UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

Form 10-K

(Mark One)

R ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended September 30, 2011

or

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _________ to __________

Commission file number: 0-4408

RESOURCE AMERICA, INC.

(Exact name of registrant as specified in its charter)

|

Delaware

|

72-0654145

|

|

|

(State or other jurisdiction of

|

(I.R.S. Employer

|

|

|

incorporation or organization)

|

Identification No.)

|

|

One Crescent Drive, Suite 203, Navy Yard Corporate Center, Philadelphia, PA 19112

|

||

|

(Address of principal executive offices) (Zip code)

|

||

|

(215) 546-5005

|

||

|

(Registrant's telephone number, including area code)

|

||

|

Securities registered pursuant to Section 12(g) of the Act:

|

||

|

Common stock, par value $.01 per share

|

NASDAQ

|

|

|

Title of class

|

Name of exchange on which registered

|

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No R

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(a) of the Act. Yes o No R

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes R No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes R No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. R

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer

|

o |

Accelerated filer

|

x | |

|

Non-accelerated filer

|

o |

(Do not check if a smaller reporting company)

|

Smaller reporting company

|

o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No R

The aggregate market value of the voting common equity held by non-affiliates of the registrant, based on the closing price of such stock on the last business day of the registrant’s most recently completed second fiscal quarter (March 31, 2011) was approximately $36,833,000.

The number of outstanding shares of the registrant’s common stock on December 1, 2011 was 19,504,693 shares.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s proxy statement to be filed with the Commission in connection with the 2012 Annual Meeting of Stockholders

are incorporated by reference in Part III of this Form 10-K.

RESOURCE AMERICA, INC. AND SUBSIDIARIES

ON FORM 10-K

|

Page

|

|||

|

PART I

|

|||

|

Item 1:

|

3

|

||

|

Item 1A:

|

10

|

||

|

Item 1B:

|

14

|

||

|

Item 2:

|

14

|

||

|

Item 3:

|

15

|

||

|

Item 4:

|

15

|

||

|

PART II

|

|||

|

Item 5:

|

15

|

||

|

Item 6:

|

18

|

||

|

Item 7:

|

19

|

||

|

Item 7A:

|

44

|

||

|

Item 8:

|

45

|

||

|

Item 9:

|

99

|

||

|

Item 9A:

|

99

|

||

|

Item 9B:

|

101

|

||

|

PART III

|

|||

|

Item 10:

|

101

|

||

|

Item 11:

|

101

|

||

|

Item 12:

|

101

|

||

|

Item 13:

|

101

|

||

|

Item 14:

|

101

|

||

|

PART IV

|

|||

|

Item 15:

|

102

|

||

|

104

|

|||

PART I

|

ITEM 1.

|

This report contains certain forward-looking statements. Forward-looking statements relate to expectations, beliefs, projections, future plans and strategies, anticipated events or trends and similar expressions concerning matters that are not historical facts. In some cases, you can identify forward-looking statements by terms such as “anticipate,” “believe,” “could,” “estimate,” “expects,” “intend,” “may,” “plan,” “potential,” “project,” “should,” “will” and “would” or the negative of these terms or other comparable terminology. Such statements are subject to the risks and uncertainties more particularly described in Item 1A, under the caption “Risk Factors.” These risks and uncertainties could cause actual results and financial position to differ materially from those anticipated in such statements. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. We undertake no obligation to publicly revise or update these forward-looking statements to reflect events or circumstances after the date of this report, except as may be required under applicable law. We make references to the fiscal years ended September 30, 2011, 2010 and 2009 as fiscal 2011, fiscal 2010 and fiscal 2009, respectively.

General

We are a specialized asset management company that uses industry specific expertise to evaluate, originate, service and manage investment opportunities through our real estate, commercial finance and financial fund management subsidiaries. As a specialized asset manager, we seek to develop investment funds for outside investors for which we provide asset management services, typically under long-term management arrangements either through a contract with, or as the manager or general partner of, our sponsored investment funds. We typically maintain an investment in the funds we sponsor. As of September 30, 2011, we managed $13.3 billion of assets.

We limit our fund development and management services to asset classes where we own existing operating companies or have specific expertise. We believe this strategy enhances the return on investment we can achieve for our funds. In our real estate operations, we concentrate on the ownership, operation and management of multifamily and commercial real estate and real estate mortgage loans including whole mortgage loans, first priority interests in commercial mortgage loans, known as A notes, subordinated interests in first mortgage loans, known as B notes, mezzanine loans, investments in discounted and distressed real estate loans and investments in “value-added” properties (properties which, although not distressed, need substantial improvements to reach their full investment potential). In our commercial finance operations, we have focused on originating small and middle-ticket equipment leases and commercial loans secured by business-essential equipment, including technology, commercial and industrial equipment and medical equipment. In our financial fund management operations, we concentrate on trust preferred securities of banks, bank holding companies, insurance companies and other financial companies, bank loans and asset-backed securities, or ABS.

In January 2011, we contributed the leasing origination and servicing business platform of LEAF Financial Corporation, or LEAF Financial, into a new subsidiary, LEAF Commercial Capital, Inc., or LEAF, to facilitate outside investment into the leasing business platform. We obtained a contemporaneous investment in LEAF from Resource Capital Corp (NYSE: RSO), or RCC, a publicly-traded real estate investment trust, or REIT, that we manage, and a revolving securitized leasing warehouse facility with an independent third-party, Guggenheim Securities LLC and its affiliate, or Guggenheim. LEAF Financial will continue the asset management business by managing our commercial finance leasing partnerships. Subsequent to our fiscal year end, on November 16, 2011, we obtained an additional outside investment in LEAF by a third-party private equity firm, which we refer to as the November 2011 LCC Transaction. As a result of this outside investment, our equity interest in LEAF was reduced from 78.7% to 15.7% (on a fully diluted basis). Accordingly, we have determined that we no longer control LEAF and, effective with that investment, have deconsolidated it for financial reporting purposes. On a go-forward basis, our investment in LEAF will be accounted for under the equity method of accounting.

We have developed and manage public and private investment entities, REITs and, historically, collateralized debt obligation, or CDO, issuers. Our funds are marketed principally through an extensive broker-dealer/financial planner network that we have developed. During fiscal 2011, we focused on developing investment opportunities in our real estate segment, specifically for Resource Real Estate Opportunity REIT, Inc., or RRE Opportunity REIT, which is seeking to obtain up to $750.0 million in investor funding. Resource Real Estate Opportunity REIT commenced a public offering of its common stock for which we have raised $51.6 million in funds through September 30, 2011.

