UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

10-K

(Mark

One)

[x] ANNUAL

REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE

SECURITIES EXCHANGE ACT OF 1934

For

the fiscal year ended December 31, 2004

OR

[

] TRANSITION

REPORT PURSUANT TO SECTION 13 OR 15(d)

OF

THE SECURITIES EXCHANGE ACT OF 1934

For

the transition period from .......... to ..........

Commission

file number 1-9916

Freeport-McMoRan

Copper & Gold Inc.

(Exact

name of registrant as specified in its charter)

|

Delaware |

74-2480931 | |||

|

(State

or other jurisdiction of incorporation or

organization) |

(I.R.S.

Employer Identification No.) |

|

1615

Poydras Street |

||||

|

New Orleans,

Louisiana 70112 |

|

70112 | ||

|

(Address

of principal executive offices) |

(Zip

Code) |

Registrant’s

telephone number, including area code: (504) 582-4000

Securities

registered pursuant to Section 12(b) of the Act:

|

Title

of each class |

Name

of each exchange on which registered | |

|

Class

B Common Stock, par value $0.10 per share |

New

York Stock Exchange | |

|

Depositary

Shares, Series II, representing 0.05 shares of Gold- |

||

|

Denominated

Preferred Stock, Series II, par value $0.10 per share |

New

York Stock Exchange | |

|

Depositary

Shares representing 0.00625 shares of Silver- |

||

|

Denominated

Preferred Stock, par value $0.10 per share |

New

York Stock Exchange | |

|

10⅛%

Senior Notes due 2010 of the registrant |

New

York Stock Exchange | |

|

7%

Convertible Senior Notes due 2011 of the registrant |

New

York Stock Exchange |

Securities

registered pursuant to Section 12(g) of the Act: None

Indicate

by check mark whether the registrant (1) has filed all reports required to be

filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

preceding 12 months (or for such shorter period that the registrant was required

to file such reports), and (2) has been subject to such filing requirements for

the past 90 days. Yes X No

__

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K is not contained herein, and will not be contained, to the best

of the registrant’s

knowledge, in definitive proxy or information statements incorporated by

reference in Part III of this Form 10-K or any amendment to this Form 10-K.

X

Indicate

by check mark whether the registrant is an accelerated filer (as defined in Rule

12b-2 of the Act). Yes X No

__

The

aggregate market value of classes of common stock held by non-affiliates of the

registrant was approximately $5.6 billion on March 1, 2005, and approximately

$4.9 billion on June 30, 2004.

On March

1, 2005, there were issued and outstanding 179,580,551 shares of Class B Common

Stock and on June 30, 2004, there were issued and outstanding 173,770,485

shares.

DOCUMENTS

INCORPORATED BY REFERENCE

Portions

of our Proxy Statement for our 2005 Annual Meeting to be held on May 5, 2005 are

incorporated by reference into Part III (Items 10, 11, 12, 13 and 14) of this

report.

|

TABLE

OF CONTENTS | |

|

Page | |

|

Part

I |

1 |

|

Items

1. and 2. Business and Properties |

1 |

|

Item

3. Legal Proceedings |

33 |

|

Item

4. Submission of Matters to a Vote of Security Holders |

33 |

|

Executive

Officers of the Registrant |

33 |

|

Part

II |

34 |

|

Item

5. Market for Registrant’s Common Equity, Related Stockholder Matters

and

Issuer Purchases of Equity Securities |

34 |

|

Item

6. Selected Financial Data |

35 |

|

Items

7. and 7A. Management’s Discussion and Analysis of Financial Condition and

Results

of

Operation and Quantitative and Qualitative Disclosures about Market

Risks |

35 |

|

Item

8. Financial Statements and Supplementary Data |

35 |

|

Item

9. Changes in and Disagreements with Accountants on Accounting and

Financial Disclosure |

35 |

|

Item

9A. Controls and Procedures |

35 |

|

Item

9B. Other Information |

36 |

|

Part

III |

36 |

|

Item

10. Directors and Executive Officers of the Registrant |

36 |

|

Item

11. Executive Compensation |

36 |

|

Item

12. Security Ownership of Certain Beneficial Owners and Management and

Related

Stockholder Matters |

36 |

|

Item

13. Certain Relationships and Related Transactions |

36 |

|

Item

14. Principal Accounting Fees and Services |

36 |

|

Part

IV |

36 |

|

Item

15. Exhibits and Financial Statement Schedules |

36 |

|

Signatures |

S-1 |

|

Index

to Financial Statements |

F-1 |

|

Exhibit

Index |

E-1 |

i

PART

I

Items

1. and 2. Business and Properties.

All

of our periodic report filings with the Securities and Exchange Commission (SEC)

pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as

amended, are available, free of charge, through our web site, www.fcx.com,

including our annual reports on Form 10-K, quarterly reports on Form 10-Q,

current reports on Form 8-K and any amendments to those reports. These reports

and amendments are available through our web site as soon as reasonably

practicable after we electronically file or furnish such material to the

SEC.

General

We have

one of the world’s largest

copper and gold mining and production operations in terms of reserves and

production. We are also one of the lowest-cost copper producers in the world,

after taking into account credits for related gold and silver production. Our

principal asset is the Grasberg minerals district. We discovered the largest ore

body in the district, Grasberg, in 1988. The Grasberg minerals district contains

the largest single gold reserve and the second-largest copper reserves of any

mine in the world.

Our

principal operating subsidiary is PT Freeport Indonesia, a limited liability

company organized under the laws of the Republic of Indonesia and incorporated

as a corporation in Delaware. We own approximately 90.64 percent of PT Freeport

Indonesia, and the Government of Indonesia owns the remaining approximate 9.36

percent. PT Freeport Indonesia mines, processes and explores for ore containing

copper, gold and silver. It operates in the remote highlands of the Sudirman

Mountain Range in the province of Papua, Indonesia, which is on the western half

of the island of New Guinea. PT Freeport Indonesia markets its concentrates

containing copper, gold and silver worldwide.

PT

Freeport Indonesia conducts its operations pursuant to an agreement, called a

Contract of Work, with the Government of Indonesia (see “Contracts of Work”).

The Contract of Work allows us to conduct extensive mining, production and

exploration activities in a 24,700-acre area that we call Block A, which

contains the Grasberg minerals district, and governs our rights and obligations

relating to taxes, exchange controls, royalties, repatriation and other matters.

The Contract of Work also allows us to explore for minerals in an approximately

500,000-acre area that we call Block B. Exploration activities in Block B have

been suspended in recent years, but we are currently assessing the possible

timing for the resumption of those activities (see “Contracts of Work”). The

term of our Contract of Work expires in 2021, but we can extend it for two

10-year periods subject to Indonesian government approval, which cannot be

withheld or delayed unreasonably.

Another

of our operating subsidiaries, PT Irja Eastern Minerals, which we refer to as

Eastern Minerals, holds an additional Contract of Work in Papua covering

approximately 1.2 million acres and conducts exploration activities, which have

been suspended in recent years, under this Contract of Work (see “Contracts of

Work”). We are assessing the possible timing for the resumption of exploration

activities in Eastern Minerals’ exploration area. We have a 100 percent

ownership interest in Eastern Minerals.

In 1996,

we established joint ventures with Rio Tinto plc, which is an international

mining company with headquarters in London, England. Rio Tinto conducts mining

operations in North America, South America, Asia, Australia, Europe and southern

Africa. One of our joint ventures with Rio Tinto covers PT Freeport

Indonesia’s mining

operations in Block A. This joint venture gives Rio Tinto, through 2021, a 40

percent interest in certain assets and in production above specified levels from

operations in Block A and, after 2021, a 40 percent interest in all production

in Block A. Under our joint venture arrangements, Rio Tinto also has a 40

percent interest in PT Freeport Indonesia’s Contract

of Work and Eastern Minerals’ Contract

of Work. In addition, Rio Tinto has the option to participate in 40 percent of

any of our other future exploration projects in Papua. To date, Rio Tinto has

elected to participate in all exploration projects, including PT Nabire Bakti

Mining.

