Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-05567

MFS INTERMEDIATE HIGH INCOME FUND

(Exact name of registrant as specified in charter)

111 Huntington Avenue, Boston, Massachusetts 02199

(Address of principal executive offices) (Zip code)

Christopher R. Bohane

Massachusetts Financial Services Company

111 Huntington Avenue

Boston, Massachusetts 02199

(Name and address of agents for service)

Registrant’s telephone number, including area code: (617) 954-5000

Date of fiscal year end: November 30

Date of reporting period: November 30, 2020

Table of Contents

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

Item 1(a):

Table of Contents

Annual Report

November 30, 2020

MFS® Intermediate High

Income Fund

CIH-ANN

Table of Contents

MANAGED DISTRIBUTION POLICY DISCLOSURE

The MFS Intermediate High Income Fund’s (the fund) Board of Trustees adopted a managed distribution policy. The fund seeks to pay monthly distributions based on an annual rate of 9.50% of the fund’s average monthly net asset value. The primary purpose of the managed distribution policy is to provide shareholders with a constant, but not guaranteed, fixed minimum rate of distribution each month. You should not draw any conclusions about the fund’s investment performance from the amount of the current distribution or from the terms of the fund’s managed distribution policy. The Board may amend or terminate the managed distribution policy at any time without prior notice to fund shareholders. The amendment or termination of the managed distribution policy could have an adverse effect on the market price of the fund’s shares.

With each distribution, the fund will issue a notice to shareholders and an accompanying press release which will provide detailed information regarding the amount and composition of the distribution and other related information. The amounts and sources of distributions reported in the notice to shareholders are only estimates and are not being provided for tax reporting purposes. The actual amounts and sources of the amounts for tax reporting purposes will depend upon the fund’s investment experience during its fiscal year and may be subject to changes based on tax regulations. The fund will send you a Form 1099-DIV for the calendar year that will tell you how to report these distributions for federal income tax purposes. Please refer to “Tax Matters and Distributions” under Note 2 of the Notes to Financial Statements for information regarding the tax character of the fund’s distributions.

Under a managed distribution policy the fund may at times distribute more than its net investment income and net realized capital gains; therefore, a portion of your distribution may result in a return of capital. A return of capital may occur, for example, when some or all of the money that you invested in the fund is paid back to you. Any such returns of capital will decrease the fund’s total assets and, therefore, could have the effect of increasing the fund’s expense ratio. In addition, in order to make the level of distributions called for under its managed distribution policy, the fund may have to sell portfolio securities at a less than opportune time. A return of capital does not necessarily reflect the fund’s investment performance and should not be confused with ‘yield’ or ‘income’. The fund’s total return in relation to changes in net asset value is presented in the Financial Highlights.

Table of Contents

MFS® Intermediate High Income Fund

New York Stock Exchange Symbol: CIF

| Contact information | back cover |

NOT FDIC INSURED • MAY LOSE VALUE • NO BANK GUARANTEE

Table of Contents

Dear Shareholders:

Markets experienced dramatic swings this year as the coronavirus pandemic brought the global economy to a standstill for several months early in the year. The speedy

development of vaccines and therapeutics later brightened the economic and market outlook, but a great deal of uncertainty remains as case counts in the United States and Europe remain very high and it is still unclear how quickly vaccines can be made widely available. In the United States, political uncertainty eased after former Vice President Joe Biden won the presidential election and the Democrats gained control of a closely divided Senate.

Global central banks have taken aggressive steps to cushion the economic and market fallout related to the virus, and governments are deploying unprecedented levels of fiscal support. Additional U.S. stimulus is anticipated with the Democrats in the

White House and holding a majority in both houses of Congress. The measures already put in place have helped build a supportive environment and are encouraging economic recovery; however, if markets disconnect from fundamentals, they can also sow the seeds of instability. In the aftermath of the crisis, societal changes may be likely as households, businesses, and governments adjust to a new reality, and any such alterations could affect the investment landscape. For investors, events such as the COVID-19 outbreak demonstrate the importance of having a deep understanding of company fundamentals, and we have built our global research platform to do just that.

At MFS®, we put our clients’ assets to work responsibly by carefully navigating the increasing complexity of our global markets and economies. Guided by our long-term philosophy and adhering to our commitment to sustainable investing, we tune out the noise and aim to uncover what we believe are the best, most durable investment opportunities in the market. Our unique global investment platform combines collective expertise, long-term discipline and thoughtful risk management to create sustainable value for investors.

Respectfully,

Michael W. Roberge

Chief Executive Officer

MFS Investment Management

January 14, 2021

The opinions expressed in this letter are subject to change and may not be relied upon for investment advice. No forecasts can be guaranteed.

1

Table of Contents

| (a) | For all securities other than those specifically described below, ratings are assigned to underlying securities utilizing ratings from Moody’s, Fitch, and Standard & Poor’s rating agencies and applying the following hierarchy: If all three agencies provide a rating, the middle rating (after dropping the highest and lowest ratings) is assigned; if two of the three agencies rate a security, the lower of the two is assigned. If none of the 3 rating agencies above assign a rating, but the security is rated by DBRS Morningstar, then the DBRS Morningstar rating is assigned. Ratings are shown in the S&P and Fitch scale (e.g., AAA). Securities rated BBB or higher are considered investment grade. All ratings are subject to change. Not Rated includes fixed income securities and fixed income derivatives that have not been rated by any rating agency. Non-Fixed Income includes equity securities (including convertible bonds and equity derivatives) and/or commodity-linked derivatives. The fund may or may not have held all of these instruments on this date. The fund is not rated by these agencies. |

| (d) | Duration is a measure of how much a bond’s price is likely to fluctuate with general changes in interest rates, e.g., if rates rise 1.00%, a bond with a 5-year duration is likely to lose about 5.00% of its value due to the interest rate move. |

2

Table of Contents

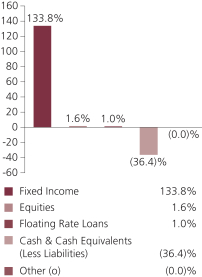

Portfolio Composition – continued

| (i) | For purposes of this presentation, the components include the value of securities, and reflect the impact of the equivalent exposure of derivative positions, if any. These amounts may be negative from time to time. Equivalent exposure is a calculated amount that translates the derivative position into a reasonable approximation of the amount of the underlying asset that the portfolio would have to hold at a given point in time to have the same price sensitivity that results from the portfolio’s ownership of the derivative contract. When dealing with derivatives, equivalent exposure is a more representative measure of the potential impact of a position on portfolio performance than value. The bond component will include any accrued interest amounts. |

| (m) | In determining each instrument’s effective maturity for purposes of calculating the fund’s dollar-weighted average effective maturity, MFS uses the instrument’s stated maturity or, if applicable, an earlier date on which MFS believes it is probable that a maturity-shortening device (such as a put, pre-refunding or prepayment) will cause the instrument to be repaid. Such an earlier date can be substantially shorter than the instrument’s stated maturity. |

| (o) | Less than 0.1%. |

Where the fund holds convertible bonds, they are treated as part of the equity portion of the portfolio.

Cash & Cash Equivalents includes any cash, investments in money market funds, short-term securities, and other assets less liabilities. Please see the Statement of Assets and Liabilities for additional information related to the fund’s cash position and other assets and liabilities.

From time to time Cash & Cash Equivalents may be negative due to borrowings for leverage transactions and/or timing of cash receipts and disbursements.

Other includes equivalent exposure from currency derivatives and/or any offsets to derivative positions and may be negative.

Percentages are based on net assets as of November 30, 2020.

The portfolio is actively managed and current holdings may be different.

3

Table of Contents

Summary of Results

For the twelve months ended November 30, 2020, shares of the MFS Intermediate High Income Fund (fund) provided a total return of 6.40%, at net asset value and a total return of 0.89%, at market value. This compares with a return of 7.17% for the fund’s benchmark, the Bloomberg Barclays U.S. High-Yield Corporate Bond 2% Issuer Capped Index.

The performance commentary below is based on the net asset value performance of the fund, which reflects the performance of the underlying pool of assets held by the fund. The total return at market value represents the return earned by owners of the shares of the fund, which are traded publicly on the exchange.

Market Environment

Markets experienced an extraordinarily sharp selloff and, in many cases, an unusually rapid recovery late in the period. Central banks and fiscal authorities undertook astonishing levels of stimulus to offset the economic effects of government-imposed social-distancing measures implemented to slow the spread of the COVID-19 virus. At this point, the global economy looks to have experienced the deepest, steepest and possibly shortest recession in the postwar period. However, the recovery remains subject to more than the usual number of uncertainties due to questions about the evolution of the virus, what its continued impact will be and how quickly vaccines to guard against it can be manufactured and distributed at scale, as well as the public’s willingness to be inoculated.

Around the world, central banks responded quickly and massively to the crisis with programs to improve liquidity and support markets. These programs proved largely successful in helping to restore market function, ease volatility and stimulate a continued market rebound. Late in the period, the US Federal Reserve adopted a new, flexible average-inflation-targeting framework, which is expected to result in the federal funds rate remaining at low levels for a longer period. In developed countries, monetary easing measures were complemented by large fiscal stimulus initiatives, although late in the period there was uncertainty surrounding the timing and scope of additional US recovery funding. Due to relatively manageable external liabilities and balances of payments in many countries, along with persistently low inflation, even emerging market countries were able to implement countercyclical policies – a departure from the usual market-dictated response to risk-off crises.

