UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_____________________________

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE FISCAL YEAR ENDED DECEMBER 31 , 2023

Commission file No. 1-4422

_____________________________

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||

| (Address of principal executive offices) | (Zip Code) | ||||

_____________________________

Registrant’s telephone number, including area code: (404) 888-2000

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Securities registered pursuant to section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and emerging growth company in Rule 12b-2 of the Exchange Act.

| x | Accelerated filer | o | |||||||||||||||

| Non-accelerated filer | o | Smaller reporting company | |||||||||||||||

| Emerging growth company | |||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C.7262(b)) by the registered public accounting firm that prepared or issued its audit report. Yes x No o

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. x

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The aggregate market value of Rollins, Inc. Common Stock held by non-affiliates on June 30, 2023 was $10,383,238,055 based on the reported last sale price of common stock on June 30, 2023, which is the last business day of the registrant’s most recently completed second fiscal quarter.

Rollins, Inc. had 483,885,114 shares of Common Stock outstanding as of January 31, 2024.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for the 2024 Annual Meeting of Stockholders of Rollins, Inc. are incorporated by reference into Part III, Items 10-14.

Rollins, Inc.

Form 10-K

For the Year Ended December 31, 2023

Table of Contents

| Page | |||||||||||

2

PART I

Item 1. Business

General Overview

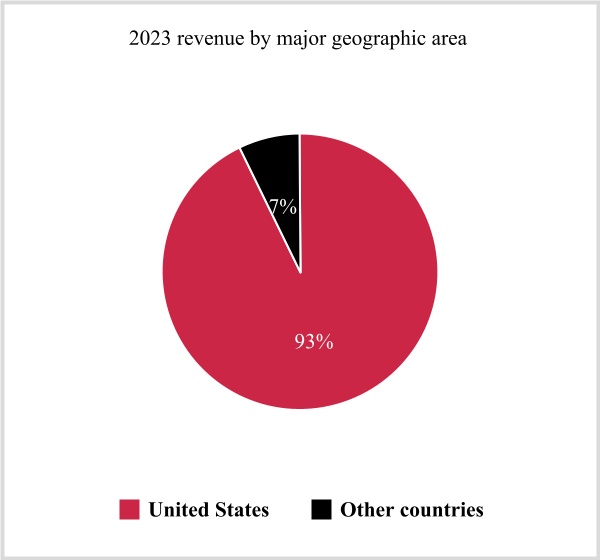

Rollins, Inc. (“Rollins,” “we,” “us,” “our,” or the “Company”), is an international services company headquartered in Atlanta, Georgia. Through our family of leading brands, we provide essential pest and wildlife control services and protection against termite damage, rodents and insects to more than two million residential and commercial customers from more than 800 Company-owned and franchised locations in approximately 70 countries. Over the course of our lengthy operating history, we have garnered a reputation for providing great customer service. The contracted and recurring nature of our services provide us with visibility into a significant portion of our future revenue.

In 1964, brothers O. Wayne and John Rollins acquired Orkin Exterminating Company and in 1965 we changed our name from Rollins Broadcasting, Inc to Rollins, Inc. In 1968, Rollins began trading on the New York Stock Exchange under the symbol “ROL.” Since then, we have grown into a premier consumer and commercial services business with numerous industry leading brands including the world renowned Orkin, as well as HomeTeam Pest Defense, Clark Pest Control, Western Pest Services, Critter Control Wildlife, Northwest Exterminating, and Fox Pest Control, among others.

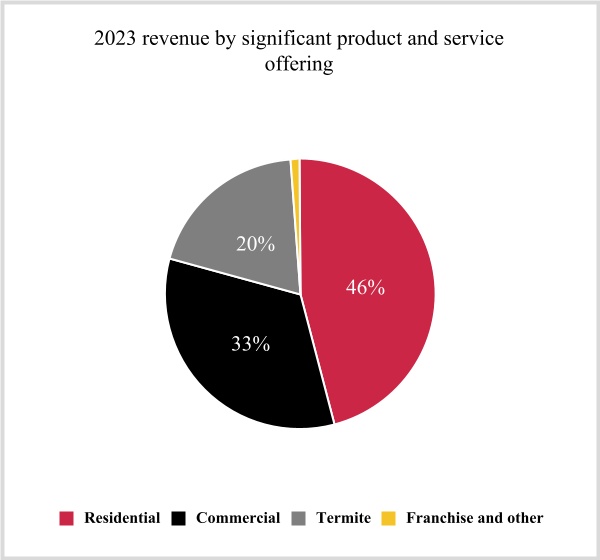

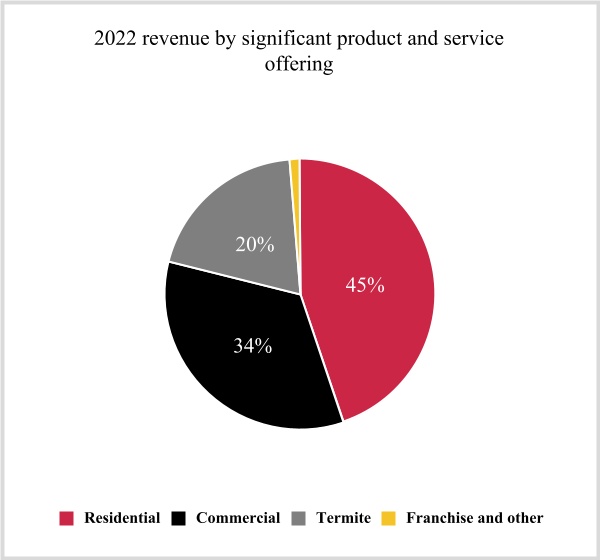

Pest control generally consists of assessing a customer's property for conditions that invite pests, tackling current infestations, and stopping the life cycle to prevent future invaders. Termite protection programs include liquid treatments, wet and dry foam applications, termite baiting and wood treatments. We operate under one reportable segment which contains our three service offerings:

•Residential: Pest control services protecting residential properties from common pests, including rodents, insects and wildlife;

•Commercial: Workplace pest control solutions for customers across diverse end markets such as healthcare, food service, logistics; and

•Termite: Termite protection services and ancillary services for both residential and commercial customers.

Risk factors associated with our business are discussed in Item 1.A. "Risk Factors."

Our Strategic Objectives

We regularly assess the business environment, as well as our own strengths and opportunities, and have aligned around key strategic objectives that will help us to drive continued success for Rollins.

People First

We promote a people first mindset that prioritizes the well-being and development of the individual, as well as our collective team, in all aspects of our business. To provide our customers with the best customer experience, we must focus on cultivating our position as the employer of choice in our industry. This means not only investing in competitive wages and benefits, but also providing tools, training and development opportunities that drive a high level of employee engagement.

Customer Loyalty

We focus on creating the best customer experience that will enable a loyal customer base and in turn reduce the amount of churn across our customer base. This starts with our people and the interactions they have with our customers. By focusing on this key objective, we expect it to enable growth that will outpace our market growth.

Growth Mindset

A growth mindset helps us consider ways to improve and best position our business. Our focus here is to identify changes that may present both risks and opportunities to our business. We focus on evaluating changes in the markets we compete

3

in but also across other industries to continue to identify changing dynamics that may impact our people and our customers that may impact our position in the markets we compete.

