Filed Pursuant to Rule 433

Registration No. 333-158385

May 23, 2011

FREE WRITING PROSPECTUS

(To Prospectus dated April 2, 2009 and

Prospectus Supplement dated April 9, 2009)

HSBC USA Inc.

EM Currency Accelerated Return Securities (“CARS”)

|

}

|

CARS linked to a basket of:

|

– Brazilian Real, Indian Rupee and Chinese Renminbi (Yuan)

|

}

|

2-year maturity

|

|

}

|

90% return of principal at maturity, subject to the credit risk of HSBC USA Inc.

|

|

}

|

Between 160% and 190% exposure to any positive Basket Return (to be determined on the Pricing Date)

|

The EM Currency Accelerated Return Securities (“CARS” or each a “security” and collectively the “securities") offered hereunder are not deposit liabilities or other obligations of a bank and are not insured by the Federal Deposit Insurance Corporation or any other governmental agency of the United States or any other jurisdiction and include investment risks including possible loss of the Principal Amount invested due to the credit risk of HSBC USA Inc.

The CARS will not be listed on any U.S. securities exchange or automated quotation system.

Neither the U.S. Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of the securities or passed upon the accuracy or the adequacy of this document, the accompanying prospectus or prospectus supplement. Any representation to the contrary is a criminal offense. We have appointed HSBC Securities (USA) Inc., an affiliate of ours, as the agent for the sale of the securities. HSBC Securities (USA) Inc. will purchase the securities from us for distribution to other registered broker dealers or will offer the securities directly to investors. We may use this free writing prospectus in the initial sale of securities. In addition, HSBC Securities (USA) Inc. or another of its affiliates or agents may use the pricing supplement to which this free writing prospectus relates in market-making transactions in any securities after their initial sale. Unless we or our agent informs you otherwise in the confirmation of sale, the pricing supplement to which this free writing prospectus relates is being used in a market-making transaction. See “Supplemental Plan of Distribution (Conflicts of Interest)” on page FWP-16 of this free writing prospectus.

Investment in the securities involves certain risks. You should refer to “Selected Risk Considerations” beginning on page FWP-7 of this free writing prospectus and page S-3 of the accompanying prospectus supplement.

|

Price to Public

|

Fees and Commissions1

|

Proceeds to Issuer

|

|

|

Per security

|

$1,000

|

||

|

Total

|

1HSBC USA Inc. or one of our affiliates may pay varying discounts and commissions of up to 2.30% per $1,000 Principal Amount of securities in connection with the distribution of the securities, which may consist of selling concessions of up to 2.30% and fees of up to 0.80%. See “Supplemental Plan of Distribution (Conflicts of Interest)” on page FWP-16 of this free writing prospectus.

HSBC USA Inc.

EM Currency Accelerated Return Securities (“CARS”)

This FWP relates to an offering of CARS by HSBC USA Inc. linked to the performance of a basket of three currencies as indicated below.

Indicative Terms*

|

Principal Amount

|

$1,000 per security

|

|

Term

|

2 years

|

|

Basket Currencies

|

Brazilian Real (“BRL”), Indian Rupee (“INR”) and Chinese Renminbi (Yuan) (“CNY”) (each, a “Basket Currency”)

|

|

Payment at Maturity per security

|

If the Basket Return is positive, you will receive a cash payment per $1,000 Principal Amount of securities, equal to: $1,000 + ($1,000 × Basket Return × Upside Participation Rate).

If the Basket Return is zero or negative, you will receive a cash payment per $1,000 Principal Amount of securities, equal to the greater of:

(a) $900; and

(b) $1,000 + ($1,000 × Basket Return).

|

|

Basket Return

|

[(BRL Return × 1/3) + (INR Return × 1/3) + (CNY Return × 1/3)]

|

|

Upside Participation Rate

|

Between 160% and 190% (1.6x – 1.9x) exposure to any positive Basket Return (to be determined on the Pricing Date)

|

|

Currency Performance

|

Initial Spot Rate – Final Spot Rate

Initial Spot Rate

|

|

Trade Date

|

June 15, 2011

|

|

Pricing Date

|

June 16, 2011

|

|

Settlement Date

|

June 21, 2011

|

|

Final Valuation Date

|

June 17, 2013†

|

|

Maturity Date

|

June 20, 2013†

|

|

CUSIP

|

4042K1HW6

|

* As more fully described beginning on page FWP-4.

†Subject to postponement as described in “Market Disruption Events.”

The CARS

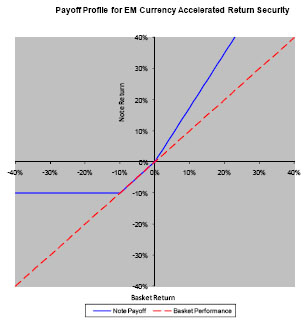

The CARS are designed for investors who seek exposure to the potential appreciation of an equally weighted basket of emerging market currencies (the “Basket”) consisting of the Brazilian Real, the Indian Rupee and the Chinese Renminbi (Yuan) relative to the U.S. Dollar.

At maturity, if the Basket has appreciated, you will realize a return equal to 160% to 190% (to be determined on the Pricing Date) of the appreciation of the Basket. However, if the Basket has declined, you may lose up to 10% of your Principal Amount at maturity.

|

The offering period for the CARS is through June 15, 2011

|

FWP-2

|

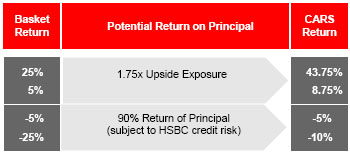

Payoff Example

The table to the right shows the hypothetical payout profile of an investment in the CARS assuming a 175% (1.75x) Upside Participation Rate (the actual Upside Participation Rate will be determined on the Pricing Date and will not be less than 160% or greater than 190%).

