UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2020

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

| For the transition period from to | |||||

Commission file number 1-10235

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||||||||||||||

| (Address of principal executive offices) | (Zip Code) | |||||||||||||||||||

Registrant’s telephone number, including area code:

(847 ) 498-7070

Securities Registered Pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol(s) | Name of Each Exchange on Which Registered | ||||||

Securities Registered Pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes þ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☑ | Accelerated filer ☐ | Non-accelerated filer ☐ | Smaller reporting company | |||||||||||||||||||||||

| Emerging growth company | ||||||||||||||||||||||||||

| If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐ | ||||||||||||||||||||||||||

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No þ

The aggregate market value, as of the last business day of the registrant’s most recently completed second fiscal quarter, of the common stock (based on the June 30, 2020 closing price of $158.04) held by non-affiliates of IDEX Corporation was $11,866,931,226 .

The number of shares outstanding of IDEX Corporation’s common stock, par value $.01 per share, as of February 22, 2021 was 75,889,737 .

DOCUMENTS INCORPORATED BY REFERENCE

Table of Contents

| PART I. | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 1B. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| PART II. | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

| Item 7. | ||||||||

| Item 7A. | ||||||||

| Item 8. | ||||||||

| Item 9. | ||||||||

| Item 9A. | ||||||||

| Item 9B. | ||||||||

| PART III. | ||||||||

| Item 10. | ||||||||

| Item 11. | ||||||||

| Item 12. | ||||||||

| Item 13. | ||||||||

| Item 14. | ||||||||

| PART IV. | ||||||||

| Item 15. | ||||||||

| Item 16. | ||||||||

PART I

Cautionary Statement Under the Private Securities Litigation Reform Act

This report contains “forward-looking” statements within the meaning of the Private Securities Litigation Reform Act of 1995, as amended. These statements may relate to, among other things, the Company’s expected organic sales growth, the expected timing and anticipated benefits of the Company’s acquisition of Abel Pumps, L.P. and certain of its affiliates, and the anticipated continuing effects of the coronavirus pandemic, including with respect to the Company's sales, improvements in the Company’s end markets, facility closures, supply chains and access to capital, capital expenditures, acquisitions, cost reductions, cash flow, revenues, earnings, market conditions, global economies and operating improvements, and are indicated by words or phrases such as “anticipates,” “estimates,” “plans,” “expects,” “projects,” “forecasts,” “should,” “could,” “will,” “management believes,” “the Company believes,” “the Company intends” and similar words or phrases. These statements are subject to inherent uncertainties and risks that could cause actual results to differ materially from those anticipated at the date of this report. The risks and uncertainties include, but are not limited to, the following: the duration of the coronavirus pandemic and the continuing effects of the coronavirus pandemic on our ability to operate our business and facilities, on our customers, on supply chains and on the U.S. and global economy generally; economic and political consequences resulting from terrorist attacks and wars; levels of industrial activity and economic conditions in the U.S. and other countries around the world; pricing pressures and other competitive factors and levels of capital spending in certain industries, all of which could have a material impact on order rates and the Company’s results, particularly in light of the low levels of order backlogs it typically maintains; the Company’s ability to make acquisitions and to integrate and operate acquired businesses on a profitable basis; the relationship of the U.S. dollar to other currencies and its impact on pricing and cost competitiveness; political and economic conditions in foreign countries in which the Company operates; developments with respect to trade policy and tariffs; interest rates; capacity utilization and the effect this has on costs; labor markets; market conditions and material costs; and developments with respect to contingencies, such as litigation and environmental matters, and the other risk factors discussed in Item 1A, “Risk Factors” of this annual report. The forward-looking statements included here are only made as of the date of this report, and management undertakes no obligation to publicly update them to reflect subsequent events or circumstances, except as may be required by law. Investors are cautioned not to rely unduly on forward-looking statements when evaluating the information presented here.

Item 1. Business.

IDEX Corporation (“IDEX,” the “Company,” “us,” “our,” or “we”) is a Delaware corporation incorporated on September 24, 1987. The Company is an applied solutions business that sells an extensive array of pumps, valves, flow meters and other fluidics systems and components and engineered products to customers in a variety of markets around the world. Substantially all of the Company’s business activities are carried out through wholly-owned subsidiaries.

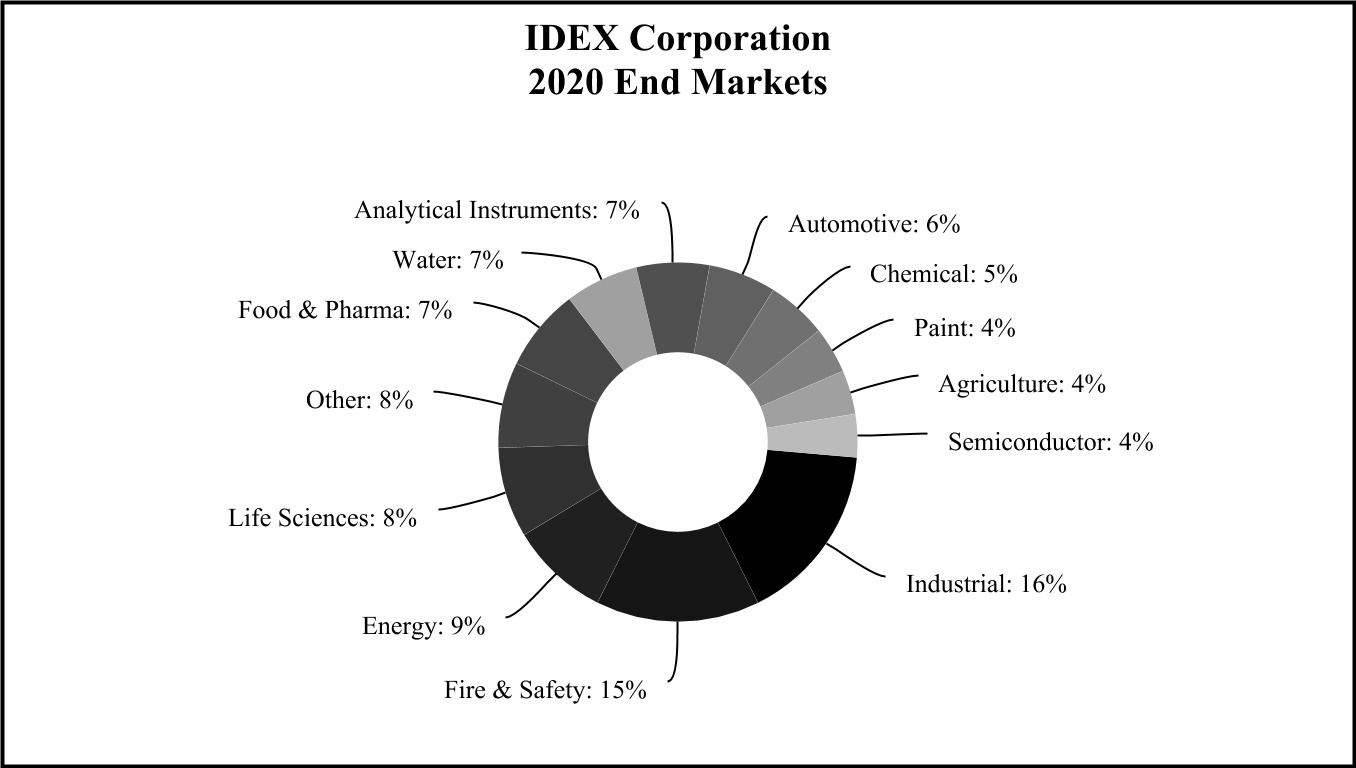

The Company has three reportable business segments: Fluid & Metering Technologies (“FMT”), Health & Science Technologies (“HST”) and Fire & Safety/Diversified Products (“FSDP”). Within our three reportable segments, the Company maintains 13 platforms where we focus on organic growth and strategic acquisitions. Each of our 13 platforms is also a reporting unit that we annually test for goodwill impairment.

1

The FMT segment contains the Energy platform (comprised of Corken, Liquid Controls, SAMPI, Toptech and Flow Management Devices, LLC (“Flow MD”)), the Valves platform (comprised of Alfa Valvole, Richter and Aegis), the Water platform (comprised of Pulsafeeder, OBL, Knight, ADS, Trebor and iPEK), the Pumps platform (comprised of Viking and Warren Rupp) and the Agriculture platform (comprised of Banjo). The HST segment contains the Scientific Fluidics & Optics platform (comprised of Eastern Plastics, Rheodyne, Sapphire Engineering, Upchurch Scientific, ERC, CiDRA Precision Services, thinXXS, CVI Melles Griot, Semrock, Advanced Thin Films and FLI), the Sealing Solutions platform (comprised of Precision Polymer Engineering, FTL Seals Technology, Novotema, SFC Koenig and Velcora), the Gast platform, the Micropump platform and the Material Processing Technologies platform (comprised of Quadro, Fitzpatrick, Microfluidics and Matcon). The FSDP segment is comprised of the Fire & Safety platform (comprised of Class 1, Hale, Godiva, Akron Brass, Weldon, AWG Fittings, Dinglee, Hurst Jaws of Life, Lukas and Vetter), the BAND-IT platform and the Dispensing platform.

IDEX believes that each of its reporting units is a leader in its product and service areas. The Company also believes that its strong financial performance has been attributable to its ability to design and engineer specialized quality products, coupled with its ability to successfully identify, acquire and integrate strategic acquisitions.