Operational Efficiency

As a complement to our growth mindset, our dedication to continuous improvement and operational efficiency is another key tenet of our strategy and culture. We approach our operations from the perspective that everything we do can be improved upon. We are constantly striving to improve our service levels by optimizing our business model and modernizing our business.

We believe that our alignment around the key strategic areas will enable us to grow faster than our market, position our business for the future, and deliver value for all stakeholders, including our customers, our employees, our communities and our shareholders.

Our Competitive Strengths

Rollins is a leader in the global pest control market. We have established a portfolio of premier brands with extensive service capabilities across a deep operating network with a focus on our core pest control market. Our scale enables delivery of great service and provides a significant and reinforcing competitive advantage through (i) comprehensive capabilities to win new residential and commercial accounts, (ii) technology investments for operations optimization and enhanced customer experience, (iii) route density to manage variable costs, and (iv) financial flexibility to generate organic growth and pursue M&A.

Robust Operating Platform with Proprietary Technology

Our extensive footprint creates an efficient and scalable operating platform to facilitate exceptional customer service delivery, increased cross-selling opportunities, and cost efficiencies. We have strategically invested in proprietary routing and scheduling technologies to increase our competitive advantage, which includes real-time service tracking and customer internet communication to personalize the customer experience. The majority of our business runs our proprietary Branch Operating Support System (“BOSS”), which offers a back-end interface to facilitate service tracking and payment processing for technicians. BOSS also provides virtual route management tools to increase route efficiency across our network, reducing miles driven and associated costs while increasing customer retention through on-time and rapid response service.

Differentiated Employee Base and Service Delivery

Our employees are critical to delivering an outstanding customer experience, and we are highly focused on providing our team with best-in-class training and development opportunities. We operate the 27,000 square foot Rollins Learning Center training facility located in Atlanta, GA, which is a distance-learning and global broadcast facility with simulated environments and classrooms for training. In addition to in-person training, the Rollins Learning Center offers on-demand training sessions that employees can access from anywhere in the world that are produced at our on-site, state-of-the-art broadcast studio. Our unique programs contribute to our position as an employer of choice and have earned us recognition from Training magazine among the Top 125 U.S. Training Companies 17 times in the past 21 years. We were also recognized by the Top Workplaces program as a top workplace on both a national and local level. This marks the seventh consecutive year to be recognized in Atlanta. We continuously monitor co-worker engagement and customer loyalty.

Experienced Management Team

Our management team combines extensive business and consumer services experience with robust local pest control leadership. Consistent with our culture of attracting, developing and progressing talented individuals, our senior leadership team consists of a combination of long-term internal leaders and strategic hires from well-respected external platforms.

Our Chairman, Gary Rollins, is the son of Rollins, Inc. co-founder O. Wayne Rollins and has spent his entire career with the Company, serving as Chief Executive Officer (“CEO”) from 2001 to 2022. John Wilson, having served in various roles of increasing responsibility at the Company for over 26 years, serves as Vice Chairman of the Company.

Effective January 1, 2023, Jerry Gahlhoff, Jr. assumed the role of CEO and now serves as President and CEO. Mr. Gahlhoff joined the Company as part of the HomeTeam acquisition in 2008. Mr. Gahlhoff has extensive knowledge of the

4

Company’s business and industry, having served in various roles of increasing responsibility at HomeTeam and the Company, collectively, for over 22 years. He is also a trained Entomologist.

Kenneth Krause has served as the Executive Vice President, Chief Financial Officer and Treasurer of the Company since September 2022. Mr. Krause brings over eight years of public company Chief Financial Officer experience and over 20 years of global finance and strategy experience. Elizabeth Chandler has served as the Vice President, General Counsel since she joined the Company in 2013 and as Corporate Secretary since 2018. Ms. Chandler brings over 35 years of legal experience. Pat Chrzanowski, President of Orkin US, joined the Company in 2007 and has over 21 years of pest control experience. Steve Leavitt, President of Rollins Brands, joined the Company in 1994 and has over 28 years of pest control experience. Thomas Tesh joined the Company in 2012 and served as the Vice President of Information Technology from 2012 to 2020, then as Chief Information Officer from 2020-2023. He has served as Chief Information and Administrative Officer beginning in 2023. Mr. Tesh brings over 23 years of pest control experience.

International Business

We continue to expand our international presence through organic growth, acquisitions, and our international franchise programs. In 2023, we saw revenue growth in our company-owned operations in Canada, Australia, and the United Kingdom. We believe geographic diversity allows us to increase brand recognition, meet demands of global customers, and draw on business and technical expertise from teams in several countries, and offers us an opportunity to access new markets.

Franchising Programs

We have franchise programs through Orkin, Critter Control, Missquito, and our Australian subsidiaries. We had a total of 138, 137 and 135 domestic franchise agreements as of December 31, 2023, 2022 and 2021, respectively. International franchise agreements totaled 86, 89 and 103 as of December 31, 2023, 2022 and 2021, respectively. Transactions with our franchises involve sales of territories and customer contracts to establish new franchises and the payment of initial franchise fees and royalties by franchisees. The territories, customer contracts and initial franchise fees are typically paid for by a combination of cash and notes.

Acquisition Strategy

We have extensive experience acquiring companies of all sizes. Over the last three years, we have completed approximately 90 acquisitions, including 24 acquisitions in 2023. Our acquisition strategy targets high quality, profitable businesses with strong leadership, a healthy level of brand awareness, and customer loyalty in the markets they serve that would benefit from incremental growth capital and have the potential to achieve organic growth and margin expansion.

Seasonality

Our business is affected by weather conditions, including climate change and the seasonal nature of our pest and termite control services. The increase in pest presence and activity, as well as the metamorphosis of termites in the spring and summer (the occurrence of which is determined by the timing of the change in seasons), has historically resulted in an increase in the revenue of our pest and termite control operations during such periods as evidenced by the following chart.

| Consolidated Net Revenues | |||||||||||||||||

| (in thousands) | 2023 | 2022 | 2021 | ||||||||||||||

| First Quarter | $ | 658,015 | $ | 590,680 | $ | 535,554 | |||||||||||

| Second Quarter | 820,750 | 714,049 | 638,204 | ||||||||||||||

| Third Quarter | 840,427 | 729,704 | 650,199 | ||||||||||||||

| Fourth Quarter | 754,086 | 661,390 | 600,343 | ||||||||||||||

| Year to date | $ | 3,073,278 | $ | 2,695,823 | $ | 2,424,300 | |||||||||||

Our quarterly profitability correlates with our revenue due to seasonality, as profit is lower in the first and fourth quarters and higher in the second and third quarters.

5

Materials and Supplies

Our Company has relationships with a vast network of national pest control product distributors, manufacturers and other suppliers for pest and termite treatment products. We maintain a sufficient level of products, materials, and other supplies to fulfill our immediate servicing needs and to mitigate any potential short-term shortage in availability from our national network of suppliers. We also have qualified comparable products and materials for key categories to have alternatives ready as needed. However, at any time supply chain disruptions that are more than short-term in nature could impact our levels of products, materials and other supplies. We proactively work with our supplier base and in 2023, we hosted our first ever Supplier Summit, with over 30 of our top suppliers in attendance at our corporate headquarters, to enhance collaboration and strategic relationships.