Assets Under Management

As of September 30, 2011 and 2010, we managed assets in the following classes for the accounts of institutional and individual investors, RCC, and for our own account (in millions):

|

September 30,

|

||||||||||||||||||||

|

September 30, 2011

|

2010

|

|||||||||||||||||||

|

Institutional and Individual Investors

|

RCC

|

Company

|

Total

|

Total

|

||||||||||||||||

|

Trust preferred securities (1)

|

$ | 3,890 | $ | − | $ | − | $ | 3,890 | $ | 4,213 | ||||||||||

|

Bank loans (1)

|

2,704 | 2,814 | − | 5,518 | 4,037 | |||||||||||||||

|

Asset-backed securities (1)

|

1,576 | − | − | 1,576 | 1,689 | |||||||||||||||

|

Real properties (2)

|

607 | 120 | 29 | 756 | 601 | |||||||||||||||

|

Mortgage and other real estate-related loans (2)

|

15 | 827 | 19 | 861 | 956 | |||||||||||||||

|

Commercial finance assets (3)

|

393 | − | 192 | 585 | 878 | |||||||||||||||

|

Private equity and other assets (1)

|

87 | 31 | − | 118 | 70 | |||||||||||||||

| $ | 9,272 | $ | 3,792 | $ | 240 | $ | 13,304 | $ | 12,444 | |||||||||||

|

(1)

|

We value these assets at their amortized cost.

|

|

(2)

|

We value our managed real estate assets as the sum of: (i) the amortized cost of our commercial real estate loans; and (ii) the book value of each of the following: (a) real estate and other assets held by our real estate investment entities, (b) our outstanding legacy loan portfolio, and (c) our interests in real estate.

|

|

(3)

|

We value our commercial finance assets as the sum of the book value of the equipment, and leases and notes financed by us.

|

Our assets under management are primarily managed through the investment entities we sponsor. The following table sets forth the number of entities we manage by operating segment, including tenant in common, or TIC, property interests:

|

CDOs

|

Limited Partnerships

|

TIC Programs

|

Other Investment Funds

|

|||||||||||||

|

As of September 30, 2011 (1)

|

||||||||||||||||

|

Financial fund management

|

37 | 13 | − | 1 | ||||||||||||

|

Real estate

|

2 | 8 | 6 | 5 | ||||||||||||

|

Commercial finance

|

− | 4 | − | 2 | ||||||||||||

| 39 | 25 | 6 | 8 | |||||||||||||

|

As of September 30, 2010 (1)

|

||||||||||||||||

|

Financial fund management

|

32 | 13 | − | − | ||||||||||||

|

Real estate

|

2 | 8 | 7 | 4 | ||||||||||||

|

Commercial finance

|

− | 4 | − | 1 | ||||||||||||

| 34 | 25 | 7 | 5 | |||||||||||||

|

(1)

|

All of our operating segments manage assets on behalf of RCC.

|

Real Estate

General. Through our real estate segment, we focus on four different areas:

|

|

●

|

the acquisition, ownership and management of portfolios of discounted real estate and real estate related debt, which we have acquired through two sponsored real estate investment entities as well as through joint ventures with institutional investors;

|

|

|

●

|

the sponsorship and management of real estate investment entities that principally invest in multifamily housing;

|

|

|

●

|

the management, principally for RCC, of general investments in commercial real estate debt, including first mortgage debt, whole loans, mortgage participations, B notes, mezzanine debt and related commercial real estate securities; and

|

|

|

●

|

to a lesser extent, the management and resolution of a portfolio of real estate loans and property interests that we acquired at various times between 1991 and 1999, which we collectively refer to as our legacy portfolio.

|

Discounted Real Estate Operations. RRE Opportunity REIT intends to purchase a diversified portfolio of U.S. commercial real estate and real estate related debt that has been significantly discounted due to the effects of economic events and high levels of leverage, including properties that may benefit from extensive renovations intended to increase their long-term values. Through September 30, 2011, RRE Opportunity REIT raised an aggregate of $64.1 million, of which $51.6 million was through its public offering, acquired one property and eight real estate loans, foreclosed on three loans, and has received a discounted settlement payment on one loan.

In September 2007, we entered into a joint venture with an institutional partner that acquired a pool of eleven mortgage loans from the United States Department of Housing and Urban Development. This portfolio was acquired at an overall discount of 51% to the approximately $75.0 million face value of the mortgage loans. Through September 30, 2011, we have sold three of the mortgages, foreclosed on the properties underlying eight of the mortgage loans and sold six of the foreclosed properties.

In May 2008, we entered into a second joint venture, structured as a credit facility, with the same institutional investor, that makes available up to $500.0 million to finance the acquisition of distressed properties and mortgage loans and that has the objective of repositioning both the directly owned properties and the properties underlying the mortgage loans to enhance their value. On December 1, 2009, we sold our interest in this joint venture to RCC at its book value, while retaining management of the assets and continue to receive fees in connection with the acquisition, investment management and disposition of new assets acquired. Through September 30, 2011, this joint venture had acquired 18 distressed loans and two properties for an aggregate of $163.7 million and has foreclosed on 10 of the loans and sold three of the properties.

We record quarterly asset management fees from our joint ventures with an institutional partner which range from 0.83% to 1% of the gross funds invested in distressed real estate loans and assets. We recognize these fees monthly.

Real Estate Investment Entities. Since 2003, we have sponsored and manage 18 real estate investment entities (two of which have since been merged into a single entity and excluding the two real estate CDOs we sponsored and manage for RCC) having raised a total of $319.3 million in investor funds. Through September 30, 2011, these entities have acquired interests in 42 multifamily apartment complexes comprising 10,734 units at a combined acquisition cost of $581.0 million, including interests owned by third parties and excluding properties sold.

We receive acquisition and debt placement fees from the investment entities in their acquisition stage. These fees, in the aggregate, have ranged from 1% to 2% of the net purchase price of properties acquired and 0.5% to 5% of the debt financing in the case of debt placement fees. In their operational stage, we receive property management fees of 4.5% to 5% of gross revenues.

Additionally, we record an annual investment management fee from our investment partnerships equal to 1% of the gross offering proceeds of each partnership for our services. We record an annual asset management fee from our TIC programs equal to 1% to 2% of the gross revenues from the property in connection with our performance of our asset management responsibilities. We record an annual asset management fee from one limited liability company equal to 1.5% of the gross revenues of the underlying properties. These investment management fees and asset management fees are recognized monthly when earned and are discounted to the extent that these fees are deferred.

Resource Capital Corp. As of September 30, 2011, our real estate operations managed approximately $827.2 million of commercial real estate loan assets, including $676.7 million held in CDOs we sponsored in which RCC holds the equity interests and $119.9 million of property interests on behalf of RCC. We discuss RCC in more detail in “− Resource Capital Corp.,” below.

Resource Residential. Our internal property management division, Resource Real Estate Management, Inc., or Resource Residential, has provided us with a source of stable revenues for our real estate operations. Furthermore, we believe that having direct management control over the properties in our investment programs has not only enabled us to enhance their profitability, but also provides us with a competitive edge in marketing our funds by distinguishing us from other sponsors of real estate investment funds. As of September 30, 2011, our property management division manages 37 fund multifamily properties in nine states, 16 distressed/value-added properties in eight states and one commercial property. In total, Resource Residential manages 54 properties in 14 states.

Legacy Portfolio of Loan and Property Interests. Between fiscal 1991 and 1999, our real estate operations focused on the purchase of commercial real estate loans at a discount to their outstanding loan balances and the appraised value of their underlying properties. Since 1999, management has focused on resolving and disposing of these assets. At September 30, 2011, the remaining legacy portfolio consisted of one loan with a book value of $933,000 and five property interests with a book value of $17.5 million.

