|

ISSUER FREE WRITING PROSPECTUS

Filed Pursuant to Rule 433

Registration Statement No. 333-158385

Dated July 1, 2011

|

|

HSBC USA Inc. Buffered Return Optimization Securities

Linked to the S&P MidCap 400® Index due on or about July 31, 2013

|

Investment Description

|

|

These Buffered Return Optimization Securities Linked to the S&P MidCap 400® Index (the "Index") are senior unsecured debt securities issued by HSBC USA Inc. (“HSBC”), which we refer to as the “Securities”. The Securities will rank equally with all of our other unsecured and unsubordinated debt obligations. If the Index Return is positive, HSBC will repay the Principal Amount at maturity plus pay a return equal to the Multiplier of 1.25 times the Index Return, up to the Maximum Gain, which will be set on the Trade Date and is expected to be between 17.00% and 21.00%. If the Index Return is zero or negative but the Index's percentage decline is less than the 10% Buffer, HSBC will repay the full Principal Amount at maturity. However, if the Index Return is negative and the Index's percentage decline is more than the 10% Buffer, HSBC will pay less than the full Principal Amount at maturity, resulting in a loss of principal to investors that is equal to the Index's decline in excess of 10%. Investing in the Securities involves significant risks. HSBC will not pay any interest on the Securities. You may lose up to 90% of your Principal Amount if the Index Return is less than -10%. The buffered downside market exposure applies only if you hold the Securities to maturity. Any payment on the Securities, including any repayment of principal, is subject to the creditworthiness of HSBC. If HSBC were to default on its payment obligations you may not receive any amounts owed to you under the Securities and you could lose your entire investment.

|

|

Features

|

|

q

|

Enhanced Growth Potential: At maturity, the Securities enhance any positive Index Return up to the Maximum Gain. If the Index Return is negative, investors may be exposed to the negative Index Return at maturity.

|

|

q

|

Buffered Downside Market Exposure: If the Index Return is zero or negative, but the Index's percentage decline is less than the 10% Buffer, HSBC will repay the full Principal Amount at maturity. However, if the Index Return is negative and the Index’s decline is more than the 10% Buffer, HSBC will pay less than the full Principal Amount at maturity resulting in a loss of principal to investors that is equal to the Index's decline in excess of 10%. Accordingly, you could lose up to 90% of the Principal Amount. The buffered downside market exposure applies only if you hold the Securities to maturity. Any payment on the Securities, including any repayment of principal, is subject to the creditworthiness of HSBC.

|

|

Key Dates1

|

|

Trade Date

|

July 26, 2011

|

|

Settlement Date

|

July 29, 2011

|

|

Final Valuation Date2

|

July 25, 2013

|

|

Maturity Date2

|

July 31, 2013

|

|

1 Expected. In the event we make any change to the expected Trade Date and Settlement Date, the Final Valuation Date and Maturity Date will be changed so that the stated term of the Securities remains the same.

|

2 Subject to adjustment as described in the accompanying underlying supplement no. 3.

|

THE SECURITIES ARE SIGNIFICANTLY RISKIER THAN CONVENTIONAL DEBT INSTRUMENTS. THE TERMS OF THE SECURITIES MAY NOT OBLIGATE HSBC TO REPAY THE FULL PRINCIPAL AMOUNT OF THE SECURITIES. THE SECURITIES CAN HAVE DOWNSIDE MARKET RISK SIMILAR TO THE INDEX, SUBJECT TO THE BUFFER, WHICH CAN RESULT IN A LOSS OF UP TO 90% OF THE PRINCIPAL AMOUNT AT MATURITY. THIS MARKET RISK IS IN ADDITION TO THE CREDIT RISK INHERENT IN PURCHASING A DEBT OBLIGATION OF HSBC. YOU SHOULD NOT PURCHASE THE SECURITIES IF YOU DO NOT UNDERSTAND OR ARE NOT COMFORTABLE WITH THE SIGNIFICANT RISKS INVOLVED IN INVESTING IN THE SECURITIES.

YOU SHOULD CAREFULLY CONSIDER THE RISKS DESCRIBED UNDER ‘‘KEY RISKS’’ BEGINNING ON PAGE 7 OF THIS FREE WRITING PROSPECTUS AND THE MORE DETAILED ‘‘RISK FACTORS’’ BEGINNING ON PAGE US3-1 OF THE ACCOMPANYING UNDERLYING SUPPLEMENT NO. 3, BEGINNING ON PAGE PS-3 OF THE ACCOMPANYING PRODUCT SUPPLEMENT AND BEGINNING ON PAGE S-3 OF THE ACCOMPANYING PROSPECTUS SUPPLEMENT BEFORE PURCHASING ANY SECURITIES. EVENTS RELATING TO ANY OF THOSE RISKS, OR OTHER RISKS AND UNCERTAINTIES, COULD ADVERSELY AFFECT THE MARKET VALUE OF, AND THE RETURN ON, YOUR SECURITIES.

|

|

Security Offering

|

HSBC USA Inc. is offering Buffered Return Optimization Securities Linked to the S&P MidCap 400® Index. The return on the Securities is subject to, and will not exceed, the predetermined Maximum Gain, which will be determined on the Trade Date. The Securities are offered at a minimum investment of $1,000 in denominations of $10 and integral multiples thereof. The indicative Maximum Gain for the Securities is listed below. The actual Maximum Gain and Initial Level for the Securities will be determined on the Trade Date.

|

Index

|

Multiplier

|

Maximum Gain

|

Buffer

|

Initial Level

|

CUSIP

|

ISIN

|

|

S&P MidCap 400® Index

|

1.25

|

17.00% to 21.00%

|

10%

|

40433C676

|

US40433C6764

|

See “Additional Information about HSBC USA Inc. and the Securities” on page 2 of this free writing prospectus. The Securities offered will have the terms specified in the accompanying prospectus dated April 2, 2009, the accompanying prospectus supplement dated April 9, 2009, the accompanying underlying supplement no. 3, dated October 22, 2010 and the terms set forth herein.

Neither the U.S. Securities and Exchange Commission (“SEC”) nor any state securities commission has approved or disapproved of the Securities or passed upon the accuracy or the adequacy of this document, the accompanying underlying supplement no. 3, prospectus or prospectus supplement. Any representation to the contrary is a criminal offense. The Securities are not deposit liabilities or other obligations of a bank and are not insured by the Federal Deposit Insurance Corporation or any other governmental agency of the United States or any other jurisdiction.