Competition

We operate in a highly competitive environment with fragmented markets and low barriers to entry. The principal factors of competition in our pest and termite control markets are quality and speed of service, customer proximity, customer satisfaction, brand awareness and reputation, terms of guarantees, safety, technical proficiency and price. Due to our strong direct partnerships with product manufacturers, distributors, and visibility into the inventories, ordering and distribution of materials and supplies, we are able to foresee potential supply disruptions and to quickly adapt. The use of an innovative and industry changing distribution model and technology enables us to maintain adequate supplies for our field operations without a significant investment in warehousing and inventory.

We believe that, through our wholly-owned subsidiaries, we compete effectively and favorably with our competitors as one of the world’s largest pest and termite control companies. Our major competitors include Rentokil, Ecolab, Anticimex, and numerous other regional companies.

Research and Development

Our expenditures on research activities relating to the development of new products or services are not significant. We utilize the relationships with our manufacturers and materials suppliers to provide new and innovative products and services, coupled with in-depth reviews by our tenured Entomology Department to ensure they meet our strict requirements. We also conduct tests of new products with the specific manufacturers of such products and we rely on research performed by leading universities.

We maintain close relationships with several universities for research and validation of treatment procedures and material selection. Some of the new and improved service methods and products are also researched, developed and produced by unaffiliated universities and companies with a portion of these methods and products being produced to the specifications provided by us.

Human Capital

We believe one of the largest contributors to our Company’s success is the quality of our people. Attracting, developing and retaining high-quality talent is the primary objective of our human capital management strategy. The development and retention of high-quality talent enables a better customer experience and improved customer retention. We develop and engage our people through our training at all levels of our organization.

As of December 31, 2023, the Company had 19,031 employees. Approximately 17,100 of our employees were located in the United States, with approximately 15,420 employees at U.S. branch offices. Of the U.S. employees, less than 2% are represented by a labor union or covered by a collective bargaining agreement.

| At December 31, | 2023 | 2022 | 2021 | ||||||||||||||

| Employees | 19,031 | 17,515 | 16,482 | ||||||||||||||

Leadership Development

Each Rollins brand cultivates its own leadership development programs that support its own values and culture while considering the best practices of all Rollins brands. Our leaders are trained on the fundamentals of people leadership, business acumen, sales excellence, and technical expertise. Having the right leaders at all levels of our organization is critical to our current and future success. This includes establishing effective succession planning to support our business

6

growth plans. While each of our brands is focused on developing operational leadership capabilities that are brand-specific, Rollins is focused on developing overall leadership capabilities through our Region Manager Development Program (RMDP). The RMDP is a comprehensive leadership development program for mid-level leaders across the organization who lead multiple business units or departments and those preparing to lead at that level. The 12-month program offers a blended learning approach that includes facilitator-led training, executive and peer mentoring, immersive field learning experiences, 360-degree assessments, a 6-month executive coaching engagement, and supported individualized development plans. Since the program was established in 2018, we have graduated a total of 85 senior leaders in five different RMDP classes with continued successes.

Workplace Inclusion

We make it a priority to promote and create a diverse, equitable and inclusive workplace that results in higher levels of satisfaction and engagement, stronger staff retention, higher productivity, and a heightened sense of belonging. Our mission is to have a culture of inclusion, where all individuals feel respected, are treated fairly, with an equitable opportunity to excel.

Our Workplace Inclusion (WPI) mission to build an inclusive workplace has continued since 2020 under the guidance of our Executive Sponsor and Inclusion Advisory Council which is made up of employees from Rollins brands across the United States. In January 2022, we hired a Director of WPI. The Director’s primary role is to implement the WPI Strategic Plan (the “Plan”) which was approved by the Executive Leadership team in April of 2022. The Plan includes 5 Strategic Focus Areas which will be implemented across all brands. The 5 Strategic Focus areas are Training & Education, Talent Acquisition & Career Development, Policies & Programs, Communication and Employee Resource Groups.

Additionally, we changed various policies, practices and programs to be more inclusive, we recognized cultural holidays and events that are celebrated by our employees throughout the year, and we launched our first Employee Resource Groups (ERGs). Our ERGs are led by Rollins employees, are inclusive to all and represent our employee population. Each ERG provides a platform for employees to connect, collaborate, and advocate for their shared interests and experiences. These groups promote inclusivity, provide networking opportunities, and contribute to a sense of belonging among employees. Thus far, we have established the following ERGs:

•R-Collective: Strives to improve company culture and employee engagement and retention through multigenerational networking.

•Women+ Resource Community: Provides a resource for women+ at any career level to achieve their goals and celebrate their accomplishments resulting in an enhanced work experience at Rollins.

•Women of Orkin Pest (WOOP): Increases communication between the women of Orkin by providing opportunities for professional development, mentoring, and networking.

•PRIDE: Provides a network that supports the professional development of LGBTQ+ employees and allies, promotes recruitment and retention, and builds community.

•P.E.A.C.E.: To build community for People who Embrace and Advocate for Cultural Equity through networking, team building, and allyship to foster a racially inclusive workplace so that all people can have thriving careers at Rollins.

We are excited about the accomplishments on our journey to create a workplace of inclusion and will continue to execute on the strategic plan.

Health and Safety

We are committed to the health and safety of our employees, customers and communities where we work, live and play. Rollins undertakes a variety of efforts to support the health and well-being of our team members, including their physical and mental health. This includes investing in competitive compensation and benefits while also providing the culture, tools, training and development opportunities to make working at Rollins an enjoyable and rewarding experience. Our employees can take advantage of a range of benefits, including healthcare and wellness programs, vacation and leave of absence benefits including paid sick/personal time off, a 401(k) match, our Employee Stock Purchase Program (ESPP), personal

7

finance education and advisory services, assistance programs to help with managing personal and work-life challenges, family support programs, and educational assistance.

In 2022, we formed a partnership with Everside Health to build an on-site medical clinic at our Rollins Support Center in Atlanta. That clinic provides no-cost primary care to Rollins team members who participate in one of our medical plans in the state of Georgia. Everside provides these services either virtually or through the existing nationwide network of Everside Health clinics for all our team members participating in one of our insurance plans in the U.S. This is an enhanced medical benefit, provided at no cost to team members.

We motivate our team members to be leaders in safety by continuously evaluating and improving our safety performance, implementing best practices and regulations, and maintaining safety excellence in everything we do. We have set measurable safety goals and are expanding our tracking mechanisms to ensure compliance. Additionally, we are constantly reviewing and refining safety policies and procedures to ensure they remain efficient and relevant. For example, throughout 2023 we made considerable progress with respect to the implementation and adoption of our driver safety application. The application monitors driving behaviors once a vehicle is in motion, detecting unsafe driving maneuvers related to acceleration, braking, distractions, and speed. We are pleased that in 2023, our average driver safety score for drivers that we monitor showed improvement. We continue our work to increase safety awareness and training, while recognizing and rewarding those that are the safest.

We have an established safety governance structure that helps our company prioritize measures to progressively reduce motor vehicle collision and injury-related risk. We have established an ongoing process that requires commitment, communication, and collaboration at all levels of the organization. Our structure is designed to ensure it remains effective and aligned with our organization’s goals and objectives.