|

|

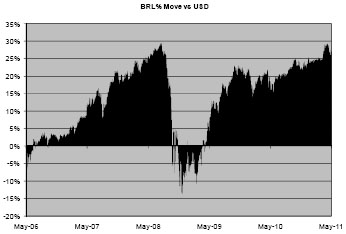

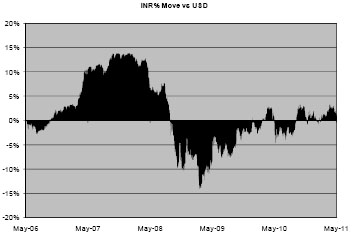

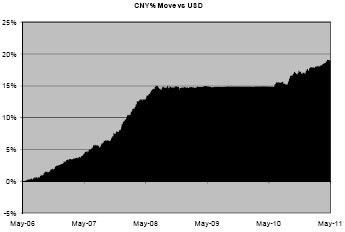

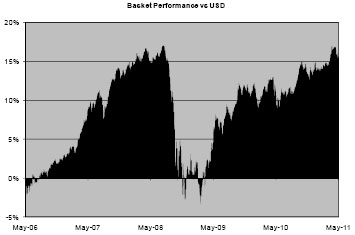

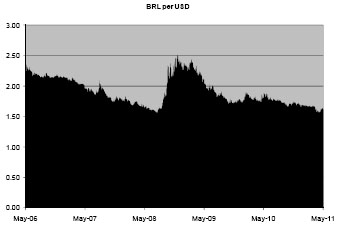

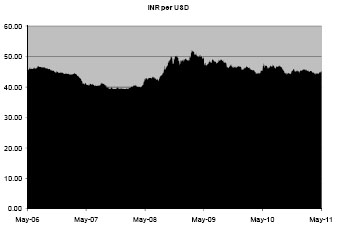

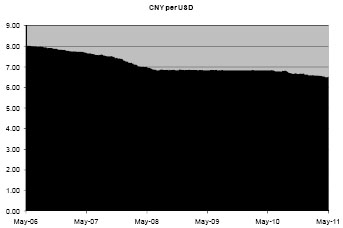

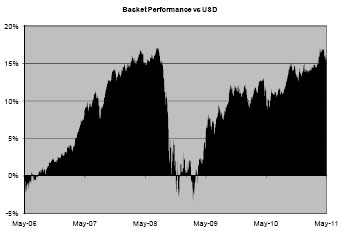

Historical Percentage Movement of Each Basket Currency and the Basket

|

Brazilian Real

|

Indian Rupee

|

|

|

|

Chinese Renminbi (Yuan)

|

Basket

|

|

|

The first three graphs above reflect the daily percentage movement of each Basket Currency relative to the value of the U.S. Dollar on May 19, 2006 over the past five years. The last graph above shows the hypothetical daily performance of the Basket from May 19, 2006 through May 19, 2011, assuming that each Basket Currency had a 1/3 weight in the Basket on that date and that the historical exchange rates of each Basket Currency on the relevant dates were the Spot Rates on such dates. The foregoing graphs and their corresponding data are resented for illustrative purposes only. The information in the graphs above was obtained from Bloomberg Financial Markets, which may be different than the information provided on the relevant Reuters pages. Past performance is not indicative of future performance. See “Historical Information” beginning on FWP-15 for the actual historical daily exchange rates, as shown on Bloomberg Financial Markets, of each Basket Currency from May 19, 2006 to May 19, 2011.

FWP-3

|

HSBC USA Inc.

EM Currency Accelerated Return Securities (“CARS”)

due June 20, 2013 |

The offering of EM Currency Accelerated Return Securities due June 20, 2013 (the “CARS”) will have the terms described in this free writing prospectus and the accompanying prospectus supplement and prospectus. If the terms of the securities offered hereby are inconsistent with those described in the accompanying prospectus supplement or prospectus, the terms described in this free writing prospectus shall control. In reviewing the accompanying prospectus supplement, all references to “Reference Asset” therein shall refer to the Basket (as defined below).

This free writing prospectus relates to a single offering of securities. The purchaser of a security will acquire a senior unsecured debt security of HSBC USA Inc. linked to the Basket as described below. The following key terms relate to the offering of these securities:

|

Issuer:

|

HSBC USA Inc.

|

|

Issuer Rating:

|

AA- (S&P), A1 (Moody’s), AA (Fitch)†

|

|

Principal Amount:

|

$1,000 per security

|

|

Basket:

|

The securities are linked to an equally weighted basket consisting of three currencies that measures the performance of such currencies relative to the U.S. Dollar.

|

|

Basket Currency

|

Fixing Source

|

Initial Spot Rate

|

Basket Currency Performance

Weighting |

|

Brazilian Real

|

BRL PTAX at Reuters Page BRFR

|

1/3

|

|

|

Indian Rupee

|

INR RBIB at Reuters Page RBIB

|

1/3

|

|

|

Chinese Renminbi (Yuan)

|

CNY SAEC at Reuters Page SAEC

|

1/3

|

|

Reference Currency:

|

U.S. Dollar (“USD”)

|

|

Payment at Maturity:

|

If the Basket Return is positive, you will receive a cash payment per $1,000 Principal Amount of securities, equal to: $1,000 + ($1,000 × Basket Return × Upside Participation Rate).

If the Basket Return is zero or negative, you will receive a cash payment per $1,000 Principal Amount of securities, equal to the greater of:

(a) $900; and

(b) $1,000 + ($1,000 × Basket Return).

|

|

Upside Participation Rate:

|

Between 160% and 190% (to be determined on the Pricing Date)

|

|

Basket Return:

|

[(BRL Return × 1/3) + (INR Return × 1/3) + (CNY Return × 1/3)]

The BRL Return, INR Return and CNY Return refer to the Currency Performance for the Brazilian Real, Indian Rupee and Chinese Renminbi (Yuan), respectively, relative to the USD over the term of the securities.

|

|

Currency Performance:

|

With respect to each Basket Currency, the performance of the respective Basket Currency from the Initial Spot Rate to the Final Spot Rate, relative to the Initial Spot Rate, calculated as follows:

Initial Spot Rate – Final Spot Rate

Initial Spot Rate

|

|

Spot Rate:

|

The Spot Rate, as determined by the Calculation Agent by reference to the Spot Rate definitions set forth in this free writing prospectus under “Spot Rates,” will be the U.S. Dollar/Basket Currency spot rate (representing the applicable Basket Currency that can be exchanged for one U.S. Dollar) at 6:00 p.m. São Paulo time for the BRL, at 12:30 p.m. Mumbai time for the INR and at 9:15 a.m. Beijing time for the CNY, expressed as the amount of foreign currency per one U.S. Dollar, which appears on the relevant Reuters page or any successor page. The Spot Rates are subject to the provisions set forth under “Market Disruption Events” in this free writing prospectus.

|

|

Initial Spot Rate:

|

For each Basket Currency, the Spot Rate on the Pricing Date.

|

|

Final Spot Rate:

|

For each Basket Currency, the Spot Rate on the Final Valuation Date.

