|

Filed Pursuant to Rule 433

Registration No. 333-158385

October 11, 2011

FREE WRITING PROSPECTUS

(To Prospectus dated April 2, 2009,

Prospectus Supplement dated April 9, 2009,

and Product Supplement dated April 9, 2009)

|

|

Structured

Investments

|

HSBC USA Inc.

$

Buffered Return Enhanced Notes Linked to the iShares® MSCI Emerging Markets Index Fund due October 31, 2012 (the “Notes”)

|

General

|

|

·

|

Terms used in this free writing prospectus are described or defined herein, in the accompanying product supplement, prospectus supplement and prospectus. The Notes offered will have the terms described herein and in the accompanying product supplement, prospectus supplement and prospectus. The Notes are not principal protected, and you may lose up to 100.00% of your initial investment.

|

|

|

·

|

All references to “Enhanced Market Participation Notes” in the product supplement shall refer to these Buffered Return Enhanced Notes.

|

|

|

·

|

This free writing prospectus relates to a single note offering. The purchaser of a Note will acquire a security linked to a single Reference Asset described below.

|

|

|

·

|

Although the offering relates to a Reference Asset, you should not construe that fact as a recommendation as to the merits of acquiring an investment linked to the Reference Asset or any component security included in the Reference Asset or as to the suitability of an investment in the related Notes.

|

|

|

·

|

Senior unsecured debt obligations of HSBC USA Inc. maturing October 31, 2012.

|

|

|

·

|

Minimum denominations of $10,000 and integral multiples of $1,000 in excess thereof.

|

|

|

·

|

If the terms of the Notes set forth below are inconsistent with those described in the accompanying product supplement, the terms set forth below will supersede.

|

Key Terms

|

Issuer:

|

HSBC USA Inc.

|

|

Issuer Rating:

|

AA- (S&P), A1 (Moody’s), AA (Fitch)*

|

|

Reference Asset:

|

The iShares® MSCI Emerging Markets Index Fund (“EEM”)

|

|

Principal Amount:

|

$1,000 per Note.

|

|

Trade Date:

|

October 14, 2011

|

|

Pricing Date:

|

October 14, 2011

|

|

Original Issue Date:

|

October 19, 2011

|

|

Ending Averaging Dates:

|

October 22, 2012, October 23, 2012, October 24, 2012, October 25, 2012 and October 26, 2012 (the Final Valuation Date), subject to adjustment as described herein and in the accompanying product supplement.

|

|

Final Valuation Date:

|

October 26, 2012 , subject to adjustment as described herein and in the accompanying product supplement.

|

|

Maturity Date:

|

3 business days after the Final Valuation Date and is expected to be October 31, 2012. The Maturity Date is subject to further adjustment as described under “Market Disruption Events” herein and under “Specific Terms of the Notes — Market Disruption Events” in the accompanying product supplement.

|

|

Payment at Maturity:

|

For each Note, the Cash Settlement Value.

|

|

Cash Settlement Value:

|

For each Note, you will receive a cash payment on the Maturity Date that is based on the Reference Return (as described below):

|

|

If the Reference Return is greater than or equal to 0.00%, you will receive an amount equal to 100.00% of the Principal Amount plus the lesser of:

|

|

|

(i) the product of (a) the Principal Amount multiplied by (b) the Reference Return multiplied by the Upside Participation Rate; and

|

|

|

(ii) the product of (a) the Principal Amount multiplied by (b) the Maximum Return.

|

|

|

If the Reference Return is less than 0.00% but greater than or equal to -10.00%, meaning that the price of the Reference Asset declines by no more than the 10.00% Buffer Amount, at maturity, you will receive 100.00% of the Principal Amount.

|

|

|

If the Reference Return is less than -10.00%, meaning that the price of the Reference Asset declines by more than the 10.00% Buffer Amount, at maturity, you will lose 1.11111% of the Principal Amount for each percentage point that the Reference Return is below -10.00%. This means that if the Reference Return is -100.00%, you will lose your entire investment.

|

|

|

Upside Participation Rate:

|

200.00%

|

|

Maximum Return:

|

25.00%

|

|

Buffer Amount:

|

10.00%

|

|

Downside Leverage Factor:

|

1.11111

|

|

Reference Return:

|

The quotient, expressed as a percentage, calculated as follows:

|

|

Final Price – Initial Price

|

|

|

Initial Price

|

|

|

Initial Price:

|

The Official Closing Price of the Reference Asset on the Pricing Date.

|

|

Final Price:

|

The arithmetic average of the Official Closing Prices of the Reference Asset on the five Ending Averaging Dates, as determined by the calculation agent.

|

|

Official Closing Price:

|

The Official Closing Price of the Reference Asset on any scheduled trading day as determined by the calculation agent based upon the value displayed on Bloomberg Professional® service page “EEM UP <EQUITY>” or any successor page on Bloomberg Professional® service or any successor service, as applicable, adjusted by the calculation agent as described under “Adjustments to an ETF” in the accompanying product supplement.

|

|

Calculation Agent:

|

HSBC USA Inc. or one of its affiliates

|

|

CUSIP/ISIN:

|

4042K1QK2 /

|

|

Form of Notes:

|

Book-Entry

|

|

Listing:

|

The Notes will not be listed on any U.S. securities exchange or quotation system.

|

* A credit rating reflects the creditworthiness of HSBC USA Inc. and is not a recommendation to buy, sell or hold securities, and it may be subject to revision or withdrawal at any time by the assigning rating organization. The Notes themselves have not been independently rated. Each rating should be evaluated independently of any other rating.

Investment in the Notes involves certain risks. You should refer to “Selected Risk Considerations” beginning on page 5 of this document and “Risk Factors” on page PS-4 of the product supplement and page S-3 of the prospectus supplement.

