|

Filed Pursuant to Rule 433 Registration No. 333-158385 March 6, 2012 FREE WRITING PROSPECTUS (To Prospectus dated April 2, 2009 and Prospectus Supplement dated April 9, 2009) |

| Structured Investments |

HSBC USA Inc. $ Autocallable Notes Linked to S&P 500® Index due March 13, 2014 (the “Notes”) |

General

| · | Terms used in this free writing prospectus are described or defined herein, in the accompanying prospectus supplement and prospectus. The Notes offered will have the terms described in the prospectus supplement or prospectus. The Notes do not guarantee return of principal and you may lose up to 100.00% of your initial investment. The Notes will not bear interest. |

| · | This free writing prospectus relates to a single note offering. The purchaser of a Note will acquire a security linked to the Reference Asset described below. |

| · | Although the offering relates to the Reference Asset, you should not construe that fact as a recommendation as to the merits of acquiring an investment linked to the Reference Asset or any component security included in the Reference Asset or as to the suitability of an investment in the related Notes. |

| · | Senior unsecured debt obligations of HSBC USA Inc. maturing March 13, 2014. |

| · | Minimum denominations of $10,000 and integral multiples of $1,000 in excess thereof. |

Key Terms

| Issuer: | HSBC USA Inc. | |

| Issuer Rating: | A+ (S&P), A1 (Moody’s), AA (Fitch)* | |

| Reference Asset: | The S&P 500® Index (“SPX”) | |

| Principal Amount: | $1,000 per Note | |

| Trade Date: | March 9, 2012 | |

| Pricing Date: | March 9, 2012 | |

| Original Issue Date: | March 14, 2012 | |

| Final Valuation Date: | March 10, 2014, subject to adjustment as described below under the caption “Observation Dates, Cash Settlement Date and Maturity Date.” | |

| Maturity Date: | 3 business days after the Final Valuation Date and is expected to be March 13, 2014. The Maturity Date is subject to further adjustment as described herein under “Observation Dates, Cash Settlement Date and Maturity Date.” | |

| Call Feature: | The Notes will be automatically called if the Official Closing Level of the Reference Asset on any Observation Date is at or above the Initial Level. In such a case, you will receive a cash payment equal to the Call Price. | |

| Call Price: | If the Notes are automatically called, you will receive, on the applicable Call Settlement Date, a cash payment per $1,000 Principal Amount of Notes equal to the Principal Amount plus a Call Premium calculated as follows: | |

| · | 10.40% × $1,000 if automatically called on the first Observation Date; | |

| · | 15.60% × $1,000 if automatically called on the second Observation Date; and | |

| · | 20.80% × $1,000 if automatically called on the Final Valuation Date. | |

| Observation Dates: | March 18, 2013, September 10, 2013 and the Final Valuation Date (March 10, 2014), subject to postponement because of market disruption events as described herein. | |

| Call Settlement Date: | With respect to each Observation Date, including the Final Valuation Date, three business days following the applicable Observation Date. A Call Settlement Date is also subject to adjustment as described below under the caption “Observation Dates, Cash Settlement Date and Maturity Date.” | |

| Payment at Maturity: | If the Notes are not automatically called, you will receive a cash payment per $1,000 Principal Amount of Notes on the Maturity Date calculated as follows: | |

| · | If the Reference Return is less than zero but greater than or equal to the Buffer Level, you will receive a cash payment on the Maturity Date equal to 100% of the Principal Amount. | |

| · | If the Reference Return is less than the Buffer Level, you will receive a cash payment on the Maturity Date equal to: | |

| $1,000 + [$1,000 × (Reference Return + 10%) × 1.1111]. | ||

| For example, if the Reference Return is -11%, you will suffer a 1.1111% loss and receive 98.8889% of the Principal Amount. If the Reference Return is less than the Buffer Level, you may lose your entire investment. For additional clarification, please see “What is the Total Return on the Notes at Maturity Assuming a Range of Performance for the Reference Asset?” herein. | ||

| Buffer Level: | -10% | |

| Downside Leverage Factor: | 1.1111 | |

| Reference Return: | The quotient, expressed as a percentage, calculated as follows: | |

| Final Level – Initial Level | ||

| Initial Level | ||

| Initial Level: | The Official Closing Level of the Reference Asset on the Pricing Date. | |

| Final Level: | The Official Closing Level of the Reference Asset on the Final Valuation Date. | |

| Official Closing Level: | The closing level of the Reference Asset on any scheduled trading day as determined by the calculation agent based on the value displayed on Bloomberg Professional® service page “SPX <INDEX>” or any successor page on Bloomberg Professional® service or any successor service, as applicable. | |

| CUSIP/ISIN: | 4042K1ZS5 / | |

| Form of Notes: | Book-Entry | |

| Listing: | The Notes will not be listed on any U.S. securities exchange or quotation system. | |

* A credit rating reflects the creditworthiness of HSBC USA Inc. and is not indicative of the market risk associated with the Notes or the Reference Asset nor is it a recommendation to buy, sell or hold the Notes, and it may be subject to revision or withdrawal at any time by the assigning rating organization. The Notes themselves have not been independently rated. Each rating should be evaluated independently of any other rating.

Investment in the Notes involves certain risks. You should refer to “Selected Risk Considerations” beginning on page 3 of this document and “Risk Factors” on page and page S-3 of the prospectus supplement.

Neither the U.S. Securities and Exchange Commission, or the SEC, nor any state securities commission has approved or disapproved of the Notes or determined that this free writing prospectus, or the accompanying prospectus supplement and prospectus, is truthful or complete. Any representation to the contrary is a criminal offense.

