|

ISSUER FREE WRITING PROSPECTUS

Filed Pursuant to Rule 433

Registration Statement No. 333-158385

Dated November 29, 2011

|

|

HSBC USA Inc. Trigger Digital Optimization Securities

Linked to the Performance of a Basket of Currencies Relative to the U.S. Dollar, Maturing December 16, 2013

|

Investment Description

|

|

These Trigger Digital Optimization Securities (the “Securities”) are senior unsecured debt securities issued by HSBC USA Inc. (“HSBC”) that provide exposure to the performance of an equally-weighted basket of currencies (the “Basket”) relative to the U.S. dollar (USD). The Basket consists of the Brazilian real (BRL), the Russian ruble (RUB), the Indian rupee (INR) and the Chinese renminbi (Yuan) (CNY) (the “Basket Currencies”). The Securities will rank equally with all of our other unsecured and unsubordinated debt obligations. If the Basket Return is zero or positive (overall the Basket Currencies remain flat or appreciate relative to the USD), HSBC will repay your Principal Amount at maturity plus pay a return equal to the Digital Return, which will be set on the Trade Date and is expected to be between 30% and 35%, regardless of the Basket’s appreciation. If the Basket Return is negative (overall the Basket Currencies depreciate relative to the USD) and the Basket Ending Level is equal to or greater than the Trigger Level, HSBC will repay the full Principal Amount at maturity. However, if the Basket Return is negative and the Basket Ending Level is less than the Trigger Level, HSBC will pay less than the full Principal Amount at maturity, if anything, resulting in a loss of principal to investors that is proportionate to the negative Basket Return, but, in no case will the Payment at Maturity be less than zero. Investing in the Securities involves significant risks. You may lose some or all of your Principal Amount. You will not receive interest payments during the term of the Securities. The contingent repayment of principal applies only if you hold the Securities to maturity. Any payment on the Securities, including any repayment of principal at maturity, is subject to the creditworthiness of HSBC. If HSBC were to default on its payment obligations, you may not receive any amounts owed to you under the Securities and you could lose your entire investment.

|

|

Features

|

|

q

|

Digital Return Feature: If the Basket Return is zero or positive, HSBC will repay the Principal Amount at maturity plus pay a return equal to the Digital Return, regardless of the Basket’s appreciation. If the Basket Return is negative, investors may be exposed to the percentage decline in the Basket at maturity.

|

|

q

|

Contingent Repayment of Principal at Maturity: If the Basket Return is negative and the Basket Ending Level is equal to or greater than the Trigger Level, HSBC will repay the full Principal Amount at maturity. However, if the Basket Ending Level is less than the Trigger Level, HSBC will pay less than the full Principal Amount, if anything, resulting in a loss of principal to investors that is proportionate to the negative Basket Return but, in no case, will the Payment at Maturity be less than zero. You may lose some or all of your Principal Amount. The contingent repayment of principal applies only if you hold the Securities to maturity. Any payment on the Securities, including any repayment of principal, is subject to the creditworthiness of HSBC.

|

|

r

|

Exposure to Foreign Currencies: The Securities provide an opportunity to diversify your portfolio through exposure to the Basket Currencies.

|

|

Key Dates1

|

|

Trade Date

|

December 9, 2011

|

|

Settlement Date

|

December 14, 2011

|

|

Final Valuation Date2

|

December 11, 2013

|

|

Maturity Date2

|

December 16, 2013

|

1 Expected.

2 See page 3 for additional details.

THE SECURITIES ARE SIGNIFICANTLY RISKIER THAN CONVENTIONAL DEBT INSTRUMENTS. THE TERMS OF THE SECURITIES MAY NOT OBLIGATE HSBC TO REPAY THE FULL PRINCIPAL AMOUNT OF THE SECURITIES. THE SECURITIES MAY HAVE DOWNSIDE MARKET RISK SIMILAR TO THE BASKET, WHICH CAN RESULT IN A LOSS OF SOME OR ALL OF YOUR INVESTMENT AT MATURITY. THIS MARKET RISK IS IN ADDITION TO THE CREDIT RISK INHERENT IN PURCHASING A DEBT OBLIGATION OF HSBC. YOU SHOULD NOT PURCHASE THE SECURITIES IF YOU DO NOT UNDERSTAND OR ARE NOT COMFORTABLE WITH THE SIGNIFICANT RISKS INVOLVED IN INVESTING IN THE SECURITIES.

YOU SHOULD CAREFULLY CONSIDER THE RISKS DESCRIBED UNDER ‘‘KEY RISKS’’ BEGINNING ON PAGE 7 OF THIS FREE WRITING PROSPECTUS AND THE MORE DETAILED ‘‘RISK FACTORS’’ BEGINNING ON PAGE S-3 OF THE ACCOMPANYING PROSPECTUS SUPPLEMENT BEFORE PURCHASING ANY SECURITIES. EVENTS RELATING TO ANY OF THOSE RISKS, OR OTHER RISKS AND UNCERTAINTIES, COULD ADVERSELY EFFECT THE MARKET VALUE OF, AND THE RETURN ON, YOUR SECURITIES.

|

Security Offering

|

HSBC is offering Trigger Digital Optimization Securities linked to the performance of a basket of currencies relative to the U.S. dollar. The return on the Securities at maturity will be determined by the performance of the Basket Currencies relative to the U.S. dollar. The Securities are offered at a minimum investment of 100 Securities at the Price to Public described below. The Initial Spot Rate for each Basket Currency and the Digital Return will be set on the Trade Date.

|

Basket Currencies and Weightings

|

Basket Starting Level

|

Digital Return

|

Trigger Level

|

CUSIP

|

ISIN

|

|

BRL – 25%

RUB – 25%

INR –25%

CNY – 25%

|

100

|

30% to 35%,

to be determined on the Trade Date

|

80, which is equal to 80% of the Basket Starting Level

|

40433C114

|

US40433C1146

|

See “Additional Information about HSBC USA Inc. and the Securities” on page 2 of this free writing prospectus. The Securities offered will have the terms specified in the accompanying prospectus dated April 2, 2009, the accompanying prospectus supplement dated April 9, 2009 and the terms set forth herein.

Neither the U.S. Securities and Exchange Commission, or the SEC, nor any state securities commission has approved or disapproved of the Securities or passed upon the accuracy or the adequacy of this document, the accompanying prospectus or prospectus supplement. Any representation to the contrary is a criminal offense. The Securities are not deposit liabilities or other obligations of a bank and are not insured by the Federal Deposit Insurance Corporation or any other governmental agency of the United States or any other jurisdiction.

The Securities will not be listed on any U.S. securities exchange or quotation system. HSBC Securities (USA) Inc., an affiliate of HSBC USA Inc., will purchase the Securities from HSBC USA Inc. for distribution to UBS Financial Services Inc, acting as agent. See “Supplemental Plan of Distribution (Conflicts of Interest)” on the last page of this free writing prospectus for the distribution arrangement.

|

Price to Public

|

Underwriting Discount(1)

|

Proceeds to Issuer

|

|

|

Per Security

|

$10.00

|

$0.20

|

$9.80

|

|

Total

|

|||

|

(1) UBS Financial Services Inc. will act as placement agent for sales to certain advisory accounts at a purchase price to such accounts of $9.80 per Security, and will not receive a sales commission with respect to such sales. See “Supplemental Plan of Distribution (Conflicts of Interest)” on the last page of this free writing prospectus.

|

|||

|

UBS Financial Services Inc.

|

HSBC USA Inc.

|

|

Additional Information about HSBC USA Inc. and the Securities

|

This free writing prospectus relates to the offering of Securities linked to the Basket identified on the cover page. The Basket described in this free writing prospectus is a reference asset as defined in the prospectus supplement, and the Securities being offered hereby are “notes” for purposes of the prospectus supplement. As a purchaser of a Security, you will acquire a senior unsecured debt instrument linked to the Basket which will rank equally with all of our other unsecured and unsubordinated debt obligations. Although the offering of Securities relates to the Basket identified on the cover page, you should not construe that fact as a recommendation of the merits of acquiring an investment linked to the Basket, the Basket Currencies, or as to the suitability of an investment in the Securities.