Under

another joint venture agreement through PT Nabire Bakti Mining, we conduct

exploration activities, which have been suspended in recent years (see

“Contracts of Work”), in an area covering approximately 500,000 acres in five

parcels contiguous to PT Freeport Indonesia’s Block B

and one of Eastern Minerals’ blocks.

We are assessing the possible timing for the resumption of exploration

activities in PT Nabire Bakti Mining’s

exploration area.

1

At

December 31, 2004, PT Freeport Indonesia’s share of

proven and probable recoverable reserves totaled 40.5 billion pounds of copper

and 46.5 million ounces of gold, all of which are located in Block A. Our

approximate 90.64 percent equity share of these proven and probable recoverable

reserves totaled 36.7 billion pounds of copper and 42.1 million ounces of gold

(see “Ore Reserves”). In this annual report, we refer to (1) aggregate reserves,

which means all reserves for the operations we manage, (2) PT Freeport

Indonesia’s share of

reserves, which means the reserves net of Rio Tinto’s interest

under our joint venture arrangements and which are the reserves reported as

those of our operations in our consolidated financial statements and (3) our

equity share of reserves, which means PT Freeport Indonesia’s share

net of the 9.36 percent interest that the Government of Indonesia

owns.

In July

2003, we acquired the 85.7 percent ownership interest in PT Puncakjaya Power

owned by affiliates of Duke Energy Corporation. Puncakjaya Power is the owner of

assets supplying power to PT Freeport Indonesia’s

operations, including the 3x65 megawatt coal-fired power facilities (see

“Infrastructure”).

We also

smelt and refine copper concentrates in Spain and market the refined copper

products through our wholly owned subsidiary, Atlantic Copper, S.A. In addition,

PT Freeport Indonesia has a 25 percent interest in PT Smelting, an Indonesian

company that operates a copper smelter and refinery in Gresik, Indonesia. These

smelters play an important role in our concentrate marketing strategy, as

approximately one-half of PT Freeport Indonesia’s

concentrate production has been sold to Atlantic Copper and PT Smelting over the

last several years (see “Investment in Smelters”).

The

diagram below shows our corporate structure.

_______________

(a) FM

Services Company, a Delaware corporation, provides us and two other

publicly-traded companies with executive, administrative, financial, accounting,

legal, tax and similar services.

The

following four maps indicate

| - |

the

distance from Papua to Bali (approximately 1,500 miles) and to Jakarta

(approximately 2,000 miles); |

| - |

the

location of the Papua province in which we

operate; |

| - |

the

location of our Contracts of Work areas within the Papua province;

and |

| - |

the

infrastructure of our Contract of Work project area.

|

2

3

4

5

Contracts

of Work

By virtue

of their Contracts of Work, PT Freeport Indonesia and Eastern Minerals conduct

their current exploration operations and PT Freeport Indonesia conducts its

mining operations in Indonesia. Both Contracts of Work govern our rights and

obligations relating to taxes, exchange controls, royalties, repatriation and

other matters. Both Contracts of Work were concluded pursuant to the 1967

Foreign Capital Investment Law, which expresses Indonesia’s foreign

investment policy and provides basic guarantees of remittance rights and

protection against nationalization, a framework for economic incentives and

basic rules regarding other rights and obligations of foreign investors.

Specifically, the Contracts of Work provide that the Government of Indonesia

will not nationalize or expropriate PT Freeport Indonesia’s or

Eastern Minerals’ mining operations. Any disputes regarding the provisions of

the Contracts of Work are subject to international arbitration. We have

experienced no disputes requiring arbitration during the 37 years we have

operated in Indonesia.

PT

Freeport Indonesia’s Contract

of Work covers both Block A, which was first included in a 1967 Contract of Work

that was replaced by a new Contract of Work in 1991, and Block B, to which we

gained rights in 1991. The initial term of our Contract of Work expires in

December 2021, but we can extend it for two 10-year periods subject to

Indonesian government approval, which cannot be withheld or delayed

unreasonably. We originally had the rights to explore 6.5 million acres in Block

B, but pursuant to the Contract of Work we have only retained the rights to

approximately 500,000 acres, which we believe, following significant geological

assessment, contain the most promising exploration opportunities.

Eastern

Minerals signed its Contract of Work in August 1994. The Contract of Work

originally covered approximately 2.5 million acres. Eastern Minerals' Contract

of Work provides for a four-to-seven year exploratory term and a 30-year term

for mining operations. Subject to Indonesian government approval, which cannot

be withheld or delayed unreasonably, we can extend this period for two 10-year

periods. Eastern Minerals’ Contract of Work requires us to relinquish our rights

to 25 percent of the original 2.5-million-acre Contract of Work area at the end

of each of three specified periods. As of December 31, 2004, we had relinquished

approximately 1.3 million acres and must relinquish an additional 0.6 million

acres at the end of the three-year exploration period, which can be extended by

the Government of Indonesia for as much as two additional years.

We

suspended our exploration activities outside of Block A in recent years because

of safety and security issues and regulatory uncertainty relating to a possible

conflict between our mining and exploration rights in certain forest areas and

an Indonesian Forestry law enacted in 1999 prohibiting open-pit mining in forest

preservation areas. In 2001, we requested and received from the Government of

Indonesia formal temporary suspensions of our obligations under the Contracts of

Work in all areas outside of Block A. The current suspensions were granted for

one-year periods ending February 26, 2005, for Block B; March 31, 2005, for PT

Nabire Bakti Mining; and November 15, 2004, for Eastern Minerals. Recent

Indonesian legislation permits open-pit mining in PT Freeport

Indonesia’s Block B

area, subject to certain requirements. We are currently assessing these

requirements and security issues. The timing for our resumption of exploration

activities in our Contract of Work areas outside of Block A depends on the

resolution of these matters.

PT

Freeport Indonesia pays a copper royalty under its Contact of Work that varies

from 1.5 percent of copper net revenue at a copper price of $0.90 or less per

pound to 3.5 percent at a copper price of $1.10 or more per pound. The Contract

of Work royalty rate for gold and silver sales is 1.0 percent.

A large

part of the mineral royalties under Government of Indonesia regulations are

designated to the provinces from which the minerals are extracted. In connection

with our “fourth concentrator mill expansion,” PT Freeport Indonesia agreed to

pay the Government of Indonesia additional royalties (royalties not required by

our Contract of Work) to provide further support to the local governments and

the people of Papua. PT Freeport Indonesia pays the additional royalties on

metal from production above 200,000 metric tons of ore per day. The additional

royalty for copper equals the Contract of Work royalty rate and for gold and

silver equals twice the Contract of Work royalty rates. Therefore, our royalty

rate on copper net revenues from production above 200,000 metric tons of ore per

day is double the Contract of Work royalty rate, and our royalty rates on gold

and silver sales from production above 200,000 metric tons of ore per day are

triple the Contract of Work royalty rates. PT Freeport Indonesia’s share of

the combined royalties, including the additional royalties which became

effective January 1, 1999, totaled $43.5 million in 2004, $26.5 million in 2003

and $24.5 million in 2002.

6

Republic

of Indonesia

General. The

Republic of Indonesia consists of more than 17,000 islands stretching 3,000

miles along the equator from Malaysia to Australia and is the fourth most

populous nation in the world with over 230 million people. Following many years

of Dutch colonial rule, Indonesia gained independence in 1945 and now has a

presidential republic system of government.

Our

mining complex was Indonesia’s first

copper mining project and was the first major foreign investment in Indonesia

following the economic development program instituted by the Indonesian

government in 1967. We work closely with the central, provincial and local

governments in development efforts in the area surrounding our operations. We

have had positive relations with the Indonesian government since we commenced

business activities in Indonesia in 1967, and we intend to continue to maintain

positive working relationships with the central, provincial and local branches

of the Indonesian government.