|

|

Trade Date:

|

June 15, 2011

|

|

Pricing Date:

|

June 16, 2011

|

|

Settlement Date:

|

June 21, 2011

|

FWP-4

|

Final Valuation Date:

|

June 17, 2013. The Final Valuation Date is subject to postponement in the event of a market disruption event as described under “Market Disruption Events” in this free writing prospectus.

|

|

Maturity Date:

|

3 business days after the Final Valuation Date, which is expected to be June 20, 2013. The Maturity Date is subject to postponement in the event of a market disruption event as described under “Market Disruption Events” in this free writing prospectus.

|

|

Calculation Agent:

|

HSBC USA Inc.

|

|

Listing:

|

The securities will not be listed on any U.S. securities exchange or quotation system.

|

|

CUSIP / ISIN:

|

4042K1HW6 /

|

|

Form of Securities:

|

Book-Entry

|

† A credit rating reflects the creditworthiness of HSBC USA Inc. and is not a recommendation to buy, sell or hold securities, and it may be subject to revision or withdrawal at any time by the assigning rating organization. The securities themselves have not been independently rated. Each rating should be evaluated independently of any other rating.

FWP-5

GENERAL

This free writing prospectus relates to a single security offering linked to the Basket identified on the cover page. The purchaser of a security will acquire a senior unsecured debt security linked to the Basket. We reserve the right to withdraw, cancel or modify any offering and to reject orders in whole or in part. Although the security offering relates only to the Basket identified on the cover page, you should not construe that fact as a recommendation as to the merits of acquiring an investment linked to the Basket or any Basket Currency or as to the suitability of an investment in the securities.

You should read this document together with the prospectus dated April 2, 2009 and the prospectus supplement dated April 9, 2009. If the terms of the securities offered hereby are inconsistent with those described in the accompanying prospectus supplement or prospectus, the terms described in this free writing prospectus shall control. You should carefully consider, among other things, the matters set forth in “Selected Risk Considerations” beginning on page FWP-7 of this free writing prospectus and “Risk Factors” on page S-3 of the prospectus supplement, as the securities involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting and other advisors before you invest in the securities. As used herein, references to the “Issuer”, “HSBC”, “we”, “us” and “our” are to HSBC USA Inc.

HSBC has filed a registration statement (including a prospectus and a prospectus supplement) with the SEC for the offering to which this free writing prospectus relates. Before you invest, you should read the prospectus and prospectus supplement in that registration statement and other documents HSBC has filed with the SEC for more complete information about HSBC and this offering. You may get these documents for free by visiting EDGAR on the SEC’s web site at www.sec.gov. Alternatively, HSBC Securities (USA) Inc. or any dealer participating in this offering will arrange to send you the prospectus and prospectus supplement if you request them by calling toll-free 1-866-811-8049.

You may also obtain:

|

•

|

the prospectus supplement at www.sec.gov/Archives/edgar/data/83246/000114420409019785/v145824_424b2.htm

|

|

•

|

We are using this free writing prospectus to solicit from you an offer to purchase the securities. You may revoke your offer to purchase the securities at any time prior to the time at which we accept your offer by notifying HSBC Securities (USA) Inc. We reserve the right to change the terms of, or reject any offer to purchase, the securities prior to their issuance. In the event of any material changes to the terms of the securities, we will notify you.

TRUSTEE

Notwithstanding anything contained in the accompanying prospectus supplement to the contrary, the securities will be issued under the senior indenture dated March 31, 2009, between HSBC USA Inc., as Issuer, and Wells Fargo Bank, National Association, as trustee. Such indenture has substantially the same terms as the indenture described in the accompanying prospectus supplement.

PAYING AGENT

Notwithstanding anything contained in the accompanying prospectus supplement or product supplement to the contrary, HSBC Bank USA, N.A. will act as paying agent with respect to the securities pursuant to a Paying Agent and Securities Registrar Agreement dated June 1, 2009, between HSBC USA Inc. and HSBC Bank USA, N.A.

CALCULATION AGENT

We or one of our affiliates will act as calculation agent with respect to the securities.

SELECTED PURCHASE CONSIDERATIONS

Partial preservation of capital at maturity.

You will receive at least 90% of the Principal Amount of your securities, subject to the credit risk of HSBC, if you hold the securities to maturity, regardless of the performance of the Basket. You should be willing to lose up to 10% of your initial investment. Because the securities are our senior unsecured debt obligations, payment of any amount at maturity is subject to our ability to pay our obligations as they become due.

FWP-6

Diversification among the Basket Currencies.

The return on the securities is linked to the performance of a basket of three currencies, which we refer to as the Basket Currencies, relative to the U.S. Dollar, and will enable you to participate in any appreciation of the Basket Currencies relative to the U.S. Dollar, during the term of the securities. Accordingly, the level of the Basket increases if the Basket Currencies appreciate in value relative to the U.S. Dollar. The Basket derives its value from an equally weighted group of currencies consisting of the Brazilian Real, the Indian Rupee and the Chinese Renminbi (Yuan).

You will receive the Basket Return multiplied by the Upside Participation Rate if the Basket Return is positive at maturity.

At maturity, if the Basket Return is positive, you will receive a cash payment per $1,000 Principal Amount of securities, equal to $1,000 + ($1,000 × Basket Return × Upside Participation Rate). The Upside Participation Rate will be between 160% and 190% and will be determined on the Pricing Date.

SELECTED RISK CONSIDERATIONS

An investment in the securities involves significant risks. Investing in the securities is not equivalent to investing directly in one or more of the Basket Currencies. These risks are explained in more detail in the “Risk Factors” section of the accompanying prospectus supplement. You should understand the risks of investing in the securities and should reach an investment decision only after careful consideration, with your advisors, of the suitability of the securities in light of your particular financial circumstances and the information set forth in this free writing prospectus and the accompanying prospectus and prospectus supplement.

Your investment in the securities may result in a loss.

The securities do not guarantee the full return of your investment. The return on the securities at maturity is linked to the performance of the Basket Currencies relative to the U.S. Dollar and will depend on whether, and the extent to which, the Basket Return is positive or negative. Because the securities provide for only a 90% return of principal (subject to HSBC credit risk), you will receive less than your initial investment at maturity if the Basket Return is negative.

The securities do not pay interest.

You will not receive periodic or other interest payments on the securities during the term of the securities.

The securities are subject to the credit risk of HSBC USA Inc.