Compounding market uncertainty earlier in the pandemic was a crash in the price of crude oil due to a sharp drop in global demand and a disagreement between Saudi Arabia and Russia over production cuts, which resulted in an oil price war. The subsequent decline in prices undercut oil exporters, many of which are in emerging markets, as well as a large segment of the high-yield credit market. The OPEC+ group later agreed on output cuts, with shale oil producers in the US also decreasing production, which, along with the gradual reopening of some major economies and the resultant boost in demand, helped stabilize the price of crude oil.

As has often been the case in a crisis, market vulnerabilities have been revealed. For example, companies that have added significant leverage to their balance sheets in recent years by borrowing to fund dividend payments and stock buybacks have, in

4

Table of Contents

Management Review – continued

many cases, halted share repurchases and cut dividends, while some firms have been forced to recapitalize. Conversely, some companies find themselves flush with liquidity, having borrowed preemptively during the worst of the crisis, only to end up with excess cash on their balance sheets.

Factors Affecting Performance

Relative to the Bloomberg Barclays U.S. High-Yield Corporate Bond 2% Issuer Capped Index, the fund’s greater allocation to “BB” rated (r) bonds within the energy, capital goods and communications sectors held back performance. Bond selection within “BB” rated bonds further weighed on the fund’s relative results, led by security selection within the energy sector.

Conversely, the fund’s greater allocation to “CCC” rated bonds, particularly within the energy and capital goods sectors, contributed to relative performance. The fund’s yield curve (y) positioning, including its longer duration (d) stance, was another factor that supported relative returns as interest rates generally declined throughout the reporting period.

The fund employs leverage that has been created through the use of loan agreements with a bank. To the extent that investments are purchased through the use of leverage, the fund’s net asset value will increase or decrease at a greater rate than a comparable unleveraged fund. During the reporting period, the fund’s use of leverage was a positive contributor to relative performance.

Respectfully,

Portfolio Manager(s)

David Cole and Michael Skatrud

| (d) | Duration is a measure of how much a bond’s price is likely to fluctuate with general changes in interest rates, e.g., if rates rise 1.00%, a bond with a 5-year duration is likely to lose about 5.00% of its value. |

| (r) | Bonds rated “BBB”, “Baa”, or higher are considered investment grade; bonds rated “BB”, “Ba”, or below are considered non-investment grade. The source for bond quality ratings is Moody’s Investors Service, Standard & Poor’s, and Fitch, Inc. and are applied using the following hierarchy: If all three agencies provide a rating, the middle rating (after dropping the highest and lowest ratings) is assigned; if two of the three agencies rate a security, the lower of the two is assigned. If none of the 3 rating agencies above assign a rating, but the security is rated by DBRS Morningstar, then the DBRS Morningstar rating is assigned. Ratings are shown in the S&P and Fitch scale (e.g., AAA). For securities that are not rated by any of the three agencies, the security is considered Not Rated. |

| (y) | A yield curve graphically depicts the yields of different maturity bonds of the same credit quality and type; a normal yield curve is upward sloping, with short-term rates lower than long-term rates. |

The views expressed in this report are those of the portfolio manager(s) only through the end of the period of the report as stated on the cover and do not necessarily reflect the views of MFS or any other person in the MFS organization. These views are subject to change at any time based on market or other conditions, and MFS disclaims any responsibility to update such views. These views may not be relied upon as investment advice or an indication of trading intent on behalf of any MFS portfolio. References to specific securities are not recommendations of such securities, and may not be representative of any MFS portfolio’s current or future investments.

5

Table of Contents

PERFORMANCE SUMMARY THROUGH 11/30/20

The following chart presents the fund’s historical performance in comparison to its benchmark(s). Investment return and principal value will fluctuate, and shares, when sold, may be worth more or less than their original cost; current performance may be lower or higher than quoted. The performance shown does not reflect the deduction of taxes, if any, that a shareholder would pay on fund distributions or the sale of fund shares. Performance data shown represents past performance and is no guarantee of future results.

Price Summary for MFS Intermediate High Income Fund

| Date | Price | |||||||||||

|

Year Ended 11/30/20 |

Net Asset Value | 11/30/20 | $2.47 | |||||||||

| 11/30/19 | $2.56 | |||||||||||

| New York Stock Exchange Price | 11/30/20 | $2.47 | ||||||||||

| 2/07/20 | (high) (t) | $2.96 | ||||||||||

| 3/23/20 | (low) (t) | $1.60 | ||||||||||

| 11/30/19 | $2.70 | |||||||||||

Total Returns vs Benchmark(s)

|

Year Ended 11/30/20 |

MFS Intermediate High Income Fund at | |||||||

| New York Stock Exchange Price (r) |

0.89% | |||||||

| Net Asset Value (r) |

6.40% | |||||||

| Bloomberg Barclays U.S. High-Yield Corporate Bond 2% Issuer Capped Index (f) | 7.17% | |||||||

| (f) | Source: FactSet Research Systems Inc. |

| (r) | Includes reinvestment of all distributions. |

| (t) | For the period December 1, 2019 through November 30, 2020. |

Benchmark Definition(s)

Bloomberg Barclays U.S. High-Yield Corporate Bond 2% Issuer Capped Index (a) – a component of the Bloomberg Barclays U.S. High-Yield Corporate Bond Index, which measures performance of non-investment grade, fixed rate debt. The index limits the maximum exposure to any one issuer to 2%.

It is not possible to invest directly in an index.

| (a) | BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. |

6

Table of Contents

Performance Summary – continued

| Neither Bloomberg nor Barclays approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom, and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith. |

Notes to Performance Summary

The fund’s shares may trade at a discount or premium to net asset value. When fund shares trade at a premium, buyers pay more than the net asset value underlying fund shares, and shares purchased at a premium would receive less than the amount paid for them in the event of the fund’s concurrent liquidation.

The fund’s target annual distribution rate is calculated based on an annual rate of 9.50% of the fund’s average monthly net asset value, not a fixed share price, and the fund’s dividend amount will fluctuate with changes in the fund’s average monthly net assets.

Net asset values and performance results based on net asset value per share do not include adjustments made for financial reporting purposes in accordance with U.S. generally accepted accounting principles and may differ from amounts reported in the Statement of Assets and Liabilities or the Financial Highlights.

From time to time the fund may receive proceeds from litigation settlements, without which performance would be lower.

In accordance with Section 23(c) of the Investment Company Act of 1940, the fund hereby gives notice that it may from time to time repurchase shares of the fund in the open market at the option of the Board of Trustees and on such terms as the Trustees shall determine.

7

Table of Contents

INVESTMENT OBJECTIVE, PRINCIPAL INVESTMENT STRATEGIES, PRINCIPAL INVESTMENT TYPES AND PRINCIPAL RISKS

Investment Objective

The fund’s investment objective is to seek high current income, but may also consider capital appreciation. The fund’s objective may be changed without shareholder approval.

Principal Investment Strategies

MFS normally invests at least 80% of the fund’s net assets, including borrowings for investment purposes, in high income debt instruments.

MFS may invest the fund’s assets in other types of debt instruments and equity securities.

MFS may invest up to 100% of the fund’s assets in below investment grade quality debt instruments.

MFS may invest the fund’s assets in foreign securities.

MFS normally invests the fund’s assets across different industries and sectors, but MFS may invest a significant percentage of the fund’s assets in issuers in a single industry or sector.

The fund’s dollar-weighted average effective maturity will normally be between three and ten years. In determining an instrument’s effective maturity, MFS uses the instrument’s stated maturity or, if applicable, an earlier date on which MFS believes it is probable that a maturity-shortening device (such as a call, put, pre-refunding, prepayment or redemption provision, or an adjustable coupon) will cause the instrument to be repaid. Such an earlier date can be substantially shorter than the instrument’s stated maturity.

The fund seeks to make a monthly distribution at an annual fixed rate of 9.50% of the fund’s average monthly net asset value.

While MFS may use derivatives for any investment purpose, to the extent MFS uses derivatives, MFS expects to use derivatives primarily to increase or decrease exposure to a particular market, segment of the market, or security, to increase or decrease interest rate exposure, or as alternatives to direct investments.

MFS uses an active bottom-up investment approach to buying and selling investments for the fund. Investments are selected primarily based on fundamental analysis of individual issuers and/or instruments in light of the issuer’s financial condition and market, economic, political, and regulatory conditions. Factors considered for debt instruments may include the instrument’s credit quality, collateral characteristics, and indenture provisions, and the issuer’s management ability, capital structure, leverage, and ability to meet its current obligations. Factors considered for equity securities may include analysis of an issuer’s earnings, cash flows, competitive position, and management ability. MFS may also consider environmental, social, and governance (ESG) factors in its fundamental investment analysis. Quantitative screening tools that systematically evaluate the structure of a debt instrument and its features or the valuation, price and earnings momentum, earnings quality, and other factors of the issuer of an equity security may also be considered.

