Document

|

| | | | | | | | | | |

As filed with the Securities and Exchange Commission on April 1, 2019 |

| | | | | | | Registration No. 333-225544 |

| | | | | | | | | | |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION |

| | | | | | | | | | |

Washington, D.C. 20549 |

| | | | | | | | | | |

| | | | | | | | | | |

Pre-effective Amendment No. 2 |

to |

FORM S-1 |

| | | | | | | | | | |

| | | REGISTRATION STATEMENT | | | |

| | | | | | | | | | |

UNDER |

| | | | | | | | | | |

THE SECURITIES ACT OF 1933 |

| | | | | | | | | | |

| | | | | | | | | | |

Athene Annuity and Life Company |

(Exact name of registrant as specified in its charter) |

| | | | | | | | | | |

| Iowa | 6311 | 42-0175020 | |

| (State or other jurisdiction of | (Primary Standard Industrial | (I.R.S. Employer | |

| incorporation or organization) | Classification Code) | Identification Number) | |

| | | | | | | | | | |

7700 Mills Civic Parkway |

West Des Moines, IA 50266-3862 |

(888) 266-8489 |

| | | | | | | | | | |

| | | | | | | | | | |

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices) |

| | | | | | | | | | |

| | | | Blaine Doerrfeld | | | | |

| | | | Athene Annuity and Life Company | | | | |

| | | | 7700 Mills Civic Parkway | | | | |

| | | | West Des Moines, IA 50266-3862 | | | | |

| | | | (888) 266-8489 | | | | |

(Name, address, including zip code, and telephone number, including area code, of agent for service) |

| | | | | | | | | | |

| | Copy to: | | |

| | | | |

| | Stephen E. Roth, Esq. | | |

| | Eversheds Sutherland (US) LLP | | |

| | 700 Sixth Street, N.W. | | |

| | Washington, DC | | |

| | 20001-3980 | | |

| | | | | | | | | | |

| Approximate date of commencement of proposed sale to the public: Continuously on and after the effective date of this Registration Statement. |

| If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check |

the following box. x |

| If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the |

Securities Act registration statement number of earlier effective registration statement for the same offering. ¨ | |

| If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration |

statement number of the earlier effective registration statement for the same offering. ¨ | |

| If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration |

statement number of the earlier effective registration statement for the same offering. ¨ | |

| Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging |

growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” |

Large accelerated filer ¨ | | | | | Accelerated filer ¨ | |

Non-accelerated filer x | | | | | Smaller reporting company ¨ | |

| | | | | Emerging growth company ¨ | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for |

complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ¨ |

CALCULATION OF REGISTRATION FEE | |

Title of Each Class of Securities to be Registered | Amount to be Registered(1) | Proposed Maximum Offering Price Per Unit(1) | Proposed Maximum Aggregate Offering Price(1) | Amount of Registration Fee(2) | |

Interests in Single Purchase Payment Index-Linked Deferred Annuity Contract | N/A | N/A | $1,300,000,000.00 | $157,563.30 | |

(1) | The proposed maximum aggregate offering price is estimated solely for the purpose of determining the registration fee. The amount to be registered and the proposed maximum offering price per unit are not applicable because the securities are not issued in predetermined amounts or units. | |

(2) | The registrant previously paid a total of $124.50 in connection with the initial filing of the Registration Statement on June 8, 2018, based upon a proposed maximum aggregate offering price of $1,000,000. This amendment to the Registration Statement increases the proposed maximum aggregate offering price by $1,299,000,000. In accordance with Rule 457(o), an additional $157,438.80 is being paid herewith. |

| The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment |

which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement |

shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine. |

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion Dated April 1, 2019

Athene® Amplify

Single Purchase Payment Index-Linked

Deferred Annuity Contract

Issued by:

Athene Annuity and Life Company

7700 Mills Civic Parkway

West Des Moines, IA 50266-3862

Tel. (888) 266-8489

This prospectus describes the Athene® Amplify Single Purchase Payment Index-Linked Deferred Annuity Contract (the Contract) issued by Athene Annuity and Life Company (the Company, we or us) that is designed for retirement or other long-term investment purposes.

The Contract offers index-linked investment options (Index-Linked Segment Options) that provide returns (Segment Credits) based on the performance of a broad-based index or indices (the Reference Index). Segment Credits are paid by the Company and are subject to its claims paying ability. We calculate Segment Credits based on the changes in the value of the Reference Index of the Segment Option. Currently the Segment Options calculate Segment Credits based on the S&P 500® Price Return Index (S&P 500® Index), the Russell 2000® Price Return Index (Russell 2000® Index), the MSCI EAFE Price Return Index (MSCI EAFE Index) or a weighted combination of the return on the three indices (the Performance Blend Segment Option) that is available in a Buffer Segment Option with a 6-year Segment Term. Additionally, the Contract offers Fixed Segment Options that determine Segment Credits at a guaranteed interest rate.

Index-Linked Segment Options offer different levels of protection. Floor Segment Options include a Floor, which establishes the maximum amount of negative Index Change that may be applied to determine Segment Credits for the Segment Option. Buffer Segment Options include a Buffer, which establishes the maximum amount of negative index performance on a Segment End Date that we will absorb before applying negative Segment Credits to the Segment Option. A negative Segment Credit will apply for any negative Index Change or Aggregate Index Change in excess of the Buffer Rate. Index-Linked Segment Options will also have a Cap Rate, which establishes the maximum positive Index performance that may be applied to the Segment Option, and a Participation Rate that is multiplied by positive Index performance after the application of the Cap to determine the amount of Segment Credits applied to the Segment Option. The Performance Blend Segment Option will also include Index Allocation Percentages to determine the Aggregate Index Change.

Segment Credits applied to the Index-Linked Segment Options on the Segment End Date will fluctuate in value based on the performance of the Reference Index, and you may lose money, including your principal and previously credited Segment Credits. Depending on the performance of the Reference Index and the Segment Option you select, such losses may be significant. Segment Credits will reflect only the difference in the value of the Reference Index on the Segment Start Date and the Segment End Date, which will vary from and can be significantly lower than the difference on intermediate dates during the Segment Term Period. In addition, the ongoing deduction of Segment Fees from Index-Linked Segment Option will reduce Segment Value.

The risk of loss becomes greater if you take a Withdrawal or surrender the Contract. The Interest Adjustment, which applies to all Withdrawals and surrenders during the first six Contract Years, will be negative if interest rates have risen since your Contract Date. The Equity Adjustment, which applies to Withdrawals and surrenders from Index-Linked Segment Options before the Segment End Date, may be negative even when the value of the Reference Index has increased or has declined less than the Buffer Rate for a Buffer Segment Option. Similarly, the Equity Adjustment may reduce the Segment Interim Value of a Floor Segment Option by more than the applicable Floor Rate. During the first six Contract Years, the Withdrawal Charge will further reduce proceeds payable on a Withdrawal greater than the Free Withdrawal amount or on a surrender of the Contract.

The Company is not an investment advisor and does not provide any investment advice to you with respect to the Contract. Athene Securities LLC (Athene Securities) is the distributing underwriter for the Contract and does not provide any investment advice to you with respect to the Contract. Prospective purchasers may apply to purchase a Contract through broker-dealers or other financial institutions that have entered into a selling agreement with Athene Securities.

The Contract is a complex insurance and investment vehicle. Before you invest, you should speak with your Financial Professional about the Contract’s features, benefits, risks, and fees and whether the Contract is appropriate for you based on your financial situation and objectives.

The prospectus describes all material rights and obligations under the Contract. You should study this prospectus and retain it along with a copy of the Contract for future reference.

All guarantees under the Contract are obligations of the Company and are subject to its creditworthiness and financial strength.

For additional information on risks associated with owning the Contract see Section 4 “Contract Risk Factors” on page 13.

Neither the Securities and Exchange Commission (SEC) nor any state securities commission has approved or disapproved these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

This prospectus is not an offer to sell those securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

This Contract is not a bank deposit and is not insured by the FDIC or NCUSIF.

This Contract is a security. It involves investment risk and may lose value.

|

| | | |

| | Table of Contents | |

1. | | |

2. | | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

3. | | |

| | |

| | |

| | |

4. | | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

5. | | |

| | |

| | |

| | |

| | |

| | |

6. | | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

7. | | |

| | |

| | |

| | |

8. | | |

| | |

| | |

|

| | | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

9. | | |

| | |

10. | | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

11. | | |

12. | | |

| | |

| | |

| | |

13. | | |

14. | | |

| | |

| | |

15. | | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

16. | | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

1. Glossary

Accumulation Phase: The period of time between the Contract Date and the Annuity Date, unless the Contract is terminated.

