|

August 2011

Free Writing Prospectus

Registration Statement No. 333-158385

Dated August 25, 2011

Filed pursuant to Rule 433

|

STRUCTURED INVESTMENTS

Opportunities in U.S. and International Equities

PLUS Based on the Value of a Weighted Basket Composed of the S&P 500® Index, the Russell 2000® Index and the iShares® MSCI EAFE Index Fund due October 1, 2012

Performance Leveraged Upside SecuritiesSM

PLUS are senior unsecured debt securities of HSBC USA Inc. (“HSBC”), will pay no interest, do not guarantee any return of principal at maturity and have the terms described in the accompanying underlying supplement no. 3, underlying supplement no. 4, product supplement, prospectus supplement and prospectus, as supplemented or modified by this free writing prospectus. All references to “Enhanced Market Participation Notes” in the product supplement shall refer to these PLUS. All references to “Reference Asset” in the prospectus supplement, product supplement, underlying supplement no. 3 and underlying supplement no. 4 shall refer to the “basket” herein. At maturity, if the basket has appreciated, investors will receive the stated principal amount of their investment plus leveraged upside performance of the basket, subject to the maximum payment at maturity. At maturity, if the basket has depreciated, the investor will lose 1% for every 1% decline in the basket from the pricing date to the valuation date. Investors may lose up to 100% of the stated principal amount of the PLUS. All payments on the PLUS are subject to the credit risk of HSBC.

|

INDICATIVE TERMS

|

||||||

|

Issuer:

|

HSBC USA Inc.

|

|||||

|

Maturity date:

|

October 1, 2012, subject to adjustment as described below under the caption “Valuation Date and Maturity Date”

|

|||||

|

Basket:

|

The underlying basket is weighted and composed of two indices and one index fund (each, a “basket component”), as set forth in the table below.

|

|||||

|

Basket component

|

Bloomberg ticket symbol

|

Component weighting

|

Initial component value*

|

|||

|

S&P 500® Index (“SPX”)

|

SPX

|

60.00%

|

||||

|

Russell 2000® Index (“RTY”)

|

RTY

|

20.00%

|

||||

|

iShares® MSCI EAFE Index Fund (“EFA”)

|

EFA

|

20.00%

|

||||

|

*The initial component value for each basket component will be determined on the pricing date.

|

||||||

|

Aggregate principal amount:

|

||||||

|

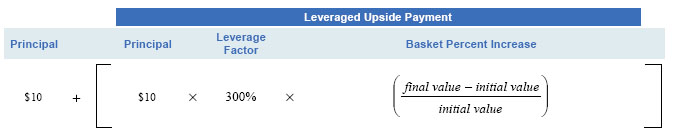

Payment at maturity:

|

· If the final value is greater than the initial value:

$10 + the leveraged upside payment

In no event will the payment at maturity exceed the maximum payment at maturity.

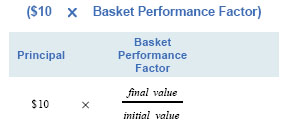

· If the final value is less than or equal to the initial value:

$10 x the basket performance factor

This amount will be less than or equal to the stated principal amount of $10.

|

|||||

|

Leveraged upside payment:

|

$10 x leverage factor x basket percent increase

|

|||||

|

Leverage factor:

|

300%

|

|||||

|

Basket percent increase:

|

(final value – initial value) / initial value

|

|||||

|

Initial value:

|

Set equal to 100 on the pricing date

|

|||||

|

Final value:

|

The closing value on the valuation date

|

|||||

|

Closing value:

|

On any scheduled trading day, the closing value of the basket will be calculated as follows:

100 × [1 + (sum of the basket component return multiplied by the respective component weighting for each basket component)]

Each of the basket component returns set forth in the formula above refers to the return for the basket component, which reflects the performance of the basket component, expressed as the percentage change from the initial component value of that basket component to the final component value of that basket component.

|

|||||

|

Initial component value:

|

With respect to each basket component, the value of such basket component as set forth under “Initial component value” above, and as determined by the calculation agent on the pricing date. The initial component value for each basket component will not necessarily be the component closing value on the pricing date.

|

|||||

|

Final component value:

|

With respect to each basket component, the component closing value of the respective basket component on the valuation date.

|

|||||

|

Component closing value:

|

With respect to each basket component, the component closing value on any scheduled trading day will be determined by the calculation agent based upon the closing level of such index or closing price of such index fund, as applicable, displayed on the relevant Bloomberg Professional® service page (with respect to the SPX, “SPX <INDEX>”, with respect to the RTY, “RTY <INDEX>” and with respect to the EFA, “EFA UP <EQUITY>”) and with respect to the EFA, adjusted by the calculation agent as described under “Additional Terms of the Notes—Antidilution and Reorganization Adjustments” in the accompanying underlying supplement no. 4 or, for each basket component, any successor page on Bloomberg Professional® service or any successor service, as applicable.

|

|||||

|

Valuation date:

|

September 26, 2012, subject to adjustment as described below under the caption “Valuation Date and Maturity Date”

|

|||||

|

Basket performance factor:

|

final value / initial value

|

|||||

|

Maximum payment at maturity:

|

$11.90 to $12.00 per PLUS (119.00% to 120.00% of the stated principal amount). The actual maximum payment at maturity will be determined on the pricing date.

|

|||||

|

Stated principal amount:

|

$10 per PLUS

|

|||||

|

Issue price:

|

$10 per PLUS

|

|||||

|

Pricing date:

|

On or about August 26, 2011

|

|||||

|

Original issue date:

|

On or about August 31, 2011 (3 business days after the pricing date)

|

|||||

|

CUSIP:

|

40433C510

|

|||||

|

ISIN:

|

US40433C5105

|

|||||

|

Listing:

|

The PLUS will not be listed on any securities exchange.

|

|||||

|

Agent:

|

HSBC Securities (USA) Inc., an affiliate of HSBC. See “Supplemental plan of distribution (conflicts of interest)”.

|

|||||

|

Commissions and Issue Price:

|

Price to Public

|

Fees and Commissions(1)

|

Proceeds to Issuer

|

|||

|

Per PLUS

|

$10

|

$0.1875

|

$9.8125

|

|||

|

Total

|

$

|

$

|

$

|

|||

PLUS Based on the Value of a Weighted Basket Composed of the S&P 500® Index, the Russell 2000® Index and the iShares® MSCI EAFE Index Fund due October 1, 2012

Performance Leveraged Upside SecuritiesSM

|

(1)

|

HSBC Securities (USA) Inc., acting as agent for HSBC, will receive a fee of $0.1875 per $10 stated principal amount and will pay the entire fee to Morgan Stanley Smith Barney LLC as a fixed sales commission of $0.1875 for each PLUS they sell. See “Supplemental plan of distribution (conflicts of interest).”

|

Investment in the PLUS involves certain risks. See “Risk Factors” beginning on page 13 of this free writing prospectus, page US3-1 of the underlying supplement no. 3, US4-2 of the underlying supplement no. 4, page PS-4 of the product supplement and page S-3 of the prospectus supplement.

Neither the U.S. Securities and Exchange Commission, or SEC, nor any state securities commission has approved or disapproved the PLUS, or determined that this free writing prospectus or the accompanying underlying supplement no. 3, underlying supplement no. 4, product supplement, prospectus supplement or prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

HSBC has filed a registration statement (including a prospectus, a prospectus supplement, a product supplement, underlying supplement no. 3 and underlying supplement no. 4) with the SEC for the offering to which this free writing prospectus relates. Before you invest, you should read the prospectus, prospectus supplement, product supplement, underlying supplement no. 3 and underlying supplement no. 4 in that registration statement and other documents HSBC has filed with the SEC for more complete information about HSBC and this offering. You may get these documents for free by visiting EDGAR on the SEC’s web site at www.sec.gov. Alternatively, HSBC Securities (USA) Inc. or any dealer participating in this offering will arrange to send you the prospectus, prospectus supplement, product supplement, underlying supplement no. 3 and underlying supplement no. 4 if you request them by calling toll-free 1-866-811-8049.