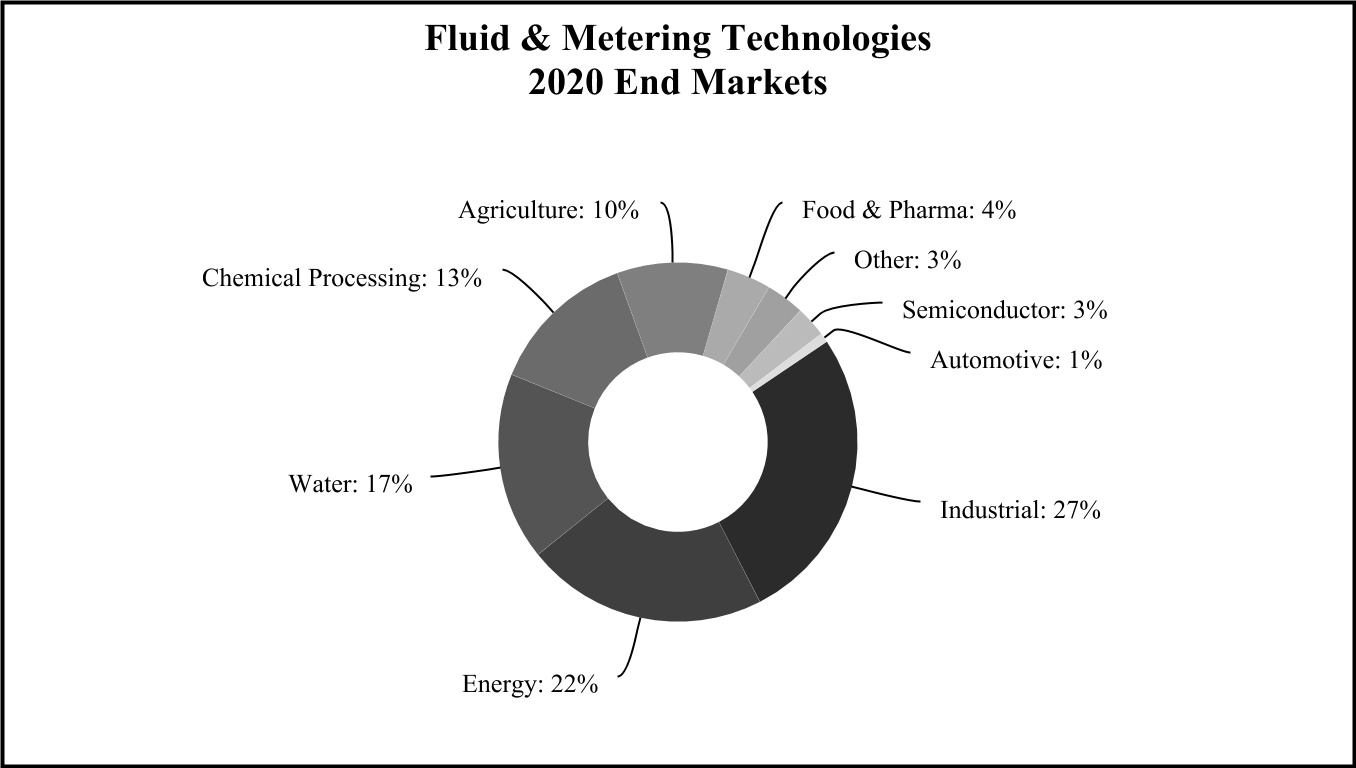

FLUID & METERING TECHNOLOGIES SEGMENT

The Fluid & Metering Technologies segment designs, produces and distributes positive displacement pumps, small volume provers, flow meters, injectors and other fluid-handling pump modules and systems and provides flow monitoring and other services for the food, chemical, general industrial, water and wastewater, agriculture and energy industries. Fluid & Metering Technologies application-specific pump and metering solutions serve a diverse range of end markets, including industrial infrastructure (fossil fuels, refined and alternative fuels and water and wastewater), chemical processing, agriculture, food and beverage, pulp and paper, transportation, plastics and resins, electronics and electrical, construction and mining, pharmaceutical and bio-pharmaceutical, machinery and numerous other specialty niche markets.

2

Fluid & Metering Technologies accounted for 38% of IDEX’s sales in each of 2020, 2019 and 2018, respectively, with approximately 44% of its 2020 sales to customers outside the U.S. The segment accounted for 40%, 44% and 42% of total segment operating income in 2020, 2019 and 2018, respectively.

Energy. Energy consists of the Company’s Corken, Liquid Controls, SAMPI, Toptech and Flow MD businesses. Energy is a leading supplier of flow meters, small volume provers, electronic registration and control products, rotary vane and turbine pumps, reciprocating piston compressors and terminal automation control systems. Applications for Liquid Controls and SAMPI consist of positive displacement flow meters and electronic registration and control products, including mobile and stationary metering installations for wholesale and retail distribution of petroleum and liquefied petroleum gas, aviation refueling and industrial metering and dispensing of liquids and gases. Corken products consist of positive-displacement rotary vane pumps, single and multistage regenerative turbine pumps and small horsepower reciprocating piston compressors. Toptech supplies terminal automation hardware and software to control and manage inventories as well as transactional data and invoicing to customers in the oil, gas and refined-fuels markets. Flow MD engineers and manufactures small volume provers that ensure custody transfer accuracy in the oil and gas industry. Energy maintains facilities in Lake Bluff, Illinois (Liquid Controls products); Longwood, Florida and Zwijndrecht, Belgium (Toptech products); Oklahoma City, Oklahoma (Corken and Flow MD products); Altopascio, Italy (SAMPI products); and Phoenix, Arizona (Flow MD products). Approximately 33% of Energy’s 2020 sales were to customers outside the U.S.

Valves. Valves consists of the Company’s Alfa Valvole, Richter and Aegis businesses. Valves is a leader in the design, manufacture and sale of specialty valve products for use in the chemical, petro-chemical, energy and sanitary markets as well as a leading producer of fluoroplastic lined corrosion-resistant magnetic drive and mechanical seal pumps, shut-off, control and safety valves for corrosive, hazardous, contaminated, pure and high-purity fluids. Alfa Valvole’s products are used in various industrial fields for fluid control, in both gas and liquid form, in all sectors of plant engineering, cosmetics, detergents, food industry, electric energy, pharmaceutical, chemical plants, petrochemical plants, oil, heating/air conditioning and also on ships, ferries and marine oil platforms. Richter’s products offer superior solutions for demanding and complex pump and valve applications in the process industry. Aegis produces specialty chemical processing valves for use in the chemical, petro-chemical, chlor-alkali and pulp and paper industries. Valves maintains operations in Casorezzo, Italy (Alfa Valvole products); Cedar Falls, Iowa, Kempen, Germany and Suzhou, China (Richter products); and Geismar, Louisiana (Aegis products). Approximately 83% of Valves’ 2020 sales were to customers outside the U.S.

Water. Water consists of the Company’s ADS, iPEK, Knight, Trebor, Pulsafeeder and OBL businesses. Water is a leading provider of metering technology, flow monitoring products and underground surveillance services for wastewater markets, alloy and non-metallic gear pumps, peristaltic pumps, transfer pumps as well as dispensing equipment for industrial

3

laundries, commercial dishwashing and chemical metering. ADS’ products and services provide comprehensive integrated solutions that enable industry, municipalities and government agencies to analyze and measure the capacity, quality and integrity of wastewater collection systems, including the maintenance and construction of such systems. iPEK supplies remote controlled systems used for infrastructure inspection. Knight is a leading manufacturer of pumps and dispensing equipment for industrial laundries, commercial dishwashing and chemical metering. Trebor is a leader in high-purity fluid handling products, including air-operated diaphragm pumps and deionized water-heating systems. Trebor products are used in the manufacturing of semiconductors, disk drives and flat panel displays. Pulsafeeder products (which also include OBL products) are used to introduce precise amounts of fluids into processes to manage water quality and chemical composition as well as peristaltic pumps. Its markets include water and wastewater treatment, oil and gas, power generation, pulp and paper, chemical and hydrocarbon processing and swimming pools. Water maintains operations in Huntsville, Alabama and various other locations in the United States, Canada and Australia (ADS products and services); Hirschegg, Austria and Sulzberg, Germany (iPEK products); Rochester, New York, Punta Gorda, Florida, and Milan, Italy (Pulsafeeder products); West Jordan, Utah (Trebor products); Irvine, California, Mississauga, Ontario, Canada, and Lewes, England (Knight products); and a maquiladora in Ciudad Juarez, Chihuahua, Mexico (Knight products). Approximately 45% of Water’s 2020 sales were to customers outside the U.S.

Pumps. Pumps consists of the Company’s Viking and Warren Rupp businesses. Pumps is a leading manufacturer of rotary internal gear, external gear, vane and rotary lobe pumps, custom-engineered OEM pumps, strainers, gear reducers and engineered pump systems. Viking’s products consist of external gear pumps, strainers and reducers and related controls used for transferring and metering thin and viscous liquids sold under the Viking and Wright Flow brands. Viking products primarily serve the chemical, petroleum, pulp and paper, plastics, paints, inks, tanker trucks, compressor, construction, food and beverage, personal care, pharmaceutical and biotech markets. Warren Rupp products (which include Versa-Matic products) are used for abrasive and semisolid materials as well as for applications where product degradation is a concern or where electricity is not available or should not be used. Warren Rupp products, which include air-operated double diaphragm pumps, primarily serve the chemical, paint, food processing, electronics, construction, utilities, oil and gas, mining and industrial maintenance markets. Pumps maintains operations in Cedar Falls, Iowa (Viking and Wright Flow products); Eastbourne, England (Wright Flow products); Shannon, Ireland (Viking and Blagdon products); and Mansfield, Ohio (Warren Rupp products). Pumps primarily uses independent distributors to market and sell its products. Approximately 42% of Pumps’ 2020 sales were to customers outside the U.S.

Agriculture. Agriculture consists of the Company’s Banjo business. Banjo is a provider of special purpose, severe-duty pumps, valves, fittings and systems used in liquid handling. Banjo is based in Crawfordsville, Indiana with distribution facilities in Didam, The Netherlands and Valinhos, Brazil. Its products are used in agriculture (approximately 71% of revenue) and industrial (approximately 29% of revenue) applications. Approximately 21% of Banjo’s 2020 sales were to customers outside the U.S.