Administrative Office: Mail Processing Center, P.O. Box 1555, Des Moines, IA 50306-1555; (888) 266-8489.

Aggregate Index Change: Used in the calculation of the Segment Credit on the Performance Blend Segment Option. This Segment Option uses three indices in its calculation. On the Segment End Date, we calculate the Index Change for each of these indices. The Aggregate Index Change is the sum of the Index Change for the best performing index multiplied by Index Allocation Percentage 1 (50%) plus the Index Change for the second best performing index multiplied by Index Allocation Percentage 2 (30%) plus the Index Change for the third best performing index multiplied by Index Allocation Percentage 3 (20%).

Annuitant, Joint Annuitant: The Annuitant is the natural person named on the Contract schedule whose life determines the Annuity Payments made under your Contract. We will allow you to name two natural persons on the application as Joint Annuitants. If there is a Joint Annuitant, the Joint Annuitant must be the Annuitant’s spouse.

Annuity Date: The Contract Anniversary on or first following the later of the Annuitant’s age 95, or the 10th Contract Anniversary. In the case of Joint Annuitants, the Annuity Date will be set based on the age of the older Joint Annuitant. You may select an earlier Annuity Date, which may be any time after the Contract Date, by Notice provided to us. The revised Annuity Date must be at least 10 days after our receipt of your Notice.

Annual Interest Rate: The annual rate used to calculate Segment Credits on the Fixed Segment Option.

Annuity Payments: Payments paid to you or your designated payee in accordance with the terms and conditions of the Settlement Option elected by the Owner. The payments are made by us and commence on the Annuity Date.

Annuity Phase: The phase of the Contract when Annuity Payments are being made.

Bailout Rate: The threshold rate(s) set for each Segment Option for use in the initial Segment Term Period bailout provision, provided at the time of application and printed in your Contract schedule. Each Fixed Segment Option will have a Bailout Annual Interest Rate. Each Index-Linked Segment Option will have a Bailout Cap Rate and a Bailout Participation Rate. If the Annual Interest Rate, Cap Rate, or Participation Rate set at the first Segment Start Date is less than the corresponding Bailout Rate for a Segment Option to which you have allocated funds, you may cancel your Contract during the first sixty (60) days after your Contract Date and receive your Purchase Payment less any Withdrawals.

Beneficiary: The person(s) or entity(ies) named by the Owner to receive the Death Benefit.

Buffer Rate (“Buffer”): The amount of negative Index Change that we will absorb when calculating Segment Credits for a Buffer Segment Option. A negative Segment Credit will apply for any negative Index Change or Aggregate Index Change in excess of the Buffer Rate.

Buffer Segment Option: An Index-Linked Segment Option that includes a Buffer Rate.

Business Day: Any day of the week except for Saturday, Sunday, and U.S. Federal holidays where U.S. stock exchanges are closed. Our Business Day ends at 4:00 p.m. Eastern Time.

Cap Rate: The maximum positive Index Change that will be used in the calculation of Segment Credits that may be applied to a Segment Option on the Segment End Date. There is one Cap Rate per Segment Term Period, which applies to the entire Segment Term Period.

Cash Surrender Value: The Interim Value adjusted for any applicable Withdrawal Charge. You may surrender your Contract by making a request to our Administrative Office at any time before the Annuity Date and before the Death Benefit becomes payable.

Company (“we”, “us”, “our”, “ours”): Athene Annuity and Life Company.

Confinement Waiver of Withdrawal Charges: The waiver of Withdrawal Charges on a Withdrawal from your Contract upon meeting certain qualification requirements.

Contract: The Single Purchase Payment Index-Linked Deferred Annuity Contract described by this prospectus.

Contract Anniversary: Any twelve-month anniversary of the Contract Date. For example, if the Contract Date is January 10, 2018, then the first Contract Anniversary is January 10, 2019.

Contract Date: The date your Contract is issued, as shown on the Contract schedule.

Contract Value: The Contract Value at any time is equal to the sum of the Segment Values.

Contract Year: The twelve-month period that begins on the Contract Date and each Contract Anniversary. For example, if the Contract Date is January 17, 2018, then the first Contract Year is the twelve-month period between January 17, 2018 and January 16, 2019.

Death Benefit: During the Withdrawal Charge Period, the Death Benefit will be equal to the greater of the Interim Value or the Purchase Payment less net proceeds from prior Withdrawals. After the Withdrawal Charge Period, the Death Benefit will be equal to the Interim Value. The Death Benefit will be calculated as of the date of death. If the Owner is changed or an additional Owner is added during the Withdrawal Charge Period, the Death Benefit will equal the Interim Value.

Equity Adjustment: A positive or negative adjustment to Segment Value that is applied to any Withdrawal from an Index-Linked Segment Option on a day other than a Segment End Date. The Equity Adjustment is equal to zero on the Segment End Date. The Equity Adjustment does not apply to a Fixed Segment Option.

Financial Professional: A registered representative of a broker-dealer that has a selling agreement with our principal underwriter, Athene Securities.

Fixed Segment Option: A Segment Option that calculates Segment Credits daily based on a declared Annual Interest Rate. A Fixed Segment Option does not include a Reference Index.

Free Withdrawal: A Withdrawal amount on which no Withdrawal Charge applies.

Floor Rate (“Floor”): The maximum negative Index Change that may be applied in the calculation of Segment Credits to a Floor Segment Option on the Segment End Date.

Floor Segment Option: An Index-Linked Segment Option that includes a Floor Rate.

Good Order: A request, including an application, is in Good Order if it contains all the information we require to process the request. Good Order also includes delivering information on the correct form, with any required certifications, guarantees, and/or signatures to our Administrative Office.

Holding Account: An account that holds the Purchase Payment until it is allocated to the Segment Options according to the Segment Allocation Percentages you select. Interest is credited daily to the Holding Account at the Holding Account Fixed Interest Rate.

Holding Account Fixed Interest Rate: The annual rate used to calculate interest credited on amounts held in the Holding Account.

Index Allocation Percentage: The percentage used to calculate the portion of Index Change from each index that will be used in the Aggregate Index Change for our Performance Blend Segment Option.

Index Change: The percentage change in the Index Price of the Reference Index for the selected Segment Option, as measured from the Segment Start Date to the Segment End Date.

Index-Linked Segment Option: Any Segment Option that is not the Fixed Segment Option. An Index-Linked Segment Option includes a Reference Index.

Index Price: The Index Price for any date, including any Segment Start Date, Segment End Date, Annuity Date or date of death is the closing price of the Reference Index on that date. The closing price of the Reference Index is the price determined and published by the provider of the Reference Index at the end of each Business Day. Any change in price after the closing price has been published will not be reflected.

Interim Value: The Interim Value at any time is equal to the sum of the Segment Interim Values.

Interest Adjustment: A positive or negative adjustment to Segment Value that is applied to any Withdrawal during the first six years of the Contract, including Withdrawals taken on a Segment End Date. The Interest Adjustment approximates the change in value of debt instruments supporting the Contract, which we sell to fund the Withdrawal. The Interest Adjustment does not apply to any Withdrawal taken after the first six Contract Years.

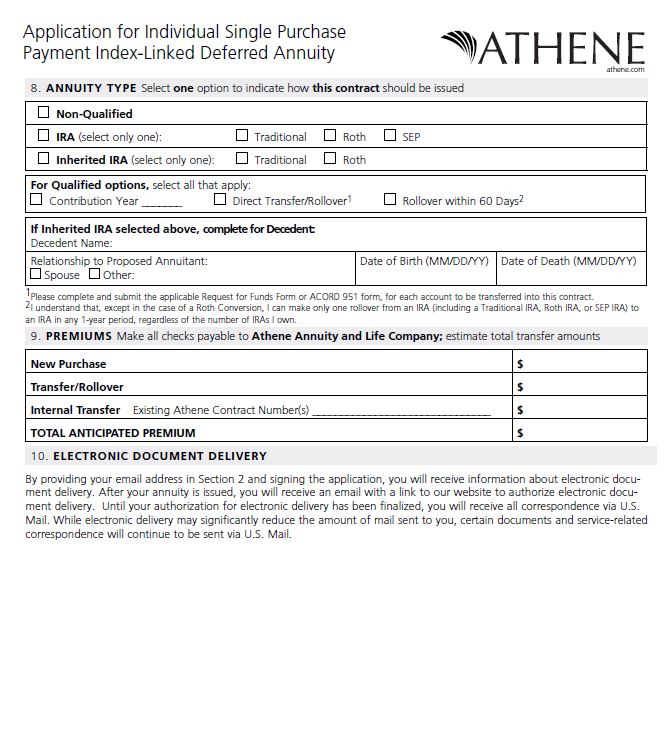

IRA Account: The traditional Roth or other Individual Retirement Account established for the Owner and the Owner’s beneficiaries, through which a Contract may be purchased.