HSBC Securities (USA) Inc. or another of our affiliates or agents may use the pricing supplement to which this free writing prospectus relates in market-making transactions in any Notes after their initial sale. Unless we or our agent informs you otherwise in the confirmation of sale, the pricing supplement to which this free writing prospectus relates will be used in a market-making transaction. HSBC Securities (USA) Inc., an affiliate of ours, will purchase the Notes from us for distribution to the placement agent. See “Supplemental Plan of Distribution (Conflicts of Interest)” on the last page of this free writing prospectus.

We have appointed J.P. Morgan Securities LLC and certain of its registered broker-dealer affiliates as placement agent for the sale of the Notes. J.P. Morgan Securities LLC and certain of its registered broker-dealer affiliates will offer the Notes to investors directly or through other registered broker-dealers.

| Price to Public(1) | Fees and Commissions | Proceeds to Issuer | |

| Per Note | $1,000 | $15 | $985 |

| Total | $ | $ | $ |

(1) Certain fiduciary accounts will pay a purchase price of $985 per Note, and the placement agents with respect to sales made to such accounts will forgo any fees.

The Notes:

| Are Not FDIC Insured | Are Not Bank Guaranteed | May Lose Value |

JPMorgan

Placement Agent

March 6, 2012

Additional Terms Specific to the Notes

This free writing prospectus relates to a single Note offering linked to the Reference Asset identified on the cover page. The purchaser of a Note will acquire a senior unsecured debt security linked to the Reference Asset. We reserve the right to withdraw, cancel or modify any offering and to reject orders in whole or in part. Although the Note offering relates only to the Reference Asset identified on the cover page, you should not construe that fact as a recommendation as to the merits of acquiring an investment linked to the Reference Asset or any securities derivative of or relating to the Reference Asset or as to the suitability of an investment in the Notes.

You should read this document together with the prospectus dated April 2, 2009, the prospectus supplement dated April 9, 2009. If the terms of the Notes offered hereby are inconsistent with those described in the accompanying prospectus supplement or prospectus, the terms described in this free writing prospectus shall control. You should carefully consider, among other things, the matters set forth in “Selected Risk Considerations” beginning on page 3 of this free writing prospectus and “Risk Factors” on page S-3 of the prospectus supplement, as the Notes involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting and other advisors before you invest in the Notes. As used herein, references to the “Issuer”, “HSBC”, “we”, “us” and “our” are to HSBC USA Inc.

HSBC has filed a registration statement (including a prospectus and a prospectus supplement) with the SEC for the offering to which this free writing prospectus relates. Before you invest, you should read the prospectus and prospectus supplement in that registration statement and other documents HSBC has filed with the SEC for more complete information about HSBC and this offering. You may get these documents for free by visiting EDGAR on the SEC’s web site at www.sec.gov. Alternatively, HSBC Securities (USA) Inc. or any dealer participating in this offering will arrange to send you the prospectus and prospectus supplement if you request them by calling toll-free 1 866 811 8049.

You may also obtain:

| • | the prospectus supplement at www.sec.gov/Archives/edgar/data/83246/000114420409019785/v145824_424b2.htm |

| • | the prospectus at www.sec.gov/Archives/edgar/data/83246/000104746909003736/a2192100zs-3asr.htm |

We are using this free writing prospectus to solicit from you an offer to purchase the Notes. You may revoke your offer to purchase the Notes at any time prior to the time at which we accept your offer by notifying HSBC Securities (USA) Inc. We reserve the right to change the terms of, or reject any offer to purchase, the Notes prior to their issuance. In the event of any material changes to the terms of the Notes, we will notify you.

Supplemental Information Relating to the Terms of the Notes

Notwithstanding anything contained in the accompanying prospectus supplement to the contrary, the Notes will be issued under the senior indenture dated March 31, 2009, between HSBC USA Inc., as Issuer, and Wells Fargo Bank, National Association, as trustee. Such indenture has substantially the same terms as the indenture described in the accompanying prospectus supplement. HSBC Bank USA, N.A. will act as paying agent with respect to the Notes pursuant to a Paying Agent and Securities Registrar Agreement dated June 1, 2009, between HSBC USA Inc. and HSBC Bank USA, N.A.

Selected Purchase Considerations

| · | CALL FEATURE — The Notes will be automatically called if the Official Closing Level on any Observation Date is at or above the Initial Level. If the Notes are automatically called, you will receive, on the applicable Call Settlement Date, a cash payment per $1,000 Principal Amount of Notes equal to the Principal Amount plus a Call Premium amount indicated on the cover hereof. |

| · | LIMITED BUFFER AGAINST LOSS — If the Notes are not automatically called, we will pay you your principal back at maturity if the Final Level is not less than the Initial Level by more than 10%. If the Final Level is less than the Initial Level by more than 10%, for every 1% that the Final Level is less than the Initial Level by more than 10%, you will lose an amount equal to 1.1111% of the $1,000 Principal Amount of Notes. You could lose your entire initial investment if the value of the Reference Asset falls to zero. |

| · | DIVERSIFICATION OF THE S&P 500® INDEX — The return on the Notes is linked to the S&P 500® Index. The S&P 500® Index consists of 500 component stocks selected to provide a performance benchmark for the U.S. equity markets. For additional information about the Reference Asset, see the information set forth under “Description of the Reference Asset” herein. |