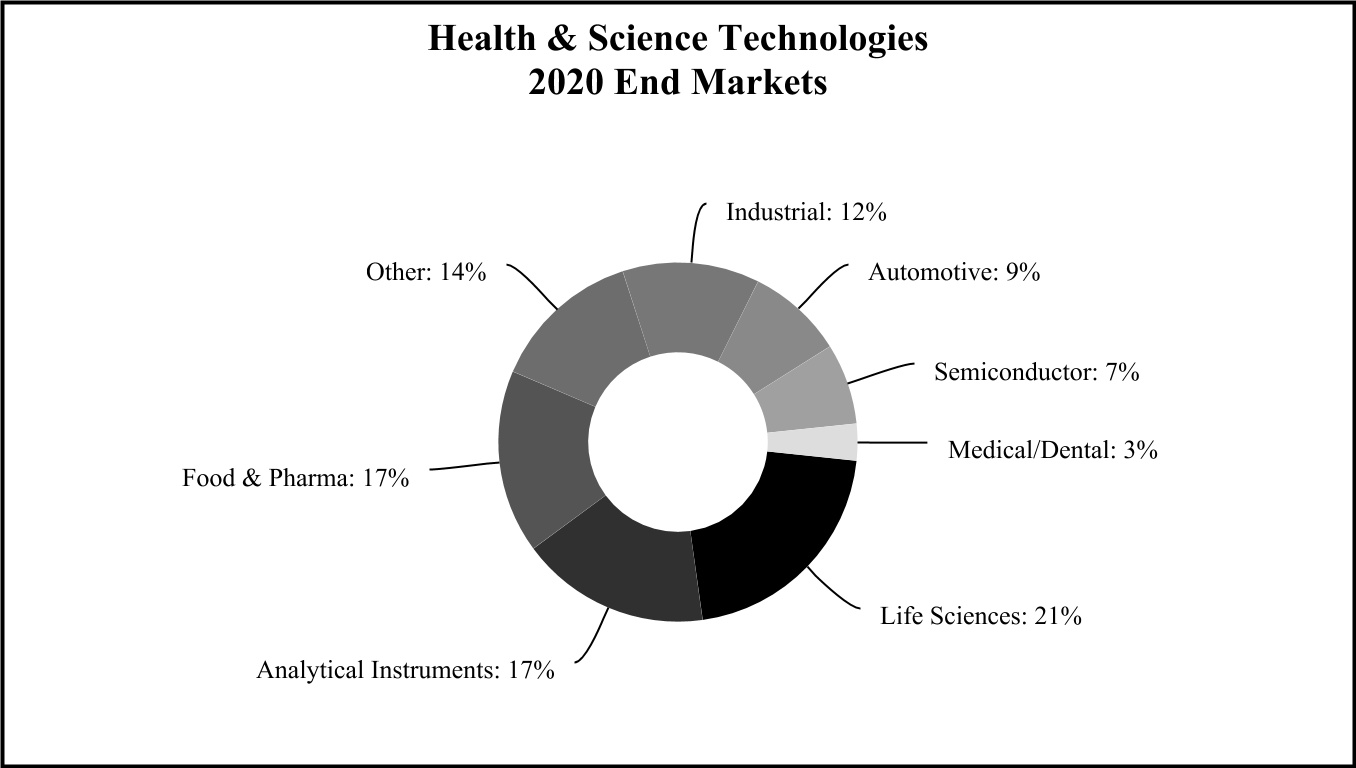

HEALTH & SCIENCE TECHNOLOGIES SEGMENT

The Health & Science Technologies segment designs, produces and distributes a wide range of precision fluidics, rotary lobe pumps, centrifugal and positive displacement pumps, roll compaction and drying systems used in beverage, food processing, pharmaceutical and cosmetics, pneumatic components and sealing solutions, including very high precision, low-flow rate pumping solutions required in analytical instrumentation, clinical diagnostics and drug discovery, high performance molded and extruded sealing components, custom mechanical and shaft seals for a variety of end markets including food and beverage, marine, chemical, wastewater and water treatment, engineered hygienic mixers and valves for the global biopharmaceutical industry, biocompatible medical devices and implantables, air compressors used in medical, dental and industrial applications, optical components and coatings for applications in the fields of scientific research, defense, biotechnology, aerospace, telecommunications and electronics manufacturing, laboratory and commercial equipment used in the production of micro and nano scale materials, precision photonic solutions used in life sciences, research and defense markets and precision gear and peristaltic pump technologies that meet exacting original equipment manufacturer specifications.

4

Health & Science Technologies accounted for 38%, 37% and 36% of IDEX’s sales in 2020, 2019 and 2018, respectively, with approximately 57% of its 2020 sales to customers outside the U.S. The segment accounted for 35%, 31% and 32% of total segment operating income in 2020, 2019 and 2018, respectively.

Scientific Fluidics & Optics. Scientific Fluidics & Optics consists of the Company’s Eastern Plastics, Rheodyne, Sapphire Engineering, Upchurch Scientific, ERC, CiDRA Precision Services, thinXXS, CVI Melles Griot, Semrock, Advanced Thin Films and FLI businesses. Eastern Plastics products, which consist of high-precision integrated fluidics and associated engineered manifolds, are used in a broad set of end markets including medical diagnostics, analytical instrumentation and laboratory automation. Rheodyne products consist of injectors, valves, fittings and accessories for the analytical instrumentation market. These products are used by manufacturers of high pressure liquid chromatography (“HPLC”) equipment servicing the pharmaceutical, biotech, life science, food and beverage, and chemical markets. Sapphire Engineering and Upchurch Scientific products consist of fluidic components and systems for the analytical, biotech and diagnostic instrumentation markets, such as fittings, precision-dispensing pumps and valves, tubing and integrated tubing assemblies, filter sensors and other micro-fluidic and nano-fluidic components as well as advanced column hardware and accessories for the high performance liquid chromatography market. The products produced by Sapphire Engineering and Upchurch Scientific primarily serve the pharmaceutical, drug discovery, chemical, biochemical processing, genomics/proteomics research, environmental labs, food/agriculture, medical lab, personal care and plastics/polymer/rubber production markets. ERC manufactures gas liquid separations and detection solutions for the life science, analytical instrumentation and clinical chemistry markets. ERC’s products consist of in-line membrane vacuum degassing solutions, refractive index detectors and ozone generation systems. CiDRA Precision Services’ products consist of microfluidic components serving the life science, health and industrial markets and thinXXS is a leader in the design, manufacture and sale of microfluidic components serving the point of care, veterinary and life science markets. CVI Melles Griot is a global leader in the design and manufacture of precision photonic solutions used in the life science, research, semiconductor, security and defense markets. CVI Melles Griot’s innovative products are focused on the generation, control and productive use of light for a variety of key science and industrial applications. Products consist of specialty lasers and light sources, electro-optical components, specialty shutters, opto-mechanical assemblies and components. In addition, CVI Melles Griot produces critical components for life science research, electronics manufacturing, military and other industrial applications, including lenses, mirrors, filters and polarizers. These components are utilized in a number of important applications such as spectroscopy, cytometry (cell counting), guidance systems for target designation, remote sensing, menology and optical lithography. Semrock is a provider of optical filters for biotech and analytical instrumentation in the life science market. Semrock’s optical filters are produced using state-of-the-art manufacturing processes which enable it to offer its customers significant improvements in instrument performance and reliability. Advanced Thin Films specializes in optical components and coatings for applications in the fields of scientific research, defense, aerospace, telecommunications and electronics manufacturing. Advanced Thin Films’ core competence is the design and manufacture of filters, splitters,

5

reflectors and mirrors with the precise physical properties required to support their customers’ most challenging and cutting-edge optical applications. The Precision Photonics portion of its business specializes in optical components and coatings for applications in the fields of scientific research, aerospace, telecommunications and electronics manufacturing. FLI specializes in the design, development and production of low-noise cooled charge-coupled device (“CCD”) and high speed, high-sensitivity scientific complementary metal-oxide semiconductor (“CMOS”) cameras for the astronomy and life science markets. Scientific Fluidics & Optics has facilities in Bristol, Connecticut (Eastern Plastics products); Rohnert Park, California (Rheodyne products); Middleboro, Massachusetts (Sapphire Engineering products); Oak Harbor, Washington (Upchurch Scientific products); Kawaguchi, Japan (ERC products); Wallingford, Connecticut (CiDRA Precision Services products); Zweibrücken, Germany (thinXXS products); Albuquerque, New Mexico, Rochester, New York, Leicester, England and Didam, The Netherlands (CVI Melles Griot products); Rochester, New York (Semrock products); Boulder, Colorado (Advanced Thin Films products); and Lima, New York (FLI products). Approximately 54% of Scientific Fluidics & Optics’ 2020 sales were to customers outside the U.S.