Non-Qualified Contract: A Contract that is not qualified for special tax treatment under sections of the Internal Revenue Code.

Notice, Notify, Notifying: Requests and information that you sign and that we receive and accept at our Administrative Office in any form offered by and acceptable to us.

Owner (“you”, “your”): The Contract Owner named in the application, or their successor or assignee if you provide Notice and the Company has acknowledged the assignment. If no Owner is named on the application, the Annuitant will be the Owner. If Joint Owners are named, all references to Owner shall mean the Joint Owners. The Joint Owner must be the Owner’s spouse.

Participation Rate: A percentage that is multiplied by any positive Index Change, after the application of the Cap Rate, to calculate the Segment Credit. This percentage will not be less than 100%. There is one Participation Rate per Segment Term Period, which applies to the entire Segment Term Period.

Performance Blend Segment Option: A sub-type of the Buffer Segment Option that calculates an Aggregate Index Change using three underlying indices, rather than an Index Change based on a single underlying index.

Premium Tax: The amount of tax, if any, charged by the state or municipality in which your Contract is issued.

Purchase Payment: The amount you pay to us under your Contract, as shown on the Contract schedule. The Purchase Payment is due on the Contract Date. We may limit the amount of Purchase Payment that we will accept for your Contract.

Qualified Contract: A Contract that qualifies for special tax benefits under the Internal Revenue Code, such as a Section 408(b) Individual Retirement Annuity.

Qualified Care Facility: A facility licensed and operated as a Convalescent Care Facility, Hospice Facility or Hospital.

Reference Index: The index or indices used in the calculation of the Segment Credit for a Segment Option.

Right to Cancel Period: The period of time you may examine your Contract after you receive it. The Right to Cancel Period may vary according to state law.

Securities Act: The Securities Act of 1933, as amended.

Segment Credit: The amount we credit to each Segment Option according to the terms of the Segment Option. Segment Credits are credited to Fixed Segment Options daily based on the Annual Interest Rate. Segment Credits on Fixed Segment Options cannot be negative. Segment Credits are credited to Index-Linked Segment Options on the Segment End Date based on the performance of the Reference Index subject to the applicable Cap Rate, Participation Rate, and Floor Rate or Buffer Rate. Segment Credits on Index-Linked Segment Options may be negative amounts, which will reduce the Segment Value.

Segment End Date: The last day of a Segment Term Period. The Segment Credit for Index-Linked Segment Options is calculated and applied to the Segment Value on the Segment End Date. The next Segment Start Date coincides with the Segment End Date.

Segment Fee: An annualized rate that is assessed daily as a percentage of the Segment Fee Base on Index-Linked Segment Options. The Segment Fee amount for that Segment Option is then deducted daily from that Segment Option’s Segment Value during the Accumulation Phase. The Segment Fee will never reduce the Segment Value below zero. The Segment Fee does not apply to Fixed Segment Options.

Segment Fee Base: The initial Segment Fee Base for each Segment Option during each Segment Term Period is the Segment Value on the Segment Start Date. The Segment Fee Base on any other day in the Segment Term Period is the Segment Value on the Segment Start Date less any Withdrawals deducted from the Segment Option through the prior Business Day. We use the Segment Fee Base to determine the Segment Fee amount we will deduct from that Segment Option’s Segment Value.

Segment Options: Segment Options include Floor Segment Options, Buffer Segment Options and Fixed Segment Options available under your Contract. Each Segment Option will have a Segment Term Period. Each Floor or Buffer Segment Option (Index-Linked Segment Options) will also have a Reference Index, a Cap Rate, a Participation Rate, a Floor Rate or Buffer Rate, as applicable, and will be subject to a Segment Fee. The Performance Blend Segment Option will also have Index Allocation Percentages. The Segment Options available on the first Segment Start Date following your Contract Date will be shown on the Contract schedule.

Segment Interim Value: The Segment Value adjusted for any applicable Equity Adjustment and Interest Adjustment.

Segment Start Date: The first date of a Segment Term Period.

Segment Term Period: The Segment Term Period for each Segment Option will be shown on the Contract schedule. The Segment Term Period ends on the Segment End Date. Upon expiration of each Segment Term Period, a new Segment Term Period will begin. Please see the section “Setting Your Segment Start and End Date” for further details.

Segment Value: On the initial Segment Start Date, the Segment Value is equal to the portion of the Purchase Payment plus any Holding Account interest allocated to the Segment Option. On any other day, the Segment Value is equal to the Segment Value on the Segment Start Date decreased by any Segment Fee amounts applied to that Segment Option since the Segment Start Date, increased by Segment Credits applied to the Segment Option, increased by amounts transferred from another Segment Option, decreased by amounts transferred into another Segment Option, and decreased by Withdrawals from the Segment Option. Segment Credits are applied daily to the Fixed Segment Option and are applied to Index-Linked Segment Options only on the Segment End Date. Transfers between Segment Options will occur only on a Segment End Date.

Separate Account: The segregated account, established by the Company under Iowa Law in which we hold reserves for our guarantees under the Contract and our other general obligations. The portion of the assets of the Separate Account equal to the reserves and other Contract liabilities with respect to the Separate Account will not be chargeable with liabilities arising out of any other business we may conduct. As owner of the Contract, you do not participate in the performance of assets held in the Separate Account and do not have any direct claim on them. The Separate Account is not registered under the Investment Company Act of 1940.

Settlement Option: An option available under the Contract for receiving Annuity Payments, which we guarantee as to the dollar amount.

Spouses: Individuals who are recognized as legally married under Federal law.

Terminal Illness Waiver of Withdrawal Charges: The waiver of Withdrawal Charges on a Withdrawal from your Contract upon meeting certain qualification requirements.

Underlying IRA Holder: The natural person who is treated under the Internal Revenue Code as having a beneficial interest in the assets of a custodial or trusteed IRA Account.

Withdrawal: Unless otherwise specified, it is a Withdrawal of any type taken under your Contract, including a partial Withdrawal, a surrender of your Contract, payment of a Death Benefit or the application of Interim Value to a Settlement Option. Withdrawal refers to the amount of Contract Value withdrawn for such benefits prior to the application of Withdrawal Charges, Interest Adjustments, and Equity Adjustments. We do not treat the deduction of the Segment Fee amount as a Withdrawal.

Withdrawal Charge: The charge we assess when you surrender the Contract or make a partial withdrawal during the first six Contract Years. The Withdrawal Charge is assessed on the Contract Value on any amounts withdrawn. The Withdrawal Charge does not apply to the Free Withdrawal amount.

Withdrawal Charge Period: The Contract years during which you pay a Withdrawal Charge on amounts withdrawn. The Withdrawal Charge Period ends when the Withdrawal Charge Rate declines to 0% in the Withdrawal Charge Rate schedule set forth in your Contract schedule.

Withdrawal Charge Rate: The percentage used to calculate the Withdrawal Charge.

2. At a Glance Product Summary

General Product Description and Purpose

Athene® Amplify is a Single Purchase Payment Index-Linked Deferred Annuity Contract that may help you accumulate retirement savings. The Contract is intended for long term investment purposes and is designed for people who are looking for a level of protection for their principal while providing potentially higher returns than are available on traditional fixed annuities. This Contract is not intended for someone who is seeking complete protection from downside risk.

The Contract can be owned in the following ways:

| |

• | Sole Owner who is an individual or trust with a natural person as grantor. |

| |

• | Sole Owner who is an individual and his or her spouse as the Joint Owner or trust with a natural person and his or her spouse as grantors (available for Non-Qualified Contract only). |

The Contract has an Accumulation Phase and an Annuity Phase. During the Accumulation Phase, you may allocate your Contract Value to available Segment Options that offer different levels of protection against investment loss. The Annuity Phase begins when you apply the Interim Value to a Settlement Option. Please see the “Annuity Phase” section for more details on the Annuity Phase. The following is a brief description of the key features related to the Contract. See the Glossary in the preceding pages for more detailed explanations of the terms in this section.