8

Table of Contents

Investment Objective, Principal Investment Strategies, Principal Investment Types and Principal Risks – continued

The fund may use leverage by borrowing up to 33 1/3% of the fund’s assets, including borrowings for investment purposes, and investing the proceeds pursuant to its investment strategies. If approved by the fund’s Board of Trustees, the fund may use leverage by other methods.

MFS may engage in active and frequent trading in pursuing the fund’s principal investment strategies.

In response to market, economic, political, or other conditions, MFS may depart from the fund’s principal investment strategies by temporarily investing for defensive purposes.

Principal Investment Types

The principal investment types in which the fund may invest are:

Debt Instruments: Debt instruments represent obligations of corporations, governments, and other entities to repay money borrowed, or other instruments believed to have debt-like characteristics. The issuer or borrower usually pays a fixed, variable, or floating rate of interest, and must repay the amount borrowed, usually at the maturity of the instrument. Debt instruments generally trade in the over-the-counter market and can be less liquid than other types of investments, particularly during adverse market and economic conditions. During certain market conditions, debt instruments in some or many segments of the debt market can trade at a negative interest rate (i.e., the price to purchase the debt instrument is more than the present value of expected interest payments and principal due at the maturity of the instrument). Some debt instruments, such as zero coupon bonds or payment-in-kind bonds, do not pay current interest. Other debt instruments, such as certain mortgage-backed securities and other securitized instruments, make periodic payments of interest and/or principal. Some debt instruments are partially or fully secured by collateral supporting the payment of interest and principal.

Corporate Bonds: Corporate bonds are debt instruments issued by corporations or similar entities.

U.S. Government Securities: U.S. Government securities are securities issued or guaranteed as to the payment of principal and interest by the U.S. Treasury, by an agency or instrumentality of the U.S. Government, or by a U.S. Government-sponsored entity. Certain U.S. Government securities are not supported as to the payment of principal and interest by the full faith and credit of the U.S. Treasury or the ability to borrow from the U.S. Treasury. Some U.S. Government securities are supported as to the payment of principal and interest only by the credit of the entity issuing or guaranteeing the security. U.S. Government securities include mortgage-backed securities and other types of securitized instruments guaranteed by the U.S. Treasury, by an agency or instrumentality of the U.S. Government, or by a U.S. Government-sponsored entity.

Foreign Government Securities: Foreign government securities are debt instruments issued, guaranteed, or supported, as to the payment of principal and interest, by foreign governments, foreign government agencies, foreign semi-governmental entities or supranational entities, or debt instruments issued by entities organized and operated

9

Table of Contents

Investment Objective, Principal Investment Strategies, Principal Investment Types and Principal Risks – continued

for the purpose of restructuring outstanding foreign government securities. Foreign government securities may not be supported as to the payment of principal and interest by the full faith and credit of the foreign government.

Floating Rate Loans: Floating rate loans are debt instruments issued by companies or other entities with interest rates that reset periodically (typically daily, monthly, quarterly, or semiannually), based on a base lending rate such as the London Interbank Bank Offered Rate (LIBOR), plus a premium. Floating rate loans are typically structured and administered by a third party that acts as agent for the lenders participating in the floating rate loan. Floating rate loans can be acquired directly through the agent, by assignment from a third party holder of the loan, or as a participation interest in a third party holder’s portion of the loan. Senior floating rate loans are secured by specific collateral of the borrower, and are senior to most other securities of the borrower (e.g., common stocks or other debt instruments) in the event of bankruptcy. Floating rate loans can be subject to restrictions on resale and can be less liquid than other types of securities.

Equity Securities: Equity securities represent an ownership interest, or the right to acquire an ownership interest, in a company or other issuer. Different types of equity securities provide different voting and dividend rights and priorities in the event of bankruptcy of the issuer. Equity securities include common stocks, preferred stocks, securities convertible into stocks, equity interests in real estate investment trusts, and depositary receipts for such securities.

Derivatives: Derivatives are financial contracts whose value is based on the value of one or more underlying indicators or the difference between underlying indicators. Underlying indicators may include a security or other financial instrument, asset, currency, interest rate, credit rating, commodity, volatility measure, or index. Derivatives often involve a counterparty to the transaction. Derivatives include futures, forward contracts, options, swaps, and certain complex structured securities.

Principal Risks

The share price of the fund will change daily based on changes in market, economic, industry, political, regulatory, geopolitical, environmental, public health, and other conditions. As with any mutual fund, the fund may not achieve its objective and/or you could lose money on your investment in the fund. An investment in the fund is not a bank deposit and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency. The significance of any specific risk to an investment in the fund will vary over time depending on the composition of the fund’s portfolio, market conditions, and other factors. You should read all of the risk information below carefully, because any one or more of these risks may result in losses to the fund.

The principal risks of investing in the fund are:

Investment Selection Risk: MFS’ investment analysis and its selection of investments may not produce the intended results and/or can lead to an investment focus that results in the fund underperforming other funds with similar investment strategies

10

Table of Contents

Investment Objective, Principal Investment Strategies, Principal Investment Types and Principal Risks – continued

and/or underperforming the markets in which the fund invests. In addition, MFS or the fund’s other service providers may experience disruptions or operating errors that could negatively impact the fund.

Debt Market Risk: Debt markets can be volatile and can decline significantly in response to, or investor perceptions of, issuer, market, economic, industry, political, regulatory, geopolitical, environmental, public health, and other conditions. These conditions can affect a single instrument, issuer, or borrower, a particular type of instrument, issuer, or borrower, a segment of the debt markets, or debt markets generally. Certain changes or events, such as political, social, or economic developments, including increasing and negative interest rates or the U.S. government’s inability at times to agree on a long-term budget and deficit reduction plan (which has in the past resulted and may in the future result in a government shutdown); market closures and/or trading halts; government or regulatory actions, including the imposition of tariffs or other protectionist actions and changes in fiscal, monetary, or tax policies; natural disasters; outbreaks of pandemic and epidemic diseases; terrorist attacks; war; and other geopolitical changes or events can have a dramatic adverse effect on debt markets and may lead to periods of high volatility and reduced liquidity in a debt market or a segment of a debt market.

Interest Rate Risk: The price of a debt instrument typically changes in response to interest rate changes. Interest rates can change in response to the supply and demand for credit, government and/or central bank monetary policy and action, inflation rates, and other factors. In general, the price of a debt instrument falls when interest rates rise and rises when interest rates fall. Interest rate risk is generally greater for instruments with longer maturities, or that do not pay current interest. In addition, short-term and long-term interest rates, and interest rates in different countries, do not necessarily move in the same direction or by the same amount. An instrument’s reaction to interest rate changes depends on the timing of its interest and principal payments and the current interest rate for each of those time periods. Instruments with floating interest rates can be less sensitive to interest rate changes. The price of an instrument trading at a negative interest rate responds to interest rate changes like other debt instruments; however, an instrument purchased at a negative interest rate is expected to produce a negative return if held to maturity. Changes in government and/or central bank monetary policy may affect the level of interest rates.

Credit Risk: The price of a debt instrument depends, in part, on the issuer’s or borrower’s credit quality or ability to pay principal and interest when due. The price of a debt instrument is likely to fall if an issuer or borrower defaults on its obligation to pay principal or interest, if the instrument’s credit rating is downgraded by a credit rating agency, or based on other changes in, or perceptions of, the financial condition of the issuer or borrower. For certain types of instruments, including derivatives, the price of the instrument depends in part on the credit quality of the counterparty to the transaction. For other types of debt instruments, including securitized instruments, the price of the debt instrument also depends on the credit quality and adequacy of the underlying assets or collateral as well as whether there is a security interest in the underlying assets or collateral. Enforcing rights, if any, against the underlying assets or collateral may be difficult.

11

Table of Contents

Investment Objective, Principal Investment Strategies, Principal Investment Types and Principal Risks – continued

Below investment grade quality debt instruments can involve a substantially greater risk of default or can already be in default, and their values can decline significantly over short periods of time. Below investment grade quality debt instruments are regarded as having predominantly speculative characteristics with respect to capacity to pay interest and principal. Below investment grade quality debt instruments tend to be more sensitive to adverse news about the issuer, or the market or economy in general, than higher quality debt instruments. The market for below investment grade quality debt instruments can be less liquid, especially during periods of recession or general market decline.

Foreign Risk: Investments in securities of foreign issuers, securities of companies with significant foreign exposure, and foreign currencies can involve additional risks relating to market, economic, industry, political, regulatory, geopolitical, environmental, public health, and other conditions. Political, social, diplomatic, and economic developments, U.S. and foreign government action such as the imposition of currency or capital blockages, controls, or tariffs, economic and trade sanctions or embargoes, security suspensions, entering or exiting trade or other intergovernmental agreements, or the expropriation or nationalization of assets in a particular country, can cause dramatic declines in certain or all securities with exposure to that country and other countries. In the event of nationalization, expropriation, or other confiscation, the fund could lose its entire foreign investment in a particular country. Economies and financial markets are interconnected, which increases the likelihood that conditions in one country or region can adversely impact issuers in different countries and regions. Less stringent regulatory, accounting, auditing, and disclosure requirements for issuers and markets are more common in certain foreign countries. Enforcing legal rights can be difficult, costly, and slow in certain foreign countries, and can be particularly difficult against foreign governments. Changes in currency exchange rates can significantly impact the financial condition of a company or other issuer with exposure to multiple countries as well as affect the U.S. dollar value of foreign currency investments and investments denominated in foreign currencies. Additional risks of foreign investments include trading, settlement, custodial, and other operational risks, and withholding and other taxes. These factors can make foreign investments, especially those tied economically to emerging and frontier markets (emerging markets that are early in their development), more volatile and less liquid than U.S. investments. In addition, foreign markets can react differently to market, economic, industry, political, regulatory, geopolitical, environmental, public health, and other conditions than the U.S. market.