Sealing Solutions. Sealing Solutions consists of the Company’s Precision Polymer Engineering, FTL Seals Technology, Novotema, SFC Koenig and Velcora businesses. Precision Polymer Engineering is a provider of proprietary high performance seals and advanced sealing solutions for a diverse range of global industries and applications, including hazardous duty, analytical instrumentation, semiconductor, process technologies, oil and gas, pharmaceutical, electronics and food applications. Precision Polymer Engineering is headquartered in Blackburn, England with an additional manufacturing facility in Brenham, Texas. Precision Polymer Engineering also entered into a joint venture with a third party to manufacture and sell high performance elastomer seals for the oil and gas industry to customers within the Kingdom of Saudi Arabia as well as export these high performance elastomer seals outside of the Kingdom of Saudi Arabia. The joint venture is headquartered in Damman, Saudi Arabia. FTL Seals Technology, located in Leeds, England, specializes in the design and application of high integrity rotary seals, specialty bearings and other custom products for the mining, power generation and marine markets. Novotema, located in Villongo, Italy, is a leader in the design, manufacture and sale of specialty sealing solutions for use in the building products, gas control, transportation, industrial and water markets. SFC Koenig is a producer of highly engineered expanders and check valves for critical applications across the transportation, hydraulic, aviation and medical markets. SFC Koenig is based in Dietikon, Switzerland, with additional facilities in North Haven, Connecticut, Illerrieden, Germany, and Suzhou, China. Velcora and its operating subsidiaries under the Roplan name are headquartered in Sweden with operations in China, the United Kingdom and the United States. Roplan is a global manufacturer of custom mechanical and shaft seals for a variety of end markets including food and beverage, marine, chemical, wastewater and water treatment. Approximately 75% of Sealing Solutions’ 2020 sales were to customers outside the U.S.

Gast. The Gast business is a leading manufacturer of air-moving products, including air motors, low-range and medium-range vacuum pumps, vacuum generators, regenerative blowers and fractional horsepower compressors. Gast products are used in a variety of long-life applications requiring a quiet, clean source of moderate vacuum or pressure. Gast products primarily serve the medical equipment, environmental equipment, computers and electronics, printing machinery, paint mixing machinery, packaging machinery, graphic arts and industrial manufacturing markets. Based in Benton Harbor, Michigan, Gast also has a logistics and commercial center in Redditch, England. Approximately 27% of Gast’s 2020 sales were to customers outside the U.S.

Micropump. Micropump, headquartered in Vancouver, Washington, is a leader in small, precision-engineered, magnetically and electromagnetically driven rotary gear, piston and centrifugal pumps. Micropump products are used in low-flow abrasive and corrosive applications. Micropump products primarily serve the continuous ink-jet printing, medical equipment, chemical processing, pharmaceutical, refining, laboratory, electronics, textiles, peristaltic metering pumps, analytical process controllers and sample preparation systems markets. Approximately 73% of Micropump’s 2020 sales were to customers outside the U.S.

Material Processing Technologies. Material Processing Technologies consists of the Company’s Quadro, Fitzpatrick, Steridose, Microfluidics and Matcon businesses. Quadro is a leading provider of particle control solutions for the pharmaceutical and bio-pharmaceutical markets. Based in Waterloo, Canada, Quadro’s core capabilities include fine milling, emulsification and special handling of liquid and solid particulates for laboratory, pilot phase and production scale processing. Fitzpatrick is a global leader in the design and manufacture of process technologies for the pharmaceutical, food and personal care markets. Fitzpatrick designs and manufactures customized size reduction, roll compaction and drying systems to support their customers’ product development and manufacturing processes. Fitzpatrick is headquartered in Waterloo, Canada. In June 2020, the Steridose business was moved from an operating subsidiary of Velcora to an operating subsidiary of Quadro. Steridose develops engineered hygienic mixers and valves for the global biopharmaceutical industry. Microfluidics is a global leader in the design and manufacture of laboratory and commercial equipment used in the production of micro and nano scale materials for the pharmaceutical and chemical markets. Microfluidics is the exclusive producer of the Microfluidizer family of high shear fluid processors for uniform particle size reduction, robust cell disruption and nanoparticle creation. Microfluidics is

6

also based in Waterloo, Canada and has offices in Newton, Massachusetts. Matcon is a global leader in material processing solutions for high value powders used in the manufacture of pharmaceuticals, food, plastics and fine chemicals. Matcon’s innovative products consist of the original cone valve powder discharge system and filling, mixing and packaging systems, all of which support its customers’ automation and process requirements. These products are critical to its customers’ need to maintain clean, reliable and repeatable formulations of prepackaged foods and pharmaceuticals while helping them achieve lean and agile manufacturing. Matcon is located in Evesham, England. Approximately 63% of Material Processing Technologies’ 2020 sales were to customers outside the U.S.

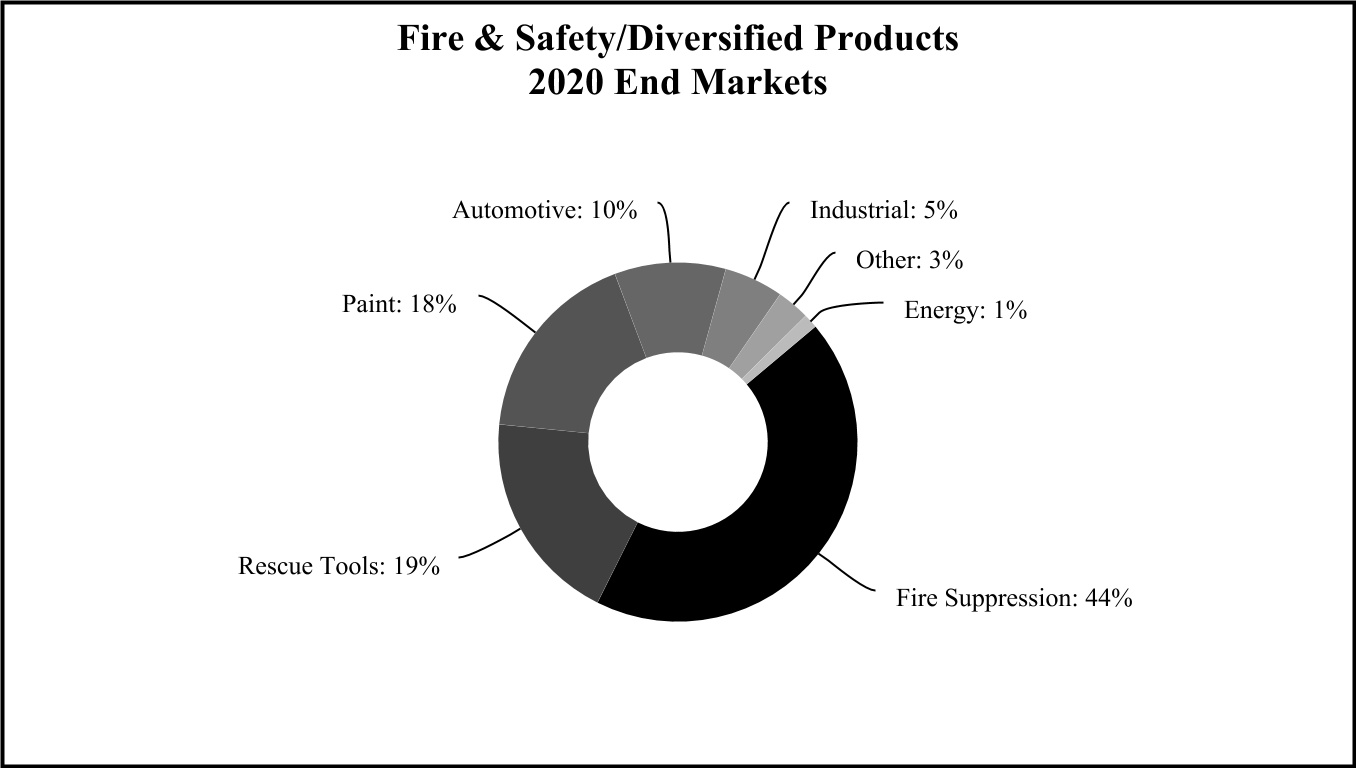

FIRE & SAFETY/DIVERSIFIED PRODUCTS SEGMENT

The Fire & Safety/Diversified Products segment designs, produces and distributes firefighting pumps, valves and controls, rescue tools, lifting bags and other components and systems for the fire and rescue industry, engineered stainless steel banding and clamping devices used in a variety of industrial and commercial applications and precision equipment for dispensing, metering and mixing colorants and paints used in a variety of retail and commercial businesses around the world.

The Fire & Safety/Diversified Products segment accounted for 24%, 25% and 26% of IDEX’s sales in 2020, 2019 and 2018, respectively, with approximately 52% of its 2020 sales to customers outside the U.S. The segment accounted for 25%, 25% and 26% of total segment operating income in 2020, 2019 and 2018, respectively.

Fire & Safety. Fire & Safety consists of the Company’s Class 1, Hale, Godiva, Akron Brass, Weldon, AWG Fittings, Dinglee, Hurst Jaws of Life, Lukas and Vetter businesses, which produce truck-mounted and portable fire pumps, stainless steel valves, monitors, apparatus valves, nozzles, foam and compressed air foam systems, pump modules and pump kits, electronic controls and information systems, conventional and networked electrical systems, mechanical components for the fire, rescue and specialty vehicle markets, hydraulic, battery, gas and electric-operated rescue equipment, hydraulic re-railing equipment, hydraulic tools for industrial applications, recycling cutters, pneumatic lifting and sealing bags for vehicle and aircraft rescue, environmental protection and disaster control and shoring equipment for vehicular or structural collapse. Fire & Safety’s customers are OEMs as well as public and private fire and rescue organizations. Fire & Safety maintains facilities in Ocala, Florida (Class 1 and Hale products); Warwick, England (Godiva products); Wooster and Columbus, Ohio (Akron Brass and Weldon products); Ballendorf, Germany (AWG Fittings products); Shelby, North Carolina (Hurst Jaws of Life products); Tianjin, China (Dinglee products); Erlangen, Germany (Lukas products); and Zulpich, Germany (Vetter products). Approximately 50% of Fire & Safety’s 2020 sales were to customers outside the U.S.

7

BAND-IT. BAND-IT is a leading producer of high-quality stainless steel banding, buckles and clamping systems. The BAND-IT brand is highly recognized worldwide. BAND-IT products are used for securing exhaust system heat and sound shields, industrial hose fittings, traffic signs and signals, electrical cable shielding, identification and bundling and in numerous other industrial and commercial applications. BAND-IT products primarily serve the automotive, transportation equipment, oil and gas, general industrial maintenance, electronics, electrical, communications, aerospace, utility, municipal and subsea marine markets. BAND-IT is based in Denver, Colorado, with additional operations in Staveley, England. Approximately 44% of BAND-IT’s 2020 sales were to customers outside the U.S.