The Company is not an investment advisor and does not provide any investment advice to you in connection with the Contract.

Premium Taxes may be applicable in certain states. Premium Tax applicability and rates vary by state and may change. We reserve the right to deduct such tax from the Purchase Payment when received or from the Contract Value of your Contract upon any Withdrawal from your Contract or upon the surrender of your Contract, the election of a Settlement Option, or the payment of a Death Benefit.

Purchase Payment

| |

• | Minimum Purchase Payment: $10,000 (amounts less than this threshold may be accepted at the sole discretion of the Company) |

| |

• | Maximum Purchase Payment: $1,000,000 (amounts exceeding this threshold may be accepted at the sole discretion of the Company) |

Issue Ages

| |

• | These issue age limitations apply to Owners (if natural persons) and Annuitants |

Segment Options

The Contract offers Floor Segment Options, Buffer Segment Options and Fixed Segment Options, which provide different levels of protection against investment losses. Each Segment Option will have a Segment Term Period. In addition, each Index-Linked Segment Option will have a Reference Index, a Cap Rate, a Participation Rate, and a Floor Rate or Buffer Rate. The Performance Blend Segment Option will also have Index Allocation Percentages. In addition, Index-Linked Segment Options will be subject to an annual fee rate, called the Segment Fee, equal to 0.95%. Segment Fees are set at issue and are guaranteed not to change for the life of the Contract. Each Fixed Segment Option will have an Annual Interest Rate. Segment Credits for Fixed Segment Options may not be negative. Segment Credits applied to the Index-Linked Segment Options on Segment End Dates may be negative if the value of the Reference Index declines.

The Floor Rate establishes the maximum amount of negative Index Change that will be used in the determination of the Segment Credit for a Floor Segment Option on a Segment End Date. For a Segment Option with a 10% Floor Rate, this means that any negative Segment Credit will not be more than 10% in a Segment Term Period. Over multiple Floor Segment Term Periods, cumulative negative Segment Credits may exceed the Floor Rate established by the Segment Option because a negative Segment Credit up to the amount of the Floor Rate may be applied on each Segment End Date.

| |

• | Buffer Segment Options - |

The Buffer Rate establishes the amount of loss attributable to negative index performance that we will absorb before we apply a negative Segment Credit to the Buffer Segment Option on a Segment End Date. A negative Segment Credit will apply for any negative Index Change or Aggregate Index Change in excess of the Buffer Rate. For example, if a Segment Option has a 10% Buffer Rate and the Index Change or Aggregate Index Change is -15%, the excess decline of 5% (-15% minus -10%) will be used to determine the Segment Credit. Theoretically, for a Segment Option with a 10% Buffer Rate, the negative Index Change or Aggregate Index Change that is used to calculate the Segment Credit may be as high as 90%, which could lead to a substantial loss of principal and previously credited Segment Credits. Consequently, selecting a Segment Option with a Buffer, rather than a Floor, will result in a larger negative Segment Credit during periods of steep declines in the stock market.

A Fixed Segment Option credits interest daily at a declared Annual Interest Rate. The daily rate is calculated as [(1+Annual Interest Rate) ^ (1/365)-1].

The following Segment Options are currently available:

|

| | | |

Segment Option | Index | Segment Term Period | Protection Level (Buffer or Floor Rate) |

Buffer Segment Options: |

1 | S&P 500® | 1-year | 10% |

2 | Russell 2000® | 1-year | 10% |

3 | MSCI EAFE | 1-year | 10% |

4 | S&P 500® | 2-year | 10% |

5 | Russell 2000® | 2-year | 10% |

6 | MSCI EAFE | 2-year | 10% |

7 | S&P 500® | 6-year | 20% |

8 | Performance Blend (S&P 500®, Russell 2000®, MSCI EAFE) | 6-year | 10% |

Floor Segment Options: |

9 | S&P 500® | 1-year | 10% |

10 | Russell 2000® | 1-year | 10% |

11 | MSCI EAFE | 1-year | 10% |

12 | S&P 500® | 2-year | 10% |

13 | Russell 2000® | 2-year | 10% |

14 | MSCI EAFE | 2-year | 10% |

Fixed Segment Options: |

15 | N/A | 1-year | N/A |

In the table above, “N/A” denotes Not Applicable.

You may elect a Segment Option with a six-year Segment Term Period only during the first Contract Year. The Performance Blend Segment Option is available only as a Buffer Segment Option with a six-year Segment Term Period. After the first six Contract Years, you will be limited to One-Year Segment Options upon renewal. Six-Year Segment Options are not available for renewal. Two-Year Segment Options are not available for renewal after the first six Contract Years.

Each Index-Linked Segment Option will have a Cap Rate and Participation Rate. The Cap Rate is the maximum positive Index Change we will use to calculate the Segment Credit on a Segment End Date. If the Index Change is positive, we will multiply the lesser of the Index Change and the Cap Rate by the Participation Rate. Each Fixed Segment Option will have an Annual Interest Rate. For the initial Segment Term Period, we will determine the Cap Rate, Participation Rate, and Annual Interest Rate for each Segment Option on the Segment Start Date. You will not know the applicable rates at the time you purchase your Contract. But if the declared Cap Rate, Participation Rate or Annual Interest Rate for a Segment Option to which you have allocated Contract Value is lower than the Bailout Rate specified in your Contract schedule, you may cancel your Contract during the first sixty (60) days after your Contract Date and receive your Purchase Payment less any Withdrawals. See the section “Initial Segment Term Period Bailout Provision” for additional information. After the initial Segment Term Period has ended, we will notify you of the Cap Rate, Participation Rate, and Annual Interest Rate for each available Segment Option at least fifteen calendar days prior to the new Segment Start Date. The

Cap Rate, Participation Rate, and Annual Interest Rate may be higher, lower, or the same as the Cap Rate, Participation Rate, and Annual Interest Rate offered during the previous Segment Term Period and may be significantly lower than the Bailout Rate provided for the first Segment Term Period, but will not be less than the Minimum Cap Rate, the Minimum Participation Rate, or the Minimum Annual Interest Rate shown for each Segment Option in the Contract schedule.

On each Segment End Date, you will have the option of transferring all or part of your Segment Value among the available Segment Options. We will send you a letter at least fifteen calendar days prior to the Segment End Date advising you that your Segment Option is expiring and stating the new Cap Rate, Participation Rate, and Annual Interest Rate, as applicable, that will be available for the next Segment Term Period. You will have the choice of continuing in the Segment Option with the new Cap Rate, Participation Rate, and Annual Interest Rate or transferring your Segment Value to another Segment Option with the same Segment Start Date. See the section “Transfers Between Segment Options by Request” for additional information. If you do not inform us that you want to move all or part of your Segment Value to another Segment Option at least two Business Days prior to the next Segment Start Date, you will stay in the current Segment Option, subject to the new Cap Rate, Participation Rate, and Annual Interest Rate, as applicable. If you do not wish to allocate your Segment Value to any available Segment Option, you may surrender the Contract for the Cash Surrender Value on any date. Such surrender would be subject to any applicable Withdrawal Charge, Interest Adjustment, and Equity Adjustment.

| |

• | Initial Segment Term Period Bailout Provision - |

For the initial Segment Term Period, if the declared Cap Rate, Participation Rate, or Annual Interest Rate for a Segment Option to which you have allocated Contract Value is less than the Bailout Rate we specified in your Contract schedule for the Segment Option, you may cancel the Contract during the first 60 days after your Contract Date and receive your Purchase Payment less any Withdrawals. No Withdrawal Charge, Interest Adjustment, or Equity Adjustment will apply if you exercise this provision.

Setting Your Segment Start and End Date

There are two dates each month when a new Segment Term Period may start. Your initial Segment Term Period will start on the 8th or 22nd day of the month, at which time your Purchase Payment plus any Holding Account interest will be allocated to the Segment Option(s) you have selected. Contracts which have been issued through the end of the Business Day prior to a scheduled Segment Start Date will participate in that Segment Start Date. Contracts which have been issued on or after a scheduled Segment Start Date will participate in the following Segment Start Date.