Focus Risk: Issuers in a single industry, sector, country, or region can react similarly to market, currency, political, economic, regulatory, geopolitical, environmental, public health, and other conditions. These conditions include business environment changes; economic factors such as fiscal, monetary, and tax policies; inflation and unemployment rates; and government and regulatory changes. The fund’s performance will be affected by the conditions in the industries, sectors, countries and regions to which the fund is exposed.

Prepayment/Extension Risk: Many types of debt instruments, including mortgage-backed securities, securitized instruments, certain corporate bonds, and municipal housing bonds, and certain derivatives, are subject to the risk of prepayment and/or

12

Table of Contents

Investment Objective, Principal Investment Strategies, Principal Investment Types and Principal Risks – continued

extension. Prepayment occurs when unscheduled payments of principal are made or the instrument is called or redeemed prior to an instrument’s maturity. When interest rates decline, the instrument is called, or for other reasons, these debt instruments may be repaid more quickly than expected. As a result, the holder of the debt instrument may not be able to reinvest the proceeds at the same interest rate or on the same terms, reducing the potential for gain. When interest rates increase or for other reasons, these debt instruments may be repaid more slowly than expected, increasing the potential for loss. In addition, prepayment rates are difficult to predict and the potential impact of prepayment on the price of a debt instrument depends on the terms of the instrument.

Equity Market Risk: Equity markets can be volatile and can decline significantly in response to, or investor perceptions of, issuer, market, economic, industry, political, regulatory, geopolitical, environmental, public health, and other conditions. These conditions can affect a single issuer or type of security, issuers within a broad market sector, industry or geographic region, or the equity markets in general. Different parts of the market and different types of securities can react differently to these conditions. For example, the stocks of growth companies can react differently from the stocks of value companies, and the stocks of large cap companies can react differently from the stocks of small cap companies. Certain changes or events, such as political, social, or economic developments, including increasing or negative interest rates or the U.S. government’s inability at times to agree on a long-term budget and deficit reduction plan (which has in the past resulted and may in the future result in a government shutdown); market closures and/or trading halts; government or regulatory actions, including the imposition of tariffs or other protectionist actions and changes in fiscal, monetary, or tax policies; natural disasters; outbreaks of pandemic and epidemic diseases; terrorist attacks; war; and other geopolitical changes or events, can have a dramatic adverse effect on equity markets and may lead to periods of high volatility in an equity market or a segment of an equity market.

Company Risk: Changes in the financial condition of a company or other issuer, changes in specific market, economic, industry, political, regulatory, geopolitical, environmental, public health, and other conditions that affect a particular type of investment or issuer, and changes in general market, economic, political, regulatory, geopolitical, environmental, public health, and other conditions can adversely affect the prices of investments. The prices of securities of smaller, less well-known issuers can be more volatile than the prices of securities of larger issuers or the market in general.

Leveraging Risk: If the fund utilizes investment leverage, there can be no assurance that such a leveraging strategy will be successful during any period in which it is employed. The use of leverage is a speculative investment technique that results in greater volatility in the fund’s net asset value. To the extent that investments are purchased with the proceeds from the borrowings from a bank, the issuance of preferred shares, or the creation of tender option bonds, the fund’s net asset value will increase or decrease at a greater rate than a comparable unleveraged fund. If the investment income or gains earned from the investments purchased with the proceeds from the borrowings from a bank, the issuance of preferred shares, or the creation of tender option bonds, fails to cover the expenses of leveraging, the fund’s net asset

13

Table of Contents

Investment Objective, Principal Investment Strategies, Principal Investment Types and Principal Risks – continued

value is likely to decrease more quickly than if the fund weren’t leveraged. In addition, the fund’s distributions could be reduced. The fund is currently required under the 1940 Act to maintain asset coverage of 200% on outstanding preferred shares and 300% on outstanding indebtedness. The fund may be required to sell a portion of its investments at a time when it may be disadvantageous to do so in order to redeem preferred shares or to reduce outstanding indebtedness to comply with asset coverage or other restrictions including those imposed by the 1940 Act and the rating agencies that rate the preferred shares. The expenses of leveraging are paid by the holders of

common shares. Borrowings from a bank or preferred shares may have a stated maturity. If this leverage is not extended prior to maturity or replaced with the same or a different form of leverage, distributions to common shareholders may be decreased.

Certain transactions and investment strategies can result in leverage. Because movements in a fund’s share price generally correlate over time with the fund’s net asset value, the market price of a leveraged fund will also tend to be more volatile than that of a comparable unleveraged fund. The costs of an offering of preferred shares and/or borrowing program would be borne by shareholders.

Under the terms of any loan agreement or of a purchase agreement between the fund and the investor in the preferred shares, as the case may be, the fund may be required to, among other things, limit its ability to pay distributions in certain circumstances, incur additional debts, engage in certain transactions, and pledge some or all of its assets. Such agreements could limit the fund’s ability to pursue its investment strategies. The terms of any loan agreement or purchase agreement could be more or less restrictive than those described.

Managed Distribution Plan Risk: The fund may not be able to maintain a monthly distribution at an annual fixed rate of up to 9.50% of the fund’s average monthly net asset value due to many factors, including but not limited to, changes in market returns, fluctuations in market interest rates, and other factors. If income from the fund’s investments is less than the amount needed to make a monthly distribution, portfolio investments may be sold at less than opportune times to fund the distribution. Distributions that are treated as tax return of capital will have the effect of reducing the fund’s assets and could increase the fund’s expense ratio. If a portion of the fund’s distributions represents returns of capital over extended periods, the fund’s assets may be reduced over time to levels where the fund is no longer viable and might be liquidated.

Derivatives Risk: Derivatives can be highly volatile and involve risks in addition to, and potentially greater than, the risks of the underlying indicator(s). Gains or losses from derivatives can be substantially greater than the derivatives’ original cost and can sometimes be unlimited. Derivatives can involve leverage. Derivatives can be complex instruments and can involve analysis and processing that differs from that required for other investment types used by the fund. If the value of a derivative does not change as expected relative to the value of the market or other indicator to which the derivative is intended to provide exposure, the derivative may not have the effect intended. Derivatives can also reduce the opportunity for gains or result in losses by offsetting positive returns in other investments. Derivatives can be less liquid than other types of investments.

14

Table of Contents

Investment Objective, Principal Investment Strategies, Principal Investment Types and Principal Risks – continued

Anti-Takeover Provisions Risk: The fund’s declaration of trust includes provisions that could limit the ability of other persons or entities to acquire control of the fund, to convert the fund to an open-end fund, or to change the composition of the fund’s Board of Trustees. These provisions could reduce the opportunities for shareholders to sell their shares at a premium over the then-current market price.

Market Discount/Premium Risk: The market price of shares of the fund will be based on factors such as the supply and demand for shares in the market and general market, economic, industry, political or regulatory conditions. Whether shareholders will realize gains or losses upon the sale of shares of the fund will depend on the market price of shares at the time of the sale, not on the fund’s net asset value. The market price may be lower or higher than the fund’s net asset value. Shares of closed-end funds frequently trade at a discount to their net asset value.

Counterparty and Third Party Risk: Transactions involving a counterparty other than the issuer of the instrument, including clearing organizations, or a third party responsible for servicing the instrument or effecting the transaction, are subject to the credit risk of the counterparty or third party, and to the counterparty’s or third party’s ability or willingness to perform in accordance with the terms of the transaction. If a counterparty or third party fails to meet its contractual obligations, goes bankrupt, or otherwise experiences a business interruption, the fund could miss investment opportunities, lose value on its investments, or otherwise hold investments it would prefer to sell, resulting in losses for the fund.

Liquidity Risk: Certain investments and types of investments are subject to restrictions on resale, may trade in the over-the-counter market, or may not have an active trading market due to adverse market, economic, industry, political, regulatory, geopolitical, environmental, public health, and other conditions, including investors trying to sell large quantities of a particular investment or type of investment, or lack of market makers or other buyers for a particular investment or type of investment. At times, all or a significant portion of a market may not have an active trading market. Without an active trading market, it may be difficult to value, and it may not be possible to sell, these investments and the fund could miss other investment opportunities and hold investments it would prefer to sell, resulting in losses for the fund. In addition, the fund may have to sell certain of these investments at prices or times that are not advantageous in order to meet redemptions or other cash needs, which could result in dilution of remaining investors’ interests in the fund. The prices of illiquid securities may be more volatile than more liquid investments.

Defensive Investing Risk: When MFS invests defensively, different factors could affect the fund’s performance and the fund may not achieve its investment objective. In addition, the defensive strategy may not work as intended.

