Filed Pursuant to Rule 433

Registration No. 333-202524

FREE WRITING PROSPECTUS

Dated May 31, 2017

(To Prospectus dated March 5, 2015,

Prospectus Supplement dated March 5, 2015,

Equity Index Underlying Supplement dated March 5, 2015 and

ETF Underlying Supplement dated March 5, 2015)

HSBC USA Inc.

Buffered Autocallable Yield

Notes with Rebate Return

| 4 | Buffered Autocallable Yield Notes with Rebate Return Linked to the Worst of the Russell 2000® Index and the iShares® MSCI EAFE ETF |

| 4 | 18-month term |

| 4 | Callable semi-annually at the applicable call premium (equivalent to 9% per annum) on or after November 30, 2017 if the value of each underlying is at or above its initial value |

| 4 | If the notes are not called, a rebate return of 7% if the value of the least performing underlying does not decrease by more than 20% |

| 4 | If the notes are not called, 1.25x exposure to any decrease in the value of the least performing underlying beyond -20% |

| 4 | All payments on the notes are subject to the credit risk of HSBC USA Inc. |

The Buffered Autocallable Yield Notes with Rebate Return (each a “Note” and collectively the “Notes”) offered hereunder will not be listed on any U.S. securities exchange or automated quotation system. The Notes will not bear interest.

Neither the U.S. Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of the Notes or passed upon the accuracy or the adequacy of this document, the accompanying prospectus, prospectus supplement, Equity Index Underlying Supplement or ETF Underlying Supplement. Any representation to the contrary is a criminal offense.

We have appointed HSBC Securities (USA) Inc., an affiliate of ours, as the agent for the sale of the Notes. HSBC Securities (USA) Inc. will purchase the Notes from us for distribution to other registered broker-dealers or will offer the Notes directly to investors. HSBC Securities (USA) Inc. or another of its affiliates or agents may use the pricing supplement to which this free writing prospectus relates in market-making transactions in any Notes after their initial sale. Unless we or our agent informs you otherwise in the confirmation of sale, the pricing supplement to which this free writing prospectus relates is being used in a market-making transaction. See “Supplemental Plan of Distribution (Conflicts of Interest)” on page FWP-17 of this free writing prospectus.

Investment in the Notes involves certain risks. You should refer to “Risk Factors” beginning on page FWP-9 of this document, page S-1 of the accompanying prospectus supplement, page S-2 of the accompanying Equity Index Underlying Supplement and page S-1 of the accompanying ETF Underlying Supplement.

The Estimated Initial Value of the Notes on the Pricing Date is expected to be between $980 and $1,000 per Note, which may be less than the price to public. The market value of the Notes at any time will reflect many factors and cannot be predicted with accuracy. See “Estimated Initial Value” on page FWP-5 and “Risk Factors” beginning on page FWP-9 of this document for additional information.

| Price to Public | Underwriting Discount1 | Proceeds to Issuer | |

| Per Note | $1,000.00 | $0.50 | $999.50 |

| Total |

1HSBC USA Inc. or one of our affiliates may pay varying underwriting discounts of up to 0.05% per $1,000 Principal Amount of Notes in connection with the distribution of the Notes to other registered broker-dealers. See “Supplemental Plan of Distribution (Conflicts of Interest)” on page FWP-17 of this free writing prospectus.

The Notes:

| Are Not FDIC Insured | Are Not Bank Guaranteed | May Lose Value |

![]()

HSBC USA Inc.

Buffered Autocallable Yield Notes with Rebate Return

Linked to the Worst of the Russell 2000® Index and the iShares® MSCI EAFE ETF

Indicative Terms*

| Principal Amount | $1,000 per Note |

| Term | 18 months |

| Reference Asset | The Russell 2000® Index (“RTY”) and the iShares® MSCI EAFE ETF (“EFA”) (each an “Underlying” and together the “Underlyings”). |

| Call Feature | The Notes will be automatically called if the Official Closing Value of each Underlying is at or above its Initial Value on any semi-annual Call Observation Date. In such a case, you will receive a cash payment, per $1,000 Principal Amount, equal to the applicable Call Price, reflecting a return equal to the applicable Call Premium. |

| Call Prices and Call Premiums | $1,045 per Note (representing a Call Premium of 4.50%) if called on the first Call Observation Date, $1,090 per Note (representing a Call Premium of 9.00%) if called on the second Call Observation Date, and $1,135 per Note (representing a Call Premium of 13.50%) if called on the final Call Observation Date. |

| Payment at Maturity per Note |

Unless the Notes are automatically called, for each $1,000 Principal Amount, you will receive a cash payment on the Maturity Date, calculated as follows: n If the Final Return of the Least Performing Underlying is less than zero but greater than or equal to -20%: $1,000 + ($1,000 x Rebate Return). n If the Final Return of the Least Performing Underlying is less than -20%: $1,000 + [$1,000

× (Final Return of the Least Performing Underlying + 20%) x Downside Leverage Factor]. |

| Rebate Return | 7% |

| Downside Leverage Factor | 1.25 |

| Buffer Value | For each Underlying, 80% of its Initial Value. |

| Final Return |

For each Underlying: Final Value – Initial Value Initial Value |

| Least Performing Underlying | The Underlying with the lowest Final Return. |

| Trade Date | May 31, 2017 |

| Pricing Date | May 31, 2017 |

| Original Issue Date | June 5, 2017 |

| Final Valuation Date† | November 30, 2018 |

| Maturity Date† | December 5, 2018 |

| CUSIP / ISIN | 40433U7C4 / US40433U7C45 |

* As more fully described beginning on page FWP-4.

†Subject to adjustment as described under “Additional Terms of the Notes” in the accompanying Equity Index Underlying Supplement and ETF Underlying Supplement.

The Notes

The Notes may be suitable for investors who believe the value of both Underlyings will not decrease by more than 20% from the pricing date to the Final Valuation Date.

If both Underlyings are at or above their respective Initial Values on any Call Observation Date, your Notes will be automatically called and you will receive a return equal to the applicable Call Premium.

If the Notes are not automatically called and the Final Value of the Least Performing Underlying is greater than or equal to its Buffer Value, you will receive a return equal to the Rebate Return.

If the Notes are not automatically called and the Final Value of the Least Performing Underlying is less than its Buffer Value, you will lose 1.25% of your principal for every 1% decline in value of the Least Performing Underlying beyond -20%. You may lose up to 100% of the Principal Amount.

| The offering period for the Notes is through May 31, 2017 |

| FWP-2 |

| Illustration of Payment Scenarios | |

| Your payment on the Notes will depend on whether the Notes have been automatically called and, if they have not been called, whether the Final Value of the Least Performing Underlying is below its Buffer Value. |  |

|

Information about the Underlyings

| |

| The Russell 2000® Index | |

|

The RTY is designed to track the performance of the small-capitalization segment of the U.S. equity market. It consists of the smallest 2,000 companies included in the Russell 3000® Index, which is composed of the 3,000 largest U.S. companies as determined by market capitalization.

The top 5 industry groups by market capitalization as of April 30, 2017 were: Financial Services, Technology, Producer Durables, Consumer Discretionary and Health Care. |

|

| iShares® MSCI EAFE ETF | |

|

The EFA seeks investment results that correspond generally to the price and yield performance, before fees and expenses, of publicly traded securities in the European, Australasian, and Far Eastern markets, as measured by the MSCI EAFE® Index, which is the underlying index of the EFA. As of April 30, 2017, the MSCI EAFE Index consisted of the following 21 component country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, The Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, and the United Kingdom. The returns of the EFA may be affected by certain management fees and other expenses, which are detailed in its prospectus. |

|

The graphs above illustrate the daily performance of each Underlying from January 1, 2008 through May 30, 2017. Past performance is not necessarily an indication of future results. For further information on the Underlyings, please see “Information Relating to the Underlyings” beginning on page FWP-15 and “The Russell 2000® Index” in the accompanying Equity Index Underlying Supplement and “The iShares® MSCI EAFE ETF” in the accompanying ETF Underlying Supplement. We have derived all disclosure regarding the Underlyings from publicly available information. Neither HSBC USA Inc. nor any of its affiliates have undertaken any independent review of, or made any due diligence inquiry with respect to, the publicly available information about the Underlyings.

| FWP-3 |

|

HSBC USA Inc. Buffered Autocallable Yield Notes with Rebate Return |

This free writing prospectus relates to a single offering of Buffered Autocallable Yield Notes with Rebate Return. The Notes will have the terms described in this free writing prospectus and the accompanying prospectus supplement, prospectus and Equity Index Underlying Supplement. If the terms of the Notes offered hereby are inconsistent with those described in the accompanying prospectus supplement, prospectus or Equity Index Underlying Supplement, the terms described in this free writing prospectus shall control.