You should read this document together with the prospectus dated April 2, 2009 and the prospectus supplement dated April 9, 2009. If the terms of the Securities offered hereby are inconsistent with those described in the accompanying prospectus supplement or prospectus, the terms described in this free writing prospectus shall control. You should carefully consider, among other things, the matters set forth in “Key Risks” on page 7 of this free writing prospectus and in “Risk Factors” beginning on page S-3 of the prospectus supplement, as the Securities involve risks not associated with conventional debt securities. You are urged to consult your investment, legal, tax, accounting and other advisors before you invest in the Securities.

HSBC USA Inc. has filed a registration statement (including the prospectus and prospectus supplement) with the SEC for the offering to which this free writing prospectus relates. Before you invest, you should read the prospectus and prospectus supplement in that registration statement and other documents HSBC USA Inc. has filed with the SEC for more complete information about HSBC USA Inc. and this offering. You may get these documents for free by visiting EDGAR on the SEC’s web site at www.sec.gov. Alternatively, HSBC Securities (USA) Inc. or any dealer participating in this offering will arrange to send you the prospectus and prospectus supplement if you request them by calling toll-free 1-866-811-8049.

You may access these documents on the SEC web site at www.sec.gov as follows:

|

¨

|

Prospectus supplement dated April 9, 2009:

|

|

¨

|

Prospectus dated April 2, 2009:

|

As used herein, references to the “Issuer,” “HSBC”, “we,” “us” and “our” are to HSBC USA Inc. References to the “prospectus supplement” mean the prospectus supplement dated April 9, 2009 and references to “accompanying prospectus” mean the HSBC USA Inc. prospectus, dated April 2, 2009.

|

Investor Suitability

|

|||

|

The Securities may be appropriate for you if:

¨ You fully understand the risks inherent in an investment in the Securities, including the risk of loss of your entire initial investment.

¨ You can tolerate a loss of all or a substantial portion of your investment and are willing to make an investment that may have similar downside market risk as an investment in the Basket.

¨ You seek an investment with a return linked to the performance of a Basket consisting of the Brazilian real, Russian ruble, Indian rupee and Chinese renminbi (Yuan) relative to the U.S. dollar.

¨ You believe that the Basket will remain flat or strengthen relative to the U.S. dollar, but will not strengthen by more than the Digital Return.

¨ You understand and accept that you will not participate in any appreciation of the Basket and your potential return is limited by the Digital Return, which will be set on the Trade Date, regardless of the Basket's appreciation.

¨ You would be willing to invest in the Securities if the Digital Return was set equal to the bottom of the range indicated on the cover hereof (the actual Digital Return will be determined on the Trade Date).

¨ You do not seek current income from this investment.

¨ You are willing and able to hold the Securities to maturity, a term of 2 years, and are aware that there is likely to be little or no secondary market for the Securities.

¨ You are willing to assume the creditworthiness of HSBC, as issuer of the Securities, and understand that if HSBC defaults on its obligations you may not receive any amounts due to you including any repayment of principal.

|

The Securities may not be appropriate for you if:

¨ You do not fully understand the risks inherent in an investment in the Securities, including the risk of loss of your entire initial investment.

¨ You cannot tolerate a loss of all or a substantial portion of your investment, and you are not willing to make an investment that may have similar downside market risk as an investment in the Basket.

¨ You do not seek an investment with a return linked to the performance of a Basket consisting of the Brazilian real, Russian ruble, Indian rupee and Chinese renminbi (Yuan) relative to the U.S. dollar.

¨ You believe that the Basket will weaken relative to the U.S. dollar or strengthen by more than the Digital Return.

¨ You require an investment designed to provide a full return of principal at maturity.

¨ You seek an investment that participates in the full appreciation of the Basket or has unlimited return potential.

¨ You would be unwilling to invest in the Securities if the Digital Return was set equal to the bottom of the range indicated on the cover hereof (the actual Digital Return will be determined on the Trade Date).

¨ You prefer the lower risk, and therefore accept the potentially lower returns, of conventional debt securities with comparable maturities issued by HSBC or another issuer with a similar credit rating.

¨ You seek current income from this investment.

¨ You are unable or unwilling to hold the Securities to maturity, a term of 2 years, and seek an investment for which there will be an active secondary market.

¨ You are not willing or are unable to assume the credit risk associated with HSBC, as issuer of the Securities, for any payment on the Securities, including any repayment of principal.

|

||

|

The suitability considerations identified above are not exhaustive. Whether or not the Securities are a suitable investment for you will depend on your individual circumstances, and you should reach an investment decision only after you and your investment, legal, tax, accounting and other advisors have carefully considered the suitability of an investment in the Securities in light of your particular circumstances. You should also review “Key Risks” on page 7 of this free writing prospectus and “Risk Factors” on page S-3 of the prospectus supplement.

|

|||

2

|

Indicative Terms

|

||

|

Issuer

|

HSBC USA Inc. (A1/A+/AA)1

|

|

|

Issue Price

|

$10.00 per Security for brokerage account holders;

$9.80 per Security for advisory account holders.

|

|

|

Principal Amount

|

$10 per Security. The Payment at Maturity will be based on the Principal Amount.

|

|

|

Term

|

2 years

|

|

|

Trade Date2

|

December 9, 2011

|

|

|

Settlement Date2

|

December 14, 2011

|

|

|

Final Valuation Date2

|

December 11, 2013, subject to postponement in the event of a Market Disruption Event or certain other circumstances as described under “Market Disruption Events” below.

|

|

|

Maturity Date2

|

December 16, 2013, subject to postponement in the event of a Market Disruption Event or certain other circumstances as described under “Market Disruption Events” below.

|

|

|

Basket

|

The Securities are linked to the performance of an equally-weighted basket of currencies (the “Basket”) relative to the U.S. dollar. The currencies comprising the Basket (each a “Basket Currency”), along with their respective weightings, are set forth below:

|

|

|

Basket Currency

|

Currency Weighting

|

||

|

Brazilian real (BRL)

|

25%

|

||

|

Russian ruble (RUB)

|

25%

|

||

|

Indian rupee (INR)

|

25%

|

||

|

Chinese renminbi (Yuan) (CNY)

|

25%

|

|

Digital Return

|

30% to 35%. The actual Digital Return will be determined on the Trade Date.

|

|

|

Trigger Level

|

80, which is equal to 80% of the Basket Starting Level

|

|

|

Payment at Maturity

(per $10 Security)3

|

If the Basket Return is zero or positive, HSBC will pay a cash payment per Security that provides you with the Principal Amount of $10 per Security plus a return equal to the Digital Return, calculated as follows:

$10 + ($10 × Digital Return)

If the Basket Return is negative and the Basket Ending Level is equal to or greater than the Trigger Level, HSBC will pay you a cash payment at maturity equal to the Principal Amount of $10 per Security.

If the Basket Return is negative and the Basket Ending Level is less than the Trigger Level, HSBC will pay you a cash payment at maturity less than the Principal Amount of $10 per Security, if anything, resulting in a loss of principal that is proportionate to the negative Basket Return, equal to the greater of:

a) $10 + ($10 × Basket Return); and

b) zero.

In this scenario you will be fully exposed to the negative performance of the Basket and will lose some or all of your Principal Amount. However, in no case will the Payment at Maturity be less than zero.

|

|

|

Basket Return

|

Basket Ending Level — Basket Starting Level

Basket Starting Level

|

|

|

Basket Starting Level

|

Set equal to 100 on the Trade Date

|

|

|

Basket Ending Level

|

The Basket Ending Level will be calculated as follows:

100 x [1 + (BRL Currency Return × 25%) + (RUB Currency Return × 25%) + (INR Currency Return × 25%) + (CNY Currency Return × 25%)]

The returns set forth in the formula above reflect the performance of the Basket Currencies as described under “Currency Return” below.

|

|

|

Currency Return

|

For each Basket Currency:

Initial Spot Rate – Final Spot Rate

Initial Spot Rate

Because the Currency Return is calculated pursuant to the formula above, the maximum possible Currency Return will equal 100%. However, your return at maturity, if any, will be limited to the Digital Return. There is no comparable limit on the negative performance of a Currency Return or the Basket Return. However, in no case will the Payment at Maturity be less than zero.

|

|

|

Initial Spot Rate

|

For each Basket Currency, the currency exchange rate for that Basket Currency relative to the U.S. dollar on the Trade Date, determined as described under “Spot Rate” below.

|

|

|

Final Spot Rate

|

For each Basket Currency, the currency exchange rate for that Basket Currency relative to the U.S. dollar on the Final Valuation Date, determined as described under “Spot Rate” below.

|

1 HSBC USA Inc. is rated A1 by Moody’s, A+ by Standard & Poor’s and AA by Fitch Ratings. A credit rating reflects the creditworthiness of HSBC USA Inc. and is not a recommendation to buy, sell or hold securities, and it may be subject to revision or withdrawal at any time by the assigning rating organization. The Securities themselves have not been independently rated. Each rating should be evaluated independently of any other rating.

