Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-05749

THE CHINA FUND, INC.

(Exact name of registrant as specified in charter)

C/O STATE STREET BANK & TRUST COMPANY

ONE LINCOLN STREET

P.O. BOX 5049

BOSTON, MA 02206-5049

(Address of principal executive offices)(Zip code)

| Copy to: | ||

| Brian F. Link Secretary The China Fund, Inc. 100 Huntington Avenue CPH-0326 Boston, MA 02116 |

Leonard B. Mackey, Jr., Esq. Clifford Chance US LLP 31 West 52nd Street New York, New York 10019-6131 | |

| (Name and Address of Agent for Service) | ||

Registrant’s telephone number, including area code: (888) 246-2255

Date of fiscal year end: October 31

Date of reporting period: October 31, 2015

Table of Contents

Item 1. Report to Stockholders.

Table of Contents

|

THE CHINA FUND, INC.

|

ANNUAL REPORT

October 31, 2015

| The China Fund, Inc. | ||||

| Table of Contents | ||||

| Page | ||||

| 1 | ||||

| 2 | ||||

| 3 | ||||

| 4 | ||||

| 5 | ||||

| 7 | ||||

| 8 | ||||

| 13 | ||||

| 17 | ||||

| 26 | ||||

| 27 | ||||

| Dividends and Distributions: Summary of Dividend Reinvestment and Cash Purchase Plan |

29 | |||

| 32 | ||||

Table of Contents

THE CHINA FUND, INC.

| FUND DATA | ||

| NYSE Stock Symbol | CHN | |

| Listing Date | July 10, 1992 | |

| Shares Outstanding | 15,682,029 | |

| Total Net Assets (10/31/15) | $312,190,641 | |

| Net Asset Value Per Share (10/31/15) | $19.91 | |

| Market Price Per Share (10/31/15) | $17.49 | |

| TOTAL RETURN(1) | ||||

| Performance as of 10/31/15: |

Net Asset Value | Market Price | ||

| 1-Year Cumulative |

-1.16% | -1.95% | ||

| 3-Year Cumulative |

30.75% | 28.79% | ||

| 3-Year Annualized |

9.35% | 8.80% | ||

| 5-Year Cumulative |

14.60% | 3.71% | ||

| 5-Year Annualized |

2.76% | 0.73% | ||

| 10-Year Cumulative |

293.22% | 227.13% | ||

| 10-Year Annualized |

14.67% | 12.58% | ||

| DIVIDEND HISTORY | ||||

| Record Date | Income | Capital Gains | ||

| 12/22/14 |

$ 0.2982 | $ 3.4669 | ||

| 12/23/13 |

$ 0.4387 | $ 2.8753 | ||

| 12/24/12 |

$ 0.3473 | $ 2.9044 | ||

| 12/23/11 |

$ 0.1742 | $ 2.8222 | ||

| 12/24/10 |

$ 0.3746 | $ 1.8996 | ||

| 12/24/09 |

$ 0.2557 | — | ||

| 12/24/08 |

$ 0.4813 | $ 5.3361 | ||

| 12/21/07 |

$ 0.2800 | $ 11.8400 | ||

| 12/21/06 |

$ 0.2996 | $ 3.7121 | ||

| 12/21/05 |

$ 0.2172 | $ 2.2947 | ||

| 12/22/04 |

$ 0.1963 | $ 3.3738 | ||

(1) Total investment returns reflect changes in net asset value or market price, as the case may be, during each period and assumes that dividends and capital gains distributions, if any, were reinvested in accordance with the dividend reinvestment plan. The net asset value returns are not an indication of the performance of a stockholder’s investment in the Fund, which is based on market price. Total investment returns do not reflect the deduction of taxes that a stockholder would pay on Fund distributions or the sale of Fund shares. Total investment returns are historical and do not guarantee future results. Market price returns do not reflect broker commissions in connection with the purchase or sale of Fund shares.

1

Table of Contents

THE CHINA FUND, INC.

ASSET ALLOCATION AS OF October 31, 2015 (Unaudited)

| Ten Largest Listed Equity Investments * | ||

| Ping An Insurance (Group) Company of China, Ltd. |

6.5% | |

| TaiwanSemiconductor Manufacturing Co., Ltd. |

5.5% | |

| Industrial& Commercial Bank of China, Ltd. |

5.3% | |

| TencentHoldings, Ltd. |

4.6% | |

| HongKong Exchanges and Clearing, Ltd. |

4.2% | |

| ChinaMobile, Ltd. |

4.0% | |

| ChinaEverbright International, Ltd. |

3.2% | |

| ChinaMerchants Bank Co., Ltd. |

3.2% | |

| DigitalChina Holdings, Ltd. |

3.1% | |

| DeltaElectronics, Inc. |

3.0% | |

| * | Percentages based on net assets at October 31, 2015 |

2

Table of Contents

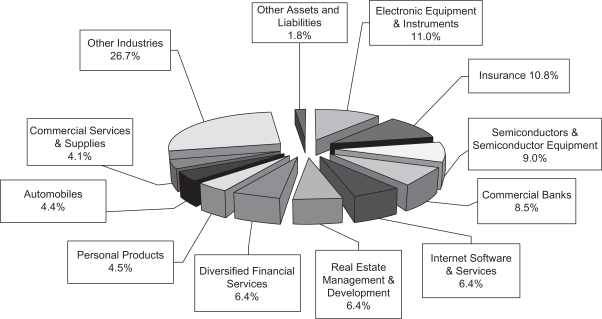

INDUSTRY ALLOCATION (Unaudited)

Industry Allocation (as a percentage of net assets)

Fund holdings are subject to change and percentages shown above are based on net assets at October 31, 2015. A complete list of holdings at October 31, 2015 is contained in the Schedule of Investments included in this report. The most current available data regarding portfolio holdings can be found on our website, www.chinafundinc.com. You may also obtain holdings by calling 1-888-246-2255.

3

Table of Contents

THE CHINA FUND, INC.

CHAIRMAN’S STATEMENT (Unaudited)

Dear Stockholders,

2015 has proven to be a mixed year for Chinese equity investors. The A share market went on something of a roller coaster ride over the last 12 months as market participants reacted to various events that shaped their expectations. This volatility is evidenced by significant fluctuations in the direction of returns of both the market and the Fund over various periods during the year.

In the one-year period ending October 31, 2015, the Fund did better than the broader market but still finished in slightly negative territory, returning -1.16%. Over the three years ended October 31, 2015, our Fund managed a healthy 9.35% average annual return.

The depreciation of the Renmimbi (“RMB”) in August was not a surprise to our investment manager who saw it as a logical move towards a more fair valuation of a currency that had been on a multi-year appreciation trajectory. However, investors who interpreted this as a competitive devaluation clearly introduced volatility to the market. Government intervention measures to shore up the equity market also caused concern among investors.

We believe that China’s continued efforts to transition to a more service-led economy, specifically the move from low cost manufacturing to higher value added industries like finance, bode well for our long term investment prospects. This structural change clearly will result in winners and losers, and companies that stand to benefit from this shift should be expected to outperform for our Fund.

Against the backdrop of an optimistic long term view, we do expect continued volatility in the market as certain events unfold. One closely followed event is the International Monetary Fund’s decision to include the RMB in the Special Drawing Rights bucket. The resulting buying of the RMB by governments worldwide will be supportive of the currency. Investors also are watching how various initiatives to open up China’s financial markets and internationalize the currency develop.

As in most cases, change represents both risk and opportunity. While the ride may be bumpy, we think that our investment manager has clearly mapped out a plan to navigate the portfolio through the volatility and take advantage of our long term investment horizon to capitalize on the opportunities that this environment presents. The investment manager’s comments in this report contain more details on some of the current positioning and strategy.

The entire Board joins me in thanking you for your support.

Sincerely,

Joe O. Rogers

Chairman

4

Table of Contents

THE CHINA FUND, INC.

INVESTMENT MANAGER’S STATEMENT (Unaudited)

Market Review

It has been a volatile twelve months for the Greater China equity markets. The first six months saw a massive liquidity driven rally in the Chinese A-share market where the Shanghai Composite Index more than doubled, reaching a high of 5,166.35. The rally was fueled on expectations of monetary easing and supportive measures by the Chinese Government to manage the economic slowdown. At the same time, various policy announcements, such as the Local Government Financing Vehicle replacement program and the deposit insurance scheme, were regarded as significant breakthroughs on the fiscal reforms front and that further spurred investors to buy into the rally. The share prices of brokers, banks and exchanges did particularly well during this period.