If the intended date for the initial Segment Start Date is not a Business Day, the Index Price from the prior Business Day will be used. If the date for the Segment End Date is not a Business Day, the Index Price from the prior Business Day will be used. The Segment End Date for maturing Segments will coincide with the next Segment Start Date. Below are some examples showing the effect holidays and weekends have on selecting the Segment Start and End Date Index Prices.

|

| | |

If Segment End Date is scheduled on a holiday: | Segment End Date Index Price will be from: | Next Segment Start Date Index Price will be from: |

Wednesday the 8th | Tuesday, the 7th | Tuesday, the 7th |

If Segment End Date is scheduled on a weekend: | Segment End Date Index Price will be from: | Next Segment Start Date Index Price will be from: |

Saturday the 22nd | Friday, the 21st | Friday, the 21st |

| | |

If initial Segment Start Date is scheduled on a holiday: | Initial Segment Start Date Index Price will be from: | |

Friday the 22nd | Thursday, the 21st | |

If initial Segment Start Date is scheduled on a weekend: | Initial Segment Start Date Index Price will be from: | |

Sunday, the 8th | Friday, the 6th | |

Accessing Your Contract Value

During the Accumulation Phase before any Death Benefit becomes payable, you may access your Contract Value by surrendering the Contract or taking a partial Withdrawal. If you surrender your Contract or if you take a partial Withdrawal in excess of the Free Withdrawal amount during the first six Contract Years, a maximum Withdrawal Charge of 8% will apply. You may request a partial Withdrawal or surrender up to 60 days in advance of the day that the partial Withdrawal or surrender will occur.

Interim Value Calculation

Any Withdrawal, including any Free Withdrawal amount, will also be subject to an Interim Value calculation comprised of two components: an Interest Adjustment and an Equity Adjustment, each of which may increase or decrease your Withdrawal proceeds. An Interest Adjustment will apply if you take a Withdrawal at any time during the first six Contract Years, including Withdrawals taken on a Segment End Date. An Equity Adjustment will apply if you take a Withdrawal from an Index-Linked Segment Option on any date other than a Segment End Date. See the “Contract Values” section for additional information about how Interim Values are calculated. Even if Segment Credits are positive, the deduction of fees and charges, including Segment Fee amounts, Withdrawal Charges, and any applicable Equity Adjustments or Interest Adjustments, may reduce your Cash Surrender Value below your Purchase Payment and previously credited Segment Credits.

Death Benefit

If an Owner dies before the Annuity Phase of the Contract, we will pay the Death Benefit. During the Withdrawal Charge Period, the Death Benefit is equal to the greater of:

| |

1. | The Purchase Payment less net proceeds from prior Withdrawals; or |

| |

2. | The Interim Value on the date of death. |

Withdrawal Charges will not be applied in determining the Death Benefit payable to your Beneficiary. After the Withdrawal Charge Period, the Death Benefit will be equal to the Interim Value on the date of death. Net proceeds from prior Withdrawals are equal to the Contract Value withdrawn after the application of Withdrawal Charges, Interest Adjustments, and Equity Adjustments. Withdrawals do not include any Segment Fee amounts.

If the Owner is changed or a new Owner is added during the Withdrawal Charge Period, the Death Benefit will be equal to the Interim Value on the date of death.

See the “Death Benefit” section for more information.

Settlement Options Description

The Annuity Phase commences when you or your designated payee begin receiving Annuity Payments under the Contract on the Annuity Date, according to the Settlement Option you select. You may select Annuity Payments based on the life of the Annuitant or Joint Annuitant, on the life subject to period certain or any other option acceptable to the Company. See the "Annuity Phase" section for information on available Settlement Options. The Annuity Phase ends when we make the last payment under your selected Settlement Option.

Right to Cancel

After you receive your Contract, you may examine it for 20 days (the "Right to Cancel Period"), or longer if required by state law (in some states, up to 30 days, or longer for replacement annuity Contracts), during which time you may cancel your Contract for any reason by Notifying us at our Administrative Office. Please see Appendix B to examine any applicable variations in your state.

If you exercise your right to cancel, the Contract will terminate and we will refund your Purchase Payment less any Withdrawals, unless applicable state or federal law requires otherwise. No Withdrawal Charge, Interest Adjustment, or Equity Adjustment will apply if you exercise your right to cancel your Contract during this period.

3. Contract Fees and Charges

You will pay the following fees and expenses when purchasing, owning, and taking a Withdrawal from the Contract.

Segment Fees

Indexed-Linked Segment Options include a Segment Fee equal to 0.95%. We deduct a Segment Fee amount daily from each Index-Linked Segment Option, starting on the Segment Start Date. The Segment Fee for a Segment Option is an annualized rate that is calculated on a daily basis as a percentage of that Segment Option’s Segment Fee Base.

On the Segment Start Date, the Segment Fee Base for a Segment Option is equal to the Segment Value of that Segment Option. For any other day during the Segment Term Period, the Segment Fee Base is equal to A-B, where:

| |

A | is the Segment Value on the Segment Start Date; and |

| |

B | is any Withdrawals deducted from the Segment Option from the Segment Start Date through the prior |

Business Day;

The Segment Fee amount deducted on any day is equal to the annualized Segment Fee rate divided by the number of calendar days in the current year of the Segment Term Period and multiplied by the Segment Fee Base on that day. For example, if you have elected a 2-Year Segment Option with a Segment Start date of February 8, 2019, the annualized rate will be divided by 365 during the first year of the Segment Term Period (from February 8, 2019 to February 8, 2020) and will be divided by 366 during the second year of the Segment Term Period (From February 8, 2020 to February 8, 2021) due to the leap year.

We begin calculating the daily Segment Fee amount on the Segment Start Date. Changes to the Segment Fee Base change the Segment Fee amount. For example, if you make a Withdrawal from a Segment Option, the Segment Fee Base and resulting Segment Fee amount for that Segment Option will decrease. We do not treat the deduction of the Segment Fee from a Segment Option as a Withdrawal in the determination of the Segment Fee Base or in the determination of the Death Benefit.

The deduction of the Segment Fee will never reduce Segment Value below zero. If the Segment Value is reduced to zero due to a Withdrawal, Transfer, or Segment Fee, we will cease the deduction of the Segment Fee from that Segment Option and no Segment Fees will accrue while the Segment Value is zero. If you chose to transfer

or allocate funds to the Segment Option for a future Segment Term Period, Segment Fees will begin being deducted based on the Segment Value on the new Segment Start Date.

The Segment Fee amount is deducted daily before any other activity is processed on the Segment Value, including the calculation of Segment Credits. If you take a Withdrawal from a Segment Option, we deduct the Segment Fee amount for that Segment Option before processing the Withdrawal. On the Annuity Date, we deduct the Segment Fee amounts for all Segment Options before determining the Interim Value that will be used to calculate the Annuity Payments. Upon the death of any Owner (or, if the Owner is a non-natural person, any Annuitant), we deduct the Segment Fee amounts for all Segment Options before calculating the Death Benefit.

The Segment Fee compensates us for all of your Contract’s benefits and certain expenses and risks associated with the Contract, including the risk that current charges are less than future contract administration costs. If the Segment Fee is less than these costs and risks, we will bear the loss. If the Segment Fee covers these benefits and risks, any excess amount is profit to us. We anticipate making a profit from this fee.

Withdrawal Charges

If, during the first six Contract Years, you surrender your Contract or make a partial Withdrawal from your Contract in excess of the Free Withdrawal amount, we will assess a Withdrawal Charge. The Withdrawal Charge offsets promotion and distribution expenses and investment risks born by the Company.

The amount of the Withdrawal Charge depends on the length of time you have owned your Contract and the amount you withdraw. The Contract provides a Free Withdrawal privilege that allows you to withdraw 10% of your Contract Value as of the previous Contract Anniversary annually without incurring a Withdrawal Charge.

|

| | | | | | | |

Contract Year | 1 | 2 | 3 | 4 | 5 | 6 | 7+ |

Withdrawal Charge Rate | 8% | 8% | 7% | 6% | 5% | 4% | 0% |

Withdrawal Charges may vary by state, please see Appendix B.

For purposes of calculating the Withdrawal Charge, we treat the Contract Year in which we receive your Purchase Payment as “Contract Year 1”.

We will deduct the Withdrawal Charge as a percentage of the Contract Value being withdrawn, excluding the Free Withdrawal amount, as applicable. The Withdrawal Charge will be calculated as the Contract Value associated with the Withdrawal multiplied by the applicable Withdrawal Charge Rate.