2 Expected. In the event any change is made to the expected Trade Date and Settlement Date, the Final Valuation Date and Maturity Date will be changed so that the stated term of the Securities remains the same.

3 Payment at maturity, including any repayment of principal is provided by HSBC USA Inc., and therefore, is dependent on the ability of HSBC USA Inc. to satisfy its obligations when they come due.

3

|

Spot Rate

|

The Spot Rate for the Brazilian real (the “BRL Spot Rate”) on each date of calculation will be the U.S. dollar/Brazilian real offered rate for U.S. dollars, expressed as the amount of Brazilian reals per one U.S. dollar, for settlement in two business days, as reported by Banco Central do Brasil on SISBACEN Data System under transaction code PTAX-800 (“Consulta de Cambio” or Exchange Rate Inquiry), Option 5 (“Cotacoes para Contabilidade” or Rates for Accounting Purposes), by approximately 2:00 p.m., Sao Paulo time, on such date of calculation, which appears on Reuters Page "BRFR" to the right of the caption “Dollar PTAX” or any successor page, on such date of calculation. Four decimal figures shall be used for the determination of such BRL exchange rate.

The Spot Rate for the Russian ruble on each date of calculation will be the U.S. dollar/Russian ruble specified rate, expressed as the amount of Russian rubles per one U.S. dollar, for settlement in one business day, calculated by the Chicago Mercantile Exchange (“CME”) and as published on CME’s website, which appears on the Reuters Screen EMTA Page or any successor page, at approximately 1:30 p.m., Moscow time, on such date of calculation. The Spot Rate shall be calculated by the CME pursuant to the Chicago Mercantile Exchange/EMTA, Inc. Daily Russian Ruble Per U.S. Dollar Reference Rate Methodology (which means a methodology, effective as of June 16, 2005, as amended from time to time, for a centralized industry-wide survey of financial institutions in Russia that are active participants in the U.S. Dollar/Russian Ruble spot market for the purpose of determining the RUB/CME-EMTA Rate). Four decimal figures shall be used for the determination of such RUB exchange rate.

The Spot Rate for the Indian rupee on each date of calculation will be the U.S. dollar/Indian rupee reference rate, expressed as the amount of Indian rupees per one U.S. dollar, for settlement in two business days, as reported by the Reserve Bank of India, which appears on the Reuters Screen RBIB Page or any successor page, at approximately 12:30 p.m., Mumbai time, or as soon thereafter as practicable, on such date of calculation. Four decimal figures shall be used for the determination of such INR exchange rate.

The Spot Rate for the Chinese renminbi (Yuan) on each date of calculation will be the U.S. dollar/Chinese renminbi (Yuan) official fixing rate, expressed as the amount of Chinese renminbi (Yuan) per one U.S. Dollar, for settlement in two business days, as reported by the People’s Bank of China, Beijing, People’s Republic of China, which appears on Reuters Screen SAEC Page opposite the symbol “USDCNY=” or any successor page, at approximately 9:15 a.m., Beijing time, on such date of calculation. Four decimal figures shall be used for the determination of such CNY exchange rate.

If any of the foregoing Spot Rates is unavailable (including being published in error, as determined by the Calculation Agent in its sole discretion), the Spot Rate for such Basket Currency shall be selected by the Calculation Agent in good faith and in a commercially reasonable manner, or the Final Valuation Date may be postponed by the Calculation Agent as described under “Market Disruption Events” below.

|

|

|

Calculation Agent

|

HSBC USA Inc. or one of its affiliates

|

|

|

CUSIP / ISIN

|

40433C114 / US40433C1146

|

|

|

Trustee

|

Notwithstanding anything contained in the accompanying prospectus supplement to the contrary, the Securities will be issued under the senior indenture dated March 31, 2009, between HSBC USA Inc., as Issuer, and Wells Fargo Bank, National Association, as trustee. Such indenture has substantially the same terms as the indenture described in the accompanying prospectus supplement.

|

|

|

Paying Agent

|

HSBC Bank USA, N.A. will act as paying agent with respect to the Securities pursuant to a Paying Agent and Securities Registrar Agreement dated June 1, 2009, between HSBC USA Inc. and HSBC Bank USA, N.A.

|

|

Investment Timeline

|

|

The Initial Spot Rate for each Basket Currency is determined.

The Basket Starting Level is set equal to 100.

The Digital Return is set.

The Final Spot Rate for each Basket Currency is determined on the Final Valuation Date.

The Final Basket Level and Basket Return are calculated.

If the Basket Return is zero or positive, HSBC will pay a cash payment per Security that provides you with the Principal Amount of $10 per Security plus a return equal to the Digital Return, calculated as follows:

$10 + ($10 × Digital Return)

If the Basket Return is negative and the Basket Ending Level is equal to or greater than the Trigger Level, HSBC will pay you a cash payment at maturity equal to the Principal Amount of $10 per Security.

If the Basket Return is negative and the Basket Ending Level is less than the Trigger Level, HSBC will pay you a cash payment at maturity less than the Principal Amount of $10 per Security, if anything, resulting in a loss of principal that is proportionate to the negative Basket Return, equal to the greater of:

a) $10 + ($10 × Basket Return); and

b) zero.

Under these circumstances, you will lose a significant portion, and could lose all, of your initial investment.

|

INVESTING IN THE SECURITIES INVOLVES SIGNIFICANT RISKS. YOU MAY LOSE SOME OR ALL OF YOUR PRINCIPAL AMOUNT. ANY PAYMENT ON THE SECURITIES, INCLUDING ANY REPAYMENT OF PRINCIPAL AT MATURITY, IS SUBJECT TO THE CREDITWORTHINESS OF HSBC. IF HSBC WERE TO DEFAULT ON ITS PAYMENT OBLIGATIONS, YOU MAY NOT RECEIVE ANY AMOUNTS OWED TO YOU UNDER THE SECURITIES AND YOU COULD LOSE YOUR ENTIRE INVESTMENT.

4

|

How will the Basket Return be calculated?

|

Your Payment at Maturity will depend on the Basket Return. The following steps are necessary to calculate the Basket Return.

Step 1: Calculate the Currency Return for each of the Basket Currencies.

The BRL Currency Return is the difference between the BRL Initial Spot Rate and the BRL Final Spot Rate relative to the BRL Initial Spot Rate, expressed as a percentage and calculated as follows:

|

BRL Currency Return =

|

BRL Initial Spot Rate – BRL Final Spot Rate

|

|

BRL Initial Spot Rate

|

An increase in the value of the Brazilian real relative to the U.S. dollar is expressed as a decrease in the BRL Spot Rate.

The RUB Currency Return is the difference between the RUB Initial Spot Rate and the RUB Final Spot Rate relative to the RUB Initial Spot Rate, expressed as a percentage and calculated as follows:

|

RUB Currency Return =

|

RUB Initial Spot Rate – RUB Final Spot Rate

|

|

RUB Initial Spot Rate

|

An increase in the value of the Russian ruble relative to the U.S. dollar is expressed as a decrease in the RUB Spot Rate.

The INR Currency Return is the difference between the INR Initial Spot Rate and the INR Final Spot Rate relative to the INR Initial Spot Rate, expressed as a percentage and calculated as follows:

|

INR Currency Return =

|

INR Initial Spot Rate – INR Final Spot Rate

|

|

INR Initial Spot Rate

|

An increase in the value of the Indian rupee relative to the U.S. dollar is expressed as a decrease in the INR Spot Rate.

The CNY Currency Return is the difference between the CNY Initial Spot Rate and the CNY Final Spot Rate relative to the CNY Initial Spot Rate, expressed as a percentage and calculated as follows:

|

CNY Currency Return =

|

CNY Initial Spot Rate – CNY Final Spot Rate

|

|

CNY Initial Spot Rate

|

An increase in the value of the Chinese renminbi (Yuan) relative to the U.S. dollar is expressed as a decrease in the CNY Spot Rate.