| · | TAX TREATMENT — There is no direct legal authority as to the proper tax treatment of the Notes, and therefore significant aspects of the tax treatment of the Notes are uncertain as to both the timing and character of any inclusion in income in respect of the Notes. Under one approach, the Notes should be treated as pre-paid forward or other executory contracts with respect to the Reference Asset. We intend to treat the Notes consistent with this approach. Pursuant to the terms of the Notes, you agree to treat the Notes under this approach for all U.S. federal income tax purposes. Notwithstanding any disclosure in the accompanying prospectus supplement to the contrary, our special U.S. tax counsel in this transaction is Sidley Austin llp. Subject to the limitations described therein, and based on certain factual representations received from us, in the opinion of our special U.S. tax counsel, Sidley Austin llp, it is reasonable to treat the Notes as pre-paid forward or other executory contracts with respect to the Reference Asset. Pursuant to this approach, we do not intend to report any income or gain with respect to the Notes prior to their maturity or an earlier sale, call or exchange and we intend to treat any gain or loss upon maturity or an earlier sale, call or exchange as long-term capital gain or loss, provided that you have held the Note for more than one year at such time for U.S. federal income tax purposes. For a discussion of the U.S. federal income tax consequences of your investment in a Note, please see the discussion under “Certain U.S. Federal Income Tax Considerations” in the accompanying prospectus supplement. |

| -2- |

Selected Risk Considerations

An investment in the Notes involves significant risks. Investing in the Notes is not equivalent to investing directly in the Reference Asset. These risks are explained in more detail in the “Risk Factors” sections of the accompanying prospectus supplement.

| · | SUITABILITY OF NOTES FOR INVESTMENT – You should only reach a decision to invest in the Notes after carefully considering, with your advisors, the suitability of the Notes in light of your investment objectives and the information set out in this free writing prospectus. Neither HSBC nor any dealer participating in the offering makes any recommendation as to the suitability of the Notes for investment. |

| · | YOUR INVESTMENT IN THE NOTES MAY RESULT IN A LOSS — The Notes do not guarantee any return of principal. The Notes differ from ordinary debt securities in that we will not pay you 100% of the Principal Amount of your Notes if the Notes are not automatically called and the Reference Return is less than the Buffer Level. In this case, the Payment at Maturity you will be entitled to receive will be less than the Principal Amount of the Notes and you could lose your entire initial investment if the level of the Reference Asset falls to zero. An investment in the Notes does not guarantee return of principal and you may receive less at maturity than you originally invested in the Notes, or you may receive nothing at maturity. |

| · | Your return on the Notes is limited —If the Notes are not automatically called and the Final Level is greater than or equal to the Buffer Level, for each $1,000 Principal Amount Note, you will receive $1,000 at maturity, regardless of any appreciation in the level of the Reference Asset, which may be significant. Accordingly, the return on the Notes may be significantly less than the return on a direct investment in the Reference Asset during the term of the Notes. |

| · | CREDIT RISK OF HSBC USA INC. — The Notes are senior unsecured debt obligations of the Issuer, HSBC, and are not, either directly or indirectly, an obligation of any third party. As further described in the accompanying prospectus supplement and prospectus, the Notes will rank on par with all of the other unsecured and unsubordinated debt obligations of HSBC, except such obligations as may be preferred by operation of law. Any payment to be made on the Notes, including any return of principal at maturity or on the Call Settlement Date, as applicable, depends on the ability of HSBC to satisfy its obligations as they come due. As a result, the actual and perceived creditworthiness of HSBC may affect the market value of the Notes and, in the event HSBC were to default on its obligations, you may not receive the amounts owed to you under the terms of the Notes. |

| · | Potentially Inconsistent Research, Opinions or Recommendations by HSBC and JPMorgan — HSBC, JPMorgan, or their affiliates may publish research, express opinions or provide recommendations that are inconsistent with investing in or holding the Notes and which may be revised at any time. Any such research, opinions or recommendations could affect the level of the Reference Asset, and therefore, the market value of the Notes. |

| · | CERTAIN BUILT-IN COSTS ARE LIKELY TO ADVERSELY AFFECT THE VALUE OF THE NOTES PRIOR TO MATURITY — While the Payment at Maturity described in this free writing prospectus is based on the full Principal Amount of your Notes, the original issue price of the Notes includes the placement agent’s commission and the estimated cost of hedging our obligations under the Notes through one or more of our affiliates. As a result, the price, if any, at which HSBC Securities (USA) Inc. will be willing to purchase Notes from you in secondary market transactions, if at all, will likely be lower than the original issue price, and any sale of Notes by you prior to the Maturity Date could result in a substantial loss to you. The Notes are not designed to be short-term trading instruments. Accordingly, you should be able and willing to hold your Notes to maturity. |

| · | THE NOTES LACK LIQUIDITY — The Notes will not be listed on any securities exchange. HSBC Securities (USA) Inc. may offer to purchase the Notes in the secondary market but is not required to do so and may cease making such offers at any time if at all. Because other dealers are not likely to make a secondary market for the Notes, the price at which you may be able to trade your Notes is likely to depend on the price, if any, at which HSBC Securities (USA) Inc. is willing to buy the Notes. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell the Notes easily. |

| · | POTENTIAL CONFLICTS — HSBC and its affiliates play a variety of roles in connection with the issuance of the Notes, including acting as calculation agent and hedging its obligations under the Notes. In performing these duties, the economic interests of the calculation agent and other affiliates of HSBC are potentially adverse to your interests as an investor in the Notes. HSBC will not have any obligation to consider your interests as a holder of the Notes in taking any corporate action that might affect the level of the Reference Asset and the value of the Notes. |

