 0.0% | |||||||

| Collateral Total | 701,266 | 100.0% | |||||||

| (1) | Tenant NRSF excludes the 23,860 square feet of shared building amenities space. |

| (2) | Annual U/W Rent PSF and Annual U/W Rent include straight-line rent for Facebook from February 2020 through Facebook’s lease term totaling $8,564,468. Facebook has executed a lease for and has taken possession of each of its spaces but has not yet commenced paying rent. Facebook is required to commence paying rent as of the related rent commencement date of each respective Facebook lease. On the origination date, the borrower reserved approximately $16.1 million for the free rent period preceding the December 2019 and January 2020 rent commencement dates for each of the two Facebook leases. |

| (3) | U/W Rent PSF and U/W Rent includes average rent for each of the two Facebook leases from February 2020 through the maturity of the Moffett Towers II – Buildings 3 & 4 Whole Loan and excludes the related amenities rent. |

| (4) | Facebook has two, seven-year renewal option at 95% of the fair market rent at the time of the renewal. |

The following table presents certain information relating to the lease rollover schedule at the Moffett Towers II – Buildings 3 & 4 Property:

Lease Expiration Schedule(1)

| Year

Ending December 31, |

No.

of Leases Expiring |

Expiring

NRSF(2) |

%

of Total NRSF |

Cumulative

Expiring NRSF(2) |

Cumulative % of Total NRSF | Annual U/W Rent(3) |

% of Total Annual U/W Rent | Annual U/W Rent PSF(3) |

| MTM | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2019 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2020 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2021 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2022 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2023 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2024 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2025 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2026 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2027 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2028 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2029 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| Thereafter | 2 | 701,266 | 100.0% | 701,266 | 100.0% | $46,272,943 | 100.0% | $65.98 |

| Vacant | 0 | 0 | 0.0% | 701,266 | 100.0% | $0 | 0.0% | $0.00 |

| Total/Weighted Average | 2 | 701,266 | 100.0% | $46,272,943 | 100.0% | $65.98 |

| (1) | Information obtained from the underwritten rent roll. |

| (2) | Expiring NRSF and Cumulative Expiring NRSF excludes 23,860 square feet of shared amenities space. |

| (3) | Annual U/W Rent PSF and Annual U/W Rent include straight-line rent for Facebook from February 2020 through Facebook’s lease term totaling $8,564,468. Facebook has executed a lease for and has taken possession of each of its spaces but has not yet commenced paying rent. Facebook is required to commence paying rent as of the related rent commencement date of each respective Facebook lease. On the origination date, the borrower reserved approximately $16.1 million for the free rent period preceding the December 2019 and January 2020 rent commencement dates for each of the two Facebook leases. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

11

| Office - Suburban | Loan #1 | Cut-off Date Balance: | $49,750,000 | |

| 1190 Discovery Way & 900 5th Avenue | Moffett Towers II – Buildings 3 & 4 | Cut-off Date LTV: | 44.3% | |

| Sunnyvale, CA 94089 | U/W NCF DSCR: | 3.45x | ||

| U/W NOI Debt Yield: | 13.2% |

The following table presents historical occupancy percentages at the Moffett Towers II – Buildings 3 & 4 Property:

Historical Occupancy

12/31/2015(1) |

12/31/2016(1) |

12/31/2017(1) |

12/31/2018(1) |

8/1/2019(2) | ||||

| NAP | NAP | NAP | NAP | 100.0% |

| (1) | Historical occupancy is not available as the Moffett Towers II – Buildings 3 & 4 Property was constructed in 2019. |

| (2) | Information obtained from the underwritten rent roll. |

Operating History and Underwritten Net Cash Flow. The following table presents certain information relating to the historical operating performance and underwritten net cash flow at the Moffett Towers II – Buildings 3 & 4 Property:

Cash Flow Analysis(1)

| U/W | %(2) | U/W $ per SF(3) | ||||

| Base Rent(4) | $37,708,475 | 63.8% | $52.00 | |||

| Amenities Rent(4) | 1,282,857 | 2.2 | 1.77 | |||

| Straight-line Office Rent(4) | 8,564,468 | 14.5 | 11.81 | |||

| Straight-line Amenities Rent(4) | 291,524 | 0.5 | 0.40 | |||

| Grossed Up Vacant Space | 0 |

0.0 |

0.00 |

|||

| Gross Potential Rent | $47,847,323 | 80.9% | $65.98 | |||

| Other Income | 0 | 0.0 | 0.00 | |||

| Total Recoveries | 11,259,997 |

19.1 |

15.53 |

|||

| Net Rental Income | $59,107,320 | 100.0% | $81.51 | |||

| (Vacancy & Credit Loss) | (1,477,683)(5) |

(3.1) |

(2.04) |

|||

| Effective Gross Income | $57,629,637 | 97.5% | $79.48 | |||

| Real Estate Taxes | 6,490,000 | 11.3 | 8.95 | |||

| Insurance | 430,152 | 0.7 | 0.59 | |||

| Management Fee | 1,152,593 | 2.0 | 1.59 | |||

| Other Operating Expenses | 3,187,252 |

5.5 |

4.40 |

|||

| Total Operating Expenses | $11,259,997 | 19.5% | $15.53 | |||

| Net Operating Income | $46,369,641 | 80.5% | $63.95 | |||

| Replacement Reserves | 145,025 | 0.3 | 0.20 | |||

| TI/LC | 0 |

0.0 |

0.00 |

|||

| Net Cash Flow | $46,224,616 | 80.2% | $63.75 | |||

| NOI DSCR(6) | 3.46x | |||||

| NCF DSCR(6) | 3.45x | |||||

| NOI Debt Yield(6) | 13.2% | |||||

| NCF Debt Yield(6) | 13.2% | |||||

| (1) | Historical financial information is not available as the Moffett Towers II – Buildings 3 & 4 Property was constructed in 2019. |

| (2) | Represents (i) percent of Net Rental Income for all revenue fields, (ii) percent of Gross Potential Rent for Vacancy & Credit Loss and (iii) percent of Effective Gross Income for all other fields. |

| (3) | Based on 725,126 square feet which is inclusive of 23,860 square feet of the non-collateral fitness/amenities building. The amenities building is a two-story structure located at the center of the Moffett Towers II Campus that contains 59,648 square feet of net rentable area. Each building is assessed a 20% portion for common use of this facility. |

| (4) | Straight-line Office Rent includes straight-line rent for Facebook from February 2020 through its lease term totaling $8,564,468. Facebook has executed a lease for and has taken possession of each of its spaces but has not yet commenced paying rent. Facebook is required to commence paying rent as of the related rent commencement date of each respective Facebook lease. Base Rent PSF and Base Rent reflect annualized amounts due in February 2020, after the dates in which Facebook is required to commence paying rent. On the origination date, the borrower reserved approximately $16.1 million for the free rent period preceding the December 2019 and January 2020 rent commencement dates for each of the two Facebook leases. Rents in place also includes approximately $1.3 million in amenities rent and $291,524 in straight-lined amenities rent. |

| (5) | The underwritten economic vacancy is 2.5%. The Moffett Towers II – Buildings 3 & 4 Property was 100.0% physically occupied as of August 1, 2019. |

| (6) | Based on the Moffett Towers II – Buildings 3 & 4 Senior Loan. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

12

| Office - Suburban | Loan #1 | Cut-off Date Balance: | $49,750,000 | |

| 1190 Discovery Way & 900 5th Avenue | Moffett Towers II – Buildings 3 & 4 | Cut-off Date LTV: | 44.3% | |

| Sunnyvale, CA 94089 | U/W NCF DSCR: | 3.45x | ||

| U/W NOI Debt Yield: | 13.2% |

Appraisal. The appraiser concluded to an appraised value for the Moffett Towers II – Buildings 3 & 4 Property of $790,000,000. The valuation date for Building 3 is January 1, 2020, and the valuation date for Building 4 is December 1, 2019. The appraised value assumes that any rent concessions and/or outstanding tenant improvements and leasing commissions are deposited into a reserve account. At loan origination, the borrower deposited $16,127,329 for free rent for Facebook and $23,165,933 for outstanding tenant improvements and leasing commissions for Facebook. As of the valuation date of May 3, 2019, the Moffett Towers II – Buildings 3 & 4 Property had an “as-is” appraised value of $726,000,000. The appraiser also concluded a “hypothetical go-dark” appraised value of $610,000,000 equating to a Cut-off Date LTV Ratio and LTV Ratio at Maturity or ARD of 57.4%.