Step 2: Calculate the Basket Ending Level.

The Basket Ending Level will be calculated as follows:

100 x [1 + (25% x BRL Currency Return) + (25% x RUB Currency Return) + (25% x INR Currency Return) + (25% x CNY Currency Return)]

Step 3: Calculate the Basket Return.

The Basket Return will be calculated as follows:

Basket Ending Level – Basket Starting Level

Basket Starting Level

5

|

What are the tax consequences of the Securities?

|

|

You should carefully consider, among other things, the matters set forth in the section “Certain U.S. Federal Income Tax Considerations” in the prospectus supplement. The following discussion summarizes the U.S. federal income tax consequences of the purchase, beneficial ownership, and disposition of each of the Securities. This summary supplements the section “Certain U.S. Federal Income Tax Considerations” in the prospectus supplement and supersedes it to the extent inconsistent therewith. Notwithstanding any disclosure in the accompanying prospectus supplement to the contrary, HSBC’s special U.S. tax counsel in this transaction is Sidley Austin llp.

There are no statutory provisions, regulations, published rulings or judicial decisions addressing the characterization for U.S. federal income tax purposes of securities with terms that are substantially the same as those of the Securities. Under one reasonable approach, the Securities should be treated as pre-paid forward or other executory contracts with respect to the Basket. HSBC intends to treat the Securities consistent with this approach and pursuant to the terms of the Securities, you agree to treat the Securities under this approach for all U.S. federal income tax purposes. Subject to certain limitations described in the prospectus supplement, and based on certain factual representations received from HSBC, in the opinion of HSBC’s special U.S. tax counsel, Sidley Austin llp, it is reasonable to treat the Securities in accordance with this approach. Assuming this characterization is respected, upon a sale or exchange of a Security (including redemption of the Securities at maturity), you should recognize gain or loss equal to the difference between the amount realized on the sale, exchange or redemption and your tax basis in the Security, which should equal the amount you paid to acquire the Security. Your gain or loss will generally be ordinary income or loss (as the case may be) for U.S. federal income tax purposes. However, holders of certain forward contracts, futures contracts or option contracts generally are entitled to make an election under Section 988 of the Internal Revenue Code of 1986, as amended (the “Code”) to treat ordinary gain or loss realized with respect to such instruments as capital gain or loss (a “Section 988 Capital Treatment Election”). Although the matter is uncertain, we believe that it would be reasonable to treat the Section 988 Capital Treatment Election as being available to the Securities. Assuming that the Section 988 Capital Treatment Election is available, if you make this election before the close of the day on which you acquire a Security, all gain or loss you recognize on a sale or exchange of that Security should be treated as long-term capital gain or loss, provided that you have held the Security for more than one year at such time. A U.S. Holder (as defined in the accompanying prospectus supplement) must make the Section 988 Capital Treatment Election with respect to a Security by (a) clearly identifying the transaction on its books and records on the date the transaction is entered into as being subject to this election and either (b) filing the relevant statement verifying this election with the U.S. Holder’s U.S. federal income tax return or (c) otherwise obtaining independent verification as set forth in the Treasury Regulations promulgated under Section 988 of the Code. You should consult your tax advisor regarding the U.S. tax considerations with respect to an investment in the Securities, as well as the availability, mechanics and consequences of a Section 988 Capital Treatment Election. Due to the absence of authorities that directly address the proper characterization of the Securities, no assurance can be given that the Internal Revenue Service (the “IRS”) will accept, or that a court will uphold, this characterization and tax treatment of the Securities, in which case the timing and character of any income or loss on the Securities could be significantly and adversely affected. For example, the Securities could be treated either as “foreign currency contracts” within, the meaning of Section 1256 of the Code or as “contingent payment debt instruments”, as discussed in the section entitled “Certain U.S. Federal Income Tax Considerations” in the accompanying prospectus supplement.

In 2007, the IRS released a revenue ruling holding that a financial instrument with some arguable similarity to the Securities is properly treated as a debt instrument denominated in a foreign currency. The Securities are distinguishable in meaningful respects from the instruments described in the revenue ruling. If, however, the reach of the revenue ruling were to be extended, it could materially and adversely affect the tax consequences of an investment in the Securities for U.S. Holders, possibly with retroactive effect.

In Notice 2008-2, IRS and the Treasury Department requested comments as to whether the purchaser of an exchange traded note or prepaid forward contract (which may include the Securities) should be required to accrue income during its term under a mark-to-market, accrual or other methodology, whether income and gain on such a note or contract should be ordinary or capital, and whether foreign holders should be subject to withholding tax on any deemed income accrual. Accordingly, it is possible that regulations or other guidance could provide that a U.S. holder (as defined in the prospectus supplement) of the Securities is required to accrue income in respect of the Securities prior to the receipt of payments with respect to the Securities or their earlier sale. Moreover, it is possible that any such regulations or other guidance could treat all income and gain of a U.S. holder in respect of the Securities as ordinary income (including gain on a sale). Finally, it is possible that a non-U.S. holder (as defined in the prospectus supplement) of the Securities could be subject to U.S. withholding tax in respect of the Securities. It is unclear whether any regulations or other guidance would apply to the Securities (possibly on a retroactive basis). Prospective investors are urged to consult with their tax advisors regarding Notice 2008-2 and the possible effect to them of the issuance of regulations or other guidance that affects the U.S. federal income tax treatment of the Securities.

For a discussion of the U.S. federal income tax consequences of your investment in a Security, please see the discussion under “Certain U.S. Federal Income Tax Considerations” in the accompanying prospectus supplement.

PROSPECTIVE PURCHASERS OF SECURITIES SHOULD CONSULT THEIR TAX ADVISORS AS TO THE U.S. FEDERAL, STATE, LOCAL, AND OTHER TAX CONSEQUENCES TO THEM OF THE PURCHASE, OWNERSHIP AND DISPOSITION OF SECURITIES.

|

6

|

Key Risks

|

|

An investment in the Securities involves significant risks. Some of the risks that apply to the Securities are summarized here, but you are urged to read the more detailed explanation of risks relating to the Securities generally in the “Risk Factors” section of the accompanying prospectus supplement. You are also urged to consult your investment, legal, tax, accounting and other advisors before you invest in the Securities.

¨ Risk of Loss at Maturity — The Securities differ from ordinary debt securities in that HSBC will not necessarily pay the full Principal Amount of the Securities at maturity. The return on the Securities at maturity is linked to the performance of the Basket and will depend on whether, and to the extent which, the Basket Return is positive or negative. If the Basket Return is negative and the Basket Ending Level is less than the Trigger Level, you will be fully exposed to any negative Basket Return and HSBC will pay you less than the Principal Amount, if anything, resulting in a loss of principal that is proportionate to the decline in the Basket Ending Level as compared to the Basket Starting Level, but, in no case will the Payment at Maturity be less than zero. Under these circumstances, you will lose a significant portion, and could lose all, of your initial investment.

¨ The Contingent Repayment of Principal Applies Only if You Hold the Securities to Maturity — You should be willing to hold your Securities to maturity. If you are able to sell your Securities prior to maturity in the secondary market, you may have to sell them at a loss even if the Basket level is above the Trigger Level at the time of sale.

¨ The Digital Return Applies Only if You Hold the Securities to Maturity — You should be willing to hold your Securities to maturity. If you are able to sell your Securities prior to maturity in the secondary market, the price you receive will likely not reflect the full economic value of the Digital Return or the Securities themselves, and the return you realize may be less than the Basket's return even if such return is positive and below the Digital Return. You can receive the full benefit of the Digital Return from HSBC only if you hold your Securities to maturity.

¨ Certain Built-in Costs are Likely to Adversely Affect the Value of the Securities Prior to Maturity — You should be willing to hold your Securities to maturity. The Securities are not designed to be short-term trading instruments. The price at which you will be able to sell your Securities to HSBC, its affiliates or any party in the secondary market prior to maturity, if at all, may be at a substantial discount from the Principal Amount of the Securities, even in cases where the Basket has appreciated since the Trade Date.

¨ No Interest — HSBC will not make any interest payments with respect to the Securities.