The Securities will not be listed on any U.S. securities exchange or quotation system. HSBC Securities (USA) Inc., an affiliate of HSBC, will purchase the Securities from HSBC for distribution to UBS Financial Services Inc., acting as agent. See “Supplemental Plan of Distribution (Conflicts of Interest)” on page 12 for a description of the distribution arrangement.

|

Price to Public (1)

|

Underwriting Discount (1)

|

Proceeds to Us

|

|

|

Per Security

|

$10.00

|

$0.20

|

$9.80

|

|

Total

|

|

(1)

|

UBS Financial Services Inc. will act as placement agent for sales to certain advisory accounts at a purchase price to such accounts of $9.80 per Security, and will not receive a sales commission with respect to such sales. See “Supplemental Plan of Distribution (Conflicts of Interest)” on page 12 of this free writing prospectus.

|

|

UBS Financial Services Inc.

|

HSBC USA Inc.

|

|

Additional Information about HSBC USA Inc. and the Securities

|

This free writing prospectus relates to one offering linked to the Index identified on the cover page. The Index described in this free writing prospectus is a reference asset as defined in underlying supplement no. 3 and the prospectus supplement, and the Securities being offered hereby are “notes” for purposes of underlying supplement no. 3 and the prospectus supplement. As a purchaser of a Security, you will acquire an investment instrument linked to the Index. Although the Security offering relates to the Index identified on the cover page, you should not construe that fact as a recommendation of the merits of acquiring an investment linked to the Index, or as to the suitability of an investment in the Securities.

You should read this document together with the underlying supplement no. 3 dated October 22, 2010, the prospectus dated April 2, 2009 and the prospectus supplement dated April 9, 2009. If the terms of the Securities offered hereby are inconsistent with those described in the accompanying underlying supplement no. 3, prospectus supplement or prospectus, the terms described in this free writing prospectus will control. You should carefully consider, among other things, the matters set forth in “Key Risks” beginning on page 7 of this free writing prospectus and in “Risk Factors” beginning on page US3-1 of the underlying supplement no. 3 and beginning on page S-3 of the prospectus supplement, as the Securities involve risks not associated with conventional debt securities. You are urged to consult your investment, legal, tax, accounting and other advisors before you invest in the Securities.

HSBC has filed a registration statement (including underlying supplement no. 3, a prospectus and prospectus supplement) with the SEC for the offering to which this free writing prospectus relates. Before you invest, you should read underlying supplement no. 3, the prospectus and prospectus supplement in that registration statement and other documents HSBC has filed with the SEC for more complete information about HSBC and this offering. You may get these documents for free by visiting EDGAR on the SEC web site at www.sec.gov. Alternatively, HSBC Securities (USA) Inc. or any dealer participating in this offering will arrange to send you the prospectus and prospectus supplement if you request them by calling toll-free 1-866-811-8049.

You may access these documents on the SEC web site at www.sec.gov as follows:

|

|

¨

|

Underlying supplement no. 3 dated October 22, 2010:

|

|

|

http://www.sec.gov/Archives/edgar/data/83246/000114420410055205/v198039_424b2.htm

|

|

|

¨

|

Prospectus supplement dated April 9, 2009:

|

|

|

www.sec.gov/Archives/edgar/data/83246/000114420409019785/v145824_424b2.htm

|

|

|

¨

|

Prospectus dated April 2, 2009:

|

|

|

www.sec.gov/Archives/edgar/data/83246/000104746909003736/a2192100zs-3asr.htm

|

As used herein, references to “HSBC”, “we”, “the issuer”, “us” and “our” are to HSBC USA Inc. References to the “underlying supplement no. 3” mean the underlying supplement no. 3 dated October 22, 2010, references to “prospectus supplement” mean the prospectus supplement dated April 9, 2009 and references to “accompanying prospectus” mean the HSBC prospectus dated April 2, 2009.

|

Investor Suitability

|

||

|

The Securities may be suitable for you if:

¨ You fully understand the risks inherent in an investment in the Securities, including the risk of loss of up to 90% of your Principal Amount.

¨ You can tolerate the loss of up to 90% of your Principal Amount and you are willing to make an investment that has similar downside market risk as a hypothetical investment in the Index, subject to the Buffer at maturity.

¨ You believe the Index will appreciate over the term of the Securities and that the appreciation is unlikely to exceed the Maximum Gain of between 17.00% and 21.00% (the actual Maximum Gain will be determined on the Trade Date).

¨ You understand and accept that your potential return is limited by the Maximum Gain and you would be willing to invest in the Securities if the Maximum Gain were set to the bottom of the range indicated on the cover (the actual Maximum Gain for the Securities will be determined on the Trade Date and will not be less than 17.00%).

¨ You are willing to hold the Securities to maturity, a term of two years, and accept that there may be little or no secondary market for the Securities.

¨ You do not seek current income from your investment and are willing to forego dividends paid on the stocks included in the Index.

¨ You are willing to assume the credit risk of HSBC, as issuer of the Securities, and understand that if HSBC defaults on its obligation you may not receive any amounts due to you including the repayment of your principal.

|

The Securities may not be suitable for you if:

¨ You do not fully understand the risks inherent in an investment in the Securities, including the risk of loss of up to 90% of your Principal Amount.

¨ You cannot tolerate the loss of up to 90% of your Principal Amount and you are not willing to make an investment that has similar downside market risk as a hypothetical investment in the Index, subject to the Buffer at maturity.

¨ You seek an investment that provides a full return of principal at maturity.

¨ You believe that the level of the Index will decline during the term of the Securities, or you believe the Index will appreciate over the term of the Securities by a percentage that exceeds the Maximum Gain.

¨ You seek an investment that has unlimited return potential without a cap on appreciation.

¨ You would be unwilling to invest in the Securities if the Maximum Gain were set equal to the bottom of the range indicated on the cover (the actual Maximum Gain will be determined on the Trade Date and will not be less than 17.00%).

¨ You prefer the lower risk, and therefore accept the potentially lower returns, of conventional debt securities with comparable maturities issued by HSBC or another issuer with a similar credit rating.

¨ You seek current income from this investment or prefer to receive the dividends paid on the stocks included in the Index.

¨ You are unable or unwilling to hold the Securities to maturity, a term of two years, or you seek an investment for which there will be an active secondary market.

¨ You are not willing or are unable to assume the credit risk associated with HSBC, as issuer of the Securities, for any payment on the Securities, including any repayment of principal.

|

|

The suitability considerations identified above are not exhaustive. Whether or not the Securities are a suitable investment for you will depend on your individual circumstances, and you should reach an investment decision only after you and your investment, legal, tax, accounting and other advisors have carefully considered the suitability of an investment in the Securities in light of your particular circumstances. You should also review “Key Risks” on page 7 of this free writing prospectus and the more detailed “Risk Factors” beginning on page US3-1 of the underlying supplement no. 3 and beginning on page S-3 of the accompanying prospectus supplement.

2

|

Indicative Terms

|

|

Issuer

|

HSBC USA Inc. (A1/AA-/AA)1

|

|

Issue Price

|

$10.00 per Security for brokerage accounts; $9.80 per Security for certain advisory accounts.

|

|

Principal Amount

|

$10 per Security. The Payment at Maturity will be based on the Principal Amount per Security.

|

|

Term

|

2 years

|

|

Index

|

S&P MidCap 400® Index (“MID”)

|

|

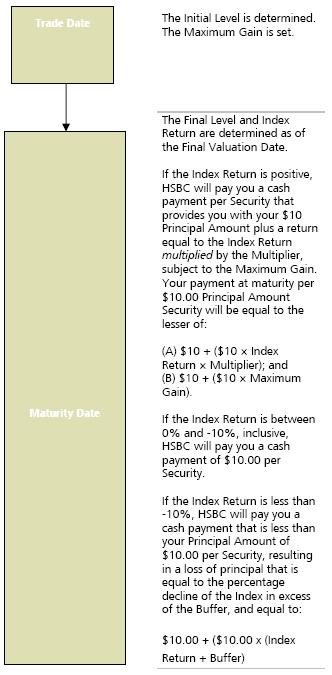

Payment at Maturity (per $10 Principal Amount Security)

|

You will receive a cash payment at maturity linked to the performance of the Index during the term of the Securities.