The securities are senior unsecured debt obligations of the issuer, HSBC, and are not, either directly or indirectly, an obligation of any third party. As further described in the accompanying prospectus supplement and prospectus, the securities will rank on par with all of the other unsecured and unsubordinated debt obligations of HSBC, except such obligations as may be preferred by operation of law. Any payment to be made on the securities, including any return of principal at maturity, depends on the ability of HSBC to satisfy its obligations as they come due. As a result, the actual and perceived creditworthiness of HSBC may affect the market value of the securities and, in the event HSBC were to default on its obligations, you may not receive the amounts owed to you under the terms of the securities.

The securities are not insured or guaranteed by any governmental agency of the United States or any other jurisdiction.

The securities are not deposit liabilities or other obligations of a bank and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency or program of the United States or any other jurisdiction. An investment in the securities is subject to the credit risk of HSBC, and in the event that HSBC is unable to pay its obligations as they become due, you may not receive the full Payment at Maturity of the securities.

Investing in the securities is not equivalent to investing directly in the Basket Currencies.

You may receive a lower Payment at Maturity than you would have received if you had invested directly in the Basket Currencies. In addition, the Basket Return is based on the Currency Performances for each of the Basket Currencies, which is in turn based upon the formula set forth above. The Currency Performances are dependent solely on such stated formula and not on any other formula that could be used for calculating currency performances. As such, the Currency Performance of each Basket Currency may be materially different from the return on a direct investment in the respective Basket Currency.

FWP-7

Certain built-in costs are likely to adversely affect the value of the securities prior to maturity.

While the Payment at Maturity described in this free writing prospectus is based on the full Principal Amount of your securities, the original issue price of the securities includes the placement agent’s commission and the estimated cost of hedging our obligations under the securities through one or more of our affiliates. As a result, the price, if any, at which HSBC Securities (USA) Inc. will be willing to purchase securities from you in secondary market transactions, if at all, will likely be lower than the original issue price, and any sale of securities by you prior to the maturity date could result in a substantial loss to you.

The securities are not designed to be short-term trading instruments.

The securities are not designed to be short-term trading instruments. Accordingly, you should be willing and able to hold your securities to maturity.

Gains in the Currency Performance of one or more Basket Currencies may be offset by losses in the Currency Performance of other Basket Currencies.

The securities are linked to the performance of the Basket, which is composed of the three Basket Currencies with equal weightings. The performance of the Basket will be based on the appreciation or depreciation of the Basket as a whole. Therefore, positive Currency Performances of one or more Basket Currencies may be offset, in whole or in part, by negative Currency Performances of one or more other Basket Currencies of equal or greater magnitude, which may result in an aggregate Basket Return equal to or less than zero. The performance of the Basket is dependent on the Currency Performance of each Basket Currency, which is in turn based upon the formula set forth above.

Currency markets may be volatile.

Currency markets may be highly volatile, particularly in relation to emerging or developing nations’ currencies, and, in certain market conditions, also in relation to developed nations’ currencies. Significant changes, including changes in liquidity and prices, can occur in such markets within very short periods of time. Foreign currency rate risks include, but are not limited to, convertibility risk and market volatility and potential interference by foreign governments through regulation of local markets, foreign investment or particular transactions in foreign currency. These factors may affect the levels of the Basket Currencies and the value of your securities in varying ways, and different factors may cause the levels of the Basket Currencies and the volatility of their prices to move in inconsistent directions at inconsistent rates.

Legal and regulatory risks.

Legal and regulatory changes could adversely affect currency rates. In addition, many governmental agencies and regulatory organizations are authorized to take extraordinary actions in the event of market emergencies. It is not possible to predict the effect of any future legal or regulatory action relating to currency rates, but any such action could cause unexpected volatility and instability in currency markets with a substantial and adverse effect on the performance of the Basket Currencies and, consequently, the value of the securities.

The securities are subject to emerging markets’ political and economic risks.

All of the Basket Currencies are the currencies of emerging market countries. Emerging market countries are more exposed to the risk of swift political change and economic downturns than their industrialized counterparts. In recent years, emerging markets have undergone significant political, economic and social change. Such far-reaching political changes have resulted in constitutional and social tensions, and, in some cases, instability and reaction against market reforms have occurred. With respect to any emerging or developing nation, there is the possibility of nationalization, expropriation or confiscation, political changes, government regulation and social instability. There can be no assurance that future political changes will not adversely affect the economic conditions of an emerging or developing-market nation. Political or economic instability is likely to have an adverse effect on the performance of the Basket Currencies, and, consequently, the return on the securities.

The exchange rate of the Chinese Renminbi (Yuan) is currently managed by the Chinese government.

The U.S. Dollar/Chinese Renminbi (Yuan) exchange rate is managed by the Chinese government to float within a narrow band with reference to a basket of currencies and is based on a daily poll of onshore market dealers and other undisclosed factors. The People’s Bank of China, the monetary authority in China, may also use a variety of techniques, such as imposition of regulatory controls or taxes, to affect the U.S. Dollar/Chinese Renminbi (Yuan) exchange rate. The People’s Bank has stated that it will make adjustments of the Chinese Renminbi (Yuan) exchange rate band when necessary according to market developments as well as the economic and financial situation. In the future, the Chinese government may also issue a new

FWP-8

currency to replace its existing currency or alter the exchange rate or relative exchange characteristics by devaluation or revaluation of the Chinese Renminbi (Yuan) in ways that may be adverse to your interests.

The Chinese government continues to manage the valuation of the Chinese Renminbi (Yuan), and, as currently managed, its price movements may not contribute significantly to either an increase or decrease in the CNY Spot Rate. If the exchange rate of the Chinese Renminbi (Yuan) remains static, it will limit your potential return on the securities. However, changes in the Chinese government’s management of the Chinese Renminbi (Yuan) could result in a more significant movement in the U.S. Dollar/Chinese Renminbi (Yuan) exchange rate. A decrease in the value of the Chinese Renminbi (Yuan), whether as a result of a change in the government’s management of the currency or for other reasons, could result in a change in the Spot Rate.

If the liquidity of the Basket Currencies is limited, the value of the securities would likely be impaired.

Currencies and derivatives contracts on currencies may be difficult to buy or sell, particularly during adverse market conditions. Reduced liquidity on the Final Valuation Date would likely have an adverse effect on the Final Spot Rate for each Basket Currency, and therefore, on the return on your securities. Limited liquidity relating to any Basket Currency may also result in HSBC USA Inc., as Calculation Agent, being unable to determine the Currency Performances, and therefore the Basket Return using its normal means. The resulting discretion by the Calculation Agent in determining the Basket Return could, in turn, result in potential conflicts of interest.