You should read this document together with the related underlying supplement no. 3, underlying supplement no. 4, product supplement, prospectus supplement and prospectus, each of which can be accessed via the hyperlinks below.

|

|

The underlying supplement no. 3 at: http://www.sec.gov/Archives/edgar/data/83246/000114420410055205/v198039_424b2.htm

|

|

|

The underlying supplement no. 4 at: http://www.sec.gov/Archives/edgar/data/83246/000114420410055207/v199610_424b2.htm

|

|

|

The product supplement at: http://www.sec.gov/Archives/edgar/data/83246/000114420409019791/v145840_424b2.htm

|

|

|

The prospectus supplement at: http://www.sec.gov/Archives/edgar/data/83246/000114420409019785/v145824_424b2.htm

|

|

|

The PLUS are not deposit liabilities or other obligations of a bank and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency of the United States or any other jurisdiction, and involve investment risks including possible loss of the stated principal amount invested due to the credit risk of HSBC.

|

August 2011

|

Page 2

|

PLUS Based on the Value of a Weighted Basket Composed of the S&P 500® Index, the Russell 2000® Index and the iShares® MSCI EAFE Index Fund due October 1, 2012

Performance Leveraged Upside SecuritiesSM

Investment Overview

Performance Leveraged Upside Securities

The PLUS Based on the Value of a Weighted Basket Composed of the S&P 500® Index, the Russell 2000® Index and the iShares® MSCI EAFE Index Fund due October 1, 2012 (the “PLUS”) can be used:

|

|

§

|

As an alternative to direct exposure to the basket components that enhances returns for a certain range of positive performance of the basket

|

|

|

§

|

To enhance positive returns and potentially outperform the basket in a moderately bullish scenario

|

|

|

§

|

To achieve similar levels of exposure to the basket components as a direct investment, subject to the maximum payment at maturity, while using fewer dollars by taking advantage of the leverage factor

|

|

Maturity:

|

Approximately 13 Months

|

|

Leverage factor:

|

300%

|

|

Maximum payment at maturity:

|

$11.90 to $12.00 per PLUS (119.00% to 120.00% of the stated principal amount) (to be determined on the pricing date)

|

|

Minimum payment at maturity:

|

None

|

|

Coupon:

|

None

|

Information About the Basket

|

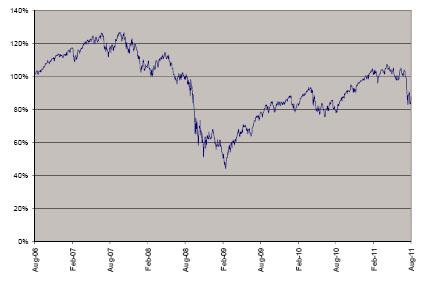

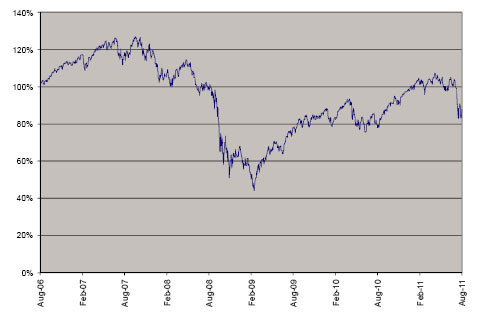

The following graph illustrates the hypothetical daily historical performance of the basket from August 24, 2006 through August 24, 2011 based on information from Bloomberg Professional® service, if the value of the basket were set to equal 100 on August 24, 2006. The hypothetical historical performance reflects the performance the basket would have exhibited based on the actual historical performance of the basket components. Neither the hypothetical historical performance of the basket nor the actual historical performance of the basket components should be taken as indications of future performance.

We cannot give you assurance that the performance of the basket will result in the return of your initial investment. All payments on the PLUS are subject to the credit risk of HSBC.

|

|

August 2011

|

Page 3

|

PLUS Based on the Value of a Weighted Basket Composed of the S&P 500® Index, the Russell 2000® Index and the iShares® MSCI EAFE Index Fund due October 1, 2012

Performance Leveraged Upside SecuritiesSM

Key Investment Rationale

The PLUS offer 300% leveraged upside on the positive performance of the basket, subject to a maximum payment at maturity of $11.90 to $12.00 per PLUS (119.00% to 120.00% of the stated principal amount). The actual maximum payment at maturity will be determined on the pricing date.

|

Leveraged Performance

|

The PLUS offer investors an opportunity to capture enhanced returns for a certain range of positive performance relative to a direct investment in the basket.

|

|

Payment Scenario 1

|

The underlying shares increase in price and, at maturity, the PLUS redeem for the stated principal amount of $10 plus 300% of the share percent increase, subject to a maximum payment at maturity of $11.90 to $12.00 per PLUS (119.00% to 120.00% of the stated principal amount).

|

|

Payment Scenario 2

|

The basket declines in price and, at maturity, the PLUS redeem for less than the stated principal amount by an amount that is proportionate to the decline.

|

Key Risks

Investment in the PLUS involve certain risks. See “Risk Factors” beginning on page 13 of this free writing prospectus, page US3-1 of the underlying supplement no. 3, page US4-2 of the underlying supplement no. 4, page PS-4 of the product supplement and page S-3 of the prospectus supplement.

In the prospectus supplement, please consider:

|

|

§

|

Risks Relating to All Note Issuances; and

|

|

|

§

|

Additional Risks Relating to Notes with an Equity Security or Equity Index as the Reference Asset; and

|

|

|

§

|

Additional Risks Relating to Certain Notes with More than One Instrument Comprising the Reference Asset.

|

In the product supplement, please consider:

|

|

§

|

Additional Risks Relating to Notes Linked to the Performance of Exchange-Traded Funds.

|

In the underlying supplement no. 3, please consider:

|

|

§

|

There are Risks Associated With Small-Capitalization Stocks.

|

In the underlying supplement no. 4, please consider:

|

|

§

|

Securities Prices Generally are Subject to Political, Economic, Financial and Social Factors that Apply to the Markets in Which They Trade and, to a Lesser Extent, Foreign Markets; and

|

|

|

§

|

The Notes are Subject to Currency Exchange Risk.

|

In this free writing prospectus, please consider:

|

|

§

|

PLUS do not pay interest and may result in a loss;

|

|

|

§

|

The appreciation potential of the PLUS is limited by the maximum payment at maturity;

|

|

|

§

|

Changes in the values of the basket components may offset each other;

|

|

|

§

|

Credit risk of HSBC USA Inc.;

|

|

|

§

|

The market price will be influenced by many unpredictable factors;

|

|

|

§

|

There is limited anti-dilution protection;

|

|

|

§

|

An index fund and its underlying index are different;

|

|

|

§

|

The EFA is subject to management risk;

|

|

August 2011

|

Page 4

|

PLUS Based on the Value of a Weighted Basket Composed of the S&P 500® Index, the Russell 2000® Index and the iShares® MSCI EAFE Index Fund due October 1, 2012

Performance Leveraged Upside SecuritiesSM

|

|

§

|

Investing in the PLUS is not equivalent to investing in the basket components;

|

|

|

§

|

Adjustments to any of the basket components could adversely affect the value of the PLUS;

|

|

|

§

|

Certain built-in costs are likely to adversely affect the value of the PLUS prior to maturity;

|

|

|

§

|

The PLUS will not be listed on any securities exchange and secondary trading may be limited;

|

|

|

§

|

The calculation agent, which is HSBC or one if its affiliates, will make determinations with respect to the PLUS;

|

|

|

§

|

Hedging and trading activity by our subsidiaries could potentially adversely affect the value of the PLUS;

|

|

|

§

|

The PLUS are not insured by any governmental agency of the United States or any other jurisdiction; and

|

|

|

§

|

The U.S. federal income tax consequences of an investment in the PLUS are uncertain.

|

|

August 2011

|

Page 5

|

PLUS Based on the Value of a Weighted Basket Composed of the S&P 500® Index, the Russell 2000® Index and the iShares® MSCI EAFE Index Fund due October 1, 2012