Neither the U.S. Securities and Exchange Commission, or the SEC, nor any state securities commission has approved or disapproved of the Notes or determined that this free writing prospectus, or the accompanying product supplement, prospectus supplement and prospectus, is truthful or complete. Any representation to the contrary is a criminal offense.

The Notes are not deposit liabilities or other obligations of a bank and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency of the United States or any other jurisdiction, and involve investment risks including possible loss of the Principal Amount invested due to the credit risk of HSBC. HSBC Securities (USA) Inc. or another of our affiliates or agents may use the pricing supplement to which this free writing prospectus relates in market-making transactions in any Notes after their initial sale. Unless we or our agent informs you otherwise in the confirmation of sale, the pricing supplement to which this free writing prospectus relates is being used in a market-making transaction. HSBC Securities (USA) Inc., an affiliate of ours, will purchase the Notes from us for distribution to the placement agent. See “Supplemental Plan of Distribution (Conflicts of Interest)” on the last page of this free writing prospectus.

We have appointed J.P. Morgan Securities LLC and certain of its registered broker dealer affiliates as placement agent for the sale of the Notes. J.P. Morgan Securities LLC and certain of its registered broker dealer affiliates will offer the Notes to investors directly or through other registered broker dealers.

|

Price to Public(1)

|

Fees and Commissions

|

Proceeds to Issuer

|

|

|

Per Note

|

$1,000

|

$10

|

$990

|

|

Total

|

(1) Certain fiduciary accounts purchasing the Notes will pay a purchase price of $990 per Note, and the placement agents with respect to sales made to such accounts will forgo any fees.

JPMorgan

Placement Agent

October 11, 2011

Additional Terms Specific to the Notes

This free writing prospectus relates to a single note offering linked to the Reference Asset identified on the cover page. The purchaser of a Note will acquire a senior unsecured debt security linked to the Reference Asset. We reserve the right to withdraw, cancel or modify any offering and to reject orders in whole or in part. Although the Note offering relates only to a single Reference Asset identified on the cover page, you should not construe that fact as a recommendation as to the merits of acquiring an investment linked to the Reference Asset or any securities comprising the Reference Asset or as to the suitability of an investment in the Notes.

You should read this document together with the prospectus dated April 2, 2009, the prospectus supplement dated April 9, 2009 and the product supplement dated April 9, 2009. If the terms of the Notes offered hereby are inconsistent with those described in the accompanying product supplement, prospectus supplement or prospectus, the terms described in this free writing prospectus shall control. You should carefully consider, among other things, the matters set forth in “Selected Risk Considerations” beginning on page 5 of this free writing prospectus and “Risk Factors” on page PS-4 of the product supplement and page S-3 of the prospectus supplement, as the Notes involve risks not associated with conventional debt securities. All references to “Enhanced Market Participation Notes” in the product supplement shall refer to these Buffered Return Enhanced Notes. We urge you to consult your investment, legal, tax, accounting and other advisors before you invest in the Notes. As used herein, references to the “Issuer”, “HSBC”, “we”, “us” and “our” are to HSBC USA Inc.

HSBC has filed a registration statement (including a prospectus, a prospectus supplement and a product supplement) with the SEC for the offering to which this free writing prospectus relates. Before you invest, you should read the prospectus, prospectus supplement and product supplement in that registration statement and other documents HSBC has filed with the SEC for more complete information about HSBC and this offering. You may get these documents for free by visiting EDGAR on the SEC’s web site at www.sec.gov. Alternatively, HSBC Securities (USA) Inc. or any dealer participating in this offering will arrange to send you the prospectus, prospectus supplement and product supplement if you request them by calling toll-free 1-866-811-8049.

You may also obtain:

|

•

|

the product supplement at www.sec.gov/Archives/edgar/data/83246/000114420409019791/v145840_424b2.htm

|

|

•

|

the prospectus supplement at www.sec.gov/Archives/edgar/data/83246/000114420409019785/v145824_424b2.htm

|

|

•

|

We are using this free writing prospectus to solicit from you an offer to purchase the Notes. You may revoke your offer to purchase the Notes at any time prior to the time at which we accept your offer by notifying HSBC Securities (USA) Inc. We reserve the right to change the terms of, or reject any offer to purchase, the Notes prior to their issuance. In the event of any material changes to the terms of the Notes, we will notify you.

Supplemental Information Relating to the Terms of the Notes

Notwithstanding anything contained in the accompanying prospectus supplement or product supplement to the contrary, the Notes will be issued under the senior indenture dated March 31, 2009, between HSBC, as Issuer, and Wells Fargo Bank, National Association, as trustee. Such indenture has substantially the same terms as the indenture described in the accompanying prospectus supplement and product supplement. HSBC Bank USA, N.A. will act as paying agent with respect to the Notes pursuant to a Paying Agent and Securities Registrar Agreement dated June 1, 2009, between HSBC and HSBC Bank USA, N.A.

-2-

What Is the Total Return on the Notes at Maturity Assuming a Range of Performance for the Reference Asset?

