Calculation of Registration Fee

| Title of Each Class of Securities Offered |

Maximum Aggregate Offering Price |

Amount of Registration Fee(1) | ||

| Debt Securities | $40,000,000 | $5,456 |

(1) Calculated in accordance with Rule 457(r) of the Securities Act of 1933, as amended.

|

Filed Pursuant to Rule 424(b)(2) Registration No. 333-180289 PRICING SUPPLEMENT Dated January 11, 2013 (To Prospectus dated March 22, 2012 and Prospectus Supplement dated March 22, 2012) |

| Structured Investments |

HSBC USA Inc. $40,000,000 Knock-Out Buffer Notes Linked to the Performance of the Mexican Peso Relative to the U.S. Dollar due January 28, 2014 |

General

| · | Terms used in this pricing supplement are described or defined herein, in the prospectus supplement and in the prospectus. The Notes will have the terms described herein and in the prospectus supplement and prospectus. The Notes do not guarantee any return of principal, and you may lose up to 100% of your initial investment. The Notes will not bear interest. |

| · | This pricing supplement relates to a single note offering. The purchaser of a Note will acquire a security linked to a single Reference Currency described below. |

| · | Although the offering relates to a Reference Currency, you should not construe that fact as a recommendation as to the merits of acquiring an investment linked to the Reference Currency or as to the suitability of an investment in the Notes. The Issuer has not undertaken any independent review of, or made any due diligence inquiry with respect to, publicly available information regarding the Reference Currency provided herein. |

| · | Senior unsecured debt obligations of HSBC USA Inc. maturing January 28, 2014. |

| · | Minimum denominations of $10,000 and integral multiples of $1,000 in excess thereof. |

| · | If the terms of the Notes set forth below are inconsistent with those described in the prospectus supplement and prospectus, the terms set forth below will supersede. |

| · | Any payment on the Notes is subject to the Issuer’s credit risk. |

Key Terms

| Issuer: | HSBC USA Inc. |

| Reference Currency: | Mexican Peso per one U.S. Dollar (“USDMXN”) |

| Knock-Out Event: | A Knock-Out Event occurs if on the Final Valuation Date the Reference Currency has depreciated, as compared to the Initial Spot Rate, by a percentage that is more than the Knock-Out Buffer Amount. |

| Knock-Out Buffer Amount: | 10% |

| Contingent Minimum Return: | 6.40% |

| Principal Amount: | $1,000 per Note. |

| Trade Date: | January 11, 2013 |

| Pricing Date: | January 11, 2013 |

| Original Issue Date: | January 18, 2013 |

| Final Valuation Date: | January 21, 2014, subject to adjustment as described herein. |

| Maturity Date: | January 28, 2014. The Maturity Date is subject to further adjustment as described under “Market Disruption Events” herein. |

| Payment at Maturity: | If a Knock-Out Event has occurred, you will receive a cash payment on the Maturity Date that will reflect the performance of the Reference Currency. Under these circumstances, your Payment at Maturity per $1,000 Principal Amount of Notes will be calculated as follows: |

| $1,000 + ($1,000 × Reference Currency Return) | |

| If a Knock-Out Event has occurred, you will lose some or all of your investment. This means that if the Reference Currency Return is -100%, you will lose your entire investment. | |

| If a Knock-Out Event has not occurred, you will receive a cash payment on the Maturity Date that will reflect the performance of the Reference Currency, subject to the Contingent Minimum Return. If a Knock-Out Event has not occurred, your Payment at Maturity per $1,000 Principal Amount of Notes will equal $1,000 plus the product of (a) $1,000 multiplied by (b) the greater of (i) the Reference Currency Return and (ii) the Contingent Minimum Return. For additional clarification, please see “What is the Total Return on the Notes at Maturity Assuming a Range of Performances for the Reference Currency?” herein. | |

| Reference Currency | The quotient, expressed as a percentage, calculated as follows: |

| Return: | Initial Spot Rate – Final Spot Rate |

| Initial Spot Rate | |

| Spot Rate: | The U.S. Dollar/Mexican Peso exchange rate expressed as the number of Mexican Pesos per one U.S. Dollar, for settlement on the same day, as reported on Reuters page “WMRSPOT01”, or any successor page, at 4:00 p.m., London time, on the date of calculation. The Spot Rate is subject to the provisions set forth under “Market Disruption Events” in this pricing supplement. The Spot Rate shall be calculated to the fourth or fifth decimal place, as reported on the applicable Reuters page. |

| Initial Spot Rate: | 12.64255 |

| Final Spot Rate: | The Spot Rate as determined by the Calculation Agent in its sole discretion on the Final Valuation Date. |

| Calculation Agent: | HSBC or one of its affiliates |

| CUSIP/ISIN: | 40432X7L9/US40432X7L99 |

| Form of Notes: | Book-Entry |

| Listing: | The Notes will not be listed on any U.S. securities exchange or quotation system. |

Investment in the Notes involves certain risks. You should refer to “Selected Risk Considerations” beginning on page 5 of this document and “Risk Factors” beginning on page S-3 of the prospectus supplement.