Financial Fund Management

General. We conduct our financial fund management operations primarily through six separate operating entities:

|

|

●

|

Apidos Capital Management, LLC, or Apidos, finances, structures and manages investments in bank loans, high yield bonds and equity investments through CDO issuers, managed accounts and a credit opportunities fund;

|

|

|

●

|

Trapeza Capital Management, LLC, or TCM, a joint venture between us and an unrelated third party, originates, structures, finances and manages investments in trust preferred securities and senior debt securities of banks, bank holding companies, insurance companies and other financial companies through CDO issuers and related partnerships. TCM, together with the Trapeza CDO issuers and Trapeza partnerships, are collectively referred to as Trapeza;

|

|

|

●

|

Resource Financial Institutions Group, Inc., or RFIG, serves as the general partner for seven company-sponsored affiliated partnerships which invest in financial institutions;

|

|

|

●

|

Ischus Capital Management, LLC, or Ischus, finances, structures and manages investments in asset-backed securities, or ABS, including residential mortgage-backed securities, or RMBS, and commercial mortgage-backed securities, or CMBS;

|

|

|

●

|

Resource Capital Markets, Inc., or Resource Capital Markets, through our registered broker-dealer subsidiary, Resource Securities, Inc., or Resource Securities, (formerly Chadwick Securities, Inc.), acts as an agent in the primary and secondary markets for structured finance securities and manages accounts for institutional investors; and

|

|

|

●

|

Resource Capital Manager, Inc., or RCM, an indirect wholly-owned subsidiary, provides investment management and administrative services to RCC under a management agreement between us, RCM and RCC.

|

We derive revenues from our existing financial fund management operations through management fees. We are also entitled to receive distributions on amounts we have invested directly in CDOs or in limited partnerships we formed that purchased equity in the CDO issuers we sponsored. Our CDO management fees generally consist of base and subordinated management fees. For the Trapeza CDO issuers we sponsored and manage, we share base management fees with our co-sponsors. For CDO issuers we sponsored and manage on behalf of RCC, we receive fees directly from RCC pursuant to our management agreement in lieu of asset management fees from the CDO issuers. We describe the management fees we receive from RCC in “− Resource Capital Corp” below. Base management fees generally are a fixed percentage of the aggregate principal balance of eligible collateral held by the CDO. Our base management fees range from 0.01% to 0.25% of a managed CDO’s assets. Subordinated management fees are also a percentage of the aggregate principal balance of eligible collateral held by the CDO, and range from 0.04% to 0.40%, but typically are subordinated to debt service payments on the CDOs. The management fees are payable monthly, quarterly or semi-annually, as long as we continue to manage portfolio assets on behalf of the CDO issuer.

Additionally, we record fees for managing the assets held by the partnerships we have sponsored and for managing their general operations. These fees, which vary by limited partnership, range between 0.75% and 2.00% of the partnership capital balance.

CDOs. In our CDO management operations, we expect that we will continue to focus on managing the assets of our existing CDOs in fiscal 2012. While we will also seek opportunities to manage additional assets where we can use our existing financial fund management platform and personnel with little or no equity investment exposure, we cannot assure you that such opportunities will arise.

As of September 30, 2011, our financial fund management operations have sponsored and/or manage 37 CDO issuers (eight of which we manage on behalf of RCC) holding approximately $11.0 billion in assets as set forth in the following table:

|

Sponsor/Manager

|

Asset Class

|

Number of

CDO Issuers

|

Assets Under Management (1)

|

|||||||

|

(in millions)

|

||||||||||

|

Trapeza (2)(3)

|

Trust preferred securities

|

13 | $ | 3,890 | ||||||

|

Apidos

|

Bank loans

|

16 | 5,509 | |||||||

|

Ischus (2)

|

RMBS/CMBS/ABS

|

8 | 1,576 | |||||||

| 37 | $ | 10,975 | ||||||||

|

(1)

|

Calculated as set forth in “Assets Under Management,” above.

|

|

(2)

|

We also own a 50% interest in the general partners of the limited partnerships that own a portion of the equity interests in each of five Trapeza CDO issuers.

|

|

(3)

|

Through Trapeza, we own a 50% interest in an entity that manages 11 of the Trapeza CDO issuers and a 33.33% interest in another entity that manages two of the Trapeza CDO issuers.

|

Resource Capital Corp. As of September 30, 2011, our financial fund management operations manage $2.8 billion of bank loans on behalf of RCC, of which $2.6 billion are in Apidos CDOs we sponsored and manage and of which RCC holds the equity interests in three of these CDOs. We discuss RCC in more detail in “ − Resource Capital Corp.,” below.

In October 2011, on behalf of RCC, we closed Apidos CLO VIII, a $317.6 million collateralized loan obligation, or CLO, for which we will receive asset management fees in the future.

Company-Sponsored Partnerships. We sponsored, structured and currently manage eight investment entities for individual and institutional investors, seven of which invest in banks and other financial institutions and one of which has been organized as a credit opportunities fund. At September 30, 2011, these partnerships held $86.8 million of assets.

Resource Capital Corp.

RCC, a publicly-traded REIT that we sponsored and manage, invests in a diversified portfolio of whole loans, B notes, CMBS and other real estate-related loans and commercial finance assets. At September 30, 2011, we owned 2.5 million shares of RCC common stock, or approximately 3.2% of RCC’s outstanding common stock, and held options to acquire 2,166 shares (at an exercise price of $15.00 per share, which expire in March 2015).

We manage RCC through RCM. At September 30, 2011, we managed a total of $3.8 billion of assets on behalf of RCC. Under our management agreement with RCC, RCM receives a base management fee, incentive compensation, property management fees and a reimbursement for out-of-pocket expenses. The base management fee is 1/12th of 1.50% of RCC’s equity per month. The management agreement defines “equity” as, essentially, shareholders’ equity, subject to adjustment for non-cash equity-based compensation expense and non-recurring charges to which the parties agree. The incentive compensation is 25% of (i) the amount by which RCC’s adjusted operating earnings (as defined in the agreement) of RCC (before incentive compensation but after the base management fee) for such quarter per common share (based on the weighted average number of common shares outstanding for such quarter) exceeds (ii) an amount equal to (a) the weighted average of the price per share of RCC’s common shares in the initial offering by RCC and the prices per share of the common shares in any subsequent offerings of RCC, in each case at the time of issuance thereof, multiplied by (b) the greater of (1) 2.00% and (2) 0.50% plus one-fourth of the ten year treasury rate (as defined in the agreement) for such quarter, multiplied by the weighted average number of common shares outstanding during such quarter; provided, that the foregoing calculation of incentive compensation will be adjusted (i) to exclude events pursuant to changes in accounting principles generally accepted in the United States, or U.S. GAAP, or the application of U.S. GAAP, as well as non-recurring or unusual transactions or events, after discussion between us, RCC and the approval of a majority of RCC’s directors in the case of non-recurring or unusual transactions or events and (ii) by deducting any fees paid directly by RCC to our employees, agents and/or affiliates with respect to profits earned by a taxable REIT subsidiary of RCC (calculated as if such fees were payable quarterly) not previously used to offset incentive compensation. RCM receives at least 25% of its incentive compensation in additional shares of RCC common stock and has the option to receive more of its incentive compensation in stock under the management agreement. Beginning in February 2011, we entered into a services agreement with RCC to provide subadvisory collateral management and administrative services for five CDOs holding approximately $1.7 billion in bank loans whose management contracts RCC had acquired. In connection with the services provided, RCC will pay us 10% of all base and additional collateral management fees and 50% of all incentive collateral management fees it collects. Prior to the formation of LEAF, we also received an acquisition fee of 1% of the carrying value of the commercial finance assets we sold to RCC. For fiscal 2011, the management, incentive, servicing and acquisition fees we received from RCC across all of our operating segments were $12.3 million, or 14% of our consolidated revenues.

Commercial Finance

General. In January 2011, we formed LEAF to conduct our equipment lease origination and servicing operations and to obtain outside equity and debt financing sources. LEAF Financial retained the management of our four equipment leasing partnerships, which are subserviced by LEAF. As a result of the equity and debt financing obtained in connection with LEAF’s formation and the additional equity and debt financing obtained in November 2011 (after the end of our 2011 fiscal year), we have determined that we no longer control LEAF and, effective with that investment, have deconsolidated it for financial reporting purposes. On a go-forward basis, our investment in LEAF will be accounted for under the equity method of accounting. See “Business- General”. We retained the management of the four leasing partnerships and a 15.7% (fully diluted) equity interest in LEAF.