The rally in China came to an abrupt halt in the middle of 2015, as the Chinese Government took measures to cool down the market on worries of the formation of a bubble. This led to a sharp correction in share prices in the domestic A-share market and the offshore markets as Chinese retail investors started selling their holdings indiscriminately. Since the correction in June, global investors have been fretting over an implosion in China as the release of poor economic data continued. China is clearly one of the biggest worries for global investors at the moment and the persistent investor unease over a hard landing has spread.

The Taiwan stock market reversed its previous technology-driven rally and saw the weakest returns over the past year among Greater China equity markets. After the launch of iPhone 6, many investors have been concerned about the maturing smartphone cycle globally, leading to poor performance of many companies along the smartphone supply chain. On the macro side, economic growth remained lackluster as the economy struggles to find the next growth driver.

To round out the twelve months, Chinese and global equity markets rebounded strongly from the recent lows, ending on a positive note.

Performance

The Fund outperformed the MSCI Golden Dragon Index (the “Benchmark”) for the year ended October 31, 2015. During this period the Fund returned -1.16% compared with -2.99% for the Benchmark.

A major part of the outperformance can be attributable to our position in Chinese companies, including high conviction names in the Chinese railway sector, life insurance space and specific China A-shares. For example, one of the top contributors for the year has been CRRC Corp., Ltd., the largest railway company in China after the merger between China CNR and China CSR. We have owned China CNR for around a year on the anticipation of rising railway infrastructure spending in China and our position played out very well in late 2014. When the share price rallied, we took advantage of the rally and trimmed the position. Another key contributor has been Ping An Insurance (Group) Company of China, Ltd., the second largest insurance provider in China. We like the company given its strong agency salesforce, high agency productivity and cross-selling opportunities with its own banking segment. The company is one of our key positions in the Chinese insurance space, benefiting from the rising penetration of life insurance in China.

5

Table of Contents

THE CHINA FUND, INC.

INVESTMENT MANAGER’S STATEMENT (continued) (Unaudited)

Conversely, Li & Fung Ltd., a global sourcing company for many US and European firms, was the top detractor during the past year. We invested in this company after a period of share price weakness, and expected that stabilization of its business should contribute to a re-rating of the stock. We were right in terms of the investment thesis but timing-wise we were early. After its sluggish performance over the past year, we are seeing more investors revisiting this name and believe that the stock should be able to re-rate from the current level. Another area of weakness was a small cap Chinese high-end steel manufacturer, Tiangong International Co., Ltd. The company is a leader in China producing high speed steel and die steel, which are often used in the automotive, machinery manufacturing and aviation industries. We expected the company to benefit from an industrial upgrade in China. However, the weak macro environment and declining industrial production growth in China has weighed negatively on this stock.

Outlook

After the Chinese equity market rebounded in October, many people have questioned the sustainability of this recovery. The overhang is whether the extremely high volatility this summer will be repeated and we could return to a market crash. We believe this is quite unlikely. Some of the reasons for the previous wave of market volatility, such as the surge in margin finance in the China A-share market, have now eased and the pressure of forced selling is largely behind us.

The key question now is whether economic conditions will continue to worsen after three quarters of weak economic readings. Yes, the economy is weak, but everything has a price. If we look at the current valuation of Hong Kong listed Chinese stocks, many of the stocks are trading close to financial crisis levels. This means that if the economic data starts to show some signs of stabilization, and therefore beats many expectations, continued recovery in the equity market is likely. On top of this, supporting government policies should help relieve the debt burden of many highly leveraged companies and ease the pain of an economic slowdown.

Under the current economic cycle, stock selection is particularly important for investors, as many parts of the economy such as energy, steel, and asset heavy manufacturers, will suffer from the weakening macro environment. We are investing in companies that can still produce sustainable growth. We like companies within the technology, environmental protection and industrial automation areas, which look to be boosted by policy support over multiple years under the 13th Five Year Plan.

6

Table of Contents

THE CHINA FUND, INC.

ABOUT THE PORTFOLIO MANAGER (Unaudited)

The Fund’s investment manager is Allianz Global Investors U.S. LLC, an Allianz Global Investors company.

Allianz Global Investors (“AGI”) is a diversified active investment manager with a strong parent company and a culture of risk management. With 24 offices in 18 countries, AGI provides global investment and research capabilities with consultative local delivery. It has $477 billion1 in assets under management for individuals, families and institutions worldwide, and employs over 500 investment professionals.

Ms. Christina Chung serves as the portfolio manager for the Fund’s portfolio of listed and direct securities. She joined the group in 1998 and has been a managing director since January 2010. She heads the Greater China Team and is the lead manager of the Hong Kong, China, China A-shares and Greater China equity mandates. The Hong Kong and China Funds that she manages have won industry recognition and awards for consistent, strong performance. She has 26 years’ experience in managing Asian regional and single country portfolios for both institutional and retail accounts.

Before joining the group, she was a senior portfolio manager with Royal Bank of Canada Investment Management. Prior to that, she was a portfolio manager with Search International and an economist with HSBC Asset Management. Christina was educated in Canada. She attained a Bachelor of Administration from Brock University, followed by an M.A. in Economics from the University of Alberta. She became a Certified Management Accountant in 1992 and qualified as a chartered financial analyst, AIMR, in 1995.

| 1 | Combined worldwide AUM as of September 30, 2015 |

7

Table of Contents

THE CHINA FUND, INC.

October 31, 2015

| Name of Issuer and Title of Issue |

Shares |

Value (Note A) |

||||||||

| COMMON STOCK AND OTHER EQUITY INTERESTS |

||||||||||

| HONG KONG |

||||||||||

| Biotechnology — (1.1%) |

||||||||||

| 3SBio Inc. 144A* |

3,175,500 | $ | 3,568,806 | |||||||

|

|

|

|||||||||

| Commercial Services & Supplies — (4.1%) |

||||||||||

| China Everbright International, Ltd.(1) |

6,140,000 | 9,934,788 | ||||||||

| Goldpac Group Ltd.#(1) |

5,521,000 | 2,863,759 | ||||||||

|

|

|

|||||||||

| 12,798,547 | ||||||||||

|

|

|

|||||||||

| Construction & Engineering — (1.0%) |

||||||||||

| China State Construction International Holdings, Ltd.(1) |

2,110,000 | 3,212,604 | ||||||||

|

|

|

|||||||||

| Diversified Financial Services — (4.2%) |

||||||||||

| Hong Kong Exchanges and Clearing, Ltd.(1) |

495,300 | 12,986,279 | ||||||||

|

|

|

|||||||||

| Electronic Equipment & Instruments — (4.6%) |

||||||||||

| Digital China Holdings, Ltd.†(1) |

9,391,000 | 9,596,872 | ||||||||

| Zhuzhou CSR Times Electric Co., Ltd. |

732,000 | 4,783,913 | ||||||||

|

|

|

|||||||||

| 14,380,785 | ||||||||||

|

|

|

|||||||||

| Food Products — (3.0%) |

||||||||||

| Want Want China Holdings Ltd.(1) |

11,207,000 | 9,341,456 | ||||||||

|

|

|

|||||||||

| Hotels, Restaurants & Leisure — (1.0%) |

||||||||||

| Sands China Ltd. |

868,000 | 3,152,759 | ||||||||

|

|

|

|||||||||

| Industrial Conglomerates — (3.6%) |

||||||||||

| Beijing Enterprises Holdings, Ltd. |

1,327,000 | 8,381,395 | ||||||||

| CK Hutchison Holdings, Ltd. |

216,500 | 2,986,265 | ||||||||

|

|

|

|||||||||

| 11,367,660 | ||||||||||

|

|

|

|||||||||

| Insurance — (1.9%) |

||||||||||

| China Life Insurance Co., Ltd. |

1,612,000 | 5,834,325 | ||||||||

|

|

|

|||||||||

| Internet Software & Services — (6.4%) |

||||||||||

| Alibaba Group Holding Ltd. ADR* |

33,166 | 2,780,306 | ||||||||

| Baidu Inc. ADR* |

15,821 | 2,965,963 | ||||||||

| Tencent Holdings, Ltd. |

757,500 | 14,289,686 | ||||||||

|

|

|

|||||||||

| 20,035,955 | ||||||||||

|

|

|

|||||||||

See notes to financial statements.