If the Index Return is greater than zero, HSBC will pay you an amount equal to the lesser of:

(A) $10 + ($10 × Index Return × Multiplier); and

(B) $10 + ($10 × Maximum Gain).

If the Index Return is zero or negative, but the Index's percentage decline is not more than the Buffer, HSBC will pay you the $10 Principal Amount.

If the Index Return is negative and the Index's percentage decline is more than the Buffer, HSBC will pay you an amount calculated as follows:

$10 + [$10 × (Index Return + Buffer)]

In this case you could lose up to 90% of your Principal Amount.

|

|

Multiplier

|

1.25

|

|

Maximum Gain

|

Between 17.00% and 21.00%. The actual Maximum Gain will be determined on the Trade Date.

|

|

Buffer

|

10%

|

|

Index Return

|

Final Level – Initial Level

|

|

Initial Level

|

|

|

Initial Level

|

The Official Closing Level of the Index on the Trade Date.

|

|

Final Level

|

The Official Closing Level of the Index on the Final Valuation Date.

|

|

Official Closing Level

|

The Official Closing Level on any scheduled trading day will be the closing level of the Index as determined by the calculation agent and based on the value displayed on Bloomberg Professional® service page “MID <INDEX>”, or on any successor page on Bloomberg Professional® service or any successor service, as applicable.

|

|

CUSIP / ISIN

|

40433C676 / US40433C6764

|

|

Calculation Agent

|

HSBC USA Inc. or one of its affiliates.

|

|

Trustee

|

Notwithstanding anything contained in the accompanying prospectus supplement to the contrary, the Securities will be issued under the senior indenture dated March 31, 2009, between HSBC USA Inc., and Wells Fargo Bank, National Association, as trustee. Such indenture has substantially the same terms as the indenture described in the accompanying prospectus supplement.

|

|

Paying Agent

|

Notwithstanding anything contained in the accompanying prospectus supplement to the contrary, HSBC Bank USA, N.A. will act as paying agent with respect to the Securities pursuant to a Paying Agent and Securities Registrar Agreement dated June 1, 2009, between HSBC USA Inc. and HSBC Bank USA, N.A.

|

|

Investment Timeline

|

Under these circumstances, you could lose up to 90% of the Principal Amount of your Securities depending on how much the level of the Index decreases over the term of the Securities.

INVESTING IN THE SECURITIES INVOLVES SIGNIFICANT RISKS. YOU MAY LOSE UP TO 90% OF YOUR PRINCIPAL AMOUNT. ANY PAYMENT ON THE SECURITIES, INCLUDING ANY REPAYMENT OF PRINCIPAL AT MATURITY, IS SUBJECT TO THE CREDITWORTHINESS OF HSBC. IF HSBC WERE TO DEFAULT ON ITS PAYMENT OBLIGATIONS, YOU MAY NOT RECEIVE ANY AMOUNTS OWED TO YOU UNDER THE SECURITIES AND YOU COULD LOSE YOUR ENTIRE INVESTMENT.

1 HSBC is rated A1 by Moody’s Investors Service, Inc., AA- by Standard & Poor’s Financial Services LLC, a subsidiary of The McGraw-Hill Companies, Inc. and AA by Fitch Ratings. A credit rating reflects the creditworthiness of HSBC and is not a recommendation to buy, sell or hold the Securities, and it may be subject to revision or withdrawal at any time by the assigning rating organization. The Securities themselves have not been independently rated. Each rating should be evaluated independently of any other rating.

3

|

What are the tax consequences of the Securities?

|

|

You should carefully consider, among other things, the matters set forth in the section “Certain U.S. Federal Income Tax Considerations” in the prospectus supplement. The following discussion summarizes certain of the material U.S. federal income tax consequences of the purchase, beneficial ownership, and disposition of each of the Securities. This summary supplements the section “Certain U.S. Federal Income Tax Considerations” in the prospectus supplement and supersedes it to the extent inconsistent therewith. Notwithstanding any disclosure in the accompanying prospectus supplement to the contrary, HSBC’s special U.S. tax counsel in this transaction is Sidley Austin llp.

|

|

There are no statutory provisions, regulations, published rulings or judicial decisions addressing the characterization for U.S. federal income tax purposes of securities with terms that are substantially the same as those of the Securities. Under one reasonable approach, the Securities should be treated as pre-paid forward or other executory contracts with respect to the Index. HSBC intends to treat the Securities consistent with this approach and pursuant to the terms of the Securities, you agree to treat the Securities under this approach for all U.S. federal income tax purposes. Subject to certain limitations described in the accompanying prospectus supplement, and based on certain factual representations received from HSBC, in the opinion of HSBC’s special U.S. tax counsel, Sidley Austin llp, it is reasonable to treat the Securities in accordance with this approach. Pursuant to this approach, HSBC does not intend to report any income or gain with respect to the Securities prior to their maturity or an earlier sale or exchange and HSBC intends to treat any gain or loss upon maturity or an earlier sale or exchange as long-term capital gain or loss, provided that you have held the Security for more than one year at such time for U.S. federal income tax purposes. See "Certain U.S. Federal Income Tax Considerations — Certain Equity-Linked Notes — Certain Notes Treated as Forward Contracts or Executory Contracts" in the prospectus supplement for certain U.S. federal income tax considerations applicable to Securities that are treated as pre-paid cash-settled forward or other executory contracts.

|

|

Because there are no statutory provisions, regulations, published rulings or judicial decisions addressing the characterization for U.S. federal income tax purposes of securities with terms that are substantially the same as those of the Securities, other characterizations and treatments are possible and the timing and character of income in respect of the Securities might differ from the treatment described above. For example, the Securities could be treated as debt instruments that are “contingent payment debt instruments” for U.S. federal income tax purposes subject to the treatment described under the heading “Certain U.S. Federal Income Tax Considerations — U.S. Federal Income Tax Treatment of the Notes as Indebtedness for U.S. Federal Income Tax Purposes — Contingent Payment Debt Instruments” in the prospectus supplement.

|

|

In Notice 2008-2, the Internal Revenue Service (“IRS”) and the Treasury Department requested comments as to whether the purchaser of an exchange traded note or pre-paid forward contract (which may include the Securities) should be required to accrue income during its term under a mark-to-market, accrual or other methodology, whether income and gain on such a note or contract should be ordinary or capital, and whether foreign holders should be subject to withholding tax on any deemed income accrual. Accordingly, it is possible that regulations or other guidance could provide that a U.S. holder (as defined in the prospectus supplement) of a Security is required to accrue income in respect of the Security prior to the receipt of payments with respect to the Security or its earlier sale. Moreover, it is possible that any such regulations or other guidance could treat all income and gain of a U.S. holder in respect of a Security as ordinary income (including gain on a sale). Finally, it is possible that a non-U.S. holder (as defined in the prospectus supplement) of the Security could be subject to U.S. withholding tax in respect of a Security. It is unclear whether any regulations or other guidance would apply to the Securities (possibly on a retroactive basis). Prospective investors are urged to consult with their tax advisors regarding Notice 2008-2 and the possible effect to them of the issuance of regulations or other guidance that affects the U.S. federal income tax treatment of the Securities.