During fiscal 2011, we originated $105.8 million in commercial finance assets. As of September 30, 2011, we managed a $585.4 million commercial finance portfolio, of which $389.0 million were on behalf of the four investment entities we sponsored and whose management we have retained and subserviced to LEAF.

Credit Facilities and Notes

As of September 30, 2011, we had two corporate credit facilities, one with TD Bank and the other with Republic Bank.

The TD Bank credit facility has two components, a revolving line of credit and a term note. As of September 30, 2011, we had outstanding borrowings of $7.5 million with availability of $1.5 million under the line of credit, and borrowings of $1.3 million outstanding under the term note. The current interest rate on the line and term note is, based on our election, at either (i) the prime rate of interest plus 2.25% (with a floor of 6%) or (ii) London Interbank Offered Rate, or LIBOR, plus 3% (with a floor of 6%). In addition, we have a $503,000 letter of credit outstanding, which reduces our availability on the line of credit, and for which we are charged a 5.5% fee. The line matures on August 31, 2012. In November 2011, we extended the maturity of the line of credit to August 31, 2013 and we repaid the remaining outstanding balance of the term loan. As of December 1, 2011, there was $5.3 million outstanding on the line of credit and $1.7 million of availability.

Borrowings on the credit facility and term note are secured by a first priority security interest in specified assets and guarantees by certain subsidiaries, including (i) the present and future fees and investment income earned in connection with the management of, and investments in, sponsored CDO issuers, (ii) a pledge of 18,972 shares of The Bancorp, Inc., or TBBK (NASDAQ: TBBK), common stock, and (iii) the pledge of 1,777,371 shares of RCC common stock. Availability under the facility is limited to the lesser of (a) 75% of the net present value of future management fees to be earned or (b) the maximum revolving credit facility amount. Weighted average borrowings for fiscal 2011 and 2010 were $10.1 million and $17.8 million, respectively, at a weighted average borrowing rate of 6.6% and 7.4% and an effective interest rate (inclusive of amortization of deferred issuance costs) of 10.5% and 10.7%, respectively.

The term note required monthly principal payments of $150,000 until June 2011. In June 2011, we completed the sale of a real estate asset and, as specified in the loan agreement, used $3.0 million of the proceeds to pay down principal on the term note. As a result of this paydown, the required monthly principal payments were lowered to $50,000 beginning in July 2011. Weighted average borrowings on the term note for fiscal 2011 were $1.7 million at a weighted average borrowing rate of 6.0%, and an effective interest rate (inclusive of amortization of deferred issuance costs) of 12.9%.

In February 2011, we entered into a new $3.5 million revolving credit facility with Republic First Bank. The facility bears interest at the prime rate of interest plus 1% with a floor of 4.5% and matures on December 28, 2012. The loan is secured by a pledge of 700,000 shares of RCC stock and a first priority security interest in certain real estate collateral located in Philadelphia, Pennsylvania. Availability under this facility is limited to the lesser of (a) the sum of (i) 25% of the appraised value of the real estate, based upon the most recent appraisal delivered to the bank and (ii) 100% of the cash and 75% of the market value of the pledged RCC shares held in the pledged account; and (b) 100% of the cash and 100% of the market value of the pledged RCC shares held in the pledged account. At September 30, 2011, there were no borrowings under this facility and availability was $3.2 million.

In September and October 2009, we completed a private offering to certain senior executives and shareholders with the sale of $18.8 million of 12% senior notes due in September and October 2012, or the Senior Notes, with 5-year detachable warrants to purchase 3,690,195 shares (at a weighted average exercise price of approximately $5.11 per share). The Senior Notes require quarterly payments of interest in arrears beginning December 31, 2009. The Senior Notes are unsecured, senior obligations and are junior to our existing and future secured indebtedness. We refinanced the Senior Notes in November 2011 through a partial redemption and modification. We redeemed $8.8 million of the existing notes for cash and modified $10.0 million of notes to a 9% interest rate and extended the maturity to October 2013.

Due to the November 2011 LCC Transaction and resulting deconsolidation of LEAF, the following commercial finance credit facilities that were outstanding and reflected in our consolidated balance sheet as of September 30, 2011 will no longer be included commencing with our fiscal 2012 financial statements:

|

|

●

|

a $110.0 million secured revolving facility between Guggenheim and a wholly-owned subsidiary of LEAF;

|

|

|

●

|

a $10.0 million loan to LEAF by RCC ($6.9 million was outstanding as of September 30, 2011); and

|

|

|

●

|

$75.4 million of equipment contract-backed notes issued by a subsidiary of LEAF, LEAF Receivables Funding 3, LLC, or LRF3, to provide financing for leases and loans.

|

Asset Sourcing

Real Estate. We maintain relationships with asset owners, institutions, existing partners and borrowers, who often source investment opportunities directly to us. We maintain offices in Philadelphia, New York, Denver and El Segundo, California that provide us with a national platform of acquisition and loan origination specialists that source deals from key intermediaries such as commercial real estate brokers, mortgage brokers and specialists in selling discounted and foreclosed assets. We systematically work to exchange market data and asset knowledge across the platform to provide instant market feedback on potential investments that is based on empirical data as well as on data generated by our $1.6 billion portfolio of assets under management.

Commercial Finance. All commercial finance sourcing has been the responsibility of LEAF. Although LEAF will no longer be a consolidated subsidiary effective November 2011, LEAF Financial will continue to manage our four leasing partnerships through LEAF as sub-servicer.

Employees

As of September 30, 2011, excluding our property management team, we employed 327 full-time workers, an increase of 4 from 323 employees at September 30, 2010. The following table summarizes our employees by operating segment:

|

Total

|

Real Estate

|

Financial Fund Management

|

Commercial Finance(1)

|

Corporate/

Other

|

||||||||||||||||

|

September 30, 2011

|

||||||||||||||||||||

|

Investment professionals

|

106 | 38 | 27 | 39 | 2 | |||||||||||||||

|

Other

|

221 | 18 | 12 | 152 | 39 | |||||||||||||||

| 327 | 56 | 39 | 191 | 41 | ||||||||||||||||

|

Property management

|

410 | 410 | − | − | − | |||||||||||||||

|

Total

|

737 | 466 | 39 | 191 | 41 | |||||||||||||||

|

September 30, 2010

|

||||||||||||||||||||

|

Investment professionals

|

101 | 32 | 30 | 37 | 2 | |||||||||||||||

|

Other

|

222 | 15 | 13 | 158 | 36 | |||||||||||||||

| 323 | 47 | 43 | 195 | 38 | ||||||||||||||||

|

Property management

|

333 | 333 | − | − | − | |||||||||||||||

|

Total

|

656 | 380 | 43 | 195 | 38 | |||||||||||||||

|

(1)

|

As a result of the November 2011 LCC Transaction, we will no longer have any commercial finance employees.

|

Operating Segments and Geographic Information

We provide operating segment and geographic information about foreign operations in Note 25 of the notes to our consolidated financial statements included in Item 8, “Financial Statements and Supplementary Data.” We provide additional narrative discussion of our operating segments in Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Available Information

We file annual, quarterly and current reports, proxy statements and other information with the United States Securities and Exchange Commission, or SEC. Our internet address is http://www.resourceamerica.com. We make our SEC filings available free of charge on or through our internet website as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. We are not incorporating by reference in this report any material from our website.

|

ITEM 1A.

|

You should carefully consider the following risks together with all of the other information contained in this report in evaluating our company. If any of these risks develop into actual events, our business, financial condition and results of operations could be materially adversely affected and the trading price of our common stock could decline.