Political

Developments. In May

1998, President Suharto, Indonesia’s

political leader for more than 30 years, resigned in the wake of an economic

crisis in Indonesia and other parts of Southeast Asia and in the face of growing

social unrest. Vice President B.J. Habibie succeeded Suharto. In June 1999,

Indonesia held a new parliamentary election on a generally peaceful basis as the

first step in the process of electing a new president. In October 1999, in

accordance with the Indonesian constitution, the country’s highest

political institution (the People’s

Consultative Assembly), composed of the newly elected national parliament along

with additional provincial and other representatives, elected Abdurrahman Wahid

as president and Megawati Sukarnoputri as vice president.

There

were repeated challenges to the political leadership of President Wahid after

his election in October 1999. In July 2001, the People’s

Consultative Assembly voted to remove President Wahid, and elected Vice

President Megawati Sukarnoputri as president. The 2004 presidential election was

conducted peacefully and after a runoff, Susilo Bambang Yudhoyono was elected

the new president in October.

Recent

Developments. On

December 26, 2004, a massive earthquake - one of the five strongest ever

recorded - struck off the coast of North Sumatra in Indonesia, triggering

powerful tsunamis that devastated the coastlines of Aceh province in Indonesia

and areas of Thailand, India, Sri Lanka and other nations as far away as Somalia

in Africa. The human lives lost are currently estimated to total more than

166,000 in Indonesia alone. Aceh province, at the western tip of Sumatra, is

Indonesia’s

westernmost province. Our operations, located 3,000 miles away in

Indonesia’s

easternmost province of Papua, were not impacted by the tsunamis. PT Freeport

Indonesia has provided cash contributions in Indonesia and FCX, in the United

States for immediate assistance and to encourage fundraising efforts. We also

provided airplanes to transport food and medical supplies, aid workers and

government officials to the stricken area, including some of the first aid

shipments to arrive, which were received by President Yudhoyono.

On August

31, 2002, three people were killed and 11 others were wounded in an ambush by a

group of unidentified assailants. The assailants shot at several vehicles

transporting international contract teachers from PT Freeport

Indonesia’s school

in Tembagapura, their family members, and other contractors to PT Freeport

Indonesia on the road near Tembagapura, the mining town where the majority of PT

Freeport Indonesia’s

personnel reside. Indonesian authorities and the United States Federal Bureau of

Investigation investigated the incident, which resulted in the U.S. indictment

of an alleged operational commander in the Free Papua Movement/National Freedom

Force.

On

October 12, 2002, a bombing killed 202 people in the Indonesian province of

Bali, which is 1,500 miles west of our mining and milling operations. Indonesian

authorities arrested 35 people in connection with this bombing and 29 of those

arrested have been tried and convicted. On August 5, 2003, 12 people were killed

and over 100 others were injured by a car bomb detonated outside of the JW

Marriott Hotel in Jakarta, Indonesia. On September 9, 2004, 11 people were

killed and over 200 others injured by a car bomb detonated in front of the

Australian embassy. The same international terrorist organizations are suspected

in each of these incidents. Our mining and milling operations were not

interrupted by these incidents. However, our corporate offices in Jakarta

sustained damages as a result of the bombing in front of the Australian embassy.

After relocating for several months our corporate offices in Jakarta were

reestablished.

The

Government of Indonesia, which provides security for PT Freeport

Indonesia’s

personnel and operations (see “Security Matters”), has expressed a strong

commitment to protect natural resources businesses operating in Indonesia,

including PT Freeport Indonesia, with heightened security following the

incidents discussed above.

7

Economic

and Social Conditions. The

Indonesian economy grew by an estimated 5 percent in 2004 and 4 percent in 2003.

The Indonesian currency, the rupiah, averaged approximately 8,900 rupiah to one

U.S. dollar during 2004 and closed at 9,270 rupiah to one U.S. dollar on

December 31, 2004, compared with 8,437 rupiah to one U.S. dollar on December 31,

2003.

Despite

gradual improvements on the economic front, Indonesia’s recovery

remains vulnerable to ongoing political and social tensions. Incidents of

violence and separatist pressures continue to be reported. Pro-independence

movements in certain areas continue to be prominent, especially in the province

of Aceh, where the Indonesian government signed a peace agreement with

separatists in December 2002, and to a lesser extent in Papua. Following the

December 2004 tsunamis in Aceh, negotiations between the Government of Indonesia

and separatists in Aceh appear more promising. The area surrounding our mining

development is sparsely populated by local people and former residents of more

populous areas of Indonesia, some of whom have resettled in Papua under the

Government of Indonesia’s

transmigration program. A segment of the local population is opposing Indonesian

rule over Papua, and several separatist groups have sought political

independence for the province. In addition to the August 31, 2002, shooting

incident, there have been sporadic attacks on civilians by separatists and

sporadic but highly publicized conflicts between separatists and the Indonesian

military in Papua.

Our

Contracts of Work and the Government of Indonesia. While

the uncertainties of the regional autonomy process have created concern among

foreign investors, the Indonesian government has repeatedly assured investors

that existing contracts would be honored. Government officials have publicly

stated that the Government of Indonesia will honor existing contracts and that

they have no intention of revoking or unilaterally amending such contracts,

specifically including PT Freeport Indonesia’s Contract

of Work. Our belief that our Contracts of Work will continue to be honored is

further supported by U.S. laws, which prohibit U.S. aid to countries that

nationalize property owned by, or take steps to nullify a contract with, a U.S.

citizen or company at least 50 percent owned by U.S. citizens if the foreign

country does not within a reasonable time take appropriate steps to provide full

value compensation or other relief under international law.

In July

2004, we received a request from the Indonesian Department of Energy and Mineral

Resources that we offer to sell to Indonesian nationals shares in PT Indocopper

Investama at fair market value. PT Indocopper Investama, which we wholly own,

has an approximate 9.36 percent ownership interest in PT Freeport Indonesia. In

response to this request and in view of the potential benefits of having

additional Indonesian ownership in our project, we have agreed to consider a

potential sale of an interest in PT Indocopper Investama at fair market value.

Neither our Contract of Work nor Indonesian law requires us to divest any

portion of our ownership interest in PT Freeport Indonesia or PT Indocopper

Investama. See “Nusamba Loan Guarantee.”

Our

Investment in Indonesia and Papua. We have a

board-approved policy statement on social, employment and human rights, and have

comprehensive and extensive social, cultural and community development programs,

to which we have committed significant financial and managerial resources. See

“Social Development, Employment and Human Rights.” These policies and programs

are designed to address the impact of our operations on the local villages and

people and to provide assistance for the development of the local people. While

we believe these efforts should serve to avoid damage to and disruptions of our

mining operations, our operations could be damaged or disrupted by social,

economic and political forces beyond our control.

PT

Freeport Indonesia contributes to the economies of Papua and the Republic of

Indonesia through the payment of taxes, dividends and royalties; voluntary

economic development programs; infrastructure development; employment; and the

purchase of local and national goods. In fact, PT Freeport Indonesia has

frequently been one of the largest taxpayers in the Republic of Indonesia. In

addition, it pays royalties on all minerals removed from the

ground.

Since it

began development activities more than 35 years ago, PT Freeport Indonesia has

made significant investments in infrastructure both for its use and for use by

the Papuan public. These infrastructure improvements include medical facilities,

roads, an airport and heliports, schools, housing, community buildings and

places of worship.

PT

Freeport Indonesia is also one of the largest private employers in Indonesia and

by far the largest in Papua. As of December 31, 2004, PT Freeport Indonesia

directly employed 7,858 people; and 6,247 contract workers provided services to

PT Freeport Indonesia. In addition, 4,587 persons worked for privatized

companies providing services within PT Freeport Indonesia’s

operations area.

8

Besides

the estimated $2.6 billion paid in direct benefits to the Indonesian government

under the Contract of Work from 1992 through 2004, PT Freeport

Indonesia’s

operations have provided another $9.3 billion during this period in indirect

benefits to Papua and the Republic of Indonesia in the form of wages and

benefits paid to workers, purchases of goods and services, charitable

contributions and reinvestments in operations. For 2004, direct benefits totaled

approximately $260 million and indirect benefits totaled approximately $623

million.