PROSPECTIVE PURCHASERS OF SECURITIES SHOULD CONSULT THEIR TAX ADVISORS AS TO THE U.S. FEDERAL, STATE, LOCAL, AND OTHER TAX CONSEQUENCES TO THEM OF THE PURCHASE, OWNERSHIP AND DISPOSITION OF SECURITIES.

|

4

|

Scenario Analysis and Examples at Maturity

|

The below scenario analysis and examples are provided for illustrative purposes only and are purely hypothetical. They do not purport to be representative of every possible scenario concerning increases or decreases in the level of the Index relative to the Initial Level. We cannot predict the Final Level or the Official Closing Level of the Index on any other scheduled trading day. You should not take the scenario analysis and these examples as an indication or assurance of the expected performance of the Index. The numbers set forth in the examples below have been rounded for ease of analysis. The following scenario analysis and examples illustrate the Payment at Maturity for a $10.00 Principal Amount of Securities on a hypothetical offering of the Securities. The scenario analysis provides different hypothetical returns depending on the purchase price of the Securities.

The following scenario analysis and examples assume an Initial Level of 980.00 and a Maximum Gain of 19.00% (the midpoint of the expected range of 17.00% to 21.00%, the actual Maximum Gain will be determined on the Trade Date), and reflect the Multiplier of 1.25.

Example 1 — The level of the Index increases from an Initial Level of 980.00 to a Final Level of 1,029.00. The Index Return is calculated as follows:

(1,029.00 – 980.00) / 980.00 = 5.00%

Because the Index Return is greater than zero, the Payment at Maturity for each $10.00 Principal Amount of Securities is calculated as the lesser of:

(A) $10.00 + ($10.00 × Index Return × Multiplier), and

(B) $10.00 + ($10.00 × Maximum Gain)

= the lesser of (A) $10.00 + ($10.00 × 5.00% × 1.25) and (B) $10.00 + ($10.00 × 19.00%)

= the lesser of (A) $10.00 + ($10.00 × 6.25%) and (B) $10.00 + ($10.00 × 19.00%)

=$10.00 + ($10.00 × 6.25%)

=$10.00 + $0.625

=$10.625

Because the Index Return of 5.00% multiplied by the Multiplier is less than the hypothetical Maximum Gain of 19.00%, for each $10.00 Principal Amount of Securities, HSBC will pay you $10.625, resulting in a total return on the Securities of 6.25% for purchases by brokerage accounts at $10.00 per $10.00 Principal Amount and 8.42% for purchases by advisory accounts at $9.80 per $10.00 Principal Amount.

Example 2 — The level of the Index increases from an Initial Level of 980.00 to a Final Level of 1,176.00. The Index Return is calculated as follows:

(1,176.00 – 980.00) / 980.00 = 20.00%

Because the Index Return is greater than zero, the Payment at Maturity for each $10.00 Principal Amount of Securities is calculated as the lesser of:

(A) $10.00 + ($10.00 × Index Return × Multiplier), and

(B) $10.00 + ($10.00 × Maximum Gain)

= the lesser of (A) $10.00 + ($10.00 × 20.00% × 1.25) and (B) $10.00 + ($10.00 × 19.00%)

= the lesser of (A) $10.00 + ($10.00 × 25.00%) and (B) $10.00 + ($10.00 × 19.00%)

=$10.00 + ($10.00 × 19.00%)

=$10.00 + $1.90

=$11.90

Because the Index Return of 20.00% multiplied by the Multiplier is greater than the hypothetical Maximum Gain of 19.00%, for each $10.00 Principal Amount of Securities, HSBC will pay you $11.90, the maximum payment on the Securities, resulting in a total return on the Securities of 19.00% for purchases by brokerage accounts at 10.00 per $10.00 Principal Amount and 21.43% for purchases by advisory accounts at $9.80 per $10.00 Principal Amount.

Example 3 — The level of the Index decreases from an Initial Level of 980.00 to a Final Level of 931.00. The Index Return is calculated as follows:

(931.00 – 980.00) / 980.00 = -5.00%

Because the Index Return is negative, but the Index's percentage decline of 5% is less than the Buffer of 10%, at maturity, for each $10.00 Principal Amount of Securities, HSBC will pay you the $10.00 Principal Amount, resulting in a zero percent return for purchases by brokerage accounts at 10.00 per $10.00 Principal Amount and a 2.04% return for purchases by advisory accounts at $9.80 per $10.00 Principal Amount.

Example 4 — The level of the Index decreases from an Initial Level of 980.00 to a Final Level of 784.00. The Index Return is calculated as follows:

(784.00 – 980.00) / 980.00 = -20.00%

Because the Index Return is negative and the Index's percentage decline of 20% is more than the Buffer of 10%, at maturity, for each $10.00 Principal Amount of Securities HSBC will pay you an amount equal to the Principal Amount reduced by 1% for every 1% by which the Index's percentage decline exceeds the Buffer, and the Payment at Maturity is calculated as follows:

$10.00 + [$10.00 × (Index Return + Buffer Amount)

=$10.00 + [$10.00 × (-20.00% + 10.00%)]

5

=$10.00 + [$10.00 × -10.00%]

=$10.00 - $1.00

=$9.00

In this scenario, the total loss on the Securities is 10% for purchases by brokerage accounts at 10.00 per $10.00 Principal Amount and 8.16% for purchases by advisory accounts at $9.80 per $10.00 Principal Amount.

Scenario Analysis – hypothetical Payment at Maturity for each $10.00 Principal Amount of Securities

|

Hypothetical Final Level

|

Hypothetical Index Return

|

Multiplier

|

Hypothetical Payment at Maturity

|

Hypothetical

Return on Securities Purchased at $10.00 (1)

|

Hypothetical Return on Securities Purchased at $9.80 by Advisory

Accounts (2)