Environmental Matters. According to the Phase I environmental site assessment dated May 13, 2019, there was no evidence of any recognized environmental conditions at the Moffett Towers II – Buildings 3 & 4 Property.

Market Overview and Competition. The Moffett Towers II – Buildings 3 & 4 Property is located in Moffett Park, in Sunnyvale, California within Silicon Valley. Moffett Park is an approximately 519-acre area comprised of recently redeveloped office spaces and research and development buildings. Notable technology firms currently in Moffett Park include Google, Hewlett Packard, Juniper Networks, Amazon, Lockheed Martin, Microsoft, Motorola, NetApp and Rambus. The Moffett Towers II – Buildings 3 & 4 Property is north of State Highway 237, which forms the southern border of the Moffett Park area and provides access from Interstate 680 and Interstate 280 to the northeast and U.S. Highway 101 in Sunnyvale to the southwest. U.S. Highway 101 runs northward through San Francisco and southward through San Jose, terminating in Los Angeles. The Santa Clara County Transit System station is located across the street from the Moffett Towers II Campus and services the surrounding residential communities. Moffett Towers II is comprised of five buildings owned by members of Moffett Towers II Association, LLC, whose current members include the Moffett Towers II – Buildings 3 & 4 Borrower and three other members, all of which are currently indirectly owned by the parent of the borrower sponsor. See “Description of the Mortgage Pool – Tenant Issues – Competition from Certain Nearby Properties.”

Submarket Information - According to the appraisal, the Moffett Towers II – Buildings 3 & 4 Property is located in the Moffett Park office submarket of Silicon Valley. As of the first quarter of 2019, the submarket contained approximately 10.3 million square feet of office inventory with a vacancy rate of approximately 0.8%. The overall NNN asking rental rate for office space in Sunnyvale, which includes the Moffett Park submarket, is $6.55 per square foot per month.

The following table presents certain information relating to the appraiser’s market rent conclusions for the Moffett Towers II – Buildings 3 & 4 Property:

Market Rent Summary(1)

| Market Rent (PSF) | $60.00 |

| Lease Term (Years) | 10 |

| Concessions | 6 mos. |

| Lease Type (Reimbursements) | NNN |

| Rent Increase Projection | 3.0% per annum |

| Tenant Improvements (New Tenants) (PSF) | $40.00 |

| Tenant Improvements (Renewals) (PSF) | $20.00 |

| (1) | Information obtained from the appraisal. |

The table below presents certain information relating to comparable sales pertaining to the Moffett Towers II – Buildings 3 & 4 Property identified by the appraiser:

Comparable Sales(1)

| Property Name | Location | Rentable Area (SF) | Sale Date | Sale Price | Sale Price (PSF) |

| 221 North Mathilda Avenue | Sunnyvale, CA | 154,987 | Mar-19 | $182,999,350 | $1,180.74 |

| 601 South California Avenue | Palo Alto, CA | 111,653 | Apr-18 | $145,099,773 | $1,299.56 |

| 1001 North Shoreline Boulevard | Mountain View, CA | 132,960 | Mar-18 | $153,999,590 | $1,158.24 |

| 10900 North Tantau Avenue | Cupertino, CA | 100,481 | Feb-17 | $78,000,386 | $776.27 |

| 410-430 North Mary Avenue | Sunnyvale, CA | 349,758 | Feb-17 | 290,701,362 | $831.15 |

| (1) | Information obtained from the appraisal. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

13

| Office - Suburban | Loan #1 | Cut-off Date Balance: | $49,750,000 | |

| 1190 Discovery Way & 900 5th Avenue | Moffett Towers II – Buildings 3 & 4 | Cut-off Date LTV: | 44.3% | |

| Sunnyvale, CA 94089 | U/W NCF DSCR: | 3.45x | ||

| U/W NOI Debt Yield: | 13.2% |

The following table presents certain information relating to comparable properties to Moffett Towers II – Buildings 3 & 4 Property:

Comparable Leases(1)

| Property Name/Location | Year Built/ Renovated | Total GLA (SF) | Distance from Subject | Occupancy | Lease Term | Tenant Size (SF) | Adjusted Annual Base Rent PSF | TI Allowance PSF | Lease Type |

Moffett Towers II 1111 Lockheed Martin Way Sunnyvale, CA |

2017/NAP | 350,663 | 1.0 miles | 100.0% | 10.5 Yrs | 350,663 | $51.60 | $65.00 | NNN |

520 Almanor Avenue 520 Almanor Avenue Sunnyvale, CA |

2019/NAP | 231,000 | 1.6 miles | 100.0% | 12.5 Yrs | 231,000 | $58.08 | $80.00 | NNN |

599 North Mathilda Avenue 599 North Mathilda Avenue Sunnyvale, CA |

2000/NAP | 76,031 | 1.6 miles | 100.0% | 5.3 Yrs | 76,031 | $50.16 | $10.00 | NNN |

Grove 221 221 North Mathilda Avenue Sunnyvale, CA |

2018/NAP | 154,987 | 2.2 miles | 100.0% | 12.0 Yrs | 154,987 | $69.60 | $83.71 | NNN |

Pathline Park Phase A Building 10 North Mary Avenue Sunnyvale, CA |

2019/NAP | 360,100 | 3.3 miles | 100.0% | 12.0 Yrs | 360,100 | $60.36 | $70.00 | NNN |

1001 North Shoreline Boulevard 1001 North Shoreline Boulevard Mountain View, CA |

2017/NAP | 132,960 | 3.9 miles | 100.0% | 12.0 Yrs | 132,960 | $67.20 | $50.00 | NNN |

| (1) | Information obtained from appraisal. |

Escrows.

Real Estate Taxes – At origination, the borrower was required to escrow $525,523 for real estate taxes. The borrower is required to make monthly payments of one-twelfth of the taxes payable during the next twelve months, currently equal to $87,587, adjusted to reflect a credit for any prepaid taxes.

Insurance – The borrower will not be required to make monthly payments of one-twelfth of the insurance premiums the lender estimates will be payable during the next twelve months as long as the borrower maintains a blanket policy acceptable to the lender.

Replacement Reserve – The borrower is required to make monthly payments of $12,085 into the replacement reserve account upon the occurrence and continuance of a Trigger Period.

Free Rent Reserve – The borrower is required to deposit $16,127,329 into a free rent reserve fund at closing to fund free rent for Facebook from August 2019 to December 2019.

Outstanding TI/LC Reserve – The borrower is required to deposit $23,165,933 into a reserve to fund outstanding tenant improvements and leasing commissions for Facebook.

Lease Sweep Reserve – Upon the occurrence of a Lease Sweep Period (as defined below), the borrower is required to escrow $1,031,600 on each monthly payment date during the continuance of such Lease Sweep Period up to the Lease Sweep and Debt Service Reserve Cap (as defined below).

Lockbox and Cash Management. The Moffett Towers II – Buildings 3 & 4 Whole Loan documents require a hard lockbox with upfront cash management. At origination, the borrower was required to deliver written instructions to tenants directing them to deposit all rents payable under such leases directly into a lender-controlled lockbox account. The Moffett Towers II – Buildings 3 & 4 Whole Loan documents require that all rents and other funds from operations received by the borrower or the property manager be deposited into the lockbox within one business day after receipt. Funds on deposit in the lockbox account are required to be swept on each business day into a lender-controlled cash management account and applied on each payment date to the payment of debt service, the funding of required reserves, budgeted monthly operating expenses, common charges under various reciprocal easement agreements, including the CCR (as defined below), approved extraordinary operating expenses, debt service on the Moffett Towers II – Buildings 3 & 4 Mezzanine Loan (as defined below) and, during a Lease Sweep Period, to the payment of an amount equal to $1,031,600 on each monthly payment date to fund a lease sweep reserve account (the “Lease Sweep Reserve Account”) until the aggregate funds swept in the Lease Sweep Reserve Account during such lease sweep equals the Lease Sweep and Debt Service Reserve Cap. Provided no Trigger Period is continuing, excess cash in the deposit account will be disbursed to the borrower in accordance with the Moffett Towers II – Buildings 3 & 4 Whole Loan documents. If a Trigger Period is continuing (other than a Trigger Period due to a Lease Sweep Period), excess cash in the deposit account will be transferred to an account (the “Cash Collateral Account”) held by the lender as additional collateral for the Moffett Towers II – Buildings 3 & 4 Whole Loan.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