8

Table of Contents

THE CHINA FUND, INC.

SCHEDULE OF INVESTMENTS (continued)

October 31, 2015

| Name of Issuer and Title of Issue |

Shares |

Value (Note A) |

||||||||||

| COMMON STOCK AND OTHER EQUITY INTERESTS (continued) |

||||||||||||

| HONG KONG (continued) |

||||||||||||

| Metals & Mining — (0.5%) |

||||||||||||

| Tiangong International Co., Ltd.(1) |

15,318,000 | $ | 1,423,073 | |||||||||

|

|

|

|||||||||||

| Personal Products — (3.3%) |

||||||||||||

| Hengan International Group Co., Ltd. |

425,500 | 4,592,595 | ||||||||||

| Natural Beauty Bio-Technology, Ltd.# |

50,320,000 | 5,583,825 | ||||||||||

|

|

|

|||||||||||

| 10,176,420 | ||||||||||||

|

|

|

|||||||||||

| Pharmaceuticals — (1.7%) |

||||||||||||

| CSPC Pharmaceutical Group Ltd.(1) |

5,804,000 | 5,407,012 | ||||||||||

|

|

|

|||||||||||

| Real Estate Management & Development — (6.4%) |

||||||||||||

| China Overseas Land & Investment Ltd. |

2,134,000 | 6,938,853 | ||||||||||

| China Overseas Property Holdings Ltd.(1)* |

711,332 | 121,154 | ||||||||||

| Hongkong Land Holdings, Ltd. |

497,000 | 3,732,470 | ||||||||||

| Sun Hung Kai Properties, Ltd.†(1) |

688,000 | 9,232,397 | ||||||||||

|

|

|

|||||||||||

| 20,024,874 | ||||||||||||

|

|

|

|||||||||||

| Semiconductors & Semiconductor Equipment — (1.9%) |

||||||||||||

| ASM Pacific Technology, Ltd.(1) |

295,700 | 2,109,935 | ||||||||||

| Semiconductor Manufacturing International Corp.(1)* |

40,687,000 | 3,779,905 | ||||||||||

|

|

|

|||||||||||

| 5,889,840 | ||||||||||||

|

|

|

|||||||||||

| Specialty Retail — (0.2%) |

||||||||||||

| Zhongsheng Group Holdings, Ltd.(1) |

1,844,500 | 766,350 | ||||||||||

|

|

|

|||||||||||

| Textiles, Apparel & Luxury Goods — (2.6%) |

||||||||||||

| Li & Fung, Ltd.(1) |

9,798,000 | 7,977,365 | ||||||||||

|

|

|

|||||||||||

| Wireless Telecommunication Services — (4.0%) |

||||||||||||

| China Mobile, Ltd. |

1,055,500 | 12,631,789 | ||||||||||

|

|

|

|||||||||||

| TOTAL HONG KONG — (Cost $171,856,712) |

51.5 | % | 160,975,899 | |||||||||

|

|

|

|

|

|||||||||

| HONG KONG — “H” SHARES |

||||||||||||

| Automobiles — (3.0%) |

||||||||||||

| Qingling Motors Co., Ltd.†#(1) |

28,960,000 | 9,341,815 | ||||||||||

|

|

|

|||||||||||

See notes to financial statements.

9

Table of Contents

THE CHINA FUND, INC.

SCHEDULE OF INVESTMENTS (continued)

October 31, 2015

| Name of Issuer and Title of Issue |

Shares |

Value (Note A) | ||||||||||

| COMMON STOCK AND OTHER EQUITY INTERESTS (continued) |

||||||||||||

| HONG KONG — “H” SHARES (continued) |

||||||||||||

| Commercial Banks — (8.5%) |

||||||||||||

| China Merchants Bank Co., Ltd. |

3,743,000 | $ | 9,828,267 | |||||||||

| Industrial & Commercial Bank of China, Ltd. |

25,873,000 | 16,525,122 | ||||||||||

|

|

|

|||||||||||

| 26,353,389 | ||||||||||||

|

|

|

|||||||||||

| Insurance — (6.5%) |

||||||||||||

| Ping An Insurance (Group) Company of China, Ltd.(1) |

3,594,000 | 20,265,261 | ||||||||||

|

|

|

|||||||||||

| Machinery — (1.5%) |

||||||||||||

| CRRC Corp., Ltd. (1)* |

3,697,000 | 4,741,640 | ||||||||||

|

|

|

|||||||||||

| Transportation Infrastructure — (1.0%) |

||||||||||||

| Qingdao Port International Co., Ltd. 144A#(1) |

6,596,000 | 3,183,061 | ||||||||||

|

|

|

|||||||||||

| TOTAL HONG KONG — “H” SHARES — |

20.5 | % | 63,885,166 | |||||||||

|

|

|

|

|

|||||||||

| TOTAL HONG KONG (INCLUDING “H” SHARES) — |

72.0 | % | 224,861,065 | |||||||||

|

|

|

|

|

|||||||||

| TAIWAN |

||||||||||||

| Computers & Peripherals — (2.8%) |

||||||||||||

| Advantech Co., Ltd. |

1,203,841 | 8,658,859 | ||||||||||

|

|

|

|||||||||||

| Diversified Financial Services — (2.2%) |

||||||||||||

| Fubon Financial Holdings Co., Ltd. |

4,270,000 | 6,931,754 | ||||||||||

|

|

|

|||||||||||

| Electronic Equipment & Instruments — (5.2%) |

||||||||||||

| Delta Electronics, Inc. |

1,835,000 | 9,383,153 | ||||||||||

| Largan Precision Co., Ltd. |

88,000 | 6,871,718 | ||||||||||

|

|

|

|||||||||||

| 16,254,871 | ||||||||||||

|

|

|

|||||||||||

| Insurance — (2.4%) |

||||||||||||

| Cathay Financial Holding Co., Ltd. |

5,305,000 | 7,582,423 | ||||||||||

|

|

|

|||||||||||

| Leisure Equipment & Products — (1.5%) |

||||||||||||

| Merida Industry Co., Ltd.(1) |

805,000 | 4,723,844 | ||||||||||

|

|

|

|||||||||||

| Semiconductors & Semiconductor Equipment — (7.1%) |

||||||||||||

| Hermes Microvision, Inc.(1) |

124,000 | 4,793,691 | ||||||||||

|

|

|

|||||||||||

See notes to financial statements.

10

Table of Contents

THE CHINA FUND, INC.

SCHEDULE OF INVESTMENTS (continued)

October 31, 2015

| Name of Issuer and Title of Issue |

Shares |

Value (Note A) | ||||||||||

| COMMON STOCK AND OTHER EQUITY INTERESTS (continued) |

||||||||||||

| TAIWAN (continued) |

||||||||||||

| Semiconductors & Semiconductor Equipment (continued) |

||||||||||||

| Taiwan Semiconductor Manufacturing Co., Ltd. |

4,109,000 | $ | 17,277,204 | |||||||||

|

|

|

|||||||||||

| 22,070,895 | ||||||||||||

|

|

|

|||||||||||

| TOTAL TAIWAN — (Cost $55,005,407) |

21.2 | % | 66,222,646 | |||||||||

|

|

|

|

|

|||||||||

| TOTAL COMMON STOCK AND OTHER EQUITY INTERESTS — (Cost $287,646,268) |

93.2 | % | 291,083,711 | |||||||||

|

|

|

|

|

|||||||||

| EQUITY-LINKED SECURITIES |

||||||||||||

| Automobiles — (1.4%) |

||||||||||||

| Chongqing Changan Automobile Co., Ltd. Access Product (expiration 01/15/16)(2)144A |

558,897 | 1,358,120 | ||||||||||

| Chongqing Changan Automobile Co., Ltd. Access Product (expiration 02/10/25)(3)144A |

487,000 | 1,186,332 | ||||||||||

| Chongqing Changan Automobile Co., Ltd. Access Product (expiration 04/23/20)(4)144A |

739,970 | 1,793,687 | ||||||||||

|

|

|

|||||||||||

| 4,338,139 | ||||||||||||

|

|

|

|||||||||||

| Electronic Equipment & Instruments — (1.2%) |

||||||||||||

| XJ Electric Co., Ltd. Access Product (expiration 02/12/16)(2)144A |

419,748 | 1,276,034 | ||||||||||

| XJ Electric Co., Ltd. Access Product (expiration 07/03/24)(3)144A |

864,000 | 2,632,608 | ||||||||||

|

|

|

|||||||||||

| 3,908,642 | ||||||||||||

|

|

|

|||||||||||

| Hotels, Restaurants & Leisure — (1.2%) |

||||||||||||

| China CYTS Tours Holding Co., Ltd. Access Product (expiration 02/12/16)(2)144A |

1,143,908 | 3,603,310 | ||||||||||

|

|

|

|||||||||||

| Personal Products — (1.2%) |

||||||||||||

| Shanghai Jahwa United Co., Ltd. Access Product (expiration 01/15/16)(2)144A |

371,242 | 2,012,132 | ||||||||||

| Shanghai Jahwa United Co., Ltd. Access Product (expiration 04/06/20)(4)144A |

315,651 | 1,713,038 | ||||||||||

|

|

|

|||||||||||

| 3,725,170 | ||||||||||||

|

|

|

|||||||||||

| TOTAL EQUITY-LINKED SECURITIES — |

5.0 | % | 15,575,261 | |||||||||

|

|

|

|

|

|||||||||

| COLLATERAL FOR SECURITIES ON LOAN — (6.8%) |

||||||||||||

| State Street Navigator Securities Lending Prime Portfolio |

21,195,809 | 21,195,809 | ||||||||||

|

|

|

|||||||||||

See notes to financial statements.