We review and refine our health and safety policies and procedures on an ongoing basis to ensure they remain efficient and relevant for our business.

Community Involvement

We are a family of brands that has always upheld service – to our employees, customers, and communities – as a cornerstone. While each of our diverse brands has their own culture of service, we are firmly united in our commitment to engaging with our local communities.

We offer employees the opportunity to participate in various community outreach programs. We created Rollins United in 2019 to unify our brands’ philanthropic visions and consolidate our community outreach efforts. Our overarching goal is to create a significant impact in local communities over an extended period of time. The core mission of Rollins United is that everyone deserves a safe place to live, work, and play.

Since 1985, we have partnered with the United Way of Greater Atlanta through employee and company-matching funds, helping make Rollins a community leader for many years. Rollins ranked #7 in the top 25 corporate contributors in 2022 compared to ranking #9 and #11 in 2021 and 2020, respectively. Along with personal contributions from employees, the company hosts rallies, contests, and a silent auction to raise funds. Rollins has contributed approximately $1 million annually for each of the past 4 years.

We have a partnership with the Grove Park Foundation (the “Foundation”) to help serve our Atlanta community. The partnership allows our employees to volunteer and support the Foundation, which is committed to neighborhood revitalization to improve the quality of life in the Grove Park neighborhood. Representatives from our Atlanta family of brands participate in volunteer opportunities in the Grove Park neighborhood throughout the year. Additionally, many of our operations engage regularly with their local community efforts throughout the year.

Our Orkin brand demonstrates its culture of service through its OrkinServes program, which is designed to help take care of communities through employee volunteer opportunities. In 2022, OrkinServes introduced 5 new Division Advocates to serve as a voice for volunteering within their divisions across the United States and Canada. Similarly, our Northwest Exterminating brand developed the Northwest Good Deed Team ("GDT") in 2011 with the focus of being active and involved in the communities where they serve. Led by 2 full-time teammates, the GDT works with local organizations across 6 states and is supported by our team across Northwest.

8

Regulatory Considerations

Our business is subject to various local and national legislative and regulatory enactments including, but not limited to, environmental laws, antitrust laws, employment and benefit laws (including wage and hour laws, payroll taxes, anti-discrimination laws, pension laws and regulations, and ERISA), immigration laws, motor vehicle laws and regulations, human health and safety laws, securities laws including, but not limited to, SEC regulations, and federal, state and local laws and regulations governing worker safety and the pest and termite control industry. If we were to fail to comply with any of these applicable laws or regulations, we could be subject to substantial fines or damages, be involved in lawsuits, enforcement actions and other claims by third parties or governmental authorities, suffer losses to our reputation and our business or suffer the loss of licenses or penalties that may affect how the business is operated.

Consumer Protection, Privacy and Solicitation Matters

We are subject to international, federal, state, provincial and local laws and regulations designed to protect consumers generally, including laws governing lending, debt collection and consumer finance; consumer privacy and fraud; collection and use of consumer data; telemarketing; and other forms of solicitation. Specifically, rules adopted by the Federal Communications Commission and Federal Trade Commission, including the Telephone Consumer Protection Act and the Telemarketing Sales Rule, along with state laws and other legal authorities, govern our telephone and texting sales practices. The CAN-SPAM Act regulates our email solicitations, and the Consumer Review Fairness Act regulates consumer opinions on social media regarding our products and services. The California Consumer Privacy Act, including amendments under the California Privacy Rights Act, and laws in other states provide consumers and sometimes employees the right to know what personal data businesses collect, how the data is used, and give them the right to access, delete and opt out of the sale of their personal information to third parties. We are subject to some of these states’ laws depending on the number of customers or amount of revenue in the specific state. Similarly, we are bound by foreign laws and regulations governing data protection in the United Kingdom (UK General Data Protection Regulation and Data Protection Act 2018; Canada (Personal Information Protection and Electronic Documents Act); Australia (Privacy Act and its Australian Privacy Principles); and Singapore (Personal Data Protection Act and Spam Control Act), when applicable.

Environmental, Health and Safety Matters

Specifically, our businesses are subject to various international, federal, state and local laws and regulations regarding environmental, health and safety matters. Among other things, these laws regulate the emission or discharge of materials into the environment, govern the use, storage, treatment, disposal, transportation and management of hazardous substances and wastes and protect the health and safety of our employees. In addition, the use of certain pesticide products is also regulated by various federal, state, provincial and local environmental and public health agencies. These laws also impose liability for the costs of investigating and remediating, and damages resulting from, present and past releases of hazardous substances, including releases by prior owners or operators of sites we currently own or operate. Compliance with environmental, health and safety laws increases our operating costs, limits or restricts the services we provide and subjects us to the possibility of regulatory or private actions or proceedings. Penalties for noncompliance with these laws may include criminal sanctions or civil remedies, including, but not limited to, cancellation of licenses, fines, and other corrective actions. Noncompliance with, changes in, expanded enforcement of, or adoption of new laws and regulations governing hazardous waste disposal and other environmental matters, could result in operational changes and increased costs.

Franchise Matters

Certain of our subsidiaries are subject to various international, federal, state, provincial and local laws and regulations governing franchise sales, marketing and licensing and franchise trade practices generally, including applicable rules and regulations of the Federal Trade Commission. These laws and regulations generally require disclosure of business information in connection with the sale and licensing of our franchises. Certain state regulations also affect our ability as a franchisor to revoke or refuse to renew a franchise. From time to time, we and one or more franchisees have been, and may in the future become, involved in a dispute regarding the franchise relationship, including payment of royalties or fees, location of branches, advertising, purchase of products by franchisees, non-competition covenants, compliance with our standards or franchise renewal criteria.

9

Employment Laws

We are subject to a myriad of complex laws and regulations in the various federal, state, provincial, regional, and local governments in the countries in which we operate related to employees, including, but not limited to wage and hour laws, anti-discrimination laws, immigration, pension benefit plans, ERISA laws, and retirement benefits. Any failure to comply with such applicable laws or regulations could result in fines or legal proceedings.

Intellectual Property

We rely on a combination of intellectual property rights, including a patent, trademarks, copyrights, trade secrets, and contractual provisions to protect our intellectual property. Our worldwide intellectual property portfolio is strengthened through innovation and brand recognition, and a comprehensive approach for protection and enforcement.

We protect and promote our intellectual property portfolio and take those actions we deem appropriate to enforce our intellectual property rights and to defend our rights both domestically and internationally. Although in the aggregate, our global portfolio of more than 450 trademarks is a valuable asset that is important to our operations, we believe that our competitive advantage is also largely attributable to the technical, marketing, and sales competence and capabilities of our employees, rather than on any individual trademark; however, the loss of the Orkin trademark could be material to our business as a whole.

Available Information

Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to these reports, are available free of charge on our website at www.rollins.com, under the heading “SEC Filings,” as soon as reasonably practicable after those reports are electronically filed with or furnished to the Securities and Exchange Commission (“SEC”).

Cautionary Statement Regarding Forward-Looking Statements

Statements made in this Annual Report on Form 10-K contain “forward-looking statements” as defined in the Private Securities Litigation Reform Act of 1995 that involve risks and uncertainties concerning the business and financial results of Rollins, Inc. We have based these forward-looking statements largely on our current opinions, expectations, beliefs, plans, objectives, assumptions and projections about future events and financial trends affecting the operating results and financial condition of our business.