Performance Leveraged Upside SecuritiesSM

Fact Sheet

The PLUS are senior unsecured debt securities of HSBC, will pay no interest, do not guarantee any return of principal at maturity and have the terms described in the accompanying underlying supplement no. 3, underlying supplement no. 4, product supplement, prospectus supplement and prospectus, as supplemented or modified by this free writing prospectus. All references to “Enhanced Market Participation Notes” in the product supplement shall refer to these PLUS. All references to “Reference Asset” in the prospectus supplement, product supplement, underlying supplement no. 3 and underlying supplement no. 4 shall refer to the “basket” herein. At maturity, an investor will receive for each stated principal amount of PLUS that the investor holds an amount in cash that may be greater than, equal to or less than the stated principal amount based upon the value of the basket on the valuation date. All payments on the PLUS are subject to the credit risk of HSBC.

|

Expected Key Dates

|

|||||

|

Pricing date:

|

Original issue date (settlement date):

|

Maturity date:

|

|||

|

On or about August 26, 2011

|

On or about August 31, 2011 (3 business days after the pricing date)

|

October 1, 2012, subject to adjustment as described below under the caption “Valuation Date and Maturity Date”

|

|||

|

Key Terms

|

||||

|

Issuer:

|

HSBC USA Inc.

|

|||

|

Basket:

|

The underlying basket is weighted and composed of two indices and one index fund (each, a “basket component”), as set forth in the table below.

|

|||

|

Basket component

|

Bloomberg ticket symbol

|

Component weighting

|

Initial component value*

|

|

|

S&P 500® Index (“SPX”)

|

SPX

|

60.00%

|

||

|

Russell 2000® Index (“RTY”)

|

RTY

|

20.00%

|

||

|

iShares® MSCI EAFE Index Fund (“EFA”)

|

EFA

|

20.00%

|

||

|

*The initial component value for each basket component will be determined on the pricing date.

|

||||

|

Original issue price:

|

$10 per PLUS

|

|||

|

Stated principal amount:

|

$10 per PLUS

|

|||

|

Denominations:

|

$10 per PLUS and integral multiples thereof

|

|||

|

Interest:

|

None

|

|||

|

Aggregate principal amount:

|

||||

|

Payment at maturity:

|

· If the final value is greater than the initial value:

$10 + leveraged upside payment

In no event will the payment at maturity exceed the maximum payment at maturity.

|

|||

|

· If the final value is less than or equal to the initial value:

$10 x the basket performance factor

|

||||

|

This amount will be less than or equal to the stated principal amount of $10.

|

||||

|

Leveraged upside payment:

|

$10 x leverage factor x basket percent increase

|

|||

|

Leverage factor:

|

300%

|

|||

|

Basket percent increase:

|

(final value – initial value) / initial value

|

|||

|

Initial value:

|

Set equal to 100 on the pricing date

|

|||

|

Final value:

|

The closing value on the valuation date

|

|||

|

Closing value:

|

On any scheduled trading day, the closing value of the basket will be calculated as follows:

100 × [1 + (sum of the basket component return multiplied by the respective component weighting for each basket component)]

Each of the basket component returns set forth in the formula above refers to the return for the basket component, which reflects the performance of the basket component, expressed as the percentage change from the initial component value of that basket component to the final component value of that basket component.

|

|||

|

Initial component value:

|

With respect to each basket component, the value of such basket component as set forth under “Initial component value” above, and as determined by the calculation agent on the pricing date. The initial component value for each basket component will not necessarily be the component closing value on the pricing date.

|

|||

|

Final component value:

|

With respect to each basket component, the component closing value of the respective basket component on the valuation date.

|

|||

|

Component closing value:

|

With respect to each basket component, the component closing value on any scheduled trading day will be determined by the calculation agent based upon the closing level of such index or closing price of such index fund, as applicable, displayed on the relevant Bloomberg Professional® service page (with respect to the SPX, “SPX <INDEX>”, with respect to the RTY, “RTY <INDEX>” and with respect

|

|||

|

August 2011

|

Page 6

|

PLUS Based on the Value of a Weighted Basket Composed of the S&P 500® Index, the Russell 2000® Index and the iShares® MSCI EAFE Index Fund due October 1, 2012

Performance Leveraged Upside SecuritiesSM

|

to the EFA, “EFA UP <EQUITY>”) and with respect to the EFA, adjusted by the calculation agent as described under “Additional Terms of the Notes—Antidilution and Reorganization Adjustments” in the accompanying underlying supplement no. 4 or, for each basket component, any successor page on Bloomberg Professional® service or any successor service, as applicable.

|

|

|

Valuation date:

|

September 26, 2012, subject to adjustment as described below under the caption “Valuation Date and Maturity Date”

|

|

Basket performance factor:

|

final value / initial value

|

|

Maximum payment at maturity:

|

$11.90 to $12.00 per PLUS (119.00% to 120.00% of the stated principal amount). The actual maximum payment at maturity will be determined on the pricing date.

|

|

Risk factors:

|

Please see “Risk Factors” beginning on page 13 of this free writing prospectus, page US3-1 of the underlying supplement no. 3, page US4-2 of the underlying supplement no. 4, page PS-4 of the product supplement and page S-3 of the prospectus supplement.

|

|

August 2011

|

Page 7

|

PLUS Based on the Value of a Weighted Basket Composed of the S&P 500® Index, the Russell 2000® Index and the iShares® MSCI EAFE Index Fund due October 1, 2012

Performance Leveraged Upside SecuritiesSM

|

General Information

|

|

|

Listing:

|

The PLUS will not be listed on any securities exchange.

|

|

CUSIP:

|

40433C510

|

|

ISIN:

|

US40433C5105

|

|

Minimum ticketing size:

|

100 PLUS

|

|

Tax considerations:

|

There is no direct legal authority as to the proper tax treatment of each PLUS, and therefore significant aspects of the tax treatment of each PLUS is uncertain as to both the timing and character of any inclusion in income in respect of each PLUS. Under one approach, each PLUS could be treated as a pre-paid forward or other executory contract with respect to the basket. We intend to treat each PLUS consistent with this approach. Pursuant to the terms of each PLUS, you agree to treat each PLUS under this approach for all U.S. federal income tax purposes. Notwithstanding any disclosure in the accompanying product supplement to the contrary, our special U.S. tax counsel in this transaction is Sidley Austin llp. Subject to the limitations described therein, and based on certain factual representations received from us, in the opinion of our special U.S. tax counsel, Sidley Austin llp, it is reasonable to treat each PLUS as a pre-paid forward or other executory contract with respect to the basket. Pursuant to this approach and subject to the discussion below regarding “constructive ownership transactions,” we do not intend to report any income or gain with respect to each PLUS prior to maturity or an earlier sale or exchange and we intend to treat any gain or loss upon maturity or an earlier sale or exchange as long-term capital gain or loss, provided that you have held the PLUS for more than one year at such time for U.S. federal income tax purposes.

Despite the foregoing, U.S. holders (as defined under “Certain U.S. Federal Income Tax Considerations” in the accompanying prospectus supplement) should be aware that the Internal Revenue Code of 1986, as amended (the “Code”) contains a provision, Section 1260 of the Code, which sets forth rules which are applicable to what it refers to as “constructive ownership transactions.” Due to the manner in which it is drafted, the precise applicability of Section 1260 of the Code to any particular transaction is often uncertain. In general, a “constructive ownership transaction” includes a contract under which an investor will receive payment equal to or credit for the future value of any equity interest in a regulated investment company (such as shares of the EFA (the “Underlying Shares”)). Under the “constructive ownership” rules, if an investment in a PLUS is treated as a “constructive ownership transaction,” any long-term capital gain recognized by a U.S. holder in respect of the PLUS will be recharacterized as ordinary income to the extent such gain exceeds the amount of “net underlying long-term capital gain” (as defined in Section 1260 of the Code) of the U.S. holder (the “Excess Gain”). In addition, an interest charge will also apply to any deemed underpayment of tax in respect of any Excess Gain to the extent such gain would have resulted in gross income inclusion for the U.S. holder in taxable years prior to the taxable year of the sale, exchange or maturity of the PLUS (assuming such income accrued at a constant rate equal to the applicable federal rate as of the date of sale, exchange or maturity of the PLUS).