| · | The Notes are Not Insured by any Governmental Agency of the United States or any Other Jurisdiction — The Notes are not deposit liabilities or other obligations of a bank and are not insured by the Federal Deposit Insurance Corporation or any other governmental agency or program of the United States or any other jurisdiction. An investment in the Notes is subject to the credit risk of HSBC, and in the event that HSBC is unable to pay its obligations as they become due, you may not receive the full Payment at Maturity of the Notes. |

| · | MANY ECONOMIC AND MARKET FACTORS WILL IMPACT THE VALUE OF THE NOTES — In addition to the Official Closing Level of the Reference Asset on any day, the value of the Notes will be affected by a number of economic and market factors that may either offset or magnify each other, including: |

| · | the expected volatility of the Reference Asset; |

| · | the time to maturity of the Notes; |

| · | the dividend rate on the equity securities underlying the Reference Asset; |

| · | interest and yield rates in the market generally; |

| · | a variety of economic, financial, political, regulatory or judicial events that affect the Reference Asset or the stock markets generally; and |

| · | our creditworthiness, including actual or anticipated downgrades in our credit ratings. |

| -3- |

What Is the Total Return on the Notes at Maturity Assuming a Range of Performance for the Reference Asset?

The following table illustrates the hypothetical total return on the Notes that could be realized on the applicable Observation Date for a range of performances in the Reference Asset. There will be only one payment on the Notes whether automatically called or at maturity. The “total return” as used in this free writing prospectus is the number, expressed as a percentage, that results from comparing the Payment at Maturity per $1,000 Principal Amount of Notes to $1,000. The hypothetical total returns set forth below assumes an Initial Level of 1,400, and reflects the Buffer Level of -10% and the Call Premium of 10.40%, 15.60% and 20.80% for the first Observation Date, second Observation Date and Final Valuation Date, respectively. The hypothetical total returns set forth below are for illustrative purposes only and may not be the actual total returns applicable to a purchaser of the Notes. The numbers appearing in the following table and examples have been rounded for ease of analysis.

| Official Closing Level on Observation Date | Reference Asset Performance on Observation Date | Total Return at First Call Settlement Date | Total Return at Second Call Settlement Date | Total Return at Maturity |

| 2,520 | 80.00% | 10.40% | 15.60% | 20.80% |

| 2,380 | 70.00% | 10.40% | 15.60% | 20.80% |

| 2,100 | 50.00% | 10.40% | 15.60% | 20.80% |

| 1,960 | 40.00% | 10.40% | 15.60% | 20.80% |

| 1,820 | 30.00% | 10.40% | 15.60% | 20.80% |

| 1,680 | 20.00% | 10.40% | 15.60% | 20.80% |

| 1,610 | 15.00% | 10.40% | 15.60% | 20.80% |

| 1,540 | 10.00% | 10.40% | 15.60% | 20.80% |

| 1,470 | 5.00% | 10.40% | 15.60% | 20.80% |

| 1,400 | 0.00% | 10.40% | 15.60% | 20.80% |

| 1,330 | -5.00% | N/A | N/A | 0.00% |

| 1,260 | -10.00% | N/A | N/A | 0.00% |

| 1,120 | -20.00% | N/A | N/A | -11.11% |

| 980 | -30.00% | N/A | N/A | -22.22% |

| 840 | -40.00% | N/A | N/A | -33.33% |

| 700 | -50.00% | N/A | N/A | -44.44% |

| 560 | -60.00% | N/A | N/A | -55.56% |

| 420 | -70.00% | N/A | N/A | -66.67% |

| 280 | -80.00% | N/A | N/A | -77.78% |

| 140 | -90.00% | N/A | N/A | -88.89% |

| 0 | -100.00% | N/A | N/A | -100.00% |

Hypothetical Examples of Amounts Payable at Maturity

The following examples illustrate how the total returns set forth in the table above are calculated.

Example 1: The level of the Reference Asset increases from the Initial Level of 1,400 to an Official Closing Level of 1,470 on the first Observation Date. Because the Official Closing Level on the first Observation Date of 1,470 is greater than the Initial Level, the Notes are automatically called, and the investor receives a single payment of $1,104.00 per $1,000 Principal Amount of Notes on the first Call Settlement Date.

Example 2: The level of the Reference Asset decreases from the Initial Level of 1,400 to an Official Closing Level of 700 on the first Observation Date, 1,120 on the second Observation Date and 1,330 on the Final Valuation Date. Because (a) the Official Closing Level on each of the Observation Dates (700, 1,120 and 1,330) is less than the Initial Level and (b) the Final Level has not declined by more than 10% from the Initial Level, the Notes are not automatically called and the investor receives a Payment at Maturity of $1,000 per $1,000 Principal Amount of Notes.

Example 3: The level of the Reference Asset decreases from the Initial Level of 1,400 to an Official Closing Level of 1,260 on the first Observation Date, 980 on the second Observation Date and 840 on the Final Valuation Date. Because (a) the Official Closing Level on each of the Observation Dates (1,260, 980 and 840) is less than the Initial Level, and (b) the Final Level is more than 10% below the Initial Level, the Notes are not automatically called and the investor receives a Payment at Maturity that is less than the Principal Amount for each $1,000 Principal Amount of Notes, calculated as follows:

$1,000 + [$1,000 × (-40% + 10%) × 1.1111] = $666.67

| -4- |

Description of the Reference Asset

General

This free writing prospectus is not an offer to sell and it is not an offer to buy interests in the Reference Asset or any of the securities comprising the Reference Asset. All disclosures contained in this free writing prospectus regarding the Reference Asset, including its make-up, performance, method of calculation and changes in its components, where applicable, are derived from publicly available information. Neither HSBC nor any of its affiliates assumes any responsibilities for the adequacy or accuracy of information about the Reference Asset or any constituent included in the Reference Asset contained in this free writing prospectus. You should make your own investigation into each Reference Asset.