Forward-looking statements can be identified by words such as: “may,” “should,” “will,” “expect,” “believe,” “anticipate,” “intend,” “plan,” “seek,” “project,” “estimate,” “aim,” “continue,” “continually,” “could,” “likely,” “design,” “strategies,” “outlook,” “trend,” the negative of such terms and different forms thereof (e.g., different tenses or number or principle parts, as well as gerunds and other parts of speech such as adjectives, adverbs and nouns derived therefrom), and similar expressions used in this document that do not relate to historical facts. Such forward-looking statements include, but are not limited to, statements regarding: (1) our investments in proprietary routing and scheduling technologies to increase our competitive advantage; (2) our belief that we will continue to expand our international presence through organic growth, acquisitions, and our international franchise programs and our belief that such geographic diversity allow us to increase brand recognition, meet demands of global customers and draw on business and technical expertise from teams in several countries, as well as access new markets; (3) our acquisition strategy targets high quality, profitable businesses with strong leadership that would benefit from incremental growth capital and has the potential to achieve margin expansion through cost and revenue synergies: (4) our belief that we maintain a sufficient level of products, materials and other supplies to fulfill our immediate servicing needs and to alleviate any potential short-term shortage in availability from our national network of suppliers and we have qualified comparable products and materials for key categories to have alternatives ready as needed; (5) our ability to foresee and quickly adapt to potential supply disruptions because of our strong direct partnerships with product manufacturers, distributors, and visibility into the inventories, ordering and distribution of materials and supplies; (6) our ability to maintain adequate supplies for our field operations without a significant investment in warehousing and inventory because of the use of an innovative and industry changing distribution model and technology; (7) our belief that we compete effectively and favorably with our competitors as one of the world’s largest pest and termite control companies; (8) our belief that our competitive advantage is largely attributable to the technical, marketing, and sales competence and capabilities of our employees, rather than on any individual trademark and our belief that the expiration or loss of any single trademark or intellectual property right would not be material to our business as a whole; (9) our belief that one of the largest contributors to our success is the quality of our people and our belief that the

10

development and retention of high-quality talent leads to a better customer experience and better customer retention; (10) we are continuously improving our safety culture and monitoring our measurable safety goals; (11) our acquisitions may continue to be an important element of our business strategy; (12) our belief that maintaining and enhancing our brands increases our ability to enter new markets and launch new and innovative services that better serve the needs of our customers; (13) our ability to remain productive and profitable will depend substantially on our ability to compete with other pest control and service companies to attract, adequately train, and retain skilled workers and key employees (including executive officers), create leadership opportunities, and successfully implement diversity, equity and inclusion initiatives; (14) new information technology systems and technology will lead to new or improving business capabilities and streamline business processes, financial reporting, and acquisition integration; (15) an element of our business includes further expansion in international markets; (16) our plans to continue to monitor pandemics and plans to take actions that may alter our operations, including those that may be required by federal, state, or local authorities, or that we determine are in the best interests of our employees and customers; (17) the suitability and adequacy of our facilities to meet our current and reasonably anticipated future needs; (18) our belief that no pending claim, proceeding or litigation, regulatory action or investigation, either alone or in the aggregate, will have a material adverse effect on the Company’s financial position, results of operations or liquidity; (19) our belief that we establish sufficient loss contingency reserves based upon outcomes of such pending claims, proceedings or litigation that we currently believe to be probable and reasonably estimable; (20) our expectation that we will continue to pay cash dividends to the common stockholders, subject to the earnings and financial condition of the Company and other relevant factors; (21) our plans to continue to carry out various strategies previously implemented to help mitigate the impact of certain economic disruptors (such as high inflation, increases in interest rates, business interruptions due to natural disasters and changes in weather patterns, employee shortages and supply chain issues); (22) our belief that we are starting 2024 with favorable demand and a healthy balance sheet that positions us well to continue to invest in growth programs; (23) our belief that pricing efforts helped offset inflationary pressures we experienced in people associated cost; (24) our belief that our current cash and cash equivalents balances, future cash flows expected to be generated from operating activities, and available borrowings under our Credit Facility will be sufficient to finance our current operations and obligations, and fund expansion of the business for the foreseeable future; (25) our belief that we have adequate liquid assets, funding sources and insurance accruals to accommodate claims related to the retained loss program subject to assumptions and judgments as discussed under "Critical Accounting Estimates"; (26) our belief that our foreign exchange rate risk will not have a material impact upon our results of operations going forward; (27) our belief that we maintain adequate liquidity and capital resources, without regard to our foreign deposits, to finance domestic operations and obligations and to fund expansion of our domestic business; (28) our belief that the FPC Holdings, LLC acquisition will expand the Rollins family of brands and drive long term value; (29) our expectation to continue our payment of cash dividends, subject to our earnings and financial condition and other relevant factors; (30) the expected impact and amount of our contractual obligations; (31) our expectations regarding termite claims and factors that impact future costs from those claims; (32) the expected collectability of accounts receivable; (33) our belief that our tax positions are fully supportable; (34) our beliefs about our accounting policies and the impact of recent accounting pronouncements; (35) our reasonable certainty that we will exercise the renewal options on our vehicle leases; (36) expectations regarding the recognition of compensation costs related to performance-based shares as well as time-lapse restricted shares; (37) our ability to be proactive in safety and risk management to develop and maintain ongoing programs to reduce and prevent incidents and claims under our insurance programs and arrangements; (38) our potential suspension of future services for customers with past due balances; (39) any implication that our trends of seasonality will continue to hold true in the future (i.e., that profit will be lower in the first and fourth quarters and higher in the second and third quarters); (40) statements regarding our mission to have a culture of inclusion, where all individuals feel respected, are treated fairly, with an equitable opportunity to excel, and description of our plans to create and enhance inclusion in the workplace; (41) statements regarding our leadership development and successor planning; (42) our policies and procedures that are designed to identify, assess, and manage material risks arising from cybersecurity incidents; (43) our belief that the outcome of the investigations by certain local California governments regarding management of hazardous waste and pesticide disposal will not have a material adverse effect on our financials; (44) our strategic objectives described in Item 1, Part 1 (“Business”) and Item 7, Part II (“Management’s Discussion and Analysis of Financial Condition and Results of Operations”); (45) our intention to continue to grow the business in foreign markets in the future through reinvestment of foreign deposits and future earnings as well as acquisitions of unrelated companies; (46) our assertion that foreign cash earnings in excess of working capital and cash needed for strategic investments and acquisitions are not intended to be indefinitely reinvested offshore; (47) estimates, assumptions and projections related to our application of critical accounting policies, including those related to the accrued loss program and reserves related to same, goodwill, and acquisitions, described in more detail below under “Critical Accounting Estimates."

Forward-looking statements are based on information available at the time those statements are made. These statements are not guarantees of future performance and are subject to risks and uncertainties beyond our ability to control, and in many cases, we cannot predict the risks and uncertainties that could cause our actual results to differ materially from those

11

indicated by the forward-looking statements. These risks and uncertainties include, but are not limited to, those described in Item 1A "Risk Factors" of Part I, Item 7 “Management’s Discussion and Analysis of Financial condition and Results of Operations” of Part II, and elsewhere in this Annual Report on Form 10-K for our fiscal year ended December 31, 2023 and may also be described from time to time in our future reports filed with the SEC. You should not rely on our forward-looking statements. The Company does not undertake to update its forward-looking statements.