This free writing prospectus relates to an offering of Notes linked to the performance of two indices. The purchaser of a Note will acquire a senior unsecured debt security of HSBC USA Inc. as described below. The following key terms relate to the offering of Notes:

| Issuer: | HSBC USA Inc. | |

| Principal Amount: | $1,000 per Note | |

| Reference Asset: | The Russell 2000® Index (“RTY”) and the iShares® MSCI EAFE ETF (“EFA”) (each an “Underlying” and together the “Underlyings”) | |

| Trade Date: | May 31, 2017 | |

| Pricing Date: | May 31, 2017 | |

| Original Issue Date: | June 5, 2017 | |

| Final Valuation Date: | November 30, 2018, subject to adjustment as described under “Additional Terms of the Notes―Valuation Dates” in the accompanying Equity Index Underlying Supplement. | |

| Maturity Date: | 3 business days after the Final Valuation Date, expected to be December 5, 2018. The Maturity Date is subject to adjustment as described under “Additional Terms of the Notes―Coupon Payment Dates, Call Payment Dates and Maturity Date” in the accompanying Equity Index Underlying Supplement and ETF Underlying Supplement. | |

| Call Feature: | If the Official Closing Value of each Underlying is at or above its Initial Value on any Call Observation Date, the Notes will be automatically called, and you will receive the applicable Call Price on the corresponding Call Payment Date. | |

| Call Observation Dates: | November 30, 2017, May 31, 2018, and November 30, 2018 (the Final Valuation Date), each subject to postponement as described under “Additional Terms of the Notes—Valuation Dates” in the accompanying Equity Index Underlying Supplement and ETF Underlying Supplement | |

| Call Payment Dates: | December 5, 2017, June 5, 2018, and December 5, 2018 (the Maturity Date), each subject to postponement as described under “Additional Terms of the Notes—Coupon Payment Dates, Call Payment Dates and Maturity Date” in the accompanying Equity Index Underlying Supplement and Underlying Supplement. | |

| Call Prices: | The applicable Call Prices and Call Premiums are as follows: |

| Expected Call Observation Dates | Call Prices (per $1,000 Principal Amount) |

Call Premiums | |

| November 30, 2017 | $1,045 | 4.50% | |

| May 31, 2018 | $1,090 | 9.00% | |

| November 30, 2018 (Final Valuation Date) | $1,135 | 13.50% |

| Payment at Maturity: | Unless the Notes are automatically called, on the Maturity Date, for each $1,000 Principal Amount of Notes, we will pay you the Final Settlement Value. |

| FWP-4 |

| Final Settlement Value: |

Unless the Notes are automatically called, for each $1,000 Principal Amount, you will receive a cash payment on the Maturity Date, calculated as follows:

n If the Final Return of the Least Performing Underlying is less than zero but greater than or equal to -20%:

$1,000 + ($1,000 x Rebate Return).

n If the Final Return of the Least Performing Underlying is less than -20%:

$1,000 + [$1,000 × (Final Return of the Least Performing Underlying + 20%) x Downside Leverage Factor].

For example, if the Final Return of the Least Performing Underlying is -30%, you will suffer a 12.50% loss and receive 87.50% of the Principal Amount. If the Final Value of the Least Performing Underlying is less than its Buffer Value, you will lose up to 100% of the Principal Amount. | |

| Rebate Return: | 7% | |

| Downside Leverage Factor: | 1.25 | |

| Buffer Value: | For each Underlying, 80% of its Initial Value. | |

| Least Performing Underlying: | The Underlying with the lowest Final Return. | |

|

Final Return: |

With respect to each Underlying, the quotient, expressed as a percentage, calculated as follows:

Final Value – Initial Value Initial Value | |

| Initial Value: | The Official Closing Value of the relevant Underlying on the Pricing Date. | |

| Final Value: | The Official Closing Value of the relevant Underlying on the Final Valuation Date. | |

| Official Closing Value: | The closing level or closing price, as applicable, of the Underlying on any scheduled trading day as determined by the calculation agent based upon the value displayed on the relevant Bloomberg Professional® service page (with respect to the RTY, “RTY <INDEX>”, and with respect to the EFA, “EFA UP <EQUITY>”), or, for each Underlying, any successor page on the Bloomberg Professional® service or any successor service, as applicable. | |

| CUSIP/ISIN: | 40433U7C4 / US40433U7C45 | |

| Form of Notes: | Book-Entry | |

| Listing: | The Notes will not be listed on any U.S. securities exchange or quotation system. | |

| Estimated Initial Value: | The Estimated Initial Value of the Notes may be less than the price you pay to purchase the Notes. The Estimated Initial Value does not represent a minimum price at which we or any of our affiliates would be willing to purchase your Notes in the secondary market, if any, at any time. The Estimated Initial Value will be calculated on the Pricing Date and will be set forth in the pricing supplement to which this free writing prospectus relates. See “Risk Factors — The Estimated Initial Value of the Notes, which will be determined by us on the Pricing Date, may be less than the price to public and may differ from the market value of the Notes in the secondary market, if any.” |

The Trade Date, the Pricing Date and the other dates set forth above are subject to change, and will be set forth in the final pricing supplement relating to the Notes.

| FWP-5 |

GENERAL

This free writing prospectus relates to the offering of Notes identified on the cover page. The purchaser of a Note will acquire a senior unsecured debt security of HSBC USA Inc. We reserve the right to withdraw, cancel or modify this offering and to reject orders in whole or in part. Although the offering of Notes relates to the Reference Asset identified on the cover page, you should not construe that fact as a recommendation as to the merits of acquiring an investment linked to the Reference Asset or any component security included in the Reference Asset or as to the suitability of an investment in the Notes.

You should read this document together with the prospectus dated March 5, 2015, the prospectus supplement dated March 5, 2015, the Equity Index Underlying Supplement dated March 5, 2015 and the ETF Underlying Supplement dated March 5, 2015. If the terms of the Notes offered hereby are inconsistent with those described in the accompanying prospectus supplement, prospectus, Equity Index Underlying Supplement or ETF Underlying Supplement, the terms described in this free writing prospectus shall control. You should carefully consider, among other things, the matters set forth in “Risk Factors” beginning on page FWP-9 of this free writing prospectus, beginning on page S-1 of the prospectus supplement, beginning on page S-2 of the Equity Index Underlying Supplement and beginning on page S-1 of the ETF Underlying Supplement, as the Notes involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting and other advisors before you invest in the Notes. As used herein, references to the “Issuer”, “HSBC”, “we”, “us” and “our” are to HSBC USA Inc.

HSBC has filed a registration statement (including a prospectus, prospectus supplement, Equity Index Underlying Supplement and ETF Underlying Supplement) with the SEC for the offering to which this free writing prospectus relates. Before you invest, you should read the prospectus, prospectus supplement, Equity Index Underlying Supplement and ETF Underlying Supplement in that registration statement and other documents HSBC has filed with the SEC for more complete information about HSBC and this offering. You may get these documents for free by visiting EDGAR on the SEC’s web site at www.sec.gov. Alternatively, HSBC Securities (USA) Inc. or any dealer participating in this offering will arrange to send you the prospectus, prospectus supplement, Equity Index Underlying Supplement and ETF Underlying Supplement if you request them by calling toll-free 1-866-811-8049.

You may also obtain:

| 4 | The Equity Index Underlying Supplement at: http://www.sec.gov/Archives/edgar/data/83246/000114420415014327/v403626_424b2.htm |

| 4 | The ETF Underlying Supplement at: http://www.sec.gov/Archives/edgar/data/83246/000114420415014329/v403640_424b2.htm |

| 4 | The prospectus supplement at: http://www.sec.gov/Archives/edgar/data/83246/000114420415014311/v403645_424b2.htm |

| 4 | The prospectus at: http://www.sec.gov/Archives/edgar/data/83246/000119312515078931/d884345d424b3.htm |

We are using this free writing prospectus to solicit from you an offer to purchase the Notes. You may revoke your offer to purchase the Notes at any time prior to the time at which we accept your offer by notifying HSBC Securities (USA) Inc. We reserve the right to change the terms of, or reject any offer to purchase, the Notes prior to their issuance. In the event of any material changes to the terms of the Notes, we will notify you.