11

Table of Contents

THE CHINA FUND, INC.

SCHEDULE OF INVESTMENTS (continued)

October 31, 2015

| Name of Issuer and Title of Issue |

Face Amount |

Value (Note A) | ||||||||||

| SHORT TERM INVESTMENT — (0.9%) |

||||||||||||

| Repurchase Agreement with State Street Bank and Trust, dated 10/30/15, 0.00%, due 11/02/15, proceeds $2,810,000; collateralized by U.S. Treasury Note, 3.13%, due 05/15/21, valued at $2,866,826, including interest. (Cost $2,810,000) |

$ | 2,810,000 | $ | 2,810,000 | ||||||||

|

|

|

|||||||||||

| TOTAL INVESTMENTS — (Cost $333,302,161) |

105.9 | % | 330,664,781 | |||||||||

|

|

|

|

|

|||||||||

| OTHER ASSETS AND LIABILITIES |

(5.9 | )% | (18,474,140 | ) | ||||||||

|

|

|

|

|

|||||||||

| NET ASSETS |

100.0 | % | $ | 312,190,641 | ||||||||

|

|

|

|

|

|||||||||

Notes to Schedule of Investments

| * | Denotes non-income producing security. |

| † | Affiliated issuer (see Note F). |

| # | Illiquid security. At October 31, 2015, these securities amounted to $20,972,460, which represented 6.7% of total net assets. |

| (1) | Security (or a portion of the security) is on loan. As of October 31, 2015, the market value of securities loaned was $39,669,593. The loaned securities were secured with cash collateral of $21,195,809 and non-cash collateral with a value of $20,948,025. The non-cash collateral received consists of equity securities, and is held for the benefit of the Fund at the Fund’s custodian. The Fund cannot repledge or resell this collateral. Collateral is calculated based on prior day’s prices. |

| (2) | Equity linked securities issued by Citigroup Global Markets Holdings. |

| (3) | Equity linked securities issued by Hongkong and Shanghai Banking Corporation (HSBC). |

| (4) | Equity linked securities issued by Credit Lyonnais (CLSA). |

144A Securities restricted for resale to Qualified Institutional Buyers in the United States or to non-US persons. At October 31, 2015, these restricted securities amounted to $22,327,128, which represented 7.2% of total net assets.

ADR American Depositary Receipt

See notes to financial statements.

12

Table of Contents

THE CHINA FUND, INC.

STATEMENT OF ASSETS AND LIABILITIES

October 31, 2015

| ASSETS |

||||

| Investments in securities, at value (cost $299,564,065) (including securities on loan, at value, $39,669,593) (Note A) |

$ | 302,493,697 | ||

| Investments in non-controlled affiliates, at value (cost $33,738,096) (Notes A and F) |

28,171,084 | |||

|

|

|

|||

| Total Investments (cost $333,302,161) |

330,664,781 | |||

| Cash |

339 | |||

| Foreign currency, at value (cost $5,262,225) |

5,198,377 | |||

| Receivable for securities lending income |

33,977 | |||

| Prepaid expenses |

105,705 | |||

|

|

|

|||

| TOTAL ASSETS |

336,003,179 | |||

|

|

|

|||

| LIABILITIES |

||||

| Payable upon return of collateral for securities on loan |

21,195,809 | |||

| Investment management fee payable (Note B) |

211,844 | |||

| Administration and custodian fees payable (Note B) |

138,740 | |||

| Capital gains tax reimbursement payable (Note A) |

2,001,458 | |||

| Chief Compliance Officer fees payable |

5,000 | |||

| Directors’ fees payable (Note B) |

31,499 | |||

| Other accrued expenses and liabilities |

228,188 | |||

|

|

|

|||

| TOTAL LIABILITIES |

23,812,538 | |||

|

|

|

|||

| TOTAL NET ASSETS |

$ | 312,190,641 | ||

|

|

|

|||

| COMPOSITION OF NET ASSETS: |

||||

| Par value, 100,000,000 shares authorized, 15,682,029 shares outstanding (Note C) |

156,820 | |||

| Paid in capital in excess of par |

291,728,538 | |||

| Undistributed net investment income |

3,344,508 | |||

| Accumulated net realized gain on investments and foreign currency transactions |

19,662,004 | |||

| Net unrealized depreciation on investments and foreign currency |

(2,701,229 | ) | ||

|

|

|

|||

| TOTAL NET ASSETS |

$ | 312,190,641 | ||

|

|

|

|||

| NET ASSET VALUE PER SHARE |

||||

| ($312,190,641/15,682,029 shares of common stock outstanding) |

$19.91 | |||

|

|

|

|||

See notes to financial statements.

13

Table of Contents

THE CHINA FUND, INC.

STATEMENT OF OPERATIONS

Year Ended October 31, 2015

| INVESTMENT INCOME: |

||||

| Dividend income — (including dividends of $2,013,036 from non-controlled affiliates, net of tax withheld of $705,039) (Note F) |

$ | 7,911,435 | ||

| Securities lending income |

535,566 | |||

| Interest income — (net of tax withheld of $2,626) |

170,249 | |||

|

|

|

|||

| TOTAL INVESTMENT INCOME |

8,617,250 | |||

|

|

|

|||

| EXPENSES |

||||

| Investment Management fees (Note B) |

2,341,216 | |||

| Custodian fees (Note B) |

658,658 | |||

| Directors’ fees and expenses (Note B) |

592,875 | |||

| Administration fees (Note B) |

486,221 | |||

| Audit and tax service fees |

92,500 | |||

| Insurance |

88,843 | |||

| Legal fees |

82,199 | |||

| Chief Compliance Officer fee |

60,000 | |||

| Shareholder service fees |

47,905 | |||

| Printing and postage |

45,637 | |||

| Principal Financial Officer fee |

30,000 | |||

| Transfer agent fees |

27,856 | |||

| Stock exchange listing fee |

26,378 | |||

| Miscellaneous expenses |

35,249 | |||

|

|

|

|||

| TOTAL EXPENSES |

4,615,537 | |||

|

|

|

|||

| NET INVESTMENT INCOME |

4,001,713 | |||

|

|

|

|||

| NET REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS AND FOREIGN CURRENCY TRANSACTIONS |

||||

| Net realized gain on investments |

25,949,218 | |||

| Net realized loss on non-controlled affiliate transactions (Note F) |

(6,286,564 | ) | ||

| Net realized loss on foreign currency transactions |

(656,592 | ) | ||

|

|

|

|||

| 19,006,062 | ||||

|

|

|

|||

| Net change in unrealized appreciation/depreciation on investments |

(31,050,117 | ) | ||

| Net change in unrealized appreciation/depreciation on foreign currency |

(414,631 | ) | ||

|

|

|

|||

| (31,464,748 | ) | |||

|

|

|

|||

| NET REALIZED AND UNREALIZED LOSS ON INVESTMENTS AND FOREIGN CURRENCY TRANSACTIONS |

(12,458,686 | ) | ||

|

|

|

|||

| NET DECREASE IN NET ASSETS FROM OPERATIONS |

$ | (8,456,973 | ) | |

|

|

|

|||

See notes to financial statements.

14

Table of Contents

THE CHINA FUND, INC.