The following table illustrates the hypothetical total return at maturity on the Notes. The “total return” as used in this free writing prospectus is the number, expressed as a percentage, that results from comparing the Payment at Maturity per $1,000 Principal Amount of Notes to $1,000. The hypothetical total returns set forth below reflect the Upside Participation Rate of 200.00%, the Buffer Amount of 10.00%, the Downside Leverage Factor of 1.11111 and the Maximum Return on the Notes of 25.00% and assume an Initial Price of $38.07. The actual Initial Price will be determined on the Pricing Date. The hypothetical total returns set forth below are for illustrative purposes only and may not be the actual total returns applicable to a purchaser of the Notes. The numbers appearing in the following table and examples have been rounded for ease of analysis.

|

Hypothetical

Final Price |

Hypothetical

Reference Return |

Hypothetical Total

Return on the Notes |

|

$76.14

|

100.00%

|

25.000%

|

|

$68.53

|

80.00%

|

25.000%

|

|

$64.72

|

70.00%

|

25.000%

|

|

$60.91

|

60.00%

|

25.000%

|

|

$57.11

|

50.00%

|

25.000%

|

|

$53.30

|

40.00%

|

25.000%

|

|

$49.49

|

30.00%

|

25.000%

|

|

$45.68

|

20.00%

|

25.000%

|

|

$42.83

|

12.50%

|

25.000%

|

|

$41.88

|

10.00%

|

20.000%

|

|

$39.97

|

5.00%

|

10.000%

|

|

$39.02

|

2.50%

|

5.000%

|

|

$38.45

|

1.00%

|

2.000%

|

|

$38.07

|

0.00%

|

0.000%

|

|

$37.69

|

-1.00%

|

0.000%

|

|

$36.17

|

-5.00%

|

0.000%

|

|

$34.26

|

-10.00%

|

0.000%

|

|

$30.46

|

-20.00%

|

-11.111%

|

|

$26.65

|

-30.00%

|

-22.222%

|

|

$22.84

|

-40.00%

|

-33.333%

|

|

$19.04

|

-50.00%

|

-44.444%

|

|

$15.23

|

-60.00%

|

-55.555%

|

|

$11.42

|

-70.00%

|

-66.666%

|

|

$7.61

|

-80.00%

|

-77.777%

|

|

$3.81

|

-90.00%

|

-88.888%

|

|

$0.00

|

-100.00%

|

-100.000%

|

Hypothetical Examples of Amounts Payable at Maturity

The following examples illustrate how the total returns set forth in the table above are calculated.

Example 1: The price of the Reference Asset increases from the Initial Price of $38.07 to a Final Price of $39.97. Because the Final Price of $39.97 is greater than the Initial Price of $38.07 and the Reference Return of 5.00% multiplied by the Upside Participation Rate of 200.00% does not exceed the Maximum Return of 25.00%, the investor receives a Payment at Maturity of $1,100.00 per $1,000 Principal Amount of Notes, calculated as follows:

$1,000 + [$1,000 × (5.00% × 200.00%)] = $1,100.00

Example 2: The price of the Reference Asset increases from the Initial Price of $38.07 to a Final Price of $45.68. Because the Final Price of $45.68 is greater than the Initial Price of $38.07 and the Reference Return of 20.00% multiplied by the Upside Participation Rate of 200.00% exceeds the Maximum Return of 25.00%, the investor receives a Payment at Maturity of $1,250.00 per $1,000 Principal Amount of Notes, the maximum payment on the Notes, calculated as follows:

$1,000 + ($1,000 × 25.00%) = $1,250.00

-3-

Example 3: The price of the Reference Asset decreases from the Initial Price of $38.07 to a Final Price of $36.17. Because the Reference Return is -5.00% and the Final Price of $36.17 is less than the Initial Price of $38.07 but not by more than the Buffer Amount of 10.00%, the investor receives a Payment at Maturity of 100.00% of the principal amount, which equals $1,000.00 per $1,000 Principal Amount of Notes.

Example 4: The price of the Reference Asset decreases from the Initial Price of $38.07 to a Final Price of $26.65. Because the Reference Return is -30.00% and the Final Price of $26.65 is less than the Initial Price of $38.07 by more than the Buffer Amount of 10.00%, the investor receives a Payment at Maturity of $777.78 per $1,000 Principal Amount of Notes, calculated as follows:

$1,000 + [$1,000 × (-30.00% + 10.00%) × 1.11111] = $777.78

Selected Purchase Considerations

|

|

·

|

APPRECIATION POTENTIAL — The Notes provide the opportunity for enhanced returns at maturity by multiplying a positive Reference Return by 200.00%, up to the Maximum Return on the Notes of 25.00%, or a maximum Payment at Maturity of $1,250.00 for every $1,000 Principal Amount of Notes. Because the Notes are our senior unsecured obligations, payment of any amount at maturity is subject to our ability to pay our obligations as they become due.

|

|

|

·

|

LIMITED BUFFER AGAINST LOSS — We will pay you your principal back at maturity if the Final Price is not less than the Initial Price by more than the Buffer Amount of 10.00%. If the price of the Reference Asset declines by more than 10.00%, you will lose 1.11111% of the Principal Amount for every 1.00% decline of the price of the Reference Asset over the term of the Notes beyond 10.00%. If the Reference Return is -100.00%, you will lose your entire investment.

|

|

|

·

|

EXPOSURE TO PERFORMANCE OF THE iSHARES® MSCI EMERGING MARKET INDEX FUND — The Reference Asset is an exchange-traded fund of iShares, Inc., which is a registered investment company that consists of numerous separate investment portfolios. The Reference Asset seeks to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of the MSCI Emerging Markets Index (the “underlying index”). The underlying index is a free-float adjusted average of the U.S. dollar values of all of the equity securities constituting the underlying index. For additional information about the Reference Asset, see the information set forth under “Description of the Reference Asset” herein.