Frequent Trading Risk: Frequent trading increases transaction costs, which may reduce the fund’s return. Frequent trading can also result in the realization of a higher percentage of short-term capital gains and a lower percentage of long-term capital gains as compared to a fund that trades less frequently. Because short-term capital gains are distributed as ordinary income, this would generally increase your tax liability unless you hold your shares through a tax-advantaged or tax-exempt vehicle.

15

Table of Contents

The following table is furnished in response to requirements of the Securities and Exchange Commission (the “SEC”). It is designed to, among other things, illustrate the effects of leverage through the use of senior securities, as that term is defined under Section 18 of the Investment Company Act of 1940 (the “1940 Act”), on fund total return, assuming investment portfolio total returns (consisting of income and changes in the value of investments held in a fund’s portfolio) of –10%, –5%, 0%, 5% and 10%. The table below assumes the fund’s continued use of line of credit borrowings (“leverage”), as applicable, as of November 30, 2020, as a percentage of total assets (including assets attributable to such leverage), the estimated annual effective interest expense rate payable by the fund on such line of credit borrowings (based on market conditions as of November 30, 2020), and the annual return that the fund’s portfolio would need to experience (net of expenses) in order to cover such costs. The information below does not reflect the fund’s possible use of certain other forms of economic leverage through the use of other instruments or transactions not considered to be senior securities under the 1940 Act, if any.

The assumed investment portfolio returns in the table below are hypothetical figures and are not necessarily indicative of the investment portfolio returns experienced or expected to be experienced by the fund. Your actual returns may be greater or less than those appearing below. In addition, actual borrowing expenses associated with line of credit borrowings used by the fund may vary frequently and may be significantly higher or lower than the rate used for the example below.

| Line of Credit Borrowings as a Percentage of Total Assets (Including Assets Attributable to Leverage) | 27.99% | |||

| Estimated Annual Effective Rate of Interest Expense on Line of Credit Borrowings | 0.80% | |||

| Annual Return Fund Portfolio Must Experience (net of expenses) to Cover Estimated Annual Effective Interest Expense on Line of Credit Borrowings | 0.22% |

| Assumed Return on Portfolio (Net of Expenses) | -10.00% | -5.00% | 0.00% | 5.00% | 10.00% | |||||||||||||||

| Corresponding Return to Shareholder | -14.20% | -7.25% | -0.31% | 6.63% | 13.58% |

Fund total return is composed of two elements – the distributions paid by the fund to fund shareholders (the amount of which is largely determined by the net investment income of the fund after paying interest and other expenses on any line of credit borrowings and expenses on any other forms of leverage outstanding) and gains or losses on the value of the securities and other instruments the fund owns. As required by SEC rules, the table assumes that the fund is more likely to suffer capital losses than to enjoy capital appreciation. For example, to assume a total return of 0%, the fund must assume that the income it receives on its investments is entirely offset by losses in the value of those investments. The table reflects hypothetical performance of the fund’s portfolio and not the actual performance of the fund’s shares, the value of which is determined by market forces and other factors.

Should the fund elect to add additional leverage to its portfolio, any benefits of such additional leverage cannot be fully achieved until the proceeds resulting from the use of such leverage have been received by the fund and invested in accordance with the fund’s investment objectives and policies. The fund’s willingness to use additional leverage, and the extent to which leverage is used at any time, will depend on many factors.

16

Table of Contents

| Portfolio Manager | Primary Role | Since | Title and Five Year History | |||

| David Cole | Portfolio Manager |

2007 | Investment Officer of MFS; employed in the investment management area of MFS since 2004. | |||

| Michael Skatrud | Portfolio Manager |

2018 | Investment Officer of MFS; employed in the investment management area of MFS since 2013. | |||

17

Table of Contents

DIVIDEND REINVESTMENT AND CASH PURCHASE PLAN

The fund offers a Dividend Reinvestment and Cash Purchase Plan (the “Plan”) that allows common shareholders to reinvest either all of the distributions paid by the fund or only the long-term capital gains. Generally, purchases are made at the market price unless that price exceeds the net asset value (the shares are trading at a premium). If the shares are trading at a premium, purchases will be made at a price of either the net asset value or 95% of the market price, whichever is greater. You can also buy shares on a quarterly basis in any amount $100 and over. The Plan Agent will purchase shares under the Cash Purchase Plan on the 15th of January, April, July, and October or shortly thereafter.

If shares are registered in your own name, new shareholders will automatically participate in the Plan, unless you have indicated that you do not wish to participate. If your shares are in the name of a brokerage firm, bank, or other nominee, you can ask the firm or nominee to participate in the Plan on your behalf. If the nominee does not offer the Plan, you may wish to request that your shares be re-registered in your own name so that you can participate. There is no service charge to reinvest distributions, nor are there brokerage charges for shares issued directly by the fund. However, when shares are bought on the New York Stock Exchange or otherwise on the open market, each participant pays a pro rata share of the transaction expenses, including commissions. The tax status of dividends and capital gain distributions does not change whether received in cash or reinvested in additional shares – the automatic reinvestment of distributions does not relieve you of any income tax that may be payable (or required to be withheld) on the distributions.

If your shares are held directly with the Plan Agent, you may withdraw from the Plan at any time by going to the Plan Agent’s Web site at www.computershare.com/investor, by calling 1-800-637-2304 any business day from 9 a.m. to 5 p.m. Eastern time or by writing to the Plan Agent at P.O. Box 505005, Louisville, KY 40233-5005. Please have available the name of the fund and your account number. For certain types of registrations, such as corporate accounts, instructions must be submitted in writing. Please call for additional details. When you withdraw from the Plan, you can receive the value of the reinvested shares in one of three ways: your full shares will be held in your account, the Plan Agent will sell your shares and send the proceeds to you, or you may transfer your full shares to your investment professional who can hold or sell them. Additionally, the Plan Agent will sell your fractional shares and send the proceeds to you.

If you have any questions or for further information or a copy of the Plan, contact the Plan Agent Computershare Trust Company, N.A. (the Transfer Agent for the fund) at 1-800-637-2304, at the Plan Agent’s Web site at www.computershare.com/investor, or by writing to the Plan Agent at P.O. Box 505005, Louisville, KY 40233-5005.

18

Table of Contents

11/30/20

The Portfolio of Investments is a complete list of all securities owned by your fund. It is categorized by broad-based asset classes.

| Issuer | Shares/Par | Value ($) | ||||||

| Bonds - 132.0% | ||||||||

| Aerospace - 3.3% | ||||||||

| Bombardier, Inc., 7.5%, 3/15/2025 (n) | $ | 353,000 | $ | 304,462 | ||||

| Bombardier, Inc., 7.875%, 4/15/2027 (n) | 155,000 | 132,138 | ||||||

| F-Brasile S.p.A./F-Brasile U.S. LLC, 7.375%, 8/15/2026 (n) | 200,000 | 183,000 | ||||||

| Moog, Inc., 4.25%, 12/15/2027 (n) | 250,000 | 257,587 | ||||||

| TransDigm, Inc., 6.5%, 7/15/2024 | 185,000 | 187,775 | ||||||

| TransDigm, Inc., 6.25%, 3/15/2026 (n) | 200,000 | 212,000 | ||||||

| TransDigm, Inc., 6.375%, 6/15/2026 | 185,000 | 192,160 | ||||||

| TransDigm, Inc., 5.5%, 11/15/2027 | 120,000 | 123,840 | ||||||

|

|

|

|||||||

| $ | 1,592,962 | |||||||

| Automotive - 3.2% | ||||||||

| Adient Global Holdings Ltd., 4.875%, 8/15/2026 (n) | $ | 200,000 | $ | 201,690 | ||||

| Adient U.S. LLC, 7%, 5/15/2026 (n) | 20,000 | 21,650 | ||||||

| Allison Transmission, Inc., 5.875%, 6/01/2029 (n) | 125,000 | 139,375 | ||||||

| American Axle & Manufacturing, Inc., 6.25%, 3/15/2026 | 90,000 | 92,025 | ||||||

| Dana, Inc., 5.5%, 12/15/2024 | 20,000 | 20,414 | ||||||

| Dana, Inc., 5.375%, 11/15/2027 | 143,000 | 152,116 | ||||||

| Dana, Inc., 5.625%, 6/15/2028 | 47,000 | 50,701 | ||||||

| IAA Spinco, Inc., 5.5%, 6/15/2027 (n) | 250,000 | 263,750 | ||||||

| KAR Auction Services, Inc., 5.125%, 6/01/2025 (n) | 210,000 | 216,500 | ||||||

| Panther BR Aggregator 2 LP/Panther Finance Co., Inc., 8.5%, 5/15/2027 (n) |

245,000 | 263,681 | ||||||

| PM General Purchaser LLC, 9.5%, 10/01/2028 (n) | 90,000 | 98,100 | ||||||

|

|

|

|||||||

| $ | 1,520,002 | |||||||

| Broadcasting - 3.8% | ||||||||

| Diamond Sports Group LLC/Diamond Sports Finance Co., 6.625%, 8/15/2027 (n) |

$ | 35,000 | $ | 20,071 | ||||

| Diamond Sports Group, LLC/Diamond Sports Finance Co., 5.375%, 8/15/2026 (n) |

65,000 | 50,375 | ||||||

| iHeartCommunications, Inc., 6.375%, 5/01/2026 (n) | 120,000 | 127,050 | ||||||

| iHeartCommunications, Inc., 8.375%, 5/01/2027 | 110,000 | 116,696 | ||||||

| iHeartCommunications, Inc., 5.25%, 8/15/2027 (n) | 55,000 | 56,375 | ||||||

| Netflix, Inc., 5.875%, 2/15/2025 | 335,000 | 382,737 | ||||||

| Netflix, Inc., 3.625%, 6/15/2025 (n) | 150,000 | 159,000 | ||||||

| Netflix, Inc., 5.875%, 11/15/2028 | 170,000 | 205,306 | ||||||

| Netflix, Inc., 5.375%, 11/15/2029 (n) | 50,000 | 59,702 | ||||||

| Nexstar Escrow Corp., 5.625%, 7/15/2027 (n) | 275,000 | 293,219 | ||||||

| WMG Acquisition Corp., 3.875%, 7/15/2030 (n) | 340,000 | 351,658 | ||||||

|

|

|

|||||||

| $ | 1,822,189 | |||||||

19

Table of Contents

Portfolio of Investments – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Bonds - continued | ||||||||