Although the matter is not clear, there exists a risk that an investment in a PLUS will be treated as a “constructive ownership transaction.” If such treatment applies, it is not entirely clear to what extent any long-term capital gain recognized by a U.S. holder in respect of a PLUS will be recharacterized as ordinary income. Accordingly, U.S. holders should consult their tax advisors regarding the potential application of the “constructive ownership” rules.

We will not attempt to ascertain whether any of the entities whose stock is included in, or owned by, one or more of the basket components, as the case may be, would be treated as a passive foreign investment company (a “PFIC”) or United States real property holding corporation (a “USRPHC”), both as defined for U.S. federal income tax purposes. If one or more of the entities whose stock is included in, or owned by, one or more of the basket components, as the case may be, were so treated, certain adverse U.S. federal income tax consequences might apply to a U.S. holder or non-U.S. holder, as the case may be. You should refer to information filed with the SEC and other authorities by the entities whose stock is included in, or owned by, one or more of the basket components, as the case may be, and consult your tax advisor regarding the possible consequences to you if one or more of the entities whose stock is included in, or owned by, one or more of the basket components, as the case may be, is or becomes a PFIC or a USRPHC.

In Notice 2008-2, the Internal Revenue Service and the Treasury Department requested comments as to whether the purchaser of certain securities (which may include the PLUS) should be required to accrue income during its term under a mark-to-market, accrual or other methodology, whether income and gain on such a security or contract should be ordinary or capital and whether foreign holders should be subject to withholding tax on any deemed income accrual. Accordingly, it is possible that regulations or other guidance could provide that a U.S. holder of a PLUS is required to accrue income in respect of the PLUS prior to the receipt of payments under the PLUS or its earlier sale or exchange. Moreover, it is possible that any such regulations or other guidance could treat all income and gain of a U.S. holder in respect of a PLUS as ordinary income (including gain on a sale or exchange). Finally, it is possible that a non-U.S. holder (as defined under “Certain U.S. Federal Income Tax Considerations” in the accompanying prospectus supplement) of the PLUS could be subject to U.S. withholding tax in respect of a PLUS. It is unclear whether any regulations or other guidance would apply to the PLUS (possibly on a retroactive basis). Prospective investors are urged to consult with their tax advisors

|

|

August 2011

|

Page 8

|

PLUS Based on the Value of a Weighted Basket Composed of the S&P 500® Index, the Russell 2000® Index and the iShares® MSCI EAFE Index Fund due October 1, 2012

Performance Leveraged Upside SecuritiesSM

|

regarding Notice 2008-2 and the possible effect to them of the issuance of regulations or other guidance that affects the U.S. federal income tax treatment of the PLUS.

For a further discussion of U.S. federal income tax consequences related to each PLUS, see the section “Certain U.S. Federal Income Tax Considerations” in the accompanying product supplement and the section “Certain U.S. Federal Income Tax Considerations” in the accompanying prospectus supplement.

|

|

|

Trustee:

|

Notwithstanding anything contained in the accompanying prospectus supplement to the contrary, the PLUS will be issued under the senior indenture dated March 31, 2009, between HSBC USA Inc., as Issuer, and Wells Fargo Bank, National Association, as trustee. Such indenture has substantially the same terms as the indenture described in the accompanying prospectus supplement.

|

|

Paying Agent

|

Notwithstanding anything contained in the accompanying prospectus supplement or product supplement to the contrary, HSBC Bank USA, N.A. will act as paying agent with respect to the securities pursuant to a Paying Agent and Securities Registrar Agreement dated June 1, 2009, between HSBC USA Inc. and HSBC Bank USA, N.A.

|

|

Calculation agent:

|

HSBC USA Inc., or one of its affiliates.

|

|

Supplemental plan of distribution (conflicts of interest):

|

Pursuant to the terms of a distribution agreement, HSBC Securities (USA) Inc., an affiliate of HSBC, will purchase the PLUS from HSBC for distribution to Morgan Stanley Smith Barney LLC. HSBC Securities (USA) Inc. will act as agent for the PLUS and will receive a fee of $0.1875 per $10 stated principal amount and will pay the entire fee to Morgan Stanley Smith Barney LLC as a fixed sales commission of $0.1875 for each PLUS they sell.

In addition, HSBC Securities (USA) Inc. or another of its affiliates or agents may use the pricing supplement to which this free writing prospectus relates in market-making transactions after the initial sale of the PLUS, but is under no obligation to do so and may discontinue any market-making activities at any time without notice.

See “Supplemental Plan of Distribution” on page S-52 in the prospectus supplement. All references to NASD Rule 2720 in the prospectus supplement shall be to FINRA Rule 5121.

|

This is a summary of the terms and conditions of the PLUS. We encourage you to read the accompanying underlying supplement no. 4, product supplement, prospectus supplement and prospectus for this offering, which can be accessed via the hyperlinks on the front page of this document.

|

August 2011

|

Page 9

|

PLUS Based on the Value of a Weighted Basket Composed of the S&P 500® Index, the Russell 2000® Index and the iShares® MSCI EAFE Index Fund due October 1, 2012

Performance Leveraged Upside SecuritiesSM

How PLUS Work

Payoff Diagram

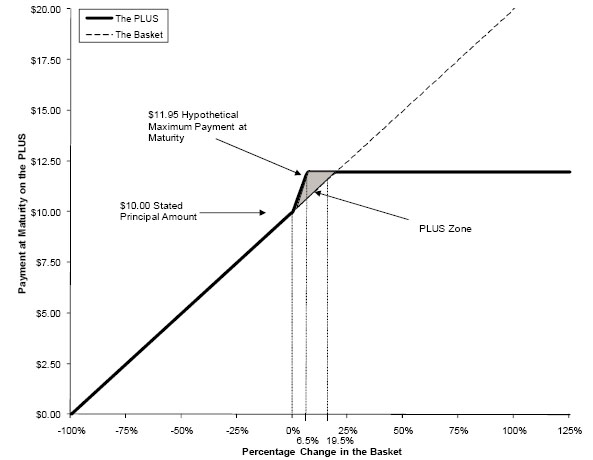

The payoff diagram below illustrates the payment at maturity on the PLUS based on the following terms:

|

Stated principal amount:

|

$10 per PLUS

|

|

Leverage factor:

|

300%

|

|

Hypothetical maximum payment at maturity:

|

$11.95 per PLUS (119.50% of the stated principal amount). The actual maximum payment at maturity will be between $11.90 to $12.00 per PLUS (119.00% to 120.00% of the stated principal amount) and will be determined on the pricing date.

|

|

PLUS Payoff Diagram

|

|

How it works

|

§

|

If the final value is greater than the initial value, investors would receive the $10 stated principal amount plus 300% of the appreciation of the basket over the term of the PLUS, subject to the hypothetical maximum payment at maturity of $11.95 per PLUS. Under the payoff diagram, an investor would realize the hypothetical maximum payment at maturity at a final share price of 106.50% of the initial share price.

|

|

|

§

|

For example, if the basket appreciates 3%, investors would receive a 9% return, or $10.90 per PLUS.

|

|

August 2011

|

Page 10

|

PLUS Based on the Value of a Weighted Basket Composed of the S&P 500® Index, the Russell 2000® Index and the iShares® MSCI EAFE Index Fund due October 1, 2012

Performance Leveraged Upside SecuritiesSM

|

|

§

|

For example, if the basket appreciates 20%, investors would receive only the maximum payment at maturity of $11.95 per PLUS, or 119.50% of the stated principal amount.

|

|

§

|

If the final value is less than or equal to the initial value, investors would receive an amount that is less than or equal to the stated principal amount by an amount, based on a 1% loss of principal for each 1% decline in the value of the basket.

|

|

|

§

|

For example, if the basket depreciates 20%, investors would lose 20% of their principal and receive only $8.00 per PLUS at maturity, or 80% of the stated principal amount.

|

|

August 2011

|

Page 11

|

PLUS Based on the Value of a Weighted Basket Composed of the S&P 500® Index, the Russell 2000® Index and the iShares® MSCI EAFE Index Fund due October 1, 2012

Performance Leveraged Upside SecuritiesSM

Payment at Maturity

At maturity, investors will receive for each $10 stated principal amount of PLUS that they hold an amount in cash based upon the closing value of the basket on the valuation date, as determined as follows:

If the final value is greater than the initial value:

$10 + leveraged upside payment; subject to the maximum payment at maturity.