¨ Credit of Issuer — The Securities are senior unsecured debt obligations of the issuer, HSBC, and are not, either directly or indirectly, an obligation of any third party. As further described in the accompanying prospectus supplement and prospectus, the Securities will rank on par with all of the other unsecured and unsubordinated debt obligations of HSBC, except such obligations as may be preferred by operation of law. Any payment to be made on the Securities, including any repayment of principal at maturity, depends on the ability of HSBC to satisfy its obligations as they come due. As a result, the actual and perceived creditworthiness of HSBC may affect the market value of the Securities and, in the event HSBC were to default on its obligations, you may not receive any amounts owed to you under the terms of the Securities and could lose your entire investment.

¨ Your Maximum Possible Return on The Securities is Limited — You will not participate in any appreciation of the Basket and will receive a return equal to the Digital Return if the Basket Return is zero or positive. Therefore, the return on the Securities at maturity is capped by the Digital Return regardless of the appreciation of the Basket, which could be significant. YOU WILL NOT RECEIVE A RETURN ON THE PRINCIPAL AMOUNT GREATER THAN THE DIGITAL RETURN. As a result, your return on the Securities could be less than a direct investment in the Basket Currencies. In addition, because the Currency Return for each Basket Currency is calculated by dividing (i) the difference of the Initial Spot Rate minus the Final Spot Rate by (ii) the Initial Spot Rate, there is no comparable limit on the negative performance of a Basket Currency or resulting overall negative performance of the Basket Return. Consequently, even if three of the Basket Currencies were to appreciate significantly relative to the U.S. dollar, that positive performance could be offset by a severe depreciation of the fourth Basket Currency. However, in no case will the Payment at Maturity be less than zero.

¨ The Securities are Not Insured by any Governmental Agency of The United States or any Other Jurisdiction — The Securities are not deposit liabilities or other obligations of a bank and are not insured by the Federal Deposit Insurance Corporation or any other governmental agency or program of the United States or any other jurisdiction. An investment in the Securities is subject to the credit risk of HSBC, and in the event HSBC is unable to pay its obligations when due, you may not receive any amounts owed to you under the Securities and you could lose your entire investment.

¨ Gains in the Currency Return of One or More Basket Currencies May be Offset by Losses in the Currency Returns of Other Basket Currencies — The Securities are linked to the performance of an equally-weighted basket comprised of the Basket Currencies relative to the U.S. dollar. The performance of the Basket will be based on the appreciation or depreciation of the Basket as a whole. Therefore, the positive Currency Return of one or more Basket Currencies may be offset, in whole or in part, by the negative Currency Return of one or more of the other Basket Currencies of equal or greater magnitude, which may result in an aggregate Basket Return less than zero. The performance of the Basket is dependent on the Currency Return of each Basket Currency, which is in turn based on the formula set forth above.

¨ The Payment at Maturity on Your Securities is Not Based on the Performance of the Basket Currencies Relative to the U.S. Dollar at any Time Other than the Final Valuation Date — The Basket Return will be based solely on the Spot Rates as of the Final Valuation Date relative to the respective Initial Spot Rates. Therefore, if the value of one or more of the Basket Currencies drops precipitously relative to the U.S. dollar on the Final Valuation Date, the Payment at Maturity may be significantly less than it would otherwise have been had the Payment at Maturity been linked to the related currency exchange rates at a time prior to such drop. Although the value of the Basket Currencies relative to the U.S. dollar on the Maturity Date or at other times during the term of your Securities may be higher than on the Final Valuation Date, you will not benefit from any currency exchange rates other than the Spot Rates as of the Final Valuation Date.

¨ Lack of Liquidity — The Securities will not be listed on any securities exchange or quotation system. One of our affiliates may offer to repurchase the Securities in the secondary market but is not required to do so and may cease any such market-making activities at any time without notice. Because other dealers are not likely to make a secondary market for the Securities, the price at which you may be able to trade your Securities is likely to depend on the price, if any, at which one of our affiliates is willing to buy the Securities. This price, if any, will exclude any fees or commissions paid by brokerage account holders when the Securities were purchased and therefore will generally be lower than such purchase price.

¨ Impact of Fees and Hedging on Secondary Market Prices — Generally, the price of the Securities in the secondary market is likely to be lower than the initial offering price since the issue price includes, and the secondary market prices are likely to exclude, hedging costs

|

7

|

or, for brokerage account holders, commissions and other compensation paid with respect to the Securities.

¨ Potential Conflicts Of Interest — The Calculation Agent, which may be HSBC or any of its affiliates, will determine the Payment at Maturity based on the observed Final Spot Rates and resulting Basket Ending Level. The Calculation Agent can postpone the determination of the Basket Ending Level or the Maturity Date if a market disruption event occurs and is continuing on the Final Valuation Date. Such determinations can create a conflict of interest between the obligations of HSBC as the Calculation Agent and you, as a holder of the Securities.

¨ Investing in the Securities Is not Equivalent to Investing Directly in the Basket Currencies — You may receive a lower Payment at Maturity than you would have received if you had invested directly in the Basket Currencies. Additionally, the Basket Return is based on the Currency Return of each of the Basket Currencies, which is in turn based on the formula set forth above. The Currency Returns are based solely on such stated formula and not on any other formula that could be used to calculate currency returns.

¨ The Market Price of the Securities May be Influenced by Unpredictable Factors — The market price of your Securities may fluctuate between the date you purchase them and the Final Valuation Date when the Calculation Agent will determine your Payment at Maturity. Several factors, many of which are beyond our control, will influence the market price of the Securities. We expect that generally the BRL Spot Rate, RUB Spot Rate, INR Spot Rate and CNY Spot Rate on any day will affect the market price of the Securities. Other factors that may influence the market price of the Securities include:

o supply and demand for the Securities;

o Brazilian real, Russian ruble, Indian rupee and Chinese renminbi (Yuan) interest rates, as well as interest and yield rates in the market generally;

o the time remaining to maturity of the Securities;

o economic, financial, political, regulatory or judicial events that affect the financial markets generally, including volatility of the markets; and

o currency exchange rates and the volatility of the currency exchange rates between the Basket Currencies and the U.S. dollar.

¨ Legal and Regulatory Risks — Legal and regulatory changes could adversely affect currency rates. In addition, many governmental agencies and regulatory organizations are authorized to take extraordinary actions in the event of market emergencies. It is not possible to predict the effect of any future legal or regulatory action relating to currency rates, but any such action could cause unexpected volatility and instability in currency markets with a substantial and adverse effect on the performance of the Basket Currencies and, consequently, on the value of the Securities.

¨ The Securities are Subject to Emerging Markets’ Political and Economic Risks — Each Basket Currency is the currency of an emerging market country. Emerging market countries are more exposed to the risk of swift political change, military activity, including wars, and economic downturns than their industrialized counterparts. In recent years, emerging markets have undergone significant political, economic and social change. Such far-reaching political changes have resulted in constitutional, military and social tensions, and, in some cases, instability and reaction against market reforms have occurred. With respect to any emerging or developing nation, there is the possibility of nationalization, expropriation or confiscation, political changes, government regulation and social instability. There can be no assurance that future political or military changes will not adversely affect the economic conditions of an emerging or developing-market nation. Political or economic instability, including the possibility of military activity or war, is likely to have an adverse effect on the performance of the Basket Currencies, and, consequently, the return on the Securities.

¨ The Exchange Rate Of the Chinese Renminbi (Yuan) is Currently Managed by the Chinese Government — The U.S. dollar/Chinese renminbi (Yuan) exchange rate is managed by the Chinese government to float within a narrow band with reference to a basket of currencies and is based on a daily poll of onshore market dealers and other undisclosed factors. The People’s Bank of China, the monetary authority in China, may also use a variety of techniques, such as imposition of regulatory controls or taxes, to affect the U.S. dollar/Chinese renminbi (Yuan) exchange rate. The People’s Bank has stated that it will make adjustments of the Chinese renminbi (Yuan) exchange rate band when necessary according to market developments as well as the economic and financial situation. In the future, the Chinese government may also issue a new currency to replace its existing currency or alter the exchange rate or relative exchange characteristics by devaluation or revaluation of the Chinese renminbi (Yuan) in ways that may be adverse to your interests.

The Chinese government continues to manage the valuation of the Chinese renminbi (Yuan), and, as currently managed, its price movements may not contribute significantly to either an increase or decrease in the CNY Spot Rate. If the exchange rate of the Chinese renminbi (Yuan) declines, it will limit your potential return on the Securities. However, changes in the Chinese government’s management of the Chinese renminbi (Yuan) could result in a more significant movement in the U.S. dollar/Chinese renminbi (Yuan) exchange rate. A decrease in the value of the Chinese renminbi (Yuan), whether as a result of a change in the government’s management of the currency or for other reasons, could result in a change in the CNY Spot Rate.