Ore

Reserves

During

2004, additions to the aggregate proven and probable reserves of the Grasberg

and other Block A ore bodies in the Grasberg minerals district totaled

approximately 141 million metric tons of ore representing increases of 2.9

billion recoverable pounds of copper, 2.2 million recoverable ounces of gold and

18.9 million recoverable ounces of silver. The additions were primarily the

result of positive drilling results at the Deep Mill Level Zone ore body, a

146-million-metric-ton ore body. Year-end aggregate proven and probable

recoverable reserves, net of 2004 production, were 2.8 billion metric tons of

ore averaging 1.09 percent copper, 0.97 grams per metric ton (g/t) of gold and

3.84 g/t of silver representing 56.2 billion pounds of copper, 61.0 million

ounces of gold and 174.5 million ounces of silver. Our aggregate exploration

budget for 2005, including Rio Tinto’s share,

is expected to total approximately $21 million ($15 million for our share) with

most of the effort focused on testing the Mill Level Zone and Deep Mill Level

Zone deposits to the northwest, expansion of the underground Grasberg resource,

and testing reconnaissance targets along the Wanagon and Idenberg fault trends.

Pursuant

to joint venture arrangements between PT Freeport Indonesia and Rio Tinto, Rio

Tinto has a 40 percent interest in production from reserves above those reported

at December 31, 1994. Net of Rio Tinto’s share,

PT Freeport Indonesia’s share of

proven and probable recoverable reserves as of December 31, 2004, was 40.5

billion pounds of copper, 46.5 million ounces of gold and 124.5 million ounces

of silver. FCX’s equity

interest in proven and probable recoverable reserves as of December 31, 2004,

was 36.7 billion pounds of copper, 42.1 million ounces of gold and 112.8 million

ounces of silver. We estimated recoverable reserves using an average copper

price of $0.85 per pound and an average gold price of $270 per ounce. If metal

prices were adjusted to the approximate average London spot prices for the past

three years, i.e., copper prices adjusted from $0.85 per pound to $0.94 per

pound and gold prices adjusted from $270 per ounce to $361 per ounce, the

additions to proven and probable reserves would not be material to our reported

reserves.

All of

our proven and probable recoverable reserves lie within Block A. The Grasberg

minerals district contains the largest single gold reserve and the

second-largest copper reserves of any mine in the world. Aggregate Grasberg open

pit and underground proven and probable recoverable ore reserves as of December

31, 2004, are shown below along with those of our other deposits. Reserve

calculations were prepared by our employees under the supervision of George D.

MacDonald, our Vice President of Exploration, and were reviewed and verified by

Independent Mining Consultants, Inc., experts in mining, geology and reserve

determination. See “Risk Factors.” We developed our current mine plan based on

completing the mining of all of our currently designated recoverable reserves

before the end of 2041, which would be the expiration of our Contract of Work

including two 10-year extensions. Prior to the expiration of the initial term of

our Contract of Work in December 2021, under our current mine plan we expect to

mine approximately 47 percent of aggregate proven and probable ore, representing

approximately 55 percent of PT Freeport Indonesia’s share of

recoverable copper reserves and approximately 69 percent of PT Freeport

Indonesia’s share of

recoverable gold reserves.

9

|

Proven |

Probable |

Total | |||||||

|

Metric

Tons of Ore (000s)a |

Average

Ore Grade |

Metric

Tons of Ore (000s)a |

Average

Ore Grade |

Metric

Tons | |||||

|

Copper |

Gold |

Silver |

Copper |

Gold |

Silver |

of

Ore (000s)a | |||

|

(%) |

(g/t) |

(g/t) |

(%) |

(g/t) |

(g/t) |

||||

|

Developed

and producing: |

|||||||||

|

Grasberg

open pit |

234,908 |

1.11 |

1.50 |

2.55 |

475,699 |

1.10 |

1.21 |

2.60 |

710,607 |

|

Deep

Ore Zone |

70,178 |

0.97 |

0.65 |

4.96 |

85,065 |

0.88 |

0.61 |

5.01 |

155,243 |

|

Undeveloped: |

|||||||||

|

Grasberg

block cave |

133,567 |

1.09 |

1.04 |

2.87 |

740,225 |

0.98 |

0.72 |

2.81 |

873,792 |

|

Kucing

Liar |

190,147 |

1.29 |

1.01 |

4.89 |

308,852 |

1.31 |

1.27 |

6.06 |

498,999 |

|

Mill

Level Zone |

71,774 |

0.92 |

0.78 |

3.91 |

86,999 |

0.83 |

0.74 |

3.95 |

158,773 |

|

Deep

Mill Level Zone |

24,464 |

1.39 |

1.13 |

6.90 |

121,953 |

1.19 |

0.91 |

6.12 |

146,417 |

|

Ertsberg

Stockwork Zone |

25,941 |

0.52 |

0.94 |

1.74 |

95,773 |

0.49 |

0.89 |

1.63 |

121,714 |

|

Dom

block cave |

11,894 |

1.18 |

0.31 |

6.40 |

31,757 |

1.05 |

0.31 |

5.72 |

43,651 |

|

Big

Gossan |

2,468 |

2.20 |

0.93 |

14.08 |

30,438 |

2.67 |

0.92 |

15.85 |

32,906 |

|

Dom

open pit |

6,882 |

1.87 |

0.46 |

9.88 |

20,118 |

1.78 |

0.42 |

9.50 |

27,000 |

|

Total |

772,223 |

1.12 |

1.10 |

3.80 |

1,996,879 |

1.07 |

0.93 |

3.86 |

2,769,102 |

|

Mill

Recoveries (%) |

Proven

and Probable

Recoverable

Reservesb | |||||||

|

Copper |

Gold |

Silver |

Copper |

Gold |

Silver | |||

|

(Billions

of Lbs.) |

(Millions

of Ozs.) |

(Millions

of Ozs.) | ||||||

|

Developed

and producing: |

||||||||

|

Grasberg

open pit |

88.6 |

86.5 |

65.9 |

14.9 |

24.9 |

29.9 | ||

|

Deep

Ore Zone |

83.7 |

74.0 |

66.1 |

2.5 |

2.3 |

12.6 | ||

|

Undeveloped: |

||||||||

|

Grasberg

block cave |

87.4 |

68.6 |

69.2 |

16.2 |

14.2 |

42.2 | ||

|

Kucing

Liar |

89.4 |

50.7 |

55.9 |

12.4 |

9.3 |

38.7 | ||

|

Mill

Level Zone |

87.6 |

77.7 |

81.5 |

2.6 |

3.0 |

12.6 | ||

|

Deep

Mill Level Zone |

88.9 |

78.5 |

81.2 |

3.4 |

3.4 |

18.4 | ||

|

Ertsberg

Stockwork Zone |

87.8 |

78.1 |

85.6 |

1.1 |

2.7 |

4.2 | ||

|

Dom

block cave |

82.6 |

75.2 |

62.0 |

0.8 |

0.3 |

4.0 | ||

|

Big

Gossan |

85.0 |

79.1 |

63.8 |

1.6 |

0.7 |

8.1 | ||

|

Dom

open pit |

69.0 |

68.0 |

59.0 |

0.7 |

0.2 |

3.8 | ||

|

Total |

87.6 |

72.5 |

66.3 |

56.2 |

61.0 |

174.5 | ||

|

PT

Freeport Indonesia’s

share |

40.5 |

46.5 |

124.5 | |||||

|

FCX’s

equity share |

36.7 |

42.1 |

112.8 | |||||

a. Ore

reserve tonnage estimates are after application of applicable mining recovery

factors.

|

b. |

Proven

and probable recoverable reserves represent estimated metal quantities

from which we expect to be paid after application of estimated mill

recovery rates and smelter recovery rates of 96.5 percent for copper, 97.0

percent for gold and 76.9 percent for silver. The term “recoverable

reserve” means that part of a mineral deposit which we estimate can be

economically and legally extracted or produced at the time of the reserve

determination. |

In

defining its open-pit reserves, PT Freeport Indonesia applies an “economic

cutoff grade” strategy. The objective of this strategy is to maximize the net

present value of its operations. PT Freeport Indonesia uses a break-even cutoff

grade to define the insitu reserves for its underground ore bodies. The

break-even cutoff grade is defined for a metric ton of ore, as that equivalent

copper grade, once produced and sold, that generates sufficient revenue to cover

all operating and administrative costs associated with its production.