|

|

|

·

|

TAX TREATMENT — There is no direct legal authority as to the proper tax treatment of the Notes, and therefore significant aspects of the tax treatment of the Notes are uncertain as to both the timing and character of any inclusion in income in respect of the Notes. Under one approach, a Note should be treated as a pre-paid forward or other executory contract with respect to the Reference Asset. We intend to treat the Notes consistent with this approach. Pursuant to the terms of the Notes, you agree to treat the Notes under this approach for all U.S. federal income tax purposes. Notwithstanding any disclosure in the accompanying product supplement to the contrary, our special U.S. tax counsel in this transaction is Sidley Austin llp. Subject to the limitations described therein, and based on certain factual representations received from us, in the opinion of our special U.S. tax counsel, Sidley Austin llp, it is reasonable to treat a Note as a pre-paid forward or other executory contract with respect to the Reference Asset. Pursuant to this approach, and subject to the discussion below regarding “constructive ownership transactions”, we do not intend to report any income or gain with respect to the Notes prior to their maturity or an earlier sale or exchange and we intend to treat any gain or loss upon maturity or an earlier sale or exchange as long-term capital gain or loss, provided that you have held the Note for more than one year at such time for U.S. federal income tax purposes.

|

Despite the foregoing, U.S. holders (as defined under “Certain U.S. Federal Income Tax Considerations” in the accompanying prospectus supplement) should be aware that the Internal Revenue Code of 1986, as amended (the “Code”) contains a provision, Section 1260 of the Code, which sets forth rules which are applicable to what it refers to as “constructive ownership transactions.” Due to the manner in which it is drafted, the precise applicability of Section 1260 of the Code to any particular transaction is often uncertain. In general, a “constructive ownership transaction” includes a contract under which an investor will receive payment equal to or credit for the future value of any equity interest in a regulated investment company (such as shares of the Reference Asset (the “Underlying Shares”)). Under the “constructive ownership” rules, if an investment in the Notes is treated as a “constructive ownership transaction,” any long-term capital gain recognized by a U.S. holder in respect of a Note will be recharacterized as ordinary income to the extent such gain exceeds the amount of “net underlying long-term capital gain” (as defined in Section 1260 of the Code) of the U.S. holder determined as if the U.S. holder had acquired the Underlying Shares on the Original Issue Date of the Note at fair market value and sold them at fair market value on the Maturity Date (if the Note was held until the Maturity Date) or on the date of sale or exchange of the Note (if the Note was sold or exchanged prior to the Maturity Date) (the “Excess Gain”). In addition, an interest charge will also apply to any deemed underpayment of tax in respect of any Excess Gain to the extent such gain would have resulted in gross income inclusion for the U.S. holder in taxable years prior to the taxable year of the sale, exchange or maturity of the Note (assuming such income accrued at a constant rate equal to the applicable federal rate as of the date of sale, exchange or maturity of the Note).

Although the matter is not clear, there exists a substantial risk that an investment in the Notes will be treated as a “constructive ownership transaction.” If such treatment applies, it is not entirely clear to what extent any long-term capital gain recognized by a U.S. holder in respect of a Note will be recharacterized as ordinary income. It is possible, for example, that the amount of the Excess Gain (if any) that would be recharacterized as ordinary income in respect of each Note will equal the excess of (i) any long-term capital gain recognized by the U.S. holder in respect of such a

-4-

Note over (ii) the “net underlying long-term capital gain” such U.S. holder would have had if such U.S. holder had acquired a number of the Underlying Shares at fair market value on the Original Issue Date of such Note for an amount equal to the “issue price” of the Note and, upon the date of sale, exchange or maturity of the Note, sold such Underlying Shares at fair market value (which would reflect the percentage increase in the value of the Underlying Shares over the term of the Note). Accordingly, U.S. holders should consult their tax advisors regarding the potential application of the “constructive ownership” rules.

We will not attempt to ascertain whether the issuer of any stock owned by the Reference Asset would be treated as a “passive foreign investment company,” within the meaning of Section 1297 of the Code. In the event that the issuer of any stock owned by the Reference Asset were treated as a passive foreign investment company, certain adverse U.S. federal income tax consequences might apply. You should refer to information filed with the SEC or other authorities by the issuers of stock owned by the Reference Asset and consult your tax advisor regarding the possible consequences to you, if any, in the event that one or more issuers of stock owned by the Reference Asset is or becomes a passive foreign investment company.

For a discussion of certain of the U.S. federal income tax consequences of your investment in a Note, please see the discussion under “Certain U.S. Federal Income Tax Considerations” in the accompanying product supplement and the discussion under “Certain U.S. Federal Income Tax Considerations” in the accompanying prospectus supplement.

Selected Risk Considerations

An investment in the Notes involves significant risks. Investing in the Notes is not equivalent to investing directly in any of the component securities of the Reference Asset. These risks are explained in more detail in the “Risk Factors” sections of the accompanying product supplement and prospectus supplement.

|

|

·

|

YOUR INVESTMENT IN THE NOTES MAY RESULT IN A LOSS — The Notes do not guarantee any return of principal if the Reference Return is less than -10.00%. The return on the Notes at maturity is linked to the performance of the Reference Asset and will depend on whether, and the extent to which, the Reference Return is positive or negative. Your investment will be exposed on a leveraged basis to any decline in the Final Price of the Reference Asset beyond the Buffer Amount as compared to the Initial Price. You may lose up to 100.00% of your investment.

|

|

|

·

|

CREDIT RISK OF HSBC USA INC. — The Notes are senior unsecured debt obligations of the issuer, HSBC, and are not, either directly or indirectly, an obligation of any third party. As further described in the accompanying prospectus supplement and prospectus, the Notes will rank on par with all of the other unsecured and unsubordinated debt obligations of HSBC, except such obligations as may be preferred by operation of law. Any payment to be made on the Notes, including any return of principal at maturity, depends on the ability of HSBC to satisfy its obligations as they come due. As a result, the actual and perceived creditworthiness of HSBC may affect the market value of the Notes and, in the event HSBC were to default on its obligations, you may not receive the amounts owed to you under the terms of the Notes.