Dispensing. Dispensing produces precision equipment for dispensing, metering and mixing colorants and paints used in a variety of retail and commercial businesses around the world. Dispensing is a global supplier of precision-designed tinting, mixing, dispensing and measuring equipment for auto refinishing and architectural paints. Dispensing products are used in retail and commercial stores, hardware stores, home centers, department stores, automotive body shops as well as point-of-purchase dispensers. Dispensing maintains facilities in Sassenheim, The Netherlands, Wheeling, Illinois, Unanderra, Australia and Milan, Italy as well as IDEX shared manufacturing facilities in India and China. Approximately 66% of Dispensing’s 2020 sales were to customers outside the U.S.

INFORMATION APPLICABLE TO THE COMPANY’S BUSINESS IN GENERAL AND ITS SEGMENTS

Competitors

The Company’s businesses participate in highly competitive markets. IDEX believes that the principal points of competition are product quality, design and engineering capabilities, product development, conformity to customer specifications, quality of post-sale support, timeliness of delivery and effectiveness of our distribution channels.

Principal competitors of the Fluid & Metering Technologies segment are the Pumps Group (Maag, Blackmer and Wilden products) of Dover Corporation (with respect to pumps and small horsepower compressors used in liquefied petroleum gas distribution facilities, rotary gear pumps and air-operated double-diaphragm pumps); Milton Roy LLC (with respect to metering pumps and controls); and Tuthill Corporation (with respect to rotary gear pumps).

Principal competitors of the Health & Science Technologies segment are the Thomas division of Ingersoll Rand (with respect to vacuum pumps and compressors); Thermo Scientific Dionex products (with respect to analytical instrumentation); Parker Hannifin (with respect to sealing devices); Valco Instruments Co., Inc. (with respect to fluid injectors and valves); and Gooch & Housego PLC (with respect to electro-optic and precision photonics solutions used in the life sciences market).

The principal competitors of the Fire & Safety/Diversified Products segment are Waterous Company, a unit of American Cast Iron Pipe Company (with respect to truck-mounted firefighting pumps); Holmatro, Inc. (with respect to rescue tools); Corob S.p.A. (with respect to dispensing and mixing equipment for the paint industry); and Panduit Corporation (with respect to stainless steel bands, buckles and clamping systems).

Customers

None of our customers in 2020 accounted for more than two percent of net sales.

Employees

At December 31, 2020, the Company had 7,075 employees. Approximately 7% of its employees in the U.S. were represented by labor unions, with various contracts expiring through November 2023. Management believes that the Company has a positive relationship with its employees. The Company historically has been able to renegotiate its collective bargaining agreements satisfactorily, with its last work stoppage occurring in March 1993.

Human Capital Management

We recognize that our success would not be possible without the valuable contributions of our workforce. Investment in our people enables us to accomplish our goals and deliver innovative customer solutions. Our corporate Human Capital strategy is overseen by our Chief Human Resource Officer (“CHRO”). Annually, the CHRO presents a talent review to the Company’s Board of Directors. As part of the review, the team details each enterprise-level senior leadership position and outlines succession plans to ensure the Board is informed of the Company’s plans for business continuity and success.

8

Our workforce advancement strategy succeeds through investment in three pillars: skill-building for the entire workforce, leadership development aligned with the Company’s methodology and fostering a great culture. Our approach to training and education helps drive long-term value by providing our employees with opportunities to develop skills both individually and as teams:

•Employees have access to learning through a variety of sources, including the IDEX Academy, which is our primary platform for global leadership development programs, local development programs and specific individual development plans. These trainings also help to develop future and potential leaders in the IDEX leadership methodology.

•We also enable employee development and growth by offering our full-time U.S. employees who have at least six months of service the ability to participate in our Tuition Reimbursement program. Through the program, employees can have certain expenses from secondary educational institutions reimbursed up to $5,250 per year.

•The Company also built the IDEX Accelerating Management Potential (“I-AMP”) Collegiate Talent Program in 2018 to give early career professionals the opportunity to learn the Company’s values and business, and to grow within our Company in both full-time and internship roles. Since the program began, over 75 percent of participants have represented either gender or ethnic minority groups, and we will continue our focus on providing opportunities for diverse early career professionals through I-AMP.

•We prioritize hiring team members who will embrace our team-driven culture and also place considerable emphasis on leveraging the talented employees within our internal pipeline, filling many leadership positions with Company employees.

•Across the enterprise, our goal is to achieve manufacturing company top quartile employee engagement as measured by our engagement survey. Given the challenges that the COVID-19 pandemic brought to the work environment, we are thrilled that our employees are staying engaged as we remain in the 85th percentile among manufacturing companies with employee engagement at 78%.

Employee Pay and Benefits

Attracting and retaining top talent is critical to the success of the Company’s business. We offer a highly competitive pay and benefits package for our employees in all the markets where we operate. The performance-based pay packages provide many employees with short-term performance incentives. We also provide equity-based, long-term incentives to the Company’s senior leaders.

The Company’s U.S. employees can participate in two 401(k) retirement plans and the Employee Stock Purchase Plan, which allows an employee to purchase IDEX stock through payroll deductions.

Diversity, Equity & Inclusion

The Company has always recognized diversity as foundational to creativity and resilience; the three pillars of Innovation, Diversity and Excellence form the acronym that is our name, IDEX. Gender, ethnic, cultural and other human diversity is critical to our success.

In 2020, the Company engaged a Diversity, Equity & Inclusion (“DE&I”) coach to work with the CEO and entire Executive Leadership Team to further the DE&I strategic framework. In 2021, the Company intends to fill the currently vacant executive role for DE&I, which will report directly to the CEO.

At least once per year, the Board of Directors reviews employee diversity performance through its CHRO-led senior talent review. Additionally, the Company tracks diversity performance of the top 400 leaders and provides regular updates to the Board on how leadership demographics are changing over time. The Board has also recently pledged to include a DE&I topic on the agenda of every regularly scheduled Board meeting moving forward. In 2020, we increased representation for both women and people of color in our leadership ranks. Since 2018, we have increased the number of senior leaders globally who are women by more than 27% and leaders in the U.S. who are racially or ethnically diverse of color by 23%.

Further, the Company has been conducting pay equity analysis for U.S. employees since 2018 to ensure that employees’ actual pay was substantially similar to their predicted pay. Where appropriate, we provided base pay adjustments for employees that were outliers from their predicted pay, further reinforcing the Company’s commitment to diversity and a culture of inclusion, equality and respect.

Workplace Health & Safety

We are proud to manufacture product components that save lives; this would not be possible without the health and safety of our employees and contractors. The Company’s Employee Health & Safety (“EH&S”) Vision Policy outlines our approach for health and safety governance and applies to all of the Company’s business units and provides for both monthly and annual

9

risk assessments which are reviewed by the Company’s senior leaders. We also require safety trainings on topics such as CPR, electrical safety, ergonomics, first aid and machine guarding that all business unit employees must complete every year.

We also encourage all our full-time employees enrolled in our U.S. Healthcare Benefit Plan to participate in our third-party operated Wellness Program which provides access to annual biometric screenings, health evaluations and wellness credits that can be earned for meeting individual wellness goals each year. A number of our business units organize complementary wellness programs, including walking clubs, health fairs and lunch and learns with nutritionists for their employees.

At the beginning of the COVID-19 pandemic, we acted quickly, forming the IDEX COVID-19 Task Force to protect our employees from the virus, focusing on our safety-first approach. Among other safety measures, we also implemented COVID-19 Temporary Pay and Benefits Policy for employees who regularly work 20 or more hours per week, which provided four weeks of leave with 100% pay and benefits, in order to assist employees impacted by COVID-19 circumstances with additional flexibility.

Suppliers

The Company manufactures many of the parts and components used in its products. Substantially all materials, parts and components purchased by the Company are available from multiple sources.

Inventory and Backlog

The Company regularly and systematically adjusts production schedules and quantities based on the flow of incoming orders. Backlogs typically are limited to two months of production. While total inventory levels also may be affected by changes in orders, the Company generally tries to maintain relatively stable inventory levels based on its assessment of the requirements of the various industries served.

Raw Materials

The Company uses a wide variety of raw materials which are generally available from a number of sources. As a result, shortages from any single supplier have not had, and are not likely to have a material impact on operations.

Shared Services

The Company has production facilities in Suzhou, China and Vadodara, India that support multiple business units. IDEX also has personnel in China, India, Dubai, Mexico, Latin America and Singapore that provide sales and marketing, product design and engineering and sourcing support to its business units as well as personnel in various locations in South America, the Middle East, Korea and Japan to support sales and marketing efforts of IDEX businesses in those regions.

Segment Information

For segment financial information for the years 2020, 2019 and 2018, including financial information about foreign and domestic sales and operations, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and Note 14 of the Notes to Consolidated Financial Statements in Part II, Item 8, “Financial Statements and Supplementary Data.”