We urge you to read the section “Sponsors or Issuers and Reference Asset” on page S-37 in the accompanying prospectus supplement.

The S&P 500® Index

HSBC has derived all information relating to the Reference Asset, including, without limitation, its make-up, performance, method of calculation and changes in its components, from publicly available sources. That information reflects the policies of and is subject to change by, Standard & Poor’s Financial Services LLC (“S&P”). S&P is under no obligation to continue to publish, and may discontinue or suspend the publication of the Reference Asset at any time.

S&P publishes the Reference Asset

The Reference Asset is intended to provide an indication of the pattern of common stock price movement. The calculation of the level of the Reference Asset, discussed below in further detail, is based on the relative value of the aggregate Market Value (as defined below) of the common stocks of 500 companies as of a particular time compared to the aggregate average Market Value of the common stocks of 500 similar companies during the base period of the years 1941 through 1943. S&P chooses companies for inclusion in the Reference Asset with the aim of achieving a distribution by broad industry groupings that approximates the distribution of these groupings in the common stock population of the Standard & Poor’s Stock Guide Database, which S&P uses as an assumed model for the composition of the total market. S&P may from time to time in its sole discretion, add companies to or delete companies from, the Reference Asset to achieve these objectives.

Relevant criteria employed by S&P include the viability of the particular company, the extent to which that company represents the industry group to which it is assigned, the extent to which the market price of that company’s common stock is generally responsive to changes in the affairs of the respective industry and the market value and trading activity of the common stock of that company. Ten main industry groups comprise the Reference Asset: Information Technology, Financials, Consumer Staples, Health Care, Energy, Industrials, Consumer Discretionary, Utilities, Materials and Telecommunication Services. Changes in the Reference Asset are reported daily in the financial pages of many major newspapers, on Bloomberg Professional® service under the symbol “SPX” and on the S&P website. Information contained in the S&P website is not incorporated by reference in, and should not be considered a part of, this document.

The Reference Asset does not reflect the payment of dividends on the stocks included in the Reference Asset and therefore the payment on the Notes will not produce the same return you would receive if you were able to purchase such underlying stocks and hold them until the Maturity Date.

Computation of the Reference Asset

Prior to March 2005, the Market Value of a component stock was calculated as the product of the market price per share and the total number of outstanding shares of the component stock. In March 2004, S&P announced that it would transition the Reference Asset to float-adjusted market capitalization weights. The transition began in March 2005 and was completed in September 2005. S&P’s criteria for selecting stock for the Reference Asset was not changed by the shift to float adjustment. However, the adjustment affects each company’s weight in the Reference Asset (i.e., its Market Value). Currently, S&P calculates the Reference Asset based on the total float-adjusted market capitalization of each component stock, where each stock’s weight in the Reference Asset is proportional to its float-adjusted Market Value.

Under float adjustment, the share counts used in calculating the Reference Asset reflect only those shares that are available to investors, not all of a company’s outstanding shares. S&P defines three groups of shareholders whose holdings are subject to float adjustment:

| · | holdings by other publicly traded corporations, venture capital firms, private equity firms, strategic partners, or leveraged buyout groups; |

| · | holdings by government entities, including all levels of government in the U.S. or foreign countries; and |

| · | holdings by current or former officers and directors of the company, founders of the company, or family trusts of officers, directors, or founders, as well as holdings of trusts, foundations, pension funds, employee stock ownership plans or other investment vehicles associated with and controlled by the company. |

However, treasury stock, stock options, restricted shares, equity participation units, warrants, preferred stock, convertible stock, and rights are not part of the float. In cases where holdings in a group exceed 10% of the outstanding shares of a

| -5- |

company, the holdings of that group are excluded from the float-adjusted count of shares to be used in the index calculation. Mutual funds, investment advisory firms, pension funds, or foundations not associated with the company and investment funds in insurance companies, shares of a U.S. company traded in Canada as “exchangeable shares,” shares that trust beneficiaries may buy or sell without difficulty or significant additional expense beyond typical brokerage fees, and, if a company has multiple classes of stock outstanding, shares in an unlisted or non-traded class if such shares are convertible by shareholders without undue delay and cost, are also part of the float.

For each stock, an investable weight factor (“IWF”) is calculated by dividing the available float shares, defined as the total shares outstanding less shares held in one or more of the three groups listed above where the group holdings exceed 10% of the outstanding shares, by the total shares outstanding. The float-adjusted index is then calculated by dividing the sum of the IWF multiplied by both the price and the total shares outstanding for each stock by an Index divisor (the “Divisor”). For companies with multiple classes of stock, S&P calculates the weighted average IWF for each stock using the proportion of the total company market capitalization of each share class as weights.

As of the date of this document, the Reference Asset is also calculated using a base-weighted aggregate methodology: the level of the Reference Asset reflects the total Market Value of all the component stocks relative to the Reference Asset base period of 1941-43. The daily calculation of the Reference Asset is computed by dividing the Market Value of the Reference Asset component stocks by a Divisor, which is adjusted from time to time as discussed below.

The simplest capitalization weighted index can be thought of as a portfolio consisting of all available shares of the stocks in the index. While this might track this portfolio’s value in dollar terms, it would probably yield an unwieldy number in the trillions. Therefore, the actual number used in the Reference Asset is scaled to a more easily handled number, currently in the thousands, by dividing the portfolio Market Value by the Divisor.