|

|

1,960.00

|

100.00%

|

1.25

|

$11.900

|

19.00%

|

21.43%

|

|

1,862.00

|

90.00%

|

1.25

|

$11.900

|

19.00%

|

21.43%

|

|

1,764.00

|

80.00%

|

1.25

|

$11.900

|

19.00%

|

21.43%

|

|

1,666.00

|

70.00%

|

1.25

|

$11.900

|

19.00%

|

21.43%

|

|

1,568.00

|

60.00%

|

1.25

|

$11.900

|

19.00%

|

21.43%

|

|

1,470.00

|

50.00%

|

1.25

|

$11.900

|

19.00%

|

21.43%

|

|

1,372.00

|

40.00%

|

1.25

|

$11.900

|

19.00%

|

21.43%

|

|

1,274.00

|

30.00%

|

1.25

|

$11.900

|

19.00%

|

21.43%

|

|

1,176.00

|

20.00%

|

1.25

|

$11.900

|

19.00%

|

21.43%

|

|

1,128.96

|

15.20%

|

1.25

|

$11.900

|

19.00%

|

21.43%

|

|

1,078.00

|

10.00%

|

1.25

|

$11.250

|

12.50%

|

14.80%

|

|

1,029.00

|

5.00%

|

1.25

|

$10.625

|

6.25%

|

8.42%

|

|

1,004.50

|

2.50%

|

1.25

|

$10.313

|

3.13%

|

5.23%

|

|

980.00

|

0.00%

|

N/A

|

$10.000

|

0.00%

|

2.04%

|

|

955.50

|

-2.50%

|

N/A

|

$10.000

|

0.00%

|

2.04%

|

|

931.00

|

-5.00%

|

N/A

|

$10.000

|

0.00%

|

2.04%

|

|

882.00

|

-10.00%

|

N/A

|

$10.000

|

0.00%

|

2.04%

|

|

833.00

|

-15.00%

|

N/A

|

$9.500

|

-5.00%

|

-3.06%

|

|

784.00

|

-20.00%

|

N/A

|

$9.000

|

-10.00%

|

-8.16%

|

|

686.00

|

-30.00%

|

N/A

|

$8.000

|

-20.00%

|

-18.37%

|

|

588.00

|

-40.00%

|

N/A

|

$7.000

|

-30.00%

|

-28.57%

|

|

490.00

|

-50.00%

|

N/A

|

$6.000

|

-40.00%

|

-38.78%

|

|

392.00

|

-60.00%

|

N/A

|

$5.000

|

-50.00%

|

-48.98%

|

|

294.00

|

-70.00%

|

N/A

|

$4.000

|

-60.00%

|

-59.18%

|

|

196.00

|

-80.00%

|

N/A

|

$3.000

|

-70.00%

|

-69.39%

|

|

98.00

|

-90.00%

|

N/A

|

$2.000

|

-80.00%

|

-79.59%

|

|

0.00

|

-100.00%

|

N/A

|

$1.000

|

-90.00%

|

-89.80%

|

(1) This “Hypothetical Return on Securities” is the number, expressed as a percentage, that results from comparing the Payment at Maturity per $10 Principal Amount Security to the purchase price of $10 per Security for all brokerage accounts.

(2) This “Hypothetical Return on Securities” is the number, expressed as a percentage, that results from comparing the Payment at Maturity per $10 Principal Amount Security to the purchase price of $9.80 per Security, which is the purchase price for investors in certain advisory accounts. See "Supplemental Plan of Distribution (Conflicts of Interest)" on page 12 of this free writing prospectus.

6

|

Key Risks

|

An investment in the Securities involves significant risks. Some of the risks that apply to the Securities are summarized here, but we urge you to read the more detailed explanation of risks relating to the Securities generally in the “Risk Factors” section of the accompanying underlying supplement no. 3 and the accompanying prospectus supplement. We also urge you to consult your investment, legal, tax, accounting and other advisors before you invest in the Securities.

|

|

¨

|

Your Investment in the Securities May Result in a Loss: The Securities differ from ordinary debt securities in that HSBC is not necessarily obligated to repay the full Principal Amount of the Securities at maturity. The return on the Securities at maturity is linked to the performance of the Index and will depend on whether, and the extent to which, the Index Return is positive or negative. If the Index Return is negative and the Index 's percentage decline is more than 10%, HSBC will pay you less than your Principal Amount at maturity resulting in a loss of principal equal to the negative Index Return in excess of the 10% Buffer. Accordingly, you could lose up to 90% of the Principal Amount of the Securities.

|

|

|

¨

|

Buffered Downside Market Exposure Applies Only if You Hold the Securities to Maturity: You should be willing to hold your Securities to maturity. If you are able to sell your Securities in the secondary market, you may have to sell them at a loss even if the level of the Index has not declined by more than the Buffer.

|

|

|

¨

|

The Multiplier Applies Only if You Hold the Securities to Maturity: You should be willing to hold your Securities to maturity. If you are able to sell your Securities prior to maturity in the secondary market, the price you receive will likely not reflect the full economic value of the Multiplier or the Securities themselves, and the return you realize may be less than the Index’s return even if such return is positive and does not exceed the Maximum Gain. You can receive the full benefit of the Multiplier and earn the potential Maximum Gain from HSBC only if you hold your Securities to maturity.

|

|

|

¨

|

Maximum Gain: You will not participate in any increase in the level of the Index (as magnified by the Multiplier) beyond the Maximum Gain that will be between 17.00% and 21.00% (to be determined on the Trade Date), which could be significant. YOU WILL NOT RECEIVE A RETURN ON THE PRINCIPAL AMOUNT GREATER THAN THE MAXIMUM GAIN. As a result, your return on the Securities is limited and could be less than a hypothetical direct investment in the Index.

|

|

|

¨

|

No Interest Payments: HSBC will not make any interest payments in respect to the Securities.

|

|

|

¨

|

The Securities are Subject to the Credit Risk of the Issuer: The Securities are senior unsecured debt obligations of HSBC, and are not, either directly or indirectly, an obligation of any third party. As further described in the accompanying prospectus supplement and prospectus, the Securities will rank on par with all of the other unsecured and unsubordinated debt obligations of HSBC, except such obligations as may be preferred by operation of law. Any payment to be made on the Securities, including any repayment of principal at maturity, depends on the ability of HSBC to satisfy its obligations as they come due. As a result, the actual and perceived creditworthiness of HSBC may affect the market value of the Securities and, in the event HSBC were to default on its obligations, you may not receive amount owed to you under the terms of the Securities.

|

|

|

¨

|

The Securities Lack Liquidity: The Securities will not be listed on any securities exchange or quotation system. An affiliate of HSBC intends to offer to repurchase the Securities in the secondary market but is not required to do so and may cease any such market-making activities at any time without notice. Because other dealers are not likely to make a secondary market for the Securities, the price at which you may be able to trade your Securities is likely to depend on the price, if any, at which an affiliate of HSBC is willing to buy the Securities. This price, if any, will exclude any fees or commissions paid by brokerage account holders when the Securities were purchased and therefore will generally be lower than such purchase price.

|

|

|

¨

|

Owning the Securities is Not the Same as Owning the Stocks Comprising the Index: The return on your Securities may not reflect the return you would realize if you actually owned the stocks included in the Index. As a holder of the Securities, you will not have voting rights or rights to receive dividends or other distributions or other rights that holders of stocks included in the Index would have.

|

|

|

¨

|

Price Prior to Maturity: The market price of the Securities will be influenced by many factors including the level of the Index, volatilities, dividends, the time remaining to maturity of the Securities, interest rates, geopolitical conditions, economic, political, financial and regulatory or judicial events, and the creditworthiness of HSBC.