| Brokerage & Asset Managers - 0.7% | ||||||||

| LPL Holdings, Inc., 4.625%, 11/15/2027 (n) | $ | 330,000 | $ | 338,250 | ||||

| Building - 8.0% | ||||||||

| ABC Supply Co., Inc., 5.875%, 5/15/2026 (n) | $ | 220,000 | $ | 229,075 | ||||

| ABC Supply Co., Inc., 4%, 1/15/2028 (n) | 290,000 | 300,875 | ||||||

| Beacon Escrow Corp., 4.875%, 11/01/2025 (n) | 303,000 | 307,090 | ||||||

| Core & Main LP, 8.625%, (8.625% cash or 9.375% PIK) 9/15/2024 (p) | 85,000 | 87,037 | ||||||

| Core & Main LP, 6.125%, 8/15/2025 (n) | 228,000 | 233,700 | ||||||

| Cornerstone Building Brands, Inc., 8%, 4/15/2026 (n) | 160,000 | 168,504 | ||||||

| Cornerstone Building Brands, Inc., 6.125%, 1/15/2029 (n) | 45,000 | 47,475 | ||||||

| CP Atlas Buyer, Inc., 7%, 12/01/2028 (n) | 76,000 | 78,660 | ||||||

| HD Supply, Inc., 5.375%, 10/15/2026 (n) | 255,000 | 270,300 | ||||||

| Interface, Inc., 5.5%, 12/01/2028 (n) | 150,000 | 155,063 | ||||||

| James Hardie International Finance Ltd., 5%, 1/15/2028 (n) | 300,000 | 317,250 | ||||||

| New Enterprise Stone & Lime Co., Inc., 6.25%, 3/15/2026 (n) | 211,000 | 217,594 | ||||||

| New Enterprise Stone & Lime Co., Inc., 9.75%, 7/15/2028 (n) | 109,000 | 118,810 | ||||||

| Patrick Industries, Inc., 7.5%, 10/15/2027 (n) | 210,000 | 227,850 | ||||||

| PriSo Acquisition Corp., 9%, 5/15/2023 (n) | 188,000 | 188,564 | ||||||

| Specialty Building Products Holdings LLC, 6.375%, 9/30/2026 (n) | 135,000 | 140,400 | ||||||

| SRM Escrow Issuer LLC, 6%, 11/01/2028 (n) | 155,000 | 160,812 | ||||||

| SRS Distribution, Inc., 8.25%, 7/01/2026 (n) | 130,000 | 137,800 | ||||||

| Standard Industries, Inc., 4.375%, 7/15/2030 (n) | 196,000 | 207,270 | ||||||

| Standard Industries, Inc., 3.375%, 1/15/2031 (n) | 96,000 | 96,360 | ||||||

| White Cap Buyer LLC, 6.875%, 10/15/2028 (n) | 125,000 | 132,992 | ||||||

|

|

|

|||||||

| $ | 3,823,481 | |||||||

| Business Services - 3.3% | ||||||||

| Ascend Learning LLC, 6.875%, 8/01/2025 (n) | $ | 225,000 | $ | 231,750 | ||||

| CDK Global, Inc., 4.875%, 6/01/2027 | 255,000 | 268,470 | ||||||

| Iron Mountain, Inc., 5.25%, 3/15/2028 (n) | 75,000 | 78,469 | ||||||

| Iron Mountain, Inc., 5.25%, 7/15/2030 (n) | 95,000 | 101,175 | ||||||

| Iron Mountain, Inc., REIT, 4.875%, 9/15/2027 (n) | 175,000 | 181,344 | ||||||

| MSCI, Inc., 4.75%, 8/01/2026 (n) | 245,000 | 254,187 | ||||||

| Refinitiv U.S. Holdings, Inc., 8.25%, 11/15/2026 (n) | 100,000 | 109,000 | ||||||

| Switch, Ltd., 3.75%, 9/15/2028 (n) | 160,000 | 162,334 | ||||||

| Verscend Escrow Corp., 9.75%, 8/15/2026 (n) | 165,000 | 179,231 | ||||||

|

|

|

|||||||

| $ | 1,565,960 | |||||||

| Cable TV - 12.0% | ||||||||

| Cable One, Inc., 4%, 11/15/2030 (n) | $ | 60,000 | $ | 62,475 | ||||

| CCO Holdings LLC/CCO Holdings Capital Corp., 5.75%, 2/15/2026 (n) | 570,000 | 590,662 | ||||||

| CCO Holdings LLC/CCO Holdings Capital Corp., 5.875%, 5/01/2027 (n) |

360,000 | 375,930 | ||||||

| CCO Holdings LLC/CCO Holdings Capital Corp., 4.75%, 3/01/2030 (n) | 575,000 | 610,046 | ||||||

20

Table of Contents

Portfolio of Investments – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Bonds - continued | ||||||||

| Cable TV - continued | ||||||||

| CCO Holdings LLC/CCO Holdings Capital Corp., 4.5%, 8/15/2030 (n) | $ | 150,000 | $ | 158,063 | ||||

| CSC Holdings LLC, 5.5%, 5/15/2026 (n) | 200,000 | 208,000 | ||||||

| CSC Holdings LLC, 5.5%, 4/15/2027 (n) | 800,000 | 844,400 | ||||||

| CSC Holdings LLC, 5.75%, 1/15/2030 (n) | 200,000 | 216,500 | ||||||

| DISH DBS Corp., 5.875%, 11/15/2024 | 200,000 | 212,707 | ||||||

| DISH DBS Corp., 7.75%, 7/01/2026 | 200,000 | 228,250 | ||||||

| Intelsat Jackson Holdings S.A., 5.5%, 8/01/2023 (a)(d) | 180,000 | 121,050 | ||||||

| Intelsat Jackson Holdings S.A., 9.75%, 7/15/2025 (a)(d)(n) | 90,000 | 63,900 | ||||||

| LCPR Senior Secured Financing DAC, 6.75%, 10/15/2027 (n) | 200,000 | 217,420 | ||||||

| Sirius XM Holdings, Inc., 4.625%, 7/15/2024 (n) | 305,000 | 315,943 | ||||||

| Sirius XM Holdings, Inc., 5.5%, 7/01/2029 (n) | 105,000 | 115,238 | ||||||

| Telenet Finance Luxembourg S.A., 5.5%, 3/01/2028 (n) | 400,000 | 428,200 | ||||||

| Telesat Holdings, Inc., 6.5%, 10/15/2027 (n) | 190,000 | 195,700 | ||||||

| Videotron Ltd., 5.375%, 6/15/2024 (n) | 20,000 | 22,204 | ||||||

| Videotron Ltd., 5.125%, 4/15/2027 (n) | 460,000 | 487,025 | ||||||

| Ziggo Bond Finance B.V., 5.125%, 2/28/2030 (n) | 200,000 | 212,000 | ||||||

|

|

|

|||||||

| $ | 5,685,713 | |||||||

| Chemicals - 1.5% | ||||||||

| Axalta Coating Systems Ltd., 4.75%, 6/15/2027 (n) | $ | 150,000 | $ | 158,250 | ||||

| Consolidated Energy Finance S.A., 6.875%, 6/15/2025 (n) | 200,000 | 196,292 | ||||||

| Element Solutions, Inc., 3.875%, 9/01/2028 (n) | 158,000 | 161,081 | ||||||

| Ingevity Corp., 3.875%, 11/01/2028 (n) | 195,000 | 197,437 | ||||||

|

|

|

|||||||

| $ | 713,060 | |||||||

| Computer Software - 1.3% | ||||||||

| Camelot Finance S.A., 4.5%, 11/01/2026 (n) | $ | 295,000 | $ | 308,644 | ||||

| PTC, Inc., 3.625%, 2/15/2025 (n) | 215,000 | 219,633 | ||||||

| PTC, Inc., 4%, 2/15/2028 (n) | 95,000 | 98,919 | ||||||

|

|

|

|||||||

| $ | 627,196 | |||||||

| Computer Software - Systems - 2.2% | ||||||||

| BY Crown Parent LLC, 4.25%, 1/31/2026 (n) | $ | 65,000 | $ | 66,787 | ||||

| Fair Isaac Corp., 5.25%, 5/15/2026 (n) | 405,000 | 453,600 | ||||||

| Fair Isaac Corp., 4%, 6/15/2028 (n) | 36,000 | 37,609 | ||||||

| JDA Software Group, Inc., 7.375%, 10/15/2024 (n) | 175,000 | 178,229 | ||||||

| SS&C Technologies Holdings, Inc., 5.5%, 9/30/2027 (n) | 275,000 | 294,594 | ||||||