PT

Freeport Indonesia’s ores contain three recoverable metals; copper, gold and

silver. We value all three metals in terms of a copper equivalent percentage to

determine a single break-even cutoff grade. Copper equivalent percentage is used

to express the relative value of multi-metal ores in terms of one metal, in this

case, copper. The calculation expresses the relative value of the ore using

estimates of contained metal quantities, metals prices as used for reserve

determination, recovery rates, treatment charges and royalties. The table below

shows the break-even cutoff grade, expressed as a copper equivalent percentage,

for each of our existing ore bodies as of December 31, 2004.

10

|

Ore

Body |

Copper

Equivalent

Percentage |

||

|

Grasberg

open pit |

0.54% |

||

|

Deep

Ore Zone |

0.70% |

||

|

Grasberg

block cave |

0.73% |

||

|

Kucing

Liar |

0.86% |

||

|

Mill

Level Zone |

0.85% |

||

|

Deep

Mill Level Zone |

0.84% |

||

|

Ertsberg

Stockwork Zone |

0.77% |

||

|

Dom

block cave |

|

0.73% |

|

|

Big

Gossan |

1.75% |

||

|

Dom

open pit |

0.71% |

||

|

Average |

0.73% |

The

following table sets forth the average drill hole spacing for each of our ore

bodies. Drill hole spacing data is used by mining professionals, such as mining

engineers, in determining the suitability of data coverage (on a relative basis)

in a given deposit type and mining method scenario so as to achieve a given

level of confidence in the resource estimate. Drill hole spacing is only one of

several criteria necessary to establish confidence level for resource

classification. Drilling programs are typically designed to achieve an optimum

sample spacing to support the level of confidence in results that fit a

particular stage of development of a mineral deposit. We calculated the average

drill hole spacing within each ore body using the distance from the center of

each block in the resource model to the nearest drill hole composite. We then

calculated the averages of these values within the volume of each ore body and

reported them under the column entitled “Average Distance: To Nearest Sample.”

This value represents at least one-half of the average drill hole spacing within

each deposit. We calculated the value under the column entitled “Average

Distance: Between Drill Holes” by multiplying the average minimum distance value

by two, and this value represents the maximum average drill hole spacing.

|

Spacing

(in

meters) |

Average

Distance

(in

meters) | |||||

|

Deposit |

Mining

Unit |

Surface

Drilling

Grids |

Underground

(&

Surface)

Drill

Fans |

Drilling

Method |

To

Nearest

Sample |

Between

Drill

Holes

(less

than) |

|

Grasberg |

Open

Pit |

50 |

75 |

Core |

45 |

89 |

|

Deep

Ore Zone |

Block

Cave |

- |

50 |

Core |

13 |

25 |

|

Grasberg |

Block

Cave |

- |

100 |

Core |

46 |

92 |

|

Kucing

Liar |

Block

Cave |

- |

75 |

Core |

36 |

72 |

|

Mill

Level Zone |

Block

Cave |

- |

50 |

Core |

19 |

38 |

|

Deep

Mill Level Zone |

Block

Cave |

- |

75 |

Core |

28 |

57 |

|

Ertsberg

Stockwork Zone |

Block

Cave |

100 |

50 |

Core |

26 |

52 |

|

Dom |

Block

Cave |

- |

50 |

Core |

26 |

52 |

|

Big

Gossan |

Open

Stope |

100 |

50 |

Core |

22 |

45 |

|

Dom |

Open

Pit |

- |

50 |

Core |

25 |

50 |

Mining

Operations - Mines in Production

We and

our predecessors have conducted exploration and mining operations in Block A

since 1967 and have been the only operator of these operations. We currently

have two mines in operation: the Grasberg open pit and the Deep Ore Zone.

11

We began

open-pit mining of the Grasberg ore body in 1990. Open-pit operations are

expected to continue until 2015 at which time the Grasberg underground mining

operations are scheduled to begin. Production is currently at the 3,520- to

4,060-meter elevation level and totaled 48.9 million metric tons of ore in 2004

and 57.4 million metric tons of ore in 2003, which provided 76 percent or our

2004 mill feed and 77 percent of our 2003 mill feed. Our open-pit mining rate,

including ore and overburden, totaled 592,700 metric tons per day in 2004 and

598,800 metric tons per day in 2003. Annual production rates are expected to

range between 600,000 metric tons per day and 750,000 metric tons per day

through 2010 and then decline through 2015. The Grasberg open pit is fully

developed and we do not expect to incur any significant development costs other

than our deferred mining costs discussed below.

The

current Grasberg equipment fleet consists of over 800 pieces of equipment. As of

December 31, 2004, the larger mining equipment directly associated with

production includes 150 haul trucks with payloads ranging from 135 metric tons

to 290 metric tons, 17 shovels with bucket sizes ranging from 30 cubic meters to

42 cubic meters and 58 bulldozers and graders. We believe our current equipment

level is adequate to meet our projected production levels over the remaining

life of the pit.

In

addition to the mining equipment, Grasberg crushing and conveying systems are

integral to the mine and provide the capacity to transport up to 225,000 metric

tons per day of Grasberg ore to the mill and 135,000 metric tons per day of

overburden to the overburden stockpiles.

Mining

costs are charged to operations as incurred. However, because of the

configuration and location of the Grasberg open-pit ore body and the location

and extent of the related surrounding overburden, the ratio of overburden to ore

is much higher in the initial mining of the open pit than in later years. As a

result, surface mining costs associated with overburden removal at PT Freeport

Indonesia’s Grasberg open-pit mine that are estimated to relate to future

production are initially deferred when the ratio of actual overburden removed to

ore mined exceeds the estimated average ratio of overburden removed to ore mined

over the life of the Grasberg open-pit mine. Those deferred costs are

subsequently charged to operating costs when the ratio of actual overburden

removed to ore mined falls below the estimated average ratio of overburden to

ore over the life of the Grasberg open-pit mine. The reserve quantities used to

develop the life of mine ratio are the proven and probable ore quantities for

the Grasberg open pit shown above.

The

application of the deferred mining cost method has resulted in an asset on FCX’s

balance sheets (“Deferred Mining Costs”), which based on current mine plans, is

estimated to increase through about 2010. Subsequently, these costs are expected

to be amortized as a charge to production and delivery costs until they are

fully amortized at the end of the open pit’s life, which is estimated to be in

approximately 2015. This is because PT Freeport Indonesia expects to mine higher

than average amounts of overburden through 2010 and less than average

thereafter. Deferred mining costs totaled $220.4 million at December 31, 2004,

and $142.6 million at December 31, 2003. Additions to deferred mining costs are

classified as increases in deferred mining costs in operating activities in the

consolidated statements of cash flows and totaled $77.8 million in 2004, $64.4

million in 2003 and $30.6 million in 2002. See Note 1 of “Notes to Consolidated

Financial Statements” included in our 2004 Annual Report incorporated herein by

reference.

The Deep

Ore Zone ore body lies vertically below the now depleted Intermediate Ore Zone.

We began production from the Deep Ore Zone ore body in 1989, but we suspended

production in 1991 in favor of production from the Grasberg deposit. Production

using the block-cave method restarted in September 2000. Production is at the

3,110-meter elevation level and totaled 15.9 million metric tons of ore in 2004

and 14.8 million metric tons of ore in 2003. The Deep Ore Zone has performed

above design capacity of 35,000 metric tons of ore per day and we are expanding

the Deep Ore Zone operation to sustained production of 50,000 metric tons of ore

per day with the installation of a second crusher and additional ventilation.