Ongoing maintenance of the Reference Asset includes monitoring and completing the adjustments for additions and deletions of the constituent companies, share changes, stock splits, stock dividends and stock price adjustments due to company restructurings or spin-offs. Continuity in the level of the Reference Asset is maintained by adjusting the Divisor for all changes in the Reference Asset constituents’ share capital after the base period of 1941-43 with the level of the Reference Asset as of the base period set at 10. Some corporate actions, such as stock splits and stock dividends do not require Divisor adjustments because following a stock split or stock dividend, both the stock price and number of shares outstanding are adjusted by S&P so that there is no change in the Market Value of the component stock. All stock split and dividend adjustments are made after the close of trading on the day before the ex-date.

To prevent the level of the Reference Asset from changing due to corporate actions, all corporate actions which affect the total Market Value of the Reference Asset also require a Divisor adjustment. By adjusting the Divisor for the change in total Market Value, the level of the Reference Asset remains constant. This helps maintain the level of the Reference Asset as an accurate barometer of stock market performance and ensures that the movement of the Reference Asset does not reflect the corporate actions of individual companies in the Reference Asset. All Divisor adjustments are made after the close of trading and after the calculation of the closing levels of the Reference Asset. As noted in the preceding paragraph, some corporate actions, such as stock splits and stock dividends, require simple changes in the common shares outstanding and the stock prices of the companies in the Reference Asset and do not require Divisor adjustments.

The table below summarizes the types of Reference Asset maintenance adjustments and indicates whether or not a Divisor adjustment is required.

|

Type of Corporate Action |

Comments |

Divisor | |

| Company added/deleted | Net change in market value determines Divisor adjustment. | Yes | |

| Change in shares outstanding | Any combination of secondary issuance, share repurchase or buy back—share counts revised to reflect change. | Yes | |

| Stock split | Share count revised to reflect new count. Divisor adjustment is not required since the share count and price changes are offsetting. | No | |

| Spin-off | If spun-off company is not being added to the index, the divisor adjustment reflects the decline in Index Market Value (i.e., the value of the spun-off unit). | Yes | |

| Spin-off | Spun-off company added to the Reference Asset, no company removed from the Reference Asset. | No | |

| Spin-off | Spun-off company added to the Reference Asset, another company removed to keep number of names fixed. Divisor adjustment reflects deletion. | Yes | |

| Change in IWF | Increasing (decreasing) the IWF increases (decreases) the total market value of the Reference Asset. The Divisor change reflects the | Yes |

| -6- |

|

Type of Corporate Action |

Comments |

Divisor | |

| change in market value caused by the change to an IWF. | |||

| Special dividend | When a company pays a special dividend the share price is assumed to drop by the amount of the dividend; the divisor adjustment reflects this drop in Index Market Value. | Yes | |

| Rights offering | Each shareholder receives the right to buy a proportional number of additional shares at a set (often discounted) price. The calculation assumes that the offering is fully subscribed. Divisor adjustment reflects increase in market cap measured as the shares issued multiplied by the price paid. | Yes |

Each of the corporate events exemplified in the table requiring an adjustment to the Divisor has the effect of altering the Market Value of the component stock and consequently of altering the aggregate Market Value of the Reference Asset component stocks (the “Post-Event Aggregate Market Value”). In order that the level of the Reference Asset (the “Pre-Event Index Value”) not be affected by the altered Market Value (whether increase or decrease) of the affected component stock, a new Divisor (“New Divisor”) is derived as follows:

| • |

Post-Event Aggregate Market Value New Divisor |

= | Pre-Event Index Value |

| • | New Divisor | = |

Post-Event Aggregate Market Value Pre-Event Index Value |

Another large part of the Reference Asset maintenance process involves tracking the changes in the number of shares outstanding of each of the companies whose stocks are included in the Reference Asset. Four times a year, on a Friday close to the end of each calendar quarter, the share totals of companies in the Reference Asset are updated as required by any changes in the number of shares outstanding and then the Index Divisor is adjusted accordingly. In addition, changes in a company’s shares outstanding of 5% or more due to mergers, acquisitions, public offerings, private placements, tender offers, Dutch auctions or exchange offers are made as soon as reasonably possible. Other changes of 5% or more (due to, for example, company stock repurchases, redemptions, exercise of options, warrants, conversion of preferred stock, notes, debt, equity participations or other recapitalizations) are made weekly, and are announced on Wednesdays for implementation after the close of trading on the following Wednesday. If a 5% or more change causes a company’s IWF to change by 5 percentage points or more (for example from 0.80 to 0.85), the IWF will be updated at the same time as the share change, except IWF changes resulting from partial tender offers will be considered on a case-by-case basis. Changes to an IWF of less than 5 percentage points are implemented at the next IWF review, which occurs annually. In the case of certain rights issuances, in which the number of rights issued and/or terms of their exercise are deemed substantial, a price adjustment and share increase may be implemented immediately.

License Agreement with S&P

HSBC has entered into a nonexclusive license agreement providing for the license to it, in exchange for a fee, of the right to use indices owned and published by S&P in connection with some products, including the Notes.