10

Information about Our Executive Officers

Set forth below are the names of the executive officers of the Company, their ages, years of service, the positions held by them and their business experience during the past five years.

| Name | Age | Years of Service | Position | |||||||||||||||||

| Eric D. Ashleman | 53 | 12 | Chief Executive Officer and President | |||||||||||||||||

| William K. Grogan | 42 | 9 | Senior Vice President and Chief Financial Officer | |||||||||||||||||

| Denise R. Cade | 58 | 5 | Senior Vice President, General Counsel and Corporate Secretary | |||||||||||||||||

| Melissa S. Flores | 38 | 10 | Senior Vice President-Chief Human Resources Officer | |||||||||||||||||

| Daniel J. Salliotte | 54 | 16 | Senior Vice President-Corporate Development | |||||||||||||||||

| Michael J. Yates | 55 | 15 | Vice President and Chief Accounting Officer | |||||||||||||||||

Mr. Ashleman has served as President and Chief Executive Officer since December 2020. Prior to that, Mr. Ashleman was Senior Vice President and Chief Operating Officer from July 2015 to December 2020, Vice President-Group Executive of the Company’s Health & Science Technologies and Fire & Safety/Diversified Products segments from January 2014 through July 2015 and President-Group Executive of the Company’s Fire & Safety/Diversified Products segment from 2011 through January 2014. Mr. Ashleman joined IDEX in 2008 as the President of Gast Manufacturing.

Mr. Grogan has served as Senior Vice President and Chief Financial Officer since January 2017. Prior to that, Mr. Grogan served as Vice President of Finance, Operations from July 2015 through January 2017. From January 2012 through July 2015, Mr. Grogan was Vice President-Finance for the Company’s Health & Science Technologies and Fire & Safety/Diversified Products segments.

Ms. Cade has served as Senior Vice President, General Counsel and Corporate Secretary since joining IDEX in October 2015. Prior to joining IDEX, Ms. Cade was Senior Vice President, General Counsel, Corporate Secretary and Chief Compliance Officer for SunCoke Energy, Inc. from March 2011 to October 2015 and held various roles at PPG Industries, Inc. before joining SunCoke.

Ms. Flores has served as Senior Vice President and Chief Human Resources Officer since February 2021. Prior to that, Ms. Flores served as Global, Vice President Talent from May 2019 through February 2021. From February 2018 through May 2019, Ms. Flores was Group Vice President Human Resources. Prior to that she served as Vice President, Talent Management and Development from March 2017 to February 2018, after being promoted from Director, Talent Development, a position she served in from March 2015 to March 2017.

Mr. Salliotte has served as Senior Vice President-Corporate Development since March 2018. Prior to that, Mr. Salliotte served as Senior Vice President-Corporate Strategy, Mergers & Acquisitions and Treasury since February 2011. Mr. Salliotte joined IDEX in October 2004 as Vice President-Strategy and Business Development.

Mr. Yates has served as Vice President and Chief Accounting Officer since February 2010 and served as interim Chief Financial Officer from September 2016 to December 2016. Mr. Yates joined IDEX as Vice President-Controller in October 2005.

The Company’s executive officers are elected at a meeting of the Board of Directors immediately following the annual meeting of stockholders, and they serve until the meeting of the Board immediately following the next annual meeting of stockholders, or until their successors are duly elected and qualified or until their death, resignation or removal.

Public Filings

Copies of the Company’s annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports are made available free of charge at www.idexcorp.com as soon as reasonably practicable after being filed electronically with the United States Securities and Exchange Commission (the “SEC”). Our reports are also available free of charge on the SEC’s website, www.sec.gov. Information on the Company’s website is not incorporated into this Form 10-K.

11

Item 1A. Risk Factors.

For an enterprise as diverse and complex as the Company, a wide range of factors present risks to the Company and could materially affect future developments and performance. In addition to the factors affecting specific business operations identified in connection with the description of our operations and the financial results of our operations elsewhere in this report, the most material of these factors are included below. Current global economic events and conditions may amplify many of these risks. These risks are not the only risks that may affect us. Additional risks that we are not aware of or do not believe are material at the time of this filing may also become important factors that adversely affect our business.

Risks Related to Our Operations

Our business, results of operations and financial condition have been and may continue to be materially adversely impacted by the ongoing COVID-19 pandemic.

The ongoing COVID-19 pandemic has been a rapidly-changing situation that has negatively impacted and could continue to negatively impact the global economy. Our operating results are subject to fluctuations based on general economic conditions and have been adversely affected by the negative general economic conditions. The extent to which COVID-19 continues to impact our business will depend on future developments, which are highly uncertain and cannot be predicted with confidence, such as the duration of the outbreak and business closures or business disruptions for our Company, our suppliers and our customers.

The deterioration in economic conditions materially reduced, and could continue to reduce, the Company’s sales and profitability. Although we began to see improvement in our end markets beginning in the third quarter of 2020 and continuing through the fourth quarter of 2020, the financial distress our customers have experienced due to the deterioration in economic conditions has resulted in and could continue to result in reduced sales which has and could continue to negatively impact our results of operations. Any changes in or resurgence of the COVID-19 outbreak could also have a material impact on our ability to get the raw materials, parts and components we need to manufacture our products as our suppliers face disruptions in their businesses, closures or bankruptcy as a result of the COVID-19 outbreak. We depend greatly on our suppliers for items that are essential to the manufacturing of our products. Although we have not experienced material supply chain disruptions to date, if our suppliers fail to meet our manufacturing needs in the future, it would delay our production and our product shipments to customers and negatively affect our operations.

U.S and international government responses to the COVID-19 outbreak have included “shelter in place”, “stay at home” and similar types of orders. These orders exempt certain individuals needed to maintain continuity of operations of critical infrastructure sectors as determined by the U.S. federal and international governmental bodies. Although the Company’s operations are currently considered essential and exempt, if any of the applicable exemptions are curtailed or revoked in the future, including in response to any COVID-19 resurgence, that would adversely impact our business, operating results and financial condition. Furthermore, to the extent these exemptions do not extend to our key suppliers and customers, this would also adversely impact our business, operating results and financial condition. We have also implemented work-from-home policies for certain “non-essential” employees. Although these work-from-home policies have not negatively impacted our business in any material respect to date, the COVID-19 outbreak is dynamic and any future resurgences could negatively impact productivity, disrupt conduct of our business in the ordinary course and delay our production timelines.

Due to the large remote workforce populations, we may also face informational technology infrastructure and connectivity issues from the vendors that we rely on for certain information technologies to administer, store and support the Company’s multiple business activities. IDEX is heavily dependent on the availability and support of our technology landscape, several of which are provided by external third party service providers (e.g., Microsoft, AT&T and Verizon). Although we have not suffered any disruptions to date, any future disruptions in their operations could also negatively impact our business, operating results and financial condition.

To the extent the COVID-19 outbreak continues to adversely affect our business and financial results, it may also have the effect of heightening many of the other risks described in Item 1A, “Risk Factors” of this annual report, such as those relating to our international operations, our ability to develop new products, our ability to execute on our growth strategy of acquisitions, our dependency on raw materials, parts and components, the effects on movements in foreign currency exchange rates on our Company, the effects on our Company that result from declines in commodity prices and our reliance on labor availability to operate and grow our business.

12

Our Inability to Continue to Develop New Products Could Limit Our Sales Growth.

Our ability to continue to grow organically is tied in large part to our ability to continue to develop new products. A failure to continue to develop and deliver new, innovative and competitive products to the market could limit our sales growth and negatively impact our business, financial condition, results of operations and cash flow.

Our Growth Strategy Includes Acquisitions and We May Not be Able to Make Acquisitions of Suitable Candidates or Integrate Acquisitions Successfully.

Our historical growth has included, and our future growth is likely to continue to include, acquisitions. We intend to continue to seek acquisition opportunities both to expand into new markets and to enhance our position in existing markets throughout the world. We may not be able to successfully identify suitable candidates, negotiate appropriate acquisition terms, obtain financing needed to consummate those acquisitions, complete proposed acquisitions or successfully integrate acquired businesses into our existing operations. In addition, any acquisition, once successfully integrated, may not perform as planned, be accretive to earnings, or otherwise prove beneficial to us.

Acquisitions involve numerous risks, including the assumption of undisclosed or unindemnified liabilities, difficulties in the assimilation of the operations, technologies, services and products of the acquired companies and the diversion of management’s attention from other business concerns. In addition, prior acquisitions have resulted in, and future acquisitions could result in, the incurrence of substantial additional indebtedness and other expenses.

The Markets We Serve are Highly Competitive and this Competition Could Reduce our Sales and Operating Margins.

Most of our products are sold in competitive markets. Maintaining and improving our competitive position will require continued investment by us in manufacturing, engineering, quality standards, marketing, customer service and support and our distribution networks. We may not be successful in maintaining our competitive position. Our competitors may develop products that are superior to our products or may develop methods of more efficiently and effectively providing products and services or may adapt more quickly than us to new technologies or evolving customer requirements. Pricing pressures may require us to adjust the prices of our products to stay competitive. We may not be able to compete successfully with our existing competitors or with new competitors. Failure to continue competing successfully could reduce our sales, operating margins and overall financial performance.

We are Dependent on the Availability of Raw Materials, Parts and Components Used in Our Products.

While we manufacture certain parts and components used in our products, we require substantial amounts of raw materials and purchase some parts and components from suppliers. The availability and prices for raw materials, parts and components may be subject to curtailment or change due to, among other things, suppliers’ allocations to other purchasers, interruptions in production by suppliers, including due to geopolitical or civil unrest, unfavorable economic or industry conditions, labor disruptions, catastrophic weather events, natural disasters or the occurrence of a contagious disease or illness, changes in exchange rates and prevailing price levels. Any change in the supply of, or price for, these raw materials or parts and components could materially affect our business, financial condition, results of operations and cash flow.

Our Business Operations May Be Adversely Affected by Information Systems Interruptions or Intrusion.