Neither the U.S. Securities and Exchange Commission, or SEC, nor any state securities commission has approved or disapproved of the Notes or determined that this pricing supplement, or the accompanying prospectus supplement and prospectus, is truthful or complete. Any representation to the contrary is a criminal offense.

HSBC Securities (USA) Inc. or another of our affiliates or agents may use this pricing supplement in market-making transactions in any Notes after their initial sale. Unless we or our agent informs you otherwise in the confirmation of sale, this pricing supplement is being used in a market-making transaction. HSBC Securities (USA) Inc., an affiliate of ours, will purchase the Notes from us for distribution to the placement agent. See “Supplemental Plan of Distribution (Conflicts of Interest)” on page 10 of this pricing supplement.

J.P. Morgan Securities LLC and certain of its registered broker-dealer affiliates are purchasing the Notes for resale.

| Price to Public | Fees and Commissions | Proceeds to Issuer | |

| Per Note | $1,000 | $10 | $990 |

| Total | $40,000,000 | $400,000 | $39,600,000 |

The Notes:

| Are Not FDIC Insured | Are Not Bank Guaranteed | May Lose Value |

JPMorgan

Placement Agent

January 11, 2013

Additional Terms Specific to the Notes

This pricing supplement relates to a single note offering linked to the Reference Currency identified on the cover page. The purchaser of a Note will acquire a senior unsecured debt security linked to the Reference Currency. Although the Note offering relates only to the Reference Currency identified on the cover page, you should not construe that fact as a recommendation as to the merits of acquiring an investment linked to the Reference Currency or as to the suitability of an investment in the Notes.

You should read this document together with the prospectus dated March 22, 2012 and the prospectus supplement dated March 22, 2012. If the terms of the Notes offered hereby are inconsistent with those described in the accompanying prospectus supplement or prospectus, the terms described in this pricing supplement shall control. You should carefully consider, among other things, the matters set forth in “Selected Risk Considerations” beginning on page 5 of this pricing supplement and “Risk Factors” beginning on page S-3 of the prospectus supplement, as the Notes involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting and other advisors before you invest in the Notes. As used herein, references to the “Issuer”, “HSBC”, “we”, “us” and “our” are to HSBC USA Inc.

HSBC has filed a registration statement (including a prospectus and a prospectus supplement) with the SEC for the offering to which this pricing supplement relates. Before you invest, you should read the prospectus and prospectus supplement in that registration statement and other documents HSBC has filed with the SEC for more complete information about HSBC and this offering. You may get these documents for free by visiting EDGAR on the SEC’s web site at www.sec.gov. Alternatively, HSBC Securities (USA) Inc. or any dealer participating in this offering will arrange to send you the prospectus and prospectus supplement if you request them by calling toll-free 1-866-811-8049.

You may also obtain:

| • | The prospectus supplement at: www.sec.gov/Archives/edgar/data/83246/000104746912003151/a2208335z424b2.htm |

| • | The prospectus at: www.sec.gov/Archives/edgar/data/83246/000104746912003148/a2208395z424b2.htm |

| -2- |

Summary

The four charts below provide a summary of the Notes, including Note characteristics and risk considerations as well as an illustrative diagram and table reflecting hypothetical returns at maturity. These charts should be reviewed together with the disclosure regarding the Notes contained in this pricing supplement as well as in the accompanying prospectus and prospectus supplement.

The following charts illustrate the hypothetical total return at maturity on the Notes. The “total return” as used in this pricing supplement is the number, expressed as a percentage, that results from comparing the Payment at Maturity per $1,000 Principal Amount of Notes to $1,000. The hypothetical total returns set forth below reflect the Initial Spot Rate of 12.64255 and the other terms set forth below. The hypothetical total returns set forth below are for illustrative purposes only and may not be the actual total returns applicable to a purchaser of the Notes. The numbers appearing in the following table and examples have been rounded for ease of analysis.