The Notes are not sponsored, endorsed, sold or promoted by S&P or its third party licensors. Neither S&P nor its third party licensors makes any representation or warranty, express or implied, to the owners of the Notes or any member of the public regarding the advisability of investing in securities generally or in the Notes particularly or the ability of the SPX to track general stock market performance. S&P's and its third party licensor’s only relationship to HSBC USA Inc. is the licensing of certain trademarks and trade names of S&P and the third party licensors and of the SPX which is determined, composed and calculated by S&P or its third party licensors without regard to HSBC USA Inc. or the Notes. S&P and its third party licensors have no obligation to take the needs of HSBC USA Inc. or the owners of the Notes into consideration in determining, composing or calculating the SPX. Neither S&P nor its third party licensors is responsible for and has not participated in the determination of the prices and amount of the Notes or the timing of the issuance or sale of the Notes or in the determination or calculation of the equation by which the Notes are to be converted into cash. S&P has no obligation or liability in connection with the administration, marketing or trading of the Notes.

NEITHER STANDARD & POOR’S, ITS AFFILIATES NOR THEIR THIRD PARTY LICENSORS GUARANTEE THE ADEQUACY, ACCURACY, TIMELINESS OR COMPLETENESS OF THE SPX OR ANY DATA INCLUDED THEREIN OR ANY COMMUNICATIONS, INCLUDING BUT NOT LIMITED TO, ORAL OR WRITTEN COMMUNICATIONS (INCLUDING ELECTRONIC COMMUNICATIONS) WITH RESPECT THERETO. STANDARD & POOR’S, ITS AFFILIATES AND THEIR THIRD PARTY LICENSORS SHALL NOT BE SUBJECT TO ANY DAMAGES OR LIABILITY FOR ANY ERRORS, OMISSIONS OR DELAYS THEREIN. STANDARD & POOR’S MAKES NO EXPRESS OR IMPLIED WARRANTIES, AND EXPRESSLY DISCLAIMS ALL WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR

| -7- |

USE WITH RESPECT TO THE MARKS, THE SPX OR ANY DATA INCLUDED THEREIN. WITHOUT LIMITING ANY OF THE FOREGOING, IN NO EVENT WHATSOEVER SHALL STANDARD & POOR’S, ITS AFFILIATES OR THEIR THIRD PARTY LICENSORS BE LIABLE FOR ANY INDIRECT, SPECIAL, INCIDENTAL, PUNITIVE OR CONSEQUENTIAL DAMAGES, INCLUDING BUT NOT LIMITED TO, LOSS OF PROFITS, TRADING LOSSES, LOST TIME OR GOODWILL, EVEN IF THEY HAVE BEEN ADVISED OF THE POSSIBILITY OF SUCH DAMAGES, WHETHER IN CONTRACT, TORT, STRICT LIABILITY OR OTHERWISE.

“Standard & Poor’s®”, “S&P®” and “S&P 500®” are trademarks of Standard and Poor’s and have been licensed for use by HSBC USA Inc.

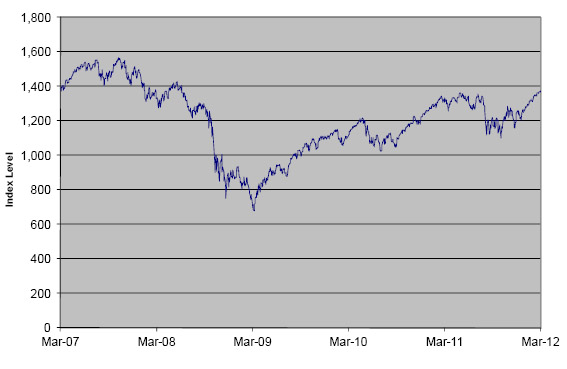

Historical Performance of the Reference Asset

The following graph sets forth the historical performance of the Reference Asset based on the daily historical closing levels from March 2, 2007 through March 2, 2012. The closing level for the Reference Asset on March 2, 2012 was 1,369.63. We obtained the closing levels below from Bloomberg Professional® service. We make no representation or warranty as to the accuracy or completeness of the information obtained from Bloomberg Professional® service.

The historical Official Closing Levels of the Reference Asset should not be taken as an indication of future performance, and no assurance can be given as to the Official Closing Level on the Pricing Date or on any Observation Date. We cannot give you assurance that the performance of the Reference Asset will result in the return of any of your initial investment.

Historical Performance of the S&P 500® Index

Source: Bloomberg

| -8- |

Supplemental Information Relating to the Terms of the Notes

Market Disruption Events

“Market disruption event” means any scheduled trading day on which any relevant exchange or related exchange fails to open for trading during its regular trading session or on which any of the following events has occurred and is continuing which the calculation agent determines is material:

| (i) | Any suspension of or limitation imposed on trading by any relevant exchanges or related exchanges or otherwise, (A) relating to any component security included in the Reference Asset then constituting 20.00% or more of the level of the Reference Asset or (B) in futures or options contracts relating to the Reference Asset on any related exchange; or |

| (ii) | Any event (other than any event described in (iii) below) that disrupts or impairs the ability of market participants in general (A) to effect transactions in, or obtain market values for any component security included in the Reference Asset then constituting 20.00% or more of the level of the Reference Asset or (B) to effect transactions in, or obtain market values for, futures or options contracts relating to the Reference Asset on any relevant related exchange; or |

| (iii) | The closure on any scheduled trading day of any relevant exchange or related exchange prior to its scheduled closing time (unless the earlier closing time is announced by the relevant exchange or related exchange at least one hour prior to the earlier of (i) the actual closing time for the regular trading session on the exchange and (ii) the submission deadline for orders to be entered into the relevant exchange or related exchange for execution at the close of trading on that day). |

“Related exchange” means each exchange or quotation system or any successor or temporary substitute for such exchange or quotation system (provided HSBC has determined, for a substitute exchange or quotation system, that liquidity on such substitute is comparable to liquidity on the original related exchange) and where trading has a material effect (as determined by the calculation agent) on the overall market for futures or options contracts relating to the Reference Asset.