Risks Related to Our Business Generally

Our business depends upon our ability to sponsor, and raise debt and equity capital for, our investment funds.

Our business as a specialized asset manager depends upon our ability to sponsor investment funds, raise sufficient equity capital and debt financing for these funds and to generate management fees by managing these funds and the assets they hold. If we are unable to raise capital or obtain financing through these funds, we will not be able to increase our assets under management and, accordingly, increase our revenues from management fees. Moreover, because many of our investment funds have limited terms, an inability to sponsor new investment funds could result in reduced assets under management and, accordingly, reduce our management fee revenues over time. Our ability to raise capital and obtain financing through these funds depends upon numerous factors, many of which are beyond our control, including:

|

|

●

|

existing capital markets conditions which may affect interest rates, asset valuation and pricing, our ability to exit and realize value from investments and returns on assets;

|

|

|

●

|

market acceptance of the types of funds we sponsor and market perceptions about the types of assets which we seek to acquire for our funds;

|

|

|

●

|

the willingness or ability of investors to invest in long-term, relatively illiquid investments of the type we sponsor;

|

|

|

●

|

the performance of our existing funds relative to market performance generally and to the performance of similar types of funds;

|

|

|

●

|

the availability of qualified personnel to manage our funds;

|

|

|

●

|

the availability of suitable investments on acceptable terms in the types of assets and other assets that we seek to acquire for our funds; and

|

|

|

●

|

interest rate changes and their effect on both the assets we seek to acquire for our funds, and the amount, cost and availability of acquisition financing.

|

Under current market conditions, our ability to raise equity capital from both retail and institutional investors may not be at the same levels that we have achieved historically. While we have sought to counteract this decline by sponsorship of RRE Opportunity REIT, we cannot assure you that it will succeed in doing so.

Declines in the market values of our investments may reduce our earnings and the availability of credit.

We classify a material portion of our assets for accounting purposes as “available-for-sale.” As a result, changes in the market values of those assets are directly charged or credited to stockholders’ equity. A decline in these values will reduce the book value of our assets. Moreover, if the decline in value of an available-for-sale asset is other-than-temporary, such decline will reduce earnings. As a result of market conditions, the market value of many of our assets has declined. We cannot assure you that there will not be further declines in the value of our assets, or that the declines will not be material.

A decline in the market value of our assets may also adversely affect us in instances where we have borrowed money based on the market value of those assets or seek new borrowings. If the market value of assets securing an existing loan declines, the lender may reduce availability (if the loan is a line of credit), require us to post additional collateral or require us to paydown the loan so that it meets specified loan to collateral value ratios. If we were unable to post the additional collateral, we could have to sell the assets under adverse market conditions which could result in losses and which could result in us failing our debt covenants. Moreover, a decline in asset values could limit our ability to obtain financing in the amounts we seek or require us to provide more collateral to secure proposed financing.

Market changes, including changes in interest rates, may reduce the value of our assets, our returns on these assets and our ability to generate and increase our management fee revenues.

Market changes, including changes in interest rates, will affect the market value of assets we hold for our own account and our returns from such assets. In general, as interest rates rise, the value of fixed-rate investments will decrease, while as interest rates fall, the return on variable rate assets will fall. In addition, changes in interest rates may affect the value and return on assets we manage for our investment funds, thereby affecting both our management fees from those funds (and, in particular, any performance-based or incentive fees) as well as our ability to sponsor additional investment funds, which, in turn, may affect our ability to generate and increase our management fee revenues.

Increases in interest rates will increase our operating costs.

As of September 30, 2011, excluding credit facilities related to our commercial finance operations, we had two corporate credit facilities that were subject to variable interest rates. We may seek to obtain other credit facilities depending upon capital markets conditions. Any facilities that we may be able to obtain may also be at variable rates. As a result, increases in interest rates on such credit facilities, to the extent they are with recourse to us and are not matched by increased interest rates or other income from the assets whose acquisition was financed by these facilities, or are not subject to effective hedging arrangements, will increase our interest costs, which would reduce our net income or cause us to sustain losses.

Changes in interest rates may impair the operating results of our investment funds and thereby impair our operating results.

The investments made by many of our funds are interest rate sensitive. As a result, changes in interest rates could reduce the value of the assets held by those funds and the returns to investors, thereby impairing our ability to raise capital (see “- Our business depends upon our ability to sponsor, and raise debt and equity capital for, our investment funds,” above), reducing the management and other fees from those funds and reducing our returns on, and the value of, amounts we have invested in those funds.

If we cannot generate sufficient cash to fund our participations in our investment funds, our ability to maintain and increase our revenues may be impaired.

We typically participate in our investment funds along with our investors, and believe that our participation enhances our ability to raise capital from investors. We typically fund our participations through cash derived from operations or from financing. If our cash from operations is insufficient to fund our participation in future investment funds we sponsor, and we cannot arrange for financing, our continuing ability to raise funds from investors and, thus, our ability to maintain and increase the revenues we receive from fund management, will be impaired.

Termination of management arrangements with one or more of our investment funds could harm our business.

We provide management services to our investment funds through management agreements, through our position as the sole or managing general partner of partnership funds, through our position as the operating manager of other fund entities, or combinations thereof. Our arrangements are long-term, and frequently have no specified termination dates. However, our management arrangements with, or our position as general partner or operating manager of, an investment fund typically may be terminated by action taken by the investors. Upon any such termination, our management fees, after payment of any termination payments required, would cease, thereby reducing our expected future revenues.

We may have difficulty managing our asset portfolios under current market conditions.

Current market conditions have increased the complexity of managing the assets held by us and our investment funds. As a result, we depend on the ability of our officers and key employees to continue to implement and improve our operational, financial and management controls, reporting systems and procedures to deal effectively with the complexity of the conditions under which we operate. We may not be able to implement improvements to our management information and control systems in an efficient or timely manner and may discover deficiencies in existing systems and controls. Consequently, we may experience strains on our administrative and operations infrastructure, increasing our costs or reducing or eliminating our profitability.

Our allowance for credit losses may not be sufficient to cover future losses.

At September 30, 2011, our allowance for possible credit losses was $10.5 million on receivables from managed entities, primarily representing 17.5% of the book value of the receivables from our commercial finance and real estate managed funds. We cannot assure you that these allowances will prove to be sufficient to cover future losses, or that any future provisions for credit losses that we may record will not be materially greater than those we have recorded to date. Losses that exceed our allowance for credit losses, or cause an increase in our provision for credit losses, could materially reduce our earnings.

Many of our assets are illiquid, and we may not be able to divest them in response to changing economic, financial and investment conditions.

Many of our assets, including those of VIEs included in our consolidated financial statements, do not have ready markets. Moreover, we believe that the market for many of these assets, particularly real estate and CDO interests, has become more limited in the past several years due to recessionary and low growth economic conditions in the United States and elsewhere. As a result, many of our portfolio assets are relatively illiquid investments. We may be unable to vary our portfolio in response to changing economic, financial and investment conditions or to sell our investments on acceptable terms should we desire or need to do so.

We are subject to substantial competition in all aspects of our business.

Our ability to sponsor investment funds depends upon our access to various distribution systems of national, regional and local securities firms, and our ability to locate and acquire appropriate assets for our investment funds. We are subject to substantial competition in each area. In the distribution area, our investment funds compete with those sponsored by other asset managers, which are being distributed through the same networks, as well as investments sponsored by the securities firms themselves. While we have been successful in maintaining access to these distribution channels, we cannot assure you that we will continue to do so. The inability to have continued access to our distribution channels could reduce the number of funds we sponsor and assets we manage, thereby impeding and possibly impairing our revenues and revenue growth.