PAYMENT ON THE NOTES

Call Feature

The Notes will be automatically called if the Official Closing Value of each Underlying is at or above its Initial Value on any Call Observation Date. If the Notes are automatically called, investors will receive the applicable Call Price on the corresponding Call Payment Date.

Maturity

Unless the Notes are automatically called, on the Maturity Date and for each $1,000 Principal Amount of Notes, you will receive a cash payment equal to the Final Settlement Value determined as follows:

n If the Final Return of the Least Performing Underlying is less than zero but greater than or equal to -20%:

$1,000 + ($1,000 x Rebate Return)

n If the Final Return of the Least Performing Underlying is less than -20%:

$1,000 + [$1,000 × (Final Return of the Least Performing Underlying + 20%) x Downside Leverage Factor]

For example, if the Final Return of the Least Performing Underlying is -30%, you will suffer a 12.50% loss and receive 87.50% of the Principal Amount. If the Final Value of the Least Performing Underlying is less than the Buffer Value, you will lose up to 100% of the Principal Amount.

| FWP-6 |

Official Closing Value

The closing level or closing price, as applicable, of the Underlying on any scheduled trading day as determined by the calculation agent based upon the value displayed on the relevant Bloomberg Professional® service page (with respect to the RTY, “RTY <INDEX>”, and with respect to the EFA, “EFA UP <EQUITY>”), or, for each Underlying, any successor page on the Bloomberg Professional® service or any successor service, as applicable.

Calculation Agent

We or one of our affiliates will act as calculation agent with respect to the Notes.

Reference Sponsor and Reference Issuer

With respect to RTY, FTSE Russell is the reference sponsor. With respect to EFA, iShares, Inc. is the reference issuer.

| FWP-7 |

INVESTOR SUITABILITY

The Notes may be suitable for you if:

| 4 | You believe that the Official Closing Value of each Underlying will be at or above its Initial Value on at least one Call Observation Date, including the Final Valuation Date, and if not, the Final Value of the Least Performing Underlying will be at or above its Buffer Value. |

| 4 | You are willing to make an investment that is exposed to the potential downside performance of the Least Performing Underlying on a 1.25-to-1 basis. |

| 4 | You are willing to lose up to 100% of the Principal Amount. |

| 4 | You are willing to hold the Notes that will be automatically called on any Call Observation Date on which the Official Closing Value of each Underlying is at or above its Initial Value, or you are otherwise willing to hold the Notes to maturity. |

| 4 | You are willing to make an investment whose return is limited to the pre-specified Call Premiums or the Rebate Return, as applicable. |

| 4 | You are willing to forgo dividends or other distributions paid on the stocks held by or included in the relevant Underlying. |

| 4 | You do not seek current income from this investment. |

| 4 | You do not seek an investment for which there will be an active secondary market. |

| 4 | You are willing to accept the risk and return profile of the Notes versus a conventional debt security with a comparable maturity issued by HSBC or another issuer with a similar credit rating. |

| 4 | You are comfortable with the creditworthiness of HSBC, as Issuer of the Notes. |

The Notes may not be suitable for you if:

| 4 | You believe that the Official Closing Value of at least one Underlying will be below its Initial Value on each Call Observation Date, including the Final Valuation Date, and the Final Value of the Least Performing Underlying will be below its Buffer Value. |

| 4 | You are unwilling to make an investment that is exposed to the potential downside performance of the Least Performing Underlying on a 1.25-to-1 basis. |

| 4 | You seek an investment that provides full return of principal at maturity. |

| 4 | You are unable or unwilling to hold Notes that will be automatically called on any Call Observation Date on which the Official Closing Value of each Underlying is at or above its Initial Value, or you are otherwise unable or unwilling to hold the Notes to maturity. |

| 4 | You seek an investment whose return is not limited to the pre-specified Call Premiums or the Rebate Return. |

| 4 | You prefer to receive the dividends or other distributions paid on the stocks held by or included in the relevant Underlying. |

| 4 | You seek an investment with current income. |

| 4 | You seek an investment for which there will be an active secondary market. |

| 4 | You prefer the lower risk, and therefore accept the potentially lower returns, of conventional debt securities with comparable maturities issued by HSBC or another issuer with a similar credit rating. |

| 4 | You are not willing or are unable to assume the credit risk associated with HSBC, as Issuer of the Notes. |

| FWP-8 |

RISK FACTORS

We urge you to read the section “Risk Factors” beginning on page S-1 in the accompanying prospectus supplement, beginning on page S-1 of the accompanying Equity Index Underlying Supplement and beginning on page S-1 of the accompanying ETF Underlying Supplement. Investing in the Notes is not equivalent to investing directly in any of the stocks comprising or held by any Underlying. You should understand the risks of investing in the Notes and should reach an investment decision only after careful consideration, with your advisors, of the suitability of the Notes in light of your particular financial circumstances and the information set forth in this free writing prospectus and the accompanying prospectus, prospectus supplement, Equity Index Underlying Supplement and ETF Underlying Supplement.

In addition to the risks discussed below, you should review “Risk Factors” in the accompanying prospectus supplement, Equity Index Underlying Supplement and ETF Underlying Supplement including the explanation of risks relating to the Notes described in the following sections:

| 4 | “— Risks Relating to All Note Issuances” in the prospectus supplement; |

| 4 | “— General Risks Related to Indices” in the Equity Index Underlying Supplement; |

| 4 | “— Securities Prices Generally are Subject to Political, Economic, Financial and Social Factors that Apply to the Markets in which They Trade and, to a Lesser Extent, Foreign Markets” in the Equity Index Underlying Supplement; |

| 4 | “— Time Differences Between the Domestic and Foreign Markets and New York City May Create Discrepancies in the Trading Level or Price of the Notes” in the Equity Index Underlying Supplement; |

| 4 | “— General Risks Related to Index Funds” in the ETF Underlying Supplement; |

| 4 | “— Securities Prices Generally Are Subject to Political, Economic, Financial, and Social Factors that Apply to the Markets in which They Trade and, to a Lesser Extent, Foreign Markets” in the ETF Underlying Supplement; and |

| 4 | “— Time Differences Between the Domestic and Foreign Markets and New York City May Create Discrepancies in the Trading Level or Price of the Notes” in the ETF Underlying Supplement. |

You will be subject to significant risks not associated with conventional fixed-rate or floating-rate debt securities.

The Notes do not guarantee any return of principal and you may lose your entire initial investment.

The Notes do not guarantee any return of principal. The Notes differ from ordinary debt securities in that we will not pay you 100% of the Principal Amount of your Notes if the Notes are not automatically called and the Final Value of the Least Performing Underlying is less than its Buffer Value. In this case, the Payment at Maturity you will be entitled to receive may be less than the Principal Amount of the Notes and you will lose 1.25% for each 1% that the Final Return of the Least Performing Underlying is less than -20%. You may lose up to 100% of your investment at maturity.

You will not participate in any appreciation in the value of any of the Underlyings included in the Reference Asset.

The Notes will not pay more than the Principal Amount, plus any unpaid call payment, at maturity or if the Notes are automatically called. Even if the Final Return of each Underlying in the Reference Asset is greater than zero, you will not participate in the appreciation of any Underlying. Assuming the Notes are held to maturity, the maximum amount payable with respect to the Notes will not exceed the sum of the Principal Amount plus any call payments. Under no circumstances, regardless of the extent to which the value of any Underlying appreciates, will your return exceed the total amount of the call payments. In some cases, you may earn significantly less by investing in the Notes than you would have earned by investing in an instrument directly linked to the performance of the Underlyings included in the Reference Asset.

Your return on the Notes is limited.

Your potential gain on the Notes will be limited to the Call Premium applicable to a Call Observation Date or the Rebate Return, regardless of the appreciation in the Underlyings, which may be significant. You will not receive a return on the Notes greater than the Call Premiums or the Rebate Return, as applicable.