If the final value is less than or equal to the initial value:

Because the basket performance factor will be less than or equal to 1.0, the payment at maturity will be less than or equal to the stated principal amount.

|

August 2011

|

Page 12

|

PLUS Based on the Value of a Weighted Basket Composed of the S&P 500® Index, the Russell 2000® Index and the iShares® MSCI EAFE Index Fund due October 1, 2012

Performance Leveraged Upside SecuritiesSM

Risk Factors

We urge you to read the section “Risk Factors” on page S-3 in the accompanying prospectus supplement, on page PS-4 of the accompanying product supplement, on page US3-1 of underlying supplement no. 3 and on page US4-2 of underlying supplement no. 4. Investing in the PLUS is not equivalent to investing directly in any of the stocks comprising the basket components or the basket components themselves, as applicable. You should understand the risks of investing in the PLUS and should reach an investment decision only after careful consideration, with your advisors, of the suitability of the PLUS in light of your particular financial circumstances and the information set forth in this free writing prospectus and the accompanying underlying supplement no. 3, underlying supplement no. 4, product supplement, prospectus supplement and prospectus.

In addition to the risks discussed below, you should review “Risk Factors” in the accompanying prospectus supplement, product supplement, underlying supplement no. 3 and underlying supplement no. 4, including the explanation of risks relating to the PLUS described in the following sections:

“— Risks Relating to All Note Issuances” in the prospectus supplement; and

“— Additional Risks Relating to Notes with an Equity Security or Equity Index as the Reference Asset” in the prospectus supplement;

“— Additional Risks Relating to Certain Notes with More than One Instrument Comprising the Reference Asset” in the prospectus supplement;

“—Additional Risks Relating to Notes Linked to the Performance of Exchange-Traded Funds” in the product supplement;

“—There are Risks Associated With Small-Capitalization Stocks” in underlying supplement no. 3;

“—Securities Prices Generally are Subject to Political, Economic, Financial and Social Factors that Apply to the Markets in Which They Trade and, to a Lesser Extent, Foreign Markets” in underlying supplement no. 4; and

“—The Notes are Subject to Currency Exchange Risk” in underlying supplement no. 4.

You will be subject to significant risks not associated with conventional fixed-rate or floating-rate debt securities.

|

|

§

|

PLUS do not pay interest and may result in a loss. The terms of the PLUS differ from those of ordinary debt securities in that the PLUS do not pay interest nor guarantee payment of the principal amount at maturity. If the final value is less than the initial value, you will receive for each PLUS that you hold a payment at maturity that is less than the stated principal amount of each PLUS by an amount proportionate to the decline in the value of the basket, subject to the credit risk of HSBC. You may lose up to 100% of the stated principal amount of the PLUS.

|

|

|

§

|

The appreciation potential of the PLUS is limited by the maximum payment at maturity. The appreciation potential of the PLUS is limited by the maximum payment at maturity of $11.90 to $12.00 per PLUS (119.00% to 120.00% of the stated principal amount). The actual maximum payment at maturity will be determined on the pricing date. Although the leverage factor provides 300% exposure to any increase in the final value over the initial value, because the payment at maturity will be limited to 119.00% to 120.00% of the stated principal amount for the PLUS, any increase in the final value over the initial value by more than approximately 6.33% to 6.67% of the initial value will not further increase the return on the PLUS.

|

|

|

§

|

Changes in the values of the basket components may offset each other. Movements in the values of the basket components may not correlate with each other. At a time when the value of one of the basket components increases, the values of the other basket components may not increase as much or may even decline. Therefore, in calculating the final value and therefore the basket return and payment at maturity, increases in the value of one or more of the basket components may be moderated, or more than offset, by lesser increases or declines in the values of the other basket components. Furthermore, the basket components are not equally weighted. As a result, a percentage change in the final component value of a basket component with a lower weighting relative to another basket component will have a lesser impact on the final value than will a similar percentage change in the final component value of such other basket components. As a result, the payment at maturity may be

|

|

August 2011

|

Page 13

|

PLUS Based on the Value of a Weighted Basket Composed of the S&P 500® Index, the Russell 2000® Index and the iShares® MSCI EAFE Index Fund due October 1, 2012

Performance Leveraged Upside SecuritiesSM

adversely affected even if the value of some of the basket components increase during the term of the PLUS. For example, because the basket component weighting for the SPX is greater than the basket component weighting for the EFA, a 5% decrease in the value of the SPX will have a greater effect on the closing value than a 5% increase in the price of the EFA. Because the SPX makes up 60% of the basket, we expect that generally the market value of your PLUS and your payment at maturity will depend significantly on the performance of the SPX.

|

|

§

|

Credit risk of HSBC USA Inc. The PLUS are senior unsecured debt obligations of the issuer, HSBC, and are not, either directly or indirectly, an obligation of any third party. As further described in the accompanying prospectus supplement and prospectus, the PLUS will rank on par with all of the other unsecured and unsubordinated debt obligations of HSBC, except such obligations as may be preferred by operation of law. Any payment to be made on the PLUS depends on the ability of HSBC to satisfy its obligations as they come due. As a result, the actual and perceived creditworthiness of HSBC may affect the market value of the PLUS and, in the event HSBC were to default on its obligations, you may not receive the amounts owed to you under the terms of the PLUS.

|

|

|

§

|

The market price will be influenced by many unpredictable factors. Several factors will influence the value of the PLUS in the secondary market and the price at which HSBC Securities (USA) Inc. may be willing to purchase or sell the PLUS in the secondary market, including: the value, volatility and dividend yield, as applicable, of the basket components and securities underlying the basket components, interest and yield rates, time remaining to maturity, geopolitical conditions and economic, financial, political and regulatory or judicial events and any actual or anticipated changes in our credit ratings or credit spreads. The values of the basket components may be, and have recently been, volatile, and we can give you no assurance that the volatility will lessen. You may receive less, and possibly significantly less, than the stated principal amount per PLUS if you try to sell your PLUS prior to maturity.

|

|

|

§

|

There is limited anti-dilution protection. For certain events affecting shares of a basket component that is an index fund, such as stock splits or extraordinary dividends, the calculation agent may make adjustments to the final component value which may affect your payment at maturity. However, the calculation agent is not required to make an adjustment for every corporate action which affects shares of the relevant basket component. If an event occurs that does not require the calculation agent to adjust the amount of the shares of the relevant basket component, the market price of the PLUS and the final settlement value may be materially and adversely affected.

|

|

|

§

|

An index fund and its underlying index are different. The performance of an index fund may not exactly replicate the performance of its underlying index, because the index fund will reflect transaction costs and fees that are not included in the calculation of its underlying index. It is also possible that an index fund may not fully replicate or may in certain circumstances diverge significantly from the performance of its underlying index due to the temporary unavailability of certain securities in the secondary market, the performance of any derivative instruments contained in the index fund or due to other circumstances. An index fund may use futures contracts, options, swap agreements, currency forwards and repurchase agreements in seeking performance that corresponds to its underlying index and in managing cash flows.

|

|

|

§

|

The EFA is subject to management risk. The index fund included in the basket is not managed according to traditional methods of “active” investment management, which involve the buying and selling of securities based on economic, financial and market analysis and investment judgment. Instead, the index fund, utilizing a “passive” or indexing investment approach, attempts to approximate the investment performance of its underlying index by investing in a portfolio of securities that generally replicates the underlying index. Therefore, unless a specific security is removed from the underlying index, the index fund generally would not sell a security because the security’s issuer was in financial trouble. In addition, the index fund is subject to the risk that the investment strategy of the index fund’s investment advisor may not produce the intended results.