Production from the Deep Ore Zone averaged 43,600 metric tons of ore per day in

2004 and 40,500 metric tons of ore per day in 2003.

The Deep

Ore Zone mine fleet consists of over 160 pieces of mobile equipment. The primary

mining equipment directly associated with production and development includes 26

load-haul-dump (LHD) units and 15 haul trucks. Our LHD units typically carry

approximately 11 metric tons of ore. The units dump into a gyratory crusher and

ore is then conveyed to the surface stockpiles.

12

During

2004 at the Deep Ore Zone mine, we completed 9,550 meters of development

drifting in support of the block-cave mining method and the ongoing expansion to

50,000 metric tons of ore per day. The expansion to 50,000 metric tons of ore

per day is expected to be completed in 2007 with aggregate development costs

from 2004 through 2007 to total approximately $62 million (approximately $37

million for PT Freeport Indonesia’s share).

Our

development costs include costs incurred resulting from mine pre-production

activities undertaken to gain access to proven and probable reserves including

adits, drifts, ramps, permanent excavations, infrastructure and removal of

overburden. Depreciation for mining and milling life-of-mine assets is

determined using the unit-of-production method based on estimated recoverable

proven and probable copper reserves. Development costs that relate to a specific

ore body are depreciated using the unit-of-production method based on estimated

recoverable proven and probable copper reserves for the ore body benefited. PT

Freeport Indonesia’s total development costs at December 31, 2004 for the Deep

Ore Zone mine, currently our only operating underground mine, totaled $189.5

million, which are being depreciated on a unit-of-production basis over the life

of the Deep Ore Zone proven and probable reserves. See Note 1 of “Notes to

Consolidated Financial Statements” included in our 2004 Annual Report

incorporated herein by reference.

The

majority of maintenance activities is performed on site by a combination of PT

Freeport Indonesia employees and contract workers. As of December 31, 2004, we

had approximately 7,500 employees and contract workers directly involved in

Grasberg open-pit and Deep Ore Zone underground mining, milling and ore flow

operations.

The

Intermediate Ore Zone was an underground block-cave operation that began

production in the first half of 1994. The Intermediate Ore Zone was depleted

during the third quarter of 2003. Production totaled 2.5 million metric tons of

ore in 2003 and 7.1 million metric tons of ore in 2002. During its 10-year life,

the Intermediate Ore Zone operation produced almost 30 percent more copper and

gold than the initial reserve estimates.

Our

principal source of power for all our operations is a coal-fired power plant

that we built in conjunction with our fourth concentrator expansion (see

“Infrastructure”). Medium-speed diesel generators supply peaking and backup

power. A combination of naturally occurring mountain streams and water derived

from our underground operations provides water for our operations. The average

annual rainfall in the project area is 180 inches.

Mining

Operations - Mines in Development

Seven

other ore bodies, referred to as the underground Grasberg, Kucing Liar, Mill

Level Zone, Deep Mill Level Zone, Ertsberg Stockwork Zone, Big Gossan and the

Dom are located in Block A. These ore bodies are at various stages of

development, and are included in our proven and probable recoverable reserves.

We incurred $2.9 million for mine development, expansion and infrastructure

capital expenditures related to these ore bodies and $26.7 million for common

underground infrastructure during the three years ended December 31, 2004. See

“Risk Factors.”

The

underground Grasberg reserves will be mined using the block-cave method at the

end of open-pit mining, which is expected to continue until approximately 2015.

The Kucing Liar ore body lies on the southern flank of and underneath the

southern portion of the Grasberg open pit at the 2,600- to 3,200-meter elevation

level. We are reviewing development plans for Kucing Liar.

The Mill

Level Zone ore body lies directly below the Deep Ore Zone mine at the

2,900-meter elevation. The Deep Mill Level Zone ore body lies beneath the Mill

Level Zone ore body at the 2,600-meter elevation. This ore represents the

downward continuation of mineralization in the Ertsberg East Skarn system and

neighboring Ertsberg porphyry. Drilling efforts continue to determine the extent

of these ore bodies. We expect to mine the Mill Level Zone ore body using a

block-cave method after we complete mining at the Deep Ore Zone ore body. Near

the end of mining the Mill Level Zone ore body, we expect to mine the Deep Mill

Level Zone ore body also using a block-cave method.

The

Ertsberg Stockwork Zone ore body extends off the southwest side of the Deep Ore

Zone ore body at the 3,100- to 3,600-meter elevation level. Drilling efforts

continue to determine the extent of this ore body, which we expect to mine using

a block-cave method starting in about 2009.

13

The Big

Gossan ore body is located approximately 1,000 meters southwest of the original

Ertsberg open-pit deposit. We began the initial underground development of the

ore body in 1993 when we drove tunnels from the mill area into the ore zone at

the 2,600-meter elevation level. A stope and fill mining method will be used on

the Big Gossan deposit. A feasibility study and an update to the site-wide

development plan will be completed in 2005 to determine is the timing of initial

production, currently projected to be 2007.

The Dom

ore body lies approximately 1,500 meters southeast of the depleted Ertsberg

open-pit deposit. Production at the open-pit portion of the ore body will begin

after completion of open-pit mining at Grasberg, subsequently followed by

block-cave mining of the underground portion of the Dom ore body.

The

projected aggregate capital expenditures required to reach full production

capacity for each of our undeveloped ore bodies based on our latest mine plans

and our proven and probable recoverable reserves as of December 31, 2004, are

shown below (in millions). Actual costs could differ materially from these

estimates as we will not incur most of the expenditures for several years and we

will incur them over a period of several years. Based on our current estimates,

we expect aggregate expenditures will range between $25 million and $265 million

annually, during the next 15 years. In addition, these costs will be shared with

Rio Tinto in accordance with our joint venture agreement.

|

Grasberg

block cave |

$ 980 |

|

Kucing

Liar block cave |

500 |

|

Mill

Level Zone block cave |

265 |

|

Deep

Mill Level Zone block cave |

260 |

|

Big

Gossan open stope |

225 |

|

Dom

block cave |

185 |

|

Ertsberg

Stockwork Zone block cave |

180 |

|

Dom

open pit |

30 |

|

Total |

$2,625 |

Description

of Ore Bodies. Our ore

bodies are located within and around two main igneous intrusions, the Grasberg

monzodiorite and the Ertsberg diorite. The host rocks of these ore bodies

include both carbonate and clastic rocks that form the ridge crests and upper

flanks of the Sudirman Range, and the igneous rocks of monzonitic to dioritic

composition that intrude them. The igneous-hosted ore bodies (the Grasberg open

pit and block cave, and the Ertsberg Stockwork Zone block cave) occur as vein

stockworks and disseminations of copper sulphides, dominated by chalcopyrite

and, to a much lesser extent, bornite. The sedimentary-rock hosted ore bodies

occur as “magnetite-rich, calcium/magnesian skarn” replacements, whose location

and orientation are strongly influenced by major faults and by the chemistry of

the carbonate rocks along the margins of the intrusions.

The

copper mineralization in these skarn deposits is also dominated by chalcopyrite,

but higher bornite concentrations are common. Moreover, gold occurs in

significant concentrations in all of the district’s ore

bodies, though rarely visible to the naked eye. These gold concentrations

usually occur as inclusions within the copper sulphide minerals, though, in some

deposits, these concentrations can also be strongly associated with

pyrite.

14

The

following diagram indicates the relative elevations (in meters) of our reported

reserve ore bodies.

15

The

following map, which encompasses an area of approximately 42 square kilometers

(approximately 16 square miles), indicates the relative positions and sizes of

our reported reserve ore bodies and their locations.