Potential conflicts.

We and our affiliates play a variety of roles in connection with the issuance of the securities, including acting as Calculation Agent and hedging our obligations under the securities. In performing these duties, the economic interests of the Calculation Agent and other affiliates of ours are potentially adverse to your interests as an investor in the securities. We will not have any obligation to consider your interests as a holder of the securities in taking any corporate action that might affect the level of the Basket and the value of the securities.

The securities lack liquidity.

The securities will not be listed on any securities exchange. HSBC Securities (USA) Inc. may offer to purchase the securities in the secondary market but is not required to do so and may cease making such offers at any time. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell the securities easily. Because other dealers are not likely to make a secondary market for the securities, the price at which you may be able to trade your securities is likely to depend on the price, if any, at which HSBC Securities (USA) Inc. is willing to buy the securities.

We have no control over exchange rates.

Foreign exchange rates can either float or be fixed by sovereign governments. Exchange rates of the currencies used by most economically developed nations are permitted to fluctuate in value relative to the U.S. Dollar and to each other. However, from time to time governments may use a variety of techniques, such as intervention by a central bank, the imposition of regulatory controls or taxes or changes in interest rates to influence the exchange rates of their currencies. Governments may also issue a new currency to replace an existing currency or alter the exchange rate or relative exchange characteristics by a devaluation or revaluation of a currency. These governmental actions could change or interfere with currency valuations and currency fluctuations that would otherwise occur in response to economic forces, as well as in response to the movement of currencies across borders. As a consequence, these government actions could adversely affect an investment in a security that is linked to an exchange rate.

The payment formula for the securities will not take into account all developments in the Basket Currencies.

Changes in the Basket Currencies during the term of the securities before the Final Valuation Date will not be reflected in the calculation of the Payment at Maturity. Generally, the Calculation Agent will calculate the Basket Return by multiplying the Currency Performance for each Basket Currency by its respective weighting and then taking the sum of the weighted Currency Performances, as described above. The Currency Performances will be calculated only as of the Final Valuation Date. As a result, the Basket Return may be less than zero even if the Basket Currencies had moved favorably at certain times during the term of the securities before moving to unfavorable values on the Final Valuation Date.

FWP-9

Potentially inconsistent research, opinions, or recommendations by HSBC.

We, our affiliates and agents publish research from time to time on financial markets and other matters that may influence the value of the securities, or express opinions or provide recommendations that may be inconsistent with purchasing or holding the securities. We, our affiliates and agents may publish research or other opinions that are inconsistent with the investment view implicit in the securities. Any research, opinions or recommendations expressed by us, our affiliates or agents may not be consistent with each other and may be modified from time to time without notice. Investors should make their own independent investigation of the merits of investing in the securities and the Basket Currencies to which the securities are linked.

Economic and market factors will impact the value of the securities.

We expect that, generally, the exchange rates for the Basket Currencies on any day will affect the value of the securities more than any other single factor. However, you should not expect the value of the securities in the secondary market to vary in proportion to the appreciation or depreciation of the Basket Currencies relative to the U.S. Dollar. The value of the securities will be affected by a number of other factors that may either offset or magnify each other, including:

· the expected volatility of the Basket Currencies and the U.S. Dollar, as Reference Currency;

· the time to maturity of the securities;

· the volatility of the exchange rate between each Basket Currency and the U.S. Dollar;

· interest and yield rates in the market generally and in the markets of the Basket Currencies and the U.S. Dollar;

· a variety of economic, financial, political, regulatory or judicial events;

· supply and demand for the securities; and

· our creditworthiness, including actual or anticipated downgrades in our credit ratings.

Historical performance of the Basket Currencies should not be taken as an indication of the future performance of the Basket Currencies during the term of the securities.

It is impossible to predict whether any of the Spot Rates for the Basket Currencies will rise or fall. The Basket Currencies will be influenced by complex and interrelated political, economic, financial and other factors.

Market disruptions may adversely affect your return.

The Calculation Agent may, in its sole discretion, determine that the markets have been affected in a manner that prevents it from determining the Basket Return in the manner described herein, and calculating the amount that we are required to pay you upon maturity, or from properly hedging its obligations under the securities. These events may include disruptions or suspensions of trading in the markets as a whole or general inconvertibility or non-transferability of one or more currencies. If the Calculation Agent, in its sole discretion, determines that any of these events prevents us or any of our affiliates from properly hedging our obligations under the securities or prevents the Calculation Agent from determining the Basket Return or Payment at Maturity in the ordinary manner, the Calculation Agent will determine the Basket Return or Payment at Maturity in good faith and in a commercially reasonable manner, and it is possible that the Final Valuation Date and the Maturity Date will be postponed, which may adversely affect the return on your securities. For example, if the source for an exchange rate is not available on the Final Valuation Date, the Calculation Agent may determine the exchange rate for such date, and such determination may adversely affect the return on your securities.

FWP-10

WHAT IS THE PAYMENT AT MATURITY ON THE SECURITIES ASSUMING A RANGE OF PERFORMANCES FOR THE BASKET?

The table below illustrates the Payment at Maturity for a $1,000 Principal Amount of securities for a hypothetical range of performances for the Basket Return. The table below assumes an Upside Participation Rate of 175% (the midpoint of the expected range for the Upside Participation Rate which will be determined on the Pricing Date and will not be less than 160% or greater than 190%). The following results are based solely on the hypothetical example cited. You should consider carefully whether the securities are suitable to your investment goals.

|

Hypothetical

Basket Return |

Hypothetical Payment

at Maturity |

Hypothetical

Total Return |

|

80.00%

|

$2,400.00

|

140.00%

|

|

70.00%

|

$2,225.00

|

122.50%

|

|

60.00%

|

$2,050.00

|

105.00%

|

|

50.00%

|

$1,875.00

|

87.50%

|

|

40.00%

|

$1,700.00

|

70.00%

|

|

30.00%

|

$1,525.00

|

52.50%

|

|

20.00%

|

$1,350.00

|

35.00%

|

|

10.00%

|

$1,175.00

|

17.50%

|

|

5.00%

|

$1,087.50

|

8.75%

|

|

1.00%

|

$1,017.50

|

1.75%

|

|

0.00%

|

$1,000.00

|

0.00%

|

|

-1.00%

|

$990.00

|

-1.00%

|

|

-5.00%

|

$950.00

|

-5.00%

|

|

-10.00%

|

$900.00

|

-10.00%

|

|

-20.00%

|

$900.00

|

-10.00%

|

|

-30.00%

|

$900.00

|

-10.00%

|

|

-40.00%

|

$900.00

|

-10.00%

|

|

-50.00%

|

$900.00

|

-10.00%

|

|

-60.00%

|

$900.00

|

-10.00%

|

|

-70.00%

|

$900.00

|

-10.00%

|

|

-80.00%

|

$900.00

|

-10.00%

|

FWP-11

HYPOTHETICAL EXAMPLES OF AMOUNTS PAYABLE AT MATURITY

The following examples illustrate how the total returns set forth in the table above are calculated assuming an Upside Participation Rate of 175%. The actual Upside Participation Rate will be determined on the Pricing Date and will not be less than 160% or greater than 190%.