|

|

|

·

|

YOUR MAXIMUM GAIN ON THE NOTES IS LIMITED TO THE MAXIMUM RETURN — If the Final Price is greater than the Initial Price, for each $1,000 Principal Amount of Notes you hold, you will receive at maturity $1,000 plus an additional amount that will not exceed the Maximum Return of 25.00% of the Principal Amount, regardless of the appreciation in the Reference Asset, which may be significantly greater than the Maximum Return. You will not receive a return on the Notes greater than the Maximum Return.

|

|

|

·

|

SUITABILITY OF NOTES FOR INVESTMENT – A person should reach a decision to invest in the Notes after carefully considering, with his or her advisors, the suitability of the Notes in light of his or her investment objectives and the information set out in this free writing prospectus. Neither the Issuer nor any dealer participating in the offering makes any recommendation as to the suitability of the Notes for investment.

|

|

|

·

|

AN INVESTMENT IN THE NOTES IS SUBJECT TO RISKS ASSOCIATED WITH FOREIGN SECURITIES MARKETS — The stocks held by the underlying index, which is the underlying index for the Reference Asset, and that are generally tracked by the Reference Asset have been issued by companies in various foreign markets which MSCI, Inc. classifies as “emerging markets”. Although the trading prices of shares of the Reference Asset are not directly tied to the value of the underlying index or the trading prices of the stocks comprising the underlying index, the trading prices of shares of the Reference Asset are expected to correspond generally to the value of publicly traded equity securities in the aggregate in the emerging markets, as measured by the underlying index. This means that the trading prices of shares of the Reference Asset are expected to be affected by factors affecting such foreign securities markets.

|

Investments in securities linked to the value of foreign securities markets involve certain risk. Foreign securities markets may be more volatile than U.S. or other securities markets and may be affected by market developments in different ways than U.S. or other securities markets. Also, there generally may be less publicly available information about companies in foreign securities markets than about U.S. companies, and companies in foreign securities markets are subject to accounting, auditing and financial reporting standards and requirements that differ from those applicable to U.S. companies. Although many of the component stocks in the underlying index are listed or traded on foreign securities markets which constitute “designated offshore securities markets” under Regulation S, certain of the component stocks in the underlying index are primarily traded on foreign securities markets which have not been approved by U.S. securities regulatory agencies or U.S. exchanges. In addition, regardless of their status as designated offshore securities markets, certain component stocks in the underlying index may be subject to accounting, auditing and financial reporting standards and requirements that differ from those applicable to United States reporting companies. In addition, foreign securities issuers may be subject to accounting, auditing and financial reporting standards and requirements that differ from those applicable to United States reporting companies. Securities prices generally are subject to political, economic, financial and social factors that apply to the markets in

-5-

which they trade and, to a lesser extent, foreign markets.

Securities prices outside the United States are subject to political, economic, financial and social factors that apply in foreign countries. These factors, which could negatively affect foreign securities markets, include the possibility of changes in a foreign government’s economic and fiscal policies, the possible imposition of, or changes in, currency exchange laws or other laws or restrictions applicable to foreign companies or investments in foreign equity securities and the possibility of fluctuations in the rate of exchange between currencies. Moreover, foreign economies may differ favorably or unfavorably from the United States economy in important respects such as growth of gross national product, rate of inflation, capital reinvestment, resources and self-sufficiency.

|

|

·

|

THE NOTES ARE SUBJECT TO EMERGING MARKETS RISK — Investments in notes linked directly or indirectly to emerging market equity securities involve many risks, including, but not limited to: economic, social, political, financial and military conditions in the emerging market; regulation by national, provincial, and local governments; less liquidity and smaller market capitalizations than exist in the case of many large U.S. companies; different accounting and disclosure standards; and political uncertainties. Stock prices of emerging market companies may be more volatile and may be affected by market developments differently than U.S. companies. Government interventions to stabilize securities markets and cross-shareholdings may affect prices and volume of trading of the securities of emerging market companies. Economic, social, political, financial and military factors could, in turn, negatively affect such companies’ value. These factors could include changes in the emerging market government’s economic and fiscal policies, possible imposition of, or changes in, currency exchange laws or other laws or restrictions applicable to the emerging market companies or investments in their securities, and the possibility of fluctuations in the rate of exchange between currencies. Moreover, emerging market economies may differ favorably or unfavorably from the U.S. economy in a variety of ways, including growth of gross national product, rate of inflation, capital reinvestment, resources and self-sufficiency. You should carefully consider the risks related to emerging markets, to which the notes are highly susceptible, before making a decision to invest in the notes.

|

|

|

·

|

AN INVESTMENT IN THE NOTES IS SUBJECT TO CURRENCY EXCHANGE RISK — Because the underlying index is denominated in U.S. Dollars, the prices of the component stocks comprising the underlying index will be converted into U.S. Dollars for the purposes of calculating the value of the underlying index and, thus, noteholders will be exposed to currency exchange rate risk with respect to each of the currencies in which the equity securities held by the underlying index trade. A noteholder’s net exposure will depend on the extent to which the currencies in which the equity securities held by the underlying index trade strengthens or weakens against the U.S. Dollar. If the U.S. Dollar strengthens against the currencies in which the equity securities held by the underlying index trade, the value of the Reference Asset may be adversely affected, and the principal payment at maturity of the notes may be reduced.

|

|

|

·

|

THE VALUE OF SHARES OF THE REFERENCE ASSET MAY NOT COMPLETELY TRACK THE VALUE OF THE UNDERLYING INDEX — Although the trading characteristics and valuations of shares of the Reference Asset will usually mirror the characteristics and valuations of the underlying index, the value of the shares of the Reference Asset may not completely track the value of the underlying index. The Reference Asset may reflect transaction costs and fees that are not included in the calculation of the underlying index. Additionally, because the Reference Asset may not actually hold all of the stocks comprising the underlying index but invests in a representative sample of securities which have a similar investment profile as the stocks comprising the underlying index, the Reference Asset may not fully replicate the performance of the underlying index.