| -3- |

Selected Purchase Considerations

| · | APPRECIATION POTENTIAL — The Notes provide the opportunity to participate in the appreciation of the Reference Currency at maturity. If a Knock-Out Event has not occurred, in addition to the Principal Amount, you will receive at maturity at least the Contingent Minimum Return on the Notes of 6.40%, or a minimum Payment at Maturity of at least $1,064.00 for every $1,000 Principal Amount of Notes. Because the Notes are our senior unsecured debt obligations, payment of any amount at maturity is subject to our ability to pay our obligations as they become due. | |

| · | THE CONTINGENT MINIMUM RETURN APPLIES ONLY IF A KNOCK-OUT EVENT HAS NOT OCCURRED — If a Knock-Out Event has not occurred, you will receive at least the Principal Amount and the Contingent Minimum Return at maturity even if the Reference Currency has depreciated against the U.S. Dollar as compared to the Initial Spot Rate. If a Knock-Out Event has occurred, you will lose 1% of your Principal Amount for every 1% that the Reference Currency has depreciated against the U.S. Dollar as compared to the Initial Spot Rate. If the Reference Currency Return is -100%, you will lose your entire investment. | |

| · | EXPOSURE TO THE MEXICAN PESO VERSUS THE U.S. DOLLAR — The return on the Notes is linked to the performance of the Mexican Peso, which we refer to as the Reference Currency, relative to the U.S. Dollar, and will enable you to participate in any appreciation of the Reference Currency relative to the U.S. Dollar from the Pricing Date to the Final Valuation Date. | |

| · | TAX TREATMENT — There is no direct legal authority as to the proper tax treatment of the Notes, and therefore significant aspects of the tax treatment of the Notes are uncertain as to both the timing and character of any inclusion in income in respect of the Notes. Under one approach, a Note should be treated as a pre-paid executory contract with respect to the Reference Currency. We intend to treat the Notes consistent with this approach. Pursuant to the terms of the Notes, you agree to treat the Notes under this approach for all U.S. federal income tax purposes. Subject to the limitations described therein, and based on certain factual representations received from us, in the opinion of our special U.S. tax counsel, Morrison & Foerster LLP, it is reasonable to treat a Note as a pre-paid executory contract with respect to the Reference Currency. Assuming this characterization is respected, upon a sale or exchange of a Note, you should recognize gain or loss equal to the difference between the amount realized on the sale or exchange and your tax basis in the Note, which should equal the amount you paid to acquire the Note. Your gain or loss should generally be exchange gain or loss that is taxable as ordinary income or loss for U.S. federal income tax purposes, unless an election under Section 988 of the Internal Revenue Code of 1986, as amended (the “Code”) is available and made to treat such gain or loss as capital gain or loss (“Section 988 election”). The Section 988 election is generally available for a forward contract, a futures contract, or option on foreign currencies as described in Section 988 of the Code. Although not clear, a U.S. Holder (as defined in the accompanying prospectus supplement) may be entitled to make a Section 988 election with respect to the Notes. If a Section 988 election is available in respect of the Notes, in order for the election to be valid, a U.S. Holder must: (A) make the Section 988 election by clearly identifying the investment in the Notes on its books and records on the date the holder acquires the Notes as being subject to the Section 988 election (although no specific language or account is necessary for identifying a transaction on the holder’s books and records, the method of identification must be consistently applied and must clearly identify the pertinent transaction as subject to the Section 988 election); and (B) verify the election by attaching a statement to the holder’s income tax return, which must include (i) a description and the date of the Section 988 election, (ii) a statement that the Section 988 election was made before the close of the date that the Notes were acquired, (iii) a description of the Notes and the maturity date of the Notes or, alternatively, the date on which the Notes were sold or exchanged, (iv) a statement that the Notes were never part of a “straddle” as defined in Section 1092 of the Code, and (v) a statement that all transactions subject to the Section 988 election are included on the statement attached to the holder’s income tax return. If a Section 988 election is available and validly made in respect of the Notes, gain or loss recognized upon the sale or exchange of the Notes should be treated as capital gain or loss. Capital gain recognized by an individual U.S. Holder is generally taxed at preferential rates where the property is held for more than one year and is generally taxed at ordinary income rates where the property is held for one year or less. The deductibility of capital losses is subject to limitations. Prospective investors should consult their tax advisors regarding the availability, applicable procedures and requirements, and consequences of making a Section 988 election in respect of the Notes. | |

Due to the absence of authorities that directly address the proper characterization of the Notes, no assurance can be given that the Internal Revenue Service (the “IRS”) will accept, or that a court will uphold, this characterization and tax treatment of the Notes, in which case the timing and character of any income or loss on the notes could be significantly and adversely affected. For example, the Notes could be treated either as ”foreign currency contracts” within the meaning of Section 1256 of the Code or as “contingent payment debt instruments”, as discussed in the section entitled “U.S. Federal Income Tax Considerations” in the accompanying prospectus supplement.

In 2007, the IRS released a revenue ruling holding that a financial instrument with some arguable similarity to the Notes is properly treated as a debt instrument denominated in a foreign currency. The Notes are distinguishable in meaningful respects from the instruments described in the revenue ruling. If, however, the reach of the revenue

| -4- |

ruling were to be extended, it could materially and adversely affect the tax consequences of an investment in the Notes for U.S. Holders, possibly with retroactive effect.

For a discussion of the U.S. federal income tax consequences of your investment in a Note, please see the discussion under “U.S. Federal Income Tax Considerations” in the accompanying prospectus supplement.