|

|

|

§

|

Investing in the PLUS is not equivalent to investing in the basket components. Investing in the PLUS is not equivalent to investing in the basket components or the securities underlying the basket components. Investors

|

|

August 2011

|

Page 14

|

PLUS Based on the Value of a Weighted Basket Composed of the S&P 500® Index, the Russell 2000® Index and the iShares® MSCI EAFE Index Fund due October 1, 2012

Performance Leveraged Upside SecuritiesSM

in the PLUS will not have voting rights or rights to receive dividends or other distributions or any other rights with respect to the underlying shares or the stocks that constitute the basket components.

|

|

§

|

Adjustments to any of the basket components could adversely affect the value of the PLUS. The respective publishers of each of the basket components that is an index may add, delete or substitute the stocks constituting the basket components or, in the case of the EFA, the index tracked by the basket component, or make other methodological changes that could change the value of the basket components. Further, the publishers may discontinue or suspend calculation or publication of the basket components at any time. In these circumstances, the calculation agent will have the sole discretion to substitute a successor index that is comparable to the discontinued index and is permitted to consider indices that are calculated and published by the calculation agent or any of its affiliates.

|

|

|

§

|

Certain built-in costs are likely to adversely affect the value of the PLUS prior to maturity. The original issue price of the PLUS includes the agent’s fees and commissions and the estimated cost of HSBC hedging its obligations under the PLUS. As a result, the price, if any, at which HSBC Securities (USA) Inc. will be willing to purchase PLUS from you in secondary market transactions, if at all, will likely be lower than the original issue price, and any sale prior to the stated maturity date could result in a substantial loss to you. The PLUS are not designed to be short-term trading instruments. Accordingly, you should be able and willing to hold your PLUS to maturity.

|

|

|

§

|

The PLUS will not be listed on any securities exchange and secondary trading may be limited. The PLUS will not be listed on any securities exchange. Therefore, there may be little or no secondary market for the PLUS. HSBC Securities (USA) Inc. may, but is not obligated to, make a market in the PLUS. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell the PLUS easily. Because we do not expect that other broker-dealers will participate significantly in the secondary market for the PLUS, the price at which you may be able to trade your PLUS is likely to depend on the price, if any, at which HSBC Securities (USA) Inc. is willing to transact. If, at any time, HSBC Securities (USA) Inc. were to cease making a market in the PLUS, it is likely that there would be no secondary market for the PLUS. Accordingly, you should be willing to hold your PLUS to maturity.

|

|

|

§

|

The calculation agent, which is HSBC or one of its affiliates, will make determinations with respect to the PLUS. As calculation agent, HSBC or one of its affiliates will determine the initial component value, will determine the final component value and final value and will calculate the amount of cash, if any, you will receive at maturity. Determinations made by HSBC or one of its affiliates in its capacity as calculation agent, including with respect to the occurrence or non-occurrence of market disruption events, adjustments related to corporate events affecting the index fund, and the selection of a successor index or calculation of the final index value in the event of a discontinuance of a basket component that is an index, may adversely affect the payout to you at maturity. In addition, the calculation agent will determine the initial component value of each basket component, which will be the level of the respective basket component on the pricing date. Although the calculation agent will make all determinations and take all action in relation to the establishment of the initial component values in good faith, it should be noted that such discretion could have an impact (positive or negative) on the value of your PLUS. The calculation agent is under no obligation to consider your interests as a holder of the PLUS in taking any actions, including the determination of the initial component values, that might affect the value of your PLUS.

|

|

|

§

|

Hedging and trading activity by our affiliates could potentially adversely affect the value of the PLUS. One or more of our affiliates expect to carry out hedging activities related to the PLUS (and possibly to other instruments linked to the basket components or their respective component stocks), including trading in the stocks that constitute the basket components as well as in other instruments related to the basket. Some of our affiliates also trade the stocks that constitute the basket components and other financial instruments related to the basket on a regular basis as part of their general broker-dealer and other businesses. Such hedging or trading activities during the term of the PLUS, including on the valuation date, could adversely affect the value of the basket on the valuation date and, accordingly, the amount of cash, if any, an investor will receive at maturity.

|

|

|

§

|

The PLUS are not insured by any governmental agency of the United States or any other jurisdiction. The PLUS are not deposit liabilities or other obligations of a bank and are not insured by the Federal Deposit

|

|

August 2011

|

Page 15

|

PLUS Based on the Value of a Weighted Basket Composed of the S&P 500® Index, the Russell 2000® Index and the iShares® MSCI EAFE Index Fund due October 1, 2012

Performance Leveraged Upside SecuritiesSM

Insurance Corporation or any other governmental agency or program of the United States or any other jurisdiction. An investment in the PLUS is subject to the credit risk of HSBC, and in the event that HSBC is unable to pay its obligations as they become due, you may not receive the full payment at maturity of the PLUS.

|

|

§

|

The U.S. federal income tax consequences of an investment in the PLUS are uncertain. For a discussion of certain of the U.S. federal income tax consequences of your investment in a PLUS, please see the discussion under “Tax considerations” herein, the discussion under “Certain U.S. Federal Income Tax Considerations” in the accompanying product supplement and the discussion under “Certain U.S. Federal Income Tax Considerations” in the accompanying prospectus supplement.

|

|

August 2011

|

Page 16

|

PLUS Based on the Value of a Weighted Basket Composed of the S&P 500® Index, the Russell 2000® Index and the iShares® MSCI EAFE Index Fund due October 1, 2012

Performance Leveraged Upside SecuritiesSM

Information About the Basket Components

The S&P 500® Index

The SPX is a capitalization-weighted index of 500 U.S. stocks. It is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The top 5 industry groups by market capitalization as of August 24, 2011 were: Information Technology, Financials, Energy, Industrials and Consumer Staples.

For more information about the SPX, see “The S&P 500Ò Index” on page US3-4 of the accompanying underlying supplement no. 3.

Historical Information

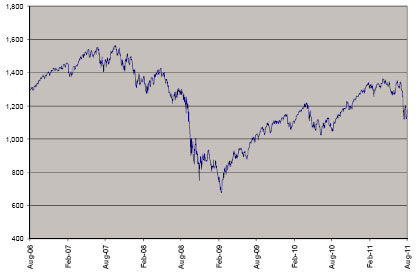

The following table sets forth the published high and low closing values, as well as end-of-quarter closing values, of the SPX for each quarter in the period from April 3, 2006 through August 24, 2011. The following graph sets forth the historical performance of the SPX based on the daily historical closing values from August 24, 2006 through August 24, 2011. The closing value for the SPX on August 24, 2011 was 1,177.60. We obtained the closing values below from Bloomberg Professional® service. We make no representation or warranty as to the accuracy or completeness of the information obtained from Bloomberg Professional® service. The historical values of the SPX should not be taken as an indication of future performance, and no assurance can be given as to the value of the SPX on the valuation date.