14

| Office - Suburban | Loan #1 | Cut-off Date Balance: | $49,750,000 | |

| 1190 Discovery Way & 900 5th Avenue | Moffett Towers II – Buildings 3 & 4 | Cut-off Date LTV: | 44.3% | |

| Sunnyvale, CA 94089 | U/W NCF DSCR: | 3.45x | ||

| U/W NOI Debt Yield: | 13.2% |

A “Trigger Period” will commence following the occurrence of (i) July 6, 2029; (ii) an event of default under the Moffett Towers II – Buildings 3 & 4 Whole Loan or Moffett Towers II – Buildings 3 & 4 Mezzanine Loan; (ii) a Low DSCR Period (as defined below); (iv) a Lease Sweep Period; or (v) an event of default under the mezzanine loan and end at such time, if ever, as the foregoing clauses (i) to (v) giving rise to the Trigger Period have been cured in the manner set forth in the Moffett Towers II – Buildings 3 & 4 Whole Loan documents.

A “Low DSCR Period” will commence if as on any calculation date (i) the Moffett Towers II – Buildings 3 & 4 Property is not fully leased to either (a) Facebook or (b) one or more investment grade entities pursuant to a lease(s) that is substantially on the same or better terms as the Facebook lease and (ii) the debt service coverage ratio is less than 1.90x or the combined debt service coverage ratio being less than 1.50x.

A “Lease Sweep Period” means, prior to the ARD, any period (i) commencing upon the date that Facebook (or any replacement tenant) cancels, terminates or delivers notice of cancellation or termination of its lease with respect to all or a material portion of its space (at least 40,000 or more square feet of space (or, if a full floor of space is less than 40,000 square feet of space, a full floor of space)) and ending when (a) both (1) a replacement tenant acceptable to the lender has accepted delivery of the premises in question and the occupancy conditions are satisfied and (2) the debt service coverage ratio (as calculated under the Moffett Towers II – Buildings 3 & 4 Whole Loan documents) is at least equal to the debt service coverage ratio immediately prior to such period or (b) $35.00 per rentable square foot for the terminated space has been reserved, (ii) commencing upon the date that Facebook (or any replacement tenant) goes dark at 20% or more of its leased space (unless such tenant or replacement tenant is an investment grade entity) and ending when (a) a replacement tenant acceptable to the lender has accepted delivery of the premises in question and is paying rent under a qualified replacement lease or an investment grade subtenant has assumed the lease or (b) $50.00 per rentable square foot for the terminated space has been reserved, (iii) during the continuance of a default of the lease of Facebook (or any replacement tenant) beyond any applicable notice and cure period and ending when (a) such default is cured and no other default occurs for three consecutive months following such cure or (b) $35.00 per rentable square foot for the terminated space has been reserved, (iv) commencing upon the occurrence of an insolvency proceeding involving Facebook (or any replacement tenant) (an “Insolvency Trigger”) and ending when such insolvency proceedings have been terminated and the lease has been affirmed, assumed or assigned in a manner satisfactory to the lender, or (v) commencing upon the date on which Facebook becomes rated by at least two Fitch Ratings, Inc., Moody’s Investors Service, Inc., and S&P Global Ratings, acting through Standard & Poor’s Financial Services LLC) and is subsequently downgraded below investment grade and ending when (a) a replacement tenant or an investment grade subtenant has assumed the lease, (b) Facebook (or its parent entity) is restored as an investment grade entity or (c) $50.00 per rentable square foot for terminated space has been reserved.

A Lease Sweep Period (other than a Lease Sweep Period triggered by an Insolvency Trigger) will not be triggered (or, if already triggered, may be terminated) if the borrower delivers to the lender an acceptable letter of credit in an amount equal to the Lease Sweep and Debt Service Reserve Cap.