Selected Risk Considerations

An investment in the Notes involves significant risks. Investing in the Notes is not equivalent to investing directly in the Reference Currency. These risks are explained in more detail in the “Risk Factors” section of the accompanying prospectus supplement.

| · | SUITABILITY OF THE NOTES FOR INVESTMENT — You should only reach a decision to invest in the Notes after carefully considering, with your advisors, the suitability of the Notes in light of your investment objectives and the information set out in this pricing supplement. Neither HSBC nor any dealer participating in the offering makes any recommendation as to the suitability of the Notes for investment. | |

| · | YOUR INVESTMENT IN THE NOTES MAY RESULT IN A LOSS — The Notes do not guarantee any return of principal. The return on the Notes at maturity is linked to the performance of the Reference Currency and will depend on whether, and the extent to which, the Reference Currency appreciates or depreciates. If the Reference Currency has depreciated, as compared to the Initial Spot Rate, by more than the Knock-Out Buffer Amount of 10%, a Knock-Out Event has occurred, and the benefit provided by the Knock-Out Buffer Amount will terminate. In such a case, you will lose 1% of the Principal Amount of the Notes for every 1% depreciation of the Reference Currency as compared to the Initial Spot Rate. IF A KNOCK-OUT EVENT OCCURS, YOU MAY LOSE UP TO 100% OF YOUR INVESTMENT. | |

| · | THE NOTES ARE SUBJECT TO THE CREDIT RISK OF HSBC USA INC. — The Notes are senior unsecured debt obligations of the Issuer, HSBC, and are not, either directly or indirectly, an obligation of any third party. As further described in the accompanying prospectus supplement and prospectus, the Notes will rank on par with all of the other unsecured and unsubordinated debt obligations of HSBC, except such obligations as may be preferred by operation of law. Any payment to be made on the Notes, including any return of principal at maturity, depends on the ability of HSBC to satisfy its obligations as they come due. As a result, the actual and perceived creditworthiness of HSBC may affect the market value of the Notes and, in the event HSBC were to default on its obligations, you may not receive the amounts owed to you under the terms of the Notes. | |

| · | INVESTING IN THE NOTES IS NOT EQUIVALENT TO INVESTING DIRECTLY IN THE REFERENCE CURRENCY — You may receive a lower return than you would have received if you had invested directly in the Reference Currency. The Reference Currency Return is dependent solely on the formula set forth above and not on any other formula that could be used for calculating currency performances. As such, the Reference Currency Return may be materially different from the return on a direct investment in the Reference Currency. | |

| · | CURRENCY MARKETS MAY BE VOLATILE — Currency markets may be highly volatile. Significant changes, including changes in liquidity and prices, can occur in such markets within very short periods of time. Foreign currency rate risks include, but are not limited to, convertibility risk and market volatility and potential interference by foreign governments through regulation of local markets, foreign investment or particular transactions in foreign currency. These factors may affect the value of the Reference Currency on the Final Valuation Date, and therefore, the value of your Notes. | |

| · | LEGAL AND REGULATORY RISKS — Legal and regulatory changes could adversely affect exchange rates. In addition, many governmental agencies and regulatory organizations are authorized to take extraordinary actions in the event of market emergencies. It is not possible to predict the effect of any future legal or regulatory action relating to exchange rates, but any such action could cause unexpected volatility and instability in currency markets with a substantial and adverse effect on the performance of the Reference Currency and, consequently, the value of the Notes. | |

| · | IF THE LIQUIDITY OF THE REFERENCE CURRENCY IS LIMITED, THE VALUE OF THE NOTES WOULD LIKELY BE IMPAIRED — Currencies and derivatives contracts on currencies may be difficult to buy or sell, particularly during adverse market conditions. Reduced liquidity on the Final Valuation Date would likely have an adverse effect on the Final Spot Rate for the Reference Currency, and therefore, on the return of your Notes. Limited liquidity relating to the Reference Currency may also result in HSBC USA Inc. or one of its affiliates, as Calculation Agent, being unable to determine the Reference Currency Return using its normal means. The resulting discretion by the Calculation Agent in determining the Reference Currency Return could, in turn, result in potential conflicts of interest. | |

| · | WE HAVE NO CONTROL OVER THE EXCHANGE RATE BETWEEN THE REFERENCE CURRENCY AND THE U.S. DOLLAR — Foreign exchange rates can either float or be fixed by sovereign governments. Exchange rates of the currencies used by most economically developed nations are permitted to fluctuate in value relative to the U.S. Dollar and to each other. However, from time to time, governments may use a variety of techniques, such as intervention by a central bank, the imposition of regulatory controls or taxes or changes in interest rates to influence the exchange rates of their currencies. Governments may also issue a new currency to replace an existing currency or alter the exchange rate or relative exchange characteristics by a devaluation or revaluation of a currency. These governmental actions could change or interfere with currency valuations and currency fluctuations that would otherwise occur in response to economic forces, as well as in response to the movement of currencies across borders. As a consequence, these government actions could adversely affect an investment in the Notes which are affected by the exchange rate between the Reference Currency and the U.S. Dollar. | |