¨ If the Liquidity of the Basket Currencies is Limited, the Value of the Securities Would Likely be Impaired — Currencies and derivatives contracts on currencies may be difficult to buy or sell, particularly during adverse market conditions. Reduced liquidity on the Final Valuation Date would likely have an adverse effect on the Final Spot Rate for each Basket Currency, and therefore, on the return on your Securities. Limited liquidity relating to any Basket Currency may also result in the Calculation Agent being unable to determine the Currency Returns, and therefore the Basket Return, using its normal means. The resulting discretion by the Calculation Agent in determining the Basket Return could, in turn, result in potential conflicts of interest.

¨ Currency Markets May Be Volatile — Foreign currency rate risks include, but are not limited to, convertibility risk, market volatility and potential interference by foreign governments through regulation of local markets, foreign investment or particular transactions in foreign currency. The liquidity, trading value and amount payable under the Securities could be affected by actions of the governments of the United States, Brazil, Russia, India or China. These factors may affect the values of the Basket Currencies and the value of your Securities in varying ways, and different factors may cause the values of the Basket Currencies, as well as the volatility of their prices, to move in inconsistent directions at inconsistent rates.

¨ Historical Performance of the Basket Currencies Should Not be Taken as an Indication of the Future Performance of the Basket Currencies During the Term of the Securities — It is impossible to predict whether any of the Spot Rates for the Basket Currencies will rise or fall. The Basket Currencies will be influenced by complex and interrelated political, economic, financial and other factors and the past performance of the Basket Currencies is not indicative of the future performance of the Basket Currencies.

¨ We Have No Control Over Exchange Rates — Foreign exchange rates can either float or be fixed by sovereign governments. Exchange rates of the currencies used by most economically developed nations are permitted to fluctuate in value relative to the U.S. dollar and to each other. However, from time to time governments may use a variety of techniques, such as intervention by a central bank, the imposition of regulatory controls or taxes or changes in interest rates to influence the exchange rates of their currencies. Governments may also issue a new currency to replace an existing currency or alter the exchange rate or relative exchange characteristics by a devaluation or revaluation of a currency. These governmental actions could change or interfere with currency valuations and currency fluctuations that would otherwise occur in response to economic forces, as well as in response to the movement of currencies across borders. As a consequence, these government actions could adversely affect an investment in a security that is linked to an exchange rate,

|

8

such as the Securities.

¨ Market Disruptions May Adversely Affect Your Return — The Calculation Agent may, in its sole discretion, determine that the markets have been affected in a manner that prevents it from determining the Basket Return in the manner described herein, and calculating the amount that we are required to pay you upon maturity, or from properly hedging its obligations under the Securities. These events may include disruptions or suspensions of trading in the markets as a whole or general inconvertibility or non-transferability of one or more currencies. If the Calculation Agent, in its sole discretion, determines that any of these events prevents us or any of our affiliates from properly hedging our obligations under the Securities or prevents the Calculation Agent from determining the Basket Return or payment on the Maturity Date in the ordinary manner, the Calculation Agent will determine the Basket Return or payment on the Maturity Date in good faith and in a commercially reasonable manner, and it is possible that the Final Valuation Date and the Maturity Date will be postponed, which may adversely affect the return on your Securities. For example, if the source for an exchange rate is not available on the Final Valuation Date, the Calculation Agent may determine the exchange rate for such date, and such determination may adversely affect the return on your Securities.

¨ Potentially Inconsistent Research, Opinions or Recommendations by HSBC, UBS or Their Respective Affiliates — HSBC, UBS Financial Services Inc., or their respective affiliates may publish research, express opinions or provide recommendations that are inconsistent with investing in or holding the Securities and which may be revised at any time. Any such research, opinions or recommendations could affect the level of the Basket, and therefore, the market price of the Securities.

¨ Uncertain Tax Treatment — There is no direct legal authority as to the proper tax treatment of the Securities, and therefore significant aspects of the tax treatment of the Securities are uncertain as to both the timing and character of any inclusion in income in respect of the Securities. Under one reasonable approach, the Securities should be treated as pre-paid forward or other executory contracts with respect to the Basket. HSBC intends to treat the Securities consistent with this approach and pursuant to the terms of the Securities, you agree to treat the Securities under this approach for all U.S. federal income tax purposes. See “Certain U.S. Federal Income Tax Considerations — Certain Equity-Linked Notes — Certain Notes Treated as Forward Contracts or Executory Contracts” in the prospectus supplement for the U.S. federal income tax considerations applicable to Securities that are treated as pre-paid cash-settled forward or other executory contracts. Because of the uncertainty regarding the tax treatment of the Securities, we urge you to consult your tax advisor as to the tax consequences of your investment in a Security.

In Notice 2008-2, the Internal Revenue Service (“IRS”) and the Treasury Department requested comments as to whether the purchaser of an exchange traded note or prepaid forward contract (which may include the Securities) should be required to accrue income during its term under a mark-to-market, accrual or other methodology, whether income and gain on such a note or contract should be ordinary or capital, and whether foreign holders should be subject to withholding tax on any deemed income accrual. Accordingly, it is possible that regulations or other guidance could provide that a U.S. holder (as defined in the prospectus supplement) of the Securities is required to accrue income in respect of the Securities prior to the receipt of payments with respect to the Securities or their earlier sale. Moreover, it is possible that any such regulations or other guidance could treat all income and gain of a U.S. holder in respect of the Securities as ordinary income (including gain on a sale). Finally, it is possible that a non-U.S. holder (as defined in the prospectus supplement) of the Securities could be subject to U.S. withholding tax in respect of the Securities. It is unclear whether any regulations or other guidance would apply to the Securities (possibly on a retroactive basis). Prospective investors are urged to consult with their tax advisors regarding Notice 2008-2 and the possible effect to them of the issuance of regulations or other guidance that affects the U.S. federal income tax treatment of the Securities.

For a more complete discussion of the U.S. federal income tax consequences of your investment in a Security, please see the discussion under “Certain U.S. Federal Income Tax Considerations” in the prospectus supplement.

9

|

Scenario Analysis and Hypothetical Examples

|

The following tables and examples illustrate the hypothetical Payment at Maturity per $10 Security for a hypothetical range of Basket Returns, reflect the Trigger Level of 80 and assume a Digital Return of 30%. The actual Digital Return will be determined on the Trade Date and will not be less than 30% or greater than 35%. The hypothetical total returns set forth below are for illustrative purposes only and may not be the actual total returns applicable to a holder of the Securities. The numbers appearing in the following tables and examples have been rounded for ease of analysis.

|

Basket Ending

Level

|

Hypothetical Basket Return

|

Payment at Maturity

|

Total Return on the

Securities Purchased

at $10.00 (1)

|

Total Return on

Securities Purchased at

$9.80 by Advisory

Accounts (2)