We depend on various information technologies throughout our Company to administer, store and support multiple business activities. If these systems (or the systems of our customers or third-party hosting services) are damaged, cease to function properly or are subject to cyber-security attacks, such as those involving unauthorized access, malicious software and/or other intrusions, we could experience production downtimes, operational delays, other detrimental impacts on our operations or ability to provide products and services to our customers, the compromising of confidential or otherwise protected information, destruction or corruption of data, security breaches, other manipulation or improper use of our systems or networks, financial losses from remedial actions, loss of business or potential liability, penalties, fines and/or damage to our reputation. While we attempt to mitigate these risks by employing a number of measures, including employee training, technical security controls and maintenance of backup and protective systems, our systems, networks, products and services remain potentially vulnerable to known or unknown threats, any of which could have a material adverse effect on our business, financial condition or results of operations. Further, given the unpredictability, nature and scope of cyber-security attacks, it is possible that potential vulnerabilities could go undetected for an extended period.

13

Risks Related to Economic Conditions

Changes in U.S. or International Economic Conditions Could Materially Adversely Affect the Sales and Profitability of Our Businesses.

In 2020, 49% of the Company’s sales were derived from domestic operations while 51% were derived from international operations. The Company’s largest end markets include industrial, semiconductor, automotive, life sciences and medical technologies, fire and rescue, oil and gas, paint and coatings, chemical processing, agriculture, water and wastewater treatment and optical filters and components. A slowdown in the U.S. or global economy and, in particular, any of these specific end markets could materially reduce the Company’s sales and profitability.

Changes to Geopolitical and Economic Conditions in the U.S. and Foreign Countries in Which We Operate Could Adversely Affect Our Business.

In 2020, approximately 51% of our total sales were to customers outside the U.S. We expect our international operations and export sales to continue to be significant for the foreseeable future. Our sales from international operations and our sales from export are both subject in varying degrees to risks inherent in doing business outside the U.S. These risks include the following:

•possibility of unfavorable circumstances arising from host country laws or regulations;

•risks of economic instability;

•currency exchange rate fluctuations and restrictions on currency repatriation;

•potential negative consequences from changes to taxation policies;

•disruption of operations from labor and political disturbances;

•withdrawal from or renegotiation of international trade agreements and other restrictions on the trade between the United States and other countries;

•risks related to other government regulation or required compliance with local laws;

•effects of the United Kingdom’s decision to exit the European Union and related potential disruption to trade, including the effects of the Trade and Cooperation Agreement between the European Union, the European Atomic Energy Community and the United Kingdom signed on December 30, 2020;

•changes in tariff and trade barriers, including uncertainty caused by the evolving relations between the United States and China; and

•geopolitical events, including natural disasters, public health issues, political instability, terrorism, insurrection or war.

Any of these events could have a materially adverse impact on our business and operations.

Significant Movements in Foreign Currency Exchange Rates May Harm Our Financial Results.

We are exposed to fluctuations in foreign currency exchange rates, particularly with respect to the Euro, Swiss Franc, Canadian Dollar, British Pound, Indian Rupee, Chinese Renminbi and Swedish Krona. Any significant change in the value of the currencies of the countries in which we do business against the U.S. Dollar could affect our ability to sell products competitively and control our cost structure, which could have a material adverse effect on our results of operations. For additional detail related to this risk, see Part II, Item 7A, “Quantitative and Qualitative Disclosures About Market Risk.”

Fluctuations in Interest Rates Could Adversely Affect Our Results of Operations and Financial Position.

Our profitability may be adversely affected during any periods of unexpected or rapid increases in interest rates. We maintain a revolving credit facility, which bears interest at either an alternate base rate or adjusted LIBOR plus, in each case, an applicable margin based on the lower of the Company's senior, unsecured, long-term debt rating or the Company’s applicable leverage ratio. A significant increase in LIBOR would significantly increase our cost of borrowings. Further, any changes in regulatory standards or industry practices, such as the expected transition away from LIBOR may result in the usage of higher interest rates under our revolving credit facility, and our current or future indebtedness may be adversely affected.We are also exposed to risks if the U.S. Federal Reserve raises its benchmark interest rate, which may reduce the availability and increase the cost of obtaining new debt and refinancing existing indebtedness. For additional detail related to this risk, see Part II, Item 7A, "Quantitative and Qualitative Disclosures About Market Risk."

14

A Significant or Sustained Decline in Commodity Prices, Including Oil, Could Negatively Impact the Levels of Expenditures by Certain of Our Customers.

Demand for our products depends, in part, on the level of new and planned expenditures by certain of our customers. The level of expenditures by our customers is dependent on, among other factors, general economic conditions, availability of credit, economic conditions within their respective industries and expectations of future market behavior. Volatility in commodity prices, including oil, can negatively affect the level of these activities and can result in postponement of capital spending decisions or the delay or cancellation of existing orders. The ability of our customers to finance capital investment and maintenance may also be affected by the conditions in their industries. Reduced demand for our products could result in the delay or cancellation of existing orders or lead to excess manufacturing capacity, which unfavorably impacts our absorption of fixed manufacturing costs. This reduced demand could have a material adverse effect on our business, financial condition and results of operations.

Risks Related to Legal, Accounting and Regulatory Matters

An Unfavorable Outcome of Any of Our Pending Contingencies or Litigation Could Adversely Affect Us.

We are currently involved in pending and threatened legal, regulatory and other proceedings arising in the ordinary course of business. These proceedings may pertain to matters such as product liability or contract disputes, and may also involve governmental inquiries, inspections, audits or investigations relating to issues such as tax matters, intellectual property, environmental, health and safety issues, governmental regulations, employment and other matters. Where it is reasonably possible to do so, we accrue estimates of the probable costs for the resolution of these matters. These estimates are developed in consultation with outside counsel and are based upon an analysis of potential results and the availability of insurance coverage, assuming a combination of litigation and settlement strategies. It is possible, however, that future operating results for any particular quarter or annual period could be materially affected by changes in our assumptions, the continued availability of insurance coverage or the effectiveness of our strategies related to these proceedings. For additional detail related to this risk, see Item 3, “Legal Proceedings” and Note 11 in Part II, Item 8, “Financial Statements and Supplementary Data.”

Our Intangible Assets, Including Goodwill, are a Significant Portion of Our Total Assets and a Write-off of Our Intangible Assets or Goodwill Would Adversely Impact Our Operating Results and Significantly Reduce Our Net Worth.

Our total assets reflect substantial intangible assets, primarily goodwill and identifiable intangible assets. At December 31, 2020, goodwill and intangible assets totaled $1,895.6 million and $415.6 million, respectively. These assets primarily result from our acquisitions, representing the excess of the purchase price over the fair value of the tangible net assets we have acquired. Annually, or when certain events occur that require a more current valuation, we assess whether there has been an impairment in the value of our goodwill and identifiable intangible assets. If future operating performance at one or more of our reporting units were to fall significantly below forecasted levels, we could be required to reflect, under current applicable accounting rules, a non-cash charge to operating income for an impairment. Any determination requiring the write-off of a significant portion of our goodwill or identifiable intangible assets would adversely impact our results of operations and net worth. See Note 6 in Part II, Item 8, “Financial Statements and Supplementary Data” for further discussion on goodwill and intangible assets.

Failure To Comply with the U.S. Foreign Corrupt Practices Act, the U.K. Bribery Act or Other Applicable Anti-bribery Laws Could Have an Adverse Effect on Our Business.

The U.S. Foreign Corrupt Practices Act, the U.K. Bribery Act and similar anti-bribery laws in other jurisdictions generally prohibit companies and their intermediaries from making improper payments for the purpose of obtaining or retaining business. Recent years have seen a substantial increase in anti-bribery law enforcement activity with more frequent and aggressive investigations and enforcement proceedings by both the Department of Justice and the SEC, increased enforcement activity by non-U.S. regulators and increases in criminal and civil proceedings brought against companies and individuals. Our policies mandate compliance with all anti-bribery laws. However, we operate in certain countries that are recognized as having governmental and commercial corruption. Our internal control policies and procedures may not always protect us from reckless or criminal acts committed by our employees or third-party intermediaries. Violations of these anti-bribery laws may result in criminal or civil sanctions, which could have a material adverse effect on our business, financial condition and results of operations.

15

General Risk Factors

Our Success Depends on Our Executive Management and Other Key Personnel.

Our future success depends to a significant degree on the skills, experience and efforts of our executive management and other key personnel and their ability to provide the Company with uninterrupted leadership and direction. The loss of the services of any of our executive officers or a failure to provide adequate succession plans for key personnel could have an adverse impact. The availability of highly qualified talent is limited and the competition for talent is robust. However, we provide long-term equity incentives and certain other benefits for our executive officers which provide incentives for them to make a long-term commitment to our Company. Our future success will also depend on our ability to have adequate succession plans in place and to attract, retain and develop qualified personnel. A failure to efficiently replace executive management members and other key personnel and to attract, retain and develop new qualified personnel could have an adverse effect on our operations and implementation of our strategic plan.

Challenges with Respect to Labor Availability Could Negatively Impact our Ability to Operate or Grow our Business.

Our success depends in part on the ability of our businesses to proactively attract, motivate and retain a qualified and highly skilled workforce in an intensely competitive labor market. A failure to attract, motivate and retain highly skilled personnel could adversely affect our operating results or our ability to operate or grow our business. Additionally, any labor stoppages or labor disruptions, including due to geopolitical unrest, unfavorable economic or industry conditions, catastrophic weather events, natural disasters or the occurrence of a contagious disease or illness could adversely affect our operating results or our ability to operate or grow our business.

Item 1B. Unresolved Staff Comments.

None.

Item 2. Properties.

The Company’s principal plants and offices have an aggregate floor space area of approximately 4.9 million square feet, of which 3.2 million square feet (66%) are located in the U.S. and approximately 1.7 million square feet (34%) are located outside the U.S., primarily in Germany (10%), U.K. (7%), Italy (5%), India (3%), China (2%), Canada (2%) and The Netherlands (2%). Management considers these facilities suitable and adequate for the Company’s operations. Management believes the Company can meet demand increases over the near term with its existing facilities, especially given its operational improvement initiatives that usually increase capacity. The Company’s executive office occupies 40,261 square feet of leased space in Northbrook, Illinois and 16,268 square feet of leased space in Chicago, Illinois.