|

|

|

·

|

MANAGEMENT RISK — The Reference Asset is not managed according to traditional methods of ‘‘active’’ investment management, which involve the buying and selling of securities based on economic, financial and market analysis and investment judgment. Instead, the Reference Asset, utilizing a ‘‘passive’’ or indexing investment approach, attempts to approximate the investment performance of the underlying index by investing in a portfolio of securities that generally replicate the underlying index. Therefore, unless a specific security is removed from the underlying index, the Reference Asset generally would not sell a security because the security’s issuer was in financial trouble. In addition, the Reference Asset is subject to the risk that the investment strategy of the investment adviser may not produce the intended results. Your investment is linked to the Reference Asset, which is an index fund. Any information relating to the underlying index is only relevant to understanding the index that the Reference Asset seeks to replicate.

|

|

|

·

|

POTENTIALLY INCONSISTENT RESEARCH, OPINIONS OR RECOMMENDATIONS BY HSBC AND JPMORGAN — HSBC, JPMorgan, or their affiliates may publish research, express opinions or provide recommendations that are inconsistent with investing in or holding the Notes and which may be revised at any time. Any such research, opinions or recommendations could affect the price of the Reference Asset, the level of the underlying index or the price of the stocks included in the underlying index, and therefore, the market value of the Notes.

|

|

|

·

|

CERTAIN BUILT-IN COSTS ARE LIKELY TO ADVERSELY AFFECT THE VALUE OF THE NOTES PRIOR TO MATURITY — While the Payment at Maturity described in this free writing prospectus is based on the full Principal Amount of your Notes, the original issue price of the Notes includes the placement agent’s commission and the estimated cost of hedging our obligations under the Notes through one or more of our affiliates. As a result, the price, if any, at which HSBC Securities (USA) Inc. will be willing to purchase Notes from you in secondary market transactions, if at all, will likely be lower than the original issue price, and any sale of Notes by you prior to the Maturity Date could result in a substantial loss to you. The Notes are not designed to be short-term trading instruments. Accordingly, you should be able and willing to hold your Notes to maturity.

|

|

|

·

|

THERE IS LIMITED ANTI-DILUTION PROTECTION — The calculation agent will adjust the Final Price, for certain events affecting the shares of the Reference Asset, such as stock splits and corporate actions which may affect the Payment at Maturity. The calculation agent is not required to make an adjustment for every corporate action which affects the shares of the Reference Asset. If an event occurs that does not require the calculation agent to adjust the amount of the shares of the Reference Asset, the market price of the relevant Notes and the Payment at Maturity may be materially and adversely affected. See the “Adjustments” section on page PS-23 of the accompanying product supplement.

|

-6-

|

|

·

|

NO INTEREST OR DIVIDEND PAYMENTS OR VOTING RIGHTS — As a holder of the Notes, you will not receive interest payments, and you will not have voting rights or rights to receive cash dividends or other distributions or other rights that holders of shares of the Reference Asset or shares of the securities held by the Reference Asset or included in the underlying index would have.

|

|

|

·

|

LACK OF LIQUIDITY — The Notes will not be listed on any securities exchange. HSBC Securities (USA) Inc. may offer to purchase the Notes in the secondary market but is not required to do so and may cease making such offers at any time. Because other dealers are not likely to make a secondary market for the Notes, the price at which you may be able to trade your Notes is likely to depend on the price, if any, at which HSBC Securities (USA) Inc. is willing to buy the Notes. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell the Notes easily.

|

|

|

·

|

POTENTIAL CONFLICTS — We and our affiliates play a variety of roles in connection with the issuance of the Notes, including acting as calculation agent and hedging our obligations under the Notes. In performing these duties, the economic interests of the calculation agent and other affiliates of ours are potentially adverse to your interests as an investor in the Notes. We will not have any obligation to consider your interests as a holder of the Notes in taking any corporate action that might affect the price of the Reference Asset and the value of the Notes. The calculation agent is under no obligation to consider your interests as a holder of the Notes in taking any actions that might affect the value of your Notes.

|

|

|

·

|

THE NOTES ARE NOT INSURED BY ANY GOVERNMENTAL AGENCY OF THE UNITED STATES OR ANY OTHER JURISDICTION — The Notes are not deposit liabilities or other obligations of a bank and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency or program of the United States or any other jurisdiction. An investment in the Notes is subject to the credit risk of the Issuer, and in the event that we are unable to pay our obligations as they become due, you may not receive the full Payment at Maturity of the Notes.

|

|

|

·

|

MANY ECONOMIC AND MARKET FACTORS WILL IMPACT THE VALUE OF THE NOTES — In addition to the Official Closing Price of the Reference Asset on any day, the value of the Notes will be affected by a number of economic and market factors that may either offset or magnify each other, including:

|

|

|

·

|

the expected volatility of the Reference Asset;

|

|

|

·

|

the time to maturity of the Notes;

|

|

|

·

|

the dividend rate on the equity securities held by the Reference Asset or comprising the underlying index;

|

|

|

·

|

interest and yield rates in the market generally;

|

|

|

·

|

the exchange rate and the volatility of the exchange rate between the U.S. dollar and each of the currencies in which the equity securities held by the Reference Asset trade and the correlation between those rates and the prices of shares of the Reference Asset;

|

|

|

·

|

a variety of economic, financial, political, regulatory or judicial events that affect the equity securities held by the Reference Asset or the stock markets generally; and

|

|

|

·

|

our creditworthiness, including actual or anticipated downgrades in our credit ratings.

|

-7-

Description of the Reference Asset

General

This free writing prospectus is not an offer to sell and it is not an offer to buy interests in the Reference Asset or any of the securities comprising the Reference Asset. All disclosures contained in this free writing prospectus regarding the Reference Asset, including its make-up, performance, method of calculation and changes in its components, where applicable, are derived from publicly available information. Neither HSBC nor any of its affiliates assumes any responsibilities for the adequacy or accuracy of information about the Reference Asset or any constituent included in the Reference Asset contained in this free writing prospectus. You should make your own investigation into each Reference Asset.