|

|

|

|||||||

| $ | 1,030,819 | |||||||

| Conglomerates - 6.5% | ||||||||

| Amsted Industries Co., 5.625%, 7/01/2027 (n) | $ | 270,000 | $ | 286,538 | ||||

| BWX Technologies, Inc., 5.375%, 7/15/2026 (n) | 335,000 | 347,981 | ||||||

| BWX Technologies, Inc., 4.125%, 6/30/2028 (n) | 68,000 | 70,805 | ||||||

| CFX Escrow Corp., 6.375%, 2/15/2026 (n) | 210,000 | 225,225 | ||||||

21

Table of Contents

Portfolio of Investments – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Bonds - continued | ||||||||

| Conglomerates - continued | ||||||||

| EnerSys, 5%, 4/30/2023 (n) | $ | 275,000 | $ | 287,719 | ||||

| EnerSys, 4.375%, 12/15/2027 (n) | 55,000 | 58,283 | ||||||

| Gates Global LLC, 6.25%, 1/15/2026 (n) | 250,000 | 261,875 | ||||||

| Granite Holdings U.S. Acquisition Co., 11%, 10/01/2027 (n) | 135,000 | 148,500 | ||||||

| Griffon Corp., 5.75%, 3/01/2028 | 223,000 | 236,380 | ||||||

| MTS Systems Corp., 5.75%, 8/15/2027 (n) | 230,000 | 238,625 | ||||||

| Stevens Holding Co., Inc., 6.125%, 10/01/2026 (n) | 220,000 | 238,425 | ||||||

| TriMas Corp., 4.875%, 10/15/2025 (n) | 485,000 | 494,850 | ||||||

| WESCO Distribution, Inc., 7.125%, 6/15/2025 (n) | 81,000 | 88,189 | ||||||

| WESCO Distribution, Inc., 7.25%, 6/15/2028 (n) | 80,000 | 89,875 | ||||||

|

|

|

|||||||

| $ | 3,073,270 | |||||||

| Construction - 3.2% | ||||||||

| Lennar Corp., 4.75%, 11/29/2027 | $ | 175,000 | $ | 207,594 | ||||

| Mattamy Group Corp., 5.25%, 12/15/2027 (n) | 95,000 | 100,463 | ||||||

| Mattamy Group Corp., 4.625%, 3/01/2030 (n) | 155,000 | 162,362 | ||||||

| Shea Homes LP/Shea Homes Funding Corp., 4.75%, 2/15/2028 (n) | 200,000 | 207,000 | ||||||

| Taylor Morrison Communities, Inc., 5.875%, 6/15/2027 (n) | 60,000 | 67,844 | ||||||

| Taylor Morrison Communities, Inc., 5.125%, 8/01/2030 (n) | 65,000 | 72,313 | ||||||

| Toll Brothers Finance Corp., 4.875%, 11/15/2025 | 180,000 | 203,175 | ||||||

| Toll Brothers Finance Corp., 4.35%, 2/15/2028 | 250,000 | 277,500 | ||||||

| Weekley Homes LLC/Weekley Finance Corp., 4.875%, 9/15/2028 (n) | 231,000 | 241,467 | ||||||

|

|

|

|||||||

| $ | 1,539,718 | |||||||

| Consumer Products - 1.8% | ||||||||

| Coty, Inc., 6.5%, 4/15/2026 (n) | $ | 190,000 | $ | 185,250 | ||||

| Energizer Holdings, Inc., 4.375%, 3/31/2029 (n) | 150,000 | 153,067 | ||||||

| Mattel, Inc., 6.75%, 12/31/2025 (n) | 185,000 | 194,564 | ||||||

| Mattel, Inc., 5.875%, 12/15/2027 (n) | 109,000 | 120,173 | ||||||

| Prestige Brands, Inc., 5.125%, 1/15/2028 (n) | 170,000 | 179,860 | ||||||

|

|

|

|||||||

| $ | 832,914 | |||||||

| Consumer Services - 3.1% | ||||||||

| Allied Universal Holdco LLC, 6.625%, 7/15/2026 (n) | $ | 59,000 | $ | 63,425 | ||||

| Allied Universal Holdco LLC, 9.75%, 7/15/2027 (n) | 175,000 | 194,078 | ||||||

| ANGI Group LLC, 3.875%, 8/15/2028 (n) | 155,000 | 153,256 | ||||||

| Frontdoor, Inc., 6.75%, 8/15/2026 (n) | 155,000 | 165,269 | ||||||

| Garda World Security Corp., 4.625%, 2/15/2027 (n) | 75,000 | 75,188 | ||||||

| GW B-CR Security Corp., 9.5%, 11/01/2027 (n) | 131,000 | 146,065 | ||||||

| Match Group, Inc., 5%, 12/15/2027 (n) | 200,000 | 211,500 | ||||||

| Match Group, Inc., 4.625%, 6/01/2028 (n) | 220,000 | 231,000 | ||||||

| Realogy Group LLC, 9.375%, 4/01/2027 (n) | 235,000 | 257,378 | ||||||

|

|

|

|||||||

| $ | 1,497,159 | |||||||

22

Table of Contents

Portfolio of Investments – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Bonds - continued | ||||||||

| Containers - 5.1% | ||||||||

| ARD Finance S.A., 6.5%, (6.5% cash or 7.25% PIK) 6/30/2027 (p) | $ | 200,000 | $ | 210,750 | ||||

| Ardagh Packaging Finance PLC/Ardagh MP Holdings USA, Inc., 5.25%, 8/15/2027 (n) | 255,000 | 265,927 | ||||||

| Berry Global Group, Inc., 4.875%, 7/15/2026 (n) | 140,000 | 148,632 | ||||||

| Berry Global Group, Inc., 5.625%, 7/15/2027 (n) | 95,000 | 101,175 | ||||||

| Crown Americas LLC/Crown Americas Capital Corp. IV, 4.5%, 1/15/2023 | 276,000 | 291,180 | ||||||

| Crown Americas LLC/Crown Americas Capital Corp. V, 4.25%, 9/30/2026 | 290,000 | 312,475 | ||||||

| Crown Americas LLC/Crown Americas Capital Corp. VI, 4.75%, 2/01/2026 | 75,000 | 77,813 | ||||||

| Flex Acquisition Co., Inc., 6.875%, 1/15/2025 (n) | 175,000 | 179,319 | ||||||

| Greif, Inc., 6.5%, 3/01/2027 (n) | 50,000 | 52,875 | ||||||

| Reynolds Group, 4%, 10/15/2027 (n) | 160,000 | 162,712 | ||||||

| Silgan Holdings, Inc., 4.75%, 3/15/2025 | 225,000 | 229,922 | ||||||

| Silgan Holdings, Inc., 4.125%, 2/01/2028 | 152,000 | 157,700 | ||||||

| Trivium Packaging Finance B.V., 8.5%, 8/15/2027 (n) | 200,000 | 216,500 | ||||||

|

|

|

|||||||

| $ | 2,406,980 | |||||||

| Electrical Equipment - 0.7% | ||||||||

| CommScope Technologies LLC, 6%, 6/15/2025 (n) | $ | 129,000 | $ | 132,186 | ||||

| CommScope Technologies LLC, 5%, 3/15/2027 (n) | 180,000 | 179,100 | ||||||

|

|

|

|||||||

| $ | 311,286 | |||||||

| Electronics - 2.3% | ||||||||

| Diebold Nixdorf, Inc., 9.375%, 7/15/2025 (n) | $ | 106,000 | $ | 116,335 | ||||

| Entegris, Inc., 4.625%, 2/10/2026 (n) | 270,000 | 278,100 | ||||||

| Entegris, Inc., 4.375%, 4/15/2028 (n) | 90,000 | 95,129 | ||||||

| Sensata Technologies B.V., 5.625%, 11/01/2024 (n) | 140,000 | 156,800 | ||||||

| Sensata Technologies B.V., 5%, 10/01/2025 (n) | 320,000 | 355,200 | ||||||

| Sensata Technologies, Inc., 4.375%, 2/15/2030 (n) | 75,000 | 80,250 | ||||||

|

|

|

|||||||

| $ | 1,081,814 | |||||||

| Energy - Independent - 3.7% | ||||||||

| Apache Corp., 4.875%, 11/15/2027 | $ | 63,000 | $ | 65,803 | ||||

| Apache Corp., 4.375%, 10/15/2028 | 255,000 | 260,100 | ||||||

| CNX Resources Corp., 6%, 1/15/2029 (n) | 30,000 | 30,300 | ||||||

| CrownRock LP/CrownRock Finance, Inc., 5.625%, 10/15/2025 (n) | 170,000 | 171,700 | ||||||