|

|

|

¨

|

Changes Affecting the Index: The policies of the reference sponsor concerning additions, deletions and substitutions of the stocks included in the Index and the manner in which the reference sponsor takes account of certain changes affecting those stocks included in the Index may adversely affect the level of the Index. The policies of the reference sponsor with respect to the calculation of the Index could also adversely affect the level of the Index. The reference sponsor may discontinue or suspend calculation or dissemination of the Index. Any such actions could have an adverse effect the value of the Securities.

|

|

|

¨

|

The Index Reflects Price Return, Not Total Return: The return on your Securities is based on the performance of the Index, which reflects the changes in the market prices of the component stocks underlying the Index. It is not, however, linked to a ‘total return’ index or strategy, which, in addition to reflecting those price returns, would also reflect dividends paid on the component stocks. The return on your Securities will not include such a total return feature or dividend component.

|

|

|

¨

|

Potential HSBC Impact on Price: Trading or transactions by HSBC USA Inc. or any of its affiliates in the stocks held by the Index or in futures, options, exchange-traded funds or other derivative products on the stocks held by the Index, may adversely affect the market value of the stocks held by the Index, and, therefore, the market value of the Securities.

|

|

|

¨

|

Impact of Fees on Secondary Market Prices: Generally, the price of the Securities in the secondary market, if any, is likely to be lower than the initial offering price since the issue price includes and the secondary market prices are likely to exclude hedging costs, and for brokerage accounts, commissions or other compensation paid with respect to the Securities.

|

|

|

¨

|

Potential Conflict of Interest: HSBC and its affiliates may engage in business with the issuers of the stocks comprising the Index, which may present a conflict between the obligations of HSBC and you, as a holder of the Securities. The Calculation Agent, who is

|

7

|

|

the issuer of the Securities, will determine the Payment at Maturity based on the observed Final Level. The Calculation Agent can postpone the determination of the Final Level or the Maturity Date if a market disruption event occurs and is continuing on the Final Valuation Date.

|

|

|

¨

|

Potentially Inconsistent Research, Opinions or Recommendations by HSBC, UBS or Their Respective Affiliates: HSBC, UBS Financial Services Inc., or any of their respective affiliates may publish research, express opinions or provide recommendations that are inconsistent with investing in or holding the Securities and such research, opinions or recommendations may be revised at any time. Any such research, opinions or recommendations could affect the price of the stocks included in the Index, and therefore, the market value of the Securities.

|

|

|

¨

|

The Securities are Not Insured by any Governmental Agency of the United States or any Other Jurisdiction: The Securities are not deposit liabilities or other obligations of a bank and are not insured by the Federal Deposit Insurance Corporation or any other governmental agency or program of the United States or any other jurisdiction. An investment in the Securities is subject to the credit risk of HSBC, and in the event that HSBC is unable to pay its obligations as they become due, you may not receive the full Payment at Maturity of the Securities.

|

|

|

¨

|

Uncertain Tax Treatment: There is no direct legal authority as to the proper tax treatment of the Securities, and therefore significant aspects of the tax treatment of the Securities are uncertain, as to both the timing and character of any inclusion in income in respect of the Securities. Under one reasonable approach, the Securities should be treated as pre-paid forward or other executory contracts with respect to the Index. HSBC intends to treat the Securities consistent with this approach and pursuant to the terms of the Securities, you agree to treat the Securities under this approach for all U.S. federal income tax purposes. Subject to certain limitations described in the accompanying prospectus supplement, and based on certain factual representations received from HSBC, in the opinion of HSBC’s special U.S. tax counsel, Sidley Austin llp, it is reasonable to treat the Securities in accordance with this approach. Pursuant to this approach, HSBC does not intend to report any income or gain with respect to the Securities prior to their maturity or an earlier sale or exchange and HSBC intends to treat any gain or loss upon maturity or an earlier sale or exchange as long-term capital gain or loss, provided that you have held the Security for more than one year at such time for U.S. federal income tax purposes. See "Certain U.S. Federal Income Tax Considerations — Certain Equity-Linked Notes — Certain Notes Treated as Forward Contracts or Executory Contracts" in the prospectus supplement for certain U.S. federal income tax considerations applicable to Securities that are treated as pre-paid cash-settled forward or other executory contracts. Because of the uncertainty regarding the tax treatment of the Securities, we urge you to consult your tax adviser as to the tax consequences of your investment in a Security.

|

In Notice 2008-2, the Internal Revenue Service (“IRS”) and the Treasury Department requested comments as to whether the purchaser of an exchange traded note or pre-paid forward contract (which may include the Securities) should be required to accrue income during its term under a mark-to-market, accrual or other methodology, whether income and gain on such a note or contract should be ordinary or capital, and whether foreign holders should be subject to withholding tax on any deemed income accrual. Accordingly, it is possible that regulations or other guidance could provide that a U.S. holder (as defined in the prospectus supplement) of a Security is required to accrue income in respect of the Security prior to the receipt of payments with respect to the Security or its earlier sale. Moreover, it is possible that any such regulations or other guidance could treat all income and gain of a U.S. holder in respect of a Security as ordinary income (including gain on a sale). Finally, it is possible that a non-U.S. holder (as defined in the prospectus supplement) of the Security could be subject to U.S. withholding tax in respect of a Security. It is unclear whether any regulations or other guidance would apply to the Securities (possibly on a retroactive basis). Prospective investors are urged to consult with their tax advisors regarding Notice 2008-2 and the possible effect to them of the issuance of regulations or other guidance that affects the U.S. federal income tax treatment of the Securities. For a more complete discussion of the U.S. federal income tax consequences of your investment in a Security, please see the discussion under “Certain U.S. Federal Income Tax Considerations” in the prospectus supplement.

8

|

Information about the S&P MidCap 400® Index (“MID”)

|

General

HSBC has derived all information relating to the MID, including, without limitation, its make-up, performance, method of calculation and changes in its components, from publicly available sources. That information reflects the policies of and is subject to change by Standard & Poor’s, a division of The McGraw-Hill Companies, Inc. (“S&P”). S&P is under no obligation to continue to publish, and may discontinue or suspend the publication of the MID at any time. The consequences of S&P discontinuing the MID are discussed in the accompanying underlying supplement no. 3.

S&P publishes the MID

The MID is comprised of 400 companies with mid-sized market capitalizations ranging from $850 million to $3.8 billion and covers over 7% of the United States equities market. The calculation of the value of the MID (discussed below in further detail) is based on the relative value of the aggregate Market Value (as defined below) of the common stocks of 400 companies as of a particular time compared to the aggregate average Market Value of the common stocks of 400 similar companies during the base period of June 28, 1991. Historically, the “Market Value” of any S&P component stock was calculated as the product of the market price per share and the number of the then-outstanding shares of such S&P component stock. As discussed below, during March 2005, S&P began to use a new methodology to calculate the Market Value of the S&P component stocks and S&P completed its transition to the new calculation methodology during September 2005.