The Notes will not bear interest.

As a holder of the Notes, you will not receive interest payments.

The Notes are subject to the credit risk of HSBC USA Inc.

The Notes are senior unsecured debt obligations of the Issuer, HSBC, and are not, either directly or indirectly, an obligation of any third party. As further described in the accompanying prospectus supplement and prospectus, the Notes will rank on par with all of the other unsecured and unsubordinated debt obligations of HSBC, except such obligations as may be preferred by operation of law. Any payment to be made on the Notes, including any return of principal at maturity or upon early redemption, as applicable, depends on the ability of HSBC to satisfy its obligations as they come due. As a result, the actual and perceived creditworthiness of HSBC may affect the

| FWP-9 |

market value of the Notes and, in the event HSBC were to default on its obligations, you may not receive the amounts owed to you under the terms of the Notes.

If the Notes are not called, your return will be based on the Reference Return of the Least Performing Underlying.

If the Notes are not automatically called, your return will be based on the Reference Return of the Least Performing Underlying without regard to the performance of the other Underlying. As a result, you could lose all or some of your initial investment if the Final Value of the Least Performing Underlying is less than its Buffer Value, even if there is an increase in the value of the other Underlying. This could be the case even if the other Underlying increased by an amount greater than the decrease in the Least Performing Underlying.

The Notes may be automatically called prior to the Maturity Date.

If the Notes are automatically called, the holding period over which you will receive the applicable Call Premium could be as little as 6 months. There is no guarantee that you would be able to reinvest the proceeds from an investment in the Notes at a comparable return for a similar level of risk in the event the Notes are automatically called prior to the Maturity Date.

Since the Notes are linked to the performance of more than one Underlying, you will be fully exposed to the risk of fluctuations in the value of each Underlying.

Since the Notes are linked to the performance of more than one Underlying, the Notes will be linked to the individual performance of each Underlying. Because the Notes are not linked to a weighted basket, in which the risk is mitigated and diversified among all of the components of a basket, you will be exposed to the risk of fluctuations in the values of the Underlyings to the same degree for each Underlying. For example, in the case of notes linked to a weighted basket, the return would depend on the weighted aggregate performance of the basket components reflected as the basket return. Thus, the depreciation of any basket component could be mitigated by the appreciation of another basket component, as scaled by the weightings of such basket components. However, in the case of these Notes, the individual performance of each of the Underlyings would not be combined to calculate your return and the depreciation of one Underlying would not be mitigated by the appreciation of the other Underlying. Instead, your return would depend on the Least Performing Underlying.

Changes that affect the Underlyings may affect the market value of the Notes and the amount you will receive at maturity.

The policies of the reference sponsor or reference issuer of the relevant Underlying concerning additions, deletions and substitutions of the constituents comprising such Underlying and the manner in which the reference sponsor or reference issuer takes account of certain changes affecting those constituents included in such Underlying may affect the value of that Underlying. The policies of the reference sponsor or reference issuer with respect to the calculation of the relevant Underlying could also affect the value of such Underlying. The reference sponsor or reference issuer may discontinue or suspend calculation or dissemination of its relevant Underlying. Any such actions could affect the value of the Notes and the return on the Notes.

The Notes are not insured or guaranteed by any governmental agency of the United States or any other jurisdiction.

The Notes are not deposit liabilities or other obligations of a bank and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency or program of the United States or any other jurisdiction. An investment in the Notes is subject to the credit risk of HSBC, and in the event that HSBC is unable to pay its obligations as they become due, you may not receive the full Payment at Maturity on the Notes.

The Estimated Initial Value of the Notes, which will be determined by us on the Pricing Date, may be less than the price to public and may differ from the market value of the Notes in the secondary market, if any.

The Estimated Initial Value of the Notes will be calculated by us on the Pricing Date and may be less than the price to public. The Estimated Initial Value will reflect our internal funding rate, which is the borrowing rate we pay to issue market-linked securities, as well as the mid-market value of the embedded derivatives in the Notes. This internal funding rate is typically lower than the rate we would use when we issue conventional fixed or floating rate debt securities. As a result of the difference between our internal funding rate and the rate we would use when we issue conventional fixed or floating rate debt securities, the Estimated Initial Value of the Notes may be lower if it were based on the levels at which our fixed or floating rate debt securities trade in the secondary market. In addition, if we were to use the rate we use for our conventional fixed or floating rate debt issuances, we would expect the economic terms of the Notes to be more favorable to you. We will determine the value of the embedded derivatives in the Notes by reference to our or our affiliates’ internal pricing models. These pricing models consider certain assumptions and variables, which can include volatility and interest rates. Different pricing models and assumptions could provide valuations for the Notes that are different from our Estimated Initial Value. These pricing models rely in part on certain forecasts about future events, which may prove to be incorrect. The Estimated Initial Value does not represent a minimum price at which we or any of our affiliates would be willing to purchase your Notes in the secondary market (if any exists) at any time.

The price of your Notes in the secondary market, if any, immediately after the Pricing Date may be less than the price to public.

The price to public takes into account certain costs. These costs, which will be used or retained by us or one of our affiliates, include the underwriting discount, our affiliates’ projected hedging profits (which may or may not be realized) for assuming risks inherent in hedging our obligations under the Notes, and the costs associated with structuring and hedging our obligations under the Notes. If you were to sell your Notes in the secondary market, if any, the price you would receive for your Notes may be less than the price you paid for them

| FWP-10 |

because secondary market prices will not take into account these costs. The price of your Notes in the secondary market, if any, at any time after issuance will vary based on many factors, including the values of the Underlyings and changes in market conditions, and cannot be predicted with accuracy. The Notes are not designed to be short-term trading instruments, and you should, therefore, be able and willing to hold the Notes to maturity. Any sale of the Notes prior to maturity could result in a loss to you.

If we were to repurchase your Notes immediately after the Original Issue Date, the price you receive may be higher than the Estimated Initial Value of the Notes.

Assuming that all relevant factors remain constant after the Original Issue Date, the price at which HSBC Securities (USA) Inc. may initially buy or sell the Notes in the secondary market, if any, and the value that we may initially use for customer account statements, if we provide any customer account statements at all, may exceed the Estimated Initial Value on the Pricing Date for a temporary period expected to be approximately 4 months after the Original Issue Date. This temporary price difference may exist because, in our discretion, we may elect to effectively reimburse to investors a portion of the estimated cost of hedging our obligations under the Notes and other costs in connection with the Notes that we will no longer expect to incur over the term of the Notes. We will make such discretionary election and determine this temporary reimbursement period on the basis of a number of factors, including the tenor of the Notes and any agreement we may have with the distributors of the Notes. The amount of our estimated costs which we effectively reimburse to investors in this way may not be allocated ratably throughout the reimbursement period, and we may discontinue such reimbursement at any time or revise the duration of the reimbursement period after the Original Issue Date of the Notes based on changes in market conditions and other factors that cannot be predicted.

The amount payable on the Notes is not linked to the values of the Underlyings at any time other than the Call Observation Dates and the Final Valuation Date.

The payments on the Notes will be based on the Official Closing Values of the Underlyings on the Call Observation Dates, including the Final Valuation Date, subject to postponement for non-trading days and certain market disruption events. Even if the value of each Underlying is greater than or equal to its Initial Value during the term of the Notes other than on a Call Observation Date but then drops on a Call Observation Date to a value that is less than its Initial Value, the Notes will not be automatically called. Further, if the Notes are not called, even if the value of the Least Performing Underlying is greater than or equal to its Buffer Value during the term of the Notes other than on the Final Valuation Date but then decreases on the Final Valuation Date to a value that is less than the Buffer Value, the Payment at Maturity will be less, possibly significantly less, than it would have been had the Payment at Maturity been linked to the value of the Least Performing Underlying prior to such decrease. Although the actual values of the Underlyings on the Maturity Date or at other times during the term of the Notes may be higher than their respective values on the Call Observation Dates, whether the Notes will be called and the Payment at Maturity will be based solely on the Official Closing Values of the Underlyings on the Call Observation Dates.

The Notes lack liquidity.

The Notes will not be listed on any securities exchange. HSBC Securities (USA) Inc. is not required to offer to purchase the Notes in the secondary market, if any exists. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell the Notes easily. Because other dealers are not likely to make a secondary market for the Notes, the price at which you may be able to trade your Notes is likely to depend on the price, if any, at which HSBC Securities (USA) Inc. is willing to buy the Notes.