STATEMENTS OF CHANGES IN NET ASSETS

| Year Ended October 31, 2015 |

Year Ended October 31, 2014 |

|||||||

| INCREASE (DECREASE) IN NET ASSETS FROM OPERATIONS |

||||||||

| Net investment income |

$ | 4,001,713 | $ | 5,157,827 | ||||

| Net realized gain on investments and foreign currency transactions |

19,006,062 | 54,219,171 | ||||||

| Net change in unrealized appreciation/depreciation on investments and foreign currency |

(31,464,748 | ) | (31,877,604 | ) | ||||

|

|

|

|

|

|||||

| Net increase (decrease) in net assets from operations |

(8,456,973 | ) | 27,499,394 | |||||

|

|

|

|

|

|||||

| DIVIDENDS AND DISTRIBUTIONS TO SHAREHOLDERS FROM: |

||||||||

| Net investment income |

(4,676,381 | ) | (6,879,707 | ) | ||||

| Net realized gains |

(54,368,026 | ) | (45,090,537 | ) | ||||

|

|

|

|

|

|||||

| Total dividends and distributions to shareholders |

(59,044,407 | ) | (51,970,244 | ) | ||||

|

|

|

|

|

|||||

| NET DECREASE IN NET ASSETS |

(67,501,380 | ) | (24,470,850 | ) | ||||

|

|

|

|

|

|||||

| NET ASSETS: |

||||||||

| Beginning of Year |

379,692,021 | 404,162,871 | ||||||

|

|

|

|

|

|||||

| End of Year |

$ | 312,190,641 | $ | 379,692,021 | ||||

|

|

|

|

|

|||||

| Undistributed net investment income, end of year |

$ | 3,344,508 | $ | 4,675,768 | ||||

|

|

|

|

|

|||||

See notes to financial statements.

15

Table of Contents

THE CHINA FUND, INC.

Selected data for a share of common stock outstanding for the years indicated

| Year Ended October 31, | ||||||||||||||||||||

| 2015 | 2014 | 2013 | 2012(1)(2) | 2011(1) | ||||||||||||||||

| Per Share Operating Performance |

||||||||||||||||||||

| Net asset value, beginning of year |

$ | 24.21 | $ | 25.77 | $ | 24.50 | $ | 28.99 | $ | 34.46 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net investment income* |

0.26 | 0.33 | 0.41 | 0.28 | 0.27 | |||||||||||||||

| Net realized and unrealized gain (loss) on investments and foreign currency transactions |

(0.79 | ) | 1.43 | 4.05 | (1.95 | ) | (3.83 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total from investment operations |

(0.53 | ) | 1.76 | 4.46 | (1.67 | ) | (3.56 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Less dividends and distributions: |

||||||||||||||||||||

| Dividends from net investment income |

(0.30 | ) | (0.44 | ) | (0.35 | ) | (0.17 | ) | (0.37 | ) | ||||||||||

| Distributions from net realized gains |

(3.47 | ) | (2.88 | ) | (2.90 | ) | (2.82 | ) | (1.90 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total dividends and distributions |

(3.77 | ) | (3.32 | ) | (3.25 | ) | (2.99 | ) | (2.27 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net increase from payment by affiliate |

— | — | — | — | 0.36 | |||||||||||||||

| Capital Share Transactions: |

||||||||||||||||||||

| Accretion to net asset value, resulting from share repurchase program, tender offer or issuance of shares in stock dividend |

— | — | 0.06 | 0.17 | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net asset value, end of year |

$ | 19.91 | $ | 24.21 | $ | 25.77 | $ | 24.50 | $ | 28.99 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Market price, end of year |

$ | 17.49 | $ | 21.44 | $ | 22.66 | $ | 21.85 | $ | 25.88 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Investment Return (Based on Market Price) |

(1.95 | )% | 9.71 | % | 19.67 | % | (3.02 | )% | (16.96 | )%(3) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Investment Return (Based on Net Asset Value) |

(1.16 | )% | 8.93 | % | 21.38 | % | (2.93 | )% | (9.71 | )%(3)(4) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Ratios and Supplemental Data |

||||||||||||||||||||

| Net assets, end of year (000’s) |

$ | 312,191 | $ | 379,692 | $ | 404,163 | $ | 396,094 | $ | 660,444 | ||||||||||

| Ratio of expenses to average net assets |

1.34 | % | 1.31 | % | 1.34 | % | 1.41 | % | 1.11 | %(5) | ||||||||||

| Ratio of net investment income to average net assets |

1.16 | % | 1.39 | % | 1.73 | % | 1.12 | % | 0.82 | % | ||||||||||

| Portfolio turnover rate |

64 | % | 67 | % | 45 | % | 78 | % | 20 | % | ||||||||||

| * | Per share amounts have been calculated using the average share method. |

| (1) | Beginning with the year ended October 31, 2012, the Fund was audited by Tait, Weller & Baker. The previous years were audited by another independent registered public accounting firm. |

| (2) | The Fund’s investment management arrangements changed in November 2011, and February 2012. |

| (3) | Without the indemnity payment the Fund received from the insurers of one of the Fund’s former investment managers, the Fund’s total return on net asset value would have been (10.83)%. |

| (4) | Unaudited. |

| (5) | The ratio of expenses, net of management fee reimbursements, was 1.01%. |

See notes to financial statements.

16

Table of Contents

THE CHINA FUND, INC.

OCTOBER 31, 2015

NOTE A — SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The China Fund, Inc. (the “Fund”) was incorporated under the laws of the State of Maryland on April 28, 1992, and is a non-diversified, closed-end management investment company registered under the Investment Company Act of 1940, as amended (the “1940 Act”). The Fund’s investment objective is long-term capital appreciation which it seeks to achieve by investing primarily in equity securities (i) of companies for which the principal securities trading market is the People’s Republic of China (“China”), (ii) of companies for which the principal securities trading market is outside of China, or constituting direct equity investments in companies organized outside of China, that in both cases derive at least 50% of their revenues from goods and services sold or produced, or have at least 50% of their assets, in China and (iii) constituting direct equity investments in companies organized in China. The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements.

Use of estimates: The preparation of financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of income and expenses for the period. Actual results could differ from these estimates.

Security valuation: Portfolio securities listed on recognized United States or foreign security exchanges are valued at the last quoted sales price in the principal market where they are traded. Listed securities with no such sales price and unlisted securities are valued at the mean between the current bid and asked prices, if any, from brokers. Short-term investments having maturities of sixty days or less are valued at amortized cost (original purchase cost as adjusted for amortization of premium or accretion of discount) which when combined with accrued interest approximates market value. Securities for which market quotations are not readily available or are deemed unreliable are valued at fair value in good faith by or at the direction of the Board of Directors considering relevant factors, data and information including, if relevant, the market value of freely tradable securities of the same class in the principal market on which such securities are normally traded. Direct Investments, if any, are valued at fair value as determined by or at the direction of the Board of Directors based on financial and other information supplied by the Direct Investment Manager regarding each Direct Investment. Forward currency contracts are valued at the current cost of offsetting the contract. Equity linked securities are valued at fair value primarily based on the value(s) of the underlying security (or securities), which normally follows the same methodology as the valuation of securities listed on recognized exchanges.

Factors used in determining fair value may include, but are not limited to, the type of security, the size of the holding, the initial cost of the security, the existence of any contractual restrictions on the security’s disposition, the price and extent of public trading in similar securities of the issuer or of comparable companies, the availability of quotations from broker-dealers, the availability of values of third parties other than the Investment Manager or Direct Investment Manager, information obtained from the issuer, analysts, and/or the appropriate stock exchange (if available), an analysis of the company’s financial statements, an evaluation of the forces that influence the issuer and the market(s) in which the security is purchased and sold and with respect to debt securities, the maturity, coupon, creditworthiness, currency denomination, and the movement of the market in which they trade.

17

Table of Contents

NOTES TO FINANCIAL STATEMENTS (continued)

Repurchase Agreements: In connection with transactions in repurchase agreements, it is the Fund’s policy that its custodian take possession of the underlying collateral securities, the fair value of which exceeds the principal amount of the repurchase transaction, including accrued interest, at all times. In the event of default on the obligation to repurchase, the Fund has the right to liquidate the collateral and apply the proceeds in satisfaction of the obligation. Realization of the collateral proceeds may be subject to costs and delays.