Item 1.A. Risk Factors

An investment in our common stock involves certain risks. Before making an investment decision, you should carefully consider the following risks and all of the other information included in this Annual Report on Form 10-K. Our business, reputation, financial condition, results of operations, or cash flows could be materially adversely affected by any of these risks. The trading price of our common stock could decline due to any of these risks, and you may lose all or part of your investment. This Annual Report on Form 10-K also contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those anticipated in these forward-looking statements as a result of certain factors, including the risks faced by us described below and elsewhere in this Annual Report on Form 10-K. You are cautioned that the risk factors discussed below are not exhaustive.

Risks Related to our Business, Brand, Industry and Operations

We face risks regarding our ability to compete in the pest control industry in the future.

We operate in a highly competitive industry with fragmented markets and low barriers to entry. Our revenues and earnings are affected by changes in competitors’ services, markets, and prices and general economic issues. We compete with other large pest control companies, as well as numerous smaller pest control companies, for a finite number of customers. We believe that the principal competitive factors in the market areas that we serve are quality and speed of service, customer proximity, customer satisfaction, brand awareness and reputation, terms of guarantees, technical proficiency and price. Although we believe that our customer experience and quality service are excellent, we cannot assure investors that we will be able to maintain our competitive position in the future.

We may not be able to identify, complete or successfully integrate acquisitions or guarantee that any acquisitions will achieve the anticipated financial benefits.

Acquisitions have been and may continue to be an important element of our business strategy. We cannot assure investors that we will be able to identify and acquire acceptable acquisition targets on terms favorable to us in the future, that we will receive necessary regulatory approvals, or that any acquisitions will achieve the anticipated financial benefits. Our inability to achieve the anticipated financial benefits from any acquisition transactions may not be realized due to any number of factors, including, but not limited to, unsuccessful integration efforts, unexpected or underestimated liabilities or increased costs, fees, expenses and charges related to such transactions. Such adverse events could result in a decrease in the estimated fair value of goodwill or other intangible assets established as a result of such transactions, triggering an impairment.

Our business depends on our strong brands and failing to maintain and enhance our brands and develop a positive client reputation and experience could hurt our ability to retain and expand our base of customers.

Our strong brands, such as Orkin, HomeTeam Pest Defense, Clark Pest Control, Northwest Exterminating, Fox Pest Control, Trutech, Western Pest Services, The Industrial Fumigant Company (IFC), Waltham Services, Okolona Pest Control (OPC), and Critter Control, have significantly contributed to the success of our business. Maintaining and enhancing our brands increases our ability to enter new markets and launch new and innovative services that better serve the needs of our customers. Our brands may be negatively impacted by a number of factors, including, among others, reputational issues, product/technical failures, and customer experience. We continue to develop strategies and innovative tools to gain a deeper understanding of customer acquisition and retention in order to more effectively expand and retain our customer base. Maintaining and enhancing our brands will depend largely on our brands’ ability to remain service leaders and continue to provide high-quality pest control services that are truly beneficial and play a meaningful role in people’s lives.

12

Labor shortages, our ability to attract and retain skilled workers, and increased labor costs may impair growth potential and profitability.

Our ability to remain productive and profitable will depend substantially on our ability to compete with other pest control and service companies to attract, adequately train, and retain skilled workers and key employees (including executive officers), create leadership opportunities, and successfully implement diversity, equity and inclusion initiatives. Our ability to expand our operations is in part impacted by our ability to increase our labor force. The demand for employees is high, and the supply is limited. Ongoing labor shortages could negatively affect our ability to efficiently operate at full capacity or lead to increased costs, such as increased overtime to meet demand and increased wage rates to attract and retain employees. A significant increase in the wages paid and benefits offered by competing employers could also result in a reduction in our labor force, increases in our labor costs, or both. Prolonged labor shortages, increased turnover or labor inflation could diminish our profitability and impair our growth potential.

In addition, decisions and rules by the National Labor Relations Board, including “expedited elections” and restrictions on appeals, could lead to increased organizing activities at our subsidiaries. If these labor organizing activities are successful, it could further increase labor costs, decrease operating efficiency and productivity in the future, or otherwise disrupt or negatively impact our operations which could have a material adverse effect on our reputation and business.

We may experience difficulties integrating, streamlining and optimizing our information technology (“IT”) systems and processes.

We have invested in, and expect to continue to invest in, new systems and technology to implement new or improve existing business capabilities and streamline business processes, financial reporting, and acquisition integration. Many of these efforts impact customers, suppliers, employees, and others, and any disruption or failure could adversely affect our business and operations. We may experience significant delays, increased costs, and other difficulties, which could adversely affect our ability to process work orders, send invoices, track, and collect payments, fulfill contractual obligations, or otherwise operate our business in compliance with laws. In addition, our efforts to centralize various business processes within our organization in connection with the implementations may disrupt operations. We may also experience difficulties, costs or delays in migrating acquired businesses to our systems, processes, and technologies.

Distributor or supply chain issues may result in product shortages or disruptions to our business.

We have a complex global network of distributors and suppliers that has expanded to meet increased customer demand and may, in the future, further evolve in response to market conditions. Although the majority of the products we use are generally available from multiple sources, and alternatives have been generally available in the event of disruption in the past, we could experience material disruptions in production, transportation, and other supply chain issues on specific products, which could result in out-of-stock conditions, and our results of operations and relationships with customers could be adversely affected (a) if new or existing distributors or suppliers are unable to meet any standards that we set or that are set by government or industry regulations or customers, (b) if we are unable to contract with distributors or suppliers at the quantity, quality and price levels needed for our business, or (c) if any of our key distributors or suppliers has shipping disruptions or becomes insolvent, ceases or significantly reduces its operations or experiences financial distress.

Our inability to fully or substantially meet customer demand due to distributor or supply chain issues could result in, among other things, unmet consumer demand leading to reduced preference for our products or services in the future, customers purchasing services from competitors as a result of such shortage of products, strained customer relationships, termination of customer contracts, additional competition and new entrants into the market, and loss of potential sales and revenue.

Climate change and unfavorable weather conditions could adversely impact our financial results.

Our operations are directly impacted by the weather conditions worldwide, including catastrophic events, natural disasters and potential impacts from climate change. Our business is also affected by extreme weather such as hurricanes which can impact our ability to operate as well as drought which can greatly reduce the pest population for extended periods. Climate change continues to receive increasing global attention. The possible effects of climate change could include changes in rainfall patterns, water shortages, changing storm patterns and intensities, changing temperature levels and changes in legislation, regulation, and international accords, all of which could adversely impact our costs and business operations. Our business is also affected by seasonality associated with our pest and termite control services. The increase in pest

13

presence and activity, as well as the metamorphosis of termites in the spring and summer (the occurrence of which is determined by the timing of the change in seasons), has historically resulted in an increase in the revenue and income of our pest and termite control operations during such periods.

We may not successfully execute our business strategies, including achieving our growth objectives.