| · | THE PAYMENT FORMULA FOR THE NOTES WILL NOT TAKE INTO ACCOUNT ALL DEVELOPMENTS IN THE REFERENCE CURRENCY — Changes in the Reference Currency during the term of the Notes other than on the Final Valuation Date may not be reflected in the calculation of the Payment at Maturity. The Reference Currency | |

| -5- |

| Return will be calculated only as of the Final Valuation Date. As a result, the Reference Currency Return may be less than zero even if the Reference Currency had moved favorably at certain times during the term of the Notes before moving to an unfavorable level on the Final Valuation Date. | ||

| · | THE NOTES ARE SUBJECT TO EMERGING MARKETS’ POLITICAL AND ECONOMIC RISKS — The Reference Currency is the currency of an emerging market country. Emerging market countries are more exposed to the risk of swift political change and economic downturns than their industrialized counterparts. In recent years, emerging markets have undergone significant political, economic and social change. Such far-reaching political changes have resulted in constitutional and social tensions, and, in some cases, instability and reaction against market reforms have occurred. With respect to any emerging or developing nation, there is the possibility of nationalization, expropriation or confiscation, political changes, government regulation and social instability. There can be no assurance that future political changes will not adversely affect the economic conditions of an emerging or developing-market nation. Political or economic instability is likely to have an adverse effect on the performance of the Reference Currency, and, consequently, the return on the Notes. | |

| · | THE NOTES ARE SUBJECT TO CURRENCY EXCHANGE RISK — Foreign currency exchange rates vary over time, and may vary considerably during the term of the Notes. The relative values of the U.S. Dollar and the Reference Currency are at any moment a result of the supply and demand for such currencies. Changes in foreign currency exchange rates result over time from the interaction of many factors directly or indirectly affecting economic and political developments in other relevant countries. Of particular importance to currency exchange risk are: | |

| · | existing and expected rates of inflation; | |

| · | existing and expected interest rate levels; | |

| · | the balance of payments in the United States and Mexico between each country and its major trading partners; and | |

| · | the extent of governmental surplus or deficit in the United States and Mexico. | |

Each of these factors, among others, are sensitive to the monetary, fiscal and trade policies pursued by the United States, Mexico, and those of other countries important to international trade and finance.

| · | NO INTEREST PAYMENTS — As a holder of the Notes, you will not receive interest payments. | |

| · | Potentially inconsistent research, opinions or recommendations by HSBC and JPMorgan — HSBC, JPMorgan, or their respective affiliates may publish research, express opinions or provide recommendations that are inconsistent with investing in or holding the Notes and which may be revised at any time. Any such research, opinions or recommendations could affect the exchange rate between the Reference Currency and the U.S. Dollar, and therefore, the market value of the Notes. | |

| · | CERTAIN BUILT-IN COSTS ARE LIKELY TO ADVERSELY AFFECT THE VALUE OF THE NOTES PRIOR TO MATURITY — While the Payment at Maturity described in this pricing supplement is based on the full Principal Amount of your Notes, the original issue price of the Notes includes the placement agent’s commission and the estimated cost of hedging our obligations under the Notes through one or more of our affiliates. As a result, the price, if any, at which HSBC Securities (USA) Inc. will be willing to purchase Notes from you in secondary market transactions, if at all, will likely be lower than the original issue price, and any sale of Notes by you prior to the Maturity Date could result in a substantial loss to you. The Notes are not designed to be short-term trading instruments. Accordingly, you should be able and willing to hold your Notes to maturity. | |

| · | THE NOTES LACK LIQUIDITY — The Notes will not be listed on any securities exchange. HSBC Securities (USA) Inc. may offer to purchase the Notes in the secondary market. However, it is not required to do so and may cease making such offers at any time if at all. Because other dealers are not likely to make a secondary market for the Notes, the price at which you may be able to trade your Notes is likely to depend on the price, if any, at which HSBC Securities (USA) Inc. is willing to buy the Notes. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell the Notes easily. | |

| · | POTENTIAL CONFLICTS — HSBC and its affiliates play a variety of roles in connection with the issuance of the Notes, including acting as Calculation Agent and hedging its obligations under the Notes. In performing these duties, the economic interests of the Calculation Agent and other affiliates of HSBC are potentially adverse to your interests as an investor in the Notes. The Initial Spot Rate for the Reference Currency is an intra-day level on the Pricing Date that was determined by the Calculation Agent. Although the Calculation Agent has made all determinations and taken all actions in relation to the establishment of the Initial Spot Rate in good faith, it should be noted that such discretion could have an impact (positive or negative) on the value of your Notes. HSBC and the Calculation Agent are under no obligation to consider your interests as a holder of the Notes in taking any corporate actions or other actions, including the determination of the Initial Spot Rate, that might affect the Reference Currency and the value of your Notes. | |