Potential conflicts of interest may exist.

HSBC and its affiliates play a variety of roles in connection with the issuance of the Notes, including acting as calculation agent and hedging our obligations under the Notes. In performing these duties, the economic interests of the calculation agent and other affiliates of ours are potentially adverse to your interests as an investor in the Notes. We will not have any obligation to consider your interests as a holder of the Notes in taking any action that might affect the value of your Notes.

Small-capitalization risk.

The RTY tracks companies that are considered small-capitalization. These companies often have greater stock price volatility, lower trading volume and less liquidity than large-capitalization companies and therefore the value of the RTY may be more volatile than an investment in stocks issued by large-capitalization companies. Stock prices of small-capitalization companies may also be more vulnerable than those of large-capitalization companies to adverse business and economic developments, and the stocks of small-capitalization companies may be thinly traded, making it difficult for the RTY to track them. In addition, small-capitalization companies are often less stable financially than large-capitalization companies and may depend on a small number of key personnel, making them more vulnerable to loss of personnel. Small-capitalization companies are often subject to less analyst coverage and may be in early, and less predictable, periods of their corporate existences. These companies tend to have smaller revenues, less diverse product lines, smaller shares of their product or service markets, fewer financial resources and competitive strengths than large-capitalization companies and are more susceptible to adverse developments related to their products.

Risks associated with non-U.S. companies.

The value of the EFA depends upon the stocks of non-U.S. companies, and thus involves risks associated with the home countries of those non-U.S. companies. The prices of these non-U.S. stocks may be affected by political, economic, financial and social factors in the home country of each applicable company, including changes in that country’s government, economic and fiscal policies, currency

| FWP-11 |

exchange laws or other laws or restrictions, which could affect the value of the Notes. These foreign securities may have less liquidity and could be more volatile than many of the securities traded in U.S. or other securities markets. Direct or indirect government intervention to stabilize the relevant foreign securities markets, as well as cross shareholdings in foreign companies, may affect trading levels or prices and volumes in those markets. The other special risks associated with foreign securities may include, but are not limited to: less liquidity and smaller market capitalizations; less rigorous regulation of securities markets; different accounting and disclosure standards; governmental interference; currency fluctuations; higher inflation; and social, economic and political uncertainties. These factors may adversely affect the performance of the EFA and, as a result, the value of the Notes.

The performance and market value of the EFA during periods of market volatility may not correlate with the performance of its underlying index as well as the net asset value per share of the EFA.

During periods of market volatility, securities underlying the EFA may be unavailable in the secondary market, market participants may be unable to calculate accurately the net asset value per share of the EFA and the liquidity of the EFA may be adversely affected. This kind of market volatility may also disrupt the ability of market participants to create and redeem shares of the EFA. Further, market volatility may adversely affect, sometimes materially, the prices at which market participants are willing to buy and sell shares of the EFA. As a result, under these circumstances, the market value of shares of the EFA may vary substantially from the net asset value per share of the EFA. For all of the foregoing reasons, the performance of the EFA may not correlate with the performance of its underlying index as well as the net asset value per share of the EFA, which could materially and adversely affect the value of the Notes in the secondary market and/or reduce your payment at maturity.

The Notes will not be adjusted for changes in exchange rates.

Although the equity securities that are held by the EFA are traded in currencies other than U.S. dollars, and your Notes are denominated in U.S. dollars, the amount payable on your Notes, if any, will not be adjusted for changes in the exchange rates between the U.S. dollar and the currencies in which these non-U.S. equity securities are denominated. Changes in exchange rates, however, may also reflect changes in the applicable non-U.S. economies that in turn may affect the value of the EFA, and therefore the value of your Notes. The amount we pay in respect of your Notes, if any, will be determined solely in accordance with the procedures described in this free writing prospectus.

Uncertain tax treatment.

For a discussion of the U.S. federal income tax consequences of your investment in a Note, please see the discussion under “U.S. Federal Income Tax Considerations” herein and the discussion under “U.S. Federal Income Tax Considerations” in the accompanying prospectus supplement.

| FWP-12 |

ILLUSTRATIVE EXAMPLES

The following table and examples are provided for illustrative purposes only and are hypothetical. They do not purport to be representative of every possible scenario concerning increases or decreases in the value of any Underlying relative to its Initial Value. We cannot predict the Official Closing Value of either Underlying on any Call Observation Date or the Final Valuation Date. The assumptions we have made in connection with the illustrations set forth below may not reflect actual events. You should not take this illustration or these examples as an indication or assurance of the expected performance of the Underlyings or return on the Notes.

The table below illustrates the Payment at Maturity on a $1,000 investment in the Notes for a hypothetical range of Final Returns of the Least Performing Underlying from 0% (the Notes will be automatically called if the Final Return of Least Performing Underlying is greater than or equal to 0%) to +100%. The following results are based solely on the assumptions outlined below. The “Hypothetical Return on the Notes” as used below is the number, expressed as a percentage, that results from comparing the Payment at Maturity per $1,000 Principal Amount to $1,000. You should consider carefully whether the Notes are suitable to your investment goals. The numbers appearing in the following table and examples have been rounded for ease of analysis. The following table and examples assume the following:

| 4 | Principal Amount: | $1,000 |

| 4 | Hypothetical Initial Values: | 1,000 for the RTY and 50 for the EFA |

| 4 | Buffer Value: | with respect to each Underlying, 80% of its Initial Value |

| 4 | Rebate Return: | 7% |

| 4 | Downside Leverage Factor: | 1.25 |

| 4 | Call Premiums and Call Prices on the Call Observation Dates: | |

| Call Observation Dates | Call Prices | Call Premiums |

| November 30, 2017 | $1,045 | 4.50% |

| May 31, 2018 | $1,090 | 9.00% |

| November 30, 2018 (Final Valuation Date) | $1,135 | 13.50% |

Hypothetical Final Return of the Least Performing Underlying |

Hypothetical Payment at Maturity |

Hypothetical Return on the Notes |

| 0.00% | N/A | N/A |

| -5.00% | $1,070.00 | 7.00% |

| -10.00% | $1,070.00 | 7.00% |

| -15.00% | $1,070.00 | 7.00% |

| -20.00% | $1,070.00 | 7.00% |

| -30.00% | $875.00 | -12.50% |

| -40.00% | $750.00 | -25.00% |

| -60.00% | $500.00 | -50.00% |

| -80.00% | $250.00 | -75.00% |

| -100.00% | $0.00 | -100.00% |

Summary of the Examples

| Notes Are Called on a Call Observation Date | Notes Are Not

Called on Any Call Observation Date | |||||||||

| Example 1 | Example 2 | Example 3 | Example 4 | Example 5 | ||||||

| RTY | EFA | RTY | EFA | RTY | EFA | RTY | EFA | RTY | EFA | |

| Initial Values | 1,000 | 50 | 1,000 | 50 | 1,000 | 50 | 1,000 | 50 | 1,000 | 50 |

| Buffer Values | 800 | 40 | 800 | 40 | 800 | 40 | 800 | 40 | 800 | 40 |

| Official Closing Values /Percentage Changes on the First Call Observation Date | 1,200/ 20% |

60/ 20% |

900/ -10% |

55/ 10% |

900/ -10% |

55/ 10% |

900/ -10% |

55/ 10% |

900/ -10% |

45/ -10% |

| Official Closing Values /Percentage Changes on the Second Call Observation Date | N/A | N/A | 1,100/ 10% |

60/ 20% |

850/ -15% |

45/ -10% |

780/ -22% |

60/ 20% |

950/ -5% |

55/ 10% |

| Official Closing Values /Percentage Changes on the Final Call Observation Date | N/A | N/A | N/A | N/A | 1,350/ 35% |

75/ 50% |

850/ -15% |

65/ 30% |

600/ -40% |

60/ 20% |

| Return of the Notes | 4.50% | 9.00% | 13.50% | 7.00% | -25.00% | |||||

Call Price or Payment at Maturity per Note |

$1,045 | $1,090 | $1,135 | $1,070 | $750.00 | |||||

| FWP-13 |

Notes Are Called on a Call Observation Date

The Notes are called because the Official Closing Value of each Underlying is at or above its Initial Value on one of the three Call Observation Dates, and you will receive the applicable Call Price.