|

S&P 500® Index

|

High

|

Low

|

Period End

|

|

2006

|

|||

|

Second Quarter

|

1,326.70

|

1,219.29

|

1,270.20

|

|

Third Quarter

|

1,340.28

|

1,224.54

|

1,335.85

|

|

Fourth Quarter

|

1,431.81

|

1,327.10

|

1,418.30

|

|

2007

|

|||

|

First Quarter

|

1,461.57

|

1,363.98

|

1,420.86

|

|

Second Quarter

|

1,540.56

|

1,416.37

|

1,503.35

|

|

Third Quarter

|

1,555.90

|

1,370.60

|

1,526.75

|

|

Fourth Quarter

|

1,576.09

|

1,406.10

|

1,468.36

|

|

2008

|

|||

|

First Quarter

|

1,471.77

|

1,256.98

|

1,322.70

|

|

Second Quarter

|

1,440.24

|

1,272.00

|

1,280.00

|

|

Third Quarter

|

1,313.15

|

1,106.42

|

1,166.36

|

|

Fourth Quarter

|

1,167.03

|

741.02

|

903.25

|

|

2009

|

|||

|

First Quarter

|

943.85

|

666.79

|

797.87

|

|

Second Quarter

|

956.23

|

783.32

|

919.32

|

|

Third Quarter

|

1,080.15

|

869.32

|

1,057.08

|

|

Fourth Quarter

|

1,130.38

|

1,019.95

|

1,115.10

|

|

2010

|

|||

|

First Quarter

|

1,180.69

|

1,044.50

|

1,169.43

|

|

Second Quarter

|

1,219.80

|

1,028.33

|

1,030.71

|

|

Third Quarter

|

1,157.16

|

1,010.91

|

1,141.20

|

|

Fourth Quarter

|

1,262.60

|

1,131.87

|

1,257.64

|

|

2011

|

|||

|

First Quarter

|

1,344.07

|

1,249.05

|

1,325.83

|

|

Second Quarter

|

1,370.58

|

1,258.07

|

1,320.64

|

|

Third Quarter (through August 24, 2011)

|

1,356.48

|

1,101.54

|

1,177.60

|

|

August 2011

|

Page 17

|

PLUS Based on the Value of a Weighted Basket Composed of the S&P 500® Index, the Russell 2000® Index and the iShares® MSCI EAFE Index Fund due October 1, 2012

Performance Leveraged Upside SecuritiesSM

|

SPX Historical Performance – Daily Closing Values

August 24, 2006 to August 24, 2011

|

|

The Russell 2000® Index

The RTY is designed to track the performance of the small capitalization segment of the United States equity market. All 2,000 stocks are traded on the New York Stock Exchange or NASDAQ, and the RTY consists of the smallest 2,000 companies included in the Russell 3000® Index. The Russell 3000® Index is composed of the 3,000 largest United States companies as determined by market capitalization and represents approximately 98% of the United States equity market.

For more information about the RTY, see “The Russell 2000Ò Index” on page US3- of the accompanying underlying supplement no. 3.

Historical Information

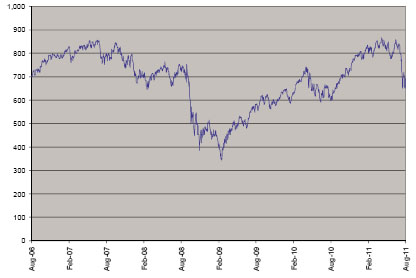

The following table sets forth the published high and low closing values, as well as end-of-quarter closing values, of the RTY for each quarter in the period from April 3, 2006 through August 24, 2011. The following graph sets forth the historical performance of the RTY based on the daily historical closing values from August 24, 2006 through August 24, 2011. The closing value for the RTY on August 24, 2011 was 692.57. We obtained the closing values below from Bloomberg Professional® service. We make no representation or warranty as to the accuracy or completeness of the information obtained from Bloomberg Professional® service. The historical values of the RTY should not be taken as an indication of future performance, and no assurance can be given as to the value of the RTY on the valuation date.

|

Russell 2000® Index

|

High

|

Low

|

Period End

|

|

2006

|

|||

|

Second Quarter

|

784.62

|

669.88

|

724.67

|

|

Third Quarter

|

738.16

|

668.58

|

725.59

|

|

Fourth Quarter

|

801.01

|

712.17

|

787.66

|

|

2007

|

|||

|

First Quarter

|

830.01

|

760.06

|

800.71

|

|

Second Quarter

|

856.39

|

798.17

|

833.70

|

|

Third Quarter

|

856.48

|

736.00

|

805.45

|

|

Fourth Quarter

|

852.06

|

734.4

|

766.03

|

|

August 2011

|

Page 18

|

PLUS Based on the Value of a Weighted Basket Composed of the S&P 500® Index, the Russell 2000® Index and the iShares® MSCI EAFE Index Fund due October 1, 2012

Performance Leveraged Upside SecuritiesSM

|

Russell 2000® Index

|

High

|

Low

|

Period End

|

|

2008

|

|||

|

First Quarter

|

768.46

|

643.28

|

687.97

|

|

Second Quarter

|

763.27

|

684.88

|

689.66

|

|

Third Quarter

|

764.38

|

647.37

|

679.58

|

|

Fourth Quarter

|

679.57

|

371.26

|

499.45

|

|

2009

|

|||

|

First Quarter

|

519.18

|

342.57

|

422.75

|

|

Second Quarter

|

535.85

|

412.77

|

508.28

|

|

Third Quarter

|

625.31

|

473.54

|

604.28

|

|

Fourth Quarter

|

635.99

|

553.32

|

625.39

|

|

2010

|

|||

|

First Quarter

|

693.32

|

580.49

|

678.64

|

|

Second Quarter

|

745.95

|

607.30

|

609.49

|

|

Third Quarter

|

678.90

|

587.60

|

676.14

|

|

Fourth Quarter

|

793.28

|

669.43

|

783.65

|

|

2011

|

|||

|

First Quarter

|

843.73

|

771.71

|

843.55

|

|

Second Quarter

|

868.57

|

772.62

|

827.43

|

|

Third Quarter (through August 24, 2011)

|

860.37

|

639.85

|

692.57

|

|

RTY Historical Performance – Daily Closing Values

August 24, 2006 to August 24, 2011

|

|

The iShares® MSCI Emerging Markets Index Fund

The EFA seeks investment results that correspond generally to the price and yield performance, before fees and expenses, of publicly traded securities in the European, Australasian, and Far Eastern markets, as measured by the MSCI EAFE® Index, which is the Underlying Index of the EFA. As of August 24, 2011, the MSCI EAFEÒ Index consisted of the following 22 component country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Greece, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, and the United Kingdom.

|

August 2011

|

Page 19

|

PLUS Based on the Value of a Weighted Basket Composed of the S&P 500® Index, the Russell 2000® Index and the iShares® MSCI EAFE Index Fund due October 1, 2012

Performance Leveraged Upside SecuritiesSM

For more information about the EAFE, see “The iShares® MSCI EAFE Index Fund” on page US4-25 of the accompanying underlying supplement no. 4.

Historical Information

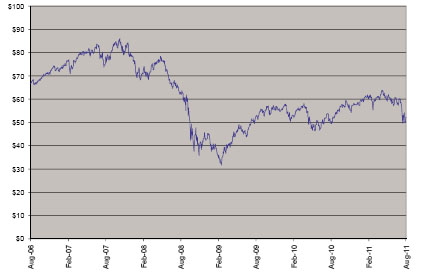

The following table sets forth the published high and low closing prices, as well as end-of-quarter closing prices, of the iShares® MSCI EAFE Index Fund for each quarter in the period from April 3, 2006 through August 24, 2011. The following graph sets forth the historical performance of the iShares® MSCI EAFE Index Fund based on the daily historical closing prices from August 24, 2006 through August 24, 2011. The closing price for the EFA on August 24, 2011 was $52.15. We obtained the closing prices below from Bloomberg Professional® service. We make no representation or warranty as to the accuracy or completeness of the information obtained from Bloomberg Professional® service. The historical prices of the iShares® MSCI EAFE Index Fund should not be taken as an indication of future performance, and no assurance can be given as to the price of the shares of the iShares® MSCI EAFE Index Fund on the valuation date.