S&P chooses companies for inclusion in the MID with the aim of achieving a distribution by broad industry groupings that approximates the distribution of these groupings in the common stock population of the Standard & Poor’s Stock Guide Database, which S&P uses as an assumed model for the composition of the total market. Relevant criteria employed by S&P include the viability of the particular company, the extent to which that company represents the industry group to which it is assigned, the extent to which the market price of that company’s common stock is generally responsive to changes in the affairs of the respective industry and the market value and trading activity of the common stock of that company. S&P may from time to time, in its sole discretion, add companies to, or delete companies from, the MID to achieve the objectives stated above.

Computation of the MID

Prior to March 2005, the Market Value of a component stock was calculated as the product of the market price per share and the total number of outstanding shares of the component stock. In March 2004, S&P announced that it would transition the MID to float-adjusted market capitalization weights. The transition began in March 2005 and was completed in September 2005. S&P’s criteria for selecting stock for the MID was not changed by the shift to float adjustment. However, the adjustment affects each company’s weight in the MID (i.e., its Market Value). Currently, S&P calculates the MID based on the total float-adjusted market capitalization of each component stock, where each stock’s weight in the MID is proportional to its float-adjusted Market Value.

Under float adjustment, the share counts used in calculating the MID reflect only those shares that are available to investors, not all of a company’s outstanding shares. S&P defines three groups of shareholders whose holdings are subject to float adjustment:

|

|

·

|

holdings by other publicly traded corporations, venture capital firms, private equity firms, strategic partners, or leveraged buyout groups;

|

|

|

·

|

holdings by government entities, including all levels of government in the U.S. or foreign countries; and

|

|

|

·

|

holdings by current or former officers and directors of the company, founders of the company, or family trusts of officers, directors, or founders, as well as holdings of trusts, foundations, pension funds, employee stock ownership plans, or other investment vehicles associated with and controlled by the company.

|

However, treasury stock, stock options, restricted shares, equity participation units, warrants, preferred stock, convertible stock, and rights are not part of the float. In cases where holdings in a group exceed 10% of the outstanding shares of a company, the holdings of that group are excluded from the float-adjusted count of shares to be used in the index calculation. Mutual funds, investment advisory firms, pension funds, or foundations not associated with the company and investment funds in insurance companies, shares of a U.S. company traded in Canada as “exchangeable shares,” shares that trust beneficiaries may buy or sell without difficulty or significant additional expense beyond typical brokerage fees, and, if a company has multiple classes of stock outstanding, shares in an unlisted or non-traded class if such shares are convertible by shareholders without undue delay and cost, are also part of the float.

For each stock, an investable weight factor (“IWF”) is calculated by dividing the available float shares, defined as the total shares outstanding less shares held in one or more of the three groups listed above where the group holdings exceed 10% of the outstanding shares, by the total shares outstanding. The float-adjusted index is then calculated by dividing the sum of the IWF multiplied by both the price and the total shares outstanding for each stock by an index divisor (the “Divisor”). For companies with multiple classes of stock, S&P calculates the weighted average IWF for each stock using the proportion of the total company market capitalization of each share class as weights.

As of the date of this document, the MID is calculated using a base-weighted aggregate methodology: the level of the MID reflects the total Market Value of all the component stocks relative to the MID base date of June 28, 1991. The daily calculation of the MID is computed by dividing the Market Value of the MID component stocks by the Divisor.

The MID maintenance includes monitoring and completing the adjustments for additions and deletions of the constituent companies, share changes, stock splits, stock dividends and stock price adjustments due to company restructurings or spin-offs. Continuity in index values is maintained by adjusting the Divisor for all changes in the MID constituents’ share capital after the base date of June 28, 1991 with the index value as of the base date set at 100. Some corporate actions, such as stock splits and stock dividends do not require Divisor adjustments because following a stock split or stock dividend, both the stock price and number of shares outstanding are adjusted by S&P so that there is no change in the Market Value of the component stock. All stock split and dividend adjustments are made after the close of trading on the day before the ex-date.

To prevent the level of the MID from changing due to corporate actions, all corporate actions which affect the total Market Value of the MID require a Divisor adjustment. By adjusting the Divisor for the change in total Market Value, the level of the MID remains constant. This helps maintain the level of the MID as an accurate barometer of stock market performance and ensures that the movement of the

9

MID does not reflect the corporate actions of individual companies in the MID. All Divisor adjustments are made after the close of trading and after the calculation of the closing levels of the MID. Some corporate actions, such as stock splits and stock dividends, require simple changes in the common shares outstanding and the stock prices of the companies in the MID and do not require Divisor adjustments.

The table below summarizes the types of index maintenance adjustments and indicates whether or not a Divisor adjustment is required.

|

Type of Corporate Action

|

Comments

|

Divisor

Adjustment

|

|

Company added/deleted

|

Net change in market value determines Divisor adjustment.

|

Yes

|

|

Change in shares outstanding

|

Any combination of secondary issuance, share repurchase or buy back—share counts revised to reflect change.

|

Yes

|

|

Stock split

|

Share count revised to reflect new count. Divisor adjustment is not required since the share count and price changes are offsetting.

|

No

|

|

Spin-off

|

If spun-off company is not being added to the index, the divisor adjustment reflects the decline in Index Market Value (i.e., the value of the spun-off unit).

|

Yes

|

|

Spin-off

|

Spun-off company added to the MID, no company removed from the MID.

|

No

|

|

Spin-off

|

Spun-off company added to the MID, another company removed to keep number of names fixed. Divisor adjustment reflects deletion.

|

Yes

|

|

Change in IWF

|

Increasing (decreasing) the IWF increases (decreases) the total market value of the index. The Divisor change reflects the change in market value caused by the change to an IWF.

|

Yes

|

|

Special dividend

|

When a company pays a special dividend the share price is assumed to drop by the amount of the dividend; the divisor adjustment reflects this drop in Index Market Value.

|

Yes

|

|

Rights offering

|

Each shareholder receives the right to buy a proportional number of additional shares at a set (often discounted) price. The calculation assumes that the offering is fully subscribed. Divisor adjustment reflects increase in market cap measured as the shares issued multiplied by the price paid.

|

Yes

|

Each of the corporate events exemplified in the table requiring an adjustment to the Divisor has the effect of altering the Market Value of the component stock and consequently of altering the aggregate Market Value of the MID component stocks (the “Post-Event Aggregate Market Value”). In order that the level of the MID (the “Pre-Event Index Value”) not be affected by the altered Market Value (whether increase or decrease) of the affected component stock, a new Divisor (“New Divisor”) is derived as follows:

|

Post-Event Aggregate Market Value

|

=

|

Pre-Event Index Value

|

|

New Divisor

|

|

New Divisor

|

=

|

Post-Event Aggregate Market Value

|

|

Pre-Event Index Value

|

A large part of the MID maintenance process involves tracking the changes in the number of shares outstanding of each of the companies whose stocks are included in the MID. Four times a year, on a Friday close to the end of each calendar quarter, the share totals of companies in the MID are updated as required by any changes in the number of shares outstanding and then the index divisor is adjusted accordingly. In addition, changes in a company’s shares outstanding of 5% or more due to mergers, acquisitions, public offerings, private placements, tender offers, Dutch auctions or exchange offers are made as soon as reasonably possible. Other changes of 5% or more (due to, for example, company stock repurchases, redemptions, exercise of options, warrants, conversion of preferred stock, notes, debt, equity participations or other recapitalizations) are made weekly, and are announced on Wednesdays for implementation after the close of trading on the following Wednesday. If a 5% or more change causes a company’s IWF to change by 5 percentage points or more (for example from 0.80 to 0.85), the IWF will be updated at the same time as the share change, except IWF changes resulting from partial tender offers will be considered on a case-by-case basis. Changes to an IWF of less than 5 percentage points are implemented at the next IWF review, which occurs annually. In the case of certain rights issuances, in which the number of rights issued and/or terms of their exercise are deemed substantial, a price adjustment and share increase may be implemented immediately.