Example 1: The level of the Basket increases by 10%.

For example, the BRL Currency Performance is 20%, the INR Currency Performance is 10% and the CNY Currency Performance is 0%, resulting in a Basket Return of 10%. The final Payment at Maturity is equal to $1,175.00 per $1,000 Principal Amount of securities, representing a total return of 17.50% on the securities.

Payment at Maturity per $1,000 Principal Amount of securities = $1,000 + ($1,000 × Basket Return × Upside Participation Rate)

$1,000 + ($1,000 × 10% × 175%) = $1,175.00

The table below illustrates how the Basket Return in the above example was calculated:

|

Basket Currency

|

Basket Currency Initial Spot Rate

|

Basket Currency Final Spot Rate

|

Currency Performance

|

Basket Currency Weighting

|

|

BRL

INR

CNY

|

1.6163

44.9763

6.5046

|

1.2930

40.4787

6.5046

|

20%

10%

0%

|

1/3

1/3

1/3

|

Basket Return = (20%×1/3) + (10%×1/3) + (0%×1/3) = 0.10 = 10%

Example 2: The level of the Basket decreases by 20%.

For example, the BRL Currency Performance is -40%, the INR Currency Performance is -15% and the CNY Currency Performance is -5%, resulting in a Basket Return of -20%. The final Payment at Maturity is equal to $900 per $1,000 Principal Amount of securities, representing a total return of -10% on the securities.

Payment at Maturity per $1,000 Principal Amount of securities = $900.00

The table below illustrates how the Basket Return in the above example was calculated:

|

Basket Currency

|

Basket Currency Initial Spot Rate

|

Basket Currency Final Spot Rate

|

Currency Performance

|

Basket Currency Weighting

|

|

BRL

INR

CNY

|

1.6163

44.9763

6.5046

|

2.2628

51.7227

6.8298

|

-40%

-15%

-5%

|

1/3

1/3

1/3

|

Basket Return = (-40%×1/3) + (-15%×1/3) + (-5%×1/3) = -0.20 = -20%

Example 3: The level of the Basket decreases by 5%.

For example, the BRL Currency Performance is -10%, the INR Currency Performance is -5% and the CNY Currency Performance is 0%, resulting in a Basket Return of -5%. The final Payment at Maturity is equal to $950.00 per $1,000 Principal Amount of securities, representing a total return of -5% on the securities.

Payment at Maturity per $1,000 Principal Amount of securities = $1,000 + ($1,000 × Basket Return)

$1,000 + ($1,000 × -5%) = $950.00

The table below illustrates how the Basket Return in the above example was calculated:

|

Basket Currency

|

Basket Currency Initial Spot Rate

|

Basket Currency Final Spot Rate

|

Currency Performance

|

Basket Currency Weighting

|

|

BRL

INR

CNY

|

1.6163

44.9763

6.5046

|

1.7779

47.2251

6.5046

|

-10%

-5%

0%

|

1/3

1/3

1/3

|

Basket Return = (-10%×1/3) + (-5%×1/3) + (0%×1/3) = -0.05 = -5%

FWP-12

USE OF PROCEEDS AND HEDGING

Part of the net proceeds we receive from the sale of the securities will be used in connection with hedging our obligations under the securities through one or more of our affiliates. The hedging or trading activities of our affiliates on or prior to the Trade Date and during the term of the securities (including on the Final Valuation Date) could adversely affect the amount you may receive on the securities at maturity.

SPOT RATES

The Spot Rate for the Brazilian Real on each date of calculation will be the U.S. Dollar/Brazilian Real offered rate for U.S. Dollars, expressed as the amount of Brazilian Reals per one U.S. Dollar, for settlement in two business days, as reported by Banco Central do Brasil on SISBACEN Data System under transaction code PTAX-800 (“Consulta de Cambio” or Exchange Rate Inquiry), Option 5 (“Cotacoes para Contabilidade” or Rates for Accounting Purposes), by approximately 6:00 p.m., São Paulo time, on such date of calculation, which appears on Reuters Page "BRFR" to the right of the caption “Dollar PTAX” or any successor page, on such date of calculation. Four decimal figures shall be used for the determination of such USDBRL exchange rate.

The Spot Rate for the Indian Rupee on each date of calculation will be the U.S. Dollar/Indian Rupee reference rate, expressed as the amount of Indian Rupees per one U.S. Dollar, for settlement in two business days, as reported by the Reserve Bank of India, which appears on the Reuters Screen RBIB Page or any successor page, at approximately 12:30 p.m., Mumbai time, or as soon thereafter as practicable, on such date of calculation. Four decimal figures shall be used for the determination of such USDINR exchange rate.

The Spot Rate for the Chinese Renminbi (Yuan) on each date of calculation will be the U.S. Dollar/Chinese Renminbi (Yuan) official fixing rate, expressed as the amount of Chinese Renminbi (Yuan) per one U.S. Dollar, for settlement in two business days, as reported by the People’s Bank of China, Beijing, People’s Republic of China, which appears on Reuters Screen SAEC Page opposite the symbol “USDCNY=” or any successor page, at approximately 9:15 a.m., Beijing time, on such date of calculation. Four decimal figures shall be used for the determination of such USDCNY exchange rate.

If any of the foregoing Spot Rates is unavailable (including being published in error, as determined by the Calculation Agent in its sole discretion), the Spot Rate for such Basket Currency shall be selected by the Calculation Agent in good faith and in a commercially reasonable manner or the Final Valuation Date may be postponed by the Calculation Agent as described below in “Market Disruption Events.”