In acquiring appropriate assets for our investment funds, we compete with numerous public and private investment entities, commercial banks, investment banks and other financial institutions, as well as industry participants, in each of our separate asset management areas. Many of our competitors are substantially larger and have considerably greater financial, technical and marketing resources than we do. Competition for desirable investments may result in higher costs and lower investment returns, and may delay our sponsorship of investment funds.

There are few economic barriers to entry in the asset management business.

Our investment funds compete against an ever-increasing number of investment and asset management products and services sponsored by investment banks, banks, insurance companies, financial services companies and others. There are few economic barriers to entry into the investment or asset management industries and, as a result, we expect that competition for access to distribution channels and appropriate assets to acquire will increase.

Our ability to realize our deferred tax asset may be reduced, which may adversely impact results of operations.

Realization of a deferred tax asset requires us to exercise significant judgment and is inherently uncertain because it requires the prediction of future occurrences. We may reduce our deferred tax asset in the future if estimates of projected income or our tax planning strategies do not support the amount of the deferred tax asset or due to unanticipated changes in future tax rates. If we determine that a valuation allowance of our deferred tax asset is necessary, we may incur a charge to earnings.

The recently enacted Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”) may be detrimental to our business.

We expect that the Dodd-Frank Act will have a significant impact on the financial services industry, and may particularly impact us with respect to increased compliance costs, hedging activities, our broker-dealer operations and, possibly, our ability to obtain financing to increase our assets under management or revenues. Because much of the Dodd-Frank Act creates a framework through which regulatory reform will be promulgated, rather than providing regulatory reform itself, we cannot predict the magnitude of the effect that the Dodd-Frank Act will ultimately have on us.

Failure to maintain adequate infrastructure could impede our productivity and growth.

Our infrastructure, excluding our technological capacity, is important to our ability to conduct our operations. Failure to maintain an adequate infrastructure and to adapt it to growth we may achieve could harm our business operations, revenue, growth and profitability.

Risks Relating to Particular Aspects of Our Real Estate, Financial Fund Management and Commercial Finance Operations

As a result of current conditions in the global credit markets, our ability to sponsor investment entities and increase our assets under management may be limited.

Our financial fund management business historically has consisted of the sponsorship and management of CDO issuers. As a result of conditions in the global credit markets, sponsorship of new CDOs was impracticable in fiscal 2009 and 2010 and was constrained significantly in fiscal 2011. Moreover, our ability to sponsor investment funds in our commercial finance and real estate segments is significantly affected by our ability to obtain financing for the funds and the assets they acquire. Although in both fiscal 2010 and 2011 we were able to obtain financing necessary for us and our investment funds, we are aware that, in general, there has been a tightening of lending standards and a consequent reduction in credit availability. We cannot assure you that we will be able to obtain new financing or refinance existing financing in the future on acceptable financial terms, or at all. An inability to obtain financing could limit or eliminate our ability to sponsor investment entities and increase our assets under management and, accordingly, impair our ability to generate asset management fees.

We typically have retained some portion or all of the equity in the CDOs we sponsored. CDO equity receives distributions from the CDO only if the CDO generates enough income to first pay the holders of the debt securities and the CDO’s expenses.

We typically have retained some portion or all of the equity interest in CDOs we sponsored either directly or through limited partnership investments. The equity is usually entitled to all of the income generated by the CDO after the CDO pays all of the interest due on the debt securities and its other expenses, and is entitled to a return on capital only when the principal amount and accrued interest of all of the debt securities has been paid. However, there will be little or no income available to the CDO equity if covenants regarding the operations of a CDO (primarily relating to the value of collateral and interest coverage) are not met, or if there are excessive payment defaults, payment deferrals or rating agency downgrades with respect to the issuers of the underlying collateral, and there may be little or no amounts available to return our capital. In that event, the value of our direct or indirect investment in the CDO’s equity, which for all CDOs was approximately $2.4 million at September 30, 2011, could decrease substantially or be eliminated. In addition, the equity securities of CDOs are generally illiquid, and because they represent a leveraged investment in the CDO’s assets, the value of the equity securities will generally have greater fluctuations than the value of the underlying collateral.

In some of our investment funds, a portion of our management fees may depend upon the performance of the fund and, as a result, our management fee income may be volatile.

As of September 30, 2011, a portion of our management fees is subordinated to the investors’ receipt of specified returns in 14 of the CDOs we manage. In addition, with respect to RCC and nine of our investment entities, we receive incentive or subordinated compensation in addition to our base management fee, depending upon whether RCC or those partnerships achieve returns above specified levels. During fiscal 2011 and 2010, we earned incentive and subordinated management fees from RCC and from 14 and 11 CDOs, respectively, which constituted 23% and 22%, respectively, of our aggregate management fee income for both periods. The continuing recessionary condition in the national economy may result in the amount of incentive or subordinated management fee income we receive being reduced or possibly eliminated, and may cause these fees to be subject to high volatility.

Our real estate investment funds hold loans in their portfolios that are subject to a higher risk of loss than conventional mortgage loans.

The real estate investment funds that we have sponsored and manage, which we refer to as our RRE Funds, and from which we derive management and other fees, typically have loans in their portfolios that differ significantly from conventional mortgage loans. In particular, these loans may:

|

|

●

|

be junior mortgage loans;

|

|

|

●

|

involve payment structures other than equal periodic payments that retire a loan over its term;

|

|

|

●

|

require the borrower to pay a large lump sum at loan maturity (which will depend upon the borrower’s ability to obtain financing or otherwise raise a substantial amount of cash at maturity); and

|

|

|

●

|

while producing income, not generate sufficient revenues to pay the full amount of debt service on the loan as originally structured.

|

As a result, these real estate loans may have a higher risk of default and loss than conventional mortgage loans, and may require the RRE Funds to become involved in expensive and time-consuming workouts, or bankruptcy, reorganization or foreclosure proceedings.

In addition, the principal or sole source of recovery for these real estate loans is typically the underlying property and, accordingly, the value of these loans, and the ability of the RRE Funds to collect loan payments will depend upon local, regional and national economic conditions, and conditions affecting the property specifically, including the cost of compliance with, and liability under environmental, health and safety laws, changes in interest rates and the availability of financing, casualty losses, the attractiveness of the property, the availability of tenants, the ability of tenants to pay rent, competition from similar properties in the area and neighborhood values. Operating and other expenses of real properties, particularly significant expenses such as real estate taxes, insurance and maintenance costs, generally do not decrease when revenues decrease and, even if revenues increase, operating and other expenses may increase faster than revenues. Accordingly, the revenues we derive from the RRE Funds may be negatively impacted.

We will likely incur losses from our retention of the management of four equipment partnership funds.

In fiscal 2010, we transferred substantially all of our commercial finance operations to LEAF and, in November 2011, as a result of the November 2011 LCC Transaction, we deconsolidated LEAF, while retaining a minority interest in it. However, we retained the obligation to manage four equipment leasing partnerships funds. In connection therewith, we have entered into a subservicing agreement with LEAF to service the leases held by these funds. Although we waived receipt of all future management fees, we are still obligated to pay subservicing fees to LEAF.

The amount of our equity investment in LEAF following the November 2011 LCC Transaction will be reduced to the extent of LEAF’s losses.