Securities Lending: The Fund may lend up to 33 1/3% of the Fund’s total assets held by State Street Bank and Trust Company (“State Street”) as custodian to certain qualified brokers, except those securities which the Fund or the Investment Manager specifically identifies as not being available. By lending its investment securities, the Fund attempts to increase its net investment income through the receipt of interest on the loan. Any gain or loss in the market price of the securities loaned that might occur and any interest or dividends declared during the term of the loan would accrue to the account of the Fund. Risks of delay in recovery of the securities or even loss of rights in the collateral may occur should the borrower of the securities fail financially. Risks may also arise to the extent that the value of the collateral decreases below the value of the securities loaned. Upon entering into a securities lending transaction, the Fund receives cash or other securities as collateral in an amount equal to or exceeding 100% of the current market value of the loaned securities with respect to securities of the U.S. government or its agencies, 102% of the current market value of the loaned securities with respect to U.S. securities and 105% of the current market value of the loaned securities with respect to foreign securities. Any cash received as collateral is generally invested by State Street, acting in its capacity as securities lending agent (the “Agent”), in the State Street Navigator Securities Lending Prime Portfolio. Non-cash collateral is not disclosed in the Fund’s Statement of Assets and Liabilities as it is held by the lending agent on behalf of the Fund and the Fund does not have the ability to re-hypothecate those securities. A portion of the dividends received on the collateral is rebated to the borrower of the securities and the remainder is split between the Agent and the Fund.

As of October 31, 2015, the Fund had loaned securities which were collateralized by cash, short term investments, long term bonds and equities. The value of the securities on loan and the value of the related collateral were as follows:

| Value of Securities |

Value of Cash Collateral |

Value of Non-Cash Collateral* |

Total Collateral |

|||||||||||

| $39,669,593 | $ | 21,195,809 | $ | 20,948,025 | $ | 42,143,834 | ||||||||

| * | Fund cannot repledge or dispose of this collateral, nor does the Fund earn any income or receive dividends with respect to this collateral. |

The following table presents financial instruments that are subject to enforceable netting arrangements as of October 31, 2015.

| Gross Amounts Not Offset in the Statement of Assets and Liabilities | ||||||||||||||

| Gross Asset Amounts Presented in Statement of Assets and Liabilities(a) |

Financial Instrument | Collateral Received(b) | Net Amount (not less than $0) |

|||||||||||

| $39,669,593 | — | ($ | 39,669,593 | ) | $ | 0 | ||||||||

| (a) | Represents market value of loaned securities at period end. |

| (b) | The actual collateral received is greater than the amount shown here due to collateral requirements of the security lending agreement. |

18

Table of Contents

NOTES TO FINANCIAL STATEMENTS (continued)

Foreign currency translations: The records of the Fund are maintained in U.S. dollars. Foreign currencies, investments and other assets and liabilities are translated into U.S. dollars at the current exchange rates. Purchases and sales of investment securities and income and expenses are translated on the respective dates of such transactions. Net realized gains and losses on foreign currency transactions represent net gains and losses from the disposition of foreign currencies, currency gains and losses realized between the trade dates and settlement dates of security transactions, and the difference between the amount of net investment income accrued and the U.S. dollar amount actually received. The effects of changes in foreign currency exchange rates on investments in securities are not segregated in the Statement of Operations from the effects of changes in market prices of those securities, but are included in realized and unrealized gain or loss on investments. Net unrealized foreign currency gains and losses arise from changes in the value of assets and liabilities, other than investments in securities, as a result of changes in exchange rates.

Forward Foreign Currency Contracts: The Fund may enter into forward foreign currency contracts to hedge against foreign currency exchange rate risks. A forward currency contract is an agreement between two parties to buy or sell currency at a set price on a future date. Upon entering into these contracts, risks may arise from the potential inability of counterparties to meet the terms of their contracts and from unanticipated movements in the value of the foreign currency relative to the U.S. dollar. The U.S. dollar value of forward currency contracts is determined using forward exchange rates provided by quotation services. Daily fluctuations in the value of such contracts are recorded as unrealized gain or loss on the Statement of Assets and Liabilities. When the contract is closed, the Fund records a realized gain or loss equal to the difference between the value at the time it was opened and the value at the time it was closed. Such gain or loss is disclosed in the realized and unrealized gain or loss on foreign currency in the Fund’s accompanying Statement of Operations. At October 31, 2015, the Fund did not hold forward foreign currency contracts.

Option Contracts: The Fund may purchase and write (sell) call options and put options provided the transactions are for hedging purposes and the initial margin and premiums do not exceed 5% of total assets. Option contracts are valued daily and unrealized gains or losses are recorded on the Statement of Assets and Liabilities based upon the last sales price on the principal exchange on which the options are traded. The Fund will realize a gain or loss upon the expiration or closing of the option contract. Such gain or loss is disclosed in the realized and unrealized gain or loss on options in the Fund’s accompanying Statement of Operations. When an option is exercised, the proceeds on sales of the underlying security for a written call option, the purchase cost of the security for a written put option, or the cost of the security for a purchased put or call option is adjusted by the amount of premium received or paid.

The risk in writing a call option is that the Fund gives up the opportunity for profit if the market price of the security increases and the option is exercised. The risk in writing a put option is that the Fund may incur a loss if the market price of the security decreases and the option is exercised. The risk in buying an option is that the Fund pays a premium whether or not the option is exercised. Risks may also arise from an illiquid secondary market or from the inability of counter parties to meet the terms of the contract. At October 31, 2015, the Fund did not hold any option contracts.

19

Table of Contents

NOTES TO FINANCIAL STATEMENTS (continued)

Equity-Linked Securities: The Fund may invest in equity-linked securities such as linked participation notes, equity swaps and zero-strike options and securities warrants. Equity-linked securities currently held by the Fund are privately issued securities whose investment results are designed to correspond generally to the performance of a specified stock index or “basket” of stocks, or a single stock. Equity-linked securities may be used by the Fund to gain exposure to countries that place restrictions on investments by foreigners. To the extent that the Fund invests in equity-linked securities whose return corresponds to the performance of a foreign securities index or one or more foreign stocks, investing in equity-linked securities will involve risks similar to the risks of investing in foreign securities. In addition, the Fund bears the risk that the issuer of any equity-linked securities may default on its obligation under the terms of the arrangement with the counterparty. Equity-linked securities are often used for many of the same purposes as, and share many of the same risks with, derivative instruments. In addition, equity-linked securities may be considered illiquid.

At October 31, 2015, the Fund held equity-linked securities, in the form of warrants issued by Credit Lyonnais, Citigroup Global Markets Holdings and Hongkong and Shanghai Banking Corporation (HSBC), (the “Issuers”). Under the terms of the agreements, each warrant entitles the Fund to receive from the related Issuer an amount in U.S. dollars linked to the performance of specific equity shares. Under these agreements, the Fund has agreed to pay or provide reimbursement for any taxes imposed on the China A Share investments underlying the equity-linked securities. Non-resident corporate investors in China, such as the Issuers of the equity-linked securities, are subject to a statutory 10% withholding tax on both dividend and interest income sourced from China, absent an applicable tax treaty. During the year ended October 31, 2015, pursuant to an indemnification agreement entered into on February 28, 2007, the Fund incurred a liability to reimburse Citigroup Global Markets Holdings $2,001,458 for capital gains taxes paid related to investments in equity-linked securities from the period of November 2009 through November 2014.

Direct Investments: The Fund may invest up to 25% of the net proceeds from its offering of its outstanding common stock in direct investments; however, the Board of Directors of the Fund has suspended additional investments in direct investments. Direct investments are generally restricted and do not have a readily available resale market. Because of the absence of any public trading market for these investments, the Fund may take longer to liquidate these positions than would be the case for publicly traded securities. Although these securities may be resold in privately negotiated transactions, the prices on these sales could be less than those originally paid by the Fund. Issuers whose securities are not publicly traded may not be subject to public disclosure and other investor protections requirements applicable to publicly traded securities. At October 31, 2015, the Fund did not hold direct investments.

Indemnification Obligations: Under the Fund’s organizational documents, its Officers and Directors are indemnified against certain liabilities arising out of the performance of their duties to the Fund. In addition, in the normal course of business the Fund enters into contracts that provide general indemnifications to other parties. The Fund’s maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Fund that have not yet occurred.