Example 1—The Official Closing Value of each Underlying on the first Call Observation Date is greater than or equal to its Initial Value.

Because the Official Closing Value of each Underlying on the first Call Observation Date (expected to be November 30, 2017) is at or above its Initial Value, the Notes are automatically called at the applicable Call Price of $1,045 per Note, representing a 4.50% return on the Notes.

Example 2—The Official Closing Value of each Underlying on the second Call Observation Date is greater than or equal to its Initial Value.

Because (i) the Official Closing Value of one Underlying on the first Call Observation Date is below its Initial Value and (ii) the Official Closing Value of each Underlying on the second Call Observation Date (expected to be May 31, 2018) is above its Initial Value, the Notes are not called on the first Call Observation Date but are automatically called on the second Call Observation Date at the applicable Call Price of $1,090 per Note, representing a 9% return on the Notes.

Example 3—The Official Closing Value of each Underlying on the final Call Observation Date is greater than or equal to its Initial Value.

Because (i) the Official Closing Values of at least one Underlying on the first two Call Observation Dates are below its Initial Value and (ii) the Official Closing Value of each Underlying on the final Call Observation Date (which is also the Final Valuation Date) is above its Initial Value, the Notes are not called on the first two Call Observation Dates but are automatically called on the final Call Observation Date at the applicable Call Price of $1,135 per Note, representing a 13.50% return on the Notes.

Notes Are Not Called on any Call Observation Date

The Notes are not automatically called because the Official Closing Value of at least one Underlying is below its Initial Value on each Call Observation Date. Since the Notes are not called, the Payment at Maturity will be based on the Final Return of the Least Performing Underlying.

Example 4—The Final Value of the Least Performing Underlying is greater than or equal to its Buffer Value.

Because the Final Value of the Least Performing Underlying is greater than or equal to its Buffer Value, you will receive $1,070 per $1,000 in Principal Amount, calculated as follows:

Payment at Maturity = $1,000 + ($1,000 × 7%) = $1,070

Example 5—The Final Value of the Least Performing Underlying is less than its Buffer Value.

Because the Final Value of the Least Performing Underlying is less than its Buffer Value, you will receive $750.00 per $1,000 in Principal Amount, calculated as follows:

Payment at Maturity = $1,000 + [$1,000 × (-40.00% + 20%) × 1.25] = $750.00

In this example, you would lose some or all of your Principal Amount at maturity.

If the Notes are not called and the Final Value of the Least Performing Underlying is less than its Buffer Value, you will be exposed to any decrease in the value of the Least Performing Underlying beyond -20% on a 1.25:1 basis and could lose up to 100% of your principal at maturity.

| FWP-14 |

INFORMATION RELATING TO THE UNDERLYINGS

Description of the RTY

The RTY is designed to track the performance of the small capitalization segment of the United States equity market. All 2,000 stocks are traded on the New York Stock Exchange or NASDAQ, and the RTY consists of the smallest 2,000 companies included in the Russell 3000® Index. The Russell 3000® Index is composed of the 3,000 largest United States companies as determined by market capitalization and represents approximately 98% of the United States equity market.

The top 5 industry groups by market capitalization as of April 30, 2017 were: Financial Services, Technology, Producer Durables, Consumer Discretionary and Health Care.

For more information about the RTY, see “The Russell 2000Ò Index” beginning on page S-36 of the accompanying Equity Index Underlying Supplement. |

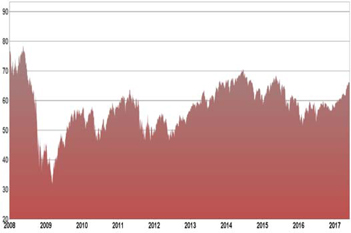

Historical Performance of the RTY

The following graph sets forth the historical performance of the RTY based on the daily historical closing values from January 1, 2008 through May 30, 2017. We obtained the closing values below from the Bloomberg Professional® service. We have not undertaken any independent review of, or made any due diligence inquiry with respect to, the information obtained from the Bloomberg Professional® service.

|

The historical values of the RTY should not be taken as an indication of future performance, and no assurance can be given as to the Official Closing Value of the RTY on any Call Observation Date or the Final Valuation Date.

| FWP-15 |

Description of the EFA

The EFA seeks investment results that correspond generally to the price and yield performance, before fees and expenses, of publicly traded securities in the European, Australasian, and Far Eastern markets, as measured by the MSCI EAFE® Index, which is the underlying index of the EFA. As of April 30, 2017, the MSCI EAFE Index consisted of the following 21 component country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, The Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, and the United Kingdom. The returns of the EFA may be affected by certain management fees and other expenses, which are detailed in its prospectus.

For more information about the EFA, see “The iShares® MSCI EAFE Index Fund” beginning on page S-21 of the accompanying ETF Underlying Supplement. |

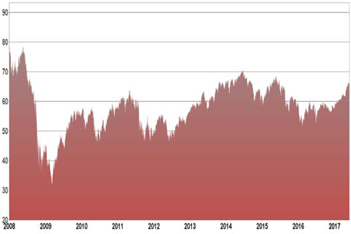

Historical Performance of the EFA

The following graph sets forth the historical performance of the EFA based on the daily historical closing values from January 1, 2008 through May 26, 2017. We obtained the closing values below from the Bloomberg Professional® service. We have not undertaken any independent review of, or made any due diligence inquiry with respect to, the information obtained from the Bloomberg Professional® service.

|

The historical closing levels below of the EFA should not be taken as an indication of future performance, and no assurance can be given as to the Official Closing Value of the EFA on any Observation Date or the Final Valuation Date.

| Quarter Begin | Quarter End | Quarterly High | Quarterly Low | Quarterly Close |