The “Lease Sweep and Debt Service Reserve Cap” means (i) with respect to a Lease Sweep Period continuing solely pursuant to clause (iii) above, $24,544,310 ($35.00 per square foot), (ii) with respect to a Lease Sweep Period continuing solely pursuant to clause (i) above, $35.00 per square foot of terminated space, (iii) with respect to a Lease Sweep Period continuing pursuant to clause (ii) above, whether or not a Lease Sweep Period pursuant to clause (i) and/or (iii) above is concurrently continuing, $50.00 per square foot of dark space or (iv) with respect to clause (v) above, whether or not a Lease Sweep Period pursuant to clause (i), (ii) and/or (iii) above, $35,063,300 ($50.00 per square foot).

The “Lease Sweep Reserve Threshold” means (i) with respect to a Lease Sweep Period continuing under clauses (iii) and/or (v) of the definition thereof, $21,037,980 or (ii) with respect to a Lease Sweep Period continuing under clauses (i) and/or (ii) of the definition thereof, $30.00 per rentable square foot of dark space and/or terminated space, as applicable.

Property Management. The Moffett Towers II – Buildings 3 & 4 Property is managed by an affiliate of the borrower.

Partial Release. Not permitted.

Real Estate Substitution. Not permitted.

Subordinate and Mezzanine Indebtedness. The Moffett Towers II – Buildings 3 & 4 B Notes, which have an aggregate principal balance of $155,000,000, are subordinate to the Moffett Towers II – Buildings 3 & 4 Senior Loan and accrue at an interest rate of 3.76386% per annum. The Moffett Towers II – Buildings 3 & 4 B Notes are coterminous with the Moffett Towers II – Buildings 3 & 4 Senior Loan. The holders of the Moffett Towers II – Buildings 3 & 4 B Notes and the Moffett Towers II – Buildings 3 & 4 Senior Loan have entered into a co-lender agreement that sets forth the allocation of collections on the Moffett Towers II – Buildings 3 & 4 Whole Loan. Based on the Moffett Towers II – Buildings 3 & 4 Whole Loan, the cumulative Cut-off Date LTV, cumulative UW NCF DSCR and cumulative UW NOI Debt Yield are 63.9%, 2.39x and 9.2%, respectively.

Additionally, a $85,000,000 mezzanine loan was funded concurrently with the origination of the Moffett Towers II – Buildings 3 & 4 Whole Loan (the “Moffett Towers II – Buildings 3 & 4 Mezzanine Loan”), which is secured by the direct equity ownership in the borrower. Following loan origination, the Moffett Towers II – Buildings 3 & 4 Mezzanine Loan was sold to a third-party investor. The Moffett Towers II – Buildings 3 & 4 Mezzanine Loan accrues interest at a rate of (i) prior to the ARD, 5.75000% per annum and (ii) from and after the ARD, the greater of (a) 7.25000% and (b) the 10-year swap rate on the ARD plus 150 basis points. The Moffett Towers II – Buildings 3 & 4 Mezzanine Loan is coterminous with the Moffett Towers II – Buildings 3 & 4 Whole Loan. Based on the Moffett Towers

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

15

| Office - Suburban | Loan #1 | Cut-off Date Balance: | $49,750,000 | |

| 1190 Discovery Way & 900 5th Avenue | Moffett Towers II – Buildings 3 & 4 | Cut-off Date LTV: | 44.3% | |

| Sunnyvale, CA 94089 | U/W NCF DSCR: | 3.45x | ||

| U/W NOI Debt Yield: | 13.2% |

II – Buildings 3 & 4 Whole Loan and Moffett Towers II – Buildings 3 & 4 Mezzanine Loan, the total Cut-off Date LTV, total UW NCF DSCR and total UW NOI Debt Yield are 74.7%, 1.90x and 7.9%, respectively. The lenders of the Moffett Towers II – Buildings 3 & 4 Whole Loan have entered into an intercreditor agreement with the Moffett Towers II – Buildings 3 & 4 Mezzanine Loan lenders, which agreement governs their relationship.