We urge you to read the section “Sponsors or Issuers and Reference Asset” on page S-37 in the accompanying prospectus supplement.

The iShares® MSCI Emerging Markets Index Fund

We have derived all information relating to the EEM, including, without limitation, its make-up, method of calculation and changes in its components, from publicly available information. The information reflects the policies of and is subject to change by iShares®, Inc. (“iShares”) and BlackRock Fund Advisors (“BFA”). The iShares® MSCI Emerging Markets Index Fund is an investment portfolio maintained and managed by iShares®. BFA is the investment adviser to the iShares® MSCI Emerging Markets Index Fund. The iShares® MSCI Emerging Markets Index Fund is an exchange traded fund (“ETF”) that trades on the New York Stock Exchange (the “NYSE”) under the ticker symbol “EEM”.

The EEM seeks investment results that correspond generally to the price and yield performance, before fees and expenses, of the MSCI Emerging Markets Index. The EEM uses a representative sampling strategy to try to track the MSCI Emerging Markets Index. In order to improve its portfolio liquidity and its ability to track the MSCI Emerging Markets Index, the EEM may invest up to 10% of its assets in shares of other iShares funds that seek to track the performance of equity securities of constituent countries of the MSCI Emerging Markets Index. BFA will not charge portfolio management fees on that portion of the EEM’s assets invested in shares of other iShares funds.

For additional information regarding iShares, BFA, the EEM and the risk factors attributable to the EEM, please see the relevant portion of the Prospectus, dated January 1, 2010, filed on Form 497 with the SEC on January 20, 2010 under the Securities Act of 1933, as amended, and under the Investment Company Act of 1940, as amended (File Nos. 033-97598 and 811-09102, respectively). Information provided to or filed with the SEC can be inspected and copied at the public reference facilities maintained by the SEC or through the SEC’s website at www.sec.gov.

Representative Sampling

BFA, as the investment advisor to the EEM, employs a technique known as representative sampling to track the MSCI Emerging Markets Index. Representative sampling is a strategy in which a fund invests in a representative sample of stocks in its underlying index, which have a similar investment profile as the underlying index. Stocks selected have aggregate investment characteristics (based on market capitalization and industry weightings), fundamental characteristics, and liquidity measures similar to those of the relevant underlying index. Funds that use representative sampling generally do not hold all of the stocks that are included in the relevant underlying index.

Correlation

The underlying index is a theoretical financial calculation, while the EEM is an actual investment portfolio. The performance of the EEM and the MSCI Emerging Markets Index will vary somewhat due to transaction costs, market impact, corporate actions (such as mergers and spin-offs), and timing variances. A figure of 100% would indicate perfect correlation. Any correlation of less than 100% is called “tracking error.” The EEM, using a representative sampling strategy, can be expected to have a greater tracking error than a fund using replication strategy. Replication is a strategy in which a fund invests in substantially all of the securities in its underlying index in approximately the same proportions as in the underlying index.

Industry Concentration Policy

The EEM will concentrate its investments (i.e., hold 25% or more of its total assets) in a particular industry or group of industries to approximately the same extent that the underlying index is concentrated.

The Underlying Index

All information in this free writing prospectus regarding the underlying index, including, without limitation, its make-up, method of calculation and changes in its components, is derived from publicly available information. Such information reflects the policies of, and is subject to change by, MSCI or any of its affiliates (the “underlying index sponsor”). The underlying index sponsor owns the copyright and all other rights to the underlying index. The underlying index has no obligation to continue to publish, and may discontinue publication of, the underlying index. We do not assume any responsibility for the accuracy or completeness of such information. Historical performance of the underlying index is not an indication of future performance. Future performance of the underlying index may differ significantly from historical performance, either positively or negatively.

-8-

The underlying index is published by MSCI and is intended to measure the performance of equity markets in the global emerging markets. The underlying index is a free float-adjusted market capitalization index with a base date of December 31, 1987 and an initial price of 100. As of the date of this document, the underlying index holdings by country consisted of the following 22 countries: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Morocco, Peru, Philippines, Poland, Russia, South Korea, Taiwan, Thailand and Turkey.

The underlying index is part of the MSCI equity indices series. MSCI aims to include in its indices 85% of the free float-adjusted market capitalization in each industry sector, within each country included in an index.

Constructing the MSCI Global Investable Market Indices

MSCI undertakes an index construction process, which involves: (i) defining the Equity Universe; (ii) determining the Market Investable Equity Universe for each market; (iii) determining market capitalization size segments for each market; (iv) applying Index Continuity Rules for the MSCI Standard Index; (v) creating style segments within each size segment within each market; and (vi) classifying securities under the Global Industry Classification Standard (the “GICS”).

Maintenance

The MSCI Global Investable Market Indices are maintained with the objective of reflecting the evolution of the underlying equity markets and segments on a timely basis, while seeking to achieve index continuity, continuous investability of constituents and replicability of the indices, and index stability and low index turnover.