| 1/2/2008 | 3/31/2008 | 78.5 | 68.31 | 71.90 |

| 4/1/2008 | 6/30/2008 | 78.52 | 68.1 | 68.70 |

| 7/1/2008 | 9/30/2008 | 68.7 | 53.08 | 56.30 |

| 10/1/2008 | 12/31/2008 | 56.3 | 35.71 | 44.87 |

| 1/2/2009 | 3/31/2009 | 45.44 | 31.69 | 37.59 |

| 4/1/2009 | 6/30/2009 | 49.04 | 37.59 | 45.81 |

| 7/1/2009 | 9/30/2009 | 55.81 | 43.91 | 54.70 |

| 10/1/2009 | 12/31/2009 | 57.28 | 52.66 | 55.30 |

| 1/4/2010 | 3/31/2010 | 57.96 | 50.45 | 56.00 |

| 4/1/2010 | 6/30/2010 | 58.03 | 46.29 | 46.51 |

| 7/1/2010 | 9/30/2010 | 55.42 | 46.51 | 54.92 |

| 10/1/2010 | 12/31/2010 | 59.46 | 54.25 | 58.23 |

| 1/3/2011 | 3/31/2011 | 61.91 | 55.31 | 60.09 |

| 4/1/2011 | 6/30/2011 | 63.87 | 57.1 | 60.14 |

| 7/1/2011 | 9/30/2011 | 60.8 | 46.66 | 47.75 |

| 10/3/2011 | 12/30/2011 | 55.57 | 46.45 | 49.53 |

| 1/3/2012 | 3/30/2012 | 55.8 | 49.15 | 54.90 |

| 4/2/2012 | 6/29/2012 | 55.51 | 46.55 | 49.96 |

| 7/2/2012 | 9/28/2012 | 55.15 | 47.62 | 53.00 |

| 10/1/2012 | 12/31/2012 | 56.88 | 51.96 | 56.82 |

| 1/2/2013 | 3/29/2013 | 59.89 | 56.82 | 58.98 |

| 4/1/2013 | 6/28/2013 | 63.53 | 57.03 | 57.38 |

| 7/1/2013 | 9/30/2013 | 65.05 | 57.38 | 63.79 |

| 10/1/2013 | 12/31/2013 | 67.06 | 62.71 | 67.06 |

| 1/1/2014 | 3/31/2014 | 68.03 | 62.31 | 67.17 |

| 4/1/2014 | 6/30/2014 | 70.67 | 66.26 | 68.37 |

| 7/1/2014 | 9/30/2014 | 69.25 | 64.12 | 64.12 |

| 10/1/2014 | 12/31/2014 | 64.51 | 59.53 | 60.84 |

| 1/1/2015 | 3/31/2015 | 65.99 | 58.48 | 64.17 |

| 4/1/2015 | 6/30/2015 | 68.42 | 63.49 | 63.49 |

| 7/1/2015 | 9/30/2015 | 65.46 | 56.25 | 57.32 |

| 10/1/2015 | 12/31/2015 | 62.06 | 57.32 | 58.75 |

| 1/1/2016 | 3/31/2016 | 58.75 | 51.38 | 57.13 |

| 4/1/2016 | 6/30/2016 | 59.87 | 52.64 | 55.81 |

| 7/1/2016 | 9/30/2016 | 59.86 | 54.44 | 59.13 |

| 10/1/2016 | 12/31/2016 | 59.20 | 56.20 | 57.73 |

| 1/1/2017 | 3/31/2017 | 62.60 | 58.09 | 62.29 |

| 4/1/2017 | 5/26/2017* | 66.24 | 61.44 | 65.98 |

* This free writing prospectus includes information for the second calendar quarter of 2017 for the period from April 1, 2017 through May 30, 2017. Accordingly, the “Quarterly High,” “Quarterly Low” and “Quarterly Close” data indicated are for this shortened period only and do not reflect complete data for the second calendar quarter of 2017.

| FWP-16 |

EVENTS OF DEFAULT AND ACCELERATION

If the Notes have become immediately due and payable following an Event of Default (as defined in the accompanying prospectus) with respect to the Notes, the calculation agent will determine the accelerated payment due and payable in the same general manner as described in this free writing prospectus except that in such a case, the scheduled trading day immediately preceding the date of acceleration will be used as the final Call Observation Date and the Final Valuation Date. If the Notes are called, the calculation agent will determine the applicable Call Price based upon the Call Premiums and the amount of time that the Notes have been outstanding through the date of acceleration. If a market disruption event exists with respect to an Underlying on that scheduled trading day, then the accelerated Final Valuation Date will be postponed for up to five scheduled trading days (in the same manner used for postponing the originally scheduled Final Valuation Date). The accelerated Maturity Date will also be postponed by an equal number of business days following the postponed accelerated Final Valuation Date. For the avoidance of doubt, if no market disruption event exists with respect to an Underlying on the scheduled trading day preceding the date of acceleration, the determination of such Underlying’s Final Value will be made on such date, irrespective of the existence of a market disruption event with respect to the other Underlying occurring on such date.

If the Notes have become immediately due and payable following an Event of Default, you will not be entitled to any additional payments with respect to the Notes. For more information, see “Description of Debt Securities — Senior Debt Securities — Events of Default” in the accompanying prospectus.

SUPPLEMENTAL PLAN OF DISTRIBUTION (CONFLICTS OF INTEREST)

We have appointed HSBC Securities (USA) Inc., an affiliate of HSBC, as the agent for the sale of the Notes. Pursuant to the terms of a distribution agreement, HSBC Securities (USA) Inc. will purchase the Notes from HSBC at the price to public less the underwriting discount set forth on the cover page of the pricing supplement to which this free writing prospectus relates, for distribution to other registered broker-dealers or will offer the Notes directly to investors. HSBC Securities (USA) Inc. proposes to offer the Notes at the price to public set forth on the cover page of this free writing prospectus. HSBC USA Inc. or one of our affiliates may pay varying underwriting discounts of up to 0.05% per $1,000 Principal Amount of Notes in connection with the distribution of the Notes to other registered broker-dealers.

An affiliate of HSBC has paid or may pay in the future an amount to broker-dealers in connection with the costs of the continuing implementation of systems to support the Notes.

In addition, HSBC Securities (USA) Inc. or another of its affiliates or agents may use the pricing supplement to which this free writing prospectus relates in market-making transactions after the initial sale of the Notes, but is under no obligation to make a market in the Notes and may discontinue any market-making activities at any time without notice.

See “Supplemental Plan of Distribution (Conflicts of Interest)” on page S-59 in the prospectus supplement.

| FWP-17 |

U.S. FEDERAL INCOME TAX CONSIDERATIONS

There is no direct legal authority as to the proper tax treatment of the Notes, and therefore significant aspects of the tax treatment of the Notes are uncertain as to both the timing and character of any inclusion in income in respect of the Notes. Under one approach, a Note should be treated as a pre-paid executory contract with respect to the Reference Asset. We intend to treat the Notes consistent with this approach. Pursuant to the terms of the Notes, you agree to treat the Notes under this approach for all U.S. federal income tax purposes. Subject to the limitations described therein, and based on certain factual representations received from us, in the opinion of our special U.S. tax counsel, Morrison & Foerster LLP, it is reasonable to treat a Note as a pre-paid executory contract with respect to the Reference Asset. Pursuant to this approach and subject to the discussion below regarding “constructive ownership transactions,” we do not intend to report any income or gain with respect to the Notes prior to their maturity or an earlier sale, call or exchange and we intend to treat any gain or loss upon maturity or an earlier sale, call or exchange as long-term capital gain or loss provided that you have held the Note for more than one year at such time for U.S. federal income tax purposes.

Despite the foregoing, U.S. holders should be aware that the Internal Revenue Code of 1986, as amended (the “Code”), contains a provision, Section 1260 of the Code, which sets forth rules which are applicable to what it refers to as “constructive ownership transactions.” Due to the manner in which it is drafted, the precise applicability of Section 1260 of the Code to any particular transaction is often uncertain. In general, a “constructive ownership transaction” includes a contract under which an investor will receive payment equal to or credit for the future value of any equity interest in a regulated investment company (such as shares of the EFA (the “Underlying Shares”)). Under the “constructive ownership” rules, if an investment in the Notes is treated as a “constructive ownership transaction,” any long-term capital gain recognized by a U.S. holder in respect of a Note will be recharacterized as ordinary income to the extent such gain exceeds the amount of “net underlying long-term capital gain” (as defined in Section 1260 of the Code) (the “Excess Gain”). In addition, an interest charge will also apply to any deemed underpayment of tax in respect of any Excess Gain to the extent such gain would have resulted in gross income inclusion for the U.S. holder in taxable years prior to the taxable year of the sale, call, exchange or maturity of the Note (assuming such income accrued at a constant rate equal to the applicable federal rate as of the date of sale, call, exchange or maturity of the Note). Furthermore, unless otherwise established by clear and convincing evidence, the “net underlying long-term capital gain” is treated as zero.

Although the matter is not clear, there exists a risk that an investment in the Notes will be treated as a “constructive ownership transaction.” If such treatment applies, it is not entirely clear to what extent any long-term capital gain recognized by a U.S. holder in respect of a Note will be recharacterized as ordinary income. It is possible, for example, that the amount of the Excess Gain (if any) that would be recharacterized as ordinary income in respect of each Note will equal the excess of (i) any long-term capital gain recognized by the U.S. holder in respect of such a Note and attributable to the Underlying Shares over (ii) the “net underlying long-term capital gain” such U.S. holder would have had if such U.S. holder had acquired a number of the Underlying Shares at fair market value on the Original Issue Date of such Note for an amount equal to the “issue price” of the Note allocable to the Underlying Shares and, upon the date of sale, call, exchange or maturity of the Note, sold such Underlying Shares at fair market value (which would reflect the percentage increase in the value of the Underlying Shares over the term of the Note). Accordingly, it is possible that all or a portion of any gain upon maturity, sale, call or exchange of a Note after one year could be treated as “Excess Gain” from a “constructive ownership transaction,” which gain would be recharacterized as ordinary income, and subject to an interest charge. U.S. holders should consult their tax advisors regarding the potential application of the “constructive ownership” rules.

We will not attempt to ascertain whether an Underlying or any of the entities whose stock is included in, or owned by, an Underlying, as the case may be, would be treated as a passive foreign investment company (“PFIC”) or United States real property holding corporation (“USRPHC”), both as defined for U.S. federal income tax purposes. If an Underlying or one or more of the entities whose stock is included in, or owned by, an Underlying, as the case may be, were so treated, certain adverse U.S. federal income tax consequences might apply. You should refer to information filed with the SEC and other authorities by the Underlyings and the entities whose stock is included in, or owned by the Underlyings, as the case may be, and consult your tax advisor regarding the possible consequences to you if an Underlying or one or more of the entities whose stock is included in, or owned by, an Underlying, as the case may be, is or becomes a PFIC or a USRPHC.