Following the November 2011 LCC Transaction and resulting deconsolidation of LEAF, the GAAP value of our retained interest in LEAF will be reduced by our equity in any losses subsequently incurred by LEAF. We anticipate that LEAF will initially incur losses while it ramps up that business.

|

ITEM 1B.

|

None

|

ITEM 2.

|

Philadelphia, Pennsylvania:

We maintain our executive and corporate offices at One Crescent Drive in the Philadelphia Navy Yard under a lease for 13,484 square feet that expires in May 2019. Certain of our financial fund management and certain real estate operations are also located in these offices. Certain of our real estate and commercial finance operations are located in another office building at One Commerce Square, 2005 Market Street, Philadelphia, Pennsylvania under a lease for 59,448 square feet that expires in August 2013. In addition, we lease 21,554 square feet of office space at 1845 Walnut Street, Philadelphia, Pennsylvania, which is primarily sublet to Atlas Energy, L.P., an affiliated entity. This lease, which expires in May 2013, is in an office building in which we own a 5% equity interest.

New York, New York:

We maintain additional executive offices in a 12,930 square foot location at 712 5th Avenue, New York, New York under a lease agreement that expires in July 2020. We sublease a portion of this office space to The Bancorp, Inc.

Other Locations:

Our commercial finance operations own a 29,500 square foot building at 1720A Crete Street, Moberly, Missouri. In addition, we maintain various office leases in the following cities: Omaha, Nebraska; El Segundo and Tustin, California; and Denver, Colorado.

We also lease office space in London, England.

As of September 30, 2011, we believe that the properties we lease are suitable for our operations and adequate for our needs.

|

ITEM 3.

|

In September 2011, First Community Bank, or First Community, filed a complaint against First Tennessee Bank and approximately thirty other defendants – investment banks, rating agencies, collateral managers, including Trapeza Capital Management, LLC, or TCM, and issuers of CDOs, including Trapeza CDO XIII, Ltd. and Trapeza CDO XIII, Inc. The complaint includes causes of action against TCM for fraud, negligent misrepresentation, violation of the Tennessee Securities Act of 1980 and unjust enrichment. First Community alleges, among other things, that it invested in certain CDOs, that the defendant rating agencies assigned inflated investment grade ratings to the CDOs, and that the defendant investment banks, collateral managers and issuers (including Trapeza), fraudulently and/or negligently made “materially false and misleading representations and omissions” that First Community relied on in investing in the CDOs, including both written representations in offering materials and unspecified oral representations. Specifically, with respect to Trapeza, First Community alleges that it purchased $20 million of notes in the D tranche of the Trapeza CDO XIII transaction from J.P. Morgan. Trapeza believes that none of First Community’s claims have merit and intends to vigorously contest this action.

We are also a party to various routine legal proceedings arising out of the ordinary course of our business. Management believes that none of these actions, individually or in the aggregate, will have a material adverse effect on our financial condition or operations.

|

ITEM 4.

|

PART II

|

ITEM 5.

|

|

|

MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES.

|

Our common stock is quoted on the NASDAQ Global Select Market under the symbol "REXI." The following table sets forth the high and low sale prices as reported by NASDAQ on a quarterly basis for our last two fiscal years:

|

As Reported

|

||||||||

|

High

|

Low

|

|||||||

|

Fiscal 2011

|

||||||||

|

Fourth Quarter

|

$ | 6.25 | $ | 4.39 | ||||

|

Third Quarter

|

$ | 6.43 | $ | 5.87 | ||||

|

Second Quarter

|

$ | 7.18 | $ | 6.18 | ||||

|

First Quarter

|

$ | 6.86 | $ | 5.75 | ||||

|

Fiscal 2010

|

||||||||

|

Fourth Quarter

|

$ | 5.68 | $ | 3.59 | ||||

|

Third Quarter

|

$ | 6.30 | $ | 3.59 | ||||

|

Second Quarter

|

$ | 5.39 | $ | 3.81 | ||||

|

First Quarter

|

$ | 5.17 | $ | 3.69 | ||||

As of December 1, 2011, there were 19,504,693 shares of common stock outstanding held by 320 holders of record.

We have paid regular quarterly cash dividends since the fourth quarter of fiscal 1995. Commencing with the dividend payable in the first quarter of fiscal 2006, we increased our quarterly dividend by 20% to $0.06 per common share and, beginning with the dividend payable in the first quarter of fiscal 2007 and continuing to the second quarter of fiscal 2009, we further increased our quarterly dividend by 17% to $0.07 per common share. In the third quarter of fiscal 2009, we reduced the dividend to $0.03 per common share, a decrease of 57%, in part due to the impact on us of the volatility and reduction in liquidity in the global credit markets. We have continued to declare a $0.03 quarterly dividend through the remainder of fiscal 2009 and for fiscal 2010 and 2011.

Until the remaining $10.0 million of outstanding Senior Notes are paid in full (due in 2013), retired or repurchased, we cannot declare or pay future quarterly cash dividends in excess of $0.03 per share without the prior approval of all the holders of the senior notes unless basic earnings per share from continuing operations from the preceding fiscal quarter exceeds $0.25 per share.

There are no restrictions imposed on the declaration of dividends under our credit facilities.

Securities Authorized for Issuance under Equity Compensation Plans

|

(a)

|

(b)

|

(c)

|

|

|

Plan category

|

Number of securities to

be issued upon exercise

of outstanding options,

warrants and rights

|

Weighted-average

exercise price of

outstanding options,

warrants and rights

|

Number of securities remaining

available for future issuance

under equity compensation plans

excluding securities reflected in

column (a)

|

|

Equity compensation plans

approved by security holders

|

2,766,337

|

$8.93

|

796,148

|

Issuer Purchases of Equity Securities

The following table provides information about purchases by us during the quarter ended September 30, 2011 of equity securities that are registered under Section 12 of the Securities Exchange Act of 1934:

Issuer Purchases of Equity Securities

|

Period

|

Total

Number of

Shares

Purchased

|

Average

Price Paid

per Share (1)

|

Total Number of Shares Purchased

as Part of

Publicly Announced

Plans or

Programs

|

Maximum Number

(or Approximate

Dollar Value) of Shares that May Yet be Purchased Under the Plans or

Programs

|

||||||||||||

|

July 1 to July 31, 2011

|

− | $ | − | − | $ | 20,000,000 | ||||||||||

|

August 1 to August 31, 2011

|

− | $ | − | − | $ | 20,000,000 | ||||||||||

|

September 1 to September 30, 2011

|

51,600 | $ | 4.67 | 51,600 | $ | 19,759,000 | ||||||||||

|

Total

|

51,600 | $ | 4.67 | 51,600 | ||||||||||||

|

(1)

|

The average price per share as reflected above includes broker fees/commissions.

|

In December 2010, the Board of Directors approved a new share repurchase program under which we may buy up to $20.0 million of our outstanding common stock. Through December 1, 2011, we have repurchased a total of 207,889 shares at an aggregate cost of $1.0 million (or an average cost of $4.73 per share) under this program. In December 2010, the Board of Directors also terminated the previous share repurchase program.

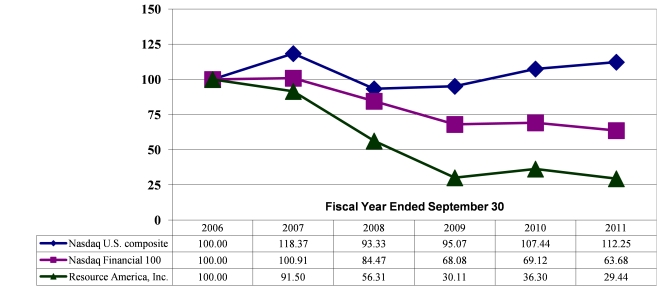

Performance Graph

The following graph assumes that $100 was invested on October 1, 2006 in our common stock, or in the indicated index, and that all cash dividends were reinvested as received. The cumulative total stockholder return on our common stock is then compared with the cumulative total return of two other stock market indices, the NASDAQ United States Composite and the NASDAQ Financial 100.