We may not be able to fully implement our business strategies or realize, in whole or in part within the expected time frames, the anticipated benefits of various growth or other initiatives. Our ability to implement our business strategy may be adversely affected by factors that we cannot foresee currently, such as unanticipated costs and expenses, global health crises, technological change, recession and economic slowdown, the level of interest rates, foreign exchange risks, failure to integrate acquisitions, or a decline in the effectiveness of our marketing (including digital marketing).

In addition, we will incur certain costs to achieve efficiency improvements, systems implementations, and growth in our business, and we may not meet anticipated implementation timetables or stay within budgeted costs. As these initiatives are implemented, we may not fully achieve the desired results, including but not limited to, expected cost savings or growth rates, and these initiatives may adversely impact customer retention or our operations. Also, our business strategies may change in light of our ability to implement new business initiatives, competitive pressures, economic uncertainties or developments or other factors.

Expanding into international markets presents unique challenges, and our expansion efforts with respect to international operations may not be successful.

An element of our business includes further expansion in international markets. Our ability to successfully operate in international markets may be adversely affected by political, economic and social conditions beyond our control and geopolitical conflicts, such as the conflict between Russia and Ukraine and the conflict in Gaza. Also, we may be adversely affected by local laws and customs and legal and regulatory constraints, including compliance with applicable export, anti-corruption and currency laws and regulations of the countries or regions in which we currently operate or intend to operate in the future. Risks inherent in our existing and future international operations also include, among others, the costs and difficulties of managing international operations, difficulties in identifying and gaining access to local distributors and suppliers, suffering possible adverse tax consequences from changes in tax laws or the unfavorable resolution of tax assessments or audits, maintaining product quality and greater difficulty in enforcing intellectual property rights. Additionally, foreign currency exchange rates and fluctuations could have an adverse effect on our financial results.

Our franchisees, subcontractors, and vendors could take actions that could harm our business.

Our franchisees, subcontractors, and vendors are contractually obligated to operate their businesses in accordance with the standards set forth in our agreements with them and applicable laws and regulations. Each of our brands that are franchised also provides training and support to franchisees. However, franchisees, subcontractors, and vendors are independent third parties that we do not control, and who own, operate and oversee the daily operations of their businesses, and the ultimate success of any business operation rests with the business owner. If franchisees do not successfully operate their businesses in a manner consistent with required standards, royalty payments owed to us will be adversely affected and our brands’ image and reputation could be harmed. Similarly, if franchisees, subcontractors, and vendors do not successfully operate their businesses in a manner consistent with required laws, standards and regulations, we could be subject to claims from regulators or legal claims for the actions or omissions of such third-party franchisees, subcontractors, and vendors. In addition, our relationship with our franchisees, subcontractors, and vendors could become strained (including resulting in litigation) as we impose new standards or assert more rigorous enforcement practices of the existing required standards.

Risks Related to Cybersecurity, Privacy Compliance and Business Disruptions

The Company, our wholly-owned subsidiaries, third-party business partners and service providers have been subject to cybersecurity incidents in the past and could be the targets of future attacks that could result in disruption to our business operations, economic and reputational damage, and possible fines, penalties and private litigation, if there is unauthorized access to or unintentional distribution of personal, financial, proprietary, confidential, or other protected data or information the Company is entrusted to keep about its customers, employees, business practices, or third parties, or there are significant operational disruptions that result from a cybersecurity incident.

Our internal IT systems contain certain personal, financial, health, or other protected and confidential information that is entrusted to us by our customers and employees. Our IT systems also contain our and our wholly-owned subsidiaries’

14

proprietary and other confidential information related to our business, such as business plans, customer lists, pricing, and service development initiatives. From time to time, we have integration with new IT systems due to organic growth and acquisitions. In addition, we grant third-party business partners and service providers access to confidential information in order to facilitate business operations and administer employee benefits. Employees, third-party business partners, and service providers can knowingly or unknowingly disseminate such information or serve as an entry point for bad actors to access such information.

The Company has assigned Board responsibility for oversight of cybersecurity risk to the Audit Committee, which monitors the cybersecurity risk management and cyber control functions, including external security audits, and receives periodic updates from experienced senior management knowledgeable about assessing and managing cyber risks, including, as appropriate, updates on the prevention, detection, mitigation, and remediation of cyber incidents.

We continue to evaluate and modify our systems and protocols for data security compliance purposes, and such standards may change from time to time. We have processes in place to oversee and identify cybersecurity risks and vulnerability related to certain third-party business partners, vendors, and service providers. We have processes to address risks of a key service provider experiencing a significant cybersecurity incident that renders their services unavailable, but those processes may not cover all business losses. Activities by bad actors, changes in computer and software capabilities and encryption technology, new tools and discoveries, cloud applications, changes in multi-jurisdictional regulations, and other events or developments may result in a compromise or breach of our systems. Any compromises, breaches, application errors or human mistakes related to our systems or failures to comply with applicable standards could not only disrupt our financial operations, including our customers’ ability to pay for our services and products by credit card or their willingness to purchase our services and products, but could also result in violations of applicable laws, regulations, orders, industry standards or agreements and subject us to costs, penalties and liabilities. A breach of data security or failure to comply with rigorous multi-jurisdictional consumer privacy requirements could expose us to customer litigation, regulatory actions and costs related to the reporting and handling of such a violation or breach. Furthermore, while we maintain cybersecurity insurance, our insurance may not cover all liabilities incurred due to a security breach or incident.

Risks Related to Legal, Regulatory and Risk Management Matters

In the countries in which we operate, our business is subject to various federal, state, provincial, and local laws and regulations pertaining to environmental, public health and safety matters, including those related to the pest control industry, and any noncompliance with, changes to, or increased enforcement of such laws, could significantly impact our business.

Our business is subject to various federal, state, and local laws and regulations pertaining to environmental, public health and safety matters, including those related to the pest control industry. Among other things, these laws also govern the use, storage, treatment, disposal, transportation and management of certain pesticides and hazardous substances and waste and regulate the emission or discharge of materials into the environment. In addition, the use of certain pesticide products is also regulated by various federal, state, provincial and local environmental and public health agencies. These regulations may also apply to our third-party suppliers. Penalties for noncompliance with these laws may include criminal sanctions or civil remedies, including, but not limited to, cancellation of licenses, fines, and other corrective actions. Noncompliance with, changes in, expanded enforcement of, or adoption of new laws and regulations governing hazardous waste disposal and other environmental matters, could result in operational changes and increased costs.

We are subject to regulation in the countries in which we operate related to employment laws, and noncompliance could lead to fines or legal proceedings.

We are subject to a myriad of complex laws and regulations in the various federal, state, provincial, regional, and local governments in the countries in which we operate related to employees, including, but not limited to wage and hour laws, anti-discrimination laws, immigration, pension benefit plans, ERISA laws, and retirement benefits. Any failure to comply with such applicable laws or regulations could result in fines or legal proceedings.

New or proposed regulation regarding climate change could have uncertain impacts on our business.