“Relevant exchange” means the primary exchange or quotation system for any stock or other security then included in the Reference Asset.

“Scheduled closing time” means the scheduled weekday closing time of the relevant exchange or related exchange, without regard to after hours or any other trading outside of the regular trading session hours.

“Scheduled trading day” means any day on which all of the relevant exchanges and related exchanges are scheduled to be open for their respective regular trading sessions.

Discontinuance or Modification of the Reference Asset; Alteration of Method of Calculation

If Standard and Poor’s Financial Services LLC, a subsidiary of The McGraw-Hill Companies, Inc. (the “reference sponsor”) discontinues publication of or otherwise fails to publish the Reference Asset on any day on which the Reference Asset is scheduled to be published and the reference sponsor or another entity publishes a successor or substitute index that the calculation agent determines to be comparable to the discontinued index (the comparable index, the “successor index”), then that successor index will be deemed to be the Reference Asset for all purposes relating to the Notes, including for purposes of determining whether a market disruption event exists. Upon any selection by the calculation agent of a successor index, the calculation agent will furnish written notice to us and the holders of the Notes.

If the Reference Asset is discontinued or if the reference sponsor fails to publish the Reference Asset and the calculation agent determines that no successor index is available at that time, then the calculation agent will determine the applicable Official Closing Level using the same general methodology previously used by such reference sponsor. The calculation agent will continue to make that determination until the earlier of (i) the Final Valuation Date or (ii) a determination by the calculation agent that the Reference Asset or a successor index is available. In that case, the calculation agent will furnish written notice to us and the holders of the Notes.

If at any time the method of calculating the Reference Asset or a successor index, or the level thereof, is changed in a material respect, or if the Reference Asset or a successor index is in any other way modified so that, in the determination of the calculation agent, the level of Reference Asset does not fairly represent the level of the Reference Asset or successor index that would have prevailed had those changes or modifications not been made, then the calculation agent will make the calculations and adjustments as may be necessary in order to determine a level comparable to the level that would have prevailed had those changes or modifications not been made. In that case, the calculation agent will furnish written notice to us and the holders of the Notes.

In each of the foregoing events, the Initial Level, the Official Closing Level on any Observation Date and the Final Level may be different than each would have been if the original Reference Asset had not been discontinued or modified. Thus, discontinuation or modification of the Reference Asset may adversely affect the value of the Notes.

| -9- |

Observation Dates, Call Settlement Date and Maturity Date

If any Observation Date, including the Final Valuation Date, is not a scheduled trading day, then such Observation Date or the Final Valuation Date, respectively, will be the next scheduled trading day. If a Market Disruption Event (as described above) exists on any Observation Date including the Final Valuation Date, then such Observation Date or the Final Valuation Date, respectively, will be the next scheduled trading day for which there is no Market Disruption Event. If a Market Disruption Event exists with respect to any Observation Date including the Final Valuation Date on five consecutive scheduled trading days, then that fifth scheduled trading day will nonetheless be such Observation Date or the Final Valuation Date (as applicable), and the Official Closing Level on such day will be determined by the calculation agent by means of the formula for, and method of calculating of, the Reference Asset which applied just prior to the Market Disruption Event. If an Observation Date other than the Final Valuation Date is postponed, then the corresponding Call Settlement Date, if applicable, will also be postponed by the same number of business days and no interest will be paid in respect of such postponement. If the Final Valuation Date is postponed, then the Maturity Date will also be postponed by the same number of business days and no interest will be paid in respect of such postponement.

Events of Default and Acceleration

If the Notes have become immediately due and payable following an Event of Default (as defined in the accompanying prospectus) with respect to the Notes, the calculation agent will determine the accelerated Payment at Maturity due and payable in the same general manner as described in “Payment at Maturity”. In that case, the scheduled trading day preceding the date of acceleration will be used as the Final Valuation Date for purposes of determining the accelerated Reference Return. If a market disruption event exists on that scheduled trading day, then the accelerated Final Valuation Date will be postponed for up to five scheduled trading days (in the same general manner used for postponing the originally scheduled Final Valuation Date). The accelerated Maturity Date will also be postponed by an equal number of business days.

If the Notes have become immediately due and payable following an Event of Default, you will not be entitled to any additional payments with respect to the Notes. For more information, see “Description of Debt Securities — Events of Default” in the accompanying prospectus.

Supplemental Plan of Distribution (Conflicts of Interest)

Pursuant to the terms of a distribution agreement, HSBC Securities (USA) Inc., an affiliate of HSBC, will purchase the Notes from HSBC for distribution to J.P. Morgan Securities LLC and certain of its registered broker-dealer affiliates, at the price indicated on the cover of the pricing supplement, the document that will be filed pursuant to Rule 424(b)(2) containing the final pricing terms of the Notes. J.P. Morgan Securities LLC and certain of its registered broker-dealer affiliates will act as placement agent for the Notes and will receive a fee that will not exceed $15.00 per $1,000 Principal Amount of Notes.

In addition, HSBC Securities (USA) Inc. or another of its affiliates or agents may use the pricing supplement to which this free writing prospectus relates in market-making transactions after the initial sale of the Notes, but is under no obligation to do so and may discontinue any market-making activities at any time without notice.

See “Supplemental Plan of Distribution” on page S-52 in the prospectus supplement. All references to NASD Rule 2720 in the prospectus supplement shall be to FINRA Rule 5121.

| -10- |