Comparison of Five Year Cumulative Total Return*

|

ITEM 6.

|

The following selected financial data should be read together with our consolidated financial statements, the notes to our consolidated financial statements and "Management's Discussion and Analysis of Financial Condition and Results of Operations" in Item 7 of this report. We derived the selected consolidated financial data for each of the fiscal years ended September 30, 2011, 2010 and 2009, and as of September 30, 2011 and 2010 from our consolidated financial statements appearing elsewhere in this report, which have been audited by Grant Thornton LLP, an independent registered public accounting firm. We derived the selected financial data for the fiscal years ended September 30, 2008 and 2007 and as of September 30, 2009, 2008 and 2007 from our consolidated internal financial statements for those periods. The following table sets forth selected operating and balance sheet data (in thousands, except per share data):

|

As of and for the Years Ended September 30,

|

||||||||||||||||||||

|

2011

|

2010

|

2009

|

2008

|

2007

|

||||||||||||||||

|

Statement of operations data:

|

||||||||||||||||||||

|

Revenues:

|

||||||||||||||||||||

|

Real estate

|

$ | 38,380 | $ | 31,911 | $ | 25,417 | $ | 31,519 | $ | 22,987 | ||||||||||

|

Financial fund management

|

25,841 | 33,140 | 33,344 | 27,536 | 63,089 | |||||||||||||||

|

Commercial finance

|

21,795 | 23,677 | 48,767 | 93,016 | 40,124 | |||||||||||||||

|

Total revenues

|

$ | 86,016 | $ | 88,728 | $ | 107,528 | $ | 152,071 | $ | 126,200 | ||||||||||

|

(Loss) income from continuing operations

|

$ | (5,227 | ) | $ | (17,297 | ) | $ | (16,090 | ) | $ | (29,949 | ) | $ | 7,211 | ||||||

|

(Loss) income from discontinued operations,

net of tax

|

(2,202 | ) | 622 | (444 | ) | (1,299 | ) | (1,558 | ) | |||||||||||

|

Net (loss) income

|

(7,429 | ) | (16,675 | ) | (16,534 | ) | (31,248 | ) | 5,653 | |||||||||||

|

Less: Net (income) loss attributable to

noncontrolling interests

|

(799 | ) | 3,224 | 1,603 | 5,005 | (1,957 | ) | |||||||||||||

|

Net (loss) income attributable to common

shareholders

|

$ | (8,228 | ) | $ | (13,451 | ) | $ | (14,931 | ) | $ | (26,243 | ) | $ | 3,696 | ||||||

|

Basic (loss) earnings per share attributable

to common shareholders:

|

||||||||||||||||||||

|

Continuing operations

|

$ | (0.31 | ) | $ | (0.74 | ) | $ | (0.78 | ) | $ | (1.40 | ) | $ | 0.30 | ||||||

|

Discontinued operations

|

(0.11 | ) | 0.03 | (0.03 | ) | (0.07 | ) | (0.09 | ) | |||||||||||

|

Net (loss) income

|

$ | (0.42 | ) | $ | (0.71 | ) | $ | (0.81 | ) | $ | (1.47 | ) | $ | 0.21 | ||||||

|

Diluted (loss) earnings per share attributable

to common shareholders:

|

||||||||||||||||||||

|

Continuing operations

|

$ | (0.31 | ) | $ | (0.74 | ) | $ | (0.78 | ) | $ | (1.40 | ) | $ | 0.27 | ||||||

|

Discontinued operations

|

(0.11 | ) | 0.03 | (0.03 | ) | (0.07 | ) | (0.08 | ) | |||||||||||

|

Net (loss) income

|

$ | (0.42 | ) | $ | (0.71 | ) | $ | (0.81 | ) | $ | (1.47 | ) | $ | 0.19 | ||||||

|

Dividends declared per common share

|

$ | 0.12 | $ | 0.09 | $ | 0.20 | $ | 0.28 | $ | 0.27 | ||||||||||

|

Amounts attributable to common shareholders:

|

||||||||||||||||||||

|

(Loss) income from continuing operations

|

$ | (6,026 | ) | $ | (14,073 | ) | $ | (14,487 | ) | $ | (24,944 | ) | $ | 5,254 | ||||||

|

Discontinued operations

|

(2,202 | ) | 622 | (444 | ) | (1,299 | ) | (1,558 | ) | |||||||||||

|

Net (loss) income

|

$ | (8,228 | ) | $ | (13,451 | ) | $ | (14,931 | ) | $ | (26,243 | ) | $ | 3,696 | ||||||

|

Balance sheet data:

|

||||||||||||||||||||

|

Total assets

|

$ | 422,506 | $ | 233,842 | $ | 373,794 | $ | 757,297 | $ | 955,328 | ||||||||||

|

Borrowings

|

$ | 222,659 | $ | 66,110 | $ | 191,383 | $ | 554,059 | $ | 706,372 | ||||||||||

|

Total equity

|

$ | 157,728 | $ | 129,084 | $ | 140,141 | $ | 146,343 | $ | 191,918 | ||||||||||

|

ITEM 7.

|

|

|

AND RESULTS OF OPERATIONS.

|

Overview

We are a specialized asset management company that uses industry specific expertise to evaluate, originate, service and manage investment opportunities through our real estate, commercial finance and financial fund management sectors. As a specialized asset manager, we seek to develop investment funds for outside investors for which we provide asset management services, typically under long-term management arrangements either through a contract with, or as the manager or general partner of, our sponsored investment funds. We typically maintain an investment in the funds we sponsor. Assets under management have grown from $7.1 billion at September 30, 2005 to $13.3 billion at September 30, 2011.

We limit our fund development and management services to asset classes where we own existing operating companies or have specific expertise. We believe this strategy enhances the return on investment we can achieve for our funds. In our real estate operations, we concentrate on the ownership, operation and management of multifamily and commercial real estate and real estate mortgage loans including whole mortgage loans, first priority interests in commercial mortgage loans, known as A notes, subordinated interests in first mortgage loans, known as B notes, mezzanine loans, investments in discounted and distressed real estate loans and investments in “value-added” properties (properties which, although not distressed, need substantial improvements to reach their full investment potential). In our commercial finance operations, we focus on originating small and middle-ticket equipment leases and commercial loans secured by business-essential equipment, including technology, commercial and industrial equipment and medical equipment. In our financial fund management operations, we concentrate on trust preferred securities of banks, bank holding companies, insurance companies and other financial companies, bank loans and ABS.

As a specialized asset manager, we are affected by conditions in the financial markets and, in particular, the continued volatility and reduced liquidity in the global credit markets which have reduced our revenues from, and the values of, many of the types of financial assets which we manage or own and have reduced our ability to access debt financing for our operations.

In our real estate segment, we have focused our efforts primarily on acquiring and managing a diversified portfolio of commercial real estate and real estate related debt that has been significantly discounted due to the effects of current economic conditions and high levels of leverage. We expect to continue to expand this business by raising investor funds through our retail broker channel for investment programs, principally through RRE Opportunity REIT. We also continue to monetize our legacy real estate portfolio. In conjunction with the June 2011 sale by the owner of a building in Washington, DC in which we owned a 25% interest, we received net proceeds of $17.4 million (including $800,000 that was released from escrow in October 2011) and recorded a gain on our investment of $8.4 million.