License Agreement with S&P

HSBC has entered into a nonexclusive license agreement providing for the license to it, in exchange for a fee, of the right to use indices owned and published by S&P in connection with some products, including the Securities.

The Securities are not sponsored, endorsed, sold or promoted by S&P or its third party licensors. Neither S&P nor its third party licensors

10

make any representation or warranty, express or implied, to the owners of the Securities or any member of the public regarding the advisability of investing in securities generally or in the Securities particularly or the ability of the MID to track general stock market performance. S&P's and its third party licensor’s only relationship to HSBC USA Inc. is the licensing of certain trademarks and trade names of S&P and the third party licensors and of the MID which is determined, composed and calculated by S&P or its third party licensors without regard to HSBC USA Inc. or the Securities. S&P and its third party licensors have no obligation to take the needs of HSBC USA Inc. or the owners of the Securities into consideration in determining, composing or calculating the SPX. Neither S&P nor its third party licensors is responsible for or has participated in the determination of the prices and amount of the Securities or the timing of the issuance or sale of the Securities or in the determination or calculation of the equation by which the Securities are to be converted into cash. S&P has no obligation or liability in connection with the administration, marketing or trading of the Securities.

NEITHER STANDARD & POOR’S, ITS AFFILIATES NOR THEIR THIRD PARTY LICENSORS GUARANTEE THE ADEQUACY, ACCURACY, TIMELINESS OR COMPLETENESS OF THE INDEX OR ANY DATA INCLUDED THEREIN OR ANY COMMUNICATIONS, INCLUDING BUT NOT LIMITED TO, ORAL OR WRITTEN COMMUNICATIONS (INCLUDING ELECTRONIC COMMUNICATIONS) WITH RESPECT THERETO. STANDARD & POOR’S, ITS AFFILIATES AND THEIR THIRD PARTY LICENSORS SHALL NOT BE SUBJECT TO ANY DAMAGES OR LIABILITY FOR ANY ERRORS, OMISSIONS OR DELAYS THEREIN. STANDARD & POOR’S MAKES NO EXPRESS OR IMPLIED WARRANTIES, AND EXPRESSLY DISCLAIMS ALL WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE WITH RESPECT TO THE MARKS, THE INDEX OR ANY DATA INCLUDED THEREIN. WITHOUT LIMITING ANY OF THE FOREGOING, IN NO EVENT WHATSOEVER SHALL STANDARD & POOR’S, ITS AFFILIATES OR THEIR THIRD PARTY LICENSORS BE LIABLE FOR ANY INDIRECT, SPECIAL, INCIDENTAL, PUNITIVE OR CONSEQUENTIAL DAMAGES, INCLUDING BUT NOT LIMITED TO, LOSS OF PROFITS, TRADING LOSSES, LOST TIME OR GOODWILL, EVEN IF THEY HAVE BEEN ADVISED OF THE POSSIBILITY OF SUCH DAMAGES, WHETHER IN CONTRACT, TORT, STRICT LIABILITY OR OTHERWISE.

“Standard & Poor’s®”, “S&P®” and “S&P MidCap 400®” are trademarks of Standard and Poor’s and have been licensed for use by HSBC USA Inc.

Historical Performance of the MID

The following graph sets forth the historical performance of the MID based on the daily historical closing levels from June 30, 2006 to June 30, 2011 as reported on Bloomberg Professional® service. We make no representation or warranty as to the accuracy or completeness of the information obtained from Bloomberg Professional® service. The historical levels of the MID should not be taken as an indication of future performance.

Source: Bloomberg Professional® service

The Closing Level of the MID on June 30, 2011 was 978.64.

|

Events of Default and Acceleration

|

If the Securities have become immediately due and payable following an event of default (as defined in the accompanying prospectus) with respect to the Securities, the Calculation Agent will determine the accelerated Payment at Maturity due and payable in the same general manner as described in “Indicative Terms” in this free writing prospectus. In that case, the scheduled trading day preceding the date of acceleration will be used as the Final Valuation Date for purposes of determining the accelerated Index Return. If a market disruption event exists on that scheduled trading day, then the accelerated Final Valuation Date will be postponed for up to five scheduled trading days (in the same general manner used for postponing the originally scheduled Final Valuation Date). The accelerated Maturity Date will be the fifth business day following the postponed accelerated Final Valuation Date.

If the Securities have become immediately due and payable following an event of default, you will not be entitled to any additional payments with respect to the Securities. For more information, see “Description of Debt Securities — Events of Default” and “— Events of Default; Defaults” in the accompanying prospectus.

11

|

Supplemental Plan of Distribution (Conflicts of Interest)

|

Pursuant to the terms of a distribution agreement, HSBC Securities (USA) Inc., an affiliate of ours, will purchase the Securities from us for distribution to UBS Financial Services Inc. (the “Agent”). We will agree to sell to the Agent, and the Agent will agree to purchase, all of the Securities at the price indicated on the cover of the pricing supplement, the document that will be filed pursuant to Rule 424(b)(2) containing the final pricing terms of the Securities. We have agreed to indemnify the Agent against liabilities, including liabilities under the Securities Act of 1933, as amended, or to contribute to payments that the Agent may be required to make relating to these liabilities as described in the accompanying prospectus supplement and the prospectus. The price to public for all purchases of Securities in brokerage accounts is $10.00 per Security. The Agent may allow a concession not in excess of the underwriting discount set forth on the cover of the pricing supplement to its affiliates for distribution of the Securities to such brokerage accounts. The Agent will act as placement agent for sales to certain advisory accounts at a purchase price to such accounts of $9.80 per Security, and will not receive a sales commission with respect to such sales.

Subject to regulatory constraints, HSBC (or an affiliate thereof) intends to offer to purchase the Securities in the secondary market, but is not required to do so. We or our affiliate will enter into swap agreements or related hedge transactions with one of our other affiliates or unaffiliated counterparties, which may include the Agent, in connection with the sale of the Securities and the Agent and/or an affiliate may earn additional income as a result of payments pursuant to the swap or related hedge transactions.

In addition, HSBC Securities (USA) Inc. or another of its affiliates or agents may use the pricing supplement to which this free writing prospectus relates in market-making transactions after the initial sale of the Securities, but is under no obligation to do so and may discontinue any market-making activities at any time without notice.

See “Supplemental Plan of Distribution” on page S-52 in the accompanying prospectus supplement. All references to NASD Rule 2720 in the prospectus supplement shall be to FINRA Rule 5121.

12