MARKET DISRUPTION EVENTS

The Calculation Agent may, in its sole discretion, determine that an event has occurred that prevents it from valuing one or more of the Basket Currencies or the Payment at Maturity in the manner initially provided for herein. These events may include disruptions or suspensions of trading in the markets as a whole or general inconvertibility or non-transferability of one or more Basket Currencies. If the Calculation Agent, in its sole discretion, determines that any of these events prevents us or our affiliates from properly hedging our obligations under the securities or prevents the Calculation Agent from determining such value or amount in the ordinary manner on such date, the Calculation Agent may determine such value or amount in good faith and in a commercially reasonable manner on such date or, in the discretion of the Calculation Agent, the Final Valuation Date, and Maturity Date may be postponed for up to five scheduled trading days, each of which may adversely affect the return on your securities. If the Final Valuation Date has been postponed for five consecutive scheduled trading days, then that fifth scheduled trading day will be the Final Valuation Date and the Calculation Agent will determine the level of such Basket Currency or Basket Currencies using the formula for and method of determining such level which applied just prior to the market disruption event (or in good faith and in a commercially reasonable manner) on such date.

EVENTS OF DEFAULT AND ACCELERATION

If the securities have become immediately due and payable following an event of default (as defined in the accompanying prospectus) with respect to the securities, the Calculation Agent will determine the accelerated Payment at Maturity due and payable in the same general manner as described in “Key Terms” in this free writing prospectus. In that case, the business day preceding the date of acceleration will be used as the Final Valuation Date for purposes of determining the accelerated

FWP-13

Basket Return (including each Final Spot Rate). The accelerated Maturity Date will be the third business day following the accelerated Final Valuation Date (including each Final Spot Rate).

If the securities have become immediately due and payable following an event of default, you will not be entitled to any additional payments with respect to the securities. For more information, see “Description of Debt Securities — Events of Default” and “— Events of Default; Defaults” in the accompanying prospectus.

FWP-14

HISTORICAL INFORMATION

The following first three graphs below show the historical daily performance of each Basket Currency expressed in terms of the conventional market quotation, as shown on Bloomberg Financial Markets, for each currency (in each case the amount of the applicable Basket Currency that can be exchanged for one U.S. Dollar, which we refer to in this term sheet as the exchange rate) from May 19, 2006 through May 19, 2011. The exchange rates of the Brazilian Real, Indian Rupee and Chinese Renminbi (Yuan), relative to the U.S. Dollar on May 19, 2011, were 1.6163, 44.9763 and 6.5046, respectively.

The exchange rates displayed in the graphs below are for illustrative purposes only and do not form part of the calculation of the Basket Return. The level of the Basket, and thus the Basket Return, increases when the individual Basket Currencies appreciate in value against the U.S. Dollar.

The last graph below shows the daily performance of the Basket from May 19, 2006 through May 19, 2011 assuming that each Basket Currency had a 1/3 weight in the Basket on that date and that the historical exchange rates of each Basket Currency on the relevant dates were the Spot Rates on such dates. The closing exchange rates and the historical daily Basket performance data in the graphs below were the rates reported by Bloomberg Financial Markets and may not be indicative of the Basket performance using the Spot Rates of the Basket Currencies that would be derived from the applicable Reuters page.

|

Brazilian Real

|

Indian Rupee

|

|

|

|

Chinese Renminbi (Yuan)

|

Basket

|

|

|

FWP-15

SUPPLEMENTAL PLAN OF DISTRIBUTION (CONFLICTS OF INTEREST)

We have appointed HSBC Securities (USA) Inc., an affiliate of HSBC, as the agent for the sale of the securities. Pursuant to the terms of a distribution agreement, HSBC Securities (USA) Inc. will purchase the securities from HSBC for distribution to other registered broker dealers or will offer the securities directly to investors. HSBC Securities (USA) Inc. proposes to offer the securities at the offering price set forth on the cover page of this free writing prospectus and will receive underwriting discounts and commissions of up to 2.30%, or $23.00, per $1,000 Principal Amount of securities. HSBC Securities (USA) Inc. may allow selling concessions on sales of such securities by other brokers or dealers of up to 2.30%, or $23.00, and may pay referral fees to other broker-dealers of up to 0.80%, or $8.00, per $1,000 Principal Amount of securities.

In addition, HSBC Securities (USA) Inc. or another of its affiliates or agents may use the pricing supplement to which this free writing prospectus relates in market-making transactions after the initial sale of the securities, but is under no obligation to do so and may discontinue any market-making activities at any time without notice.

See “Supplemental Plan of Distribution” on page S-52 in the prospectus supplement. All references to NASD Rule 2720 in the prospectus supplement shall be to FINRA Rule 5121.

We expect that delivery of the securities will be made against payment for the securities on or about the Settlement Date set forth on page FWP-2 of this document, which is expected to be the fourth business day following the Trade Date of the securities. Under Rule 15c6-1 under the Securities Exchange Act of 1934, as amended, trades in the secondary market generally are required to settle in three business days, unless the parties to that trade expressly agree otherwise. Accordingly, purchasers who wish to trade securities on the Trade Date will be required to specify an alternate settlement cycle at the time of any such trade to prevent a failed settlement and should consult their own advisors.

CERTAIN U.S. FEDERAL INCOME TAX CONSIDERATIONS

You should carefully consider the matters set forth in “Certain U.S. Federal Income Tax Considerations” in the accompanying prospectus supplement. The following discussion summarizes certain of the material U.S. federal income tax consequences of the purchase, beneficial ownership, and disposition of the securities. This summary supplements the section “Certain U.S. Federal Income Tax Considerations” in the accompanying prospectus supplement and supersedes it to the extent inconsistent

therewith. Notwithstanding any disclosure in the accompanying prospectus supplement to the contrary, our special U.S. tax counsel in this transaction is Sidley Austin llp.

There are no statutory provisions, regulations, published rulings or judicial decisions addressing the characterization for U.S. federal income tax purposes of securities with terms that are substantially the same as those of the securities. We intend to treat the securities as contingent payment debt instruments for U.S. federal income tax purposes. Pursuant to the terms of the securities, you agree to treat the securities as contingent payment debt instruments for all U.S. federal income tax purposes and, in the opinion of Sidley Austin llp, special U.S. tax counsel to us, it is reasonable to treat the securities as contingent payment debt instruments. Assuming the securities are treated as contingent payment debt instruments, a U.S. holder will be required to include original issue discount (“OID”) in gross income each year, even though no payments will be made on the securities until maturity.