| · | The Notes are Not Insured OR GUARANTEED by any Governmental Agency of the United States or any Other Jurisdiction — The Notes are not deposit liabilities or other obligations of a bank and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency or program of the United States or any other jurisdiction. An investment in the Notes is subject to the credit risk of HSBC, and in the event that HSBC is unable to pay its obligations as they become due, you may not receive the full Payment at Maturity of the Notes. | |

| · | HISTORICAL PERFORMANCE OF THE REFERENCE CURRENCY SHOULD NOT BE TAKEN AS AN INDICATION OF THE FUTURE PERFORMANCE OF THE REFERENCE CURRENCY DURING THE TERM OF THE NOTES — It is impossible to predict whether the Spot Rate for the Reference Currency will rise or fall. The Reference Currency will be influenced by complex and interrelated political, economic, financial and other factors. | |

| -6- |

| · | MARKET DISRUPTIONS MAY ADVERSELY AFFECT YOUR RETURN — The Calculation Agent may, in its sole discretion, determine that the markets have been affected in a manner that prevents it from determining the Reference Currency Return in the manner described herein, and calculating the amount that we are required to pay you upon maturity, or from properly hedging its obligations under the Notes. These events may include disruptions or suspensions of trading in the markets as a whole or general inconvertibility or non-transferability of one or more currencies. If the Calculation Agent, in its sole discretion, determines that any of these events prevents us or any of our affiliates from properly hedging our obligations under the Notes or prevents the Calculation Agent from determining the Reference Currency Return or Payment at Maturity in the ordinary manner, the Calculation Agent will determine the Reference Currency Return or Payment at Maturity in good faith and in a commercially reasonable manner, and it is possible that the Final Valuation Date and the Maturity Date will be postponed, which may adversely affect the return on your Notes. For example, if the source for an exchange rate is not available on the Final Valuation Date, the Calculation Agent may determine the exchange rate for such date, and such determination may adversely affect the return on your Notes. | |

| · | MANY ECONOMIC AND MARKET FACTORS WILL IMPACT THE VALUE OF THE NOTES — In addition to the Spot Rate of the Reference Currency on any day, the value of the Notes will be affected by a number of economic and market factors that may either offset or magnify each other, including: | |

| · | the actual and expected exchange rates and volatility of the exchange rates between the Reference Currency and the U.S. Dollar; | |

| · | the time to maturity of the Notes; | |

| · | interest and yield rates in the market generally and in the markets of the Reference Currency and the U.S. Dollar; | |

| · | a variety of economic, financial, political, regulatory or judicial events; and | |

| · | our creditworthiness, including actual or anticipated downgrades in our credit ratings. | |

| -7- |

What Is the Total Return on the Notes at Maturity Assuming a Range of Performances for the Reference Currency?

The following table illustrates the hypothetical total return at maturity on the Notes. The “total return,” as used in this pricing supplement, is the number, expressed as a percentage, that results from comparing the Payment at Maturity per $1,000 Principal Amount of Notes to $1,000. The hypothetical total returns set forth below reflect the Knock-Out Buffer Amount of 10%, the Initial Spot Rate of 12.64255 and the Contingent Minimum Return on the Notes of 6.40%. The hypothetical total returns set forth below are for illustrative purposes only and may not be the actual total returns applicable to a purchaser of the Notes. The numbers appearing in the following table and examples have been rounded for ease of analysis.

| Hypothetical Final Spot Rate |

Hypothetical Reference Currency Return |

Hypothetical Total Return on the Notes |

| 0.00000 | 100.00% | 100.00% |

| 2.52851 | 80.00% | 80.00% |

| 5.05702 | 60.00% | 60.00% |

| 6.32128 | 50.00% | 50.00% |

| 7.58553 | 40.00% | 40.00% |

| 8.84979 | 30.00% | 30.00% |

| 9.48191 | 25.00% | 25.00% |

| 10.11404 | 20.00% | 20.00% |

| 11.37830 | 10.00% | 10.00% |

| 11.83343 | 6.40% | 6.40% |

| 12.01042 | 5.00% | 6.40% |

| 12.38970 | 2.00% | 6.40% |

| 12.64255 | 0.00% | 6.40% |

| 12.89540 | -2.00% | 6.40% |

| 13.27468 | -5.00% | 6.40% |

| 13.45167 | -6.40% | 6.40% |

| 13.90681 | -10.00% | 6.40% |

| 15.17106 | -20.00% | -20.00% |

| 15.80319 | -25.00% | -25.00% |

| 16.43532 | -30.00% | -30.00% |

| 17.69957 | -40.00% | -40.00% |

| 18.96383 | -50.00% | -50.00% |

| 20.22808 | -60.00% | -60.00% |

| 22.75659 | -80.00% | -80.00% |

| 25.28510 | -100.00% | -100.00% |

Hypothetical Examples of Amounts Payable at Maturity

The following examples illustrate how the total returns set forth in the table above are calculated.