| EQT Corp., 5%, 1/15/2029 | 73,000 | 77,015 | ||||||

| Laredo Petroleum, Inc., 10.125%, 1/15/2028 | 110,000 | 73,634 | ||||||

| Leviathan Bond Ltd., 6.5%, 6/30/2027 (n) | 159,000 | 174,502 | ||||||

| Magnolia Oil & Gas Operating LLC/Magnolia Oil & Gas Finance Corp., 6%, 8/01/2026 (n) | 150,000 | 148,500 | ||||||

| Murphy Oil Corp., 6.875%, 8/15/2024 | 50,000 | 49,500 | ||||||

23

Table of Contents

Portfolio of Investments – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Bonds - continued | ||||||||

| Energy - Independent - continued | ||||||||

| Murphy Oil Corp., 5.875%, 12/01/2027 | $ | 60,000 | $ | 54,600 | ||||

| Newfield Exploration Co., 5.375%, 1/01/2026 | 70,000 | 73,340 | ||||||

| Occidental Petroleum Corp., 5.875%, 9/01/2025 | 155,000 | 156,519 | ||||||

| Ovintiv, Inc., 6.5%, 8/15/2034 | 55,000 | 59,106 | ||||||

| Parsley Energy LLC/Parsley Finance Corp., 5.625%, 10/15/2027 (n) | 95,000 | 102,315 | ||||||

| Southwestern Energy Co., 6.45%, 1/23/2025 | 93,300 | 95,166 | ||||||

| Southwestern Energy Co., 7.5%, 4/01/2026 | 132,700 | 138,234 | ||||||

| Southwestern Energy Co., 7.75%, 10/01/2027 | 35,000 | 36,925 | ||||||

|

|

|

|||||||

| $ | 1,767,259 | |||||||

| Entertainment - 2.6% | ||||||||

| Carnival Corp. PLC, 7.625%, 3/01/2026 (n) | $ | 75,000 | $ | 79,125 | ||||

| Cedar Fair LP/Canada’s Wonderland Co./Magnum Management Corp./Millennium Operations LLC, 5.5%, 5/01/2025 (n) | 60,000 | 63,000 | ||||||

| Cedar Fair LP/Canada’s Wonderland Co./Magnum Management Corp./Millennium Operations LLC, 5.375%, 4/15/2027 | 105,000 | 105,525 | ||||||

| Live Nation Entertainment, Inc., 5.625%, 3/15/2026 (n) | 218,000 | 220,180 | ||||||

| Merlin Entertainments, 5.75%, 6/15/2026 (n) | 200,000 | 209,000 | ||||||

| NCL Corp. Ltd., 3.625%, 12/15/2024 (n) | 80,000 | 71,460 | ||||||

| NCL Corp. Ltd., 10.25%, 2/01/2026 (n) | 95,000 | 107,825 | ||||||

| Royal Caribbean Cruises Ltd., 10.875%, 6/01/2023 (n) | 90,000 | 101,813 | ||||||

| Six Flags Entertainment Corp., 4.875%, 7/31/2024 (n) | 185,000 | 184,304 | ||||||

| Six Flags Entertainment Corp., 7%, 7/01/2025 (n) | 70,000 | 75,885 | ||||||

|

|

|

|||||||

| $ | 1,218,117 | |||||||

| Financial Institutions - 4.3% | ||||||||

| Avation Capital S.A., 6.5%, 5/15/2021 (n) | $ | 200,000 | $ | 130,000 | ||||

| Avolon Holdings Funding Ltd., 5.125%, 10/01/2023 | 175,000 | 184,111 | ||||||

| Avolon Holdings Funding Ltd., 3.95%, 7/01/2024 (n) | 130,000 | 133,381 | ||||||

| Credit Acceptance Corp., 5.125%, 12/31/2024 (n) | 220,000 | 224,950 | ||||||

| Freedom Mortgage Corp., 7.625%, 5/01/2026 (n) | 120,000 | 122,394 | ||||||

| Global Aircraft Leasing Co. Ltd., 6.5%, (6.5% cash or 7.25% PIK) 9/15/2024 (p) | 462,348 | 411,536 | ||||||

| Nationstar Mortgage Holdings, Inc., 6%, 1/15/2027 (n) | 135,000 | 139,976 | ||||||

| Navient Corp., 5%, 3/15/2027 | 130,000 | 128,700 | ||||||

| OneMain Financial Corp., 6.875%, 3/15/2025 | 110,000 | 125,675 | ||||||

| OneMain Financial Corp., 7.125%, 3/15/2026 | 100,000 | 115,109 | ||||||

| Park Aerospace Holdings Ltd., 5.5%, 2/15/2024 (n) | 120,000 | 128,110 | ||||||

| Springleaf Finance Corp., 8.875%, 6/01/2025 | 99,000 | 110,385 | ||||||

| Springleaf Finance Corp., 5.375%, 11/15/2029 | 80,000 | 87,200 | ||||||

|

|

|

|||||||

| $ | 2,041,527 | |||||||

24

Table of Contents

Portfolio of Investments – continued

| Issuer | Shares/Par | Value ($) | ||||||

| Bonds - continued | ||||||||

| Food & Beverages - 2.7% | ||||||||

| Aramark Services, Inc., 6.375%, 5/01/2025 (n) | $ | 215,000 | $ | 228,975 | ||||

| JBS USA LLC/JBS USA Finance, Inc., 6.75%, 2/15/2028 (n) | 295,000 | 328,187 | ||||||

| JBS USA Lux S.A./JBS USA Finance, Inc., 5.5%, 1/15/2030 (n) | 115,000 | 129,272 | ||||||

| Lamb Weston Holdings, Inc., 4.625%, 11/01/2024 (n) | 295,000 | 306,800 | ||||||

| Lamb Weston Holdings, Inc., 4.875%, 5/15/2028 (n) | 43,000 | 47,730 | ||||||

| Performance Food Group Co., 5.5%, 10/15/2027 (n) | 210,000 | 223,387 | ||||||

|

|

|

|||||||

| $ | 1,264,351 | |||||||

| Gaming & Lodging - 8.0% | ||||||||

| Boyd Gaming Corp., 6.375%, 4/01/2026 | $ | 80,000 | $ | 83,100 | ||||

| Boyd Gaming Corp., 4.75%, 12/01/2027 | 130,000 | 132,106 | ||||||

| Caesars Resort Collection LLC / CRC Finco, Inc., 5.25%, 10/15/2025 (n) |

180,000 | 180,000 | ||||||

| CCM Merger, Inc., 6.375%, 5/01/2026 (n) | 135,000 | 141,088 | ||||||

| Churchill Downs, Inc., 5.5%, 4/01/2027 (n) | 90,000 | 94,725 | ||||||

| Colt Merger Sub, Inc., 5.75%, 7/01/2025 (n) | 91,000 | 96,346 | ||||||

| Colt Merger Sub, Inc., 8.125%, 7/01/2027 (n) | 162,000 | 178,191 | ||||||

| Hilton Domestic Operating Co., Inc., 5.125%, 5/01/2026 | 155,000 | 160,307 | ||||||

| Hilton Domestic Operating Co., Inc., 3.75%, 5/01/2029 (n) | 208,000 | 213,504 | ||||||

| Hilton Worldwide Finance LLC, 4.625%, 4/01/2025 | 330,000 | 337,630 | ||||||

| MGM Growth Properties LLC, 4.625%, 6/15/2025 (n) | 185,000 | 195,175 | ||||||

| MGM Growth Properties LLC, 5.75%, 2/01/2027 | 75,000 | 83,594 | ||||||

| MGM Growth Properties LLC, 3.875%, 2/15/2029 (n) | 135,000 | 136,350 | ||||||

| MGM Resorts International, 6.75%, 5/01/2025 | 185,000 | 198,759 | ||||||

| Scientific Games Corp., 8.25%, 3/15/2026 (n) | 120,000 | 128,712 | ||||||

| Scientific Games International, Inc., 7%, 5/15/2028 (n) | 85,000 | 88,538 | ||||||

| VICI Properties LP, REIT, 4.25%, 12/01/2026 (n) | 170,000 | 176,375 | ||||||

| VICI Properties LP, REIT, 3.75%, 2/15/2027 (n) | 235,000 | 239,700 | ||||||

| Wyndham Hotels & Resorts, Inc., 4.375%, 8/15/2028 (n) | 39,000 | 39,926 | ||||||

| Wyndham Hotels Group LLC, 5.375%, 4/15/2026 (n) | 305,000 | 314,912 | ||||||

| Wynn Las Vegas LLC/Wynn Las Vegas Capital Corp., 5.5%, 3/01/2025 (n) |

150,000 | 153,000 | ||||||

| Wynn Las Vegas LLC/Wynn Las Vegas Capital Corp., 5.25%, 5/15/2027 (n) |

235,000 | 237,350 | ||||||

| Wynn Macau Ltd., 5.5%, 1/15/2026 (n) | 105,000 | 106,838 | ||||||

| Wynn Resorts Finance LLC/Wynn Resorts Capital Corp., 5.125%, 10/01/2029 (n) |

85,000 | 86,488 | ||||||

|

|

|

|||||||

| $ | 3,802,714 | |||||||

| Industrial - 0.4% | ||||||||