Security transactions and investment income: Security transactions are recorded as of the trade date. Realized gains and losses from securities sold are recorded on the identified cost basis. Dividend income is recorded on the

20

Table of Contents

NOTES TO FINANCIAL STATEMENTS (continued)

ex-dividend date, or, in the case of dividend income on foreign securities, on the ex-dividend date or when the Fund becomes aware of its declaration. Interest income is recorded on the accrual basis. All premiums and discounts are amortized/accreted for both financial reporting and federal income tax purposes.

Dividend and interest income generated in Taiwan is subject to a 20% withholding tax. Stock dividends received are taxable at 20% of the par value of the stock dividends received. The Fund records the taxes paid on stock dividends as an operating expense.

Dividends and distributions: The Fund intends to distribute to its stockholders, at least annually, substantially all of its net investment income and any net realized capital gains. Distributions to stockholders are recorded on the ex-dividend date. Income and capital gains distributions are determined in accordance with federal income tax regulations, which may differ from U.S. generally accepted accounting principles. Certain capital accounts in the financial statements are periodically adjusted for permanent differences in order to reflect their tax character. These adjustments have no impact on net assets or net asset value per share. Temporary differences which arise from recognizing certain items of income, expense, gain or loss in different periods for financial statement and tax purposes will reverse at some time in the future. Unless the Board of Directors elects to make distributions in shares of the Fund’s common stock, the distributions will be paid in cash, except with respect to stockholders who have elected to participate in the Fund’s Dividend Reinvestment and Cash Purchase Plan.

Federal Taxes: It is the Fund’s policy to qualify each year as a regulated investment company under Subchapter M of the Internal Revenue Code, as amended (“Code”) and to distribute to stockholders each year substantially all of its income. Accordingly, no provision for federal income tax is necessary. As of and during the period ended October 31, 2015, the Fund did not have a liability for any uncertain tax positions. The Fund recognizes interest and penalties, if any, related to tax liabilities as income tax expense in the Statement of Operations. For the tax years ending October 31, 2012, October 31, 2013 and October 31, 2014, the Fund remains subject to examination by the Fund’s major tax jurisdictions, which include the United States of America and the State of Maryland. The Fund may be subject to taxes imposed by governments of countries in which it invests. Such taxes are generally based on either income or gains earned or repatriated. The Fund accrues and applies such taxes to net investment income, net realized gains and net unrealized gains as income and/or gains are earned.

The tax character of distributions the Fund made during the year ended October 31, 2015, was $4,676,381 from ordinary income and $54,368,026 from long-term capital gains. For the year ended October 31, 2014, the Fund distributed $6,879,707 from ordinary income and $45,090,537 from long-term capital gains.

Tax components of distributable earnings are determined in accordance with income tax regulations which may differ from the composition of net assets reported under GAAP. Accordingly, for the year ended October 31, 2015, the effects of certain differences were reclassified. The Fund decreased undistributed net investment income by $656,592 and increased accumulated net realized gain by $656,592. These differences were primarily due to the differing tax treatment of foreign currency. Net assets of the Fund were unaffected by the reclassifications and the calculation of net investment income per share in the Financial Highlights excludes these adjustments.

21

Table of Contents

NOTES TO FINANCIAL STATEMENTS (continued)

As of October 31, 2015, the components of distributable earnings on a tax basis were $10,185,434 of undistributed ordinary income and $13,270,001 of undistributed capital gains, the Fund also had $3,150,152 of net unrealized depreciation on investments and currency, resulting in a total accumulated earnings of $20,305,283. Permanent book/tax differences relate to foreign currency gains and losses.

At October 31, 2015, the cost of investments for federal income tax purposes was $333,751,084. Gross unrealized appreciation of investments was $38,448,817 while gross unrealized depreciation of investments was $41,535,120, resulting in net unrealized depreciation of investments of $3,086,303.

NOTE B — ADVISORY FEE AND OTHER TRANSACTIONS

Allianz Global Investors U.S. LLC (“AllianzGI U.S.”) is the Investment Manager for the Fund’s listed assets (the “Listed Assets”). AllianzGI U.S. receives a fee, computed weekly and payable monthly, at the following annual rates: 0.70% of the first US$315 million of the Fund’s average weekly net assets invested in Listed Assets; and 0.50% of the Fund’s average weekly net assets invested in Listed Assets in excess of US$315 million. For the year ended October 31, 2015, the Listed Assets investment management fee rate was equivalent to an annual effective rate of 0.68% of the Fund’s average weekly net assets. AllianzGI U.S. is the Investment Manager for the Fund’s direct investments. AllianzGI U.S. receives a fee computed weekly and payable monthly, at an annual rate of 1.50% of the average weekly value of the Fund’s assets invested in direct investments, if any. For the year ended October 31, 2015, the Investment Manager was paid no fees for direct investments as the Fund held no such investments during the period.

No director, officer or employee of the Investment Manager or Direct Investment Manager or any affiliates of those entities will receive any compensation from the Fund for serving as an officer or director of the Fund. The Fund pays the Chairman of the Board and each of the directors (who is not a director, officer or employee of the Investment Manager or Direct Investment Manager or any affiliate thereof) an annual fee of $35,000 and $20,000 respectively, plus $3,000 for each Board of Directors’ meeting or Audit and Nominating Committee meeting attended, $3,000 for each telephonic meeting attended. In addition, the Fund will reimburse each of the directors for travel and out-of-pocket expenses incurred in connection with attending Board of Directors’ meetings.

State Street provides, or arranges for the provision of certain administrative services for the Fund, including preparing certain reports and other documents required by federal and/or state laws and regulations. The Fund pays State Street a fee that is calculated daily and paid monthly at an annual rate based on aggregate average daily assets of the Fund. The Fund also pays State Street an annual fee for certain legal administration services, including corporate secretarial services and preparing regulatory filings.

The Fund has also contracted with State Street to provide custody and fund accounting services to the Fund. For these services, the Fund pays State Street asset-based fees that vary according to the number of positions and transactions plus out-of-pocket expenses.

NOTE C — FUND SHARES

At October 31, 2015, there were 100,000,000 shares of $0.01 par value capital stock authorized, of which 15,682,029 were issued and outstanding.

22

Table of Contents

NOTES TO FINANCIAL STATEMENTS (continued)

NOTE D — INVESTMENT TRANSACTIONS

For the year ended October 31, 2015, the Fund’s cost of purchases and proceeds from sales of investment securities, other than short-term securities, were $192,738,495 and $201,510,773, respectively.

NOTE E — INVESTMENTS IN CHINA

The Fund’s investments in Chinese companies involve certain risks not typically associated with investments in securities of U.S. companies or the U.S. Government, including risks relating to (1) social, economic and political uncertainty; (2) price volatility, lesser liquidity and smaller market capitalization of securities markets in which securities of Chinese companies trade; (3) currency exchange fluctuations, currency blockage and higher rates of inflation; (4) controls on foreign investment and limitations on repatriation of invested capital and on the Fund’s ability to exchange local currencies for U.S. dollars; (5) governmental involvement in and control over the economy; (6) risk of nationalization or expropriation of assets; (7) the nature of the smaller, less seasoned and newly organized Chinese companies, particularly in China; and (8) the absence of uniform accounting, auditing and financial reporting standards, practices and disclosure requirements and less government supervision and regulation.

NOTE F — INVESTMENTS IN NON-CONTROLLED AFFILIATES*:

| Name of Issuer |

Balance

of Shares/Par Held October 31, 2014 |

Gross Purchases and Additions |

Gross Sales and Reductions |

Balance of Shares/Par Held October 31, 2015 |

Value October 31, 2015 |

Income

From Non-Controlled Affiliates |

Gain (Loss) Realized on Sale of Shares during the Year Ended October 31, 2015 |

|||||||||||||||||||||

| China Suntien Green Energy Corp., Ltd.(1) |

12,785,000 | — | 12,785,000 | — | $ | — | $ | 36,824 | $ | (2, 091,903 | ) | |||||||||||||||||

| Digital China Holdings, Ltd. |

8,865,000 | 526,000 | — | 9,391,000 | 9,596,872 | 242,141 | — | |||||||||||||||||||||

| Li & Fung, Ltd.(1) |

9,282,000 | 2,762,000 | 2,246,000 | 9,798,000 | 7,977,365 | 599,321 | (954,998 | ) | ||||||||||||||||||||

| Qingling Motors Co., Ltd. |

28,960,000 | — | — | 28,960,000 | 9,341,815 | 681,942 | — | |||||||||||||||||||||

| Sun Hung Kai Properties, Ltd. |

788,000 | 63,000 | 163,000 | 688,000 | 9,232,397 | 341,453 | 19,292 | |||||||||||||||||||||

| Tong Hsing Electronic Industries, Ltd.(1) |

2,067,000 | — | 2,067,000 | — | — | 111,355 | (3,258,955 | ) | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| 62,747,000 | 3,351,000 | 17,261,000 | 48,837,000 | $ | 36,148,449 | $ | 2,013,036 | $ | (6,286,564 | ) | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| * | Affiliated issuers, as defined in the 1940 Act as amended, include issuers in which the Fund held 5% or more of the outstanding voting securities. |

| (1) | Not affiliated as of October 31, 2015. |

23

Table of Contents

NOTES TO FINANCIAL STATEMENTS (continued)