Example 1: A Knock-Out Event has not occurred and the Reference Currency depreciates from the Initial Spot Rate of 12.64255 to a hypothetical Final Spot Rate of 13.27468. Because a Knock-Out Event has not occurred and the Reference Currency Return of -5.00% is less than the Contingent Minimum Return of 6.40%, the investor benefits from the Contingent Minimum Return and receives a Payment at Maturity of $1,064.00 per $1,000 Principal Amount of Notes.

$1,000 + ($1,000 × 6.40%) = $1,064.00

Example 2: A Knock-Out Event has not occurred and the Reference Currency appreciates from the Initial Spot Rate of 12.64255 to a hypothetical Final Spot Rate of 11.37830. Because a Knock-Out Event has not occurred and the Reference Currency Return of 10.00% is greater than the Contingent Minimum Return of 6.40%, the investor receives a Payment at Maturity of $1,100.00 per $1,000 Principal Amount of Notes, calculated as follows:

$1,000 + ($1,000 × 10.00%) = $1,100.00

Example 3: A Knock-Out Event has occurred and the Reference Currency depreciates from the Initial Spot Rate of 12.64255 to a hypothetical Final Spot Rate of 17.69957. Because a Knock-Out Event has occurred and the Reference Currency Return of -40.00% is greater than the Knock-Out Buffer Amount, the investor is exposed to the negative performance of the Reference Currency and receives a Payment at Maturity of $600.00 per $1,000 Principal Amount of Notes, calculated as follows:

$1,000 + ($1,000 × -40.00%) = $600.00

| -8- |

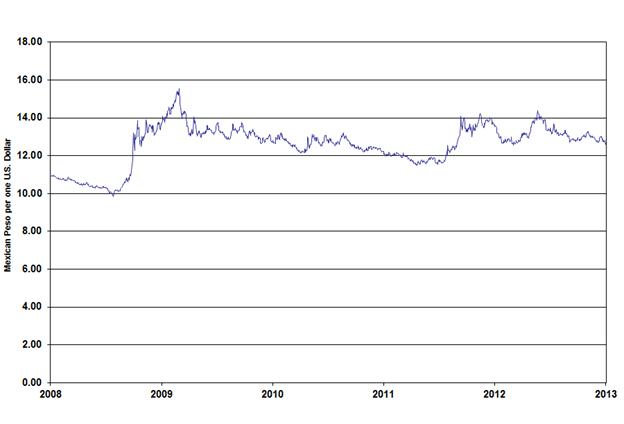

Historical Performance of the Reference Currency

The following graph sets forth the historical performance of the Reference Currency based on exchange rates of the Reference Currency relative to the U.S. Dollar from January 11, 2008 through January 11, 2013. The USDMXN exchange rate on January 11, 2013 was 12.64255. We obtained the exchange rates below from the Bloomberg Professional® service. We have not undertaken any independent review of, or made any due diligence inquiry with respect to, the information obtained from the Bloomberg Professional® service. The exchange rates displayed in the graph below are for illustrative purposes only and do not form part of the calculation of the Reference Currency Return.

The historical exchange rates should not be taken as an indication of future performance, and no assurance can be given as to the exchange rate on the Final Valuation Date. We cannot give you assurance that the performance of the Reference Currency will result in the return of any of your initial investment. The closing exchange rates in the graph below were the rates reported by the Bloomberg Professional® service and may not be indicative of the Reference Currency performance using the Spot Rates of the Reference Currency that would be derived from the applicable Reuters page that will be used to calculate the Reference Currency Return.

Historical Performance of the Mexican Peso

(expressed as the number of Mexican Pesos per one U.S. Dollar)

Source: Bloomberg Professional® service

| -9- |

Spot Rate

The Spot Rate for the Mexican Peso will be the U.S. Dollar/Mexican Peso rate for U.S. Dollars, expressed as the amount of Mexican Pesos per one U.S. Dollar, for settlement on the same day, as reported on Reuters page “WMRSPOT01”, or any successor page, at 4:00 p.m., London time, on the date of calculation. The Spot Rate shall be calculated to the fourth or fifth decimal place, as reported on the applicable Reuters page.

If the Spot Rate is unavailable (including being published in error, as determined by the Calculation Agent in its sole discretion), the Spot Rate for the Reference Currency shall be selected by the Calculation Agent in good faith and in a commercially reasonable manner, or the Final Valuation Date may be postponed by the Calculation Agent, as described below in “Market Disruption Events.”