On surrender, you will receive the Interim Value reduced by any applicable Withdrawal Charges. Free Withdrawal amounts do not apply to surrenders. If you surrender your Contract, a Withdrawal Charge will be applied to any Free Withdrawal amounts previously taken in the same Contract Year.

We will not assess the Withdrawal Charge on:

| |

• | Free Withdrawal amounts; |

| |

• | Partial Withdrawals taken as Required Minimum Distributions under the Internal Revenue Code (see the “Required Minimum Distribution” section below); |

| |

• | Withdrawals taken after the sixth Contract Year; |

| |

• | A qualifying Withdrawal under the Confinement Waiver (see the “Confinement Waiver” section below); |

| |

• | A qualifying Withdrawal under the Terminal Illness Waiver (see the “Terminal Illness Waiver” section below); |

| |

• | The application of the Interim Value to a Settlement Option; |

| |

• | Payments during the Annuity Phase; or |

| |

• | Withdrawals taken under the initial Segment Term Period bailout provision (See the “Initial Segment Term Period Bailout Provision” section below). |

During the Accumulation Phase, you are entitled to a Free Withdrawal amount each year. We also reserve the right to waive the Withdrawal Charge in certain circumstances. For information on Free Withdrawal amounts and Withdrawal Charge waivers, see the “Contract Values” section. Any Free Withdrawal amount not used in a Contract Year may not be carried forward to a future Contract Year.

Premium Tax

Premium Tax………………………………………..3.5%

(as a percentage of the Purchase Payment)

We may be required to pay state Premium Taxes, currently ranging from 0% to 3.5%, in connection with a Purchase Payment or values under the Contract. Depending upon applicable state law, we may deduct charges for the Premium Taxes we incur with respect to your Purchase Payments, from amounts withdrawn or from the amount applied under a Settlement Option. In some states, charges for both direct Premium Taxes and retaliatory Premium Taxes may be imposed at the same or different times with respect to the same Purchase Payment, depending on applicable state law. Premium Tax is not currently deducted, but we reserve the right to do so in the future. The maximum charge we may deduct if we exercise the right in accordance with state law is currently 3.5%.

4. Contract Risk Factors

Your Contract has various risks associated with it. We list these risk factors below, as well as other important information you should know before purchasing a Contract.

Risk of Loss

Amounts allocated to the Index-Linked Segment Options will fluctuate in value based on the performance of the Reference Index. You may lose money, including your principal and previously credited Segment Credits. Such losses may be substantial, depending on the performance of the Reference Index and the Index-Linked Segment Options to which you allocate your Purchase Payment. Due to negative index performance, Segment Credits on Index-Linked Segment Options may be negative after application of the Buffer Rate or negative down to the amount of the Floor Rate, and you bear the portion of the loss that exceeds the Buffer Rate or a loss up to the amount of the Floor Rate, as applicable. The deduction of the Segment Fee will also reduce your Segment Value.

If there is a steep decline in the Reference Index, the risk of loss due to negative Segment Credits is substantially higher on a Buffer Segment Option than a Floor Segment Option where the Buffer Rate and the Floor Rate are identical. For example, if two otherwise identical Segment Options have a Buffer Rate of 10% and a Floor Rate of 10%, respectively, and the Reference Index declines by 30% during the Segment Term Period, the Segment Credit for the Buffer Segment Option will use a a rate of -20% (the excess of the 30% decline over the 10% Buffer Rate), while the rate used for the Floor Segment Option will be limited to -10% (the actual decline, up to the 10% Floor Rate). The risk of loss on the Performance Blend Segment Option may differ from Buffer Segment Options based on a single Reference Index because the Segment Credit applied on the Performance Blend Segment Option is based on the ranked and weighted performance of three indices, which may have different returns.

The Index Change or Aggregate Index Change used in the determination of Segment Credits for the Index-Linked Segment Options reflects only the difference in the value of the Reference Index on the Segment Start Date

and the Segment End Date. Therefore, the Segment Credit will be different than and could be significantly lower than the performance of the Reference Index at intermediate points during or through most of the Segment Term Period.

The risk of loss becomes greater if you take a Withdrawal or surrender the Contract. The Interest Adjustment, which applies to all Withdrawals and surrenders during the first six Contract Years, will be negative if interest rates have risen since your Contract Date. The Equity Adjustment, which applies to Withdrawals and surrenders from Index-Linked Segment Options before the Segment End Date, may be negative even when the value of the Reference Index has increased or has declined less than the Buffer Rate for a Buffer Segment Option. Similarly, the Equity Adjustment may reduce the Segment Interim Value of a Floor Segment Option by more than the applicable Floor Rate. During the first six Contract Years, the Withdrawal Charge will further reduce proceeds payable on a Withdrawal greater than the Free Withdrawal amount or on a surrender of the Contract.

Liquidity Risk

We designed the Contract to be a long-term investment, which you can use to help build and provide income for retirement. As such, it is not suitable as a short-term investment vehicle. You may withdraw up to 10% of your Contract Value annually without incurring a Withdrawal Charge; however, this amount may still be subject to an Interest Adjustment and Equity Adjustment. An Interest Adjustment will apply if you take a Withdrawal at any time during the first six Contract Years, including on a Segment End Date. An Equity Adjustment will apply if you take a Withdrawal from an Index-Linked Segment Option on any date other than a Segment End Date.

Segment Credits for Index-Linked Segment Options are credited to the Segment Value on the Segment End Date. The method we use to calculate Interim Value on Withdrawals taken from an Index-Linked Segment Option on any day other than a Segment End Date may result in an amount that is less than the amount you would receive if you waited until the Segment End Date to withdraw funds. Even if the performance of the Reference Index has been positive during the Segment Term Period, or losses are within the Buffer Rate for a Buffer Segment Option, the Interim Value adjustment may be negative until the Segment End Date. Similarly, if the Index Change is less than the Floor Rate for the Floor Segment Options, the Interim Value adjustment may be below the Floor Rate prior to the Segment End Date.

Changes to Cap Rates, Participation Rates, Buffer Rates, Floor Rates, and Annual Interest Rates

The Buffer and Floor Rates offered and the Segment Fee imposed on available Index-Linked Segment Options are stated in your Contract schedule and will not change after the Issue Date. Cap Rates, Participation Rates, and Annual Interest Rates may vary from one Segment Term Period to another. The Cap Rate may limit your participation in any increases in the underlying Reference Index associated with a Segment Option and could cause your returns to be lower than if you had invested in a mutual fund or exchange-traded fund designed to track the performance of the applicable Reference Index.

We declare a Cap Rate for each new Segment Term Period for Index-Linked Segment Options. The Cap Rate for a new Segment Term Period may be higher, lower, or equal to the Cap Rate for the current Segment Term Period. If it is lower, it will reduce the amount of positive Segment Credit you may receive. You risk the possibility that the Cap Rate declared for a new Segment Term Period will be lower than you would find acceptable.

We declare a Participation Rate for each new Segment Term Period for Index-Linked Segment Options. The Participation Rate for a new Segment Term Period may be higher, lower, or equal to the Participation Rate for the current Segment Term Period. If it is lower, it will reduce the amount of positive Segment Credit you may receive. You risk the possibility that the Participation Rate declared for a new Segment Term Period will be lower than you would find acceptable.

We declare an Annual Interest Rate for each new Segment Term Period for the Fixed Segment Options. The Annual Interest Rate for a new Segment Term Period may be higher, lower, or equal to the Annual Interest Rate for

the current Segment Term Period. If it is lower, it will reduce the amount of Segment Credit you will receive. You risk the possibility that the Annual Interest Rate declared for a new Segment Term Period will be lower than you would find acceptable.

Risks Associated with Indices

Index-Linked Segment Options do not directly participate in the returns of the underlying securities of any Reference Index and do not receive any dividends that may become payable on the underlying securities. The Index Change would be higher if the dividends from the underlying securities were included.

The historical performance of the indices does not guarantee future results. The S&P 500® Index, the Russell 2000® Index, and the MSCI EAFE Price Return Index are each comprised of a collection of equity securities. For each index, the value of the component securities is subject to market risk, or the risk that market fluctuations may cause the value of the component securities to go up or down, sometimes rapidly and unpredictably. In addition, the value of equity securities may decline for reasons directly related to the issuers of the securities.

S&P 500® Price Return Index.

The S&P 500® Index is comprised of equity securities issued by large-capitalization U.S. companies. In general, large-capitalization companies may be unable to respond quickly to new competitive challenges and may not be able to attain the high growth rate of successful smaller companies, especially during periods of economic expansion.