Ground Lease. None.

Amenities and Common Areas. The Moffett Towers II – Buildings 3 & 4 Property features access to the fitness/amenities building and the enclosed parking structure (the “Common Area Spaces”). To govern access to the Common Area Spaces, the borrower is subject to a declaration of covenants, conditions, restrictions and easement and charges agreement (the “CCR”) made by MT II LLC, an affiliate of the borrower sponsor and the owner of the common area non-collateral buildings at the Moffett Towers II II Campus. The CCR grants the borrower non-exclusive easement rights over the Common Area Spaces. Ownership of the Common Area Spaces governed by the CCR is held by Moffett Towers II Association LLC (the “Association”), whose membership is comprised of the borrower and the owners of buildings 1, 2 and 5. The Association is obligated to maintain insurance coverage for the Common Area Spaces and is also responsible for the maintenance of the Common Area Spaces, subject to the terms of the Facebook leases. The CCR delineates shares of the voting interest in the Association based on the number of buildings at the Moffett Towers II Campus, with each completed building entitled to a proportionate share of the voting interest. Each building is entitled to a one-fifth share (20.0%) share of the voting interest in the Association.

The borrower may consent to a subdivision of the Common Areas to a reduced common area parcel and a separate parcel owned by and on which an affiliate of the borrower may construct an office building, additional parking and other common area improvements.

Such subdivision would be subject to certain conditions, including but not limited to, lender’s consent not to be unreasonably withheld and provided that the release may not adversely affect use or access to or from the common area and the Moffett Towers II – Buildings 3 & 4 Property.

Right of First Refusal. Pursuant to its leases, Facebook has the right of first refusal to purchase Building 3 and/or Building 4 upon a proposed sale to a direct competitor (which currently includes Alphabet Inc., Amazon, Inc., Apple Inc. and Microsoft Corporation, subject to change each year and capped at four entities).

Terrorism Insurance. The Moffett Towers II – Buildings 3 & 4 Whole Loan documents require that the “all risk” insurance policy required to be maintained by the borrower provides coverage for terrorism in an amount equal to the full replacement cost of the Moffett Towers II – Buildings 3 & 4 Property, as well as business interruption insurance covering no less than the 24-month period following the occurrence of a casualty event, together with a 12-month extended period of indemnity.

Earthquake Insurance: The Moffett Towers II – Buildings 3 & 4 Property is located within seismic zone 4 and has a probable maximum loss of 3%. The borrower obtained earthquake insurance under a blanket policy with a limit of $170.0 million per occurrence.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

16

| No. 2 – University Town Center | |||||||

| Mortgage Loan Information | Mortgaged Property Information | ||||||

| Mortgage Loan Seller: | Rialto Mortgage Finance, LLC | Single Asset/Portfolio: | Single Asset | ||||

Credit Assessment

(Fitch/KBRA/Moody’s):

|

NR/NR/NR | Property Type – Subtype: | Retail – Anchored | ||||

| Original Principal Balance: | $41,580,000 | Location: | Norman, OK | ||||

| Cut-off Date Balance: | $41,580,000 | Size: | 348,877 SF | ||||

| % of Initial Pool Balance: | 4.6% | Cut-off Date Balance Per SF: | $119.18 | ||||

| Loan Purpose: | Acquisition | Maturity Date Balance Per SF: | $119.18 | ||||

| Borrower Sponsors: | J. Kenneth Dunn | Year Built/Renovated: | 2007/NAP | ||||

| Guarantors: | J. Kenneth Dunn | Title Vesting: | Fee | ||||

| Mortgage Rate: | 4.0000% | Property Manager: | Self-managed | ||||

| Note Date: | June 24, 2019 | Current Occupancy (As of): | 94.4% (5/9/2019) | ||||

| Seasoning: | 1 month | YE 2018 Occupancy: | 88.5% | ||||

| Maturity Date: | July 6, 2029 | YE 2017 Occupancy: | 88.0% | ||||

| IO Period: | 120 months | YE 2016 Occupancy: | 86.9% | ||||

| Loan Term (Original): | 120 months | YE 2015 Occupancy: | NAV | ||||

| Amortization Term (Original): | NAP | As-Is Appraised Value: | $66,000,000 | ||||