|

iShares® MSCI EAFE Index Fund

|

High

|

Low

|

Period End

|

|

2006

|

|||

|

Second Quarter

|

$70.65

|

$59.40

|

$65.35

|

|

Third Quarter

|

$68.52

|

$60.94

|

$67.78

|

|

Fourth Quarter

|

$74.66

|

$67.61

|

$73.26

|

|

2007

|

|||

|

First Quarter

|

$77.18

|

$70.95

|

$76.27

|

|

Second Quarter

|

$81.79

|

$76.05

|

$80.63

|

|

Third Quarter

|

$85.50

|

$67.99

|

$82.56

|

|

Fourth Quarter

|

$86.49

|

$78.00

|

$78.50

|

|

2008

|

|||

|

First Quarter

|

$79.22

|

$65.63

|

$71.90

|

|

Second Quarter

|

$78.76

|

$68.06

|

$68.70

|

|

Third Quarter

|

$68.39

|

$52.36

|

$56.30

|

|

Fourth Quarter

|

$56.42

|

$35.53

|

$44.87

|

|

2009

|

|||

|

First Quarter

|

$45.61

|

$31.56

|

$37.59

|

|

Second Quarter

|

$49.18

|

$37.28

|

$45.81

|

|

Third Quarter

|

$56.31

|

$43.49

|

$54.70

|

|

Fourth Quarter

|

$57.66

|

$52.42

|

$55.30

|

|

2010

|

|||

|

First Quarter

|

$58.00

|

$49.94

|

$56.00

|

|

Second Quarter

|

$58.08

|

$45.86

|

$46.51

|

|

Third Quarter

|

$55.81

|

$46.45

|

$54.92

|

|

Fourth Quarter

|

$59.50

|

$53.85

|

$58.23

|

|

2011

|

|||

|

First Quarter

|

$61.98

|

$54.69

|

$60.09

|

|

Second Quarter

|

$64.35

|

$56.71

|

$60.14

|

|

Third Quarter (through August 24, 2011)

|

$60.86

|

$49.64

|

$52.15

|

|

August 2011

|

Page 20

|

PLUS Based on the Value of a Weighted Basket Composed of the S&P 500® Index, the Russell 2000® Index and the iShares® MSCI EAFE Index Fund due October 1, 2012

Performance Leveraged Upside SecuritiesSM

|

EFA Historical Performance – Daily Closing Prices

August 24, 2006 to August 24, 2011

|

|

Information About the Basket

The following graph illustrates the hypothetical daily historical performance of the basket from August 24, 2006 through August 24, 2011 based on information from Bloomberg Professional® service, if the level of the basket was made to equal 100 on August 24, 2006. The hypothetical historical performance reflects the performance the basket would have exhibited based on the actual historical performance of the basket components. Neither the hypothetical historical performance of the basket nor the actual historical performance of the basket components should be taken as indications of future performance.

We cannot give you assurance that the performance of the basket will result in the return of your initial investment. All payments on the PLUS are subject to the credit risk of HSBC.

|

August 2011

|

Page 21

|

PLUS Based on the Value of a Weighted Basket Composed of the S&P 500® Index, the Russell 2000® Index and the iShares® MSCI EAFE Index Fund due October 1, 2012

Performance Leveraged Upside SecuritiesSM

Valuation Date and Maturity Date

If the valuation date is not a scheduled trading day for any basket component, then the valuation date for such basket component will be the next succeeding day that is a scheduled trading day (as defined in underlying supplement no. 3 with respect to each basket component that is an index and in underlying supplement no. 4 with respect to the basket component that is an index fund) for such basket component. For each basket component, the calculation agent will determine whether a market disruption event (as defined in underlying supplement no. 3 with respect to each basket component that is an index and in underlying supplement no. 4 with respect to the basket component that is an index fund) exists on the valuation date with respect to such basket component independent from other basket components; therefore, a market disruption event may exist for certain basket components and not exist for other basket components. If a market disruption event exists for a basket component on the valuation date, then the valuation date for such basket component will be the next scheduled trading day for which there is no market disruption event for such basket component. If such market disruption event continues for five consecutive scheduled trading days, then that fifth scheduled trading day will nonetheless be the valuation date for such basket component, and the final component value with respect to such basket component will be determined (1) with respect to a basket component that is an index, by means of the formula for and method of calculating such index which applied just prior to the market disruption event, using the relevant exchange’s traded or quoted price of each stock or other security included in such index (or if an event giving rise to a market disruption event has occurred with respect to a stock or other security in such index and is continuing on that fifth scheduled trading day, the calculation agent’s good faith estimate of the value for that stock or other security), or (2) with respect to the basket component that is an index fund, by the calculation agent, in its sole discretion, using its estimate of the exchange traded prices for such index fund that would have prevailed but for that market disruption event. For the avoidance of doubt, if no market disruption event exists with respect to a basket component on the originally scheduled valuation date, the determination of such basket component’s final component value will be made on the originally scheduled valuation date, irrespective of the existence of a market disruption event with respect to any other basket component. If the valuation date for any basket component is postponed, then the maturity date will also be postponed to the third business day following the latest of such postponed valuation dates.

Events of Default and Acceleration

If the securities have become immediately due and payable following an event of default (as defined in the accompanying prospectus) with respect to the PLUS, the calculation agent will determine the accelerated payment at maturity due and payable in the same general manner as described in “payment at maturity” in this free writing prospectus. In such a case, the third scheduled trading day for all of the basket components immediately preceding the date of acceleration will be used as the valuation date for purposes of determining the accelerated basket component return for each basket component. If a market disruption event exists with respect to a basket component on that scheduled trading day, then the accelerated valuation date will be postponed for up to five scheduled trading days (in the same general manner used for postponing the originally scheduled valuation date). The accelerated maturity date will be the fifth business day following such accelerated postponed valuation date.

For more information, see “Description of Debt Securities — Events of Default” in the accompanying prospectus.

Where You Can Find More Information

This free writing prospectus relates to an offering of securities linked to the basket identified on the cover page. The purchaser of a PLUS will acquire a senior unsecured debt security of HSBC USA Inc. linked to the basket. We reserve the right to withdraw, cancel or modify any offering and to reject orders in whole or in part. Although the offering of PLUS relates to the basket identified on the cover page, you should not construe that fact as a recommendation as to the merits of acquiring an investment linked to the basket or any component security included in the basket or as to the suitability of an investment in the PLUS.

HSBC has filed a registration statement (including a prospectus, a prospectus supplement, a product supplement, underlying supplement no. 3 and underlying supplement no. 4) with the SEC for the offering to which this free writing prospectus relates. Before you invest, you should read the prospectus, prospectus supplement, product supplement, underlying supplement no. 3 and underlying supplement no. 4 in that registration statement and other documents HSBC has filed with the SEC for more complete information about HSBC and this offering. You may get these documents for free by

|

August 2011

|

Page 22

|

PLUS Based on the Value of a Weighted Basket Composed of the S&P 500® Index, the Russell 2000® Index and the iShares® MSCI EAFE Index Fund due October 1, 2012

Performance Leveraged Upside SecuritiesSM

visiting EDGAR on the SEC’s web site at www.sec.gov. Alternatively, HSBC Securities (USA) Inc. or any dealer participating in this offering will arrange to send you the prospectus, prospectus supplement, product supplement, underlying supplement no. 3 and underlying supplement no. 4 if you request them by calling toll-free 1-866-811-8049.

You should read this document together with the prospectus dated April 2, 2009, the prospectus supplement dated April 9, 2009, the product supplement dated April 9, 2009, underlying supplement no. 3 dated October 22, 2010 and the underlying supplement no. 4 dated October 22, 2010. All references to “Enhanced Market Participation Notes” in the accompanying product supplement shall refer to these PLUS. If the terms of the PLUS offered hereby are inconsistent with those described in the accompanying product supplement, prospectus supplement, prospectus, underlying supplement no. 3 or underlying supplement no. 4, the terms described in this free writing prospectus shall control. You should carefully consider, among other things, the matters set forth in “Risk Factors” herein, on page PS-4 of the product supplement, on page S-3 of the prospectus supplement and on page US4-2 of underlying supplement no. 4, as the PLUS involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting and other advisors before you invest in the securities. As used herein, references to the “Issuer”, “HSBC”, “we”, “us” and “our” are to HSBC USA Inc.

You may access these documents on the SEC web site at .www.sec.gov as follows:

|

|

·

|

The underlying supplement no. 3 at:

|

|

|

·

|

The underlying supplement no. 4 at:

|

|

|

·

|

The product supplement at:

|

|

|

·

|

The prospectus supplement at:

|

|

|

·

|

The prospectus at:

|

“Performance Leveraged Upside SecuritiesSM” and “PLUSSM” are service marks of Morgan Stanley.

|

August 2011

|

Page 23

|