Russell 2000® Price Return Index.

The Russell 2000® Index is comprised of equity securities of small-capitalization U.S. companies. In general, the securities of small-capitalization companies may be more volatile and may involve more risk than the securities of larger companies.

MSCI EAFE Price Return Index.

MSCI EAFE Index is an equity index that captures large and mid-cap representation across developed markets around the world. The securities comprising the MSCI EAFE Price Return Index are subject to the risks related to investments in foreign markets (e.g. increased price volatility; changing currency exchange rates; and greater political, regulatory, and economic uncertainty). In general, foreign markets may be less liquid, more volatile, and subject to less government supervision than domestic markets.

Discontinuation or Substitution of an Index

We have the right to discontinue or substitute an existing Reference Index for a comparable index prior to the Segment End Date if:

| |

• | Any Reference Index is discontinued, |

| |

• | We are engaged in a contractual dispute with the Reference Index provider, |

| |

• | We determine that our use of the Reference Index should be discontinued because, for example, changes to the Reference Index make it impractical or expensive to purchase securities or derivatives to hedge the Reference Index, or |

| |

• | There is a substantial change in the calculation of the Reference Index, resulting in significantly different values and performance. |

Although we will attempt to choose a new index that has a similar investment objective and risk profile to the existing Reference Index, there is risk that the performance of the new index may not be as good as the performance of the existing Reference Index. As a result, funds allocated to the substituted index may earn a return that is lower than the return they would have earned if the index were not substituted. The substituted index will also

be incorporated within the Performance Blend Segment Option. If we substitute a Reference Index, we will Notify you at your last known address that we have on file, at least 30 days in advance of the substitution date.

If a Reference Index is discontinued and a similar Reference Index cannot be found, funds allocated to the discontinued Reference Index will not participate in any index performance during the period from the discontinuation until the Segment End Date.

Elimination of Segment Options After the Withdrawal Charge Period

Segment Options beyond the Withdrawal Charge Period will be limited to one-year Segment Term Periods. Segment Options with a two-year Segment Term Period expiring on or after the last day of the Withdrawal Charge Period will automatically transfer the Segment Value to the Segment Option’s one-year counterpart at the end of the Segment Term Period, unless you instruct otherwise. Segment Options with a six-year Segment Term Period are available only during the first Contract Year. If you do not request a Transfer of the Segment Value of an expiring Segment Option with a six-year Segment Term Period or withdraw the Segment Value, we will allocate the Segment Value to the Fixed Segment Option with the shortest Segment Term Period.

Our Financial Strength and Claims-Paying Ability

No company other than Athene Annuity and Life Company has any legal responsibility to pay amounts owed under the Contract. You should look to the financial strength of the Company for its claims-paying ability. See “Company Risk Factors”.

Regulatory Protection

The Company is not an investment company and is not registered as an investment company under the Investment Company Act of 1940. The protections provided to investors by that Act are not applicable to the Contract.

No Ownership of Underlying Securities

Purchasing the Contract is not equivalent to purchasing shares in a mutual fund that invests in securities comprising the indices, nor is it equivalent to directly investing in such securities. Hence, you will not be investing in the Reference Index, in any stock included in the Reference Index, in a mutual fund or exchange-traded fund that tracks the Reference Index, or any underlying securities.

The Separate Account

The Separate Account, in which we hold reserves for guarantees we provide under the Contract, is established under Iowa law. The portion of the assets of the Separate Account equal to the reserves and other Contract liabilities with respect to the separate account will not be chargeable with liabilities arising out of any other business we conduct. Contract Owners do not participate in the performance of assets held in the Separate Account and do not have any claim on such assets. The Separate Account is not registered under the Investment Company Act of 1940.

We own the assets of the Separate Account, as well as any favorable investment performance on those assets. We are obligated to pay all money we owe under the Contract. If the obligation exceeds the assets of the Separate Account, funds will be transferred to the Separate Account from our General Account. We may, as permitted by applicable State law, transfer all assets allocated to the Separate Account to our General Account.

General Account assets support guarantees under the Contract as well as our other general obligations. General Account assets are not segregated for the benefit of any particular contract or obligation. We guarantee all benefits relating to your value in the Contract, regardless of whether assets supporting it are held in the Separate Account or our General Account. You should look to the financial strength of the Company for its claims-paying ability.

Cybersecurity Risk

Because our business is highly dependent upon the effective operation of our computer systems and those of our business partners, our business is vulnerable to disruptions from utility outages and susceptible to operational and information security risks resulting from information systems failure (e.g. hardware and software malfunctions) and cyberattacks. These risks include, among other things, the theft, misuse, corruption and destruction of data maintained online or digitally, interference with or denial of service on our website, attacks on websites and other operational disruption and unauthorized release of confidential customer information. Such systems failures and cyberattacks affecting us, the indices, the underlying funds, intermediaries and other affiliated or third-party service providers may adversely affect us and your Contract Value. For instance, systems failures and cyberattacks may interfere with our processing of Contract transactions, including the processing of Transfer Requests, impact our ability to calculate Segment Values or Segment Interim Values, cause the release and possible destruction of confidential customer or business information, impede order processing, subject us and/or our service providers and intermediaries to regulatory fines, litigation, and financial losses and/or cause reputational damage. Cybersecurity risks may also impact the underlying securities in which the indices invest, which may cause the indices in your Contract to lose value. There can be no assurance that we, the indices, or our service providers will avoid losses affecting your Contract due to cyberattacks or information security breaches in the future.

5. About the Indices

S&P 500® Price Return Index

The S&P 500® Price Return Index was established by Standard & Poor’s. The S&P 500® Price Return Index includes 500 leading companies in leading industries of the US economy, capturing 75% coverage of U.S. Equities. The S&P 500® Price Return Index does not include dividends declared by any of the companies included in this Index.

S&P Dow Jones Indices LLC requires that the following disclaimer be included in this Prospectus:

The S&P 500® (the “Index”) is a product of S&P Dow Jones Indices LLC or its affiliates (“SPDJI”), and has been licensed for use by Athene Annuity and Life Company. Standard & Poor’s® and S&P 500® are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”); Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”); and these trademarks have been licensed for use by SPDJI and sublicensed for certain purposes by Athene Annuity and Life Company.

Athene Annuity and Life Company’s Products are not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, any of their respective affiliates (collectively, “S&P Dow Jones Indices”). S&P Dow Jones Indices makes no representation or warranty, express or implied, to the owners of the Athene Annuity and Life Company’s Products particularly or the ability of the S&P 500® to track general market performance. S&P Dow Jones Indices’ only relationship to Athene Annuity and Life Company with respect to the S&P 500® is the licensing of the S&P 500® and certain trademarks, service marks and/or trade names of S&P Dow Jones Indices and/or its licensors. The S&P 500® is determined, composed and calculated by S&P Dow Jones Indices without regard to Athene Annuity and Life Company or the Athene Annuity and Life Company’s Products. S&P Dow Jones Indices have no obligation to take the needs of Athene Annuity and Life Company or the owners of Athene Annuity and Life Company’s Products into consideration in determining, composing or calculating the S&P 500®. S&P Dow Jones Indices are not responsible for and have not participated in the determination of the prices, and amount of Athene Annuity and Life Company’s products or the timing of the issuance or sale of Athene Annuity and Life Company’s Products or in the determination or calculation of the equation by which Athene Annuity and Life Company’s products are to be converted into cash, surrendered or redeemed, as the case may be. S&P Dow Jones Indices have no obligation or liability in connection with the administration, marketing or trading of Athene Annuity and Life Company’s Products. There is no assurance that investment products based on the S&P 500® will accurately track index performance or provide positive investment returns. S&P Dow Jones Indices LLC is not an investment advisor.

Inclusion of a security within an index is not a recommendation by S&P Dow Jones Indices to buy, sell, or hold such security, nor is it considered to be investment advice.