In particular, index maintenance involves:

(i) Semi-Annual Index Reviews (“SAIRs”) in May and November of the Size Segment and Global Value and Growth Indices which include:

|

•

|

Updating the indices on the basis of a fully refreshed Equity Universe.

|

||

|

|

•

|

Taking buffer rules into consideration for migration of securities across size and style segments.

|

|

|

|

•

|

Updating FIFs and Number of Shares (“NOS”).

|

(ii) Quarterly Index Reviews (“QIRs”) in February and August of the Size Segment Indices aimed at:

|

•

|

Including significant new eligible securities (such as IPOs that were not eligible for earlier inclusion) in the index.

|

||

|

|

•

|

Allowing for significant moves of companies within the Size Segment Indices, using wider buffers than in the SAIR.

|

|

|

|

•

|

Reflecting the impact of significant market events on FIFs and updating NOS.

|

(iii) Ongoing event-related changes. Changes of this type are generally implemented in the indices as they occur. Significantly large IPOs are included in the indices after the close of the company’s tenth day of trading.

-9-

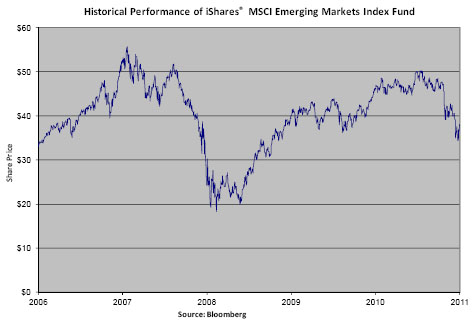

Historical Performance of Reference Asset

The following graph sets forth the historical performance of the Reference Asset based on the daily historical closing prices from October 10, 2006 through October 10, 2011. The closing price for the Reference Asset on October 10, 2011 was $38.07. We obtained the closing prices below from Bloomberg Professional® service. We make no representation or warranty as to the accuracy or completeness of the information obtained from Bloomberg Professional® service.

The historical prices of the Reference Asset should not be taken as an indication of future performance, and no assurance can be given as to the Official Closing Price on the Final Valuation Date or any of the Ending Averaging Dates. We cannot give you assurance that the performance of the Reference Asset will result in the return of any of your initial investment.

|

Quarter Begin

|

Quarter End

|

Quarterly High

|

Quarterly Low

|

Quarterly Close

|

|

1/3/2006

|

3/31/2006

|

$33.79

|

$30.00

|

$33.02

|

|

4/3/2006

|

6/30/2006

|

$37.08

|

$27.12

|

$31.23

|

|

7/3/2006

|

9/29/2006

|

$33.33

|

$29.03

|

$32.29

|

|

10/2/2006

|

12/29/2006

|

$38.26

|

$31.63

|

$38.10

|

|

1/3/2007

|

3/30/2007

|

$39.85

|

$34.52

|

$38.75

|

|

4/2/2007

|

6/29/2007

|

$44.62

|

$38.74

|

$43.82

|

|

7/2/2007

|

9/28/2007

|

$50.49

|

$37.15

|

$49.78

|

|

10/1/2007

|

12/31/2007

|

$55.83

|

$47.22

|

$50.10

|

|

1/2/2008

|

3/31/2008

|

$50.75

|

$40.68

|

$44.79

|

|

4/1/2008

|

6/30/2008

|

$52.48

|

$44.43

|

$45.19

|

|

7/1/2008

|

9/30/2008

|

$44.76

|

$30.88

|

$34.53

|

|

10/1/2008

|

12/31/2008

|

$34.29

|

$18.22

|

$24.97

|

|

1/2/2009

|

3/31/2009

|

$27.28

|

$19.87

|

$24.81

|

|

4/1/2009

|

6/30/2009

|

$34.88

|

$24.72

|

$32.23

|

|

7/1/2009

|

9/30/2009

|

$39.51

|

$30.25

|

$38.91

|

|

10/1/2009

|

12/31/2009

|

$42.52

|

$37.30

|

$41.50

|

|

1/4/2010

|

3/30/2010

|

$43.47

|

$35.01

|

$42.12

|

|

4/1/2010*

|

6/30/2010

|

$44.02

|

$35.21

|

$37.32

|

|

7/1/2010

|

9/30/2010

|

$44.99

|

$36.76

|

$44.77

|

|

10/1/2010

|

12/31/2010

|

$48.62

|

$44.51

|

$47.62

|

|

1/3/2011

|

3/31/2011

|

$48.75

|

$44.25

|

$48.69

|

|

4/1/2011

|

6/30/2011

|

$50.43

|

$44.77

|

$47.60

|

|

7/1/2011

|

9/30/2011

|

$48.63

|

$34.71

|

$35.07

|

|

10/3/2011

|

10/10/2011*

|

$38.12

|

$33.43

|

$38.07

|

* As of the date of this free writing prospectus available information for the fourth calendar quarter of 2011 includes data for the period from October 3, 2011 through October 10, 2011. Accordingly, the “Quarterly High,” “Quarterly Low” and “Quarterly Close” data indicated are for this shortened period only and do not reflect complete data for the fourth calendar quarter of 2011.

-10-

Supplemental Plan of Distribution (Conflicts of Interest)

Pursuant to the terms of a distribution agreement, HSBC Securities (USA) Inc., an affiliate of HSBC, will purchase the Notes from HSBC for distribution to J.P. Morgan Securities LLC and certain of its registered broker dealer affiliates, at the price indicated on the cover of the pricing supplement, the document that will be filed pursuant to Rule 424(b)(2) containing the final pricing terms of the Notes. J.P. Morgan Securities LLC and certain of its registered broker dealer affiliates will act as placement agent for the Notes and will receive a fee that will not exceed $10.00 per $1,000 Principal Amount of Notes.

In addition, HSBC Securities (USA) Inc. or another of its affiliates or agents may use the pricing supplement to which this free writing prospectus relates in market-making transactions after the initial sale of the securities, but is under no obligation to do so and may discontinue any market-making activities at any time without notice.

See “Supplemental Plan of Distribution” on page S-52 in the prospectus supplement. All references to NASD Rule 2720 in the prospectus supplement shall be to FINRA Rule 5121.

-11-