16

The

following chart illustrates our current plans for sequencing and producing each

of our ore bodies and the years in which we currently expect that production of

each ore body will begin and end. Production volumes are typically lower in the

first few years of each ore body as development activities are ongoing and as

the mine ramps up to full production. Currently, the Grasberg open pit and Deep

Ore Zone are our only producing mines. The ultimate timing of the start of

production from our undeveloped mines is dependent upon a number of factors,

including the results of our exploration efforts, and may vary from the dates

shown below. In addition, we develop our mine plans for the Grasberg open pit

and underground mines based on maximizing the net present value from the ore

bodies.

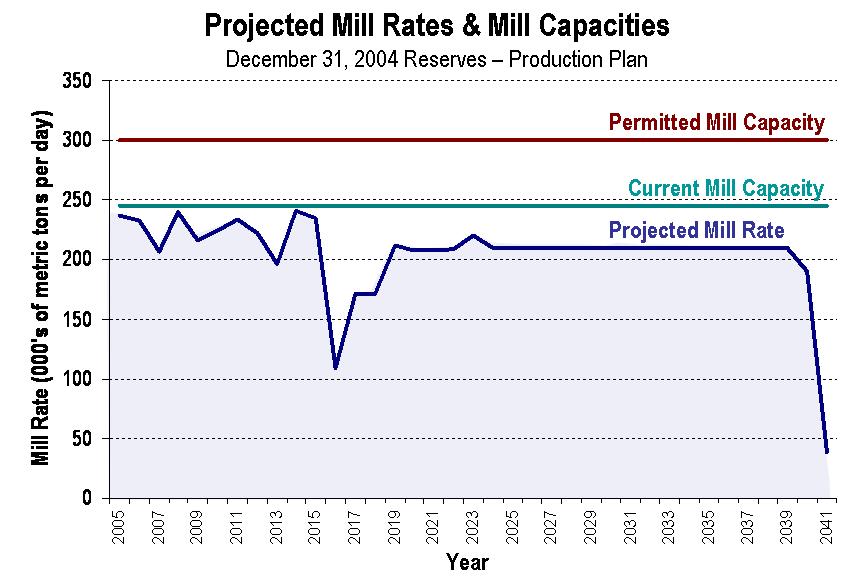

During

2004, we mined an average of 636,200 metric tons of material per day, including

ore and overburden, and we do not require any additional approvals for higher

rates. During 2003, we mined an average of 646,100 metric tons of material per

day. The following chart illustrates our current aggregate mill capacity; our

aggregate permitted mill capacity; and our projected milling rates. The decline

in milling rates in 2016 reflects the expected completion date of open-pit

mining at the Grasberg ore body. We are continuing to develop mine plans to

optimize production levels and to offset the anticipated decline in

2016.

17

Milling

and Production

The ore

from our mines moves by a conveyor system to a series of shafts through which it

drops to our milling and concentrating complex located approximately 2,900

meters above sea level. At the mill, the ore is crushed and ground and mixed in

tanks with water and small amounts of flotation reagents where it is

continuously agitated with air. During this physical separation process,

copper-, gold- and silver-bearing particles rise to the top of the tanks and are

collected and thickened into a concentrate. The concentrate leaves the mill

complex as a slurry, consisting of approximately 65 percent solids by weight,

and is pumped through three parallel 115-kilometer pipelines to our coastal port

site facility at Amamapare where it is filtered, dried and stored for shipping.

Ships are loaded at dock facilities at the port until they draw their maximum

dock-side water, and they then move to deeper water, where loading is completed

from shuttling barges.

Our

production results for the last three years are as follows:

|

Years

Ended December 31, |

Percentage

Change | ||||

|

2004 |

2003 |

2002 |

2003

to 2004 |

2002

to 2003 | |

|

Mill

throughput (metric tons of ore per day) |

185,100 |

203,000

|

235,600 |

(9)% |

(14)% |

|

Copper

production, net to PT Freeport Indonesia (000 pounds) |

996,500 |

1,291,600

|

1,524,200 |

(23)% |

(15)% |

|

Gold

production, net to PT Freeport Indonesia (ounces) |

1,456,200 |

2,463,300

|

2,296,800 |

(41)% |

7% |

|

Average

net cash production costs (credits) per pound of coppera |

$0.40 |

$(0.02) |

$0.08 |

N.M. |

125% |

N.M. Not

Meaningful

a. Includes

site production and delivery costs, smelting and refining costs, and royalties,

less credits for gold and silver sales. See our 2004 Annual Report incorporated

herein by reference for a reconciliation of average net cash production costs

per pound to production and delivery costs applicable to sales reported in our

consolidated financial statements.

In

October 2003, a slippage of material occurred in a section of the Grasberg open

pit and in December 2003, a smaller debris flow occurred in the same section.

The area affected by the slippage events included two active mining areas which

were scheduled to be mined in the fourth quarter of 2003 (see “Grasberg Open-Pit

Slippage”). Mill throughput and production in 2003 and 2004 were negatively

affected by PT Freeport Indonesia’s efforts

to accelerate removal of overburden material and restore safe access to

higher-grade areas in the pit. Mill throughput averaged 185,100 metric tons of

ore per day in 2004, a nine percent decrease from the 203,000 metric tons

average in 2003. Copper and gold production was lower in 2004 compared with 2003

reflecting the lower mill throughput and lower average ore grades. Copper

production for 2004 totaled 1.0 billion pounds, 295.1 million pounds lower than

2003 production. Gold production for 2004 totaled 1.46 million ounces, 1.0

million ounces lower than 2003 production. The lower sales volumes and the

primarily fixed nature of a large portion of PT Freeport Indonesia’s cost

structure resulted in average net cash production costs for 2004 increasing to

$0.40 per pound compared with a net credit of $0.02 per pound for

2003.

Copper

production for 2003 was 1.3 billion pounds, 232.6 million pounds lower than 2002

production primarily because of lower average copper ore grades and lower mill

throughput caused by the slippage and debris flow events. Gold production for

2003 was 166,500 ounces higher than that for 2002 primarily because of higher

average gold grades.

Average

net cash production costs per pound of copper of a net credit of $(0.02) for

2003 were an annual record low compared with $0.08 for 2002. Higher gold credits

in 2003 offset higher site production and delivery costs. Our average net cash

production costs per pound of copper vary with the amount of gold we sell and

gold prices, among other factors. Once we complete our open-pit mining

operations at the Grasberg mine in approximately 2015 and transition to

underground, we expect our share of annual copper and gold production to be

lower than current levels, and all other factors being equal, our average net

cash production costs to increase. For more information regarding our operating

and financial results, see our 2004 Annual Report incorporated herein by

reference.

18

Geotechnical

Programs

Our

geotechnical programs support several phases of the operations, including our

open-pit mine (pit slope and overburden stockpile stability), our underground

mine, our infrastructure and our tailings management program. For information

regarding our tailings management program, see “Environmental

Matters.”

A group

of our senior level employees has the responsibility, authority and oversight

for our overall geotechnical programs. Our multi-disciplinary approach combines

in-house personnel with backgrounds in civil, geotechnical, mining engineering,

geology and hydrology to form a technical services group that reports to our

senior managers. Our technical services group develops information that our mine

engineering group uses to develop mine and stockpile designs, production

schedules and related plans. Our technical services group also monitors slope

stability and other geotechnical and hydrological developments.

Our

technical services group is composed of expatriates and Indonesian nationals,

who are university educated. International consulting experts in each of the

applicable technical fields support this group. In-house training provided by

consultants as well as off-site seminars and industry conferences supports the

training of our staff. Our joint venture partner has also provided geotechnical

and engineering support to our operations. Consultants and our joint venture

partner provide input into program development and assess performance of these

critical roles.

Our

technical services group uses information from geological drilling for the

development and updating of our geological, geotechnical and hydrologic models.