|

|

170.00

|

70.00%

|

$13.00

|

30.00%

|

32.65%

|

|

160.00

|

60.00%

|

$13.00

|

30.00%

|

32.65%

|

|

150.00

|

50.00%

|

$13.00

|

30.00%

|

32.65%

|

|

140.00

|

40.00%

|

$13.00

|

30.00%

|

32.65%

|

|

130.00

|

30.00%

|

$13.00

|

30.00%

|

32.65%

|

|

120.00

|

20.00%

|

$13.00

|

30.00%

|

32.65%

|

|

110.00

|

10.00%

|

$13.00

|

30.00%

|

32.65%

|

|

105.00

|

5.00%

|

$13.00

|

30.00%

|

32.65%

|

|

101.00

|

1.00%

|

$13.00

|

30.00%

|

32.65%

|

|

100.00

|

0.00%

|

$13.00

|

30.00%

|

32.65%

|

|

95.00

|

-5.00%

|

$10.00

|

0.00%

|

2.04%

|

|

90.00

|

-10.00%

|

$10.00

|

0.00%

|

2.04%

|

|

80.00

|

-20.00%

|

$10.00

|

0.00%

|

2.04%

|

|

70.00

|

-30.00%

|

$7.00

|

-30.00%

|

-28.57%

|

|

60.00

|

-40.00%

|

$6.00

|

-40.00%

|

-38.78%

|

|

50.00

|

-50.00%

|

$5.00

|

-50.00%

|

-48.98%

|

|

40.00

|

-60.00%

|

$4.00

|

-60.00%

|

-59.18%

|

|

30.00

|

-70.00%

|

$3.00

|

-70.00%

|

-69.39%

|

|

20.00

|

-80.00%

|

$2.00

|

-80.00%

|

-79.59%

|

|

10.00

|

-90.00%

|

$1.00

|

-90.00%

|

-89.80%

|

|

0.00

|

-100.00%

|

$0.00

|

-100.00%

|

-100.00%

|

|

-10.00

|

-110.00%

|

$0.00

|

-100.00%

|

-100.00%

|

|

-20.00

|

-120.00%

|

$0.00

|

-100.00%

|

-100.00%

|

|

-30.00

|

-130.00%

|

$0.00

|

-100.00%

|

-100.00%

|

* Because you will receive a return equal to the Digital Return if the Basket Return is zero or positive, the return on the Securities at maturity is capped at the Digital Return regardless of the appreciation of the Basket, which could be significant. Since the Currency Return is calculated pursuant to the formula set forth in "Indicative Terms", there is no comparable limit on the negative performance of a Currency Return or the Basket Return. However, in no case will the Payment at Maturity be less than zero.

(1) This “Return on Securities” is the number, expressed as a percentage, that results from comparing the Payment at Maturity per $10 Principal Amount Security to the purchase price of $10 per Security for all brokerage account holders.

(2) This “Return on Securities” is the number, expressed as a percentage, that results from comparing the Payment at Maturity per $10 Principal Amount Security to the purchase price of $9.80 per Security, which is the purchase price for investors in advisory accounts. See "Supplemental Plan of Distribution (Conflicts of Interest)" on the last page of this free writing prospectus.

10

The following table illustrates hypothetical Currency Returns at maturity for one of the Basket Currencies (USD/BRL) calculated for a hypothetical range of Final Spot Rates and assuming an Initial Spot Rate of 1.8454. The actual Initial Spot Rate will be determined on the Trade Date and the Final Spot Rate may be higher than 5.3148. Your return on the Securities will be based on the Basket Return, which is determined using the Currency Returns for each Basket Currency as described in “Indicative Terms” herein. The following results are based solely on the hypothetical example cited.

|

Hypothetical Final Spot Rate

|

Currency Return

|

|

5.3148

|

-188%

|

|

4.8534

|

-163%

|

|

4.7980

|

-160%

|

|

4.3921

|

-138%

|

|

4.2444

|

-130%

|

|

4.1522

|

-125%

|

|

3.9307

|

-113%

|

|

3.6908

|

-100%

|

|

3.4694

|

-88%

|

|

3.2295

|

-75%

|

|

3.0080

|

-63%

|

|

2.7681

|

-50%

|

|

2.5467

|

-38%

|

|

2.3068

|

-25%

|

|

2.0853

|

-13%

|

|

1.8454

|

0%

|

|

1.6055

|

13%

|

|

1.3841

|

25%

|

|

1.1441

|

38%

|

|

0.9227

|

50%

|

|

0.6828

|

63%

|

|

0.4614

|

75%

|

|

0.2214

|

88%

|

|

0.0000

|

100%

|

The Final Spot Rate for each Basket Currency cannot be below zero, however there is no comparable upside limitation. Accordingly, the method of calculating the Currency Returns may result in gains of any Basket Currency (the relevant currency appreciates against the U.S. dollar resulting in a declining Final Spot Rate) being subject to a maximum Currency Return of 100%, while losses of any Basket Currency (the relevant currency depreciates against the U.S. dollar resulting in an increasing Final Spot Rate) are unlimited. However, in no event will the Payment at Maturity exceed an amount based on the Digital Return, or be less than $0.00.

11

Hypothetical Examples:

The following payment examples for the Securities show scenarios for the Payment at Maturity on the Securities, illustrating positive and negative Basket Returns reflecting either correlated or offsetting appreciation and depreciation in the Basket Currencies relative to the U.S. dollar. The following examples are based on the Trigger Level of 80, a hypothetical Digital Return of 30%, as well as hypothetical Initial Spot Rates (the actual value of each will be determined on the Trade Date) and Final Spot Rates (which will be determined on the Final Valuation Date). The hypothetical Initial Spot Rate and Final Spot Rate values have been chosen arbitrarily for the purpose of illustration only, and should not be taken as indicative of the future performance of any Basket Currency relative to the U.S. dollar.

Example 1: As of the Final Valuation Date, all Basket Currencies strengthen against the U.S. dollar. (This occurs when the Final Spot Rate decreases from the Initial Spot Rate, reflecting a fewer number of the Basket Currency per U.S. dollar.)

Step 1: Calculate the Currency Return for each of the Basket Currencies.

|

Basket Currency

|

Hypothetical

Initial Spot

Rate

|

Hypothetical

Final Spot

Rate

|

Hypothetical

Currency

Return

|

|||

|

BRL

|

1.8454

|

1.7347

|

6.00%

|

|||

|

RUB

|

31.2410

|

28.7417

|

8.00%

|

|||

|

INR

|

52.0188

|

49.4179

|

5.00%

|

|||

|

CNY

|

6.3770

|

6.1857

|

3.00%

|

The Currency Return for each Basket Currency is calculated as follows:

Initial Spot Rate – Final Spot Rate

Initial Spot Rate

Step 2: Calculate the Basket Ending Level.

The Basket Ending Level is calculated as follows:

100 x [1 + (25% × 6.00%) + (25% × 8.00%) + (25% × 5.00%) + (25% × 3.00%)] = 105.50

Step 3: Calculate the Basket Return.

The Basket Return is calculated as follows:

Step 4: Calculate the Payment at Maturity.

Because the Basket Return of 5.50% is positive, HSBC will pay a Payment at Maturity calculated as follows per $10 Security:

$10 + ($10 × Digital Return)

$10 + ($10 × 30%) = $10 + $3 = $13.00

The Payment at Maturity of $13.00 per $10 Security represents a total return on the Securities of 30.00% for brokerage accounts and 32.65% for advisory accounts.

Example 2: As of the Final Valuation Date, all Basket Currencies strengthen against the U.S. dollar. (This occurs when the Final Spot Rate decreases from the Initial Spot Rate, reflecting a fewer number of the Basket Currency per U.S. dollar.)

Step 1: Calculate the Currency Return for each of the Basket Currencies.

|

Basket Currency

|

Hypothetical

Initial Spot

Rate

|

Hypothetical

Final Spot

Rate

|

Hypothetical

Currency

Return

|

|||

|

BRL

|

1.8454

|

0.9227

|

50.00%

|

|||

|

RUB

|

31.2410

|

12.4964

|

60.00%

|

|||

|

INR

|

52.0188

|

28.6103

|

45.00%

|

|||

|

CNY

|

6.3770

|

2.8697

|

55.00%

|

12

The Currency Return for each Basket Currency is calculated as follows:

Initial Spot Rate – Final Spot Rate

Initial Spot Rate

Step 2: Calculate the Basket Ending Level.

The Basket Ending Level is calculated as follows:

100 x [1 + (25% × 50.00%) + (25% × 60.00%) + (25% × 45.00%) + (25% × 55.00%)] = 152.50

Step 3: Calculate the Basket Return.

The Basket Return is calculated as follows:

Step 4: Calculate the Payment at Maturity.

Because the Basket Return of 52.50% is positive, HSBC will pay a Payment at Maturity calculated as follows per $10 Security:

$10 + ($10 × Digital Return)

$10 + ($10 × 30%) = $10 + $3 = $13.00

The Payment at Maturity of $13.00 per $10 Security represents a total return on the Securities of 30.00% for brokerage accounts and 32.65% for advisory accounts.

Example 3: As of the Final Valuation Date, three of the Basket Currencies strengthen against the U.S. dollar (this occurs when the Final Spot Rate decreases from the Initial Spot Rate, reflecting a fewer number of the Basket Currency per U.S. dollar) and one of the Basket Currencies weakens against the U.S. dollar (this occurs when the Final Spot Rate increases from the Initial Spot Rate, reflecting a greater number of the Basket Currency per U.S. dollar).