Climate change has been the subject of increased focus by various governmental authorities and regulators around the world. In particular, the US is considering the enactment of legislative and regulatory proposals that would impose requirements on greenhouse gas emissions. Such laws, if enacted, are likely to impact our business in a number of ways. For example, we use gasoline and electricity in conducting our operations. Increased government regulations to limit

15

carbon dioxide and other greenhouse gas emissions may result in increased compliance costs and legislation or regulation affecting energy inputs, which could materially affect our profitability. Further the SEC has proposed rule amendments that would implement a framework for reporting of climate-related risks and create new climate-related disclosure obligations for all registrants, including us. Compliance with any new or more stringent laws or requirements, or stricter interpretations of existing laws, could require additional expenditures by us or our suppliers. We cannot predict how the proposed rules, if finalized, or any future legislation or regulations pertaining to climate change, will ultimately affect our business.

Termite claims and lawsuits related thereto could increase our legal expenses.

From time to time, we are subject to claims brought by our customers for termite protection services, generally based on alleged termite damage to the structure(s) covered by our contracts with those customers. In some instances of these claims, the customer may initiate litigation or arbitration proceedings or these matters could be brought as a class action against us or one of our brands.

Our safety and risk management programs may not have the intended effect of reducing our liability for employee-work related injuries, third party-liability claims or property loss.

Our auto or other safety management system and performance measures are critical to our reputation and results of operation. We attempt to mitigate risks relating to employee work-related injuries, automobile collision, third-party liability, or property loss through the implementation of company-wide safety management programs designed to focus on prevention and decrease the occurrence of incidents or events that may occur. We expect that any such decreases could also have the effect of stabilizing or reducing our insurance costs. However, incidents involving injury or property loss may be caused by multiple potential factors, a significant number of which are beyond our control. Therefore, there is no guarantee that our safety and risk management and safety programs will have the desired effect of avoiding or controlling all potential expenses and liability exposure.

Additionally, we retain certain risks related to general liability, workers’ compensation, and auto liability. The accruals and reserves we hold are based on estimates that involve a degree of judgment and are inherently variable and could be overestimated or insufficient. If actual claims exceed our estimates, our operating results could be materially affected, and our ability to take timely corrective actions to limit future costs may be limited.

Further, some of our commercial customers require that we meet certain safety criteria to be eligible to provide service and bid for contracts, and many contracts provide for automatic termination or forfeiture of some or all of our contract fees or profit in the event we fail to meet certain measures. Accordingly, if we fail to maintain adequate safety standards, we could experience reduced profitability or the loss of projects or clients.

Our insurance coverage may be inadequate to cover all significant risk exposures and our accruals and reserves for uninsured claims are variable.

We are exposed to liabilities that are unique to our business and the services we provide. We maintain commercial liability insurance that extends to products liability. In addition, we also maintain other insurance and other traditional risk transfer tools to respond to certain types of liabilities and risks. However, such tools are subject to terms such as deductibles, retentions, limits and policy exclusions, as well as risk of denial of coverage, default or insolvency. If we experience unexpected or uncovered losses, or if any of our insurance policies are terminated for any reason or are not effective in mitigating our risks, we may incur losses that are not covered or that exceed our coverage limits. In addition, there can be no assurance that the types or levels of coverage maintained are adequate to cover these potential significant and catastrophic risks. Further, we may not be able to continue to maintain our existing insurance coverage or obtain comparable or additional insurance coverage at a reasonable cost in the event a significant product or service claim arises.

We have been and may in the future be subject to lawsuits, investigations and other proceedings which could have a material adverse effect on our business.

In the normal course of business, we have been and may in the future be involved in various claims, contractual disputes, investigations, arbitration and litigation, including (1) claims that our acts, omissions, services or vehicles caused damage or injury, (2) claims that our services did not achieve the desired results, (3) claims related to acquisitions, (4) claims related to violations of antitrust laws or consumer protection laws, (4) claims related to allegations by federal, state or local authorities, including the Securities and Exchange Commission, the Federal Trade Commission and Department of Justice, of violations of regulations or statutes, (5) claims related to federal securities laws, (6) claims related to employment law

16

violations, (7) claims related to environmental matters, and (8) claims related to additional laws and regulations. These claims, proceedings or litigation, either alone or in the aggregate, could have a material adverse effect on our business.

Risks Related to Certain Intellectual Property Rights

Our brand recognition or reputation could be impacted if we are not able to adequately protect our intellectual property and other proprietary rights that are material to our business.

Our ability to compete effectively depends in part on our rights to service marks, trademarks, trade names and other intellectual property rights we own or license. Although we have sought to register or protect many of our marks either in the United States or in the countries in which they are or may be used, we have not sought to protect our marks in every country. Furthermore, because of the differences in foreign trademark, patent and other intellectual property or proprietary rights laws, we may not receive the same protection in other countries as we would in the United States. If we are unable to protect our proprietary information and brand names, we could suffer a material adverse effect to our reputation and business. Litigation may be necessary to enforce our intellectual property rights and protect our proprietary information, or to defend against claims by third parties that our products, services or activities infringe their intellectual property rights.

Risks Related to Public Health Crises

The effects of a pandemic or other major public health concern, could materially impact our business.

The impact of a pandemic or other major public health concerns, including changes in consumer behavior and discretionary spending, market downturns, and restrictions on business and individual activities, could create significant volatility in the global economy. Additionally, government or regulatory responses to pandemics or other public health concerns, such as mandatory lockdowns, vaccine mandates or other restrictions on operations, could negatively impact our business.

The ultimate impact of a pandemic or other major public health concern also depends on events beyond our knowledge or control, including the duration and severity of such pandemics and other major public health concerns, and related remedial or containment measures taken by parties other than us to respond to them.

We are unable to completely predict the full impact that a pandemic, or other major public health concern will have on our business due to numerous uncertainties. In addition, our compliance with remedial or containment measures could impact our day-to-day operations and could disrupt our business and operations, as well as that of our customers and suppliers, for an indefinite period of time. Furthermore, labor force availability may be impaired due to exposure, reluctance to comply with governmental, regulatory or contractual mandates, or other restrictions, which could negatively affect our operating costs and profitability or negatively impact our ability to provide quality services.

Risks Related to Market Conditions

Adverse economic conditions, including inflation and restrictions in customer discretionary expenditures, increases in interest rates or other disruptions in credit or financial markets, increases in fuel prices, raw material costs, or other operating costs could materially adversely affect our business.

Economic downturns may adversely affect our commercial customers, including food service, hospitality and food processing industries whose business levels are particularly sensitive to adverse economies. For example, we may lose commercial customers and related revenues because of consolidation or cessation of commercial businesses or because these businesses switch to a lower cost provider. Pest and termite services represent discretionary expenditures to many of our residential customers. If consumers restrict their discretionary expenditures, due to inflation or other economic hardships, we may suffer a decline in revenues from our residential service lines. Disruptions in credit or financial markets could make it more difficult for us to obtain, or increase the cost of obtaining, financing in the future. Increases in interest rates may cause a reduction in new home construction or real estate transactions, which could result in a decrease in revenue. In addition, there can be no assurances that fuel prices, raw material costs, or other operating costs, all of which may be subject to inflationary pressures, will not materially increase in future years.

17

Risks Related to our Capital and Ownership Structure

A group that includes members of the Company’s Board of Directors and management has a significant ownership interest; public stockholders may have no effective voice in the Company’s management.

The Company has a significant shareholder group, which includes the Company’s Executive Chairman of the Board, Gary W. Rollins, Board member, Pam Rollins, and certain persons acting as a group with them (the “Significant Shareholder”).