S&P DOW JONES INDICES DOES NOT GUARANTEE THE ADEQUACY, ACCURACY, TIMELINESS AND/OR THE COMPLETENESS OF THE INDEX OR ANY DATA RELATED THERETO OR ANY COMMUNICATION, INCLUDING BUT NOT LIMITED TO, ORAL OR WRITTEN COMMUNICATION (INCLUDING ELECTRONIC COMMUNICATIONS) WITH RESPECT THERETO. S&P DOW JONES INDICES SHALL NOT BE SUBJECT TO ANY DAMAGES OR LIABILITY FOR ANY ERRORS, OMISSIONS, OR DELAYS THEREIN. S&P DOW JONES INDICES MAKE NO EXPRESS OR IMPLIED WARRANTIES, AND EXPRESSLY DISCLAIMS ALL WARRANTIES, OR MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE OR AS TO RESULTS TO BE OBTAINED BY ATHENE ANNUITY AND LIFE COMPANY, OWNERS OF THE ATHENE ANNUITY AND LIFE COMPANY’S PRODUCTS, OR ANY OTHER PERSON OR ENTITY FROM THE USE OF THE INDEX OR WITH RESPECT TO ANY DATA RELATED THERETO. WITHOUT LIMITING ANY OF THE FOREGOING, IN NO EVENT WHATSOEVER SHALL S&P DOW JONES INDICES BE LIABLE FOR ANY INDIRECT, SPECIAL, INCIDENTAL, PUNITIVE, OR CONSEQUENTIAL DAMAGES INCLUDING BUT NOT LIMITED TO, LOSS OF PROFITS, TRADING LOSSES, LOST TIME OR GOODWILL, EVEN IF THEY HAVE BEEN ADVISED OF THE POSSIBILITY OF SUCH DAMAGES, WHETHER IN CONTRACT, TORT, STRICT LIABILITY, OR OTHERWISE. THERE ARE NO THIRD PARTY BENEFICIARIES OF ANY AGREEMENTS OR ARRANGEMENTS BETWEEN S&P DOW JONES INDICES AND ATHENE ANNUITY AND LIFE COMPANY, OTHER THAN THE LICENSORS OF S&P DOW JONES INDICES.

Russell 2000® Price Return Index

The Russell 2000® Price Return Index was established by Russell Investments. The Russell 2000® Price Return Index measures the performance of the small-cap segment of the US equity universe. The Russell 2000® Price Return Index is a subset of the Russell 3000® Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2,000 of the smallest securities based on a combination of their market cap and current index membership. The Russell 2000® Price Return Index does not include dividends declared by any of the companies included in this index.

The LSE Group requires that the following disclosure be included in this Prospectus:

Athene® Amplify (the “Product”) has been developed solely by Athene Annuity and Life Company. The Product is not in any way connected to or sponsored, endorsed, sold or promoted by the London Stock Exchange Group plc and its group undertakings (collectively, the “LSE Group”). FTSE Russell is a trading name of certain of the LSE Group companies.

All rights in the Russell 2000 Index (the “Index”) vest in the relevant LSE Group company which owns the Index. “Russell®” and “Russell 2000®” are trade-marks of the relevant LSE Group company and are used by any other LSE Group company under license.

The Index is calculated by or on behalf of FTSE International Limited or its affiliate, agent or partner. The LSE Group does not accept any liability whatsoever to any person arising out of (a) the use of, reliance on or any error in the Index or (b) investment in or operation of the Product. The LSE Group makes no claim, prediction, warranty or representation either as to the results to be obtained from the Product or the suitability of the Index for the purpose to which it is being put by Athene Annuity and Life Company.

MSCI EAFE Price Return Index

The MSCI EAFE Price Return Index is a free float-adjusted market capitalization index that is designed to measure the equity performance of developed markets, excluding the US and Canada. As of the date of this prospectus, the MSCI EAFE consists of securities from the following 21 developed countries: Australia, Austria,

Belgium, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, and the United Kingdom. The MSCI EAFE Price Return Index does not include dividends declared by any of the companies included in this Index.

MSCI Inc. requires that the following disclosure be included in this Prospectus:

THIS PRODUCT IS NOT SPONSORED, ENDORSED, SOLD OR PROMOTED BY MSCI INC. (“MSCI”), ANY OF ITS AFFILIATES, ANY OF ITS INFORMATION PROVIDERS OR ANY OTHER THIRD PARTY INVOLVED IN, OR RELATED TO, COMPILING, COMPUTING OR CREATING ANY MSCI INDEX (COLLECTIVELY, THE “MSCI PARTIES”). THE MSCI INDEXES ARE THE EXCLUSIVE PROPERTY OF MSCI. MSCI AND THE MSCI INDEX NAMES ARE SERVICE MARK(S) OF MSCI OR ITS AFFILIATES AND HAVE BEEN LICENSED FOR USE FOR CERTAIN PURPOSES BY ATHENE ANNUITY AND LIFE COMPANY. NONE OF THE MSCI PARTIES MAKES ANY REPRESENTATION OR WARRANTY, EXPRESS OR IMPLIED, TO THE ISSUER OR OWNERS OF THIS PRODUCT OR ANY OTHER PERSON OR ENTITY REGARDING THE ADVISABILITY OF INVESTING IN PRODUCTS GENERALLY OR IN THIS PRODUCT PARTICULARLY OR THE ABILITY OF ANY MSCI INDEX TO TRACK CORRESPONDING STOCK MARKET PERFORMANCE. MSCI OR ITS AFFILIATES ARE THE LICENSORS OF CERTAIN TRADEMARKS, SERVICE MARKS AND TRADE NAMES AND OF THE MSCI INDEXES WHICH ARE DETERMINED, COMPOSED AND CALCULATED BY MSCI WITHOUT REGARD TO THIS PRODUCT OR THE ISSUER OR OWNERS OF THIS PRODUCT OR ANY OTHER PERSON OR ENTITY. NONE OF THE MSCI PARTIES HAS ANY OBLIGATION TO TAKE THE NEEDS OF THE ISSUER OR OWNERS OF THIS PRODUCT OR ANY OTHER PERSON OR ENTITY INTO CONSIDERATION IN DETERMINING, COMPOSING OR CALCULATING THE MSCI INDEXES. NONE OF THE MSCI PARTIES IS RESPONSIBLE FOR OR HAS PARTICIPATED IN THE DETERMINATION OF THE TIMING OF, PRICES AT, OR QUANTITIES OF THIS PRODUCT TO BE ISSUED OR IN THE DETERMINATION OR CALCULATION OF THE EQUATION BY OR THE CONSIDERATION INTO WHICH THIS PRODUCT IS REDEEMABLE. FURTHER, NONE OF THE MSCI PARTIES HAS ANY OBLIGATION OR LIABILITY TO THE ISSUER OR OWNERS OF THIS PRODUCT OR ANY OTHER PERSON OR ENTITY IN CONNECTION WITH THE ADMINISTRATION, MARKETING OR OFFERING OF THIS PRODUCT.

ALTHOUGH MSCI SHALL OBTAIN INFORMATION FOR INCLUSION IN OR FOR USE IN THE CALCULATION OF THE MSCI INDEXES FROM SOURCES THAT MSCI CONSIDERS RELIABLE, NONE OF THE MSCI PARTIES WARRANTS OR GUARANTEES THE ORIGINALITY, ACCURACY AND/OR THE COMPLETENESS OF ANY MSCI INDEX OR ANY DATA INCLUDED THEREIN. NONE OF THE MSCI PARTIES MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO RESULTS TO BE OBTAINED BY THE ISSUER OF THE PRODUCT, OWNERS OF THE PRODUCT, OR ANY OTHER PERSON OR ENTITY, FROM THE USE OF ANY MSCI INDEX OR ANY DATA INCLUDED THEREIN. NONE OF THE MSCI PARTIES SHALL HAVE ANY LIABILITY FOR ANY ERRORS, OMISSIONS OR INTERRUPTIONS OF OR IN CONNECTION WITH ANY MSCI INDEX OR ANY DATA INCLUDED THEREIN. FURTHER, NONE OF THE MSCI PARTIES MAKES ANY EXPRESS OR IMPLIED WARRANTIES OF ANY KIND, AND THE MSCI PARTIES HEREBY EXPRESSLY DISCLAIM ALL WARRANTIES OF MERCHANTABILITY AND FITNESS FOR A PARTICULAR PURPOSE, WITH RESPECT TO EACH MSCI INDEX AND ANY DATA INCLUDED THEREIN. WITHOUT LIMITING ANY OF THE FOREGOING, IN NO EVENT SHALL ANY OF THE MSCI PARTIES HAVE ANY LIABILITY FOR ANY DIRECT, INDIRECT, SPECIAL, PUNITIVE, CONSEQUENTIAL OR ANY OTHER DAMAGES (INCLUDING LOST PROFITS) EVEN IF NOTIFIED OF THE POSSIBILITY OF SUCH DAMAGES.