Approximately 2.9 million square feet (60%) of the principal plant and office floor area are owned by the Company and the balance is held under lease. Approximately 1.8 million square feet (36%) of the principal plant and office floor area are held by business units in the Fluid & Metering Technologies segment; 1.4 million square feet (29%) are held by business units in the Health & Science Technologies segment; and 1.5 million square feet (30%) are held by business units in the Fire & Safety/Diversified Products segment. The remaining 0.2 million square feet (5%) include the executive office as well as shared services locations.

16

Item 3. Legal Proceedings.

The Company and its subsidiaries are party to legal proceedings as described in Note 11 in Part II, Item 8, “Commitments and Contingencies,” and such disclosure is incorporated by reference into this Item 3, “Legal Proceedings.” In addition, the Company and six of its subsidiaries are presently named as defendants in a number of lawsuits claiming various asbestos-related personal injuries, allegedly as a result of exposure to products manufactured with components that contained asbestos. These components were acquired from third party suppliers and were not manufactured by the Company or any of the defendant subsidiaries. To date, the majority of the Company’s settlements and legal costs, except for costs of coordination, administration, insurance investigation and a portion of defense costs, have been covered in full by insurance, subject to applicable deductibles. However, the Company cannot predict whether and to what extent insurance will be available to continue to cover these settlements and legal costs, or how insurers may respond to claims that are tendered to them. Asbestos-related claims have been filed in jurisdictions throughout the United States and the United Kingdom. Most of the claims resolved to date have been dismissed without payment. The balance of the claims have been settled for various immaterial amounts. Only one case has been tried, resulting in a verdict for the Company’s business unit. No provision has been made in the financial statements of the Company, other than for insurance deductibles in the ordinary course, and the Company does not currently believe the asbestos-related claims will have a material adverse effect on the Company’s business, financial position, results of operations or cash flows.

Item 4. Mine Safety Disclosures.

Not applicable.

17

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

The Company’s common stock trades on the New York Stock Exchange under the symbol “IEX”. As of February 22, 2021, there were approximately 5,629 stockholders of record of our common stock and there were 75,889,737 shares outstanding.

Our payment of dividends in the future will be determined by our Board of Directors and will depend on business conditions, our earnings and other factors.

For information pertaining to securities authorized for issuance under equity compensation plans and the related weighted average exercise price, see Part III, Item 12, “Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters.”

The Company did not purchase any shares of common stock during the quarter ended December 31, 2020. As of December 31, 2020, the amount of share repurchase authorization remaining was $712.0 million.

On March 17, 2020, the Company’s Board of Directors approved an increase of $500.0 million in the authorized level of repurchases of common stock. This approval is in addition to the prior repurchase authorizations of the Board of Directors of $300.0 million on December 1, 2015 and $400.0 million on November 6, 2014. These authorizations have no expiration date.

18

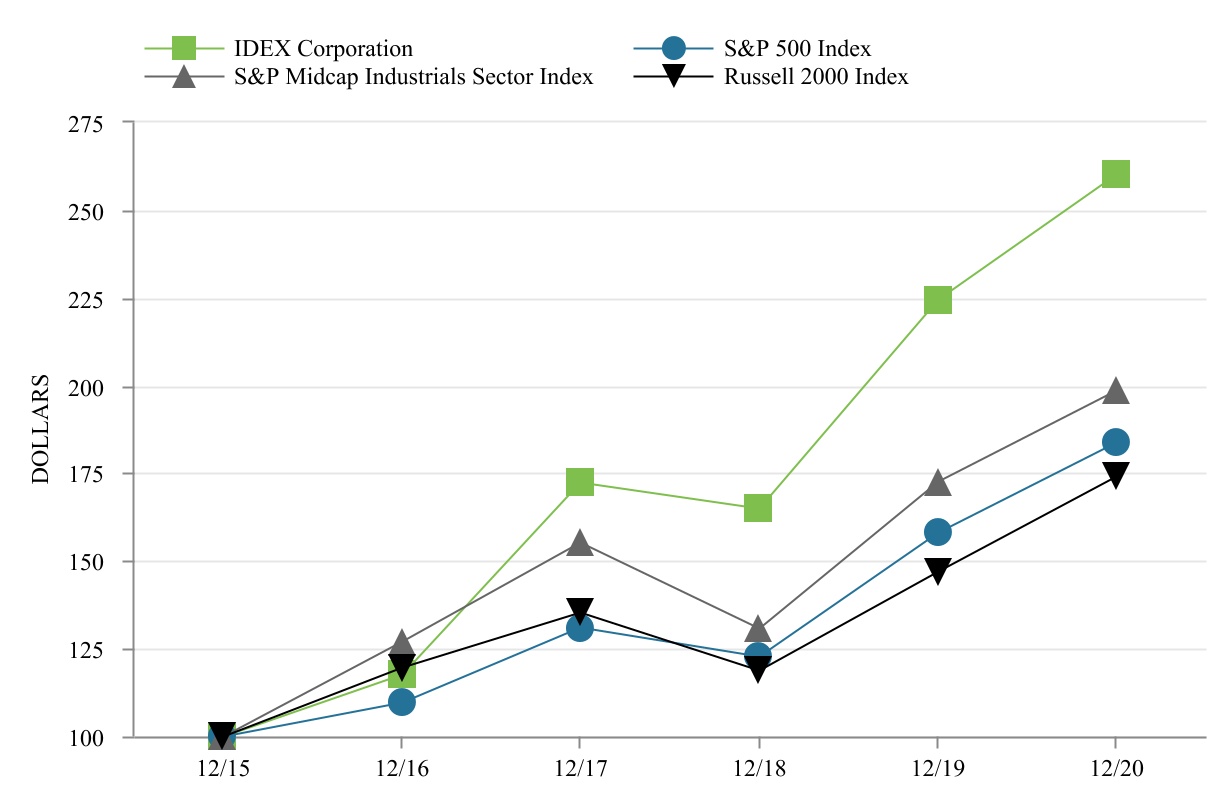

Performance Graph. The following table compares total stockholder returns over the last five years to the Standard & Poor’s (the “S&P”) 500 Index, the S&P Midcap Industrials Sector Index and the Russell 2000 Index assuming the value of the investment in our common stock and each index was $100 on December 31, 2015. Total return values for our common stock, the S&P 500 Index, S&P Midcap Industrials Sector Index and the Russell 2000 Index were calculated on cumulative total return values assuming reinvestment of dividends. The stockholder return shown on the graph below is not necessarily indicative of future performance.

| 12/15 | 12/16 | 12/17 | 12/18 | 12/19 | 12/20 | |||||||||||||||

| IDEX Corporation | $ | 100.00 | $ | 117.56 | $ | 172.26 | $ | 164.81 | $ | 224.51 | $ | 260.02 | ||||||||

| S&P 500 Index | $ | 100.00 | $ | 109.54 | $ | 130.81 | $ | 122.65 | $ | 158.07 | $ | 183.77 | ||||||||

| S&P Midcap 400 Industrials Sector Index | $ | 100.00 | $ | 127.07 | $ | 155.26 | $ | 130.62 | $ | 172.42 | $ | 198.59 | ||||||||

| Russell 2000 Index | $ | 100.00 | $ | 119.48 | $ | 135.18 | $ | 118.72 | $ | 146.89 | $ | 173.86 | ||||||||

The information contained in this Performance Graph section shall not be deemed to be “soliciting material” or “filed” with the SEC, nor shall such information be incorporated by reference into any future filing under the Securities Act of 1933 or the Securities Exchange Act of 1934.

19

Item 6. Selected Financial Data.(1)

| (Dollars in thousands, except per share data) | 2020 | 2019 | 2018 | 2017 | 2016 | ||||||||||||||||||||||||

| RESULTS OF OPERATIONS | |||||||||||||||||||||||||||||

| Net sales | $ | 2,351,646 | $ | 2,494,573 | $ | 2,483,666 | $ | 2,287,312 | $ | 2,113,043 | |||||||||||||||||||

| Gross profit | 1,027,424 | 1,125,034 | 1,117,895 | 1,026,678 | 930,767 | ||||||||||||||||||||||||

| Selling, general and administrative expenses | 494,935 | 524,987 | 536,724 | 524,940 | 492,398 | ||||||||||||||||||||||||

| Loss (gain) on sale of businesses - net | — | — | — | (9,273) | 22,298 | ||||||||||||||||||||||||

| Restructuring expenses and asset impairments | 11,776 | 21,044 | 12,083 | 8,455 | 3,674 | ||||||||||||||||||||||||

| Operating income | 520,713 | 579,003 | 569,088 | 502,556 | 412,397 | ||||||||||||||||||||||||

| Other (income) expense - net | 5,627 | 1,759 | (3,985) | 2,394 | (1,731) | ||||||||||||||||||||||||

| Interest expense | 44,746 | 44,341 | 44,134 | 44,889 | 45,616 | ||||||||||||||||||||||||

| Provision for income taxes | 92,562 | 107,382 | 118,366 | 118,016 | 97,403 | ||||||||||||||||||||||||

| Net income | 377,778 | 425,521 | 410,573 | 337,257 | 271,109 | ||||||||||||||||||||||||

Earnings per share: (2) | |||||||||||||||||||||||||||||

| — basic | $ | 4.98 | $ | 5.62 | $ | 5.36 | $ | 4.41 | $ | 3.57 | |||||||||||||||||||

| — diluted | $ | 4.94 | $ | 5.56 | $ | 5.29 | $ | 4.36 | $ | 3.53 | |||||||||||||||||||

| Weighted average shares outstanding: | |||||||||||||||||||||||||||||

| — basic | 75,741 | 75,594 | 76,412 | 76,232 | 75,803 | ||||||||||||||||||||||||