Step 1: Calculate the Currency Return for each of the Basket Currencies.

|

Basket Currency

|

Hypothetical

Initial Spot

Rate

|

Hypothetical

Final Spot

Rate

|

Hypothetical

Currency

Return

|

|||

|

BRL

|

1.8454

|

2.3990

|

-30.00%

|

|||

|

RUB

|

31.2410

|

29.9914

|

4.00%

|

|||

|

INR

|

52.0188

|

49.9380

|

4.00%

|

|||

|

CNY

|

6.3770

|

6.1219

|

4.00%

|

The Currency Return for each Basket Currency is calculated as follows:

Initial Spot Rate – Final Spot Rate

Initial Spot Rate

Step 2: Calculate the Basket Ending Level.

The Basket Ending Level is calculated as follows:

100 × [1 + (25% × -30.00%) + (25% × 4.00%) + (25% × 4.00%) + (25% × 4.00%)] = 95.50

Step 3: Calculate the Basket Return.

The Basket Return is calculated as follows:

Step 4: Calculate the Payment at Maturity.

Because the Basket Return of -4.50% is negative but the Basket Ending Level of 95.50 is greater than or equal to the Trigger Level of 80, HSBC will pay a Payment at Maturity equal to the $10 Principal Amount for a total return on the Securities of 0.00% for brokerage accounts and 2.04% for advisory accounts.

13

Example 4: As of the Final Valuation Date, all Basket Currencies weaken against the U.S. dollar. (This occurs when the Final Spot Rate increases from the Initial Spot Rate, reflecting a greater number of the Basket Currency per U.S. dollar.)

Step 1: Calculate the Currency Return for each of the Basket Currencies.

|

Basket Currency

|

Hypothetical

Initial Spot

Rate

|

Hypothetical

Final Spot

Rate

|

Hypothetical

Currency

Return

|

|||

|

BRL

|

1.8454

|

2.2145

|

-20.00%

|

|||

|

RUB

|

31.2410

|

43.7374

|

-40.00%

|

|||

|

INR

|

52.0188

|

72.8263

|

-40.00%

|

|||

|

CNY

|

6.3770

|

8.2901

|

-30.00%

|

The Currency Return for each Basket Currency is calculated as follows:

Initial Spot Rate – Final Spot Rate

Initial Spot Rate

Step 2: Calculate the Basket Ending Level.

The Basket Ending Level is calculated as follows:

100 × [1 + (25% × -20.00%) + (25% × -40.00%) + (25% × -40.00%) + (25% × -30.00%)] = 67.50

Step 3: Calculate the Basket Return.

The Basket Return is calculated as follows:

Step 4: Calculate the Payment at Maturity.

Because the Basket Return of -32.50% is negative and the Basket Ending Level of 67.50 is less than the Trigger Level of 80, HSBC will pay a Payment at Maturity less than the Principal Amount calculated as follows per $10 Security:

$10 + [$10 × Basket Return]

$10 + ($10 × -32.50%) = $10 + -$3.25 = $6.75

The Payment at Maturity of $6.75 per $10 Security represents a total return on the Securities of -32.50% for brokerage accounts and -31.12% for advisory accounts.

14

|

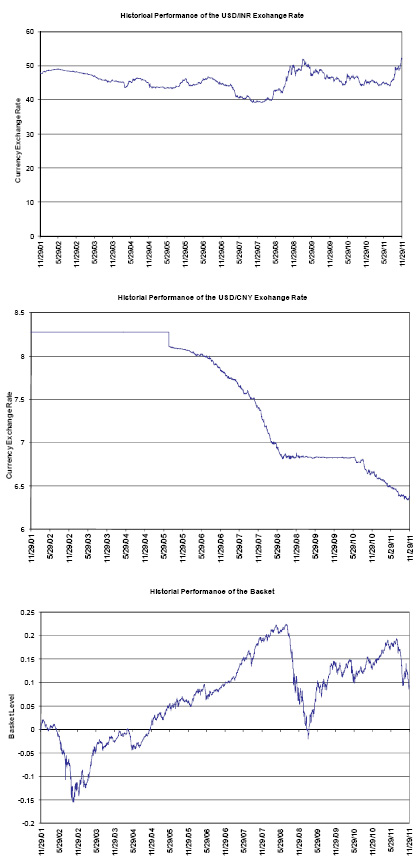

Historical Performance of the Basket Currencies

|

The first four graphs below set forth the historical performance of the USD/BRL, USD/RUB, USD/INR and USD/CNY currency exchange rates from November 29, 2001 through November 29, 2011 (based on the daily closing spot exchange rates from Bloomberg L.P.). On November 29, 2011, such closing spot exchange rates of BRL, RUB, INR and CNY were 1.8454, 31.2410, 52.0188 and 6.3770, respectively.

The last graph shows the hypothetical historical performance of the Basket from November 29, 2001 through November 29, 2011, assuming that the Basket Ending Level on November 29, 2001 was 100, that each Basket Currency had a 25% weight in the Basket on that date, and that the historical exchange rates of each Basket Currency on the relevant dates were the closing spot exchange rates on such dates. The hypothetical basket performance is based on actual historical data of the Basket Currencies and the hypothetical basket performance displayed in the graph below is a reflection of this aggregated actual historical data. The hypothetical historical performance of the Basket should not be taken as an indication of the Basket's future performance.

We obtained the information regarding the currency exchange rates of the BRL, RUB, INR and CNY against the USD below from Bloomberg L.P. We make no representation or warranty as to the accuracy or completeness of the information obtained from Bloomberg L.P. The actual spot rates for each Basket Currency will be determined as described in "Indicative Terms" on page 4, and not from Bloomberg L.P. The historical performance of the closing currency exchange rates of the BRL, RUB, INR and CNY against the USD should not be taken as an indication of future performance of such currency exchange rates, and no assurance can be given as to the currency exchange rates on the Final Valuation Date. We cannot give you assurance that the performance of the USD/BRL, USD/RUB, USD/INR and USD/CNY currency exchange rates will result in a positive Basket Return at maturity and we cannot assure that you will receive any of your initial investment in the Securities at maturity.

Your Payment at Maturity will be based on the performance of an equally-weighted basket of currencies relative to the U.S. dollar. The decline of the exchange rate of any Basket Currency (meaning such Basket Currency strengthens relative to the U.S. dollar) will have a positive impact on the overall Basket Return. Conversely, the increase in the exchange rate of any Basket Currency (meaning such Basket Currency weakens relative to the U.S. dollar) will have a negative impact on the overall Basket Return. Exchange rate movements in the Basket Currencies may not correlate with each other, and the decrease in the exchange rate (or strengthening) of one Basket Currency relative to the U.S. dollar may be moderated, or more than offset, by lesser decreases or an increase in the exchange rate (or weakening) of the other Basket Currencies relative to the U.S. dollar.

15

16

|

Market Disruption Events

|

The Calculation Agent may, in its sole discretion, determine that an event has occurred that prevents it from valuing one or more of the Basket Currencies or the Payment at Maturity in the manner initially provided for herein. These events may include disruptions or suspensions of trading in the markets as a whole or general inconvertibility or non-transferability of one or more Basket Currencies. If the Calculation Agent, in its sole discretion, determines that any of these events prevents us or our affiliates from properly hedging our obligations under the Securities or prevents the Calculation Agent from determining such value or amount in the ordinary manner on such date, the Calculation Agent may determine such value or amount in good faith and in a commercially reasonable manner on such date or, in the discretion of the Calculation Agent, the Final Valuation Date, and Maturity Date may be postponed for up to five scheduled trading days, each of which may adversely affect the return on your Securities. If the Final Valuation Date has been postponed for five consecutive scheduled trading days, then that fifth scheduled trading day will be the Final Valuation Date and the Calculation Agent will determine the level of such Basket Currency or Basket Currencies using the formula for and method of determining such level which applied just prior to the market disruption event (or in good faith and in a commercially reasonable manner) on such date.

|

Events of Default and Acceleration

|

|

If the Securities have become immediately due and payable following an event of default (as defined in the accompanying prospectus) with respect to the Securities, the Calculation Agent will determine the accelerated payment due and payable at maturity in the same general manner as described in “Indicative Terms” in this free writing prospectus. In that case, the business day preceding the date of acceleration will be used as the Final Valuation Date for purposes of determining the accelerated Basket Return (including each Final Spot Rate). The accelerated Maturity Date will then be the fourth business day following the postponed accelerated Final Valuation Date (including each Final Spot Rate).