NOTE G — FAIR VALUE MEASUREMENT

The Fund has adopted fair valuation accounting standards which establish a definition of fair value and set out a hierarchy for measuring fair value. These standards require additional disclosures about the various inputs and valuation techniques used to develop the measurements of fair value and a discussion of changes in valuation techniques and related inputs during the period. These inputs are summarized in the three broad levels listed below:

| • | Level 1 — Inputs that reflect unadjusted quoted prices in active markets for identical assets or liabilities that the Fund has the ability to access at the measurement date; |

| • | Level 2 — Inputs other than quoted prices that are observable for the asset or liability either directly or indirectly, including inputs in markets that are not considered to be active; |

| • | Level 3 — Inputs that are unobservable. |

The following is a summary of the inputs used as of October 31, 2015 in valuing the Fund’s investments carried at value:

ASSETS VALUATION INPUT

| Description |

Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| Common Stock And Other Equity Interests |

$ | 291,083,711 | $ | — | $ | — | $ | 291,083,711 | ||||||||

| Equity-linked Securities |

— | 15,575,261 | — | 15,575,261 | ||||||||||||

| Collateral For Securities On Loan |

21,195,809 | — | — | 21,195,809 | ||||||||||||

| Short Term Investments |

— | 2,810,000 | — | 2,810,000 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| TOTAL INVESTMENTS |

$ | 312,279,520 | $ | 18,385,261 | $ | — | $ | 330,664,781 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

The Fund’s policy is to disclose transfers between levels based on valuations at the end of the reporting period. As of October 31, 2015, there were no transfers between Level 1, 2 or 3.

NOTE H — DERIVATIVE INSTRUMENTS AND HEDGING ACTIVITIES

The Fund did not enter into any derivatives transactions or hedging activities for the year ended October 31, 2015.

NOTE I — ACCOUNTING PRONOUNCEMENT

In April 2015, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) 2015-7, Disclosures for Investments in Certain Entities That Calculate Net Asset Value per Share (or Its Equivalent), modifying Accounting Standards Codification (“ASC”) 946 Financial Services — Investment Companies. Under the modifications, investments in affiliated and private investment funds valued at NAV are no longer included in the fair value hierarchy. ASU 2015-7 is effective for fiscal years beginning on or after December 15, 2015, and interim periods within those annual periods. Early application is permitted. Management is currently evaluating the implications of ASU 2015-7 and the impact on the Fund’s financial statements and related disclosures.

24

Table of Contents

NOTES TO FINANCIAL STATEMENTS (continued)

NOTE J — SUBSEQUENT EVENT

At the Board of Director’s meeting on December 4, 2015, the Board approved an increase to the Audit Committee Chairman’s annual fee to $30,000.

25

Table of Contents

REGISTERED PUBLIC ACCOUNTING FIRM

To the Shareholders and The Board of Directors of

The China Fund, Inc.

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of The China Fund, Inc. (the “Fund”), as of October 31, 2015 and the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended and the financial highlights for each of the four years in the period then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits. The financial highlights for the period ended October 31, 2011 have been audited by other auditors whose report dated December 23, 2011 expressed an unqualified opinion on such financial highlights.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of October 31, 2015, by correspondence with the custodian and brokers or through other appropriate auditing procedures where replies from brokers were unable to be obtained. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of The China Fund, Inc. as of October 31, 2015, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and the financial highlights for each of the four years in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

/s/ TAIT, WELLER & BAKER LLP

Philadelphia, Pennsylvania

December 21, 2015

26

Table of Contents

THE CHINA FUND, INC.

TAX INFORMATION

Foreign Taxes Credit: The Fund designates $668,531 as foreign taxes paid and $8,540,751 as foreign source income earned for regular Federal income tax purposes.

Qualified Dividend Income: For the fiscal year ended October 31, 2015, the Fund will designate up to the maximum amount allowable pursuant to the Internal Revenue Code, as qualified dividend income eligible for reduced tax rates. These lower rates range from 5% to 15% depending on the individual’s tax bracket. Complete information will be reported in conjunction with the Form 1099-DIV. For the year ended October 31, 2015, the Fund had $2,999,281 in Qualified Dividend Income and 0.09% of total ordinary income dividends paid qualified for the corporate dividends received deduction.

PRIVACY POLICY

| Privacy Notice

The China Fund, Inc. collects nonpublic personal information about its stockholders from the following sources:

¨ Information it receives from stockholders on applications or other forms; and

¨ Information about stockholder transactions with the Fund.

The Fund’s policy is to not disclose nonpublic personal information about its stockholders to nonaffiliated third parties (other than disclosures permitted by law).

The Fund restricts access to nonpublic personal information about its stockholders to those agents of the Fund who need to know that information to provide products or services to stockholders. The Fund maintains physical, electronic and procedural safeguards that comply with federal standards to guard its stockholders’ nonpublic personal information. |

PROXY VOTING POLICIES AND PROCEDURES

A description of the policies and procedures that are used by the Fund’s investment advisers to vote proxies relating to the Fund’s portfolio securities is available (1) without charge, upon request, by calling 1-888-CHN-CALL (246-2255); and (2) as an exhibit to the Fund’s annual report on Form N-CSR which is available on the website of the Securities and Exchange Commission (the “Commission”) at http://www.sec.gov. Information regarding how the investment advisers vote these proxies is now available by calling the same number and on the Commission’s website. The Fund has filed its report on Form N-PX covering the Fund’s proxy voting record for the 12 month period ending June 30, 2015.

QUARTERLY PORTFOLIO OF INVESTMENTS

A Portfolio of Investments will be filed as of the end of the first and third quarter of each fiscal year on Form N-Q and will be available on the Securities and Exchange Commission’s website at http://www.sec.gov. Form N-Q has

27

Table of Contents

THE CHINA FUND, INC.

Other Information (continued) (Unaudited)

been filed as of July 31, 2015 for the third quarter of this fiscal year and is available on the Securities and Exchange Commission’s website at http://www.sec.gov. Additionally, the Portfolio of Investments may be reviewed and copied at the Commission’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330. The quarterly Portfolio of Investments will be made available with out charge, upon request, by calling 1-888-246-2255.

CERTIFICATIONS

The Fund’s chief executive officer has certified to the New York Stock Exchange that, as of April 2, 2015, he was not aware of any violation by the Fund of applicable New York Stock Exchange corporate governance listing standards. The Fund also has included the certifications of the Fund’s chief executive officer and chief financial officer required by Section 302 and Section 906 of the Sarbanes-Oxley Act of 2002 in the Fund’s Form N-CSR filed with the Securities and Exchange Commission, for the period of this report.

28

Table of Contents

SUMMARY OF DIVIDEND REINVESTMENT AND CASH PURCHASE PLAN

The Fund will distribute to stockholders, at least annually, substantially all of its net investment income from dividends and interest earnings and expects to distribute any net realized capital gains annually. Pursuant to the Dividend Reinvestment and Cash Purchase Plan (the “Plan”), adopted by the Fund, each stockholder will automatically be a participant (a “Participant”) in the Plan unless Computershare Trust Company, N.A., the Plan Agent, is otherwise instructed by the stockholder in writing, to have all distributions, net of any applicable U.S. withholding tax, paid in cash. Stockholders who do not participate in the Plan will receive all distributions in cash paid by check in U.S. dollars mailed directly to the stockholder by Computershare Trust Company, N.A., as paying agent. Stockholders who do not wish to have distributions automatically reinvested should notify the Fund by contacting Computershare Trust Company, N.A. c/o The China Fund, Inc. at P.O. Box 43078, Providence, Rhode Island 02940-3078, by telephone at 1-800-426-5523 or via the Internet at www.computershare.com/investor.