Market Disruption Events

The Calculation Agent may, in its sole discretion, determine that an event has occurred that prevents us or our affiliates from properly hedging our obligations under the Notes or prevents the Calculation Agent from valuing the Reference Currency in the manner initially provided for herein. These events may include disruptions or suspensions of trading in the markets as a whole or general inconvertibility or non-transferability of the Reference Currency. If the Calculation Agent, in its sole discretion, determines that any of these events has occurred or is occurring on the Final Valuation Date, the Calculation Agent may determine the Final Spot Rate in good faith and in a commercially reasonable manner on such date, or, in the discretion of the Calculation Agent, may determine to postpone the Final Valuation Date and Maturity Date for up to five scheduled trading days, each of which may adversely affect the return on your Notes. If the Final Valuation Date has been postponed for five consecutive scheduled trading days and a market disruption event continues on the fifth scheduled trading day, then that fifth scheduled trading day will nevertheless be the Final Valuation Date and the Calculation Agent will determine the Spot Rate of the Reference Currency using the formula for and method of determining such Spot Rate which applied just prior to the market disruption event (or in good faith and in a commercially reasonable manner) on such date.

If the Maturity Date is not a business day, the amounts payable on the Notes will be paid on the next following business day and no interest will be paid in respect of such postponement.

A “business day” means any day, other than a Saturday or Sunday, that is neither a legal holiday nor a day on which banking institutions are authorized or required by law or regulation to close in the City of New York.

Events of Default and Acceleration

If the Notes have become immediately due and payable following an event of default (as defined in the accompanying prospectus) with respect to the Notes, the Calculation Agent will determine the accelerated Payment at Maturity due and payable in the same general manner as described in “Key Terms” in this pricing supplement. In that case, the business day preceding the date of acceleration will be used as the Final Valuation Date for purposes of determining the accelerated Reference Currency Return (including the Final Spot Rate). The accelerated Maturity Date will be the fifth business day following the accelerated Final Valuation Date.

If the Notes have become immediately due and payable following an event of default, you will not be entitled to any additional payments with respect to the Notes. For more information, see “Description of Debt Securities — Senior Debt Securities — Events of Default” in the accompanying prospectus.

Supplemental Plan of Distribution (Conflicts of Interest)

Pursuant to the terms of a distribution agreement, HSBC Securities (USA) Inc., an affiliate of HSBC, will purchase the Notes from HSBC for distribution to J.P. Morgan Securities LLC and certain of its registered broker-dealer affiliates, acting as placement agent, at the price indicated on the cover of this pricing supplement. The placement agents for the Notes will receive a fee that will not exceed $10 per $1,000 Principal Amount of Notes.

In addition, HSBC Securities (USA) Inc. or another of its affiliates or agents may use this pricing supplement in market-making transactions after the initial sale of the Notes, but is under no obligation to make a market in the Notes and may discontinue any market-making activities at any time without notice.

See “Supplemental Plan of Distribution (Conflicts of Interest)” on page S-49 in the prospectus supplement.

Delivery of the Notes will be made against payment for the Notes on the Original Issue Date set forth on the cover page of this document, which is the fifth business day following the Trade Date of the Notes. Under Rule 15c6-1 under the Securities Exchange Act of 1934, trades in the secondary market generally are required to settle in three business days, unless the parties to that trade expressly agree otherwise. Accordingly, purchasers who wish to trade Notes on the Trade Date and the following business day thereafter will be required to specify an alternate settlement cycle at the time of any such trade to prevent a failed settlement, and should consult their own advisors.

| -10- |

Validity of the Notes

In the opinion of Morrison & Foerster LLP, as counsel to the Issuer, when the Notes offered by this pricing supplement have been executed and delivered by the Issuer and authenticated by the trustee pursuant to the Senior Indenture referred to in the prospectus supplement dated March 22, 2012, and issued and paid for as contemplated herein, such Notes will be valid, binding and enforceable obligations of the Issuer, entitled to the benefits of the Senior Indenture, subject to applicable bankruptcy, insolvency and similar laws affecting creditors’ rights generally, concepts of reasonableness and equitable principles of general applicability (including, without limitation, concepts of good faith, fair dealing and the lack of bad faith). This opinion is given as of the date hereof and is limited to the laws of the State of New York, the Maryland General Corporation Law (including the statutory provisions, all applicable provisions of the Maryland Constitution and the reported judicial decisions interpreting the foregoing) and the federal laws of the United States of America. This opinion is subject to customary assumptions about the trustee’s authorization, execution and delivery of the Senior Indenture and the genuineness of signatures and to such counsel’s reliance on the Issuer and other sources as to certain factual matters, all as stated in the legal opinion dated July 27, 2012, which has been filed as Exhibit 5.1 to the Issuer’s Current Report on Form 8-K dated July 27, 2012.

| -11- |