Based on the factors described in the section, “Certain U.S. Federal Income Tax Considerations — U.S. Federal Income Tax Treatment of the Notes as Indebtedness for U.S. Federal Income Tax Purposes — Contingent Payment Debt Instruments”, in order to illustrate the application of the noncontingent bond method to the securities, we have estimated that the comparable yield of the securities, solely for U.S. federal income tax purposes, will be 1.43% per annum (compounded annually). Further, based upon the method described in the section, “Certain U.S. Federal Income Tax Considerations — U.S. Federal Income Tax Treatment of the Notes as Indebtedness for U.S. Federal Income Tax Purposes — Contingent Payment Debt Instruments” and based upon the estimate of the comparable yield, we have estimated that the projected payment schedule for securities that have a Principal Amount of $1,000 and an issue price of $1,000 consists of a single payment of $1,023.47 at maturity.

Based upon the estimate of the comparable yield, a U.S. holder that pays taxes on a calendar year basis, buys a security for $1,000, and holds the security until maturity will be required to pay taxes on the following amounts of ordinary income in respect of the securities in each year:

FWP-16

|

Year

|

OID

|

|

2011

|

$6.17

|

|

2012

|

$11.74

|

|

2013

|

$5.56

|

However, the ordinary income reported in the taxable year the securities mature will be adjusted to reflect the actual payment received at maturity. U.S. holders should also note that the actual comparable yield and projected payment schedule may be different than as provided in this summary depending upon market conditions on the date the securities are issued. U.S. holders may obtain the actual comparable yield and projected payment schedule as determined by us by submitting a written request to: Structured Equity Derivatives – Structuring HSBC Bank USA, National Association, 452 Fifth Avenue, 3rd Floor, New York, NY 10018. A U.S. holder is generally bound by the comparable yield and the projected payment schedule established by us for the securities. However, if a U.S. holder believes that the projected payment schedule is unreasonable, a U.S. holder must determine its own projected payment schedule and explicitly disclose the use of such schedule and the reason the holder believes the projected payment schedule is unreasonable on its timely filed U.S. federal income tax return for the taxable year in which it acquires the securities.

The comparable yield and projected payment schedule are not provided for any purpose other than the determination of a U.S. holder’s interest accruals for U.S. federal income tax purposes and do not constitute a projection or representation by us regarding the actual yield on a security. We do not make any representation as to what such actual yield will be.

Because there are no statutory provisions, regulations, published rulings or judicial decisions addressing the characterization for U.S. federal income tax purposes of securities with terms that are substantially the same as those of the securities, other characterizations and treatments are possible. As a result, the timing and character of income in respect of the securities might differ from the treatment described above. You should carefully consider the discussion of all potential tax consequences as set forth in “Certain U.S. Federal Income Tax Considerations” in the accompanying prospectus supplement.

PROSPECTIVE PURCHASERS OF SECURITIES SHOULD CONSULT THEIR TAX ADVISORS AS TO THE FEDERAL, STATE, LOCAL, AND OTHER TAX CONSEQUENCES TO THEM OF THE PURCHASE, OWNERSHIP AND DISPOSITION OF SECURITIES.

FWP-17

|

TABLE OF CONTENTS

|

You should only rely on the information contained in this free writing prospectus, any accompanying prospectus supplement and prospectus. We have not authorized anyone to provide you with information or to make any representation to you that is not contained in this free writing prospectus, any accompanying prospectus supplement and prospectus. If anyone provides you with different or inconsistent information, you should not rely on it. This free writing prospectus, any accompanying prospectus supplement and prospectus are not an offer to sell these securities, and these documents are not soliciting an offer to buy these securities, in any jurisdiction where the offer or sale is not permitted. You should not, under any circumstances, assume that the information in this free writing prospectus, any accompanying prospectus supplement and prospectus is correct on any date after their respective dates.

HSBC USA Inc.

$ EM Currency Accelerated Return

Securities due June 20, 2013 May 23, 2011

FREE WRITING PROSPECTUS

|

||

|

Free Writing Prospectus

|

|||

|

General

|

FWP-6

|

||

|

Trustee

|

FWP-6

|

||

|

Paying Agent

|

FWP-6

|

||

|

Calculation Agent

|

FWP-6

|

||

|

Selected Purchase Considerations

|

FWP-6

|

||

|

Selected Risk Considerations

|

FWP-7

|

||

|

What is the Payment at Maturity on the Securities

Assuming a Range of Performances for the Basket? |

FWP-11

|

||

|

Hypothetical Examples of Amounts Payable at Maturity

|

FWP-12

|

||

|

Use of Proceeds and Hedging

|

FWP-13

|

||

|

Spot Rates

|

FWP-13

|

||

|

Market Disruption Events

|

FWP-13

|

||

|

Events of Default and Acceleration

|

FWP-13

|

||

|

Historical Information

|

FWP-15

|

||

|

Supplemental Plan of Distribution (Conflicts of Interest)

|

FWP-16

|

||

|

Certain U.S. Federal Income Tax Considerations

|

FWP-16

|

||

|

Prospectus Supplement

|

|||

|

Risk Factors

|

S-3

|

||

|

Pricing Supplement

|

S-16

|

||

|

Description of Notes

|

S-16

|

||

|

Sponsors or Issuers and Reference Asset

|

S-37

|

||

|

Use of Proceeds and Hedging

|

S-37

|

||

|

Certain ERISA

|

S-38

|

||

|

Certain U.S. Federal Income Tax Considerations

|

S-39

|

||

|

Supplemental Plan of Distribution

|

S-52

|

||

|

Prospectus

|

|||

|

About this Prospectus

|

2

|

||

|

Special Note Regarding Forward-Looking Statements

|

2

|

||

|

HSBC USA Inc.

|

3

|

||

|

Use of Proceeds

|

3

|

||

|

Description of Debt Securities

|

4

|

||

|

Description of Preferred Stock

|

16

|

||

|

Description of Warrants

|

22

|

||

|

Description of Purchase Contracts

|

26

|

||

|

Description of Units

|

29

|

||

|

Book-Entry Procedures

|

32

|

||

|

Limitations on Issuances in Bearer Form

|

36

|

||

|

Certain U.S. Federal Income Tax Considerations Relating

to Debt Securities |

37

|

||

|

Plan of Distribution

|

52

|

||

|

Notice to Canadian Investors

|

54

|

||

|

Certain ERISA Matters

|

58

|

||

|

Where You Can Find More Information

|

59

|

||

|

Legal Opinions

|

59

|

||

|

Experts

|

59

|

||

FWP-18