We develop computer-based geologic models for mine design and dewatering

programs. We provide continuous ground and slope monitoring in our mines, on all

overburden stockpiles, and around all infrastructure using various computerized

and automated systems. We also daily inspect all open-pit working areas, with

any items of concern being reported to our senior managers. Our hydrology

function measures and tracks water flow patterns to determine the effectiveness

and need for de-watering and depressurization programs. We drain all surface

flows away from the open pit and pump any in-pit surface water to dedicated

drain holes connected to our underground de-watering drift system. We also

continuously monitor rainfall at our operations so that we may adjust for

operational impacts and safety considerations.

Grasberg

Open-Pit Slippage

On

October 9, 2003, a slippage of material occurred in a section of the Grasberg

open pit. Eight workers perished and five workers were injured in the incident.

The area affected by the slippage, comprising approximately five percent of the

surface area of the massive Grasberg pit, included two active mining areas that

were scheduled to be mined in 2003 and 2004. On December 12, 2003, a debris flow

involving a relatively small amount of loose material occurred in the same area

of the Grasberg open pit resulting in only minor property damage. Following

these two events, PT Freeport Indonesia redirected its open-pit operations to

accelerate removal of waste material from the south wall to restore safe access

to the higher-grade ore areas in the pit. These activities resulted in reduced

production levels. In April 2004, PT Freeport Indonesia established safe access

and initiated mining in higher-grade ore areas while continuing waste removal

activities. PT Freeport Indonesia resumed normal milling rates in June

2004.

As a

result of the fourth-quarter 2003 slippage and debris flow events, PT Freeport

Indonesia notified its copper concentrate customers that it was declaring force

majeure under the terms of its contracts as it would be unable to satisfy its

annual sales and delivery commitments. In December 2004, PT Freeport Indonesia

terminated the force majeure that had been in effect since December 2003 under

its concentrate sales contracts.

PT

Freeport Indonesia maintains property damage and business interruption insurance

related to its operations. In December 2004, we entered into an insurance

settlement agreement and settled all claims that arose from the fourth-quarter

2003 slippage and debris flow events in the Grasberg open-pit mine. PT Freeport

Indonesia’s insurers

agreed to pay an aggregate of $125.0 million in connection with its claims.

After considering our joint venture partner’s interest

in the proceeds, PT Freeport Indonesia’s share of

proceeds totaled $95.0 million.

19

Exploration

As a

result of our joint venture arrangements, Rio Tinto generally pays for 40

percent of our joint venture exploration and exploratory drilling costs in

Papua. The joint ventures incurred total exploration costs of $13.6 million in

2004 and $10.5 million in 2003. The joint ventures’ exploration budget for 2005

totals approximately $21 million with most of the effort focused on testing the

Mill Level Zone and Deep Mill Level Zone deposits to the northwest, expansion of

the underground Grasberg resource, and testing reconnaissance targets along the

Wanagan and Idenberg fault trends.

In June

1998, we entered into a joint venture agreement to conduct exploration

activities in PT Nabire Bakti Mining’s Contract

of Work area, which currently covers approximately 500,000 acres in several

blocks contiguous to PT Freeport Indonesia’s Block B

and one of Eastern Minerals’ blocks in Papua. Rio Tinto shares in 40 percent of

our interest and costs in this exploration joint venture. We and Rio Tinto can

earn up to a 62 percent interest in the PT Nabire Bakti Mining Contract of Work

by spending up to $21 million on exploration and other activities in the joint

venture areas. We have spent $17.0 million through December 31,

2004.

With the

subsequent approval of the Indonesian government, in 2000 we suspended our field

exploration activities in Block B, which includes the Wabu Ridge gold prospect,

as well as in the other Contract of Work areas of Eastern Minerals and PT Nabire

Bakti Mining. The suspensions are due to safety and security issues and

regulatory uncertainty relating to a possible conflict between our mining and

exploration rights in certain forest areas and an Indonesian Forestry law

enacted in 1999 prohibiting open-pit mining in forest preservation areas. All of

the suspended areas are outside of our current mining operations area. We are

assessing the possible timing for resumption of our exploration

activities.

Infrastructure

The

location of our mining operations in a remote area requires that our operations

be virtually self-sufficient. In addition to the mining facilities described

above, in the course of the development of our project we have constructed

ourselves or participated with others in the construction of an airport, a port,

a 119 kilometer road, an aerial tramway, two hospitals and related medical

facilities, and two town sites with housing, schools and other facilities

sufficient to support more than 17,000 persons.

In 1996,

we completed a significant infrastructure program, which includes various

residential, community and commercial facilities. We designed the program to

provide the infrastructure needed for our operations, to enhance the living

conditions of our employees, and to develop and promote the growth of local and

other third party activities and enterprises in Papua. We have developed the

facilities through joint ventures or direct ownership involving local Indonesian

interests and other investors.

In July

2003, we acquired the 85.7 percent ownership interest in Puncakjaya Power owned

by affiliates of Duke Energy Corporation for $68.1 million cash, net of $9.9

million of cash acquired. Puncakjaya Power is the owner of assets supplying

power to PT Freeport Indonesia’s

operations, including the 3x65 megawatt coal-fired power facilities. PT Freeport

Indonesia purchases power from Puncakjaya Power under infrastructure asset

financing arrangements. At December 31, 2004, PT Freeport Indonesia had

infrastructure asset financing obligations to Puncakjaya Power totaling $258.7

million. As a result of our acquisition of the 85.7 percent ownership interest,

our consolidated balance sheet no longer reflects PT Freeport

Indonesia’s

obligation to Puncakjaya Power, but instead reflects the Puncakjaya Power bank

debt which totaled $187.0 million and a receivable from Rio Tinto totaling $73.5

million for its share of the obligation to Puncakjaya Power at December 31,

2004.

Marketing

PT

Freeport Indonesia sells its copper concentrates, which contain significant

quantities of gold and silver, under United States dollar-denominated sales

agreements, mostly to companies in Asia and Europe and to international trading

companies. We sell substantially all of our budgeted production of copper

concentrates under long-term contracts with selling prices based on world metals

prices (generally the London Metal Exchange settlement prices for Grade A

copper). Under these contracts, initial billing occurs at the time of shipment

and final settlement on the copper portion is generally based on average prices

for a specified future period. Gold generally is sold at the average London

Bullion Market Association price for a specified month near the month of

shipment.

20

Revenues

from concentrate sales are recorded net of royalties (see “Contracts of Work”),

treatment and refining charges (including participation charges, if applicable,

based on the market prices of metals), and the impact of derivative financial

instruments, if any, used to hedge against risks from metals price fluctuations.

Moreover, because a portion of the metals contained in copper concentrates is

unrecoverable as a result of the smelting process, our revenues from concentrate

sales are also recorded net of allowances based on the quantity and value of

these unrecoverable metals. These allowances are a negotiated term of our

contracts and vary by customer. Treatment and refining charges represent

payments to smelters and refiners and are either fixed or in certain cases vary

with the price of copper. We sell a small amount of copper concentrates in the

spot market. See “Risk Factors.”

We have

commitments, including commitments from Atlantic Copper and PT Smelting, for

essentially all of our estimated 2005 production. We estimate our share of sales

for 2005 to approximate 1.5 billion pounds of copper and 2.9 million ounces of

gold. Projected 2005 copper and gold sales reflect the expectation of higher

production following completion of efforts to restore safe access to high-grade

ore areas in the Grasberg open pit. See “Risk Factors.”

PT

Freeport Indonesia has a long-term contract through 2007 to provide Atlantic

Copper with a quantity of copper concentrates at market prices which currently

approximates 60 percent of Atlantic Copper’s annual

copper concentrate requirements. PT Freeport Indonesia’s

agreement with PT Smelting provides, for the life of PT Freeport

Indonesia’s mines,

for the supply of 100 percent of the copper concentrate requirements necessary

to produce 205,000 metric tons of copper (essentially the Gresik

smelter’s original

design capacity) on a priority basis. In 2004, PT Smelting increased its stated

production capacity to 250,000 metric tons of copper per year. For the first 15

years of PT Smelting’s

commercial operations beginning December 1998, PT Freeport Indonesia agreed that