Under current law, while the matter is not entirely clear, individual non-U.S. holders, and entities whose property is potentially includible in those individuals’ gross estates for U.S. federal estate tax purposes (for example, a trust funded by such an individual and with respect to which the individual has retained certain interests or powers), should note that, absent an applicable treaty benefit, the Notes are likely to be treated as U.S. situs property, subject to U.S. federal estate tax. These individuals and entities should consult their own tax advisors regarding the U.S. federal estate tax consequences of investing in the Notes.

A “dividend equivalent” payment is treated as a dividend from sources within the United States and such payments generally would be subject to a 30% U.S. withholding tax if paid to a non-U.S. holder. Under U.S. Treasury Department regulations, payments (including deemed payments) with respect to equity-linked instruments (“ELIs”) that are “specified ELIs” may be treated as dividend equivalents if such specified ELIs reference an interest in an “underlying security,” which is generally any interest in an entity taxable as a corporation for U.S. federal income tax purposes if a payment with respect to such interest could give rise to a U.S. source dividend. However, U.S. Treasury regulations provide that withholding on dividend equivalent payments will not apply to specified ELIs that are not delta-one instruments and that are issued before January 1, 2018. Based on the Issuer’s determination that the Notes are not “delta-one” instruments, non-U.S. holders should not be subject to withholding on dividend equivalent payments, if any, under the Notes. However, it

| FWP-18 |

is possible that the Notes could be treated as deemed reissued for U.S. federal income tax purposes upon the occurrence of certain events affecting an Underlying or the Notes, and following such occurrence the Notes could be treated as subject to withholding on dividend equivalent payments. Non-U.S. holders that enter, or have entered, into other transactions in respect of an Underlying or the Notes should consult their tax advisors as to the application of the dividend equivalent withholding tax in the context of the Notes and their other transactions. If any payments are treated as dividend equivalents subject to withholding, we (or the applicable paying agent) would be entitled to withhold taxes without being required to pay any additional amounts with respect to amounts so withheld.

Additionally, the IRS has announced that withholding under the Foreign Account Tax Compliance Act (as discussed in the accompanying prospectus supplement) on payments of gross proceeds from a sale, exchange, redemption, or other disposition of the Notes will only apply to dispositions after December 31, 2018.

For a discussion of the U.S. federal income tax consequences of your investment in a Note, please see the discussion under “U.S. Federal Income Tax Considerations” in the accompanying prospectus supplement.

| FWP-19 |

| TABLE OF CONTENTS | |||

You should only rely on the information contained in this free writing prospectus, the accompanying Equity Index Underlying Supplement, ETF Underlying Supplement, prospectus supplement and prospectus. We have not authorized anyone to provide you with information or to make any representation to you that is not contained in this free writing prospectus, the accompanying Equity Index Underlying Supplement, ETF Underlying Supplement, prospectus supplement and prospectus. If anyone provides you with different or inconsistent information, you should not rely on it. This free writing prospectus, the accompanying Equity Index Underlying Supplement, ETF Underlying Supplement, prospectus supplement and prospectus are not an offer to sell these Notes, and these documents are not soliciting an offer to buy these Notes, in any jurisdiction where the offer or sale is not permitted. You should not, under any circumstances, assume that the information in this free writing prospectus, the accompanying Equity Index Underlying Supplement, ETF Underlying Supplement, prospectus supplement and prospectus is correct on any date after their respective dates.

HSBC USA Inc.

$

Buffered Autocallable Yield Notes

May 31, 2017

FREE WRITING PROSPECTUS

| |||

| Free Writing Prospectus | |||

| General | FWP-6 | ||

| Payment on the Notes | FWP-6 | ||

| Investor Suitability | FWP-8 | ||

| Risk Factors | FWP-9 | ||

| Illustrative Examples | FWP-13 | ||

| Information Relating to the Underlyings | FWP-15 | ||

| Events of Default and Acceleration | FWP-17 | ||

| Supplemental Plan of Distribution (Conflicts of Interest) | FWP-17 | ||

| U.S. Federal Income Tax Considerations | FWP-18 | ||

| Equity Index Underlying Supplement | |||

| Disclaimer | S-1 | ||

| Risk Factors | S-2 | ||

| The DAX® Index | S-7 | ||

| The Dow Jones Industrial AverageSM | S-9 | ||

| The EURO STOXX 50® Index | S-11 | ||

| The FTSETM 100 Index | S-13 | ||

| The Hang Seng® Index | S-14 | ||

| The Hang Seng China Enterprises Index® | S-16 | ||

| The KOSPI 200 Index | S-19 | ||

| The MSCI Indices | S-22 | ||

| The NASDAQ-100 Index® | S-26 | ||

| The Nikkei 225 Index | S-30 | ||

| The PHLX Housing SectorSM Index | S-32 | ||

| The Russell 2000® Index | S-36 | ||

| The S&P 100® Index | S-40 | ||

| The S&P 500® Index | S-44 | ||

| The S&P 500® Low Volatility Index | S-47 | ||

| The S&P BRIC 40 Index | S-50 | ||

| The S&P MidCap 400® Index | S-52 | ||

| The TOPIX® Index | S-55 | ||

| Additional Terms of the Notes | S-57 | ||

| ETF Underlying Supplement | |||

| Risk Factors | S-1 | ||

| Reference Sponsors and Index Funds | S-7 | ||

| The Energy Select Sector SPDR® Fund | S-8 | ||

| The Financial Select Sector SPDR® Fund | S-10 | ||

| The Health Care Select Sector SPDR® Fund | S-12 | ||

| The iShares® China Large-Cap ETF | S-14 | ||

| The iShares® Latin America 40 ETF | S-17 | ||

| The iShares® MSCI Brazil Capped ETF | S-19 | ||

| The iShares® MSCI EAFE ETF | S-21 | ||

| The iShares® MSCI Emerging Markets ETF | S-23 | ||

| The iShares® MSCI Mexico Capped ETF | S-25 | ||

| The iShares® Transportation Average ETF | S-27 | ||

| The iShares® U.S. Real Estate ETF | S-28 | ||

| The Market Vectors® Gold Miners ETF | S-29 | ||

| The Powershares QQQ TrustSM, Series 1 | S-31 | ||

| The SPDR® Dow Jones Industrial AverageSM ETF Trust | S-34 | ||

| The SPDR® S&P 500® ETF Trust | S-36 | ||

| The Vanguard® FTSE Emerging Markets ETF | S-39 | ||

| The WisdomTree® Japan Hedged Equity Fund | S-42 | ||

| Additional Terms of the Notes | S-44 | ||

| Prospectus Supplement | |||

| Risk Factors | S-1 | ||

| Pricing Supplement | S-8 | ||

| Description of Notes | S-10 | ||

| Use of Proceeds and Hedging | S-33 | ||

| Certain ERISA Considerations | S-34 | ||

| U.S. Federal Income Tax Considerations | S-37 | ||

| Supplemental Plan of Distribution (Conflicts of Interest) | S-59 | ||

| Prospectus | |||

| About this Prospectus | 1 | ||

| Risk Factors | 2 | ||

| Where You Can Find More Information | 3 | ||

| Special Note Regarding Forward-Looking Statements | 4 | ||

| HSBC USA Inc. | 6 | ||

| Use of Proceeds | 7 | ||

| Description of Debt Securities | 8 | ||

| Description of Preferred Stock | 19 | ||

| Description of Warrants | 25 | ||

| Description of Purchase Contracts | 29 | ||

| Description of Units | 32 | ||

| Book-Entry Procedures | 35 | ||

| Limitations on Issuances in Bearer Form | 40 | ||

| U.S. Federal Income Tax Considerations Relating to Debt Securities | 40 | ||

| Plan of Distribution (Conflicts of Interest) | 49 | ||

| Notice to Canadian Investors | 52 | ||

| Notice to EEA Investors | 53 | ||

| Notice to UK Investors | 54 | ||

| UK Financial Promotion | 54 | ||

| Certain ERISA Matters | 54 | ||

| Legal Opinions | 57 | ||

| Experts | 58 |