| Loan Amortization Type: | Interest-only, Balloon | As-Is Appraised Value Per SF: | $189.18 | ||||

| Call Protection: | L(25), D(91),O(4) | As-Is Appraisal Valuation Date: | May 3, 2019 | ||||

| Lockbox Type: | Springing | Underwriting and Financial Information | |||||

| Additional Debt: | None | TTM NOI (4/30/2019): | $5,108,043 | ||||

| Additional Debt Type (Balance): | NAP | YE 2018 NOI: | $5,047,012 | ||||

| YE 2017 NOI: | $4,791,393 | ||||||

| YE 2016 NOI: | $4,534,865 | ||||||

| U/W Revenues: | $6,783,922 | ||||||

| U/W Expenses: | $1,625,824 | ||||||

| Escrows and Reserves(1) | U/W NOI: | $5,158,098 | |||||

| Initial | Monthly | Cap | U/W NCF: | $4,844,107 | |||

| Taxes | $397,688 | $47,344 | NAP | U/W DSCR based on NOI/NCF: | 3.05x / 2.86x | ||

| Insurance | $0 | Springing | NAP | U/W Debt Yield based on NOI/NCF: | 12.4% / 11.7% | ||

| Replacement Reserve | $0 | $4,361 | NAP | U/W Debt Yield at Maturity based on NOI/NCF: | 12.4% / 11.7% | ||

| TI/LC Reserve | $1,500,000 | Springing | $1,500,000 | Cut-off Date LTV Ratio: | 63.0% | ||

| Deferred Maintenance | $20,250 | $0 | NAP | LTV Ratio at Maturity: | 63.0% | ||

| Sources and Uses | ||||||||

| Sources | Uses | |||||||

| Original loan amount | $41,580,000 | 59.9% | Purchase Price | $63,000,000 | 90.8% | |||

| Sponsors contribution | 27,799,091 | 40.1 | Closing Costs | 4,461,153 | 6.4 | |||

| Upfront Reserves | 1,917,938 | 2.8 | ||||||

| Total Sources | $69,379,091 | 100.0% | Total Uses | $69,379,091 | 100.0% | |||

| (1) | See “Escrows” section for a full description of Escrows and Reserves. |

The Mortgage Loan. The mortgage loan (the “University Town Center Mortgage Loan”) is evidenced by a single promissory note secured by a first mortgage encumbering the fee interest in a 348,877 square feet power center located in Norman, Oklahoma (the “University Town Center Property”).

The Borrower and Borrower Sponsor. The borrower is Rainier UTC Acquisitions, LLC (the “University Town Center Borrower”) a Delaware limited liability company and single purpose entity with two independent directors. Legal counsel to the University Town Center Borrower delivered a non-consolidation opinion in connection with the origination of the University Town Center Mortgage Loan. The nonrecourse carve-out guarantor and borrower sponsor of the University Town Center Mortgage Loan is J. Kenneth Dunn.

J. Kenneth Dunn is cofounder of The Rainier Companies (“Rainier”), which are based in Dallas, Texas. Founded in 2003, Rainier has over $2.0 billion of investment assets under management for individual, corporate and institutional investment partners. Rainier’s portfolio includes multifamily, office, retail, medical office, hotel/lifestyle, and government building assets. Co-founders Tim Nichols and J. Kenneth Dunn have been investing together since 1996, and the principals at Rainier have more than one hundred years of collective experience in real estate acquisitions, financing and operations. Rainier specializes in value-add equity investing, preferred equity and mezzanine debt investments, and third-party asset management.

The Property. The University Town Center Property is a power center containing 348,878 square feet of net rentable area located in Norman, Oklahoma. Built in phases between 2007 and 2013, the University Town Center Property consists of eight, one-story retail

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

17

| Retail - Anchored | Loan #2 | Cut-off Date Balance: | $41,580,000 | |

| 1400 24th Avenue Northwest | University Town Center | Cut-off Date LTV: | 63.0% | |

| Norman, OK 73069 | U/W NCF DSCR: | 2.86x | ||

| U/W NOI Debt Yield: | 12.4% |